UNITED STATES SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

| | | | | |

| ☑ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2020

OR

| | | | | |

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number 1-1023

S&P Global Inc.

(Exact name of registrant as specified in its charter)

| | | | | |

| New York | 13-1026995 |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

| | | | | | | | | | | | | | | | | |

| 55 Water Street | , | New York | , | New York | 10041 |

| (Address of principal executive offices) | (Zip Code) |

Registrant’s telephone number, including area code: 212-438-1000

Securities registered pursuant to Section 12(b) of the Act

| | | | | | | | |

| Title of each class | Trading Symbol | Name of exchange on which registered |

| Common Stock — $1 par value | SPGI | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes ☑ No ☐

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes ☐ No ☑

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15 (d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes ☑ No ☐

Indicate by check mark whether the Registrant has submitted electronically every Interactive Date File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the Registrant was required to submit such files).

Yes ☑ No ☐

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and "emerging growth company" in Rule 12b-2 of the Exchange Act. (Check one):

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| ☑ | Large accelerated filer | ☐ | Accelerated filer | ☐ | Non-accelerated filer | ☐ | Smaller reporting company | ☐ | Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of

the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C.

7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☑

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes ☐ No ☑

The aggregate market value of voting stock held by non-affiliates of the Registrant as of the last business day of the second fiscal quarter ended June 30, 2020, was $79.4 billion, based on the closing price of the common stock as reported on the New York Stock Exchange of $329.48 per common share. For purposes of this calculation, it is assumed that directors, executive officers and beneficial owners of more than 10% of the registrant outstanding stock are affiliates. The number of shares of common stock of the Registrant outstanding as of February 5, 2021 was 240.7 million shares.

Part III incorporates information by reference from the definitive proxy statement for the 2021 annual meeting of shareholders.

TABLE OF CONTENTS

| | | | | | | | |

| | PART I | |

| Item | | Page |

| 1 | | |

| 1A. | | |

| 1B. | | |

| 2 | | |

| 3 | | |

| 4 | | |

| Information about our Executive Officers | |

| | |

| PART II | |

| | |

| 5 | | |

| 6 | | |

| 7 | | |

| 7A. | | |

| 8. | | |

| 9. | | |

| 9A. | | |

| 9B. | | |

| | |

| PART III | |

| | |

| 10 | | |

| 11 | | |

| 12 | | |

| 13 | | |

| 14 | | |

| | |

| PART IV | |

| | |

| 15 | | |

| | |

| | |

| 16 | | |

| | |

FORWARD-LOOKING STATEMENTS

This report contains “forward-looking statements,” as defined in the Private Securities Litigation Reform Act of 1995. These statements, including statements about COVID-19 and the merger (the “Merger”) between a subsidiary of the Company and IHS Markit Ltd. (“IHS Markit”), which express management’s current views concerning future events, trends, contingencies or results, appear at various places in this report and use words like “anticipate,” “assume,” “believe,” “continue,” “estimate,” “expect,” “forecast,” “future,” “intend,” “plan,” “potential,” “predict,” “project,” “strategy,” “target” and similar terms, and future or conditional tense verbs like “could,” “may,” “might,” “should,” “will” and “would.” For example, management may use forward-looking statements when addressing topics such as: the outcome of contingencies; future actions by regulators; changes in the Company’s business strategies and methods of generating revenue; the development and performance of the Company’s services and products; the expected impact of acquisitions and dispositions; the Company’s effective tax rates; and the Company’s cost structure, dividend policy, cash flows or liquidity.

Forward-looking statements are subject to inherent risks and uncertainties. Factors that could cause actual results to differ materially from those expressed or implied in forward-looking statements include, among other things:

•worldwide economic, financial, political and regulatory conditions, and factors that contribute to uncertainty and volatility, natural and man-made disasters, civil unrest, pandemics (e.g., COVID-19), geopolitical uncertainty, and conditions that may result from legislative, regulatory, trade and policy changes;

•the satisfaction of the conditions precedent to consummation of the Merger, including the ability to secure regulatory approvals on the terms expected, the Company’s shareholder approval and the IHS Markit shareholder approval at all or in a timely manner;

•the occurrence of events that may give rise to a right of one or both of the parties to terminate the merger agreement;

•uncertainty relating to the impact of the Merger on the businesses of the Company and IHS Markit, including potential adverse reactions or changes to the market price of the Company’s common stock and IHS Markit shares resulting from the announcement or completion of the Merger and changes to existing business relationships during the pendency of the acquisition that could affect the Company’s and/or IHS Markit’s financial performance;

•risks relating to the value of the Company’s stock to be issued in the Merger, significant transaction costs and/or unknown liabilities;

•the ability of the Company to successfully integrate IHS Markit’s operations and retain and hire key personnel of both companies;

•the ability of the Company to retain customers and to implement its plans, forecasts and other expectations with respect to IHS Markit’s business after the consummation of the Merger and realize expected synergies;

•business disruption following the Merger;

•the possibility that the Merger may be more expensive to complete than anticipated, including as a result of unexpected factors or events;

•the Company’s and IHS Markit’s ability to meet expectations regarding the accounting and tax treatments of the Merger;

•the Company’s ability to successfully recover should it experience a disaster or other business continuity problem from a hurricane, flood, earthquake, terrorist attack, pandemic, security breach, cyber attack, power loss, telecommunications failure or other natural or man-made event, including the ability to function remotely during long-term disruptions such as the ongoing COVID-19 pandemic;

•the Company’s ability to maintain adequate physical, technical and administrative safeguards to protect the security of confidential information and data, and the potential for a system or network disruption that results in regulatory penalties and remedial costs or improper disclosure of confidential information or data;

•the outcome of litigation, government and regulatory proceedings, investigations and inquiries;

•the health of debt and equity markets, including credit quality and spreads, the level of liquidity and future debt issuances, demand for investment products that track indices and assessments and trading volumes of certain exchange traded derivatives;

•the demand and market for credit ratings in and across the sectors and geographies where the Company operates;

•concerns in the marketplace affecting the Company’s credibility or otherwise affecting market perceptions of the integrity or utility of independent credit ratings, benchmarks and indices;

•the effect of competitive products and pricing, including the level of success of new product developments and global expansion;

•the Company’s exposure to potential criminal sanctions or civil penalties for noncompliance with foreign and U.S. laws and regulations that are applicable in the domestic and international jurisdictions in which it operates, including sanctions laws relating to countries such as Iran, Russia, Sudan, Syria and Venezuela, anti-corruption laws such as the U.S. Foreign Corrupt Practices Act and the U.K. Bribery Act of 2010, and local laws prohibiting corrupt payments to government officials, as well as import and export restrictions;

•the continuously evolving regulatory environment, in Europe, the United States and elsewhere, affecting S&P Global Ratings, S&P Global Platts, S&P Dow Jones Indices, and S&P Global Market Intelligence, including the Company’s compliance therewith;

•the Company’s ability to make acquisitions and dispositions and successfully integrate the businesses we acquire;

•consolidation in the Company’s end-customer markets;

•the introduction of competing products or technologies by other companies;

•the impact of customer cost-cutting pressures, including in the financial services industry and the commodities markets;

•a decline in the demand for credit risk management tools by financial institutions;

•the level of merger and acquisition activity in the United States and abroad;

•the volatility and health of the energy and commodities markets;

•our ability to attract, incentivize and retain key employees;

•the level of the Company’s future cash flows and capital investments;

•the impact on the Company’s revenue and net income caused by fluctuations in foreign currency exchange rates;

•the Company's ability to adjust to changes in European and United Kingdom markets as the United Kingdom leaves the European Union, and the impact of the United Kingdom’s departure on our credit rating activities and other offerings in the European Union and United Kingdom; and

•the impact of changes in applicable tax or accounting requirements on the Company.

The factors noted above are not exhaustive. The Company and its subsidiaries operate in a dynamic business environment in which new risks emerge frequently. Accordingly, the Company cautions readers not to place undue reliance on any forward-looking statements, which speak only as of the dates on which they are made. The Company undertakes no obligation to update or revise any forward-looking statement to reflect events or circumstances arising after the date on which it is made, except as required by applicable law. Further information about the Company’s businesses, including information about factors that could materially affect its results of operations and financial condition, is contained in the Company’s filings with the SEC, including Item 1A, Risk Factors, in this Annual Report on Form 10-K.

PART I

Item 1. Business

Overview

S&P Global Inc. (together with its consolidated subsidiaries, the “Company,” the “Registrant,” “we,” “us” or “our”) is a leading provider of transparent and independent ratings, benchmarks, analytics and data to the capital and commodity markets worldwide. The capital markets include asset managers, investment banks, commercial banks, insurance companies, exchanges, trading firms and issuers; and the commodity markets include producers, traders and intermediaries within energy, metals, petrochemicals and agriculture. We serve our global customers through a broad range of products and services available through both third-party and proprietary distribution channels. We were incorporated in December of 1925 under the laws of the state of New York.

Our Businesses

Our operations consist of four reportable segments: S&P Global Ratings ("Ratings"), S&P Global Market Intelligence ("Market Intelligence"), S&P Global Platts ("Platts") and S&P Dow Jones Indices ("Indices"). For a discussion on the competitive conditions in our businesses, see “MD&A – Segment Review” contained in Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations, in this Annual Report on Form 10-K.

Beginning in the first quarter of 2019, the contract obligations for revenue from Kensho Technologies Inc.’s (“Kensho”) major customers were transferred to Market Intelligence for fulfillment. As a result of this transfer, from January 1, 2019 revenue from contracts with Kensho’s customers is reflected in Market Intelligence’s results. In 2018, the revenue from contracts with Kensho’s customers was reported in Corporate revenue. See Note 2 – Acquisitions and Divestitures to the consolidated financial statements under Item 8, Consolidated Financial Statements and Supplementary Data, in this Annual Report on Form 10-K.

In November of 2020, S&P Global and IHS Markit Ltd ("IHS Markit") entered into a merger agreement, pursuant to which, among other things, a subsidiary of S&P Global will merge with and into IHS Markit, with IHS Markit surviving the merger as a wholly owned subsidiary of S&P Global. Under the terms of the merger agreement, each share of IHS Markit issued and outstanding (other than excluded shares and dissenting shares) will be converted into the right to receive 0.2838 fully paid and nonassessable shares of S&P Global common stock (and, if applicable, cash in lieu of fractional shares, without interest), less any applicable withholding taxes. As of December 31, 2020, IHS Markit had approximately 396.6 million shares outstanding. Subject to certain closing conditions, the merger is expected to be completed in the second half of 2021.

Ratings

Ratings is an independent provider of credit ratings, research, and analytics, offering investors and other market participants information, ratings and benchmarks. Credit ratings are one of several tools investors can use when making decisions about purchasing bonds and other fixed income investments. They are opinions about credit risk and our ratings express our opinion about the ability and willingness of an issuer, such as a corporation or state or city government, to meet its financial obligations in full and on time. Our credit ratings can also relate to the credit quality of an individual debt issue, such as a corporate or municipal bond, and the relative likelihood that the debt issue may default.

With offices in over 25 countries around the world, Ratings is an important part of the world's financial infrastructure and has played a leading role for over 150 years in providing investors with information and independent benchmarks for their investment and financial decisions as well as access to the capital markets. The key constituents Ratings serves are investors, corporations, governments, municipalities, commercial and investment banks, insurance companies, asset managers, and other debt issuers.

As the capital markets continue to evolve, Ratings is well-positioned to capitalize on opportunities, driven by continuing regulatory changes, through its global network, well-established position in corporate markets and strong investor reputation.

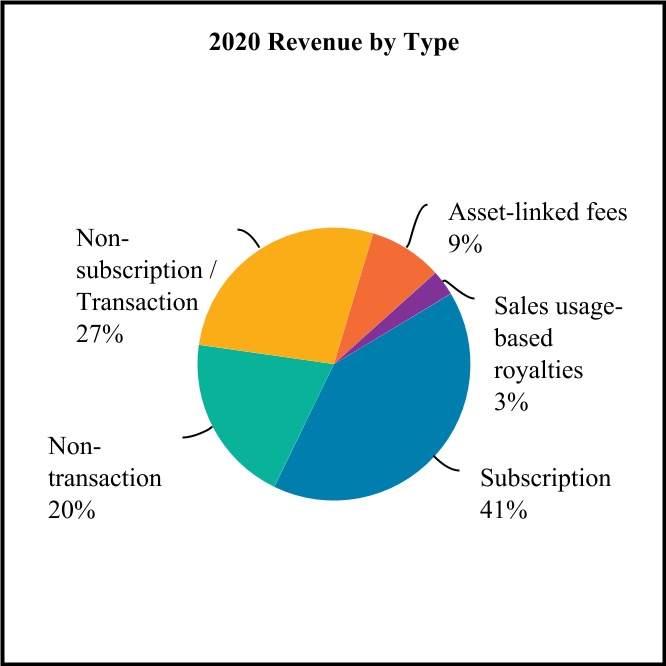

Ratings disaggregates its revenue between transaction and non-transaction. Transaction revenue primarily includes fees associated with:

•ratings related to new issuance of corporate and government debt instruments, as well as structured finance debt instruments;

•bank loan ratings; and

•corporate credit estimates, which are intended, based on an abbreviated analysis, to provide an indication of our opinion regarding creditworthiness of a company which does not currently have a Ratings credit rating.

Non-transaction revenue primarily includes fees for surveillance of a credit rating, annual fees for customer relationship-based pricing programs, fees for entity credit ratings and global research and analytics at CRISIL.

Market Intelligence

Market Intelligence's portfolio of capabilities are designed to help investment professionals, government agencies, corporations and universities track performance, generate alpha, identify investment ideas, understand competitive and industry dynamics, perform evaluations and assess credit risk. Key customers served by Market Intelligence include investment managers, investment banks, private equity firms, insurance companies, commercial banks, corporations, professional services firms, government agencies and regulators.

Market Intelligence includes the following business lines:

•Desktop — a product suite that provides data, analytics and third-party research for global finance professionals, which includes the Market Intelligence Desktop (which are inclusive of the S&P Capital IQ and SNL Desktop products);

•Data Management Solutions — integrated bulk data feeds and application programming interfaces that can be customized, which includes Compustat, GICS, Point In Time Financials and CUSIP; and

•Credit Risk Solutions — commercial arm that sells Ratings' credit ratings and related data, analytics and research, which includes subscription-based offerings, RatingsDirect® and RatingsXpress®; and Credit Analytics.

Subscription revenue at Market Intelligence is primarily derived from distribution of data, analytics, third-party research, and credit ratings-related information primarily through web-based channels, including Market Intelligence Desktop, RatingsDirect®, RatingsXpress®, and Credit Analytics. Non-subscription revenue at Market Intelligence is primarily related to certain advisory, pricing and analytical services.

Platts

Platts is the leading independent provider of information and benchmark prices for the commodity and energy markets. Platts provides essential price data, analytics, and industry insight enabling the commodity and energy markets to perform with greater transparency and efficiency. Key customers served by Platts include producers, traders and intermediaries within the energy, petrochemicals, metals and agriculture markets.

Platts' revenue is generated primarily through the following sources:

•Subscription revenue — primarily from subscriptions to our real-time news, market data and price assessments, along with other information products;

•Sales usage-based royalties — primarily from licensing of our proprietary market price data and price assessments to commodity exchanges; and

•Non-subscription revenue — conference sponsorship, consulting engagements, and events.

Indices

Indices is a global index provider maintaining a wide variety of indices to meet an array of investor needs. Indices’ mission is to provide transparent benchmarks to help with decision making, collaborate with the financial community to create innovative products and provide investors with tools to monitor world markets.

Indices derives revenue from asset-linked fees when investors direct funds into its proprietary designed or owned indexes, sales-usage royalties of its indices, and to a lesser extent data subscription arrangements. Specifically, Indices generates revenue from the following sources:

•Investment vehicles — asset-linked fees such as exchange traded funds (“ETFs”) and mutual funds, that are based on the S&P Dow Jones Indices' benchmarks that generate revenue through fees based on assets and underlying funds;

•Exchange traded derivatives — generate sales usage-based royalties based on trading volumes of derivatives contracts listed on various exchanges;

•Index-related licensing fees — fixed or variable annual and per-issue asset-linked fees for over-the-counter derivatives and retail-structured products; and

•Data and customized index subscription fees — fees from supporting index fund management, portfolio analytics and research.

Segment and Geographic Data

The relative contribution of our reportable segments to operating revenue, operating profit, long-lived assets and geographic area for the three years ended December 31, 2020 are included in Note 12 – Segment and Geographic Information to the consolidated financial statements under Item 8, Consolidated Financial Statements and Supplementary Data, in this Annual Report on Form 10-K.

Human Capital

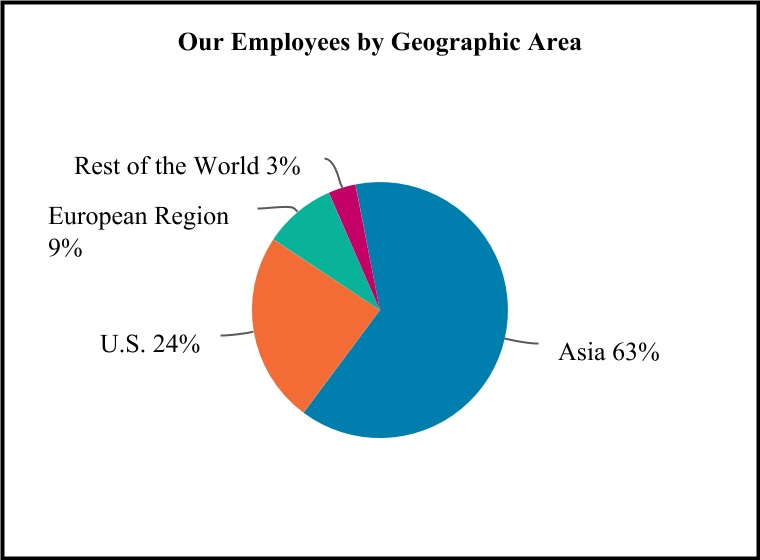

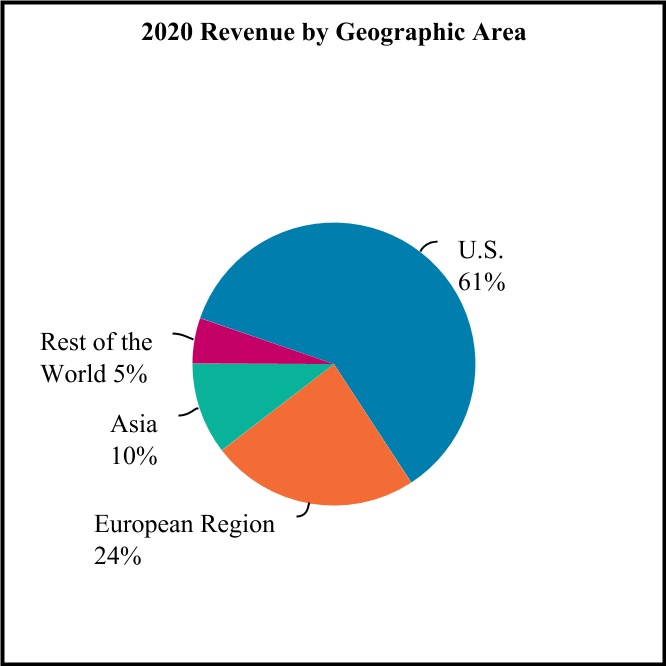

As of December 31, 2020, we had approximately 23,000 permanent employees located worldwide, including around 14,550 in Asia, 5,550 in the U.S., 2,100 in the European region, and 800 in the rest of the world.

We invest in our success as a global Company by investing in our employees across the world through our “people first” approach to human capital management, aimed at supporting everyone who works for us to reach their full potential.

Board Oversight & Management Implementation of Human Capital Strategy

Our Board of Directors and Company management view effective human capital management as critical to the Company’s ability to execute its strategy.

As a result, the Board of Directors and the Compensation and Leadership Development Committee oversee and regularly engage with our CEO, Chief People Officer and senior leadership on a broad range of human capital management topics, including culture, talent and performance management, succession planning, compensation and benefits, diversity and inclusion, and employee engagement and retention.

At the management level, our Chief People Officer is responsible for leading the development and execution of the Company’s human capital management strategy, also referred to as our “People” strategy, working together with other senior leaders across the Company. Among other things, this includes promoting an inclusive and performance-driven workplace culture; managing the Company’s initiatives to attract, recruit, develop and retain the high-quality talent needed to ensure S&P Global is equipped with the right skillsets and intellectual capital to deliver on current and future business needs; and overseeing the design of the Company’s compensation, benefits and wellness programs. In connection with these responsibilities, the Chief People Officer also partners with our Corporate Responsibility & Diversity team on the development and execution of the Company’s diversity and inclusion roadmap and works closely with the CEO on executive succession planning and development of the talent succession pipeline for the Company’s Operating Committee.

The Company’s short-term incentive plan further reflects the significant role our people play in driving our enterprise strategy to Power the Markets of the Future by linking executive pay outcomes under our enterprise and division balanced scorecards to the achievement of strategic people priorities. In 2020, we focused on delivering on the following strategic People priorities:

•Creating an inclusive performance-driven culture that drives employee engagement and aligns with our purpose of accelerating progress in the world;

•Promoting career mobility and attracting and retaining the best people; and

•Improving diversity in overall representation through talent acquisition, advancement and retention.

To achieve our strategic people objectives, we support our employees through human capital management strategies that include diversity and inclusion initiatives, learning and development programs, competitive compensation and benefits programs, workplace health and safety measures, and mechanisms for talent retention, engagement and management accountability. Examples of some of our key initiatives and programs in these focus areas are included below.

Diversity & Inclusion (D&I)

Our ability to attract and retain a diverse and inclusive workforce is critical to our long-term strategy, driving business growth and innovation and empowering our people to achieve their full potential. In connection with our commitment to create a diverse and inclusive workplace, we have taken the following steps to foster an environment where our people can bring their whole selves to work:

•In 2019, we merged our Corporate Responsibility and D&I teams, in recognition of the critical importance of diversity to our firm’s standing and future. Our People team partners with Corporate Responsibility & Diversity to lead our global D&I efforts. These efforts focus on hiring and retaining diverse talent, building an inclusive culture and enabling our people to advance their careers with us. In 2020, we have increased the people and resources devoted to our D&I programs and initiatives.

•An executive D&I Council, co-chaired by our CEO and Chief People Officer, directs and oversees our enterprise-wide diversity and inclusion strategy, advancing and ensuring coordination and accountability for diversity and inclusion programs across the organization.

•We also measure progress on our diversity and inclusion programs as part of our enterprise and division balanced scorecards, which are reviewed by the CEO quarterly and the Board at least biannually, and impact short-term incentive compensation.

•We connect colleagues across our organization through our employee resource groups. These global and employee-led networks offer career experiences and network-building opportunities that foster professional development and support workplace diversity.

Learning and Development Programs

We are committed to continuous learning and invest in development tools and programs at every level across our organization to help employees expand their knowledge, skills and experience and guide career advancement in support of our long-term strategy.

•Technology Training - We offer internal technology training programs to enhance the technology skills of our workforce and accelerate our ability to solve complex problems using a multidisciplinary blend of data inference, algorithm development and technology education for all employees.

•Career Coaching - We launched a career coaching program, offering customized support through global career coaches, to empower people to take ownership of their career and help them navigate their career path and opportunities to grow within S&P Global.

•Leadership Development - We invest in developing leaders at all levels of our organization through targeted programs designed to foster leadership excellence in career managers, develop emerging leaders and strengthen our executive talent bench, providing a robust internal succession pipeline for our Operating Committee.

Competitive Compensation and Benefits Programs

We believe compensation and benefits programs are critical to the overall employee experience. Offering market competitive, people-centric and performance driven compensation and benefits is key to our recruitment, talent management and retention strategies. As a result, management regularly assesses employee feedback, competitor research and market data to ensure our programs remain competitive and are designed with our people’s physical, financial, work-life, mental and emotional health and wellbeing in mind. Based on these insights, we have introduced new and enhanced “people first” benefits in 2018 through 2020 to advance employees’ wellbeing at work and beyond in support of our “people first” philosophy.

Workplace Health and Safety

The health and safety of our people working around the globe is a top priority, and our facilities worldwide follow rigorous, internally and externally audited, occupational health and safety policies.

We also recognize that protecting the health, safety and wellbeing of our employees is crucial to our ability to ensure crises like the global COVID-19 pandemic are effectively managed. In response to the COVID-19 pandemic, we established a crisis management committee in January to lead a coordinated workplace safety strategy and acted quickly implementing significant changes across the organization to protect our people and the communities in which we operate.

As a result of these actions, a majority of our people were working from home by late March and continue to work remotely, as we evolve our preparedness strategy for office reopenings to integrate key learnings, safety measures and employee feedback to rethink the future of work. In 2020, we also appointed our first Chief Medical Advisor to help inform decision-making on the Company’s pandemic response, hosted bi-weekly global town halls to keep our people informed about health, safety and remote working logistics, and introduced expanded health and wellness benefits to help our people cope with the health impacts of COVID-19, including:

•Expanding global care leave to 10 business days caring for a sick or healthy family member;

•Increasing minimum global sick leave to 10 paid business days while being treated for COVID-19;

•Committing to pay any employees who contract COVID-19;

•Committing to provide unlimited paid leave following loss of a loved one, and three months’ pay to family members following loss of an employee;

•Providing added flexibility for those working from home while caring for children/family; and

•Expanding telemedicine resources and access to mental health services.

Retention and Engagement

In order to attract and retain the high-quality talent needed to execute our long-term strategy to Power the Markets of the Future, we believe it is critical for our people to feel motivated and empowered. As a result, we strive to create a unified and inclusive workplace culture that promotes employee engagement, satisfaction and performance; and that reflects our common corporate purpose and values of Relevance, Integrity and Excellence.

We invite employee feedback through a variety of channels for open communication and engagement, including small group employee round-table discussions with our business leaders and members of our Board of Directors, our annual employee VIBE survey, as well as more frequent check-ins through employee “Pulse” surveys. The annual VIBE survey allows us to track progress in critical areas, such as workplace pride and satisfaction and inclusive culture, and gather actionable insights for improvements to our people strategy. We encourage managers to share VIBE survey results with their teams, prioritize action areas and pursue solutions. To reinforce management accountability, we also track employee survey scores in our enterprise and division balanced scorecards, with outcomes against survey engagement targets impacting short-term incentive outcomes.

Available Information

The Company's investor kit includes Annual Reports on Form 10-K, Proxy Statements, Quarterly Reports on Form 10-Q, current reports on Form 8-K, the current earnings release and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange Act. For online access, go to http://investor.spglobal.com. Requests for printed copies, free of charge, can be e-mailed to investor.relations@spglobal.com or mailed to Investor Relations, S&P Global Inc., 55 Water Street, New York, NY 10041-0001. Interested parties can also call Investor Relations toll-free at 866-436-8502 (domestic callers) or 212-438-2192 (international callers). The information on our website is not, and shall not be deemed to be part hereof or incorporated into this or any of our filings with the Securities and Exchange Commission (“SEC”).

Access to more than 10 years of the Company's filings made with the SEC is available through the Company's Investor Relations website. Go to http://investor.spglobal.com and click on the SEC Filings link. In addition, these filings are available to the public on the Commission's website through their EDGAR filing system at www.sec.gov. Interested parties may also read and copy materials that the Company has filed with the SEC at the SEC's public reference room located at 100 F Street, NE, Washington, D.C. 20549 on official business days between the hours of 10AM and 3PM. Please call the Commission at 1-800-SEC-0330 for further information on the public reference room.

Item 1A. Risk Factors

The following risk factors and other information included in this annual report on Form 10-K should be carefully considered. The risks and uncertainties described below are not the only ones we face. These risks could materially and adversely affect our business, financial condition and results of operations. Additional risks and uncertainties not presently known to us or which we currently believe to be immaterial may also impair our business operations.

We operate in the capital and commodities markets. The capital markets include asset managers, investment banks, commercial banks, insurance companies, exchanges, trading firms, and issuers; the commodities markets include producers, traders and intermediaries within energy, metals, petrochemicals and agriculture. Certain risk factors are applicable to certain of our individual segments while other risk factors are applicable Company-wide.

Merger Risks

The Merger is subject to conditions, some or all of which may not be satisfied, or completed on a timely basis, if at all. Failure to complete, or unexpected delays in completing, the merger or any termination of the Merger Agreement could have material adverse effects on us.

On November 29, 2020, we, our wholly-owned subsidiary, Sapphire Subsidiary, Ltd., a Bermuda exempted company limited by shares (the “Merger Sub”), and IHS Markit, entered into an Agreement and Plan of Merger (as amended on January 20, 2021, the “Merger Agreement”), pursuant to which Merger Sub will merge with and into IHS Markit, with IHS Markit surviving such merger as a wholly-owned, our direct subsidiary. Completion of the Merger is subject to a number of conditions, including, among other things, the receipt of approval from our shareholders and the shareholders of IHS Markit, and the receipt of certain regulatory approvals, as well as the accuracy of all representations and warranties of IHS Markit and the absence of a material adverse effect since the date of the merger agreement, which make the completion and timing of the Merger uncertain. In addition, the ongoing COVID-19 pandemic could delay the receipt of certain regulatory approvals. The failure to satisfy all of the required conditions could delay the completion of the merger for a significant period of time or prevent it from occurring at all. There can be no assurance that the conditions to the completion of the Merger will be satisfied or waived or that the Merger will be completed.

In addition, either S&P Global or IHS Markit may terminate the Merger Agreement under certain circumstances, including if the Merger is not completed by the outside date determined pursuant to the Merger Agreement. In certain circumstances, upon termination of the Merger Agreement, S&P Global would be required to pay a termination fee of $2.380 billion to IHS Markit, and in certain circumstances, IHS Markit would be required to pay a termination fee of $1.075 billion to S&P Global, upon termination of the Merger Agreement, each as contemplated by the Merger Agreement.

Moreover, at any time before or after the completion of the Merger, and notwithstanding the termination of applicable waiting periods, the applicable U.S. or foreign regulatory authorities or any state attorney general could take such action under antitrust or other applicable laws as such party deems necessary or desirable in the public interest. Such action could include, among other things, seeking to enjoin the completion of the merger or seeking divestiture of substantial assets of the parties.

In addition, shareholders of both S&P Global and IHS Markit have initiated private actions challenging, seeking to enjoin or seeking to impose conditions on the Merger. We may be required to devote significant resources to resolve such matters which may have a negative effect on our ability to complete the Merger and if we do complete the Merger may have a material adverse effect on our financial position, results of operations and cash flows.

If the Merger is not completed, we may be materially adversely affected and, without realizing any of the benefits of having completed the Merger, will be subject to a number of risks, including the following: the market price of our common stock could decline; if the Merger agreement is terminated and our board seeks another business combination, shareholders cannot be certain that we will be able to find a party willing to enter into a transaction on terms equivalent to or more attractive than the terms that IHS Markit has agreed to in the Merger Agreement; we will not realize the benefit of the time and resources, financial and otherwise, committed by our management to matters relating to the Merger that could have been devoted to pursuing other beneficial opportunities; we may experience negative reactions from the financial markets or from their respective customers, suppliers or employees; and we will be required to pay its expenses relating to the Merger, such as legal, accounting and financial advisory fees, whether or not the Merger is completed.

In addition, if the Merger is not completed, we could be subject to litigation related to any failure to complete the Merger or related to any enforcement proceeding commenced against such party to perform its obligations under the Merger Agreement. Any of these risks could materially and adversely impact our ongoing business, financial condition, results of operations and the market price of our common stock. Similarly, delays in the completion of the Merger could, among other things, result in

additional transaction costs, loss of revenue or other negative effects associated with delay and uncertainty about completion of the merger and could materially and adversely impact our ongoing business, financial condition, results of operations and the market price of our common stock.

We are subject to business uncertainties and contractual restrictions while the Merger is pending, which could adversely affect our business and operations.

In connection with the pendency of the Merger, it is possible that some customers, suppliers, partners and other persons with whom we have a business relationship may delay or defer certain business decisions or might decide to seek to terminate, change or renegotiate their relationships with us as a result of the Merger or otherwise, which could negatively affect our revenue, earnings and/or cash flow, as well as the market price of our common stock, regardless of whether the Merger is completed. In addition, under the terms of the Merger Agreement, we are subject to certain restrictions on the conduct of its business prior to completing the Merger, which may adversely affect our ability to execute certain of its business strategies, including the ability in certain cases to acquire or dispose of assets or pay dividends or incur capital expenditures above a certain amount. Such limitations could adversely our business and operations prior to the completion of the Merger.

We may be unable to successfully integrate the businesses of S&P Global and IHS Markit or realize the anticipated benefits of the Merger.

The success of the Merger will depend, in part, on our ability to successfully combine and integrate our existing business with that of IHS Markit, and realize the anticipated benefits, including synergies, cost savings, innovation and technological opportunities and operational efficiencies from the Merger in a manner that does not materially disrupt existing customer, supplier and employee relations and does not result in decreased revenues due to losses of, or decreases in demand by, customers. Our ability to realize these anticipated benefits is subject to certain risks, including whether we will perform as expected, the possibility that we paid more for IHS Markit than the value we will derive from the Merger and the assumption of known and unknown liabilities of IHS Markit. If we are unable to achieve these objectives within the anticipated time frame, or at all, the anticipated benefits may not be realized fully or at all, or may take longer to realize than expected, and the value of our common stock may decline. We may fail to realize some or all of the anticipated benefits of the Merger if the integration process takes longer than expected or is more costly than expected.

The integration of the two companies may result in material challenges, including: managing a larger, more complex combined business; maintaining employee morale and retaining key management and other employees; retaining existing business and operational relationships, including customers, suppliers and employees and other counterparties, as may be impacted by contracts containing consent and/or other provisions that may be triggered by the merger, and attracting new business and operational relationships; consolidating corporate and administrative infrastructures and eliminating duplicative operations, including unanticipated issues in integrating financial reporting, information technology infrastructure, data and content management systems and product platforms, communications and other systems; coordinating geographically separate organizations, including consolidating offices of S&P Global and IHS Markit that are currently in or near the same location; harmonizing both companies’ corporate cultures, operating practices, employee development and compensation programs, internal controls, compliance programs and other policies, procedures and processes; addressing possible differences in business backgrounds, and management philosophies; and unforeseen expenses or delays associated with the Merger.

Many of these factors will be outside of our control, and any one of them could result in delays, increased costs, decreases in the amount of expected revenues and other adverse impacts, which could materially affect the combined company’s business, financial condition and results of operations. Due to legal restrictions, S&P Global and IHS Markit are currently permitted to conduct only limited planning for the integration of the two companies following the Merger. The actual integration may result in additional and unforeseen expenses, and the anticipated benefits of the integration plan may not be realized on a timely basis, if at all.

We expect to incur substantial expenses and devote significant resources in connection with the completion of the Merger and the integration of the IHS Markit and our businesses.

We expect to incur substantial expenses, and devote significant resources, in connection with the completion of the Merger and the integration of a large number of processes, policies, procedures, operations, technologies and systems of S&P Global and IHS Markit in connection with the Merger. The management of the combined company may face significant challenges in implementing such integration, many of which may be beyond the control of management and which may result in increased costs and diversion of management’s time and energy, as well as materially adversely impact the anticipated synergies of the Merger and the business, financial condition and results of operations of the combined company. The integration process and other disruptions resulting from the Merger may also adversely affect the combined company’s relationships with employees, suppliers, customers, distributors and others with whom S&P Global and IHS Markit have business or other dealings, and difficulties in integrating the businesses of S&P Global and IHS Markit could harm the reputation of the combined company.

These incremental transaction-related costs may exceed the savings the combined company expects to achieve from the elimination of duplicative costs and the realization of other efficiencies related to the integration of the businesses, particularly in the near term and in the event there are material unanticipated costs. Factors beyond the parties’ control could affect the total amount or timing of these expenses, many of which, by their nature, are difficult to estimate accurately. Some of these expenses have already been incurred or may be incurred regardless of whether the merger is completed.

If the Merger is completed, our shareholders’ ownership percentage will be diluted.

If the Merger is completed, we will issue to IHS Markit shareholders shares of our common stock. As a result of the issuance of these shares of our common stock, our shareholders will own a smaller percentage of the combined company after the Merger and will therefore have a reduced voting interest.

During the pendency of the merger our ability to execute share repurchases will be restricted.

While the Merger is pending, we will have limited opportunities to launch repurchase programs and there can no guarantee that we will be able to successfully execute a repurchase program when a window of opportunity presents itself.

COVID-19 Risks

The COVID-19 pandemic and its effects have affected, and may have a material adverse effect on, our results of operations.

Following the outbreak of an infectious respiratory illness caused by the 2019 novel coronavirus (“COVID-19”), the World Health Organization declared a global emergency on January 30, 2020 and subsequently declared COVID-19 as a pandemic on March 11, 2020.

COVID-19 has spread globally, including in the United States, the United Kingdom, the European Union and other jurisdictions in which we operate. Governments across the world have taken steps to contain the virus by restricting human movement through numerous measures including travel bans and restrictions, social distancing, quarantines, shelter in place orders, enhanced health screenings at ports of entry and elsewhere, and business shutdowns. Continuation of the shutdown of businesses and entire industries, increases in unemployment, implementation of furloughs, lost wages across populations and a significant drop in consumer and business spending, resulted in a recession in the United States during 2020. While vaccines have become available, their availability and distribution is at the discretion of government agencies and it is difficult to ascertain how and when they will impact economic activity. There are no comparable recent events that can provide guidance as to the effect of the COVID-19 global pandemic, and, as a result, the ultimate impact of the coronavirus outbreak or a similar health epidemic is highly uncertain. The effects of COVID-19 have impacted our operations and may ultimately have a material adverse impact on our results of operations in the future. The extent to which the pandemic will continue to affect our businesses, financial condition and results of operations will depend on future developments, which are highly uncertain and cannot be predicted.

Increased volatility and uncertainty in the global economy, and the financial and commodities markets

The global economy has been disrupted as a result of the ongoing health crisis and the financial and commodities markets have reacted with unprecedented volatility. Governmental authorities worldwide have taken increased measures to stabilize the markets and support economic growth. The success of these measures is unknown, and they may not be sufficient to address the market dislocations or avert severe and prolonged reductions in economic activity. Even after the pandemic subsides, the U.S. economy and other major economies may continue to experience a recession, and we anticipate our businesses would be materially and adversely affected by a prolonged recession in the U.S. and other major markets. Because there are no comparable recent events that can provide guidance on the impact to the global economy, we cannot predict the extent to which our business may be impacted. In addition, the increase in revenue of Ratings in 2020 was primarily driven by higher corporate bond issuance in the U.S. mainly resulting from historically low borrowing costs, increased borrowing demand from companies to increase their liquidity in light of uncertainties associated with COVID-19, and central bank lending actions. There can be no guarantee that such favorable conditions would continue in the future, and our businesses, financial condition and results of operations could be negatively affected absent such favorable conditions. Moreover, the unprecedented volatility observed in the markets since the outset of COVID-19 may result in sudden unexpected changes in market structures that were not previously anticipated by laws, rules, regulations or general market practices. Risks posed to our businesses, financial condition and results of operations from volatility in the financial and commodities markets are described in the risk factor below entitled, “Changes in the volume of securities issued and traded in domestic and/or global capital markets, asset levels and flows into investment products, changes in interest rates and volatility in the financial markets, and volatility in the commodities markets impact our business, financial condition or results of operations”.

Decreased demand for our subscription services

Our clients are being impacted to varying degrees. Some may no longer be in business by the time the COVID-19 pandemic comes to an end, others will face significant spending constraints in order to continue to operate, and others may reduce their workforces permanently. As a result of the impact on our clients, our subscription services may face pricing pressure on renewals, delayed renewals, and challenges to new sales which would in turn reduce revenue, ultimately impacting our results of operations. Limited human mobility has, among other things, significantly reduced demand for energy used in transportation, and the decrease in demand has been exacerbated by political tensions between large oil producing countries.

This could put additional pressure on Platts clients and translate into slower demand for our subscription and related products and services. Moreover, while our business continuity program has been effective to date, the current restrictions on human mobility limit our ability to interact with subscribers and effectively demonstrate new products and may have a negative effect on our ability to secure new subscriptions and renewals.

Our businesses assess and analyze the impact of economic events

Our divisions are all actively engaged in analyzing and providing views on the quickly evolving economic conditions. We are publishing articles and research pieces that attempt to assess the impact of the COVID-19 pandemic on the world economy and its components, both geographic and sectoral. In addition, we are taking actions (including, but not limited to, rating actions, revising the composition of our indices, etc.), consistent with our business procedures, in response to the evolving conditions. Notwithstanding the care we take in carrying out our work, the views and assumptions we express, the conclusions we draw, the actions we take, and the work our divisions are producing today are likely to be heavily scrutinized with the benefit of hindsight. We have faced significant regulatory and media scrutiny following prior periods of volatility and economic uncertainty. Such scrutiny has in the past and may in the future impact our reputation, brand and credibility and result in government and regulatory proceedings, investigations, inquiries and litigation. See the below risk factors entitled “Exposure to litigation and government and regulatory proceedings, investigations and inquiries could have a material adverse effect on our business, financial condition or results of operations” and “Our reputation, credibility, and brand are key assets and competitive advantages of our Company and our business may be affected by how we are perceived in the marketplace”.

Business continuity

Our business continuity program has been effective to date. Since mid-March 2020, nearly our entire employee population was working remotely. While we have been able to continue our operations during this time, maintaining a remote work environment for an extended period of time may have a material adverse effect on our productivity and our ability to meet the needs of our clients and exposes us to operational risks. See the below risk factor entitled “Our inability to successfully recover should we experience a disaster or other business continuity problem could cause material financial loss, loss of human capital, regulatory actions, reputational harm or legal liability”. In addition, a portion of our information technology resources have been diverted to establishing and maintaining an infrastructure that supports a sustained remote working environment. Such efforts limit the resources available for improvement and innovation projects. Moreover, given the extent to which we are utilizing a remote working environment, we face increased vulnerability. Although there has not been a cyber attack that has had a material adverse effect on the Company to date, we have noted an increase in cyber threats targeted at our remote work environment and there can be no assurance that there will not be a material adverse effect in the future. See the below risk factor entitled “We are exposed to risks related to cybersecurity and protection of confidential information”. In addition, while our employee base currently has adequate resources to pursue new clients or expand existing relationships, we have no control over the business continuity resources available to our clients. As a result, our ability to maintain, expand, or establish new client relationships may be limited.

Business, Operational and Regulatory Risks

Changes in the volume of securities issued and traded in domestic and/or global capital markets, asset levels and flows into investment products, changes in interest rates and volatility in the financial markets, and volatility in the commodities markets impact our business, financial condition or results of operations.

•Our business is impacted by general economic conditions and volatility in the U.S. and world financial markets.

•Economic conditions and volatility across the globe are generally affected by negative or uncertain economic and political conditions. In addition, natural and man-made disasters as well as the outbreak of pandemic or contagious diseases introduce volatility and uncertainty into the global capital and commodities markets and negatively impact general economic conditions. Volatile, negative or uncertain economic and political conditions in our significant markets have undermined and could in the future undermine business confidence in our significant markets or in other markets, which are increasingly interdependent. Because we operate globally and have significant businesses in many markets, increased volatility or an economic slowdown in any of those markets could adversely affect our results of operations.

•Since a significant component of our credit-rating based revenue is transaction-based, and is essentially dependent on the number and dollar volume of debt securities issued in the capital markets, unfavorable financial or economic

conditions that either reduce investor demand for debt securities or reduce issuers’ willingness or ability to issue such securities tend to reduce the number and dollar volume of debt issuances for which Ratings provides credit ratings.

•Our Indices business is impacted by market volatility, asset levels of investment products tracking indices, and trading volumes of certain exchange traded derivatives. Volatile capital markets, as well as changing investment styles, among other factors, may influence an investor’s decision to invest in and maintain an investment in an index-linked investment product.

•Increases in interest rates or credit spreads, volatility in financial markets or the interest rate environment, significant political or economic events, defaults of significant issuers and other market and economic factors may negatively impact the general level of debt issuance, the debt issuance plans of certain categories of borrowers, the level of derivatives trading and/or the types of credit-sensitive products being offered, any of which could have a material adverse effect on our business, financial condition or results of operations.

•Our Platts business is impacted by volatility in the commodities markets. Weak economic conditions, especially in our key markets, including the energy industry, could reduce demand for our products, impacting our revenues and margins. As a result of volatility in commodity prices and trading activity in physical commodities and commodities derivatives, we may encounter difficulty in achieving sustained market acceptance of past or future contract terms, which could have a material adverse effect on our financial position, results of operations and cash flows.

•Any weakness in the macroeconomic environment could constrain customer budgets across the markets we serve, potentially leading to a reduction in their employee headcount and a decrease in demand for our subscription-based products.

•The foregoing factors generally affect our performance and could have a material adverse effect on our business, financial condition or results of operations.

We are exposed to risks related to cybersecurity and protection of confidential information.

•Our operations rely on the secure processing, storage and transmission of confidential, sensitive and other types of data and information in our computer systems and networks and those of our third-party vendors.

•All of our businesses have access to material non-public information concerning the Company’s customers, including sovereigns, corporate issuers and other third parties around the world, the unauthorized disclosure of which could affect the trading markets for such customers’ securities and could damage such customers’ competitive positions. The cyber risks the Company faces range from cyber attacks common to most industries, to more sophisticated and targeted attacks, some of which may be carried out by state-sponsored actors, intended to obtain unauthorized access to certain information or systems due in part to our prominence in the global marketplace, such as our ratings on debt issued by sovereigns and corporate issuers, or the composition of our indices. Unauthorized disclosure of this information could cause our customers to lose faith in our ability to protect their confidential information and therefore cause customers to cease doing business with us.

•We experience cyber attacks of varying degrees on a regular basis. Although there has not been a cyber attack that has had a material adverse effect on the Company to date, there can be no assurance that there will not be a material adverse effect in the future.

•Breaches of our or our vendors’ systems and networks, whether from circumvention of security systems, denial-of-service attacks or other cyber attacks, hacking, computer viruses or malware, employee error, malfeasance, physical breaches or other actions, may cause material interruptions or malfunctions in our or such vendors’ websites, applications or data processing, or may compromise the confidentiality and integrity of material information regarding us, our business or our customers. In the ordinary course, our third-parties, including our vendors, are subject to various forms of cyber attacks. To date, such attacks have not resulted in a material adverse impact to our business or operations, but there can be no guarantee we will not experience such an impact.

•Misappropriation, improper modification, destruction, corruption or unavailability of our data and information due to cyber incidents, attacks or other security breaches could damage our brand and reputation, result in litigation and regulatory actions, and lead to loss of customer confidence in our security measures and reliability, which would harm our ability to retain customers and gain new ones.

•Although we devote significant resources to maintain and regularly update our systems and processes that are designed to protect the security of our computer systems, software, networks and other technology assets and the confidentiality, integrity and availability of information belonging to the enterprise and our customers, clients and employees, there is no assurance that all of our security measures will provide absolute security.

•Measures that we take to avoid or mitigate material incidents can be expensive, and may be insufficient, circumvented, or become obsolete. While we have not experienced a material incident to date, any material incident could cause us to experience reputational harm, loss of customers, regulatory actions, sanctions or other statutory penalties, litigation or financial losses that are either not insured against or not fully covered through any insurance maintained by us, and increased expenses related to addressing or mitigating the risks associated with any such material incidents.

•Cyber threats are rapidly evolving and are becoming increasingly sophisticated and include denial of service attacks, ransomware, phishing attacks and payment fraud. Despite our efforts to ensure the integrity of our systems, as cyber threats evolve and become more difficult to detect and successfully defend against, one or more cyber threats might defeat the measures that we or our vendors take to anticipate, detect, avoid or mitigate such threats. Certain techniques used to obtain unauthorized access, introduce malicious software, disable or degrade service, or sabotage systems may be designed to remain dormant until a triggering event and we may be unable to anticipate these techniques or implement adequate preventative measures since techniques change frequently or are not recognized until launched.

•Given the extent to which our businesses are privy to material non-public information concerning our customers, our data could be improperly used, including for insider trading by our employees and third party vendors with access to key systems. We have experienced insider trading incidents involving employees in the past, and it is not always possible to deter misconduct by employees or third party vendors. We take precautions to detect and prevent such activity, including implementing and training on insider trading policies for our employees and contractual obligations for our third party vendors, but such precautions are not guaranteed to deter misconduct. Any breach of our clients’ confidences as a result of employee or third party vendor misconduct could harm our reputation.

•The theft, loss, or misuse of personal data collected, used, stored, or transferred by us to run our business could result in significantly increased security costs or costs related to defending legal claims.

•An actual or perceived breach of our security may harm the market perception of the effectiveness of our security measures and result in damage to our reputation and a loss of confidence in the security of our products and services. Media or other reports of existing or perceived security vulnerabilities in our systems or those of our third-party business partners or service providers can also adversely impact our brand and reputation and materially impact our business.

•Any of the foregoing could have a material adverse effect on our business, financial condition or results of operations.

Changes in the legislative, regulatory, and commercial environments in which we operate may materially and adversely impact our ability to collect, compile, use, and publish data and may impact our financial results.

•Global privacy legislation, enforcement, and policy activity in this area are rapidly expanding and creating a complex regulatory compliance environment. Costs to comply with and implement these privacy-related and data protection measures could be significant. In addition, an inadvertent failure to comply with federal, state, or international privacy-related or data protection laws and regulations despite our best efforts could result in proceedings against us by governmental entities or others.

•Certain types of information we collect, compile, use, and publish, including offerings in all our businesses, and particularly our Market Intelligence business, are subject to regulation by governmental authorities in jurisdictions in which we operate. In addition, there is increasing concern among certain privacy advocates and government regulators regarding marketing and privacy matters, particularly as they relate to individual privacy interests.

•There has been increased public attention regarding the use of personal information and data transfer, accompanied by legislation and regulations intended to strengthen data protection, information security and consumer and personal privacy. The law in these areas continues to develop and the changing nature of privacy laws in the U.S., the European Union (“EU”) and elsewhere could impact our processing of personal and sensitive information of our employees, vendors and customers.

•The EU's comprehensive General Data Privacy Regulation (the “GDPR”) became fully effective in 2018. GDPR requires companies to satisfy requirements regarding the handling of personal and sensitive data, including its use, protection and the ability of persons whose data is stored to correct or delete such data about themselves.

•Failure to comply with GDPR requirements could result in penalties of up to 4% of worldwide revenue. GDPR and other similar laws and regulations, as well as any associated inquiries or investigations or any other government actions, may be costly to comply with, result in negative publicity, increase our operating costs, require significant management time and attention, and subject us to remedies that may harm our business, including fines or demands or orders that we modify or cease existing business practices.

•The California Consumer Privacy Act (“CCPA”) became fully effective January 1, 2020, requiring, among other things, covered companies to provide new disclosures to California consumers, and afford such consumers new abilities to opt-out of certain sales of personal information. The CCPA provides a new private right of action for data breaches and requires companies that process information on California residents to make new disclosures to consumers about their data collection, use and sharing practices and allow consumers to opt out of certain data sharing with third parties.

•Our reputation and brand and our ability to attract new customers could also be adversely impacted if we fail, or are perceived to have failed, to properly respond to security breaches of our or third party’s information technology systems. Such failure to properly respond could also result in similar exposure to liability.

•We devote meaningful time and financial resources to compliance with the GDPR, the CCPA and other current and future applicable international and U.S. privacy, cybersecurity and related laws. We have made capital investments and other expenditures to address cybersecurity preparedness and prevent future breaches, including costs associated with additional security technologies, personnel, experts and credit monitoring services for those whose data has been breached, but there can be no assurance that we will not need to make significant additional expenditures. These costs, which could be material, could adversely impact our results of operations in the period in which they are incurred and may not meaningfully limit the success of future attempts to breach our information technology systems.

•In addition, the EU and other jurisdictions, including China, are considering imposing or have already imposed additional restrictions, including in relation to cross-border transfers of personal data. These requirements are increasing in complexity and number, change frequently and increasingly conflict among the various countries in which we operate, which could result in greater compliance risk and cost for us.

•Continued privacy concerns may result in new or amended laws and regulations. Future laws and regulations with respect to the collection, compilation, use, and publication of information and consumer privacy could result in limitations on our operations, increased compliance or litigation expense, adverse publicity, or loss of revenue, which could have a material adverse effect on our business, financial condition, and results of operations. It is also possible that we could be prohibited from collecting or disseminating certain types of data, which could affect our ability to meet our customers’ needs.

•We may also from time to time be subject to, or face assertions that we are subject to, additional obligations relating to personal data by contract or due to assertions that self-regulatory obligations or industry standards apply to our practices.

Exposure to litigation and government and regulatory proceedings, investigations and inquiries could have a material adverse effect on our business, financial condition or results of operations.

•In the normal course of business, both in the United States and abroad, we and our subsidiaries are defendants in numerous legal proceedings and are often the subject of government and regulatory proceedings, investigations and inquiries, as discussed under Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations, in this Annual Report on Form 10-K and in Note 13 - Commitments and Contingencies to the consolidated financial statements under Item 8, Consolidated Financial Statements and Supplementary Data, in this Annual Report on Form 10-K, and we face the risk that additional proceedings, investigations and inquiries will arise in the future.

•Many of these proceedings, investigations and inquiries relate to the activity of our Ratings, Indices, and Platts businesses. In addition, various government and self-regulatory agencies frequently make inquiries and conduct investigations into our compliance with applicable laws and regulations, including those related to our regulated activities and antitrust matters.

•Any of these proceedings, investigations or inquiries could ultimately result in adverse judgments, damages, fines, penalties or activity restrictions, which could have a material adverse effect on our business, financial condition or results of operations.

•In view of the uncertainty inherent in litigation and government and regulatory enforcement matters, we cannot predict the eventual outcome of the matters we are currently facing or the timing of their resolution, or in most cases reasonably estimate what the eventual judgments, damages, fines, penalties or impact of activity restrictions may be. As a result, we cannot provide assurance that the outcome of the matters we are currently facing or that we may face in the future will not have a material adverse effect on our business, financial condition or results of operations.

•As litigation or the process to resolve pending matters progresses, as the case may be, we continuously review the latest information available and assess our ability to predict the outcome of such matters and the effects, if any, on our consolidated financial condition, cash flows, business and competitive position, which may require that we record liabilities in the consolidated financial statements in future periods.

•Legal proceedings impose additional expenses on the Company and require the attention of senior management to an extent that may significantly reduce their ability to devote time addressing other business issues.

•Risks relating to legal proceedings may be heightened in foreign jurisdictions that lack the legal protections or liability standards comparable to those that exist in the United States. In addition, new laws and regulations have been and may continue to be enacted that establish lower liability standards, shift the burden of proof or relax pleading requirements, thereby increasing the risk of successful litigations against the Company in the United States and in foreign jurisdictions. These litigation risks are often difficult to assess or quantify and could have a material adverse effect on our business, financial condition or results of operations.

•We may not have adequate insurance or reserves to cover these risks, and the existence and magnitude of these risks often remains unknown for substantial periods of time and could have a material adverse effect on our business, financial condition or results of operations.

Increasing regulation of our Ratings business in the United States, Europe and elsewhere can increase our costs of doing business and therefore could have a material adverse effect on our business, financial condition or results of operations.

•The financial services industry is highly regulated, rapidly evolving and subject to the potential for increasing regulation in the United States, Europe and elsewhere. The businesses conducted by Ratings are in certain cases regulated under the Credit Rating Agency Reform Act of 2006 (the “Reform Act”), the Dodd-Frank Wall Street Reform and Consumer Protection Act (the “Dodd-Frank Act”), the U.S. Securities Exchange Act of 1934 (the “Exchange Act”), and/or the laws of the states or other jurisdictions in which they conduct business.

•In the past several years, the U.S. Congress, the International Organization of Securities Commissions ("IOSCO"), the SEC and the European Commission, including through the European Securities Market Authority ("ESMA"), as well as regulators in other countries in which Ratings operates, have been reviewing the role of rating agencies and their processes and the need for greater oversight or regulations concerning the issuance of credit ratings or the activities of credit rating agencies. Other laws, regulations and rules relating to credit rating agencies are being considered by local, national and multinational bodies and are likely to continue to be considered in the future, including provisions seeking to reduce regulatory and investor reliance on credit ratings, and liability standards applicable to credit rating agencies.

•These laws and regulations, and any future rule-making, could result in reduced demand for credit ratings and increased costs, which we may be unable to pass through to customers. In addition, there may be uncertainty over the scope, interpretation and administration of such laws and regulations. We may be required to incur significant expenses in order to comply with such laws and regulations and to mitigate the risk of fines, penalties or other sanctions. Legal proceedings could become increasingly lengthy and there may be uncertainty over and exposure to liability. It is difficult to accurately assess the future impact of legislative and regulatory requirements on our business and our customers’ businesses, and they may affect Ratings’ communications with issuers as part of the rating assignment process, alter the manner in which Ratings’ ratings are developed, affect the manner in which Ratings or its customers or users of credit ratings operate, impact the demand for ratings and alter the economics of the credit ratings business. Each of these developments increases the costs and legal risk associated with the issuance of credit ratings and may have a material adverse effect on our operations, profitability and competitiveness, the demand for credit ratings and the manner in which such ratings are utilized.

•Additional information regarding rating agencies is provided under Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations, in this Annual Report on Form 10-K.

Our Indices and Platts businesses are subject to new and evolving regulatory regimes in Europe and the potential for increased or changing regulations in the United States and elsewhere. Our Indices business is subject to a new regulatory regime in Australia. Our Indices and Platts businesses are subject to additional regulation in Europe. This changing regulatory landscape can increase our exposure, compliance risk and costs of doing business globally and therefore could have a material adverse effect on our business, financial condition or results of operations.

•In addition to the extensive and evolving U.S. laws and regulations, foreign jurisdictions have taken measures to increase regulation of the financial services and commodities industries.

•In October of 2012, IOSCO issued its Principles for Oil Price Reporting Agencies ("PRA Principles"), which IOSCO states are intended to enhance the reliability of oil price assessments that are referenced in derivative contracts subject to regulation by IOSCO members. Platts has taken steps to align its operations with the PRA Principles and, as recommended by IOSCO in its final report on the PRA Principles, has aligned to the PRA Principles for other commodities for which it publishes benchmarks.