| HuntMountain Resources Ltd. and Subsidiaries |

| (An Exploration Stage Enterprise) |

| | |

|

| | | Number of Shares Outstanding | | | Common Stock Amount | | | Additional Paid-In Capital | | | Retained Earnings | | | Deficit Accumulated During The Development Stage | | | Accumulated Other Comprehensive Income (Loss) | | | Total | |

| | | | | | | | | | | | | | | | | | | | | | |

| BALANCES, DECEMBER 31, 2004 | | | 7,277,934 | | | $ | 379,282 | | | $ | — | | | $ | 144,968 | | | $ | — | | | $ | 1,061 | | | $ | 525,311 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Common stock issued for cash | | | 9,222,066 | | | | 503,434 | | | | 148,500 | | | | — | | | | — | | | | — | | | | 651,934 | |

| Stock options issued to employees | | | — | | | | — | | | | 4,000 | | | | — | | | | — | | | | — | | | | 4,000 | |

| Stock options issued for services | | | — | | | | — | | | | 900 | | | | — | | | | — | | | | — | | | | 900 | |

| Reclassification due to par value change | | | — | | | | (866,216 | ) | | | 866,216 | | | | — | | | | — | | | | — | | | | — | |

| Comprehensive income (loss): | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Other comprehensive loss: | | | — | | | | — | | | | — | | | | — | | | | — | | | | 1,401 | | | | 1,401 | |

| Net loss | | | — | | | | — | | | | — | | | | (54,441 | ) | | | (187,887 | ) | | | — | | | | (242,328 | ) |

| Comprehensive loss | | | | | | | | | | | | | | | | | | | | | | | | | | | (240,927 | ) |

| BALANCES, DECEMBER 31, 2005 | | | 16,500,000 | | | $ | 16,500 | | | $ | 1,019,616 | | | $ | 90,527 | | | $ | (187,887 | ) | | $ | 2,462 | | | $ | 941,218 | |

| Common stock issued for cash | | | 15,744,132 | | | | 15,744 | | | | 1,117,126 | | | | — | | | | — | | | | — | | | | 1,132,870 | |

| Exercise of stock options | | | 18,153 | | | | 18 | | | | (18 | ) | | | — | | | | — | | | | — | | | | — | |

| Stock options issued to employees | | | — | | | | — | | | | 67,000 | | | | — | | | | — | | | | — | | | | 67,000 | |

| Stock options issued for services | | | — | | | | — | | | | 220,850 | | | | — | | | | — | | | | — | | | | 220,850 | |

| Common stock issued to rectify imbalance | | | 4,000 | | | | 4 | | | | (4 | ) | | | — | | | | — | | | | — | | | | — | |

| Comprehensive income (loss): | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Other comprehensive loss: | | | — | | | | — | | | | — | | | | — | | | | — | | | | (8,235 | ) | | | (8,235 | ) |

| Net loss | | | — | | | | — | | | | — | | | | — | | | | (2,013,647 | ) | | | — | | | | (2,013,647 | ) |

| Comprehensive loss | | | | | | | | | | | | | | | | | | | | | | | | | | | (2,021,882 | ) |

| BALANCES, DECEMBER 31, 2006 | | | 32,266,285 | | | $ | 32,266 | | | $ | 2,424,570 | | | $ | 90,527 | | | $ | (2,201,534 | ) | | $ | (5,773 | ) | | $ | 340,056 | |

| Common stock issued for executive compensation | | | 150,000 | | | | 75 | | | | 74,925 | | | | — | | | | — | | | | — | | | | 75,000 | |

| Stock options issued to employees | | | — | | | | — | | | | 52,600 | | | | | | | | — | | | | 52,600 | | | | — | |

| Stock options issued for services | | | — | | | | — | | | | 131,500 | | | | — | | | | — | | | | — | | | | 131,500 | |

| Convertible note issuance | | | — | | | | — | | | | 9,247,871 | | | | — | | | | — | | | | — | | | | 9,247,871 | |

| Convertible note conversion | | | 600,000 | | | | 150 | | | | 149,850 | | | | — | | | | — | | | | — | | | | 150,000 | |

| Comprehensive income (loss): | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Other comprehensive loss: | | | — | | | | — | | | | — | | | | — | | | | — | | | | (47,308 | ) | | | (47,308 | ) |

| Net loss | | | — | | | | — | | | | — | | | | — | | | | (9,593,448 | ) | | | — | | | | (9,593,448 | ) |

| Comprehensive loss | | | | | | | | | | | | | | | | | | | | | | | | | | | (9,640,756 | ) |

| BALANCES, DECEMBER 31, 2007 | | | 33,016,285 | | | $ | 32,491 | | | $ | 12,081,316 | | | $ | 90,527 | | | $ | (11,794,981 | ) | | $ | (53,081 | ) | | $ | 356,272 | |

| Exercise of stock options | | | 188,829 | | | | 189 | | | | (189 | ) | | | — | | | | — | | | | — | | | | — | |

| Stock options issued to employees | | | — | | | | — | | | | 229,262 | | | | | | | | — | | | | — | | | | 229,262 | |

| Stock options issued for services | | | — | | | | — | | | | 126,588 | | | | — | | | | — | | | | — | | | | 126,588 | |

| Convertible note issuance | | | — | | | | — | | | | 27,787,800 | | | | — | | | | — | | | | — | | | | 27,787,800 | |

| Convertible note conversion | | | 43,046,248 | | | | 43,046 | | | | 10,750,801 | | | | — | | | | — | | | | — | | | | 10,793,847 | |

| Miscellaneous stock adjustment | | | — | | | | 526 | | | | — | | | | | | | | | | | | | | | | 526 | |

| Comprehensive income (loss): | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Other comprehensive loss: | | | — | | | | — | | | | — | | | | — | | | | — | | | | (137,919 | ) | | | (137,919 | ) |

| Net loss | | | — | | | | — | | | | — | | | | — | | | | (40,653,678 | ) | | | — | | | | (40,653,678 | ) |

| Comprehensive loss | | | | | | | | | | | | | | | | | | | | | | | | | | | (40,791,597 | ) |

| BALANCES, DECEMBER 31, 2008 | | | 76,251,362 | | | $ | 76,251 | | | $ | 50,975,578 | | | $ | 90,527 | | | $ | (52,448,659 | ) | | $ | (190,999 | ) | | $ | (1,497,302 | ) |

| Stock options issued to employees | | | — | | | | — | | | | 218,710 | | | | — | | | | — | | | | — | | | | 218,710 | |

| Convertible note issuance | | | — | | | | — | | | | 2,837,296 | | | | — | | | | — | | | | — | | | | 2,837,296 | |

| Debt discount | | | — | | | | — | | | | 4,790,599 | | | | — | | | | — | | | | — | | | | 4,790,599 | |

| Comprehensive income (loss): | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Other comprehensive loss: | | | — | | | | — | | | | — | | | | — | | | | — | | | | (72,584 | ) | | | (72,584 | ) |

| Net loss | | | — | | | | — | | | | — | | | | — | | | | (11,155,399 | ) | | | — | | | | (11,155,399 | ) |

| Comprehensive loss | | | | | | | | | | | | | | | | | | | | | | | | | | | (11,227,983 | ) |

| BALANCES, DECEMBER 31, 2009 | | | 76,251,362 | | | $ | 76,251 | | | $ | 58,822,183 | | | $ | 90,527 | | | $ | (63,604,058 | ) | | $ | (263,583 | ) | | $ | (4,878,680 | ) |

| The accompanying notes are an integral part of these consolidated financial statements. |

HuntMountain Resources Ltd. and Subsidiaries (An Exploration Stage Enterprise) |

NOTE 1 – DESCRIPTION OF BUSINESS

HuntMountain Resources Ltd. (“the Company” or “HuntMountain”), a Washington corporation, was formed in 2005. Metaline Mining and Leasing Company, a Washington corporation since 1927, merged with and into the Company in August 2005. The Company’s business plan is to acquire interests in exploration properties in North and South America. As of the end of 2008, the Company had acquired one exploration property in Nevada, seven properties in the province of Santa Cruz in Argentina, one property in Mexico and an option on two properties in Quebec.

The accompanying consolidated financial statements include the accounts of HuntMountain, a Washington corporation, its wholly-owned Canadian subsidiary HuntMountain Resources LTD (“HMR LTD”), HuntMountain’s wholly owned Mexican subsidiary Cerro Cazador Mexico S.A. De C.V. (“CCM”), HuntMountain’s wholly-owned subsidiary HuntMountain Investments, LLC (HMI), Sinomar Capital Corp. who subsequently on February 1, 2010, changed their name to Hunt Mining Corp. (“Hunt Mining”), a Canadian subsidiary 65% owned by HuntMountain and 4% owned by HMI, Hunt Mining’s wholly owned Canadian Subsidiary Hunt Gold USA, LLC, Hunt Mining’s wholly owned Canadian Subsidiary 1494716 Alberta, Ltd., and Cerro Cazador S.A. (CCSA), Hunt Mining’s Argentine subsidiary 95% owned by Hunt Mining and 5% ow ned by 1494716 Alberta, Ltd.

HMR LTD is incorporated in British Columbia and provincially registered in the Yukon. HMR LTD was formed for the purpose of holding Canadian exploration properties, should the Company acquire an interest in any such properties. CCM was incorporated to acquire a property package in Chihuahua, Mexico. HMI was incorporated for the specific purpose of holding shares in subsidiary companies. CCSA was formed in Argentina for the purpose of holding Argentine exploration properties and executing agreements in Argentina.

Currently all exploration activities are being pursued by our majority owned subsidiary, Hunt Mining through its wholly owned subsidiary, CCSA which on December 23, 2009 the Company exchanged 100% of its shares of CCSA, which were acquired by Hunt Mining as part of a reverse takeover transaction. Hunt Mining is a mineral exploration company incorporated on January 10, 2006 under the laws of Alberta, Canada which trades on the TSX Venture Exchange under the ticker symbol HMX. Prior to December 23, 2009 Hunt Mining was a Capital Pool Company within the meaning ascribed by Policy 2.4 of the TSX Venture Exchange. Hunt Mining issued 29,118,507 common shares and 20,881,493 non-voting convertible preferred shares to the Company at a deemed price of C$0.30 per Common Share and C$0.30 per convertible preferred s hare in consideration for the acquisition of all of the common shares of CCSA. Each convertible preferred share shall be convertible into one Common Share of Hunt Mining for no additional consideration at any time as long as the public float is not less than 20%. This transaction gave the Company controlling interest in Hunt Mining, 65% owned by the Company and 4% owned by the Company’s wholly-owned subsidiary HMI.

NOTE 2 – GOING CONCERN

As shown in the accompanying financial statements, the Company has had no revenues and has incurred an accumulated deficit from the inception of the development stage of $63,604,058 through December 31, 2009. These factors raise substantial doubt about the Company’s ability to continue as a going concern.

On February 18, 2010, the Company’s board of directors recommended and authorized a shareholder meeting to consider and vote upon a proposal to approve the voluntary dissolution and liquidation of the Company pursuant to a plan of complete dissolution and liquidation dissolution. On July 16, 2010, the Company filed with the Securities and Exchange Commission (“SEC”), a preliminary schedule 14A proxy statement to submit the vote to the Company’s shareholders. As of the date of the filing of this form 10-K, the preliminary 14A proxy statement has not yet been approved by the SEC and the vote has yet to go before the shareholders. The dissolution of the Company, if approved by the shareholders, will not affect the operations of Hunt Mining which will continue in existence along with its subsidiary compan ies. See “Note 16, Subsequent Events” for further details.

The financial statements do not include any adjustments relating to the recoverability and classification of recorded assets, or the amounts and classification of liabilities that might be necessary in the event the Company does not continue in existence.

NOTE 3 – SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

This summary of significant accounting policies is presented to assist in the understanding of the financial statements. The financial statements and notes are representations of the Company’s management, which is responsible for their integrity and objectivity. These accounting policies conform to accounting principles generally accepted in the United States of America and have been consistently applied in the preparation of the financial statements.

Accounting Method

The Company’s financial statements are prepared using the accrual basis of accounting in accordance with accounting principles generally accepted in the United States of America.

Accounts Receivable

The Company carries its accounts receivable at net realizable value. On a periodic basis, the Company evaluates its accounts receivable and determines if an allowance for doubtful accounts is necessary, based on a history of past write-offs and collections and current credit conditions. At December 31, 2009 the Company’s accounts receivable balance was $22,377 compared to $153,135 at December 31, 2008. The Company’s accounts receivable balance includes no allowance for doubtful accounts based upon management’s expectations and analysis.

Use of Estimates

The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosures of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates.

Cash and Cash Equivalents

Cash and cash equivalents include short-term cash investments that have an initial maturity of 90 days or less. In the normal course of business, 30% of all funds wire transferred from the Company to CCSA are withheld by the Government of Argentina. These withheld amounts are invested in money market instruments until the Government of Argentina approves CCSA’s formal application for release. Funds held in this fashion are included in short-term cash investments. Of the $2,927,057 held in cash, $2,919,009 is held for use by Hunt Mining and is not available for distribution to the Company.

Principles of Consolidation

The consolidated financial statements include the accounts of the Company and its wholly and majority-owned subsidiaries after elimination of intercompany accounts and transactions. All of the wholly owned subsidiaries of the Company are named above in Note 1 – Description of Business.

Marketable Securities

The Company accounts for marketable securities as required by the Debt and Equity Securities topic of the FASB Accounting Standards Codification Debt securities and equity securities that have readily determinable fair values are to be classified in three categories:

Held to Maturity – the positive intent and ability to hold to maturity. Amounts are reported at amortized cost, adjusted for amortization of premiums and accretion of discounts.

Trading Securities – bought principally for purpose of selling them in the near term. Amounts are reported at fair value, with unrealized gains and losses included in earnings.

Available for Sale – not classified in one of the above categories. Amounts are reported at fair value, with unrealized gains and losses excluded from earnings and reported separately as a component of stockholders’ equity.

At this time, the Company holds securities classified as available for sale. See Note 4 - Investments for further details.

Mineral Development Costs

All exploration expenditures are expensed as incurred. Significant property acquisition payments for active exploration properties are capitalized. If no economic ore body is discovered, previously capitalized costs are expensed in the period the property is abandoned. Expenditures to develop new mines, to define further mineralization in existing ore bodies, and to expand the capacity of operating mines, are capitalized and amortized on a units-of-production basis over proven and probable reserves.

Should a property be abandoned, its capitalized costs are charged to operations. The Company charges to the consolidated statement of operations the allocable portion of capitalized costs attributable to properties sold. Capitalized costs are allocated to properties sold based on the proportion of claims sold to the claims remaining within the project area.

Equipment

The Company evaluates equipment for impairment annually, or when events or changes in circumstances indicate that the related carrying amount may not be recoverable. If the sum of estimated future net cash flows on an undiscounted basis is less than the carrying amount of the related asset grouping, an asset impairment is considered to exist. The related impairment loss is measured by comparing estimated future net cash flows on a discounted basis to the carrying amount of the asset. Changes in significant assumptions underlying future cash flow estimates may have a material effect on the Company’s financial position and results of operations. To date no such impairments have been identified.

Office Equipment and vehicles are stated at cost and depreciated on the straight-line basis over an estimated useful life of 3 years. Drilling and excavation equipment is stated at cost on the balance sheet for December 31, 2009 and 2008. The Company has not begun depreciating drilling and excavation equipment because the equipment has not yet been placed into service.

Basic and Diluted Net Loss Per Share

The Company complies with the requirements of the Earnings per Share Topic of the FASB Accounting Standards Codification, which provides for calculation of “basic” and “diluted” earnings per share. Basic earnings per share includes no dilution and is computed by dividing net income available to common shareholders by the weighted average common shares outstanding for the period. Diluted earnings per share reflects the potential dilution of securities that could share in the earnings of an entity similar to fully diluted earnings per share. Although there were common stock equivalents outstanding on December 31, 2009, they were not included in the calculation of earnings per share because they would have been considered anti-dilutive.

Basic earnings per share are computed using the weighted average number of shares outstanding during the years (76,251,362 at December 31, 2009 and 57,365,938 at December 31, 2008).

Outstanding warrants to purchase 45,646,248 and 43,646,248 shares of common stock, options to purchase 2,245,000 and 2,495,000 shares of common stock at December 31, 2009 and 2008, respectively, as well as outstanding convertible debt plus accrued interest of $5,667,479 which can be converted into 56,747,917 units, where each unit consists of one share of common stock and one warrant to purchase one share of common stock at December 31, 2009, were not included in the computation of diluted loss per share for the years ended December 31, 2009 and 2008, respectively, because to do so would have been antidilutive. Therefore, basic loss per share is the same as diluted loss per share.

Deferred Income Tax

Deferred income tax is provided for differences between the bases of assets and liabilities for financial and income tax reporting. A deferred tax asset, subject to a valuation allowance, is recognized for estimated future tax benefits of tax-basis operating losses being carried forward.

Provision for Taxes

Income taxes are provided based upon the liability method of accounting pursuant to the Income Taxes topic of the FASB Accounting Standards Codification Under this approach, deferred income taxes are recorded to reflect the tax consequences in future years of differences between the tax basis of assets and liabilities and their financial reporting amounts at each year-end. A valuation allowance is recorded against the deferred tax asset if management does not believe the Company has met the “more likely than not” standard imposed to allow recognition of such an asset.

Reclamation and Remediation

Expenditures for ongoing compliance with environmental regulations that relate to current operations are expensed or capitalized as appropriate. Expenditures resulting from the remediation of existing conditions caused by past operations that do not contribute to future revenue generations are expensed. Liabilities are recognized when environmental assessments indicate that remediation efforts are probable and the costs can be reasonably estimated.

Estimates of such liabilities are based upon currently available facts, existing technology and presently enacted laws and regulations taking into consideration the likely effects of inflation and other societal and economic factors, and include estimates of associated legal costs. These amounts also reflect prior experience in remediating contaminated sites, other companies’ clean-up experience and data released by The Environmental Protection Agency or other organizations. Such estimates are by their nature imprecise and can be expected to be revised over time because of changes in government regulations, operations, technology and inflation. Recoveries are evaluated separately from the liability and, when recovery is assured, the Company records and reports the asset separately from the associated liability.

Adoption of New Accounting Principles

Effective January 1, 2009, we adopted the provisions of Topic 810 in the Accounting Standards Codification (ASC 810) (previously Statement of Financial Accounting (“FAS” No. 160 “Non Controlling Interests in Consolidated Financial Statements - an amendment of ARB 51”) (“ASC 810”) without a material effect on our results of operations and financial position. ASC 810 establishes accounting and reporting standards for the non controlling ownership interest in a subsidiary and for the deconsolidation of a subsidiary.

Fair Value Measurements

The Company’s financial instruments as defined by FASB ASC 825-10-50, include cash, receivables, accounts payable and accrued expenses. All instruments except the performance bond are accounted for on a historical cost basis, which, due to the short maturity of these financial instruments, approximates fair value at December 31, 2009 and December 31, 2008. The performance bond was marked to market on December 31, 2009 and December 31, 2008.

FASB ASC 820 defines fair value, establishes a framework for measuring fair value in accordance with generally accepted accounting principles, and expands disclosures about fair value measurements. FASB ASC 820 establishes a three-tier fair hierarchy which prioritizes the inputs used in measuring fair value as follows:

Level 1: Quoted prices are available in active markets for identical assets or liabilities. Active markets are those in which transactions for the asset or liability occur with sufficient frequency and volume to provide pricing information on an ongoing basis.

Level 2: Pricing inputs are other than quoted prices in active markets included in Level 1, which are either directly or indirectly observable as of the reporting date. Level 2 includes those financial instruments that are valued using models or other valuation methodologies. These models are primarily industry-standard models that consider various assumptions, including quoted forward prices for commodities, time value, volatility factors, and current market and contractual prices for the underlying instruments, as well as other relevant economic measures. Substantially all of these assumptions are observable in the marketplace throughout the full term of the instrument, can be derived from observable data or are supported by observable levels at which transactions are executed in the marketplace.

Level 3: Pricing inputs include significant inputs that are generally unobservable from objective sources. These inputs may be used with internally developed methodologies that result in management’s best estimate of fair value. Level 3 instruments include those that may be more structured or otherwise tailored to the Company’s needs.

Financial assets and liabilities are classified in their entirety based on the lowest level of input that is significant to the fair value measurement. The Company’s assessment of the significance of a particular input to the fair value measurement requires judgment, and may affect the valuation of fair value assets and liabilities and their placement within the fair value hierarchy levels.

The following table discloses by level within the fair value hierarchy the Company’s assets and liabilities measured and reported on the Consolidated Balance Sheets as of December 31, 2009, at fair value on a recurring basis:

| | | Total | | | Level I | | | Level II | | | Level III | |

| Assets: | | | | | | | | | | | | |

| Performance bond | | $ | 199,508 | | | $ | 199,508 | | | $ | 0 | | | $ | 0 | |

| Receivable – V.A. Tax | | | 489,598 | | | | 0 | | | | 0 | | | | 489,598 | |

| Total: | | $ | 689,106 | | | $ | 199,508 | | | $ | 0 | | | $ | 489,598 | |

The performance bond, required to secure the Company’s rights to explore the La Josefina property, is a step-up coupon US dollar bond issued by the Government of Argentina with a face value of $600,000 and a maturity date of 2035. The bond was originally purchased for $251,613 and had a value of $98,927 at December 31, 2008. As of the year ended December 31, 2009 the value of the bond increased to $199,508.

The Receivable V.A. Tax accrued due to the payment of valued added tax on certain transactions in Argentina. This asset is reported at net present value based upon the Company’s estimate of an expected benefit period of 7 years and a discount rate of 18.6% based upon the average Argentine interest rates.

Concentration of Credit Risk

The Company maintains its cash and cash equivalents in multiple financial institutions. Balances in the United States are insured by the Federal Deposit Insurance Corporation (FDIC) up to $250,000 per institution and balances in Canada are insured by the Canada Deposit Insurance Corporation up to C$100,000 per institution. Balances on deposit may occasionally exceed insured amounts. At December 31, 2009, deposits in Canadian banks exceeded the insured amount by C$2,792,959. All of the Company’s cash in U.S. bank accounts at December 31, 2009 was FDIC insured. The Company also maintains cash in an Argentine bank. The Argentine accounts, which had a U.S. dollar balance of $13,352 at December 31, 2009, are considered uninsured.

Beneficial Conversion Feature of Convertible Notes

Following the guidance provided by ASC Topic 470 “Debt with Conversion and Other Options”, the Company allocated proceeds first to the warrants issuable upon conversion of the note. The value of the warrants was recorded on the balance sheet as debt discounts and increases to shareholder’s equity. The debt discounts are being amortized over the remaining life of the convertible note. The value of warrants in excess of the actual debt advance amounts were expensed as financing fees.

Once the Company allocated proceeds of convertible note advances to the warrant values, the embedded conversion feature of shares issuable on conversion of the notes was recognized. All amounts relating to the share values were expensed as financing fees.

Foreign Currency Translation

Our international operations use the United States Dollar as their functional currency. The financial statements of international subsidiaries are translated to their U.S. dollar equivalents at end-of-period currency exchange rates for assets and liabilities and at average currency exchange rates for revenues and expenses. Translation adjustments for international subsidiaries are recorded as a loss in the accompanying Consolidated Statements of Income. Transaction gains and losses resulting from fluctuations in currency exchange rates on transactions denominated in currencies other than the functional currency are recognized as incurred in the accompanying Consolidated Statements of Income, except for certain inter-company balances designated as long-term investments.

Other Comprehensive Income

The Company follows guidance provided by FASB ASC Topic 220 “Comprehensive Income”, which establishes guidelines for the reporting and display of comprehensive income (loss) and its components in financial statements. Comprehensive income (loss) includes the accrued gain or loss on the performance bond.

Compensated Absences

The Company has not accrued for compensated absences because the amounts are deemed to be immaterial.

Reclassifications

Certain prior year amounts in the accompanying financial statements have been reclassified to conform to the fiscal 2009 presentation. These reclassifications have resulted in no changes to the Company’s accumulated deficit or the net loss presented.

NOTE 4 – INVESTMENTS

The Company had the following investments:

| | | December 31, | |

| | | 2009 | | | 2008 | |

| Partnership interest in two units of Pondera Partners, Ltd., a drilling project located in Teton County, Montana (at cost less equity partnership losses) | | $ | 7,331 | | | $ | 7,331 | |

The Company has invested in various privately and publicly held companies. At this time, the Company holds securities classified as available for sale. Amounts are reported at fair value as determined by quoted market prices, with unrealized gains and losses excluded from earnings and reported separately as a component of stockholders’ equity.

At December 31, 2009, the Company determined that the following available-for-sale security had experienced an impairment that was other-than-temporary. Key factors used in determining whether or not the impairment was other-than-temporary included the severity of the impairment and the fact that the Company was planning on selling the shares within the first quarter of the next year, see “Note 16, Subsequent Events” for further information. In connection with this determination, the company recognized an impairment charge of $90,000. This impairment charge is presented under the caption “Other-than-temporary impairment of investments” on the Company’s Consolidated Statements of Operations at December 31, 2009.

The following table presents certain details related to the investment for which the Company determined the impairment was other-than-temporary:

| Investment | | # of shares | | | Original Value | | | Market Value at 12/31/09 | | | Recognized Impairment | |

| Black Hawk Exploration Inc. | | | 250,000 | | | $ | 250,000 | | | $ | 160,000 | | | $ | (90,000 | ) |

NOTE 5 – PROPERTY PURCHASE OPTION

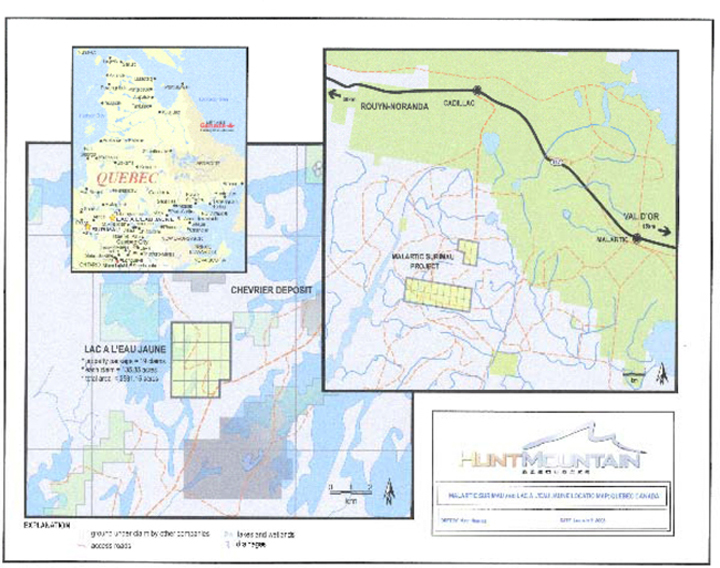

On June 19, 2006, the Company entered into an agreement with Diagnos, Inc., (Diagnos) obtaining an exclusive option to acquire a 100% interest in two prospective gold properties located in the Abitibi region of Québec, Canada. The properties consist of 46 claims covering approximately 6,500 acres.

The Company will acquire a 100% interest in the properties by paying Diagnos a sum of $70,000 and by conducting an initial exploration program comprised of at least three drill holes on each property. During the year ended December 31, 2006, the Company paid the $70,000 fee, which is shown as property purchase option on the consolidated balance sheets. Upon completion of the initial drilling programs, the Company will have the option to select up to an additional seven properties in which it may acquire a 100% interest by paying Diagnos a sum of $40,000 and completing three-hole exploration drilling programs for each property. The option will expire if the initial two properties are not drilled by March 31, 2010.

For each economic discovery made on any of the acquired properties, the Company will pay Diagnos a bonus of $500,000. The Company will also grant Diagnos a 2% Net Smelter Royalty (NSR) for economic discoveries made on the initial or additional properties, but will retain the option to acquire 1% of the NSR upon payment of $1 million to Diagnos within five (5) years of making the economic discovery. An economic discovery is defined in the agreement as being the production of a positive feasibility study for a given project in compliance with Canada’s National Instrument 43-101.

As of December 31, 2009, management of the Company determined that the $70,000 carrying value of the property purchase option had been impaired based on the fact that a drilling program would most likely not be completed by the expiration date of March 31, 2010. The Company therefore recorded a write a write-down of $70,000 which was recognized as an impairment of mineral property purchase option in the fourth quarter of 2009 leaving a carrying value of zero.

NOTE 6 – COMMITMENTS

Santa Cruz, Argentina

On March 27, 2007, CCSA, a wholly owned Argentine subsidiary of Hunt Mining, signed a definitive lease purchase agreement with FK Minera S.A. to acquire a 100% interest in the Bajo Pobré gold property located in Santa Cruz Province, Argentina. The Company may earn up to a 100% equity interest in the Bajo Pobré property by making cash payments and exploration expenditures over a five-year earn-in period. The required expenditures and ownership levels upon meeting those requirements are:

| Year of the Agreement | | Payment to FK Minera SA | | | Exploration Expenditures Required | | | Ownership | |

| First year | -2007 | | $ | 50,000 | | | $ | 250,000 | | | | 0 | % |

| Second year | -2008 | | | 50,000 | | | | 250,000 | | | | 0 | % |

| Third year | -2009 | | | 75,000 | | | | 0 | | | | 51 | % |

| Fourth year | -2010 | | | 75,000 | | | | 0 | | | | 60 | % |

| Fifth year | -2011 | | | 75,000 | | | | 0 | | | | 100 | % |

After the fifth year, the Company is obligated to pay FK Minera S.A. the greater of a 1% net smelter royalty (“NSR”) on commercial production or $100,000 per year. The Company has the option to purchase the NSR for a lump-sum payment of $1,000,000 less the sum of all royalty payments made to FK Minera S.A. to that point.

As of December 31, 2009, CCSA has not engaged in any exploration activity on the Bajo Pobré property. CCSA has not fulfilled any of our exploration obligations relative to the Bajo Pobré property. Further, CCSA has not received any form of formal relief from the contract terms relating to the Bajo Pobré property. On November 5, 2009 the Company received notification from the Santa Cruz Province Mining Authority that FK Minera S.A. and Arturo Canero, its principal, have been inhibited in the disposal of its assets, including the Bajo Pobre property. They orally stated that such inhibition would be released since it would submit other assets in replacement; however, to date there is no evidence of such replacement of assets. The Company’s ability to retain rights to explore the Bajo Pobré property is uncertain at this time.

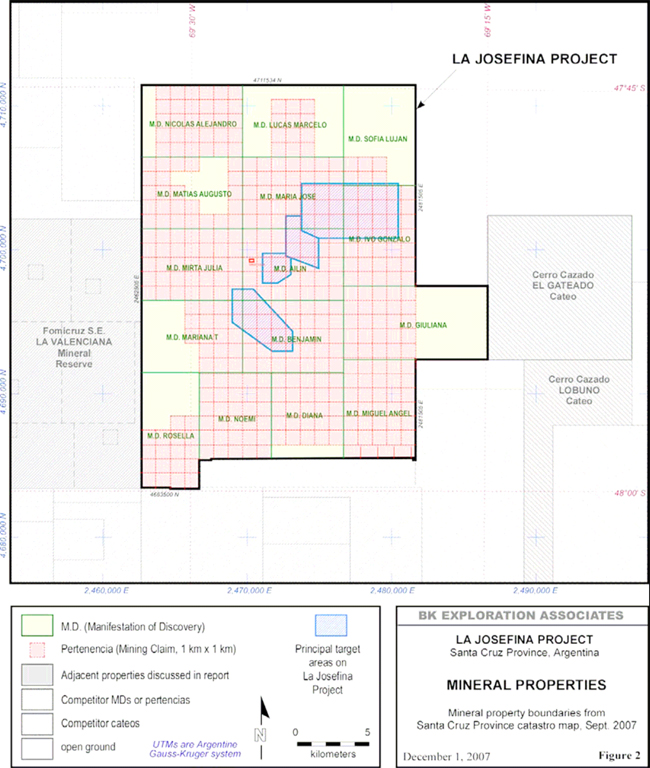

In March 2007, CCSA was the successful bidder for the exploration and development rights to the La Josefina Project from Fomento Minero de Santa Cruz Sociedad del Estado (Fomicruz). Fomicruz is a company that is owned by the government of the Santa Cruz province in Argentina. On July 24, 2007 CCSA entered into an agreement with Fomicruz pursuant to which CCSA agreed to invest a minimum of $6 million in exploration and development expenditures over a four year period, including $1.5 million before July 2008. The agreement delineates that in the event that a positive feasibility study is completed on the La Josefina property that a joint venture company would be formed; the Company would own 91% of the joint venture company and Fomicruz would own the remaining 9%.

Between November of 2007 and December of 2008 CCSA completed a 37,605 meter drilling program on the La Josefina property. To date, the $6,000,000 work commitment has been exceeded. CCSA must maintain the La Josefina mining rights by paying the annual canons due the province on the project’s 399 pertenencias. This currently amounts to 318,400 Argentine pesos per year (approximately $93,647) that can be deducted from the $6,000,000 work commitment. The annual canons were paid for both 2008 and 2009.

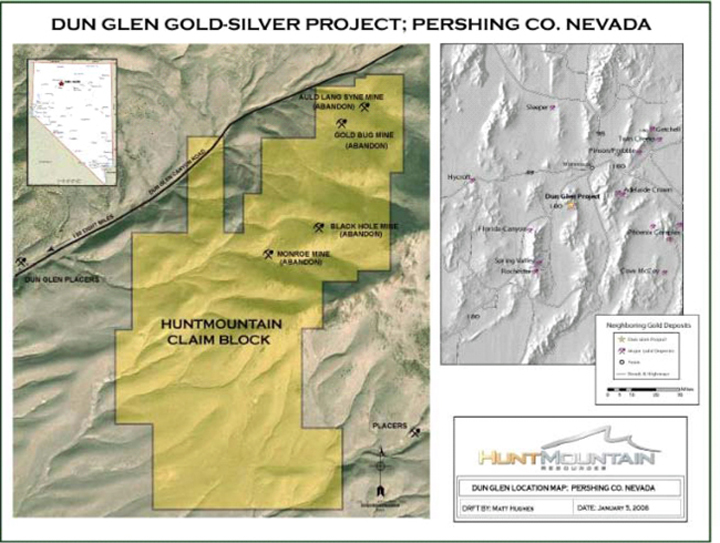

Pershing County, Nevada

The Company has a lease for the Dun Glen property with an option to purchase a 100% interest in the claims. Lease payments began in 2006 and are considered advance royalty payments. The term of the lease is 10 years, renewable at the Company’s option for an additional ten years. As of December 31, 2009, the Company has made lease payments totaling $137,500. Future lease payments are as follows:

| | ● | 5th (and each anniversary thereafter) $72,500 |

On December 10, 2009, the Company entered into an agreement with Black Hawk Exploration (Black Hawk) to transfer 75% of the company’s economic interest in the Dun Glen Project. In return, the Company received a one-time payment of $50,000 at signing, and is due to receive further payments of $25,000 on or before each of December 10, 2010, and December 10, 2011. Black Hawk also issued to the company 250,000 restricted common shares of Black Hawk Exploration and will issue a further 100,000 restricted common shares on or before December 10, 2010.

The terms of the Black Hawk Agreement state that Black Hawk has the responsibility to maintain the property in good standing at their expense, including the timely filing or payment of all claims maintenance fees or taxes and all the underlying future lease payments owed by the Company as noted above.

On February 18, 2010 the Company transferred its stock in Black Hawk and its interest in the Dun Glen property to the Hunt Family Limited Partnership (“HFLP”), a related party, along with all its Mexican assets in consideration of cancelling $600,000 of the debt that the Company owed to HFLP on an outstanding note payable. See “Note 16, subsequent events” for further information.

Quebec, Canada

As addressed in Note 5, during 2006, the Company entered into a definitive Option Agreement for the acquisition of a 100% interest in two properties in the Abitibi region of Quebec. Pursuant to the terms of the Option Agreement, the Company paid $70,000 ($35,000 for each of the two properties) in cash to the property owner. The Company has also agreed to explore these properties and drill at least three exploration drill holes in each. The payments and drilling of exploration drill holes will earn the Company a 100% interest in each of these properties and give the Company the option to acquire additional properties from the same property owner at similar terms. The Company has also agreed to keep the claims in good standing until the agreement is terminated.

As of December 31, 2009, management of the Company determined that the $70,000 carrying value of the property purchase option had been impaired based on the fact that a drilling program would most likely not be completed by the expiration date of March 31, 2010. The Company therefore recorded a write a write-down of $70,000 which was recognized as an impairment of mineral property purchase option in the fourth quarter of 2009 leaving a carrying value of zero.

Facility Leases

The Company has lease commitments on office space and storage space in Liberty Lake, Washington. The total annual lease obligation for this facility is $69,359 (not including common area maintenance charges).

NOTE 7 – INCOME TAXES

The Company accounts for income taxes and the related accounts under the liability method. Deferred tax assets and liabilities are determined based on the difference between the financial statement carrying amounts and the income tax basis of assets and liabilities. A valuation allowance is applied against any net deferred tax asset if, based on available evidence, it is more likely than not that some or all of the deferred tax assets will not be realized.

At December 31, 2009 and 2008 the Company had gross deferred tax assets calculated at the expected rate of 34% of approximately $5,895,000 and $4,810,000, respectively, principally arising from net operating loss carryforwards for income tax purposes. As management of the Company cannot determine that it is more likely than not that the Company will realize the benefit of the deferred tax asset, a valuation allowance of $5,895,000 and $4,810,000 has been established at December 31, 2009 and 2008, respectively.

The significant components of the Company’s net deferred tax asset (liabilities) at December 31, 2008 and 2007 are as follows:

| | | 2009 | | | 2008 | |

| Net operating loss carryforwards | | $ | 17,337,000 | | | $ | 14,148,000 | |

| | | | | | | | | |

| Gross deferred tax assets (liabilities): | | | | | | | | |

| Net Operating Loss | | $ | 5,895,000 | | | $ | 4,810,000 | |

| Valuation Allowance | | | (5,895,000 | ) | | | (4,810,000 | ) |

| | | | | | | | | |

| Net Deferred tax asset (liability) | | $ | — | | | $ | — | |

At December 31, 2009 and 2008, the Company has net operating loss carryforwards of approximately $17,337,000 and $14,148,000 respectively, which will expire in the years 2022 through 2023. The net change in the allowance account was an increase of $1,085,000. Some of the losses were from operations outside of the United States and may be limited in their availability because of limitations and other equity transactions.

NOTE 8 – SALES OF COMMON STOCK AND WARRANTS

During the year ended December 31, 2007, the Company issued 600,000 units consisting of one share and one warrant pursuant to the conversion of a portion of a convertible note. Each common share had a par value of $0.001 and an issuance price of $0.25. Each warrant has an exercise price of $0.40 per common share. The expiration date of each warrant is five (5) years from the date of issuance.

During the year ended December 31, 2007, the Company issued 150,000 shares for compensation to the Company’s Chief Operating Officer. The shares had a fair market value of $75,000.

During the year ended December 31, 2008 the holders of the October Note converted into units, at the conversion price of $0.25 per share outstanding principal of $10,350,000, plus accrued interest of $313,014, of the October Note. As a result the Company issued a total of 43,046,248 shares and 43,046,248 warrants (see Note 9 – Shareholder Loan).

During the year ended December 31, 2009 the Company issued 2,000,000 warrants concurrently and in consideration for the issuance of the June Note (see Note 9 – Shareholder Loan).

NOTE 9 – SHAREHOLDER LOAN

On June 2, 2009, pursuant to approval from its board of directors, the Company obtained an unsecured loan for multiple advances up to $5,000,000 (“the June 2009 Note”) from Hunt Family Limited Partnership (“HFLP”), a related party. The June 2009 Loan supersedes and replaces the shareholder loan owed to HFLP that had a principal balance of $3,762,000 on June 2, 2009. These notes are unsecured.

The June 2009 Note, which matures on December 31, 2009, bears interest at a rate of eleven percent (11%) per annum. All principal and accrued interest balances due pursuant to the June 2009 Note are convertible at the option of the holder into units of the Company’s common stock, at a conversion price of $0.10 per unit, where each unit consists of one share and one warrant to purchase a common share. Each warrant issued pursuant to conversion of the June 2009 Note shall have an exercise price of $0.10 per share and a seven (7) year expiration from the date of issuance.

The original maturity date of the June 2009 Note was December 31, 2009. By unanimous consent of the Company’s board of directors on December 17, 2009, the maturity date of the June 2009 Note was amended from December 31, 2009 to December 31, 2010. At that time, also by unanimous consent, the Company’s board of directors increased the maximum aggregate principal amount available pursuant to the June 2009 Note from $5,000,000 to $5,500,000.

In addition, concurrently and in consideration for the issuance of the June 2009 Note, all warrants previously issued to HFLP pursuant to the conversion of Notes shall be cancelled and an equal number of warrants to acquire common shares at an exercise price of $0.10 and a maturity date of April 22, 2016 shall be issued. On June 2, 2009 the Company recognized a financing fee expense of $2,837,295 to reflect the difference in the Black-Scholes valuation of the new warrants and the cancelled warrants.

Concurrently and in consideration for the issuance of the June 2009 Note the Company granted to HFLP a 3% Net Smelter Royalty (“NSR”) on all of the Company’s resource properties in Mexico, past, present and future. The Company also granted an additional 2,000,000 warrants with a $0.10 exercise price and a seven (7) year term in conjunction with the inception of the June Note structure.

The Company recognized the beneficial conversion feature associated with the June Note’s convertibility into shares and warrants. The total value of the shares was determined based on the trading price of the Company’s shares at the time of the draw on the June Note. The total value of warrants was determined using the Black Scholes option pricing model. In employing this model, the Company used the actual three month T-Bill rate on the advance dates for the risk-free rate. Similarly, the actual share price on advance dates was used in the calculation. The Company assumed expected volatility of 105.06%, no dividends and a five year horizon in all Black Scholes option pricing calculations.

Additional advances totaling $1,428,500 have been received on the June 2009 Note since it replaced the shareholder loan owed to HFLP that had a principal balance of $3,762,000 on June 2, 2009 bringing the total principal balance to $5,190,500 at December 31, 2009. The total value of warrants for 2009 from issuances of the June Note was $11,503,750 and the total value of shares was $12,661,000. Since the value of beneficial conversion feature exceeded the amount borrowed, the Company recognized a debt discount to completely offset the amount borrowed. As of December 31, 2009 the balance of the June Note is:

| Principal | | $ | 5,190,500 | |

| Discount | | | 391,851 | |

| Net | | $ | 4,798,649 | |

The remaining debt discount of $391,851 will be amortized equally over the next 12 months ending December 31, 2010. The outstanding convertible debt principal balance of $5,190,500 can be converted into 51,905,000 units, where each unit consists of one share and one warrant to purchase a common share. Each warrant issued pursuant to conversion of the June 2009 Note shall have an exercise price of $0.10 per share and a seven (7) year expiration from the date of issuance.

The following is a summary of common stock warrant activity for each of the three years ended December 31, 2009:

| | | Number of Shares Under Warrants | | | Weighted Average Exercise Price | |

| Balance at December 31, 2006 | | | — | | | | — | |

| Issued in conjunction with conversion of convertible note | | | 600,000 | | | $ | 0.40 | |

| Balance at December 31, 2007 | | | 600,000 | | | $ | 0.40 | |

| Issued in conjunction with conversion of convertible note | | | 43,046,248 | | | $ | 0.40 | |

| Balance at December 31, 2008 | | | 43,646,248 | | | $ | 0.40 | |

| Issued in conjunction with convertible note | | | 2,000,000 | | | $ | 0.10 | |

| Balance at December 31, 2009 | | | 45,646,248 | | | $ | 0.39 | |

NOTE 10 – STOCK OPTION PLAN

The Company’s 2005 Stock Plan permits the granting of up to 3,000,000 non-qualified stock options, incentive stock options, and restricted shares of common stock to employees, directors, and consultants. As of December 31, 2009, there were 2,245,000 stock options granted to employees and consultants, of which 2,195,000 are vested. These options were granted to employees and consultants to the Company. There were no options granted in 2009.

For purposes of calculating the fair value of options, volatility for the two years presented is based on the historical volatility of the Company’s common stock over its public trading life. The Company currently does not foresee the payment of dividends in the near term. The fair value for these options was estimated at the date of grant using the Black-Scholes option-pricing model with the following assumptions:

| | | Years Ended December 31, | |

| | | 2009 | | | 2008 | |

| Weighted average risk free rate: | | | 1.4 | % | | | 1.4 | % |

| Weighted average volatility: | | | 105.1 | % | | | 82.8 | % |

| Expected dividend yield: | | | 0 | | | | 0 | |

| Weighted average life (in years): | | | 5.0 | | | | 5.0 | |

Expenses of $7,000 for stock options issued to employees and zero for stock options issued to non-employees, including consultants and directors, were recorded in 2009. This compares to expenses of $229,262 for stock options issued to employees and $126,588 for stock options issued to non-employees in 2008. The following table summarizes the terms of the options outstanding at December 31, 2009:

| | | Number of Options | | | Weighted Average Exercise Price | | | Weighted Average Remaining Contractual Life (Years) | | | Number of Exercisable Options at December 31, 2009 | |

| | | | 90,000 | | | $ | 0.20 | | | | 2.14 | | | | 90,000 | |

| | | | 700,000 | | | $ | 0.25 | | | | 1.60 | | | | 700,000 | |

| | | | 100,000 | | | $ | 0.30 | | | | 1.83 | | | | 100,000 | |

| | | | 10,000 | | | $ | 0.34 | | | | .58 | | | | 10,000 | |

| | | | 50,000 | | | $ | 0.38 | | | | 3.58 | | | | 50,000 | |

| | | | 650,000 | | | $ | 0.45 | | | | 2.55 | | | | 650,000 | |

| | | | 5,000 | | | $ | 0.55 | | | | 1.50 | | | | 5,000 | |

| | | | 55,000 | | | $ | 0.60 | | | | 2.98 | | | | 55,000 | |

| | | | 150,000 | | | $ | 0.63 | | | | 2.34 | | | | 150,000 | |

| | | | 100,000 | | | $ | 0.64 | | | | 3.69 | | | | 100,000 | |

| | | | 100,000 | | | $ | 0.67 | | | | 4.55 | | | | 50,000 | |

| | | | 235,000 | | | $ | 0.76 | | | | 3.34 | | | | 235,000 | |

| TOTALS | | | 2,245,000 | | | $ | 0.44 | | | | 2.44 | | | | 2,195,000 | |

The following summarizes option activity for the years presented:

| | | | | | | | | |

| Balance at January 1, 2008 | | | 2,340,000 | | | $ | 0.35 | |

| Issued | | | 585,000 | | | | 0.72 | |

| Exercised | | | — | | | | — | |

| Cancelled | | | (60,000 | ) | | | 0.59 | |

| Forefeited (cashless exercise) | | | (370,000 | ) | | | 0.39 | |

| | | | | | | | | |

| Balance at December 31, 2008 | | | 2,495,000 | | | $ | 0.45 | |

| | | | | | | | | |

| Issued | | | — | | | | — | |

| Exercised | | | — | | | | — | |

| Cancelled | | | (250,000.00 | ) | | | 0.61 | |

| | | | | | | | | |

| Balance at December 31, 2009 | | | 2,245,000 | | | $ | 0.44 | |

Options outstanding at December 31, 2009, have a remaining contractual life of approximately 2.44 years.

NOTE 11 – LEASES

The Company has lease commitments on two mineral properties and office and storage space in Liberty Lake, Washington. The leased mineral properties are the Dun Glen property in Nevada and the Bajo Pobré property in the Santa Cruz province of Argentina. As of December 31, 2009 the annual lease obligations are:

| Year | | Office Facility | | | Dun Glen (*) | | | Bajo Pobré | | | Total | |

| 2010 | | | 69,359 | | | | 60,000 | | | | 75,000 | | | | 203,523 | |

| 2011 | | | 69,359 | | | | 72,500 | | | | 75,000 | | | | 216,023 | |

| 2012 | | | 69,359 | | | | 72,500 | | | | 100,000 | | | | 241,023 | |

| 2013 | | | 69,359 | | | | 72,500 | | | | — | | | | 141,023 | |

| 2014 | | | 69,359 | | | | 72,500 | | | | — | | | | 141,023 | |

The original commercial lease on our office space was entered into on July 1, 2005 and has a term of ten years which will expire on June 30, 2015. The rental rate shall be increased annually on the first day of July at the rate determined by the Consumer Price Index. The table above shows the minimum annual lease payments over the next five years based on the current base rent and does not take into account the rent escalations.

* On December 10, 2009, the Company entered into a Property Interest Purchase Option Agreement (“Black Hawk Agreement”) with Black Hawk Exploration (“Black Hawk”) to transfer 75% of the company’s economic interest in the Dun Glen Project. One of the terms of the Black Hawk Agreement states that Black Hawk has the responsibility to maintain the property in good standing at their expense, including the timely filing or payment of all claims maintenance fees or taxes and all the underlying future lease payments owed by the Company as noted above.

On February 18, 2010 the Company transferred its stock in Black Hawk and its interest in the Dun Glen property to the Hunt Family Limited Partnership (“HFLP”), a related party, along with all its Mexican assets in consideration of cancelling $600,000 of the debt that the Company owed to HFLP on an outstanding note payable. See “Note 16 - Subsequent Events” for further information.

NOTE 12 – RELATED PARTY TRANSACTIONS

The Company leases office space from HFLP, an entity controlled by the Company’s President, Chief Executive Officer and Chairman. The Company paid $69,359 and $68,523 in lease payments to HFLP in 2009 and 2008 respectively. These amounts do not include common area maintenance charges.

On December 18, 2009, in conjunction with the RTO, the Company received an advance of $207,990 from Hunt Mining as a refundable deposit.

At December 31, 2009 the Company transferred a note payable to Huntwood Industries, an entity controlled by the Company’s President, Chief Executive Officer and Chairman. The Company now owes an accounts payable balance of $19,953.72 to Huntwood Industries.

At December 31, 2009 the Company had an accounts payable owing to a director and officer of CCSA, for C$16,805 relating to CCSA’s lease of office space.

At December 31, 2009 the Company had fees payable advance for accounting expenses owing to a director of CCSA, of C$9,241.

During the year ended December 31, 2009 the Company paid C$57,002 to a director of CCSA for accounting fees.

During the year ended December 31, 2009 the Company paid C$144,843 to a director of CCSA for geological fees.

As of December 31, 2008 the Company had an exploration advance receivable of $200 owed by an executive officer of the Company.

During the year ended December 31, 2008 the company paid $14,938 to a director of the Company, for consulting services.

At December 31, 2008 the Company had an employee exploration expense payable of C$4,172 owing to Danilo Silva for exploration expenses incurred on behalf of the Company.

At December 31, 2008 the Company had fees payable advance for accounting expenses owing a director of CCSA of C$5,072.

During the year ended December 31, 2008 the Company paid C$24,841 to a director of CCSA for accounting fees.

During the year ended December 31, 2008 the Company paid C$122,980 to a director of CCSA for geological fees.

Additional related party transactions are included as part of Note 8, Note 9, Note 13 and Note 16.

NOTE 13 – REVERSE TAKEOVER TRANSACTION

On December 23, 2009 the company completed a reverse takeover transaction (“RTO”) in which 100% of the shares of its Argentine wholly owned subsidiary, CCSA, were acquired by Hunt Mining. Hunt Mining is a mineral exploration company incorporated on January 10, 2006 under the laws of Alberta, Canada. Prior to December 23, 2009 Hunt Mining was a Capital Pool Company within the meaning ascribed by Policy 2.4 of the TSX Venture Exchange. Hunt Mining issued 29,118,507 common shares and 20,881,493 non-voting convertible preferred shares to the Company at a deemed price of C$0.30 per Common Share and C$0.30 per convertible preferred share. Each convertible preferred share shall be convertible into one Common Share of Hunt Mining for no additional consideration at any time as long as the public floa t is not less than 20%. This transaction gave the Company controlling interest in Hunt Mining, 65% owned by the Company and 4% owned by the Company’s wholly-owned subsidiary HuntMountain Investments, LLC (“HMI”). If all options and warrants, of Hunt Mining were exercised, the Company’s interest would be reduced to 57%.

The net assets acquired from Hunt Mining were as follows:

| Cash | | $ | 245,082 | |

| Other Assets | | | 163,163 | |

| Accounts Payable | | | (3,308 | ) |

| Total | | $ | 404,937 | |

As a condition of the RTO, the Company entered into an agreement with CCSA pursuant to which the Company agreed to pay all of the CCSA’s remaining accounts payable owed to Patagonia Drill Mining Services S.A. (“PDM”). In order to pay all of the payables owing to PDM in accordance with the terms of the qualifying transaction, management negotiated an agreement with PDM pursuant to which the Company agreed to purchase all remaining accounts payable owed by the CCSA to PDM for total consideration of $1,029,373. This amount excluded the $584,000 deposit made by the Company against the PDM payables in 2008. Therefore, the $584,000 deposit amount was applied to the CCSA’s PDM payables concurrently with the signing of the agreement.

NOTE 14 – VALUE ADDED TAX CREDIT

The Company has in other assets --Receivable - V.A. tax, Argentina as of December 31, 2009 and 2008 of $489,598 and $380,153 respectively. These amounts reflect the Value Added Tax Credit accrued due to the payment of valued added tax on certain transactions in Argentina. The Company will realize this credit as an offset against V.A. taxes due on future revenues. In accordance with APB 21, the asset is reported at net present value based upon the Company’s estimate of future revenues. The Company used an expected benefit period of 7 years and a discount rate of 18.6% based upon the average Argentine interest rates and has recorded, as other expense, a $85,943 net present value adjustment in 2009, which is not deemed to be recoverable at this time.

NOTE 15 – PROPERTY AND EQUIPMENT

For the year ending December 31, 2009 the Company acquired $2,912 in office furniture and equipment and $4,045 in excavation equipment. The excavation equipment has not yet been placed into service and therefore no depreciation expense was recorded in 2009. The excavation equipment is included in the idle equipment in the table below.

In July of 2008 the Company acquired for cash a truck-mounted drilling rig for $260,634. In December of 2008 the Company acquired spare parts and other related equipment for the drilling rig at a cost of $91,418. In October of 2008 the Company acquired a bulldozer for $37,765. These items have not been placed into service as of the year ending December 31, 2009 and therefore no depreciation expense has been recorded to date. These items are shown in the table below as idle equipment.

In April, May and June of 2008 CCSA acquired three trucks, with a December 31, 2009 undepreciated value of $128,792. In 2008 CCSA acquired computer and camp equipment with a December 31, 2009 undepreciated value of $137,706. Also in 2007, CCSA acquired the La Josefina Estancia for $710,000.

The following is a summary of property, equipment and accumulated depreciation at December 31, 2009 and 2008:

| | | December 31, 2009 | | | December 31, 2008 | |

| Office Furniture & Equipment | | $ | 324,492 | | | $ | 322,047 | |

| | | | | | | | | |

| Land | | | 710,000 | | | | 710,000 | |

| Less accumulated depreciation | | | 203,005 | | | | 98,660 | |

| Subtotal: Property, Plant & Equipment, net: | | | 831,487 | | | | 933,387 | |

| Idle Equipment | | | 393,862 | | | | 389,817 | |

| Total: Property, Plant & Equipment, net: | | $ | 1,225,349 | | | $ | 1,323,204 | |

Depreciation expense was $105,547 in 2009 and $90,634 in 2008.

The Company evaluates the recoverability of property and equipment when events and circumstances indicate that such assets might be impaired. The Company determines impairment by comparing the undiscounted future cash flows estimated to be generated by these assets to their respective carrying amounts.

Maintenance and repairs are expensed as incurred. Replacements and betterments are capitalized. The cost and related reserves of assets sold or retired are removed from the accounts, and any resulting gain or loss is reflected in results of operations.

NOTE 16 - SUBSEQUENT EVENTS

Shareholder Loan

Subsequent to December 31, 2009 HFLP loaned an additional $40,000 to the Company under the same terms as discussed in Note 9.

Transfer of investments to related party

On February 18, 2010 the Company transferred its stock in Black Hawk and its interest in the Dun Glen property to the Hunt Family Limited Partnership (“HFLP”), a related party, along with all its Mexican assets in consideration of cancelling $600,000 of the debt that the Company owed to HFLP on an outstanding note payable. The book value of the properties and stock transferred was $433,532 resulting in a gain on the sale of investments of $166,468 which was recorded in the first quarter of 2010.

Loan Purchase Agreement

On March 8, 2010, Hunt Mining announced that it received acceptance from TSX Venture Exchange to enter into an agreement to purchase a portion of a loan owing from its wholly owned subsidiary CCSA to HuntMountain. Hunt Mining will acquire a portion of the loan totaling $700,000 at a 3% discount to the originally loaned amount. The total acquisition cost is therefore $679,000. Due to Argentine banking regulations, acquiring the loan in this way allows Hunt Mining to retain more working capital than if CCSA paid the loan back directly to HuntMountain.

An agreement establishing the loan from HuntMountain to Hunt Mining was effected in June of 2009. The purpose of the loan was to finance CCSA’s ongoing operations while Hunt Mining’s management was working on the RTO that closed on December 23, 2009.

Payoff of Assumed Accounts Payable

As noted in Note 13, a condition of the Share Purchase Agreement relating to the RTO was that the Company must enter into a Note Receivable Agreement with CCSA pursuant to which the Company would agree to pay the remaining accounts payable of CCSA owed to an Argentine drilling contractor in the approximate amount of $1,613,373. On March 9, 2010, the Company made a payment of $700,000 on the assumed liability from CCSA and converted $584,000 that had been recorded as a prepayment on the assumed liability which left an additional amount of $329,373 which was converted into a promissory note to the drilling contractor. The note bears is payable in 8 monthly installments of $40,000 due on the 25th of each month starting April 25, 2010 and a final payment on December 25, 2010 of $18,752. The company has made the April, May, June, July and August payments leaving an unpaid principal balance of $139,126 as of the date of this report.

Purchase of Furniture and Fixtures from a Related Party

Subsequent to March 31, 2010 Hunt Mining acquired furniture and fixtures from HFP, LLC, an entity controlled by the Company’s President and Chief Executive Officer, for US$42,368.

Purchase of Equipment from a Related Party

On June 8, 2010, HFLP, a related party, purchased from the Company a fully depreciated truck for $5,000 which the Company recorded as a gain on the sale of equipment. HFLP also purchased a tractor for $34,000 that had a carrying value of $37,764 with no depreciation because it had yet to be placed into service. The Company recorded a loss on the sale of equipment of $3,764. The final item that was purchased for $1,625 was a rock saw that had previously been expensed and had no book value. The Company recorded a gain on the sale of the rock saw of $1,625.

Deposits received for the Sale of Idle Drilling Equipment from a Related Party

Deposits in the amount of $49,263, $48,732 and $39,865 were received on July 14, 2010, September 1, 2010 and October 13, 2010 respectively, combined with the forgiveness of an accounts payable amount of $19,954 for a total of $157,814 for the sale of the Company’s idle drilling equipment to Huntwood Industries, a related party. The drilling equipment had a book value of $356,097 and the Company will recognize a loss on the sale of equipment in the amount of $198,283.

Dissolution of the Company

On February 18, 2010, the Company’s board of directors recommended and authorized a shareholder meeting to consider and vote upon a proposal to approve the voluntary dissolution and liquidation of the Company pursuant to a plan of complete dissolution and liquidation dissolution. On July 16, 2010, the Company filed with the Securities and Exchange Commission (“SEC”), a preliminary schedule 14A proxy statement to submit the vote to the Company’s shareholders. As of the date of the filing of this form 10-K, the preliminary 14A proxy statement has not yet been approved by the SEC and the vote has yet to go before the shareholders. The dissolution of the Company, if approved by the shareholders, will not affect the operations of Hunt Mining which will continue in existence along with its subsid iary companies.

Warrant and Option Cancellation Agreements

In February 18, 2010 the Company’s board of directors approved the Company to enter into warrant and option cancellation agreements with holders of the Company’s warrants and options. The terms of such agreements are to be that such holder will agree to their warrants and/or options being cancelled in exchange for a common share grant equal to 10% of the number of warrants/options held. As of July 1, 2010, most of the holders have signed such agreements, leaving only 300,000 of the Company’s warrants/options outstanding.

Subsequent events have been evaluated through November 9, 2010, the date that these financial statements were available to be issued.

| ITEM 9. | CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL DISCLOSURE |

Not applicable.

| ITEM 9A. | CONTROLS AND PROCEDURES |

EVALUATION OF DISCLOSURE CONTROLS AND PROCEDURES

In connection with the preparation of this annual report on Form 10-K, an evaluation was carried out by the Company’s management, with the participation of the Chief Executive Officer, of the effectiveness of the Company’s disclosure controls and procedures (as defined in Rules 13a-15(e) and 15d-15(e) under the Securities Exchange Act of 1934 (“Exchange Act”)) as of December 31, 2008. Disclosure controls and procedures are designed to ensure that information required to be disclosed in reports filed or submitted under the Exchange Act is recorded, processed, summarized, and reported within the time periods specified in the SEC rules and forms and that such information is accumulated and communicated to management, including the Chief Executive Officer and the Chief Financial Officer, to allow timely d ecisions regarding required disclosures.

Based on that evaluation, the Company’s management concluded, as of the end of the period covered by this report, that the Company’s disclosure controls and procedures were not effective in recording, processing, summarizing, and reporting information required to be disclosed, within the time periods specified in the Securities and Exchange Commission’s rules and forms.

MANAGEMENT’S REPORT ON INTERNAL CONTROL OVER FINANCIAL REPORTING

Management of the Company is responsible for establishing and maintaining adequate internal control over financial reporting. The Company’s internal control over financial reporting is a process, under the supervision of the Chief Executive Officer and the Chief Financial Officer, designed to provide reasonable assurance regarding the reliability of financial reporting and the preparation of the Company’s financial statements for external purposes in accordance with United States generally accepted accounting principles (GAAP). Internal control over financial reporting includes those policies and procedures that:

| | ● | Pertain to the maintenance of records that in reasonable detail accurately and fairly reflect the transactions and dispositions of the Company’s assets; |

| | | Provide reasonable assurance that transactions are recorded as necessary to permit preparation of the financial statements in accordance with generally accepted accounting principles, and that receipts and expenditures are being made only in accordance with authorizations of management and the Board of Directors; and |

| | | Provide reasonable assurance regarding prevention or timely detection of unauthorized acquisition, use, or disposition of the Company’s assets that could have a material effect on the financial statements. |

Because of its inherent limitations, internal control over financial reporting may not prevent or detect misstatements. Also, projections of any evaluation of effectiveness to future periods are subject to the risk that controls may become inadequate because of changes in conditions or that the degree of compliance with the policies or procedures may deteriorate.

The Company’s management conducted an assessment of the effectiveness of the Company’s internal control over financial reporting as of December 31, 2009, based on criteria established in Internal Control – Integrated Framework issued by the Committee of Sponsoring Organizations of the Treadway Commission (“COSO”). As a result of this assessment, management identified material weaknesses in internal control over financial reporting.

A material weakness is a control deficiency, or a combination of deficiencies, in internal control over financial reporting such that there is a reasonable possibility that a material misstatement of the Company’s annual or interim financial statements will not be prevented or detected on a timely basis.

The material weaknesses identified are described below:

Lack of Appropriate Accounting Policies, Procedures, and Sufficiency of Accounting Resources. Management of HuntMountain has not established with appropriate rigor the accounting policies, procedures, and documentation of significant judgments and estimates made by management in the preparation of the financial statements. Additionally, the Company has limited accounting personnel to prepare its financial statements, including the consolidation of the Company and its subsidiaries. As a result of the identified material weakness, required material adjustments were identified by the auditors.

As a result of the material weaknesses in internal control over financial reporting described above, HuntMountain’s management has concluded that, as of December 31, 2009, the Company’s internal control over financial reporting was not effective based on the criteria in Internal Control – Integrated Framework issued by the COSO.

This annual report does not include an attestation report of our independent registered public accounting firm regarding internal control over financial reporting. We were not required to have, nor have we, engaged our independent registered public accounting firm to perform an audit of internal control over financial reporting pursuant to the rules of the Securities and Exchange Commission that permit us to provide only management’s report in this annual report.

CHANGES IN INTERNAL CONTROL OVER FINANCIAL REPORTING

As of the end of the period covered by this report, there have been no changes in internal control over financial reporting (as defined in Rule 13a-15(f) of the Exchange Act) during the period ended December 31, 2009, that materially affected, or are reasonably likely to materially affect, the Company’s internal control over financial reporting.

| ITEM 9B. | OTHER INFORMATION. |

The Company failed to file a form 8-K on October 19, 2009 under Item 1.01 “Entry into a Material Definitive Agreement”. On October 13, 2009, the Company entered into a Share Purchase Agreement (“the Agreement”) between Sinomar Capital Corp (“Sinomar”) and Cerro Cazador S.A. (“CCSA”) and HuntMountain Resources LTD (“HuntMountain”) and HuntMountain Investments, LLC (“HMI”) whereas HuntMountain and HMI are hereinafter collectively called the “Shareholders”.

Subject to the terms and conditions of the Agreement, Sinomar agrees to purchase all of the CCSA Shares from the Shareholders and in consideration therefor Sinomar shall issue to the Shareholders an aggregate total of 29,118,507 Sinomar Common Shares and 20,881,493 Sinomar Preferred Shares, at a deemed price of $0.30 per Sinomar Common Share and $0.30 per Sinomar Preferred Share, in exchange for all of the CCSA Shares, and the Shareholders agree to sell all of the Shareholders’ CCSA Shares on the foregoing basis.

A copy of the Agreement is filed along with this form 10-K as exhibit 10.1.

PART III

| ITEM 10. | DIRECTORS, EXECUTIVE OFFICERS AND CORPORATE GOVERNANCE. |

Directors and Executive Officers

The following information is provided with respect to each executive officer and director of the Company:

| Name (age) | | Position | | Length of Service |

| | | | | |

| Tim Hunt (57) | | President, Chief Executive Officer and Chairman | | 2005 |

| | | | | |

| William R. Green (71) | | Director | | 1993* |

| | | | | |

| Eberhard A. Schmidt (72) | | Director | | 2005 |

| | | | | |

| Alastair H. Summers (73) | | Director | | 2006 |

| | | | | |

| Randal L. Hardy (48) | | Director | | 2005** |

| | | | | |

| Darrick Hunt (32) | | Director | | 2008 |

| | | | | |

| Matthew J. Hughes (49) | | Executive Vice-President of Exploration & Chief Operating Officer | | 2005*** |

| | | | | |

| Danilo Silva (47) | | President of CCSA | | 2006 |

| | | | | |

| Bryn Harman, CFA (40) | | Chief Financial Officer | | 2007*** |

*Previously held executive officer and director positions with the predecessor company, Metaline Mining & Leasing Company.

**Previously served as President and Chief Financial Officer of the Company.

*** Effective February 2, 2010 Mr. Matthew Hughes resigned from the position of Executive Vice-President of Exploration and Chief Operating Officer of the Company and Mr. Bryn Harman resigned from the position of Chief Financial Officer of the Company.

Tim Hunt, President, Chief Executive Officer and Chairman, is a general partner of HFLP and is the founder and president of Spokane, Washington-based T.R.A. Industries, Inc., dba Huntwood Industries, one of the largest building products manufacturers in the Western United States. Mr. Hunt has led the development of Huntwood Industries over the past 20 years – taking the business from a start-up venture to a significant middle-market enterprise. During his business career, Mr. Hunt has been engaged in a variety of business start-up ventures both related and unrelated to Huntwood Industries. Mr. Hunt had also previously served as a member of the board of director s at State National Bank; a community based financial institution headquartered in Eastern Washington. Mr. Hunt also spent two years as an investment banker, specializing in the mining industry, with National Securities.

William R. Green, P.E., Ph.D. is a mining engineer and geologist, and was a professor of mining engineering at the University of Idaho from 1965 to 1983. He has been actively involved in the mining industry since 1962, working as a consultant to financial managers and various US and Canadian public mining companies. He was a co-founder, and served as an officer and director, of both Bull Run Gold Mines and Yamana Resources. He was the President, CEO and Chairman of Mines Management, Inc., a U.S. public company from 1964 until 2003.

Eberhard A. Schmidt, Ph.D. has more than 35 years of experience in exploring, evaluating and developing precious and base metal properties in the western United States and Mexico. He managed regional exploration offices for Cyprus Mines, Amoco Minerals and Meridian Minerals in Spokane and for Minera Hecla in Mexico. Dr. Schmidt received his Ph.D. in Structural and Economic Geology from the University of Arizona and is a past president of the Northwest Mining Association.

Alastair H. Summers has more than 45 years of experience in mine development and production in North and South America, including over ten years as an executive with Hecla Mining Company. He was Vice President and General Manager for Minera Hecla de Mexico responsible for the design, construction, operation and reclamation of the La Choya open pit/heap leach gold mine. Mr. Summers also served as President and General Manager of Minera Hecla Venezolana initiating improvements to Hecla’s La Camorra operation which resulted in production increases from 85,000 to 250,000 ounces of gold per year. Mr. Summers’ career includes the development, design, and operat ion of several successful mines for The Bunker Hill Company, Western Nuclear, and American Mine Services. He is registered as a Professional Geologist in Idaho and Professional Engineer in Colorado.

Randal L. Hardy, serves as President and CEO Timberline Resources Corporation, a public drilling and precious metals exploration venture based in Coeur d’Alene, ID. Mr. Hardy was appointed as a Director in August 2007. Mr. Hardy was appointed to this position after previously holding the position of President of the Company since September 2006, and immediately prior to this time servicing as its Vice President and Chief Financial Officer. Mr. Hardy has over 20 years of experience in financial and operational management. He is the former President and CEO of Sunshine Minting, Inc., a precious metal custom minting and manufacturing firm. During his 8-year tenure as the Company’s President, it grew from 25 employees to over 125. Prior to this, Mr. Hardy served as Treasurer of the NYSE-listed Sunshine Mining and Refining Company for over 6 years. He graduated Magna Cum Laude from Boise State University with a BBA in Finance.

Darrick Hunt, CPA is the Chief Financial Officer of Spokane, Washington-based Huntwood Industries, the largest building materials manufacturer and one of the largest employers in the Eastern Washington/Northern Idaho region. He holds a license as a Certified Public Accountant under the Board of Accountancy of Washington State, having received his Bachelors in Business Administration from Gonzaga University.