UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

Proxy Statement Pursuant to Section 14(a) of the

Securities Exchange Act of 1934

(Amendment No. )

Filed by the Registrantx Filed by a Party other than the Registrant¨

Check the appropriate box:

| ¨ | Preliminary Proxy Statement |

| ¨ | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) |

| ¨ | Definitive Proxy Statement |

| ¨ | Definitive Additional Materials |

| x | Soliciting Material Pursuant to §240.14a-12 |

The Midland Company

(Name of Registrant as Specified In Its Charter)

Payment of Filing Fee (Check the appropriate box):

| x | No fee required. |

| ¨ | Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. |

| (1) | Title of each class of securities to which the transaction applies: |

| (2) | Aggregate number of securities to which the transaction applies: |

| (3) | Per unit price or other underlying value of the transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): |

| (4) | Proposed maximum aggregate value of the transaction: |

| (5) | Total fee paid: |

| ¨ | Fee paid previously with preliminary materials. |

| ¨ | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. |

| (1) | Amount Previously Paid: |

| (2) | Form, Schedule or Registration Statement No.: |

| (3) | Filing Party: |

| (4) | Date Filed: |

The Midland Company made available the slides filed herewith on October 29, 2007 at the insurance industry meeting identified therein.

AMERICAN MODERN INSURANCE GROUP 1 2007 PCI Presentation Boston, MA October 28-31, 2007 |

AMERICAN MODERN INSURANCE GROUP 2 AMERICAN MODERN AMERICAN MODERN INSURANCE GROUP INSURANCE GROUP 2007 PCI Annual Meeting 2007 PCI Annual Meeting Presented By: Presented By: John W. Hayden John W. Hayden President & Chief Executive Officer President & Chief Executive Officer Dan Gilene Dan Gilene Senior Vice President, Reinsurance Senior Vice President, Reinsurance |

AMERICAN MODERN INSURANCE GROUP 3 American Modern has a signed merger agreement with Munich Re • Anticipate deal will close in first half of 2008, pending regulatory and shareholder approval AMIG will operate as an independent member within the Munich Re Group - “Business as Usual” • AMIG operations will remain in Cincinnati, with existing Senior Management team and associates remaining in place American Modern to Merge with Munich Re |

AMERICAN MODERN INSURANCE GROUP 4 The strategy for Munich Re’s U.S. operations is to build a dominant presence in the niche primary specialty insurance segments • AMIG offers an excellent platform to support this strategy Joining forces with one of the largest reinsurance companies in the world will allow AMIG to: • Leverage existing P&C specialty expertise and product distribution platform • Expand in ways that may not have been possible in select specialty niches • Better serve our existing policyholders and distribution partners • Seize a wider variety of market opportunities A Unique Opportunity |

AMERICAN MODERN INSURANCE GROUP 5 Because some of you may be shareholders of the company, you will have the opportunity to vote on the merger. Any time the management team or I speak with shareholders, our communications may be considered by the SEC to be a solicitation of your vote on the transaction. As a result, I am required to refer you to the proxy materials that will be filed with the SEC and posted on our website. Shareholder Information |

AMERICAN MODERN INSURANCE GROUP 6 American Modern At A Glance American Modern Insurance Group Specialty P&C insurance company Short-tail personal lines experts 50-state platform Ratings and recognitions “A+” (Superior) A.M. Best Rating Ward’s Top 50 P&C Insurance Co’s Forbes’ “200 Best Small Co.’s” |

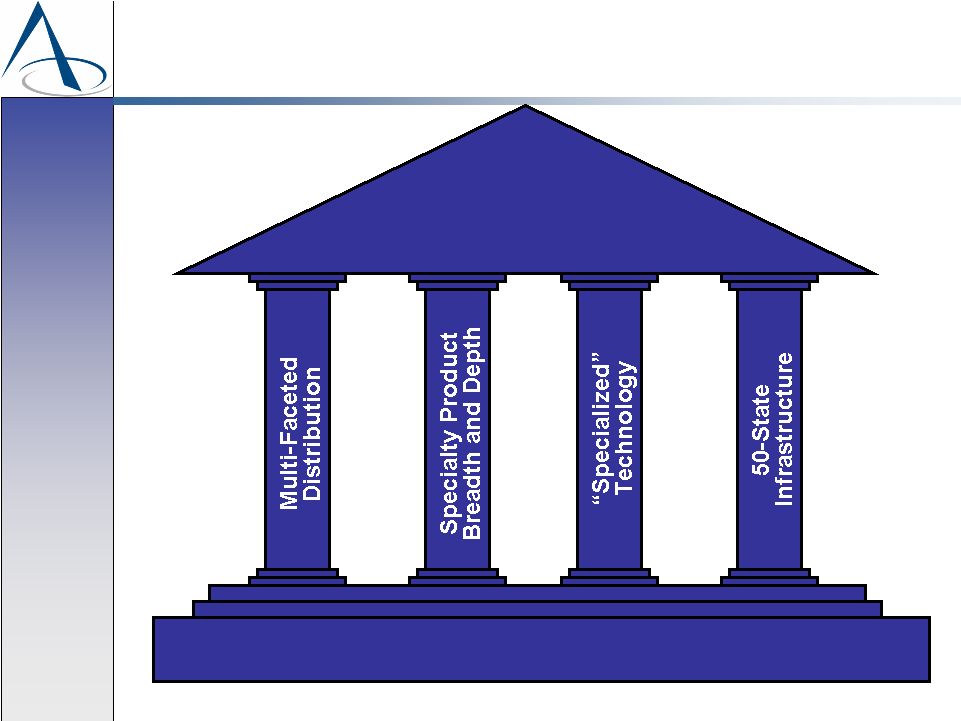

AMERICAN MODERN INSURANCE GROUP 7 American Modern Insurance Group Target Specialty Niches Outside of Standard Market “Beyond Standard” Products - Service - Performance |

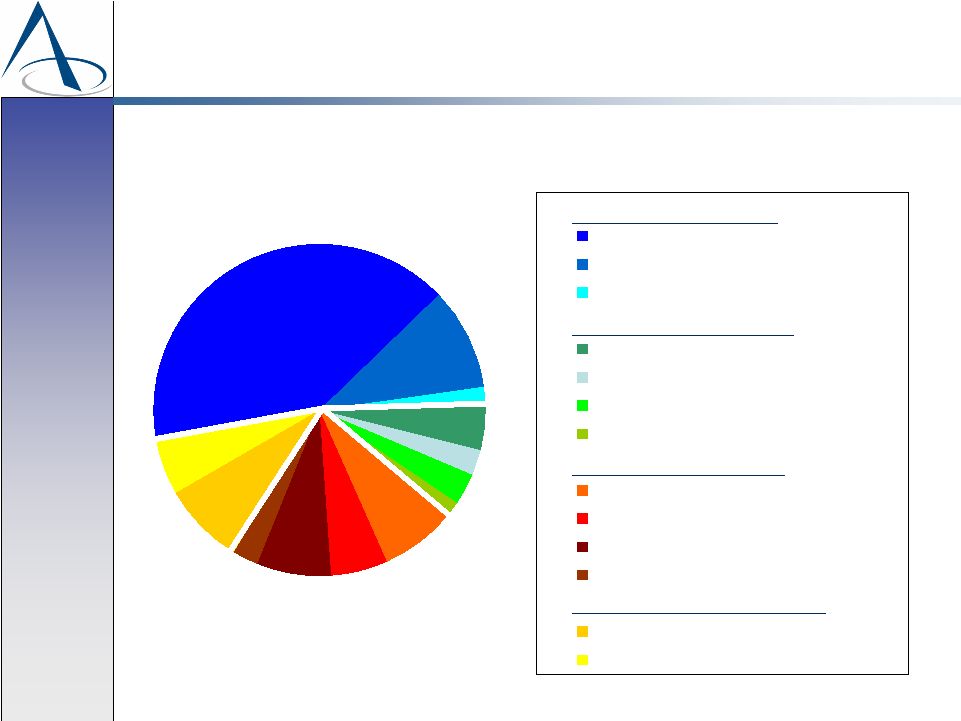

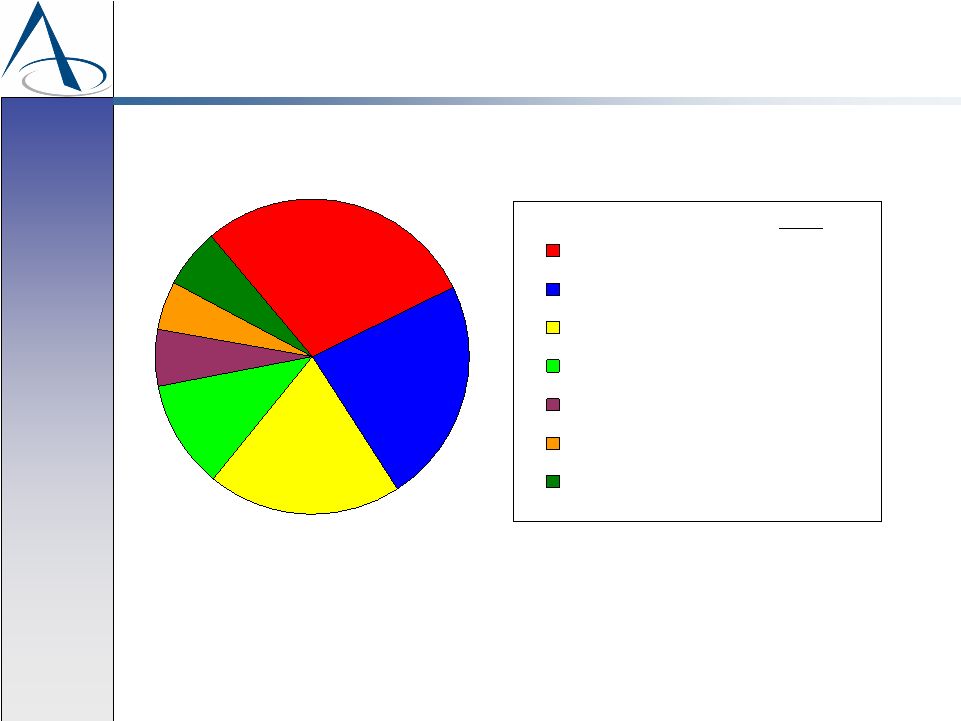

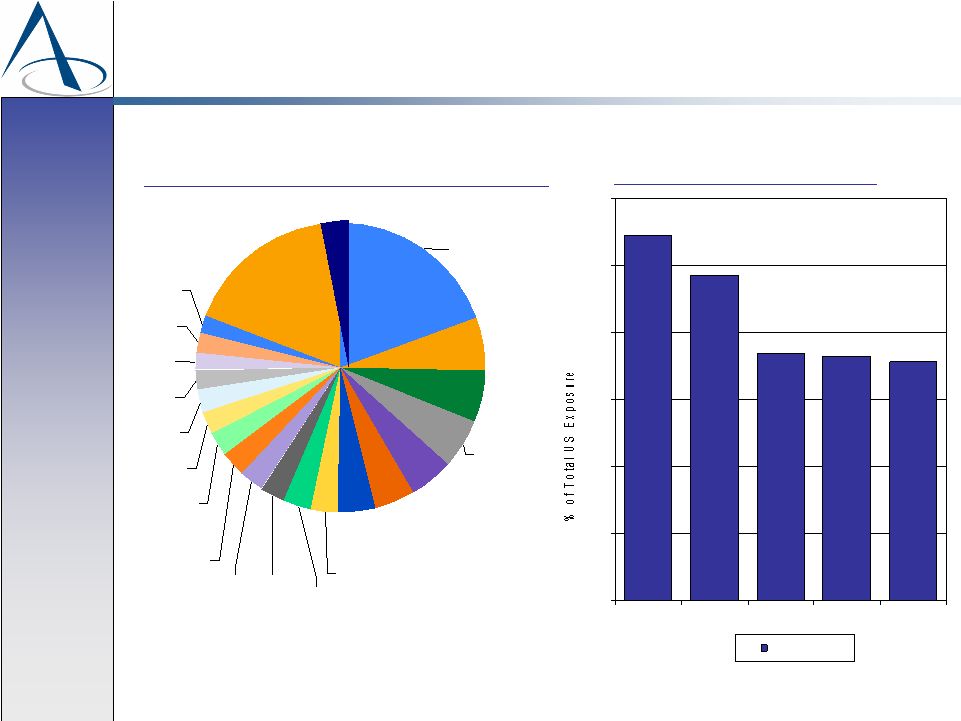

AMERICAN MODERN INSURANCE GROUP 8 Manufactured Housing - $337.8 Dwelling Fire - $81.5 Other Residential Property - $16.0 Motorcycle - $35.7 Watercraft - $22.1 Recreational Vehicle - $24.8 Collector Car / Snowmobile - $11.7 Mortgage Fire - $61.3 Collateral Protection - $46.3 Credit Life & Debt Cancellation - $60.9 Other Financial Institutions - $21.3 Excess & Surplus - $66.5 Other - $45.6 Residential Property - 52% Recreational Casualty - 11% Financial Institutions - 23% Other Specialty Products - 14% Specialty Product Platform Full Year 2006 Residential Property All Other Financial Institutions Recreational Casualty $831.8 Million Total Premiums Property, Casualty and Life Direct & Assumed Written Premium ($ in Millions) |

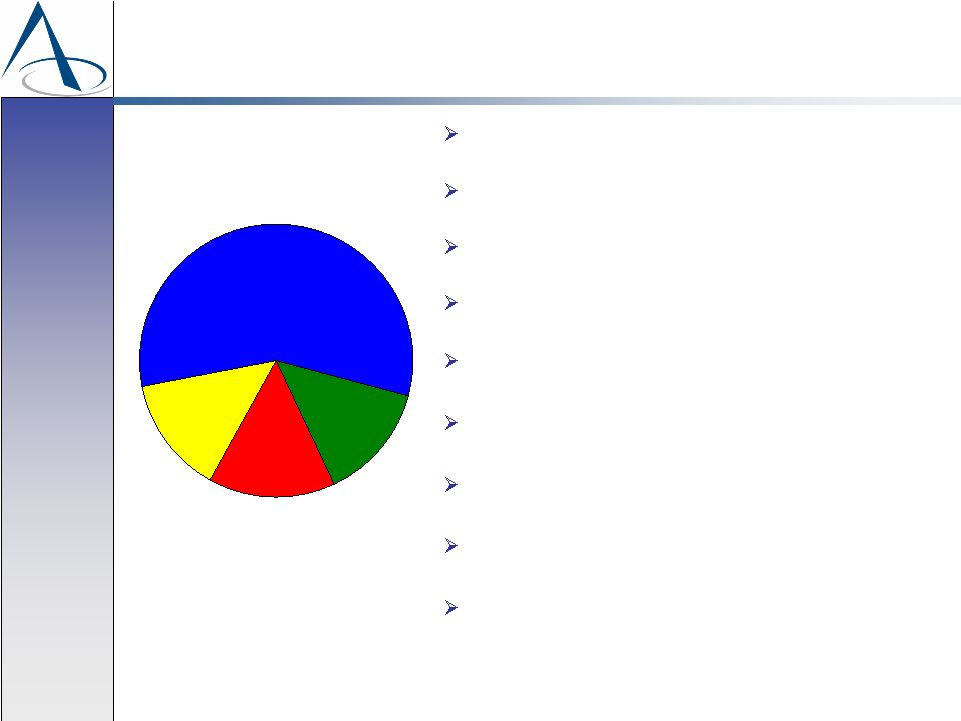

AMERICAN MODERN INSURANCE GROUP 9 Essential Product Characteristics Specialty / Niche Fragmented/Unfocused Competition Non-Cyclical Low Severity Short Tail Property Bias Predominantly Personal Lines Product, Underwriting and Claims Expertise Systems/Technology Excellence Provides an Edge Residential Property Recreational Casualty All Other Financial Institutions |

AMERICAN MODERN INSURANCE GROUP 10 Financial Objectives 12-15% Return On Beginning Equity 10-12% Top-Line Growth Double Digit Growth in Book Value Per Share Double Digit Growth in Operating Earnings Per Share “Defy Insurance Industry Cyclicality” 12% 15% |

AMERICAN MODERN INSURANCE GROUP 11 People People Core Operating Strategies “Compete on Value, Not on Price” |

AMERICAN MODERN INSURANCE GROUP 12 Profit Strategy Absolute Devotion to Rate Adequacy Product Design and Pricing Expertise Portfolio Underwriting Process Proactive Risk Management Claims Mastery Technological Superiority Policyholder Retention Business Partner Selection and Management “Compete on Value, Not on Price” |

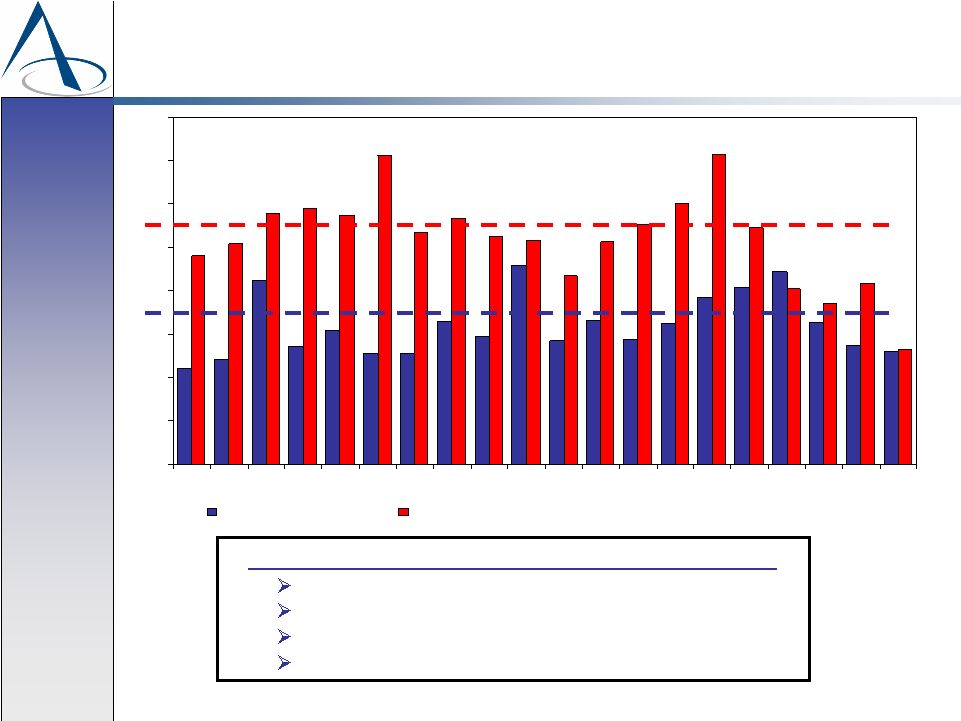

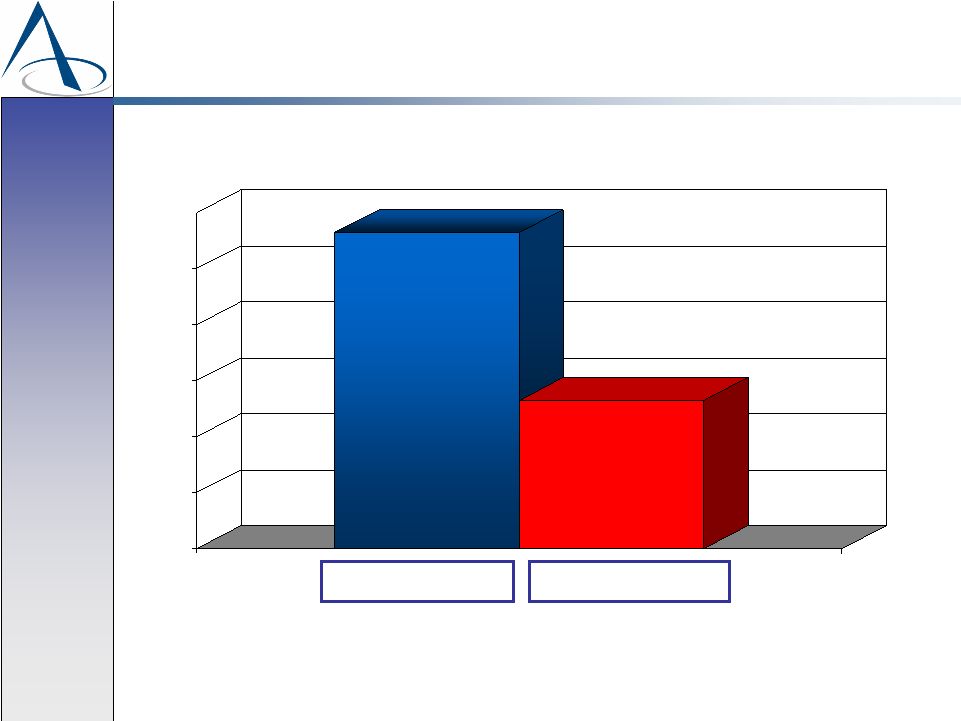

AMERICAN MODERN INSURANCE GROUP 13 96.6% 104.1% American Modern P&C Industry A Tradition of Profitable Underwriting Outperformed P&C Industry by almost 8 Points! Source: A.M. Best Company Through December, 2006 10-Year Average Combined Ratio 100% |

AMERICAN MODERN INSURANCE GROUP 14 80% 85% 90% 95% 100% 105% 110% 115% 120% 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 AMIG Combined Ratio P&C Industry Combined Ratio A Tradition of Profitable Underwriting Source: A.M. Best Company Not Another Cyclical P&C Insurance Company Consistently outperforming the industry Averaging 10 points better over 20 years 15 years at or below 20 year average 93-94% current and anticipated run-rate Industry Average 106% AMIG Average 96% |

AMERICAN MODERN INSURANCE GROUP 15 Achieving Certainty in an Uncertain Business 20-Year Statutory Combined Ratio Ex-CAT 89.9% • 13 years below 89.9% • Only 1 year above 95.0% 20-Year Catastrophe Loss Ratio 6.1% • 7 years less than 5 points • 19 years less than 10 points |

AMERICAN MODERN INSURANCE GROUP 16 160 employee field claims staff adjusters 90% of claims settled by company employees 10% lower average adjustment cost per claim by staff 90+% of property claims closed within 30 days of report Unique In-House Staff Adjuster Training Program Claims Mastery Enables Underwriting Profit |

AMERICAN MODERN INSURANCE GROUP 17 Nine month property and casualty combined ratio of 92.2 percent • Driven by solid non-catastrophe underwriting • Further enhanced by lower than normal catastrophe losses Solid profit results emanating across the breadth of our specialty product platform 2007: Another Record Year In The Making |

AMERICAN MODERN INSURANCE GROUP 18 People People Core Operating Strategies “Target Niches Where Competition is Fragmented/Unfocused” |

AMERICAN MODERN INSURANCE GROUP 19 Growth Strategy Multi-Channel Distribution Growing Producer Base “Point and Click” Easy to Use Technology Product Offering Breadth Product Offering Depth Enhanced Market Awareness Retention of Existing Policyholders Focused Acquisition Appetite “Target Niches Where Competition is Fragmented/Unfocused” |

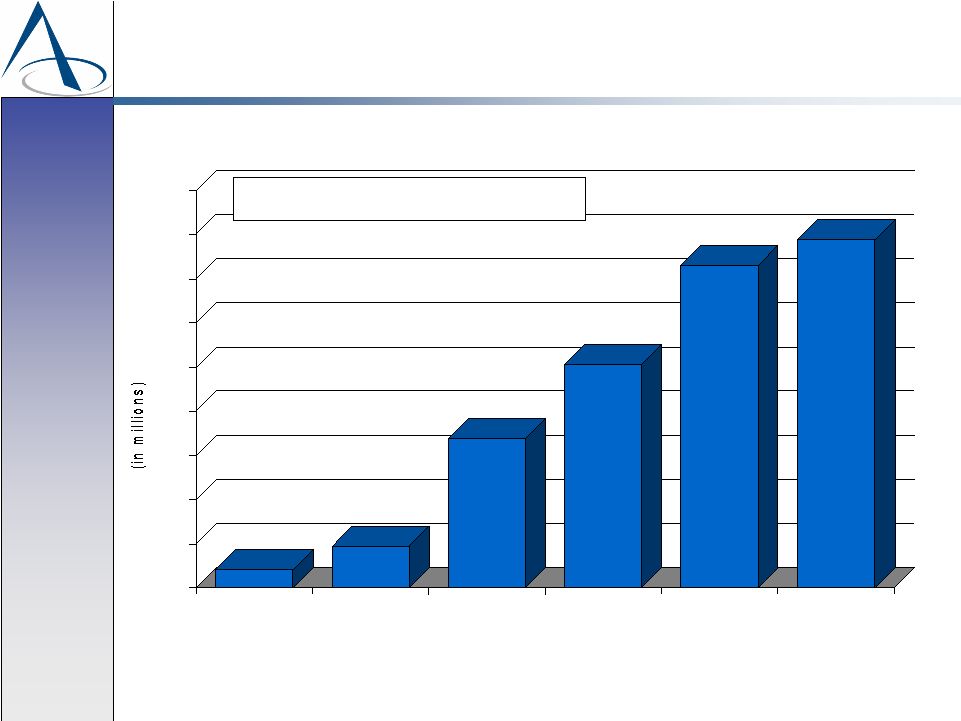

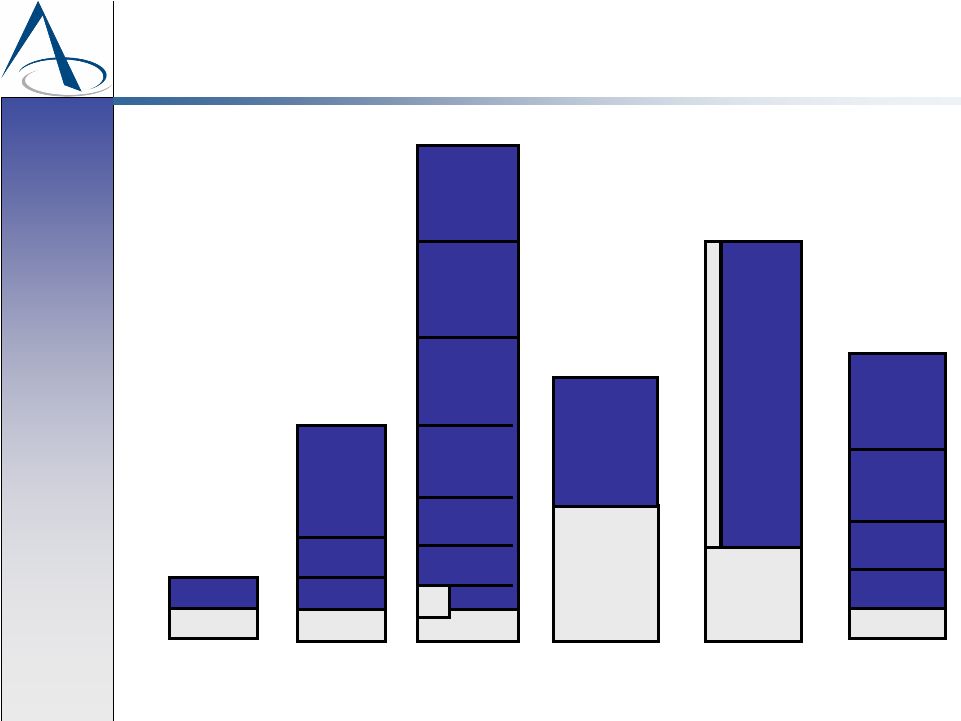

AMERICAN MODERN INSURANCE GROUP 20 $92 $143 $387 $556 $781 $840 $50 $150 $250 $350 $450 $550 $650 $750 $850 $950 '86 '91 '96 '01 '06 '07 LTM P&C Direct and Assumed Written Premium 20 Year CAGR = 11.3% A Tradition of Top-Line Growth |

AMERICAN MODERN INSURANCE GROUP 21 11.3% 5.3% 0% 2% 4% 6% 8% 10% 12% 20-Year Compounded Annual Premium Growth Rate Industry Source: A.M. Best Company American Modern P&C Industry Outpacing Industry Growth Through December 31, 2006 |

AMERICAN MODERN INSURANCE GROUP 22 General Agents 29% Financial Institutions 23% Point of Sale 20% Lender 11% Independent Agents 6% Specialty Agents 5% All Other 6% Property & Casualty and Life Direct & Assumed Written Premium Multi-Channel Distribution December 31, 2006 2006 Strategically Matching Distribution to Product and Marketplace Opportunities |

AMERICAN MODERN INSURANCE GROUP 23 How are we doing it? • Mortgage fire and collateral protection driving strong growth • Core residential property and recreational casualty lines continue to grow nicely • Retention rates at record levels and continue to trend favorable increasing in 27 out of the last 28 months • Total brand awareness has increased more than 30 percent over the last 2 years • modernLINK quote activity continues to gain momentum, increasing more than 16 percent over last year 2007: Outstanding 14% Growth Rate |

AMERICAN MODERN INSURANCE GROUP 24 People People Core Operating Strategies “Attract + Align + Invest = Retain” |

AMERICAN MODERN INSURANCE GROUP 25 People Strategy: “Attract + Align + Invest = Retain” 1,225 Associates Leadership Team Averages 20 Years Industry Experience Core Values: Integrity Win/Win Team Midland University: 165 Designations in 2006 Low Associate Turnover: 7.5%, 3-Year Average Humility Personal Growth Creativity Propriety Sharing/Caring Strong Work Ethic Excerpts from Associate Survey completed May 2007 (Source: Stanard and Associates) • +90% of Associates: - Are dedicated to a successful company future - Understand how their role contributes to the success of Midland - Feel they can have a direct impact on Midland’s success |

AMERICAN MODERN INSURANCE GROUP 26 PROFIT: Superior Underwriting; 96.0% 20-Year Statutory Combined Ratio Earnings Strength; Record Results for the Last Three Consecutive Years Broad Platform; All Product Groups Contributing to 93.8% 2006 Combined Ratio Investment Income; 8.2% 10-Year CAGR GROWTH: Impressive Growth; 11.3% 20-Year P&C Premium CAGR Significant Market Potential; Expanded From $4 Billion to $43 Billion Diverse Distribution; 45,000 Points of Production and Growing STRENGTH: Ratings; A+ (Superior) Rated by A.M. Best Recognition; Ward’s Financial Top 50 P&C Insurance Companies VALUE: Growth In Annual EPS (Before Capital Gains); 18.1% 5-Year CAGR Growth In Book Value; 13.0% 10-Year CAGR CONSISTENCY: Book Value Per Share has Increased 19 of Last 20 Years Total Revenue has Increased 19 of Last 20 Years Produced a Net Profit in Each of the Last 20 years Beyond Standard |

AMERICAN MODERN INSURANCE GROUP 27 American Modern Insurance Group Non-Cyclical Specialty P&C Insurance Company American Modern Pillars of Strength Profitable Growth |

AMERICAN MODERN INSURANCE GROUP 28 AMERICAN MODERN AMERICAN MODERN INSURANCE GROUP INSURANCE GROUP Reinsurance and Exposure Reinsurance and Exposure Management Management Dan Gilene Dan Gilene Senior Vice President, Reinsurance Senior Vice President, Reinsurance |

AMERICAN MODERN INSURANCE GROUP 29 Exposure Management and Managed Reinsurance Proactive risk management is a key component of our overall business strategy Structuring the appropriate reinsurance is critical to our ability to accurately predict our results and provide us a sustainable competitive advantage Proactive risk management is embraced across the entire organization and is a collaborative effort between reinsurance, product, sales, and all other disciplines to manage catastrophe exposures |

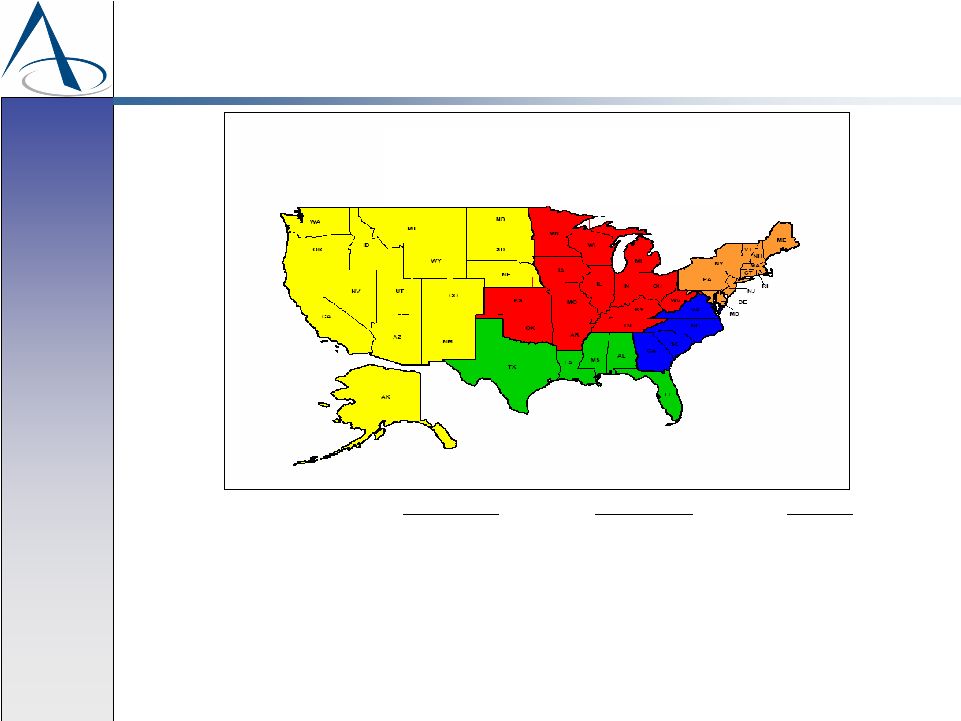

AMERICAN MODERN INSURANCE GROUP 30 NC 5.8% LA 5.7% GA 4.4% AZ 4.0% NJ 2.7% FL 2.7% NY 2.4% OK 2.2% IN 2.1% WA 2.1% KY 1.9% Other States 19.3% CA 19.5% TN 2.8% MI 2.8% MS 2.8% TX (incl. assumed business) 5.6% AR 3.2% AL 3.0% SC 5.0% Exposure Data Gulf and South Atlantic Coastal Exposure as a Percent of Total US Exposure AMIG’s business is geographically diverse and its exposures are weighted away from wind-storm risks Property Catastrophe Exposures – 12/31/06 CA w/Quake 3.0% CA w/o Quake 16.5% 54.5 48.6 37.0 36.4 35.6 0.0 10.0 20.0 30.0 40.0 50.0 60.0 '6/30/95 '6/30/00 '6/30/05 '6/30/06 '6/30/07 Time Period Note: 1. Excludes Bell & Clements alliance Total: $53,255mm 1 |

AMERICAN MODERN INSURANCE GROUP 31 Manufactured Housing Geographic Distribution Policies in Force 12/31/2000 12/31/2006 Change Southeast 26% 20% -6.0 Gulf 26% 26% ----- Midwest 27% 27% ----- East 7% 9% +2.0 West 14% 18% +4.0 Concerted effort over the past few years to grow East, Midwest and West. |

AMERICAN MODERN INSURANCE GROUP 32 Manufactured Housing – Coastal Rate Changes (First Tier) 2006 – July 2007 20.0% 09/01/06 Texas 37.3% Pending 10.0% 06/15/06 Louisiana 53.3% 10/15/07 10.0% 07/01/06 Mississippi 12.4% 07/01/07 15.0% 06/15/06 Alabama 25.0% Pending -10.0% 6/1/2007 19.6% 1/15/2007 Florida 1.9% 6/1/2007 1.1% 6/1/2006 Georgia 15.3% 05/15/07 19.4% 06/15/06 South Carolina 36.7% 05/01/07 North Carolina 3.6% 10/15/06 20.0% 04/01/06 Virginia 15.0% 09/01/06 Maryland 12.0% 11/01/06 Delaware 12.0% 07/01/07 12.0% 06/15/06 New Jersey % Change Effective Date State Aggressive plan to implement coastal rate change over last two years. |

AMERICAN MODERN INSURANCE GROUP 33 Mortgage Fire Exposure Top Ten States Percent of Countrywide MF Exposure (as of 09/30/2007) California (Only 0.10% Includes Quake) 19.3% Florida 9.5% New York 6.4% Michigan 5.0% Georgia 3.8% Texas 3.7% Illinois 3.7% Ohio 3.7% Massachusetts 2.9% Pennsylvania 2.6% TOTAL 60.6% Gulf & South Atlantic States 23.1% Remainder of United States 76.9% Mortgage Fire Business is Growing … However, Geographic Spread Remains Very Good |

AMERICAN MODERN INSURANCE GROUP 34 Mortgage Fire – Proactive Risk Management Collaborative effort between Corporate Risk Management and FID to….. • Review all new prospective loan portfolios for acceptable spread of risk and acceptable contribution to catastrophe exposures • Review monthly, in force coastal exposures by state and by account • Implement joint action plan where necessary to control catastrophe exposures Proactive Risk Management Remains a Critical Aspect of Controlling Mortgage Fire Growth |

AMERICAN MODERN INSURANCE GROUP 35 Corporate Risk Management Benchmarks/Guidelines Single event probabilistic benchmark We will manage our Regional 1 in 250 year after-tax next loss (after reinsurance) to no more than 50% of annual forecasted after-tax statutory earnings Multiple event probabilistic benchmark We will manage our Regional 1 in 100 year after-tax net loss (after reinsurance) so that 2 storms are no more than 100% of annual forecasted after-tax statutory earnings Notes: 1. Basis for after-tax net loss is RiskLink v7.0 hurricane, RMS Stochastic Event Rate, with storm surge and loss amplification |

AMERICAN MODERN INSURANCE GROUP 36 Regional Hurricane Loss Estimates Status of Single Event Probabilistic Benchmark As of June 30, 2007 Notes 1. Region Definitions: Northeast-North of Virginia, South Atlantic – Virginia to Florida, Gulf – Florida to Louisiana, Texas - Florida and Texas 2. In calculating regional PML’s, Florida is included in the South Atlantic, Gulf and Texas regions due to the probability of “double landfalls.” *Estimated at $73mm as of June 30, 2007 31.9% Texas 33.7% Gulf 34.3% South Atlantic 32.7% Northeast PERCENT OF 2007 FORECASTED AFTER - TAX STATUTORY EARNINGS* REGION |

AMERICAN MODERN INSURANCE GROUP 37 $2M $5M $250K PROPERTY PER RISK $1.5M xs $500K $3M xs $2M $250K xs $250K $500K Retention $150K RV UNDERLYING PROPERTY PER RISK $250K Retention $100K xs $150K $10M $20M $40M $150M $70M $10M $5M PROPERTY CATASTROPHE UNDERLYING CATASTROPHE Retention Retention $5M xs $5M xs $5M ($10M Annual Limit) $250M $10M xs $10M $20M xs $20M $30M xs $40M $40M xs $70M $50M xs $150M $40M xs $110M $110M Retention $10.4M $42.6M 90% of $32.1M xs $10.4M ESTIMATED 2007 FHCF LAYER + $1B TICL LAYER $200M Retention CASUALTY XS $350K xs $150K $500K xs $500K $1M xs $1M $3M xs $2M $150K $500K $1M $2M $5M 2007 Reinsurance Structure $50M xs $200M |

AMERICAN MODERN INSURANCE GROUP 38 Strategic Risk Management Solid Reinsurance Relationships Over 50 trading relationships Excellent ratings (99.5% rated A- or better) Deep long –term relationships Disciplined Exposure Management Florida not in top 10 manufactured housing states…Not an accident! Turn away multiples more business than we take on Diversified Specialty Product Offering Product expansion has broadened geographic spread Non-coastal business has grown at a rate 10 times greater than coastal business over the last 10 years Producers As Partners A culture of risk/exposure management Compensation skewed away from the coastlines |

AMERICAN MODERN INSURANCE GROUP 39 AMERICAN MODERN AMERICAN MODERN INSURANCE GROUP INSURANCE GROUP Thank You Thank You |

Important Merger Information

This communication may be deemed to be solicitation material in respect of the proposed acquisition of Midland by Munich Re. In connection with the proposed acquisition, Midland intends to file a proxy statement on Schedule 14A with the Securities and Exchange Commission, or SEC, and Midland intends to file other relevant materials with the SEC.Shareholders of Midland are urged to read all relevant documents filed with the SEC when they become available, including Midland’s proxy statement, because they will contain important information about the proposed transaction, Midland and Munich Re.A definitive proxy statement will be sent to holders of Midland stock seeking their approval of the proposed transaction. This communication is not a solicitation of a proxy from any security holder of Midland.

Investors and security holders will be able to obtain the documents (when available) free of charge at the SEC’s web site,

http://www.sec.gov. In addition, Midland shareholders may obtain free copies of the documents filed with the SEC when available by contacting Midland’s Chief Financial Officer, Todd Gray, at 513-943-7100.

Such documents are not currently available. You may also read and copy any reports, statements and other information filed by Midland or Munich Re with the SEC at the SEC public reference room at 100 F Street, N.E. Room 1580, Washington, D.C. 20549. Please call the SEC at 1-800-SEC-0330 or visit the SEC’s website for further information on its public reference room.

Participants in the Solicitation

Munich Re and its directors and executive officers, and Midland and its directors and executive officers, may be deemed to be participants in the solicitation of proxies from the holders of Midland common stock in respect of the proposed transaction. Information about the directors and executive officers of Midland is set forth in Midland’s proxy statement which was filed with the SEC on March 23, 2007. Investors may obtain additional information regarding the interest of Munich Re and its directors and executive officers, and Midland and its directors and executive officers in the proposed transaction by reading the proxy statement regarding the acquisition when it becomes available.