Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE

SECURITIES EXCHANGE ACT OF 1934

| For the fiscal year ended December 31, 2012 | Commission File No. 1-15579 |

MINE SAFETY APPLIANCES COMPANY

(Exact name of registrant as specified in its charter)

| Pennsylvania | 25-0668780 | |

(State or other jurisdiction of incorporation or organization) | (IRS Employer Identification No.) | |

1000 Cranberry Woods Drive Cranberry Township, Pennsylvania | 16066-5207 | |

| (Address of principal executive offices) | (Zip code) | |

Registrant’s telephone number, including area code: (724) 776-8600

Securities registered pursuant to Section 12(b) of the Act:

(Title of each class) | (Name of each exchange on which registered) | |

| Common Stock, no par value | New York Stock Exchange |

Indicate by check mark whether the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in the definitive proxy statement incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer x | Accelerated filer ¨ | |

Non-accelerated filer ¨ (Do not check if a smaller reporting company) | Smaller reporting company ¨ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No x

As of February 15, 2013, there were outstanding 37,010,504 shares of common stock, no par value, not including 731,922 shares held by the Mine Safety Appliances Company Stock Compensation Trust. The aggregate market value of voting stock held by non-affiliates as of June 30, 2012 was approximately $1.2 billion.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Proxy Statement for the May 7, 2013 Annual Meeting of Shareholders are incorporated by reference into Part III.

Table of Contents

Item No. | Page | |||||

Part I | ||||||

1. | 4 | |||||

1A. | 8 | |||||

1B. | 13 | |||||

2. | 13 | |||||

3. | 14 | |||||

4. | 17 | |||||

| 17 | ||||||

Part II | ||||||

5. | 18 | |||||

6. | 20 | |||||

7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | 20 | ||||

7A. | 34 | |||||

8. | 35 | |||||

9. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | 67 | ||||

9A. | 67 | |||||

9B. | 67 | |||||

Part III | ||||||

10. | 68 | |||||

11. | 68 | |||||

12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 68 | ||||

13. | Certain Relationships and Related Transactions, and Director Independence | 68 | ||||

14. | 68 | |||||

Part IV | ||||||

15. | 69 | |||||

| 72 | ||||||

2

Table of Contents

Forward-Looking Statements

This report may contain forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. These statements relate to future events or our future financial performance and involve known and unknown risks, uncertainties and other factors that may cause our actual results, levels of activity, performance or achievements to be materially different from any future results, levels of activity, performance or achievements expressed or implied by these forward-looking statements. These risks and other factors include, but are not limited to, those listed in this report under “Risk Factors,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” and elsewhere in this report. In some cases, you can identify forward-looking statements by words such as “may,” “will,” “should,” “expects,” “intends,” “plans,” “anticipates,” “believes,” “estimates,” “predicts,” “potential” or other comparable words. Actual results, performance or outcomes may differ materially from those expressed or implied by these forward-looking statements. Although we believe that the expectations reflected in the forward-looking statements are reasonable, we cannot guarantee future results, levels of activity, performance or achievements. We are under no duty to update publicly any of the forward-looking statements after the date of this report, whether as a result of new information, future events or otherwise.

3

Table of Contents

PART I

Overview—Mine Safety Appliances Company was incorporated in Pennsylvania in 1914. We are a global leader in the development, manufacture and supply of products that protect people’s health and safety. Our safety products typically integrate any combination of electronics, mechanical systems and advanced materials to protect users against hazardous or life threatening situations. Our comprehensive line of safety products is used by workers around the world in the oil and gas, fire service, mining, construction and other industries, as well as the military. Our broad product offering includes self-contained breathing apparatus, or SCBAs, gas masks, gas detection instruments, head protection, respirators, thermal imaging cameras and fall protection. We also provide a broad offering of consumer and contractor safety products through retail channels.

We dedicate significant resources to research and development, which allows us to produce innovative safety products that are often first to market and exceed industry standards. Our global product development teams include cross-geographic and cross-functional members from various functional areas throughout the company, including research and development, marketing, sales, operations and quality management. Our engineers and technical associates work closely with the safety industry’s leading standards-setting groups and trade associations, such as the National Institute for Occupational Safety and Health, or NIOSH, and the National Fire Protection Association, or NFPA, to develop industry product requirements and standards and to anticipate their impact on our product lines.

Segments—We tailor our product offerings and distribution strategy to satisfy distinct customer preferences that vary across geographic regions. We believe that we best serve these customer preferences by organizing our business into eleven geographic operating segments that are aggregated into three reportable geographic segments: North America, Europe and International. Segment information is presented in the note entitled “Segment Information” in Item 8—Financial Statements and Supplementary Data.

Because our financial statements are stated in U.S. dollars and much of our business is conducted outside the U.S., currency fluctuations may affect our results of operations and financial position and may affect the comparability of our results between financial periods.

Principal Products—We manufacture and sell a comprehensive line of safety products to protect workers around the world in the oil and gas, fire service, mining, construction and other industries, as well as the military. We also provide a broad offering of consumer and contractor safety products through retail channels. Our products protect people against a wide variety of hazardous or life-threatening situations. The following is a brief description of each of our principal product categories:

Respiratory protection.Respiratory protection products are used to protect against the harmful effects of contamination caused by dust, gases, fumes, volatile chemicals, sprays, micro-organisms, fibers and other contaminants. We offer a broad and comprehensive line of respiratory protection products.

| • | Self Contained Breathing Apparatus.SCBAs are used by first responders, petrochemical plant workers and anyone entering an environment deemed immediately dangerous to life and health. SCBAs are also used by first responders to protect against exposure to chemical, biological, radiological and nuclear, or CBRN agents. Our FireHawk®M7 SCBA meets the latest performance requirements adopted by the NFPA. The FireHawk®M7 Air Mask was the first device of its kind to be certified by the Safety Equipment Institute, or SEI, as NFPA compliant for both its breathing apparatus and Personal Alert Safety System, or PASS. The PASS device is a SCBA component that sounds a loud, piercing alarm when a firefighter becomes disabled or lies motionless for 30 seconds. |

| • | Air-purifying respirators. Air-purifying respirators range from the simple filtering types to powered full-facepiece versions for many hazardous applications, including: |

| • | full-face gas masks for industrial workers and first responders exposed to known and unknown concentrations of hazardous gases, chemicals, vapors and particulates; |

4

Table of Contents

| • | half-mask respirators for industrial workers, painters and construction workers exposed to known concentrations of gases, vapors and particulates; |

| • | powered-air purifying respirators for industrial, hazmat and remediation workers who have longer term exposures to hazards in their work environment; and |

| • | dust and pollen masks for maintenance workers, contractors and at-home consumers exposed to nuisance dusts, allergens and other particulates. |

| • | Escape respirators. Escape respirators are used by law enforcement personnel, government workers, chemical and pharmaceutical workers and anyone needing to escape from unknown concentrations of a chemical, biological or radiological release of toxic gases and vapors. Escape respirators give users respiratory protection to help them escape from threatening situations quickly and easily. |

Portable and fixed gas detection instruments.Our portable and fixed gas detection instruments are used to detect the presence or absence of various gases in the air. These instruments can be either hand-held or permanently installed. Typical applications of these instruments include the detection of the lack of oxygen in confined spaces or the presence of combustible or toxic gases.

| • | Single- and multi-gas hand-held detectors.Our single- and multi-gas detectors provide portable solutions for detecting the presence of oxygen, combustible gases and various toxic gases, including hydrogen sulfide, carbon monoxide, ammonia and chlorine, either singularly or up to six gases at once. Our hand-held portable instruments are used by chemical workers, oil and gas workers, utility workers entering confined spaces, or anywhere a user needs to continuously monitor the quality of the atmosphere they are working in and around. Our ALTAIR® 4X Multigas Detector with XCell® sensor technology provides faster response times and unsurpassed durability in a tough, easy to operate package. |

| • | Multi-point permanently installed gas detection systems.Our comprehensive line of fixed gas detection systems is used to monitor for combustible and toxic gases and oxygen deficiency in virtually any application where continuous monitoring is required. Our systems are used for gas detection in pulp and paper, refrigerant monitoring, petrochemical and general industrial applications. Our SafeSite® Multi-Threat Wireless Detection System, designed and developed for homeland security applications, detects and communicates the presence of toxic industrial chemicals and chemical warfare agents at large public events, in subways or at other facilities. |

| • | Flame detectors and open-path infrared gas detectors.Our flame and combustible gas detectors are used for plant-wide monitoring of toxic gases and for detecting the presence of flames. These systems use infrared optics to detect potentially hazardous conditions across distances as far as 120 meters, making them suitable for use in such places as offshore oil rigs, storage vessels, refineries, pipelines and ventilation ducts. First used in the oil and gas industry, our systems currently have broad applications in petrochemical facilities, the transportation industry and in pharmaceutical production. |

Thermal imaging cameras.Our hand-held infrared thermal imaging cameras, or TICs, are used in the global fire service market. TICs detect sources of heat in order to locate downed firefighters and other people trapped inside burning or smoke-filled structures. TICs can also be used to identify “hot spots.” Our Evolution® 5000 series TICs are unmatched for ease of use and durability. Our Evolution® 5800 TIC, the newest addition to our 5000 series of TICs, offers state-of-the-art imagery in a high resolution format. Our Evolution® 5600 TIC provides high resolution and an extended high sensitivity operating range in a rugged, user-friendly and affordable design.

Head, eye and face and hearing protection.Head, eye and face and hearing protection is used in work environments where hazards present dangers such as dust, flying particles, metal fragments, chemicals, extreme glare, optical radiation and items dropped from above.

| • | Industrial hard hats.Our broad line of hard hats include full-brim hats and traditional hard hats, available in custom colors and with custom logos. Hard hats are used by oil, gas and petrochemical workers, plant, steel and construction workers, and miners. |

5

Table of Contents

| • | Fire helmets.Our fire service products include leather, traditional, modern and specialty helmets designed to satisfy the preferences of firefighters across geographic regions. We believe that our CairnsHELMET is the number one helmet in the North American fire service market. Similarly, we believe that our Gallet firefighting helmet has the number one market position in Europe. |

| • | Ballistic helmets.These helmets provide ballistic head protection in combat and other high-risk environments. We do not sell ballistic helmets in North America. |

| • | Eye, face and hearing protection.Our broad line of hearing protection products, non-prescription protective eyewear and face shields is used by workers in a wide variety of industries. |

Fall protection.Our broad line of fall protection equipment includes confined space equipment, harnesses, fall arrest equipment, lanyards and lifelines. Fall protection equipment is used by construction and plant workers and anyone working at height.

Customers—Our customers generally fall into three categories: industrial and military end-users, distributors and retail consumers. In North America, we make nearly all of our non-military sales through our distributors. In our European and International segments, we make our sales through both indirect and direct sales channels. For the year ended December 31, 2012, no individual customer represented 10% of our sales.

Industrial and military end-users—Examples of the primary industrial and military end-users of our core products are listed below:

Products | Primary End-Users | |

Respiratory Protection | First Responders; General Industry Workers; Military Personnel | |

Gas Detection | Oil, Gas, Petrochemical and Chemical Workers; First Responders; Hazmat and Confined Space Workers | |

Head, Eye and Face and Hearing Protection | Construction Workers and Contractors; First Responders; General Industry Workers; Military Personnel | |

Fall Protection | Construction Workers and Contractors; Oil, Gas, Petrochemical and Chemical Workers; General Industry Workers | |

Sales and Distribution—Our sales and distribution team consists of distinct marketing, field sales and customer service organizations. We believe our sales and distribution team, totaling over 400 dedicated associates, is the largest in our industry. In most geographic areas, our field sales organizations work jointly with select distributors to call on end-users and educate them about hazards, exposure limits, safety requirements and product applications, as well as the specific performance requirements of our products. In our International segment and Eastern Europe where distributors are not as well established, our sales associates often work with and sell directly to end-users. We believe that the development of relationships with end-users is critical to increasing the overall demand for our products.

The in-depth customer training and education provided by our sales associates to our customers are critical to ensure proper use of many of our products, such as SCBAs and gas detection instruments. As a result of our sales associates working closely with end-users, they gain valuable insight into customer preferences and needs. To better serve our customers and to ensure that our sales associates are among the most knowledgeable and professional in the industry, we place significant emphasis on training our sales associates with respect to product application, industry standards and regulations, sales skills and sales force automation.

We believe our sales and distribution strategy allows us to deliver a customer value proposition that differentiates our products and services from those of our competitors, resulting in increased customer loyalty and demand.

6

Table of Contents

In areas where we use indirect selling, we promote, distribute and service our products to general industry through select authorized national, regional and local distributors. Some of our key distributors include Airgas, W.W. Grainger Inc., Fastenal and Hagemeyer. In North America, we distribute fire service products primarily through specially trained local and regional distributors who provide advanced training and service capabilities to volunteer and paid municipal fire departments. In our European and International segments, we primarily sell to and service the fire service market directly. Because of our broad and diverse product line and our desire to reach as many markets and market segments as possible, we have over 4,000 authorized distributor locations worldwide.

Our Safety Works, LLC joint venture provides a broad range of safety products and gloves to the North American do-it-yourself and independent contractor market through various channels, including distributors such as Orgill, hardware and equipment rental outlets such as United Rentals, and retail chains such as The Home Depot, TrueValue and Do-it Best.

Competition—We believe the worldwide personal protection equipment market, including the sophisticated safety products market in which we compete, generates annual sales in excess of $20 billion. The industry supplying this market is broad and highly fragmented with few participants offering a comprehensive line of safety products. Over the long-term, we believe global demand for safety products will be stable or growing because purchases of these products are non-discretionary since they protect workers in hazardous and life-threatening work environments and because their use is often mandated by government and industry regulations. Moreover, safety products industry revenues reflect the need to consistently replace many safety products that have limited life spans due to normal wear and tear or because they are one time use products by design.

The safety products market is highly competitive, with participants ranging in size from small companies focusing on a single type of personal protection equipment to a few large multinational corporations that manufacture and supply many types of sophisticated safety products. Our main competitors vary by region and product. We believe that participants in this industry compete primarily on the basis of product characteristics (such as functional performance, agency approvals, design and style), price, brand name recognition and service.

We believe we compete favorably within each of our operating segments as a result of our high quality and cost-efficient product offerings and strong brand trust and recognition.

Research and Development—To maintain our position at the forefront of safety equipment technology, we operate several sophisticated research and development facilities. We believe our dedication and commitment to innovation and research and development allow us to produce innovative safety products that are often first to market and exceed industry standards. In 2012, 2011 and 2010, on a global basis, we spent $40.9 million, $39.2 million and $32.8 million, respectively, on research and development. Our primary engineering groups are located in the United States, Germany, China and, to a lesser extent, France. Our global product development teams include cross-geographic and cross-functional members from various areas throughout the company, including research and development, marketing, sales, operations and quality management. These teams are responsible for setting product line strategy based on their understanding of the markets and the technologies, opportunities and challenges they foresee in each product area. We believe our team-based, cross-geographic and cross-functional approach to new product development is a source of competitive advantage. Our approach to the new product development process allows us to tailor our product offerings and product line strategies to satisfy distinct customer preferences and industry regulations that vary across our operating segments.

We believe another important aspect of our approach to new product development is that our engineers and technical associates work closely with the safety industry’s leading standards-setting groups and trade associations, such as the National Institute for Occupational Safety and Health, or NIOSH, and the National Fire Protection Association, or NFPA, to develop industry product requirements and standards and anticipate their impact on our product lines. For example, nearly every consensus standard-setting body around the world that impacts our product lines has one of our key managers as a voting member. Key members of our management team understand the impact that these standard-setting organizations have on our new product development

7

Table of Contents

pipeline and devote time and attention to anticipating a new standard’s impact on our sales and operating results. Because of our technological sophistication, commitment to and membership on global standard-setting bodies, resource dedication to research and development and unique approach to the new product development process, we believe we are well-positioned to anticipate and adapt to the needs of changing product standards and gain the approvals and certifications necessary to meet new government and multinational product regulations.

Patents and Intellectual Property—We own significant intellectual property, including a number of domestic and foreign patents, patent applications and trademarks related to our products, processes and business. Although our intellectual property plays an important role in maintaining our competitive position in a number of markets that we serve, no single patent, or patent application, trademark or license is, in our opinion, of such value to us that our business would be materially affected by the expiration or termination thereof, other than the “MSA” trademark. Our patents expire at various times in the future not exceeding 20 years. Our general policy is to apply for patents on an ongoing basis in the United States and other countries, as appropriate, to perfect our patent development. In addition to our patents, we have also developed or acquired a substantial body of manufacturing know-how that we believe provides a significant competitive advantage over our competitors.

Raw Materials and Suppliers—Many of the components of our products are formulated, machined, tooled or molded in-house from raw materials. For example, we rely on integrated manufacturing capabilities for breathing apparatus, gas masks, ballistic helmets, hard hats and circuit boards. The primary raw materials that we source from third parties include rubber, chemical filter media, eye and face protective lenses, air cylinders, certain metals, electronic components and ballistic resistant and non-ballistic fabrics. We purchase these materials both domestically and internationally, and we believe our supply sources are both well established and reliable. We have close vendor relationship programs with the majority of our key raw material suppliers. Although we generally do not have long-term supply contracts, we have not experienced any significant problems in obtaining adequate raw materials.

Associates—At December 31, 2012, we had approximately 5,300 associates, approximately 3,300 of whom were employed by our European and International segments. None of our U.S. associates are subject to the provisions of a collective bargaining agreement. Some of our associates outside the United States are members of unions. We have not experienced a work stoppage in over 10 years and believe our relations with our associates are good.

Available Information—Our internet address is www.MSAsafety.com. We post the following filings on the Investor Relations page on our website as soon as reasonably practicable after they have been electronically filed with or furnished to the Securities and Exchange Commission: our annual reports on Form 10-K, our quarterly reports on Form 10-Q, our current reports on Form 8-K and any amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934. All such filings on our Investor Relations web page are available to be viewed on this page free of charge. Information contained on our website is not part of this annual report on Form 10-K or our other filings with the Securities and Exchange Commission. The annual report on Form 10-K is also available in print to any shareholder who requests it. Such requests should be sent to The Chief Financial Officer, 1000 Cranberry Woods Drive, Cranberry Township, PA 16066.

Unfavorable economic and market conditions could materially and adversely affect our business, results of operations and financial condition.

We are subject to risks arising from adverse changes in global economic conditions. Although economic conditions generally improved in 2012, the global economy remains unstable and we expect economic conditions will continue to be challenging for the foreseeable future. Adverse changes in economic conditions could result in declines in revenue, profitability and cash flow due to reduced orders, payment delays, supply chain disruptions or other factors caused by the economic challenges faced by our customers and suppliers.

8

Table of Contents

A reduction in the spending patterns of government agencies could materially and adversely affect our net sales, earnings and cash flow.

The demand for our products sold to the fire service market, the homeland security market and other government agencies is, in large part, driven by available government funding. Government budgets are set annually and we cannot assure you that government funding will be sustained at the same level in the future. A significant reduction in available government funding could materially and adversely affect our net sales, earnings and cash flow.

The markets in which we compete are highly competitive, and some of our competitors have greater financial and other resources than we do. The competitive pressures faced by us could materially and adversely affect our business, results of operations and financial condition.

The safety products market is highly competitive, with participants ranging in size from small companies focusing on single types of safety products, to large multinational corporations that manufacture and supply many types of safety products. Our main competitors vary by region and product. We believe that participants in this industry compete primarily on the basis of product characteristics (such as functional performance, agency approvals, design and style), price, brand name trust and recognition and customer service. Some of our competitors have greater financial and other resources than we do and our business could be adversely affected by competitors’ new product innovations, technological advances made to competing products and pricing changes made by us in response to competition from existing or new competitors. We may not be able to compete successfully against current and future competitors and the competitive pressures faced by us could materially and adversely affect our business, results of operations and financial condition.

If we fail to introduce successful new products or extend our existing product lines, we may lose our market position and our financial performance may be materially and adversely affected.

In the safety products market, there are frequent introductions of new products and product line extensions. If we are unable to identify emerging consumer and technological trends, maintain and improve the competitiveness of our products and introduce new products, we may lose our market position, which could have a materially adverse effect on our business, financial condition and results of operations. Although we continue to invest significant resources in research and development and market research, continued product development and marketing efforts are subject to the risks inherent in the development of new products and product line extensions, including development delays, the failure of new products and product line extensions to achieve anticipated levels of market acceptance and the cost of failed product introductions.

Product liability claims and our inability to collect related insurance receivables could have a materially adverse effect on our business, operating results and financial condition.

We face an inherent business risk of exposure to product liability claims arising from the alleged failure of our products to prevent the types of personal injury or death against which they are designed to protect. Although we have not experienced any material uninsured losses due to product liability claims, it is possible that we could experience material losses in the future. In the event any of our products prove to be defective, we could be required to recall or redesign such products. In addition, we may voluntarily recall or redesign certain products that could potentially be harmful to end users. A successful claim brought against us in excess of available insurance coverage, or any claim or product recall that results in significant expense or adverse publicity against us, could have a materially adverse effect on our business, operating results and financial condition.

In the normal course of business, we make payments to settle product liability claims and for related legal fees and record receivables for the amounts covered by insurance. Our insurance receivables totaled $130.0 million at December 31, 2012. Various factors could affect the timing and amount of recovery of insurance receivables, including: the outcome of negotiations with insurers, legal proceedings with respect to product liability insurance coverage and the extent to which insurers may become insolvent in the future. Failure to recover amounts due from our insurance carriers could have a materially adverse effect on our business, operating results and financial condition.

9

Table of Contents

A failure of our information systems could materially and adversely affect our business, results of operations and financial condition.

The proper functioning and security of our information systems is critical to the operation of our business. Our information systems may be vulnerable to damage or disruption from natural or man-made disasters, computer viruses, power losses, or other system or network failures. In addition, hackers and cybercriminals could attempt to gain unauthorized access to our information systems with the intent of harming our company or obtaining sensitive information such as intellectual property, trade secrets, financial and business development information, and customer and vendor related information. If our information systems or security fail, our business, results of operations and financial condition could be materially and adversely affected.

Our ability to market and sell our products is subject to existing regulations and standards. Changes in such regulations and standards or our failure to comply with them could materially and adversely affect our results of operations.

Most of our products are required to meet performance and test standards designed to protect the health and safety of people around the world. Our inability to comply with these standards may materially and adversely affect our results of operations. Changes in regulations could reduce the demand for our products or require us to reengineer our products, thereby creating opportunities for our competitors. Regulatory approvals for our products may be delayed or denied for a variety of reasons that are outside of our control. Additionally, market anticipation of significant new standards can cause customers to accelerate or delay buying decisions.

We have significant international operations and are subject to the risks of doing business in foreign countries.

We have business operations in over 40 foreign countries. In 2012, approximately half of our net sales were made by operations located outside the United States. Our international operations are subject to various political, economic and other risks and uncertainties, which could adversely affect our business. These risks include the following:

| • | currency exchange rate fluctuations; |

| • | unexpected changes in regulatory requirements; |

| • | changes in trade policy or tariff regulations; |

| • | changes in tax laws and regulations; |

| • | intellectual property protection difficulties; |

| • | difficulty in collecting accounts receivable; |

| • | complications in complying with a variety of foreign laws and regulations, some of which may conflict with U.S. laws; |

| • | trade protection measures and price controls; |

| • | trade sanctions and embargos; |

| • | nationalization and expropriation; |

| • | increased international instability or potential instability of foreign governments; |

| • | the need to take extra security precautions for our international operations; and |

| • | costs and difficulties in managing culturally and geographically diverse international operations. |

Any one or more of these risks could have a negative impact on the success of our international operations and, thereby, materially and adversely affect our business as a whole.

10

Table of Contents

Our future results are subject to availability of, and fluctuations in the costs of, purchased components and materials due to market demand, currency exchange risks, material shortages and other factors.

We depend on various components and materials to manufacture our products. Although we have not experienced any difficulty in obtaining components and materials, it is possible that any of our supplier relationships could be terminated. Any sustained interruption in our receipt of adequate supplies could have a materially adverse effect on our business, results of operations and financial condition. We cannot assure you that we will be able to successfully manage price fluctuations due to market demand, currency risks or material shortages, or that future price fluctuations will not have a materially adverse effect on our business, results of operations and financial condition.

If we lose any of our key personnel or are unable to attract, train and retain qualified personnel, our ability to manage our business and continue our growth would be negatively impacted.

Our success depends in large part on the continued contributions of our key management, engineering and sales and marketing personnel, many of whom are highly skilled and would be difficult to replace. Our success also depends on the abilities of new personnel to function effectively, both individually and as a group. If we are unable to attract, effectively integrate and retain management, engineering or sales and marketing personnel, then the execution of our growth strategy and our ability to react to changing market requirements may be impeded, and our business could suffer as a result. Competition for personnel is intense, and we cannot assure you that we will be successful in attracting and retaining qualified personnel. In addition, we do not currently maintain key person life insurance.

We are subject to various environmental laws and any violation of these laws could adversely affect our results of operations.

We are subject to federal, state and local laws, regulations and ordinances relating to the protection of the environment, including those governing discharges to air and water, handling and disposal practices for solid and hazardous wastes and the maintenance of a safe workplace. These laws impose penalties for noncompliance and liability for response costs and certain damages resulting from past and current spills, disposals, or other releases of hazardous materials. We could incur substantial costs as a result of noncompliance with or liability for cleanup pursuant to these environmental laws. Environmental laws have changed rapidly in recent years, and we may be subject to more stringent environmental laws in the future. If more stringent environmental laws are enacted, these future laws could have a materially adverse effect on our results of operations.

Our inability to successfully identify, consummate and integrate future acquisitions or to realize anticipated cost savings and other benefits could adversely affect our business.

One of our operating strategies is to selectively pursue acquisitions. Any future acquisitions will depend on our ability to identify suitable acquisition candidates and successfully consummate such acquisitions. Acquisitions involve a number of risks including:

| • | failure of the acquired businesses to achieve the results we expect; |

| • | diversion of our management’s attention from operational matters; |

| • | our inability to retain key personnel of the acquired businesses; |

| • | risks associated with unanticipated events or liabilities; |

| • | potential disruption of our existing business; and |

| • | customer dissatisfaction or performance problems at the acquired businesses. |

If we are unable to integrate or successfully manage businesses that we have recently acquired or may acquire in the future, we may not realize anticipated cost savings, improved manufacturing efficiencies and increased revenue, which may result in materially adverse short- and long-term effects on our operating results, financial condition and liquidity. Even if we are able to integrate the operations of our acquired businesses into

11

Table of Contents

our operations, we may not realize the full benefits of the cost savings, revenue enhancements or other benefits that we may have expected at the time of acquisition. In addition, even if we achieve the expected benefits, we may not be able to achieve them within the anticipated time frame, and such benefits may be offset by costs incurred in integrating the acquired companies and increases in other expenses.

Because we derive a significant portion of our sales from the operations of our foreign subsidiaries, future currency exchange rate fluctuations may adversely affect our results of operations and financial condition, and may affect the comparability of our results between financial periods.

For the year ended December 31, 2012, the operations in our European and International segments accounted for approximately half of our net sales. The results of our foreign operations are reported in the local currency and then translated into U.S. dollars at the applicable exchange rates for inclusion in our consolidated financial statements. The exchange rates between some of these currencies and the U.S. dollar have fluctuated significantly in recent years, and may continue to do so in the future. In addition, because our financial statements are stated in U.S. dollars, such fluctuations may affect our results of operations and financial position, and may affect the comparability of our results between financial periods. We cannot assure you that we will be able to effectively manage our exchange rate risks or that any volatility in currency exchange rates will not have a materially adverse effect on our results of operations and financial condition.

Our continued success depends on our ability to protect our intellectual property. If we are unable to protect our intellectual property, our business could be materially and adversely affected.

Our success depends, in part, on our ability to obtain and enforce patents, maintain trade secret protection and operate without infringing on the proprietary rights of third parties.We have been issued patents and have registered trademarks with respect to many of our products, but our competitors could independently develop similar or superior products or technologies, duplicate any of our designs, trademarks, processes or other intellectual property or design around any processes or designs on which we have or may obtain patents or trademark protection. In addition, it is possible that third parties may have, or will acquire, licenses for patents or trademarks that we may use or desire to use, so that we may need to acquire licenses to, or to contest the validity of, such patents or trademarks of third parties. Such licenses may not be made available to us on acceptable terms, if at all, and we may not prevail in contesting the validity of third party rights.

We also protect trade secrets, know-how and other confidential information against unauthorized use by others or disclosure by persons who have access to them, such as our employees, through contractual arrangements.These agreements may not provide meaningful protection for our trade secrets, know-how or other proprietary information in the event of any unauthorized use, misappropriation or disclosure of such trade secrets, know-how or other proprietary information.If we are unable to maintain the proprietary nature of our technologies, our results of operations and financial condition could be materially and adversely affected.

If we fail to meet our debt service requirements or the restrictive covenants in our debt agreements or if interest rates increase, our results of operations and financial condition could be materially and adversely affected.

We have a substantial amount of debt upon which we are required to make scheduled interest and principal payments and we may incur additional debt in the future. A significant portion of our debt bears interest at variable rates that may increase in the future. Our debt agreements require us to comply with certain restrictive covenants. If we are unable to generate sufficient cash to service our debt or if interest rates increase, our results of operations and financial condition could be materially and adversely affected. Additionally, a failure to comply with the restrictive covenants contained in our debt agreements could result in a default, which if not waived by our lenders, could substantially increase borrowing costs and require accelerated repayment of our debt. We were in compliance with the restrictive covenants in our debt agreements as of December 31, 2012.

12

Table of Contents

Item 1B. Unresolved Staff Comments

None.

Our principal executive offices are located at 1000 Cranberry Woods Drive, Cranberry Township, PA 16066 in a 212,000 square-foot building owned by us. We own or lease our primary facilities in the United States and in a number of other countries. We believe that all of our facilities, including the manufacturing facilities, are in good repair and in suitable condition for the purposes for which they are used.

The following table sets forth a list of our primary facilities:

Location | Function | Square Feet | Owned or Leased | |||||||

North America | ||||||||||

Murrysville, PA | Manufacturing | 295,000 | Owned | |||||||

Cranberry Twp., PA | Office, Research and Development and Manufacturing | 212,000 | Owned | |||||||

New Galilee, PA | Distribution | 120,000 | Leased | |||||||

Jacksonville, NC | Manufacturing | 107,000 | Owned | |||||||

Queretaro, Mexico | Office, Manufacturing and Distribution | 77,000 | Leased | |||||||

Cranberry Twp., PA | Research and Development | 68,000 | Owned | |||||||

Lake Forest, CA | Office, Research and Development and Manufacturing | 62,000 | Leased | |||||||

Corona, CA | Manufacturing | 19,000 | Leased | |||||||

Torreon, Mexico | Office | 15,000 | Leased | |||||||

Lake Forest, CA | Office | 6,000 | Owned | |||||||

Toronto, Canada | Office and Distribution | 5,000 | Leased | |||||||

Europe | ||||||||||

Berlin, Germany | Office, Research and Development, Manufacturing and Distribution | 340,000 | Leased | |||||||

Chatillon sur Chalaronne, France | Office, Research and Development, Manufacturing and Distribution | 94,000 | Owned | |||||||

Glasgow, Scotland | Office | 25,000 | Leased | |||||||

Milan, Italy | Office and Distribution | 25,000 | Owned | |||||||

Mohammedia, Morocco | Manufacturing | 24,000 | Owned | |||||||

Galway, Ireland | Office and Manufacturing | 20,000 | Owned | |||||||

Varnamo, Sweden | Office, Manufacturing and Distribution | 18,000 | Leased | |||||||

Ballerup, Denmark | Office and Manufacturing | 10,000 | Leased | |||||||

International | ||||||||||

Suzhou, China | Office, Research and Development, Manufacturing and Distribution | 193,000 | Owned | |||||||

Johannesburg, South Africa | Office, Manufacturing and Distribution | 74,000 | Leased | |||||||

Sydney, Australia | Office, Manufacturing and Distribution | 84,000 | Owned | |||||||

Sao Paulo, Brazil | Office, Manufacturing and Distribution | 74,000 | Owned | |||||||

Lima, Peru | Office and Distribution | 34,000 | Owned | |||||||

Santiago, Chile | Office and Distribution | 32,000 | Leased | |||||||

Rajarhat, India | Office and Distribution | 10,000 | Leased | |||||||

Buenos Aires, Argentina | Office and Distribution | 9,000 | Owned | |||||||

13

Table of Contents

We categorize the product liability losses that we experience into two main categories, single incident and cumulative trauma. Single incident product liability claims are discrete incidents that are typically known to us when they occur and involve observable injuries and, therefore, more quantifiable damages. Therefore, we maintain a reserve for single incident product liability claims based on expected settlement costs for pending claims and an estimate of costs for unreported claims derived from experience, sales volumes and other relevant information. Our reserve for single incident product liability claims at December 31, 2012 and 2011 was $4.4 million and $4.7 million, respectively. Single incident product liability expense during the years ended December 31, 2012, 2011 and 2010 was $0.7 million, $1.5 million and $0.2 million, respectively. We evaluate our single incident product liability exposures on an ongoing basis and make adjustments to the reserve as new information becomes available.

Cumulative trauma product liability claims involve exposures to harmful substances (e.g., silica, asbestos and coal dust) that occurred many years ago and may have developed over long periods of time into diseases such as silicosis, asbestosis or coal worker’s pneumoconiosis. We are presently named as a defendant in 2,609 lawsuits in which plaintiffs allege to have contracted certain cumulative trauma diseases related to exposure to silica, asbestos, and/or coal dust. These lawsuits mainly involve respiratory protection products allegedly manufactured and sold by us. We are unable to estimate total damages sought in these lawsuits as they generally do not specify the injuries alleged or the amount of damages sought, and potentially involve multiple defendants.

Cumulative trauma product liability litigation is difficult to predict. In our experience, until late in a lawsuit, we cannot reasonably determine whether it is probable that any given cumulative trauma lawsuit will ultimately result in a liability. This uncertainty is caused by many factors, including the following: cumulative trauma complaints generally do not provide information sufficient to determine if a loss is probable; cumulative trauma litigation is inherently unpredictable and information is often insufficient to determine if a lawsuit will develop into an actively litigated case; and even when a case is actively litigated, it is often difficult to determine if the lawsuit will be dismissed or otherwise resolved until late in the lawsuit. Moreover, even once it is probable that such a lawsuit will result in a loss, it is difficult to reasonably estimate the amount of actual loss that will be incurred. These amounts are highly variable and turn on a case-by-case analysis of the relevant facts, which are often not learned until late in the lawsuit.

Because of these factors, we cannot reliably determine our potential liability for such claims until late in the lawsuit. We, therefore, do not record cumulative trauma product liability losses when a lawsuit is filed, but rather, when we learn sufficient information to determine that it is probable that we will incur a loss and the amount of loss can be reasonably estimated. We record expenses for defense costs associated with open cumulative trauma product liability lawsuits as incurred.

We cannot estimate any amount or range of possible losses related to resolving pending and future cumulative trauma product liability claims that we may face because of the factors described above. As new information about cumulative trauma product liability cases and future developments becomes available, we reassess our potential exposures.

A summary of cumulative trauma product liability claims activity follows:

| 2012 | 2011 | 2010 | ||||||||||

Open claims, January 1 | 2,321 | 1,900 | 2,480 | |||||||||

New claims | 750 | 479 | 260 | |||||||||

Settled and dismissed claims | (462 | ) | (58 | ) | (840 | ) | ||||||

|

|

|

|

|

| |||||||

Open claims, December 31 | 2,609 | 2,321 | 1,900 | |||||||||

|

|

|

|

|

| |||||||

14

Table of Contents

With some common contract exclusions, we maintain insurance for cumulative trauma product liability claims. We have purchased insurance policies from over 20 different insurance carriers that provide coverage for cumulative trauma product liability losses and related defense costs. In the normal course of business, we make payments to settle product liability claims and for related defense costs. We record receivables for the amounts that are covered by insurance. The available limits of these policies are many times our recorded insurance receivable balance.

Various factors could affect the timing and amount of recovery of our insurance receivables, including the outcome of negotiations with insurers, legal proceedings with respect to product liability insurance coverage and the extent to which insurers may become insolvent in the future.

Our insurance receivables at December 31, 2012 and 2011 totaled $130.0 million and $112.1 million, respectively, all of which is reported in other non-current assets.

A summary of insurance receivable balances and activity related to cumulative trauma product liability losses follows:

(In millions) | 2012 | 2011 | 2010 | |||||||||

Balance January 1 | $ | 112.1 | $ | 89.0 | $ | 91.7 | ||||||

Additions | 29.7 | 35.6 | 30.9 | |||||||||

Collections and settlements | (11.8 | ) | (12.5 | ) | (33.6 | ) | ||||||

|

|

|

|

|

| |||||||

Balance December 31 | 130.0 | 112.1 | 89.0 | |||||||||

|

|

|

|

|

| |||||||

Additions to insurance receivables in the above table represent insured cumulative trauma product liability losses and related defense costs. Uninsured cumulative trauma product liability losses during the years ended December 31, 2012, 2011, and 2010 were $2.1 million, $1.1 million and $0.2 million, respectively.

Our aggregate cumulative trauma product liability losses and administrative and defense costs for the three years ended December 31, 2012, totaled approximately $99.7 million, substantially all of which was insured.

We believe that the increase in the insurance receivable balance that we have experienced since 2005 is primarily due to disagreements among our insurance carriers, and consequently with us, as to when their individual obligations to pay us are triggered and the amount of each insurer’s obligation, as compared to other insurers. We believe that our insurers do not contest that they have issued policies to us or that these policies cover cumulative trauma product liability claims. We believe that our ability to successfully resolve our insurance litigation with various insurance carriers in recent years demonstrates that we have strong legal positions concerning our rights to coverage.

We regularly evaluate the collectability of the insurance receivables and record the amounts that we conclude are probable of collection. Our conclusions are based on our analysis of the terms of the underlying insurance policies, our experience in successfully recovering cumulative trauma product liability claims from our insurers under other policies, the financial ability of our insurance carriers to pay the claims, our understanding and interpretation of the relevant facts and applicable law and the advice of legal counsel, who believe that our insurers are required to provide coverage based on the terms of the policies.

Although the outcome of cumulative trauma product liability matters cannot be predicted with certainty and unfavorable resolutions could materially affect our results of operations on a quarter-to-quarter basis, based on information currently available and the amounts of insurance coverage available to us, we believe that the disposition of cumulative trauma product liability lawsuits that are pending against us will not have a materially adverse effect on our future results of operations, financial condition, or liquidity.

We are currently involved in insurance coverage litigations with various of our insurance carriers.

15

Table of Contents

In 2009, we sued The North River Insurance Company (North River) in the United States District Court for the Western District of Pennsylvania, alleging that North River breached one of its insurance policies by failing to pay amounts owed to us and that it engaged in bad-faith claims handling. We believe that North River’s refusal to indemnify us under the policy for product liability losses and legal fees paid by us is wholly contrary to Pennsylvania law and we are vigorously pursuing the legal actions necessary to collect all due amounts. Discovery is concluding and motions for summary judgment on certain issues will be submitted to the court in the first quarter of 2013. A trial date has not yet been scheduled.

In 2010, North River sued us in the Court of Common Pleas of Allegheny County, Pennsylvania seeking a declaratory judgment concerning their responsibilities under three additional policies shared with Allstate Insurance Company (as successor in interest to policies issued by the Northbrook Excess and Surplus Insurance Company). We asserted claims against North River and Allstate for breaches of contract for failures to pay amounts owed to us. We also alleged that North River engaged in bad-faith claims handling. We believe that North River’s and Allstate’s refusals to indemnify us under these policies for product liability losses and legal fees paid by us is wholly contrary to Pennsylvania law and we are vigorously pursuing the legal actions necessary to collect all due amounts. Discovery is concluding and motions for summary judgment on certain issues will be submitted to the court in the first quarter of 2013. A trial date has not yet been scheduled.

In July 2010, we filed a lawsuit in the Superior Court of the State of Delaware seeking declaratory and other relief from the majority of our excess insurance carriers concerning the future rights and obligations of MSA and our excess insurance carriers under various insurance policies. The reason for this insurance coverage action is to secure a comprehensive resolution of our rights under the insurance policies issued by our insurers. The case is currently in discovery. We have resolved our claims against certain of our insurance carriers on some of their policies through negotiated settlements. When settlement is reached, we dismiss the settling carrier from this action in Delaware.

16

Table of Contents

Item 4. Mine Safety Disclosures

Not applicable.

Executive Officers of the Registrant

The following sets forth the names and ages of our executive officers as of February 20, 2013, indicating all positions held during the past five years:

Name | Age | Title | ||||

William M. Lambert(a) | 54 | President and Chief Executive Officer since May 2008. | ||||

Joseph A. Bigler | 63 | Vice President and President, MSA North America since May 2007. | ||||

Steven C. Blanco(b) | 46 | Vice President, Global Operational Excellence since April 2012. | ||||

Kerry M. Bove(c) | 54 | President, MSA International, Asia-Pacific Zone and Africa/Latin America Zone since November 2011. | ||||

Ronald N. Herring, Jr.(d) | 52 | President, MSA International, Western Europe Zone and Middle Eurasia Zone since November 2011. | ||||

Douglas K. McClaine | 55 | Vice President, Secretary and General Counsel. | ||||

Stacy McMahan(e) | 49 | Senior Vice President of Finance since December 2012. | ||||

Thomas Muschter(f) | 52 | Vice President, Global Product Leadership since November 2011. | ||||

Paul R. Uhler | 54 | Vice President, Global Human Resources since May 2007. | ||||

Nishan Vartanian(g) | 52 | Vice President, Fixed Gas and Flame Detection since December 2012. | ||||

Markus H. Weber(h) | 48 | Vice President and Chief Information Officer since April 2010. | ||||

Dennis L. Zeitler | 64 | Senior Vice President, Chief Financial Officer and Treasurer since June 2007. | ||||

| (a) | Prior to his present position, Mr. Lambert was President and Chief Operating Officer. |

| (b) | Prior to joining MSA, Mr. Blanco served as Vice President of Manufacturing for the Electrical Sector of Eaton Corporation, a diversified power management company. |

| (c) | Prior to his present position, Mr. Bove was Vice President, Global Operational Excellence. |

| (d) | Prior to his present position, Mr. Herring was Vice President, Global Product Leadership. |

| (e) | Prior to joining MSA, Ms. McMahan served as Customer Channels Group Vice President, Finance, for Thermo Fisher Scientific, Inc., a global provider of laboratory equipment and supplies, and as Vice President, Finance, for Johnson & Johnson, a global manufacturer of pharmaceutical, biologic, consumer health and medical device and diagnostic products. |

| (f) | Prior to his present position, Mr. Muschter held the positions of Director, Research & Development, International; and Director, Research & Development, Europe. |

| (g) | Prior to his present position, Mr. Vartanian was Chief Operating Officer for General Monitors and Director of North American Field Sales. |

| (h) | Prior to joining MSA, Mr. Weber served as Chief Information Officer of Berlin-Chemie AG, an international research-based pharmaceutical company. |

17

Table of Contents

PART II

| Item 5. | Market for the Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities |

Our common stock is traded on the New York Stock Exchange under the symbol “MSA”. Stock price ranges and dividends declared were as follows:

| Price Range of Our Common Stock | Dividends | |||||||||||

| High | Low | |||||||||||

Year ended December 31, 2011 | ||||||||||||

First Quarter | $ | 36.98 | $ | 29.69 | $ | 0.25 | ||||||

Second Quarter | 40.91 | 32.85 | 0.26 | |||||||||

Third Quarter | 39.15 | 25.51 | 0.26 | |||||||||

Fourth Quarter | 35.74 | 24.50 | 0.26 | |||||||||

Year ended December 31, 2012 | ||||||||||||

First Quarter | $ | 42.47 | $ | 32.65 | $ | 0.26 | ||||||

Second Quarter | 44.34 | 37.38 | 0.28 | |||||||||

Third Quarter | 40.81 | 32.93 | 0.28 | |||||||||

Fourth Quarter | 42.87 | 35.37 | 0.56 | |||||||||

On February 5, 2013, there were 324 registered holders of our shares of common stock.

Issuer Purchases of Equity Securities

Period | Total Number of Shares Purchased | Average Price Paid Per Share | Total Number of Shares Purchased as Part of Publicly Announced Plans or Programs | Maximum Number of Shares that May Yet Be Purchased Under the Plans or Programs | ||||||||||||

October 1—October 31, 2012 | — | $ | — | — | 1,261,664 | |||||||||||

November 1—November 30, 2012 | 7,183 | 39.17 | — | 1,259,054 | ||||||||||||

December 1—December 31, 2012 | 7,170 | 38.90 | — | 1,140,253 | ||||||||||||

In November 2005, the Board of Directors authorized the purchase of up to $100 million of common stock from time-to-time in private transactions and on the open market. The share purchase program has no expiration date. The maximum shares that may yet be purchased is calculated based on the dollars remaining under the program and the respective month-end closing share price.

We do not have any other share purchase programs.

Share purchases are related to stock compensation transactions.

18

Table of Contents

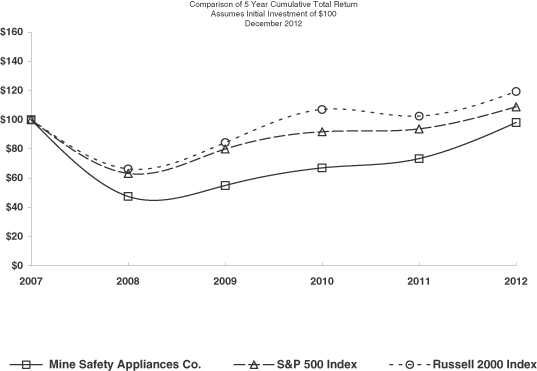

Comparison of Five-Year Cumulative Total Return

Set forth below are a line graph and table comparing the cumulative total returns (assuming reinvestment of dividends) for the five years ended December 31, 2012 of $100 invested on December 31, 2007 in each of Mine Safety Appliances Company common stock, the Standard & Poor’s 500 Composite Index and the Russell 2000 Index. Because our competitors are principally privately held concerns or subsidiaries or divisions of corporations engaged in multiple lines of business, we do not believe it feasible to construct a peer group comparison on an industry or line-of-business basis. The Russell 2000 Index, while including corporations both larger and smaller than MSA in terms of market capitalization, is composed of corporations with an average market capitalization similar to us.

COMPARISON OF 5 YEAR CUMULATIVE TOTAL RETURN*

Among Mine Safety Appliance Company, the S&P 500 Index,

and the Russell 2000 Index

| * | $100 invested on 12/31/07 in stock or index, including reinvestment of dividends. Fiscal year ending December 31. |

| Value at December 31, | ||||||||||||||||||||||||

| 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | |||||||||||||||||||

Mine Safety Appliances Co | $ | 100.00 | $ | 47.39 | $ | 54.83 | $ | 66.83 | $ | 73.23 | $ | 97.85 | ||||||||||||

S&P 500 Index | 100.00 | 63.00 | 79.68 | 91.68 | 93.61 | 108.59 | ||||||||||||||||||

Russell 2000 Index | 100.00 | 66.21 | 84.20 | 106.82 | 102.36 | 119.09 | ||||||||||||||||||

Prepared by Zacks Investment Research, Inc. Used with permission. All rights reserved. Copyright 1980-2013.

Index Data: Copyright Standard and Poor’s, Inc. Used with permission. All rights reserved.

Index Data: Copyright Russell Investments, Inc. Used with permission. All rights reserved.

19

Table of Contents

Item 6. Selected Financial Data

(In thousands, except as noted) | 2012 | 2011 | 2010(a) | 2009 | 2008 | |||||||||||||||

Statement of Income Data: | ||||||||||||||||||||

Net sales(b) | $ | 1,168,904 | $ | 1,173,227 | $ | 976,631 | $ | 909,991 | $ | 1,134,282 | ||||||||||

Net income attributable to Mine Safety Appliances Company(c) | 90,637 | 69,852 | 38,104 | 43,295 | 70,422 | |||||||||||||||

Earnings per Share Data: | ||||||||||||||||||||

Basic per common share (in dollars)(d) | $ | 2.45 | $ | 1.91 | $ | 1.06 | $ | 1.21 | $ | 1.98 | ||||||||||

Diluted per common share (in dollars)(d) | 2.42 | 1.87 | 1.05 | 1.21 | 1.96 | |||||||||||||||

Dividends paid per common share (in dollars) | 1.38 | 1.03 | .99 | .96 | .94 | |||||||||||||||

Weighted average common shares outstanding—basic | 36,564 | 36,221 | 35,880 | 35,668 | 35,593 | |||||||||||||||

Balance Sheet Data: | ||||||||||||||||||||

Total assets | $ | 1,111,746 | $ | 1,115,052 | $ | 1,197,188 | $ | 875,228 | $ | 875,810 | ||||||||||

Long-term debt(e) | 272,333 | 334,046 | 367,094 | 82,114 | 94,082 | |||||||||||||||

Mine Safety Appliances Company shareholders’ equity | 462,955 | 433,666 | 451,368 | 436,616 | 393,766 | |||||||||||||||

| (a) | Includes General Monitors from the date of acquisition on October 13, 2010. |

| (b) | For discussion of changes between 2012 and 2011 and between 2011 and 2010 see Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations. The increase in sales from 2009 to 2010 was primarily due to higher demand in oil and gas, mining and other core industrial markets. The decrease in sales from 2008 to 2009 was primarily due to the effects of the economic recession, lower military sales and unfavorable currency translation effects. |

| (c) | For discussion of changes between 2012 and 2011 and between 2011 and 2010 see Item 7. Management’s Discussion and Analysis of Financial Conditions and Results of Operations. The decrease in net income from 2009 to 2010 was primarily due to higher selling, general and administrative expenses required to support growth as we recovered from the recession. The decrease in net income for 2008 to 2009 was primarily related to lower sales. |

| (d) | See Note 6 to the Financial Statements for the basis of calculating earnings per share. |

| (e) | The increase in long-term debt in 2010 related to the acquisition of General Monitors in October 2010. |

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations

The following discussion and analysis should be read in conjunction with the historical financial statements and other financial information included elsewhere in this annual report on Form 10-K. This discussion may contain forward-looking statements that involve risks and uncertainties. The forward-looking statements are not historical facts, but rather are based on current expectations, estimates, assumptions and projections about our industry, business and future financial results. Our actual results could differ materially from the results contemplated by these forward-looking statements due to a number of factors, including those discussed in the sections of this annual report entitled “Forward-Looking Statements” and “Risk Factors.”

20

Table of Contents

BUSINESS OVERVIEW

We are a global leader in the development, manufacture and supply of products that protect people’s health and safety. Our safety products typically integrate any combination of electronics, mechanical systems and advanced materials to protect users against hazardous or life threatening situations. Our comprehensive lines of safety products are used by workers around the world in the oil and gas, fire service, mining, construction and other industries, as well as the military. We are committed to providing our customers with service unmatched in the safety industry and, in the process, enhancing our ability to provide a growing line of safety solutions for customers in key global markets.

We tailor our product offerings and distribution strategy to satisfy distinct customer preferences that vary across geographic regions. We believe that we best serve these customer preferences by organizing our business into three reportable geographic segments: North America, Europe and International. Each segment includes a number of operating segments. In 2012, 47%, 25% and 28% of our net sales were made by our North American, European and International segments, respectively.

North America. Our largest manufacturing and research and development facilities are located in the United States. We serve our North American markets with sales and distribution functions in the U.S., Canada and Mexico.

Europe. Our European segment includes companies in most Western European countries and a number of Eastern European and Middle Eastern locations. Our largest European companies, based in Germany and France, develop, manufacture and sell a wide variety of products. Operations in other European segment countries focus primarily on sales and distribution in their respective home country markets. While some of these companies may perform limited production, most of their sales are of products that are manufactured in our plants in Germany, France, the U.S. and China, or are purchased from third party vendors.

International. Our International segment includes companies in South America, Africa and the Asia Pacific region, some of which are in developing regions of the world. Principal International segment manufacturing operations are located in Australia, Brazil, China and South Africa. These companies manufacture products that are sold primarily in each company’s home country and regional markets. The other companies in the International segment focus primarily on sales and distribution in their respective home country markets. While some of these companies may perform limited production, most of their sales are of products that are manufactured in our plants in China, Germany, France and the U.S., or are purchased from third party vendors.

RESULTS OF OPERATIONS

Year Ended December 31, 2012 Compared to Year Ended December 31, 2011

Net sales. Net sales for the year ended December 31, 2012 were $1,168.9 million, a decrease of $4.3 million, from $1,173.2 million for the year ended December 31, 2011. Excluding the effects of weakening currencies and the divestitures of our ballistic vest and North American ballistic helmet businesses, sales increased $72.6 million, or 7%. Sales of ballistic vests and helmets were $36.0 million lower in 2012, reflecting the divestiture of those businesses. The unfavorable translation effects of weaker foreign currencies decreased sales, when stated in U.S. dollars, by $40.9 million.

(Dollars in millions) | 2012 | 2011 | Dollar Increase (Decrease) | Percent Increase (Decrease) | ||||||||||||

North America | $ | 551.9 | $ | 561.1 | $ | (9.2 | ) | (2 | )% | |||||||

Europe | 289.5 | 286.8 | 2.7 | 1 | ||||||||||||

International | 327.4 | 325.3 | 2.1 | 1 | ||||||||||||

Net sales by the North American segment were $551.9 million for the year ended December 31, 2012, a decrease of $9.2 million, or 2%, compared to $561.1 million for the year ended December 31, 2011. During the

21

Table of Contents

year ended December 31, 2012, we continued to see growth in the fire service and industrial markets. Shipments of instruments, head, eye and face protection and self-contained breathing apparatus (SCBA) were up $25.1 million, $4.7 million and $2.2 million, respectively. These increases were offset by a $4.7 million decrease in shipments of communication devices and a $36.0 million decrease in shipments of ballistic helmets and vests to military markets. We divested our ballistic vest and North American ballistic helmet businesses during the fourth quarter of 2011 and the second quarter of 2012, respectively.

Net sales for the European segment were $289.5 million for the year ended December 31, 2012, an increase of $2.7 million, or 1%, from $286.8 million for the year ended December 31, 2011. Local currency sales increased $22.4 million, reflecting higher shipments of instruments, SCBAs, ballistic helmets, and respirators, up $10.8 million, $4.8 million, $4.2 million, and $3.3 million, respectively. The increase was partially offset by a $2.1 million decrease in shipments of gas masks to military markets. Currency translation effects decreased European segment sales, when stated in U.S. dollars, by $19.7 million, primarily related to a weaker euro.

Net sales of our International segment were $327.4 million for the year ended December 31, 2012, an increase of $2.1 million, or 1%, compared to $325.3 million for the year ended December 31, 2011. Local currency sales in the International segment increased $21.8 million during the year ended December 31, 2012. Growth in fire service markets in China and Latin America led to increases in sales of SCBAs and fire helmets of $9.8 million and $3.8 million, respectively. In addition, sales of head, eye and face protection to industrial markets improved by $9.7 million. Currency translation effects decreased International segment sales, when stated in U.S. dollars, by $19.7 million, primarily related to a weaker South African rand and Brazilian real.

Other income.Other income for the year ended December 31, 2012 was $11.0 million, an increase of $5.6 million, from $5.4 million for the year ended December 31, 2011. During the year ended December 31, 2012, we recognized gains on the sale of assets totaling $8.4 million compared to gains of $3.3 million in 2011. These gains in both years were primarily related to property sales in our Cranberry Woods office park. In December 2012, we sold the last available parcel in Cranberry Woods. Other income for the year ended December 31, 2012 also includes a $4.8 million gain on an escrow settlement related to our October 2010 acquisition of the General Monitors group of companies. These improvements were partially offset by impairment losses on intangible assets and tooling related to our firefighter location project of $4.3 million and $0.5 million, respectively.

Cost of products sold.Cost of products sold was $666.2 million for the year ended December 31, 2012, a decrease of $36.8 million, or 5%, from $703.0 million for the year ended December 31, 2011. Cost of products sold as a percentage of sales was 57.0% in the year ended December 31, 2012 compared to 59.9% in 2011. The decrease in cost of products sold in relation to sales was primarily due to lower manufacturing costs, a more favorable product mix and improved pricing.

Gross profit. Gross profit for the year ended December 31, 2012 was $502.7 million, an increase of $32.5 million, or 7%, from $470.2 million for the year ended December 31, 2011. The ratio of gross profit to sales was 43.0% for 2012 compared to 40.1% in 2011. The higher gross profit ratio in 2012 was primarily related to lower manufacturing costs, a more favorable product mix and improved pricing.

Selling, general and administrative expenses. Selling, general and administrative expenses for the year ended December 31, 2012 were $321.2 million, an increase of $14.8 million, or 5%, from $306.4 million for the year ended December 31, 2011. Selling, general and administrative expenses were 27.5% of sales in 2012 compared to 26.1% of sales in 2011. Local currency selling, general and administrative expenses increased $24.8 million across all segments, reflecting higher selling costs, an increase in due diligence and consulting expense related to special projects and an increase in product liability related legal and administrative expenses. Currency translation effects decreased selling, general and administrative expenses for the year ended December 31, 2012, when stated in U.S. dollars, by $10.0 million, primarily related to a weaker euro, Brazilian real and South African rand.

22

Table of Contents

Research and development expenses. Research and development expenses were $40.9 million for the year ended December 31, 2012, an increase of $1.7 million, or 4%, from $39.2 million for the year ended December 31, 2011. The increase reflects our ongoing focus on developing innovative new products.

Restructuring and other charges. For the year ended December 31, 2012, we recorded charges of $2.8 million ($1.9 million after tax). Charges for the year ended December 31, 2012 were related to severance costs associated with staff reductions in our North American, European and International segments of $1.5 million, $1.1 million and $0.2 million, respectively.

For the year ended December 31, 2011, we recorded charges of $8.6 million ($5.7 million after tax). European segment charges of $5.8 million for the year ended December 31, 2011, related primarily to staff reductions and the transfer of certain production activities to China. North American segment charges for the year ended December 31, 2011 of $1.7 million included costs associated with the relocation of certain administrative and production activities. International segment charges for the year ended December 31, 2011 of $1.1 million were related primarily to severance costs associated with the relocation of our Wuxi, China operations to Suzhou, China.