3

Forward-Looking Statements and

Non-GAAP Information

Forward-Looking Statements and

Non-GAAP Information

Fiscal 2013 first quarter results are unaudited. This presentation contains “forward-looking statements” which are statements

relating to future events, including a proposed acquisition, future financial performance, strategies, expectations, and the

competitive environment. All statements, other than statements of historical facts, contained in this presentation, including

statements regarding the Company’s future financial position, future revenue, prospects, plans and objectives of

management, are forward-looking statements. Additionally, forward -looking statements include statements of expectations

regarding the proposed acquisition, including expected benefits and synergies of the transaction, future financial and

operating results, future opportunities for the combined businesses and other statements regarding events or developments

that the Company believes or anticipates will or may occur in the future as a result of the transaction. Words such as

“believe,” “expect,” “anticipate,” “estimate,” “intend,” “forecast,” “may,” “should,” “could,” “project,” “looking ahead” and similar

expressions, as well as statements in future tense, identify forward-looking statements. You should not read forward looking

statements as a guarantee of future performance or results. They will not necessarily be accurate indications of whether or

at what time such performance or results will be achieved. Forward-looking statements are based on information available

at the time those statements are made and/or management’s good faith belief at that time with respect to future

events, including the Company’s ability to consummate the proposed acquisition. Such statements are subject to risks and

uncertainties that could cause actual performance or results to differ materially from those expressed in or suggested by the

forward-looking statements. Important factors that could cause such differences include, but are not limited to factors

described under Item 1A, “Risk Factors” of the Company’s Annual Report on Form 10-K for the year ended July 28, 2012,

and other risks outlined in the Company’s periodic filings with the Securities and Exchange Commission (“SEC”). The

forward-looking statements in this presentation are expressly qualified in their entirety by this cautionary statement. Except

as required by law, the Company may not update forward-looking statements even though its situation may change in the

future.

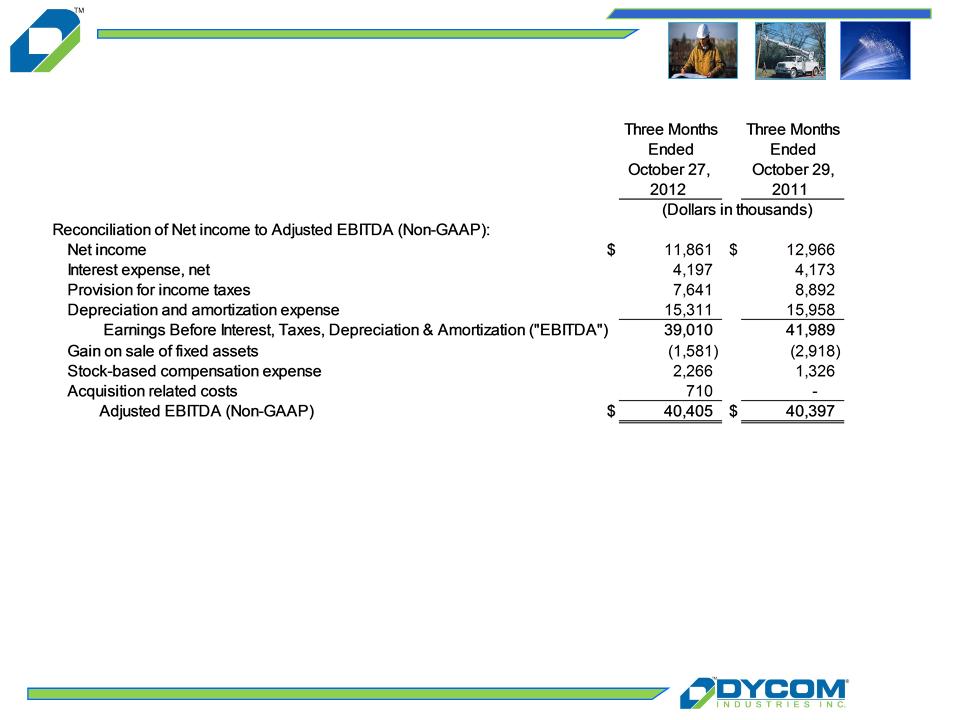

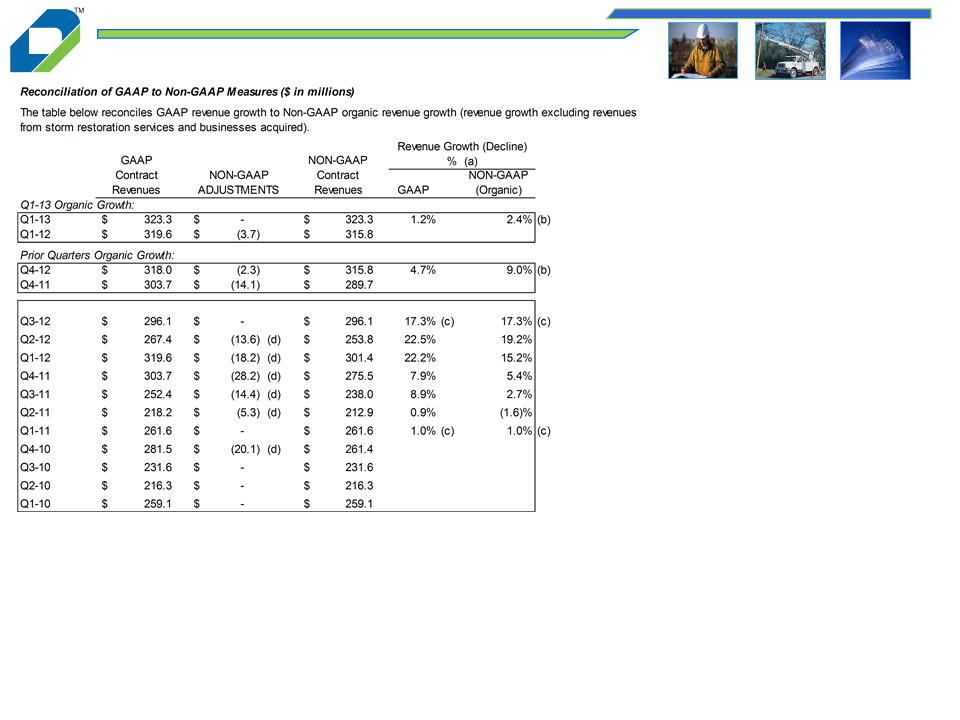

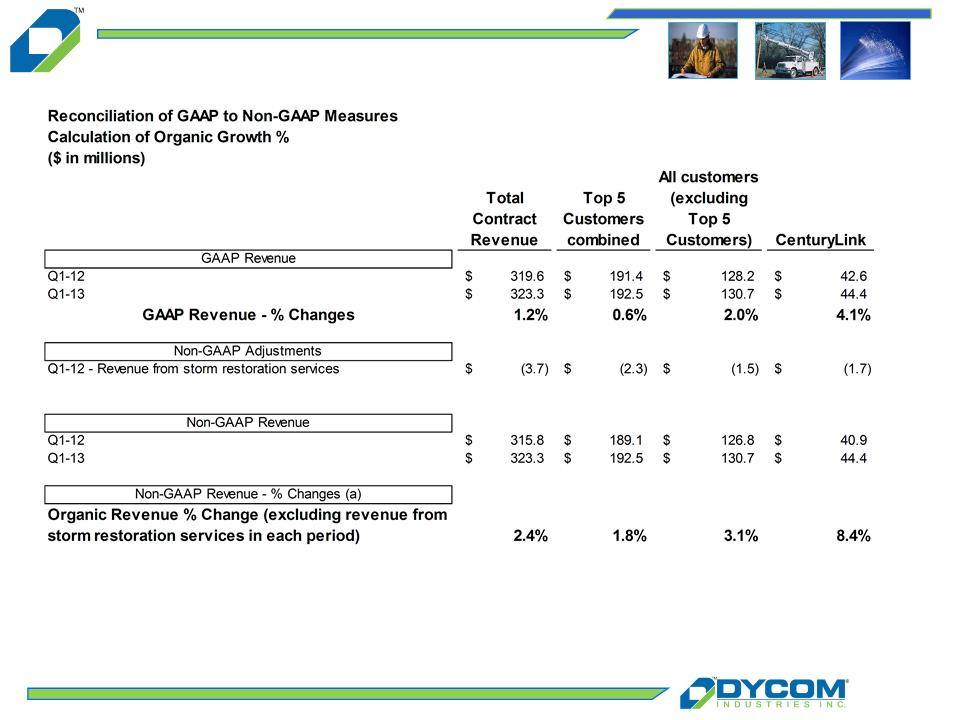

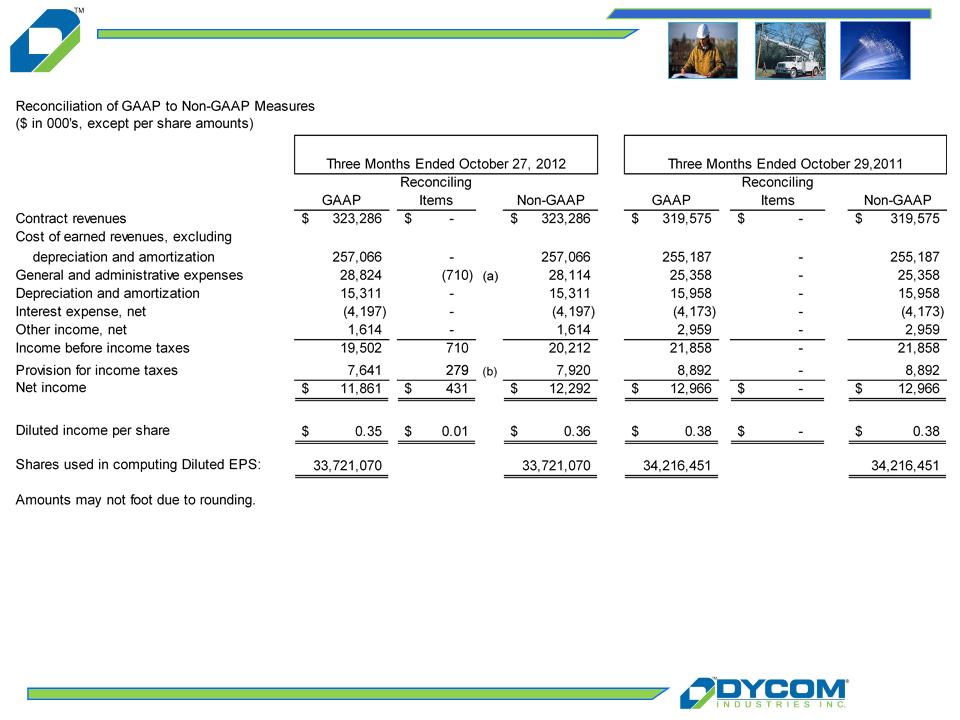

This presentation includes certain “Non-GAAP” financial measures as defined by SEC rules. We believe that the

presentation of certain Non-GAAP financial measures provides information that is useful to investors because it allows for a

more direct comparison of our performance for the period with our performance in the comparable prior-year periods. As

required by the SEC, we have provided a reconciliation of those measures to the most directly comparable GAAP measures

on the Regulation G slides included as slides 19 through 22 of this presentation. We caution that Non-GAAP financial

measures should be considered in addition to, but not as a substitute for, our reported GAAP results.