2019 Annual Reports

American Electric Power Company, Inc. and Subsidiary Companies

AEP Texas Inc. and Subsidiaries

AEP Transmission Company, LLC and Subsidiaries

Appalachian Power Company and Subsidiaries

Indiana Michigan Power Company and Subsidiaries

Ohio Power Company and Subsidiaries

Public Service Company of Oklahoma

Southwestern Electric Power Company Consolidated

Audited Financial Statements and

Management’s Discussion and Analysis of Financial Condition and Results of Operations

AMERICAN ELECTRIC POWER COMPANY, INC. AND SUBSIDIARY COMPANIES

INDEX OF ANNUAL REPORTS

|

| | | | |

| | | Page Number |

| | |

| | | |

| | |

| | | |

| AEP Common Stock Information | | |

| | | |

| | |

| | | | |

| | | | |

| | | | |

| | Management’s Report on Internal Control Over Financial Reporting | | |

| | | | |

| | | | |

| AEP Texas Inc. and Subsidiaries: | | |

| | Management’s Narrative Discussion and Analysis of Results of Operations | | |

| | Report of Independent Registered Public Accounting Firm | | |

| | Management’s Report on Internal Control Over Financial Reporting | | |

| | Consolidated Financial Statements | | |

| | | | |

| AEP Transmission Company, LLC and Subsidiaries: | | |

| | Management’s Narrative Discussion and Analysis of Results of Operations | | |

| | Report of Independent Registered Public Accounting Firm | | |

| | Management’s Report on Internal Control Over Financial Reporting | | |

| | Consolidated Financial Statements | | |

| | | | |

| | |

| | | | |

| | | | |

| | Management’s Report on Internal Control Over Financial Reporting | | |

| | | | |

| | | | |

| | |

| | | | |

| | | | |

| | Management’s Report on Internal Control Over Financial Reporting | | |

| | | | |

| | | | |

| | |

| | | | |

| | | | |

| | Management’s Report on Internal Control Over Financial Reporting | | |

| | | | |

| | | | |

| | |

| | | | |

| | | | |

| | Management’s Report on Internal Control Over Financial Reporting | | |

| | | | |

| | | | |

| | |

| | | | |

| | | | |

| | Management’s Report on Internal Control Over Financial Reporting | | |

| | | | |

| | | | |

| | |

GLOSSARY OF TERMS

When the following terms and abbreviations appear in the text of this report, they have the meanings indicated below.

|

| | |

| Term | | Meaning |

| | | |

| AEGCo | | AEP Generating Company, an AEP electric utility subsidiary. |

| AEP | | American Electric Power Company, Inc., an investor-owned electric public utility holding company which includes American Electric Power Company, Inc. (Parent) and majority owned consolidated subsidiaries and consolidated affiliates. |

| AEP Credit | | AEP Credit, Inc., a consolidated variable interest entity of AEP which securitizes accounts receivable and accrued utility revenues for affiliated electric utility companies. |

| AEP Energy | | AEP Energy, Inc., a wholly-owned retail electric supplier for customers in Ohio, Illinois and other deregulated electricity markets throughout the United States. |

| AEP System | | American Electric Power System, an electric system, owned and operated by AEP subsidiaries. |

| AEP Texas | | AEP Texas Inc., an AEP electric utility subsidiary. |

| AEP Transmission Holdco | | AEP Transmission Holding Company, LLC, a wholly-owned subsidiary of AEP. |

| AEP Utilities | | AEP Utilities, Inc., a former subsidiary of AEP and holding company for TCC, TNC and CSW Energy, Inc. Effective December 31, 2016, TCC and TNC were merged into AEP Utilities, Inc. Subsequently following this merger, the assets and liabilities of CSW Energy, Inc. were transferred to a competitive affiliate company and AEP Utilities, Inc. was renamed AEP Texas Inc. |

| AEP Wind Holdings LLC | | Acquired in April 2019 as Sempra Renewables LLC, develops, owns and operates, or holds interests in, wind generation facilities in the United States. |

| AEPEP | | AEP Energy Partners, Inc., a subsidiary of AEP dedicated to wholesale marketing and trading, hedging activities, asset management and commercial and industrial sales in deregulated markets. |

| AEPRO | | AEP River Operations, LLC, a commercial barge operation sold in November 2015. |

| AEPSC | | American Electric Power Service Corporation, an AEP service subsidiary providing management and professional services to AEP and its subsidiaries. |

| AEPTCo | | AEP Transmission Company, LLC, a wholly-owned subsidiary of AEP Transmission Holdco, is an intermediate holding company that owns the State Transcos. |

| AEPTCo Parent | | AEP Transmission Company, LLC, the holding company of the State Transcos within the AEPTCo consolidation. |

| AFUDC | | Allowance for Funds Used During Construction. |

| AGR | | AEP Generation Resources Inc., a competitive AEP subsidiary in the Generation & Marketing segment. |

| ALJ | | Administrative Law Judge. |

| AOCI | | Accumulated Other Comprehensive Income. |

| APCo | | Appalachian Power Company, an AEP electric utility subsidiary. |

| Appalachian Consumer Rate Relief Funding | | Appalachian Consumer Rate Relief Funding LLC, a wholly-owned subsidiary of APCo and a consolidated variable interest entity formed for the purpose of issuing and servicing securitization bonds related to the under-recovered ENEC deferral balance. |

| APSC | | Arkansas Public Service Commission. |

| ARAM | | Average Rate Assumption Method, an IRS approved method used to calculate the reversal of Excess ADIT for ratemaking purposes. |

| ARO | | Asset Retirement Obligations. |

| ASU | | Accounting Standards Update. |

| CAA | | Clean Air Act. |

| CLECO | | Central Louisiana Electric Company, a nonaffiliated utility company. |

CO2 | | Carbon dioxide and other greenhouse gases. |

| Conesville Plant | | A single unit coal-fired generation plant totaling 651 MW located in Conesville, Ohio. The plant is jointly owned by AGR and a nonaffiliate. |

|

| | |

| Term | | Meaning |

| | | |

| Cook Plant | | Donald C. Cook Nuclear Plant, a two-unit, 2,288 MW nuclear plant owned by I&M. |

| CRES provider | | Competitive Retail Electric Service providers under Ohio law that target retail customers by offering alternative generation service. |

| CSAPR | | Cross-State Air Pollution Rule. |

| CWA | | Clean Water Act. |

| CWIP | | Construction Work in Progress. |

| DCC Fuel | | DCC Fuel IX, DCC Fuel X, DCC Fuel XI, DCC Fuel XII, DCC Fuel XIII, and DCC Fuel XIV consolidated variable interest entities formed for the purpose of acquiring, owning and leasing nuclear fuel to I&M. |

| DOE | | U. S. Department of Energy. |

| Desert Sky | | Desert Sky Wind Farm, a 168 MW wind electricity generation facility located on Indian Mesa in Pecos County, Texas. |

| DHLC | | Dolet Hills Lignite Company, LLC, a wholly-owned lignite mining subsidiary of SWEPCo. |

| DIR | | Distribution Investment Rider. |

| EIS | | Energy Insurance Services, Inc., a nonaffiliated captive insurance company and consolidated variable interest entity of AEP. |

| ENEC | | Expanded Net Energy Cost. |

| Energy Supply | | AEP Energy Supply LLC, a nonregulated holding company for AEP’s competitive generation, wholesale and retail businesses, and a wholly-owned subsidiary of AEP. |

| Equity Units | | AEP’s Equity Units issued in March 2019. |

| ERCOT | | Electric Reliability Council of Texas regional transmission organization. |

| ESP | | Electric Security Plans, a PUCO requirement for electric utilities to adjust their rates by filing with the PUCO. |

| ETT | | Electric Transmission Texas, LLC, an equity interest joint venture between AEP Transmission Holdco and Berkshire Hathaway Energy Company formed to own and operate electric transmission facilities in ERCOT. |

| Excess ADIT | | Excess accumulated deferred income taxes. |

| FAC | | Fuel Adjustment Clause. |

| FASB | | Financial Accounting Standards Board. |

| Federal EPA | | United States Environmental Protection Agency. |

| FERC | | Federal Energy Regulatory Commission. |

| FGD | | Flue Gas Desulfurization or scrubbers. |

| FIP | | Federal Implementation Plan. |

| FTR | | Financial Transmission Right, a financial instrument that entitles the holder to receive compensation for certain congestion-related transmission charges that arise when the power grid is congested resulting in differences in locational prices. |

| GAAP | | Accounting Principles Generally Accepted in the United States of America. |

| Global Settlement | | In February 2017, the PUCO approved a settlement agreement filed by OPCo in December 2016 which resolved all remaining open issues on remand from the Supreme Court of Ohio in OPCo’s 2009 - 2011 and June 2012 - May 2015 ESP filings. It also resolved all open issues in OPCo’s 2009, 2014 and 2015 SEET filings and 2009, 2012 and 2013 FAC Audits. |

| I&M | | Indiana Michigan Power Company, an AEP electric utility subsidiary. |

| IRS | | Internal Revenue Service. |

| ITC | | Investment Tax Credit |

| IURC | | Indiana Utility Regulatory Commission. |

| KGPCo | | Kingsport Power Company, an AEP electric utility subsidiary. |

| KPCo | | Kentucky Power Company, an AEP electric utility subsidiary. |

| kV | | Kilovolt. |

| KWh | | Kilowatt-hour. |

| LPSC | | Louisiana Public Service Commission. |

| MATS | | Mercury and Air Toxics Standards. |

|

| | |

| Term | | Meaning |

| | | |

| MISO | | Midwest Independent Transmission System Operator. |

| MMBtu | | Million British Thermal Units. |

| MPSC | | Michigan Public Service Commission. |

| MTM | | Mark-to-Market. |

| MW | | Megawatt. |

| MWh | | Megawatt-hour. |

| NAAQS | | National Ambient Air Quality Standards. |

| Nonutility Money Pool | | Centralized funding mechanism AEP uses to meet the short-term cash requirements of certain nonutility subsidiaries. |

| North Central Wind Energy Facilities | | A proposed joint PSO and SWEPCo project, which includes three Oklahoma wind facilities totaling approximately 1,485 MWs of wind generation. |

NO2 | | Nitrogen dioxide. |

NOx | | Nitrogen oxide. |

| NPDES | | National Pollutant Discharge Elimination System. |

| NRC | | Nuclear Regulatory Commission. |

| NSR | | New Source Review. |

| OATT | | Open Access Transmission Tariff. |

| OCC | | Corporation Commission of the State of Oklahoma. |

| Ohio Phase-in-Recovery Funding | | Ohio Phase-in-Recovery Funding LLC, a wholly-owned subsidiary of OPCo and a consolidated variable interest entity formed for the purpose of issuing and servicing securitization bonds related to phase-in recovery property. |

| Oklaunion Power Station | | A single unit coal-fired generation plant totaling 650 MW located in Vernon, Texas. The plant is jointly owned by AEP Texas, PSO and certain nonaffiliated entities. |

| OPCo | | Ohio Power Company, an AEP electric utility subsidiary. |

| OPEB | | Other Postretirement Benefits. |

| Operating Agreement | | Agreement, dated January 1, 1997, as amended, by and among PSO and SWEPCo governing generating capacity allocation, energy pricing, and revenues and costs of third-party sales. AEPSC acts as the agent. |

| OSS | | Off-system Sales. |

| OTC | | Over-the-counter. |

| OVEC | | Ohio Valley Electric Corporation, which is 43.47% owned by AEP. |

| Parent | | American Electric Power Company, Inc., the equity owner of AEP subsidiaries within the AEP consolidation. |

| PCA | | Power Coordination Agreement among APCo, I&M, KPCo and WPCo. |

| PJM | | Pennsylvania – New Jersey – Maryland regional transmission organization. |

| PM | | Particulate Matter. |

| PPA | | Purchase Power and Sale Agreement. |

| Price River | | Rights and interests in certain coal reserves located in Carbon County, Utah. |

| PSO | | Public Service Company of Oklahoma, an AEP electric utility subsidiary. |

| PTC | | Production Tax Credits. |

| PUCO | | Public Utilities Commission of Ohio. |

| PUCT | | Public Utility Commission of Texas. |

| Racine | | A generation plant consisting of two hydroelectric generating units totaling 48 MWs located in Racine, Ohio and owned by AGR. |

| Registrant Subsidiaries | | AEP subsidiaries which are SEC registrants: AEP Texas, AEPTCo, APCo, I&M, OPCo, PSO and SWEPCo. |

| Registrants | | SEC registrants: AEP, AEP Texas, AEPTCo, APCo, I&M, OPCo, PSO and SWEPCo. |

| REP | | Texas Retail Electric Provider. |

| Restoration Funding | | AEP Texas Restoration Funding LLC, a wholly-owned subsidiary of AEP Texas and a consolidated VIE formed for the purpose of issuing and servicing securitization bonds related to storm restoration in Texas primarily caused by Hurricane Harvey. |

| Risk Management Contracts | | Trading and non-trading derivatives, including those derivatives designated as cash flow and fair value hedges. |

|

| | |

| Term | | Meaning |

| | | |

| Rockport Plant | | A generation plant, consisting of two 1,310 MW coal-fired generating units near Rockport, Indiana. AEGCo and I&M jointly-own Unit 1. In 1989, AEGCo and I&M entered into a sale-and-leaseback transaction with Wilmington Trust Company, an unrelated, unconsolidated trustee for Rockport Plant, Unit 2. |

| ROE | | Return on Equity. |

| RPM | | Reliability Pricing Model. |

| RTO | | Regional Transmission Organization, responsible for moving electricity over large interstate areas. |

| Sabine | | Sabine Mining Company, a lignite mining company that is a consolidated variable interest entity for AEP and SWEPCo. |

| Santa Rita East | | Santa Rita East Wind Holdings, LLC, a consolidated VIE whose sole purpose is to own and operate a 302 MW wind generation facility in west Texas in which AEP owns a 75% interest. |

| SEC | | U.S. Securities and Exchange Commission. |

| SEET | | Significantly Excessive Earnings Test. |

| Sempra Renewables LLC | | Sempra Renewables LLC, acquired in April 2019, consists of 724 MWs of wind generation and battery assets in the United States. |

| SIA | | System Integration Agreement, effective June 15, 2000, as amended, provides contractual basis for coordinated planning, operation and maintenance of the power supply sources of the combined AEP. |

| SIP | | State Implementation Plan. |

| SNF | | Spent Nuclear Fuel. |

SO2 | | Sulfur dioxide. |

| SPP | | Southwest Power Pool regional transmission organization. |

| SSO | | Standard service offer. |

| State Transcos | | AEPTCo’s seven wholly-owned, FERC regulated, transmission only electric utilities, each of which is geographically aligned with AEP existing utility operating companies. |

| SWEPCo | | Southwestern Electric Power Company, an AEP electric utility subsidiary. |

| Tax Reform | | On December 22, 2017, President Trump signed into law legislation referred to as the “Tax Cuts and Jobs Act” (the TCJA). The TCJA includes significant changes to the Internal Revenue Code of 1986, including a reduction in the corporate federal income tax rate from 35% to 21% effective January 1, 2018. |

| TCC | | Formerly AEP Texas Central Company, now a division of AEP Texas. |

| Texas Restructuring Legislation | | Legislation enacted in 1999 to restructure the electric utility industry in Texas. |

| TNC | | Formerly AEP Texas North Company, now a division of AEP Texas. |

| Transition Funding | | AEP Texas Central Transition Funding II LLC and AEP Texas Central Transition Funding III LLC, wholly-owned subsidiaries of TCC and consolidated variable interest entities formed for the purpose of issuing and servicing securitization bonds related to Texas Restructuring Legislation. |

| Transource Energy | | Transource Energy, LLC, a consolidated variable interest entity formed for the purpose of investing in utilities which develop, acquire, construct, own and operate transmission facilities in accordance with FERC-approved rates. |

| Trent | | Trent Wind Farm, a 154 MW wind electricity generation facility located between Abilene and Sweetwater in West Texas. |

| Turk Plant | | John W. Turk, Jr. Plant, a 600 MW coal-fired plant in Arkansas that is 73% owned by SWEPCo. |

| UMWA | | United Mine Workers of America. |

| UPA | | Unit Power Agreement. |

| Utility Money Pool | | Centralized funding mechanism AEP uses to meet the short-term cash requirements of certain utility subsidiaries. |

| VIE | | Variable Interest Entity. |

| Virginia SCC | | Virginia State Corporation Commission. |

|

| | |

| Term | | Meaning |

| | | |

| Wind Catcher Project | | Wind Catcher Energy Connection Project, a joint PSO and SWEPCo project that was cancelled in July 2018. The estimated $4.5 billion project included the acquisition of a wind generation facility, totaling approximately 2,000 MWs of wind generation, and the construction of a generation interconnection tie-line totaling approximately 350 miles. |

| WPCo | | Wheeling Power Company, an AEP electric utility subsidiary. |

| WVPSC | | Public Service Commission of West Virginia. |

FORWARD-LOOKING INFORMATION

This report made by the Registrants contains forward-looking statements within the meaning of Section 21E of the Securities Exchange Act of 1934. Many forward-looking statements appear in “Item 7 – Management’s Discussion and Analysis of Financial Condition and Results of Operations,” but there are others throughout this document which may be identified by words such as “expect,” “anticipate,” “intend,” “plan,” “believe,” “will,” “should,” “could,” “would,” “project,” “continue” and similar expressions, and include statements reflecting future results or guidance and statements of outlook. These matters are subject to risks and uncertainties that could cause actual results to differ materially from those projected. Forward-looking statements in this document are presented as of the date of this document. Except to the extent required by applicable law, management undertakes no obligation to update or revise any forward-looking statement. Among the factors that could cause actual results to differ materially from those in the forward-looking statements are:

|

| |

| • | Changes in economic conditions, electric market demand and demographic patterns in AEP service territories. |

| • | Inflationary or deflationary interest rate trends. |

| • | Volatility in the financial markets, particularly developments affecting the availability or cost of capital to finance new capital projects and refinance existing debt. |

| • | The availability and cost of funds to finance working capital and capital needs, particularly during periods when the time lag between incurring costs and recovery is long and the costs are material. |

| • | Decreased demand for electricity. |

| • | Weather conditions, including storms and drought conditions, and the ability to recover significant storm restoration costs. |

| • | The cost of fuel and its transportation, the creditworthiness and performance of fuel suppliers and transporters and the cost of storing and disposing of used fuel, including coal ash and SNF. |

| • | The availability of fuel and necessary generation capacity and the performance of generation plants. |

| • | The ability to recover fuel and other energy costs through regulated or competitive electric rates. |

| • | The ability to build or acquire renewable generation, transmission lines and facilities (including the ability to obtain any necessary regulatory approvals and permits) when needed at acceptable prices and terms and to recover those costs. |

| • | New legislation, litigation and government regulation, including oversight of nuclear generation, energy commodity trading and new or heightened requirements for reduced emissions of sulfur, nitrogen, mercury, carbon, soot or PM and other substances that could impact the continued operation, cost recovery and/or profitability of generation plants and related assets. |

| • | Evolving public perception of the risks associated with fuels used before, during and after the generation of electricity, including coal ash and nuclear fuel. |

| • | Timing and resolution of pending and future rate cases, negotiations and other regulatory decisions, including rate or other recovery of new investments in generation, distribution and transmission service and environmental compliance. |

| • | Resolution of litigation. |

| • | The ability to constrain operation and maintenance costs. |

| • | Prices and demand for power generated and sold at wholesale. |

| • | Changes in technology, particularly with respect to energy storage and new, developing, alternative or distributed sources of generation. |

| • | The ability to recover through rates any remaining unrecovered investment in generation units that may be retired before the end of their previously projected useful lives. |

| • | Volatility and changes in markets for coal and other energy-related commodities, particularly changes in the price of natural gas. |

| • | Changes in utility regulation and the allocation of costs within RTOs including ERCOT, PJM and SPP. |

| • | Changes in the creditworthiness of the counterparties with contractual arrangements, including participants in the energy trading market. |

| • | Actions of rating agencies, including changes in the ratings of debt. |

| • | The impact of volatility in the capital markets on the value of the investments held by the pension, OPEB, captive insurance entity and nuclear decommissioning trust and the impact of such volatility on future funding requirements. |

| • | Accounting standards periodically issued by accounting standard-setting bodies. |

|

| |

| • | Other risks and unforeseen events, including wars, the effects of terrorism (including increased security costs), embargoes, naturally occurring and human-caused fires, cyber security threats and other catastrophic events. |

| • | The ability to attract and retain the requisite work force and key personnel. |

The forward-looking statements of the Registrants speak only as of the date of this report or as of the date they are made. The Registrants expressly disclaim any obligation to update any forward-looking information, except as required by law. For a more detailed discussion of these factors, see “Risk Factors” in Part I of this report.

Investors should note that the Registrants announce material financial information in SEC filings, press releases and public conference calls. Based on guidance from the SEC, the Registrants may use the Investors section of AEP’s website (www.aep.com) to communicate with investors about the Registrants. It is possible that the financial and other information posted there could be deemed to be material information. The information on AEP’s website is not part of this report.

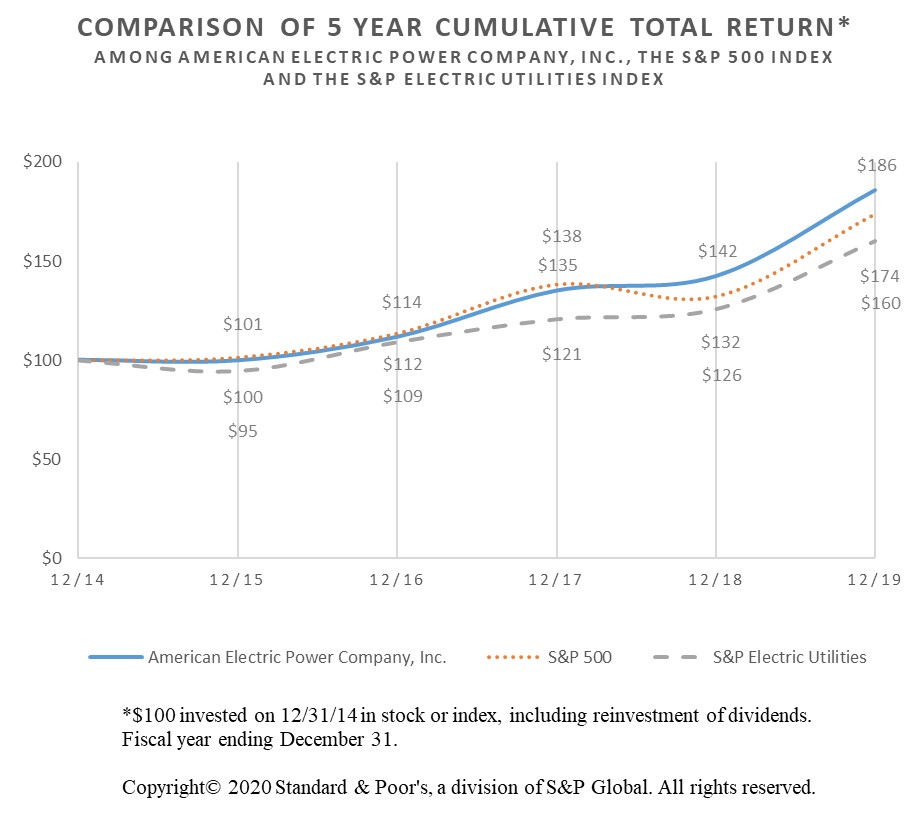

AEP COMMON STOCK INFORMATION

AEP common stock is principally traded using the trading symbol “AEP” on the New York Stock Exchange. As of December 31, 2019, AEP had approximately 57,000 registered shareholders.

|

| | | | | | | | | | | | | | | | | | | | |

| AMERICAN ELECTRIC POWER COMPANY, INC. AND SUBSIDIARY COMPANIES |

| SELECTED CONSOLIDATED FINANCIAL DATA |

| | |

| | |

| | | 2019 (a) | | 2018 | | 2017 | | 2016 | | 2015 |

| | | (dollars in millions, except per share amounts) |

| STATEMENTS OF INCOME DATA | | | | | | | | | | |

| Total Revenues | | $ | 15,561.4 |

| | $ | 16,195.7 |

| | $ | 15,424.9 |

| | $ | 16,380.1 |

| | $ | 16,453.2 |

|

| | |

|

| | | | | | | | |

| Operating Income | | $ | 2,592.3 |

| | $ | 2,682.7 |

| | $ | 3,525.0 |

| | $ | 1,163.9 |

| | $ | 3,292.4 |

|

| | | | | | | | | | | |

| Income from Continuing Operations | | $ | 1,919.8 |

| | $ | 1,931.3 |

| | $ | 1,928.9 |

| | $ | 620.5 |

| | $ | 1,768.6 |

|

| Income (Loss) From Discontinued Operations, Net of Tax | | — |

| | — |

| | — |

| | (2.5 | ) | | 283.7 |

|

| Net Income | | 1,919.8 |

| | 1,931.3 |

| | 1,928.9 |

| | 618.0 |

| | 2,052.3 |

|

| | | | | | | | | | | |

| Net Income (Loss) Attributable to Noncontrolling Interest | | (1.3 | ) | | 7.5 |

| | 16.3 |

| | 7.1 |

| | 5.2 |

|

| | | | | | | | | | | |

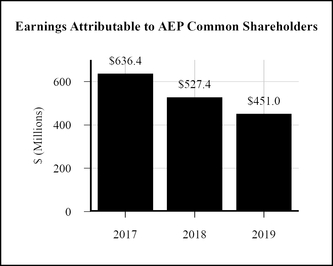

| EARNINGS ATTRIBUTABLE TO AEP COMMON SHAREHOLDERS | | $ | 1,921.1 |

| | $ | 1,923.8 |

| | $ | 1,912.6 |

| | $ | 610.9 |

| | $ | 2,047.1 |

|

| | | | | | | | | | | |

| BALANCE SHEETS DATA | | | | | | | | | | |

| Total Property, Plant and Equipment | | $ | 79,145.7 |

| | $ | 73,085.2 |

| | $ | 67,428.5 |

| | $ | 62,036.6 |

| | $ | 65,481.4 |

|

| Accumulated Depreciation and Amortization | | 19,007.6 |

| | 17,986.1 |

| | 17,167.0 |

| | 16,397.3 |

| | 19,348.2 |

|

| Total Property, Plant and Equipment – Net | | $ | 60,138.1 |

| | $ | 55,099.1 |

| | $ | 50,261.5 |

| | $ | 45,639.3 |

| | $ | 46,133.2 |

|

| | | | | | | | | | | |

| Total Assets | | $ | 75,892.3 |

| | $ | 68,802.8 |

| | $ | 64,729.1 |

| | $ | 63,467.7 |

| | $ | 61,683.1 |

|

| | |

|

| | | | | | | | |

| Total AEP Common Shareholders’ Equity | | $ | 19,632.2 |

| | $ | 19,028.4 |

| | $ | 18,287.0 |

| | $ | 17,397.0 |

| | $ | 17,891.7 |

|

| | |

|

| | | | | | | | |

| Noncontrolling Interests | | $ | 281.0 |

| | $ | 31.0 |

| | $ | 26.6 |

| | $ | 23.1 |

| | $ | 13.2 |

|

| | |

|

| | | | | | | | |

| Long-term Debt (b) | | $ | 26,725.5 |

| | $ | 23,346.7 |

| | $ | 21,173.3 |

| | $ | 20,256.4 |

| | $ | 19,572.7 |

|

| | |

|

| | | | | | | | |

| Obligations Under Finance Leases (b) | | $ | 306.8 |

| | $ | 289.0 |

| | $ | 297.8 |

| | $ | 305.5 |

| | $ | 343.5 |

|

| | |

|

| | | | | | | | |

| Obligations Under Operating Leases (b) (c) | | $ | 968.7 |

| | $ | — |

| | $ | — |

| | $ | — |

| | $ | — |

|

| | | | | | | | | | | |

| AEP COMMON STOCK DATA | |

|

| | | | | | | | |

| Basic Earnings (Loss) per Share Attributable to AEP Common Shareholders: | |

|

| | | | | | | | |

| | |

|

| | | | | | | | |

| From Continuing Operations | | $ | 3.89 |

| | $ | 3.90 |

| | $ | 3.89 |

| | $ | 1.25 |

| | $ | 3.59 |

|

| From Discontinued Operations | | — |

| | — |

| | — |

| | (0.01 | ) | | 0.58 |

|

| | |

|

| | | | | | | | |

| Total Basic Earnings per Share Attributable to AEP Common Shareholders | | $ | 3.89 |

| | $ | 3.90 |

| | $ | 3.89 |

| | $ | 1.24 |

| | $ | 4.17 |

|

| | |

|

| | | | | | | | |

| Weighted Average Number of Basic Shares Outstanding (in millions) | | 493.7 |

| | 492.8 |

| | 491.8 |

| | 491.5 |

| | 490.3 |

|

| | |

| | | | | | | | |

| Market Price Range: | |

| | | | | | | | |

| High | | $ | 96.22 |

| | $ | 81.05 |

| | $ | 78.07 |

| | $ | 71.32 |

| | $ | 65.38 |

|

| Low | | $ | 72.26 |

| | $ | 62.71 |

| | $ | 61.82 |

| | $ | 56.75 |

| | $ | 52.29 |

|

| | |

|

| | | | | | | | |

| Year-end Market Price | | $ | 94.51 |

| | $ | 74.74 |

| | $ | 73.57 |

| | $ | 62.96 |

| | $ | 58.27 |

|

| | |

|

| | | | | | | | |

| Cash Dividends Declared per AEP Common Share | | $ | 2.71 |

| | $ | 2.53 |

| | $ | 2.39 |

| | $ | 2.27 |

| | $ | 2.15 |

|

| | |

|

| | | | | | | | |

| Dividend Payout Ratio | | 69.67 | % | | 64.87 | % | | 61.44 | % | | 183.06 | % | | 51.56 | % |

| | |

|

| | | | | | | | |

| Book Value per AEP Common Share | | $ | 39.73 |

| | $ | 38.58 |

| | $ | 37.17 |

| | $ | 35.38 |

| | $ | 36.44 |

|

| |

| (a) | The 2019 financial results include pretax asset impairments of $156 million. See Note 7 - Acquisitions, Dispositions and Impairments for additional information. |

| |

| (b) | Includes portion due within one year. |

| |

| (c) | Reflects the adoption of ASU 2016-02 “Accounting for Leases.” See Note 2 - New Accounting Standards and Note 13 - Leases for additional information. |

AMERICAN ELECTRIC POWER COMPANY, INC. AND SUBSIDIARY COMPANIES MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND

RESULTS OF OPERATIONS

EXECUTIVE OVERVIEW

Company Overview

AEP is one of the largest investor-owned electric public utility holding companies in the United States. AEP’s electric utility operating companies provide generation, transmission and distribution services to more than five million retail customers in Arkansas, Indiana, Kentucky, Louisiana, Michigan, Ohio, Oklahoma, Tennessee, Texas, Virginia and West Virginia.

AEP’s subsidiaries operate an extensive portfolio of assets including:

| |

| • | Approximately 221,000 miles of distribution lines that deliver electricity to 5.5 million customers. |

| |

| • | Approximately 40,000 circuit miles of transmission lines, including approximately 2,200 circuit miles of 765 kV lines, the backbone of the electric interconnection grid in the eastern United States. |

| |

| • | Approximately 22,000 MWs of regulated owned generating capacity and approximately 4,900 MWs of regulated PPA capacity in 3 RTOs as of December 31, 2019, one of the largest complements of generation in the United States. |

Customer Demand

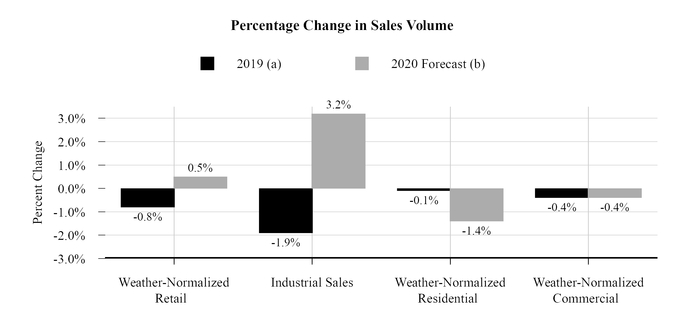

AEP’s weather-normalized retail sales volumes for the year ended December 31, 2019 decreased by 0.8% from the year ended December 31, 2018. AEP’s 2019 industrial sales volumes decreased 1.9% compared to 2018. The decline in industrial sales was spread across most operating companies and many industries. Weather-normalized residential sales decreased 0.1% despite a 0.3% growth in customer counts. Weather-normalized commercial sales decreased by 0.4% in 2019 compared to 2018.

In 2020, AEP anticipates weather-normalized retail sales volumes will increase by 0.5%. The industrial class is expected to increase by 3.2% in 2020, while weather-normalized residential sales volumes are projected to decrease by 1.4%. Weather-normalized commercial sales volumes are projected to decrease by 0.4%.

| |

| (a) | Percentage change for the year ended December 31, 2019 as compared to the year ended December 31, 2018. |

| |

| (b) | Forecasted percentage change for the year ended December 31, 2020 compared to the year ended December 31, 2019. |

Regulatory Matters

AEP’s public utility subsidiaries are involved in rate and regulatory proceedings at the FERC and their state commissions. Depending on the outcomes, these rate and regulatory proceedings can have a material impact on results of operations, cash flows and possibly financial condition. AEP is currently involved in the following key proceedings. See Note 4 - Rate Matters for additional information.

| |

| • | 2019 Texas Base Rate Case - In May 2019, AEP Texas filed a request with the PUCT for a $56 million annual increase in rates based upon a proposed 10.5% return on common equity. In November 2019, ALJs issued a Proposal for Decision recommending a $60 million annual rate reduction based upon a 9.4% return on common equity. The ALJs recommended disallowances that could potentially result in write-offs of $84 million related to capital incentives and $5 million related to other plant additions. Additionally, the ALJs recommended that AEP Texas should be required to file an application for a separate proceeding to determine if any refunds are required associated with any disallowances on distribution or transmission capital investments. In February 2020, AEP Texas, the PUCT staff and various intervenors filed a stipulation and settlement agreement with the PUCT. The agreement includes a proposed annual base rate reduction of $40 million based upon a 9.4% return on common equity with a capital structure of 57.5% debt and 42.5% common equity. The agreement provides recovery of $26 million in capitalized vegetation management expenses that were incurred through 2018. The agreement includes disallowances of $23 million related to capital investments recorded through 2018 and $4 million related to rate case expenses. In addition, AEP Texas will refund: (a) $77 million of Excess ADIT and excess federal income taxes collected as a result of Tax Reform to distribution customers over a one year period, (b) $31 million of Excess ADIT and excess federal income taxes collected as a result of Tax Reform to transmission customers as a one-time credit and (c) $30 million of previously collected rates that were subject to reconciliation in this proceeding over a one year period with no carrying costs. As a result of the stipulation and settlement agreement, AEP Texas (a) recorded an impairment of $33 million in December 2019 related to capital investments, which included $10 million of current year investments, (b) recorded a $30 million provision for refund for revenues previously collected through rates and (c) wrote-off $4 million of rate case expenses. The PUCT is expected to issue an order in the first quarter of 2020. |

| |

| • | 2019 Indiana Base Rate Case - In May 2019, I&M filed a request with the IURC for a $172 million annual increase. The requested increase in Indiana rates would be phased in through January 2021 and is based upon a proposed 10.5% return on common equity. In August 2019, certain intervenors filed testimony that includes recommended disallowances that could potentially result in write-offs of $41 million related to the remaining book value of existing Indiana jurisdictional meters if I&M is approved to deploy Automated Metering Infrastructure meters and $11 million associated with certain Cook Plant study costs. The IURC is expected to issue an order on this case in the first quarter of 2020. |

| |

| • | Virginia Legislation Affecting Earnings Reviews - In March 2018, Virginia enacted legislation requiring APCo to file its next generation and distribution base rate case by March 31, 2020 using 2017, 2018 and 2019 test years (triennial review). Triennial reviews are subject to an earnings test which provides that 70% of any earnings in excess of 70 basis points above APCo’s Virginia SCC authorized ROE would be refunded to customers. Virginia law provides that costs associated with asset impairments of retired coal generation assets, or automated meters, or both, which a utility records as an expense, shall be attributed to the test periods under review in a triennial review proceeding, and be deemed recovered. Based on management’s interpretation of Virginia law and more certainty regarding APCo’s triennial revenues, expenses and resulting earnings upon reaching the end of the three-year review period, APCo recorded a pretax expense of $93 million related to its previously retired coal-fired generation assets in December 2019. This expense is included in Asset Impairments and Other Related Charges on the statements of income. As a result, management deems these costs to be substantially recovered by APCo during the triennial review period. Inclusive of the $93 million expense associated with APCo’s Virginia jurisdictional retired coal-fired plants, APCo estimates its Virginia earnings for the triennial period to be below the authorized ROE range. |

| |

| • | 2020 Increase in West Virginia Retail Rates for WPCo 17.5% Merchant Share of Mitchell Plant - In 2015, the WVPSC approved a settlement agreement in which 82.5% of the West Virginia jurisdictional costs associated with WPCo’s acquired interest were prospectively reflected in retail rates with the remaining 17.5% of costs associated with the acquired interest to be included in rates starting January 2020. APCo and WPCo file joint retail rates in West Virginia. In June 2019, APCo and WPCo filed with the WVPSC to increase each company’s retail rates through a surcharge to reflect the recovery of WPCo’s remaining 17.5% interest in the Mitchell Plant. In December 2019, the WVPSC issued an order approving a stipulation and settlement agreement that will allow APCo and WPCo to recover the remaining 17.5% West Virginia share of costs related to the Mitchell Plant and increase pretax earnings on a combined company basis by approximately $21 million annually beginning January 1, 2020. |

| |

| • | 2012 Texas Base Rate Case - In 2012, SWEPCo filed a request with the PUCT to increase annual base rates primarily due to the completion of the Turk Plant. In 2013, the PUCT issued an order affirming the prudence of the Turk Plant. In July 2018, the Texas Third Court of Appeals reversed the PUCT’s judgment affirming the prudence of the Turk Plant and remanded the issue back to the PUCT. In January 2019, SWEPCo and the PUCT filed petitions for review with the Texas Supreme Court. In May 2019, various intervenors filed replies to the petition. In July 2019, SWEPCo filed its response to these replies. In the fourth quarter of 2019 and first quarter of 2020, SWEPCo and various intervenors filed briefs with the Texas Supreme Court. As of December 31, 2019, the net book value of Turk Plant was $1.5 billion, before cost of removal, including materials and supplies inventory and CWIP. SWEPCo’s Texas jurisdictional share of the Turk Plant investment is approximately 33%. |

| |

| • | In July 2019, clean energy legislation which offers incentives for power-generating facilities with zero or reduced carbon emissions was signed into law by the Ohio Governor. The clean energy legislation phases out current energy efficiency including lost shared savings revenues of $26 million annually and renewable mandates no later than 2020 and after 2026, respectively. The bill provides for the recovery of existing renewable energy contracts on a bypassable basis through 2032. The clean energy legislation also includes a provision for recovery of OVEC costs through 2030 which will be allocated to all electric distribution utilities on a non-bypassable basis. OPCo’s Inter-Company Power Agreement for OVEC terminates in June 2040. To the extent that OPCo is unable to recover the costs of renewable energy contracts on a bypassable basis by the end of 2032, recover costs of OVEC after 2030 or fully recover energy efficiency costs through 2020 it could reduce future net income and cash flows and impact financial condition. |

Utility Rates and Rate Proceedings

The Registrants file rate cases with their regulatory commissions in order to establish fair and appropriate electric service rates to recover their costs and earn a fair return on their investments. The outcomes of these regulatory proceedings impact the Registrants’ current and future results of operations, cash flows and financial position.

The following tables show the Registrants’ completed and pending base rate case proceedings in 2019. See Note 4 - Rate Matters for additional information.

Completed Base Rate Case Proceedings

|

| | | | | | | | | | |

| | | | | Approved Revenue | | Approved | | New Rates |

| Company | | Jurisdiction | | Requirement Increase | | ROE | | Effective |

| | | | | (in millions) | | | | |

| APCo | | West Virginia | | $ | 35.8 |

| | 9.75% | | March 2019 |

| WPCo | | West Virginia | | 8.4 |

| | 9.75% | | March 2019 |

| PSO | | Oklahoma | | 46.0 |

| | 9.4% | | April 2019 |

| SWEPCo | | Arkansas | | 52.8 |

| | 9.45% | | January 2020 |

| I&M | | Michigan | | 36.4 |

| | 9.86% | | February 2020 |

Pending Base Rate Case Proceedings

|

| | | | | | | | | | | | |

| | | | | | | | | | | Commission Staff/ |

| | | | | Filing | | Requested Revenue | | Requested | | Intervenor Range of |

| Company | | Jurisdiction | | Date | | Requirement Increase | | ROE | | Recommended ROE |

| | | | | | | (in millions) | | | | |

| AEP Texas (a) | | Texas | | May 2019 | | $ | 56.0 |

| | 10.5% | | 9% - 9.35% |

| I&M | | Indiana | | May 2019 | | 172.0 |

| | 10.5% | | 9% - 9.73% |

| |

| (a) | In February 2020, AEP Texas, the PUCT staff and various intervenors filed a stipulation and settlement agreement with the PUCT that includes a proposed annual base rate reduction of $40 million based upon a 9.4% return on common equity. See “2019 Texas Base Rate Case” section of Note 4 for additional information. |

Dolet Hills Power Station and Related Fuel Operations

During the second quarter of 2019, the Dolet Hills Power Station initiated a seasonal operating schedule. In January 2020, in accordance with the terms of SWEPCo’s settlement of its base rate review filed with the APSC, management announced that SWEPCo will seek regulatory approval to retire the Dolet Hills Power Station by the end of 2026. Management also continues to monitor the economic viability of the Dolet Hills Power Station and DHLC mining operations, which may result in a decision to seek permission from appropriate regulatory agencies to discontinue operations earlier than 2026.

The Dolet Hills Power Station costs are recoverable by SWEPCo through base rates. SWEPCo’s share of the net investment in the Dolet Hills Power Station is $157 million, including CWIP and materials and supplies, before cost of removal.

Fuel costs incurred by the Dolet Hills Power Station are recoverable by SWEPCo through active fuel clauses. Under the Lignite Mining Agreement, DHLC bills SWEPCo its proportionate share of incurred lignite extraction and associated mining-related costs as fuel is delivered. As of December 31, 2019, DHLC has unbilled fixed costs of $106 million that will be billed to SWEPCo prior to the closure of the Dolet Hills Power Station. In 2009, SWEPCo acquired interests in the Oxbow Lignite Company (Oxbow), which owns mineral rights and leases land. Under a Joint Operating Agreement pertaining to the Oxbow mineral rights and land leases, Oxbow bills SWEPCo its proportionate share of incurred costs. As of December 31, 2019, Oxbow has unbilled fixed costs of $22 million that will be billed to SWEPCo prior to the closure of the Dolet Hills Power Station. Additional operational and land-related costs are expected to be incurred by DHLC and Oxbow and billed to SWEPCo prior to the closure of the Dolet Hills Power Station and recovered through fuel clauses.

If any of these costs are not recoverable, it could reduce future net income and cash flows and impact financial condition.

Renewable Generation

The growth of AEP’s renewable generation portfolio reflects the company’s strategy to diversify generation resources to provide clean energy options to customers that meet both their energy and capacity needs.

Contracted Renewable Generation Facilities

AEP continues to develop its renewable portfolio within the Generation & Marketing segment. Activities include working directly with wholesale and large retail customers to provide tailored solutions based upon market knowledge, technology innovations and deal structuring which may include distributed solar, wind, combined heat and power, energy storage, waste heat recovery, energy efficiency, peaking generation and other forms of cost reducing energy technologies. The Generation & Marketing segment also develops and/or acquires large scale renewable generation projects that are backed with long-term contracts with creditworthy counterparties.

In April 2019, AEP acquired Sempra Renewables LLC and its ownership interests in 724 MWs of wind generation and battery assets valued at approximately $1.1 billion. AEP paid $580 million in cash and acquired a 50% ownership interest in five non-consolidated joint ventures with net assets valued at $404 million as of the acquisition date (which includes $364 million of existing debt obligations). Additionally, the transaction included the acquisition of two tax

equity partnerships and the associated recognition of noncontrolling tax equity interest of $135 million. The wind generation portfolio includes seven wind farms with long-term PPAs for 100% of their energy production. Five of the wind farms are jointly-owned with BP Wind Energy and two wind farms are consolidated by AEP and are tax equity partnerships with nonaffiliated noncontrolling interests. See “Acquisitions” section of Note 7 for additional information.

In July 2019, AEP acquired a 75% interest, or 227 MWs, in Santa Rita East for approximately $356 million. The project is located in west Texas and was placed in-service in July 2019. Long-term virtual power purchase agreements are in place with nonaffiliates for the project’s generation. See “Acquisitions” section of Note 7 for additional information.

As of December 31, 2019, subsidiaries within AEP’s Generation & Marketing segment had approximately 1,421 MWs of contracted renewable generation projects in-service. In addition, as of December 31, 2019, these subsidiaries had approximately 156 MWs of renewable generation projects under construction with total estimated capital costs of $229 million related to these projects.

Regulated Renewable Generation Facilities

In September 2018, OPCo, consistent with its commitment in the previously approved PPA application, submitted a filing with the PUCO demonstrating a need for up to 900 MWs of economically beneficial renewable resources in Ohio. This filing was followed by a separate filing for two solar Renewable Energy Purchase Agreements totaling 400 MWs. In January 2019, PUCO staff recommended that the PUCO reject OPCo’s request. In November 2019, PUCO denied OPCo’s application for a resource planning need finding. In December 2019, OPCo filed an Application for Rehearing, which was also denied.

In July 2019, PSO and SWEPCo submitted filings before their respective commissions for the approval to acquire the North Central Wind Energy Facilities, comprised of three Oklahoma wind facilities totaling 1,485 MWs, on a fixed cost turn-key basis at completion. Subject to regulatory approval, PSO will own 45.5% and SWEPCo will own 54.5% of the project, which will cost approximately $2 billion. Two wind facilities, totaling 1,286 MWs, would qualify for 80% of the federal PTC with year-end 2021 in-service dates. The third wind facility (199 MWs) would qualify for 100% of the PTC with a year-end 2020 in-service date. The acquisition can be scaled, subject to commercial limitation, to align with individual state resource needs and approvals. In December 2019, PSO reached a joint stipulation and settlement agreement with the OCC, Oklahoma Attorney General’s office and customer groups. In January 2020, SWEPCo reached a joint settlement agreement with the APSC, Arkansas Attorney General’s office and Walmart, Inc. SWEPCo continues to work through the regulatory process in Texas and Louisiana. Hearings are scheduled for the first quarter of 2020. PSO and SWEPCo are seeking regulatory approvals by July 2020.

Federal Tax Reform

Based on current regulatory orders received, management anticipates amortization of $249 million of Excess ADIT in 2020 ($68 million of Excess ADIT subject to normalization requirements and $181 million of Excess ADIT that is not subject to normalization requirements). Customer usage or new regulatory orders could result in changes to these estimates. Management anticipates amortizing the following ranges of Excess ADIT that is not subject to normalization requirements over the next five years:

Annual Amortization of Unamortized

Balance as of December 31, 2019

|

| | | | | | | | |

| Year | | Range |

| | | (in millions) |

| 2020 | | $ | 165.0 |

| - | $ | 196.0 |

|

| 2021 | | 102.0 |

| - | 134.0 |

|

| 2022 | | 75.0 |

| - | 105.0 |

|

| 2023 | | 67.0 |

| - | 98.0 |

|

| 2024 | | 34.0 |

| - | 65.0 |

|

Racine

A project to reconstruct a defective dam structure at Racine began in the first quarter of 2017. Due to a significant increase in estimated costs to complete the reconstruction project, AEP recorded impairments in 2017 and 2018. See Note 7 - Acquisitions, Dispositions and Impairments for additional information. Reconstruction activities at Racine are currently estimated to be completed in the first half of 2020. AEP expects to incur additional capital expenditures to complete the reconstruction project, at which point the fair value of Racine, as fully operational, is expected to approximate the book value once complete. Future revisions in cost estimates or delays in completion could result in additional losses which could reduce future net income and cash flows and impact financial condition.

Merchant Portion of Turk Plant

SWEPCo constructed the Turk Plant, a base load 600 MW (650 MW net maximum capacity) pulverized coal ultra-supercritical generating unit in Arkansas, which was placed into service in December 2012 and is included in the Vertically Integrated Utilities segment. SWEPCo owns 73% (440 MWs/477 MWs) of the Turk Plant and operates the facility.

The APSC granted approval for SWEPCo to build the Turk Plant by issuing a Certificate of Environmental Compatibility and Public Need (CECPN) for the SWEPCo Arkansas jurisdictional share of the Turk Plant (approximately 20%). Following an appeal by certain intervenors, the Arkansas Supreme Court issued a decision that reversed the APSC’s grant of the CECPN. In June 2010, in response to an Arkansas Supreme Court decision, the APSC issued an order which reversed and set aside the previously granted CECPN. This share of the Turk Plant output is currently not subject to cost-based rate recovery and is being sold into the wholesale market. Approximately 80% of the Turk Plant investment is recovered under cost-based rate recovery in Texas, Louisiana and through SWEPCo’s wholesale customers under FERC-based rates. As of December 31, 2019, the net book value of Turk Plant was $1.5 billion, before cost of removal, including materials and supplies inventory and CWIP. If SWEPCo cannot ultimately recover its investment and expenses related to the Turk Plant, it could reduce future net income and cash flows and impact financial condition.

FERC Transmission ROE Methodology

In November 2019, the FERC issued Opinion No. 569, which adopted a revised methodology for determining whether an existing base ROE is just and reasonable under Federal Power Act and determined the base ROE for MISO’s transmission-owning members should be reduced to 9.88% (10.38% inclusive of RTO incentive adder of 0.5%). The revised ROE methodology relies on two financial models, which include the discounted cash flow model and the capital asset pricing model, to establish a composite zone of reasonableness. In December 2019, AEP filed multiple requests for rehearing and participated in filing comments and requests for rehearing on behalf of transmission owners and industry organizations. Management believes FERC Opinion No. 569 reverses the expectation of a four-model framework proposed by FERC in 2018 and vetted widely in FERC 2019 Notice of Inquiry regarding base ROE policy. Management does not believe this ruling will have a material impact on financial results for its MISO transmission-owning subsidiaries. In the second quarter of 2019, FERC approved settlement agreements establishing base ROEs of 9.85% (10.35% inclusive of RTO incentive adder of 0.5%) and 10% (10.5% inclusive of RTO incentive adder of 0.5%) for AEP’s PJM and SPP transmission-owning subsidiaries, respectively. If FERC makes any changes to its ROE and incentive policies, they would be applied to AEP’s PJM and SPP transmission owning subsidiaries on a prospective basis, and could affect future net income and cash flows and impact financial condition.

LITIGATION

In the ordinary course of business, AEP is involved in employment, commercial, environmental and regulatory litigation. Since it is difficult to predict the outcome of these proceedings, management cannot predict the eventual resolution, timing or amount of any loss, fine or penalty. Management assesses the probability of loss for each contingency and accrues a liability for cases that have a probable likelihood of loss if the loss can be estimated. Adverse results in these proceedings have the potential to reduce future net income and cash flows and impact financial condition. See Note 4 – Rate Matters and Note 6 – Commitments, Guarantees and Contingencies for additional information.

Rockport Plant Litigation

In 2013, the Wilmington Trust Company filed a complaint in the U.S. District Court for the Southern District of New York against AEGCo and I&M alleging that it would be unlawfully burdened by the terms of the modified NSR consent decree after the Rockport Plant, Unit 2 lease expiration in December 2022. The terms of the consent decree allow the installation of environmental emission control equipment, repowering, refueling or retirement of the unit. The plaintiffs seek a judgment declaring that the defendants breached the lease, must satisfy obligations related to installation of emission control equipment and indemnify the plaintiffs. The New York court granted a motion to transfer this case to the U.S. District Court for the Southern District of Ohio.

AEGCo and I&M sought and were granted dismissal by the U.S. District Court for the Southern District of Ohio of certain of the plaintiffs’ claims, including claims for compensatory damages, breach of contract, breach of the implied covenant of good faith and fair dealing and indemnification of costs. Plaintiffs voluntarily dismissed the surviving claims that AEGCo and I&M failed to exercise prudent utility practices with prejudice, and the court issued a final judgment. The plaintiffs subsequently filed an appeal in the U.S. Court of Appeals for the Sixth Circuit.

In 2017, the U.S. Court of Appeals for the Sixth Circuit issued an opinion and judgment affirming the district court’s dismissal of the owners’ breach of good faith and fair dealing claim as duplicative of the breach of contract claims, reversing the district court’s dismissal of the breach of contract claims and remanding the case for further proceedings.

Thereafter, AEP filed a motion with the U.S. District Court for the Southern District of Ohio in the original NSR litigation, seeking to modify the consent decree. The district court granted the owners’ unopposed motion to stay the lease litigation to afford time for resolution of AEP’s motion to modify the consent decree. The consent decree was modified based on an agreement among the parties in July 2019. The district court entered a stay that expired in February 2020. Settlement negotiations are continuing, and the parties filed a joint proposed case schedule in February 2020. See “Modification of the NSR Litigation Consent Decree” section below for additional information.

Management will continue to defend against the claims. Given that the district court dismissed plaintiffs’ claims seeking compensatory relief as premature, and that plaintiffs have yet to present a methodology for determining or any analysis supporting any alleged damages, management cannot determine a range of potential losses that is reasonably possible of occurring.

Patent Infringement Complaint

In July 2019, Midwest Energy Emissions Corporation and MES Inc. (collectively, the plaintiffs) filed a patent infringement complaint against various parties, including AEP Texas, AGR, Cardinal Operating Company and SWEPCo (collectively, the AEP Defendants). The complaint alleges that the AEP Defendants infringed two patents owned by the plaintiffs by using specific processes for mercury control at certain coal-fired generating stations. The complaint seeks injunctive relief and damages. Management will continue to defend against the claims. Management is unable to determine a range of potential losses that is reasonably possible of occurring.

Claims Challenging Transition of American Electric Power System Retirement Plan to Cash Balance Formula

The American Electric Power System Retirement Plan (the Plan) has received a letter written on behalf of four participants (the Claimants) making a claim for additional plan benefits and purporting to advance such claims on behalf of a class. When the Plan’s benefit formula was changed in the year 2000, AEP provided a special provision for employees hired before January 1, 2001, allowing them to continue benefit accruals under the then benefit formula for a full 10 years alongside of the new cash balance benefit formula then being implemented. Employees who were hired on or after January 1, 2001 accrued benefits only under the new cash balance benefit formula. The Claimants have asserted claims that (a) the Plan violates the requirements under the Employee Retirement Income Security Act (ERISA) intended to preclude back-loading the accrual of benefits to the end of a participant’s career; (b) the Plan violates the age discrimination prohibitions of ERISA and the Age Discrimination in Employment Act (ADEA); and (c) the company failed to provide required notice regarding the changes to the Plan. AEP has responded to the Claimants

providing a reasoned explanation for why each of their claims have been denied, and offering an opportunity to appeal those determinations. Management will continue to defend against the claims. Management is unable to determine a range of potential losses that are reasonably possible of occurring.

ENVIRONMENTAL ISSUES

AEP has a substantial capital investment program and incurs additional operational costs to comply with environmental control requirements. Additional investments and operational changes will be made in response to existing and anticipated requirements to reduce emissions from fossil generation, rules governing the beneficial use and disposal of coal combustion by-products, clean water rules and renewal permits for certain water discharges.

AEP is engaged in litigation about environmental issues, was notified of potential responsibility for the clean-up of contaminated sites and incurred costs for disposal of SNF and future decommissioning of the nuclear units. AEP, along with other parties, challenged some of the Federal EPA requirements. Management is engaged in the development of possible future requirements including the items discussed below. Management believes that further analysis and better coordination of these environmental requirements would facilitate planning and lower overall compliance costs while achieving the same environmental goals.

AEP will seek recovery of expenditures for pollution control technologies and associated costs from customers through rates in regulated jurisdictions. Environmental rules could result in accelerated depreciation, impairment of assets or regulatory disallowances. If AEP cannot recover the costs of environmental compliance, it would reduce future net income and cash flows and impact financial condition.

Environmental Controls Impact on the Generating Fleet

The rules and proposed environmental controls discussed below will have a material impact on AEP System generating units. Management continues to evaluate the impact of these rules, project scope and technology available to achieve compliance. As of December 31, 2019, the AEP System had generating capacity of approximately 25,500 MWs, of which approximately 13,200 MWs were coal-fired. Management continues to refine the cost estimates of complying with these rules and other impacts of the environmental proposals on fossil generation. Based upon management estimates, AEP’s future investment to meet these existing and proposed requirements ranges from approximately $500 million to $1 billion through 2026.

The cost estimates will change depending on the timing of implementation and whether the Federal EPA provides flexibility in finalizing proposed rules or revising certain existing requirements. The cost estimates will also change based on: (a) potential state rules that impose more stringent standards, (b) additional rulemaking activities in response to court decisions, (c) actual performance of the pollution control technologies installed, (d) changes in costs for new pollution controls, (e) new generating technology developments, (f) total MWs of capacity retired and replaced, including the type and amount of such replacement capacity and (g) other factors. In addition, management continues to evaluate the economic feasibility of environmental investments on regulated and competitive plants.

The table below represents the net book value before cost of removal, including related materials and supplies inventory, of plants or units of plants previously retired that have a remaining net book value as of December 31, 2019.

|

| | | | | | | | | |

| | | | | Generating | | Amounts Pending |

| Company | | Plant Name and Unit | | Capacity | | Regulatory Approval |

| | | | | (in MWs) | | (in millions) |

| APCo (a) | | Kanawha River Plant | | 400 |

| | $ | 14.1 |

|

| APCo (b) | | Clinch River Plant | | 705 |

| | 25.5 |

|

| APCo (a) | | Sporn Plant, Units 1 and 3 | | 300 |

| | 2.0 |

|

| APCo (a) | | Glen Lyn Plant | | 335 |

| | 3.5 |

|

| SWEPCo (c) | | Welsh Plant, Unit 2 | | 528 |

| | 35.5 |

|

| Total | | | | 2,268 |

| | $ | 80.6 |

|

| |

| (a) | Remaining amounts pending regulatory approval represent the FERC and the West Virginia jurisdictional share. Management expensed the Virginia jurisdictional share in December 2019. See “Virginia Legislation Affecting Earnings Reviews” section of Note 4 for additional information. |

| |

| (b) | APCo obtained permits following the Virginia SCC’s and WVPSC’s approval to convert Clinch River Plant, Units 1 and 2 to natural gas. In 2015, APCo retired the coal-related assets of Clinch River Plant, Units 1 and 2. Clinch River Plant, Units 1 and 2 began operations as natural gas units in 2016. |

| |

| (c) | Remaining amount pending regulatory approval represents the FERC and Louisiana jurisdictional share. The APSC issued an order in December 2019 approving the recovery of the $15 million Arkansas jurisdictional share. See “2019 Arkansas Base Rate Case” section of Note 4 for additional information. |

Management is seeking or will seek recovery of the remaining net book value in future rate proceedings. To the extent the net book value of these generation assets is not recoverable, it could materially reduce future net income and cash flows and impact financial condition.

Modification of the New Source Review Litigation Consent Decree

In 2007, the U.S. District Court for the Southern District of Ohio approved a consent decree between AEP subsidiaries in the eastern area of the AEP System and the Department of Justice, the Federal EPA, eight northeastern states and other interested parties to settle claims that the AEP subsidiaries violated the NSR provisions of the CAA when they undertook various equipment repair and replacement projects over a period of nearly 20 years. The consent decree’s terms include installation of environmental control equipment on certain generating units, a declining cap on SO2 and NOx emissions from the AEP System and various mitigation projects.

In 2017, AEP filed a motion with the district court seeking to modify the consent decree to eliminate an obligation to install future controls at Rockport Plant, Unit 2 if AEP does not acquire ownership of that unit, and to modify the consent decree in other respects to preserve the environmental benefits of the consent decree. The other parties to the consent decree opposed AEP’s motion. The district court granted AEP’s request to delay the deadline to install Selective Catalytic Reduction technology at Rockport Plant, Unit 2 until June 2020.

In May 2019, the parties filed a proposed order to modify the consent decree. The proposed order requires AEP to enhance the dry sorbent injection system on both units at the Rockport Plant by the end of 2020, and meet 30-day rolling average emission rates for SO2 and NOx at the combined stack for the Rockport Plant beginning in 2021. Total SO2 emissions from the Rockport Plant are limited to 10,000 tons per year beginning in 2021 and reduce to 5,000 tons per year when Rockport Plant, Unit 1 retires in 2028. The proposed modification was approved by the district court and became effective in July 2019. As part of the modification to the consent decree, I&M agreed to provide an additional $7.5 million to citizens’ groups and the states for environmental mitigation projects. As joint owners in the Rockport Plant, the $7.5 million payment was shared between AEGCo and I&M based on the joint ownership agreement.

Clean Air Act Requirements

The CAA establishes a comprehensive program to protect and improve the nation’s air quality and control sources of air emissions. The states implement and administer many of these programs and could impose additional or more stringent requirements. The primary regulatory programs that continue to drive investments in AEP’s existing

generating units include: (a) periodic revisions to NAAQS and the development of SIPs to achieve any more stringent standards, (b) implementation of the regional haze program by the states and the Federal EPA, (c) regulation of hazardous air pollutant emissions under MATS, (d) implementation and review of CSAPR and (e) the Federal EPA’s regulation of greenhouse gas emissions from fossil generation under Section 111 of the CAA. Notable developments in significant CAA regulatory requirements affecting AEP’s operations are discussed in the following sections.

National Ambient Air Quality Standards

The Federal EPA issued new, more stringent NAAQS for PM in 2012 and ozone in 2015. The Federal EPA is currently reviewing both of these standards. The existing standards for NO2 and SO2 were retained after review by the Federal EPA in 2018 and 2019, respectively. Implementation of these standards is underway.

The Federal EPA finalized non-attainment designations for the 2015 ozone standard in 2018. The Federal EPA confirmed that for states included in the CSAPR program, there are no additional interstate transport obligations, as all areas of the country are expected to attain the 2008 ozone standard before 2023. Challenges to the 2015 ozone standard and the Federal EPA’s determination that CSAPR satisfies certain states’ interstate transport obligations were filed in the U.S. Court of Appeals for the District of Columbia Circuit. In August 2019, the court upheld the 2015 primary ozone standard, but remanded the secondary welfare-based standard for further review. The court vacated the Federal EPA’s determination that CSAPR fulfilled the states’ interstate transport obligations, because the Federal EPA’s modeling analysis did not demonstrate that all significant contributions would be eliminated by the attainment deadlines for downwind states. Any further changes will require additional rulemaking. Management cannot currently predict the nature, stringency or timing of additional requirements for AEP’s facilities based on the outcome of these activities.

Regional Haze

The Federal EPA issued a Clean Air Visibility Rule (CAVR), detailing how the CAA’s requirement that certain facilities install best available retrofit technology (BART) would address regional haze in federal parks and other protected areas. BART requirements apply to power plants. CAVR will be implemented through SIPs or FIPs. In 2017, the Federal EPA revised the rules governing submission of SIPs to implement the visibility programs, including a provision that postpones the due date for the next comprehensive SIP revisions until 2021. Petitions for review of the final rule revisions have been filed in the U.S. Court of Appeals for the District of Columbia Circuit.

The Federal EPA initially disapproved portions of the Arkansas regional haze SIP, but has approved a revised SIP and all of SWEPCo's affected units are in compliance with the relevant requirements.

The Federal EPA also disapproved portions of the Texas regional haze SIP. In 2017, the Federal EPA finalized a FIP that allows participation in the CSAPR ozone season program to satisfy the NOx regional haze obligations for electric generating units in Texas. Additionally, the Federal EPA finalized an intrastate SO2 emissions trading program based on CSAPR allowance allocations. A challenge to the FIP was filed in the U.S. Court of Appeals for the Fifth Circuit and the case is pending the Federal EPA’s reconsideration of the final rule. In August 2018, the Federal EPA proposed to affirm its 2017 FIP approval. In November 2019, in response to comment, the Federal EPA proposed revisions to the intrastate trading program. Management supports the intrastate trading program as a compliance alternative to source-specific controls.

Cross-State Air Pollution Rule

In 2011, the Federal EPA issued CSAPR as a replacement for the Clean Air Interstate Rule, a regional trading program designed to address interstate transport of emissions that contributed significantly to downwind non-attainment with the 1997 ozone and PM NAAQS. CSAPR relies on SO2 and NOx allowances and individual state budgets to compel further emission reductions from electric utility generating units. Interstate trading of allowances is allowed on a restricted sub-regional basis.

Petitions to review the CSAPR were filed in the U.S. Court of Appeals for the District of Columbia Circuit. In 2015, the court found that the Federal EPA over-controlled the SO2 and/or NOx budgets of 14 states. The court remanded the rule to the Federal EPA for revision consistent with the court’s opinion while CSAPR remained in place.

In 2016, the Federal EPA issued a final rule, the CSAPR Update, to address the remand and to incorporate additional changes necessary to address the 2008 ozone standard. The CSAPR Update significantly reduced ozone season budgets in many states and discounted the value of banked CSAPR ozone season allowances beginning with the 2017 ozone season. In 2019, the appeals court remanded the CSAPR Update to the Federal EPA because it determined the Federal EPA had not properly considered the attainment dates for downwind areas in establishing its partial remedy, and should have considered whether there were available measures to control emissions from sources other than generating units. Any further changes to the CSAPR rule will require additional rulemaking.

Mercury and Other Hazardous Air Pollutants (HAPs) Regulation

In 2012, the Federal EPA issued a rule addressing a broad range of HAPs from coal and oil-fired power plants. The rule established unit-specific emission rates for units burning coal on a 30-day rolling average basis for mercury, PM (as a surrogate for particles of non-mercury metals) and hydrogen chloride (as a surrogate for acid gases). In addition, the rule proposed work practice standards for controlling emissions of organic HAPs and dioxin/furans, with compliance required within three years. Management obtained administrative extensions for up to one year at several units to facilitate the installation of controls or to avoid a serious reliability problem.

In 2014, the U.S. Court of Appeals for the District of Columbia Circuit denied all of the petitions for review of the 2012 final rule. Various intervenors filed petitions for further review in the U.S. Supreme Court.

In 2015, the U.S. Supreme Court reversed the decision of the U.S. Court of Appeals for the District of Columbia Circuit. The court remanded the MATS rule to the Federal EPA to consider costs in determining whether to regulate emissions of HAPs from power plants. In 2016, the Federal EPA issued a supplemental finding concluding that, after considering the costs of compliance, it was appropriate and necessary to regulate HAP emissions from coal and oil-fired units. Petitions for review of the Federal EPA’s determination were filed in the U.S. Court of Appeals for the District of Columbia Circuit. In 2018, the Federal EPA released a revised finding that the costs of reducing HAP emissions to the level in the current rule exceed the benefits of those HAP emission reductions. The Federal EPA also determined that there are no significant changes in control technologies and the remaining risks associated with HAP emissions do not justify any more stringent standards. Therefore, the Federal EPA proposed to retain the current MATS standards without change.

Climate Change, CO2 Regulation and Energy Policy

In 2015, the Federal EPA published the final CO2 emissions standards for new, modified and reconstructed fossil generating units, and final guidelines for the development of state plans to regulate CO2 emissions from existing sources, known as the Clean Power Plan (CPP).

In 2016, the U.S. Supreme Court issued a stay of the final CPP, including all of the deadlines for submission of initial or final state plans until a final decision is issued by the U.S. Court of Appeals for the District of Columbia Circuit and the U.S. Supreme Court considers any petition for review. In 2017, the President issued an Executive Order directing the Federal EPA to reconsider the CPP and the associated standards for new sources. The Federal EPA filed a motion to hold the challenges to the CPP in abeyance pending reconsideration. In September 2019, following the Federal EPA’s repeal of the CPP and promulgation of a replacement rule, the Court of Appeals for the District of Columbia Circuit dismissed the challenges.

In July 2019, the Federal EPA finalized the Affordable Clean Energy (ACE) rule to replace the CPP with new emission guidelines for regulating CO2 from existing sources. ACE establishes a framework for states to adopt standards of performance for utility boilers based on heat rate improvements for such boilers. The final rule applies to generating units that commenced construction prior to January 2014, generate greater than 25 MWs, have a baseload rating above 250 MMBtu per hour and burn coal for more than 10% of the annual average heat input over the preceding three calendar years, with certain exceptions. States must establish standards of performance for each affected facility in terms of pounds of CO2 emitted per MWh, based on certain heat rate improvement measures and the degree of emission reduction achievable through each applicable measure, together with consideration of certain site-specific factors and the unit’s remaining useful life. State plans are required to be submitted in 2022, and the Federal EPA has up to two

years to review and approve a plan or disapprove it and adopt a federal plan. The final ACE rule has been challenged in the courts.

In 2018, the Federal EPA filed a proposed rule revising the standards for new sources and determined that partial carbon capture and storage is not the best system of emission reduction because it is not available throughout the U.S. and is not cost-effective. Management continues to actively monitor these rulemaking activities.

AEP has taken action to reduce and offset CO2 emissions from its generating fleet. AEP expects CO2 emissions from its operations to continue to decline due to the retirement of some of its coal-fired generation units, and actions taken to diversify the generation fleet and increase energy efficiency where there is regulatory support for such activities. The majority of the states where AEP has generating facilities passed legislation establishing renewable energy, alternative energy and/or energy efficiency requirements that can assist in reducing carbon emissions. Management is taking steps to comply with these requirements, including increasing wind and solar installations, purchasing renewable power and broadening AEP System’s portfolio of energy efficiency programs.

In September 2019, AEP announced new intermediate and long-term CO2 emission reduction goals, based on the output of the company’s integrated resource plans, which take into account economics, customer demand, grid reliability and resiliency, regulations and the company’s current business strategy. The intermediate goal is a 70% reduction from 2000 CO2 emission levels from AEP generating facilities by 2030; the long-term goal is to surpass an 80% reduction of CO2 emissions from AEP generating facilities from 2000 levels by 2050. AEP’s total estimated CO2 emissions in 2019 were approximately 58 million metric tons, a 65% reduction from AEP’s 2000 CO2 emissions. AEP has made significant progress in reducing CO2 emissions from its power generation fleet and expects its emissions to continue to decline. AEP’s aspirational emissions goal is zero CO2 emissions by 2050. Technological advances, including energy storage, will determine how quickly AEP can achieve zero emissions while continuing to provide reliable, affordable power for customers.

Federal and state legislation or regulations that mandate limits on the emission of CO2 could result in significant increases in capital expenditures and operating costs, which in turn, could lead to increased liquidity needs and higher financing costs. Excessive costs to comply with future legislation or regulations might force AEP to close some coal-fired facilities, which could possibly lead to impairment of assets.

Coal Combustion Residual (CCR) Rule