Fulton Financial Corporation

Investor Presentation

May 2009

(Data as of March 31, 2009)

The following presentation may contain forward-looking statements about Fulton Financial Corporation’s

financial condition, business, strategies, products and services. Forward-looking statements are encouraged

by the Private Securities Litigation Reform Act of 1995. Such forward-looking statements reflect the

Corporation’s current views and expectations based largely on information currently available to its

management, and on its current expectations, assumptions, plan, estimates, judgments, and projections about

its business and its industry, and they involve inherent risks, contingencies, uncertainties and other factors.

Although the Corporation believes that these forward-looking statements are based on reasonable estimates

and assumptions, the Corporation is unable to provide any assurance that its expectations will, in fact, occur

or that its estimates or assumptions will be correct and actual results could differ materially from those

expressed or implied by such forward-looking statements and such statements are not guarantees of future

performance. The Corporation undertakes no obligation to update or revise any forward-looking statements.

Accordingly, investors and others are cautioned not to place undue reliance on such forward-looking statements.

Many factors could affect future financial results including, without limitation, acquisition and growth

strategies; market risk; changes or adverse developments in economic, political or regulatory conditions; a

continuation or worsening of the current disruption in credit and other markets, including the lack of or

reduced access to, and the abnormal functioning of markets for mortgage and other asset-backed securities

and for commercial paper and other short-term borrowings; the effect of competition and interest rates on net

interest margin and net interest income; investment strategy and income growth; investment securities gains;

declines in the value of securities which may result in charges to earnings; changes in rates of deposit and

loan growth; asset quality and the impact on assets from adverse changes in the economy and in credit and

other markets and resulting effects on credit risk and asset values; balances of risk-sensitive assets to risk-

sensitive liabilities; salaries and employee benefits and other expenses; amortization of intangible assets;

goodwill impairment; capital and liquidity strategies; and other financial and business matters for future periods.

For a more complete discussion of certain risks and uncertainties affecting the Corporation, please see the

sections entitled “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and

Results of Operations” set forth in the Corporation’s filings with the Securities and Exchange Commission.

Forward-Looking Statement

Presentation Outline

Corporate Overview

Franchise and Markets

Capital

Credit

First Quarter Performance

Summary

Fulton Financial Profile

Mid-Atlantic regional financial holding company

A family of 10 community banks in 5 states

Fulton Financial Advisors

Fulton Mortgage Company

268 community banking offices

Asset size: $ 16.5 billion

3900 Team Members

Market capitalization: $ 1.2 billion

Book value per common share: $ 8.50

Tangible book value per common share: $ 5.33

Shares outstanding: 175 million

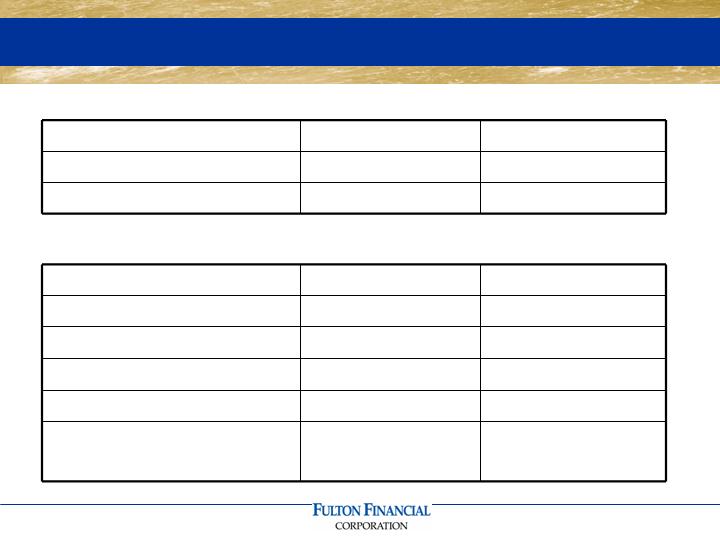

Capital

With CPP

Without CPP

GAAP Capital

$1.86 billion

$1.48 billion

Total Risk-Based Capital

$1.85 billion

$1.48 billion

Ratios:

With CPP

Without CPP

Total Risk-Based Capital

14.00%

11.10%

Tier 1 Risk-Based Capital

11.20%

8.40%

Leverage Capital

9.50%

7.10%

Tangible Common Equity

5.90%

5.90%

Tangible Common Equity

to Risk-Weighted Assets

7.00%

7.00%

Superior Customer Experience

Care, Listen, Understand and Deliver

Superior Customer Satisfaction

*Retail:

90% extremely/very satisfied

Commercial:

90% extremely/very satisfied

*Compared to national average of 63%

Source: American Banker/Gallup Consumer Survey

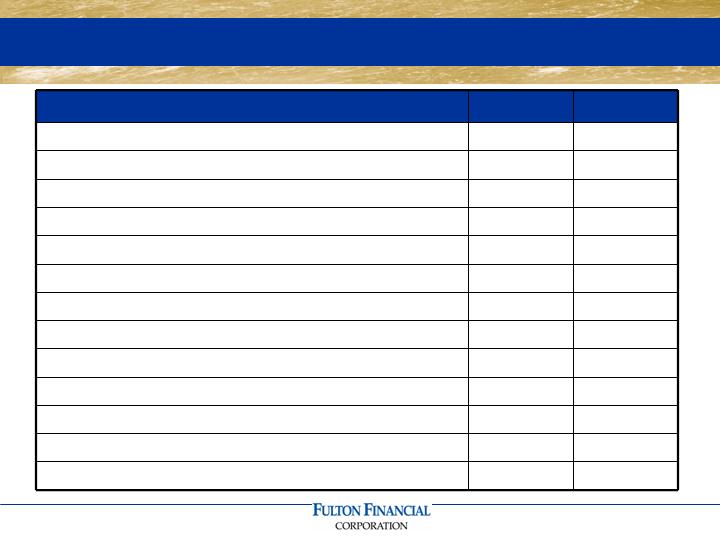

Customers’ satisfaction with FFC

Attribute

Q4/2007

Q4/2008

Employees are friendly and helpful

9.6

9.6

Bank seems easy to work with

9.5

9.6

Employees are knowledgeable

9.3

9.4

Wait times are brief

9.2

9.3

Wide range of products and services

9.1

9.3

Listens to my needs

9.1

9.3

Convenient branches and ATMs

9.1

9.0

Resolves problems quickly

8.7

9.2

Offers ability to conduct transactions on Internet

7.9

8.7

Fees are generally low

7.8

8.5

Competitive interest rates

7.8

8.4

Bank is involved in the community

7.7

8.5

Meeting the branch manager

6.8

8.5

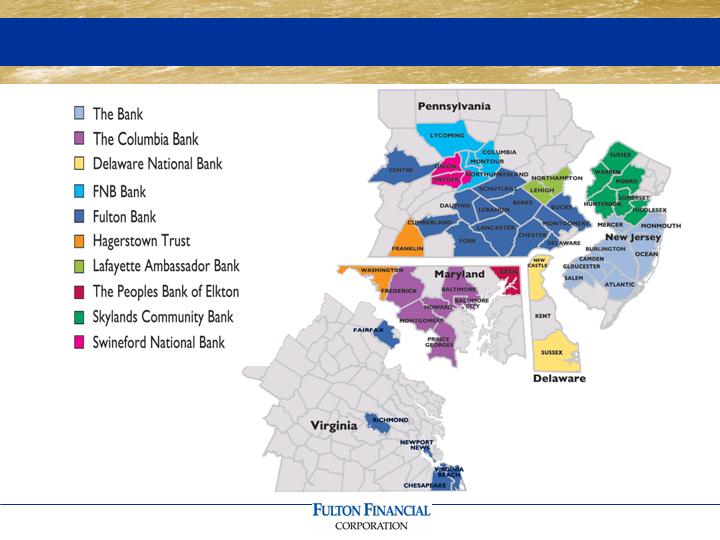

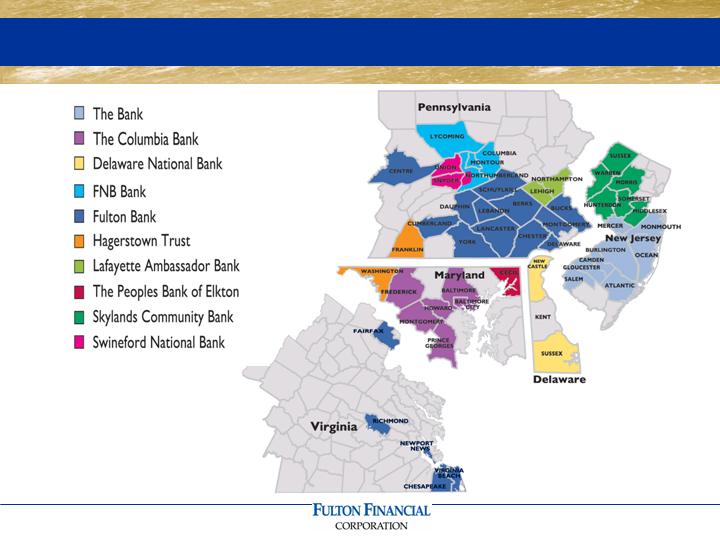

A Valuable Geographic Franchise

*Source: SNL, Median HH Income, 2008 data

Serving PA’s Strongest Markets*

County

Rank

#

Branches

Projected Population

Change 2008-2013 (%)

Median HH

Income 2008 ($)

Projected HH

Income Change

2008-2013 (%)

Chester, PA

1

7

7.96

87,480

22.46

Montgomery, PA

2

3

2.34

79,875

22.45

Bucks, PA

3

5

3.78

79,610

22.28

Delaware, PA

4

1

0.70

66,587

17.73

Cumberland, PA

5

3

4.81

61,897

13.45

Northampton, PA

6

3

7.38

60,429

13.16

Lancaster, PA

8

27

4.08

59,151

12.98

Lehigh, PA

9

3

6.17

59,036

14.67

York, PA

10

15

7.74

58,782

12.58

Berks, PA

11

9

4.74

58,222

12.93

Average

4.97

67,107

16.47

Average of all

other (57)

0.80

44,312

15.54

FFC Affiliates in Affluent Markets*

*Source: SNL Financial, 2008

County

#

Branches

National

Ranking

Ranking in

State

Median HH

Ranking

Hunterdon, NJ

3

#3

#1

$109,245

Morris, NJ

6

#7

#2

$103,406

Somerset, NJ

7

#8

#3

$102,548

Howard, MD

9

#9

#1

$101,251

Montgomery, MD

3

#22

#2

$91,571

Loan Distribution by State (First Quarter)

Average

% of

09 v. 08

%

Balance

Total

Growth

Growth

(dollars in thousands)

Pennsylvania

6,466,000

$

53.7%

440,000

$

7%

New Jersey

2,496,000

20.7%

186,000

8%

Maryland

1,592,000

13.2%

30,000

2%

Virginia

1,140,000

9.5%

74,000

7%

Delaware

347,000

2.9%

16,000

5%

12,041,000

$

Residential Mortgage and HE Loans

Q1 2009

% of

Avg. Bal.

Total

Pennsylvania

1,375,000

$

51.8%

Maryland

459,000

17.3%

New Jersey

459,000

17.3%

Virginia

204,000

7.7%

Delaware

159,000

6.0%

2,656,000

$

(dollars in thousands)

Commercial Loans by Industry

Industry

%

Services

17.3

Manufacturing

13.4

RE - Rental and Leasing

12.4

Construction

11.2

Agriculture

8.8

Retail

8.8

Wholesale

8.5

Other

6.1

Health Care

5.9

Financial Services

3.1

Transportation

2.4

Arts and Entertainment

2.1

100.0

Commercial Loans by State

Q1 2009

% of

Avg. Bal.

Total

Pennsylvania

2,354,000

$

63.9%

Maryland

444,000

12.1%

New Jersey

548,000

14.9%

Virginia

306,000

8.3%

Delaware

30,000

0.8%

3,682,000

$

(dollars in thousands)

Construction Loans by State (March 31, 2009)

Ending

% of

NPL

Specific

Balance

Total

Balance

Allocations

(dollars in thousands)

Pennsylvania

330,000

$

27.4%

3,910

$

2,170

$

Maryland

322,000

26.7%

39,760

17,890

New Jersey

242,000

20.1%

20,180

4,660

Virginia

295,000

24.5%

29,570

7,220

Delaware

17,000

1.4%

-

130

1,206,000

$

93,420

$

32,070

$

CRE Loans by State (March 31, 2009)

Ending

% of

NPL

Specific

Balance

Total

Balance

Allocations

(dollars in thousands)

Pennsylvania

2,084,000

$

51.2%

21,110

$

9,170

$

New Jersey

1,183,000

29.1%

23,490

4,160

Maryland

345,000

8.5%

9,850

450

Virginia

328,000

8.1%

4,040

1,120

Delaware

128,000

3.1%

1,410

1,430

4,068,000

$

59,900

$

16,330

$

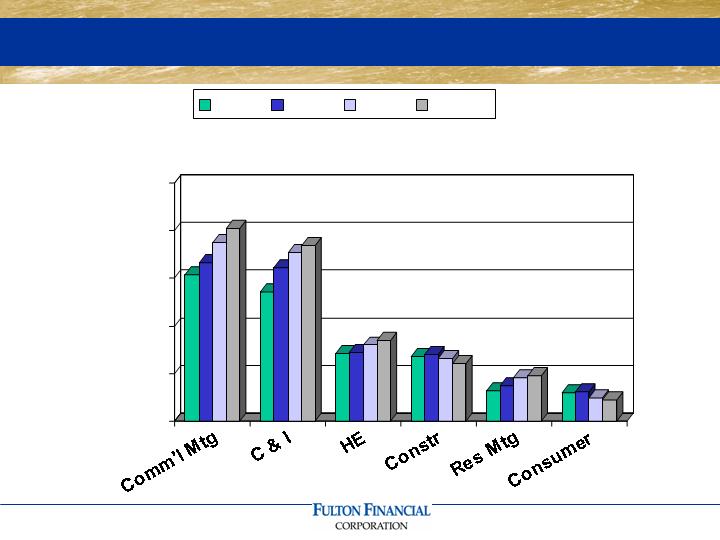

Loan Delinquency (Key Sectors)

Category

Total (%)

3/31/08

90-Days

3/31/08

Total (%)

3/31/09

90-Days

3/31/09

Commercial

Loans

1.48

.99

2.26

1.59

Consumer

Direct

.77

.33

1.27

0.54

Commercial

Mortgage

1.38

.83

1.88

1.27

Residential

Mortgage

5.49

3.14

6.88

3.20

Construction

3.30

2.05

8.78

7.65

Total

Portfolio

1.87

1.13

3.00

2.04

Net Charge-offs (Q1 2009)

Comm'l

Res. Mtg.

Comm'l

Mortgage

Constr.

and HE

Other

Total

(in thousands)

Pennsylvania

336

$

420

$

2,444

$

2,103

$

545

$

5,848

$

Maryland

209

1,880

7,406

451

108

10,054

New Jersey

2,333

1,067

696

186

317

4,599

Virginia

6,782

-

1,584

218

22

8,606

Delaware

58

583

-

296

30

967

9,718

$

3,950

$

12,130

$

3,254

$

1,022

$

30,074

$

Avg Loans

3,682,000

4,049,000

1,204,000

2,656,000

450,000

12,041,000

NCO %

1.06%

0.39%

4.03%

0.49%

0.91%

1.00%

Non-performing Loans* (March 31, 2009)

Comm'l

Res. Mtg.

Comm'l

Mortgage

Constr.

and HE

Other

Total

(in thousands)

Pennsylvania

19,272

$

21,107

$

3,907

$

5,902

$

3,984

$

54,172

$

Maryland

4,297

9,853

39,764

3,076

1,422

58,412

New Jersey

15,374

23,490

20,183

4,277

2,496

65,820

Virginia

11,214

4,037

29,571

16,465

1,569

62,856

Delaware

336

1,412

-

1,645

1,396

4,789

50,493

$

59,899

$

93,425

$

31,365

$

10,867

$

246,049

$

End Loans

3,654,000

4,068,000

1,205,000

2,622,000

461,000

12,010,000

NPL%

1.38%

1.47%

7.75%

1.20%

2.36%

2.05%

* Includes accruing loans > 90 days past due.

52 relationships with commitments to lend

of $20 million or more

Maximum individual commitment- $33

million

Maximum commitment land development-

$28 million

Average commercial lending relationship

size is $440,953

Loans and corresponding relationships are

within Fulton’s geographic market area

Summary of Larger Loans

Overview of First Quarter

Strong deposit growth

Robust residential mortgage activity

Good growth in other income

Reduced reliance on wholesale

funding

Improved efficiency

Controllable expenses flat

Loan portfolio challenges

Margin compression

Financial Performance

2009 Financial Results (First Quarter)

2009

2008

Net income

13,080,000

$

41,500,000

$

Cost of preferred stock

(5,030,000)

-

Net income available

to common shareholders

8,050,000

$

41,500,000

$

Earnings per share

0.05

$

0.24

$

Return on tangible equity

3.88%

18.45%

Income Statement Summary (First Quarter)

2009

2008

$

%

(dollars in thousands)

Net Interest Income

124,120

$

125,900

$

(1,780)

$

-1%

Loan Loss Provision

(50,000)

(11,220)

(38,780)

346%

Other Income

44,000

36,430

7,570

21%

Securities Gains

2,920

1,250

1,670

134%

Other Expenses

(106,390)

(96,660)

(9,730)

10%

Pre-Tax Income

14,650

55,700

(41,050)

-74%

Income Taxes

(1,570)

(14,200)

12,630

-89%

Net Income

13,080

$

41,500

$

(28,420)

$

-68%

Income Summary Proforma (First Quarter)

2009

2008

$

%

(dollars in thousands)

Pre-tax Income

14,650

$

55,700

$

(41,050)

$

-74%

Loan Loss Provision

50,000

11,220

38,780

346%

Security Gains

(2,920)

(1,250)

(1,670)

134%

ARC Charges

6,160

-

6,160

-

Proforma

67,890

65,670

2,220

3%

International Bancshares Corporation

Old National Bancorp

South Financial Group, Inc.

Susquehanna Bancshares, Inc.

TCF Financial Corporation

Trustmark Corporation

UMB Financial Corporation

United Bankshares, Inc.

Valley National Bancorp

Whitney Holding Corporation

Wilmington Trust Corporation

Associated Banc-Corp

BancorpSouth, Inc.

Bank of Hawaii Corporation

BOK Financial Corporation

Citizens Republic Bancorp

City National Corporation

Colonial BancGroup, Inc.

Commerce Bancshares, Inc.

Cullen/Frost Bankers, Inc.

First Citizens BancShares, Inc.

First Midwest Bancorp, Inc.

First Merit Corporation

Peer Group

Net Interest Margin

3.45

3.45

3.15

3.00

3.50

4.00

4.50

5.00

FFC

Peer

Top 50

Average Loans

$0.0

$1.0

$2.0

$3.0

$4.0

$5.0

Billions

2006

2007

2008

Q1 09

Average Deposits

$0.0

$1.0

$2.0

$3.0

$4.0

$5.0

$6.0

Billions

2006

2007

2008

Q1 09

Other Income

$0

$20

$40

$60

$80

$100

$120

$140

$160

Millions

Other Income (First Quarter)

2009

2008

$

%

(dollars in thousands)

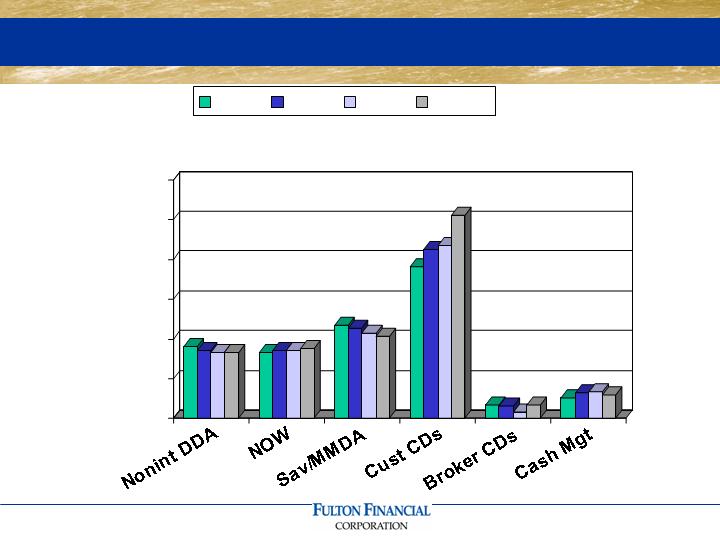

Mort. Sales Gains

8,590

$

2,310

$

6,280

$

272%

Overdraft & NSF Fees

8,440

7,690

750

10%

Invt Mgt & Trust

7,900

8,760

(860)

-10%

Service Charges

3,250

3,040

210

7%

Cash Mgt Fees

3,200

3,230

(30)

-1%

Success Card Fees

2,440

2,260

180

8%

Credit Card Fees

1,190

-

1,190

N/A

Other

8,990

9,140

(150)

-2%

Total

44,000

$

36,430

$

7,570

$

21%

Other Income (Linked Quarter)

Q1 09

Q4 08

$

%

(dollars in thousands)

Mort. Sales Gains

8,590

$

3,080

$

5,510

$

179%

Overdraft & NSF Fees

8,440

9,530

(1,090)

-11%

Invt Mgt & Trust

7,900

7,540

360

5%

Service Charges

3,250

3,300

(50)

-2%

Cash Mgt Fees

3,200

3,340

(140)

-4%

Success Card Fees

2,440

2,460

(20)

-1%

Credit Card Fees

1,190

1,150

40

N/A

Other

8,990

8,350

640

8%

Total

44,000

$

38,750

$

5,250

$

14%

Efficiency Ratio

61.0

62.1

62.1

50.0

52.0

54.0

56.0

58.0

60.0

62.0

64.0

93

94

95

96

97

98

99

00

01

02

03

04

05

06

07

08

3/09

FFC

Peer

Top 50

Other Expense (First Quarter)

2009

2008

$

%

(dollars in thousands)

Salaries & Benefits

55,320

$

55,200

$

120

$

0%

Occupancy & Equip.

14,100

13,970

130

1%

Operating Risk Loss

6,200

1,240

4,960

400%

Data Proc. & Software

4,630

4,660

(30)

-1%

FDIC Insurance

4,290

860

3,430

399%

Supplies & Postage

2,660

2,810

(150)

-5%

Marketing

2,570

2,910

(340)

-12%

Other Expenses

16,620

15,010

1,610

11%

Total

106,390

$

96,660

$

9,730

$

10%

Other Expense (Linked Quarter)

Q1 09

Q4 08

$

%

(dollars in thousands)

Salaries & Benefits

55,320

$

48,770

$

6,550

$

13%

Occupancy & Equip.

14,100

14,660

(560)

-4%

Operating Risk Loss

6,200

5,200

1,000

19%

Data Proc. & Software

4,630

4,740

(110)

-2%

FDIC Insurance

4,290

1,880

2,410

128%

Supplies & Postage

2,660

2,730

(70)

-3%

Marketing

2,570

3,750

(1,180)

-31%

Other Expenses

16,620

19,140

(2,520)

-13%

Total

106,390

$

100,870

$

5,520

$

5%

Allowance for Credit Losses

2009

2008

(dollars in thousands)

Beginning Balance

180,140

$

112,210

$

Loan Loss Provision

50,000

11,220

Net Charge-Offs

(30,080)

(4,360)

Ending Balance

200,060

$

119,070

$

Allowance to Loans

1.67%

1.05%

Nonperforming Assets to Assets

1.63%

0.90%

Net Charge-offs to Loans

1.00%

0.15%

Net Charge-Offs To Average Loans

1.00

0.94

1.40

0.00

0.30

0.60

0.90

1.20

1.50

91

92

93

94

95

96

97

98

99

00

01

02

03

04

05

06

07

08

3/09

FFC

Peer

Top 50

Investment Portfolio

ENDING

MODIFIED

BALANCE

DURATION

(in millions)

Agency mortgage-backed securities

1,120.5

$

4.38

Municipal bonds

513.3

4.15

Agency collateralized mortgage obligations

489.7

4.34

Auction rate securities

208.3

5.14

Corporate & trust preferred securities

152.0

9.98

U.S. Treasuries and agencies

87.8

2.28

FHLB & FRB stock

85.2

NA

Bank stocks

43.1

NA

Other investments

28.8

NA

Net unrealized loss

(3.9)

Total Investments

2,724.8

$

4.68

Status of the Corporation

Valuable geographic franchise

Positive market demographics

Strong capital

Deposit trends improving

Strong mortgage activity

Continued expense reduction

Positioned for economic rebound

Fulton Financial Corporation

One Penn Square

Lancaster, PA 17602

www.fult.com

Where are we located?