Fulton Financial

Corporation

-------------------------------------------------

October 2009

Corporate Presentation

Data as of September 30, 2009

The following presentation may contain forward-looking statements about Fulton Financial Corporation’s

financial condition, business, strategies, products and services. Forward-looking statements are encouraged

by the Private Securities Litigation Reform Act of 1995. Such forward-looking statements reflect the

Corporation’s current views and expectations based largely on information currently available to its

management, and on its current expectations, assumptions, plan, estimates, judgments, and projections about

its business and its industry, and they involve inherent risks, contingencies, uncertainties and other factors.

Although the Corporation believes that these forward-looking statements are based on reasonable estimates

and assumptions, the Corporation is unable to provide any assurance that its expectations will, in fact, occur

or that its estimates or assumptions will be correct and actual results could differ materially from those

expressed or implied by such forward-looking statements and such statements are not guarantees of future

performance. The Corporation undertakes no obligation to update or revise any forward-looking statements.

Accordingly, investors and others are cautioned not to place undue reliance on such forward-looking

statements.

Many factors could affect future financial results including, without limitation, acquisition and growth

strategies; market risk; changes or adverse developments in economic, political or regulatory conditions; a

continuation or worsening of the current disruption in credit and other markets, including the lack of or

reduced access to, and the abnormal functioning of markets for mortgage and other asset-backed securities

and for commercial paper and other short-term borrowings; the effect of competition and interest rates on net

interest margin and net interest income; investment strategy and income growth; investment securities gains;

declines in the value of securities which may result in charges to earnings; changes in rates of deposit and

loan growth; asset quality and the impact on assets from adverse changes in the economy and in credit and

other markets and resulting effects on credit risk and asset values; balances of risk-sensitive assets to risk-

sensitive liabilities; salaries and employee benefits and other expenses; amortization of intangible assets;

goodwill impairment; capital and liquidity strategies; and other financial and business matters for future

periods.

For a more complete discussion of certain risks and uncertainties affecting the Corporation, please see the

sections entitled “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and

Results of Operations” set forth in the Corporation’s filings with the Securities and Exchange Commission.

Forward-Looking Statement

Presentation Outline

Corporate Overview

Franchise and Markets

Customer Experience / Satisfaction

Capital

Credit

Third Quarter Performance

Summary

Fulton Financial Profile

Mid-Atlantic regional financial holding company

A family of 8 community banks in 5 states

Fulton Financial Advisors

Fulton Mortgage Company

270 community banking offices

Asset size: $ 16.5 billion

3850 Team Members

Market capitalization: $ 1.4 billion

Book value per common share: $ 8.82

Tangible book value per common share: $ 5.68

Shares outstanding: 176 million

*Source: SNL, Median HH Income, 2009 data

Serving PA’s Strongest Markets*

County

Rank

#

Branches

Projected Population

Change 2009-2014 (%)

Median HH

Income 2009 ($)

Projected HH

Income Change

2009-2014 (%)

Chester, PA

1

7

6.64

87,308

7.36

Montgomery, PA

2

3

1.85

80,212

5.01

Bucks, PA

3

6

2.22

79,444

4.95

Delaware, PA

4

1

0.10

66,300

5.25

Cumberland, PA

5

3

4.06

61,622

6.42

Northampton, PA

6

15

5.48

60,207

6.11

Lancaster, PA

8

28

3.46

59,484

5.61

York, PA

9

15

6.36

59,123

3.89

Berks, PA

10

9

3.73

58,885

4.18

Lehigh, PA

11

8

4.76

58,555

4.95

Average

3.87

67,114

5.37

Average of all

other (57)

-0.33

44,560

5.97

FFC Affiliates in Affluent Markets*

*Source: SNL Financial, 2009

County

# FFC

Branches

National

Ranking

Ranking in

State

Median HH

Income

Hunterdon, NJ

3

#3

#1

$110,147

Fairfax, VA

1

#4

#1

$109,067

Morris, NJ

6

#6

#2

$104,797

Somerset, NJ

7

#8

#3

$102,357

Howard, MD

12

#9

#1

$101,954

Unemployment Rates*

FFC Counties

Unemployment

Rate (%)**

State

Unemployment

Rate (%)***

United States

9.8

9.8

Delaware

7.7

8.2

Maryland

7.6

7.1

New Jersey

9.3

9.6

Pennsylvania

8.2

8.3

Virginia

6.8

6.6

*FFC Averages are an average of the unemployment

rates of the counties in which FFC has branches.

*Source: SNL & US Department of Labor

** County Data is as of August 2009

***State Data is as of September 2009

US Home Price Index*

*Source: Freddie Mac, Q2 2009 Data

Metropolitan Statistical Area

Annual Change

Q2 2008 - Q2 2009

# Branches

United States

-4.2

Average FFC Regions

-5.5

Harrisburg-Carlisle, PA

-1.4

12

Lebanon, PA

-0.9

9

York-Hanover, PA

-4.0

15

Lancaster, PA

-1.6

27

Philadelphia, PA

-3.3

16

Reading, PA

-3.6

9

Allentown-Bethlehem-Easton, PA

-5.7

24

Wilmington, DE-MD-NJ

-5.6

14

Camden, NJ

-6.3

27

Trenton-Ewing, NJ

-6.9

5

Edison, NJ

-5.8

20

Baltimore-Towson, MD

-8.6

13

Newark-Union, NJ-PA

-6.3

12

Hagerstown-Martinsburg, MD-WV

-13.2

11

Washington-Arlington-Alexandria, DC-VA

-8.5

10

Our Brand

COMMUNITY BANKING

SMALL BUSINESS

HIGH NET WORTH

RETAIL BANKING

LISTENING IS JUST THE BEGINNING.

Superior Customer Satisfaction

*Retail:

90% extremely/very satisfied

Commercial:

90% extremely/very satisfied

*Compared to national average of 63%

Source: American Banker/Gallup Consumer Survey

Customer Satisfaction Metrics

Attribute

Q1/2008

Q1/2009

Employees are friendly and helpful

9.6

9.6

Bank seems easy to work with

9.5

9.5

Safety and security of a local bank

NA

9.3

Wait times are brief

9.1

9.3

Wide range of products and services

9.0

9.1

Listens to my needs

9.1

9.1

Convenient branches and ATMs

8.9

8.8

Resolves problems quickly

8.8

9.1

Offers ability to conduct transactions on Internet

8.2

8.4

Fees are generally low

8.0

8.3

Competitive interest rates

8.1

8.8

Bank is involved in the community

7.9

8.4

Capital (9/30/09 Est.)

With CPP

Without CPP

GAAP Capital

$1.92 billion

$1.55 billion

Total Risk-Based Capital

$1.89 billion

$1.51 billion

Ratios:

With CPP

Without CPP

Total Risk-Based Capital

13.90%

11.10%

Tier 1 Risk-Based Capital

11.20%

8.40%

Leverage Capital

9.50%

7.10%

Tangible Common Equity

6.26%

6.26%

Tangible Common Equity

to Risk-Weighted Assets

7.50%

7.50%

Loan Distribution by State (Third Quarter)

Average

% of

09 v. 08

%

Balance

Total

Growth

Growth

(dollars in thousands)

Pennsylvania

6,442,000

$

54.1%

225,000

$

4%

New Jersey

2,481,000

20.8%

79,000

3%

Maryland

1,529,000

12.8%

(62,000)

-4%

Virginia

1,122,000

9.4%

(22,000)

-2%

Delaware

340,000

2.9%

(3,000)

-1%

11,914,000

$

Residential Mortgage and HE Loans

Q3 2009

% of

Avg. Bal.

Total

Pennsylvania

1,313,000

$

50.8%

New Jersey

453,000

17.5%

Maryland

452,000

17.5%

Virginia

213,000

8.2%

Delaware

154,000

6.0%

2,585,000

$

(dollars in thousands)

Commercial Loans by Industry

Industry

%

Services

18.8

Manufacturing

13.7

RE - Rental and Leasing

12.4

Construction

11.2

Agriculture

8.6

Retail

8.1

Wholesale

7.3

Other

5.8

Health Care

5.7

Financial Services

3.1

Arts and Entertainment

3.0

Transportation

2.3

100.0

Commercial Loans by State

Q3 2009

% of

Avg. Bal.

Total

(dollars in thousands)

Pennsylvania

2,380,000

$

64.9%

New Jersey

556,000

15.2%

Maryland

400,000

10.9%

Virginia

302,000

8.2%

Delaware

30,000

0.8%

3,668,000

$

Construction Loans (September 30, 2009)

Ending

% of

NPL

Specific

Balance

Total

Balance

Allocations

(dollars in thousands)

Pennsylvania

285,000

$

27.7%

14,800

$

2,860

$

Virginia

266,000

25.9%

23,950

9,300

Maryland

260,000

25.3%

47,120

21,360

New Jersey

202,000

19.6%

18,920

3,640

Delaware

16,000

1.6%

-

130

1,029,000

$

104,790

$

37,290

$

Construction Loans by Type

Ending

% of

Balance

Total

(dollars in thousands)

Commercial Residential

690,000

$

67.0%

Commercial

260,000

25.3%

Real Estate

63,000

6.1%

Other Commercial

16,000

1.6%

1,029,000

$

CRE Loans by State (September 30, 2009)

Ending

% of

NPL

Specific

Balance

Total

Balance

Allocations

(dollars in thousands)

Pennsylvania

2,160,000

$

51.6%

19,180

$

10,630

$

New Jersey

1,198,000

28.6%

28,310

5,000

Maryland

372,000

8.9%

1,360

1,180

Virginia

328,000

7.8%

4,100

2,520

Delaware

129,000

3.1%

1,980

1,030

4,187,000

$

54,930

$

20,360

$

Loan Delinquency (Key Sectors)

Category

Total (%)

9/30/08

90-Days

9/30/08

Total (%)

9/30/09

90-Days

9/30/09

Commercial

Loans

1.68

1.14

2.26

1.65

Consumer

Direct

.91

.35

1.69

0.65

Commercial

Mortgage

1.43

.84

1.84

1.31

Residential

Mortgage

5.76

2.81

8.50

4.71

Construction

5.84

4.26

11.37

10.12

Total

Portfolio

2.29

1.39

3.32

2.32

Shared National Credits

Ending

Balance

(dollars in thousands)

Commercial / Industrial

116,849

$

Commercial Real Estate

47,485

Total Outstanding

164,334

$

Delinquency: 6.2%

Net Charge-offs (Q3 2009)

Comm'l

Res. Mtg.

Comm'l

Mortgage

Constr.

and HE

Other

Total

(in thousands)

Pennsylvania

1,326

$

1,383

$

267

$

90

$

1,980

$

5,046

$

Maryland

818

9

2,640

150

419

4,036

New Jersey

2,421

1,668

3,936

-

486

8,511

Virginia

2,545

-

2,487

824

58

5,914

Delaware

233

-

-

-

493

726

7,343

$

3,060

$

9,330

$

1,064

$

3,436

$

24,233

$

Avg Loans

3,668,000

4,159,000

1,050,000

2,585,000

452,000

11,914,000

NCO %

0.80%

0.29%

3.55%

0.16%

3.04%

0.81%

Net Charge-offs (YTD September 2009)

Comm'l

Res. Mtg.

Comm'l

Mortgage

Constr.

and HE

Other

Total

(in thousands)

Pennsylvania

3,020

$

3,327

$

4,242

$

1,778

$

5,084

$

17,451

$

Maryland

1,607

2,683

16,408

572

1,378

22,648

New Jersey

8,680

6,354

6,073

223

1,533

22,863

Virginia

9,428

-

5,816

1,875

1,189

18,308

Delaware

294

583

-

232

1,037

2,146

23,029

$

12,947

$

32,539

$

4,680

$

10,221

$

83,416

$

Avg Loans

3,660,000

4,100,000

1,143,000

2,615,000

453,000

11,971,000

NCO %

0.84%

0.42%

3.80%

0.24%

3.01%

0.93%

Non-performing Loans* (September 30, 2009)

Comm'l

Res. Mtg.

Comm'l

Mortgage

Constr.

and HE

Other

Total

(in thousands)

Pennsylvania

27,398

$

19,177

$

8,638

$

10,109

$

4,805

$

70,127

$

Maryland

7,064

1,356

47,118

4,674

3,123

63,335

New Jersey

14,597

28,312

18,924

7,856

3,187

72,876

Virginia

13,930

4,102

30,109

20,298

270

68,709

Delaware

228

1,983

-

3,255

1,245

6,711

63,217

$

54,930

$

104,789

$

46,192

$

12,630

$

281,758

$

End Loans

3,720,000

4,187,000

1,029,000

2,582,000

450,000

11,968,000

NPL%

1.70%

1.31%

10.18%

1.79%

2.81%

2.35%

* Includes accruing loans > 90 days past due.

53 relationships with commitments to lend

of $20 million or more

Maximum individual commitment- $33

million

Maximum commitment land development-

$28 million

Average commercial lending relationship

size is $466,247

Loans and corresponding relationships are

within Fulton’s geographic market area

Summary of Larger Loans

Overview of Third Quarter

Continued core deposit growth

Improved net interest margin

Slightly lower provision

Reduced construction exposure

Lower net charge-offs

Credit deterioration slowed

Stable other income

Expenses flat

2009 Financial Results (Q3 vs. Q2 2009)

Q3 2009

Q2 2009

Net income

23,345,000

$

13,110,000

$

Cost of preferred stock

(5,045,000)

(5,045,000)

Net income available

to common shareholders

18,300,000

$

8,065,000

$

Earnings per share

0.10

$

0.05

$

Return on tangible equity

7.91%

3.83%

Income Statement Summary (Q3 vs. Q2 2009)

Q3 2009

Q2 2009

$

%

(dollars in thousands)

Net Interest Income

132,800

$

127,940

$

4,860

$

4%

Loan Loss Provision

(45,000)

(50,000)

5,000

-10%

Other Income

41,230

45,300

(4,070)

-9%

Securities Gains (Losses)

(50)

80

(130)

-163%

Other Expenses

(99,810)

(107,810)

8,000

-7%

Pre-Tax Income

29,170

15,510

13,660

88%

Income Taxes

(5,820)

(2,400)

(3,420)

143%

Net Income

23,350

$

13,110

$

10,240

$

78%

Pre-Tax Income Summary (Q3 vs. Q2 2009)

Q3 2009

Q2 2009

$

%

(dollars in thousands)

Net Interest Income

132,800

$

127,940

$

4,860

$

4%

Other Income

41,230

45,300

(4,070)

-9%

Other Expenses

(99,810)

(100,080)

270

0%

Pre-Tax Income Before

LLP, CC Gain, Sec Gains

(Losses), Special FDIC

74,220

73,160

1,060

1%

Loan Loss Provision

(45,000)

(50,000)

5,000

-10%

Securities Gains (Losses)

(50)

80

(130)

-163%

Special FDIC Assessment

-

(7,730)

7,730

-100%

Pre-Tax Income

29,170

$

15,510

$

13,660

88%

2009 Financial Results (YTD September)

2009

2008

Net income

49,540,000

$

96,250,000

$

Cost of preferred stock

(15,120,000)

-

Net income available

to common shareholders

34,420,000

$

96,250,000

$

Earnings per share

0.20

$

0.55

$

Return on tangible equity

5.24%

14.00%

Income Statement Summary (YTD September)

2009

2008

$

%

(dollars in thousands)

Net Interest Income

384,860

$

391,810

$

(6,950)

$

-2%

Loan Loss Provision

(145,000)

(54,630)

(90,370)

165%

Other Income

130,520

116,640

13,880

12%

Credit Card Sale Gain

-

13,910

(13,910)

nm

Securities Gains (Losses)

2,950

(29,900)

32,850

-110%

Other Expenses

(313,990)

(305,750)

(8,240)

3%

Pre-Tax Income

59,340

132,080

(72,740)

-55%

Income Taxes

(9,800)

(35,830)

26,030

-73%

Net Income

49,540

$

96,250

$

(46,710)

$

-49%

Pre-Tax Income Summary (YTD September)

2009

2008

$

%

(dollars in thousands)

Net Interest Income

384,860

$

391,810

$

(6,950)

$

-2%

Other Income

130,520

116,440

14,080

12%

Other Expenses

(300,023)

(289,690)

(10,333)

4%

Pre-Tax Income Before

LLP, CC Gain, Sec Gains

(Losses), FDIC and ARC

215,357

218,560

(3,203)

-1%

Loan Loss Provision

(145,000)

(54,630)

(90,370)

165%

Credit Card Sale Gain

-

13,910

(13,910)

nm

Securities Gains (Losses)

2,950

(29,900)

32,850

-110%

Special FDIC Assessment

(7,730)

-

(7,730)

nm

ARC Losses

(6,237)

(15,860)

9,623

-61%

Pre-Tax Income

59,340

$

132,080

$

(72,740)

-55%

International Bancshares Corporation

Old National Bancorp

South Financial Group, Inc.

Susquehanna Bancshares, Inc.

TCF Financial Corporation

Trustmark Corporation

UMB Financial Corporation

United Bankshares, Inc.

Valley National Bancorp

Whitney Holding Corporation

Wilmington Trust Corporation

*Fulton’s peer group as of September 30, 2009

Associated Banc-Corp

BancorpSouth, Inc.

Bank of Hawaii Corporation

BOK Financial Corporation

Citizens Republic Bancorp

City National Corporation

Commerce Bancshares, Inc.

Cullen/Frost Bankers, Inc.

First Citizens BancShares, Inc.

First Midwest Bancorp, Inc.

First Merit Corporation

Peer Group*

Average Loans (Q3 vs. Q2 2009)

Q3 2009

Q2 2009

$

%

(dollars in millions)

Commercial

3,670

$

3,660

$

10

$

0%

Comm'l Mort

4,160

4,090

70

2%

Resid Mort

930

940

(10)

-1%

Home Equity

1,650

1,670

(20)

-1%

Construction

1,050

1,150

(100)

-9%

Cons./Other

450

450

-

0%

Total Loans

11,910

$

11,960

$

(50)

0%

Ending Loans (Q3 vs. Q2 2009)

Q3 2009

Q2 2009

$

%

(dollars in millions)

Commercial

3,720

$

3,610

$

110

$

3%

Comm'l Mort

4,190

4,120

70

2%

Resid Mort

930

930

-

0%

Home Equity

1,650

1,650

-

0%

Construction

1,030

1,100

(70)

-6%

Cons./Other

450

460

(10)

-2%

Total Loans

11,970

$

11,870

$

100

1%

Average Loans (YTD September)

2009

2008

$

%

(dollars in millions)

Commercial

3,660

$

3,500

$

160

$

5%

Comm'l Mort

4,100

3,670

430

12%

Resid Mort

940

900

40

4%

Home Equity

1,670

1,570

100

6%

Construction

1,140

1,330

(190)

-14%

Cons./Other

460

500

(40)

-8%

Total Loans

11,970

$

11,470

$

500

4%

Average Deposits (Q3 vs. Q2 2009)

Q3 2009

Q2 2009

$

%

(dollars in millions)

Nonint DDA

1,920

$

1,810

$

110

$

6%

Int DDA

1,880

1,820

60

3%

Savings/MMDA

2,560

2,310

250

11%

CD's

5,560

5,630

(70)

-1%

Cash Management

510

550

(40)

-7%

Total Deposits

12,430

$

12,120

$

310

3%

Average Deposits (YTD September)

2009

2008

$

%

(dollars in millions)

Nonint DDA

1,800

$

1,650

$

150

$

9%

Int DDA

1,820

1,710

110

6%

Savings/MMDA

2,310

2,180

130

6%

CD's

5,540

4,390

1,150

26%

Cash Management

550

700

(150)

-21%

Total Deposits

12,020

$

10,630

$

1,390

13%

Other Borrowings (YTD September)

2009

2008

$

%

(dollars in millions)

Federal Funds

570

$

1,300

$

(730)

$

-56%

FHLB Advances

1,370

1,450

(80)

-6%

Other LT Debt

380

380

-

0%

Other ST Borrowings

70

370

(300)

-81%

Total Borrowings

2,390

$

3,500

$

(1,110)

$

-32%

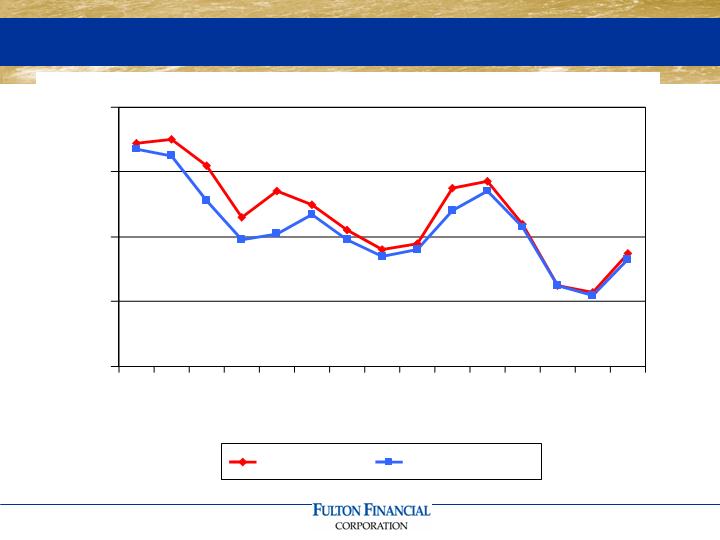

Net Interest Margin Trend

3.70

3.62

3.56

3.58

3.77

3.64

3.45

3.43

3.55

3.67

3.59

3.54

3.56

3.68

3.74

3.63

3.45

3.42

3.53

3.75

3.20

3.40

3.60

3.80

4.00

Q1

06

Q2

06

Q3

06

Q4

06

Q1

07

Q2

07

Q3

07

Q4

07

Q1

08

Q2

08

Q3

08

Q4

08

Q1

09

Q2

09

Q3

09

Reported

Normalized

Other Income (Q3 vs. Q2 2009)

Q3 2009

Q2 2009

$

%

(dollars in thousands)

Overdraft & NSF Fees

9,340

$

8,790

$

550

$

6%

Invt Mgt & Trust

8,190

7,880

310

4%

Service Charges

3,340

3,180

160

5%

Success Card Fees

2,870

2,750

120

4%

Mort. Sales Gains

2,780

7,400

(4,620)

-62%

Cash Mgt Fees

2,650

3,090

(440)

-14%

Merchant Fees

2,150

1,870

280

15%

Foreign Currency

1,940

1,790

150

8%

Letters of Credit

1,740

1,820

(80)

-4%

Credit Card Fees

1,520

1,360

160

12%

Life Insurance (COLI)

710

1,090

(380)

-35%

ATM Fees

630

680

(50)

-7%

Other

3,370

3,600

(230)

-6%

Total

41,230

$

45,300

$

(4,070)

$

-9%

Other Income (YTD September)

2009

2008

$

%

(dollars in thousands)

Overdraft & NSF Fees

26,570

$

25,790

$

780

$

3%

Invt Mgt & Trust

23,970

25,190

(1,220)

-5%

Mort. Sales Gains

18,760

7,250

11,510

159%

Service Charges

9,760

9,740

20

0%

Cash Mgt Fees

8,940

9,930

(990)

-10%

Success Card Fees

8,060

7,340

720

10%

Merchant Fees

5,650

5,860

(210)

-4%

Foreign Currency

5,120

5,360

(240)

-4%

Letters of Credit

5,090

4,360

730

17%

Credit Card Fees

4,070

2,440

1,630

67%

Life Insurance (COLI)

2,700

2,420

280

12%

ATM Fees

1,940

2,130

(190)

-9%

Other

9,890

8,830

1,060

12%

Total

130,520

$

116,640

$

13,880

$

12%

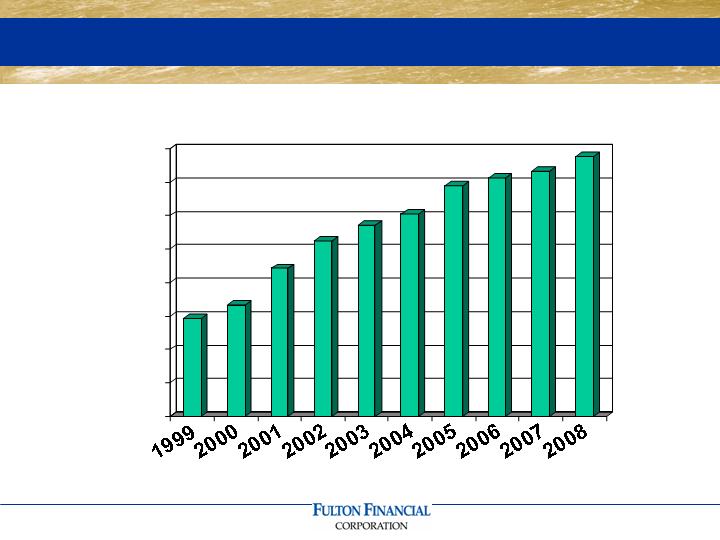

Efficiency Ratio

58.8

61.4

61.6

50.0

52.0

54.0

56.0

58.0

60.0

62.0

64.0

93

94

95

96

97

98

99

00

01

02

03

04

05

06

07

08

YTD

6/09

YTD

6/09

FFC

Peer

Top 50

Other Expense (Q3 vs. Q2 2009)

Q3 2009

Q2 2009

$

%

(dollars in thousands)

Salaries & Benefits

54,090

$

55,800

$

(1,710)

$

-3%

Occupancy & Equip.

13,450

13,540

(90)

-1%

FDIC Insurance

5,240

12,210

(6,970)

-57%

Data Proc. & Software

4,740

4,610

130

3%

Supplies & Postage

2,820

2,700

120

4%

Legal & Audit

2,390

2,090

300

14%

Telecommunications

2,140

2,180

(40)

-2%

Marketing

1,980

1,720

260

15%

Outside Services

1,880

1,830

50

3%

Amortization

1,430

1,430

-

0%

Travel & Entertain.

1,220

1,360

(140)

-10%

OREO Expenses

1,090

1,870

(780)

-42%

State Tax

610

1,050

(440)

-42%

Operating Risk Loss

340

140

200

143%

Other Expenses

6,390

5,280

1,110

21%

Total

99,810

$

107,810

$

(8,000)

$

-7%

Other Expense (YTD September)

2009

2008

$

%

(dollars in thousands)

Salaries & Benefits

165,190

$

164,790

$

400

$

0%

Occupancy & Equip.

41,090

40,910

180

0%

FDIC Insurance

21,740

2,680

19,060

nm

Data Proc. & Software

13,970

13,810

160

1%

Supplies & Postage

8,190

8,520

(330)

-4%

Legal & Audit

6,700

5,720

980

17%

Operating Risk Loss

6,680

19,110

(12,430)

-65%

Telecommunications

6,480

5,960

520

9%

Marketing

6,280

9,520

(3,240)

-34%

Outside Services

5,470

5,870

(400)

-7%

Amortization

4,330

5,390

(1,060)

-20%

OREO Expenses

4,280

3,140

1,140

36%

Travel & Entertain.

4,030

4,620

(590)

-13%

State Tax

2,470

2,050

420

20%

Other Expenses

17,090

13,660

3,430

25%

Total

313,990

$

305,750

$

8,240

$

3%

Allowance for Credit Losses

Q3 2009

Q2 2009

(dollars in thousands)

Balance at beginning of period

220,950

$

200,060

$

Loan Loss Provision

45,000

50,000

Net Charge-Offs

(24,230)

(29,110)

Balance at end of period

241,720

$

220,950

$

Allowance to Loans

2.02%

1.86%

Nonperforming Assets to Assets

1.82%

1.73%

Net Charge-offs to Loans

0.81%

0.97%

Allowance for Credit Losses (YTD Sept.)

2009

2008

(dollars in thousands)

Balance at beginning of year

180,140

$

112,210

$

Loan Loss Provision

145,000

54,630

Net Charge-Offs

(83,420)

(25,010)

Balance at September 30th

241,720

$

141,830

$

Allowance to Loans

2.02%

1.20%

Nonperforming Assets to Assets

1.82%

1.15%

Net Charge-offs to Loans

0.93%

0.29%

Net Charge-Offs To Average Loans

0.93

1.10

1.67

0.00

0.30

0.60

0.90

1.20

1.50

1.80

91

92

93

94

95

96

97

98

99

00

01

02

03

04

05

06

07

08

YTD

6/09

YTD

9/09

FFC

Peer

Top 50

Investment Portfolio (September 30, 2009)

ENDING

MODIFIED

BALANCE

DURATION

(in millions)

Agency mortgage-backed securities

1,112.0

$

3.40

Agency collateralized mortgage obligations

975.4

2.83

Municipal bonds

415.8

4.44

Auction rate securities

292.3

4.02

Corporate & trust preferred securities

155.3

10.36

U.S. Treasuries and agencies

138.9

3.32

FHLB & FRB stock

85.7

NA

Bank stocks

36.2

NA

Other investments

26.2

NA

Net unrealized gain / (loss)

36.6

Total Investments

3,274.4

$

3.77

Available Funds

Securities Availabile as Collateral:

09/30/09

Total Unpledged Securities

$694,042,360

Less: Corporate / Trups / ARCs

(200,378,078)

Less: SBA / Other

(2,735,978)

Less: Securities included in FHLB MBC

(177,479,610)

Plus: Excess Securities pledged in pools

333,789,350

Total Available for Pledging

647,238,044

Less: Estimated 15% Haircut

(97,085,707)

Total Available for Collateral

$550,152,337

FHLB and Discount Window Borrowing Capacity:

FHLB Borrowing Capacity

1,174,977,911

FRB Discount Window - Securities (net)

19,830,017

FRB Discount Window - Loans (net)

1,736,764,703

Plus: Corporate / Trups pledgeable to FRB

200,378,078

Less: Haircut on securities

(40,075,616)

Less: Outstanding Discount Window Loans

-

Total Borrowing Capacity

$3,091,875,093

Total Available Collateral and Borrowing Capacity

$3,642,027,431

Federal Funds Purchased

$205,000,000

Federal Funds Line Limits

$2,385,000,000

Status of the Corporation

Strong capital position

Focus on profitable organic growth

Positioned for economic rebound

Current loan loss reserve levels believed

to be adequate

Proactive management of problem credits

Valuable 5-state franchise / strong in-state

markets

Disciplined expense control