Exhibit 99.1

Fulton Financial Corporation

Investor Presentation

November 2004

Fulton Financial Corporation

1

Forward-looking statement

The following presentation may contain forward-looking statements about Fulton Financial Corporation’s growth and acquisition strategies, new products and services, and future financial performance, including earnings and dividends per share, return on average assets, return on average equity, efficiency ratio and capital ratio. Forward-looking statements are encouraged by the Private Securities Litigation Reform Act of 1995.

Such forward-looking information is based upon certain underlying assumptions, risks and uncertainties. Because of the possibility of change in the underlying assumptions, actual results could differ materially from these forward-looking statements. Risks and uncertainties that may affect future results include: pricing pressures on loans and deposits, actions of bank and non-bank competitors, changes in local and national economic conditions, changes in regulatory requirements, actions of the Federal Reserve Board, the Corporation’s success in merger and acquisition integration, and customers’ acceptance of the Corporation’s products and services.

2

Presentation outline

Corporate profile Strategic initiatives Financial performance Asset quality Future direction

3

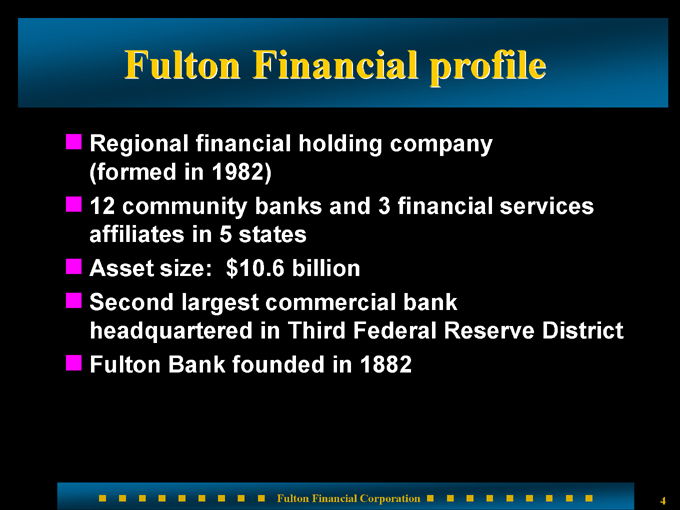

Fulton Financial profile

Regional financial holding company (formed in 1982)

12 community banks and 3 financial services affiliates in 5 states Asset size: $10.6 billion Second largest commercial bank headquartered in Third Federal Reserve District Fulton Bank founded in 1882

4

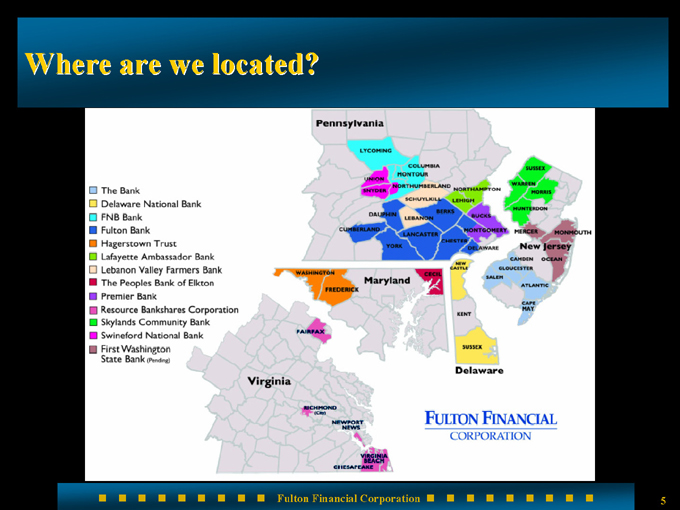

Where are we located?

The Bank

Delaware National Bank

FNB Bank

Hagerstown Trust

Lafayette Ambassador Bank

Lebanon Valley Farmers Bank

The Peoples Bank of Elkton

Premier Bank

Resource Bankshares Corporation

Skylands Community Bank

Swineford National Bank

First Washington State Bank (Pending)

5

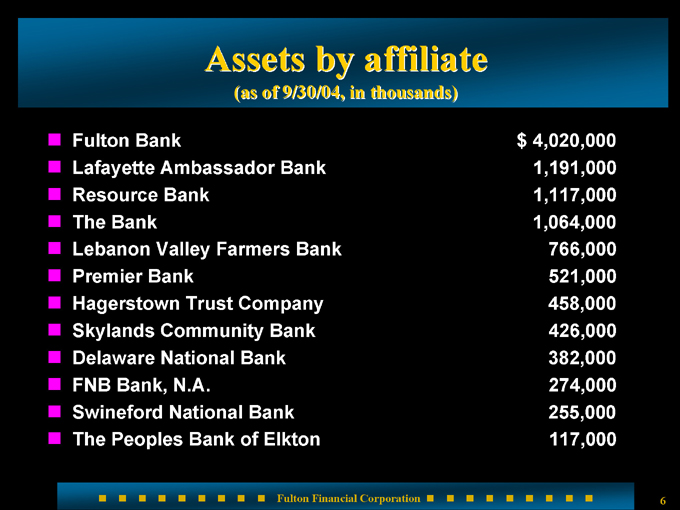

Assets by affiliate

(as of 9/30/04, in thousands)

Fulton Bank $4,020,000

Lafayette Ambassador Bank 1,191,000

Resource Bank 1,117,000

The Bank 1,064,000

Lebanon Valley Farmers Bank 766,000

Premier Bank 521,000

Hagerstown Trust Company 458,000

Skylands Community Bank 426,000

Delaware National Bank 382,000

FNB Bank, N.A. 274,000

Swineford National Bank 255,000

The Peoples Bank of Elkton 117,000

6

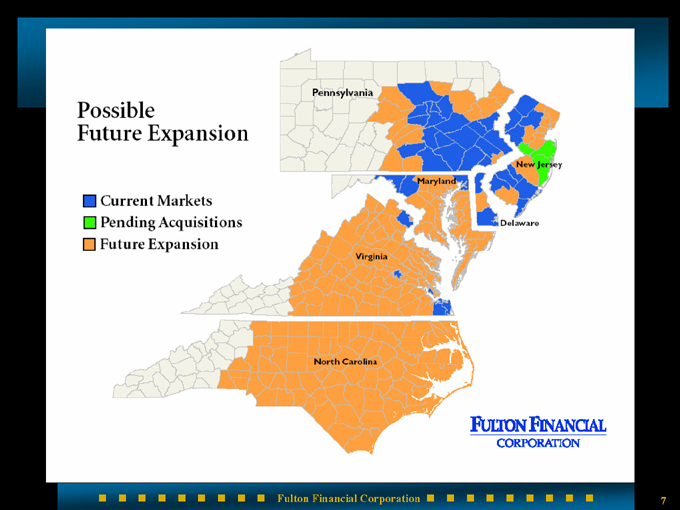

Possible future expansion

Current markets

Pending acquisitions

Future expansion

Pennsylvania

Maryland

New jersey

Delaware

Virginia

North carolina

7

Mission statement

We will increase shareholder value and enrich the communities we serve by creating financial success together with our customers and career success together with our employees.

We will conduct all of our business with honesty and integrity.

8

Corporate ethics

Longstanding written code of conduct No “gray” areas Expectations clearly outlined

9

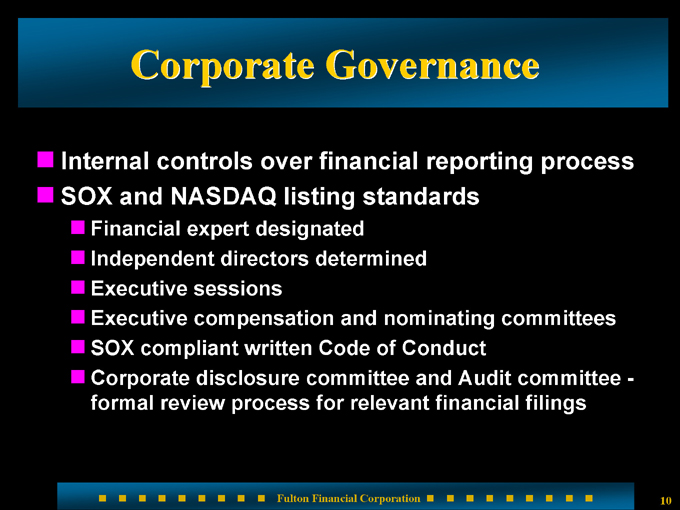

Corporate Governance

Internal controls over financial reporting process SOX and NASDAQ listing standards

Financial expert designated Independent directors determined Executive sessions

Executive compensation and nominating committees SOX compliant written Code of Conduct Corporate disclosure committee and Audit committee - -formal review process for relevant financial filings

10

What have we accomplished?

8.8% compounded annual growth rate in earnings per share 22 consecutive years of record earnings 30 consecutive years of dividend increases 10.3% compounded annual growth rate in dividends per share (approximate dividend yield: 3.01%) Proven business model Consistent performance

11

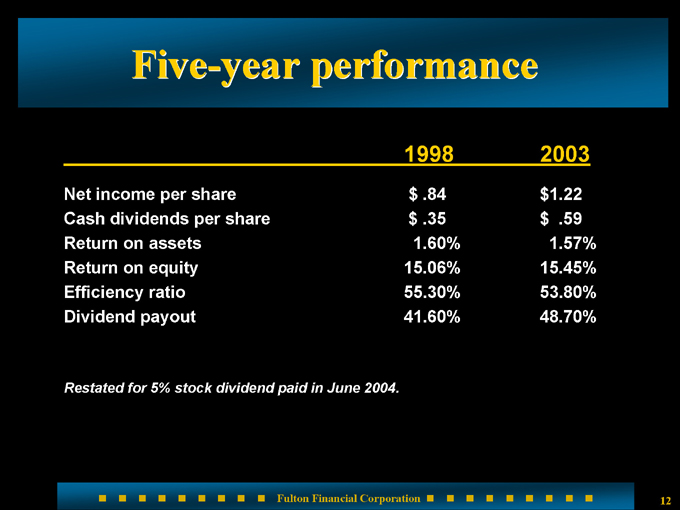

Five-year performance

1998 2003

Net income per share $.84 $1.22

Cash dividends per share $.35 $.59

Return on assets 1.60% 1.57%

Return on equity 15.06% 15.45%

Efficiency ratio 55.30% 53.80%

Dividend payout 41.60% 48.70%

Restated for 5% stock dividend paid in June 2004.

12

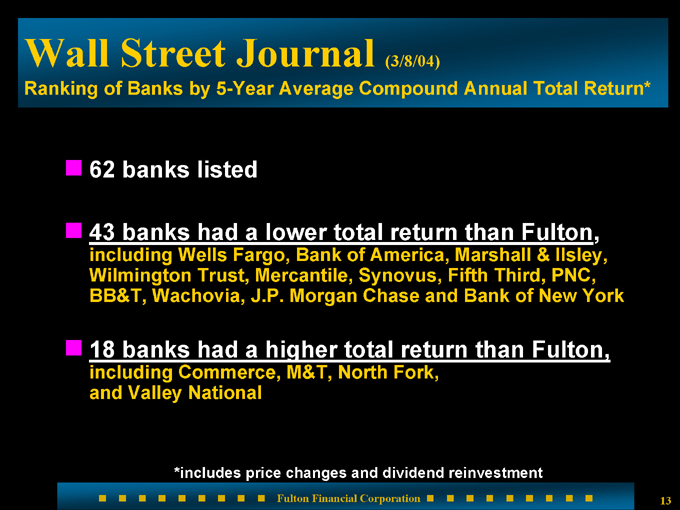

Wall Street Journal (3/8/04)

Ranking of Banks by 5-Year Average Compound Annual Total Return*

62 banks listed

43 banks had a lower total return than Fulton,

including Wells Fargo, Bank of America, Marshall & Ilsley, Wilmington Trust, Mercantile, Synovus, Fifth Third, PNC, BB&T, Wachovia, J.P. Morgan Chase and Bank of New York

18 banks had a higher total return than Fulton,

including Commerce, M&T, North Fork, and Valley National

*includes price changes and dividend reinvestment

13

Five-year total return

Peer analysis - 12/31/03

1 INTERNATIONAL BANCSHARES CORP 220.60

2 TCF FINANCIAL CORP 142.46

3 SOUTHWEST BANCORPORATION OF TX 117.92

4 FIRST REPUBLIC BANK 115.89

5 BANK OF HAWAII CORP 102.83

6 WHITNEY HOLDING CORP 96.03

7 ASSOCIATED BANC-CORP 91.25

8 VALLEY NATIONAL 88.61

9 GREATER BAY BANCORP 85.06

10 HIBERNIA CORP 83.48

11 FULTON FINANCIAL 81.15

12 FIRST MIDWEST 79.54

13 COLONIAL BANCGROUP 74.70

14 CULLEN FROST BANKERS 68.39

15 BOK FINANCIAL CORP 68.36

16 HUDSON UNITED 67.53

17 CITY NATIONAL CORP 63.47

18 COMMERCE BANKSHARES 60.18

19 BANCORP SOUTH 54.76

20 SUSQUEHANNA BANCSHS 49.05

21 TRUSTMARK CORP 46.26

22 SKY FINANCIAL GROUP 44.24

23 FIRST CITIZENS BANCSHARES 41.98

24 UNITED BANKSHARES INC 40.65

25 WILMINGTON TRUST CORP 37.82

26 MERCANTILE BANKSHARES 37.27

27 UMB FINANCIAL CORP 32.15

28 SOUTH FINANCIAL GROUP (The) 23.55

29 FIRSTMERIT CORP 22.32

30 CITIZENS BANKING CORP 20.73

31 OLD NATIONAL CORP -9.53

32 RIGGS NATIONAL -13.12

AVERAGE 66.74

14

Stock highlights (as of 09/30/04)

Average daily trading volume 139,500 shares

Number of analysts 12

Number of market makers 42

Number of shares outstanding 121.0 million

Market capitalization $2.6 billion

Annual meeting attendance 2,000 shareholders

15

Employee stock ownership

80% of our employees collectively own more than 2 million shares of Fulton Financial Corporation stock

Stock options help us to retain key high-performing employees

16

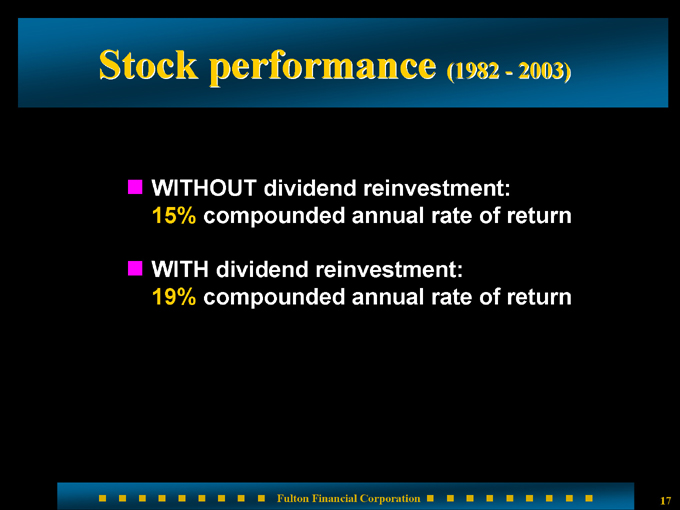

Stock performance (1982 - 2003)

WITHOUT dividend reinvestment: 15% compounded annual rate of return

WITH dividend reinvestment:

19% compounded annual rate of return

17

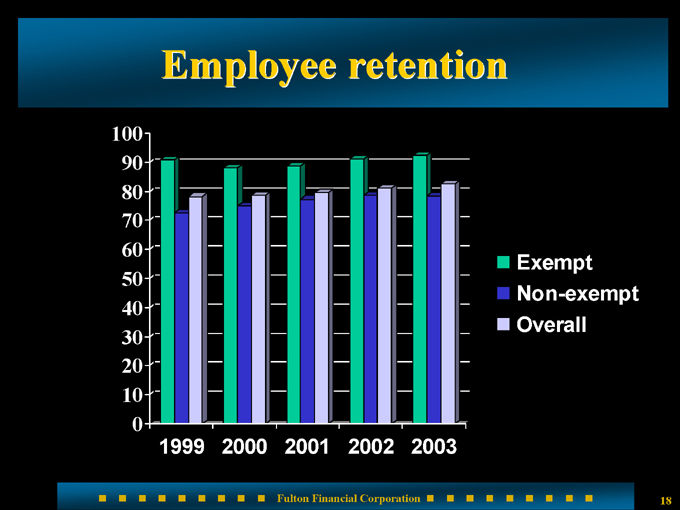

Employee retention

100 90 80 70 60

50 40 30 20 10 0

1999 2000 2001 2002 2003

Exempt Non-exempt Overall

18

Employee opinion survey

Customer service Management team performance Company image and mission Team orientation

Technology and systems

Training and development Sales orientation Work effectiveness Pay and benefits Employee satisfaction

(Survey administered by BAI Survey Services)

19

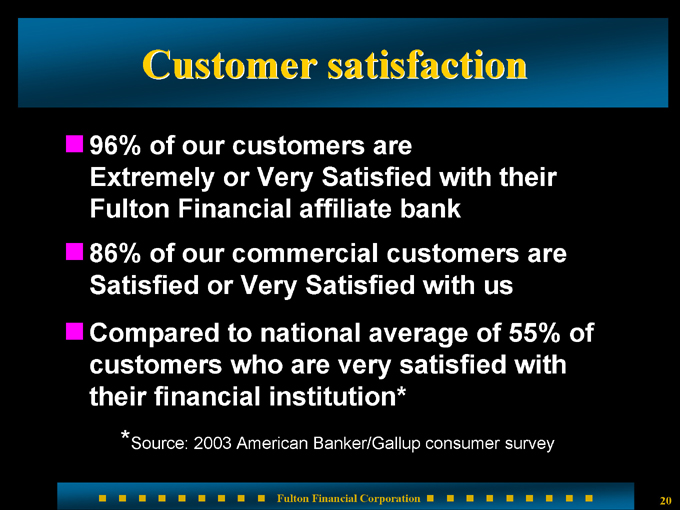

Customer satisfaction

96% of our customers are

Extremely or Very Satisfied with their Fulton Financial affiliate bank 86% of our commercial customers are Satisfied or Very Satisfied with us Compared to

national average of 55% of customers who are very satisfied with their financial institution*

* Source: 2003 American Banker/Gallup consumer survey

20

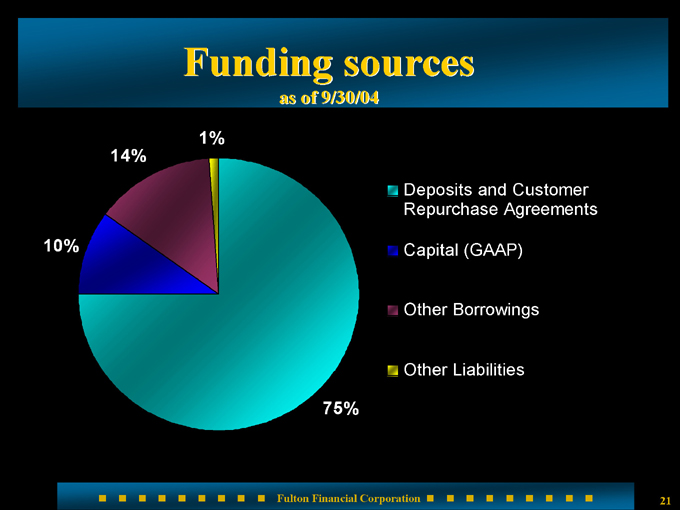

Funding sources

as of 9/30/04

10%

14%

1%

75%

Deposits and Customer Repurchase Agreements

Capital (GAAP) Other Borrowings Other Liabilities

21

Community involvement

Employees are actively involved in their own communities The community benefits from this support The banks receive additional business as a result of the relationships and goodwill that are developed

22

Corporate strategic initiatives

Achieving consistent earnings growth Maintaining high asset quality Expanding the franchise through our well-developed acquisition strategy Diversifying revenue stream by increasing the contribution of non-interest income Managing capital

23

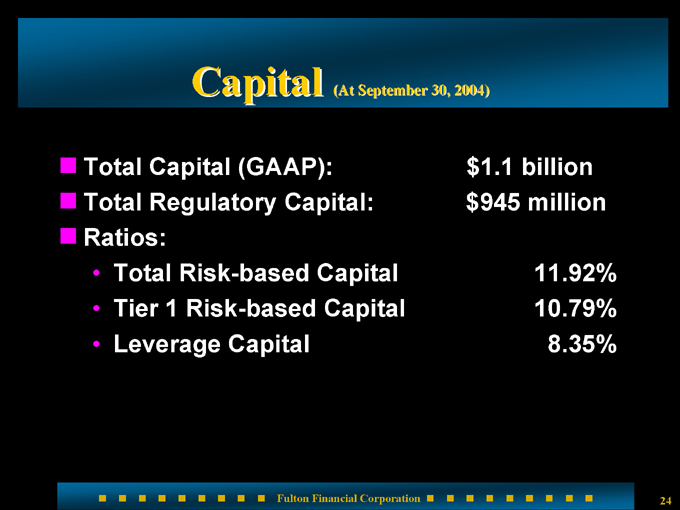

Capital (At September 30, 2004)

Total Capital (GAAP): $1.1 billion

Total Regulatory Capital: $945 million

Ratios:

Total Risk-based Capital 11.92%

Tier 1 Risk-based Capital 10.79%

Leverage Capital 8.35%

24

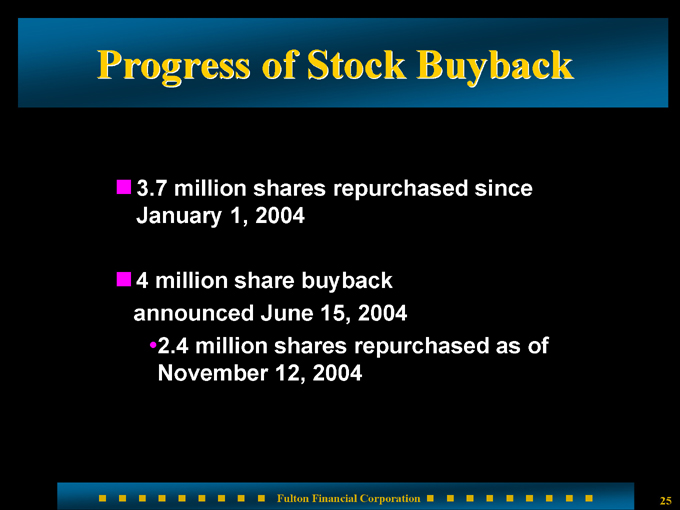

Progress of Stock Buyback

3.7 million shares repurchased since January 1, 2004

4 million share buyback announced June 15, 2004

2.4 million shares repurchased as of November 12, 2004

25

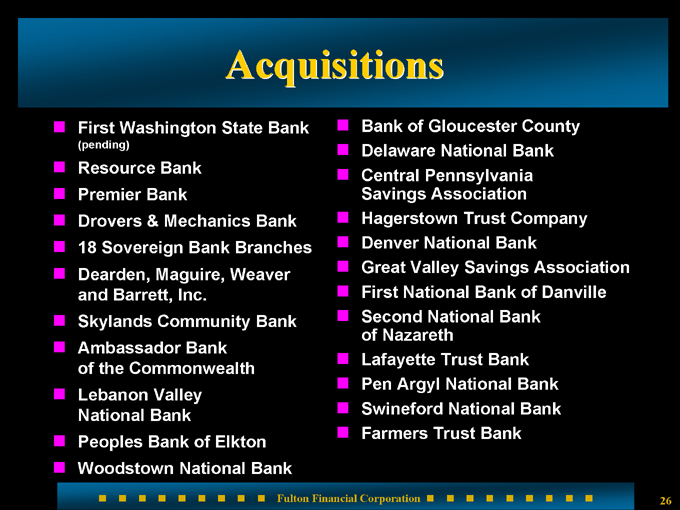

Acquisitions

First Washington State Bank

(pending)

Resource Bank Premier Bank

Drovers & Mechanics Bank 18 Sovereign Bank Branches Dearden, Maguire, Weaver and Barrett, Inc.

Skylands Community Bank Ambassador Bank of the Commonwealth Lebanon Valley National Bank Peoples Bank of Elkton

Woodstown National Bank

Bank of Gloucester County Delaware National Bank Central Pennsylvania Savings Association Hagerstown Trust Company Denver National Bank Great Valley Savings Association First National Bank of Danville Second National Bank of Nazareth Lafayette Trust Bank Pen Argyl National Bank Swineford National Bank Farmers Trust Bank

26

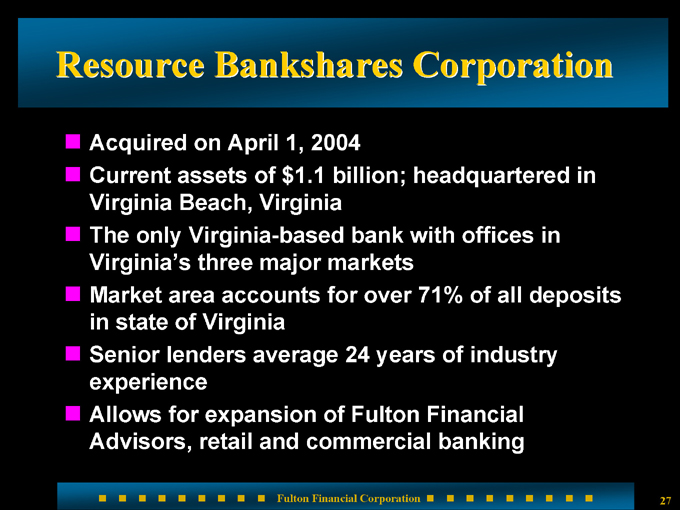

Resource Bankshares Corporation

Acquired on April 1, 2004

Current assets of $1.1 billion; headquartered in Virginia Beach, Virginia The only Virginia-based bank with offices in Virginia’s three major markets Market area accounts for over 71% of all deposits in state of

Virginia Senior lenders average 24 years of industry experience Allows for expansion of Fulton Financial Advisors, retail and commercial banking

27

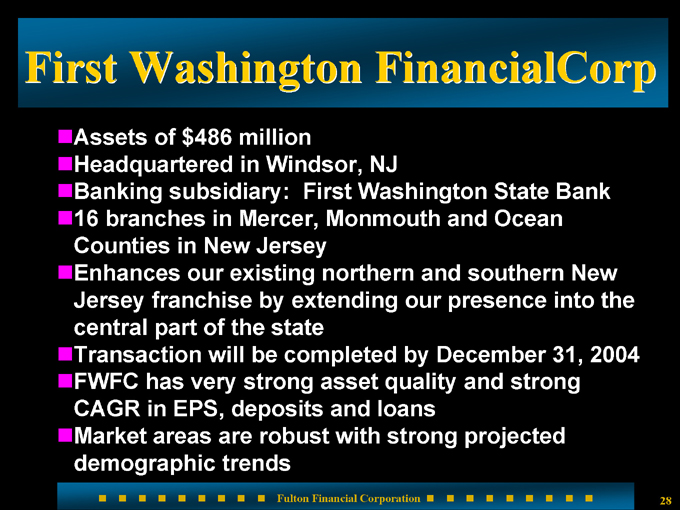

First Washington FinancialCorp

Assets of $486 million Headquartered in Windsor, NJ

Banking subsidiary: First Washington State Bank 16 branches in Mercer, Monmouth and Ocean Counties in New Jersey Enhances our existing northern and southern New Jersey franchise by extending our presence into the central part of the state Transaction will be completed by December 31, 2004 FWFC has very strong asset quality and strong CAGR in EPS, deposits and loans Market areas are robust with strong projected demographic trends

28

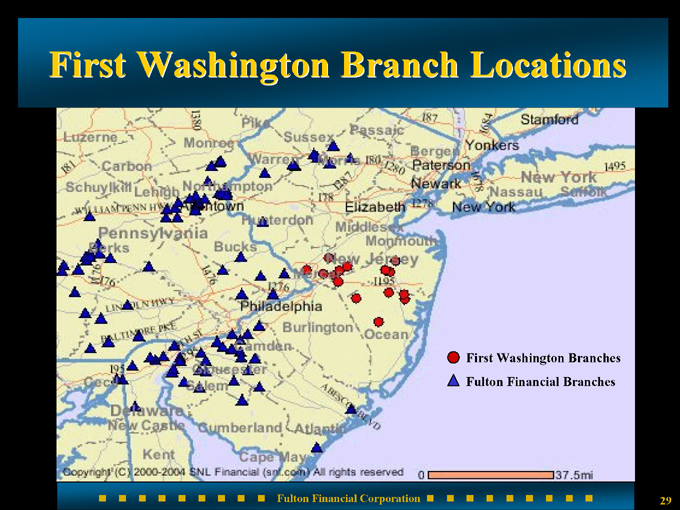

First Washington Branch Locations

First Washington Branches Fulton Financial Branches

29

What do we look for?

High growth areas

Dynamic market demographics Strong performance Asset quality Talented and dedicated staff Compatible corporate culture

30

Acquisitions in new markets

What changes?

Loan review Investments

Asset/liability management Compliance Common operating platform Audit

31

Acquisitions in new markets

What stays the same?

Bank name Board of Directors Management team Employees

32

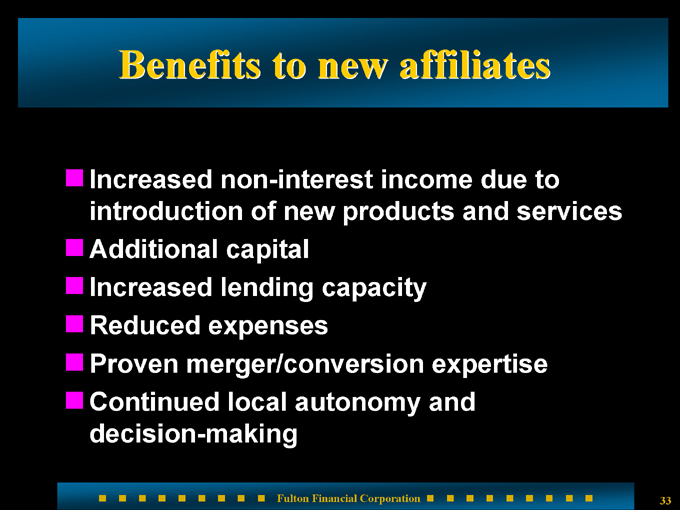

Benefits to new affiliates

Increased non-interest income due to introduction of new products and services Additional capital Increased lending capacity Reduced expenses Proven merger/conversion expertise Continued local autonomy and decision-making

33

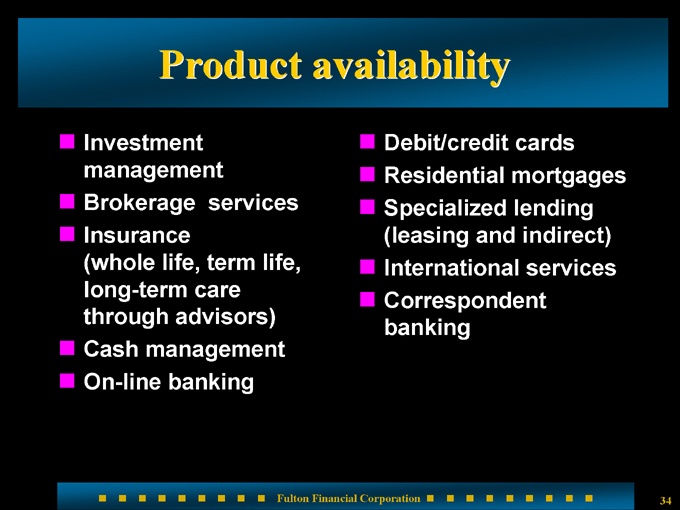

Product availability

Investment management Brokerage services Insurance (whole life, term life, long-term care through advisors) Cash management On-line banking Debit/credit cards Residential mortgages Specialized lending (leasing and indirect) International services Correspondent banking

34

Fulton Financial Advisors, N.A.

Includes Dearden Maguire Weaver and Barrett, LLC and Fulton Insurance Services Group As of September 30, 2004: $5.3 billion; $3.9 billion in assets under management

Products and Services

Personal trust Asset management Retirement services Brokerage

Insurance Corporate trust Cash management Private banking

Named Community-Based Bank Brokerage Program of the Year in 2003 by Bank Insurance and Securities Association (BISA)

35

Fulton Mortgage Company

Coordinates residential mortgage lending throughout 11 affiliates

Expanded, competitive product line to customers of all affiliates In partnership with each affiliate, focused management team on residential mortgages Entry into new markets for FFC

Record originations in 2003

Residential lending at Resource Bank provided through Resource Mortgage

36

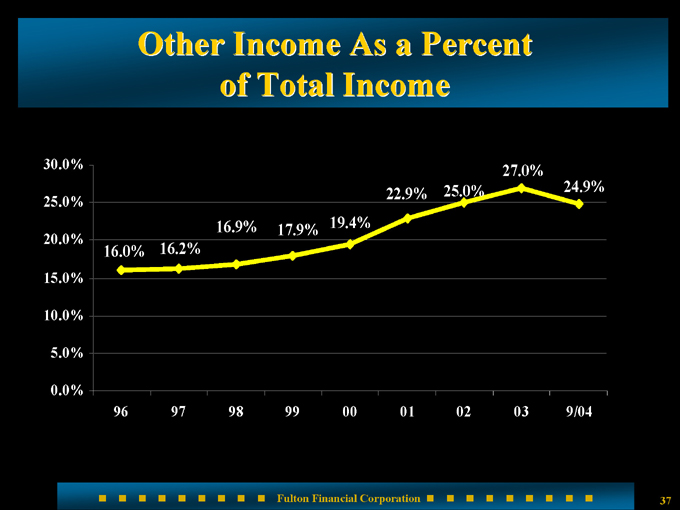

Other Income As a Percent of Total Income

30.0%

25.0%

20.0%

15.0%

10.0%

5.0%

0.0%

16.0%

16.2%

16.9%

17.9%

19.4%

22.9%

25.0%

27.0%

24.9%

96 97 98 99 00 01 02 03 9/04

37

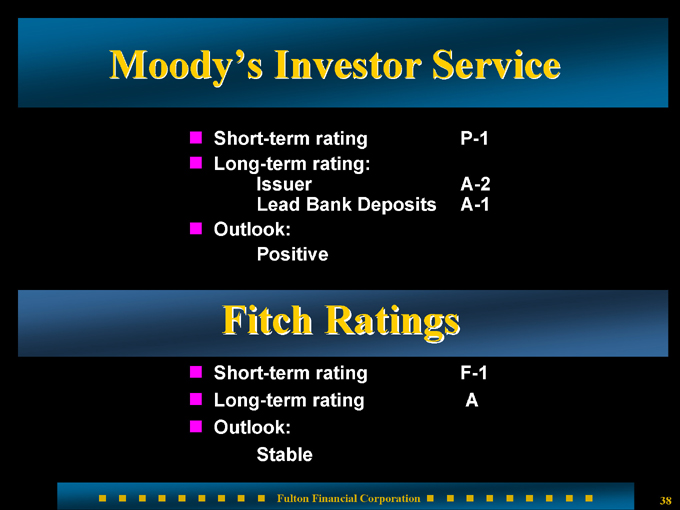

Moody’s Investor Service

Short-term rating P-1

Long-term rating:

Issuer A-2

Lead Bank Deposits A-1

Outlook:

Positive

Fitch Ratings

Short-term rating F-1

Long-term rating A

Outlook:

Stable

38

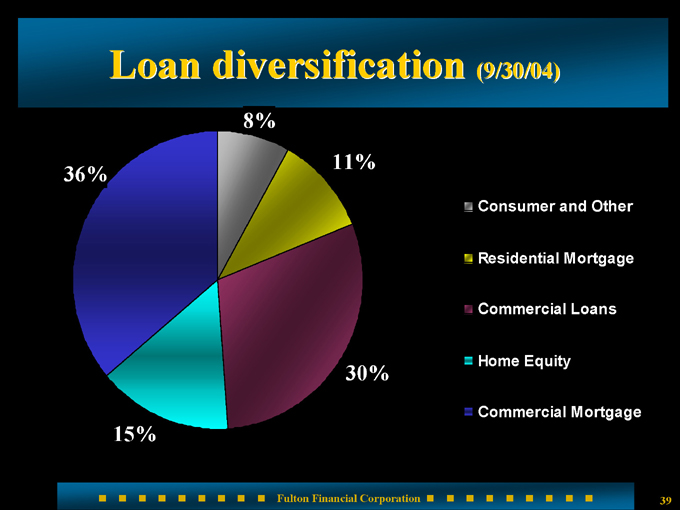

Loan diversification (9/30/04)

36%

8%

11%

30%

15%

Consumer and Other Residential Mortgage Commercial Loans Home Equity Commercial Mortgage

39

Summary of larger loans

26 relationships with commitments to lend of $20 million or more Maximum individual commitment of $30 million Average commercial loan commitment is $550,000 Loans and corresponding relationships are within Fulton’s geographical market area

40

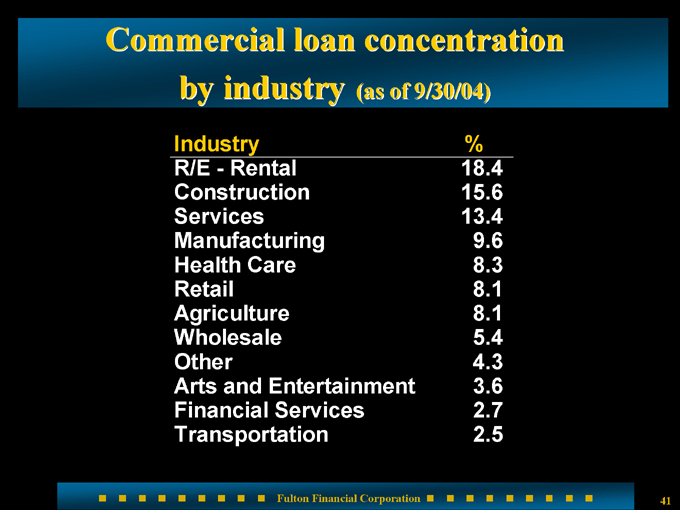

Commercial loan concentration

by industry (as of 9/30/04)

Industry %

R/E - Rental 18.4

Construction 15.6

Services 13.4

Manufacturing 9.6

Health Care 8.3

Retail 8.1

Agriculture 8.1

Wholesale 5.4

Other 4.3

Arts and Entertainment 3.6

Financial Services 2.7

Transportation 2.5

41

Quarter ended September 30, 2004 $0.32 Net income per share (6.7% increase over 2003)

$0.165 Cash dividends per share (8.6% increase over 2003)

1.48% Return on assets 14.21% Return on equity 19.37% Return on tangible equity

42

Peer group

Associated Banc-Corp BancorpSouth, Inc. Bank of Hawaii Corporation BOK Financial Corporation Citizens Banking Corporation City National Corporation Colonial BancGroup, Inc. Commerce Bancshares, Inc. Cullen/Frost Bankers, Inc. First Citizens BancShares, Inc. First Midwest Bancorp, Inc. First Republic Bank FirstMerit Corporation Greater Bay Bancorp Hibernia Corporation Hudson United Bancorp

International Bancshares Corporation Mercantile Bankshares Corporation Old National Bancorp Riggs National Corporation Sky Financial Group Inc.

South Financial Group, Inc.

Southwest Bancorporation of Texas, Inc. Susquehanna Bancshares, Inc.

TCF Financial Corporation Trustmark Corporation UMB Financial Corporation United Bankshares, Inc. Valley National Bancorp Whitney Holding Corporation Wilmington Trust Corporation

43

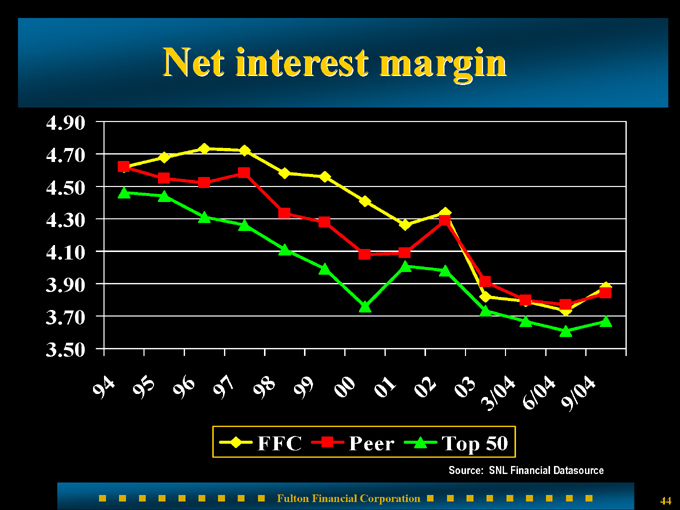

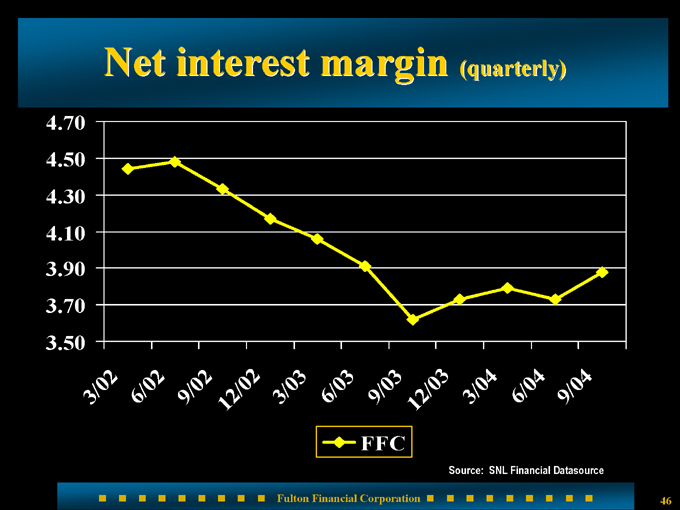

Net interest margin

4.90

4.70

4.50

4.30

4.10

3.90

3.70

3.50

94 95

96

97

98

99

00 01

02

03

3/04

6/04 9/04

FFC

Peer

Top 50

Source: SNL Financial Datasource

44

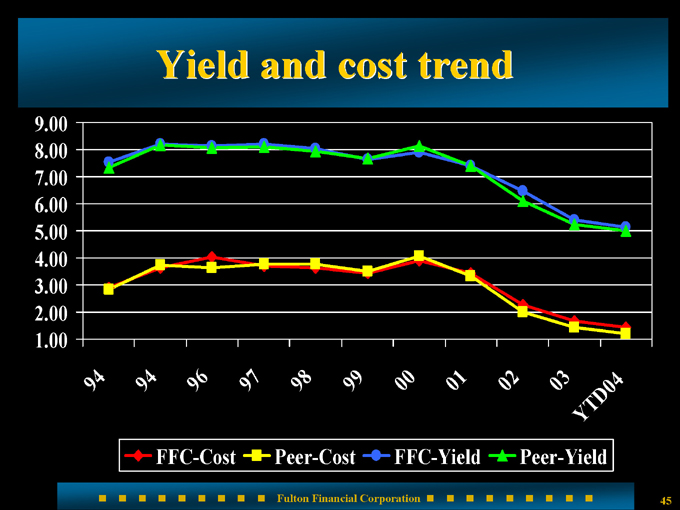

Yield and cost trend

9.00 8.00 7.00 6.00 5.00 4.00 3.00 2.00 1.00

94 94 96 97 98 99

00 01 02 03

YTD04

FFC-Cost Peer-Cost FFC-Yield Peer-Yield

45

Net interest margin (quarterly)

4.70 4.50 4.30 4.10 3.90 3.70 3.50

3/02 6/02

9/02

12/02 3/03

6/03

9/03

12/03 3/04

6/04

9/04

FFC

Source: SNL Financial Datasource

46

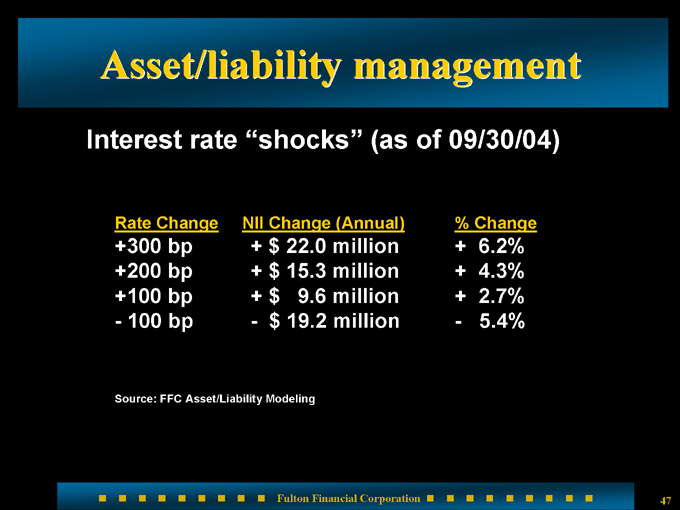

Asset/liability management

Interest rate “shocks” (as of 09/30/04)

Rate Change NII Change (Annual) % Change

+300 bp + $22.0 million + 6.2%

+200 bp + $15.3 million + 4.3%

+100 bp + $9.6 million + 2.7%

- 100 bp - $19.2 million - 5.4%

Source: FFC Asset/Liability Modeling

47

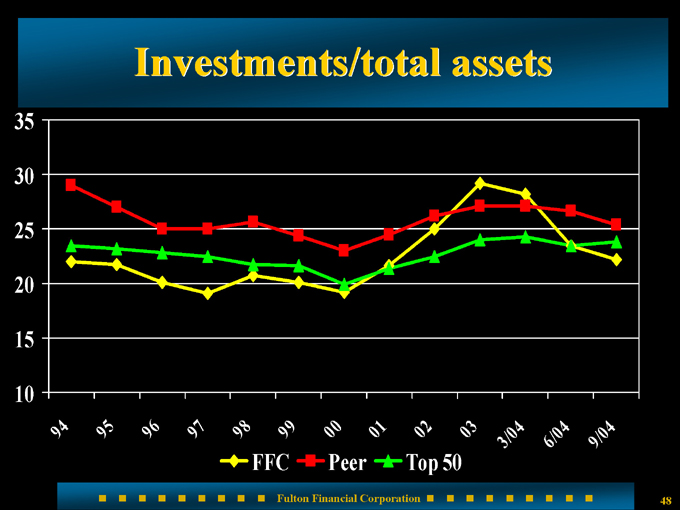

Investments/total assets

35 30

25 20 15 10

94

95 96 97

98

FFC 99 Peer 00

01

Top 50 02

03 3/04 6/04 9/04

48

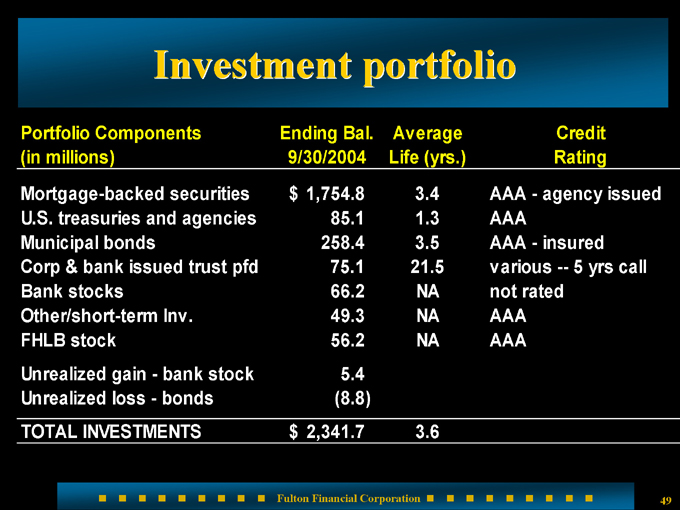

Investment portfolio

Portfolio Components (in millions) Ending Bal. 9/30/2004 Average Life (yrs.) Credit Rating

Mortgage-backed securities $1,754.8 3.4 AAA - agency issued

U.S. treasuries and agencies 85.1 1.3 AAA

Municipal bonds 258.4 3.5 AAA - insured

Corp & bank issued trust pfd 75.1 21.5 various - 5 yrs call

Bank stocks 66.2 NA not rated

Other/short-term Inv. 49.3 NA AAA

FHLB stock 56.2 NA AAA

Unrealized gain - bank stock 5.4

Unrealized loss - bonds (8.8)

TOTAL INVESTMENTS $2,341.7 3.6

49

Average loan growth (3rd Quarter)

2004 2003 $ %

(dollars in millions)

Commercial $2,150 $1,700 $450 26%

Comm’l Mortgage 2,600 2,050 550 27%

Resid Mortgage 790 550 240 44%

Home Equity 1,030 780 250 32%

Other Consumer 590 600 (10) -2%

Total Loans $7,160 $5,680 $1,480 26%

50

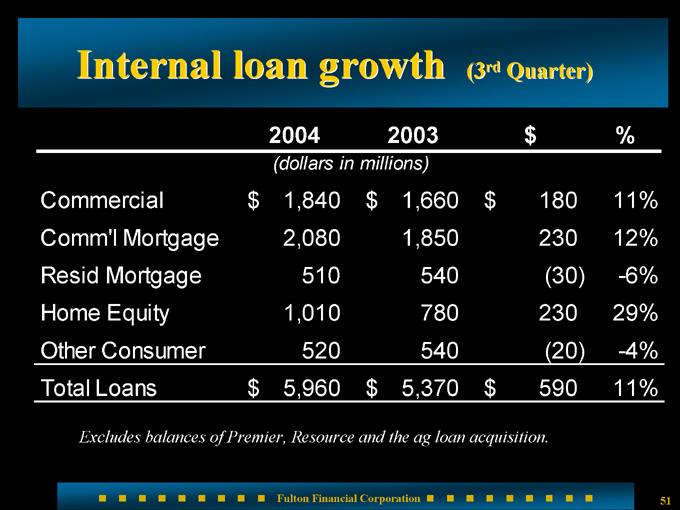

Internal loan growth (3rd Quarter)

2004 2003 $ %

(dollars in millions)

Commercial $1,840 $1,660 $180 11%

Comm’l Mortgage 2,080 1,850 230 12%

Resid Mortgage 510 540 (30) -6%

Home Equity 1,010 780 230 29%

Other Consumer 520 540 (20) -4%

Total Loans $5,960 $5,370 $590 11%

Excludes balances of Premier, Resource and the ag loan acquisition.

51

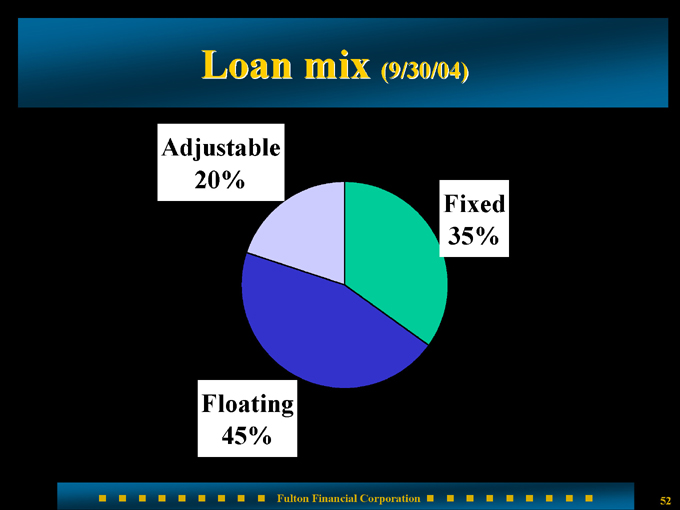

Loan mix (9/30/04)

Adjustable 20%

Fixed 35%

Floating 45%

52

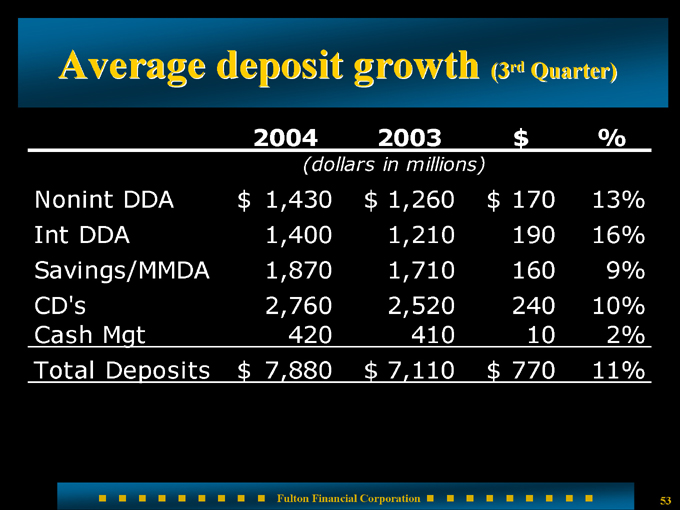

Average deposit growth (3rd Quarter)

2004 2003 $ %

(dollars in millions)

Nonint DDA $1,430 $1,260 $170 13%

Int DDA 1,400 1,210 190 16%

Savings/MMDA 1,870 1,710 160 9%

CD’s 2,760 2,520 240 10%

Cash Mgt 420 410 10 2%

Total Deposits $7,880 $7,110 $770 11%

53

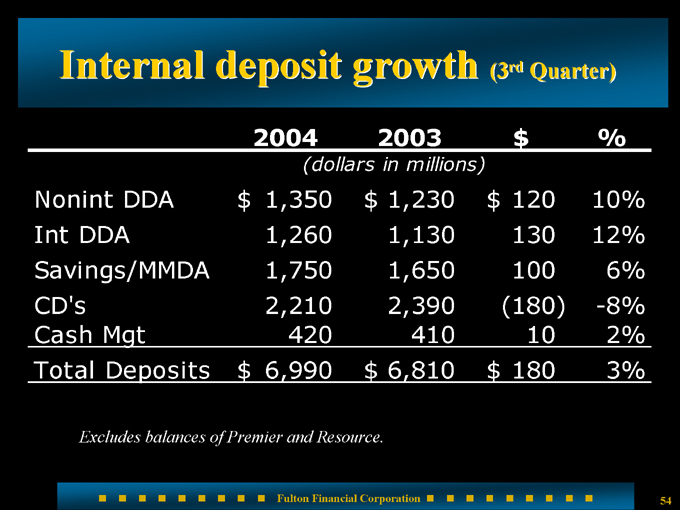

Internal deposit growth (3rd Quarter)

2004 2003 $ %

(dollars in millions)

Nonint DDA $1,350 $1,230 $120 10%

Int DDA 1,260 1,130 130 12%

Savings/MMDA 1,750 1,650 100 6%

CD’s 2,210 2,390 (180) -8%

Cash Mgt 420 410 10 2%

Total Deposits $6,990 $6,810 $180 3%

Excludes balances of Premier and Resource.

54

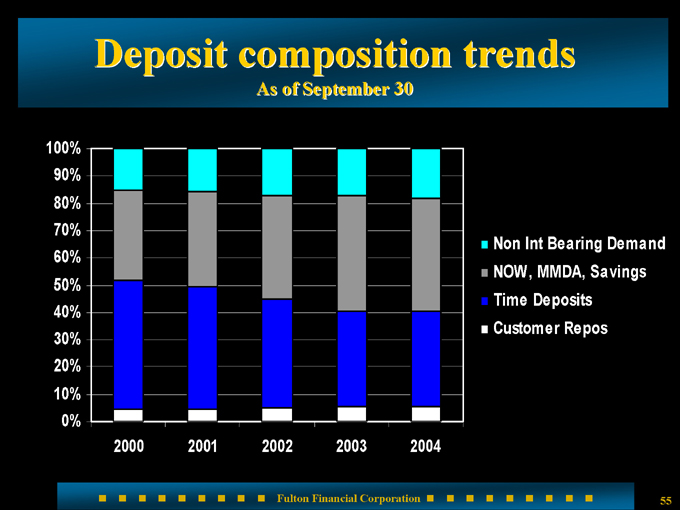

Deposit composition trends

As of September 30

100% 90% 80% 70% 60% 50% 40% 30% 20% 10% 0%

2000 2001 2002 2003 2004

Non Int Bearing Demand NOW, MMDA, Savings Time Deposits Customer Repos

55

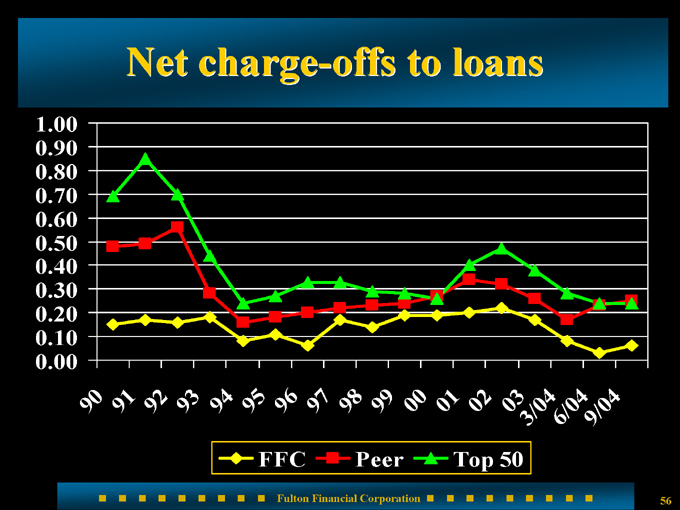

Net charge-offs to loans

1.00 0.90 0.80 0.70 0.60 0.50

0.40 0.30 0.20 0.10 0.00

90

91 92 93

94 95 96 97

98 99 00 01

02

3/04 03

6/04 9/04

FFC Peer Top 50

56

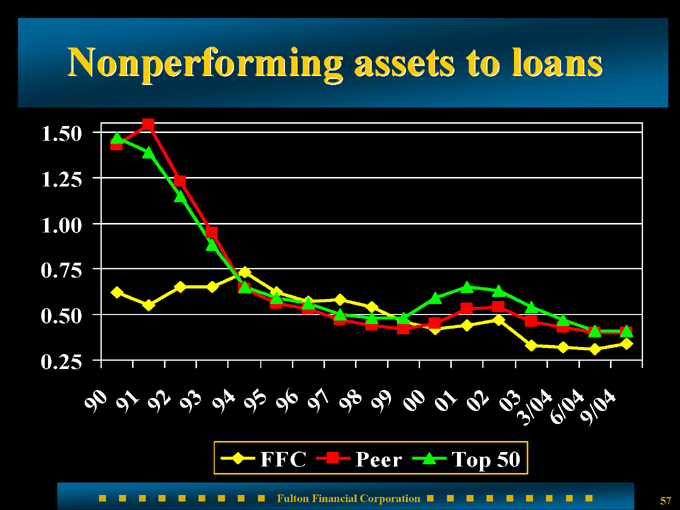

Nonperforming assets to loans

1.50 1.25

1.00 0.75 0.50 0.25

90 91 92

93

94 95 96 97 98 99 00 01

02 03

3/04 6/04 9/04

FFC Peer Top 50

57

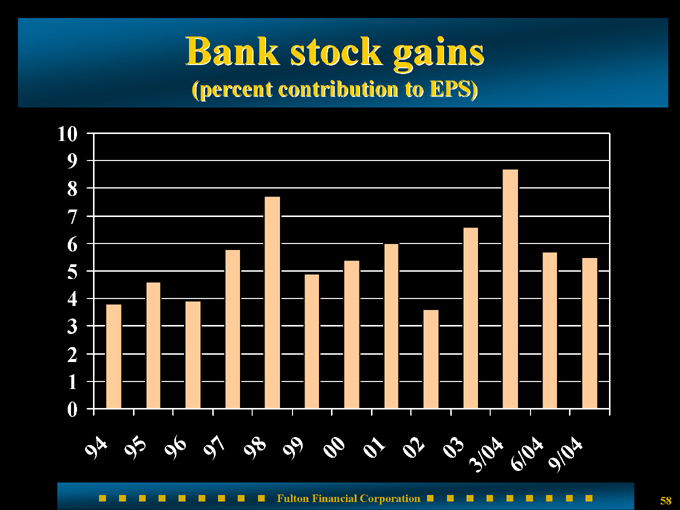

Bank stock gains

(percent contribution to EPS)

10 9 8 7 6 5 4 3 2 1 0

94 95 96

97 98 99 00 01

02 03

3/04 6/04 9/04

58

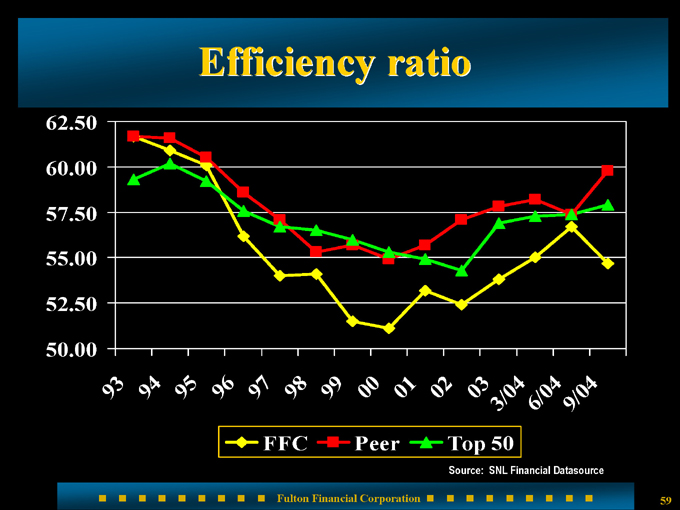

Efficiency ratio

62.50 60.00 57.50 55.00 52.50 50.00

93 94

95 96

97 98

99 00 01

02

03 3/04 6/04

9/04

FFC Peer Top 50

Source: SNL Financial Datasource

59

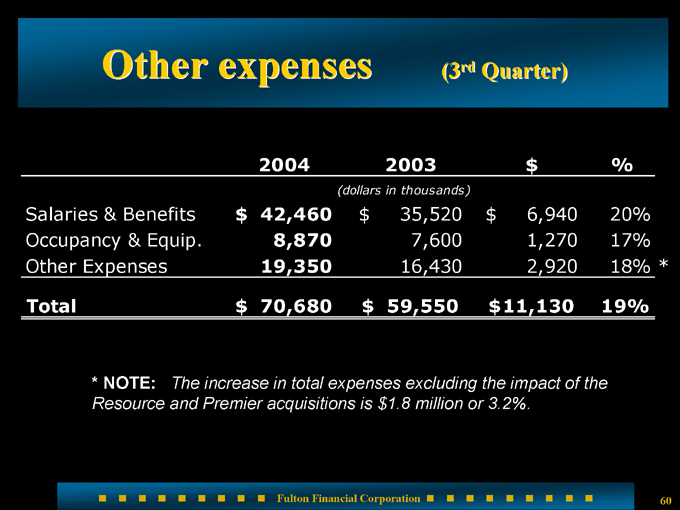

Other expenses (3rd Quarter)

2004 2003 $ %

(dollars in thousands)

Salaries & Benefits $42,460 $35,520 $6,940 20%

Occupancy & Equip. 8,870 7,600 1,270 17%

Other Expenses 19,350 16,430 2,920 18%*

Total $70,680 $59,550 $11,130 19%

* NOTE: The increase in total expenses excluding the impact of the Resource and Premier acquisitions is $1.8 million or 3.2%.

60

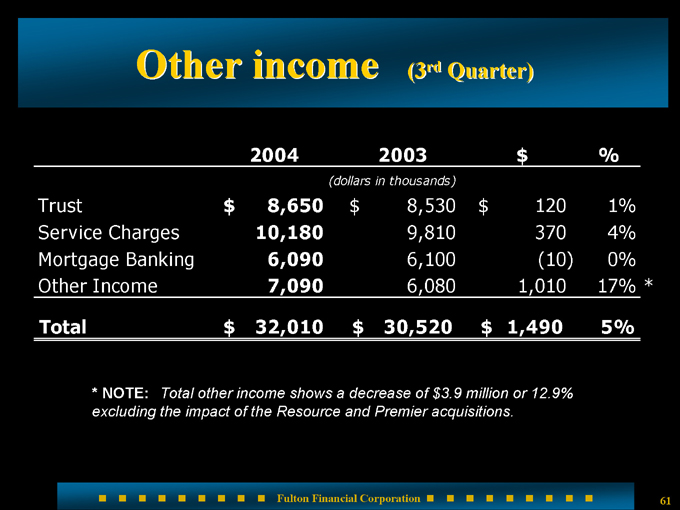

Other income (3rd Quarter)

2004 2003 $ %

(dollars in thousands)

Trust $8,650 $8,530 $120 1%

Service Charges 10,180 9,810 370 4%

Mortgage Banking 6,090 6,100 (10) 0%

Other Income 7,090 6,080 1,010 17% *

Total $32,010 $30,520 $1,490 5%

* NOTE: Total other income shows a decrease of $3.9 million or 12.9% excluding the impact of the Resource and Premier acquisitions.

61

Looking ahead

Continued focus on:

Strong asset quality

Growth in net interest margin Growth in non-interest income

Expansion of franchise geographically Increased loan activity Core deposit growth

62

Overview

Shareholders maximize shareholder value

Customers create financial success

Employees create career success

Communities create prosperity

63

Fulton Financial Corporation

One Penn Square Lancaster, PA 17602

www.fult.com

64