SCHEDULE 14A

Proxy Statement Pursuant to Section 14(a)

of the Securities Exchange Act of 1934

(Amendment No. __)

Filed by the Registrant o

Filed by a Party other than the Registrant x

Check the appropriate box:

| o | Preliminary Proxy Statement |

| o | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) |

| o | Definitive Proxy Statement |

| x | Definitive Additional Materials |

| o | Soliciting Material Pursuant to § 240.14a-12 |

Mentor Graphics Corporation

(Name of Registrant as Specified In Its Charter)

Icahn Partners LP

Icahn Partners Master Fund LP

Icahn Partners Master Fund II LP

Icahn Partners Master Fund III LP

High River Limited Partnership

Hopper Investments LLC

Barberry Corp.

Icahn Onshore LP

Icahn Offshore LP

Icahn Capital L.P.

IPH GP LLC

Icahn Enterprises Holdings L.P.

Icahn Enterprises G.P. Inc.

Beckton Corp.

Carl C. Icahn

Brett Icahn

David Schechter

Gary Meyers

José Maria Alapont

(Name of Person(s) Filing Proxy Statement, if other than the Registrant)

Payment of Filing Fee (check the appropriate box):

| o | Fee computed on table below per Exchange Act Rule 14a-6(i)(4) and 0-11. |

| | 1) | Title of each class of securities to which transaction applies: |

| | 2) | Aggregate number of securities to which transaction applies: |

| | 3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): |

| | 4) | Proposed maximum aggregate value of transaction: |

| o | Fee paid previously with preliminary materials. |

| o | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. |

| | 1) | Amount Previously Paid: |

| | 2) | Form, Schedule or Registration Statement No.: |

Mentor Graphics Icahn Presentat ion to ISS 4/12/11 1

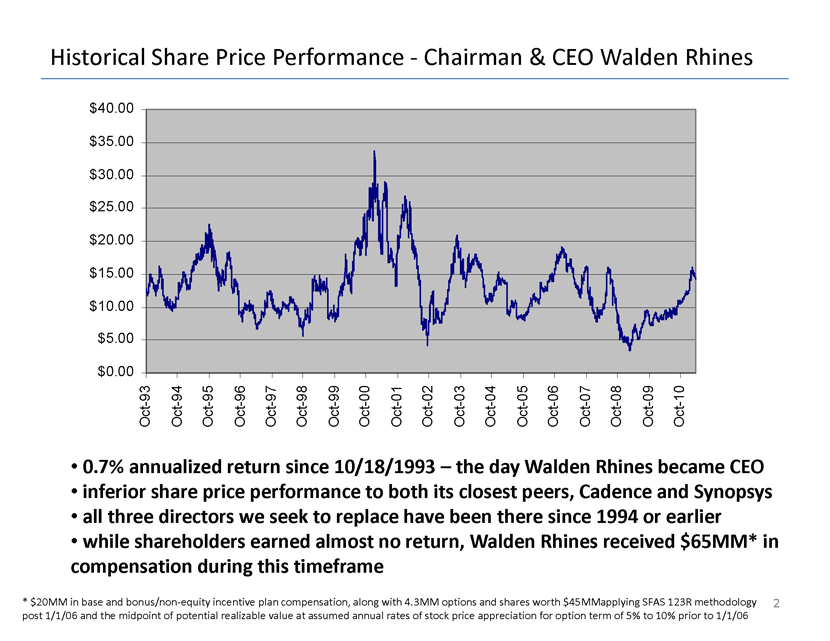

Historical Share Price Performance-Chairman & CEO Walden Rhines $40.00 $35.00 $30.00 $25.00 $20.00 $15.00 $10.00 $5.00 $0.00 3 4 5 6 7 8 9 0 1 2 3 4 5 6 7 8 9 0 9 9 9 9 9 9 9 0 0 0 0 0 0 0 0 0 0 1------------------Oct Oct Oct Oct Oct Oct Oct Oct Oct Oct Oct Oct Oct Oct Oct Oct Oct Oct • 0.7% annualized return since 10/18/1993 – the day Walden Rhines became CEO • inferior share price performance to both its closest peers, Cadence and Synopsys • all three directors we seek to replace have been there since 1994 or earlier • while shareholders earned almost no return, Walden Rhines received $65MM* in compensation during this timeframe * $20MM in base and bonus/non-equity incentive plan compensation, along with 4.3MM options and shares worth $45MMapplying SFAS 123R methodology 2 post 1/1/06 and the midpoint of potential realizable value at assumed annual rates of stock price appreciation for option term of 5% to 10% prior to 1/1/06

We Expect our Nominees to Pursue a Sale of the Company • we seek minority representation on the Board of Mentor Graphics – three out of eight seats • subject to fiduciary duties-we expect our nominees if elected, to advocate for a sale of the Company despite the Board’s rejection of Icahn’s proposal • Icahn offered $17 per share in cash subject only to cursory due diligence and the absence of anti-takeover devices-without any breakup fees-so that the Company could pursue a bid from a strategic acquirer with the safety of downside protection from our $17 per share offer • Icahn strongly believes strategic acquirers may be able to offer a superior price to $17 per share considering their ability to possibly realize significant cost synergies and the strong strategic rationale even for the Company’s closest peers (see pages 4 and 5) 3

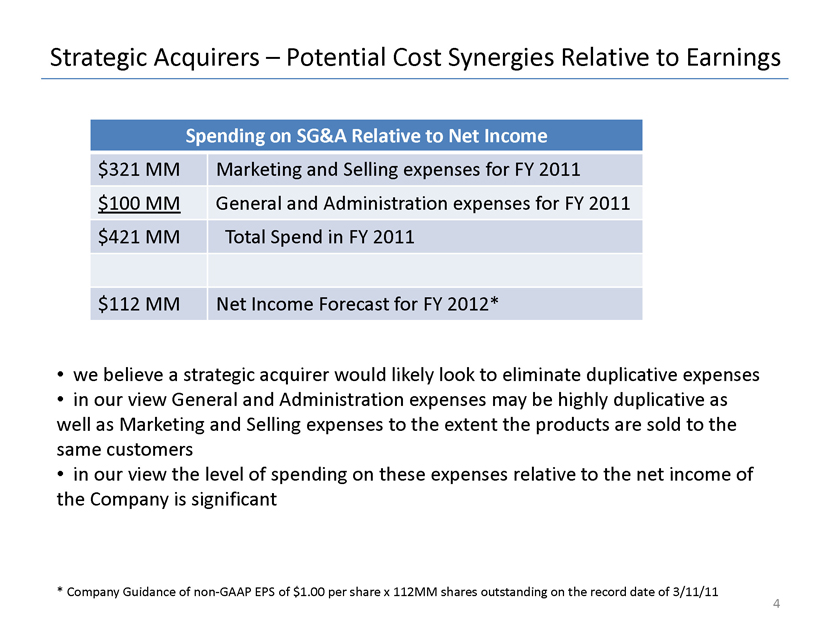

Strategic Acquirers – Potential Cost Synergies Relative to Earnings Spending on SG&A Relative to Net Income $321 MM Marketing and Selling expenses for FY 2011 $100 MM General and Administration expenses for FY 2011 $421 MM Total Spend in FY 2011 $112 MM Net Income Forecast for FY 2012* • we believe a strategic acquirer would likely look to eliminate duplicative expenses • in our view General and Administration expenses may be highly duplicative as well as Marketing and Selling expenses to the extent the products are sold to the same customers • in our view the level of spending on these expenses relative to the net income of the Company is significant * Company Guidance of non-GAAP EPS of $1.00 per share x 112MM shares outstanding on the record date of 3/11/11 4

Strategic Acquirers-Rationale is Clear • Mentor deemed Synopsys and Cadence “logical strategic buyers” • These “logical strategic buyers” are attempting to focus on end-to-end solutions with software tools that engineers use throughout the different steps required to design chips for semiconductor companies • Uniquely, Mentor has focused more narrowly on designing software tools for certain of these steps where it is dominant such as the Calibre tool family-a standard for most of the world’s largest semiconductor companies • Mentor has leveraged its R&D capabilities into integrated system design and new and emerging products that include embedded software and applications in markets such as automotive and aerospace • Due to the difference in strategy, Mentor’s focus on adjacent markets and on products where it is dominant such as Calibre, several of Mentor ’s key products represent adjacencies to these “logical strategic buyers” • Beyond the “logical strategic buyers” mentioned above, it is our belief that other strategic buyers that compete in the CAD market (computer aided design) and in the semiconductor manufacturing market may express an interest 5

Strategic Acquirers-Regulatory Risk • Mentor’s board publicly prejudged the feasibility of a third party combination highlighting “serious regulatory risks associated with a combination with either Cadence or Synopsys ” • This differs from the view expressed by Cadence in 2008: “we and our advisors have carefully analyzed the combination of Cadence and Mentor Graphics and are confident that the proposed transaction will receive the necessary regulatory approvals” • To the extent the FTC or the DOJ finds issues with certain product overlaps, such products may be divested to meet whatever standard is required • This Board could manage any such risk with a large reverse break up fee to the extent there are any significant issues, though we do not believe this scenario is likely 6

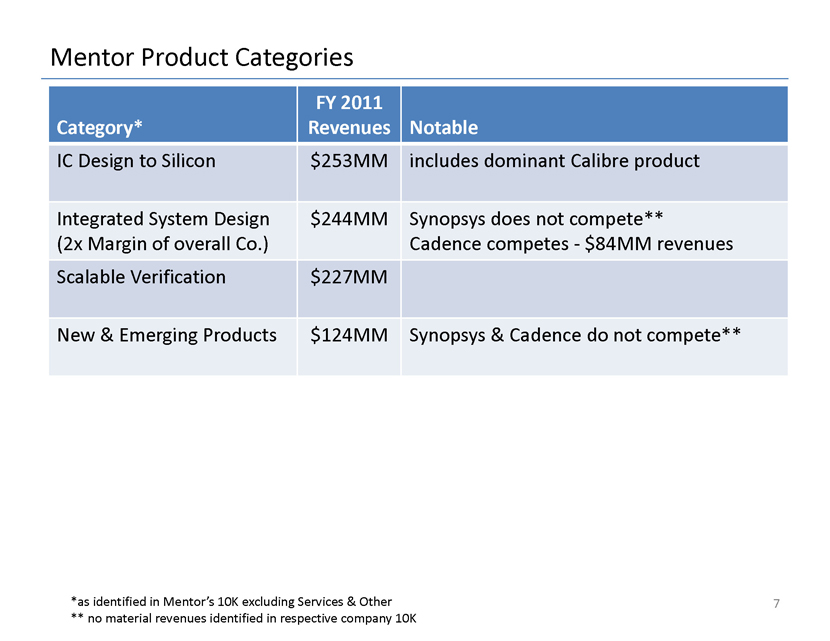

Mentor Product Categories FY 2011 Category* Revenues Notable IC Design to Silicon $253MM includes dominant Calibre product Integrated System Design $244MM Synopsys does not compete** (2x Margin of overall Co.) Cadence competes-$84MM revenues Scalable Verification $227MM New & Emerging Products $124MM Synopsys & Cadence do not compete** *as identified in Mentor’s 10K excluding Services & Other 7 ** no material revenues identified in respective company 10K

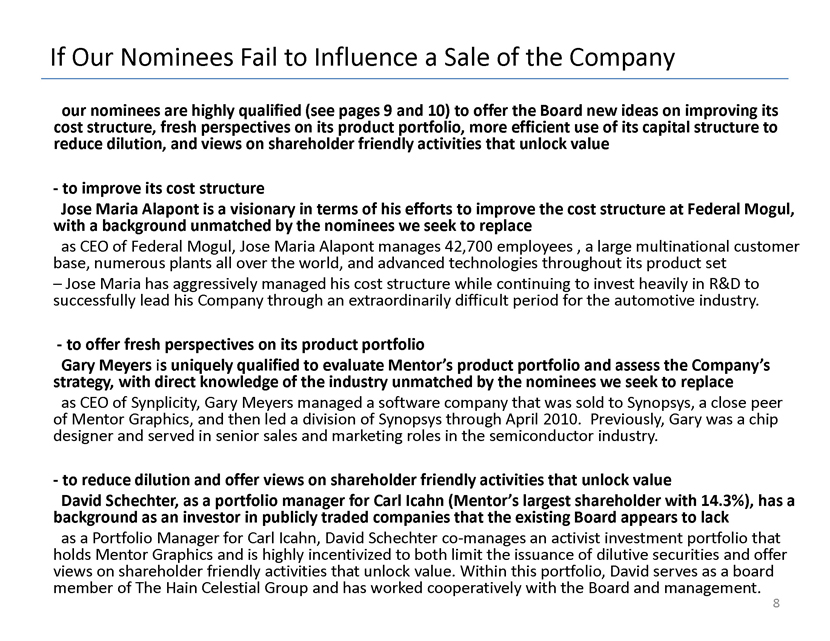

If Our Nominees Fail to Influence a Sale of the Company our nominees are highly qualified (see pages 9 and 10) to offer the Board new ideas on improving its cost structure, fresh perspectives on its product portfolio, more efficient use of its capital structure to reduce dilution, and views on shareholder friendly activities that unlock value ]to improve its cost structure Jose Maria Alapont is a visionary in terms of his efforts to improve the cost structure at Federal Mogul, with a background unmatched by the nominees we seek to replace as CEO of Federal Mogul, Jose Maria Alapont manages 42,700 employees , a large multinational customer base, numerous plants all over the world, and advanced technologies throughout its product set – Jose Maria has aggressively managed his cost structure while continuing to invest heavily in R&D to successfully lead his Company through an extraordinarily difficult period for the automotive industry . ]to offer fresh perspectives on its product portfolio Gary Meyers is uniquely qualified to evaluate Mentor’s product portfolio and assess the Company’s strategy, with direct knowledge of the industry unmatched by the nominees we seek to replace as CEO of Synplicity , Gary Meyers managed a software company that was sold to Synopsys , a close peer of Mentor Graphics, and then led a division of Synopsys through April 2010. Previously, Gary was a chip designer and served in senior sales and marketing roles in the semiconductor industry . ]to reduce dilution and offer views on shareholder friendly activities that unlock value David Schechter, as a portfolio manager for Carl Icahn (Mentor’s largest shareholder with 14.3%), has a background as an investor in publicly traded companies that the existing Board appears to lack as a Portfolio Manager for Carl Icahn, David Schechter co-manages an activist investment portfolio that holds Mentor Graphics and is highly incentivized to both limit the issuance of dilutive securities and offer views on shareholder friendly activities that unlock value. Within this portfolio, David serves as a board member of The Hain Celestial Group and has worked cooperatively with the Board and management . 8

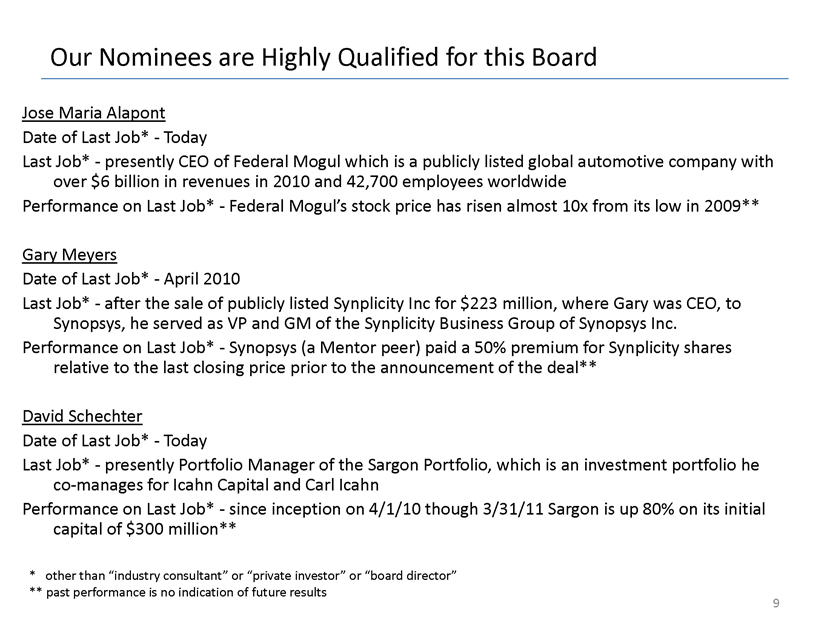

Our Nominees are Highly Qualified for this Board Jose Maria Alapont Date of Last Job*-Today Last Job* ]presently CEO of Federal Mogul which is a publicly listed global automotive company with over $6 billion in revenues in 2010 and 42,700 employees worldwide Performance on Last Job*-Federal Mogul’s stock price has risen almost 10x from its low in 2009** Gary Meyers Date of Last Job*-April 2010 Last Job*-after the sale of publicly listed Synplicity Inc for $223 million, where Gary was CEO, to Synopsys , he served as VP and GM of the Synplicity Business Group of Synopsys Inc. Performance on Last Job*-Synopsys (a Mentor peer) paid a 50% premium for Synplicity shares relative to the last closing price prior to the announcement of the deal** David Schechter Date of Last Job*-Today Last Job*-presently Portfolio Manager of the Sargon Portfolio, which is an investment portfolio he co-manages for Icahn Capital and Carl Icahn Performance on Last Job*-since inception on 4/1/10 though 3/31/11 Sargon is up 80% on its initial capital of $300 million** * other than “industry consultant” or “private investor” or “board director” ** past performance is no indication of future results 9

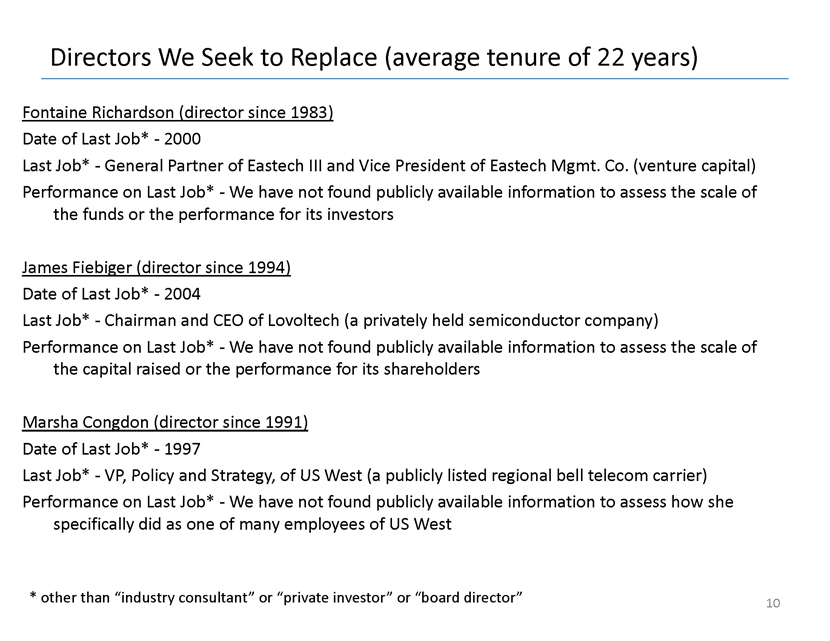

Directors We Seek to Replace (average tenure of 22 years) Fontaine Richardson (director since 1983) Date of Last Job*-2000 Last Job*-General Partner of Eastech III and Vice President of Eastech Mgmt. Co. (venture capital) Performance on Last Job*-We have not found publicly available information to assess the scale of the funds or the performance for its investors James Fiebiger (director since 1994) Date of Last Job*-2004 Last Job*-Chairman and CEO of Lovoltech (a privately held semiconductor company) Performance on Last Job*-We have not found publicly available information to assess the scale of the capital raised or the performance for its shareholders Marsha Congdon (director since 1991) Date of Last Job*-1997 Last Job* ]VP, Policy and Strategy , of US West (a publicly listed regional bell telecom carrier) Performance on Last Job*-We have not found publicly available information to assess how she specifically did as one of many employees of US West * other than “industry consultant” or “private investor” or “board director” 10

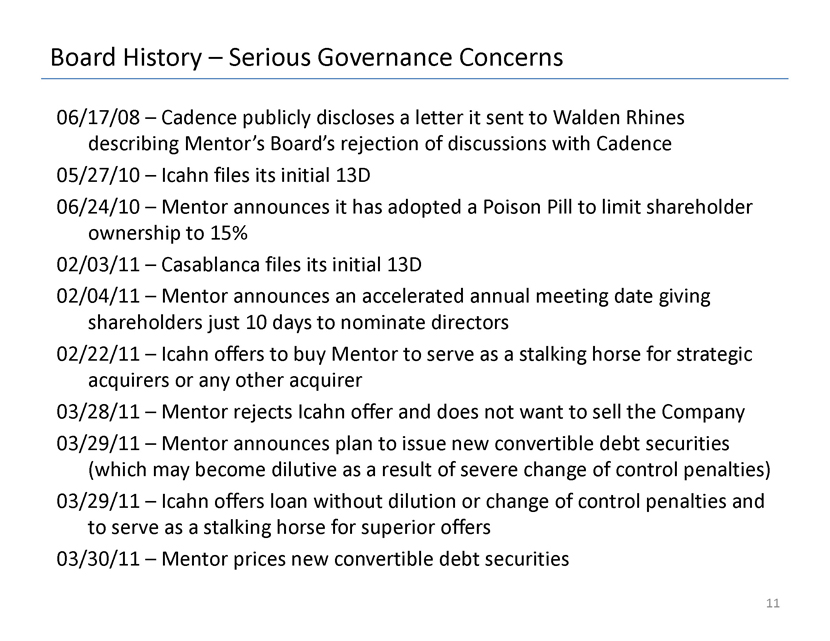

Board History – Serious Governance Concerns 06/17/08 – Cadence publicly discloses a letter it sent to Walden Rhines describing Mentor’s Board’s rejection of discussions with Cadence 05/27/10 – Icahn files its initial 13D 06/24/10 – Mentor announces it has adopted a Poison Pill to limit shareholder ownershi p to 15% 02/03/11 – Casablanca files its initial 13D 02/04/11 – Mentor announces an accelerated annual meeting date giving shareholders just 10 days to nominate directors 02/22/11 – Icahn offers to buy Mentor to serve as a stalking horse for strategic acquirers or any other acquirer 03/28/11 – Mentor rejects Icahn offer and does not want to sell the Company 03/29/11 – Mentor announces plan to issue new convertible debt securities (which may become dilutive as a result of severe change of control penalties) 03/29/11 – Icahn offers loan without dilution or change of control penalties and to serve as a stalking horse for superior offers 03/30/11 – Mentor prices new convertible debt securities 11

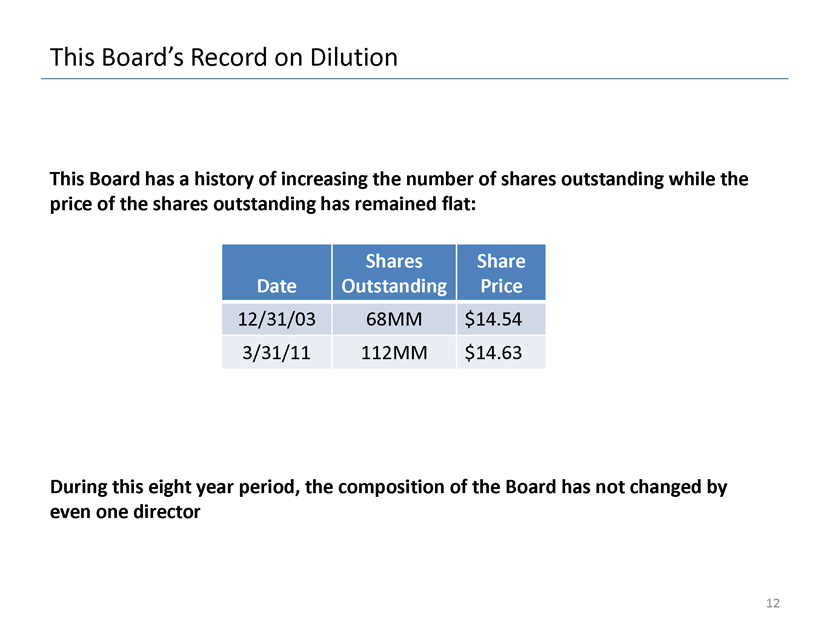

This Board’s Record on Dilution This Board has a history of increasing the number of shares outstanding while the price of the shares outstanding has remained flat: Shares Share Date Outstanding Price 12/31/03 68MM $14.54 3/31/11 112MM $14.63 During this eight year period, the composition of the Board has not changed by even one director 12

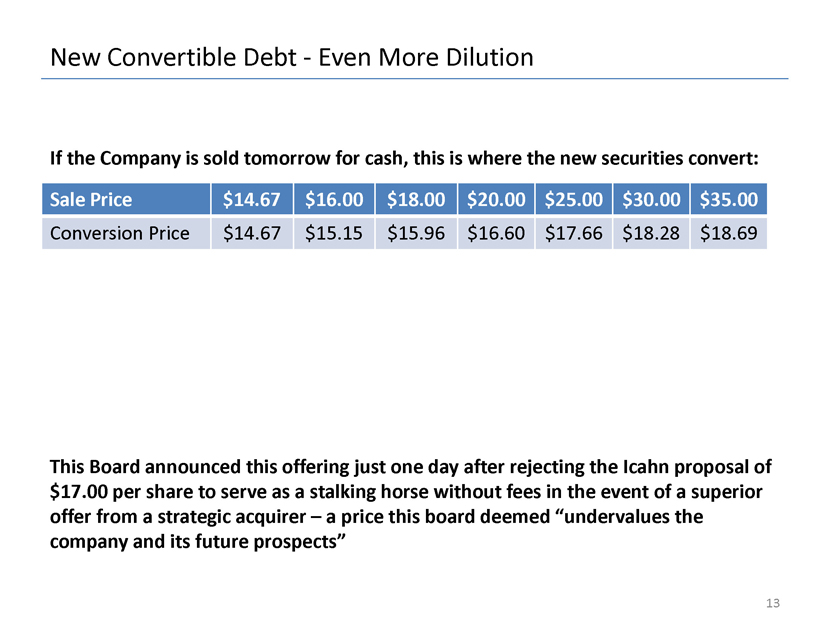

New Convertible Debt-Even More Dilution If the Company is sold tomorrow for cash, this is where the new securities convert: Sale Price $14.67 $16.00 $18.00 $20.00 $25.00 $30.00 $35.00 Conversion Price $14.67 $15.15 $15.96 $16.60 $17.66 $18.28 $18.69 This Board announced this offering just one day after rejecting the Icahn proposal of $17.00 per share to serve as a stalking horse without fees in the event of a superior offer from a strategic acquirer – a price this board deemed “undervalues the company and its future prospects” 13

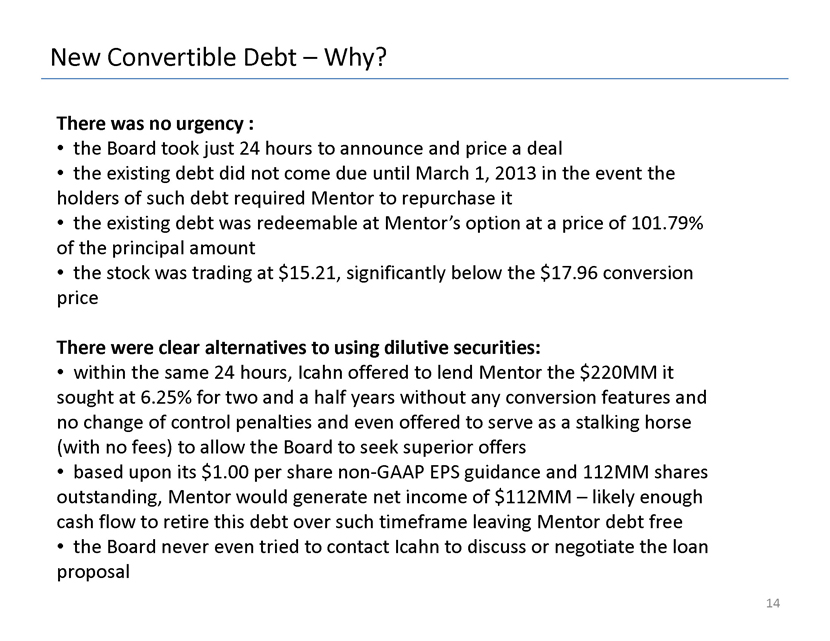

New Convertible Debt – Why? There was no urgency : • the Board took just 24 hours to announce and price a deal • the existing debt did not come due until March 1, 2013 in the event the holders of such debt required Mentor to repurchase it • the existing debt was redeemable at Mentor’s option at a price of 101.79% of the principal amount • the stock was trading at $15.21, significantly below the $17.96 conversion price There were clear alternatives to using dilutive securities: • within the same 24 hours, Icahn offered to lend Mentor the $220MM it sought at 6.25% for two and a half years without any conversion features and no change of control penalties and even offered to serve as a stalking horse (with no fees) to allow the Board to seek superior offers • based upon its $1.00 per share non-GAAP EPS guidance and 112MM shares outstanding, Mentor would generate net income of $112MM – likely enough cash flow to retire this debt over such timeframe leaving Mentor debt free • the Board never even tried to contact Icahn to discuss or negotiate the loan proposal 14

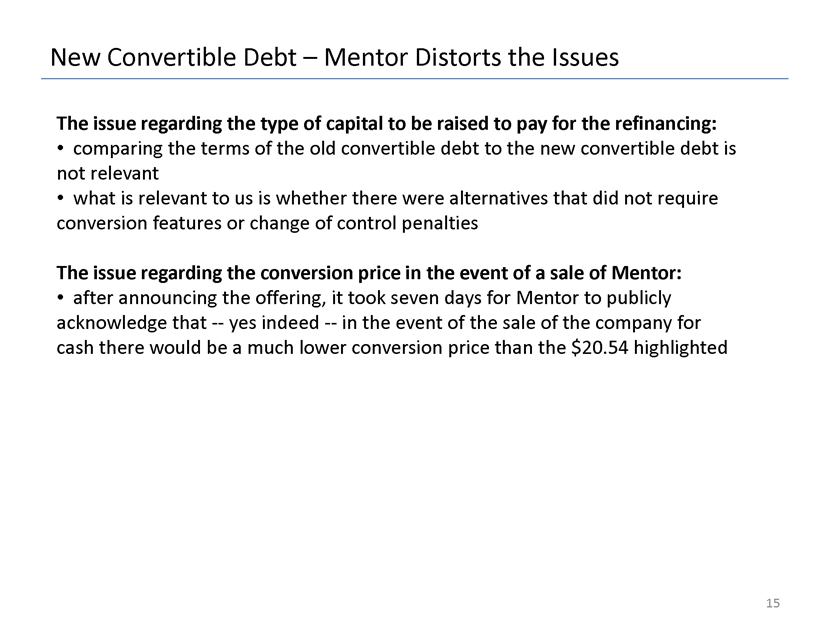

New Convertible Debt – Mentor Distorts the Issues The issue regarding the type of capital to be raised to pay for the refinancing: • comparing the terms of the old convertible debt to the new convertible debt is not relevant • what is relevant to us is whether there were alternatives that did not require conversion features or change of control penalties The issue regarding the conversion price in the event of a sale of Mentor: • after announcing the offering, it took seven days for Mentor to publicly acknowledge that-yes indeed-in the event of the sale of the company for cash there would be a much lower conversion price than the $20.54 highlighted 15

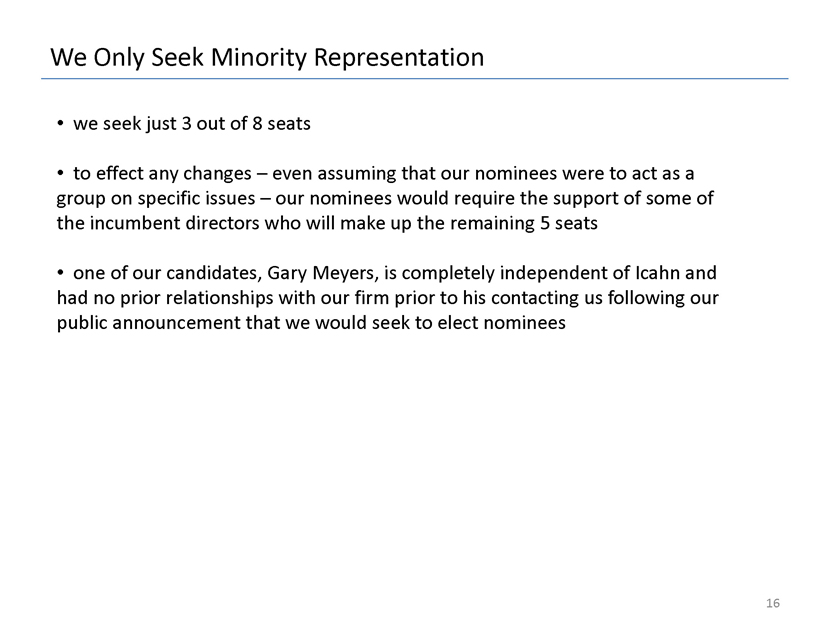

We Only Seek Minority Representation • we seek just 3 out of 8 seats • to effect any changes – even assuming that our nominees were to act as a group on specific issues – our nominees would require the support of some of the incumbent directors who will make up the remaining 5 seats • one of our candidates, Gary Meyers, is completely independent of Icahn and had no prior relationships with our firm prior to his contacting us following our public announcement that we would seek to elect nominees 16

Vote for Our Nominees – the Status Quo is Unacceptable • our nominees are highly qualified with transparent career success from a scale, performance and relevancy perspective • we anticipate that our nominees will advocate for an open and fair sale process so that Mentor may be sold to a strategic acquirer that may benefit from substantial cost synergies, which we believe could lead to a significant premium for shareholders • we question the Board’s history regarding a sale of the company in light of the introduction of a poison pill, accelerating the annual meeting (thereby giving shareholders just 10 days to nominate directors), the unwillingness to negotiate a merger with Cadence in 2008, the rejection of our $17 per share offer followed the next day by the issuance of potentially dilutive securities • we seek a minority position on the board (3 out of 8) and therefore our nominees will have no ability to effectuate any change without the support of some incumbent directors • the candidates we seek to replace have been on the board for an average tenure of 22 years, with one director on the board since 1983 • we expect that our nominees will provide improved board oversight to limit the dilution of shareholders caused by repeated stock issuances, and will also seek to more aggressively control costs • we believe that it is unacceptable to be satisfied with the status quo as only recently has the stock price approached the level it traded at following the arrival of Walden Rhines, Chairman and CEO, 17 years ago 17

Exhibits • Cadence Goes Hostile-Letter to Mentor • Initial Icahn 13D • Mentor puts in Poison Pill • Initial Casablanca 13D • Mentor Announcement of Meeting Date • Casablanca 13D – disclosin g intent to nominate board members • Icahn 13D – disclosing intent to nominate board members and saying Company should be sold to a strategic acquirer • Icahn 13D – announcing stalking horse offer for company with no breakup fees if sold to strategic • Casablanca 13D – withdrawing nominees and supporting Icahn nominees • Mentor Rejection of Icahn Offer and idea of putting company up for sale • Mentor Announcement of Dilutive Securities • Icahn Asks Mentor to withdraw Offering • Icahn Offer of Non Dilutive Financing to serve as stalking horse with no fees if superior alternative • Mentor

Important Disclosures These materials are based solely on information contained in the public domain . We have relied upon and assumed, have not attempted to independently investigate or verify, and do not assume any responsibility for, the accuracy, completeness or reasonableness of such information . No representation or warranty, express or implied, is made as to the accuracy or completeness of any information included or otherwise used herein, and nothing contained herein is, or shall be relied upon as, a representation or warranty, whether as to the past, the present or the future. These materials are necessarily based upon information available to us, and financial, stock market and other existing conditions and circumstances that are known to us, as of the date of these materials . We do not have any obligation to update or otherwise revise these materials . The information contained in these materials does not purport to be an appraisal of any of the assets or liabilities of Mentor Graphics or any of its business units or subsidiaries, or any other companies mentioned herein, and does not express any opinion as to the price at which the securities of any such entities may trade at any time. The information and opinions provided in these materials take no account of any investor's individual circumstances and should not be taken as specific advice on the merits of any investment decision . Moreover , nothing contained herein should be construed as providing any legal, tax or accounting advice, and you are encouraged to consult with your legal, tax, accounting and investment advisors . You should consider these materials as only one of many factors to be considered in making any investment or other decisions . We do not accept any liability whatsoever for any direct or consequential loss howsoever arising, directly or indirectly, from any use of these materials . ON APRIL 1, 2011, CARL C. ICAHN AND AFFILIATES (“ICAHN”) FILED A DEFINITIVE PROXY STATEMENT WITH THE SECURITIES AND EXCHANGE COMMISSION (THE "SEC") IN CONNECTION WITH THE UPCOMING 2011 ANNUAL MEETING OF SHAREHOLDERS OF MENTOR GRAPHICS . SHAREHOLDERS ARE ADVISED TO READ ICAHN'S DEFINITIVE PROXY STATEMENT, AND ANY OTHER RELEVANT DOCUMENTS FILED BY ICAHN WITH THE SEC, BEFORE MAKING ANY VOTING OR INVESTMENT DECISION BECAUSE THEY CONTAIN IMPORTANT INFORMATION . THE DEFINITIVE PROXY STATEMENT IS, AND ANY OTHER RELEVANT DOCUMENTS AND OTHER MATERIAL FILED BY ICAHN WITH THE SEC CONCERNING MENTOR GRAPHICS WILL BE, WHEN FILED, AVAILABLE FREE OF CHARGE AT HTTP://WWW .SEC.GOV AND WWW.READMATERIAL .COM/MENTOR . IN ADDITION, COPIES OF THE PROXY MATERIALS MAY BE REQUESTED FROM ICAHN'S PROXY SOLICITOR, D.F. KING & CO., INC., BY TELEPHONE AT (800) 714 3313.19

Pricing of Dilutive Securities • Mentor Explanation of “strong investor support” • Icahn asks Mentor to disclose publicly the sub rosa “make whole” provisions 18