Exhibit 99.1

Kinross Gold Corporation

management’s discussion and analysis

For the year ended December 31, 2024

This management's discussion and analysis ("MD&A"), prepared as of February 12, 2025, relates to the financial condition and results of operations of Kinross Gold Corporation together with its wholly owned subsidiaries, as at December 31, 2024 and for the year then ended, and is intended to supplement and complement Kinross Gold Corporation’s audited annual consolidated financial statements for the year ended December 31, 2024 and the notes thereto (the “financial statements”). Readers are cautioned that the MD&A contains forward-looking statements about expected future events and financial and operating performance of the Company, and that actual events may vary from management's expectations. Readers are encouraged to read the Cautionary Statement on Forward Looking Information included with this MD&A and to consult Kinross Gold Corporation's financial statements and corresponding notes to the financial statements which are available on the Company's web site at www.kinross.com and on www.sedarplus.ca. The financial statements and MD&A are presented in U.S. dollars. The financial statements have been prepared in accordance with International Financial Reporting Standards (“IFRS”) as issued by the International Accounting Standards Board (“IASB”). This discussion addresses matters we consider important for an understanding of our financial condition and results of operations as at and for the year ended December 31, 2024, as well as our outlook.

This MD&A contains forward-looking statements and should be read in conjunction with the risk factors described in "Risk Analysis" on pages 32 – 44 and in the “Cautionary Statement on Forward-Looking Information” on pages 53 – 54 of this MD&A. For additional discussion of risk factors, please refer to the Company's Annual Information Form for the year ended December 31, 2023, which is available on the Company's website www.kinross.com and on www.sedarplus.ca. In certain instances, references are made to relevant notes in the financial statements for additional information.

This MD&A references adjusted net earnings attributable to common shareholders, adjusted net earnings per share, attributable adjusted operating cash flow, attributable free cash flow, attributable all-in sustaining cost per equivalent ounce sold and per ounce sold on a by-product basis, attributable all-in cost per equivalent ounce sold and per ounce sold on a by-product basis, attributable average realized gold price per ounce, and attributable production cost of sales per equivalent ounce sold, all of which are non-GAAP financial measures or ratios. The definitions and reconciliations of these non-GAAP financial measures and ratios are included in Section 11 of this MD&A.

Where we say "we", "us", "our", the "Company" or "Kinross", we mean Kinross Gold Corporation or Kinross Gold Corporation and/or one or more or all of its subsidiaries, as it may apply. Where we refer to the "industry", we mean the gold mining industry.

1

Kinross Gold Corporation

management’s discussion and analysis

For the year ended December 31, 2024

| 1. | DESCRIPTION OF THE BUSINESS |

Kinross is engaged in gold mining and related activities, including exploration and acquisition of gold-bearing properties, the extraction and processing of gold-containing ore, and reclamation of gold mining properties. Kinross’ gold production and exploration activities are carried out principally in Canada, the United States, Brazil, Chile, Mauritania and Finland. Gold is produced in the form of doré, which is shipped to refineries for final processing. Kinross also produces and sells a quantity of silver.

The profitability and operating cash flow of Kinross are affected by various factors, including the amount of gold and silver produced, the market prices of gold and silver, operating costs, interest rates, regulatory and environmental compliance, the level of exploration activity and capital expenditures, general and administrative costs, and other discretionary costs and activities. Kinross is also exposed to fluctuations in currency exchange rates, political risks, and varying levels of taxation that can impact profitability and cash flow. Kinross seeks to manage the risks associated with its business operations; however, many of the factors affecting these risks are beyond the Company’s control.

Commodity prices continue to be volatile as economies around the world continue to experience economic challenges along with political changes and uncertainties. Volatility in the price of gold and silver impacts the Company's revenue, while volatility in the price of input costs, such as oil, and foreign exchange rates, particularly the Brazilian real, Chilean peso, Mauritanian ouguiya and Canadian dollar, may have an impact on the Company's operating costs and capital expenditures.

Segment Profile

Each of the Company's significant operating mines is generally considered to be a separate segment. The reportable segments are those operations whose operating results are reviewed by the chief operating decision maker to make decisions about resources to be allocated to the segment and assess its performance.

| Ownership percentage at December 31, | ||||||||||||||||

| Operating Segments | Operator | Location | 2024 | 2023 | ||||||||||||

| Tasiast | Kinross | Mauritania | 100% | 100% | ||||||||||||

| Paracatu | Kinross | Brazil | 100% | 100% | ||||||||||||

| La Coipa | Kinross | Chile | 100% | 100% | ||||||||||||

| Fort Knox(a) | Kinross | USA | 100%/70% | 100%/70% | ||||||||||||

| Round Mountain | Kinross | USA | 100% | 100% | ||||||||||||

| Bald Mountain | Kinross | USA | 100% | 100% | ||||||||||||

| (a) | The Fort Knox segment includes the 100%-owned Fort Knox mine and 70%-owned Manh Choh mine. |

2

Kinross Gold Corporation

management’s discussion and analysis

For the year ended December 31, 2024

Consolidated Financial and Operating Highlights

| Years ended December 31, | 2024 vs. 2023 | 2023 vs. 2022 | ||||||||||||||||||||||||||

| (in millions, except ounces, per share amounts and per ounce amounts) | 2024 | 2023 | 2022(g) | Change | % Change(h) | Change | % Change(h) | |||||||||||||||||||||

| Operating Highlights(a) | ||||||||||||||||||||||||||||

| Total gold equivalent ounces(b) | ||||||||||||||||||||||||||||

| Produced | 2,170,791 | 2,153,020 | 1,957,237 | 17,771 | 1 | % | 195,783 | 10 | % | |||||||||||||||||||

| Sold | 2,153,212 | 2,179,936 | 1,927,818 | (26,724 | ) | (1 | )% | 252,118 | 13 | % | ||||||||||||||||||

| Attributable gold equivalent ounces(b) | ||||||||||||||||||||||||||||

| Produced | 2,128,052 | 2,153,020 | 1,957,237 | (24,968 | ) | (1 | )% | 195,783 | 10 | % | ||||||||||||||||||

| Sold | 2,111,688 | 2,179,936 | 1,927,818 | (68,248 | ) | (3 | )% | 252,118 | 13 | % | ||||||||||||||||||

| Earnings(a) | ||||||||||||||||||||||||||||

| Metal sales | $ | 5,148.8 | $ | 4,239.7 | $ | 3,455.1 | $ | 909.1 | 21 | % | $ | 784.6 | 23 | % | ||||||||||||||

| Production cost of sales | $ | 2,197.1 | $ | 2,054.4 | $ | 1,805.7 | $ | 142.7 | 7 | % | $ | 248.7 | 14 | % | ||||||||||||||

| Depreciation, depletion and amortization | $ | 1,147.5 | $ | 986.8 | $ | 784.0 | $ | 160.7 | 16 | % | $ | 202.8 | 26 | % | ||||||||||||||

| Impairment (reversal) charge | $ | (74.1 | ) | $ | 38.9 | $ | 350.0 | $ | (113.0 | ) | nm | $ | (311.1 | ) | (89 | )% | ||||||||||||

| Operating earnings | $ | 1,540.3 | $ | 801.4 | $ | 117.7 | $ | 738.9 | 92 | % | $ | 683.7 | nm | |||||||||||||||

| Net earnings attributable to common shareholders | $ | 948.8 | $ | 416.3 | $ | 31.9 | $ | 532.5 | 128 | % | $ | 384.4 | nm | |||||||||||||||

| Basic and diluted earnings per share attributable to common shareholders | $ | 0.77 | $ | 0.34 | $ | 0.02 | $ | 0.43 | 126 | % | $ | 0.32 | nm | |||||||||||||||

| Adjusted net earnings attributable to common shareholders(c) | $ | 838.3 | $ | 539.8 | $ | 283.1 | $ | 298.5 | 55 | % | $ | 256.7 | 91 | % | ||||||||||||||

| Adjusted net earnings per share(c) | $ | 0.68 | $ | 0.44 | $ | 0.22 | $ | 0.24 | 55 | % | $ | 0.22 | 100 | % | ||||||||||||||

| Cash Flow(a) | ||||||||||||||||||||||||||||

| Net cash flow provided from operating activities | $ | 2,446.4 | $ | 1,605.3 | $ | 1,002.5 | $ | 841.1 | 52 | % | $ | 602.8 | 60 | % | ||||||||||||||

| Attributable adjusted operating cash flow(c) | $ | 2,143.1 | $ | 1,676.7 | $ | 1,257.7 | $ | 466.4 | 28 | % | $ | 419.0 | 33 | % | ||||||||||||||

| Capital expenditures(d) | $ | 1,075.5 | $ | 1,098.3 | $ | 764.2 | $ | (22.8 | ) | (2 | )% | $ | 334.1 | 44 | % | |||||||||||||

| Attributable capital expenditures(c) | $ | 1,050.9 | $ | 1,055.0 | $ | 755.0 | $ | (4.1 | ) | (0 | )% | $ | 300.0 | 40 | % | |||||||||||||

| Attributable free cash flow(c) | $ | 1,340.2 | $ | 559.7 | $ | 247.3 | $ | 780.5 | 139 | % | $ | 312.4 | 126 | % | ||||||||||||||

| Per Ounce Metrics(a) | ||||||||||||||||||||||||||||

| Average realized gold price per ounce(e) | $ | 2,393 | $ | 1,945 | $ | 1,793 | $ | 448 | 23 | % | $ | 152 | 8 | % | ||||||||||||||

| Attributable average realized gold price per ounce(c) | $ | 2,391 | $ | 1,945 | $ | 1,793 | $ | 446 | 23 | % | $ | 152 | 8 | % | ||||||||||||||

| Production cost of sales per equivalent ounce(b) sold(f) | $ | 1,020 | $ | 942 | $ | 937 | $ | 78 | 8 | % | $ | 5 | 1 | % | ||||||||||||||

| Attributable production cost of sales per equivalent ounce(b) sold(c) | $ | 1,021 | $ | 942 | $ | 937 | $ | 79 | 8 | % | $ | 5 | 1 | % | ||||||||||||||

| Attributable production cost of sales per ounce sold on a by-product basis(c) | $ | 988 | $ | 892 | $ | 912 | $ | 96 | 11 | % | $ | (20 | ) | (2 | )% | |||||||||||||

| Attributable all-in sustaining cost per equivalent ounce(b) sold(c) | $ | 1,388 | $ | 1,316 | $ | 1,271 | $ | 72 | 5 | % | $ | 45 | 4 | % | ||||||||||||||

| Attributable all-in sustaining cost per ounce sold on a by-product basis(c) | $ | 1,365 | $ | 1,284 | $ | 1,255 | $ | 81 | 6 | % | $ | 29 | 2 | % | ||||||||||||||

| Attributable all-in cost per equivalent ounce(b) sold(c) | $ | 1,739 | $ | 1,634 | $ | 1,545 | $ | 105 | 6 | % | $ | 89 | 6 | % | ||||||||||||||

| Attributable all-in cost per ounce sold on a by-product basis(c) | $ | 1,725 | $ | 1,619 | $ | 1,538 | $ | 106 | 7 | % | $ | 81 | 5 | % | ||||||||||||||

| (a) | All measures and ratios include 100% of the results from Manh Choh, except measures and ratios denoted as “attributable.” “Attributable” measures and ratios include Kinross’ 70% share of Manh Choh production, sales, cash flow, capital expenditures and costs, as applicable. |

| (b) | “Gold equivalent ounces” include silver ounces produced and sold converted to a gold equivalent based on a ratio of the average spot market prices for the commodities for each period. The ratio for 2024 was 84.43:1 (2023 – 83.13:1 and 2022 – 82.90:1). |

| (c) | The definition and reconciliation of these non-GAAP financial measures and ratios is included in Section 11. Non-GAAP financial measures and ratios have no standardized meaning under IFRS and therefore, may not be comparable to similar measures presented by other issuers. |

| (d) | “Capital expenditures” is as reported as “Additions to property, plant and equipment” on the consolidated statements of cash flows. |

| (e) | “Average realized gold price per ounce” is defined as gold revenue divided by total gold ounces sold. |

| (f) | “Production cost of sales per equivalent ounce sold” is defined as production cost of sales divided by total gold equivalent ounces sold. |

| (g) | Results for the year ended December 31, 2022 are from continuing operations and exclude results from the Company’s Chirano and Russian operations due to the classification of these operations as discontinued and their sale in 2022. |

| (h) | “nm” means not meaningful. |

3

Kinross Gold Corporation

management’s discussion and analysis

For the year ended December 31, 2024

Consolidated Financial Performance

2024 vs. 2023

Kinross’ 2024 production of 2,170,791 gold equivalent ounces was comparable to 2023. Higher production from Fort Knox, with the commencement of higher-grade, higher-recovery ore feed from Manh Choh, and higher production from Bald Mountain due to higher grade ore, was offset by lower production from Paracatu due to lower grade ore, in accordance with planned mine sequencing, fewer ounces recovered from the heap leach pads at Round Mountain, as well as lower silver grades and throughput at La Coipa.

Metal sales in 2024 increased by 21% to $5,148.8 million compared to 2023, due to a 23% increase in the average realized gold price to $2,393 per ounce in 2024, from $1,945 per ounce in the prior year. Total gold equivalent ounces sold in 2024 were comparable to 2023.

Production cost of sales and production cost of sales per equivalent ounce sold in 2024 were $2,197.1 million and $1,020, respectively, an increase of 7% and 8%, respectively, compared to 2023, mainly due to the production and sales mix, including higher production at Fort Knox as well as lower production from Paracatu and Round Mountain. Also contributing to the increase were higher royalties as a result of higher realized metal prices, a lower proportion of mining activities related to capital development and higher mill maintenance costs at La Coipa, and higher input costs at Paracatu. These increases were partially offset by favourable foreign exchange rates in Brazil and Chile.

Attributable all-in sustaining cost per equivalent ounce sold and per ounce sold on a by-product basis increased by 5% and 6%, respectively, and attributable all-in cost per equivalent ounce sold and per ounce sold on a by-product basis increased by 6% and 7%, respectively, compared to 2023. The increases were primarily as a result of the increase in production cost of sales per equivalent ounce sold.

Depreciation, depletion and amortization increased by 16% compared to 2023, primarily due to a higher depreciable asset base at Tasiast and Bald Mountain, the increase in gold equivalent ounces sold at Fort Knox, and a decrease in mineral reserves for Round Mountain Phase W at the end of 2023. These increases were partially offset by a decrease at La Coipa.

In the third quarter of 2024, the Company recorded an after-tax impairment reversal of $73.4 million, related to property, plant and equipment at Round Mountain. In the fourth quarter of 2023, the Company recorded an after-tax impairment charge of $35.8 million related to inventory at Fort Knox. The impairment reversal in 2024 was net of an income tax expense of $0.7 million while the impairment charge in 2023 was net of an income tax recovery of $3.1 million.

The Company recorded income tax expense of $487.4 million in 2024, an increase of $194.2 million compared to 2023 primarily due to differences in the level of income in the Company’s operating jurisdictions. Kinross' combined federal and provincial statutory tax rate for both 2024 and 2023 was 26.5%.

Net earnings attributable to common shareholders in 2024 were $948.8 million, or $0.77 per share, compared to $416.3 million, or $0.34 per share, in the prior year. The increase in net earnings was primarily a result of an increase in margins as metal sales increased by 21% while production cost of sales increased by only 7%. The impairment reversal at Round Mountain also contributed to the increase, partially offset by the increases in depreciation, depletion and amortization and income tax expense, as noted above.

Adjusted net earnings attributable to common shareholders in 2024 were $838.3 million, or $0.68 per share, compared to $539.8 million, or $0.44 per share, in 2023. The increase was primarily due to the increase in net earnings attributable to common shareholders, net of the after-tax changes in impairment.

Net cash flow provided from operating activities increased to $2,446.4 million in 2024 from $1,605.3 million in 2023, primarily due to the increase in margins and favourable working capital movements.

Attributable adjusted operating cash flow increased to $2,143.1 million in 2024 from $1,676.7 million in 2023, primarily due to the increase in margins, partially offset by an increase in current income tax expense.

Capital expenditures and attributable capital expenditures in 2024 were $1,075.5 million and $1,050.9 million, respectively, consistent with the prior year. Capital expenditures in 2024 included the start of Phase S capital development at Round Mountain, continued spending at Great Bear and increased capital development at Tasiast for West Branch 5. These were offset by reduced spending on the construction of Manh Choh, which was completed in 2024, and the completion of heap leach pad expansions at Bald Mountain at the end of 2023.

4

Kinross Gold Corporation

management’s discussion and analysis

For the year ended December 31, 2024

Attributable free cash flow increased by 139%, to $1,340.2 million in 2024 from $559.7 million in 2023, primarily due to the increase in net cash flow provided from operating activities, as the Company managed operating and capital costs as metal sales increased in the year.

2023 vs. 2022

Kinross’ 2023 production increased by 10% compared to 2022, primarily due to higher production at La Coipa due to the restart and ramp up of operations in the second half of 2022 and higher mill grades, recoveries, and throughput at Tasiast. These increases were partially offset by lower production at Bald Mountain due to lower grades and the timing of ounces recovered from the heap leach pads, consistent with the mine plan.

Metal sales increased by 23% compared to 2022, due to increases in gold equivalent ounces sold and average metal prices realized. Gold equivalent ounces sold increased to 2,179,936 ounces in 2023 compared to 1,927,818 ounces in 2022. The average realized gold price was $1,945 per ounce in 2023 compared to $1,793 per ounce in 2022.

Production cost of sales increased by 14% in 2023 compared to 2022, largely as a result of the restart and ramp up of operations at La Coipa and an increase in gold equivalent ounces sold at Round Mountain, Paracatu and Tasiast. Production cost of sales per equivalent ounce sold was comparable to 2022.

Attributable all-in sustaining cost per equivalent ounce sold and per ounce sold on a by-product basis increased by 4% and 2%, respectively, compared to 2022. Attributable all-in cost per equivalent ounce sold and per ounce sold on a by-product basis increased by 6% and 5%, respectively, compared to 2022. These increases were primarily due to the increases in production cost of sales, as described above, and an increase in capital expenditures, partially offset by the increase in ounces sold.

In 2023, depreciation, depletion and amortization increased by 26% compared to 2022, primarily due to the increase in gold equivalent ounces sold and changes to the life-of-mine plan at Round Mountain in the fourth quarter of 2022, partially offset by lower gold equivalent ounces sold at Bald Mountain.

During the year ended December 31, 2023, the Company recorded an after-tax impairment charge of $35.8 million related to inventory at Fort Knox. During the year ended December 31, 2022, the Company recorded after-tax impairment charges related to metal inventory and property, plant and equipment at Round Mountain of $87.9 million and $201.4 million, respectively. The impairment charges in 2023 and 2022 were net of income tax recoveries of $3.1 million and $60.7 million, respectively.

During the year ended December 31, 2023, the Company recorded an income tax expense of $293.2 million, an increase of $217.1 million compared to 2022 primarily due to differences in the level of income in the Company’s operating jurisdictions. Kinross’ combined federal and provincial statutory tax rate for both 2023 and 2022 was 26.5%.

Net earnings attributable to common shareholders in 2023 were $416.3 million, or $0.34 per share, compared to $31.9 million, or $0.02 per share, in 2022. The change was primarily a result of an increase in margins (metal sales less production cost of sales) and lower impairment charges in 2023, partially offset by the increase in income tax expense and depreciation, depletion and amortization in 2023.

Adjusted net earnings attributable to common shareholders in 2023 were $539.8 million, or $0.44 per share, compared to $283.1 million, or $0.22 per share, in 2022. The increase was primarily due to the increase in net earnings attributable to common shareholders, as described above, net of the decrease in after-tax impairment.

Net cash flow provided from operating activities increased to $1,605.3 million in 2023 from $1,002.5 million 2022, primarily due to the increase in margins and a favourable change in working capital compared to the prior year.

Attributable adjusted operating cash flow increased to $1,676.7 million compared to $1,257.7 million in 2022, primarily due to the increase in margins.

In 2023, capital expenditures and attributable capital expenditures increased to $1,098.3 million and $1,055.0 million, respectively, primarily due to an increase in capital development at Tasiast and Fort Knox and increased development activities at Manh Choh.

Attributable free cash flow increased to $559.7 million from $247.3 million in 2022, due to the increase in net cash flow provided from operating activities, partially offset by higher capital expenditures, as described above.

5

Kinross Gold Corporation

management’s discussion and analysis

For the year ended December 31, 2024

Mineral Reserves1

Kinross’ total estimated proven and probable gold reserves at December 31, 2024 were approximately 21.9 million ounces, a decrease of 0.9 million ounces from 22.8 million ounces at December 31, 2023. The decrease in estimated gold reserves was mainly a result of production depletion. Amongst the operating sites, 1.5 million ounces were also added to proven and probable reserves, mainly at Bald Mountain, Tasiast and Paracatu.

Proven and probable silver reserves at December 31, 2024 were approximately 16.9 million ounces, a decrease of 6.8 million ounces from 23.7 million ounces at December 31, 2023, primarily due to production depletion at La Coipa.

| 2. | IMPACT OF KEY ECONOMIC TRENDS |

Price of Gold

Source: Bloomberg – based on daily closing prices

The price of gold is the single largest factor in determining profitability and cash flow from operations. Therefore, the financial performance of the Company has been, and is expected to continue to be, closely linked to the price of gold. Historically, the price of gold has been subject to volatile price movements over short periods of time and is affected by numerous macroeconomic and industry factors that are beyond the Company’s control. Major influences on the gold price include currency exchange rate fluctuations and the relative strength of the U.S. dollar, the supply of and demand for gold and macroeconomic factors such as the level of interest rates and inflation expectations. During 2024, the price of gold fluctuated between a low of $1,985 per ounce in February and a high of $2,778 per ounce in October, with an average price for the year based on the LBMA Gold Price PM benchmark of $2,386 per ounce, compared to the 2023 average price of $1,941 per ounce. Major influences on the gold price during 2024 included market expectations of interest rate cuts, a stronger USD, ongoing geopolitical tensions, trade risks and otherwise general market volatility around the United States presidential election.

1 For details concerning mineral reserve and mineral resource estimates, refer to the Mineral Reserves and Mineral Resources tables and notes in the Company's news release filed with Canadian and U.S. regulators on February 12, 2025.

6

Kinross Gold Corporation

management’s discussion and analysis

For the year ended December 31, 2024

In 2024, Kinross’ attributable average realized gold price2 of $2,391 per ounce compared to the average LBMA Gold Price PM benchmark of $2,386 per ounce.

Source: London Bullion Marketing Association London PM Benchmark

2 These figures are non-GAAP financial measures and ratios, as applicable, and are defined, and actual results for the year ended December 31, 2024 are reconciled, in Section 11 of this MD&A. Non-GAAP financial measures and ratios have no standardized meaning under IFRS and therefore, may not be comparable to similar measures presented by other issuers.

7

Kinross Gold Corporation

management’s discussion and analysis

For the year ended December 31, 2024

Gold Supply and Demand Fundamentals

Source: World Gold Council Gold Demand Trends: Full Year 2024 report

According to the World Gold Council, total gold supply in 2024 increased by approximately 1% compared to 2023, driven by mine production and recycling.

8

Kinross Gold Corporation

management’s discussion and analysis

For the year ended December 31, 2024

Source: World Gold Council Gold Demand Trends: Full Year 2024 report

According to the World Gold Council, annual gold demand increased in 2024 by approximately 1% compared to 2023, as central bank demand continued to be strong and ETF holdings increased in the second half of 2024.

9

Kinross Gold Corporation

management’s discussion and analysis

For the year ended December 31, 2024

Cost Sensitivity

The Company’s profitability is subject to industry-wide cost pressures on development and operating costs with respect to labour, energy, capital expenditures and consumables in general. Since mining is generally an energy intensive activity, especially in open pit mining, energy prices have a significant impact on operations.

The cost of fuel as a percentage of operating costs varies amongst the Company’s mines, and overall, fuel prices in 2024 were weaker compared to 2023. Fluctuations in fuel prices are primarily due to geopolitical risk and demand and supply dynamics. Kinross manages its exposure to fuel costs by entering into various hedge positions from time to time – refer to Section 6 – Liquidity and Capital Resources for details.

Source: Bloomberg

In order to mitigate the impact of higher consumable prices, the Company continues to focus on continuous improvement, both by promoting more efficient use of materials and supplies, and by pursuing more advantageous pricing, whilst increasing performance and without compromising operational integrity.

10

Kinross Gold Corporation

management’s discussion and analysis

For the year ended December 31, 2024

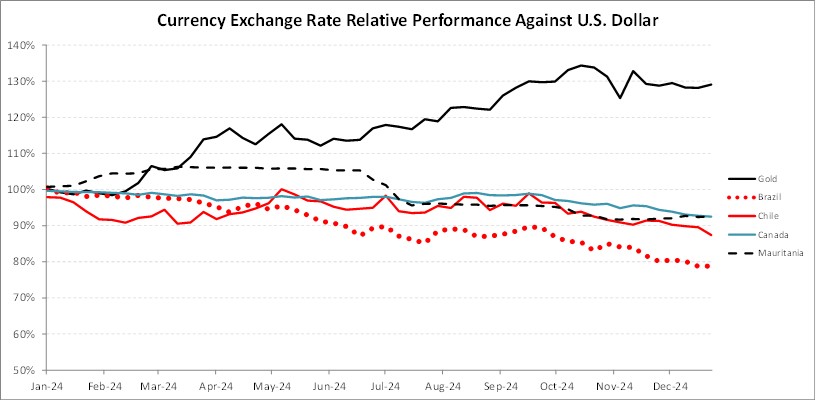

Currency Fluctuations

Source: Bloomberg

At the Company’s non-U.S. mining operations and exploration activities, which are primarily located in Brazil, Chile, Mauritania, and Canada, a portion of operating costs and capital expenditures are denominated in their respective local currencies. Generally, as the U.S. dollar strengthens, these currencies weaken, and as the U.S. dollar weakens, these foreign currencies strengthen. These currencies were subject to market volatility over the course of the year. Approximately 65% of the Company’s expected production in 2025 is forecast to come from operations outside the U.S. and costs will continue to be exposed to foreign exchange movements. In order to manage this risk, the Company uses currency hedges for certain foreign currency exposures – refer to Section 6 – Liquidity and Capital Resources for details.

| 3. | OUTLOOK |

The following section of this MD&A represents forward-looking information and users are cautioned that actual results may vary. We refer to the risks and assumptions contained in the Cautionary Statement on Forward-Looking Information on pages 53 – 54 of this MD&A.

Attributable3 Production Guidance

In 2025, Kinross expects to produce 2.0 million attributable gold equivalent ounces4 (+/- 5%) from its operations. Production is expected to remain stable at 2.0 million attributable gold equivalent ounces (+/- 5%) for each of 2026 and 2027.

3 Attributable guidance and results include Kinross’ 70% share of Manh Choh production, costs and capital expenditures. Attributable figures are non-GAAP financial measures and ratios. Refer to footnote 2.

4 Attributable gold equivalent ounce production guidance for 2025 includes approximately 4.3 million ounces of silver.

11

Kinross Gold Corporation

management’s discussion and analysis

For the year ended December 31, 2024

Attributable3 Cost Guidance

| 2025 | 2024 | |||||||

| Guidance | Full-Year | |||||||

| (+/-5%) | Results | |||||||

| Attributable production cost of sales per equivalent ounce sold2 | $ | 1,120 | $ | 1,021 | ||||

| Attributable all-in sustaining cost per equivalent ounce sold2 | $ | 1,500 | $ | 1,388 | ||||

| Production cost of sales per equivalent ounce sold5 | $ | 1,020 | ||||||

Attributable production cost of sales2 is expected to be $1,120 per equivalent ounce sold (+/- 5%) for 2025. In 2024, production cost of sales5 and attributable production cost of sales2 were $1,020 per equivalent ounce sold and $1,021 per equivalent ounce sold, respectively. The moderate year-over-year increase in 2025 is mainly due to lower overall production with a change in sales mix, including lower production at Tasiast, and inflationary impacts.

The Company expects its attributable all-in sustaining cost2 to be $1,500 per equivalent ounce sold (+/- 5%) for 2025. In 2024, attributable all-in sustaining cost2 was $1,388 per equivalent ounce sold. The expected increase in 2025 is largely a result of the increase in attributable production cost of sales, as noted above.

Material assumptions used to forecast 2025 attributable production cost of sales2 are: a gold price of $2,500 per ounce, a silver price of $30 per ounce, an oil price of $80 per barrel, and foreign exchange rates of 5.25 Brazilian reais to the U.S. dollar, 900 Chilean pesos to the U.S. dollar, 37.50 Mauritanian ouguiyas to the U.S. dollar and 1.35 Canadian dollars to the U.S. dollar.

Taking into account existing currency and oil hedges, a 10% change in all foreign currency exchange rates would be expected to result in an approximate $25 impact on attributable production cost of sales per equivalent ounce sold2; and specific to the Brazilian real and Chilean peso, a 10% change in these exchange rates would be expected to result in impacts of approximately $45 and $50 on Brazilian and Chilean attributable production cost of sales per equivalent ounce sold2, respectively. A $10 per barrel change in the price of oil would be expected to result in an approximate $3 impact on fuel consumption costs on attributable production cost of sales per equivalent ounce sold2, and a $100 change in the price of gold would be expected to result in an approximate $5 impact on attributable production cost of sales per equivalent ounce sold2 as a result of a change in royalties.

Attributable3 Capital Expenditures2 Guidance

| 2025 | 2024 | |||||||

| Guidance | Full-Year | |||||||

| (+/-5%) | Results | |||||||

| Attributable sustaining capital expenditures | $ | 535.0 | $ | 523.5 | ||||

| Attributable non-sustaining capital expenditures | $ | 615.0 | $ | 527.4 | ||||

| Total attributable capital expenditures2 | $ | 1,150.0 | $ | 1,050.9 | ||||

| Total capital expenditures6 | $ | 1,075.5 | ||||||

Attributable capital expenditures for 2025 are forecasted to be approximately $1,150 million (+/- 5%). Of this amount, sustaining capital expenditures are expected to be approximately $535 million, with non-sustaining capital expenditures of approximately $615 million. Non-sustaining capital expenditures include stripping at Tasiast West Branch 5, Round Mountain Phase S, and Bald Mountain Redbird, project studies and Advanced Exploration (“AEX”) construction at Great Bear, as well as other growth projects and studies.

Kinross’ attributable capital expenditures outlook for 2026 and 2027 is expected to be in-line with 2025, subject to ongoing inflationary impacts.

5 “Production cost of sales per equivalent ounce sold” is defined as production cost of sales divided by total gold equivalent ounces sold.

6 “Capital expenditures” is as reported as “Additions to property, plant and equipment” on the consolidated statements of cash flows.

12

Kinross Gold Corporation

management’s discussion and analysis

For the year ended December 31, 2024

Other 2025 Guidance

The 2025 forecast for exploration and business development is $200 million (+/-5%), which includes approximately $175 million (+/-5%) of exploration expenditures, mainly at Round Mountain, Curlew, Tasiast, La Coipa and Fort Knox.

The 2025 forecast for general and administrative expense is $125 million (+/-5%).

Other operating costs for 2025 are expected to be between $125 and $150 million, which primarily relates to studies and permitting activities that do not meet the criteria for capitalization, as well as care and maintenance and reclamation activities at non-operating sites.

Taxes paid are expected to be $330 million in 2025, based on a gold price of $2,500 per ounce, and are expected to increase by approximately $4 million for every $100 per ounce movement in the realized gold prices. The forecast effective tax rate (“ETR”)7 for 2025 is expected to be in the range of 32% - 37%.

Depreciation, depletion and amortization is forecast to be approximately $540 (+/-5%) per equivalent ounce sold8, compared to $533 per equivalent ounce sold8 in 2024.

The 2025 forecast for interest paid is $75 million, $55 million of which is expected to be expensed and $20 million capitalized. In 2024, $128.2 million of interest was paid with $92.6 million capitalized and $35.6 million expensed. The 2025 forecast for interest expense excludes accretion of the Company’s reclamation and remediation obligations, as well as lease liabilities, which for 2024 totaled $42.3 million.

| 4. | PROJECT UPDATES AND NEW DEVELOPMENTS |

Great Bear

At Great Bear, Kinross continues to progress its AEX program and Main Project permitting.

For the AEX program, early works, including tree clearing and earthworks, has commenced with the necessary permits received for all current activities. The two remaining permits required for full AEX completion and operation are under review by the regulatory authorities and are expected to be received later in the year, when they are required. Detailed engineering and procurement continue to advance.

The Company is focused on progressing AEX activities including construction of the exploration decline planned to commence in late 2025.

For the Main Project, Kinross is advancing detailed engineering and execution planning. The selection of design partners is well underway and work is planned to commence in the first quarter of 2025. This work will provide key engineering information for permitting and construction.

The Company continues to work with the Impact Assessment Agency of Canada on advancing its Impact Statement, which is planned to be submitted later in 2025. Consultation continues with designated Indigenous communities, including discussions to finalize related agreements.

In 2025, Kinross has shifted from deep underground resource drilling to regional exploration work with the goal of identifying new open pit and underground deposits.

Kinross released its Preliminary Economic Assessment for Great Bear on September 10, 2024. The Project is expected to produce over 500,000 ounces per year at an all-in sustaining cost of approximately $800 per ounce during the first 8 years through a conventional, modest capital 10,000 tonne per day mill. In parallel, Kinross also released an updated mineral resource estimate increasing the

7 The forecast ETR range for 2025 assumes gold price, foreign exchange and tax rates in the jurisdictions in which the Company operates remain stable and within 2025 guidance assumptions. The ETR does not include the impact of items which the Company believes are not reflective of the Company’s underlying performance, such as the impact of net foreign currency translations on tax deductions and taxes related to prior periods. Management believes that the ETR range provides investors with the ability to better evaluate the Company’s underlying performance. However, the ETR range is not necessarily an indicator of tax expense recognized under IFRS. The rate is sensitive to the relative proportion of sales between the Company’s various tax jurisdictions and realized gold prices.

8 Depreciation, depletion and amortization per equivalent ounce sold is defined as depreciation, depletion and amortization, as reported on the consolidated statements of operations, divided by total gold equivalent ounces sold.

13

Kinross Gold Corporation

management’s discussion and analysis

For the year ended December 31, 2024

inferred resource estimate by 568 thousand ounces to 3.9 million ounces which was in addition to the measured and indicated resource estimate of 2.7 million ounces.

Bald Mountain Redbird

Kinross is pleased to announce plans to proceed with mining at the Redbird pit at Bald Mountain, which contains approximately 1 million ounces of gold reserve, following the receipt of the Juniper permit in the second half of 2024.

Kinross has approved mining of Phase 1 at Redbird, which contains 270 thousand ounces and is expected to produce approximately 175 thousand ounces, extending production into 2028. Phase 2, unlocking another 680 thousand ounces contained, could begin in 2026 and extend production from Bald Mountain through 2031.

Phase 1 lowers the initial capital risk by leveraging existing heap leach infrastructure, pulls forward production into 2027, and can progress in 2025 while work continues on optimizing the design and execution plan for Phase 2.

Phase 1 initial capex of $120 million is primarily pre-strip mining cost, and the project has an all-in sustaining cost of approximately $1,500/oz.

Lobo-Marte

Kinross is progressing baseline studies to support the Environmental Impact Assessment for the Lobo-Marte project. Lobo-Marte continues to be a potential large, low-cost mine and Kinross is committed to progressing next steps to advance the project.

14

Kinross Gold Corporation

management’s discussion and analysis

For the year ended December 31, 2024

| 5. | CONSOLIDATED RESULTS OF OPERATIONS |

Operating Highlights

| Years ended December 31, | 2024 vs. 2023 | 2023 vs. 2022 | ||||||||||||||||||||||||||

| (in millions, except ounces and per ounce amounts) | 2024 | 2023 | 2022(d) | Change | % Change(e) | Change | % Change(e) | |||||||||||||||||||||

| Operating Statistics(a) | ||||||||||||||||||||||||||||

| Total gold equivalent ounces(b) | ||||||||||||||||||||||||||||

| Produced | 2,170,791 | 2,153,020 | 1,957,237 | 17,771 | 1 | % | 195,783 | 10 | % | |||||||||||||||||||

| Sold | 2,153,212 | 2,179,936 | 1,927,818 | (26,724 | ) | (1 | )% | 252,118 | 13 | % | ||||||||||||||||||

| Attributable gold equivalent ounces(b) | ||||||||||||||||||||||||||||

| Produced | 2,128,052 | 2,153,020 | 1,957,237 | (24,968 | ) | (1 | )% | 195,783 | 10 | % | ||||||||||||||||||

| Sold | 2,111,688 | 2,179,936 | 1,927,818 | (68,248 | ) | (3 | )% | 252,118 | 13 | % | ||||||||||||||||||

| Gold ounces - sold | 2,100,621 | 2,074,989 | 1,872,342 | 25,632 | 1 | % | 202,647 | 11 | % | |||||||||||||||||||

| Silver ounces - sold (000's) | 4,467 | 8,718 | 4,647 | (4,251 | ) | (49 | )% | 4,071 | 88 | % | ||||||||||||||||||

| Average realized gold price per ounce(c) | $ | 2,393 | $ | 1,945 | $ | 1,793 | $ | 448 | 23 | % | $ | 152 | 8 | % | ||||||||||||||

| Earnings(a) | ||||||||||||||||||||||||||||

| Metal sales | $ | 5,148.8 | $ | 4,239.7 | $ | 3,455.1 | $ | 909.1 | 21 | % | $ | 784.6 | 23 | % | ||||||||||||||

| Production cost of sales | $ | 2,197.1 | $ | 2,054.4 | $ | 1,805.7 | $ | 142.7 | 7 | % | $ | 248.7 | 14 | % | ||||||||||||||

| Depreciation, depletion and amortization | $ | 1,147.5 | $ | 986.8 | $ | 784.0 | $ | 160.7 | 16 | % | $ | 202.8 | 26 | % | ||||||||||||||

| Impairment (reversal) charge | $ | (74.1 | ) | $ | 38.9 | $ | 350.0 | $ | (113.0 | ) | nm | $ | (311.1 | ) | (89 | )% | ||||||||||||

| Operating earnings | $ | 1,540.3 | $ | 801.4 | $ | 117.7 | $ | 738.9 | 92 | % | $ | 683.7 | nm | |||||||||||||||

| Net earnings attributable to common shareholders | $ | 948.8 | $ | 416.3 | $ | 31.9 | $ | 532.5 | 128 | % | $ | 384.4 | nm | |||||||||||||||

| (a) | All measures and ratios include 100% of the results from Manh Choh, except measures denoted as “attributable.” “Attributable” measures include Kinross’ 70% share of Manh Choh production and sales, as appropriate. |

| (b) | “Gold equivalent ounces” include silver ounces produced and sold converted to a gold equivalent based on a ratio of the average spot market prices for the commodities for each period. The ratio for 2024 was 84.43:1 (2023 – 83.13:1, 2022 – 82.90:1). |

| (c) | “Average realized gold price per ounce” is defined as gold revenue divided by total gold ounces sold. |

| (d) | Results for the year ended December 31, 2022 are from continuing operations and exclude results from the Company’s Chirano and Russian operations due to the classification of these operations as discontinued and their sale in 2022. |

| (e) | “nm” means not meaningful. |

Operating Earnings (Loss) by Segment

| Years ended December 31, | 2024 vs. 2023 | 2023 vs. 2022 | ||||||||||||||||||||||||||

| (in millions) | 2024 | 2023 | 2022(c) | Change | % Change(d) | Change | % Change(d) | |||||||||||||||||||||

| Operating segments | ||||||||||||||||||||||||||||

| Tasiast | $ | 696.0 | $ | 549.6 | $ | 299.5 | $ | 146.4 | 27 | % | $ | 250.1 | 84 | % | ||||||||||||||

| Paracatu | 505.6 | 407.5 | 330.9 | 98.1 | 24 | % | 76.6 | 23 | % | |||||||||||||||||||

| La Coipa | 210.8 | 147.2 | 81.8 | 63.6 | 43 | % | 65.4 | 80 | % | |||||||||||||||||||

| Fort Knox(a) | 307.0 | 65.1 | 55.0 | 241.9 | nm | 10.1 | 18 | % | ||||||||||||||||||||

| Round Mountain | 15.0 | (100.3 | ) | (327.6 | ) | 115.3 | nm | 227.3 | nm | |||||||||||||||||||

| Bald Mountain | 68.0 | 13.9 | (5.6 | ) | 54.1 | nm | 19.5 | nm | ||||||||||||||||||||

| Non-operating segments | ||||||||||||||||||||||||||||

| Great Bear | (43.8 | ) | (49.9 | ) | (61.7 | ) | 6.1 | nm | 11.8 | nm | ||||||||||||||||||

| Corporate and other(b) | (218.3 | ) | (231.7 | ) | (254.6 | ) | 13.4 | nm | 22.9 | nm | ||||||||||||||||||

| Total | $ | 1,540.3 | $ | 801.4 | $ | 117.7 | $ | 738.9 | 92 | % | $ | 683.7 | nm | |||||||||||||||

| (a) | The Fort Knox segment includes Manh Choh, which was aggregated with Fort Knox during 2024. Results for all periods include 100% for Manh Choh. Comparative results are presented in accordance with the current year’s presentation. |

| (b) | “Corporate and other” includes operating costs which are not directly related to individual mining properties such as overhead expenses, insurance recoveries, gains and losses on disposal of assets and investments, and other costs relating to corporate, shutdown and other non-operating assets (including Kettle River-Buckhorn, Lobo-Marte, and Maricunga). |

| (c) | Results for the year ended December 31, 2022 are from continuing operations and exclude results from the Company’s Chirano and Russian operations due to the classification of these operations as discontinued and their sale in 2022. |

| (d) | “nm” means not meaningful. |

15

Kinross Gold Corporation

management’s discussion and analysis

For the year ended December 31, 2024

Mining Operations

Tasiast – Mauritania

| Years ended December 31, | ||||||||||||||||

| 2024 | 2023 | Change | % Change(c) | |||||||||||||

| Operating Statistics | ||||||||||||||||

| Tonnes ore mined (000's) | 7,601 | 9,801 | (2,200 | ) | (22 | )% | ||||||||||

| Tonnes processed (000's) | 8,642 | 6,723 | 1,919 | 29 | % | |||||||||||

| Grade (grams/tonne) | 2.44 | 3.19 | (0.75 | ) | (24 | )% | ||||||||||

| Recovery | 92.1 | % | 92.3 | % | (0.2 | )% | (0 | )% | ||||||||

| Gold equivalent ounces(a): | ||||||||||||||||

| Produced | 622,394 | 620,793 | 1,601 | 0 | % | |||||||||||

| Sold | 609,614 | 615,065 | (5,451 | ) | (1 | )% | ||||||||||

| Earnings (in millions) | ||||||||||||||||

| Metal sales | $ | 1,456.5 | $ | 1,200.8 | $ | 255.7 | 21 | % | ||||||||

| Production cost of sales | 415.4 | 406.8 | 8.6 | 2 | % | |||||||||||

| Depreciation, depletion and amortization | 357.1 | 244.4 | 112.7 | 46 | % | |||||||||||

| 684.0 | 549.6 | 134.4 | 24 | % | ||||||||||||

| Other operating income | (21.6 | ) | (3.9 | ) | (17.7 | ) | nm | |||||||||

| Exploration and business development | 9.6 | 3.9 | 5.7 | 146 | % | |||||||||||

| Segment operating earnings | $ | 696.0 | $ | 549.6 | $ | 146.4 | 27 | % | ||||||||

| Production cost of sales per equivalent ounce(a) sold(b) | $ | 681 | $ | 661 | $ | 20 | 3 | % | ||||||||

| (a) | “Gold equivalent ounces” include silver ounces produced and sold converted to a gold equivalent based on a ratio of the average spot market prices for the commodities for each period. The ratio for 2024 was 84.43:1 (2023 – 83.13:1). |

| (b) | “Production cost of sales per equivalent ounce sold” is defined as production cost of sales divided by total gold equivalent ounces sold. |

| (c) | “nm” means not meaningful. |

Kinross acquired its 100% interest in the Tasiast mine on September 17, 2010 upon completing its acquisition of Red Back Mining Inc. The Tasiast mine is an open pit operation located in north-western Mauritania and is approximately 300 kilometres north of the capital, Nouakchott.

2024 vs. 2023

Gold equivalent ounces produced and sold in 2024 were comparable to 2023. Mining at Tasiast in 2024 decreased at West Branch 4 and capital development increased at West Branch 5, resulting in a 22% decrease in tonnes of ore mined compared to 2023. Mill grades decreased by 24% in 2024 compared to 2023 as a result of mine sequencing, blending ore from West Branch 4 with ore from stockpiles. Mill throughput increased by 29% in 2024 compared to 2023 as Tasiast continued to achieve higher throughput levels after the completion of the 24k project in the second half of 2023, which modified the grinding circuit, added new leaching and thickening capacity, and improved onsite power generation and water supply.

Metal sales increased by 21% compared to 2023, due to the 23% increase in average metal prices realized. Production cost of sales increased by 2% in 2024, compared to 2023, primarily due to higher royalties as a result of the increase in average metal prices and higher labour costs, largely offset by a higher proportion of costs allocated to capital development. Production cost of sales per equivalent ounce sold increased by 3% in 2024 compared to 2023 as a result of the increase in production cost of sales. Depreciation, depletion and amortization increased by 46% in 2024, primarily due to an increase in the depreciable asset base and the inclusion of ore from stockpiles with a higher depreciation cost.

16

Kinross Gold Corporation

management’s discussion and analysis

For the year ended December 31, 2024

Paracatu – Brazil

| Years ended December 31, | ||||||||||||||||

| 2024 | 2023 | Change | % Change | |||||||||||||

| Operating Statistics | ||||||||||||||||

| Tonnes ore mined (000's) | 54,243 | 53,845 | 398 | 1 | % | |||||||||||

| Tonnes processed (000's) | 58,329 | 60,182 | (1,853 | ) | (3 | )% | ||||||||||

| Grade (grams/tonne) | 0.36 | 0.39 | (0.03 | ) | (8 | )% | ||||||||||

| Recovery | 80.2 | % | 79.1 | % | 1.1 | % | 1 | % | ||||||||

| Gold equivalent ounces(a): | ||||||||||||||||

| Produced | 528,574 | 587,999 | (59,425 | ) | (10 | )% | ||||||||||

| Sold | 528,209 | 592,224 | (64,015 | ) | (11 | )% | ||||||||||

| Earnings (in millions) | ||||||||||||||||

| Metal sales | $ | 1,258.9 | $ | 1,149.6 | $ | 109.3 | 10 | % | ||||||||

| Production cost of sales | 548.6 | 538.6 | 10.0 | 2 | % | |||||||||||

| Depreciation, depletion and amortization | 189.3 | 186.6 | 2.7 | 1 | % | |||||||||||

| 521.0 | 424.4 | 96.6 | 23 | % | ||||||||||||

| Other operating expense | 7.5 | 11.3 | (3.8 | ) | (34 | )% | ||||||||||

| Exploration and business development | 7.9 | 5.6 | 2.3 | 41 | % | |||||||||||

| Segment operating earnings | $ | 505.6 | $ | 407.5 | $ | 98.1 | 24 | % | ||||||||

| Production cost of sales per equivalent ounce(a) sold(b) | $ | 1,039 | $ | 909 | $ | 130 | 14 | % | ||||||||

| (a) | “Gold equivalent ounces” include silver ounces produced and sold converted to a gold equivalent based on a ratio of the average spot market prices for the commodities for each period. The ratio for 2024 was 84.43:1 (2023 – 83.13:1). |

| (b) | “Production cost of sales per equivalent ounce sold” is defined as production cost of sales divided by total gold equivalent ounces sold. |

The Company acquired a 49% ownership interest in the Paracatu open pit mine, located in the State of Minas Gerais, Brazil, upon the acquisition of TVX Gold Inc. on January 31, 2003. On December 31, 2004, the Company purchased the remaining 51% of Paracatu from Rio Tinto Plc.

2024 vs. 2023

Gold equivalent ounces produced and sold in 2024 decreased by 10% and 11%, respectively, compared to 2023 primarily due to lower grades and throughput, as a result of changes in ore hardness, consistent with Paracatu’s planned mine sequencing.

Metal sales increased by 10% compared to 2023, due to the 23% increase in average metal prices realized, partially offset by the decrease in gold equivalent ounces sold. Production cost of sales increased by 2% compared to 2023, due to higher drilling contractor and blasting supply costs, partially offset by favourable foreign exchange rates and lower gold equivalent ounces sold. Production cost of sales per equivalent ounce sold increased by 14% in 2024 compared to 2023 as a result of the decrease in gold equivalent ounces produced and increase in production cost of sales. Depreciation, depletion and amortization increased by 1% compared to 2023, primarily due to an increase in the depreciable asset base and a decrease in mineral reserves at the end of 2023, partially offset by the decrease in gold equivalent ounces sold.

17

Kinross Gold Corporation

management’s discussion and analysis

For the year ended December 31, 2024

La Coipa – Chile

| Years ended December 31, | ||||||||||||||||

| 2024 | 2023 | Change | % Change(c) | |||||||||||||

| Operating Statistics | ||||||||||||||||

| Tonnes ore mined (000's) | 3,896 | 4,345 | (449 | ) | (10 | )% | ||||||||||

| Tonnes processed (000's) | 3,535 | 3,867 | (332 | ) | (9 | )% | ||||||||||

| Grade (grams/tonne): | ||||||||||||||||

| Gold | 2.05 | 1.74 | 0.31 | 18 | % | |||||||||||

| Silver | 60.12 | 107.68 | (47.56 | ) | (44 | )% | ||||||||||

| Recovery: | ||||||||||||||||

| Gold | 82.5 | % | 81.3 | % | 1.2 | % | 1 | % | ||||||||

| Silver | 51.8 | % | 56.5 | % | (4.7 | )% | (8 | )% | ||||||||

| Gold equivalent ounces(a): | ||||||||||||||||

| Produced | 246,131 | 260,138 | (14,007 | ) | (5 | )% | ||||||||||

| Sold | 241,077 | 268,491 | (27,414 | ) | (10 | )% | ||||||||||

| Silver ounces: | ||||||||||||||||

| Produced (000's) | 3,831 | 7,670 | (3,839 | ) | (50 | )% | ||||||||||

| Sold (000's) | 3,780 | 8,021 | (4,241 | ) | (53 | )% | ||||||||||

| Earnings (in millions) | ||||||||||||||||

| Metal sales | $ | 573.3 | $ | 522.6 | $ | 50.7 | 10 | % | ||||||||

| Production cost of sales | 231.3 | 182.8 | 48.5 | 27 | % | |||||||||||

| Depreciation, depletion and amortization | 118.3 | 187.8 | (69.5 | ) | (37 | )% | ||||||||||

| 223.7 | 152.0 | 71.7 | 47 | % | ||||||||||||

| Other operating expense (income) | 9.6 | (8.2 | ) | 17.8 | nm | |||||||||||

| Exploration and business development | 3.3 | 13.0 | (9.7 | ) | (75 | )% | ||||||||||

| Segment operating earnings | $ | 210.8 | $ | 147.2 | $ | 63.6 | 43 | % | ||||||||

| Production cost of sales per equivalent ounce(a) sold(b) | $ | 959 | $ | 681 | $ | 278 | 41 | % | ||||||||

| (a) | “Gold equivalent ounces” include silver ounces produced and sold converted to a gold equivalent based on a ratio of the average spot market prices for the commodities for each period. The ratio for 2024 was 84.43:1 (2023 – 83.13:1). |

| (b) | “Production cost of sales per equivalent ounce sold” is defined as production cost of sales divided by total gold equivalent ounces sold. |

| (c) | “nm” means not meaningful. |

Kinross acquired its 100% interest in the La Coipa open pit mine, located in the Atacama region in Chile, in 2007. In February 2022, the mine poured its first gold bar after restarting operations following the suspension of activities since October 2013.

2024 vs. 2023

Gold equivalent ounces produced in 2024 decreased by 5% compared to 2023, due to a decrease in silver grades and throughput, partially offset by an increase in gold grades. Planned mine sequencing at La Coipa, with an increased focus on Phase 7 and capital development of the Puren 2 pit, resulted in an 18% increase in gold grades, a 44% decrease in silver grades, and a 10% decrease in tonnes of ore mined in 2024 compared to 2023. Tonnes processed in 2024 were 9% lower compared to 2023, due to increased maintenance activity in 2024. Gold equivalent ounces sold decreased by 10% compared to 2023, due to the decrease in production and the timing of sales in 2023.

Metal sales increased by 10% compared to 2023, due to the 23% increase in average metal prices realized, partially offset by the decrease in gold equivalent ounces sold. Production cost of sales increased by 27% compared to 2023, primarily due to a lower proportion of mining activities related to capital development in 2024 and higher mill maintenance costs, partially offset by favourable foreign exchange rates and the decrease in gold equivalent ounces sold. Production cost of sales per equivalent ounce sold increased by 41% in 2024 compared to 2023 as a result of the increase in production cost of sales and decrease in gold equivalent ounces produced. Depreciation, depletion and amortization decreased by 37% compared to 2023, due to the decrease in gold equivalent ounces sold and an adjustment recorded in the period.

18

Kinross Gold Corporation

management’s discussion and analysis

For the year ended December 31, 2024

Fort Knox (100% basis) – USA(a)

| Years ended December 31, | ||||||||||||||||

| 2024 | 2023 | Change | % Change(f) | |||||||||||||

| Operating Statistics | ||||||||||||||||

| Tonnes ore mined (000's) | 33,672 | 32,705 | 967 | 3 | % | |||||||||||

| Tonnes processed (000's)(b) | 34,131 | 36,826 | (2,695 | ) | (7 | )% | ||||||||||

| Grade (grams/tonne)(c) | 1.49 | 0.77 | 0.72 | 94 | % | |||||||||||

| Recovery(c) | 85.4 | % | 79.9 | % | 5.5 | % | 7 | % | ||||||||

| Gold equivalent ounces(d): | ||||||||||||||||

| Produced | 377,258 | 290,651 | 86,607 | 30 | % | |||||||||||

| Sold | 375,402 | 287,532 | 87,870 | 31 | % | |||||||||||

| Earnings (in millions) | ||||||||||||||||

| Metal sales | $ | 912.5 | $ | 557.9 | $ | 354.6 | 64 | % | ||||||||

| Production cost of sales | 452.5 | 343.5 | 109.0 | 32 | % | |||||||||||

| Depreciation, depletion and amortization | 140.9 | 96.8 | 44.1 | 46 | % | |||||||||||

| Impairment charge | - | 38.9 | (38.9 | ) | nm | |||||||||||

| 319.1 | 78.7 | 240.4 | nm | |||||||||||||

| Other operating expense | 0.5 | 0.8 | (0.3 | ) | (38 | )% | ||||||||||

| Exploration and business development | 11.6 | 12.8 | (1.2 | ) | (9 | )% | ||||||||||

| Segment operating earnings | $ | 307.0 | $ | 65.1 | $ | 241.9 | nm | |||||||||

| Production cost of sales per equivalent ounce(d) sold(e) | $ | 1,205 | $ | 1,195 | $ | 10 | 1 | % | ||||||||

| (a) | The Fort Knox segment includes Manh Choh, which was aggregated with Fort Knox during the year ended December 31, 2024. Results for all periods include 100% for Manh Choh. Comparative results are presented in accordance with the current year’s presentation. |

| (b) | Includes 27,649,000 tonnes placed on the heap leach pad during 2024 (2023 – 28,700,000 tonnes). |

| (c) | Amount represents mill grade and recovery only. Ore placed on the heap leach pads had an average grade of 0.22 grams per tonne during 2024 (2023 – 0.22 grams per tonne). Due to the nature of heap leach operations, point-in-time recovery rates are not meaningful. |

| (d) | “Gold equivalent ounces” include silver ounces produced and sold converted to a gold equivalent based on a ratio of the average spot market prices for the commodities for each period. The ratio for 2024 was 84.43:1 (2023 – 83.13:1). |

| (e) | “Production cost of sales per equivalent ounce sold” is defined as production cost of sales divided by total gold equivalent ounces sold. |

| (f) | “nm” means not meaningful. |

The Company has been operating the Fort Knox open pit mine, located near Fairbanks, Alaska, since it was acquired in 1998. In September 2020, the Company acquired a 70% ownership interest in Manh Choh, located approximately 400 kilometres southeast of the Fort Knox mine. Construction and commissioning of the Fort Knox mill modifications were completed in the third quarter of 2024, with production from the open pit Manh Choh mine having commenced in July 2024.

2024 vs. 2023

Gold equivalent ounces produced and sold in 2024 increased by 30% and 31%, respectively, compared to 2023, primarily due to the production of higher-grade, higher-recovery ore from Manh Choh in the second half of 2024. Tonnes of ore mined and mill grades increased by 3% and 94%, respectively, compared to 2023, due to the ramp up of mining at Manh Choh and planned mine sequencing at Fort Knox, which included Phase 9 leachable ore and the advancement of Phase 10. This was partially offset by a decrease in mill throughput as the higher-grade Manh Choh ore requires a longer retention time in the leach circuit, as well as reduced gravity circuit availability and leaching circuit performance in the first quarter of 2024.

Metal sales increased by 64% compared to 2023, due to the increase in gold equivalent ounces sold and the 23% increase in average metal prices realized. Production cost of sales increased by 32% compared to 2023, primarily due to the increase in gold equivalent ounces sold, as well as higher contractor, royalty and reagent costs, largely related to the start of Manh Choh production. Production cost of sales per equivalent ounce sold in 2024 was comparable to 2023. Depreciation, depletion, and amortization increased by 46% in 2024 compared to 2023 due to the increase in gold equivalent ounces sold as well as an increase in the depreciable asset base with the addition of Manh Choh, and a decrease in mineral reserves at the end of 2023.

During the year ended December 31, 2023, the Company recorded an impairment charge of $38.9 million related to a reduction in the estimate of recoverable ounces on the heap leach pads due to changes in estimated recovery rates. The tax impact of the impairment charge was an income tax recovery of $3.1 million.

19

Kinross Gold Corporation

management’s discussion and analysis

For the year ended December 31, 2024

Round Mountain – USA

| Years ended December 31, | ||||||||||||||||

| 2024 | 2023 | Change | % Change(e) | |||||||||||||

| Operating Statistics | ||||||||||||||||

| Tonnes ore mined (000's) | 13,271 | 28,655 | (15,384 | ) | (54 | )% | ||||||||||

| Tonnes processed (000's)(a) | 10,890 | 28,462 | (17,572 | ) | (62 | )% | ||||||||||

| Grade (grams/tonne)(b) | 1.07 | 0.78 | 0.29 | 37 | % | |||||||||||

| Recovery(b) | 76.3 | % | 74.0 | % | 2.3 | % | 3 | % | ||||||||

| Gold equivalent ounces(c): | ||||||||||||||||

| Produced | 215,387 | 235,690 | (20,303 | ) | (9 | )% | ||||||||||

| Sold | 214,996 | 234,064 | (19,068 | ) | (8 | )% | ||||||||||

| Earnings (in millions) | ||||||||||||||||

| Metal sales | $ | 506.8 | $ | 454.4 | $ | 52.4 | 12 | % | ||||||||

| Production cost of sales | 328.3 | 357.7 | (29.4 | ) | (8 | )% | ||||||||||

| Depreciation, depletion and amortization | 193.2 | 157.2 | 36.0 | 23 | % | |||||||||||

| Impairment reversal | (74.1 | ) | - | (74.1 | ) | nm | ||||||||||

| 59.4 | (60.5 | ) | 119.9 | nm | ||||||||||||

| Other operating (income) expense | (9.7 | ) | 4.1 | (13.8 | ) | nm | ||||||||||

| Exploration and business development | 54.1 | 35.7 | 18.4 | 52 | % | |||||||||||

| Segment operating earnings (loss) | $ | 15.0 | $ | (100.3 | ) | $ | 115.3 | nm | ||||||||

| Production cost of sales per equivalent ounce(c) sold(d) | $ | 1,527 | $ | 1,528 | $ | (1 | ) | (0 | )% | |||||||

| (a) | Includes 7,566,000 tonnes placed on the heap leach pads during 2024 (2023 – 24,768,000 tonnes). |

| (b) | Amount represents mill grade and recovery only. Ore placed on the heap leach pads had an average grade of 0.32 grams per tonne in 2024 (2023 – 0.39 grams per tonne). Due to the nature of heap leach operations, point-in-time recovery rates are not meaningful. |

| (c) | “Gold equivalent ounces” include silver ounces produced and sold converted to a gold equivalent based on a ratio of the average spot market prices for the commodities for each period. The ratio for 2024 was 84.43:1 (2023 – 83.13:1). |

| (d) | “Production cost of sales per equivalent ounce sold” is defined as production cost of sales divided by total gold equivalent ounces sold. |

| (e) | "nm" means not meaningful. |

The Company acquired a 50% ownership interest in the Round Mountain open pit mine, located in Nye County, Nevada, with the acquisition of Echo Bay Mines Ltd. on January 31, 2003. On January 11, 2016, the Company acquired the remaining 50% interest in Round Mountain, along with the Bald Mountain gold mine, from Barrick Gold Corporation (“Barrick”).

2024 vs. 2023

Gold equivalent ounces produced and sold in 2024 decreased by 9% and 8%, respectively, compared to 2023, due to fewer ounces recovered from the heap leach pads, partially offset by higher mill grades. Tonnes of ore mined decreased by 54% in 2024 compared to 2023, due to planned mine sequencing, which included deeper, higher-grade ore benches of Phase W2 and the start of Phase S capital development in early 2024. Tonnes processed decreased by 62%, compared to 2023, due to the decrease in tonnes of ore mined and placed on the heap leach pads. During 2024, mill grades increased by 37% as a result of mining the deeper, higher-grade benches of Phase W2.

Metal sales increased by 12% in 2024 compared to 2023, due to the 23% increase in average metal prices realized, partially offset by the decrease in gold equivalent ounces sold. Production cost of sales decreased by 8% compared to 2023 primarily due to a higher proportion of costs allocated to capital development, related to the start of Phase S development in early 2024, and the decrease in gold equivalent ounces sold, partially offset by higher royalties as a result of the increase in average metal prices. Production cost of sales per equivalent ounce sold in 2024 was comparable to 2023. Depreciation, depletion and amortization increased by 23% in 2024 compared to 2023 due to a decrease in mineral reserves at Phase W at the end of 2023 and a higher depreciable asset base as a result of the impairment reversal recognized in the third quarter of 2024, as discussed below, partially offset by the decrease in gold equivalent ounces sold.

In 2024, the Company recognized an after-tax reversal of a previously recorded impairment charge of $73.4 million related to property, plant and equipment, as a result of an increase in the Company’s estimates of future gold prices. The tax impact of the impairment reversal at Round Mountain was an income tax expense of $0.7 million.

Exploration activity at Round Mountain was higher in 2024 compared to 2023, focusing primarily on the continued development of the Phase X underground exploration decline, which began late in the first quarter of 2023, as well as exploration drilling in between the open pit and the underground target.

20

Kinross Gold Corporation

management’s discussion and analysis

For the year ended December 31, 2024

Bald Mountain – USA

| Years ended December 31, | ||||||||||||||||

| 2024 | 2023 | Change | % Change(d) | |||||||||||||

| Operating Statistics | ||||||||||||||||

| Tonnes ore mined (000's) | 18,392 | 17,312 | 1,080 | 6 | % | |||||||||||

| Tonnes processed (000's) | 18,392 | 17,306 | 1,086 | 6 | % | |||||||||||

| Grade (grams/tonne)(a) | 0.48 | 0.42 | 0.06 | 14 | % | |||||||||||

| Gold equivalent ounces(b): | ||||||||||||||||

| Produced | 181,047 | 157,749 | 23,298 | 15 | % | |||||||||||

| Sold | 182,760 | 180,139 | 2,621 | 1 | % | |||||||||||

| Earnings (in millions) | ||||||||||||||||

| Metal sales | $ | 438.2 | $ | 349.6 | $ | 88.6 | 25 | % | ||||||||

| Production cost of sales | 220.3 | 223.5 | (3.2 | ) | (1 | )% | ||||||||||

| Depreciation, depletion and amortization | 143.0 | 107.8 | 35.2 | 33 | % | |||||||||||

| 74.9 | 18.3 | 56.6 | nm | |||||||||||||

| Other operating expense | 0.9 | 1.2 | (0.3 | ) | (25 | )% | ||||||||||

| Exploration and business development | 6.0 | 3.2 | 2.8 | 88 | % | |||||||||||

| Segment operating earnings | $ | 68.0 | $ | 13.9 | $ | 54.1 | nm | |||||||||

| Production cost of sales per equivalent ounce(b) sold(c) | $ | 1,205 | $ | 1,241 | $ | (36 | ) | (3 | )% | |||||||

| (a) | Due to the nature of heap leach operations, point-in-time recovery rates are not meaningful. |

| (b) | “Gold equivalent ounces” include silver ounces produced and sold converted to a gold equivalent based on a ratio of the average spot market prices for the commodities for each period. The ratio for 2024 was 84.43:1 (2023 – 83.13:1). |

| (c) | “Production cost of sales per equivalent ounce sold” is defined as production cost of sales divided by total gold equivalent ounces sold. |

| (d) | “nm” means not meaningful. |

The Company completed the acquisition of 100% of the Bald Mountain open pit mine on January 11, 2016 from Barrick, which includes a large associated land package. On October 2, 2018, the Company acquired the remaining 50% interest in the Bald Mountain exploration joint venture that it did not already own from Barrick, giving Kinross 100% ownership of the Bald Mountain land package.

2024 vs. 2023

Gold equivalent ounces produced in 2024 increased by 15% compared to 2023 due to higher grades. Planned mine sequencing at Bald Mountain focused primarily on the development and mining of Saga 6, resulting in a 6% increase in tonnes of ore mined and processed, and a 14% increase in grade in 2024 compared to 2023. Gold equivalent ounces sold in 2024 were comparable to 2023 and were higher than production due to the timing of sales.

Metal sales increased by 25% compared to 2023, primarily due to the increases in average metal prices realized. Production cost of sales were comparable to 2023, as lower supplies costs were offset by a lower proportion of mining activities related to capital development. Production cost of sales per equivalent ounce sold decreased by 3% in 2024 compared to 2023 as a result of the increase in gold equivalent ounces produced and the slight decrease in production cost of sales. Depreciation, depletion and amortization increased by 33% compared to 2023, primarily due to an increase in the depreciable asset base, largely related to the completion of Saga 6 capital development in the first quarter of 2024.

21

Kinross Gold Corporation

management’s discussion and analysis

For the year ended December 31, 2024

Consolidated Results

Impairment (Reversal) Charge

| Years ended December 31, | ||||||||||||||||

| (in millions) | 2024 | 2023 | Change | % Change(a) | ||||||||||||

| Property, plant and equipment | $ | (74.1 | ) | $ | - | $ | (74.1 | ) | nm | |||||||

| Inventories | - | 38.9 | (38.9 | ) | nm | |||||||||||

| $ | (74.1 | ) | $ | 38.9 | $ | (113.0 | ) | nm | ||||||||

| (a) | “nm” means not meaningful. |

In the third quarter of 2024, the Company recorded a reversal of a previously recorded impairment charge of $74.1 million, related entirely to property, plant and equipment at Round Mountain, as a result of an increase in the Company’s estimates of future gold prices. The reversal was limited to the carrying value that would have been determined, net of any applicable depreciation, had no impairment charge been previously recognized, and represents the full reversal of the impairment charge previously recorded in 2022. The tax impact of the impairment reversal was an income tax expense of $0.7 million.

In the fourth quarter of 2023, the Company recognized an impairment charge of $38.9 million related to a reduction in the estimate of recoverable ounces on the Fort Knox heap leach pads due to changes in estimated recovery rates. The tax impact of the impairment was an income tax recovery of $3.1 million.

Exploration and Business Development

| Years ended December 31, | ||||||||||||||||

| (in millions) | 2024 | 2023 | Change | % Change | ||||||||||||

| Exploration and business development | $ | 197.8 | $ | 185.0 | $ | 12.8 | 7 | % | ||||||||

Included in total exploration and business development expense are expenditures on exploration and technical evaluations totaling $166.4 million compared to $158.9 million in 2023. The increase was primarily as a result of higher spending at Round Mountain Phase X, partially offset by lower spending at Great Bear.

Capitalized exploration and evaluation expenditures, which relate to Lobo-Marte and Great Bear and include capitalized interest, totaled $92.1 million compared to $93.4 million in 2023. Total expensed and capitalized exploration and evaluation expenditures were $258.5 million in 2024 compared to $252.3 million in 2023.

General and Administrative

| Years ended December 31, | ||||||||||||||||

| (in millions) | 2024 | 2023 | Change | % Change | ||||||||||||

| General and administrative(a) | $ | 126.2 | $ | 108.7 | $ | 17.5 | 16 | % | ||||||||

| (a) | Included within general and administrative expenses is $11.5 million (2023 – $8.7 million) relating to share-based compensation. |

General and administrative expenses include costs related to the overall management of the business which are not part of direct mine operating costs. These costs are incurred at corporate offices located in Canada, the United States, Brazil, Chile, the Netherlands, and Spain.

Finance Expense

| Years ended December 31, | ||||||||||||||||

| (in millions) | 2024 | 2023 | Change | % Change | ||||||||||||

| Interest expense, including accretion of lease liabilities | $ | 50.5 | $ | 69.0 | $ | (18.5 | ) | (27 | )% | |||||||

| Accretion of reclamation and remediation obligations | 40.9 | 37.0 | 3.9 | 11 | % | |||||||||||

| Finance expense | $ | 91.4 | $ | 106.0 | $ | (14.6 | ) | (14 | )% | |||||||

Interest expense decreased by $18.5 million compared to 2023. Interest capitalized in 2024 was $88.2 million, compared to $108.9 million 2023. Total interest decreased in 2024 compared to 2023, primarily due to repayments of debt in the second half of 2023 and throughout 2024.

Accretion of reclamation and remediation obligations increased by $3.9 million compared to 2023 primarily as a result of increases in the cost estimates for the Company’s reclamation and remediation obligations.

22

Kinross Gold Corporation

management’s discussion and analysis

For the year ended December 31, 2024

Income and Other Taxes

Kinross is subject to tax in various jurisdictions including Canada, the United States, Brazil, Chile and Mauritania.

The Company recorded an income tax expense of $487.4 million in 2024 (2023 – $293.2 million), including a $86.4 million deferred tax expense in 2024 (2023 – $29.3 million) resulting from the net foreign currency translation of tax deductions related to the Company’s operations in Brazil and Mauritania. Income tax expense in 2024 is also net of a $32.6 million deferred tax recovery as a result of a change in uncertain tax positions. Kinross' combined federal and provincial statutory tax rate for both 2024 and 2023 was 26.5%.

There are a number of factors that can significantly impact the Company’s effective tax rate, including geographical distribution of income, varying rates in different jurisdictions, the non-recognition of tax assets, mining allowance, mining specific taxes, foreign currency exchange movements, changes in tax laws, and the impact of specific transactions and assessments.

Kinross’ tax records, transactions and filing positions may be subject to examination by the tax authorities in the countries in which the Company has operations. The tax authorities may review the Company’s transactions in respect of the year, or multiple years, which they have chosen for examination. The tax authorities may interpret the tax implications of a transaction, in form or in fact, differently from the interpretation reached by the Company.

In circumstances where the Company and the tax authority cannot reach a consensus on the tax impact, there are processes and procedures which both parties may undertake in order to reach a resolution, which may span many years in the future. The Company assesses the expected outcome of examination of transactions by the tax authorities and accrues the expected outcome in accordance with IFRS.

Uncertainty in the interpretation and application of applicable tax laws, regulations or the relevant sections of Mining Conventions by the tax authorities, or the failure of relevant Governments or tax authorities to honour tax laws, regulations or the relevant sections of Mining Conventions could adversely affect Kinross.

Due to the number of factors that can potentially impact the effective tax rate and the sensitivity of the tax provision to these factors, as discussed above, it is expected that the Company's effective tax rate will fluctuate in future periods.

The Global Minimum Tax Act (“GMTA”) was enacted in Canada on June 20, 2024. The GMTA includes a 15% global minimum tax (“top-up tax”) that applies to large multinational enterprise groups with global consolidated revenues over €750 million. As a result, the Company will be subject to the top-up tax rules for its 2024 taxation year. The GMTA did not have a material impact on the Company in 2024 and is not expected to have a material impact going forward, as none of the Company’s jurisdictions are expected to be subject to any material top up tax amounts for 2024 and onwards.

Discontinued Operations

Chirano discontinued operations

On August 10, 2022, the Company announced that it had completed the sale of its 90% interest in the Chirano mine in Ghana to Asante Gold Corporation (“Asante”) for total consideration of $225.0 million in cash and shares. In accordance with the sale agreement, which was amended on February 10, 2023, the Company received $60.0 million in cash and 34,962,584 Asante shares on closing, and the remaining cash consideration of $128.8 million was to be received over the two-year period subsequent to closing. The total deferred consideration is secured through pledges by Asante of equity interests in certain acquired entities holding an indirect interest in the Chirano mine. The Company’s Chirano operations were classified as discontinued operations in 2022.

During the year ended December 31, 2024, the Company received $10.0 million (year ended December 31, 2023 – $5.0 million) in respect of the deferred payment consideration, which was recognized as net cash flow in discontinued operations from investing activities. As at December 31, 2024, the fair value of the remaining deferred payment consideration is $100.0 million (December 31, 2023 – $107.9 million) and is classified as a current receivable.

Russian discontinued operations

On June 15, 2022, the Company announced that it had completed the sale of its Russian operations to the Highland Gold Mining group of companies for total cash consideration of $340.0 million, of which $300.0 million was received on closing and the remaining $40.0 million was received during the second quarter of 2023 and recognized as net cash flow in discontinued operations from investing activities.

23

Kinross Gold Corporation

management’s discussion and analysis

For the year ended December 31, 2024

| 6. | LIQUIDITY AND CAPITAL RESOURCES |

The following table summarizes Kinross’ cash flow activity:

| Years ended December 31, | ||||||||||||||||

| (in millions) | 2024 | 2023 | Change | % Change(b) | ||||||||||||

| Net cash flow provided from operating activities | $ | 2,446.4 | $ | 1,605.3 | $ | 841.1 | 52 | % | ||||||||

| Net cash flow of continuing operations used in investing activities | (1,189.9 | ) | (1,167.2 | ) | (22.7 | ) | nm | |||||||||

| Net cash flow of discontinued operations provided from investing activities(a) | 10.0 | 45.0 | (35.0 | ) | (78 | )% | ||||||||||

| Net cash flow used in financing activities | (1,005.9 | ) | (549.0 | ) | (456.9 | ) | nm | |||||||||

| Effect of exchange rate changes on cash and cash equivalents | (1.5 | ) | 0.2 | (1.7 | ) | nm | ||||||||||

| Increase (decrease) in cash and cash equivalents | 259.1 | (65.7 | ) | 324.8 | nm | |||||||||||