EXHIBIT 99.1

| The Emerging Regional Bank of the Mid-South. |

| Cautionary Statements A number of statements we will be making in our presentation and in the accompanying slides will be "forward-looking statements" within the meaning of the Private Securities Litigation Reform Act of 1995, such as statements of BancorpSouth's plans, goals, objectives, expectations, projections, estimates, intentions, future performance and business of BancorpSouth, including, without limitation, (i) statements relating to non- interest revenue, growth strategies, BancorpSouth's comprehensive line of products and services,non-interest revenue products and services, customer relationships, centralized back office, loan growth and lending opportunities, dividend growth, capital resources, expansion in targeted growth markets, including East Texas, Northwest Arkansas, the Florida Panhandle and Northwest Georgia, expansion in the Mid-South region, market presence, diversification of revenue stream, retail lending products and features, lending and credit policies, future acquisitions and business expansions, asset quality, credit quality, non-performing assets and loan losses, capital position, shareholder value, stock repurchase program, retail deposits, risk management, and (ii) statements that reference a future period or that are preceded by, followed by or that include the words "may", "could", "would", "should", "believes", "expects", "anticipates", "estimates", "intends", "plans", "targets", "probably", "potentially", "projects" or similar expressions. These forward-looking statements involve significant risks and uncertainties and are subject to change based on various factors (some of which are beyond BancorpSouth's control and we caution you not to place undue reliance on these forward-looking statements). Factors that might cause BancorpSouth's financial performance to differ materially from the plans, goals, objectives, expectations and intentions expressed in such forward-looking statements include, but are not limited to: (i) revenues may be lower than expected, or deposit attrition, operating costs or customer loss and business disruption may be greater than expected; (ii) competitive pressures among depository and other financial institutions may increase significantly; (iii) the ability of BancorpSouth to manage its growth and effectively serve an expanding customer and market base; (iv) changes in BancorpSouth's operating or expansion strategy; (v) the ability of BancorpSouth to implement its retail lending strategy; (vi) a decline in asset quality; (vii) the ability of BancorpSouth to repurchase its common stock on favorable terms; (viii) general economic or business conditions, either nationally or in the states or regions in which BancorpSouth does business, may be less favorable than expected, resulting in, among other things, a deterioration in credit quality or a reduced demand for credit and reduced loan growth and lending opportunities; (ix) fluctuations in prevailing interest rates and the effectiveness of BancorpSouth's interest rate hedging strategies; (x) the ability of BancorpSouth to operate and integrate new technology; (xi) the ability of BancorpSouth to provide and market competitive services and products; (xii) legislative or regulatory changes may adversely affect the business in which BancorpSouth is engaged; (xiii) the ability of BancorpSouth to expand into growth markets; and (xiv) changes may occur in the securities markets. Additional information with respect to factors that may cause actual results to differ materially from those contemplated by such forward-looking statements is included in BancorpSouth's current and subsequent filings with the Securities and Exchange Commission. BancorpSouth does not undertake any obligation to update any forward-looking statement, whether written or oral. During this presentation, we may discuss certain non-GAAP financial measures in talking about BancorpSouth's performance. You can find the reconciliation of those measures to the most directly comparable GAAP financial measures under the link "News Releases" on the investor relations portion of our website, which is located at www.bancorpsouth.com. The link to the reconciliation is located under the link to the webcast of this presentation. |

| Profile Six-state financial holding company Approximately 256 locations $10.8 billion in assets Provides comprehensive line of financial products and services to individuals and small-to-medium sized businesses $1.6 billion market capitalization |

| Key Investment Considerations Unique market presence Substantial non-interest revenue growth Centralized back office Strong credit quality Solid capital position Shareholder value focus |

| 1999 Annual Report Map |

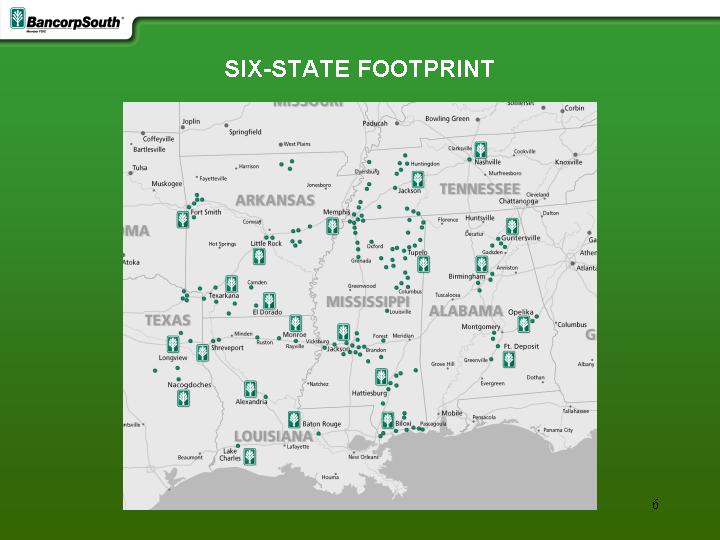

| SIX-STATE FOOTPRINT |

| BANCORPSOUTH MARKET AREA |

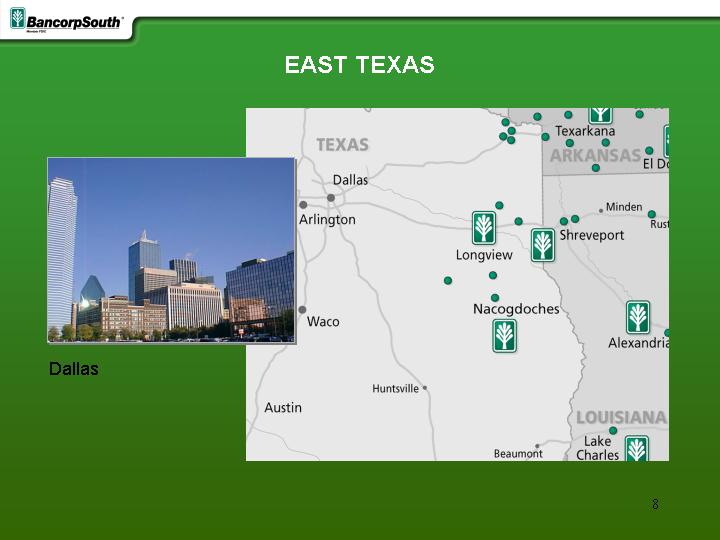

| EAST TEXAS Dallas |

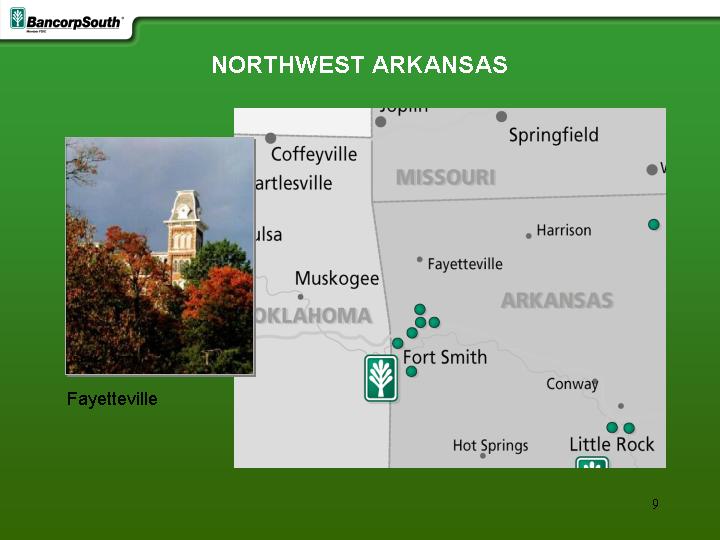

| NORTHWEST ARKANSAS Fayetteville |

| FLORIDA PANHANDLE |

| NORTHWEST GEORGIA Atlanta |

| Financial Review Nash Allen Chief Financial Officer |

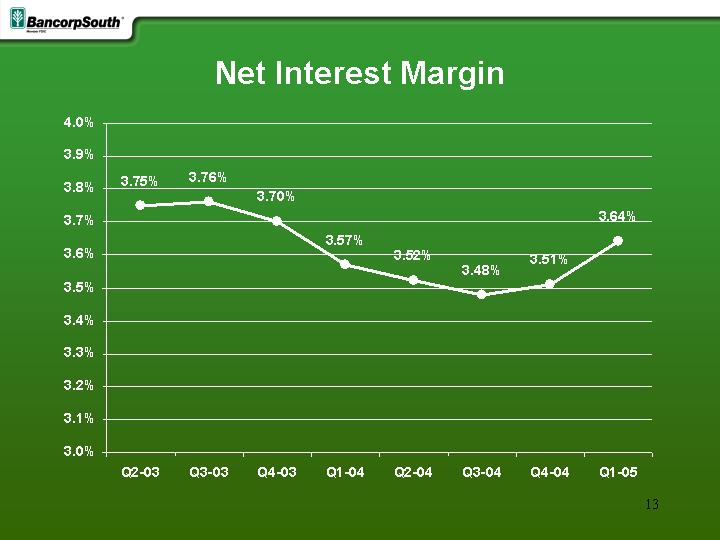

| Net Interest Margin |

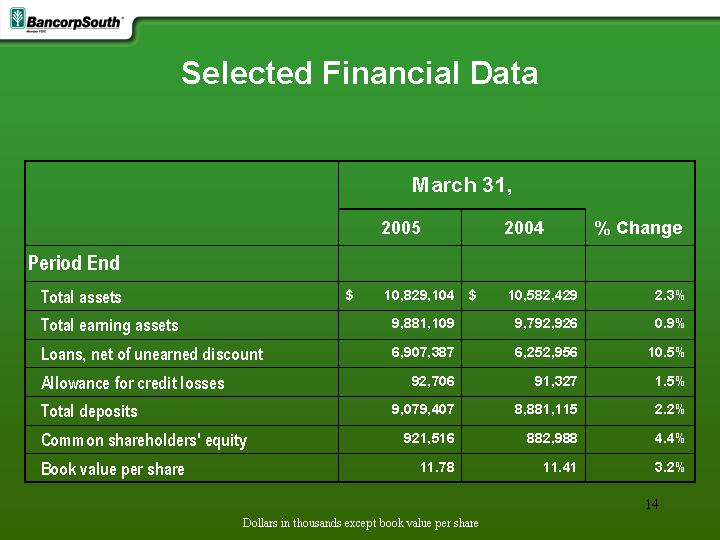

| Selected Financial Data Dollars in thousands except book value per share |

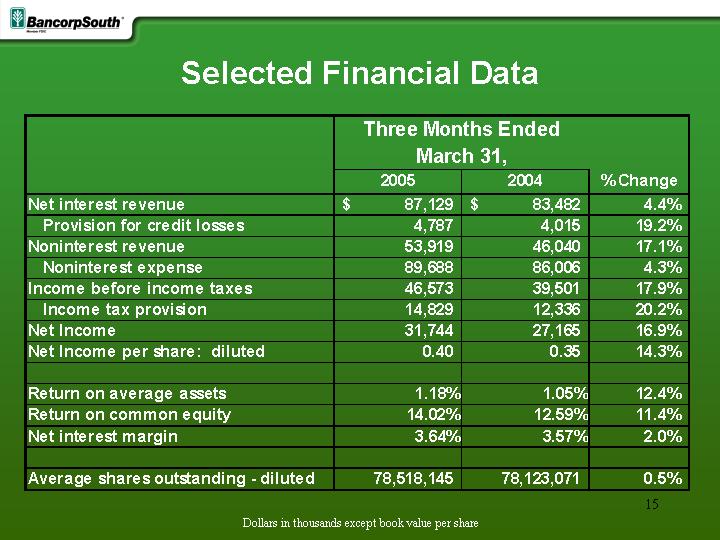

| Selected Financial Data Dollars in thousands except book value per share |

| Earnings Per Share |

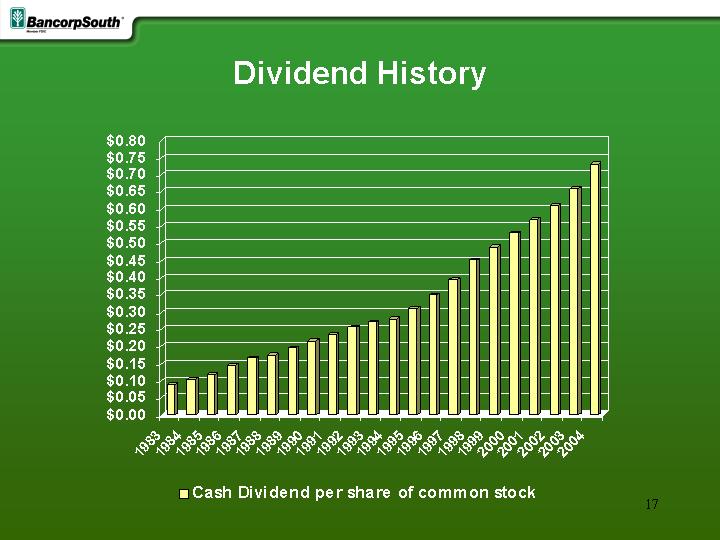

| Dividend History |

| Insurance James Threadgill Vice Chairman |

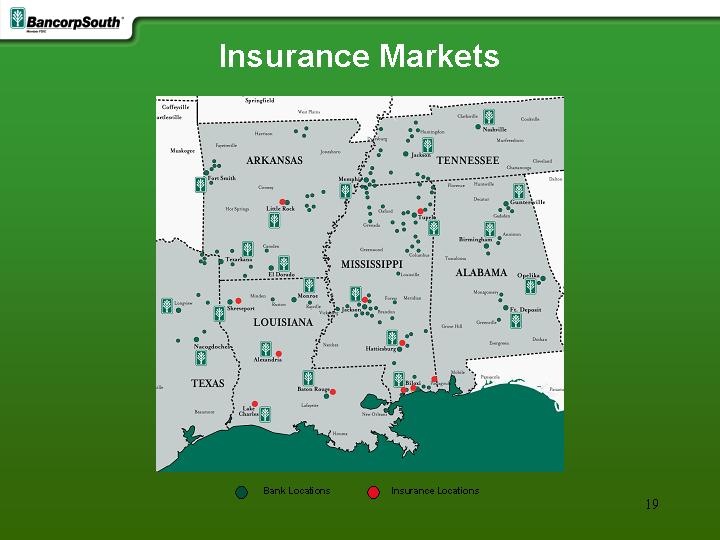

| Insurance Markets Bank Locations Insurance Locations |

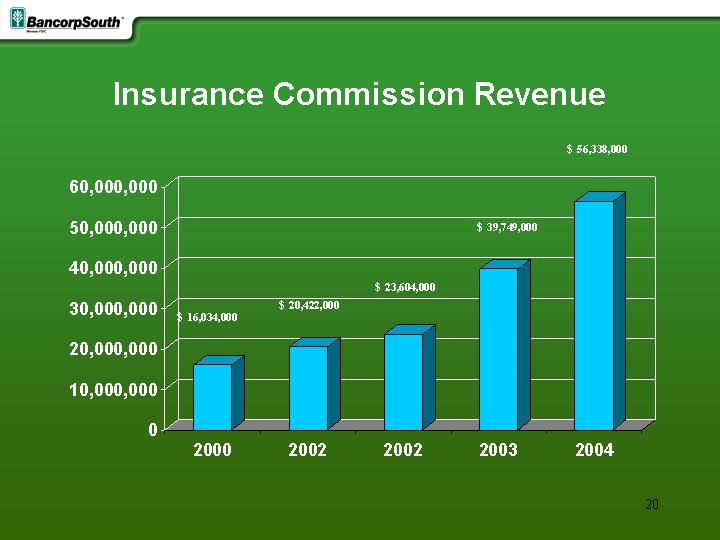

| Insurance Commission Revenue 2000 2002 2002 2003 2004 16034000 20422000 23604000 39749000 56338000 West 30.6 38.6 34.6 31.6 North 45.9 46.9 45 43.9 56,338,000 39,749,000 23,604,000 20,422,000 16,034,000 $ $ $ $ $ |

| Insurance Commission Revenue RKFL SSH W&P Insurance Services Total 2000 2001 2002 2003 2004 14,180,000 5,129,000 19,797,000 19,014,000 17,936,000 16,168,000 14,084,000 16,641,000 9,562,000 5,720,000 6,044,000 5,668,000 4,207,000 1,950,000 56,338,000 39,749,000 23,604,000 20,422,000 16,034,000 RKFL-Ramsey, Krug, Farrell & Lensing-Arkansas W&P-Wright and Percy-Louisiana SSH-Stewart Sneed Hewes-Mississippi $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ |

| 2004 Insurance Premium Volume Surety Commercial Lines Personal Lines Life & Health Total Premiums Written 11,930,000 293,000,000 26,400,000 121,900,000 453,230,000 $ $ $ $ $ (By Product Lines) |

| Selected Holding Companies Ranked by Insurance Revenues Wells Fargo & Company, San Francisco CA Rank (In hundreds) BB&T Corporation, Winston-Salem, NC Wachovia Corporation, Charlotte, NC Regions Financial Corp., Birmingham, AL SunTrust Banks, Inc., Atlanta, GA BancorpSouth, Inc., Tupelo, MS 1 4 6 12 20 21 $1,193,000 $619,055 $319,000 $86,001 $59,848 $58,103 Source: American Bankers Insurance Association 2004 |

| Lending Gregg Cowsert Vice Chairman |

| Continued Strong Asset Quality |

| Our Strategy Achieve aggressive loan growth goals Maintain asset quality levels Consistently low levels of non-performing assets and loan losses |

| Non-Performing Assets Non-Accrual Loans 12/31/02 12/31/03 12/31/04 (In hundreds) 29,124 $18,139 21,676 18,048 $10,514 $12,335 33,293 14,952 14,741 Loans 90+Days Past Due & Restructured Loans TOTAL Other Real Estate Net Charge Offs (annualized) Provision for Credit Losses (In hundreds) $57,686 $66,384 $48,752 ..41% ..33% ..31% $29,411 $25,130 $17,485 |

| Non-Performing Assets Non-Accrual Loans 2004 2005 (In hundreds) 23,346 18,804 18,176 $16,410 $13,184 15,754 Loans 90+Days Past Due & Restructured Loans TOTAL Other Real Estate Net Charge Offs (annualized) Provision for Credit Losses (In hundreds) $57,932 $47,742 ..31% ..22% $ 4,411 $ 4,787 Three Months Ended March 31 |

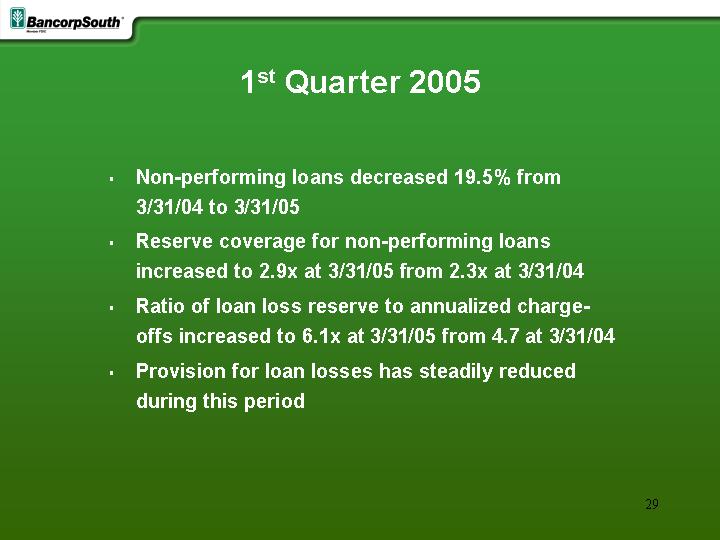

| 1st Quarter 2005 Non-performing loans decreased 19.5% from 3/31/04 to 3/31/05 Reserve coverage for non-performing loans increased to 2.9x at 3/31/05 from 2.3x at 3/31/04 Ratio of loan loss reserve to annualized charge- offs increased to 6.1x at 3/31/05 from 4.7 at 3/31/04 Provision for loan losses has steadily reduced during this period |

| Retail Lending Initiative |

| Retail Credit Administration Group Expanded products & product features Lower net losses (consistent decisions) Improved pricing (consistent risk based pricing) Enhanced fee income |

| Our Goal To implement an effective process for originating these products, driving profitable growth with appropriate risk management strategies. |

| Increasing Opportunities For Loan Growth |

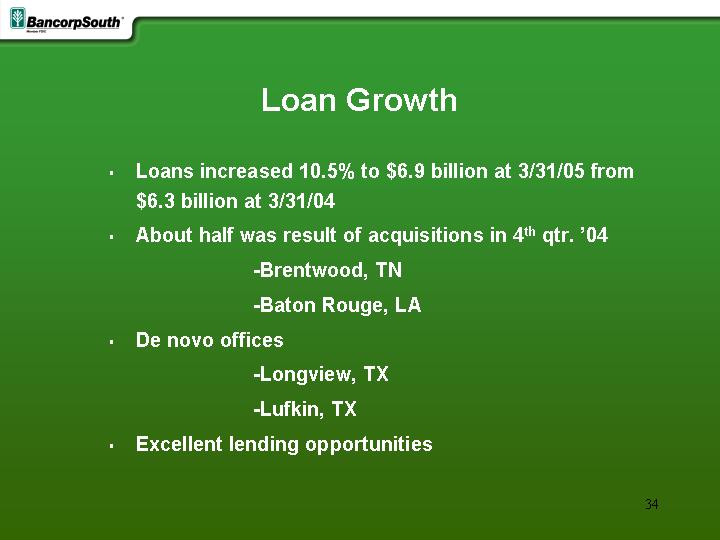

| Loan Growth Loans increased 10.5% to $6.9 billion at 3/31/05 from $6.3 billion at 3/31/04 About half was result of acquisitions in 4th qtr. '04 -Brentwood, TN -Baton Rouge, LA De novo offices -Longview, TX -Lufkin, TX Excellent lending opportunities |

| Loan Growth Birmingham Memphis Shreveport Mississippi Gulf Coast Jackson, MS (existing markets) |