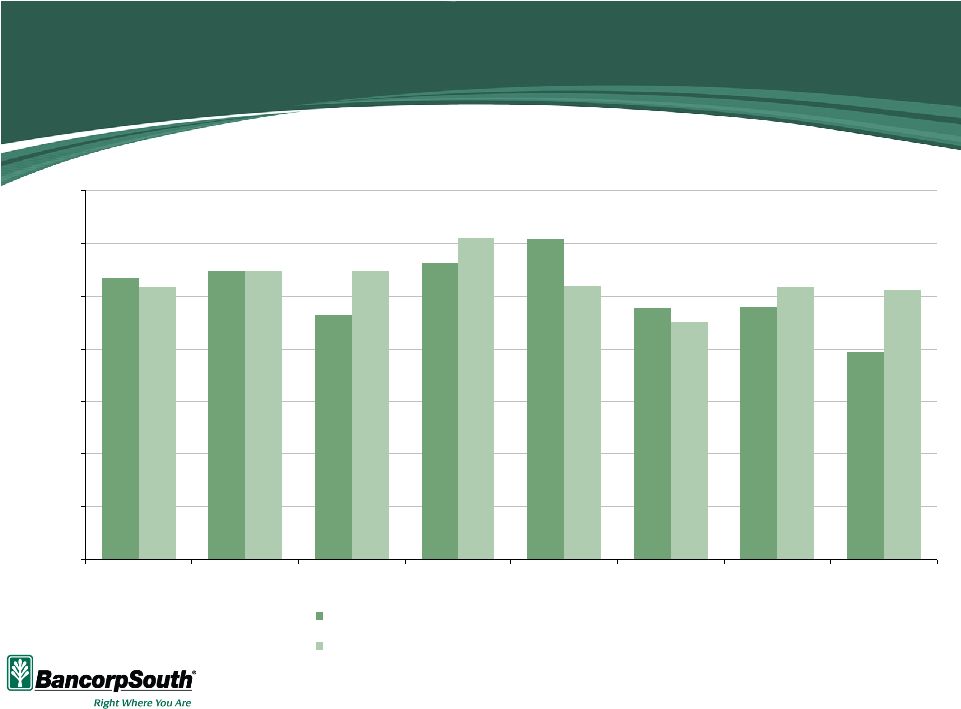

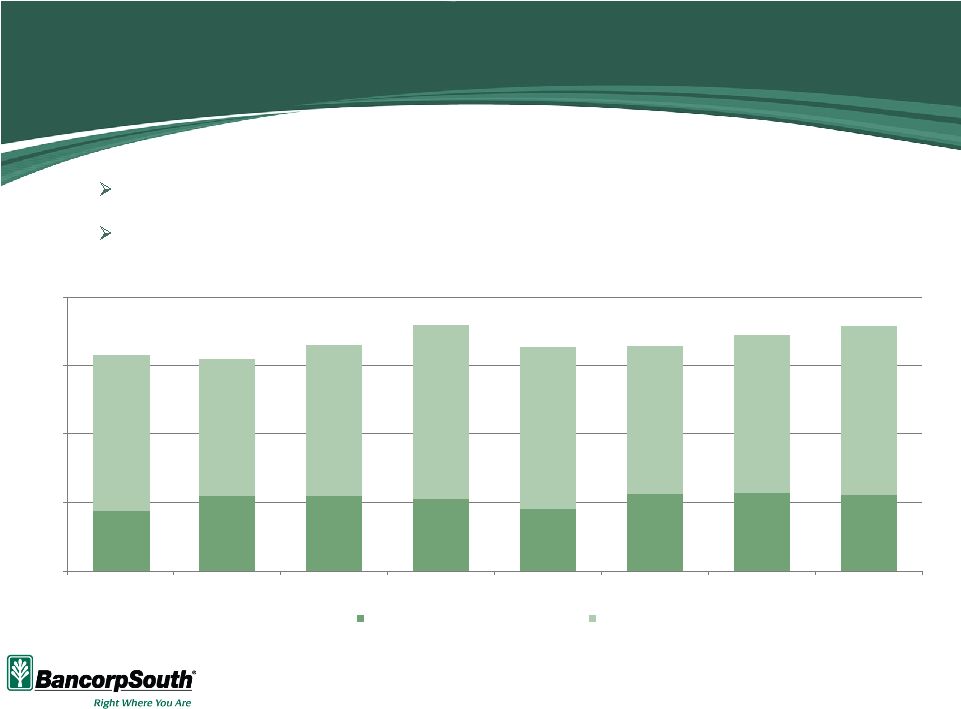

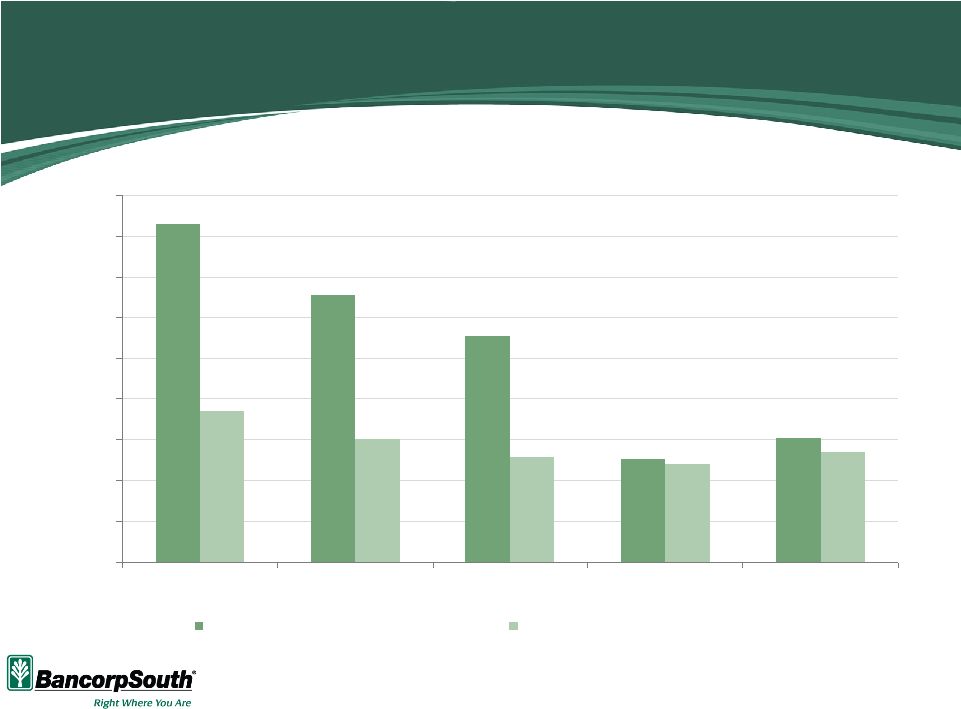

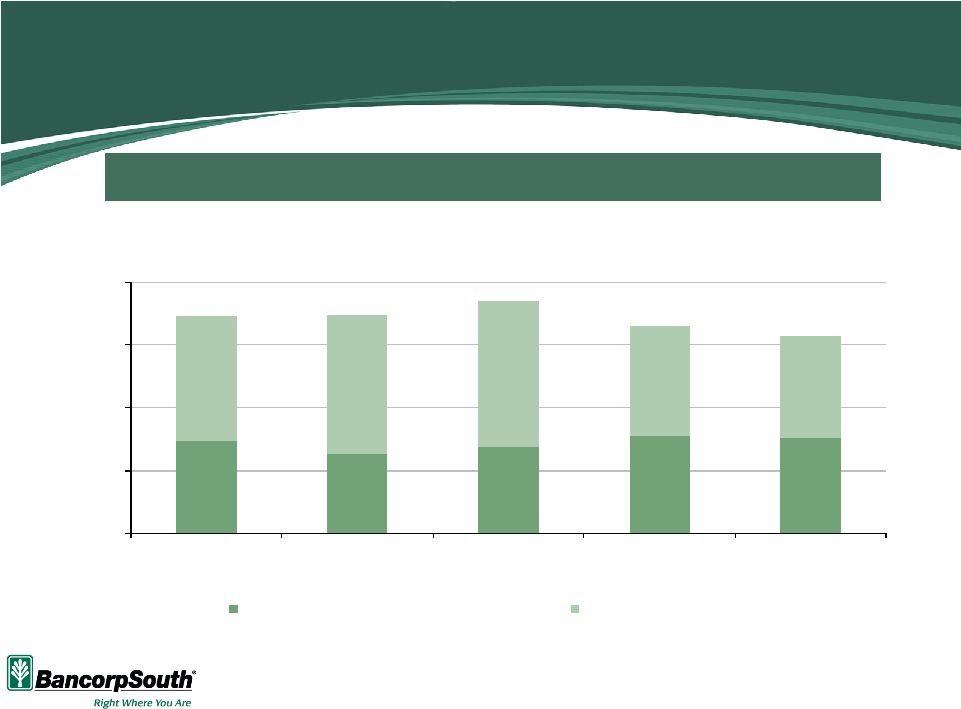

30 Non-GAAP Financial Reconciliation Pre-Tax, Pre-Provision Earnings Reconciliation Q4-09 Q1-10 Q2-10 Q3-10 Q4-10 Q1-11 Q2-11 Q3-11 (Dollars in Thousands) Net Interest Income Before Provision --> A $112,347 $111,882 $109,329 $109,678 $110,253 $109,437 $109,912 $108,075 Noninterest Income --> B 64,505 63,332 57,086 69,752 73,974 68,311 75,144 62,055 Noninterest Expense --> C 123,361 120,483 120,016 123,087 123,447 130,010 137,069 130,698 Pre-Tax Pre-Provision Earnings --> D=A+B-C 53,491 54,731 46,399 56,343 60,780 47,738 47,987 39,432 MSR Valuation Adjustment --> E 1,648 8 (8,323) (4,609) 8,895 2,540 (3,839) (11,676) Pre-Tax Pre-Provision Earnings (Excluding MSR Adjustment) --> F=D-E 51,843 54,723 54,722 60,952 51,885 45,198 51,826 51,108 Tangible Shareholders' Equity / Tangible Assets As of As of As of 9/30/2010 6/30/2011 9/30/2011 (Dollars in Thousands) Shareholders' Equity --> A $1,235,705 $1,246,703 $1,266,753 Assets --> B 13,583,016 13,367,050 13,198,518 Intangibles --> C 290,670 289,546 288,723 Tangible Shareholders' Equity --> D=A-C 945,034 957,157 978,030 Tangible Assets --> E=B-C 13,292,346 13,077,504 12,909,795 Tangible Book Value Per Share Total Equity / Total Assets (%) -- > F=A/B 9.10% 9.33% 9.60% Tangible Common Equity / Tangible Assets (%) -- > G=D/E 7.11% 7.32% 7.58% Common Shares Outstanding -- > H 83,482 83,489 83,489 Tangible Book Value Per Share -- > I=D/H 11.32 11.46 11.71 |