1

July 28, 2009

First Midwest Bancorp, Inc.

Keefe, Bruyette & Woods

Investment Conference

2

Forward Looking Statements

This presentation may contain, and during this presentation our management may

make statements that may constitute “forward-looking statements” within the

meaning of the safe harbor provisions of the Private Securities Litigation Reform Act

of 1995. Forward-looking statements are not historical facts but instead represent

only our beliefs regarding future events, many of which, by their nature, are

inherently uncertain and outside our control. Forward-looking statements include,

among other things, statements regarding our financial performance, business

prospects, future growth and operating strategies, objectives and results. Actual

results, performance or developments could differ materially from those expressed

or implied by these forward-looking statements. Important factors that could cause

actual results to differ from those in the forward-looking statements include, among

others, those discussed in our Annual Report on Form 10-K and other reports filed

with the Securities and Exchange Commission, copies of which will be made

available upon request. With the exception of fiscal year end information previously

included in our Annual Report on Form 10-K, the information contained herein is

unaudited. Except as required by law, we undertake no duty to update the contents

of this presentation after the date of this presentation.

make statements that may constitute “forward-looking statements” within the

meaning of the safe harbor provisions of the Private Securities Litigation Reform Act

of 1995. Forward-looking statements are not historical facts but instead represent

only our beliefs regarding future events, many of which, by their nature, are

inherently uncertain and outside our control. Forward-looking statements include,

among other things, statements regarding our financial performance, business

prospects, future growth and operating strategies, objectives and results. Actual

results, performance or developments could differ materially from those expressed

or implied by these forward-looking statements. Important factors that could cause

actual results to differ from those in the forward-looking statements include, among

others, those discussed in our Annual Report on Form 10-K and other reports filed

with the Securities and Exchange Commission, copies of which will be made

available upon request. With the exception of fiscal year end information previously

included in our Annual Report on Form 10-K, the information contained herein is

unaudited. Except as required by law, we undertake no duty to update the contents

of this presentation after the date of this presentation.

3

First Midwest Presentation Index

Who We Are

Credit Quality

Capital Position

Core Profitability

Why First Midwest

4

Who We Are

5

A Premier Bank | Premier Bank For Commercial | Premier Bank For Retail |

$7.8 billion assets $5.8 billion deposits -66% core transactional -90% Suburban Chicago $5.3 billion loans $3.6 billion trust/investment aum | Seven business lines 25,000 commercial 1,600 trust relationships 200 relationship managers Tenured sales force and market presence | 225,000 retail relationships 1,000 bankers 95 offices 8th largest distribution network in MSA 13th in Chicago MSA Market Share |

Source: Commercial and retail relationships obtained from Harte Hanks Marketing Customer Information System as of 3/31/09

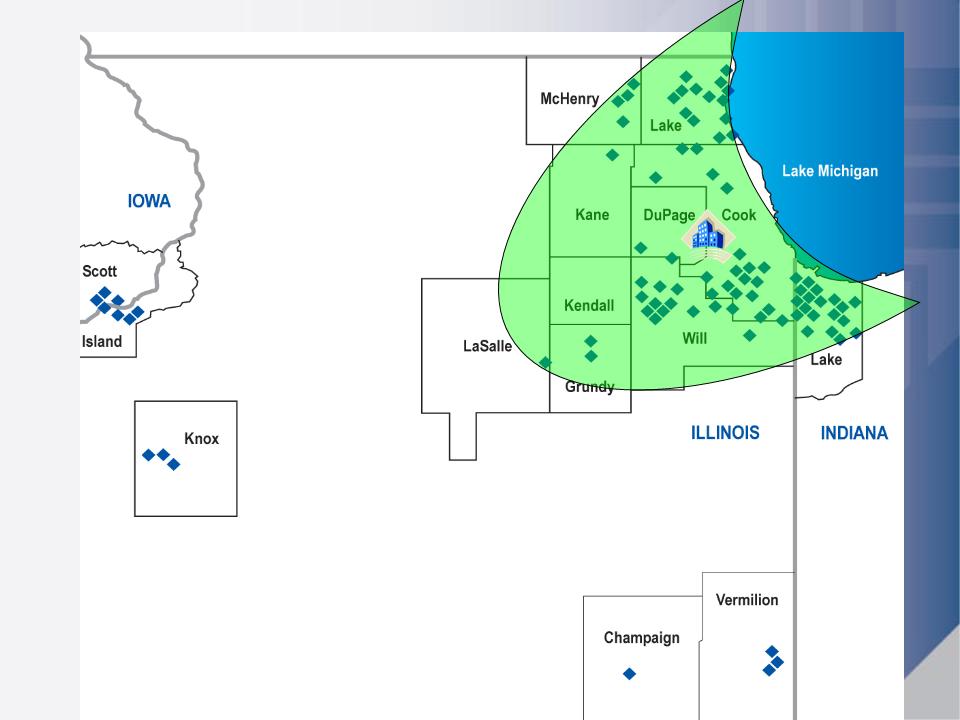

A Premier Community Bank

6

90% Suburban Chicago

7

Credit Quality

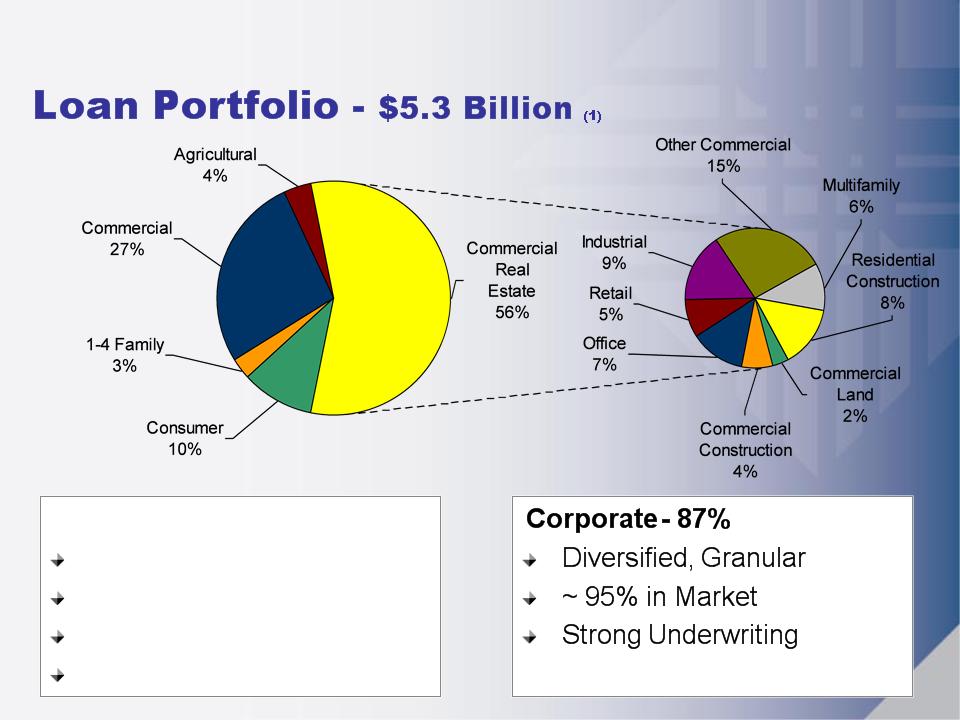

8

(1) As of 2Q09

Total Consumer - 13%

Home Equity Dominated

No Subprime Loans

No Credit Card

Conservative Underwriting

9

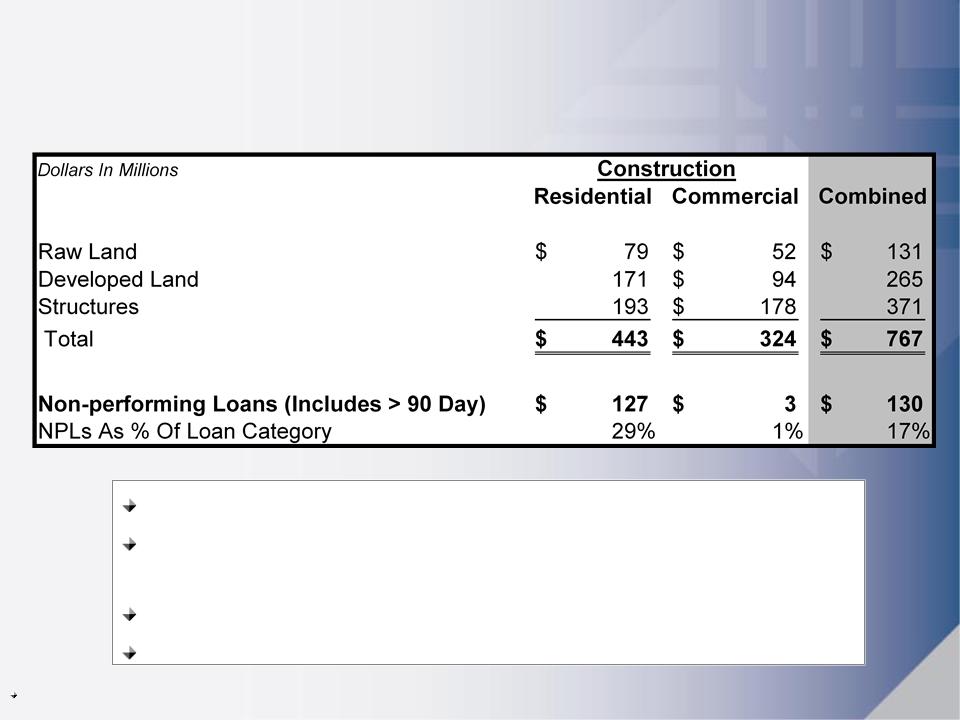

Construction And Development (1)

Performing Commercial Construction Portfolio

Residential NPL % Impacted By Continuing Illiquid

Residential Real Estate Market

Residential Real Estate Market

Substantial Reserves

Current Valuations

As of 2Q09

10

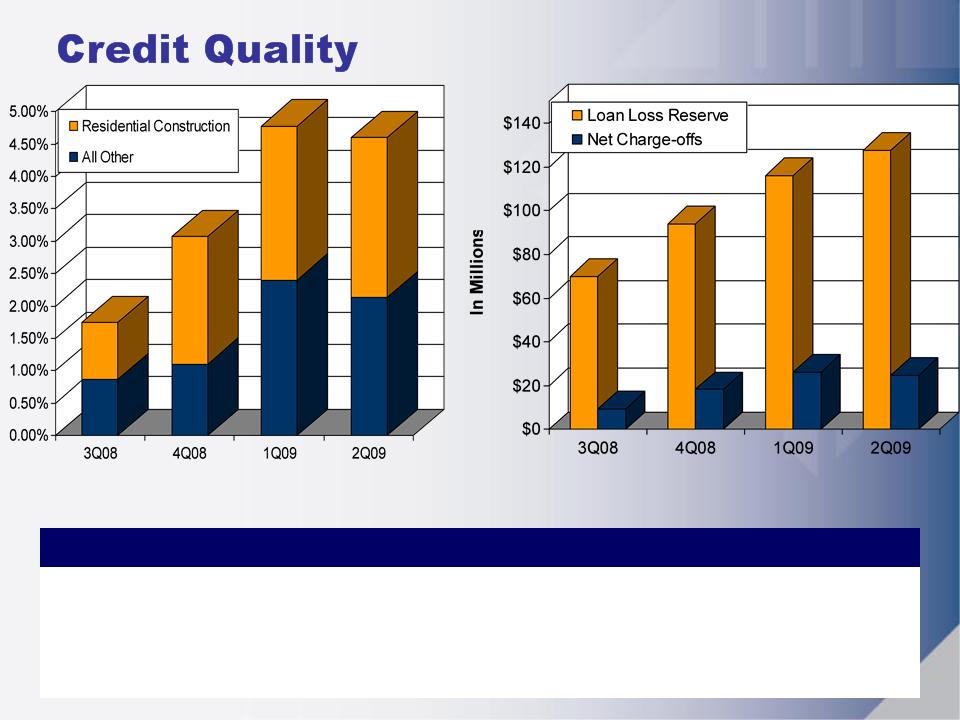

3Q08 | 4Q08 | 1Q09 | 2Q09 | |

Loan Loss Reserve / Loans | 1.34% | 1.75% | 2.15% | 2.40% |

LLR / (Non Accrual + 90 Day) | 77% | 57% | 45% | 52% |

Non Accrual + 90 Day / Total Loans | 1.74% | 3.07% | 4.78% | 4.60% |

(Non Accrual + 90 Day) / Total Loans

Loan Loss Reserve & Net Charge-offs

11

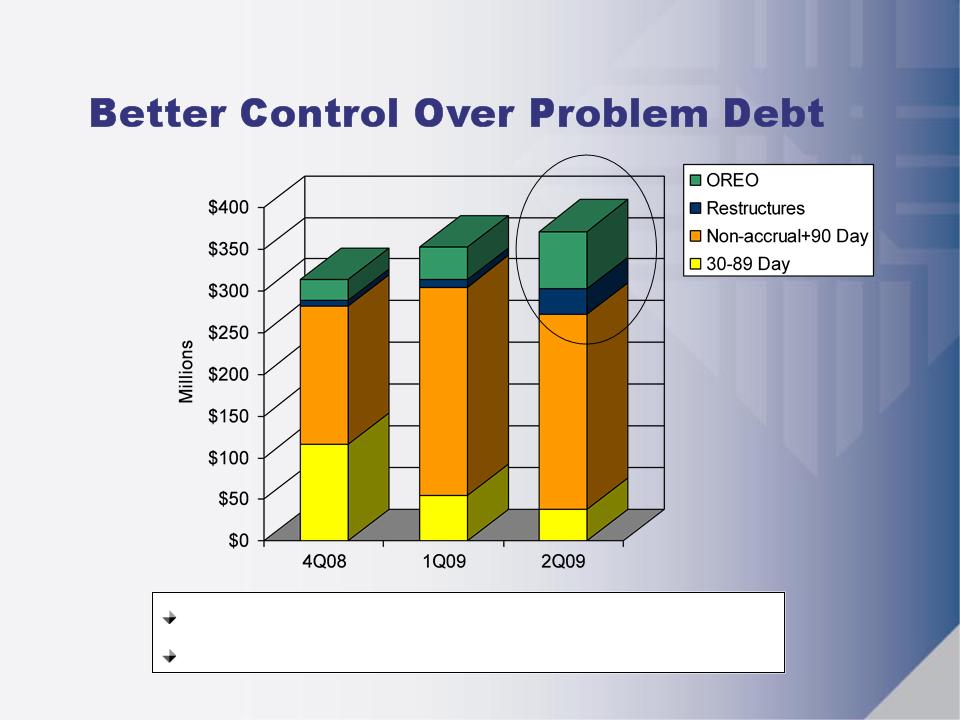

(1) Includes accruing and non-accruing Troubled Debt Restructures (TDRs)

(1)

Improved Delinquencies

Better Positioned To Reduce Problem Debts

12

Credit Focus

Early Identification And Remediation

Expanded Resources

Problem Resolution Strategies

Restructure

Accelerate Control

Varied Liquidation Strategies

13

Capital Position

14

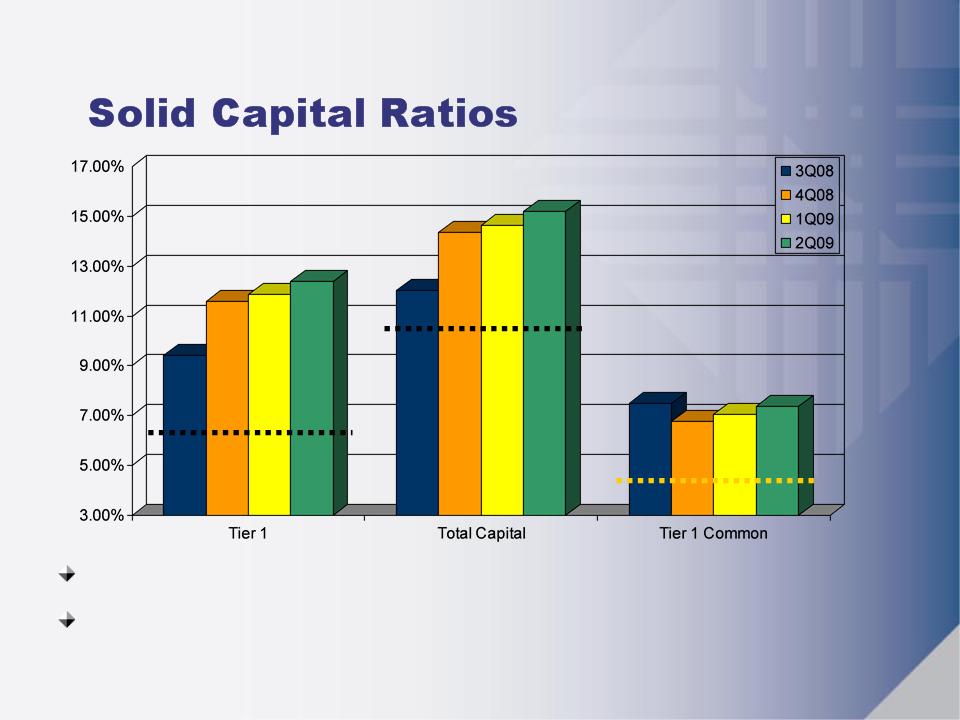

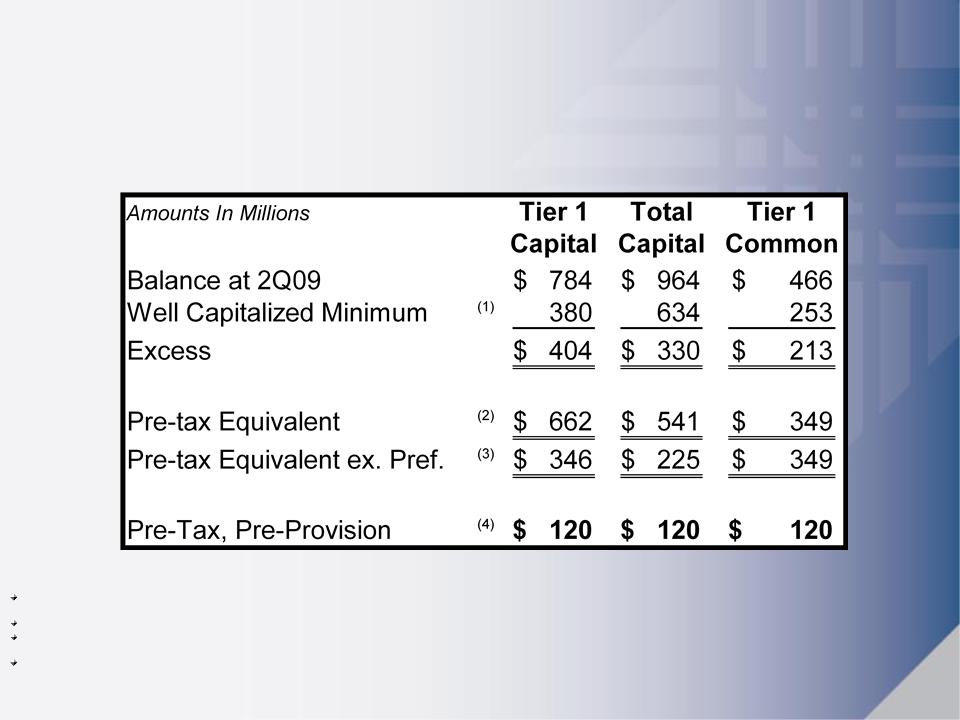

Substantially Exceed “Well Capitalized” (1)

Built Capital Ratios Through Operating Performance, De

-leveraging Securities, And Issue Of Preferred Stock

-leveraging Securities, And Issue Of Preferred Stock

(1) “Well Capitalized” minimum ratios (- - -) are currently 6% for Tier 1, 10% for Total Capital, and 4% for Tier 1 Common (applied to Supervisory Capital Assessment Program

tests on top 19 US banks)

tests on top 19 US banks)

15

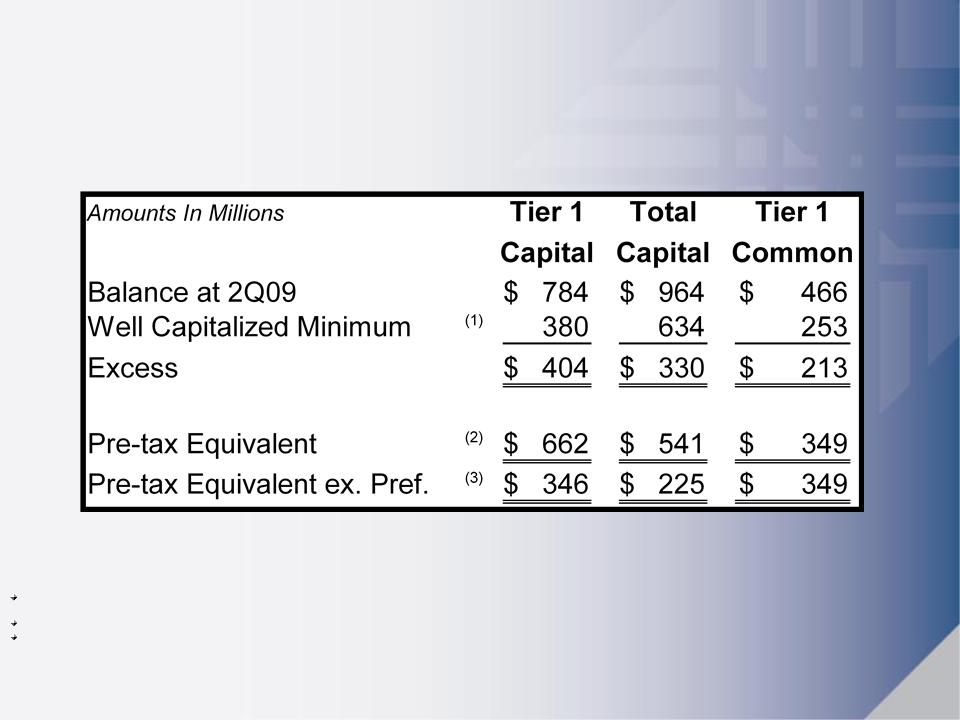

“Well Capitalized” minimum ratios are currently 6% for Tier 1, 10% for Total Capital, and 4% for Tier 1 Common (applied to Supervisory Capital Assessment Program tests on top 19 US

banks)

banks)

Excess over “Well Capitalized” grossed up using 39% marginal tax rate

Represents the Pre-tax equivalent, excluding the $193 million in regulatory capital received by FMBI through the sale of preferred shares to the US Treasury as part of its Capital Purchase

Plan

Plan

Excess Regulatory Capital

16

Core Profitability

17

Operating Leverage - Most Recent Quarter ’09 (4)

Well Above Peers

Well Above Peers

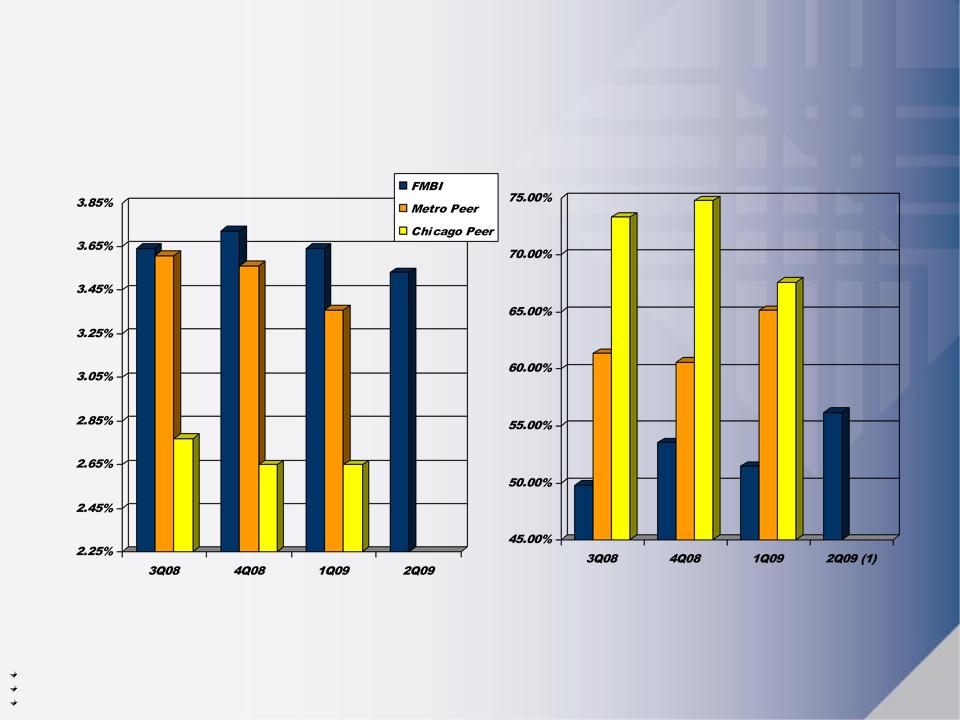

First Midwest | Metro Peers(1) | Chicago Peers(2) | |

PTPP Return on Average Assets(3) | 1.98% | 1.46% | 1.03% |

Core Drivers: | |||

Net Interest Margin | 3.64% | 3.36% | 2.65% |

Efficiency | 51% | 65% | 68% |

Data represents the peer median core performance as reported by SNL Financial

The Metro Peers consist of AMFI, BOKF, CBSH, CFR, FCF, FULT, MBFI, ONB, SUSQ, UCBH, VLY, WTNY, and WTFC

The Chicago Peers consist of AMFI, MBFI, MBHI, OSBC, TAYC, and WTFC

Pre-tax, Pre-provision Operating Income (PTPP) excludes taxes, provision for loan losses, and market related security gains (losses) from reported quarter; PTPP is

computed on a fully tax equivalent basis

computed on a fully tax equivalent basis

As of 1Q09

Almost Double

Greater Ability To Organically Generate Capital

18

Net Interest Margin

Efficiency

Excludes special FDIC assessment and market value adjustment on deferred compensation for 2Q09

The Metro Peers consist of AMFI, BOKF, CBSH, CFR, FCF, FULT, MBFI, ONB, SUSQ, UCBH, VLY, WTNY, and WTFC

The Chicago Peers consist of AMFI, MBFI, MBHI, OSBC, TAYC, and WTFC

Consistently Outperform Peers (2) (3)

19

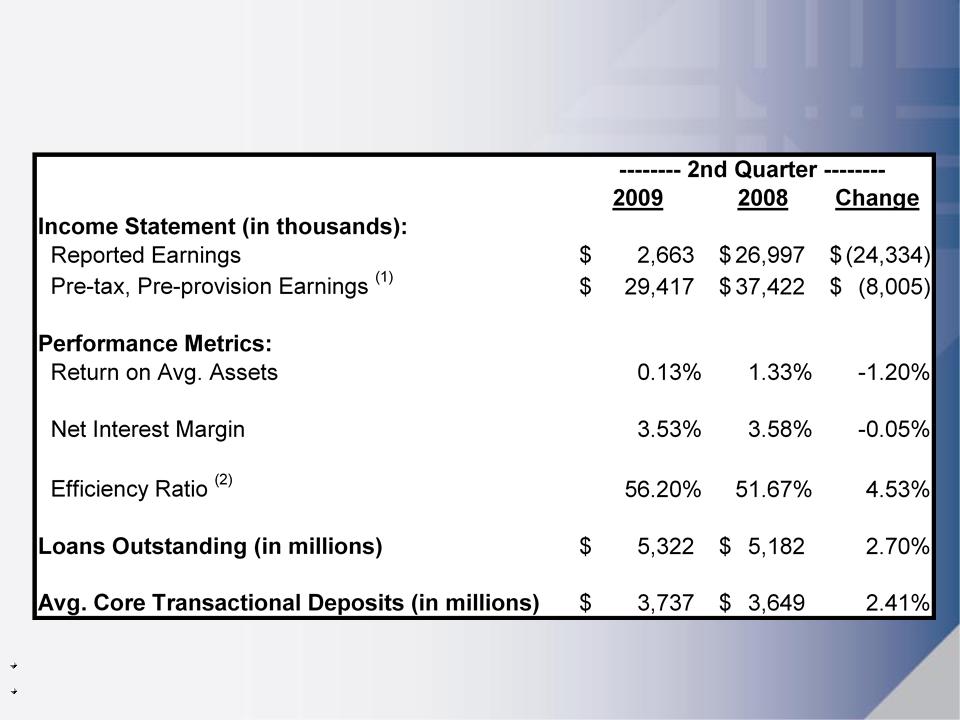

Pre-Tax, Pre-Provision Earnings excludes taxes, provision for loan losses, and market related security gains (losses) from the reported quarter and the special FDIC assessment

levied in second quarter 2009

levied in second quarter 2009

The Efficiency Ratio for second quarter 2009 has been adjusted to exclude the impact of the special FDIC assessment

2nd Quarter Performance

20

“Well Capitalized” minimum ratios are currently 6% for Tier 1, 10% for Total Capital, and 4% for Tier 1 Common (applied to Supervisory Capital Assessment Program tests on top 19 US

banks)

banks)

Excess over “Well Capitalized” grossed up using 39% marginal tax rate

Represents the pre-tax equivalent, excluding the $193 million in regulatory capital received by FMBI through the sale of preferred shares to the US Treasury as part of its Capital Purchase

Plan

Plan

Annualized 2Q09 Pre-Tax, Pre-Provision Operating Income (PTPP) excludes taxes, provision for loan losses, and market related security gains (losses)

Excess Regulatory Capital + Operating

Leverage

Leverage

21

Why First Midwest

22

Why First Midwest

Strong Franchise

Navigating Reality Of Cycle

Proactive Remediation Of Credit

Solid Capital

Leveraging Operating Performance

Strengthening Core Business

Relationship-Based Lending

Core Deposit Expansion

Able To Benefit From Market Disruption

Well Positioned For Recovery