Table of Contents

1701 Market Street | Morgan, Lewis | |

Philadelphia, PA 19103-2921 | & Bockius LLP | |

215.963.5000 | Counselors at Law | |

Fax: 215.963.5001 |

Sean Graber

215.963.5598

sgraber@morganlewis.com

March 18, 2011

FILED AS EDGAR CORRESPONDENCE

Mr. Sonny Oh

U.S. Securities and Exchange Commission

100 F Street, NE

Washington, DC 20549

| Re: | Penn Series Funds, Inc. (File No. 811-03459) |

Dear Mr. Oh:

On behalf of our client, Penn Series Funds, Inc. (the “Company”), we are filing marked for change versions of the Prospectus, Statement of Additional Information and Part C that were included in Post-Effective Amendment No. 65 to the Company’s Registration Statement on Form N-1A filed with the Securities and Exchange Commission on February 23, 2011.

If you have any additional questions or comments, please contact me at 215.963.5598.

Very truly yours,

| /s/ Sean Graber |

| Sean Graber |

Table of Contents

PROSPECTUS — MAY 1, 2011

PENN SERIES FUNDS, INC.

MONEY MARKET FUND

LIMITED MATURITY BOND FUND

QUALITY BOND FUND

HIGH YIELD BOND FUND

FLEXIBLY MANAGED FUND

BALANCED FUND

LARGE GROWTH STOCK FUND

LARGE CAP GROWTH FUND

LARGE CORE GROWTH FUND

LARGE CAP VALUE FUND

LARGE CORE VALUE FUND

INDEX 500 FUND

MID CAP GROWTH FUND

MID CAP VALUE FUND

MID CORE VALUE FUND

SMID CAP GROWTH FUND

SMID CAP VALUE FUND

SMALL CAP GROWTH FUND

SMALL CAP VALUE FUND

SMALL CAP INDEX FUND

DEVELOPED INTERNATIONAL INDEX FUND

INTERNATIONAL EQUITY FUND

EMERGING MARKETS EQUITY FUND

REAL ESTATE SECURITIES FUND

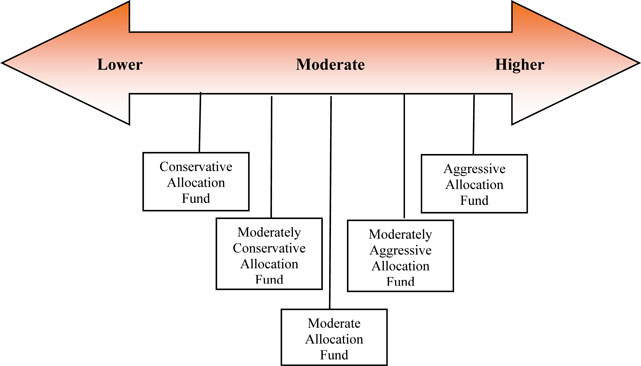

AGGRESSIVE ALLOCATION FUND

MODERATELY AGGRESSIVE ALLOCATION FUND

MODERATE ALLOCATION FUND

MODERATELY CONSERVATIVE ALLOCATION FUND

CONSERVATIVE ALLOCATION FUND

The Securities and Exchange Commission has not approved or disapproved

these securities or passed upon the adequacy of this Prospectus.

Any representation to the contrary is a criminal offense.

Table of Contents

[THIS PAGE INTENTIONALLY LEFT BLANK]

Table of Contents

| PAGE | |||

| 3 | ||||

| 3 | ||||

| 6 | ||||

| 9 | ||||

| 12 | ||||

| 15 | ||||

| 19 | ||||

| 24 | ||||

| 27 | ||||

| 30 | ||||

| 34 | ||||

| 39 | ||||

| 43 | ||||

| 46 | ||||

| 49 | ||||

| 52 | ||||

| 55 | ||||

| 58 | ||||

| 62 | ||||

| 66 | ||||

| 70 | ||||

| 74 | ||||

| 78 | ||||

| 81 | ||||

| 85 | ||||

| 89 | ||||

| 93 | ||||

| 97 | ||||

| 101 | ||||

| 105 | ||||

| ADDITIONAL FUND SUMMARY INFORMATION | ||||

| ADDITIONAL INFORMATION | 110 | |||

| 110 | ||||

More Information About the Investments of and Risks of Investing in the Penn Series Funds | 113 | |||

i

Table of Contents

| 120 | ||||

| 120 | ||||

| 121 | ||||

| 127 | ||||

| 129 | ||||

| 129 | ||||

| 129 | ||||

| 130 | ||||

| 131 | ||||

| 131 | ||||

| 131 | ||||

| 133 | ||||

ii

Table of Contents

FUND SUMMARY:MONEY MARKET FUND

| Investment Objective | The investment objective of the Fund is to preserve shareholder capital, maintain liquidity and achieve the highest possible level of current income consistent therewith. |

Fund Fees and Expenses

This table describes the fees and expenses that you may pay if you buy and hold shares of the Fund. The information in this table and the Example that follows does not reflect charges and fees deducted under your insurance contract. These charges and fees will increase expenses.

Annual Fund Operating Expenses

(expenses that you pay each year as a percentage of the value of your investment)

Investment Advisory Fees | 0.17 | % | ||

Distribution (12b-1) Fees | None | |||

Other Expenses | % | |||

Acquired Fund Fees and Expenses | % | |||

Total Annual Fund Operating Expenses | % | |||

Example

This Example is intended to help you compare the cost of investing in the Fund with the cost of investing in other mutual funds. The Example assumes that you invest $10,000 in the Fund for the time periods indicated and then redeem all of your shares at the end of those periods. The Example also assumes that your investment has a 5% return each year and that the Fund’s operating expenses remain the same. Although your actual costs and returns might be higher or lower, based on these assumptions your costs would be:

| 1 Year | 3 Years | 5 Years | 10 Years | |||

| $ | $ | $ | $ |

Principal Investment Strategy

The Fund will invest in a diversified portfolio of high-quality money market instruments, which are rated within the two highest credit categories assigned by recognized rating organizations or, if not rated, are of comparable investment quality as determined by the Adviser. Investments include commercial paper, U.S. Treasury securities, bank certificates of deposit and repurchase agreements. The Adviser looks for money market instruments that present minimal credit risks. Important factors in selecting investments include a company’s profitability, ability to generate funds, capital adequacy, and liquidity of the investment. The Fund will invest only in securities that mature in 397 days or less, as calculated in accordance with applicable law. The Fund’s policy is to seek to maintain a stable price of $1.00 per share.

Principal Risks of Investing

Investment Risk.Your investment in the Fund is not a bank deposit and is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. Although the Fund seeks to preserve the value of your investment at $1.00 per share, it is possible to lose money by investing in the Fund. Furthermore, there can be no assurance that the Fund’s investment adviser or its affiliates will make capital infusions into the Fund, purchase distressed Fund assets, enter into support agreements with the Fund or take other actions intended to maintain the Fund’s $1.00 share price.

3

Table of Contents

Interest Rate Risk.Interest rates rise and fall over time. As with any investment whose yield reflects current interest rates, the Fund’s yield will change over time. During periods when interest rates are low, the Fund’s yield (and total return) also will be low and the income generated by the Fund may not be sufficient to offset all or a significant portion of the Fund’s expenses, which could impair the Fund’s ability to provide a positive yield and maintain a stable $1.00 share price.

Credit Risk.The Fund could lose money or underperform as a result of default. The credit quality of the Fund’s portfolio holdings can change rapidly in certain markets and any default on the part of a portfolio investment could cause the Fund’s share price or yield to fall.

U.S. Government Securities Risk.Some of the U.S. government securities that the Fund invests in are not backed by the full faith and credit of the United States government, which means they are neither issued nor guaranteed by the U.S. Treasury. Also, any government guarantees on securities the Fund owns do not extend to shares of the Fund.

Repurchase Agreement Risk. The Fund’s use of repurchase agreements involves certain risks. One risk is the seller’s ability to pay the agreed-upon repurchase price on the repurchase date. If the seller defaults, the Fund may incur costs in disposing of the collateral, which would reduce the amount realized thereon.

Redemption Risk.The Fund may experience periods of heavy redemptions that could cause the Fund to liquidate its assets at inopportune times or at a loss or depressed value, particularly during periods of declining or illiquid markets. Redemptions by a few large investors in the Fund may have a significant adverse effect on the Fund’s ability to maintain a stable $1.00 share price. In the event any money market fund fails to maintain a stable net asset value, other money market funds, including the Fund, could face a universal risk of increased redemption pressures, potentially jeopardizing the stability of their $1.00 share prices.

Liquidity Risk. A particular investment may be difficult or expensive to purchase or sell. The Fund may be unable to sell illiquid securities at an advantageous time or price. The market for certain investments may become illiquid due to specific adverse changes in the condition of a particular issuer or under adverse market or economic conditions independent of the issuer. If the Fund is forced to liquidate its assets under unfavorable conditions or at inopportune times, the Fund’s ability to maintain a stable $1.00 share price may be adversely affected.

Performance Information

The bar chart and table below show the performance of the Fund both year-by-year and as an average over different periods of time. The bar chart and table demonstrate the variability of performance over time and provide an indication of the risks and volatility of an investment in the Fund. Past performance does not necessarily indicate how the Fund will perform in the future. This performance information does not include the impact of any charges deducted under your insurance contract. If it did, returns would be lower. The current yield of the Money Market Fund for the seven-day period ended December 31, 2010 was %.

Average Annual Total Return (for Periods Ended December 31, 2010)

| 1 Year | 5 Years | 10 Years | ||||

Money Market Fund | % | % | % |

Investment Adviser

Independence Capital Management, Inc.

4

Table of Contents

Purchase and Sale of Fund Shares, Tax Information and Payments to Broker-Dealers and Other Financial Intermediaries

For important information about the purchase and sale of Fund shares, tax information and payments to broker-dealers and other financial intermediaries, please turn to the “Additional Fund Summary Information” section on pageXX of this prospectus.

5

Table of Contents

FUND SUMMARY: LIMITED MATURITY BOND FUND

| Investment Objective | The investment objective of the Fund is to provide the highest available current income consistent with liquidity and low risk to principal; total return is secondary. |

Fund Fees and Expenses

This table describes the fees and expenses that you may pay if you buy and hold shares of the Fund. The information in this table and the Example that follows does not reflect charges and fees deducted under your insurance contract. These charges and fees will increase expenses.

Annual Fund Operating Expenses

(expenses that you pay each year as a percentage of the value of your investment)

Investment Advisory Fees | 0.30 | % | ||

Distribution (12b-1) Fees | None | |||

Other Expenses | % | |||

Acquired Fund Fees and Expenses | % | |||

Total Annual Fund Operating Expenses | % |

Example

This Example is intended to help you compare the cost of investing in the Fund with the cost of investing in other mutual funds. The Example assumes that you invest $10,000 in the Fund for the time periods indicated and then redeem all of your shares at the end of those periods. The Example also assumes that your investment has a 5% return each year and that the Fund’s operating expenses remain the same. Although your actual costs and returns might be higher or lower, based on these assumptions your costs would be:

| 1 Year | 3 Years | 5 Years | 10 Years | |||

| $ | $ | $ | $ |

Portfolio Turnover

The Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover may indicate higher transaction costs. These costs, which are not reflected in the annual fund operating expenses or in the Example, affect the Fund’s performance. During the most recent fiscal year, the Fund’s portfolio turnover rate was % of the average value of its portfolio.

Principal Investment Strategy

Under normal conditions, the Fund invests at least 80% of its net assets in debt securities, commonly referred to as bonds. This policy may be changed without the vote of shareholders but shareholders will be given 60 days’ advance notice of any change. The Fund will invest primarily in short- to intermediate-term investment grade debt securities (those securities rated BBB or above by S&P or Baa or above by Moody’s (or determined to be of equivalent quality by the Adviser)) of the U.S. government and corporate issuers. In addition, the Fund may invest in convertible securities. The Adviser uses an active bond management approach. It seeks to find securities that are under-valued in the marketplace based on both a relative value analysis of individual securities combined with an analysis of macro-economic factors. With this approach, the Adviser attempts to identify securities that are under-valued based on their quality, maturity, and sector in the marketplace. The Adviser will purchase an individual security when doing so is also consistent with its macro-economic outlook, including its forecast of interest rates and its analysis of the yield curve (a measure of interest rates of securities with the same quality, but different maturities). The Adviser will seek to opportunistically purchase securities to take advantage of inefficiencies of prices in the securities markets. The Adviser will sell a security when it believes that the security has been fully priced. The Adviser seeks to reduce credit risk by diversifying among many issuers and different types of securities.

6

Table of Contents

Duration: The average duration of a fixed income portfolio measures its exposure to the risk of changing interest rates. Typically, with a 1% rise in interest rates, an investment’s value may be expected to fall approximately 1% for each year of its duration. Although the Fund may invest in securities of any duration, under normal circumstances it maintains an average portfolio duration of one to three years.

Quality:The Fund will invest primarily in investment grade debt securities and no more than 10% of its assets in “junk bonds,” which are those rated below BBB by S&P and those rated below Baa by Moody’s (or determined to be of equivalent quality by the Adviser).

Sectors:The Fund will invest primarily in corporate bonds and U.S. government bonds, including mortgage-backed and asset-backed securities.

Turnover: Because the Adviser will look for inefficiencies in the market and sell when it feels a security is fully priced, portfolio turnover can be expected to be relatively high, which may result in increased transaction costs and may lower fund performance.

An investment in the Fund may be appropriate for investors who are seeking the highest current income consistent with liquidity and low risk to principal available through an investment in investment grade debt.

Principal Risks of Investing

Market Risk.Bond markets rise and fall daily. As with any investment whose performance is tied to these markets, the value of your investment in the Fund will fluctuate, which means that you could lose money.

Interest Rate Risk.The risk that the value of fixed income securities, including U.S. Government securities, will fall due to rising interest rates.

Credit Risk.The risk that the issuer of a security, or the counterparty to a contract, will default or otherwise become unable to honor a financial obligation.

High Yield Bond Risk. Investing in fixed income securities rated below investment grade (high yield or junk bonds) involves additional risks, including credit risk. High yield bonds are considered speculative with respect to their issuers’ ability to make timely payments or otherwise honor its obligations.

Prepayment and Extension Risk.Fixed income securities may be paid off earlier or later than expected. Either situation could cause the Fund to hold securities paying lower-than-market rates of interest, which could hurt the Fund’s yield or share price.

U.S. Government Securities Risk.Some of the U.S. government securities that the Fund invests in are not backed by the full faith and credit of the United States government, which means they are neither issued nor guaranteed by the U.S. Treasury. Also, any government guarantees on securities the Fund owns do not extend to shares of the Fund.

Mortgage-Backed Securities Risk. Mortgage-backed securities are affected by, among other things, interest rate changes and the possibility of prepayment of the underlying mortgage loans. Mortgage-backed securities are also subject to the risk that underlying borrowers will be unable to meet their obligations.

Asset-Backed Securities Risk.Payment of principal and interest on asset-backed securities is dependent largely on the cash flows generated by the assets backing the securities and asset-backed securities may not have the benefit of any security interest in the related assets.

Convertible Securities Risk. The value of a convertible security is influenced by changes in interest rates, with investment value declining as interest rates increase and increase as interest rates decline, and the credit standing of the issuer. The price of a convertible security will also normally vary in some proportion to changes in the price of the underlying common stock because of the conversion or exercise feature.

7

Table of Contents

Liquidity Risk. A particular investment may be difficult to purchase or sell. The Fund may be unable to sell illiquid securities at an advantageous time or price.

Performance Information

The bar chart and table below show the performance of the Fund both year-by-year and as an average over different periods of time. The bar chart and table demonstrate the variability of performance over time and provide an indication of the risks and volatility of an investment in the Fund by showing how the Fund’s average annual total returns for various periods compare with those of an index. Past performance does not necessarily indicate how the Fund will perform in the future. This performance information does not include the impact of any charges deducted under your insurance contract. If it did, returns would be lower.

The Citigroup Treasury/Agency 1 to 5 Year Index is an unmanaged index that is a widely recognized benchmark of the market performance of short- to intermediate-term bonds.

Average Annual Total Return (for Periods Ended December 31,2010)

| 1 Year | 5 Years | 10 Years | ||||

Limited Maturity Bond Fund | % | % | % | |||

Comparative Index(reflects no deduction for expenses and taxes) | ||||||

Citigroup Treasury/Agency 1 to 5 Year Index | % | % | % | |||

Investment Adviser

Independence Capital Management, Inc.

Portfolio Manager

Peter M. Sherman, President and Portfolio Manager of Independence Capital Management, Inc., has served as portfolio manager of the Fund since its inception in May 2000.

Purchase and Sale of Fund Shares, Tax Information and Payments to Broker-Dealers and Other Financial Intermediaries

For important information about the purchase and sale of Fund shares, tax information and payments to broker-dealers and other financial intermediaries, please turn to the “Additional Fund Summary Information” section on pageXX of this prospectus.

8

Table of Contents

FUND SUMMARY: QUALITY BOND FUND

| Investment Objective | The Fund seeks the highest income over the long term that is consistent with the preservation of principal. |

Fund Fees and Expenses

This table describes the fees and expenses that you may pay if you buy and hold shares of the Fund. The information in this table and the Example that follows does not reflect charges and fees deducted under your insurance contract. These charges and fees will increase expenses.

Annual Fund Operating Expenses

(expenses that you pay each year as a percentage of the value of your investment)

| Investment Advisory Fees | 0.32 | % | ||

| Distribution (12b-1) Fees | None | |||

| Other Expenses | % | |||

| Acquired Fund Fees and Expenses | % | |||

Total Annual Fund Operating Expenses | % | |||

Example

This Example is intended to help you compare the cost of investing in the Fund with the cost of investing in other mutual funds. The Example assumes that you invest $10,000 in the Fund for the time periods indicated and then redeem all of your shares at the end of those periods. The Example also assumes that your investment has a 5% return each year and that the Fund’s operating expenses remain the same. Although your actual costs and returns might be higher or lower, based on these assumptions your costs would be:

| 1 Year | 3 Years | 5 Years | 10 Years | |||

| $ | $ | $ | $ |

Portfolio Turnover

The Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover may indicate higher transaction costs. These costs, which are not reflected in the annual fund operating expenses or in the Example, affect the Fund’s performance. During the most recent fiscal year, the Fund’s portfolio turnover rate was % of the average value of its portfolio.

Principal Investment Strategy

Under normal conditions, the Fund invests at least 80% of its net assets in debt securities, commonly referred to as bonds. This policy may be changed without the vote of shareholders but shareholders will be given 60 days’ advance notice of any change. The Fund will invest primarily in marketable investment grade debt securities (those securities rated BBB or above by S&P or Baa or above by Moody’s (or determined to be of equivalent quality by the Adviser)). In addition, the Fund may invest in convertible securities. The portfolio manager heads up a team of analysts that uses an active bond-management approach. The Adviser seeks to find securities that are under-valued in the marketplace based on both a relative value analysis of individual securities combined with an analysis of macro-economic factors. With this approach, the Adviser attempts to identify securities that are under-valued based on their quality, maturity, and sector in the marketplace. The Adviser will purchase an individual security when doing so is also consistent with its macro-economic outlook, including its forecast of interest rates and its analysis of the yield curve (a measure of interest rates of securities with the same quality, but different maturities). In addition, the Adviser will seek to opportunistically purchase securities to take advantage of inefficiencies of prices in the securities markets. The Adviser will sell a security when it believes that the security has been fully priced. The Adviser seeks to reduce credit risk by diversifying among many issuers and different types of securities.

9

Table of Contents

Duration: The average duration of a fixed income portfolio measures its exposure to the risk of changing interest rates. Typically, with a 1% rise in interest rates, an investment’s value may be expected to fall approximately 1% for each year of its duration. Duration is set for the portfolio generally between 3.5 and 5.5 years, depending on the interest rate outlook.

Quality: The Fund will invest primarily in investment grade debt securities and no more than 10% of the net assets in “junk bonds,” which are those rated below BBB by S&P and those rated below Baa by Moody’s (or determined to be of equivalent quality by the Adviser).

Sectors: The Fund will invest primarily in the following sectors: corporate bonds, U.S. government bonds, U.S. government agency securities, commercial paper, mortgage-backed securities, collateralized mortgage obligations, and asset-backed securities.

An investment in the Fund may be appropriate for investors who are seeking investment income and preservation of principal.

Principal Risks of Investing

Market Risk.Bond markets rise and fall daily. As with any investment whose performance is tied to these markets, the value of your investment in the Fund will fluctuate, which means that you could lose money.

Interest Rate Risk.The risk that the value of fixed income securities, including U.S. Government securities, will fall due to rising interest rates.

Credit Risk.The risk that the issuer of a security, or the counterparty to a contract, will default or otherwise become unable to honor a financial obligation.

High Yield Bond Risk. Investing in fixed income securities rated below investment grade (high yield or junk bonds) involves additional risks, including credit risk. High yield bonds are considered speculative with respect to their issuers’ ability to make timely payments or otherwise honor its obligations.

Prepayment and Extension Risk.Fixed income securities may be paid off earlier or later than expected. Either situation could cause the Fund to hold securities paying lower-than-market rates of interest, which could hurt the Fund’s yield or share price.

U.S. Government Securities Risk.Some of the U.S. government securities that the Fund invests in are not backed by the full faith and credit of the United States government, which means they are neither issued nor guaranteed by the U.S. Treasury. Also, any government guarantees on securities the Fund owns do not extend to shares of the Fund.

Mortgage-Backed Securities Risk.Mortgage-backed securities are affected by, among other things, interest rate changes and the possibility of prepayment of the underlying mortgage loans. Mortgage-backed securities are also subject to the risk that underlying borrowers will be unable to meet their obligations.

Asset-Backed Securities Risk.Payment of principal and interest on asset-backed securities is dependent largely on the cash flows generated by the assets backing the securities and asset-backed securities may not have the benefit of any security interest in the related assets.

Convertible Securities Risk. The value of a convertible security is influenced by changes in interest rates (with investment value declining as interest rates increase and increase as interest rates decline) and the credit standing of the issuer. The price of a convertible security will also normally vary in some proportion to changes in the price of the underlying common stock because of the conversion or exercise feature.

Liquidity Risk. A particular investment may be difficult to purchase or sell. The Fund may be unable to sell illiquid securities at an advantageous time or price.

10

Table of Contents

Performance Information

The bar chart and table below show the performance of the Fund both year-by-year and as an average over different periods of time. The bar chart and table demonstrate the variability of performance over time and provide an indication of the risks and volatility of an investment in the Fund by showing how the Fund’s average annual total returns for various periods compare with those of an index. Past performance does not necessarily indicate how the Fund will perform in the future. This performance information does not include the impact of any charges deducted under your insurance contract. If it did, returns would be lower.

The Barclays U.S. Aggregate Bond Index measures the performance of the U.S. investment grade bond market.

Average Annual Total Return (for Periods Ended December 31,2010)

| 1 Year | 5 Years | 10 Years | ||||

Quality Bond Fund | % | % | % | |||

ComparativeIndex (reflects no deduction for expenses and taxes) | ||||||

Barclays U.S. Aggregate Bond Index | % | % | % | |||

Investment Adviser

Independence Capital Management, Inc.

Portfolio Manager

Peter M. Sherman, President and Portfolio Manager of Independence Capital Management, Inc., has served as portfolio manager of the Fund since November 1992.

Purchase and Sale of Fund Shares, Tax Information and Payments to Broker-Dealers and Other Financial Intermediaries

For important information about the purchase and sale of Fund shares, tax information and payments to broker-dealers and other financial intermediaries, please turn to the “Additional Fund Summary Information” section on pageXX of this prospectus.

11

Table of Contents

FUND SUMMARY: HIGH YIELD BOND FUND

| Investment Objective | The investment objective of the Fund is to realize high current income. |

Fund Fees and Expenses

This table describes the fees and expenses that you may pay if you buy and hold shares of the Fund. The information in this table and the Example that follows does not reflect charges and fees deducted under your insurance contract. These charges and fees will increase expenses.

Annual Fund Operating Expenses

(expenses that you pay each year as a percentage of the value of your investment)

Investment Advisory Fees | 0.50 | % | ||

Distribution (12b-1) Fees | None | |||

Other Expenses | % | |||

Total Annual Fund Operating Expenses | % |

Example

This Example is intended to help you compare the cost of investing in the Fund with the cost of investing in other mutual funds. The Example assumes that you invest $10,000 in the Fund for the time periods indicated and then redeem all of your shares at the end of those periods. The Example also assumes that your investment has a 5% return each year and that the Fund’s operating expenses remain the same. Although your actual costs and returns might be higher or lower, based on these assumptions your costs would be:

| 1 Year | 3 Years | 5 Years | 10 Years | |||

| $ | $ | $ | $ |

Portfolio Turnover

The Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover may indicate higher transaction costs. These costs, which are not reflected in the annual fund operating expenses or in the Example, affect the Fund’s performance. During the most recent fiscal year, the Fund’s portfolio turnover rate was % of the average value of its portfolio.

Principal Investment Strategy

Under normal conditions, the Fund invests at least 80% of its net assets in a widely diversified portfolio of high yield corporate bonds, often called “junk bonds,” income-producing convertible securities and preferred stocks. This policy may be changed without the vote of shareholders but shareholders will be given 60 days’ advance notice of any change. High yield bonds are rated below investment grade (BB and lower by S&P and Ba and lower by Moody’s or determined to be of equivalent quality by the Sub-Adviser) and generally provide high income in an effort to compensate investors for their higher risk of default, that is the failure to make required interest or principal payments. High yield bond issuers include U.S. and foreign issuers, small or relatively new companies lacking the history or capital to merit investment-grade status, former blue-chip companies downgraded because of financial problems, companies electing to borrow heavily to finance or avoid a takeover or buyout, and firms with heavy debt loads. The Fund’s dollar-weighted average maturity generally is expected to be in the six- to twelve-year range. In selecting investments for the Fund, the Sub-Adviser relies extensively on its research analysts. When the Sub-Adviser’s outlook for the economy is positive, it may purchase slightly lower rated bonds in an effort to secure additional income and appreciation potential. When the Sub-Adviser’s outlook for the economy is less positive, the Fund may gravitate toward higher rated junk bonds. The Fund may also invest in other securities, including futures and options, as well as loan assignments and participations, in keeping with its objective. In pursuing the investment objective, the Sub-Adviser has the discretion to purchase some securities that do not meet its

12

Table of Contents

normal investment criteria, as described above, when it perceives an unusual opportunity for gain. These special situations might arise when the Sub-Adviser believes a security could increase in value for a variety of reasons, including a change in management, an extraordinary corporate event, or a temporary imbalance in the supply of or demand for the securities. The Fund may sell holdings for a variety of reasons, such as to adjust a portfolio’s average maturity or quality, or to shift assets into higher yielding securities or to reduce marginal quality securities.

An investment in the Fund may be appropriate for long-term, risk-oriented investors who are willing to accept the greater risks and uncertainties of investing in high yield bonds in the hope of earning high current income.

Principal Risks of Investing

Market Risk.Bond markets rise and fall daily. As with any investment whose performance is tied to these markets, the value of your investment in the Fund will fluctuate, which means that you could lose money.

Interest Rate Risk.The risk that the value of fixed income securities, including U.S. Government securities, will fall due to rising interest rates.

Credit Risk.The risk that the issuer of a security, or the counterparty to a contract, will default or otherwise become unable to honor a financial obligation.

High Yield Bond Risk. Investing in fixed income securities rated below investment grade (high yield or junk bonds) involves additional risks, including credit risk. High yield bonds are considered speculative with respect to their issuers’ ability to make timely payments or otherwise honor its obligations.

Prepayment and Extension Risk.Fixed income securities may be paid off earlier or later than expected. Either situation could cause the Fund to hold securities paying lower-than-market rates of interest, which could hurt the Fund’s yield or share price.

Foreign Investment Risk. The Fund’s investments in securities of foreign issuers may involve certain risks that are greater than those associated with investments in securities of U.S. issuers. These include risks of adverse changes in foreign economic, political, regulatory and other conditions; changes in currency exchange rates or exchange control regulations (including limitations on currency movements and exchanges); differing accounting, auditing, financial reporting and legal standards and practices; differing securities market structures; and higher transaction costs.

Currency Risk. As a result of the Fund’s investments in securities denominated in, and/or receiving revenues in, foreign currencies, the Fund will be subject to currency risk. This is the risk that those currencies will decline in value relative to the U.S. dollar, or, in the case of hedging positions, that the U.S. dollar will decline in value relative to the currency hedged. In either event, the dollar value of an investment in the Fund would be adversely affected.

Preferred Stock Risk. Preferred stocks are sensitive to interest rate changes, and are also subject to equity market risk, which is the risk that stock prices will fluctuate and can decline and reduce the value of the Fund’s investment. The rights of preferred stocks on the distribution of a corporation’s assets in the event of a liquidation are generally subordinate to the rights associated with a corporation’s debt securities.

Derivatives Risk. The Fund may use derivatives (including futures and options) to gain market exposure and potentially to enhance returns. The Fund’s use of derivative instruments involves risks different from, or possibly greater than, the risks associated with investing directly in securities and other traditional investments and could cause the Fund to lose more than the principal amount invested. The Fund’s use of derivative instruments also involves credit risk and liquidity risk.

Liquidity Risk. A particular investment may be difficult to purchase or sell. The Fund may be unable to sell illiquid securities at an advantageous time or price.

13

Table of Contents

Performance Information

The bar chart and table below show the performance of the Fund both year-by-year and as an average over different periods of time. The bar chart and table demonstrate the variability of performance over time and provide an indication of the risks and volatility of an investment in the Fund by showing how the Fund’s average annual total returns for various periods compare with those of an index. Past performance does not necessarily indicate how the Fund will perform in the future. This performance information does not include the impact of any charges deducted under your insurance contract. If it did, returns would be lower.

The CS First Boston Global High Yield Index is a widely recognized benchmark of high yield bond performance.

Average Annual Total Return (for Periods Ended December 31,2010)

| 1 Year | 5 Years | 10 Years | ||||

High Yield Bond Fund | % | % | % | |||

| Comparative Index(reflects no deduction for expenses and taxes) | ||||||

CS First Boston Global High Yield Index | % | % | % | |||

Investment Adviser

Independence Capital Management, Inc.

Investment Sub-Adviser

T. Rowe Price Associates, Inc.

Portfolio Manager

Mark J. Vaselkiv, a Vice President of T. Rowe Price Associates, Inc., has served as portfolio manager of the Fund since November 1996.

Purchase and Sale of Fund Shares, Tax Information and Payments to Broker-Dealers and Other Financial Intermediaries

For important information about the purchase and sale of Fund shares, tax information and payments to broker-dealers and other financial intermediaries, please turn to the “Additional Fund Summary Information” section on pageXX of this prospectus.

14

Table of Contents

FUND SUMMARY: FLEXIBLY MANAGED FUND

Investment Objective | The investment objective of the Fund is to maximize total return (capital appreciation and income). |

Fund Fees and Expenses

This table describes the fees and expenses that you may pay if you buy and hold shares of the Fund. The information in this table and the Example that follows does not reflect charges and fees deducted under your insurance contract. These charges and fees will increase expenses.

Annual Fund Operating Expenses

(expenses that you pay each year as a percentage of the value of your investment)

Investment Advisory Fees | 0.60% | |||

Distribution (12b-1) Fees | None | |||

Other Expenses | % | |||

Total Annual Fund Operating Expenses | % |

Example

This Example is intended to help you compare the cost of investing in the Fund with the cost of investing in other mutual funds. The Example assumes that you invest $10,000 in the Fund for the time periods indicated and then redeem all of your shares at the end of those periods. The Example also assumes that your investment has a 5% return each year and that the Fund’s operating expenses remain the same. Although your actual costs and returns might be higher or lower, based on these assumptions your costs would be:

| 1 Year | 3 Years | 5 Years | 10 Years | |||

| $ | $ | $ | $ |

Portfolio Turnover

The Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover may indicate higher transaction costs. These costs, which are not reflected in the annual fund operating expenses or in the Example, affect the Fund’s performance. During the most recent fiscal year, the Fund’s portfolio turnover rate was % of the average value of its portfolio.

Principal Investment Strategy

The Fund invests primarily in common stocks of established U.S. companies that it believes have above-average potential for capital growth. Common stocks typically constitute at least half of total assets. The remaining assets are generally invested in other securities, including convertibles, warrants, preferred stocks, corporate and government debt securities, including high yield securities (junk bonds), foreign securities, futures and options, in keeping with the Fund’s objective. The Fund’s investments in common stocks generally fall into one of two categories. The larger category comprises long-term core holdings that the Sub-Adviser considers to be underpriced in terms of company assets, earnings, or other factors at the time they are purchased. The smaller category comprises opportunistic investments whose prices the Sub-Adviser expects to rise in the short term, but not necessarily over the long term. Since the Sub-Adviser attempts to prevent losses as well as achieve gains, it typically uses a “value approach” in selecting investments. Its in-house research team seeks to identify companies that seem under-valued by various measures, such as price/book value, and may be temporarily out of favor but have good prospects for capital appreciation. The Sub-Adviser may establish relatively large positions in companies it finds particularly attractive.

15

Table of Contents

The Fund’s approach differs from that of many other stock funds. The Sub-Adviser works as hard to reduce risk as to maximize gains and may realize gains rather than lose them in market declines. In addition, the Sub-Adviser searches for the best risk/reward values among all types of securities. The portion of the Fund invested in a particular type of security, such as common stocks, results largely from case-by-case investment decisions, and the size of the Fund’s cash reserve may reflect the Sub-Adviser’s ability to find companies that meet valuation criteria rather than its market outlook. Bonds and convertible securities may be purchased to gain additional exposure to a company or for their income or other features; maturity and quality are not necessarily major considerations. There is no limit on the Fund’s investments in convertible securities. In pursuing the investment objective, the Sub-Adviser has the discretion to purchase some securities that do not meet its normal investment criteria, as described above, when it perceives an unusual opportunity for gain. These special situations might arise when the Sub-Adviser believes a security could increase in value for a variety of reasons including a change in management, an extraordinary corporate event, or a temporary imbalance in the supply of or demand for the securities. The Fund may sell securities for a variety of reasons, such as to secure gains, limit losses, or redeploy assets into more promising opportunities.

An investment in the Fund may be appropriate for investors who are seeking a relatively conservative approach to investing for total return and are willing to accept the risks and uncertainties of investing in common stocks and bonds.

Principal Risks of Investing

Market Risk. Equity and bond markets rise and fall daily. As with any investment whose performance is tied to these markets, the value of your investment in the Fund will fluctuate, which means that you could lose money.

Equity Risk. The prices of equity securities rise and fall daily. These price movements may result from factors affecting individual companies, industries or the securities market as a whole. In addition, equity markets tend to move in cycles which may cause stock prices to fall over short or extended periods of time.

Large-Cap Risk. Large-cap stocks tend to go in and out of favor based on market and economic conditions. During a period when large-cap stocks fall behind other types of investments — small-cap stocks, for instance — the Fund’s performance could be reduced to the extent its portfolio is holding large-cap stocks.

“Value” Investing Risk.Because of its “value” style of investing, the Fund could suffer losses or produce poor results relative to other funds, even in a rising market, if the Sub-Adviser’s assessment of a company’s value or prospects for exceeding earnings expectations or market conditions is wrong.

Foreign Investment Risk. The Fund’s investments in securities of foreign issuers may involve certain risks that are greater than those associated with investments in securities of U.S. issuers. These include risks of adverse changes in foreign economic, political, regulatory and other conditions; changes in currency exchange rates or exchange control regulations (including limitations on currency movements and exchanges); differing accounting, auditing, financial reporting and legal standards and practices; differing securities market structures; and higher transaction costs.

Currency Risk. As a result of the Fund’s investments in securities denominated in, and/or receiving revenues in, foreign currencies, the Fund will be subject to currency risk. This is the risk that those currencies will decline in value relative to the U.S. dollar, or, in the case of hedging positions, that the U.S. dollar will decline in value relative to the currency hedged. In either event, the dollar value of an investment in the Fund would be adversely affected.

Interest Rate Risk.The risk that the value of fixed income securities, including U.S. Government securities, will fall due to rising interest rates.

Credit Risk.The risk that the issuer of a security, or the counterparty to a contract, will default or otherwise become unable to honor a financial obligation.

High Yield Bond Risk. Investing in fixed income securities rated below investment grade (high yield or junk bonds) involves additional risks, including credit risk. High yield bonds are considered speculative with respect to their issuers’ ability to make timely payments or otherwise honor its obligations.

16

Table of Contents

Prepayment and Extension Risk.Fixed income securities may be paid off earlier or later than expected. Either situation could cause the Fund to hold securities paying lower-than-market rates of interest, which could hurt the Fund’s yield or share price.

Derivatives Risk. The Fund may use derivatives (including futures and options) to gain market exposure and potentially to enhance returns. The Fund’s use of derivative instruments involves risks different from, or possibly greater than, the risks associated with investing directly in securities and other traditional investments and could cause the Fund to lose more than the principal amount invested. The Fund’s use of derivative instruments also involves credit risk and liquidity risk.

Warrant Risk. Changes in the value of a warrant do not necessarily correspond to changes in the value of its underlying security. The price of a warrant may be more volatile than the price of its underlying security, and a warrant may offer greater potential for capital appreciation as well as capital loss.

Convertible Securities Risk. The value of a convertible security is influenced by changes in interest rates (with investment value declining as interest rates increase and increase as interest rates decline) and the credit standing of the issuer. The price of a convertible security will also normally vary in some proportion to changes in the price of the underlying common stock because of the conversion or exercise feature.

Preferred Stock Risk. Preferred stocks are sensitive to interest rate changes, and are also subject to equity market risk, which is the risk that stock prices will fluctuate and can decline and reduce the value of the Fund’s investment. The rights of preferred stocks on the distribution of a corporation’s assets in the event of a liquidation are generally subordinate to the rights associated with a corporation’s debt securities.

Investment Style Risk. If the Fund has large holdings in a relatively small number of companies, disappointing performance by those companies will have a more adverse impact on the Fund than would be the case with a more diversified fund. A sizable cash or fixed income position may hinder the Fund from participating fully in a strong, rapidly rising bull market.

Liquidity Risk. A particular investment may be difficult to purchase or sell. The Fund may be unable to sell illiquid securities at an advantageous time or price.

Performance Information

The bar chart and table below show the performance of the Fund both year-by-year and as an average over different periods of time. The bar chart and table demonstrate the variability of performance over time and provide an indication of the risks and volatility of an investment in the Fund by showing how the Fund’s average annual total returns for various periods compare with those of an index. Past performance does not necessarily indicate how the Fund will perform in the future. This performance information does not include the impact of any charges deducted under your insurance contract. If it did, returns would be lower.

The S&P 500 Index is an unmanaged capitalization-weighted index of 500 stocks representing all major industries and is a widely recognized benchmark of general stock market performance.

Average Annual Total Return (for Periods Ended December 31,2010)

| 1 Year | 5 Years | 10 Years | ||||

Flexibly Managed Fund | % | % | % | |||

| Comparative Index(reflects no deduction for expenses and taxes) | ||||||

S&P 500 Index | % | % | % | |||

17

Table of Contents

Investment Adviser

Independence Capital Management, Inc.

Investment Sub-Adviser

T. Rowe Price Associates, Inc.

Portfolio Manager

David Giroux, a Vice President of T. Rowe Price Associates, Inc., has served as portfolio manager of the Fund since July 2006.

Purchase and Sale of Fund Shares, Tax Information and Payments to Broker-Dealers and Other Financial Intermediaries

For important information about the purchase and sale of Fund shares, tax information and payments to broker-dealers and other financial intermediaries, please turn to the “Additional Fund Summary Information” section on pageXX of this prospectus.

18

Table of Contents

Investment Objective | The investment objective of the Fund is to seek long-term growth and current income. |

Fund Fees and Expenses

This table describes the fees and expenses that you may pay if you buy and hold shares of the Fund. The information in this table and the Example that follows does not reflect charges and fees deducted under your insurance contract. These charges and fees will increase expenses.

Annual Fund Operating Expenses

(expenses that you pay each year as a percentage of the value of your investment)

Investment Advisory Fees | 0.00 | % | ||

Distribution (12b-1) Fees | None | |||

Other Expenses | % | |||

Acquired Fund Fees and Expenses | % | |||

Total Annual Fund Operating Expenses | % |

Example

This Example is intended to help you compare the cost of investing in the Fund with the cost of investing in other mutual funds. The Example assumes that you invest $10,000 in the Fund for the time periods indicated and then redeem all of your shares at the end of those periods. The Example also assumes that your investment has a 5% return each year and that the Fund’s operating expenses remain the same. Although your actual costs and returns might be higher or lower, based on these assumptions your costs would be:

| 1 Year | 3 Years | 5 Years | 10 Years | |||

| $ | $ | $ | $ |

Portfolio Turnover

The Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover may indicate higher transaction costs. These costs, which are not reflected in the annual fund operating expenses or in the Example, affect the Fund’s performance. During the most recent fiscal year, the Fund’s portfolio turnover rate was % of the average value of its portfolio.

Principal Investment Strategy

The Fund seeks to achieve its investment objective by using a “fund-of-funds” strategy. Accordingly, the Fund invests in a combination of other Penn Series Funds (each, an “underlying fund” and, together, the “underlying funds”) in accordance with its target asset allocation. These underlying funds invest their assets directly in equity, fixed income, money market and other securities in accordance with their own investment objectives and policies. The underlying funds are managed using both indexed and active management strategies. The Fund intends to invest primarily in a combination of underlying funds; however, the Fund may invest directly in equity and fixed income securities and cash equivalents, including money market securities.

19

Table of Contents

Under normal circumstances, the Fund will invest 50% -70% of its assets in stock and other equity underlying funds, 30%-50% of its assets in bond and other fixed income funds, and 0%-20% of its assets in money market funds. The Fund’s allocation strategy is designed to provide a mix of the growth opportunities of stock investing with the income opportunities of bonds and other fixed income securities.

The Fund’s underlying equity fund allocation will primarily track the performance of the large capitalization company portion of the U.S. stock market. The Fund’s underlying fixed income fund allocation will be invested primarily in a broad range of investment grade fixed income securities (although up to 10% of the underlying fund may be invested in non-investment grade securities (“junk bonds”)), and is intended to provide results consistent with the broad US fixed income market.

The following chart shows the Fund’s target asset allocation among the various asset classes. The Adviser may permit modest deviations from the target asset allocations listed below. Market appreciation or depreciation may cause the Fund to be outside of its target asset allocation range. In addition, differences in the performance of the underlying funds and the size and frequency of purchase and redemption orders may affect the Fund’s actual allocations. Accordingly, the Fund’s actual allocations may differ from this illustration.

| Asset Classes and Underlying Funds | Target Asset Allocation | |

Equity Fund - Penn Series Index 500 Fund | 50% - 70% | |

Fixed Income Fund -Penn Series Quality Bond Fund | 30% - 50% | |

Money Market Fund -Penn Series Money Market Fund | 0% - 20% | |

The Fund’s investment performance is directly related to the investment performance of the underlying funds. The underlying funds invest their assets directly in equity, fixed income, money market and other securities in accordance with their own investment objectives and policies. A brief description of each underlying fund’s principal investment strategy is provided below.

Underlying Funds | Investment Objective and Principal Investment Strategy | |

Penn Series Index 500 Fund | Seeks a total return (capital appreciation and income) which corresponds to that of the S&P 500 Index. Under normal circumstances, the Fund intends to invest substantially all of its assets in securities of companies included in the Index and close substitutes (such as index futures contracts) that are designed to track the S&P 500 Index. | |

Penn Series Quality Bond Fund | Seeks the highest income over the long term that is consistent with the preservation of principal. The Fund invests at least 80% of its net assets in debt securities. The Fund will invest primarily in investment grade debt securities and no more than 10% of the net assets in “junk bonds.” | |

Penn Series Money Market Fund | To preserve shareholder capital, maintain liquidity and achieve the highest possible level of current income consistent therewith. The Fund invests in a diversified portfolio of high-quality money market instruments. The Fund seeks to maintain a stable price of $1.00 per share. | |

An investment in the Fund may be appropriate for investors who are willing to accept the risks and uncertainties of investing in a fund which allocates its assets among various asset classes and market segments in the hope of achieving long-term growth and current income.

20

Table of Contents

Principal Risks of Investing

Asset Allocation Risk. The Fund’s particular asset allocation can have a significant effect on performance. The Fund manages its allocation with long-term performance in mind, and does not seek any particular type of performance in the short-term. Because the risks and returns of different asset classes can vary widely over any given time period, the Fund’s performance could suffer if a particular asset class does not perform as expected.

Market Risk. Equity and bond markets rise and fall daily. As with any investment whose performance is tied to these markets, the value of your investment in the Fund will fluctuate, which means that you could lose money.

Underlying Fund Investment Risk.The Fund purchases shares of the underlying funds. When the Fund invests in an underlying fund, in addition to directly bearing the expenses associated with its own operations, it will bear a pro rata portion of the underlying fund’s expenses. The value of your investment in the Fund is based primarily on the prices of the underlying funds that the Fund purchases. In turn, the price of each underlying fund is based on the value of its securities. Before investing in the Fund, investors should assess the risks associated with the underlying funds in which the Fund may invest and the types of investments made by those underlying funds. These risks include any combination of the risks described below, although the Fund’s exposure to a particular risk will be proportionate to the Fund’s overall asset allocation and underlying fund allocation.

Investment Risk. An investment in an underlying fund is not a bank deposit and is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. The Fund may experience losses with respect to its investment in an underlying fund. Further, there is no guarantee that an underlying fund will be able to achieve its objective.

Equity Risk. The prices of equity securities rise and fall daily. These price movements may result from factors affecting individual companies, industries or the securities market as a whole. In addition, equity markets tend to move in cycles which may cause stock prices to fall over short or extended periods of time.

Large-Cap Risk. Large-cap stocks tend to go in and out of favor based on market and economic conditions. During a period when large-cap stocks fall behind other types of investments — small-cap stocks, for instance — an underlying fund’s performance could be reduced to the extent its portfolio is holding large-cap stocks.

Tracking Error Risk. As an index fund, the Penn Series Index 500 Fund seeks to track the performance of its benchmark index, although it may not be successful in doing so. The divergence between the performance of a fund and its benchmark index, positive or negative, is called “tracking error.” Tracking error can be caused by many factors and it may be significant.

Sampling Risk.The Penn Series Index 500 Fund may not fully replicate S&P 500 Index and may hold securities not included in the index. As a result, the Penn Series Index 500 Fund is subject to the risk that the Sub-Adviser’s investment strategy, the implementation of which is subject to a number of constraints, may not produce the intended results. Because the Penn Series Index 500 Fund may utilize a sampling approach, it may not track the return of the index as well as it would if the Fund purchased all of the securities in the benchmark index.

Interest Rate Risk.The risk that the value of fixed income securities, including U.S. Government securities, will fall due to rising interest rates.

Credit Risk.The risk that the issuer of a security, or the counterparty to a contract, will default or otherwise become unable to honor a financial obligation.

High Yield Bond Risk. Investing in fixed income securities rated below investment grade (high yield or junk bonds) involves additional risks, including credit risk. High yield bonds are considered speculative with respect to their issuers’ ability to make timely payments or otherwise honor its obligations.

21

Table of Contents

Concentration Risk. To the extent the Penn Series Index 500 Fund concentrates its investments in issuers doing business in the same industry, the Fund will increase its investment exposure to the risks of that industry and will be subject to greater volatility.

Prepayment and Extension Risk.Fixed income securities may be paid off earlier or later than expected. Either situation could cause an underlying fund to hold securities paying lower-than-market rates of interest, which could hurt the fund’s yield or share price.

U.S. Government Securities Risk.Some of the U.S. government securities that the underlying funds invest in are not backed by the full faith and credit of the United States government, which means they are neither issued nor guaranteed by the U.S. Treasury. Also, any government guarantees on securities an underlying fund owns do not extend to shares of the fund.

Mortgage-Backed Securities Risk.Mortgage-backed securities are affected by, among other things, interest rate changes and the possibility of prepayment of the underlying mortgage loans. Mortgage-backed securities are also subject to the risk that underlying borrowers will be unable to meet their obligations.

Asset-Backed Securities Risk.Payment of principal and interest on asset-backed securities is dependent largely on the cash flows generated by the assets backing the securities and asset-backed securities may not have the benefit of any security interest in the related assets.

Convertible Securities Risk.The value of a convertible security is influenced by changes in interest rates (with investment value declining as interest rates increase and increase as interest rates decline) and the credit standing of the issuer. The price of a convertible security will also normally vary in some proportion to changes in the price of the underlying common stock because of the conversion or exercise feature.

Derivatives Risk. An underlying fund’s use of derivative instruments involves risks different from, or possibly greater than, the risks associated with investing directly in securities and other traditional investments and could cause the underlying fund to lose more than the principal amount invested. An underlying fund’s use of derivative instruments also involves credit risk and liquidity risk.

Liquidity Risk. A particular investment may be difficult to purchase or sell. An underlying fund may be unable to sell illiquid securities at an advantageous time or price.

Direct Investment Risk. The Fund may invest a portion of its assets directly in equity and fixed income securities and cash equivalents, including money market securities. The Fund’s direct investment in these securities is subject to the same or similar risks as those described for an underlying fund’s investment in the same security, and such risks are summarized above.

Performance Information

The bar chart and table below show the performance of the Fund both year-by-year and as an average over different periods of time. The bar chart and table demonstrate the variability of performance over time and provide an indication of the risks and volatility of an investment in the Fund by showing how the Fund’s average annual total returns for various periods compare with those of an index. Past performance does not necessarily indicate how the Fund will perform in the future. This performance information does not include the impact of any charges deducted under your insurance contract. If it did, returns would be lower.

22

Table of Contents

The S&P 500 Index is an unmanaged capitalization-weighted index of 500 stocks representing all major industries and is a widely recognized benchmark of general stock market performance.

Average Annual Total Return (for Periods Ended December 31,2010)

| 1 Year | Since Inception on August 25, 2008 | |||||

Balanced Fund | % | % | ||||

Comparative Index(reflects no deduction for expenses and taxes) | ||||||

S&P 500 Index | % | % | ||||

Investment Adviser

Independence Capital Management, Inc.

Portfolio Managers

Peter M. Sherman, President and Portfolio Manager of Independence Capital Management, Inc., has served as co-portfolio manager of the Fund since its inception.

Keith G. Huckerby, Vice President of Independence Capital Management, Inc., has served as co-portfolio manager of the Fund since its inception.

Purchase and Sale of Fund Shares, Tax Information and Payments to Broker-Dealers and Other Financial Intermediaries

For important information about the purchase and sale of Fund shares, tax information and payments to broker-dealers and other financial intermediaries, please turn to the “Additional Fund Summary Information” section on pageXX of this prospectus.

23

Table of Contents

FUND SUMMARY: LARGE GROWTH STOCK FUND

| Investment Objective | The investment objective of the Fund is to achieve long-term growth of capital and increase of future income. |

Fund Fees and Expenses

This table describes the fees and expenses that you may pay if you buy and hold shares of the Fund. The information in this table and the Example that follows does not reflect charges and fees deducted under your insurance contract. These charges and fees will increase expenses.

Annual Fund Operating Expenses

(expenses that you pay each year as a percentage of the value of your investment)

Investment Advisory Fees | 0.64 | % | ||

Distribution (12b-1) Fees | None | |||

Other Expenses | % | |||

Total Annual Fund Operating Expenses | % |

Example

This Example is intended to help you compare the cost of investing in the Fund with the cost of investing in other mutual funds. The Example assumes that you invest $10,000 in the Fund for the time periods indicated and then redeem all of your shares at the end of those periods. The Example also assumes that your investment has a 5% return each year and that the Fund’s operating expenses remain the same. Although your actual costs and returns might be higher or lower, based on these assumptions your costs would be:

| 1 Year | 3 Years | 5 Years | 10 Years | |||

| $ | $ | $ | $ |

Portfolio Turnover

The Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover may indicate higher transaction costs. These costs, which are not reflected in the annual fund operating expenses or in the Example, affect the Fund’s performance. During the most recent fiscal year, the Fund’s portfolio turnover rate was % of the average value of its portfolio.

Principal Investment Strategy

Under normal market conditions, the Fund invests at least 80% of its net assets in common stocks of large capitalization companies. This policy may be changed without the vote of shareholders but shareholders will be given 60 days’ advance notice of any change. For purposes of this policy, large capitalization companies have market capitalizations that fall within the market capitalization range of companies in the Russell 1000 Growth Index at the time of purchase (as of March 31, 2011, this range was between $ million and $ billion). Because the Fund’s definition of large capitalization companies is dynamic, the lower and upper limits on market capitalization will change with the markets. The Fund will invest primarily in common stocks of well established companies that the Sub-Adviser believes have long-term growth potential. In selecting the Fund’s investments, the Sub-Adviser seeks investments in companies that have the ability to pay increasing dividends through strong cash flow. The Sub-Adviser’s approach looks for companies with an above-average rate of earnings growth and a lucrative niche in the economy that gives them the ability to sustain earnings momentum even during times of slow economic growth. The Sub-Adviser believes that when a company increases its earnings faster than both inflation and the overall economy, the market will eventually reward it with a higher stock price. The Fund may sell securities for a variety of reasons, such as to secure gains, limit losses, or redeploy assets into more promising opportunities.

24

Table of Contents

In pursuing its investment objective, the Sub-Adviser has the discretion to purchase some securities that do not meet its normal investment criteria, as described above, when it perceives an unusual opportunity for gain. Those special situations might arise when the Sub-Adviser believes a security could increase in value for a variety of reasons, including a change in management, an extraordinary corporate event, or a temporary imbalance in the supply of or demand for the securities.

While most assets will be invested in U.S. common stocks, other securities may also be purchased, including foreign stocks (up to 30% of total assets), futures, and options, in keeping with Fund objectives.

An investment in the Fund may be appropriate for investors who are willing to accept the risks and uncertainties of investing in common stocks in the hope of earning above-average long-term growth of capital and income.

Principal Risks of Investing

Market Risk. Equity markets rise and fall daily. As with any investment whose performance is tied to these markets, the value of your investment in the Fund will fluctuate, which means that you could lose money.

Equity Risk. The prices of equity securities rise and fall daily. These price movements may result from factors affecting individual companies, industries or the securities market as a whole. In addition, equity markets tend to move in cycles which may cause stock prices to fall over short or extended periods of time.

Large-Cap Risk. Large-cap stocks tend to go in and out of favor based on market and economic conditions. During a period when large-cap stocks fall behind other types of investments — small-cap stocks, for instance — the Fund’s performance could be reduced.

“Growth” Investing Risk. Growth stocks can be volatile for several reasons. The prices of growth stocks are based largely on projections of the issuer’s future earnings and revenues. If a company’s earnings or revenues fall short of expectations, its stock price may fall dramatically. Growth stocks may be more expensive relative to their earnings or assets compared to value or other stocks.

Foreign Investment Risk. The Fund’s investments in securities of foreign issuers may involve certain risks that are greater than those associated with investments in securities of U.S. issuers. These include risks of adverse changes in foreign economic, political, regulatory and other conditions; changes in currency exchange rates or exchange control regulations (including limitations on currency movements and exchanges); differing accounting, auditing, financial reporting and legal standards and practices; differing securities market structures; and higher transaction costs.

Currency Risk. As a result of the Fund’s investments in securities denominated in, and/or receiving revenues in, foreign currencies, the Fund will be subject to currency risk. This is the risk that those currencies will decline in value relative to the U.S. dollar, or, in the case of hedging positions, that the U.S. dollar will decline in value relative to the currency hedged. In either event, the dollar value of an investment in the Fund would be adversely affected.

Derivatives Risk. The Fund may use derivatives (including futures and options) to gain market exposure and potentially to enhance returns. The Fund’s use of derivative instruments involves risks different from, or possibly greater than, the risks associated with investing directly in securities and other traditional investments and could cause the Fund to lose more than the principal amount invested. The Fund’s use of derivative instruments also involves credit risk and liquidity risk.

Liquidity Risk. A particular investment may be difficult to purchase or sell. The Fund may be unable to sell illiquid securities at an advantageous time or price.

Performance Information

The bar chart and table below show the performance of the Fund both year-by-year and as an average over different periods of time. The information presented prior to August 1, 2004, represents the performance of Independence Capital Management, Inc., the Fund’s current investment adviser. Since August 1, 2004, T. Rowe Price Associates,

25

Table of Contents

Inc. has been responsible for the Fund’s day-to-day portfolio management. The bar chart and table demonstrate the variability of performance over time and provide an indication of the risks and volatility of an investment in the Fund by showing how the Fund’s average annual total returns for various periods compare with those of an index. Past performance does not necessarily indicate how the Fund will perform in the future. This performance information does not include the impact of any charges deducted under your insurance contract. If it did, returns would be lower.

The Russell 1000 Growth Index is a widely-recognized, capitalization-weighted index constructed to measure the performance of the large cap growth segment of the U.S. equity market.

Average Annual Total Return (for Periods Ended December 31, 2010)

| 1 Year | 5 Years | 10 Years | ||||

Large Growth Stock Fund | % | % | % | |||

| Comparative Index(reflects no deduction for expenses and taxes) | ||||||

Russell 1000 Growth Index | % | % | % | |||

Investment Adviser

Independence Capital Management, Inc.

Investment Sub-Adviser

T. Rowe Price Associates, Inc.

Portfolio Manager

P. Robert Bartolo, a Vice President of T. Rowe Price Associates, Inc., has served as portfolio manager of the Fund since October 2007.

Purchase and Sale of Fund Shares, Tax Information and Payments to Broker-Dealers and Other Financial Intermediaries

For important information about the purchase and sale of Fund shares, tax information and payments to broker-dealers and other financial intermediaries, please turn to the “Additional Fund Summary Information” section on pageXX of this prospectus.

26

Table of Contents

FUND SUMMARY: LARGE CAP GROWTH FUND

| Investment Objective | The investment objective of the Fund is to seek long-term capital appreciation. |

Fund Fees and Expenses

This table describes the fees and expenses that you may pay if you buy and hold shares of the Fund. The information in this table and the Example that follows does not reflect charges and fees deducted under your insurance contract. These charges and fees will increase expenses.

Annual Fund Operating Expenses

(expenses that you pay each year as a percentage of the value of your investment)

Investment Advisory Fees | 0.55 | % | ||

Distribution (12b-1) Fees | None | |||

Other Expenses | % | |||

Total Annual Fund Operating Expenses | % |

Example

This Example is intended to help you compare the cost of investing in the Fund with the cost of investing in other mutual funds. The Example assumes that you invest $10,000 in the Fund for the time periods indicated and then redeem all of your shares at the end of those periods. The Example also assumes that your investment has a 5% return each year and that the Fund’s operating expenses remain the same. Although your actual costs and returns might be higher or lower, based on these assumptions your costs would be:

| 1 Year | 3 Years | 5 Years | 10 Years | |||

| $ | $ | $ | $ |

Portfolio Turnover

The Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover may indicate higher transaction costs. These costs, which are not reflected in the annual fund operating expenses or in the Example, affect the Fund’s performance. During the most recent fiscal year, the Fund’s portfolio turnover rate was % of the average value of its portfolio.

Principal Investment Strategy

Under normal conditions, the Fund invests at least 80% of its net assets in common stocks of U.S. companies with large market capitalizations. This policy may be changed without the vote of shareholders but shareholders will be given 60 days’ advance notice of any change. For purposes of this policy, large capitalization companies have market capitalizations of more than $3 billion at the time of purchase. When selecting investments for the Fund, the Sub-Adviser seeks to identify large capitalization U.S. companies with strong earnings growth potential. Further, the Fund invests in securities of companies that the Sub-Adviser believes are favorably priced in relation to their fundamental value and will likely appreciate over time. These securities may be traded over the counter or listed on an exchange. While the Fund primarily invests in the common stocks of large capitalization companies, the Fund may invest a portion of its assets (no more than 20%) in small and medium capitalization companies. The Fund may participate in initial public offerings (“IPOs”).

In selecting companies for the Fund, the Sub-Adviser typically invests for the long-term and chooses securities that it believes offer strong opportunities for long-term capital appreciation. The Sub-Adviser generally considers selling a security when it reaches a target price, when it fails to perform as expected, or when other opportunities appear more attractive.

27

Table of Contents

Due to its investment strategy, the Fund may buy and sell securities frequently, which may result in higher transaction costs and may lower fund performance. An investment in the Fund may be appropriate for investors who are willing to accept the risks and uncertainties of investing in common stocks in the hope of long-term capital appreciation.

Principal Risks of Investing

Market Risk. Equity markets rise and fall daily. As with any investment whose performance is tied to these markets, the value of your investment in the Fund will fluctuate, which means that you could lose money.