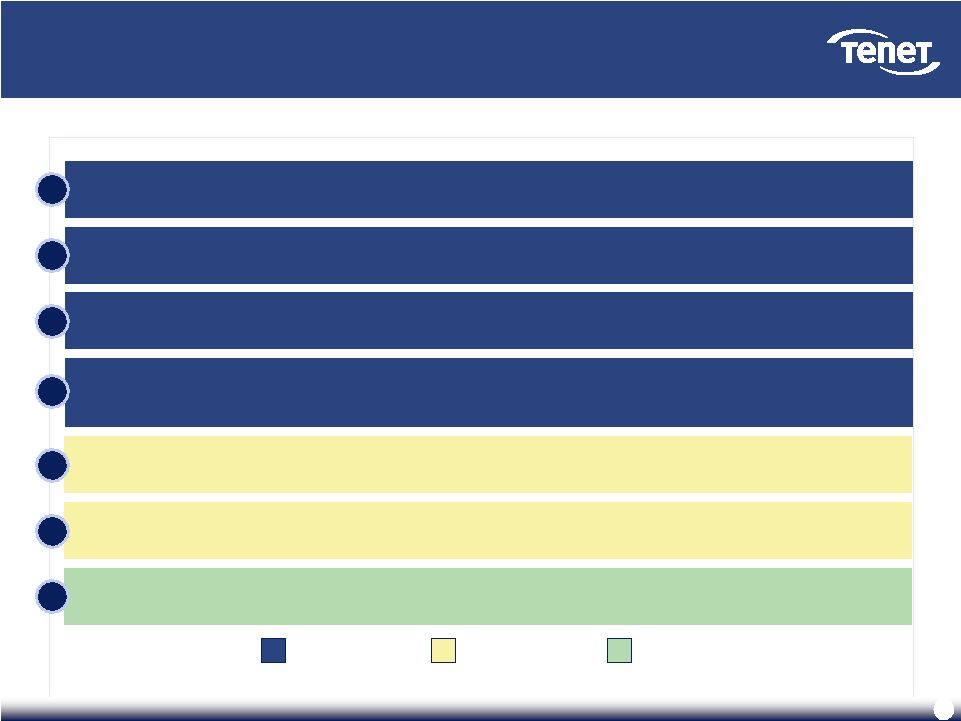

46 Tenet’s Board of Directors is aligned with shareholder interests (cont’d) Tenet’s Board of Directors is aligned with shareholder interests (cont’d) Government Experience Provider Experience Operating and Financial Expertise Edward A. Kangas, Non-Executive Chairman Global Chairman and CEO, Deloitte Touche (1989-2000) Member of Tenet Board since 2003 Other Directorships: Allscripts Healthcare Solutions, Hovnanian Enterprises, Intuit, United Technologies, Eclipsys*, EDS* Governor Jeb Bush Governor of Florida (1999-2007) Member of Tenet Board since 2007 Other Directorships: Rayonier, Swisher International, Angelica Trevor Fetter, President and CEO (Since 2003) President, Tenet (2002-2003) CEO, Broadlane (2000-2002) CFO, Tenet (1995-1999) Other Directorships: Hartford Financial Services Group Karen Garrison President, Pitney Bowes Business Services (1999-2004) Member of Tenet Board since 2005 Other Directorships: Kaman Corporation, Standard Parking, North Fork Bancorp* Floyd D. Loop, M.D. Chairman and CEO, The Cleveland Clinic Foundation (1989- 2004) Member of Tenet Board since 1999 Other Directorships: Athersys, Intuitive Surgical Ronald A. Rittenmeyer Chairman, President and CEO, Electronic Data Systems Corporation (2005-2008) Member of Tenet Board since 2010 Other Directorships: AIG, Electronic Data Systems*, R.H. Donnelley*, Safety-Kleen Systems*, RailTex* Brenda Gaines President and CEO, Diners Club North America (2002-2004) Member of Tenet Board since 2005 Other Directorships: Fannie Mae, NICOR, Office Depot, CNA Financial Corp* Senator J. Robert Kerrey President, New School University (2001-2010) Former U.S. Senator (1989-2000) Former Governor (1982-1987) Member of Tenet Board since 2001 Other Directorships: Genworth Financial, Jones Apparel Group, Scientific Games Corporation Richard R. Pettingill President and CEO, Allina Hospitals and Clinics (2002-2009) VP and COO, Kaiser Foundation Health Plans and Hospitals (1996-2002) Member of Tenet Board since 2004 Other Directorships: Mako Surgical James A. Unruh Chairman and CEO, Unisys (1990-1997) Member of Tenet Board since 2004 Other Directorships: Prudential Financial, Qwest Communications, CSG Systems International * - Indicates prior Directorship affiliation |