Exhibit 99.6

| SAS Standard Products and SAN Custom Solutions Jeff Richardson Executive Vice President Networking and Storage Products Group |

| Server Storage HPC (Clustered Computing) External RAID Controller SAN Fabric (Switches, Routers) External Disk Fabric (Drive Enclosure, Drive CRU) Investing in Our Storage Strengths SMB / RoBo Enterprise FC Disk Drive Enclosures FC-FC SATA-FC SAS-SAS Multiple Cascaded Enclosures SBB Disk Drive Enclosures SATA-SAS or AAMUX Highend (Price Band 7-9) Mid Range (Price Band 4-6) Server RAID Disk Drive Enclosure SAS-SAS or AAMUX Director FC Switch Router IB or 1Gbe for IPC Entry (Price Band 1-3) Multiple Cascaded Enclosures Total 2011 Silicon SAM Opportunity of $800M at CAGR of 14% |

| Server Storage HPC (Clustered Computing) External Storage (RAID Controllers) SAN Fabric (Switches, Routers) Disk Drive Fabric (Drive Enclosure, Drive CRU) Investing in Our Storage Strengths SMB / RoBo Enterprise FC Disk Drive Enclosures FC-FC SATA-FC SAS-SAS Multiple Cascaded Enclosures SBB Disk Drive Enclosures SATA-SAS or AAMUX Highend (Price Band 7-9) Mid Range (Price Band 4-6) Server RAID Disk Drive Enclosure SAS-SAS or AAMUX Director FC Switch Router IB or 1Gbe for IPC Entry (Price Band 1-3) Multiple Cascaded Enclosures SAS Expander SATA AAMUX External Storage SAS ROC SAS Controller Custom Solutions SAS ROC Server Storage SAS Controller PCI RAID SAS HBA SAN Fabric HBA Switch Custom Solutions Custom Solutions 2011 SAS Si SAM $360M 2011 Si SAM $200M 2011 SAS Si SAM $240M 2007-11 CAGR 9.5% 2007-11 CAGR 8% 2007-11 CAGR 26% Source: IDC, LSI |

| SAS Standard Products |

| Server Storage Product Leadership in SAS 3.5M+ SAS Controllers Shipped - #1 Share; 1M+ SAS ROC's Shipped and Ramping Server Storage Si: '07-'11 CAGR = 9.5% 2007 Top Tier OEM SAS Based New Products 2007 New SAS Platforms Shipping Proliant DL: 385 G2, 585 G2 Proliant ML/BL: ML370 G5, BL BL480c 2007 New SAS Platforms Shipping Power Edge: 6950, 2950, 1950 2007 New SAS Platforms Shipping Blades: HS21, LS21, JS21 Servers: x3250 2007 2008 2009 2010 2011 SCSI/SAS Controller IC's 118 97 89 95 120 ROC IC's 111 179 221 241 240 Controllers & HBA's ROC's e e e Source: IDC, LSI |

| Growth of LSI SAS Footprint in Servers SAS-based Servers Customer Value Higher Performance Reduced Board Space Lower Power Lower Cost Increases LSI's Server Product Content Improved Software Attach through MegaRAID Further Strengthens LSI's Storage Leadership Position LSI Has Successfully Driven the Migration From ROMB to ROC ~2X ASP Increase RAID Processor |

| 2007 2008 2009 2010 2011 Storage Processor IC's 1 2.5 21 46 91 SCSI/SATA/SAS Controller IC's 24 25 26 27 29 SAS Expander Drive CRU IC's 50 71 81 107 126 FC Controller IC's 41 41 43 46 54 FC Loop IC's 75 65 60 50 49 iSCSI Target Controller IC's 7 13 18 22 33 LSI SAS Leadership in External Storage LSI SAS "Hardened" and Shipping in External Storage Systems Significant Growth Opportunity as SAS Enables Entry Storage Systems SAS Platforms Shipping: MSA 50 Platform Shipping: F5402E SAS Platform Shipping: 1331, 1332, 1333 Platform Shipping: 2730 Significant SAS Si Revenue $500-$1K Per System due to Multiplier Effect External Storage SAS Si: '07-'11 CAGR = 26% e e e e Source: IDC, LSI |

| Creating Sustainable Leadership with Innovation Data Management Optimize Co-Existence of Solid State and Magnetic Media Lead Form Factor Evolution Tier 2: In Line Tier 3: Near Line Tier 4: Disk Archive Tier 1: On Line Tier 5: Tape Archive Current Tiered Storage Topology Cost Effective and Robust Solid State Storage will Transform Storage Architectures |

| Security Impacting ALL Storage Segments With Coverage of all Segments LSI well Positioned to Deliver End-to-End Security Solution Creating Sustainable Leadership with Innovation Data Protection RAID Architectures for Virtualization Security: DAR and DIF Deep Packet Inspection |

| Creating Sustainable Leadership with Innovation Storage Protocol SAS 2.0: 6G and Extended Features Virtualized Devices and Ports Solid State Storage Optimized Protocols |

| SAN Custom Solutions |

| SAN Custom Solution Leadership 8M+ FC HBA Silicon Shipped Since 2000 LSI #1 Share LSI + Agere Combination Extends SAN Silicon Leadership SAN HBAs SAN Switches SAN Port '06-'11 CAGR = 22% Source: Dell'Oro Group Well positioned to gain share 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 Switch 70.5 241.8 749.7 1069.8 1291.9 1745.6 2496.7 3075.2 4100 5300 6700 8500 10500 12700 HBA 58.9 196.8 553 731.6 896.7 1233.3 1556.3 2192.2 2760 3340 4050 4800 5650 6400 LSI Share Share Gain LSI SAN 15 20 85 LSI Share in '07 LSI Share Gains by '09 Additional Opportunity |

| Deep Mixed Signal Expertise Presents Significant Barrier to Entry First to Market with 1G, 2G, 4G and 8G SAN Silicon Industry Leading SerDes Package Co-Design Influence on Industry Standards Customer Experience Silicon Characterization Mixed Signal Expertise Sept 2004 Shipped Industry's first 4G FC HBA and Switch Silicon ? Sept 2004 8G FC Development begins ? July 2006 8G FC capabilities demonstrated ? Feb 2007 Shipped Industry's first 8G FC Switch Silicon ? July 2007 Shipped Industry's first 8G FC HBA Silicon ? Oct 2007 Demonstrate Multi-Protocol Capabilities In Progress July 2008 Ship Multi-Protocol Controller Silicon In Progress Scalable Architecture SerDes expertise is critical and takes several generations to master Investing years in advance of realized products |

| Leading Innovation in Enterprise Connectivity LSI+Agere Combination Creates Unique Storage & Networking Expertise Enabling Network Convergence Data Center Convergence Today's Enterprise Data Center Today's Enterprise Data Center Today's Enterprise Data Center LAN SAN HPC Ethernet RAID Next Gen 10GbE Converged Data Center Data, Storage, HPC over Ethernet Inflection Point: Data Center Convergence FC, iSCSI IB, Ethernet Ethernet FC, iSCSI IB, Eth 10Gb Ethernet |

| Storage Summary LSI Lead the Transition form SCSI to SAS in Servers Lead Evolution from ROMB to ROC in Servers Enabled Entry Storage Subsystems with SAS, now Shipping LSI, Agere Combination Extends Leadership in Custom SAN Silicon Strengthened Leadership Position Through Transition to 8G FC Double Digit Growth Opportunity in SAS and SAN Products Sustain SAS, SAN Leadership Position Through Innovation |

| Networking Jeff Richardson Executive Vice President Networking and Storage Products Group |

| Networking Business Merger Update Strategy Shift focus to growth markets Sharpen focus on markets where LSI has clear advantage Target top 5 OEMs that sell to top 10 Service Providers Products Focused product portfolio on growth markets Reduced investment in Ethernet Std Product & NAS Increase software investment to differentiate and build stickiness Expenses & Operations Merger of 3 BUs into a one organization Solution approach to product development Reduced CAD and Silicon infrastructure expense |

| Massive Network Build-Outs LSI uniquely positioned to capitalize on the next big network build-out Timeline 60s & 70s 80s & 90s Now through 2010s Market Need Increased Capacity Mobility Internet Real Time Hi BW Services On demand Video IPTV Collaboration Capability Build Out Analog to Digital Dedicated to Shared connection (circuit switched to TDM) Wireless infrastructure Copper to Fiber Packet switching Voice oriented (ATM) Data oriented (IP) Proliferation of IP based shared network Deterministic performance (QoS) over an IP network Location Entire Network Core and Transport Edge Enabler |

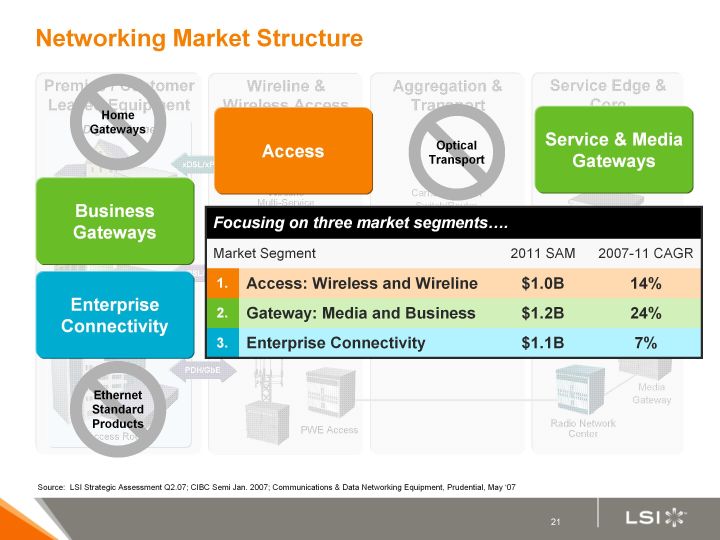

| Networking Market Structure Aggregation & Transport Wireline & Wireless Access Wireline Multi-Service Access Nodes Wireless Base Station 2/3/4G Premise / Customer Leased Equipment Digital Home Residential Gateway SMB / RoBo Business Gateway Enterprise Access Router PWE Access Carrier Ethernet Switch/Router DWDM Core Router Service Edge & Core Radio Network Center Edge Router Video Edge Core Router Long Haul DWDM Media Gateway 10GbE / DWDM xDSL/xPON GbE/10GbE PDH/GbE xDSL/xPON |

| Networking Market Structure Aggregation & Transport Wireline & Wireless Access Wireline Multi-Service Access Nodes Wireless Base Station 2/3/4G Premise / Customer Leased Equipment Digital Home Residential Gateway SMB / RoBo Business Gateway Enterprise Access Router PWE Access Carrier Ethernet Switch/Router DWDM Core Router Service Edge & Core Radio Network Center Edge Router Video Edge Core Router Long Haul DWDM Media Gateway 10GbE / DWDM xDSL/xPON GbE/10GbE PDH/GbE xDSL/xPON Ethernet Standard Products Source: LSI Strategic Assessment Q2.07; CIBC Semi Jan. 2007; Communications & Data Networking Equipment, Prudential, May '07 |

| Networking Market Structure Aggregation & Transport Wireline & Wireless Access Wireline Multi-Service Access Nodes Wireless Base Station 2/3/4G Premise / Customer Leased Equipment Digital Home Residential Gateway SMB / RoBo Business Gateway Enterprise Access Router PWE Access Carrier Ethernet Switch/Router DWDM Core Router Service Edge & Core Radio Network Center Edge Router Video Edge Core Router Long Haul DWDM Media Gateway 10GbE / DWDM xDSL/xPON GbE/10GbE PDH/GbE xDSL/xPON Service & Media Gateways Business Gateways Access Enterprise Connectivity Optical Transport Home Gateways Ethernet Standard Products Focusing on three market segments.... Focusing on three market segments.... Focusing on three market segments.... Focusing on three market segments.... Market Segment Market Segment 2011 SAM 2007-11 CAGR 1. Access: Wireless and Wireline $1.0B 14% 2. Gateway: Media and Business $1.2B 24% 3. Enterprise Connectivity $1.1B 7% Source: LSI Strategic Assessment Q2.07; CIBC Semi Jan. 2007; Communications & Data Networking Equipment, Prudential, May '07 |

| Market Trend #1: Demand for Real-Time High-Bandwidth Services & Collaboration Voice Revenues Declining Across all Service Providers New Network Requirements Video and IPTV Collaboration Fixed Mobile Convergence Need for New Services Real-Time Quality of Experience Advanced Packet Processing Advanced Traffic Management Media/Signal Processing Security Advanced Packet Processing Deep Packet Inspection Content Awareness Advanced Packet Processing Advanced Traffic Management Deep Packet Inspection Media/Signal Processing Enabling New Services with Carrier Grade Network Capabilities LSI Platform of Network Capabilities |

| LSI Solution for Customers LSI Solution for Customers Complete system solutions (both HW and SW) Flexibility to integrate silicon ingredients Ability to customize solutions for OEMs Industry Consolidation Industry Consolidation Service Providers Local, Global and Wireless Carriers consolidate to reduce costs and compete Original Equipment Manufacturers Top OEMs follow driving platform and solution consolidation and rationalization Market Trend #2: Consolidation Platform Consolidation Platform Consolidation OEM platform consolidation to improve R&D efficiency and time-to-market Consolidation requires suppliers with full suite of ingredients and flexibility to customize + DSP NP SoC Delivering OEM Platform Consolidation with Full Solutions |

| Offering Full Solutions, Not Just Components Full solutions focus enables us to deliver for our customers: Higher value platform optimized technology, e.g., power, QoS, DPI, etc. Richer partnerships and one-stop shopping convenience Deeper and more valuable end-market understanding Focus Solutions Focus Solutions Custom SoC Traffic Management Network Processing Signal Processing Gateways Business Gateways Media & Service Access Wireless Access Wireline Enterprise Connectivity LAN Enterprise Connectivity SAN LSI offering Platform Network Capabilities in Target Markets Competitor 3 Competitors offer component solutions in few market segments Competitor 2 Competitor 4 Competitor 1 Competitor 5 Competitor 6 Bringing LSI Network Expertise to the Enterprise |

| Offering Full Solutions, Not Just Components Full solutions focus enables us to deliver for our customers: Higher value platform optimized technology, e.g., power, QoS, DPI, etc. Richer partnerships and one-stop shopping convenience Deeper and more valuable end-market understanding Focus Solutions Focus Solutions Custom SoC Traffic Management Network Processing Signal Processing Gateways Business Gateways Media & Service Access Wireless Access Wireline Enterprise Connectivity LAN Enterprise Connectivity SAN LSI offering Platform Network Capabilities in Target Markets Competitor 3 Competitors offer component solutions in few market segments Competitor 2 Competitor 4 Competitor 1 Competitor 5 Competitor 6 Bringing LSI Network Expertise to the Enterprise |

| Common Hardware and Software Platform Customer A: Managed Business Gateway / NG Services Voice/WAN Gateway Wireless Access Point Ethernet PoE Switch Converged Business Gateway Portfolio New Services: Enterprise Class Security Advanced Data Capabilities Remote IT Ready for Production Lab trials now SMB trials in Sep.07 Full launch in Dec.07 Delivering Carrier Class Performance at SMB Price Points Programmable Platform Enabling Zero-Touch Service Enhancements 12-Port Business GW 8-Port Business GW Competitor A Competitor B Competitor C Competitor D |

| Customer B: Media Gateways / Platform Consolidation Wireline MGW Converged MGW 1 Common Platform LSI Delivering Platform Consolidation: Enabling R&D Efficiency & BOM Reduction for Customers Mobile MGW 3 Different Platforms Complete Portfolio Single platform Double the density Half the power Ready for NG Services Voice and Video Advanced Packet and Traffic Mgmt Competitor A Competitor B Competitor C Competitor D |

| Aggregation & Transport Wireline & Wireless Access Wireline Multi-Service Access Nodes Wireless Base Station 2/3/4G Premise / Customer Leased Equipment Digital Home Residential Gateway SMB / RoBo Business Gateway Enterprise Access Router Carrier Ethernet Switch/Router DWDM Core Router Service Edge & Core Radio Network Center Edge Router Video Edge Core Router Long Haul DWDM Media Gateway 10GbE / DWDM xDSL/xPON GbE/10GbE PDH/GbE xDSL/xPON Customer B: Engagements in 2004 / 2005 GSM RBS Agere DSP ATM Switch Agere Advanced Payload Plus Chipset |

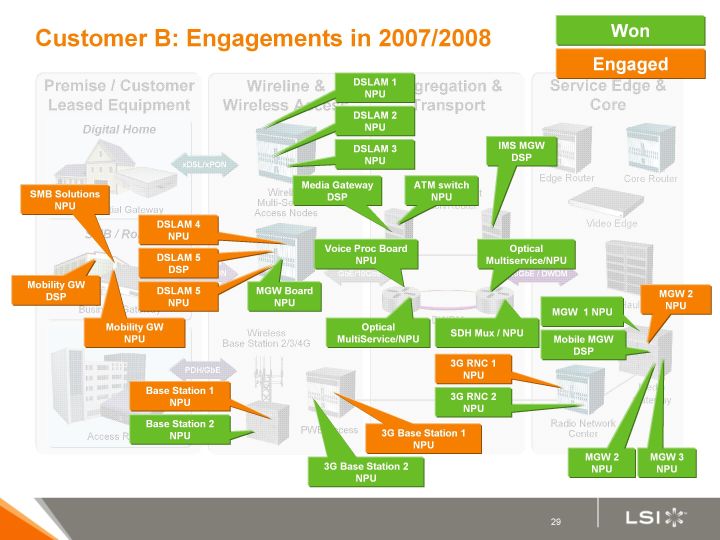

| Customer B: Engagements in 2007/2008 Aggregation & Transport Wireline & Wireless Access Wireline Multi-Service Access Nodes Wireless Base Station 2/3/4G Premise / Customer Leased Equipment Digital Home Residential Gateway SMB / RoBo Business Gateway Enterprise Access Router PWE Access Carrier Ethernet Switch/Router DWDM Core Router Service Edge & Core Radio Network Center Edge Router Video Edge Core Router Long Haul DWDM Media Gateway 10GbE / DWDM xDSL/xPON GbE/10GbE PDH/GbE xDSL/xPON SMB Solutions NPU Mobility GW DSP Mobility GW NPU DSLAM 5 DSP MGW Board NPU DSLAM 5 NPU DSLAM 4 NPU DSLAM 2 NPU DSLAM 1 NPU DSLAM 3 NPU Base Station 2 NPU Base Station 1 NPU 3G Base Station 1 NPU 3G Base Station 2 NPU 3G RNC 1 NPU 3G RNC 2 NPU SDH Mux / NPU Optical MultiService/NPU Voice Proc Board NPU Optical Multiservice/NPU MGW 3 NPU MGW 2 NPU Mobile MGW DSP IMS MGW DSP MGW 2 NPU MGW 1 NPU ATM switch NPU Media Gateway DSP Won Engaged |

| Networking Summary New network build-out is underway & LSI positioned to lead Sharpened focus on markets where LSI has clear advantage Creating solutions that enable key trends: services & consolidation Increasing software content and capabilities Winning with the top 5 OEMs and increasing momentum |