October 11, 2012

Mr. Terence O'Brien

U.S. Securities and Exchange Commission

100 F Street, N.E.

Mailstop 4628

Washington, D.C. 20549

| Re: | Legg Mason, Inc. |

| Form 10-K for the Year Ended March 31, 2012 | |

| Filed May 25, 2012 | |

| Response dated September 17, 2012 | |

| File No. 001-8529 | |

Dear Mr. O'Brien:

We are in receipt of your comment letter dated September 20, 2012, and respond below to the comments as requested, including items from our discussion on September 24, 2012.

We believe that a focus of the questions and comments in your comment letters dated September 20, August 20, and August 8, 2012, is our market capitalization at December 31, 2011 and the related implications on our intangible and goodwill impairment testing as of that date. In addition to our responses on the specific questions in those letters, we believe the expanded discussion of our intangible and goodwill impairment testing conclusions, which follows, will be helpful to your understanding of our process.

We have focused on three main points:

| 1) | The reasonableness of our implied control premium, compared to our consolidated net assets, particularly in consideration of our business model |

| 2) | Comparison of the results of a variety of valuation techniques |

| 3) | Our use of an independent valuation firm to review our process and the results of our testing |

We believe that our consideration of how the carrying value of our consolidated net assets compares to our market capitalization provides compelling contemporaneous evidence supporting our goodwill and intangible impairment testing conclusions as of December 31, 2011.

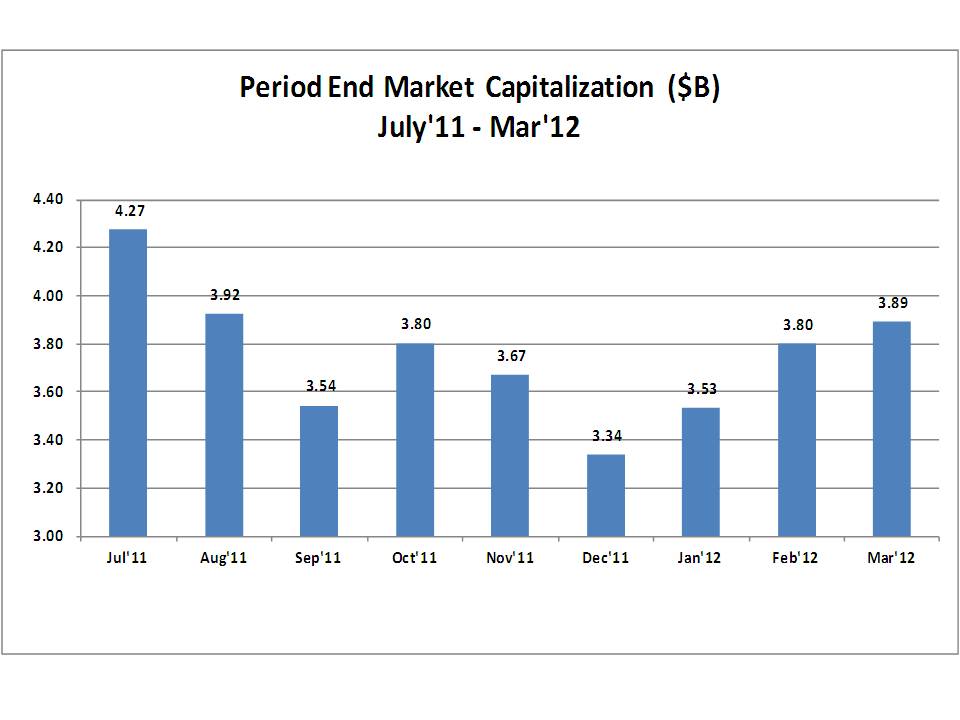

On December 31, 2011, our market capitalization was $3.34 billion ($23.88 x 139.8 million shares outstanding). This market capitalization reflects the low stock price on that day, without adjustment. Our net assets on December 31, 2011, were $5.60 billion, suggesting an implied control premium of 68%. In conjunction with our impairment testing, we performed a detailed study of actual observed relevant

Page 2 of 17

market transaction control premiums and determined a range of such values to be from 23% to 79% (with an average of 46%), which excludes outliers observed in the data, was reasonable and appropriate for consideration of Legg Mason's consolidated value. The implied control premium based on the carrying value of our consolidated net assets at December 31, 2011, was comfortably within the identified reasonable range of such values. Further, our implied control premium calculated on the same basis for the two months before and three months after December 31, 2011 would have been between 45% and 60%.

In addition, our business is such that it must be considered in developing an entity value for Legg Mason relative to other firms. Our business model involves decentralized affiliate advisory business units that are supported collectively from a corporate center that includes significant executive, administrative and distribution cost centers. While these are necessary functions in our current model, they also represent costs that would be duplicative to market participants acquiring our business. This concept is not unique to Legg Mason, but the extent of our corporate resources relative to those of other businesses and its impact on the market value of our business is not as common. In addition to the [***] of corporate cost present value we have identified in the DCF valuation analyses we have provided in response to your questions, there is another [***] to [***] of distribution cost present value that may be duplicated by the buyer's distribution resources in an acquisition of Legg Mason's consolidated business. Because an acquirer would likely eliminate these costs as being duplicated in their own cost structure, this suggests a market participant acquiring our business would pay a higher control premium than purchasers of other businesses. Quantifying the impact of our business model on the value of our consolidated business is highly subjective, but it justifies an implied control premium above the average of observed relevant market transaction control premiums. The 68% control premium implied by our total consolidated net asset carrying value to our market capitalization at December 31, 2011 is within the range of relevant observed market transaction control premiums and the nature of our business model further supports that our control premium is above the average of the observed range.

In addition to the above, we performed valuations of our reporting unit, consolidated entity and various intangible assets that have carrying values to substantiate that recorded goodwill or individual intangible assets were not impaired as of December 31, 2011. These valuations included DCF analyses that incorporated detailed growth assumptions developed at the individual affiliate business unit level and were compared to and considered in relation to other market data relevant to our business. In addition to considering our own experience and market statistics, we also developed a valuation of our entity from EBITDA multiples implied in actual control transactions of asset management businesses. These valuation methods resulted in a range of values, the variances in which we considered in relation to our conclusions and determined they were appropriate.

We also had our impairment testing process and conclusions reviewed by a large, independent and highly respected valuation practice who concluded that the methods, assumptions and calculations utilized in our valuation analyses were consistent with accepted valuation practices. These processes were also consistent with past practices, while utilizing current valuation insights and perspective.

_____________________________

[***] Information has been redacted in accordance with Legg Mason's request for confidential treatment under separate cover.

Page 3 of 17

Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations, page 23

Critical Accounting Policies and Estimates, page 46

Goodwill, page 52

Comment 1:

We note that you have one reporting unit for which you estimate the fair value for purposes of testing goodwill for impairment using the discounted cash flows methodology under the income approach. ASC 820-10-35-53 notes that the objective of unobservable inputs remains the same, which is an exit price from the perspective of a market participant. Please provide us with your reconciliation of the estimated fair value of your reporting unit to your market capitalization as of your testing date, as a corroborative step in evaluating the reasonableness of the estimated fair value. In this regard, your quoted stock price is a relevant and observable data point that market participants would utilize in pricing your single reporting unit. As part of your response, please provide us with your calculation of market capitalization, including an explanation as to the appropriateness of your calculation.

| • | In calculating your average market capitalization, why did you utilize a 60-day average stock price rather than any other period. What made this period the most appropriate and what is your routine procedure? |

| • | In calculating your average market capitalization, you indicate you utilized a simple average of shares outstanding at 12/31/10 and 10/31/11 to acknowledge share buy-backs. Please discuss why that average was appropriate and determined, rather than utilizing a point in time. Additionally, why are the periods for the average shares and average share price different? |

Response:

We have included under separate cover, with our request for both confidential treatment and return to us upon completion of your review, pursuant to Exchange Act Rule 12b-4, Attachment 1, which provides our reconciliation of the estimated fair value of our reporting unit to our market capitalization as of our testing date. In this regard, below is a discussion of this reconciliation and our assessment of the calculation in relation to our impairment testing.

The implied control premium calculation you request based on the DCF reporting unit valuation (adjusted for corporate costs and net debt) in isolation, without consideration for the weighting with the market multiple valuation, yields values of [***] and [***] as of October 31, 2011 and December 31, 2011, respectively. The October 31, 2011 value is just outside of the range of observed relevant market control premium values referenced in our comment response letter dated September 17, 2012, and the December 31, 2011 value is slightly further out of the observed range. We note that the full range of observed values (see comment letter response dated September 17, 2012, Attachment 4, page 9) was wider, but we conservatively excluded the outlying one-third of all of the values. As such, a value just outside of our range is not therefore unacceptable. We also note that at the time of our December 31, 2011 impairment testing, although the growth assumptions were appropriate, we had reason to reconsider management's assumptions for certain affiliates and therefore performed alternate impairment tests for goodwill and certain intangible assets (see further discussion in our comment response letter dated September 17, 2012, comment 3). Under these alternate tests, the implied control premium calculation you request based on the adjusted DCF reporting unit valuation in isolation, without consideration for the weighting with the market multiple valuation, yields values of [***] and [***] as of October 31, 2011 and December 31, 2011, respectively. Both of these values are in the range of observed relevant market control premium values, even with the outliers excluded. We further note, as indicated above: 1) we expect our implied control premium to be above the average of observed relevant market transaction control premiums

_____________________________

[***] Information has been redacted in accordance with Legg Mason's request for confidential treatment under separate cover.

Page 4 of 17

because of our business model and 2) our 68% implied control premium based on the carrying value of our consolidated net assets at December 31, 2011, was comfortably within the range of observed relevant market control premium values.

We understand your request to perform this control premium calculation based solely on the DCF analysis as a corroborative step in evaluating the reasonableness of the estimated fair value of our reporting unit. Although the resulting implied control premium values at October 31 and December 31, 2011 are slightly outside of the range of observed relevant market control premium values, that does not indicate the DCF analysis was therefore flawed. We also considered other indicators of value, which suggested the DCF valuation was acceptable as well as the fact that Legg Mason stock traded at a depressed value relative to prices on other dates during the fiscal year. Based on consideration of all the factors, we concluded the reporting unit carrying value as of December 31, 2011 determined under the DCF analysis was appropriate.

The other indicators of value suggesting the DCF valuation was acceptable include a comparison of the DCF value (adjusted for corporate costs and net debt) to the other market approach result discussed further below in our response to Comment 2 and the results of alternate tests. The results of the alternate tests showed that even with reduced growth rates for certain affiliates [***], the DCF result was readily comparable to the market approach result and did not change our conclusions regarding impairment.

Further, we did not believe our stock price at December 31, 2011, was an appropriate indicator of value for our impairment tests, as evidenced in the volatility of our share price during the months prior and weeks subsequent to December 31, 2011 being 10-15% higher than the December 31 price, and therefore we utilized a 60-day average price. We reference the speech of SEC staff member Robert Fox dated December 8, 2008 to support this approach:

“While it would be prudent to reconcile the combined fair value of your reporting units to your market capitalization, I believe that this should not be viewed as the only factor to consider in assessing goodwill for impairment.

When a registrant is evaluating an appropriate control premium, I believe that an important factor to consider is their recent trends in market capitalization. Note that I said recent trends in their market capitalization. Especially in volatile markets, and other unique circumstances, it may not always be reasonable to look at a single day's market capitalization. ”

_____________________________

[***] Information has been redacted in accordance with Legg Mason's request for confidential treatment under separate cover.

Page 5 of 17

Below is a chart showing the fluctuation in our market capitalization from July 31, 2011 through March 31, 2012.

Had we thought our December 31 stock market price (either the spot, 30-day or 60-day average) was reflective of a permanent price trend, we would have given additional consideration of our December 31 market capitalization. Further, as noted below, analysts' comments at the time suggested higher values for Legg Mason's stock (which was $23.88 on December 31, 2011).

Page 6 of 17

| Date | Analyst | Recommendation | Target price | Implied 12/31/11 Market Cap (000s) | ||||

| 10-Nov | [***] | Buy | $ | 35.00 | $ | 4,895,590 | ||

| 10-Nov | [***] | Buy | 32.00 | 4,475,968 | ||||

| 27-Oct | [***] | Buy | 61.00 | 8,532,314 | ||||

| 27-Oct | [***] | Buy | 31.00 | 4,336,094 | ||||

| 10-Nov | [***] | Buy | 35.00 | 4,895,590 | ||||

| 13-Dec | [***] | Hold | 27.00 | 3,776,598 | ||||

| 27-Oct | [***] | Hold | 28.00 | 3,916,472 | ||||

| 27-Oct | [***] | Hold | 25.00 | 3,496,850 | ||||

| 15-Dec | [***] | Hold | 31.00 | 4,336,094 | ||||

| 9-Nov | [***] | Hold | 27.00 | 3,776,598 | ||||

| 7-Nov | [***] | Hold | 32.00 | 4,475,968 | ||||

| 28-Oct | [***] | Hold | ||||||

| 19-Dec | [***] | Hold | 27.00 | 3,776,598 | ||||

| 27-Oct | [***] | Hold | ||||||

| 10-Nov | [***] | Hold | 28.00 | 3,916,472 | ||||

| 10-Nov | [***] | Hold | 28.00 | 3,916,472 | ||||

| 30-Oct | [***] | Underperform | 29.00 | 4,056,346 | ||||

| 27-Oct | [***] | Underperform | 32.00 | 4,475,968 | ||||

| 27-Oct | [***] | Sell | 31.00 | 4,336,094 | ||||

| 1-Nov | [***] | Sell | 22.00 | 3,077,228 | ||||

| Median | 30.00 | 4,196,220 | ||||||

| Mean | 31.17 | 4,359,406 | ||||||

We also note that standard valuation practice would not ignore other available and readily applicable indicators of value (such as our market approach using an EBITDA multiple) when reconciling a valuation result (such as the adjusted DCF result) to another indicator of value (such as the market capitalization). In the circumstances, standard valuation practice is generally to average or weight the results as appropriate.

Below is discussion of our consideration of our stock prices and shares outstanding used in our calculations of market capitalization.

We have no express policy regarding the use of our stock price in calculations of market capitalization; our process is guided by circumstances and discussion with independent valuation experts. We generally use spot prices unless circumstances suggest the spot price is not an appropriate indicator of value. When circumstances suggest other data points are relevant, we believe 60-days is a reasonable span of stock prices in considering market capitalization and well within standard valuation practice. We believe a 60-day average was more appropriate in our circumstances because the December 31, 2011 spot price was a low point compared to the preceding prices and the trend shortly after December 31. Independent valuation consultants confirmed the appropriateness of a 60-day average in our circumstances. However, we believe even the 60-day average of $25.07 was depressed in light of the above data and discussion.

_____________________________

[***] Information has been redacted in accordance with Legg Mason's request for confidential treatment under separate cover.

Page 7 of 17

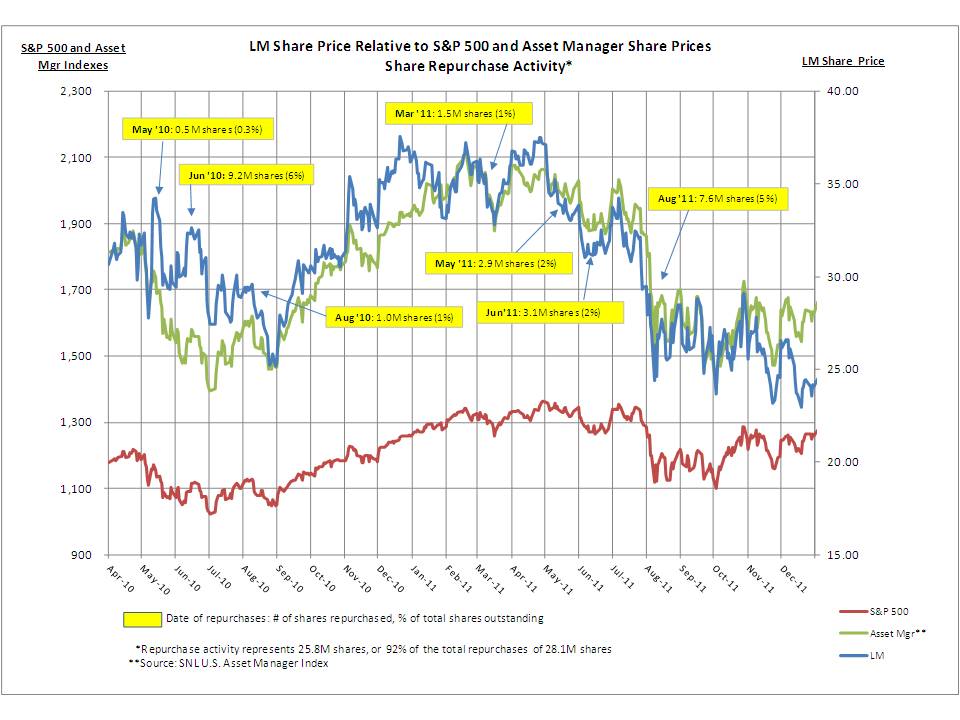

In regard to shares outstanding, during the twelve months ended December 31, 2011, we repurchased ~14 million shares (with no significant issuances) with no observable immediate impact to the price of our stock. Below is a chart that shows the market price of our stock, the average price of the stocks of our peers, and the price of an S&P 500 index, along with buy-back volumes for months of our more significant share buy-backs highlighted.

The market price of our stock, particularly during the twelve months ended December 31, 2011, generally moved in line with the average price of the stocks of our peers, and demonstrated little, if any, impact from our share buy-backs.

Using the average share price of $30 during the twelve months ended December 31, 2011, the impact of share repurchases to market capitalization was a decrease of greater than $400 million (~10%). Accordingly, we believed it appropriate to acknowledge in our market capitalization calculation that the impact of share buy-backs on share market price, if any, is gradual and therefore an average of outstanding shares is appropriate for contemplating market capitalization as an indicator of entity value. Based on our evidence and through discussion with our valuation consultants, we determined a simple average of shares during the nine months ended September 30, 2011, would be appropriate for our preliminary consideration of market capitalization (at October 31, 2011) as an indicator of entity value. Because there were no share buy-backs or significant issuances in the December 2011 quarter, we did not update the average share calculation at December 31, 2011. The periods over which our average share price and our average shares outstanding were determined differ because the factors influencing each were different, as explained separately above.

Page 8 of 17

Comment 2:

As discussed in your response to comment 4 in our letter dated August 30, 2012, we note that you compare the estimated fair value of your reporting unit using the discounted cash flow method, as adjusted for corporate debt and costs, to a market-based valuation of your equity value. Please provide us with an understanding as to how you determined the difference in the estimated fair value between these two methods is reasonable and did not require any adjustments to the assumptions and estimates used in the discounted cash flow method. ASC 820-10-35-55 notes that a reporting entity's own data used to develop unobservable inputs should be adjusted if information is reasonably available that indicates that market participants would use different assumptions.

| • | Please explain how you determined that the market approach is not a reasonable method to estimate the value of the reporting unit. |

| • | When considering one reporting unit, please explain how you considered the November 21, 2002, EITF Agenda Committee Report, Issue #2. As LM has only one reporting unit, explain why is it appropriate to exclude any assets or liabilities of the entity as a whole? Why would a market participant not be looking to acquire/value the consolidated entity? |

Response:

The valuation of a business is a complex process involving the application of professional judgments by the valuation analyst at various points in the process. There are a multitude of factors and assumptions that influence a valuation and these can vary depending on the method used to value the business. Generally, each method will yield a different value result or even a range of value results based on the sensitivity of these inputs. In theory, all of the methods used would result in a similar value. However, given the subjective nature of business valuation, it is inevitable that each methodology will generate a unique value estimate that differs from the value determined under each of the other methodologies. Sometimes the differences are minor, but in many cases the contrast in value estimates can be quite significant. Given that it is expected that contrasts in value will exist in arriving at a valuation conclusion, the standard valuation practice is for the valuation analyst to understand and analyze the results obtained under the different approaches and methods used (i.e., understand why differences exist).

The analysis of the equity value of our enterprise yielded results from the income approach and the market approach that varied by approximately [***]. As mentioned earlier, contrasts in value of this nature are not uncommon given the complexity of the valuation process and the application of professional judgment at various points in the process. In addition, the sensitivity of assumptions generally results in a range of values under each approach depending on the assumptions chosen. In order to reconcile the difference in value between our approaches, we first looked to understand the potential reasons for the difference and if adjustments to assumptions under either approach were necessary given the difference in value. We note in your comment that the difference in value may result in adjustments to the assumptions and estimates used in the DCF approach. Alternatively, however, the difference in value could also be attributable to adjustments needed to the assumptions and estimates used in the market approach.

As discussed in our previous response, our evaluation of the results of the DCF analysis of our reporting unit that incorporated management's budget assumptions considered that although the assumptions were appropriate, certain of management's early year flow assumptions were towards the higher end of a reasonable range for such inputs. The results of the alternative testing we performed, adjusted for corporate debt and costs, resulted in an equity value for the entity of [***] billion (versus the [***] billion shown in our analysis). This result showed that the range of reasonable values under the DCF method not

_____________________________

[***] Information has been redacted in accordance with Legg Mason's request for confidential treatment under separate cover.

Page 9 of 17

only still exceeded the carrying value of equity at the reporting unit level, but also were much closer in value to the result of the market approach.

As noted in our prior comment letter dated September 17, 2012, comment 3, Attachment 4, page 1, we did not include the market approach result when performing our goodwill impairment testing of the reporting unit because our market approach result, which estimates the value of Legg Mason as a whole, is not readily comparable to the fair value of the reporting unit. The market approach involves taking EBITDA multiples paid in corporate change of control transactions and applying them to the company's EBITDA to estimate the value of the entity. The market approach estimation is at the holding company entity level. In contrast, the income test is used to measure the value at the Global Asset Management reporting unit. As noted previously, the holding company entity level includes corporate costs and overhead that are not part of the reporting unit. These costs include costs associated with executive management, finance, human resources, legal and compliance, internal audit and other central corporate functions. The outcome of the market approach test is an estimate of value for the entire holding company entity, including these additional costs, and thus is not comparable to the value of the reporting unit determined under the income method, which excludes these costs. In order to adjust the entity value estimated under the market approach to make it comparable to the reporting unit value estimated under the income approach, we would have to adjust each transaction value included in the market approach calculation, at a minimum, to remove the comparable corporate costs. These adjustments would be difficult to assess, largely be arbitrary, and based on non-observable inputs.

Our evaluation of the results of the market approach also found that the market approach value was sensitive to changes in assumptions and thus could result in a range of reasonable values. In addition, although the market approach provides observable market inputs, it does have factors that can limit the validity of the results. These factors include:

| • | Sensitive to small changes in the market multiple |

| • | Comparability is subjective, and the level of comparability needs to be assessed with both objective analysis and reasoned judgment based upon specific facts |

| • | May need significant adjustments, such as removal of non-recurring items, consistency of accounting treatments, etc. |

Since specific details on actual market transactions are usually limited, the underlying drivers for transactions are often unknown. In addition, the comparability of the transaction targets to our business is a subjective assessment, and the range of possible multiples that can be derived and deemed reasonable based on the data available and adjustments made by the valuation analyst, can be significant. As such, although we chose to use the median EBITDA multiple in our analysis, we believe that a range of values under the market approach (including higher values) could be applicable. This would yield a result closer in value to the original discounted cash flow approach conclusion.

Given our understanding that the results of each approach could yield a range of reasonable values that in some cases approached each other, we determined that the difference in value between the two approaches could be explained by the sensitivity of the assumptions and judgments we made, and thus was reasonable.

It should be noted that once a valuation analyst understands and is comfortable with the results of each valuation method, the analyst then: a) assesses the reliability of the results under the different approaches and methods using the information gathered during the valuation exercise, and b) determines whether the conclusion of value should reflect the results of one valuation approach and method, or a combination of the results of more than one valuation approach and method. If a combination of results is deemed

Page 10 of 17

appropriate, then a weighting of approaches is performed based on the merits and reliability of each method.

Considerations for reconciling and weighting the valuation results include:

| • | Availability and reliability of financial and operational data (both historical and projected) |

| • | Availability of comparable guideline public companies |

| • | Existence of industry private sale transactional data |

| • | The type of business, the nature of business assets, and the type of industry subject to valuation |

| • | The nature of the business interest subject to valuation |

| • | Statutory, judicial, and administrative factors, if any |

As discussed in previous comments, in testing our entity equity value, we believed it was appropriate to give more weight to the market approach (75%) rather than the income approach (25%), because of our observations relating to the flow assumptions utilized for certain affiliates in our income approach noted above, and the premise that observable market inputs, although having their own limitations, are deemed more relevant in the fair value hierarchy.

While we did not overtly consider the issue referenced in the EITF minutes, it was never authoritative, and is arguably contradicted by other existing accounting guidance. We note that ASC 280-10-50 states:

“not every part of a public entity is necessarily an operating segment or part of an operating segment. For example, a corporate headquarters or certain functional departments may not earn revenues or may earn revenues that are only incidental to the activities of the public entity and would not be operating segments.”

As acknowledged in our comment response letter dated September 17, 2012, for comment 5 and in our proposed disclosures, we did compare our total consolidated net asset carrying value at December 31, 2011 of $5.6 billion to the assessed entity value of [***] billion and concluded no impairment. While we did not include other assets and liabilities in the documented reporting unit carrying value, based on the prior sentence, we did document that including these assets in the reporting unit carrying value would not have changed our conclusion. As previously discussed in this response letter, our model includes a corporate center that supports our affiliate asset management business units. These asset management affiliates are what comprise our operating segment for our internal reporting. Our structure is unique to the asset management industry.

Ultimately we performed our step 1 goodwill impairment test at (1) our reporting unit level that we use for internal reporting purposes and (2) at the full consolidated level, including all assets and liabilities.

For Legg Mason, as further provided by ASC 280-10-50, our operating segment is our reporting unit. Thus, authoritative accounting guidance contemplates that a reporting unit may exclude portions of an entity.

Also, our impairment testing is focused on our reporting unit and we believe that likely market participants that would buy our reporting unit would be other large asset management firms or large financial services firms. Such market participants already have established corporate functions that include executive management, finance, human resources, technology, legal, compliance and regulatory, risk management, etc., and therefore, they would not be interested in acquiring these aspects of our consolidated entity.

_____________________________

[***] Information has been redacted in accordance with Legg Mason's request for confidential treatment under separate cover.

Page 11 of 17

Comment 3:

In regards to your indefinite life intangible assets, Page 1 of Attachment 2, to the response dated September 17, 2012, indicates that the financial turmoil of 2008-2009 had a substantial impact on LM's business and the industry in the aggregate. Please discuss how LM compares to its peers in returning to a more stable environment. In doing so, please discuss the relevant data points, including long-term AUM growth rates (i.e., 2%), and how you considered this experience in setting your growth assumptions. For instance, you use a lot of market data to support your assumptions, how did you consider your specific facts and circumstances and determine that this market data was appropriate?

Response:

AUM relevant to our domestic mutual fund contract asset has tracked fairly closely to our peers, with some lag in recent years. “Long-term” AUM are assets in funds that are not liquidity funds (which investors tend to use for short-term investment of cash reserves) and include equity and fixed income funds. The total domestic mutual fund AUM is the sum of domestic liquidity fund AUM and domestic long-term fund AUM.

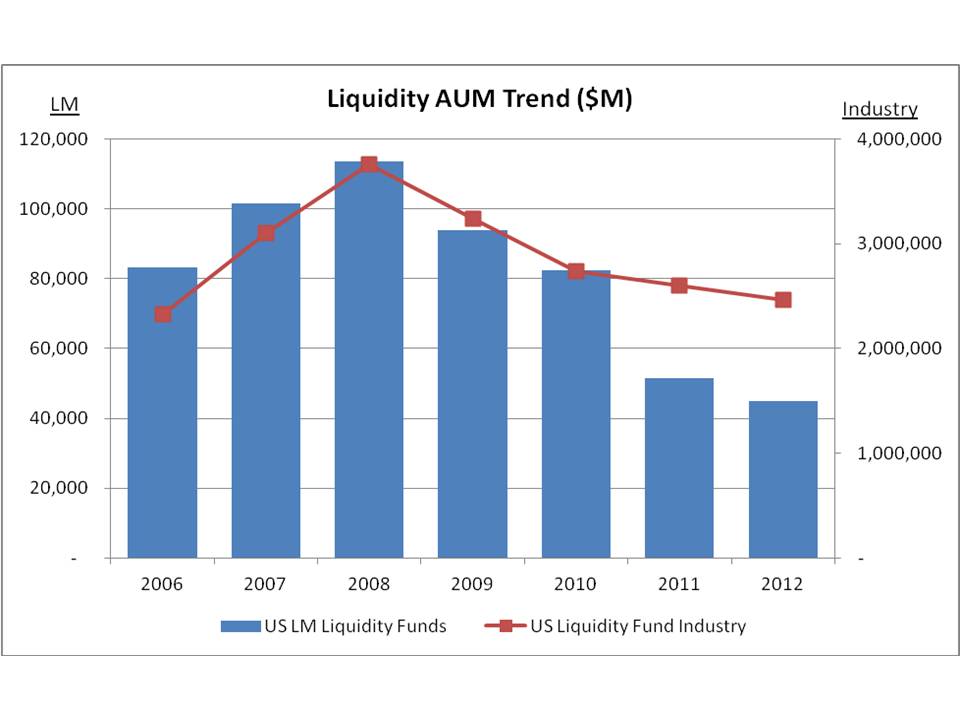

As noted below in our response to Comment 9, long-term AUM (excluding liquidity) is most relevant to the value of the domestic mutual fund contract asset, and the chart below shows the trend of our long-term AUM since 2006 compared to that of the U.S. fund industry for long-term AUM, per data from a leading industry group.

Liquidity AUM relevant to our domestic mutual fund contract asset has also followed industry trends, likewise validating the industry statistics as relevant to our assumptions. The chart below shows the trend of our liquidity AUM relevant to our domestic mutual fund contract asset since 2006 compared to that of the U.S. liquidity fund industry, per data from a leading industry group.

Page 12 of 17

We also note, and took into account in our considerations, certain aspects of Legg Mason's AUM that differentiate it from the AUM of the U.S. mutual fund industry and give rise to the lag in Legg Mason's AUM trend from that of the industry. Certain of Legg Mason's larger advisory affiliates experienced performance issues coming out of the financial turmoil in 2008 and 2009. While these advisors and their product performance have mostly recovered, the performance issues impacted our AUM trend and caused it to lag the industry trend. Legg Mason is also more dependent on third party intermediaries for distribution. Our business model is focused exclusively on advisory services without affiliation to a brokerage business that can distribute products, like some of our peers, which also gives rise to some lag from industry AUM trends. Our liquidity business, which makes up one-third or more of our U.S. fund AUM, further differentiates our AUM trend from that of the industry, which has less than one-sixth of total domestic AUM in liquidity funds. Following the financial turmoil of 2008 and 2009, investors were seeking higher yields and trended away from lower-yielding liquidity products. Also, during 2011, Morgan Stanley Smith Barney (“MSSB”) amended certain historical Smith Barney brokerage programs providing for investment in liquidity funds that our asset managers manage that resulted in an approximate $20 billion reduction of our liquidity AUM during 2011 and 2012. This was a one-time event which caused our low-fee liquidity AUM to trend lower than the industry in these years. In summary, although we fully considered aspects of Legg Mason's business that differentiate us from the industry and may cause our experience to lag that of our industry at times, we concluded that, overall, the industry statistics are very relevant to our growth assumptions.

Additionally, as disclosed in our prior comment response letter dated September 17, 2012, our historical flows before the market turmoil of 2008 and 2009 were well in excess of our projected average rate of net flows of 2% and the industry's historic long-term equity flow rate of 5%. We based our first three years of growth on the operating plan. After that point, we determined it was reasonable to use an average long-term rate of 2%, based on the industry history, our experience and our current activities.

In regard to market growth rates, as noted in our comment response letter dated August 20, 2012, Attachment 1, market growth assumptions used in the multi-year plan and 20-year projections for equity

Page 13 of 17

products are 6% during fiscal 2013 and 2014 and 7% thereafter. Support for these growth rates for equity products can be found from observations of past market history that equity returns average 7-10%, per Bloomberg, Barclays, and NASDAQ. As of September 30, 2011, 71% and 73% of our U.S. mutual fund AUM have outpaced their 3-year and 5-year Lipper category averages, further supporting the use of these historical trends in our equity growth assumptions. Market growth assumptions used in the multi-year plan and 20-year projections for fixed income products are expected to grow 3% and liquidity products are expected to grow 1% in 2013 and 2% thereafter. These estimates are more dependent on our actual experience. We note our Western Asset fixed income products have 10-year performance clearly exceeding 5% and more significant liquidity products have longer-term performance approximating or upwards of 2%.

Comment 4:

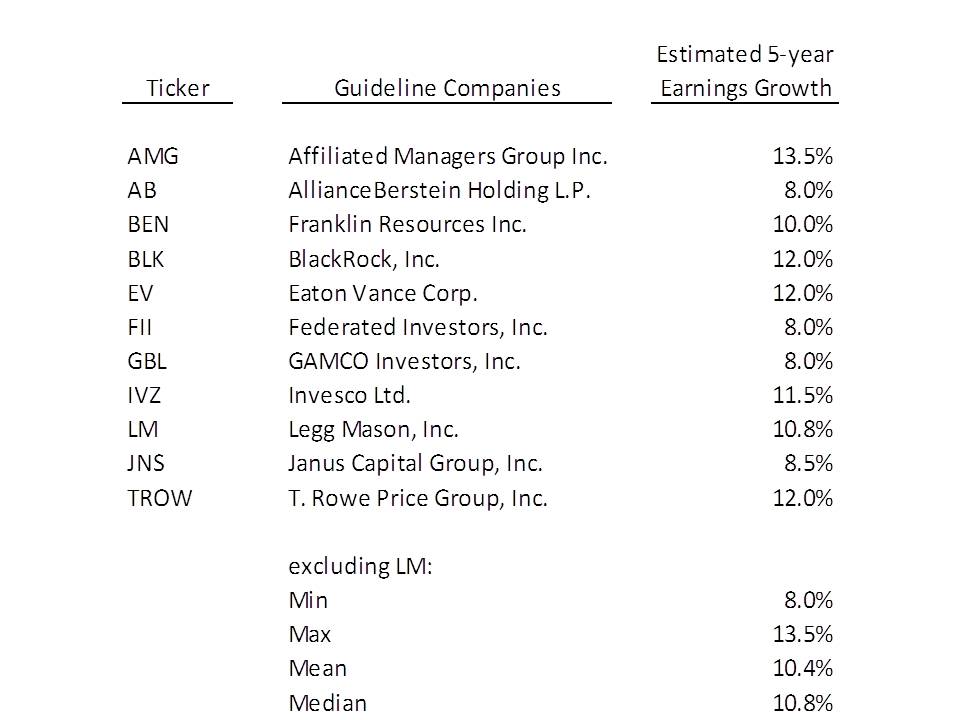

We note in your response to comment 2, dated September 17, 2012, that analysts' long-term earnings growth estimates for LM's peer group companies ranged from 8.0% to 13.5%, with LM's consensus growth estimate at 11%. Please explain the source of these estimates, and explain how these earnings growth rates compare to and are relevant with, and can be used to support, your cash flow growth rate assumptions used in your goodwill testing.

Response:

Our independent valuation consultants obtained the consensus estimates for 5-year earnings growth for each of our peer group companies as well as Legg Mason. This data is compiled by S&P CapitalIQ and as of October 31, 2011, these consensus estimates were:

As stated above, these growth rates represent consensus analyst expectations for growth in earnings over the next 5 years. While earnings growth does not directly translate into cash flow growth, in this case, given the fact that these businesses do not require significant amounts of working capital or capital expenditures/depreciation, earnings growth is a reasonable proxy for cash flow growth. As we analyzed the data contained in the table above, including consideration of our specific circumstances, we believed that it further supported the growth rates used in our projection model and provided independent data

Page 14 of 17

supporting the fact that the growth rates that are included in our projection models are consistent with, or even conservative in comparison to, expectations for our peer companies.

Comment 5:

For your domestic mutual fund contract asset, Permal funds-of-hedge funds contract asset, and goodwill; please provide specifics about how actual results have compared to projected results for the past three complete years and current year-to-date results.

Response:

We have included under separate cover, with our request for both confidential treatment and return to us upon completion of your review, pursuant to Exchange Act Rule 12b-4, Attachment 2, which provides a comparison of our cash flow growth projections for the past three complete years and current year-to-date to actual results for our domestic mutual fund contract asset, Permal funds-of-hedge funds contract asset, and our reporting unit.

We note that the growth assumptions from our December 31, 2011 impairment testing for our domestic mutual fund contract asset compare slightly favorably to year-to-date results. Also, our reporting unit's actual results have been generally favorable compared to projections. Specifically, in 2008, we were conservative and underestimated flows and market performance for our reporting units. The domestic mutual fund contract asset and the Permal funds-of-hedge funds contract asset collectively contribute approximately one-third of the reporting units' cash flow, so the projection to actual results of these assets are not indicative of the projection to actual results of the reporting units.

The ultimate impact of the differences of actual results versus projections on Legg Mason's assessments of value for impairment testing does not indicate a problem with our valuations for various reasons. Our discounted cash flow analyses include projections well beyond three years and variances in the near years may yield an offset in subsequent years. Also, fair value assessments are point-in-time and the consistency of a fair value assessment with other indicators of value that reflect expectations of market participants at that point-in-time is more critical evidence of the soundness of the estimate of value. However, we consider the differences in actual results from our projections to influence how we consider the related asset carrying values in subsequent periods, including the assumptions for impairment testing in subsequent periods. We adjust our processes as appropriate and include this information in subsequent projections. For example, early year outflows projected for [***] and [***] in our December 31, 2011 impairment testing assumptions were influenced by our past experience and comparisons to past projections.

Comment 6:

In regards to your domestic mutual fund contract asset, Permal mutual fund contract asset, and goodwill; please provide an explanation as to how the growth rates were developed for years 4 to 40. It is noted that management's projections are utilized for years 1 to 3, however, it is unclear how growth rates are developed for the out years. Specifically, years 4 to 16 seem to fluctuate in all three asset tests, before attaining a constant growth rate in year 17. Please explain.

Response:

Each year of management's three-year plan carefully considers specific assumptions by asset class for each affiliate, and projects AUM market and net flow growth, and considers known factors influencing future flows, in projecting planned operating results. In our prior response, on page 2 of Attachment 1 of

_____________________________

[***] Information has been redacted in accordance with Legg Mason's request for confidential treatment under separate cover.

Page 15 of 17

our letter dated September 17, 2012, we have explained how yields and revenue share arrangements are considered in developing projected operating results and how operating results relate to cash flows for the three-year plan.

For the subsequent 17 years, the key underlying AUM assumptions of equity market growth (7%), fixed income market growth (3%), liquidity market growth (2%), and overall net flow growth (2%) are generally held constant for each affiliate in projecting operating results. Even though these rates are held constant at the affiliate level, they continue to affect the AUM mix over time because equity assets, which are generally higher yielding, are projected to grow faster than both fixed income and liquidity assets, resulting in higher overall yields and revenues. This leads to dynamic cash flow growth rates over the twenty years. In summary, although growth rates by asset class may be constant or similar, the mix of asset classes and related revenue yields and revenue share by affiliates impacts the level of overall revenue and cash flow growth rates. Also, because the AUM growth rate projections are for end-of-year AUM (i.e., the AUM grows over the year and achieves the projected growth rate at year-end), the resulting cash flow projections for any one year for specific intangibles and the reporting unit are an average of the AUM projections for the two relevant years then ended. This is most evident in our projections that involve only one affiliate, where the year 1 and 2 AUM projections (market and flows) are [***] and [***], respectively, yet the year 2 cash flow growth projection is [***] (see page 8 of Attachment 1 of our letter dated September 17, 2012 and page 11 of Attachment 1 of our letter dated August 20, 2012). The effective cash flow growth projection for year 2 is the average of the AUM projections for the two years then ended [([***] + [***])/2 = [***]].

Certain other specific fluctuations in the cash flow projections are explained below.

| • | [***] |

| • | [***] |

| • | [***] |

For years 20 through 40, cash flow growth rates for specific intangibles and the reporting unit are held constant because of the diminished impact of more precise calculations after a discount for time value.

Comment 7:

Please explain the disparity between the values placed on the AUM related to your domestic mutual fund contract, as compared to the value of the AUM for goodwill as a whole. Specifically, the relationship of AUM to fair value for the domestic mutual fund contract asset is higher than the relationship of AUM to fair value for goodwill.

Response:

As noted in our September 17 response, comment 2, page 2, our reporting unit includes the separate account businesses of various affiliates, in addition to the domestic mutual fund and fund-of-hedge funds assets. Separate accounts generally carry lower yields than comparable fund products. More specifically, separate accounts for Western Asset Management and ClearBridge, our two largest advisors, have average fees of one-half to one-third that of their comparable respective fund products. Further, at the reporting unit level, separate accounts constitute 55% of the AUM. Accordingly, it is expected that the overall reporting unit AUM, on average, provides less value than pure fund AUM because it generates less revenue per dollar of AUM. We have included under separate cover, with our request for both confidential treatment and return to us upon completion of your review, pursuant to Exchange Act Rule

_____________________________

[***] Information has been redacted in accordance with Legg Mason's request for confidential treatment under separate cover.

Page 16 of 17

12b-4, as Attachment 3, a schedule of our separate account and fund yields and AUM by affiliate to further substantiate this observation.

Comment 8:

You have cited alternate tests of value for both the Permal mutual fund asset and goodwill. Did you perform an alternate test of value for your domestic mutual fund contract asset? If so, please provide a copy of and explanation of this analysis, including probabilities associated with each scenario. Please also explain your rationale for why you did or didn't perform this analysis.

Response:

We have included under separate cover, with our request for both confidential treatment and return to us upon completion of your review, pursuant to Exchange Act Rule 12b-4, Attachment 4, which provides our stress test of the domestic mutual fund contract asset carrying value at December 31, 2011. In this stress test, flows were reduced to [***] in year 1 and [***] in year 2 to consider reasonably possible outcomes based on past experience. Under this stress test, the assessed value of the domestic mutual fund contract asset was [***] of its carrying value at December 31, 2011. The stress test of the domestic mutual fund contract asset represented a possible outcome, but the original test assumptions were considered to be the likely outcome based on management's projection.

We distinguish stress tests from the alternate tests described in our comment letter response dated September 17, 2012, for comments 1 and 3. As described in those responses, the alternate tests were performed because certain assumptions in our original tests, while appropriate, were considered to be towards the higher end of the range of reasonable outcomes and the alternate tests were necessary to substantiate our conclusions regarding the Permal fund-of-hedge funds contract asset and the reporting unit along with management's projections in those tests. A stress test considers projection outcomes with a lesser likelihood of actually occurring than the outcomes included in our alternate tests. We generally perform stress tests for impairment tests that demonstrate narrower coverage of the related carrying value.

Comment 9:

We note on page 2 of 12 of Attachment 2, in your response dated September 17, 2012, that Legg Mason's long-term mutual fund AUM has increased approximately 25% from December 31, 2008 through July 31, 2012. Please explain what the 25% represents. Please also explain if the “long-term” assets are a subset of the total information provided.

Response:

We have included under separate cover, with our request for both confidential treatment and return to us upon completion of your review, pursuant to Exchange Act Rule 12b-4, Attachment 5, which shows AUM activity relevant to the domestic mutual fund contract asset from January 1, 2008 through July 31, 2012. As noted above, long-term AUM are assets in funds that are not liquidity funds (which investors tend to use for short-term investment of cash reserves). In this attachment, the long-term portion of the relevant AUM grows from [***] billion at December 31, 2008, to [***] billion at July 31, 2012, or 25%.

We observe that liquidity fund AUM fluctuates more widely than AUM in other fixed income or equity products because liquidity funds are often used by clients for working capital rather than long-term investment. Also, liquidity fund yields are far less than other fixed income or equity products. For these reasons, long-term AUM is a better indicator of the value of our domestic mutual fund contract value, and is therefore monitored as a separate component of the relevant data. Long-term AUM is not a distinct

_____________________________

[***] Information has been redacted in accordance with Legg Mason's request for confidential treatment under separate cover.

Page 17 of 17

“subset” of the domestic mutual fund contract asset AUM, but it is a more significant contributor to the value of the related asset and it is therefore monitored.

In connection with our response to your comment letter, we acknowledge that:

| • | We are responsible for the adequacy and accuracy of the disclosure in the filing; |

| • | Staff comments or changes to disclosure in response to staff comments do not foreclose the Commission from taking any action with respect to the filing; and |

| • | We may not assert staff comments as a defense in any proceeding initiated by the Commission or any person under the federal securities laws of the United States. |

If you have any additional questions or would like any additional clarification, please contact Brian Eakes (410-454-2965) or me (410-454-2935).

Sincerely,

/s/ Peter H. Nachtwey

Peter H. Nachtwey

Chief Financial Officer

Attachments (provided under separate cover with our request for confidential treatment and return to us upon completion of your review pursuant to Exchange Act Rule 12b-4)

Unredacted Version of Comment Letter Response

1 - Comment 1, Reconciliation of DCF Estimated Fair Value of our Reporting Unit to Market Capitalization.

2 - Comment 5, Actual Results Compared to Projected Results for the Past Three Years

3 - Comment 7, Separate Account and Fund Yields and AUM by Affiliate

4 - Comment 8, Stress Test of Domestic Mutual Fund Contract Asset at December 31, 2011

5 - Comment 9, Domestic Mutual Fund Contract Asset AUM Growth from January 1, 2008 through July 31, 2012

| cc: | Tracey Smith, U.S. Securities and Exchange Commission, Division of Corporate Finance |