UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

__________________________________

FORM 10-Q

__________________________________

| | | | | |

| ☒ | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended November 30, 2023

or

| | | | | |

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number: 1-7102

__________________________________

NATIONAL RURAL UTILITIES

COOPERATIVE FINANCE CORPORATION

(Exact name of registrant as specified in its charter)

__________________________________

| | | | | | | | |

| District of Columbia | | 52-0891669 |

| (State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification No.) |

| | | | | | | | | | | |

| 20701 Cooperative Way, | Dulles, | Virginia, | 20166 |

| (Address of principal executive offices) (Zip Code) |

Registrant’s telephone number, including area code: (703) 467-1800

__________________________________

Securities registered pursuant to Section 12(b) of the Act:

| | | | | | | | |

| Title of Each Class | Trading Symbol(s) | Name of Each Exchange on Which Registered |

| 7.35% Collateral Trust Bonds, due 2026 | NRUC 26 | New York Stock Exchange |

| 5.50% Subordinated Notes, due 2064 | NRUC | New York Stock Exchange |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes x No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer ¨ Accelerated filer ¨ Non-accelerated filer x Smaller reporting company ¨ Emerging growth company ¨

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transaction period for complying with any new or revised financial accounting standards provided pursuant to Section13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No x

The Registrant is a tax-exempt cooperative and therefore does not issue capital stock.

TABLE OF CONTENTS

CROSS REFERENCE INDEX OF MD&A TABLES

| | | | | | | | | | | | | | |

| Table | | Description | | Page |

| 1 | | Summary of Selected Financial Data | | 4 | |

| 2 | | Net Income and TIER | | 6 | |

| 3 | | Adjusted Net Income and Adjusted TIER | | 7 | |

| 4 | | Average Balances, Interest Income/Interest Expense and Average Yield/Cost | | 12 | |

| 5 | | Rate/Volume Analysis of Changes in Interest Income/Interest Expense | | 15 | |

| 6 | | Non-Interest Income | | 18 | |

| 7 | | Derivative Gains (Losses) | | 19 | |

| 8 | | Comparative Swap Curves | | 20 | |

| 9 | | Non-Interest Expense | | 21 | |

| 10 | | Debt—Total Debt Outstanding | | 23 | |

| 11 | | Debt—Member Investments | | 24 | |

| 12 | | Equity | | 25 | |

| 13 | | Loans—Loan Portfolio Security Profile | | 28 | |

| 14 | | Loans—Loan Exposure to 20 Largest Borrowers | | 29 | |

| 15 | | Allowance for Credit Losses by Borrower Member Class and Evaluation Methodology | | 32 | |

| 16 | | Available Liquidity | | 34 | |

| 17 | | Liquidity Coverage Ratios | | 35 | |

| 18 | | Committed Bank Revolving Line of Credit Agreements | | 37 | |

| 19 | | Short-Term Borrowings—Funding Sources | | 39 | |

| 20 | | Long-Term and Subordinated Debt—Issuances and Repayments | | 40 | |

| 21 | | Long-Term and Subordinated Debt—Scheduled Principal Maturities and Amortization | | 40 | |

| 22 | | Collateral Pledged | | 41 | |

| 23 | | Loans—Unencumbered Loans | | 41 | |

| 24 | | Liquidity—Projected Long-Term Sources and Uses of Funds | | 42 | |

| 25 | | Credit Ratings | | 43 | |

| 26 | | Interest Rate Sensitivity Analysis | | 45 | |

| 27 | | Adjusted Net Income | | 46 | |

| 28 | | TIER and Adjusted TIER | | 47 | |

| 29 | | Adjusted Liabilities and Equity | | 48 | |

| 30 | | Debt-to-Equity Ratio and Adjusted Debt-to-Equity Ratio | | 48 | |

| 31 | | Members’ Equity | | 49 | |

| | | | |

PART I—FINANCIAL INFORMATION

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations (“MD&A”)

| | |

| FORWARD-LOOKING STATEMENTS |

This Quarterly Report on Form 10-Q for the quarterly period ended November 30, 2023 (“this Report”) contains certain statements that are considered “forward-looking statements” as defined in and within the meaning of the safe-harbor provisions of the Private Securities Litigation Reform Act of 1995. Forward-looking statements do not represent historical facts or statements of current conditions. Instead, forward-looking statements represent management’s current beliefs and expectations, based on certain assumptions and estimates made by, and information available to, management at the time the statements are made, regarding our future plans, strategies, operations, financial results or other events and developments, many of which, by their nature, are inherently uncertain and outside our control. Forward-looking statements are generally identified by the use of words such as “intend,” “plan,” “may,” “should,” “will,” “project,” “estimate,” “anticipate,” “believe,” “expect,” “continue,” “potential,” “opportunity” and similar expressions, whether in the negative or affirmative. All statements about future expectations or projections, including statements about loan volume, the adequacy of the allowance for credit losses, operating income and expenses, leverage and debt-to-equity ratios, borrower financial performance, impaired loans, and sources and uses of liquidity, are forward-looking statements. Although we believe the expectations reflected in our forward-looking statements are based on reasonable assumptions, actual results and performance may differ materially from our forward-looking statements. Therefore, you should not place undue reliance on any forward-looking statement and should consider the risks and uncertainties that could cause our current expectations to vary from our forward-looking statements, including, but not limited to, legislative changes that could affect our tax status and other matters, demand for our loan products, lending competition, changes in the quality or composition of our loan portfolio, changes in our ability to access external financing, changes in the credit ratings on our debt, valuation of collateral supporting impaired loans, charges associated with our operation or disposition of foreclosed assets, nonperformance of counterparties to our derivative agreements, economic conditions and regulatory or technological changes within the rural electric industry, the costs and impact of legal or governmental proceedings involving us or our members, general economic conditions, governmental monetary and fiscal policies, the occurrence and effect of natural disasters, including severe weather events or public health emergencies, and the factors listed and described under “Item 1A. Risk Factors” in our Annual Report on Form 10-K for the fiscal year ended May 31, 2023 (“2023 Form 10-K”), as well as any risk factors identified under “Part II—Item 1A. Risk Factors” in this Report. Forward-looking statements speak only as of the date they are made, and, except as required by law, we undertake no obligation to update any forward-looking statement to reflect the impact of events, circumstances or changes in expectations that arise after the date any forward-looking statement is made.

Our financial statements include the consolidated accounts of National Rural Utilities Cooperative Finance Corporation (“CFC”), National Cooperative Services Corporation (“NCSC”) and Rural Telephone Finance Cooperative (“RTFC.”) Our principal operations are currently organized for management reporting purposes into three business segments, which are based on the accounts of each of the legal entities included in our consolidated financial statements: CFC, NCSC and RTFC.

CFC is a member-owned, nonprofit finance cooperative association with a principal purpose of providing financing to its members to supplement the loan programs of the Rural Utilities Service (“RUS”) of the United States Department of Agriculture (“USDA”). CFC extends loans to its rural electric members for construction, acquisitions, system and facility repairs and maintenance, enhancements and ongoing operations to support the goal of electric distribution and generation and transmission (“power supply”) systems of providing reliable, affordable power to the customers they service. CFC also provides its members and associates with credit enhancements in the form of letters of credit and guarantees of debt obligations. As a Section 501(c)(4) tax-exempt, member-owned cooperative, CFC’s objective is not to maximize profit, but rather to offer members cost-based financial products and services. The interest rates on lending products offered to our member borrowers reflect our funding costs plus a spread to cover operating expenses and estimated credit losses, while also generating sufficient earnings to cover interest owed on our debt obligations and achieve certain financial target goals. Because CFC is a tax-exempt cooperative, we cannot issue equity securities as a source of funding. CFC’s primary funding sources consist of a combination of public and private issuances of debt securities, member investments and retained equity. NCSC is a member-owned taxable cooperative that is permitted to provide financing to members of CFC, government or

quasi-government entities which own electric utility systems that meet the Rural Electrification Act definition of “rural,” and for-profit and nonprofit entities that are owned, operated or controlled by, or provide significant benefits to certain members of CFC. RTFC is a taxable Subchapter T member-owned cooperative association. RTFC’s principal purpose is to provide financing to its rural telecommunications members and their affiliates. See “Item 1. Business” in our 2023 Form 10-K for additional information on the business structure, principal purpose, members and core business activities of each of these entities. Unless stated otherwise, references to “we,” “our” or “us” relate to CFC and its consolidated entities. All references to members within this document include members, associates and affiliates of CFC and its consolidated entities, except where indicated otherwise.

The following MD&A is intended to enhance the understanding of our consolidated financial statements by providing material information that we believe is relevant in evaluating our results of operations, financial condition and liquidity and the potential impact of material known events or uncertainties that, based on management’s assessment, are reasonably likely to cause the financial information included in this Report not to be necessarily indicative of our future financial performance. Management monitors a variety of key indicators and metrics to evaluate our business performance. We discuss these key measures and factors influencing changes from period to period. Our MD&A is provided as a supplement to, and should be read in conjunction with, the unaudited consolidated financial statements included in this Report, our audited consolidated financial statements and related notes for the fiscal year ended May 31, 2023 (“fiscal year 2023”) included in our 2023 Form 10-K and additional information, including the risk factors discussed under “Item 1A. Risk Factors,” contained in our 2023 Form 10-K, as well as additional information contained elsewhere in this Report.

Our fiscal year begins on June 1 and ends on May 31. Reference to “Q2 FY2024” and “YTD FY2024” refer to three and six months ended November 30, 2023, respectively. Reference to “Q2 FY2023” and “YTD FY2023” refer to three and six months ended November 30, 2022, respectively.

| | |

| SUMMARY OF SELECTED FINANCIAL DATA |

Our reported financial results are determined in conformity with generally accepted accounting principles in the United States (“U.S. GAAP”) and are subject to period-to-period volatility due to changes in market conditions and differences in the way our financial assets and liabilities are accounted for under U.S. GAAP. Our financial assets and liabilities expose us to interest-rate risk, therefore we use derivatives, primarily interest rate swaps, to economically hedge and manage the interest-rate sensitivity mismatch between our financial assets and liabilities. We are required under U.S. GAAP to carry derivatives at fair value on our consolidated balance sheets; however, the financial assets and liabilities for which we use derivatives to economically hedge are carried at amortized cost. Changes in interest rates and the shape of the swap curve result in periodic fluctuations in the fair value of our derivatives, which may cause volatility in our earnings because we do not apply hedge accounting for our interest rate swaps. As a result, the mark-to-market changes in our interest rate swaps are recorded in earnings. The majority of our derivative portfolio consists of pay-fixed swaps with longer maturities, leading to derivative losses when interest rates decline and derivative gains when interest rates rise. This earnings volatility generally is not indicative of the underlying economics of our business, as the derivative forward fair value gains or losses recorded each period may or may not be realized over time, depending on the terms of our derivative instruments and future changes in market conditions that impact the periodic cash settlement amounts of our interest rate swaps.

Therefore, management uses non-GAAP financial measures, which we refer to as “adjusted” measures, to evaluate financial performance. Our key non-GAAP financial measures are adjusted net income, adjusted net interest income, adjusted interest expense, adjusted net interest yield, adjusted times interest earned ratio (“TIER”) and adjusted debt-to-equity ratio. The most comparable U.S. GAAP financial measures are net income, net interest income, interest expense, net interest yield, TIER and debt-to-equity ratio, respectively. The primary adjustments we make to calculate these non-GAAP financial measures consist of (i) adjusting interest expense and net interest income to include the impact of net periodic derivative cash settlements income (expense) amounts; (ii) adjusting net income, total liabilities and total equity to exclude the non-cash impact of the accounting for derivative financial instruments; (iii) adjusting total liabilities to exclude the amount that funds CFC member loans guaranteed by RUS, subordinated deferrable debt and members’ subordinated certificates; and (iv) adjusting total equity to include subordinated deferrable debt and members’ subordinated certificates and exclude cumulative derivative forward value gains and losses and accumulated other comprehensive income (“AOCI”).

We believe our non-GAAP financial measures, which should not be considered in isolation or as a substitute for measures determined in conformity with U.S. GAAP, provide meaningful information and are useful to investors because management evaluates performance based on these metrics for purposes of (i) establishing short- and long-term performance goals; (ii) budgeting and forecasting; (iii) comparing period-to-period operating results, analyzing changes in results and identifying potential trends; and (iv) making compensation decisions. In addition, certain of the financial covenants in our committed bank revolving line of credit agreements and debt indentures are based on non-GAAP financial measures, as the forward fair value gains and losses related to our interest rate swaps that are excluded from our non-GAAP financial measures do not affect our cash flows, liquidity or ability to service our debt. Our non-GAAP financial measures may not be comparable to similarly titled measures reported by other companies due to differences in the way that these measures are calculated. We provide a reconciliation of our non-GAAP adjusted measures to the most directly comparable U.S. GAAP measures in the section “Non-GAAP Financial Measures.”

Table 1 provides a summary of selected financial data and key metrics used by management in evaluating performance.

Table 1: Summary of Selected Financial Data(1)

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | |

| | | | | | | | | |

| (Dollars in thousands) | | Q2 FY2024 | | Q2 FY2023 | | Change | | YTD FY2024 | | YTD FY2023 | | Change | |

| Statements of operations | | | | | | | | | | | | | |

| Net interest income: | | | | | | | | | | | | | |

| Interest income | | $ | 388,987 | | | $ | 324,194 | | | 20 | | % | $ | 769,943 | | | $ | 631,172 | | | 22 | | % |

| Interest expense | | (323,845) | | | (245,444) | | | 32 | | | (640,126) | | | (454,912) | | | 41 | | |

| Net interest income | | 65,142 | | | 78,750 | | | (17) | | | | 129,817 | | | | 176,260 | | | (26) | | |

| Fee and other income | | 6,611 | | | 4,166 | | | 59 | | | 11,148 | | | 8,222 | | | 36 | | |

| Total revenue | | 71,753 | | | 82,916 | | | (13) | | | | 140,965 | | | | 184,482 | | | (24) | | |

| Provision for credit losses | | (628) | | | (11,628) | | | (95) | | | (1,428) | | | (15,124) | | | (91) | | |

| Derivative gains: | | | | | | | | | | | | | |

Derivative cash settlements interest income (expense)(2) | | 28,767 | | | 4,801 | | | 499 | | | 56,636 | | | (5,984) | | | ** | |

Derivative forward value gains(3) | | 78,171 | | | 141,989 | | | (45) | | | 240,189 | | | 246,361 | | | (3) | | |

| Derivative gains | | 106,938 | | | 146,790 | | | (27) | | | | 296,825 | | | 240,377 | | | 23 | | |

| Investment security gains (losses) | | 1,843 | | | (493) | | | ** | | 4,776 | | | (4,172) | | | ** | |

Operating expenses(4) | | (31,512) | | | (27,247) | | | 16 | | | (63,015) | | | (52,766) | | | 19 | | |

| Other non-interest expense | | (276) | | | (355) | | | (22) | | | (1,393) | | | (677) | | | 106 | | |

| Income before income taxes | | 148,118 | | | 189,983 | | | (22) | | | 376,730 | | | 352,120 | | | 7 | | |

| Income tax provision | | (83) | | | (219) | | | (62) | | | (411) | | | (482) | | | (15) | | |

| Net income | | $ | 148,035 | | | $ | 189,764 | | | (22) | | | $ | 376,319 | | | $ | 351,638 | | | 7 | | |

| | | | | | | | | | | | | |

| Adjusted statements of operations measures | | | | | | | | | | | | | |

| Interest income | | $ | 388,987 | | | $ | 324,194 | | | 20 | | % | $ | 769,943 | | | $ | 631,172 | | | 22 | | % |

| Interest expense | | (323,845) | | | (245,444) | | | 32 | | | (640,126) | | | (454,912) | | | 41 | | |

Include: Derivative cash settlements interest income (expense)(2) | | 28,767 | | | 4,801 | | | 499 | | | 56,636 | | | (5,984) | | | ** | |

Adjusted interest expense(5) | | (295,078) | | | (240,643) | | | 23 | | | (583,490) | | | (460,896) | | | 27 | | |

Adjusted net interest income(5) | | $ | 93,909 | | | $ | 83,551 | | | 12 | | | $ | 186,453 | | | $ | 170,276 | | | 10 | | |

| | | | | | | | | | | | | |

| Net income | | $ | 148,035 | | | $ | 189,764 | | | (22) | | | $ | 376,319 | | | $ | 351,638 | | | 7 | | |

Exclude: Derivative forward value gains(3) | | 78,171 | | | 141,989 | | | (45) | | | 240,189 | | | 246,361 | | | (3) | | |

Adjusted net income(5) | | $ | 69,864 | | | $ | 47,775 | | | 46 | | | $ | 136,130 | | | $ | 105,277 | | | 29 | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Profitability ratios | | | | | | | | | | | | | |

Times interest earned ratio (“TIER”)(6) | | 1.46 | | 1.77 | | (18) | | % | 1.59 | | 1.77 | | (10) | | % |

Adjusted TIER(5) | | 1.24 | | 1.20 | | 3 | | | 1.23 | | 1.23 | | — | | |

Net interest yield(7) | | 0.77 | % | | 0.99 | % | | (22) | | bps | 0.77 | % | | 1.12 | % | | (35) | | bps |

Adjusted net interest yield(5)(8) | | 1.12 | | | 1.05 | | | 7 | | | 1.11 | | | 1.08 | | | 3 | | |

| | | | | | | | | | | | | |

| Credit quality ratios | | | | | | | | | | | | | |

Net (recovery) charge-off rate(9) | | — | | | 0.19 | | | (19) | | bps | (0.01) | % | | 0.10 | | | (11) | | bps |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| (Dollars in thousands) | | | | | | | | November 30, 2023 | | May 31, 2023 | | Change | |

| Balance sheets | | | | | | | | | | | | | |

| Assets: | | | | | | | | | | | | | |

| Cash, cash equivalents and restricted cash | | | | | | | | $ | 139,872 | | | $ | 207,237 | | | (33) | | % |

| Time deposits | | | | | | | | 400,000 | | | — | | | ** | |

| Investment securities | | | | | | | | 416,868 | | | 510,369 | | | (18) | | |

Loans to members(10) | | | | | | | | 33,553,589 | | | 32,532,086 | | | 3 | | |

| Allowance for credit losses | | | | | | | | (55,554) | | | (53,094) | | | 5 | | |

| Loans to members, net | | | | | | | | 33,498,035 | | | 32,478,992 | | | 3 | | |

| Total assets | | | | | | | | 35,510,203 | | | 34,012,060 | | | 4 | | |

| Liabilities and equity: | | | | | | | | | | | | | |

| Short-term borrowings | | | | | | | | 5,161,583 | | | 4,546,275 | | | 14 | | |

| Long-term debt | | | | | | | | 24,640,201 | | | 23,946,548 | | | 3 | | |

| Subordinated deferrable debt | | | | | | | | 1,184,247 | | | 1,283,436 | | | (8) | | |

| Members’ subordinated certificates | | | | | | | | 1,208,819 | | | 1,223,126 | | | (1) | | |

| Total debt outstanding | | | | | | | | 32,194,850 | | | 30,999,385 | | | 4 | | |

| Total liabilities | | | | | | | | 32,614,063 | | | 31,422,811 | | | 4 | | |

| Total equity | | | | | | | | 2,896,140 | | | 2,589,249 | | | 12 | | |

| | | | | | | | | | | | | |

| Adjusted balance sheets measures | | | | | | | | | | | | | |

Adjusted total liabilities(5) | | | | | | | | $ | 30,009,747 | | | $ | 28,678,302 | | | 5 | | % |

Adjusted total equity(5) | | | | | | | | 4,705,075 | | | 4,751,712 | | | (1) | | |

Members’ equity(5) | | | | | | | | 2,275,457 | | | 2,211,092 | | | 3 | | |

| | | | | | | | | | | | | |

| Debt ratios | | | | | | | | | | | | | |

Debt-to-equity ratio(11) | | | | | | | | 11.26 | | 12.14 | | (7) | | % |

Adjusted debt-to-equity ratio(5) | | | | | | | | 6.38 | | 6.04 | | 6 | | |

Liquidity coverage ratio(12) | | | | | | | | 0.89 | | 1.03 | | (14) | | |

| | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Credit quality ratios | | | | | | | | | | | | | |

Nonperforming loans ratio(13) | | | | | | | | 0.25 | % | | 0.27 | % | | (2) | | bps |

Criticized loans ratio(14) | | | | | | | | 0.89 | | | 0.99 | | | (10) | | |

Allowance coverage ratio(15) | | | | | | | | 0.17 | | | 0.16 | | | 1 | | |

____________________________

**Calculation of percentage change is not meaningful.

(1)Certain reclassifications may have been made for prior periods to conform to the current-period presentation.

(2)Consists of net periodic contractual interest amounts on our interest rate swaps, which we refer to as derivatives cash settlements interest income (expense).

(3)Consists of derivative forward value gains (losses), which represent changes in fair value during the period, excluding net periodic contractual interest settlement amounts, attributable to derivatives not designated for hedge accounting.

(4)Consists of the total non-interest expense components (i) salaries and employee benefits and (ii) other general and administrative expenses, each of which is presented separately on the consolidated statements of operations.

(5)See “Item 7. MD&A—Non-GAAP Financial Measures” in our 2023 Form 10-K for a description of each of our non-GAAP financial measures. See the section “Non-GAAP Financial Measures” for a reconciliation of the non-GAAP financial measures presented in this Report to the most comparable U.S. GAAP financial measures.

(6)Calculated based on net income (loss) plus interest expense for the period divided by interest expense for the period.

(7)Calculated based on annualized net interest income for the period divided by average interest-earning assets for the period.

(8)Calculated based on annualized adjusted net interest income for the period divided by average interest-earning assets for the period.

(9)Calculated based on annualized net charge-offs or recoveries for the period divided by average total loans outstanding for the period.

(10)Consists of the unpaid principal balance of member loans plus unamortized deferred loan origination costs of $13 million as of both November 30, 2023 and May 31, 2023.

(11)Calculated based on total liabilities at period end divided by total equity at period end.

(12)Calculated based on available liquidity at period end, divided by the amount of maturing debt obligations over the next 12 months at period end, as of each respective date.

(13)Calculated based on total nonperforming loans at period end divided by total loans outstanding at period end.

(14)Calculated based on loans outstanding at period end to borrowers with a risk rating that falls within the criticized risk rating category, which consists of special mention, substandard and doubtful, divided by total loans outstanding at period end.

(15)Calculated based on the allowance for credit losses at period end divided by total loans outstanding at period end.

Reported Results

Net Income and TIER

The table below shows our net income and TIER for the periods presented and the variance between these periods. We provide a more detailed discussion of our reported results under the section “Consolidated Results of Operations.”

Table 2: Net Income and TIER

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| (Dollars in thousands) | | Q2 FY2024 | | Q2 FY2023 | | Change | | YTD FY2024 | | YTD FY2023 | | Change |

| Net income | | $ | 148,035 | | | $ | 189,764 | | | $ | (41,729) | | | $ | 376,319 | | | $ | 351,638 | | | $ | 24,681 | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| TIER | | 1.46 | | 1.77 | | (0.31) | | 1.59 | | 1.77 | | (0.18) |

Q2 FY2024 versus Q2 FY2023

The decrease in net income was primarily driven by:

•A decrease in derivative gains of $40 million, attributable to less pronounced increases in interest rates across the swap curve during Q2 FY2024 compared to Q2 FY2023;

•A decrease in net interest income of $14 million, attributable to a decrease in the net interest yield of 22 basis points, or 22%, to 0.77%, partially offset by an increase in average interest-earning assets of $2,105 million, or 7%; and

•An increase in operating and other non-interest expenses of $4 million;

Partially offset by:

•A reduction in the provision for credit losses of $11 million. We recorded a provision for credit losses of $1 million for Q2 FY2024, resulted primarily from an increase in the collective allowance due to loan portfolio growth. In comparison, we recorded a provision for credit losses of $12 million for Q2 FY2023, primarily driven by an increase in the asset-specific allowance for a nonperforming CFC power supply loan;

•A favorable shift from losses to gains recorded on our investment securities of $2 million, primarily due to period-to-period market fluctuations in fair value; and an increase in fee and other income of $3 million.

YTD FY2024 versus YTD FY2023

The increase in net income was primarily driven by:

•An increase in derivative gains of $56 million, primarily from an increase in the net interest rate received on our pay-fixed swaps, which drove the higher derivative cash settlements income for YTD FY2024;

•A reduction in the provision for credit losses of $14 million. We recorded a provision for credit losses of $1 million for YTD FY2024, resulted primarily from an increase in the collective allowance due to loan portfolio growth and a slight decline in the overall credit quality and risk profile of our loan portfolio. In comparison, we recorded a provision for credit losses of $15 million for YTD FY2023, driven primarily by an increase in the asset-specific allowance for a nonperforming CFC power supply loan as discussed above;

•A favorable shift from losses to gains recorded on our investment securities of $9 million, primarily due to period-to-period market fluctuations in fair value; and an increase in fee and other income of $3 million;

Partially offset by:

•A decrease in net interest income of $46 million, attributable to a decrease in the net interest yield of 35 basis points, or 31%, to 0.77%, partially offset by an increase in average interest-earning assets of $2,226 million, or 7%; and

•An increase in operating and other non-interest expenses of $11 million.

The decrease in TIER for Q2 FY2024 and YTD FY2024, compared to Q2 FY2023 and YTD FY2023, was primarily driven by increased interest expense during Q2 FY2024 and YTD FY2024.

Debt-to-Equity Ratio

Our debt-to-equity ratio decreased to 11.26 as of November 30, 2023, from 12.14 as of May 31, 2023, primarily due to an increase in equity resulting from our reported net income of $376 million for YTD FY2024, which was partially offset by a decrease in equity attributable to the CFC Board of Directors’ authorized patronage capital retirement in July 2023 of $72 million.

Non-GAAP Adjusted Results

Adjusted Net Income and Adjusted TIER

The table below shows our adjusted net income and adjusted TIER for the periods presented and the variance between these periods. Our financial goals focus on earning an annual minimum adjusted TIER of 1.10. We provide a more detailed discussion of our non-GAAP adjusted results under the section “Consolidated Results of Operations.”

Table 3: Adjusted Net Income and Adjusted TIER

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| (Dollars in thousands) | | Q2 FY2024 | | Q2 FY2023 | | Change | | YTD FY2024 | | YTD FY2023 | | Change |

| Adjusted Net income | | $ | 69,864 | | | $ | 47,775 | | | $ | 22,089 | | | $ | 136,130 | | | $ | 105,277 | | | $ | 30,853 | |

| Adjusted TIER | | 1.24 | | 1.20 | | 0.04 | | 1.23 | | 1.23 | | 0.00 |

Q2 FY2024 versus Q2 FY2023

The increase in adjusted net income was primarily driven by:

•An increase in adjusted net interest income of $10 million, driven by the combined impact of an increase in average interest-earning assets of $2,105 million, or 7%, and an increase in the adjusted net interest yield of 7 basis points, or 7%, to 1.12%;

•A reduction in the provision for credit losses of $11 million;

•A favorable shift from losses to gains recorded on our investment securities of $2 million; and an increase in fee and other income of $3 million;

Partially offset by:

•An increase in operating and other non-interest expenses of $4 million.

YTD FY2024 versus YTD FY2023

The increase in adjusted net income was primarily driven by:

•An increase in adjusted net interest income of $16 million, driven by the combined impact of an increase in average interest-earning assets of $2,226 million, or 7%, and an increase in the adjusted net interest yield of 3 basis points, or 3%, to 1.11%;

•A reduction in the provision for credit losses of $14 million;

•A favorable shift from losses to gains recorded on our investment securities of $9 million; and an increase in fee and other income of $3 million;

Partially offset by:

•An increase in operating and other non-interest expenses of $11 million.

Adjusted Debt-to-Equity Ratio

Our financial goals focus on maintaining an adjusted debt-to-equity ratio at approximately 6-to-1 or below. The adjusted debt-to-equity ratio increased to 6.38 as of November 30, 2023 from 6.04 as of May 31, 2023, due to the combined impact

of an increase in adjusted liabilities resulting from additional borrowings to fund growth in our loan portfolio and a decrease in adjusted equity. The decrease in adjusted equity was primarily due to the early redemption during YTD FY2024 of $100 million of our $400 million subordinated deferrable debt due 2043 and the CFC Board of Directors’ authorized patronage capital retirement in July 2023, partially offset by our adjusted net income for YTD FY2024.

Lending and Credit Quality

Loans to members totaled $33,554 million as of November 30, 2023, an increase of $1,022 million, or 3%, from May 31, 2023, reflecting net increases in long-term and line of credit loans of $853 million and $169 million, respectively. Our loan portfolio composition remained largely unchanged from May 31, 2023 with 77% of loans outstanding to CFC distribution borrowers, 17% to CFC power supply borrowers, and 2% to RTFC borrowers as of November 30, 2023.

We believe the overall credit quality of our loan portfolio remained strong as of November 30, 2023. We had no loan charge-offs during Q2 FY2024 and YTD FY2024. We recorded a $1 million loan recovery to previously charged-off loan amounts during the three months ended August 31, 2023 (“Q1 FY2024”), which resulted in an annualized net recovery rate of 0.01% for YTD FY2024. In comparison, we experienced charge-offs totaling $15 million during Q2 FY2023 and YTD FY2023, which resulted in an annualized net charge-off rate of 0.19% and 0.10% for Q2 FY2023 and YTD FY2023, respectively.

We had one loan totaling $85 million classified as nonperforming as of November 30, 2023. In comparison, we had two loans totaling $89 million classified as nonperforming as of May 31, 2023. The reduction was due to the receipt of $4 million in payments for a nonperforming loan.

Our allowance for credit losses and allowance coverage ratio increased to $56 million and 0.17%, respectively, as of November 30, 2023, from $53 million and 0.16%, respectively, as of May 31, 2023. The $3 million increase in the allowance for credit losses reflected an increase in the collective allowance of $4 million, partially offset by a reduction in the asset-specific allowance of $1 million.

Financing and Liquidity

Total debt outstanding increased $1,195 million, or 4%, to $32,195 million as of November 30, 2023, primarily due to borrowings to fund the increase in loans to members. Outstanding dealer commercial paper of $1,039 million as of November 30, 2023 was within our quarter-end target range of $1,000 million to $1,500 million.

In September 2023 and December 2023, Fitch Ratings (“Fitch”) and S&P Global Inc.(“S&P”), respectively, affirmed CFC’s credit ratings and stable outlook.

Our available liquidity consists of cash and cash equivalents, time deposits, investments in debt securities and availability under committed bank revolving line of credit agreements, committed loan facilities under the USDA Guaranteed Underwriter Program (“Guaranteed Underwriter Program”), and a revolving note purchase agreement with the Federal Agricultural Mortgage Corporation (“Farmer Mac”). As of November 30, 2023, our available liquidity totaled $6,556 million and was $824 million below our total scheduled debt obligations over the next 12 months of $7,380 million. In addition to our existing available liquidity, we expect to receive $1,516 million from scheduled long-term loan principal payments over the next 12 months. Subsequent to November 30, 2023, we closed on a $450 million Series U committed loan facility from the U.S. Treasury Department’s Federal Financing Bank under the Guaranteed Underwriter Program, resulting in an increase of the total availability under the Guaranteed Underwriter Program from $750 million as of November 30, 2023 to $1,200 million as of the date of this Report.

We believe we can continue to roll over our member short-term investments of $3,623 million based on our expectation that our members will continue to reinvest their excess cash primarily in short-term investment products offered by CFC. Our members historically have maintained a relatively stable level of short-term investments in CFC. Member short-term investments in CFC have averaged $3,589 million over the last 12 fiscal quarter-end reporting periods. Our available liquidity as of November 30, 2023 was $2,799 million in excess of, or 1.7 times over, our total scheduled debt obligations, excluding member short-term investments, over the next 12 months of $3,757 million.

RTFC and NCSC Consolidation

In April 2023 and June 2023, RTFC’s and NCSC’s members, respectively, approved the sale of RTFC’s business to NCSC. In October 2023, as part of the consolidation process between RTFC and NCSC, the Board of Directors approved the early retirement of allocated but unretired patronage capital at a discounted amount of $51 million, which was returned in cash to RTFC’s members in January 2024. In addition, on October 26, 2023, we early redeemed at par $12 million of members’ subordinated certificates, as approved by CFC’s and RTFC’s Board of Directors. The consolidation of RTFC and NCSC was finalized on December 1, 2023. We accounted for the transaction pursuant to ASC 805-50 “Transactions between Entities under Common Control.”

Outlook

As further described below in the “Liquidity Risk—Projected Near-Term Sources and Uses of Funds” section, we currently anticipate net long-term loan growth of $1,763 million over the next 12 months. We also expect that our variable-rate line of credit loans outstanding will remain at an elevated level over the same period.

In December 2023, the Federal Open Market Committee (“FOMC”) of the Federal Reserve signaled the expectation of no additional increases in the federal funds rate and pointed to a target rate of 5.4% by December 31, 2023. The FOMC expects a slowdown in the U.S. economy in 2024, with the median projected Gross Domestic Product (“GDP”) growth rate at 1.4% in 2024. In addition, the Federal Reserve expects that inflation will continue to remain above the 2% long-term target in 2024. As such, the FOMC projects federal funds rate cuts in 2024, bringing the target rate to 4.6% by December 31, 2024. Consensus market outlook for interest rates indicates declining interest rates across the yield curve in 2024. Although the yield curve is expected to remain inverted throughout 2024, given the expected drop in short-term interest rates, the yield curve inversion is expected to narrow in 2024.

Projected Reported Results

Based on our current forecast assumptions, including the yield curve forecast noted above, we project:

•A decrease in our reported net interest income and reported net interest yield over the next 12 months compared to the 12-month period ended November 30, 2023. See “Market Risk—Interest Rate Risk Assessment” for an additional discussion.

Projected Non-GAAP Adjusted Results

Based on our current forecast assumptions, including the yield curve forecast noted above, we project:

•A decrease in our adjusted net interest income and adjusted net interest yield over the next 12 months relative to the 12-month period ended November 30, 2023, primarily due to the current yield curve assumptions and our balance sheet position. See “Market Risk—Interest Rate Risk Assessment” for an additional discussion.

•A decrease in our adjusted net income and adjusted TIER over the next 12 months, primarily attributable to increased operating expenses and a projected decrease in adjusted net interest income.

•Our adjusted debt-to-equity ratio will remain above our target of 6-to-1, primarily due to the projected increase in total debt outstanding to fund anticipated growth in our loan portfolio and the early retirement of patronage capital as discussed above.

As stated above, we exclude the impact of unrealized derivative forward fair value gains and losses from our non-GAAP financial measures. As the majority of our swaps are long-term with an average remaining life of approximately 14 years as of November 30, 2023, the unrealized periodic derivative forward value gains and losses are largely based on future expected changes in longer-term interest rates, which we are unable to accurately predict for each reporting period over the next 12 months. Due to the difficulty in predicting these unrealized amounts, we are unable to provide without unreasonable effort a reconciliation of our forward-looking adjusted financial measures to the most directly comparable GAAP financial measures.

| | |

| CRITICAL ACCOUNTING ESTIMATES |

The preparation of financial statements in conformity with U.S. GAAP requires management to make a number of judgments, estimates and assumptions that affect the reported amount of assets, liabilities, income and expenses in our consolidated financial statements. Understanding our accounting policies and the extent to which we use management’s judgment and estimates in applying these policies is integral to understanding our financial statements. We provide a discussion of our significant accounting policies in “Note 1—Summary of Significant Accounting Policies” in our 2023 Form 10-K.

Certain accounting estimates are considered critical because they involve significant judgments and assumptions about highly complex and inherently uncertain matters, and the use of reasonably different estimates and assumptions could have a material impact on our results of operations or financial condition. The determination of the allowance for expected credit losses over the remaining expected life of the loans in our loan portfolio involves a significant degree of management judgment and level of estimation uncertainty. As such, we have identified our accounting policy governing the estimation of the allowance for credit losses as a critical accounting estimate. We describe our allowance methodology and process for estimating the allowance for credit losses under “Note 1—Summary of Significant Accounting Policies—Allowance for Credit Losses–Loan Portfolio—Current Methodology” in our 2023 Form 10-K.

We identify the key inputs used in determining the allowance for credit losses, discuss the assumptions that require the most significant management judgment and contribute to the estimation uncertainty and disclose the sensitivity of our allowance to hypothetical changes in the assumptions underlying the calculation of our reported allowance for credit losses under “Item 7. MD&A—Critical Accounting Estimates” in our 2023 Form 10-K. Management established policies and control procedures intended to ensure that the methodology used for determining our allowance for credit losses, including any judgments and assumptions made as part of such method, are well-controlled and applied consistently from period to period. We regularly evaluate the key inputs and assumptions used in determining the allowance for credit losses and update them, as necessary, to better reflect present conditions, including current trends in credit performance and borrower risk profile, portfolio concentration risk, changes in risk-management practices, changes in the regulatory environment and other factors relevant to our loan portfolio segments. We did not change our allowance methodology or the nature of the underlying key inputs and assumptions used in measuring our allowance for credit losses during the current quarter.

We discuss the risks and uncertainties related to management’s judgments and estimates in applying accounting policies that have been identified as critical accounting estimates under “Item 1A. Risk Factors—Regulatory and Compliance Risks” in our 2023 Form 10-K. We provide additional information on the allowance for credit losses under the section “Credit Risk—Allowance for Credit Losses” and “Note 5—Allowance for Credit Losses” in this Report.

| | |

| RECENT ACCOUNTING CHANGES AND OTHER DEVELOPMENTS |

Recent Accounting Changes

We provide information on recently adopted accounting standards and the adoption impact on CFC’s consolidated financial statements and recently issued accounting standards not yet required to be adopted and the expected adoption impact in “Note 1—Summary of Significant Accounting Policies.” To the extent we believe the adoption of new accounting standards has had or will have a material impact on our consolidated results of operations, financial condition or liquidity, we discuss the impact in the applicable section(s) of this MD&A.

| | |

| CONSOLIDATED RESULTS OF OPERATIONS |

This section provides a comparative discussion of our consolidated results of operations between Q2 FY2024 and Q2 FY2023, and between YTD FY2024 and YTD FY2023. Following this section, we provide a discussion and analysis of material changes between amounts reported on our consolidated balance sheets as of November 30, 2023 and May 31, 2023. You should read these sections together with our “Executive Summary—Outlook” where we discuss trends and other factors that we expect will affect our future results of operations.

Net Interest Income

Net interest income, which is our largest source of revenue, represents the difference between the interest income earned on our interest-earning assets and the interest expense on our interest-bearing liabilities. Our net interest yield represents the difference between the yield on our interest-earning assets and the cost of our interest-bearing liabilities plus the impact of non-interest bearing funding. We expect net interest income and our net interest yield to fluctuate based on changes in interest rates and changes in the amount and composition of our interest-earning assets and interest-bearing liabilities. We do not fund each individual loan with specific debt. Rather, we attempt to minimize costs and maximize efficiency by proportionately funding large aggregated amounts of loans.

Table 4 presents average balances for each major category of our interest-earning assets and interest-bearing liabilities, the interest income earned or interest expense incurred, and the average yield or cost. Table 4 also presents non-GAAP adjusted interest expense, adjusted net interest income and adjusted net interest yield, which reflect the inclusion of net accrued periodic derivative cash settlements expense in interest expense. We provide reconciliations of our non-GAAP financial measures to the most comparable U.S. GAAP financial measures under “Non-GAAP Financial Measures.”

Table 4: Average Balances, Interest Income/Interest Expense and Average Yield/Cost

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | |

| | |

| | Q2 FY2024 | | Q2 FY2023 |

| (Dollars in thousands) | | Average Balance | | Interest Income/Expense | | Average Yield/Cost | | Average Balance | | Interest Income/Expense | | Average Yield/Cost |

| Assets: | | | | | | | | | | | | |

Long-term fixed-rate loans(1) | | $ | 29,073,023 | | | $ | 311,085 | | | 4.30 | % | | $ | 27,545,890 | | | $ | 280,767 | | | 4.09 | % |

| Long-term variable-rate loans | | 900,860 | | | 16,069 | | | 7.17 | | | 823,877 | | | 9,446 | | | 4.60 | |

| Line of credit loans | | 3,159,822 | | | 55,277 | | | 7.04 | | | 2,601,805 | | | 29,001 | | | 4.47 | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

Other, net(2) | | — | | | (421) | | | — | | | — | | | (377) | | | — | |

| Total loans | | 33,133,705 | | | 382,010 | | | 4.64 | | | 30,971,572 | | | 318,837 | | | 4.13 | |

| Cash, time deposits and investment securities | | 737,768 | | | 6,977 | | | 3.80 | | | 794,794 | | | 5,357 | | | 2.70 | |

| Total interest-earning assets | | $ | 33,871,473 | | | $ | 388,987 | | | 4.62 | % | | $ | 31,766,366 | | | $ | 324,194 | | | 4.09 | % |

Other assets, less allowance for credit losses(3) | | 1,183,985 | | | | | | | 1,080,049 | | | | | |

Total assets(3) | | $ | 35,055,458 | | | | | | | $ | 32,846,415 | | | | | |

| | | | | | | | | | | | |

| Liabilities: | | | | | | | | | | | | |

| Commercial paper | | $ | 2,195,063 | | | $ | 30,045 | | | 5.51 | % | | $ | 2,901,962 | | | $ | 24,179 | | | 3.34 | % |

| Other short-term borrowings | | 1,938,120 | | | 25,455 | | | 5.28 | | | 2,262,768 | | | 17,007 | | | 3.01 | |

Short-term borrowings(4) | | 4,133,183 | | | 55,500 | | | 5.40 | | | 5,164,730 | | | 41,186 | | | 3.20 | |

| Medium-term notes | | 7,107,642 | | | 69,729 | | | 3.95 | | | 5,689,824 | | | 41,506 | | | 2.93 | |

| Collateral trust bonds | | 7,511,666 | | | 71,401 | | | 3.82 | | | 7,366,514 | | | 66,995 | | | 3.65 | |

| Guaranteed Underwriter Program notes payable | | 6,841,030 | | | 54,370 | | | 3.20 | | | 6,247,517 | | | 44,634 | | | 2.87 | |

| Farmer Mac notes payable | | 3,667,605 | | | 39,479 | | | 4.33 | | | 3,028,920 | | | 24,757 | | | 3.28 | |

| Other notes payable | | 2,460 | | | 26 | | | 4.25 | | | 4,748 | | | 29 | | | 2.45 | |

| Subordinated deferrable debt | | 1,184,215 | | | 19,972 | | | 6.78 | | | 986,590 | | | 12,887 | | | 5.24 | |

| Subordinated certificates | | 1,216,459 | | | 13,368 | | | 4.42 | | | 1,237,156 | | | 13,450 | | | 4.36 | |

| Total interest-bearing liabilities | | $ | 31,664,260 | | | $ | 323,845 | | | 4.11 | % | | $ | 29,725,999 | | | $ | 245,444 | | | 3.31 | % |

Other liabilities(3) | | 569,541 | | | | | | | 794,873 | | | | | |

Total liabilities(3) | | 32,233,801 | | | | | | | 30,520,872 | | | | | |

Total equity(3) | | 2,821,657 | | | | | | | 2,325,543 | | | | | |

Total liabilities and equity(3) | | $ | 35,055,458 | | | | | | | $ | 32,846,415 | | | | | |

Net interest spread(5) | | | | | | 0.51 | % | | | | | | 0.78 | % |

Impact of non-interest bearing funding(6) | | | | | | 0.26 | | | | | | | 0.21 | |

Net interest income/net interest yield(7) | | | | $ | 65,142 | | | 0.77 | % | | | | $ | 78,750 | | | 0.99 | % |

| | | | | | | | | | | | |

| Adjusted net interest income/adjusted net interest yield: | | | | | | | | | | | | |

| Interest income | | | | $ | 388,987 | | | 4.62 | % | | | | $ | 324,194 | | | 4.09 | % |

| Interest expense | | | | 323,845 | | | 4.11 | | | | | 245,444 | | | 3.31 | |

Add: Net periodic derivative cash settlements interest income(8) | | | | (28,767) | | | (1.49) | | | | | (4,801) | | | (0.25) | |

Adjusted interest expense/adjusted average cost(9) | | | | $ | 295,078 | | | 3.75 | % | | | | $ | 240,643 | | | 3.25 | % |

Adjusted net interest spread(7) | | | | | | 0.87 | | | | | | | 0.84 | |

Impact of non-interest bearing funding(6) | | | | | | 0.25 | | | | | | | 0.21 | |

Adjusted net interest income/adjusted net interest yield(10) | | | | $ | 93,909 | | | 1.12 | % | | | | $ | 83,551 | | | 1.05 | % |

| | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | |

| | YTD FY2024 | | YTD FY2023 |

| (Dollars in thousands) | | Average Balance | | Interest Income/Expense | | Average Yield/Cost | | Average Balance | | Interest Income/Expense | | Average Yield/Cost |

| Assets: | | | | | | | | | | | | |

Long-term fixed-rate loans(1) | | $ | 28,840,684 | | | $ | 612,788 | | | 4.25 | % | | $ | 27,399,733 | | | $ | 557,070 | | | 4.06 | % |

| Long-term variable-rate loans | | 957,159 | | | 33,821 | | | 7.07 | | | 791,958 | | | 16,317 | | | 4.11 | |

| Line of credit loans | | 3,215,388 | | | 111,791 | | | 6.95 | | | 2,498,021 | | | 48,880 | | | 3.90 | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

Other, net(2) | | — | | | (822) | | | — | | | — | | | (750) | | | — | |

| Total loans | | 33,013,231 | | | 757,578 | | | 4.59 | | | 30,689,712 | | | 621,517 | | | 4.04 | |

| Cash, time deposits and investment securities | | 690,808 | | | 12,365 | | | 3.58 | | | 788,413 | | | 9,655 | | | 2.44 | |

| Total interest-earning assets | | $ | 33,704,039 | | | $ | 769,943 | | | 4.57 | % | | $ | 31,478,125 | | | $ | 631,172 | | | 4.00 | % |

Other assets, less allowance for credit losses(3) | | 1,077,071 | | | | | | | 887,210 | | | | | |

Total assets(3) | | $ | 34,781,110 | | | | | | | $ | 32,365,335 | | | | | |

| | | | | | | | | | | | |

| Liabilities: | | | | | | | | | | | | |

| Commercial paper | | $ | 2,262,175 | | | $ | 61,575 | | | 5.44 | % | | $ | 2,878,740 | | | $ | 38,792 | | | 2.69 | % |

| Other short-term borrowings | | 1,911,555 | | | 49,374 | | | 5.17 | | | 2,216,736 | | | 26,603 | | | 2.39 | |

Short-term borrowings(4) | | 4,173,730 | | | 110,949 | | | 5.32 | | | 5,095,476 | | | $ | 65,395 | | | 2.56 | |

| Medium-term notes | | 7,075,343 | | | 137,871 | | | 3.90 | | | 5,779,703 | | | 77,421 | | | 2.67 | |

| Collateral trust bonds | | 7,545,732 | | | 143,350 | | | 3.80 | | | 7,139,270 | | | 128,562 | | | 3.59 | |

| Guaranteed Underwriter Program notes payable | | 6,767,814 | | | 106,900 | | | 3.16 | | | 6,166,294 | | | 86,630 | | | 2.80 | |

| Farmer Mac notes payable | | 3,505,531 | | | 73,762 | | | 4.21 | | | 3,018,163 | | | 44,132 | | | 2.92 | |

| Other notes payable | | 2,139 | | | 44 | | | 4.11 | | | 4,732 | | | 57 | | | 2.40 | |

| Subordinated deferrable debt | | 1,197,737 | | | 40,420 | | | 6.75 | | | 986,563 | | | 25,775 | | | 5.21 | |

| Subordinated certificates | | 1,219,363 | | | 26,830 | | | 4.40 | | | 1,235,497 | | | 26,940 | | | 4.35 | |

| Total interest-bearing liabilities | | $ | 31,487,389 | | | $ | 640,126 | | | 4.07 | % | | $ | 29,425,698 | | | $ | 454,912 | | | 3.08 | % |

Other liabilities(3) | | 563,475 | | | | | | | 688,239 | | | | | |

Total liabilities(3) | | 32,050,864 | | | | | | | 30,113,937 | | | | | |

Total equity(3) | | 2,730,246 | | | | | | | 2,251,398 | | | | | |

Total liabilities and equity(3) | | $ | 34,781,110 | | | | | | | $ | 32,365,335 | | | | | |

Net interest spread(5) | | | | | | 0.50 | % | | | | | | 0.92 | % |

Impact of non-interest bearing funding(6) | | | | | | 0.27 | | | | | | | 0.20 | |

Net interest income/net interest yield(7) | | | | $ | 129,817 | | | 0.77 | % | | | | $ | 176,260 | | | 1.12 | % |

| | | | | | | | | | | | |

| Adjusted net interest income/adjusted net interest yield: | | | | | | | | | | | | |

| Interest income | | | | $ | 769,943 | | | 4.57 | % | | | | $ | 631,172 | | | 4.00 | % |

| Interest expense | | | | 640,126 | | | 4.07 | | | | | 454,912 | | | 3.08 | |

Add: Net periodic derivative cash settlements interest (income) expense(8) | | | | (56,636) | | | (1.47) | | | | | 5,984 | | | 0.15 | |

Adjusted interest expense/adjusted average cost(9) | | | | $ | 583,490 | | | 3.71 | % | | | | $ | 460,896 | | | 3.12 | % |

Adjusted net interest spread(7) | | | | | | 0.86 | | | | | | | 0.88 | |

Impact of non-interest bearing funding(6) | | | | | | 0.25 | | | | | | | 0.20 | |

Adjusted net interest income/adjusted net interest yield(10) | | | | $ | 186,453 | | | 1.11 | % | | | | $ | 170,276 | | | 1.08 | % |

___________________________

(1)Interest income on long-term, fixed-rate loans includes loan conversion fees, which are generally deferred and recognized as interest income using the effective interest method.

(2)Consists of late payment fees and net amortization of deferred loan fees and loan origination costs.

(3)The average balance represents average monthly balances, which is calculated based on the month-end balance as of the beginning of the reporting period and the balances as of the end of each month included in the specified reporting period.

(4)Short-term borrowings reported on our consolidated balance sheets consist of borrowings with an original contractual maturity of one year or less. However, short-term borrowings presented in Table 2 consist of commercial paper, select notes, daily liquidity fund notes and secured borrowings under repurchase agreements. Short-term borrowings presented on our consolidated balance sheets related to medium-term notes, Farmer Mac notes payable and other notes payable are reported in the respective category for presentation purposes in Table 4. The period-end amounts reported as short-term borrowings on our consolidated balances sheets, which are excluded from the calculation of average short-term borrowings presented in Table 4, totaled $907 million and $398 million as of November 30, 2023 and 2022, respectively.

(5)Net interest spread represents the difference between the average yield on total average interest-earning assets and the average cost of total average interest-bearing liabilities. Adjusted net interest spread represents the difference between the average yield on total average interest-earning assets and the adjusted average cost of total average interest-bearing liabilities.

(6)Includes other liabilities and equity.

(7)Net interest yield is calculated based on annualized net interest income for the period divided by total average interest-earning assets for the period.

(8)Represents the impact of net periodic contractual interest amounts on our interest rate swaps during the period. This amount is added to interest expense to derive non-GAAP adjusted interest expense. The average (benefit)/cost associated with derivatives is calculated based on the annualized net periodic swap settlement interest amount during the period divided by the average outstanding notional amount of derivatives during the period. The average outstanding notional amount of interest rate swaps was $7,743 million and $7,753 million for Q2 FY2024 and Q2 FY2023, respectively. The average outstanding notional amount of interest rate swaps was $7,729 million and $7,864 million for the YTD FY2024 and YTD FY2023, respectively.

(9)Adjusted interest expense consists of interest expense plus net periodic derivative cash settlements interest income (expense) during the period. Net periodic derivative cash settlements interest income (expense) is reported on our consolidated statements of operations as a component of derivative gains (losses). Adjusted average cost is calculated based on annualized adjusted interest expense for the period divided by total average interest-bearing liabilities during the period.

(10)Adjusted net interest yield is calculated based on annualized adjusted net interest income for the period divided by total average interest-earning assets for the period.

Table 5 displays the change in net interest income between periods and the extent to which the variance for each category of interest-earning assets and interest-bearing liabilities is attributable to: (i) changes in volume, which represents the change in the average balances of our interest-earning assets and interest-bearing liabilities or volume and (ii) changes in the rate, which represents the change in the average interest rates of these assets and liabilities. The table also presents the change in adjusted net interest income between periods.

Table 5: Rate/Volume Analysis of Changes in Interest Income/Interest Expense

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | |

| | Q2 FY2024 | | versus | | Q2 FY2023 | | YTD FY2024 | | versus | | YTD FY2023 |

| | | Total | | Variance Due To:(1) | | Total | | Variance Due To:(1) |

| (Dollars in thousands) | | Variance | | Volume | | Rate | | Variance | | Volume | | Rate |

| Interest income: | | | | | | | | | | | | |

| Long-term fixed-rate loans | | $ | 30,318 | | | $ | 14,756 | | | $ | 15,562 | | | $ | 55,718 | | | $ | 27,694 | | | $ | 28,024 | |

| Long-term variable-rate loans | | 6,623 | | | 854 | | | 5,769 | | | 17,504 | | | 3,350 | | | 14,154 | |

| Line of credit loans | | 26,276 | | | 6,124 | | | 20,152 | | | 62,911 | | | 13,865 | | | 49,046 | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| Other, net | | (44) | | | — | | | (44) | | | (72) | | | — | | | (72) | |

| Total loans | | 63,173 | | | 21,734 | | | 41,439 | | | 136,061 | | | 44,909 | | | 91,152 | |

| Cash, time deposits and investment securities | | 1,620 | | | (398) | | | 2,018 | | | 2,710 | | | (1,218) | | | 3,928 | |

| Total interest income | | 64,793 | | | 21,336 | | | 43,457 | | | 138,771 | | | 43,691 | | | 95,080 | |

| | | | | | | | | | | | |

| Interest expense: | | | | | | | | | | | | |

| Commercial paper | | 5,866 | | | (5,940) | | | 11,806 | | | 22,783 | | | (8,392) | | | 31,175 | |

| Other short-term borrowings | | 8,448 | | | (2,480) | | | 10,928 | | | 22,771 | | | (3,725) | | | 26,496 | |

| Short-term borrowings | | 14,314 | | | (8,420) | | | 22,734 | | | 45,554 | | | (12,117) | | | 57,671 | |

| Medium-term notes | | 28,223 | | | 10,201 | | | 18,022 | | | 60,450 | | | 17,097 | | | 43,353 | |

| Collateral trust bonds | | 4,406 | | | 1,133 | | | 3,273 | | | 14,788 | | | 6,948 | | | 7,840 | |

| Guaranteed Underwriter Program notes payable | | 9,736 | | | 4,107 | | | 5,629 | | | 20,270 | | | 8,191 | | | 12,079 | |

| Farmer Mac notes payable | | 14,722 | | | 5,138 | | | 9,584 | | | 29,630 | | | 6,986 | | | 22,644 | |

| Other notes payable | | (3) | | | (14) | | | 11 | | | (13) | | | (31) | | | 18 | |

| Subordinated deferrable debt | | 7,085 | | | 2,539 | | | 4,546 | | | 14,645 | | | 5,432 | | | 9,213 | |

| Subordinated certificates | | (82) | | | (261) | | | 179 | | | (110) | | | (424) | | | 314 | |

| Total interest expense | | 78,401 | | | 14,423 | | | 63,978 | | | 185,214 | | | 32,082 | | | 153,132 | |

| Net interest income (expense) | | $ | (13,608) | | | $ | 6,913 | | | $ | (20,521) | | | $ | (46,443) | | | $ | 11,609 | | | $ | (58,052) | |

| | | | | | | | | | | | |

| Adjusted net interest income: | | | | | | | | | | | | |

| Interest income | | $ | 64,793 | | | $ | 21,336 | | | $ | 43,457 | | | $ | 138,771 | | | $ | 43,691 | | | $ | 95,080 | |

| Interest expense | | 78,401 | | | 14,423 | | | 63,978 | | | 185,214 | | | 32,082 | | | 153,132 | |

Net periodic derivative cash settlements interest expense (income)(2) | | (23,966) | | | 20 | | | (23,986) | | | (62,620) | | | (119) | | | (62,501) | |

Adjusted interest expense(3) | | 54,435 | | | 14,443 | | | 39,992 | | | 122,594 | | | 31,963 | | | 90,631 | |

| Adjusted net interest income | | $ | 10,358 | | | $ | 6,893 | | | $ | 3,465 | | | $ | 16,177 | | | $ | 11,728 | | | $ | 4,449 | |

____________________________

(1)The changes for each category of interest income and interest expense represent changes in either average balances (volume) or average rates for both interest-earning assets and interest-bearing liabilities. We allocate the amount attributable to the combined impact of volume and rate to the rate variance.

(2)For the net periodic derivative cash settlements interest amount, the variance due to average volume represents the change in the net periodic derivative cash settlements interest amount resulting from the change in the average notional amount of derivative contracts outstanding. The variance due to average rate represents the change in the net periodic derivative cash settlements amount resulting from the net difference between the average rate paid and the average rate received for interest rate swaps during the period.

(3)See “Non-GAAP Financial Measures” for additional information on our adjusted non-GAAP financial measures.

Reported Net Interest Income

Reported net interest income of $65 million for Q2 FY2024 decreased $14 million, or 17%, from Q2 FY2023, driven by a decrease in the net interest yield of 22 basis points, or 22%, to 0.77%, partially offset by an increase in average interest-earning assets of $2,105 million, or 7%.

•Average Interest-Earning Assets: The increase in average interest-earning assets of 7% was attributable to growth in average total loans of $2,162 million, or 7%, driven primarily by an increase in average long-term fixed-rate loans of $1,527 million and an increase in average line of credit loans of $558 million, as members continued to advance loans to fund capital expenditures and for working capital purposes.

•Net Interest Yield: The decrease in the net interest yield of 22 basis points, or 22%, was primarily attributable to the combined impact of an increase in our average cost of borrowings of 80 basis points to 4.11%, which was partially offset by an increase in the average yield on interest-earning assets of 53 basis points to 4.62% and an increase in the benefit from non-interest bearing funding of 5 basis points to 0.26%. Our average yield on interest-earning assets and average cost of borrowings rose mainly due to the sustained increase in the federal funds rate, which increased 150 basis points since November 30, 2022. The increase in average yields on line of credit and variable-rate loans was the primary driver for the increase in the average yield on interest-earning assets. Meanwhile, our average cost of borrowings increased due to higher interest rates on our short-term and variable-rate borrowings.

Reported net interest income of $130 million for YTD FY2024 decreased $46 million, or 26%, from YTD FY2023, driven by a decrease in the net interest yield of 35 basis points, or 31%, to 0.77%, partially offset by an increase in average interest-earning assets of $2,226 million, or 7%.

• Average Interest-Earning Assets: The increase in average interest-earning assets of 7% was attributable to growth in average total loans of $2,324 million, or 8%, driven primarily by an increase in average long-term fixed-rate loans of $1,441 million and an increase in average line of credit loans of $717 million, as members continued to advance loans to fund capital expenditures and for working capital purposes.

• Net Interest Yield: The decrease in the net interest yield of 35 basis points, or 31%, was primarily attributable to the combined impact of an increase in our average cost of borrowings of 99 basis points to 4.07%, which was partially offset by an increase in the average yield on interest-earning assets of 57 basis points to 4.57% and an increase in the benefit from non-interest bearing funding of 7 basis points to 0.27%. As mentioned above, the increases in the average cost of borrowings and average yield on interest-earning assets were driven by the continued increase in the federal funds rate.

Adjusted Net Interest Income

Adjusted net interest income of $94 million for Q2 FY2024 increased $10 million, or 12%, from Q2 FY2023, driven by the combined impact of an increase in average interest-earning assets of $2,105 million, or 7%, and an increase in the adjusted net interest yield of 7 basis points, or 7%, to 1.12%.

•Average Interest-Earning Assets: The increase in average interest-earning assets of 7% during Q2 FY2024 was driven by the growth in average total loans of $2,162 million, or 7%, attributable primarily to the increases in average long-term fixed-rate and line of credit loans as discussed above.

•Adjusted Net Interest Yield: The adjusted net interest yield increased to 1.12%, reflecting the combined impact of an increase in the average yield on interest-earning assets of 53 basis points to 4.62% and an increase in the benefit from non-interest bearing funding of 4 basis points to 0.25%, partially offset by an increase in our adjusted average cost of borrowings of 50 basis points to 3.75%, The increases in both average yield on interest-earning assets and adjusted average cost of borrowings were attributable to the continued high interest-rate environment since November 30, 2022, as discussed above.

Adjusted net interest income of $186 million for YTD FY2024 increased $16 million, or 10%, from YTD FY2023, driven by the combined impact of an increase in average interest-earning assets of $2,226 million, or 7%, and an increase in the adjusted net interest yield of 3 basis points, or 3%, to 1.11%.

•Average Interest-Earning Assets: The increase in average interest-earning assets of 7% during YTD FY2024 was driven by the growth in average total loans of $2,324 million, or 8%, attributable primarily to increases in average long-term fixed-rate and line of credit loans as discussed above.

•Adjusted Net Interest Yield: The increase in the adjusted net interest yield of 3 basis points, or 3%, reflected the combined impact of an increase in the average yield on interest-earning assets of 57 basis points to 4.57% and an increase in the benefit from non-interest bearing funding of 5 basis points to 0.25%, partially offset by an increase in our adjusted average cost of borrowings of 59 basis points to 3.71%. We discuss above the primary drivers for the increases in the

average yield on interest-earning assets and adjusted average cost of borrowings.

Derivative Cash Settlements

We include the net periodic derivative cash settlements interest income (expense) amounts on our interest rate swaps in the calculation of our adjusted average cost of borrowings, which, as a result, also impacts the calculation of adjusted net interest income and adjusted net interest yield. We recorded net periodic derivative cash settlements interest income of $29 million for Q2 FY2024, compared with $5 million for Q2 FY2023. We recorded net periodic derivative cash settlements interest income of $57 million for YTD FY2024, compared with derivative cash settlements interest expense of $6 million for YTD FY2023.

Following the cessation of LIBOR on June 30, 2023, daily compounded SOFR replaced LIBOR as the floating-rate index for our interest rate swaps. Because our derivative portfolio consists of a higher proportion of pay-fixed swaps than receive-fixed swaps, the net periodic derivative cash settlements interest income (expense) amounts generally change based on changes in the floating interest amount received each period. When floating rates increase during the period, the floating interest amounts received on our pay-fixed swaps increase and, conversely, when floating rates decrease, the floating interest amounts received on our pay-fixed swaps decrease. The higher floating rates during Q2 FY2024 and YTD FY2024 contributed to the derivative cash settlements interest income for the periods. In comparison, the lower floating rates during Q2 FY2023 and YTD FY2023 contributed to the lower derivative cash settlements income for Q2 FY2023 and derivative cash settlements interest expense for YTD FY2023.

See “Non-GAAP Financial Measures” for additional information on our non-GAAP financial measures, including a reconciliation of these measures to the most comparable U.S. GAAP financial measures.

Provision for Credit Losses

Our provision for credit losses each period is driven by changes in our measurement of lifetime expected credit losses for our loan portfolio recorded in the allowance for credit losses. Our allowance for credit losses and allowance coverage ratio was $56 million and 0.17%, respectively, as of November 30, 2023. In comparison, our allowance for credit losses and allowance coverage ratio was $53 million and 0.16%, respectively, as of May 31, 2023.

We recorded a provision for credit losses of $1 million for Q2 FY2024, resulted primarily from an increase in the collective allowance due to loan portfolio growth. In comparison, we recorded a provision for credit losses of $12 million for Q2 FY2023, primarily driven by an increase in the asset-specific allowance for a nonperforming CFC power supply loan, attributable to a decrease in the expected payments on this loan.

We recorded a provision for credit losses of $1 million for YTD FY2024, compared to a provision for credit losses of $15 million for YTD FY2023. The provision for credit losses for YTD FY2024 resulted from an increase of $4 million in the collective allowance, partially offset by a decrease of $1 million in the asset-specific allowance for a nonperforming CFC power supply loan and a recovery of $1 million attributable to additional loan payments received from Brazos Electric Power Cooperative, Inc. (“Brazos”) and its wholly-owned subsidiary Brazos Sandy Creek Electric Cooperative Inc. (“Brazos Sandy Creek”). The increase of $4 million in the collective allowance was primarily due to loan portfolio growth and a slight decline in the overall credit quality and risk profile of our loan portfolio. The provision for credit losses for the YTD FY2023 was driven primarily by an increase in the asset-specific allowance as discussed above.

We discuss our methodology for estimating the allowance for credit losses in “Note 1—Summary of Significant Accounting Policies—Allowance for Credit Losses—Current Methodology” in our 2023 Form 10-K. We also provide additional

information on our allowance for credit losses below under section “Credit Risk—Allowance for Credit Losses” and “Note 5—Allowance for Credit Losses” in this Report.

Non-Interest Income

Non-interest income consists of fee and other income, gains and losses on derivatives not accounted for in hedge accounting relationships and gains and losses on equity and debt investment securities, which consists of both unrealized and realized gains and losses.

Table 6 presents the components of non-interest income (loss) recorded in our consolidated statements of operations.

Table 6: Non-Interest Income

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | |

| (Dollars in thousands) | | Q2 FY2024 | | Q2 FY2023 | | YTD FY2024 | | YTD FY2023 |

| Non-interest income components: | | | | | | | | |

| Fee and other income | | $ | 6,611 | | | $ | 4,166 | | | $ | 11,148 | | | $ | 8,222 | |

| Derivative gains | | 106,938 | | | 146,790 | | | 296,825 | | | 240,377 | |

| Investment securities gains (losses) | | 1,843 | | | (493) | | | 4,776 | | | (4,172) | |

| Total non-interest income | | $ | 115,392 | | | $ | 150,463 | | | $ | 312,749 | | | $ | 244,427 | |

The variance in non-interest income was primarily attributable to changes in the derivative gains recognized in our consolidated statements of operations. In addition, we experienced a favorable shift from losses to gains recorded on our debt and equity investment securities of $2 million and $9 million for Q2 FY2024 and YTD FY2024, respectively, compared with Q2 FY2023 and YTD FY2023. We expect period-to-period market fluctuations in the fair value of our equity and debt investment securities, which we report together with realized gains and losses from the sale of investment securities on our consolidated statements of operations.

Derivative Gains (Losses)

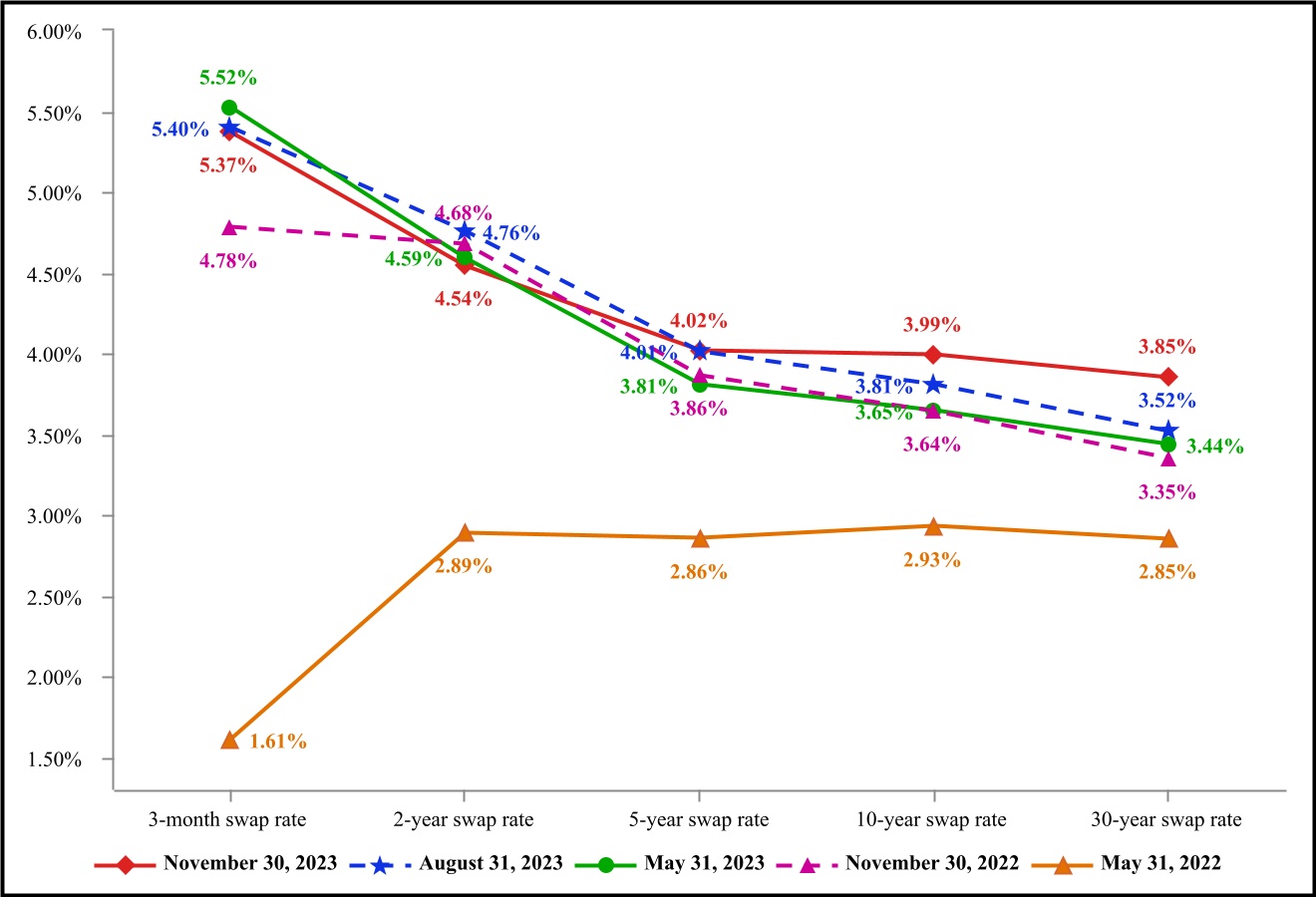

Our derivative instruments are an integral part of our interest rate risk management strategy. Our principal purpose in using derivatives is to manage our aggregate interest rate risk profile within prescribed risk parameters. The derivative instruments we use primarily include interest rate swaps, which we typically hold to maturity. In addition, we may use Treasury locks to manage the interest rate risk associated with future debt issuance or debt that is scheduled to reprice in the future. The primary factors affecting the fair value of our derivatives and derivative gains (losses) recorded in our results of operations include changes in interest rates, the shape of the swap curve and the composition of our derivative portfolio. We generally do not designate our interest rate swaps, which currently account for all our derivatives, for hedge accounting. Accordingly, changes in the fair value of interest rate swaps are reported in our consolidated statements of operations under derivative gains (losses). However, if we execute a Treasury lock, we typically designate the Treasury lock as a cash flow hedge.

We currently use two types of interest rate swap agreements: (i) we pay a fixed rate of interest and receive a variable rate of interest (“pay-fixed swaps”), and (ii) we pay a variable rate of interest and receive a fixed rate of interest (“receive-fixed swaps”). The interest amounts are based on a specified notional balance, which is used for calculation purposes only. The benchmark variable rate for the floating-rate payments under our swap agreements is daily compounded SOFR as of November 30, 2023. As interest rates decline, pay-fixed swaps generally decrease in value and result in the recognition of derivative losses, as the amount of interest we pay remains fixed, while the amount of interest we receive declines. In contrast, as interest rates rise, pay-fixed swaps generally increase in value and result in the recognition of derivative gains, as the amount of interest we pay remains fixed, but the amount we receive increases. With a receive-fixed swap, the opposite results occur as interest rates decline or rise. Our derivative portfolio consists of a higher proportion of pay-fixed swaps than receive-fixed swaps; therefore, we generally record derivative losses when interest rates decline and derivative gains when interest rates rise. Because our pay-fixed and receive-fixed swaps are referenced to different maturity terms along the swap curve, different changes in the swap curve—parallel, flattening, inversion or steepening—will also impact the fair value of our derivatives.