UNITED STATES | |||

SECURITIES AND EXCHANGE COMMISSION | |||

Washington, D.C. 20549 | |||

| |||

SCHEDULE 14A | |||

| |||

Proxy Statement Pursuant to Section 14(a) of | |||

| |||

Filed by the Registrant o | |||

| |||

Filed by a Party other than the Registrant ý | |||

| |||

Check the appropriate box: | |||

o | Preliminary Proxy Statement | ||

o | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) | ||

o | Definitive Proxy Statement | ||

ý | Definitive Additional Materials | ||

o | Soliciting Material Pursuant to §240.14a-12 | ||

| |||

CHIRON CORPORATION | |||

(Name of Registrant as Specified In Its Charter) | |||

| |||

NOVARTIS CORPORATION | |||

(Name of Person(s) Filing Proxy Statement, if other than the Registrant) | |||

| |||

Payment of Filing Fee (Check the appropriate box): | |||

ý | No fee required. | ||

o | Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. | ||

| (1) | Title of each class of securities to which transaction applies: | |

|

|

| |

| (2) | Aggregate number of securities to which transaction applies: | |

|

|

| |

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): | |

|

|

| |

| (4) | Proposed maximum aggregate value of transaction: | |

|

|

| |

| (5) | Total fee paid: | |

|

|

| |

o | Fee paid previously with preliminary materials. | ||

o | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. | ||

| (1) | Amount Previously Paid: | |

|

|

| |

| (2) | Form, Schedule or Registration Statement No.: | |

|

|

| |

| (3) | Filing Party: | |

|

|

| |

| (4) | Date Filed: | |

|

|

| |

|

| Persons who are to respond to the collection of information contained in this form are not required to respond unless the form displays a currently valid OMB control number. | |

Searchable text section of graphics shown above

Agenda

• Introduction

• An Opportunity for Growth but Not Without Risks

• $45 Per Share is a Full Value for Chiron

2

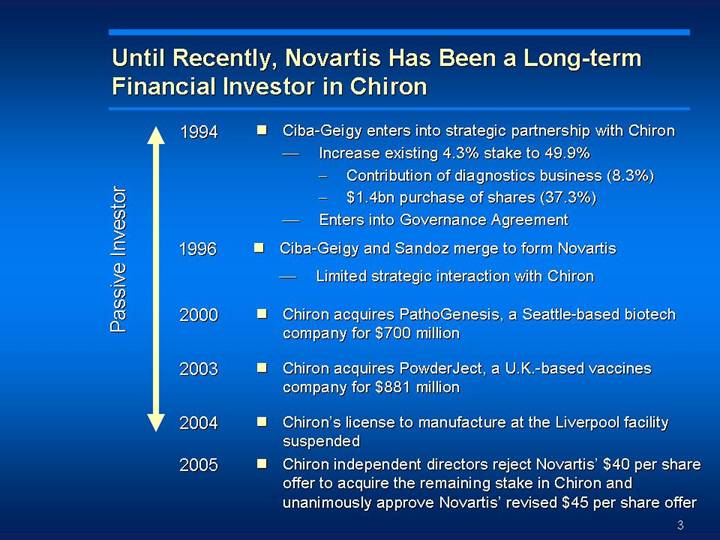

Until Recently, Novartis Has Been a Long-term Financial Investor in Chiron

Passive Investor

1994 |

| • Ciba-Geigy enters into strategic partnership with Chiron |

|

| • Increase existing 4.3% stake to 49.9% |

|

| • Contribution of diagnostics business (8.3%) |

|

| • $1.4bn purchase of shares (37.3%) |

|

| • Enters into Governance Agreement |

|

|

|

1996 |

| • Ciba-Geigy and Sandoz merge to form Novartis |

|

| • Limited strategic interaction with Chiron |

|

|

|

2000 |

| • Chiron acquires PathoGenesis, a Seattle-based biotech company for $700 million |

|

|

|

2003 |

| • Chiron acquires PowderJect, a U.K.-based vaccines company for $881 million |

|

|

|

2004 |

| • Chiron’s license to manufacture at the Liverpool facility suspended |

|

|

|

2005 |

| • Chiron independent directors reject Novartis’ $40 per share offer to acquire the remaining stake in Chiron and unanimously approve Novartis’ revised $45 per share offer |

3

The Transaction Merits Need to Be Seen Together with Chiron’s Challenges and Risks

Novartis transaction rationale |

| Chiron’s challenges and risks |

|

|

|

• Strategic platform in vaccines |

| • Strategically overstretched – underinvestment in Vaccines |

|

|

|

• Blood Testing business provides a potential basis to be extended into personalized medicine |

| • High risk, early stage pipeline in Biopharma

|

|

| • Flu vaccine manufacturing: Remediation ongoing |

• Potentially interesting early stage oncology assets |

|

|

• Preserve value of existing 44% stake |

| • Growing competition in flu vaccine market – declining market share |

|

|

|

|

| • Significant operational and investment hurdles to meet targets and expectations |

4

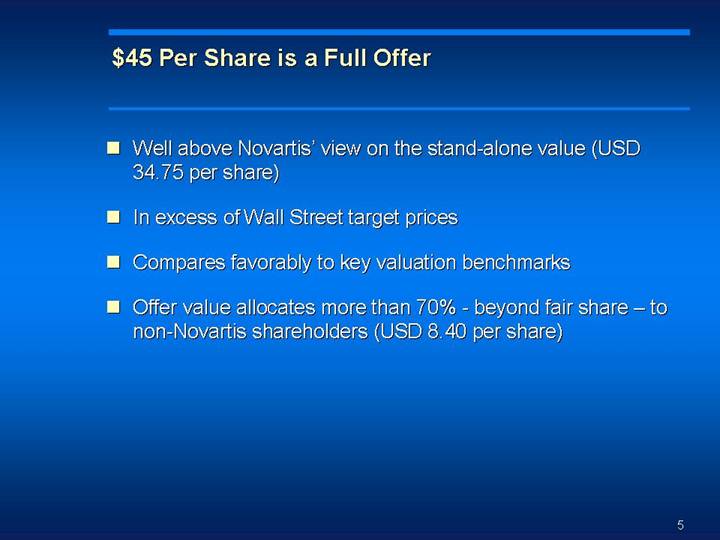

$45 Per Share is a Full Offer

• Well above Novartis’ view on the stand-alone value (USD 34.75 per share)

• In excess of Wall Street target prices

• Compares favorably to key valuation benchmarks

• Offer value allocates more than 70% - beyond fair share – to non-Novartis shareholders (USD 8.40 per share)

5

Agenda

• Introduction

• An Opportunity for Growth but Not Without Risks

• $45 Per Share is a Full Value

6

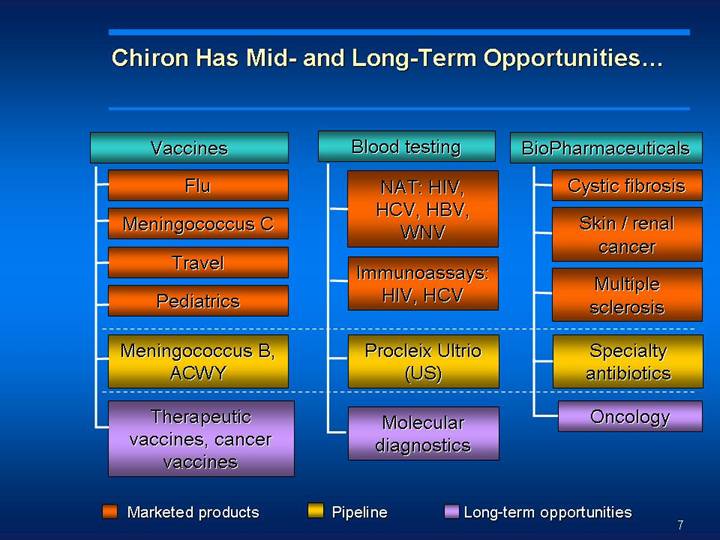

Chiron Has Mid- and Long-Term Opportunities…

Vaccines |

| Blood testing |

| BioPharmaceuticals |

|

|

|

|

|

Flu Meningococcus C Travel Pediatrics Meningococcus B, ACWY Therapeutic vaccines, cancer vaccines |

| NAT: HIV, HCV, HBV, WNV

Molecular diagnostics |

| Cystic fibrosis Oncology |

Marketed products

Pipeline

Long-term opportunities

7

… But Many Issues Remain Unresolved

• Ongoing remediation at Liverpool, Marburg and Siena facilities

• Open FDA 483 issues in Liverpool, Marburg and Emeryville

• Ongoing sterility issues in Marburg facility prevented BEGRIVAC vaccine supply for 2005-2006 and may delay cell flu program

• High risk, early-stage pipeline

• Ongoing legal issues and distractions relating to the disclosure of Chiron’s manufacturing problems in 2004

8

Remediation of Manufacturing Sites is Ongoing and Will Take Time and Capital to Complete

Liverpool |

| • Further investments needed |

|

| • 1960s facility requires environmental upgrades, air handling and water systems improvements |

|

|

|

Marburg |

| • Remediation ongoing |

|

| • Substandard engineering |

|

| • Improvement in flu cell culture facility design needed |

|

|

|

Siena |

| • Past maintenance minimised – catch-up needed to ensure ongoing critical operations |

|

|

|

Emeryville |

| • Ongoing upgrades required for BioPharma and Blood Testing |

Incremental remediation Capex through 2010 to reach $200m

9

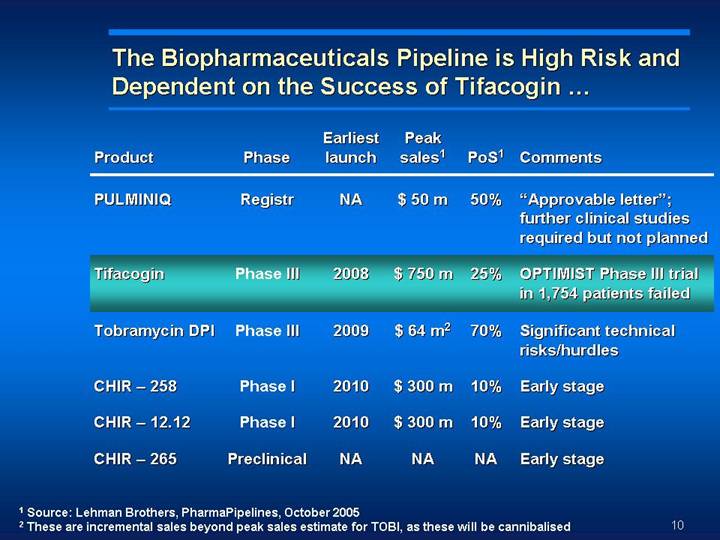

The Biopharmaceuticals Pipeline is High Risk and Dependent on the Success of Tifacogin …

|

|

|

| Earliest |

| Peak |

|

|

|

|

| |

Product |

| Phase |

| launch |

| sales(1) |

| PoS(1) |

| Comments |

| |

|

|

|

|

|

|

|

|

|

|

|

| |

PULMINIQ |

| Registr |

| NA |

| $ | 50 | m | 50 | % | “Approvable letter”; further clinical studies required but not planned |

|

|

|

|

|

|

|

|

|

|

|

|

| |

Tifacogin |

| Phase III |

| 2008 |

| $ | 750 | m | 25 | % | OPTIMIST Phase III trial in 1,754 patients failed |

|

|

|

|

|

|

|

|

|

|

|

|

| |

Tobramycin DPI |

| Phase III |

| 2009 |

| $ | 64 | m(2) | 70 | % | Significant technical risks/hurdles |

|

|

|

|

|

|

|

|

|

|

|

|

| |

CHIR – 258 |

| Phase I |

| 2010 |

| $ | 300 | m | 10 | % | Early stage |

|

|

|

|

|

|

|

|

|

|

|

|

| |

CHIR – 12.12 |

| Phase I |

| 2010 |

| $ | 300 | m | 10 | % | Early stage |

|

CHIR – 265 |

| Preclinical |

| NA |

| NA |

| NA |

| Early stage |

| |

(1) Source: Lehman Brothers, PharmaPipelines, October 2005

(2) These are incremental sales beyond peak sales estimate for TOBI, as these will be cannibalised

10

… and Tifacogin’s Success Remains Questionable

• Tifacogin failed a Phase III study to measure efficacy and safety in 1,754 patients with severe sepsis

• no survival benefit vs placebo on the primary endpoint (mortality at 28 days) and on all pre-specified sub-group analyses

• safety issues, particularly CNS bleeds, were more frequent with tifacogin than with other anticoagulants (e.g. heparin)

• In one retrospective sub-group analysis of 157 patients (sCAP patients with documented bacterial infection and not treated with heparin) tifacogin showed a benefit vs placebo

• However, other tifacogin treated sub-groups showed a trend to greater mortality, including sCAP patients not treated with heparin without documented evidence of infection

• Even if successful in showing benefit in this sCAP population in the ongoing study, commercial prospects are likely to be limited

• Only 30% of sCAP patients don’t receive heparin

• 56 000 patients / year in the US(1)

(1) Am J Resp & Crit Care Med 165:766 (2002)

11

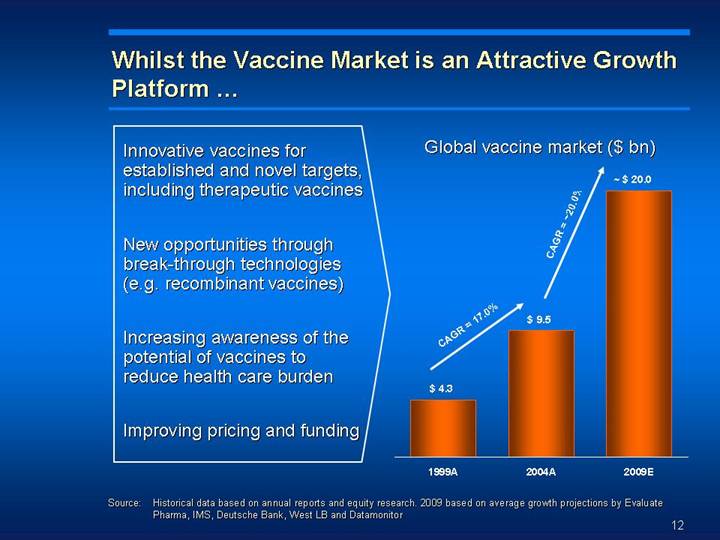

Whilst the Vaccine Market is an Attractive Growth Platform …

Innovative vaccines for established and novel targets, including therapeutic vaccines

New opportunities through break-through technologies (e.g. recombinant vaccines)

Increasing awareness of the potential of vaccines to reduce health care burden

Improving pricing and funding

Global vaccine market ($ bn)

[CHART]

Source: Historical data based on annual reports and equity research. 2009 based on average growth projections by Evaluate Pharma, IMS, Deutsche Bank, West LB and Datamonitor

12

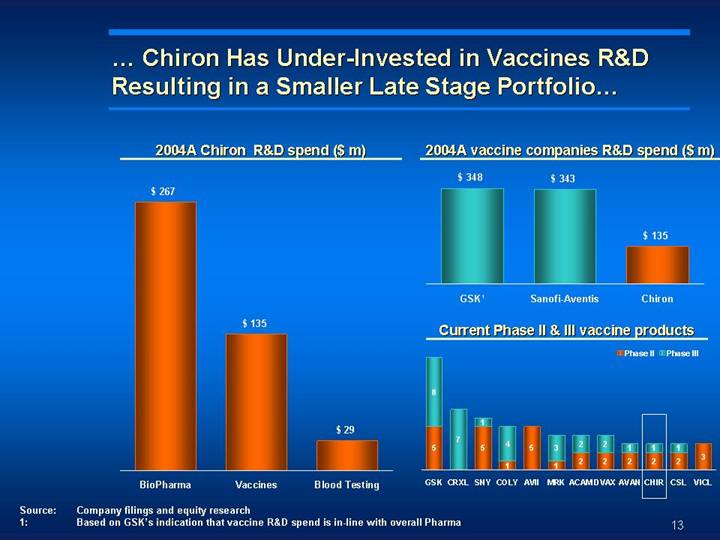

… Chiron Has Under-Invested in Vaccines R&D Resulting in a Smaller Late Stage Portfolio…

2004A Chiron R&D spend ($ m)

[CHART]

2004A vaccine companies R&D spend ($ m)

[CHART]

Current Phase II & III vaccine products

[CHART]

Source: Company filings and equity research

1: Based on GSK’s indication that vaccine R&D spend is in-line with overall Pharma

13

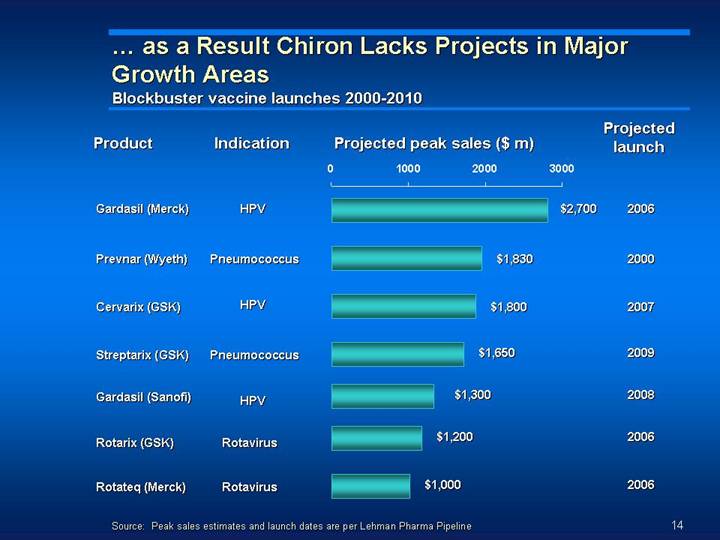

… as a Result Chiron Lacks Projects in Major Growth Areas

Blockbuster vaccine launches 2000-2010

|

|

|

|

|

| Projected |

|

Product |

| Indication |

| Projected peak sales ($ m) |

| launch |

|

|

|

|

|

|

|

|

|

Gardasil (Merck) |

| HPV |

| [CHART] |

| 2006 |

|

|

|

|

|

|

|

|

|

Prevnar (Wyeth) |

| Pneumococcus |

|

|

| 2000 |

|

|

|

|

|

|

|

|

|

Cervarix (GSK) |

| HPV |

|

|

| 2007 |

|

|

|

|

|

|

|

|

|

Streptarix (GSK) |

| Pneumococcus |

|

|

| 2009 |

|

|

|

|

|

|

|

|

|

Gardasil (Sanofi) |

| HPV |

|

|

| 2008 |

|

|

|

|

|

|

|

|

|

Rotarix (GSK) |

| Rotavirus |

|

|

| 2006 |

|

|

|

|

|

|

|

|

|

Rotateq (Merck) |

| Rotavirus |

|

|

| 2006 |

|

Source: Peak sales estimates and launch dates are per Lehman Pharma Pipeline

14

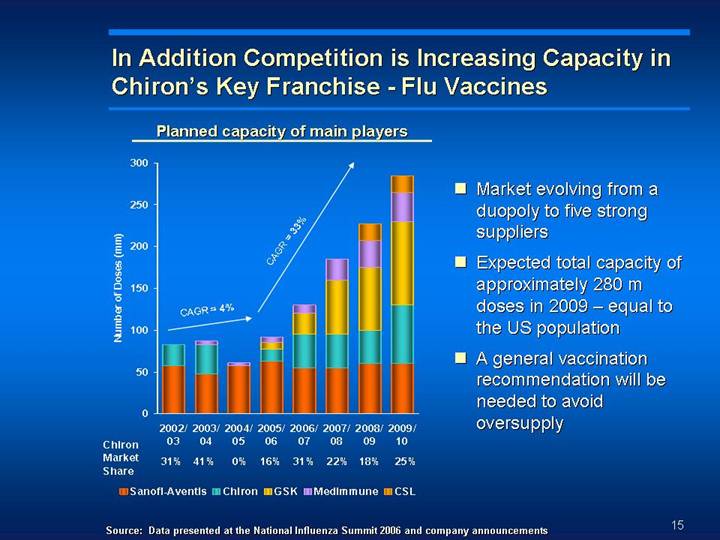

In Addition Competition is Increasing Capacity in Chiron’s Key Franchise - Flu Vaccines

Planned capacity of main players

[CHART]

• Market evolving from a duopoly to five strong suppliers

• Expected total capacity of approximately 280 m doses in 2009 – equal to the US population

• A general vaccination recommendation will be needed to avoid oversupply

Source: Data presented at the National Influenza Summit 2006 and company announcements

15

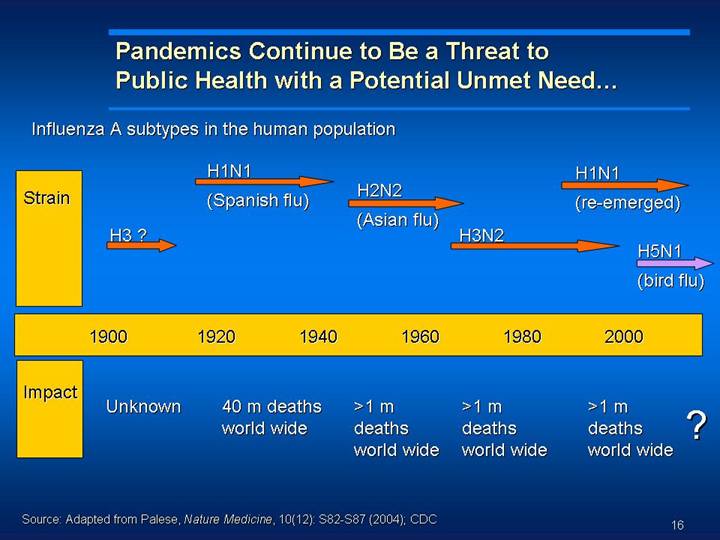

Pandemics Continue to Be a Threat to

Public Health with a Potential Unmet Need…

Influenza A subtypes in the human population

Strain |

|

|

| H1N1 |

|

|

|

|

| H1N1 |

|

|

|

|

|

|

| => |

| H2N2 |

|

|

| => |

|

|

|

|

| H3 ? |

| (Spanish flu) |

| => |

|

|

| (re-emerged) |

|

|

|

|

| => |

|

|

| (Asian flu) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| H3N2 |

|

|

|

|

|

|

|

|

|

|

|

|

| => |

|

|

| H5N1 |

|

|

|

|

|

|

|

|

|

|

|

|

| => |

|

|

|

|

|

|

|

|

|

|

|

|

| (bird flu) |

|

|

| 1900 |

| 1920 |

| 1940 |

| 1960 |

| 1980 |

| 2000 |

| |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Impact |

| Unknown |

| 40 m deaths |

| >1 m |

| >1 m |

| >1 m |

| ? |

| |||||||||||||

Source: Adapted from Palese, Nature Medicine, 10(12): S82-S87 (2004); CDC

16

...but History Teaches Us That They May Not Necessarily Materialize …

• 1976 - swine flu

• February: Influenza A Hsw1N1 strain caused severe respiratory illness in 13 soldiers with one death in Fort Dix, NJ

• Summer: Initial vaccination campaign foreseen to target 150 m patients – only 43 m were actually vaccinated

• December: Epidemic viewed as unlikely by Center for Disease Control (CDC), campaign stopped

17

… And in the Event of an Avian Flu Pandemic

There May Be Little Commercial Value

• Regulatory pathway still needs to be clarified with different Governments focusing on different specifications

• The strain may still mutate making existing products obsolete. As such, there is unclear pricing and stockpiling needs

• Production of H5N1 has low yields and will cannibalize existing flu vaccine capacity – today only small quantities are produced in the winter

• Twelve companies are involved in the development of a H5N1 vaccine with five phase II programs and over 20 earlier stage programs ongoing

• History suggests that a real pandemic will most likely require an altruistic approach by industry - which can only be funded by larger companies

18

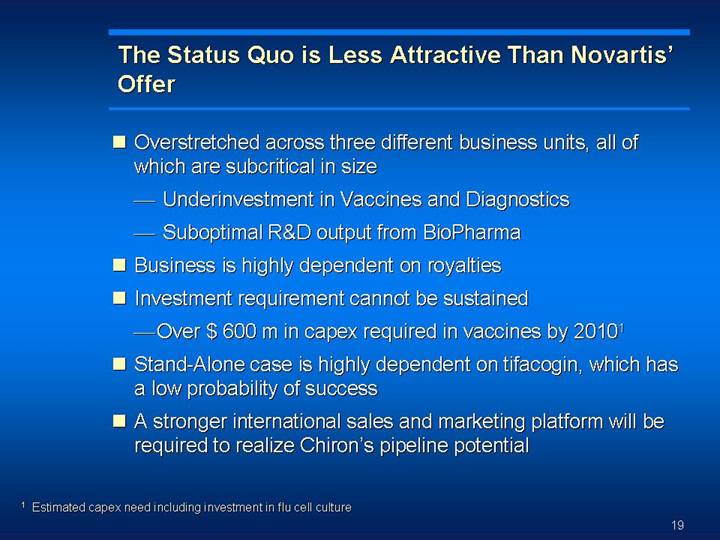

The Status Quo is Less Attractive Than Novartis’ Offer

• Overstretched across three different business units, all of which are sub critical in size

• Underinvestment in Vaccines and Diagnostics

• Suboptimal R&D output from BioPharma

• Business is highly dependent on royalties

• Investment requirement cannot be sustained

• Over $ 600 m in capex required in vaccines by 2010(1)

• Stand-Alone case is highly dependent on tifacogin, which has a low probability of success

• A stronger international sales and marketing platform will be required to realize Chiron’s pipeline potential

(1) Estimated capex need including investment in flu cell culture

19

Agenda

• Introduction

• An Opportunity for Growth but Not Without Risks

• $45 Per Share is a Full Value

20

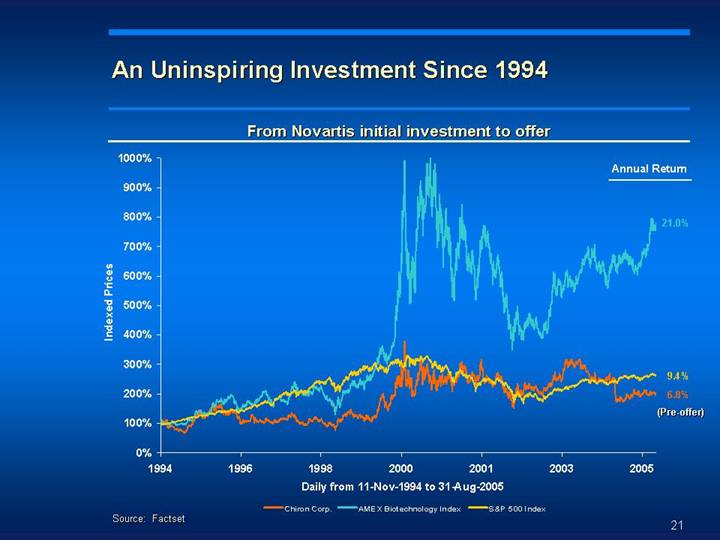

An Uninspiring Investment Since 1994

From Novartis initial investment to offer

[CHART]

Source: Factset

21

Near-Term Management Forecasts Are Below Wall Street Expectations, Long-Term Forecasts Are Very Aggressive

Revenue ($bn) |

| Net Income ($m) |

|

|

|

[CHART] |

| [CHART] |

Note: | 2005A Net Income adjusted for normalized tax rate of 25.0% |

22

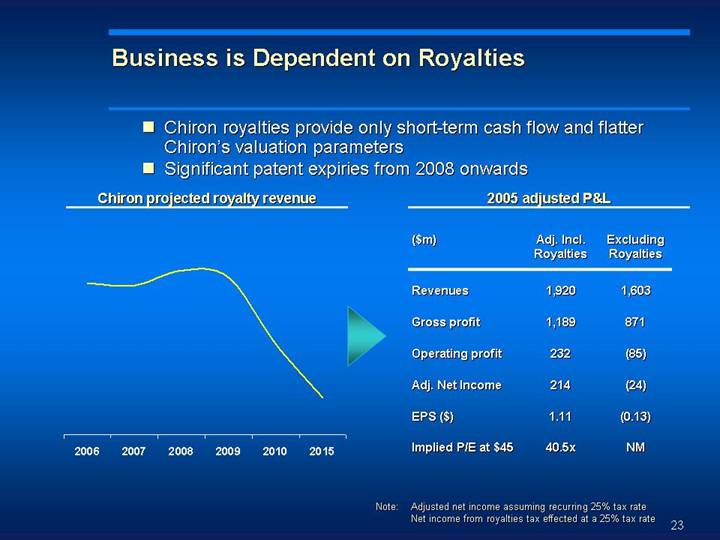

Business is Dependent on Royalties

• Chiron royalties provide only short-term cash flow and flatter Chiron’s valuation parameters

• Significant patent expiries from 2008 onwards

Chiron projected royalty revenue | 2005 adjusted P&L | |||||

|

| |||||

| ($m) |

| Adj. Incl. |

| Excluding |

|

|

|

|

|

|

|

|

| Revenues |

| 1,920 |

| 1,603 |

|

|

|

|

|

|

|

|

| Gross Profit |

| 1,189 |

| 871 |

|

|

|

|

|

|

|

|

[CHART] | Operating Profit |

| 232 |

| (85 | ) |

|

|

|

|

|

|

|

| Adj. Net Income |

| 214 |

| (24 | ) |

|

|

|

|

|

|

|

| EPS ($) |

| 1.11 |

| (0.13 | ) |

|

|

|

|

|

|

|

| Implied P/E at $45 |

| 40.5 | x | NM |

|

Note: | Adjusted net income assuming recurring 25% tax rate |

23

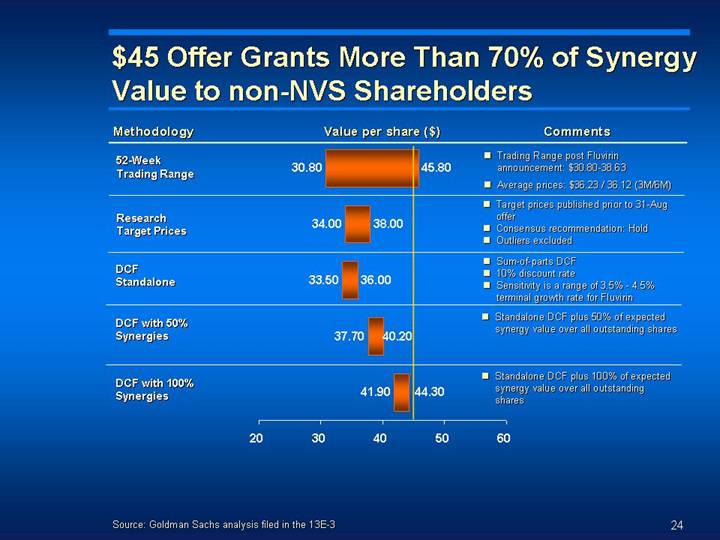

$45 Offer Grants More Than 70% of Synergy Value to non-NVS Shareholders

Methodology |

| Value per share ($) |

| Comments |

|

|

|

|

|

|

|

52-Week |

| [CHART] |

| • Trading Range post Fluvirin announcement: $30.80-38.63 • Average prices: $36.23 / 36.12 (3M/6M) |

|

|

|

|

|

|

|

Research |

|

|

| • Target prices published prior to 31-Aug offer • Consensus recommendation: Hold • Outliers excluded |

|

|

|

|

|

|

|

DCF |

|

|

| • Sum-of-parts DCF • 10% discount rate • Sensitivity is a range of 3.5% - 4.5% terminal growth rate for Fluvirin |

|

|

|

|

|

|

|

DCF with 50% Synergies |

|

|

| • Standalone DCF plus 50% of expected synergy value over all outstanding shares |

|

|

|

|

|

|

|

DCF with 100% Synergies |

|

|

| • Standalone DCF plus 100% of expected synergy value over all outstanding shares |

|

Source: Goldman Sachs analysis filed in the 13E-3

24

Limited Upcoming Share Price Catalysts

• Chiron delayed negotiations for 11 months to capture positive newsflow during discussions

• First contact December 2004

• Negotiations ended October 2005

• Newsflow incorporated in price

• Re-entry to U.S. flu market

• First Phase 3 trial in EU for flu cell culture

• Initiation of Phase 1 / Phase 2 in U.S. for flu cell culture

• Positive data on MF59 adjuvant with potential pandemic strain

• Initiation of Phase 3 for TIP

• Initiation of Phase 1 for CHIR-12.12

• Geographic expansion and ex. U.S. PROCLEIX ULTRIO penetration

• Limited upcoming newsflow left

25

Wall Street Analysts See Few Remaining Growth Drivers and Have Price Targets Below $ 45

|

| Pre-offer views |

|

|

| Post-offer views |

|

|

|

|

|

|

|

• |

| We see few remaining growth drivers over the next 12–18 months... (...) as the flu vaccine business comes under significant pressure from competition (Morgan Stanley, 31-Aug-2005) |

| • |

| Thus, we believe Chiron shareholders would get more value and reduce risk through an all-cash acquisition by Novartis than if existing management continued to run the business (Merrill Lynch, 06-Sep-2005) |

|

|

|

|

|

|

|

• |

| In our opinion, Chiron lacks depth in regards to a product pipeline in comparison to its peer group (...) (Citigroup, 27-Jul-2005) |

| • |

| We believe it is unlikely that there will be other offers/bidders... and recommend taking profits at or above our target price of $42 per share (Citigroup, 01-Sep-2005) |

|

|

|

|

|

|

|

• |

| We believe the continued funding of further development of Proleukin, as well as resurrected programs such as Tifacogin, and attempts at diversification in the testing business, will fail to bear fruit (Bernstein, 28-Jul-2005) |

| • |

| Our sum-of-the-parts valuation suggests that the company is fairly valued with a range of $37-$44 per share... (AG Edwards, 02-Sep-2005) |

Source: Wall Street research

26