Exhibit 13.1

|

MARKET FOR UNION BANKSHARE'S COMMON STOCK AND RELATED STOCKHOLDER MATTERS

On March 12, 2012, there were 4,457,204 shares of common stock outstanding held by 637 stockholders of record. The number of stockholders does not reflect the number of beneficial owners, including persons or entities who may hold the stock in nominee or “street name.”

Union Bankshares' common stock is listed on the NASDAQ Global Market trading under the symbol UNB.

| 2011 | 2010 | ||||||||||||||||||||||

| High | Low | Dividends | High | Low | Dividends | ||||||||||||||||||

| First Quarter | $ | 22.39 | $ | 17.95 | $ | 0.25 | $ | 19.82 | $ | 17.00 | $ | 0.25 | |||||||||||

| Second Quarter | $ | 20.00 | $ | 18.80 | $ | 0.25 | $ | 19.00 | $ | 17.44 | $ | 0.25 | |||||||||||

| Third Quarter | $ | 19.99 | $ | 18.75 | $ | 0.25 | $ | 18.48 | $ | 17.40 | $ | 0.25 | |||||||||||

| Fourth Quarter | $ | 19.80 | $ | 18.11 | $ | 0.25 | $ | 18.25 | $ | 17.73 | $ | 0.25 | |||||||||||

On January 18, 2012, the Company declared a regular dividend of $0.25 per share to stockholders of record as of January 28, 2012 payable February 9, 2012.

| The Renovated Railroad Street Office | |

|

In the fall of 2011 a major refurbishment of the exterior, installation of a ramp providing handicap access and new signage was completed at our Railroad Street, St. Johnsbury office. These improvements were dedicated to the Hovey Family who was very much a part of the former Citizens Savings Bank and Trust Company acquired in 1999 by Union Bankshares.

We are proud to have undertaken this initiative, have received numerous positive comments from the public and recently received the Northeast Kingdom Chamber of Commerce Kingdom Improvement Award.

LETTER TO SHAREHOLDERS

March 30, 2012

Dear Shareholders,

We experienced another successful year and increased our total assets by $100 million, added three branch offices and increased our sold but serviced loan portfolio to over $208 million. More on these achievements are included in this year's annual report and below.

On May 27, 2011 we completed the acquisition of the three Northway Bank branches located in Littleton, Groveton and North Woodstock, NH. This transaction added over $67 million to our balance sheet, 18 new staff members and thousands of new customers. The transition to Union for the employees and customers of Northway went very well and we are experiencing the positive benefits of this transaction.

Interest rates continue at historic lows which has kept us very busy as the refinancing of residential mortgages has not subsided. During the year we originated and sold over $80 million in residential mortgage loans. As this portfolio increases so do the servicing fees which reached $500 thousand in 2011.

We have also experienced an increase, in the latter part of 2011 and into 2012, in residential lending for home purchases and construction loan transactions. This appears to be in all our markets and is perhaps a sign the economy is improving.

During 2011, and for the next three to five years, we will be implementing new procedures, policies, disclosures and activities designed to comply with the myriad of new regulations Congress and the regulators have deemed necessary. There is no doubt our costs for regulatory compliance and rule implementation will increase and we have taken the necessary steps and made the commitment to full compliance. There is however an opportunity for those community banks who “get it right” to grow their franchises in the face of these challenges.

During the past year, we have been transitioning the duties of chief executive officer to David Silverman. This will be completed immediately following this year's annual meeting on May 16th. Ken Gibbons will be retiring from the Company after 21 years as CEO and will remain as Chairman of the Board. David Silverman will add the CEO responsibilities to his current duties as President at that time. This transition has gone very smoothly as the Company continues its strong financial performance, community support and leadership in 2012 and the years to come.

We want to express our sincere appreciation and gratitude to our shareholders, customers and employees. Your investment, business and diligent efforts during the past year again contributed to the growth and strength of Union Bank. Thank you!

Sincerely,

| |

| Kenneth D. Gibbons | |

| Chairman & Chief Executive Officer | |

| |

| David S. Silverman | |

| President | |

Union Bankshares, Inc.1

Union Bankshares, Inc. Board of Directors

Cynthia D. Borck Owner Consulting Services Information |  |  | ||

Steven J. Bourgeois CEO Strategic Initiatives for Business LLC | ||||

Kenneth D. Gibbons Chairman and CEO Union Bankshares, Inc. and Union Bank |  |  | ||

Timothy W. Sargent Attorney/Owner Sargent Law Office | ||||

John H. Steel Founder Steel Construction |  |  | ||

David S. Silverman President Union Bankshares, Inc. and Union Bank | ||||

Schuyler W. Sweet Owner Stony River Properties, LLC |  |  | ||

Neil J. Van Dyke President Golden Eagle Resort | ||||

Union Bankshares, Inc.2

SHAREHOLDER ASSISTANCE & INVESTOR INFORMATION

If you need assistance with a change in registration of certificates, combining your certificates into one, reporting lost certificates, non-receipt or loss of dividend checks, assistance regarding direct deposit of dividends, information about the Company, or to receive copies of financial reports, please contact either:

| JoAnn A. Tallman, Assistant Secretary | Registrar & Transfer Company | |||

| Union Bankshares, Inc. | Attn: Stock Transfer Department | |||

| P.O. Box 667 | 10 Commerce Drive | |||

| Morrisville, VT 05661-0667 | Cranford, NJ 07016 | |||

| Phone: | 802-888-6600 | Phone: | 1-800-368-5948 | |

| Fax: | 802-888-4921 | Fax: | 1-908-497-2318 | |

| Email: | ubexec@unionbankvt.com | E-mail: | info@rtco.com | |

NASDAQ Stock Market Ticker Symbol: UNB

Corporate Name: Union Bankshares, Inc.

To view additional information about the Company or to receive alerts when public filings are posted, please view the Investor Relations page at www.unionbankvt.com.

Union Bankshares, Inc., operates as a one bank holding company for Union Bank, which provides commercial, municipal, trust and retail banking services in northern Vermont and northwestern New Hampshire. As of December 31, 2011, the company operated 13 community banking locations in Lamoille, Caledonia and Franklin counties of Vermont; four community banking locations in Grafton and Coös counties of New Hampshire; and one loan center in South Burlington, (Chittenden County), Vermont; as well as 34 ATMs throughout northern Vermont and northwestern New Hampshire. Union Bank was founded in 1891 in Morrisville, Vermont, where the Bank’s and holding company headquarters are located.

Union Bank promotes personal service and banking expertise within the communities it serves, with a focus on small- to middle-market businesses, local municipalities, non-profits, retail and trust customers. To leverage its local expertise, Union Bank continues to enhance its niche capabilities and focuses on expanding to additional neighboring communities.

Union Bankshares, through Union Bank, is committed to the communities it serves, and encourages employee participation in community events and charitable services. The Company views small businesses as foundations for thriving local economies; these businesses provide jobs, attract other businesses and create wealth. Currently, Union Bank employs 180 people, many of whom are leaders in community organizations throughout the Bank’s service area.

| • | Union Bankshares’ growing asset base of over $552 million provides the financial strength to successfully serve its constituents |

| • | The Company reported a Return on Average Equity of 12.33% or greater and a Return on Average Assets of 1.04% or greater for each of the last five years |

| • | Union Bank has scored an "Outstanding" rating on ALL its CRA (Community Reinvestment Act) examinations since 1995 |

| • | Union Bank has been an SBA "Preferred Lender" since 1987 |

Union Bankshares, Inc.3

SELECTED FINANCIAL DATA

| At or For The Years Ended December 31 | |||||||||||||||

| 2011 | 2010 | 2009 | 2008 | 2007 | |||||||||||

| (Dollars in thousands, except per share data) | |||||||||||||||

| Balance Sheet Data | |||||||||||||||

| Total assets | $ | 552,751 | $ | 452,995 | $ | 447,522 | $ | 440,104 | $ | 393,264 | |||||

| Investment securities | 46,954 | 24,280 | 24,649 | 27,834 | 33,822 | ||||||||||

| Loans, net of unearned income | 429,384 | 382,071 | 358,167 | 353,310 | 318,194 | ||||||||||

| Allowance for loan losses | (4,226 | ) | (3,755 | ) | (3,493 | ) | (3,556 | ) | (3,378 | ) | |||||

| Deposits | 473,439 | 376,660 | 368,827 | 364,370 | 323,961 | ||||||||||

| Borrowed funds | 29,015 | 28,986 | 30,993 | 27,416 | 20,328 | ||||||||||

| Stockholders' equity (1) | 40,339 | 41,725 | 41,180 | 39,150 | 42,074 | ||||||||||

| Income Statement Data | |||||||||||||||

| Total interest income | $ | 23,669 | $ | 22,907 | $ | 23,217 | $ | 24,721 | $ | 26,273 | |||||

| Total interest expense | (3,908 | ) | (4,117 | ) | (5,294 | ) | (7,177 | ) | (8,228 | ) | |||||

| Net interest and dividend income | 19,761 | 18,790 | 17,923 | 17,544 | 18,045 | ||||||||||

| Provision for loan losses | (775 | ) | (520 | ) | (400 | ) | (335 | ) | (265 | ) | |||||

| Noninterest income | 7,125 | 5,649 | 5,521 | 4,329 | 4,249 | ||||||||||

| Noninterest expenses | (19,773 | ) | (16,630 | ) | (16,397 | ) | (15,412 | ) | (14,409 | ) | |||||

| Income before provision for income taxes | 6,338 | 7,289 | 6,647 | 6,126 | 7,620 | ||||||||||

| Provision for income taxes | (1,119 | ) | (1,702 | ) | (1,420 | ) | (1,020 | ) | (1,965 | ) | |||||

| Net income | $ | 5,219 | $ | 5,587 | $ | 5,227 | $ | 5,106 | $ | 5,655 | |||||

| Per Common Share Data | |||||||||||||||

| Net income (2) | $ | 1.17 | $ | 1.25 | $ | 1.17 | $ | 1.14 | $ | 1.25 | |||||

| Cash dividends paid | 1.00 | 1.00 | 1.00 | 1.12 | 1.12 | ||||||||||

| Book value (1) | 9.05 | 9.36 | 9.23 | 8.75 | 9.34 | ||||||||||

| Weighted average number of shares outstanding | 4,456,842 | 4,458,193 | 4,466,760 | 4,488,888 | 4,521,380 | ||||||||||

| Number of shares outstanding | 4,457,204 | 4,455,704 | 4,461,208 | 4,474,598 | 4,502,969 | ||||||||||

| (1) | Stockholders' equity includes unrealized gains or losses, net of applicable income taxes, on investment securities classified as “available-for-sale” and the unfunded liability for pension benefits, net of taxes for the defined benefit pension plan. |

| (2) | Computed using the weighted average number of shares outstanding for the period. |

Union Bankshares, Inc.4

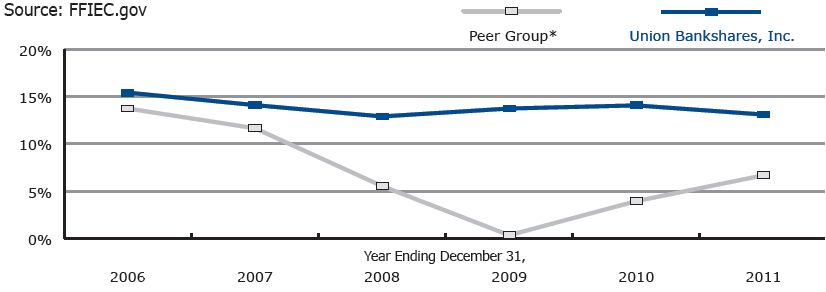

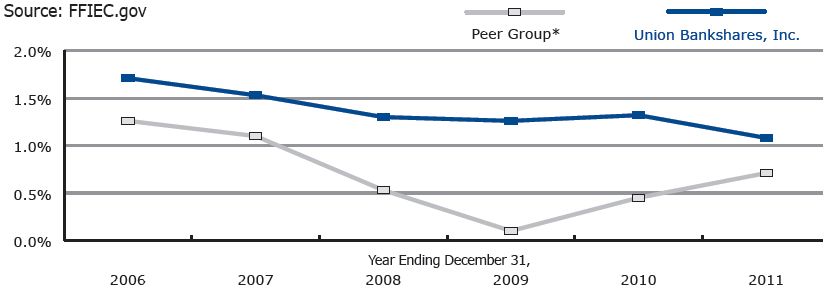

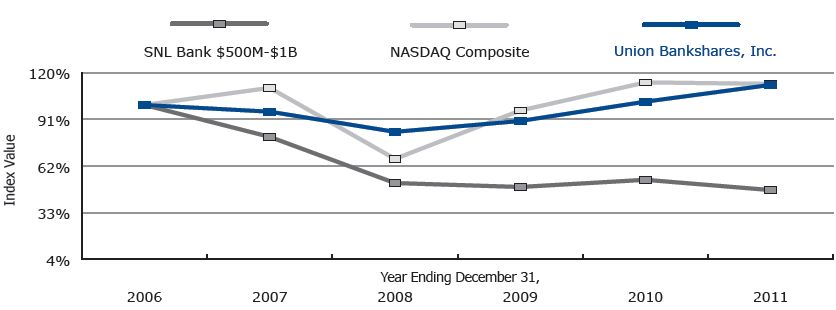

Key Financial Indicators

| Return on Average Equity | ||

| ||

| Return on Average Assets | ||

| ||

| *Peer Group is "All US Banks with $300M-$1B in Assets" (approximately 1,170 banks) | ||

| Total Return Performance | ||

| Source: SNL Financial LC | ||

| ||

Union Bankshares, Inc.5

Working Together

| A Memorable Memorial Day | |

This story begins well before Memorial Day, 2011. It begins with our long-term plans and the desire to grow our footprint through acquisition. Setting our sights on New Hampshire made good sense based on our geographic reach, our personal knowledge of the area and familiarity with the business climate. At the same time, Northway Bank decided since they did not have a strong branch presence in an adjacent or nearby market to the Littleton, Groveton and North Woodstock branches, those customers might be well served if their banking needs were met by another community bank-particularly one that had a presence in adjacent markets. Northway selected Union Bank as they knew Union had the resources, market knowledge and presence, and were very committed to making banking a great experience for their customers.

Northway and Union Bank have philosophies and systems in common. We both make the customer and community priority one. Our product lines, though not exact, are similar; we use the same vendor for our Information Technology (IT) platforms; we share a commitment to tight security. The Banks worked together to negotiate a fair transaction to transfer the Littleton, North Woodstock and Groveton branches from Northway.

A key component of the evaluation process to purchase was a thorough review of the loan portfolio. A hands-on process known as due diligence entailed a panel of lenders driving to Northway's operation center and reading through a significant sampling of the loan portfolio. An analysis was prepared and the decision was made to move forward with the purchase.

Another element of the decision was assessing the physical properties. Site surveys and building inspections had to precede a final purchase decision. It was determined that the properties were sound, and we set about learning the building systems. Vendors were chosen for the utilities: heat, electric, landscaping and plowing to name just a few. Facilities worked closely with IT to ensure our systems would be amply supported.

Purchasing three bank branches and bringing them online is no small feat. The intricacies of the negotiations, the laying out of the welcome mat, the importing of the accounts, the change out of physical mate-rials, the turning of the switch from one system to another and a myriad other details need to be anticipated, managed and tended to. Both banks worked diligently to delineate every facet of the transaction.

Welcome to the Union Bank Family!

A dinner with the soon-to-be new employees turned into a fun, informal way to meet each other. We wanted to let these employees know what they could expect from us and start to prove to them that Union Bank is committed to them, to their success and to our success in the area. Simply put, we wanted them to know that they could place their confidence in us as we would be placing our confidence in them.

Reaching out to staff was quickly followed by reaching out to those customers whose accounts we would be acquiring. Starting three months prior, our key lenders spent two to three days each week meeting with business owners. They saw these meetings as an opportunity to start forging solid relationships, to learn more about the needs, concerns and hopes of the local business people. It was imperative to everyone that the customers enjoyed a seamless transition and Northway was right there helping to make the introductions and smoothing the way. To that end, systems such as electronic banking and merchant services were tested and retested to ensure that our commercial customers would experience a smooth transition.

At the branch level, a host of branch personnel worked on making the retail customers transition seamless as well. The customers quickly saw that they were in good hands-and that the good hands they were in were the very same hands that helped them when the name on the door was Northway.

Union Bankshares, Inc.6

Behind the Scenes!

Deposit operations and loan servicing had the job of converting each Northway deposit and loan account (business and personal) to our account offering. Our security manager oversaw the security aspects of the transaction. That includes the online security, the facility security as well as security training for all the new personnel. Every Bank handles security slightly differently, but the changes were minimal.

As the three-day conversion weekend drew closer, schedules were created for the transition of each branch. Everything had to transition on this weekend. These three days were the culmination of months of preparation. Bank signs were swapped out. ATMs were converted. Cash was counted and verified, submitted to accounting at both banks and signed off on. Furniture was moved. Office supplies were stocked, phone and data lines were switched, oil and gas tanks were prorated, trucks were emptied, problems were solved and cheers were heard. Come end of day Monday, the orchestration of the vendors, trucks, cranes, handcarts, boxes, people, software and accounting was flawless.

We are thankful to our friends at Northway who worked together with us to make the outcome of the transition smooth, pleasant and positive.

|  |  | ||

| Making a Difference | |

Our employees are not new to the notion of community service, giving countless hours of their expertise and time. With the challenges of small town life and hard economic times, our local communities are critically dependent upon their involvement. From fundraising for cancer patients to celebrating the home-town, community is simply who they are.

The following organizations illustrate just some of the ways our employees touch lives and make a difference in the communities we serve.

March of Dimes: Union Bank has supported the March of Dimes' efforts since 1975 to help moms have full-term pregnancies and research the problems that threaten the health of babies. The annual March for Babies is one of several fundraisers that the Bank participates in to help with March of Dimes' mission. Barbara Olden, St. Johnsbury Branch Manager and Champion for the March of Dimes, has been involved for 21 years. She often serves as Team Captain for the Bank's Walking Team. Melissa Greene, Hardwick Branch Manager, helps coordinate the sale of March of Dimes Bean Bags for babies in our branches throughout the year.

Union Bankshares, Inc.7

LACiNg Up for Cancer: A diagnosis of cancer brings financial burdens well beyond the scope of health insurance. LACiNg Up for Cancer was designed to help assist Lamoille area residents facing these financial challenges. Funds are used for a variety of needs generated by the disease beyond treatment including rent and gas for traveling to treatments. Deb Partlow, Senior Trust Officer, is the Event Champion within the Bank. Many other employees participate by walking on the Union Bank Team to raise funds and giving personally as well. The Bank itself serves as a Corporate Sponsor.

United Way: Lorraine Willet, Training Manager, champions the United Way efforts within Union Bank. She is the current President of the local United Way Board and has been involved for over nine years. Passionate about the difference the United Way makes, Lorraine sees even greater importance in its work with today's economy. Last year the United Way contributed to the efforts of various organizations working towards more affordable housing and ensuring that people in need have enough to eat and can heat their homes.

This is just a sampling of the many ways that our employees step up to make a difference. We all benefit from their exemplary dedication to our community and our collective quality of life.

| 'Ken Do' Attitudes | |

At the annual meeting, the position of CEO of both Union Bankshares and Union Bank will transfer from Ken Gibbons to David Silverman. Ken will remain Chairman of both Companies' Boards, his wisdom never more than a phone call away. We are excited for Ken as he embarks on what we know will be a very active retirement. He leaves us ready for the transition for many reasons, just some of which are captured below.

Robyn Masi, our Branch Manager in Stowe, has worked with Ken for nearly 20 years. Robyn had this to say about her growth through the organization:

"Not only has he been a great role model, but a wonderful mentor for me. I had the pleasure to work directly under him for a brief time, and the knowledge I gained during that time was tremendous. He has taken the time, many times, to meet with me and teach me about different parts of the banking world. Without his leadership and guidance, I know I would not be where I am today. He will be greatly missed and I will never forget the valuable lessons he has taught me, both personally and professionally, as I have "grown up" with Union Bank."

Chris Latulip has been with Union Bank since 2010. She is the Regional Vice President for our New Hampshire territory. Chris saw first-hand how important it is to be accessible.

"Ken knew it was better to develop a team around him than to manage from the top down. He shows so much respect for everyone at Union Bank, and he takes the time to genuinely thank us. We have confidence in what we do, because Ken has taught us that without each and everyone of us, Union Bank couldn't be what it is today. It is important to Ken to have an open door policy; to know his staff, to be abreast of what is happening, but in a quiet way. My management style is a reflection of that model."

Tracey Holbrook is our Regional Vice President for northeastern Vermont. She began her career with us just out of college when she took a part-time teller position.

"I am a stronger person because of Ken. He has never let me, or anyone else, take the easy route. He makes us work hard and then raises the bar. I have learned that satisfactory is not good enough. At the same time, Ken has never left us to reach our goals alone. He has always been right there, guiding, pushing and helping us get to the next level... and the next."

Union Bankshares, Inc.8

As our CFO since 1989, Marsha Mongeon has a long history of working with Ken on a daily basis. Ken has taught her to see the people beyond the numbers.

"Ken has taught me that the first responsibility is to the shareholders. I used to look at numbers in a vacuum, but now I step back and ask myself 'what is best for our shareholders?' And equally as important is how Union Bank is perceived in the community. Ken has demonstrated that it's pitching in that matters. It doesn't matter if the job is heading a fund drive or flipping the burgers. What's important is getting involved and sharing your talents."

We also asked some community members if they would share their thoughts on Ken.

Melvyn Patashnick, CEO, Copley Health Systems, Inc.

"Ken cares about our community; he demonstrates it regularly with both his personal and professional actions. After many years as a trustee of the hospital, Ken continues to serve as a community member on several hospital committees. He has been instrumental in ensuring the long-term fiscal health of our community hospital. We count on Ken's solid advice and valuable perspective to fulfill our mission of promoting wellness and providing access to health care services regardless of ability to pay."

Darcy Carter, District Director, SBA Vermont District Office

"When I think of the qualities that make a great colleague and a true professional with a legacy, I think this is a person that I trust will tell me the truth and who will ask the truth of me. This person will have reasoning and principle behind decisions and will follow through on commitments. This person will be skilled and wise from experience, and ready to share knowledge, successes and failures, with the broader community. This is a familiar face I cross the room to see at events, who is ready with candid insights and who genuinely enjoys doing business together in Vermont. We wish Ken the very best and thank him for his great partnership over the years."

David Silverman sums it up for all of us:

"Though Ken will be leaving the day-to-day banking business behind, his imprint on the Company will last for years to come through the staff he has had a hand in recruiting, encouraging and mentoring. Many of us have learned valuable lessons from Ken as he has instilled a strong work ethic, desire to achieve and professional integrity throughout our ranks. We are grateful to Ken for developing a strong team as his legacy, one that is prepared to meet the future challenges and opportunities we will face together."

Union Bankshares, Inc.9

| |

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

The Board of Directors and Shareholders

Union Bankshares, Inc. and Subsidiary

We have audited the accompanying consolidated balance sheets of Union Bankshares, Inc. and Subsidiary (the Company) as of December 31, 2011 and 2010, and the related consolidated statements of income, changes in stockholders' equity, and cash flows for the years then ended. These consolidated financial statements are the responsibility of the Company's management. Our responsibility is to express an opinion on these consolidated financial statements based on our audits.

We conducted our audits in accordance with standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. The Company is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. Our audits included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Company's internal control over financial reporting. Accordingly, we express no such opinion. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the consolidated financial statements referred to above present fairly, in all material respects, the consolidated financial position of Union Bankshares, Inc. and Subsidiary as of December 31, 2011 and 2010, and the consolidated results of their operations and their consolidated cash flows for the years then ended, in conformity with accounting principles generally accepted in the United States of America.

| |

Portland, Maine

March 28, 2012

Vermont Registration No. 92-0000278

| ||

Union Bankshares, Inc.10

UNION BANKSHARES, INC. AND SUBSIDIARY

CONSOLIDATED BALANCE SHEETS

December 31, 2011 and 2010

| 2011 | 2010 | |||||

| Assets | (Dollars in thousands) | |||||

| Cash and due from banks | $ | 5,871 | $ | 5,447 | ||

| Federal funds sold and overnight deposits | 18,510 | 8,845 | ||||

| Cash and cash equivalents | 24,381 | 14,292 | ||||

| Interest bearing deposits in banks | 24,020 | 14,041 | ||||

| Investment securities available-for-sale | 42,954 | 23,780 | ||||

Investment securities held-to-maturity (fair value $4.0 million and $502 thousand at December 31, 2011 and December 31, 2010, respectively) | 4,000 | 500 | ||||

| Loans held for sale | 4,888 | 5,611 | ||||

| Loans | 424,319 | 376,272 | ||||

| Allowance for loan losses | (4,226 | ) | (3,755 | ) | ||

| Net deferred loan costs | 177 | 188 | ||||

| Net loans | 420,270 | 372,705 | ||||

| Accrued interest receivable | 1,810 | 1,560 | ||||

| Premises and equipment, net | 9,163 | 7,842 | ||||

| Core deposit intangible | 1,608 | — | ||||

| Goodwill | 2,223 | — | ||||

| Investment in real estate limited partnerships | 4,473 | 2,344 | ||||

| Company-owned life insurance | 3,676 | 1,569 | ||||

| Other assets | 9,285 | 8,751 | ||||

| Total assets | $ | 552,751 | $ | 452,995 | ||

| Liabilities and Stockholders’ Equity | ||||||

| Liabilities | ||||||

| Deposits | ||||||

| Noninterest bearing | $ | 76,656 | $ | 64,526 | ||

| Interest bearing | 239,058 | 180,386 | ||||

| Time | 157,725 | 131,748 | ||||

| Total deposits | 473,439 | 376,660 | ||||

| Borrowed funds | 29,015 | 28,986 | ||||

| Liability for defined benefit pension plan | 5,679 | 2,451 | ||||

| Accrued interest and other liabilities | 4,279 | 3,173 | ||||

| Total liabilities | 512,412 | 411,270 | ||||

| Commitments and Contingencies (Notes 8,15,16,17,18 and 21) | ||||||

| Stockholders’ Equity | ||||||

Common stock, $2.00 par value; 7,500,000 shares authorized; 4,923,286 shares issued at December 31, 2011 and 4,921,786 shares issued at December 31, 2010 | 9,847 | 9,844 | ||||

| Additional-paid-in capital | 276 | 244 | ||||

| Retained earnings | 38,385 | 37,623 | ||||

Treasury stock at cost; 466,082 shares at December 31, 2011 and December 31, 2010 | (3,823 | ) | (3,823 | ) | ||

| Accumulated other comprehensive loss | (4,346 | ) | (2,163 | ) | ||

| Total stockholders' equity | 40,339 | 41,725 | ||||

| Total liabilities and stockholders' equity | $ | 552,751 | $ | 452,995 | ||

See accompanying notes to consolidated financial statements.

Union Bankshares, Inc.11

UNION BANKSHARES, INC. AND SUBSIDIARY

CONSOLIDATED STATEMENTS OF INCOME

Years Ended December 31, 2011 and 2010

| 2011 | 2010 | |||||

| Interest income | (Dollars in thousands except per share data) | |||||

| Interest and fees on loans | $ | 22,269 | $ | 21,462 | ||

| Interest on debt securities: | ||||||

| Taxable | 716 | 710 | ||||

| Tax exempt | 326 | 298 | ||||

| Dividends | 15 | 4 | ||||

| Interest on federal funds sold and overnight deposits | 34 | 22 | ||||

| Interest on interest bearing deposits in banks | 309 | 411 | ||||

| Total interest income | 23,669 | 22,907 | ||||

| Interest expense | ||||||

| Interest on deposits | 2,825 | 2,977 | ||||

| Interest on short-term borrowed funds | 18 | 18 | ||||

| Interest on long-term debt | 1,065 | 1,122 | ||||

| Total interest expense | 3,908 | 4,117 | ||||

Net interest income | 19,761 | 18,790 | ||||

| Provision for loan losses | 775 | 520 | ||||

Net interest income after provision for loan losses | 18,986 | 18,270 | ||||

| Noninterest income | ||||||

| Trust income | 557 | 490 | ||||

| Service fees | 4,367 | 4,028 | ||||

| Net gains on sales of investment securities available-for-sale | 183 | 98 | ||||

| Net gains on sales of loans held for sale | 1,566 | 736 | ||||

| Other income | 452 | 297 | ||||

| Total noninterest income | 7,125 | 5,649 | ||||

| Noninterest expenses | ||||||

| Salaries and wages | 7,743 | 6,559 | ||||

| Pension and other employee benefits | 3,153 | 2,828 | ||||

| Occupancy expense, net | 1,121 | 937 | ||||

| Equipment expense | 1,220 | 1,057 | ||||

| ATM and debit card expense | 613 | 447 | ||||

| Communications | 363 | 261 | ||||

| Advertising and public relations | 466 | 283 | ||||

| Vermont franchise tax | 429 | 414 | ||||

| FDIC insurance assessment | 376 | 499 | ||||

| Equity in losses of limited partnerships | 515 | 426 | ||||

| Branch acquisition expenses | 407 | 13 | ||||

| Other expenses | 3,367 | 2,906 | ||||

| Total noninterest expenses | 19,773 | 16,630 | ||||

Income before provision for income taxes | 6,338 | 7,289 | ||||

| Provision for income taxes | 1,119 | 1,702 | ||||

Net income | $ | 5,219 | $ | 5,587 | ||

| Earnings per common share | $ | 1.17 | $ | 1.25 | ||

| Dividends per common share | $ | 1.00 | $ | 1.00 | ||

See accompanying notes to consolidated financial statements.

Union Bankshares, Inc.12

UNION BANKSHARES, INC. AND SUBSIDIARY

CONSOLIDATED STATEMENTS OF CHANGES IN STOCKHOLDERS' EQUITY

Years Ended December 31, 2011 and 2010

| Common Stock | ||||||||||||||||||||

Shares, net of treasury | Amount | Additional paid-in capital | Retained earnings | Treasury stock | Accumulated other comprehensive loss | Total stockholders’ equity | ||||||||||||||

| (Dollars in thousands) | ||||||||||||||||||||

| Balances, December 31, 2009 | 4,461,208 | $ | 9,844 | $ | 219 | $ | 36,494 | $ | (3,724 | ) | $ | (1,653 | ) | $ | 41,180 | |||||

| Comprehensive income: | ||||||||||||||||||||

| Net income | — | — | — | 5,587 | — | — | 5,587 | |||||||||||||

Other comprehensive loss, net of tax: | ||||||||||||||||||||

Change in net unrealized gain on investment securities available-for-sale, net of reclassification adjustment and tax effects | — | — | — | — | — | (184 | ) | (184 | ) | |||||||||||

Change in net unrealized loss on unfunded defined benefit pension plan liability, net of reclassification adjustment and tax effects | — | — | — | — | — | (326 | ) | (326 | ) | |||||||||||

Total other comprehensive loss | (510 | ) | ||||||||||||||||||

| Total comprehensive income | 5,077 | |||||||||||||||||||

Cash dividends declared ($1.00 per share) | — | — | — | (4,458 | ) | — | — | (4,458 | ) | |||||||||||

Stock based compensation expense | — | — | 25 | — | — | — | 25 | |||||||||||||

| Purchase of treasury stock | (5,504 | ) | — | — | — | (99 | ) | — | (99 | ) | ||||||||||

| Balances, December 31, 2010 | 4,455,704 | 9,844 | 244 | 37,623 | (3,823 | ) | (2,163 | ) | 41,725 | |||||||||||

| Comprehensive income: | ||||||||||||||||||||

| Net income | — | — | — | 5,219 | — | — | 5,219 | |||||||||||||

Other comprehensive income (loss), net of tax: | ||||||||||||||||||||

Change in net unrealized gain on investment securities available-for-sale, net of reclassification adjustment and tax effects | — | — | — | — | — | 718 | 718 | |||||||||||||

Change in net unrealized loss on unfunded defined benefit plan liability, net of reclassification adjustment and tax effects | — | — | — | — | — | (2,901 | ) | (2,901 | ) | |||||||||||

Total other comprehensive loss | (2,183 | ) | ||||||||||||||||||

| Total comprehensive income | 3,036 | |||||||||||||||||||

| Issuance of common stock | 1,500 | 3 | 23 | — | — | — | 26 | |||||||||||||

Cash dividends declared ($1.00 per share) | — | — | — | (4,457 | ) | — | — | (4,457 | ) | |||||||||||

| Stock based compensation expense | — | — | 9 | — | — | — | 9 | |||||||||||||

| Balances, December 31, 2011 | 4,457,204 | $ | 9,847 | $ | 276 | $ | 38,385 | $ | (3,823 | ) | $ | (4,346 | ) | $ | 40,339 | |||||

See accompanying notes to consolidated financial statements.

Union Bankshares, Inc.13

UNION BANKSHARES, INC. AND SUBSIDIARY

CONSOLIDATED STATEMENTS OF CASH FLOWS

Years Ended December 31, 2011 and 2010

| 2011 | 2010 | |||||

| (Dollars in thousands) | ||||||

| Cash Flows From Operating Activities | ||||||

| Net income | $ | 5,219 | $ | 5,587 | ||

| Adjustments to reconcile net income to net cash provided by operating activities: | ||||||

| Depreciation | 692 | 660 | ||||

| Provision for loan losses | 775 | 520 | ||||

| Deferred income tax provision (benefit) | 595 | (96 | ) | |||

| Net amortization of investment securities | 63 | 25 | ||||

| Equity in losses of limited partnerships | 515 | 426 | ||||

| Stock based compensation expense | 9 | 25 | ||||

| Net decrease (increase) in unamortized loan costs | 11 | (111 | ) | |||

| Proceeds from sales of loans held for sale | 81,939 | 53,399 | ||||

| Origination of loans held for sale | (79,650 | ) | (49,011 | ) | ||

| Net gains on sales of loans held for sale | (1,566 | ) | (736 | ) | ||

| Net losses on disposals of premises and equipment | 1 | 6 | ||||

| Net gains on sale of investment securities available-for-sale | (183 | ) | (98 | ) | ||

| Net gains on sales of repossessed property | (4 | ) | — | |||

| Write-downs of impaired assets | 278 | 9 | ||||

| Net gains on sales of other real estate owned | (133 | ) | (38 | ) | ||

| (Increase) decrease in accrued interest receivable | (53 | ) | 74 | |||

| Amortization of core deposit intangible | 100 | — | ||||

| (Increase) decrease in other assets | (150 | ) | 738 | |||

| Contribution to defined benefit pension plan | (2,000 | ) | (1,250 | ) | ||

| Increase in other liabilities | 900 | 1,128 | ||||

| Net cash provided by operating activities | 7,358 | 11,257 | ||||

| Cash Flows From Investing Activities | ||||||

| Interest bearing deposits in banks | ||||||

| Proceeds from maturities and redemptions | 7,985 | 18,543 | ||||

| Purchases | (17,964 | ) | (9,609 | ) | ||

| Investment securities held-to-maturity | ||||||

| Proceeds from maturities, calls and paydowns | 2,000 | 1,500 | ||||

| Purchases | (5,500 | ) | (2,000 | ) | ||

| Investment securities available-for-sale | ||||||

| Proceeds from sales | 2,326 | 1,097 | ||||

| Proceeds from maturities, calls and paydowns | 11,134 | 11,745 | ||||

| Purchases | (31,426 | ) | (12,180 | ) | ||

| Net increase in loans | (16,055 | ) | (28,895 | ) | ||

| Recoveries of loans charged off | 44 | 57 | ||||

| Purchases of premises and equipment | (1,497 | ) | (896 | ) | ||

| Investments in limited partnerships | (1,752 | ) | (179 | ) | ||

| Purchase of company-owned life insurance | (2,000 | ) | — | |||

| Purchase of nonmarketable equity securities | (54 | ) | — | |||

| Proceeds from sales of other real estate owned | 517 | 422 | ||||

| Proceeds from sales of repossessed property | 4 | 28 | ||||

| Cash acquired, net of cash paid, in branch acquisitions | 29,607 | — | ||||

Net cash used by investing activities | (22,631 | ) | (20,367 | ) | ||

Union Bankshares, Inc.14

| Cash Flows From Financing Activities | ||||||

| Advances of long-term debt | — | 2,978 | ||||

| Repayment of long-term debt | (4,639 | ) | (1,544 | ) | ||

| Net increase (decrease) in short-term borrowings outstanding | 1,444 | (3,440 | ) | |||

| Net increase in noninterest bearing deposits | 8,571 | 4,397 | ||||

| Net increase in interest bearing deposits | 25,160 | 6,386 | ||||

| Net decrease in time deposits | (743 | ) | (2,950 | ) | ||

| Issuance of common stock | 26 | — | ||||

| Purchase of treasury stock | — | (99 | ) | |||

| Dividends paid | (4,457 | ) | (4,458 | ) | ||

| Net cash provided by financing activities | 25,362 | 1,270 | ||||

| Net increase (decrease) in cash and cash equivalents | 10,089 | (7,840 | ) | |||

| Cash and cash equivalents | ||||||

| Beginning of year | 14,292 | 22,132 | ||||

| End of year | $ | 24,381 | $ | 14,292 | ||

| Supplemental Disclosures of Cash Flow Information | ||||||

| Interest paid | $ | 3,942 | $ | 4,285 | ||

| Income taxes paid | $ | 725 | $ | 1,605 | ||

| Supplemental Schedule of Noncash Investing and Financing Activities | ||||||

| Other real estate acquired in settlement of loans | $ | 1,127 | $ | 1,484 | ||

| Other assets acquired in settlement of loans | $ | 40 | $ | 26 | ||

| Loans originated to finance the sale of other real estate owned | $ | 597 | $ | 376 | ||

| Investment in limited partnerships acquired by capital contributions payable | $ | 893 | $ | — | ||

| Assets acquired and liabilities assumed in branch acquisitions (Note 9): | ||||||

| Loans and other non-cash assets, excluding goodwill and core deposit intangible | $ | 33,624 | $ | — | ||

| Deposits and other liabilities | $ | 67,162 | $ | — | ||

See accompanying notes to consolidated financial statements.

Union Bankshares, Inc.15

UNION BANKSHARES, INC. AND SUBSIDIARY

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

Note 1. Significant Accounting Policies

Basis of financial statement presentation

The accounting and reporting policies of Union Bankshares, Inc. and Subsidiary (the “Company”) are in conformity with U.S. generally accepted accounting principles (“GAAP”) and general practices within the banking industry. The following is a description of the more significant policies.

The consolidated financial statements include the accounts of Union Bankshares, Inc., and its wholly owned subsidiary, Union Bank (“Union”) headquartered in Morrisville, Vermont. All significant intercompany transactions and balances have been eliminated. The Company utilizes the accrual method of accounting for financial reporting purposes.

The Company meets the qualification requirements under Securities and Exchange Commission rules for smaller reporting companies and, pursuant to such rules, has elected to present audited statements of income, cash flows and changes in stockholders' equity for each of the most recent two, rather than three, fiscal years.

Certain amounts in the 2010 financial statements have been reclassified to conform to the current year presentation.

Nature of operations

The Company provides a variety of financial services to individuals, municipalities, commercial and nonprofit customers through its branches, ATMs, telebanking and internet banking systems in northern Vermont and northwestern New Hampshire. This market area encompasses primarily retail consumers, small businesses, municipalities, agricultural producers and the tourism industry. The Company's primary deposit products are checking, savings, money market accounts, certificates of deposit and individual retirement accounts and its primary lending products are commercial, real estate, municipal and consumer loans.

Concentration of risk

The Company's operations are affected by various risk factors, including interest rate risk, credit risk, and risk from geographic concentration of its deposit taking and lending activities. Management attempts to manage interest rate risk through various asset/liability management techniques designed to match maturities/repricing of assets and liabilities. Loan policies and administration are designed to provide assurance that loans will only be granted to creditworthy borrowers, although credit losses are expected to occur because of subjective factors and factors beyond the control of the Company. Although national economic conditions have been volatile during the last three years, local economic conditions have been somewhat more stable. The Company has a diversified loan portfolio with a substantial portion of the Company's loans secured by real estate and/or partially guaranteed by a U.S. Government agency. Most of its lending activities are conducted within the northern Vermont and northwestern New Hampshire market area where it is located. As a result, the Company and its borrowers may be especially vulnerable to the consequences of changes in the local economy and real estate market conditions. Notes 5 and 6 discuss the types of lending in which the Company engages.

Use of estimates in preparation of financial statements

The preparation of consolidated financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosures of contingent

Union Bankshares, Inc.16

assets and liabilities at the date of the consolidated financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could materially differ from those estimates. Material estimates that are particularly susceptible to significant change in the near term and involve inherent uncertainties relate to the determination of the allowance for losses on loans, the valuation of real estate acquired in connection with foreclosures or in satisfaction of loans, deferred tax assets, judgments regarding valuation and impairment of investment securities and other assets as well as pension plan accounting. These estimates involve a significant degree of complexity and subjectivity and the amount of the change that is reasonably possible, should any of these estimates prove inaccurate, cannot be estimated.

Presentation of cash flows

For purposes of presentation in the consolidated statements of cash flows, cash and cash equivalents includes cash on hand, amounts due from banks (including cash items in process of clearing), federal funds sold (generally purchased and sold for one day periods) and overnight deposits.

Trust operations

Assets held by the Trust & Asset Management Group of Union in a fiduciary or agency capacity, other than trust cash on deposit with Union, are not included in these consolidated financial statements because they are not assets of Union or the Company.

Fair value measurements

The Company utilizes the Financial Accounting Standards Board (“FASB”) Accounting Standards Codification (“ASC”) Topic 820, Fair Value Measurements and Disclosures, as guidance for accounting for assets and liabilities carried at fair value. This standard defines fair value as the price that would be received, without adjustment for transaction costs, to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. Fair value is a market based measurement that should be determined based on assumptions that market participants would use in pricing an asset or liability. The guidance in FASB ASC Topic 820 establishes a three-level fair value hierarchy, which prioritizes the inputs used in measuring fair value. A financial instrument's level within the fair value hierarchy is based on the lowest level of input that is significant to the fair value measurement.

The three levels of the fair value hierarchy are:

| • | Level 1 - Unadjusted quoted prices in active markets that are accessible at the measurement date for identical, unrestricted assets or liabilities; |

| • | Level 2 - Quoted prices for similar assets or liabilities in active markets, quoted prices in markets that are not active, or inputs that are observable, either directly or indirectly, for substantially the full term of the asset or liability; |

| • | Level 3 - Prices or valuation techniques that require inputs that are both significant to the fair value measurement and unobservable (i.e., supported by little or no market activity). |

Investment securities

Investment securities purchased and held primarily for resale in the near future are classified as trading securities and are reported at fair value with unrealized gains and losses included in earnings. Debt securities the Company has the positive intent and ability to hold to maturity are classified as held-to-maturity and reported at amortized cost. Debt and equity securities not classified as either held-to-maturity or trading are classified as available-for-sale. Investments classified as available-for-sale are reported at fair value.

Union Bankshares, Inc.17

Accretion of discounts and amortization of premiums arising at acquisition on investment securities are included in income using the effective interest method over the life of the securities to maturity or call date. Unrealized gains and losses on investment securities available-for-sale are excluded from earnings and reported in Accumulated other comprehensive income (loss), net of tax and reclassification adjustment, as a separate component of stockholders' equity. The specific identification method is used to determine realized gains and losses on sales of available-for-sale or trading securities.

An unrealized loss is generally deemed to be other than temporary and a credit loss on a debt security is deemed to exist if the present value of the expected future cash flows is less than the amortized cost basis of the security. The credit loss component of an other than temporary write down is reflected in earnings as realized losses in other income. The remaining portion of the impairment loss is recognized in other comprehensive income (loss), provided the Company does not intend to sell the underlying debt security and it is “more likely than not” that the Company will not have to sell the debt security prior to recovery.

Loans held for sale

Loans originated and intended for sale in the secondary market are carried at the lower of cost or estimated fair value in the aggregate. The estimated fair value of loans held for sale is based on current price quotes that determine the amount that the loans could be sold for in the secondary market. Loans transferred from held for sale to portfolio are transferred at the lower of cost or fair value in the aggregate. Sales are normally made without recourse. Gains and losses on the disposition of loans held for sale are determined on the specific identification basis. Net unrealized losses are recognized through a valuation allowance by charges to income.

Loans

Loans receivable that management has the intent and ability to hold for the foreseeable future or until maturity or payoff are reported at their unpaid principal balances, adjusted for any charge-offs, the allowance for loan losses, and any deferred fees or costs on originated loans and unamortized premiums or discounts on purchased loans.

Loan interest income is accrued daily on outstanding balances. The following accounting policies, related to accrual and nonaccrual loans, apply to all loan segments and classes. The Company considers its loan segments and loan classes to be the same. The accrual of interest is discontinued when a loan is specifically determined to be impaired and/or management believes, after considering collection efforts and other factors, that the borrowers' financial condition is such that collection of interest is doubtful. Normally, any unpaid interest previously accrued on those loans is reversed against current period interest income. A loan may be restored to accrual status when its financial status has significantly improved and there is no principal or interest past due. A loan may also be restored to accrual status if the borrower makes six consecutive monthly payments or the lump sum equivalent. Income on nonaccrual loans is generally not recognized unless a loan is placed back in accrual status or after all principal has been collected. Interest income generally is not recognized on impaired loans unless the likelihood of further loss is remote. Interest payments received on such loans are generally applied as a reduction of the loan principal balance. Delinquency status is determined based on contractual terms for all loan segments and classes.

Loans purchased in the branch acquisition are recorded at the estimated fair market value at the time of purchase. The estimated fair value contains both accretable and nonaccretable components. The accretable component is amortized as an adjustment to the related loan yield over the average life of the loan. The nonaccretable component represents probable loss due to credit risk and is reviewed by management periodically and adjusted as deemed necessary.

Union Bankshares, Inc.18

Loan origination fees and direct loan origination costs are deferred and amortized as an adjustment of the related loan's yield using methods that approximate the interest method. The Company generally amortizes these amounts over the estimated average life of the related loans.

Allowance for loan losses

The allowance for loan losses is established for estimated losses in the loan portfolio through a provision for loan losses charged to earnings. For all loan classes, loan losses are charged against the allowance when management believes the loan balance is uncollectible or in accordance with federal guidelines. Subsequent recoveries, if any, are credited to the allowance.

The allowance for loan losses is maintained at a level believed by management to be appropriate to absorb probable credit losses inherent in the loan portfolio as of the balance sheet date. The amount of the allowance is based on management's periodic evaluation of the collectability of the loan portfolio, including the nature, volume and risk characteristics of the portfolio, credit concentrations, trends in historical loss experience, estimated value of any underlying collateral, specific impaired loans and economic conditions. While management uses available information to recognize losses on loans, future additions to the allowance for loan losses may be necessary based on changes in economic conditions or other relevant factors.

In addition, various regulatory agencies, as an integral part of their examination process, regularly review the Company's allowance for loan losses. Such agencies may require the Company to recognize additions to the allowance for loan losses based on their judgments about information available to them at the time of their examination, which may not be currently available to management.

The allowance consists of specific, general and unallocated components. The specific component relates to the loans that are classified as either substandard or doubtful. For such loans, the level of allowance allocable to those loans is determined through estimating probable loss for each individual credit based on its specific risk attributes. Loans are also evaluated for impairment and may be classified as impaired when management believes it is probable that the Company will not collect all the contractual interest and principal payments as scheduled in the loan agreement. Impaired loans may also include troubled loans that are restructured. A troubled debt restructuring occurs when the Company, for economic or legal reasons related to the borrower's financial difficulties, grants a concession to the borrower that would otherwise not be granted. Troubled debt restructuring may include the transfer of assets to the Company in partial satisfaction of a troubled loan, a modification of a loan's terms (such as reduction of stated interest rates below market rates, extension of maturity that does not conform to the Company's policies or procedures, reduction of face amount of the loan, reduction of accrued interest, reduction or deferment of cash payments in the near future), or a combination of both. A specific reserve amount is allocated to the allowance for individual loans that have been classified as impaired on the basis of the fair value of the collateral for collateral dependent loans, an observable market price, or the present value of anticipated future cash flows. The Company recognizes the change in present value attributable to the passage of time as provision for loan losses. Large groups of smaller balance homogeneous loans are collectively evaluated for impairment. Accordingly, the Company does not separately identify individual consumer, residential or small balance commercial loans for impairment evaluation, unless such loans are subject to a restructuring agreement or have been identified as impaired as part of a larger customer relationship.

The general component represents the level of allowance allocable to each loan portfolio segment with similar risk characteristics and is determined based on historical loss experience, adjusted for qualitative factors, for each class of loan. The Company considers its loan segments and loan classes to be the same. Management deems a five year average to be an appropriate time frame on which to base historical losses for each portfolio segment. Qualitative factors considered include underwriting, economic and market conditions, portfolio composition, collateral values, delinquencies, lender experience and legal issues. The qualitative factors are determined based on the various risk

Union Bankshares, Inc.19

characteristics of each portfolio segment. Risk characteristics relevant to each portfolio segment are as follows:

| • | Residential real estate - Loans in this segment are collateralized by owner-occupied 1-4 family residential real estate, second and vacation 1-4 family homes, 1-4 family investment properties, home equity and second mortgage loans. Repayment is dependent on the credit quality of the individual borrower. The overall health of the economy, including unemployment rates and housing prices, could have an affect on the credit quality of this segment. |

| • | Construction real estate - Loans in this segment include residential and commercial construction properties, land and land development loans. Repayment is dependent on the credit quality of the individual borrower and/or the underlying cash flows generated by the properties being constructed. The overall health of the economy, including unemployment rates, housing prices, vacancy rates and material costs, could have an affect on the credit quality of this segment. |

| • | Commercial real estate - Loans in this segment are primarily properties occupied by businesses or income-producing properties. The underlying cash flows generated by the properties may be adversely impacted by a downturn in the economy as evidenced by a general slowdown in business or increased vacancy rates which, in turn, could have an affect on the credit quality of this segment. Management requests business financial statements at least annually and monitors the cash flows of these loans. |

| • | Commercial - Loans in this segment are made to businesses and are generally secured by non real estate assets of the business. Repayment is expected from the cash flows of the business. A weakened economy, and resultant decreased consumer spending, could have an affect on credit quality of this segment. |

| • | Consumer - Loans in this segment are made to individuals for personal expenditures, such as an automobile purchase, and include unsecured loans. Repayment is primarily dependent on the credit quality of the individual borrower. The overall health of the economy, including unemployment, could have an affect on the credit quality of this segment. |

| • | Municipal - Loans in this segment are made to municipalities located within the Company's service area. Repayment is primarily dependent on taxes or other funds collected annually by the municipalities. Management considers there to be minimal risk surrounding the credit quality of this segment. |

An unallocated component is maintained to cover uncertainties that could affect management's estimate of probable losses. The unallocated component of the allowance reflects the margin of imprecision inherent in the underlying assumptions used in the methodologies for estimating specific and general losses in the portfolio.

All evaluations are inherently subjective as they require estimates that are susceptible to significant revision as more information becomes available or as changes occur in economic conditions or other relevant factors.

Other real estate owned

Real estate properties acquired through or in lieu of loan foreclosure are to be sold and are initially recorded based on an independent appraisal or a broker price opinion at the estimated fair value less estimated selling costs at the date of acquisition establishing a new carrying basis. Thereafter, valuations are periodically performed by management, and the real estate is carried in Other assets at the lower of carrying amount or fair value, less estimated cost to sell. Costs of significant property improvements are capitalized, whereas revenue and expenses from operations and changes in valuation are charged to Other expenses on the Company's statement of income.

Union Bankshares, Inc.20

Premises and equipment

Premises and equipment are stated at cost, less accumulated depreciation. Depreciation is computed principally by the straight line method over the estimated useful lives of the assets. The cost of assets sold or otherwise disposed of and the related accumulated depreciation are eliminated from the accounts and the resulting gains or losses are reflected in the statement of income. Maintenance and repairs are charged to current expense as incurred and the costs of major renewals and betterments are capitalized. Construction in progress is stated at cost, which includes the cost of construction and other direct costs attributable to the construction. No provision for depreciation is made on construction in progress until such time as the relevant assets are completed and put into use.

Intangible assets

Intangible assets include goodwill, which represents the excess of the purchase price over the fair value of net assets acquired in the 2011 acquisition of three New Hampshire branch offices, as well as a core deposit intangible related to the deposits acquired (see Note 9). The core deposit intangible is amortized on a straight line basis over the estimated average life of the core deposit base of 10 years. The Company evaluates the valuation and amortization of the core deposit intangible if events occur that could result in possible impairment. In accordance with current authoritative guidance, the Company assesses qualitative factors to determine whether the existence of events or circumstances leads to a determination that it is more likely than not that the fair value of the Company is less than its carrying amount, which could result in goodwill impairment.

Federal Home Loan Bank stock

As a member of the Federal Home Loan Bank (“FHLB”) of Boston, Union is required to invest in Class B common stock of the FHLB of Boston. The Class B common stock has a five year notice requirement for redemption and there is no guarantee of future redemption. Also, there is the possibility of future capital calls by the FHLB of Boston on member banks to ensure compliance with its capital plan. FHLB of Boston stock is reported in Other assets at its par value of $1.9 million at December 31, 2011 and 2010. The stock is nonmarketable, and is redeemable by the FHLB of Boston at par value.

Company-owned life insurance

Company-owned life insurance (“COLI”) represents life insurance on the lives of certain current or former directors or employees who have provided positive consent allowing the Company to be the beneficiary of such policies. The Company utilizes COLI as tax-efficient funding for the benefit obligations to its employees and directors, including obligations under one of the Company's nonqualified deferred compensation plans. See Note 15. The Company is the primary beneficiary of the insurance policies. Increases in the cash value of the policies, as well as any gain on insurance proceeds received, are recorded in Other income, and are not currently subject to income taxes. COLI is recorded at the cash value of the policies, less any applicable cash surrender charges of which there are currently none. The Company reviews the financial strength of the insurance carriers prior to the purchase of COLI to ensure minimum credit ratings of at least investment grade. The financial strength of the carriers is reviewed annually and COLI with any individual carrier is limited by Company policy to 10% of capital plus reserves.

Union Bankshares, Inc.21

Servicing assets

Servicing assets are recognized as separate assets when servicing rights are acquired through purchase or sale of loans with servicing rights retained. Capitalized servicing rights are reported in Other assets, are initially recorded at estimated fair market value and are amortized against noninterest income in proportion to, and over the period of, the estimated future net servicing income of the underlying loans. The estimated fair value of capitalized servicing rights represents the present value of the future servicing fees arising from the right to service loans that have been previously sold. Servicing assets are evaluated regularly for impairment based upon the fair value of the rights as compared to amortized cost. Impairment is determined by stratifying rights by predominant characteristics, such as interest rates and terms. Fair value of a stratum is determined using prices for similar assets with similar characteristics, when available, or based upon discounted cash flows using market-based assumptions.

Impairment is recognized through a valuation allowance for an individual stratum, to the extent that estimated fair value is less than the capitalized amount for the stratum.

Investment in real estate limited partnerships

The Company has purchased various limited partnership interests in affordable housing partnerships. These partnerships were established to acquire, own and rent residential housing for elderly, low or moderate income residents in northeastern and central Vermont or in northwestern New Hampshire. The investments are accounted for under a method approximating the equity method of accounting. These equity investments are recorded at cost and adjusted for the Company's proportionate share of the partnerships' undistributed earnings or losses through the statement of income.

Pension plans

Union maintains a noncontributory defined benefit pension plan covering all eligible employees who meet certain service requirements. The costs of this plan, based on actuarial computations of current and estimated future benefits for employees, are charged to Pension and other employee benefits.

Union also has a contributory 401(k) pension plan covering all employees who meet certain service requirements. The plan is voluntary, and Union, through the discretionary matching component of the plan, contributed fifty cents for every dollar contributed by participants, up to six percent of each participant's salary in 2011 and 2010.

Advertising costs

The Company expenses advertising costs as incurred and they are included in Advertising and public relations in the Company's income statement.

Earnings per common share

Earnings per common share for the period are computed based on the weighted average number of shares of common stock issued, retroactively adjusted for stock splits and stock dividends and reduced for shares held in treasury. The weighted average shares outstanding were 4,456,842 and 4,458,193 for the years ended December 31, 2011 and 2010, respectively. There were options with respect to 14,000 shares and 15,000 shares outstanding at December 31, 2011 and December 31, 2010, respectively, excluded from the computation of diluted earnings per share since dilution resulting from these stock options would be immaterial.

Union Bankshares, Inc.22

Income taxes

The Company prepares its federal income tax return on a consolidated basis. Federal income taxes are allocated to members of the consolidated group based on taxable income. The Company recognizes income taxes under the asset and liability method. This involves estimating the Company's actual current tax exposure as well as assessing temporary differences resulting from differing treatment of items, such as timing of the deduction of expenses, for tax and GAAP purposes. These differences result in deferred tax assets and liabilities, which are netted and included in Other assets. Deferred tax assets and liabilities are measured using enacted tax rates expected to apply to taxable income in the years in which those temporary differences are expected to be recovered or settled. The Company must also assess the likelihood that any deferred tax assets will be recovered from future taxable income and to the extent that recovery is not likely, a valuation allowance must be established. Significant management judgment is required in determining the provision for income taxes and deferred tax assets and liabilities. Affordable housing tax credits are recognized as a reduction of the Provision for income taxes in the year they are earned.

Off-balance-sheet financial instruments

In the ordinary course of business, the Company is a party to off-balance-sheet financial instruments consisting of commitments to originate credit, unused lines of credit including commitments under credit card arrangements, commitments to purchase investment securities, commitments to invest in real estate limited partnerships, commercial letters of credit, standby letters of credit and risk-sharing commitments on certain sold loans. Such financial instruments are recorded in the financial statements when they become fixed and certain.

Comprehensive income (loss)

Accounting principles generally require that recognized revenue, expenses, gains and losses be included in net income or loss. Certain changes in assets and liabilities, such as the after tax effect of unrealized gains and losses on investment securities available-for-sale that are not other than temporarily impaired and the unfunded liability for the defined benefit pension plan, are not reflected in the statement of income. The cumulative effect of such items, net of tax effect, is reported as a separate component of the equity section of the balance sheet (Accumulated other comprehensive income or loss). Other comprehensive income or loss, along with net income, comprises the Company's total comprehensive income or loss.

Transfers of financial assets

Transfers of financial assets are accounted for as sales when control over the assets has been surrendered. Control over transferred assets is deemed to be surrendered when the assets have been isolated from the Company, the transferee obtains the right (free of conditions that constrain it from taking advantage of that right) to pledge or exchange the transferred assets, and the Company does not maintain effective control over the transferred assets through an agreement to repurchase them before their maturity.

Stock option plan

The Company recognizes stock-based compensation expense based on the grant date estimated fair value of stock-based awards over the vesting period of the awards. The stock to be issued upon exercise of options granted shall consist of authorized but unissued shares of the Company's $2.00 par value common stock and/or shares of such common stock held in treasury.

Union Bankshares, Inc.23

Recent accounting pronouncements

In January 2010, the FASB issued an Accounting Standards Update ("ASU"), Fair Value Measurements and Disclosures: Improving Disclosures about Fair Value Measurements, to amend the disclosure requirements and clarify existing requirements related to recurring and nonrecurring fair value measurements and employers’ disclosures about postretirement benefit plan assets. The guidance requires new disclosures regarding transfers of assets and liabilities between Level 1 (quoted prices in active market for identical assets or liabilities) and Level 2 (significant other observable inputs) of the fair value measurement hierarchy, including the reasons and the timing of the transfers. Additionally, the guidance requires a rollforward of activities, separately reporting purchases, sales, issuance, and settlements, for assets and liabilities measured using significant unobservable inputs (Level 3 fair value measurements). The new disclosure requirements apply to interim and annual reporting periods beginning after December 15, 2009, except for the new rules regarding purchases, sales, issuances and settlements associated with Level 3 measurements which are effective for fiscal years beginning after December 15, 2010, and for interim periods within those fiscal years. Other than requiring additional disclosures, adoption of this accounting standard did not have a material effect on the Company’s consolidated financial statements. See Note 19.

In January 2011, the FASB issued an ASU, Deferral of the Effective Date of Disclosures about Troubled Debt Restructuring, for public-entity creditors to temporarily delay the effective date of the disclosures about troubled debt restructurings to allow time for FASB to complete its deliberations of what constitutes a troubled debt restructuring. The Company adopted the required portions of the accounting standard as of December 31, 2010 with no material impact on the Company's consolidated financial statements. In April 2011, the FASB issued an ASU, A Creditor's Determination of Whether a Restructuring is a Troubled Debt Restructuring, which provides companies new criteria for determining whether a particular loan modification represents a troubled debt restructuring for accounting purposes and it signals when a company should also record an impairment loss associated with the same loan. This new guidance was effective for quarterly and annual reports for periods beginning on or after June 15, 2011. Adoption of the standard did not have a material effect on the Company's consolidated financial statements.

In April 2011, the FASB issued an ASU, Reconsideration of Effective Controls for Repurchase Agreements, to improve the accounting for repurchase agreements and other agreements that both entitle and obligate a transferor to repurchase or redeem financial assets before their maturity. The update removes the transferor's ability criterion from the consideration of effective control for repurchase or other agreements. The guidance in this ASU is effective for the first interim or annual period beginning on or after December 15, 2011. Management has reviewed the ASU and does not believe that it will have a material effect on the Company's consolidated financial statements.

In May 2011, the FASB issued an ASU, Amendments to Achieve Common Fair Value Measurement and Disclosure Requirements in U.S. GAAP and IFRSs, to improve the comparability of fair value measurements presented and disclosed in financial statements prepared in accordance with GAAP and International Financial Reporting Standards (IFRS). The amendments in this update explain how to measure fair value. They do not require additional fair value measurements and are not intended to establish valuation standards or affect valuation practices outside of financial reporting. The amendments change the wording used to describe many of the requirements in GAAP for measuring fair value and for disclosing information about fair value measurements. The amendments in this ASU are to be applied prospectively and are effective for interim and annual periods beginning after December 15, 2011. Early application is not permitted. Management is currently reviewing the ASU but does not believe that it will have a material effect on the Company's consolidated financial statements.

In June 2011, the FASB issued an ASU, Presentation of Comprehensive Income, to improve the comparability, consistency and transparency of financial reporting, to increase the prominence of items reported in other comprehensive income and to facilitate convergence of GAAP and IFRS. The ASU eliminates the option to present components of other comprehensive income as part of the statement of changes in stockholders' equity and requires that all nonowner changes in stockholders' equity be presented either in a single continuous statement of

Union Bankshares, Inc.24

comprehensive income or in two separate but consecutive statements. In both formats, an entity is required to present each component of net income along with total net income, each component of other comprehensive income along with a total for other comprehensive income, and a total amount for comprehensive income. The entity is required to present on the face of the financial statements reclassification adjustments for items that are reclassified from other comprehensive income to net income in the statements where the components of net income and other comprehensive income are presented. The amendments in the ASU are to be applied retrospectively and are effective for annual and interim periods beginning after December 15, 2011 except for the presentation requirements of reclassifications of items out of accumulated other comprehensive income which have been delayed indefinitely by an ASU issued by FASB in December 2011. Management is currently reviewing the ASU to determine which of the two remaining formats will be used in the Company's future consolidated financial statements.

In September 2011, the FASB issued an ASU, Intangibles - Goodwill and Other (Topic 350): Testing Goodwill for Impairment, to address concerns about the cost and complexity of the required test to determine if goodwill is impaired, or inflated on the balance sheet and in need of a writedown. The ASU amends Topic 350 to permit an entity the option to first assess qualitative factors to determine whether it is more likely than not (50% threshold) that the fair value of a reporting unit is less than its carrying amount as a basis for determining whether it is necessary to perform the two-step goodwill impairment test. The amendments are effective for annual and interim goodwill impairment tests performed for fiscal years beginning after December 15, 2011. Early adoption is permitted, including for annual and interim goodwill impairment tests performed as of a date before September 15, 2011, if an entity's financial statements for the most recent annual or interim periods have not yet been issued. Management adopted the ASU as of September 30, 2011. (See Note 9.)

In December 2011, the FASB issued an ASU, Disclosures about Offsetting Assets and Liabilities, to enhance disclosures required to facilitate comparison between those entities that prepare their financial statements on the basis of GAAP and those entities that prepare their financial statements on the basis of IFRS by requiring improved information about financial instruments and derivative instruments that are either (1) offset in accordance with either Topic 210-20-45 (Balance Sheet Offsets) or Topic 815-10-45 (Derivatives & Hedging) or (2) subject to an enforceable master netting arrangement or similar agreement, irrespective of whether they are offset in accordance with either Topic 210-20-45 or Topic 815-10-45. The amendments in the ASU are to be applied retrospectively for all comparative periods presented and are effective for annual and interim periods beginning on or after January 1, 2013. Management is currently reviewing the ASU but does not believe that it will have a material effect on the Company's consolidated financial statements.

Note 2. Restrictions on Cash and Due From Banks

The nature of the Company's business requires that it maintain amounts due from correspondent banks which, at times, may exceed federally insured limits. The balances in these accounts at December 31, were as follows:

| 2011 | 2010 | |||||

| (Dollars in thousands) | ||||||

| Noninterest bearing accounts | $ | 1,143 | $ | 1,281 | ||

| Federal Reserve Bank of Boston | 19,368 | 9,678 | ||||

| FHLB of Boston | 351 | 322 | ||||

No losses have been experienced in these accounts and the Company believes it is not exposed to any significant risk with respect to the accounts.

Union Bankshares, Inc.25