Exhibit 99.1

|

NCR Analyst Day

DECEMBER 6, 2007

NEW YORK STOCK EXCHANGE NEW YORK, NEW YORK

|

Agenda

Bill Nuti – NCR Business Strategy

Chairman & CEO

Q&A

Alan Chow – Product Development Strategy

SVP, Product Development & CTO

Peter Dorsman – Global Operations Strategy

SVP, Global Operations

Chris Wallace – Customer Services Strategy

SVP, Worldwide Customer Services

Bob Fishman – NCR Business Model

Interim CFO & Corporate Controller

Q&A

|

Note to Investors

Certain non-GAAP financial information regarding NCR’s operating results may be discussed during this presentation. Reconciliations of the differences between GAAP and non-GAAP measures are available on the Investor page of NCR’s website at www.ncr.com. Remarks and responses associated with this presentation include forward-looking statements that are based on current expectations. These forward-looking statements are subject to a number of risks and uncertainties that could cause actual results to vary materially.

These risk factors are detailed from time to time in NCR’s

SEC reports, including, but not limited to, Forms 10Q, 10K, 8K and the company’s annual report to shareholders.

|

NCR Business Strategy

Bill Nuti

Chairman & CEO

|

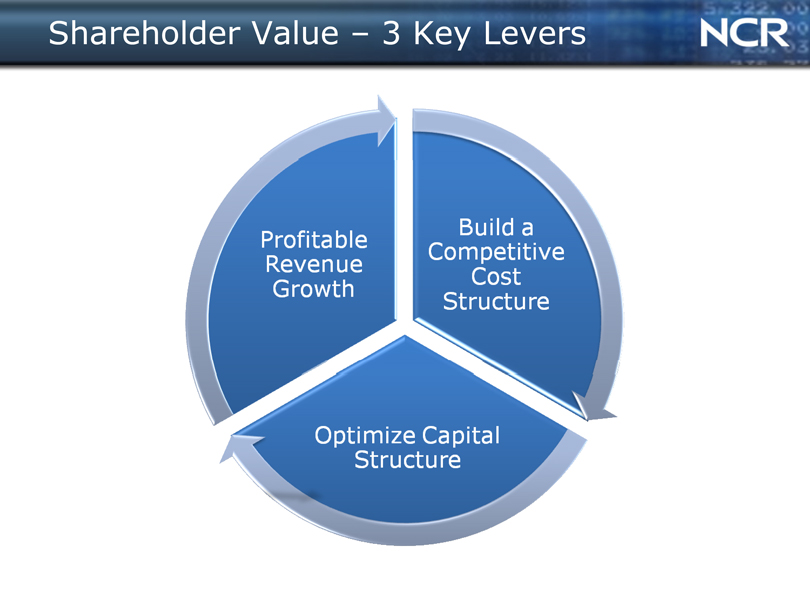

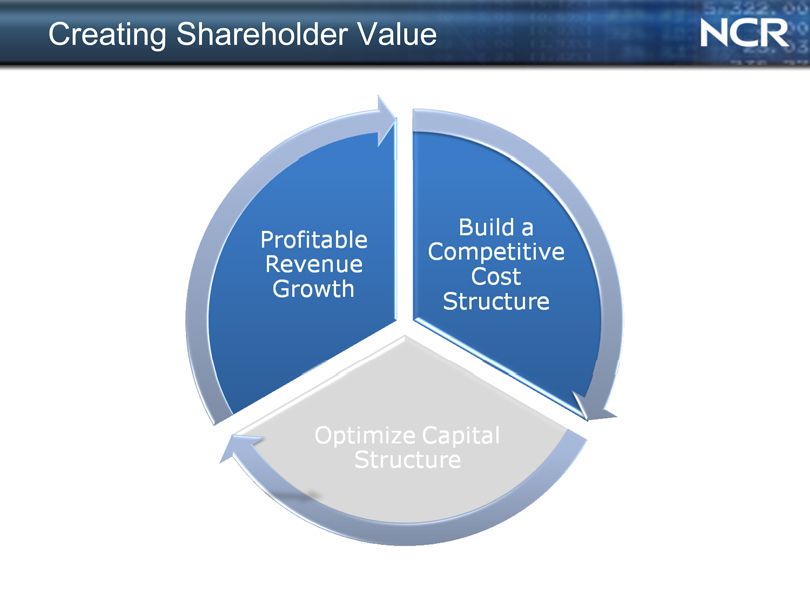

Shareholder Value – 3 Key Levers

Profitable Revenue Growth

Build a Competitive Cost Structure

Optimize Capital Structure

|

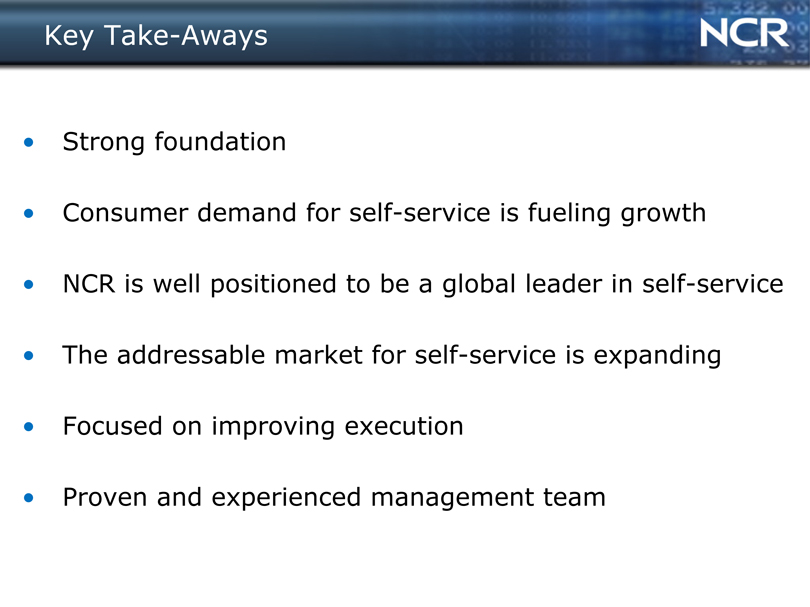

Key Take-Aways

Strong foundation

Consumer demand for self-service is fueling growth NCR is well positioned to be a global leader in self-service The addressable market for self-service is expanding Focused on improving execution Proven and experienced management team

|

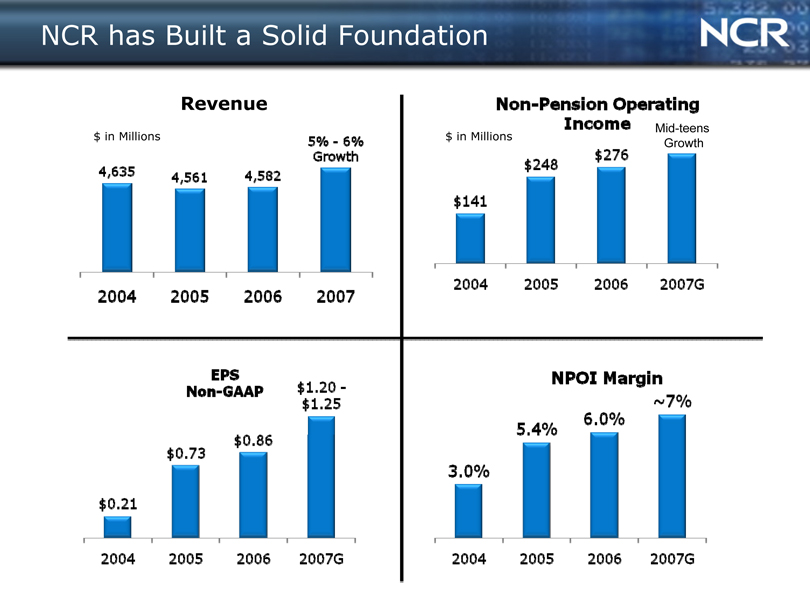

NCR has Built a Solid Foundation

Mid-teens Growth

4,582

$ in Millions

4,635

Revenue

4,561

5%—6% Growth

Non-Pension Operating

Income

$276

$ in Millions

$248

$141

2004 2005 2006 2007

2004 2005 2006 2007G

EPS Non-GAAP

$0.86

$0.73

$1.20-$1.25

3.0%

NPOI Margin

-7%

6.0%

5.4%

*— *

$0.21

2004 2005 2006 2007G

2004 2005 2006 2007G

|

Consumers Driving Self-Service

Consumer Trends

50 billion ATM transactions

$ 500 Billion in self-checkout purchases

70% of U.S. business travelers use self-check-in

8.8 billion digital photographs printed via self-service

Business Trends

New business models emerging that are 100% self-service

In all industries, businesses are adopting a multi-channel strategy including self-service

|

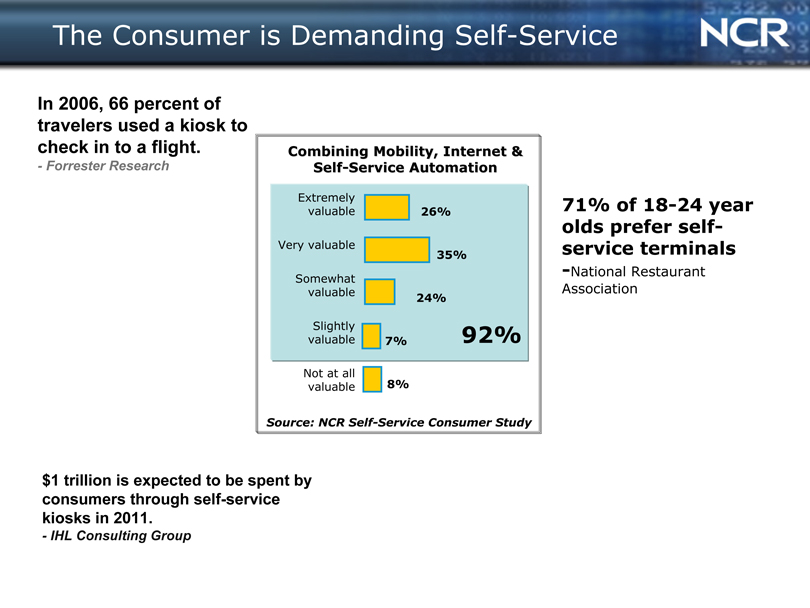

The Consumer is Demanding Self-Service

In 2006, 66 percent of travelers used a kiosk to check in to a flight.

- Forrester Research

Combining Mobility, Internet & Self-Service Automation

Extremely valuable 26%

Very valuable

35%

Somewhat valuable

24%

Slightly 92% valuable 7%

Not at all valuable 8%

Source: NCR Self-Service Consumer Study

71% of 18-24 year olds prefer self-service terminals

-National Restaurant Association $1 trillion is expected to be spent by consumers through self-service kiosks in 2011.

- IHL Consulting Group

|

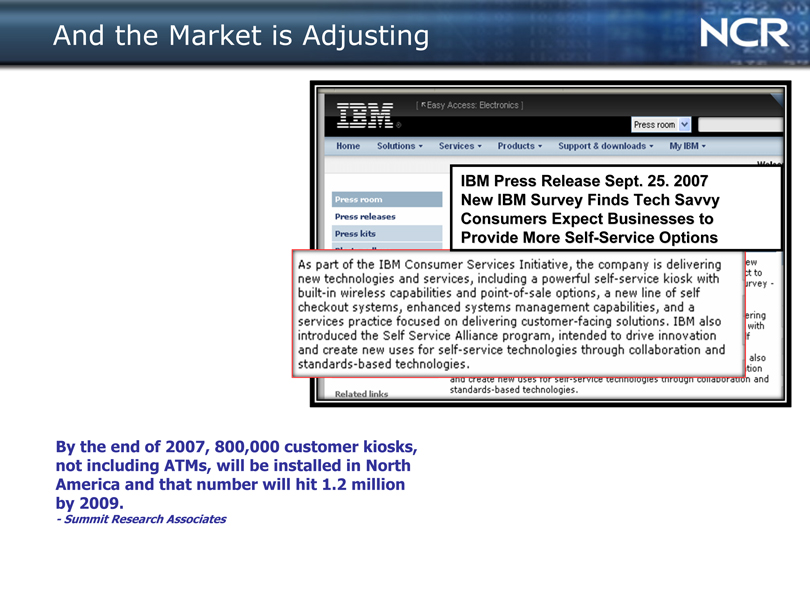

And the Market is Adjusting

IBM Press Release Sept. 25. 2007 New IBM Survey Finds Tech Savvy Consumers Expect Businesses to Provide More Self-Service Options

By the end of 2007, 800,000 customer kiosks, not including ATMs, will be installed in North America and that number will hit 1.2 million by 2009.

- Summit Research Associates

|

Businesses Recognize Customer Interaction is Changing

|

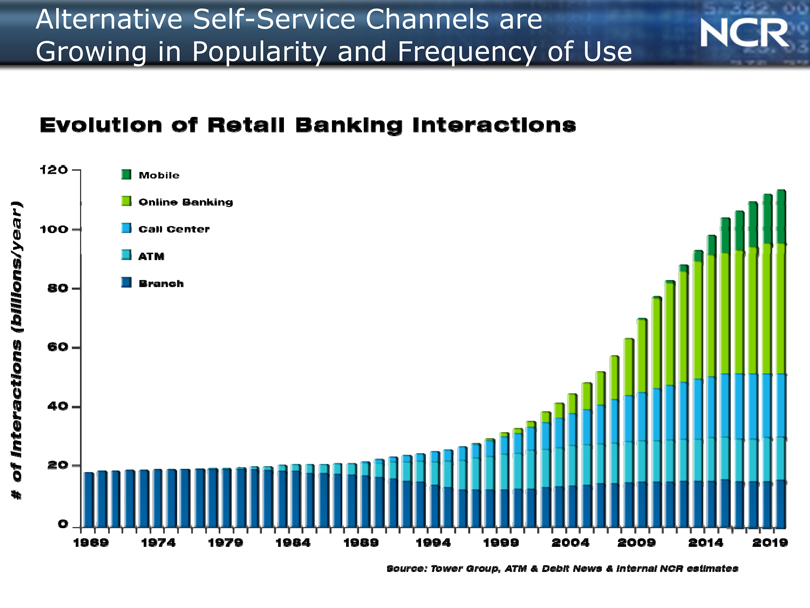

Alternative Self-Service Channels are Growing in Popularity and Frequency of Use

Evolution of Retail Banking Interactions

Mobile

Online Banking

Call Center

ATM

Branch

1969 1974 1979 1984 1989 1994 1999 2004 2009 2014 2019

source: Tower Group, ATM & Debit News & Internal NCR estimates

|

The Type of Consumer Interactions and Channels Are Changing in Retail as well….

POINT OF SERVICE

MOBILITY

INTERNET

|

And This Phenomena is

Occurring in ALL Major Industries

FINANCIAL

RETAIL

TRAVEL & HOSPITALITY

HEALTHCARE

ENTERTAINMENT & GAMING

PUBLIC SECTOR

|

And in Every Corner of the World…NOW

. CREATING AN INCREDIBLE OPPORTUNITY FOR NCR

|

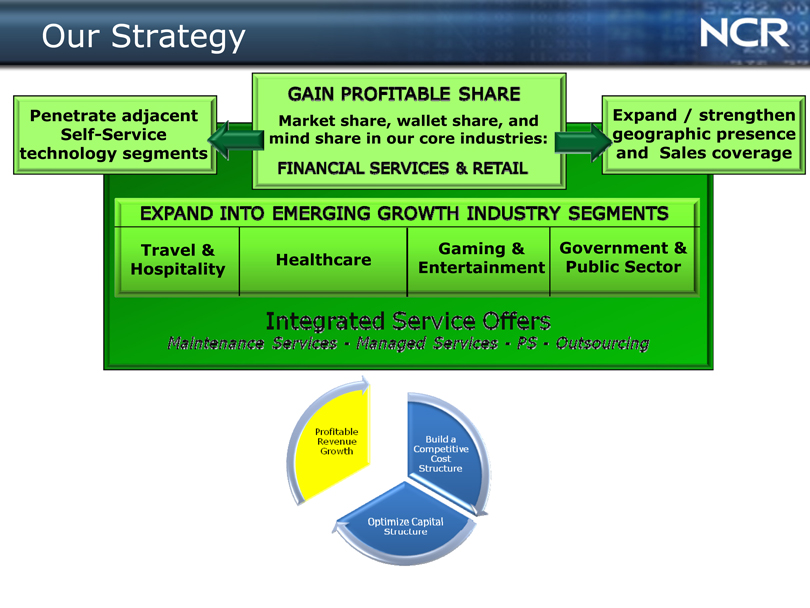

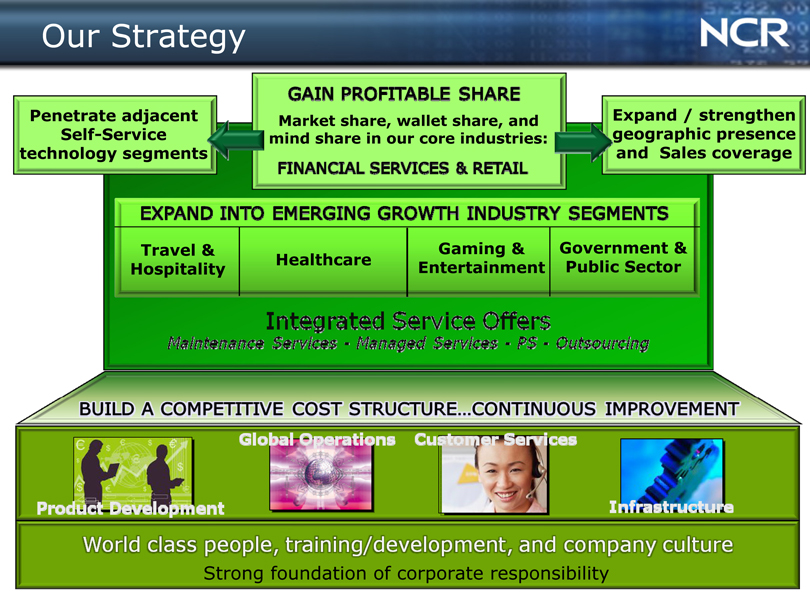

Our Strategy

Penetrate adjacent Self-Service technology segments

Market share, wallet share, and mind share in our core industries:

Expand / strengthen geographic presence and Sales coverage

Travel & Gaming & Government & Healthcare Entertainment Public Sector Hospitality

EXPAND INTO EMERGING GROWTH INDUSTRY SEGMENTS

Integrated Service Offers

Maintenance Services—Managed Services—PS—Outsourcing

Profitable Revenue Growth

Build a Competitive Cost Structure

Optimize Capital Structure

|

Our Strategy

Profitable Revenue Growth

Build a Competitive Cost Structure

Optimize Capital Structure

BUILD A COMPETITIVE COST STRUCTURE.CONTINUOUS IMPROVEMENT

PRODUCT DEVELOPMENT

GLOBAL OPERATIONS

CUSTOMER SERVICES

INFRASTRUCTURE

|

Our Strategy

Penetrate adjacent Self-Service technology segments

Market share, wallet share, and mind share in our core industries:

Expand / strengthen geographic presence and Sales coverage

Travel & Hospitality Healthcare Gaming & Entertainment Government & Public Sector

BUILD A COMPETITIVE COST STRUCTURE.CONTINUOUS IMPROVEMENT

PRODUCT DEVELOPMENT

GLOBAL OPERATIONS

CUSTOMER SERVICES

INFRASTRUCTURE

|

Strong Market Position

#1

ATM MARKET SHARE

#1

SELF-SERVICE CHECKOUT

#1

AIRLINE KIOSK

#1

HEALTHCARE KIOSK

#1

TWO-SIDED

TECHNOLOGY

(2ST)

#2

POINT-OF-SALE

THE GLOBAL LEADER IN SELF-SERVICE TECHNOLOGIES

|

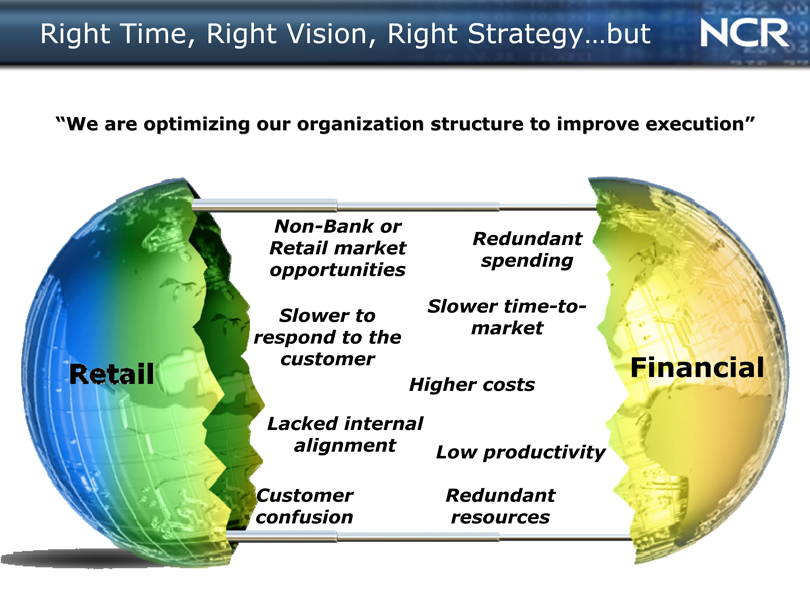

Right Time, Right Vision, Right Strategy…but

“We are optimizing our organization structure to improve execution”

Non-Bank or Retail market opportunities

Slower to respond to the customer

Lacked internal alignment

Customer confusion

Redundant spending

Slower time-to-market

Higher costs

Low productivity

Redundant resources

Financial

RETAIL

|

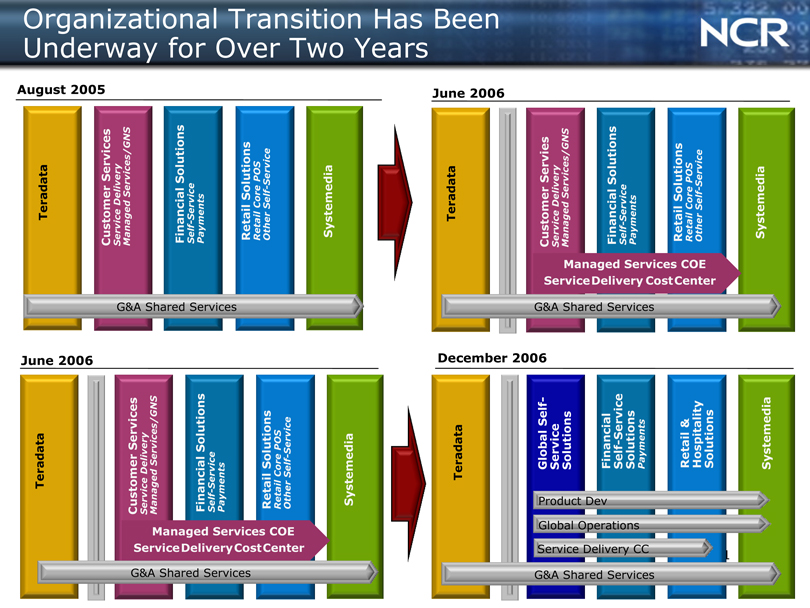

Organizational Transition Has Been Underway for Over Two Years

August 2005

G&A Shared Services

June 2006

Managed Services COE ServiceDeliveryCostCenter ServiceDeliveryCostCenter

G&A Shared Services G&A Shared Services

June 2006

Managed Services COE ServiceDelivery ServiceDeliveryCostCenter CostCenter

G&A Shared Services

December 2006

Product Dev Global Operations Service Delivery CC

G&A Shared Services

TERADATA

CUSTOMER SERVICES

SERVICE DELIVERY

MANAGED SERVICES/GNS

FINANANCIAL SOLUTIONS

Self-Service Payments

RETAIL SOLUTIONS

RETAIL CORE POS

OTHER SELF-SERVICES

SYSTEMEDIA

GLOBAL SELF-SERVICE SOLUTIONS

FINANANCIAL Self-Service SOLUTIONS

Payments

RETAIL & HOSPITALITY SOLUTIONS

|

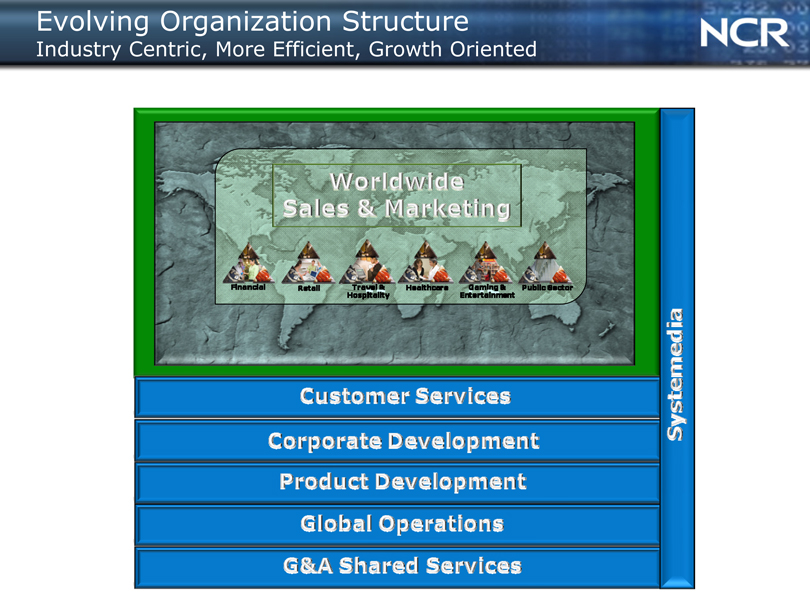

Evolving Organization Structure

Industry Centric, More Efficient, Growth Oriented

WORLDWIDE SALES & MARKETING

CUSTOMER SERVICES

CORPORATE DEVELOPMENT

PRODUCT DEVELOPMENT

GLOBAL OPERATIONS

G&A SHARED SERVICES

SYSTEMEDIA

|

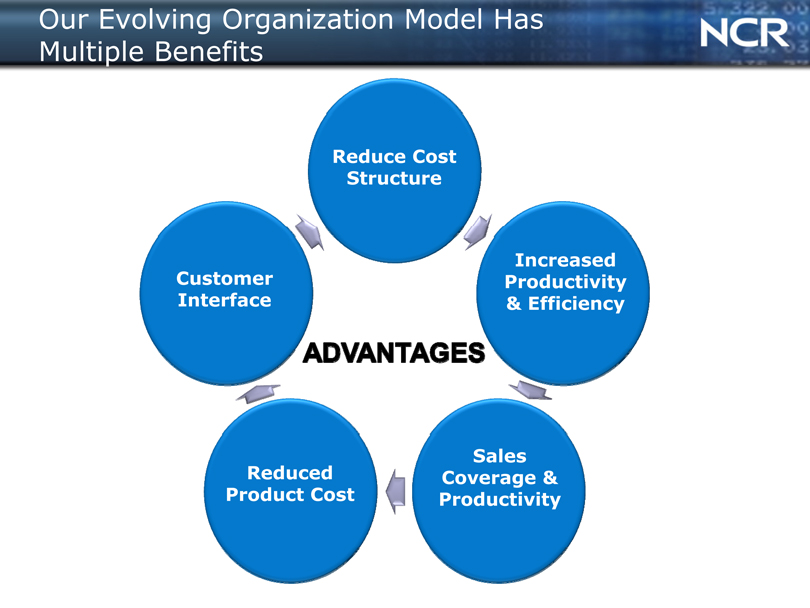

Our Evolving Organization Model Has Multiple Benefits

Reduce Cost Structure

Customer Interface

Reduced Product Cost

Sales Coverage & Productivity

Increased Productivity & Efficiency

ADVANTAGES

|

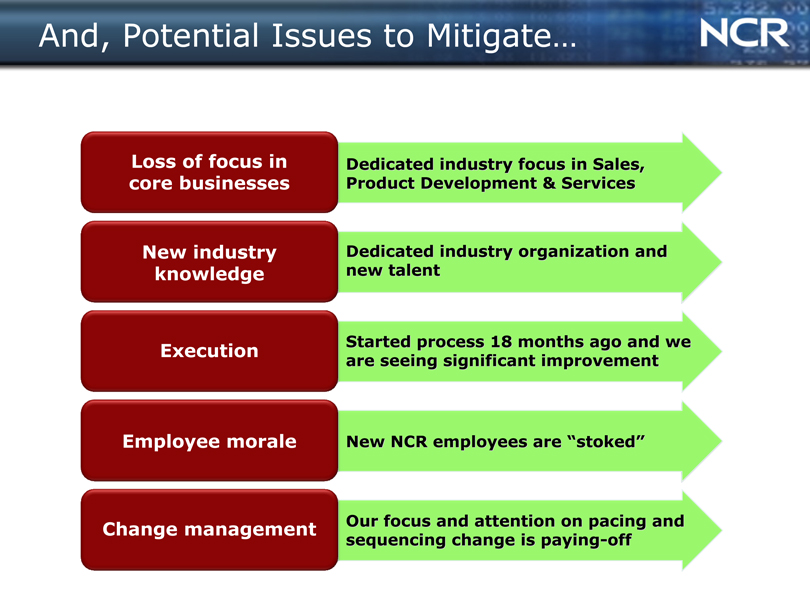

And, Potential Issues to Mitigate…

Loss of focus in core businesses Dedicated industry focus in Sales, Product Development & Services

New industry knowledge Dedicated industry organization and new talent

Execution Started process 18 months ago and we are seeing significant improvement

Employee morale New NCR employees are “stoked”

Change management Our focus and attention on pacing and sequencing change is paying-off

|

NCR is Well Positioned…

CHANNELS

CAPABILITIES

MARKETS

SOLUTIONS

“NCR is the only company with the capability to pull all these things together –web, kiosk, point-of-sale, and mobility”

– CEO, NCR Customer Fortune 500 Company

|

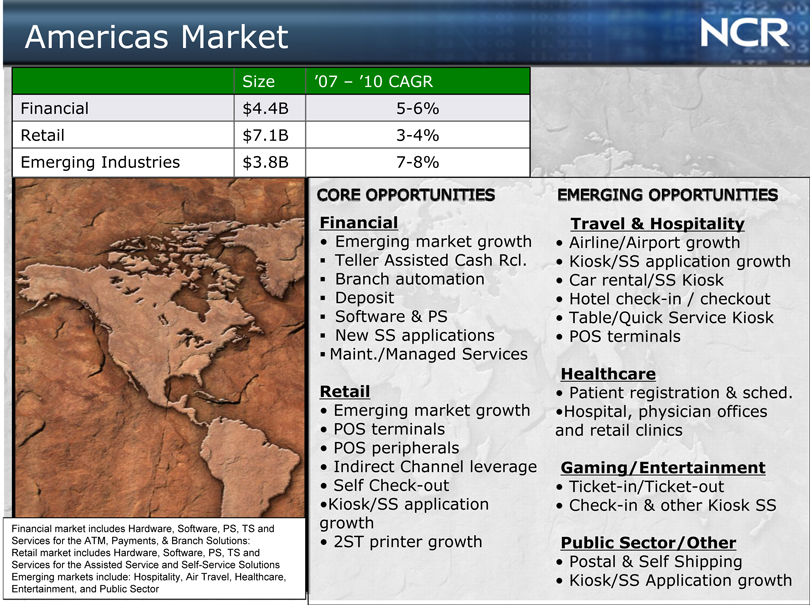

Americas Market

Size ‘07 – ‘10 CAGR Financial $4.4B 5-6% Retail

$7.1B 3-4% Emerging Industries $3.8B 7-8%

Financial market includes Hardware, Software, PS, TS and Services for the ATM, Payments, & Branch Solutions: Retail market includes Hardware, Software, PS, TS and Services for the Assisted Service and Self-Service Solutions Emerging markets include: Hospitality, Air Travel, Healthcare, Entertainment, and Public Sector

Core Opportunities

Financial

Emerging market growth ?Teller Assisted Cash Rcl. ?Branch automation ?Deposit ?Software & PS

?New SS applications ?Maint./Managed Services

Retail

Emerging market growth

POS terminals

POS peripherals

Indirect Channel leverage

Self Check-out Kiosk/SS application growth

2ST printer growth

Emerging Opportunities

Travel & Hospitality

Airline/Airport growth

Kiosk/SS application growth

Car rental/SS Kiosk

Hotel check-in / checkout

Table/Quick Service Kiosk

POS terminals

Healthcare

Patient registration & sched.

Hospital, physician offices and retail clinics

Gaming/Entertainment

Ticket-in/Ticket-out

Check-in & other Kiosk SS

Public Sector/Other

Postal & Self Shipping

Kiosk/SS Application growth

|

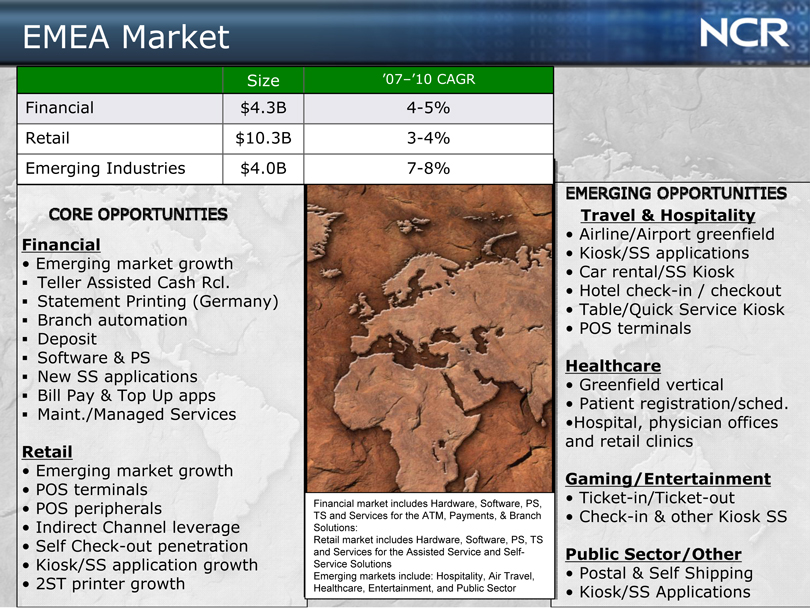

EMEA Market

Size ‘07–’10 CAGR

Financial $4.3B 4-5%

Retail $ 10.3B 3-4%

Emerging Industries $4.0B 7-8%

Core Opportunities

Financial

Emerging market growth ?Teller Assisted Cash Rcl. ?Statement Printing (Germany) ?Branch automation ?Deposit ?Software & PS

?New SS applications ?Bill Pay & Top Up apps ?Maint./Managed Services

Retail

Emerging market growth

POS terminals

POS peripherals

Indirect Channel leverage

Self Check-out penetration

Kiosk/SS application growth

2ST printer growth

Financial market includes Hardware, Software, PS, TS and Services for the ATM, Payments, & Branch Solutions: Retail market includes Hardware, Software, PS, TS and Services for the Assisted Service and Self-Service Solutions Emerging markets include: Hospitality, Air Travel, Healthcare, Entertainment, and Public Sector

Emerging Opportunities

Travel & Hospitality

Airline/Airport greenfield

Kiosk/SS applications

Car rental/SS Kiosk

Hotel check-in / checkout

Table/Quick Service Kiosk

POS terminals

Healthcare

Greenfield vertical

Patient registration/sched.

Hospital, physician offices and retail clinics

Gaming/Entertainment

Ticket-in/Ticket-out

Check-in & other Kiosk SS

Public Sector/Other

Postal & Self Shipping

Kiosk/SS Applications

|

APJ Market

Size ‘07 – ‘10 CAGR

Financial $3.5B 3-4%

Retail $8.6B 4-5%

Emerging Industries $3.7B 7-8%

Core Opportunities

Financial

Emerging market growth

Teller Assisted Cash Rcl.

Cash Recycling

Branch automation

Deposit

Software & PS

New SS applications

Bill Pay & Top Up apps

Maint/Managed Services

Retail

Emerging market growth

POS terminals

POS peripherals

Low-end market opportunity

Indirect Channel leverage

Self Check-out penetration

Kiosk/SS application growth

2ST printer growth

Emerging Opportunities

Travel & Hospitality

Airline/Airport greenfield

Kiosk/SS applications

Car rental/SS Kiosk

Hotel check-in / checkout

Table/Quick Service Kiosk

POS terminals

Healthcare

Greenfield vertical – focus on mature economies

Gaming/Entertainment

Ticket-in/Ticket-out

Macao, Sing. market

Check-in & other Kiosk SS

Public Sector/Other

Postal & Self Shipping

Kiosk/SS Applications

Financial market includes Hardware, Software, PS, TS and Services for the ATM, Payments, & Branch Solutions: Retail market includes Hardware, Software, PS, TS and Services for the Assisted Service and Self-Service Solutions Emerging markets include: Hospitality, Air Travel, Healthcare, Entertainment, and Public Sector

|

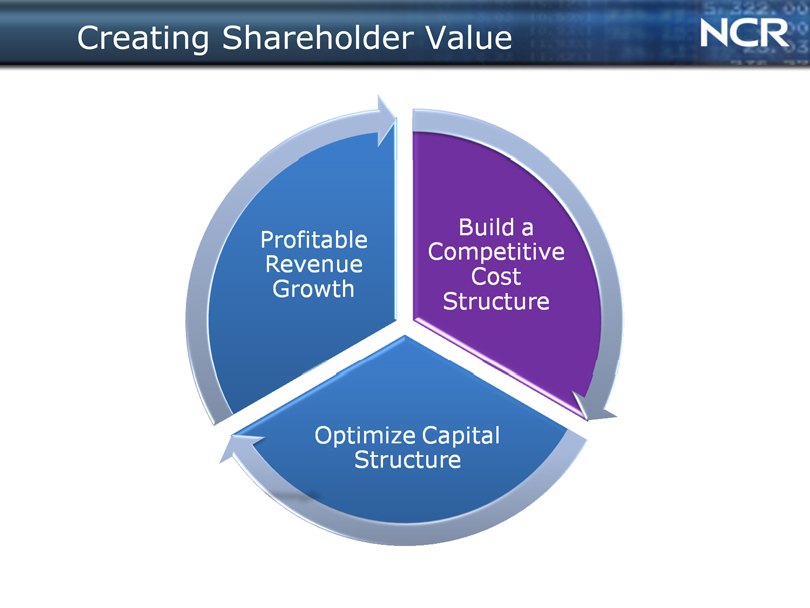

Creating Shareholder Value

|

Initiatives to Improve Cost Structure, Productivity, and Customer Satisfaction (Phase II Continued)

Product Development

PLM DFX

Common Modular Architecture

Global Operations

Lean 6 Sigma Implementation

Manufacturing (low cost, high productivity)

Supply Chain Collaboration

Customer Services

Call Center Operations

Parts & Logistics

Productivity

G&A Infrastructure

Strong financial controls

Productivity

Shared Services

|

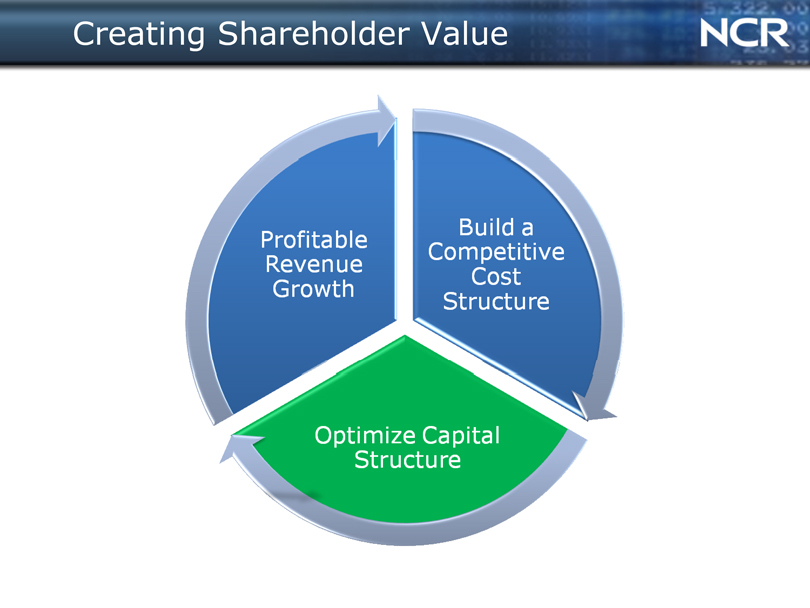

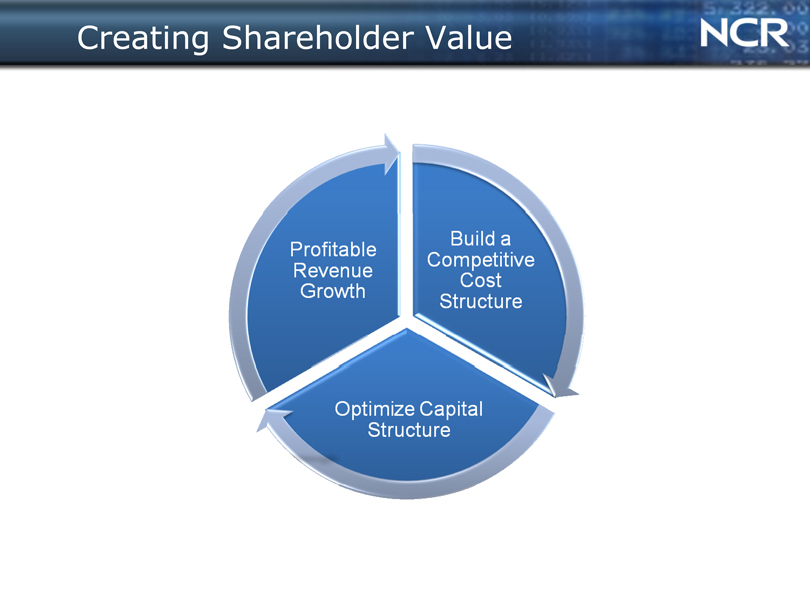

Creating Shareholder Value

Profitable Revenue Growth

Build a Competitive Cost Structure

Optimize Capital Structure

|

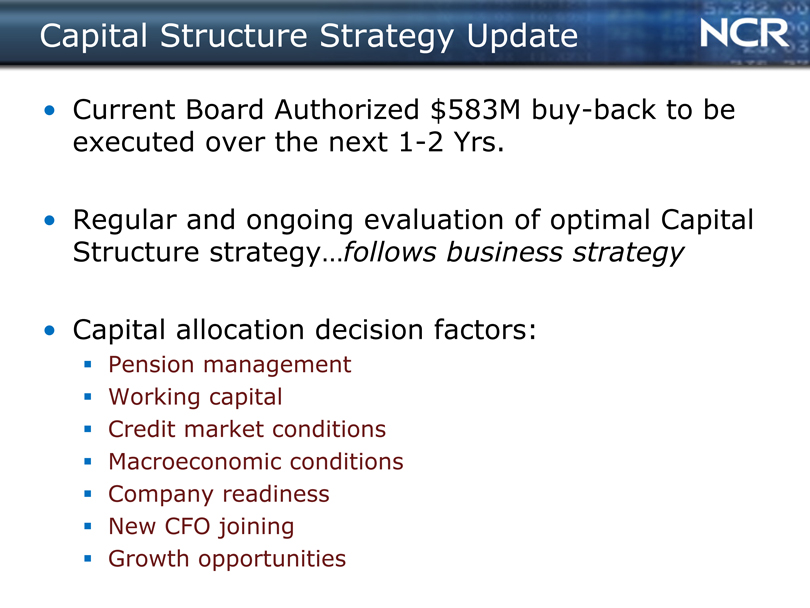

Capital Structure Strategy Update

Current Board Authorized $583M buy-back to be executed over the next 1-2 Yrs.

Regular and ongoing evaluation of optimal Capital Structure strategy…follows business strategy

Capital allocation decision factors:

?Pension management

?Working capital

?Credit market conditions

?Macroeconomic conditions

?Company readiness

?New CFO joining ?Growth opportunities

|

Experienced Management Team

Alan Chow Peter Dorsman Malcolm Collins Chris Wallace Dan Bogan

SVP Product SVP Global SVP Worldwide SVP Worldwide VP Systemedia Development & CTO Operations Sales & Marketing Customer Services Business Unit

Bill Nuti

Chairman and CEO

Mike Webster Andrea Ledford Bob Fishman Peter Lieb Mel Walter

VP Corporate Strategy SVP Human Interim CFO & SVP General VP Business & Communications Resources Corporate Controller Counsel Development

|

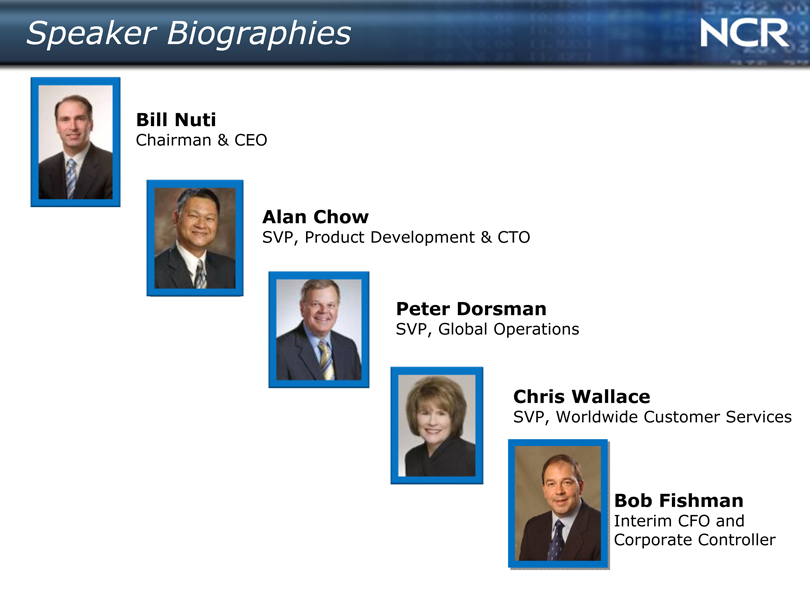

Speaker Biographies

Bill Nuti

Chairman & CEO

Alan Chow

SVP, Product Development & CTO

Peter Dorsman

SVP, Global Operations

Chris Wallace

SVP, Worldwide Customer Services

Bob Fishman

Interim CFO and Corporate Controller

|

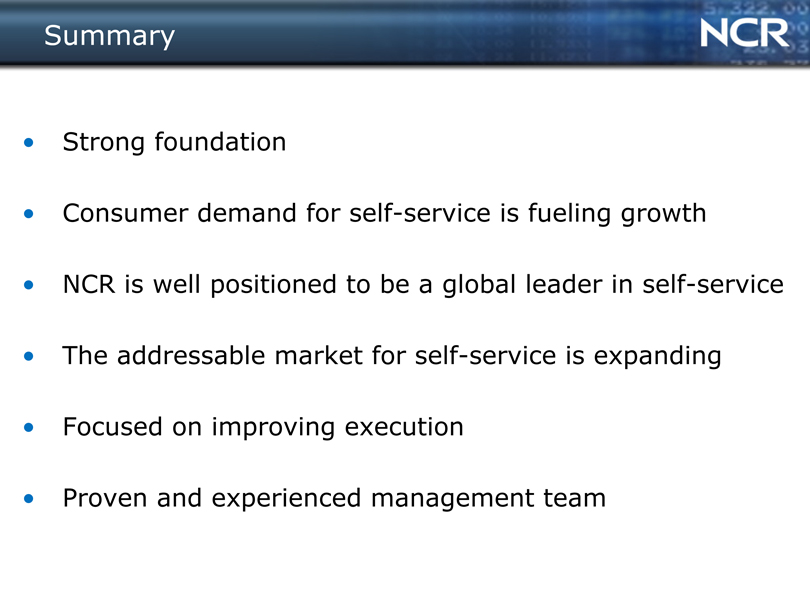

Summary

Strong foundation

Consumer demand for self-service is fueling growth NCR is well positioned to be a global leader in self-service The addressable market for self-service is expanding Focused on improving execution Proven and experienced management team

|

Product Development Strategy

Alan Chow

SVP, Product Development & CTO

|

Creating Shareholder Value

Profitable Revenue Growth

Build a Competitive Cost Structure

Omtimize Capital Structure

|

Innovation Drives Profitable Revenue Growth

ADJACENT SOLUTIONS

CORE SOLUTIONS

NEW INDUSTRY EXTENSIONS

PROFITABLE REVENUE GROWTH

|

Innovation Drives Profitable Revenue Growth

CORE SOLUTIONS

ATM

POS

SCANNER

SELF-CHECKOUT

KIOSKS

PAYMENTS SYSTEMS

|

Innovation Drives Profitable Revenue Growth

CORE SOLUTIONS

ADJACENT SOLUTIONS

CONTACTLESS

TELLER ASSISTED RECYCLING

INTELLIGENT DEPOSIT

|

Innovation Drives Profitable Revenue Growth

ADJACENT SOLUTIONS

CORE SOLUTIONS

NEW INDUSTRY EXTENSIONS

TRAVEL & HOSPITALITY

HEALTHCARE

GAMING & ENTERTAINMENT

GOVERNMENT / PUBLIC SECTOR

|

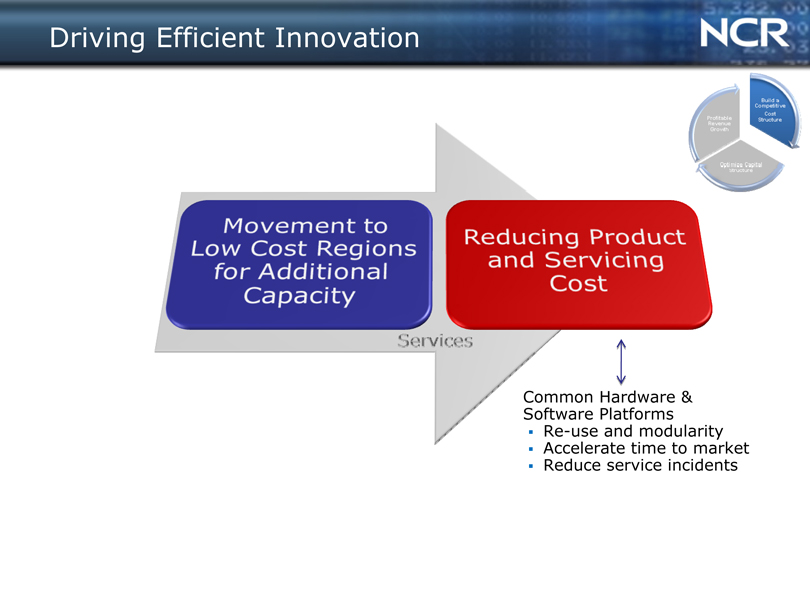

Driving Efficient Innovation

MOVEMENT TO LOW COST REGIONS FOR ADDITIONAL CAPACITY

REDUCING PRODUCT AND SERVICING COST

Common Hardware & Software Platforms ?Re-use and modularity ?Accelerate time to market ?Reduce service incidents

|

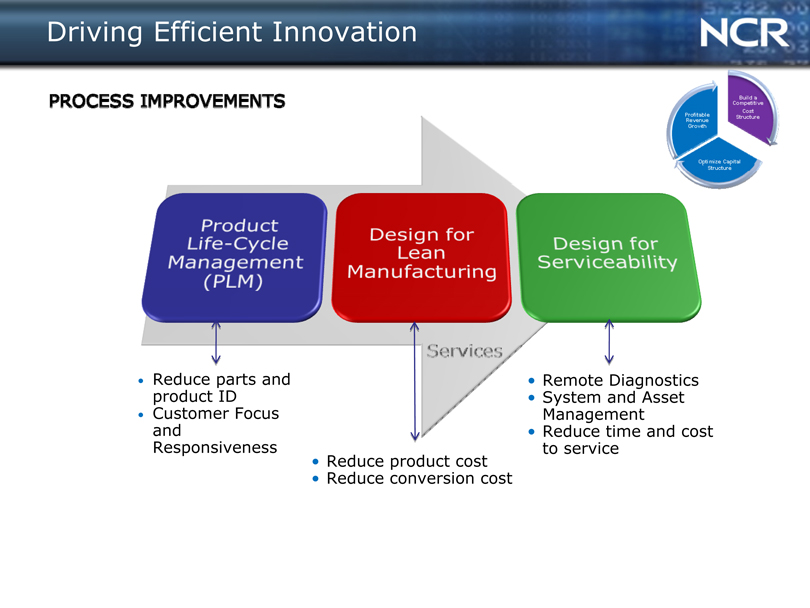

Driving Efficient Innovation

PRODUCT LIFE-CYCLE MANAGEMENT (PLM)

DESIGN FOR LEAN MANUFACTURING

DESIGN FOR SERVICEABILITY

SERVICES

Reduce parts and product ID

Customer Focus and Responsiveness

Reduce product cost Reduce conversion cost

Remote Diagnostics System and Asset Management Reduce time and cost to service

|

Global Operations Strategy

Peter Dorsman

SVP, Global Operations

|

Creating Shareholder Value

Profitable Revenue Growth

Build a Competitive Cost Srtucture

Omtimize Capital Structure

|

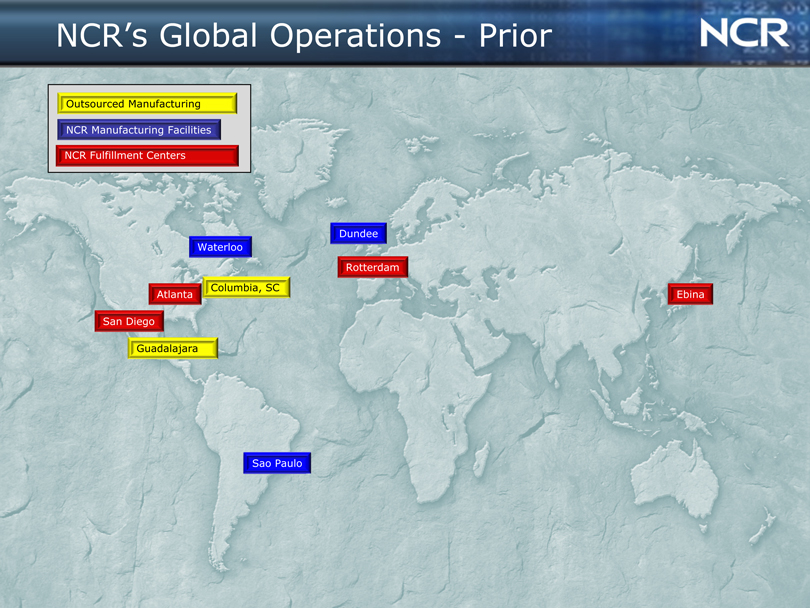

NCR’s Global Operations—Prior

Outsourced Manufacturing NCR Manufacturing Facilities NCR Fulfillment Centers

Dundee Waterloo Rotterdam Columbia, SC

Atlanta Ebina San Diego Guadalajara

Sao Paulo

|

NCR’s Global Operations—2007

Contract Manufacturing NCR Manufacturing Facilities NCR Fulfillment Centers

Budapest Columbia, SC Rotterdam

Beijing Ebina Atlanta

Guadalajara

Pondicherry

Sao Paulo

SHIFT FROM HIGH-COST TO LOW-COST REGIONS

EXPAND OUTSOURCED MANUFACTURING

|

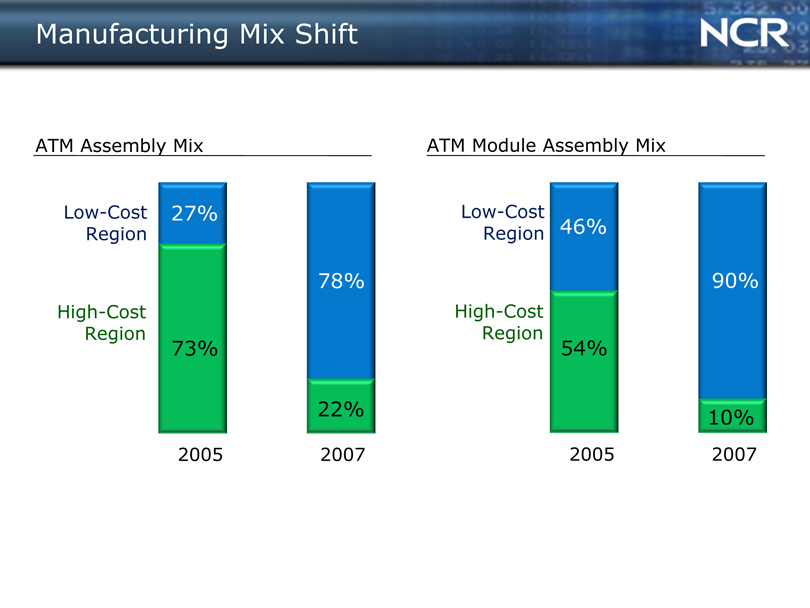

Manufacturing Mix Shift

ATM Assembly Mix

Low-Cost Region

High-Cost Region

27%

73%

2005

78%

22%

2007

ATM Module Assembly Mix

Low-Cost Region

High-Cost Region

46%

54%

2005

90%

10%

2007

|

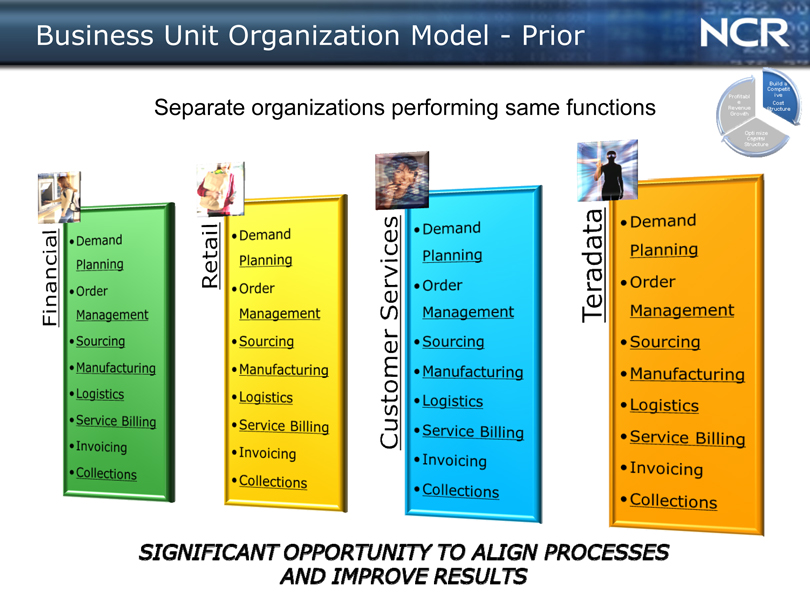

Business Unit Organization Model—Prior

Separate organizations performing same functions

FINANCIAL

DEMAND PLANNING

ORDER MANAGEMENT

SOURCING

MANUFACTURING

LOGISTICS

SERVICE BILLING

INVOICING

COLLECTIONS

RETAIL

CUSTOMER SERVICES

TERADATA

SIGNIFICANT OPPORTUNITY TO ALIGN PROCESSES AND INPROVE RESULTS

|

One Global Operations Organization (2008 Plus)

Lowers our Cost Improves Quality Increases Productivity

DEMAND PLANNING

ORDER MANAGEMENT

SOURCING

MANUFACTURING

LOGISTICS

SERVICE BILLING

INVOICING

COLLECTIONS

|

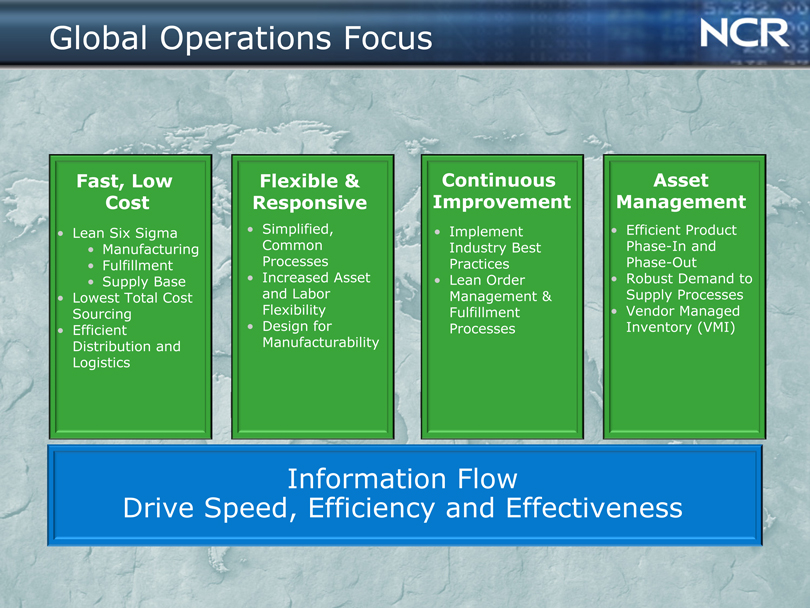

Global Operations Focus

Fast, Low Cost

Lean Six Sigma

Manufacturing

Fulfillment

Supply Base

Lowest Total Cost Sourcing

Efficient Distribution and Logistics

Flexible & Responsive

Simplified, Common Processes

Increased Asset and Labor Flexibility

Design for Manufacturability

Continuous Improvement

Implement Industry Best Practices

Lean Order Management & Fulfillment Processes

Asset Management

Efficient Product Phase-In and Phase-Out

Robust Demand to Supply Processes

Vendor Managed Inventory (VMI)

Information Flow

Drive Speed, Efficiency and Effectiveness

|

Operations: Enabling NCR’s Success

SALES

OPERATIONS

SERVICES

PRODUCT DEVELOPMENT

|

Customer Services Strategy

Chris Wallace

SVP, Customer Services

|

Creating Shareholder Value

Profitable Revenue Growth

Build a Competitive Cost Structure

Omtimize Capital Structure

|

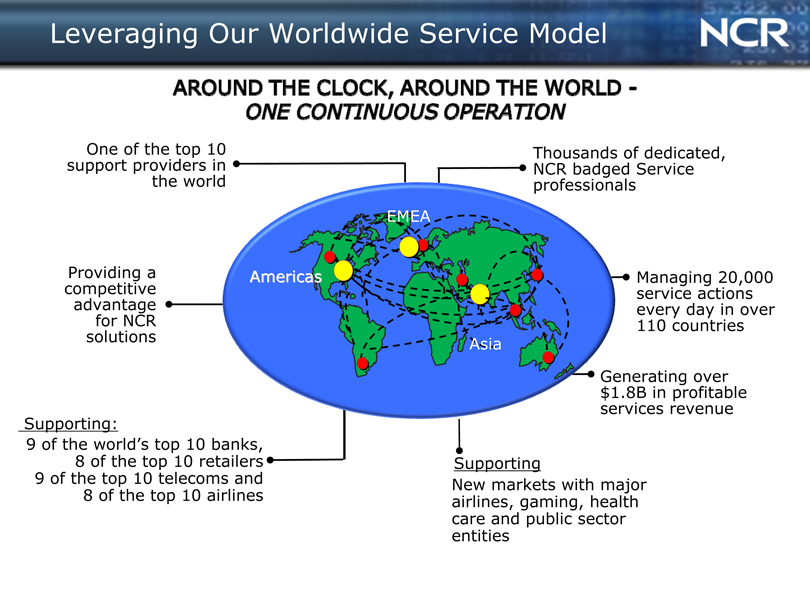

Leveraging Our Worldwide Service Model

One of the top 10 support providers in the world

Providing a competitive advantage for NCR solutions

Supporting:

9 of the world’s top 10 banks, 8 of the top 10 retailers 9 of the top 10 telecoms and 8 of the top 10 airlines

Thousands of dedicated, NCR badged Service professionals

Managing 20,000 service actions every day in over 110 countries

Generating over $1.8B in profitable services revenue

Supporting

New markets with major airlines, gaming, health care and public sector entities

EMEA

Americas

Asia

|

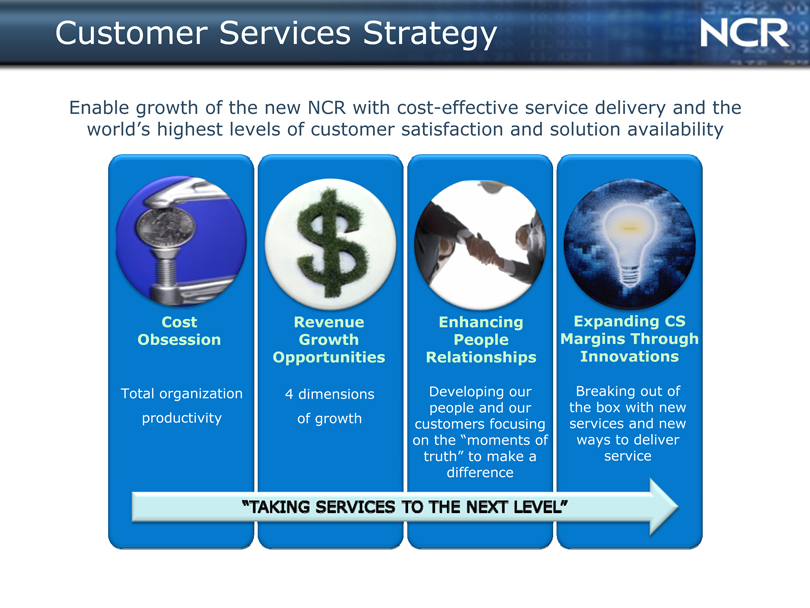

Customer Services Strategy

Enable growth of the new NCR with cost-effective service delivery and the world’s highest levels of customer satisfaction and solution availability

Cost Obsession

Total organization productivity

Growth Opportunities

4 |

| dimensions of growth |

Enhancing People Relationships

Developing our people and our customers focusing on the “moments of truth” to make a difference

Expanding CS Margins Through Innovations

Breaking out of the box with new services and new ways to deliver service

|

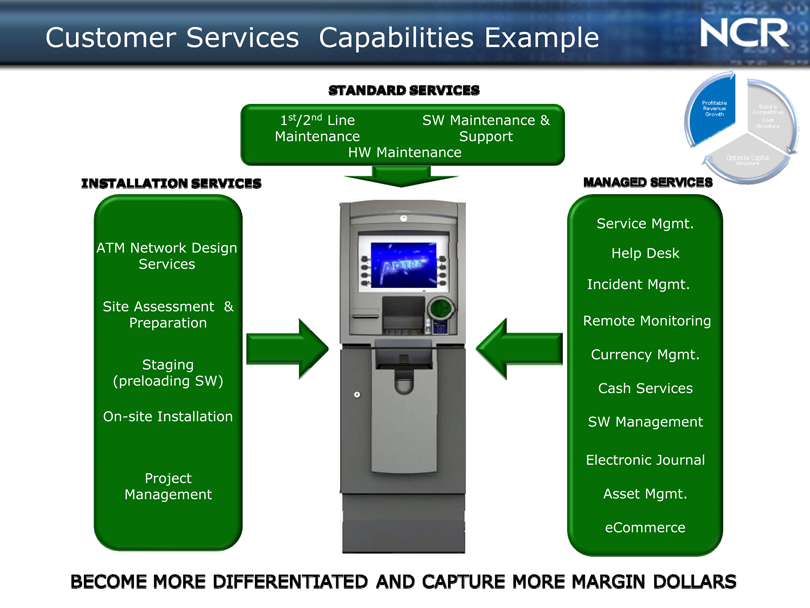

Customer Services Capabilities Example

STANDARD SERVICES

INSTALLATION SERVICES

MANAGED SERVICES

ATM Network Design Services

Site Assessment & Preparation

Staging (preloading SW)

On-site Installation

Project Management

Service Mgmt. ?

Help Desk I

Incident Mgmt. I

Remote Monitoring I

Currency Mgmt. I

Cash Services I

SW Management I

Electronic Journal I

Asset Mgmt. I

eCommerce I

BECOME MORE DIFFERENTIATED AND CAPTURE MORE MARGIN DOLLARS

|

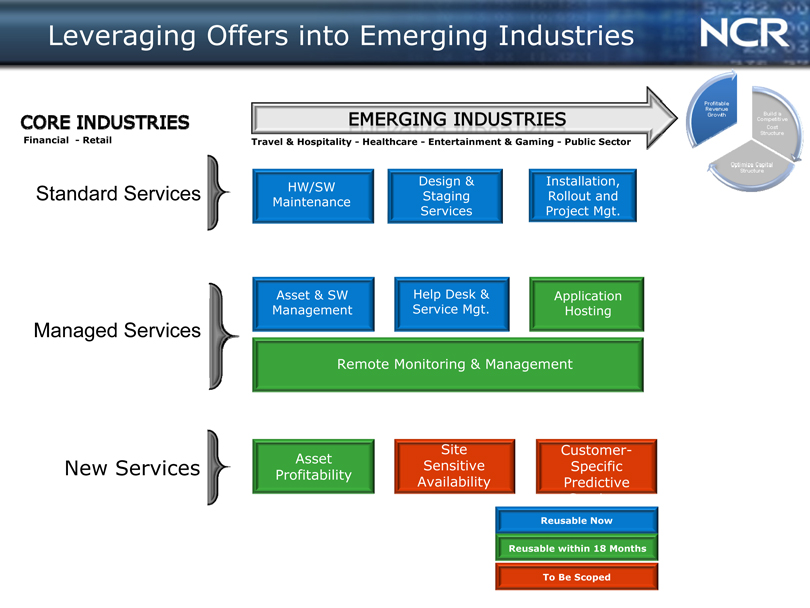

Leveraging Offers into Emerging Industries

CORE INDUSTRIES

Financial—Retail

EMERGING INDUSTRIES

Standard Services

HW/SW Maintenance

Design &

Staging

Services

Installation, Rollout and Project Mgt.

Managed Services

Asset & SW Management

Help Desk & Service Mgt.

I Application I Hosting

Remote Monitoring & Management

New Services

Asset Profitability

Site

Sensitive Availability

Customer- I

Specific I

Predictive I

|

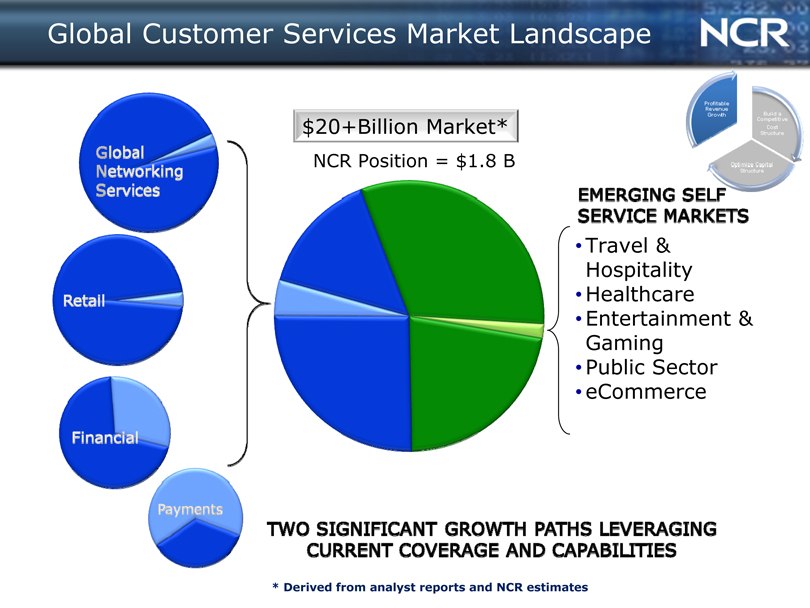

Global Customer Services Market Landscape

I Global^-^^ I Networking ^ Services

| $20+Billion Market* | NCR Position = $1.8 B

EMERGING SEL^555 SERVICE MARKETS

Retail

Travel &

Hospitality

Healthcare

Entertainment &

Gaming

Public Sector

eCommerce

I Financial

Payments 1

TWO SIGNIFICANT GROWTH PATHS LEVERAGING CURRENT COVERAGE AND CAPABILITIES

* |

| Derived from analyst reports and NCR estimates |

|

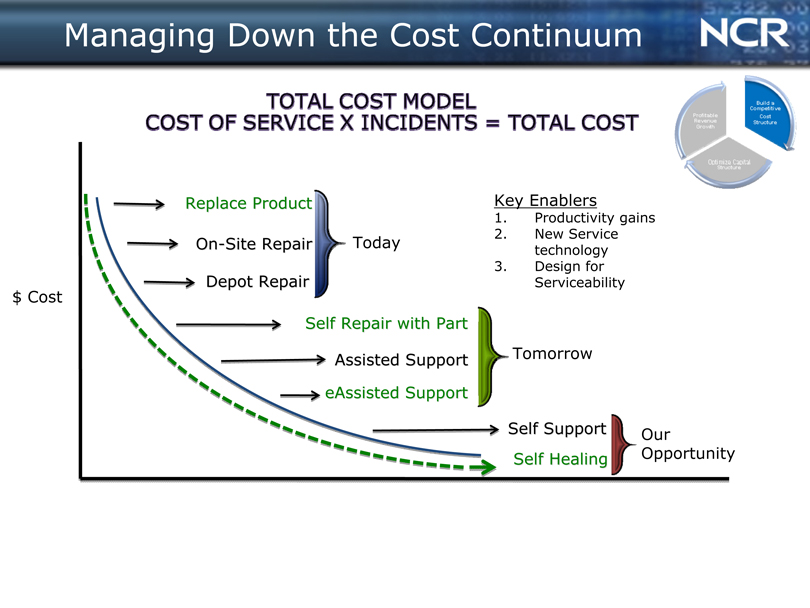

Managing Down the Cost Continuum

TOTAL COST MODEL COST OF SERVICE X INCIDENTS = TOTAL COST

|

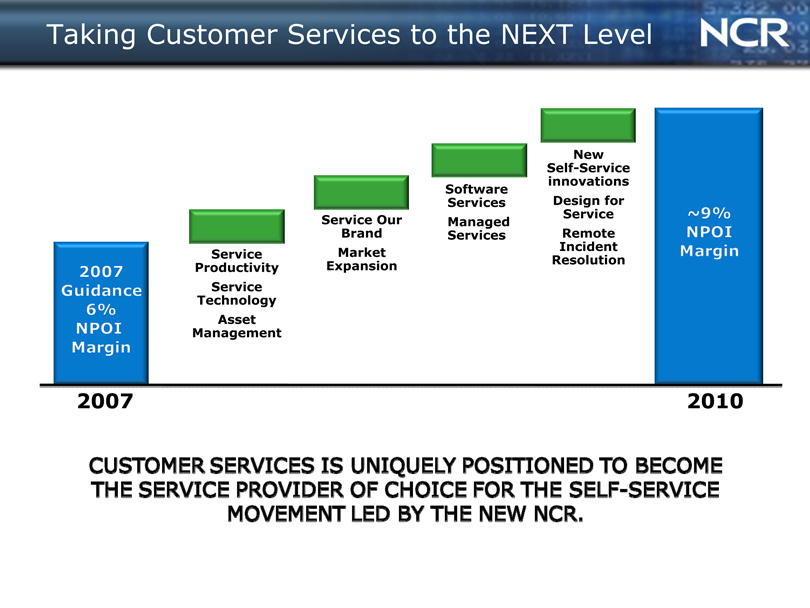

Taking Customer Services to the NEXT Level

I 2007 H Guidance H 6% H NPOI H Margin

Service Productivity

Service Technology

Asset Management

Service Our Brand

Market Expansion

Software Services

Managed Services

New

Self-Service innovations

Design for Service

Remote

Incident

Resolution

~9%

NPOI

Margin

2007

2010

CUSTOMER SERVICES IS UNIQUELY POSITIONED TO BECOME THE SERVICE PROVIDER OF CHOICE FOR THE SELF-SERVICE

MOVEMENT LED BY THE NEW NCR.

|

NCR Financial Strategy

Bob Fishman, CPA, CFA

Interim CFO and Corporate Controller

|

Creating Shareholder Value

|

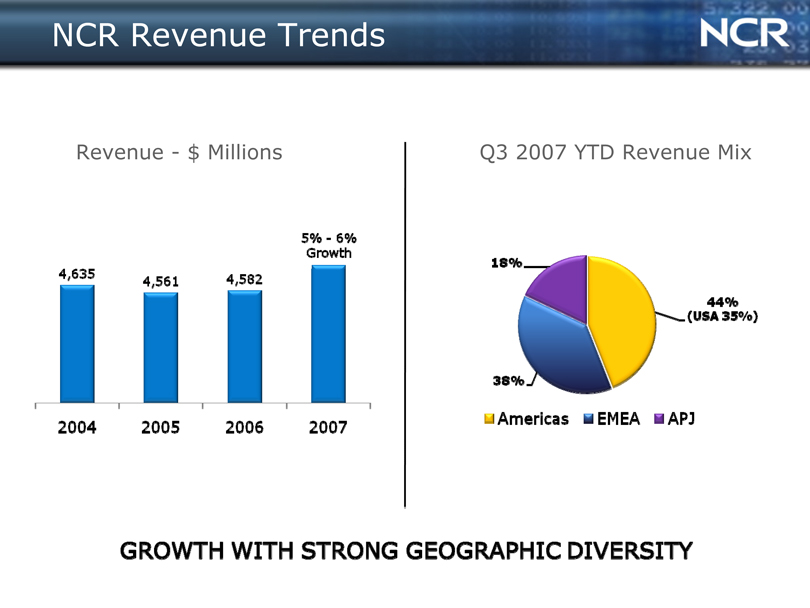

NCR Revenue Trends

Revenue—$ Millions

Q3 2007 YTD Revenue Mix

GROWTH WITH STRONG GEOGRAPHIC DIVERSITY

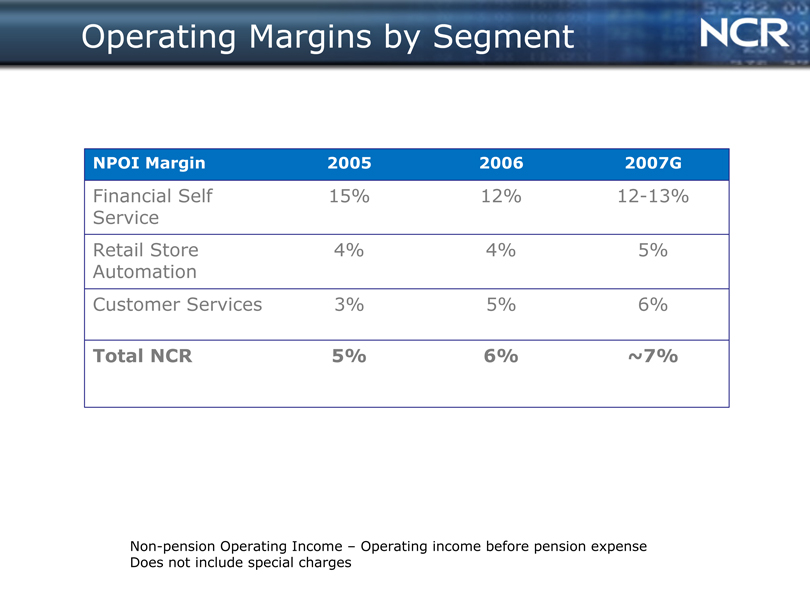

Operating Margins by Segment

F”-Ul”— “tH Hill ~m~

Financial Self 15% 12% 12-13% Service

Retail Store 4% 4% 5% Automation

Customer Services 3% 5% 6%

Total NCR 5% 6% ~7%

Non-pension Operating Income—Operating income before pension expense Does not include special charges

|

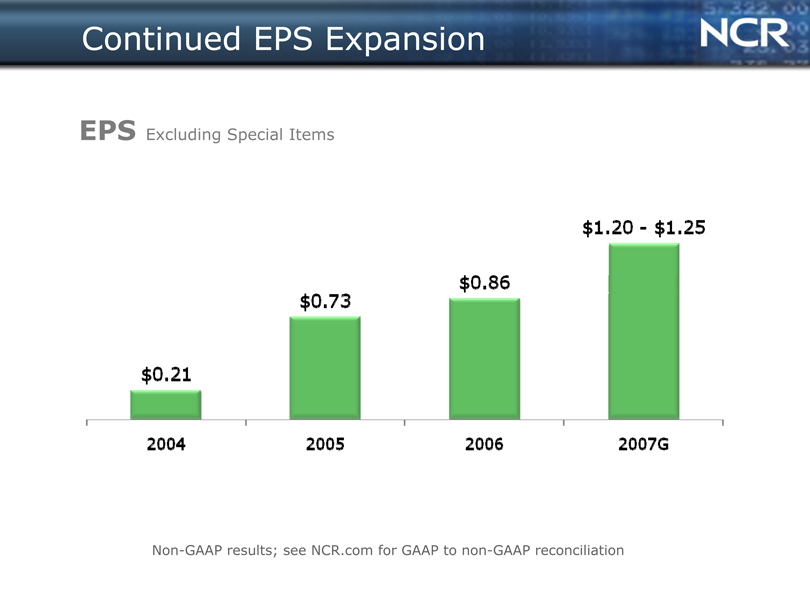

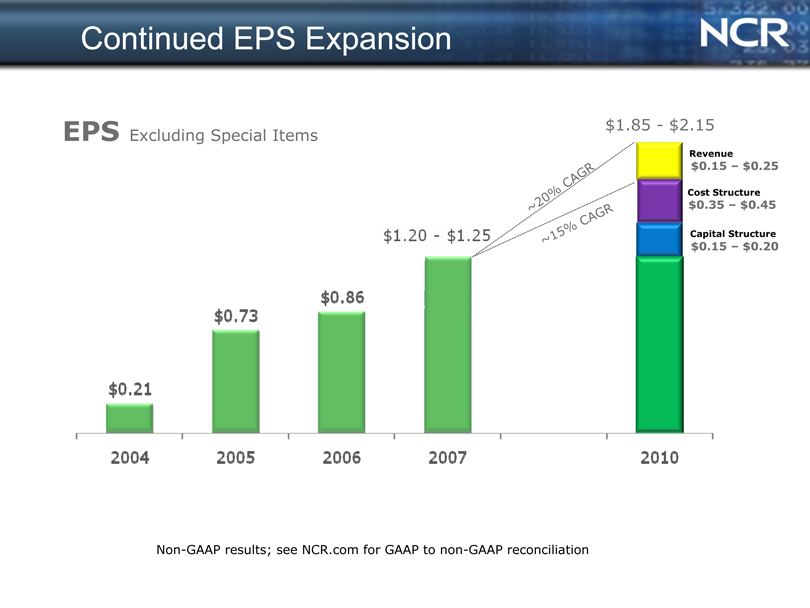

Continued EPS Expansion

EPS Excluding Special Items

Non-GAAP results; see NCR.com for GAAP to non-GAAP reconciliation

|

Creating Shareholder Value

|

Profitable Revenue Growth—2007 to 2010

|

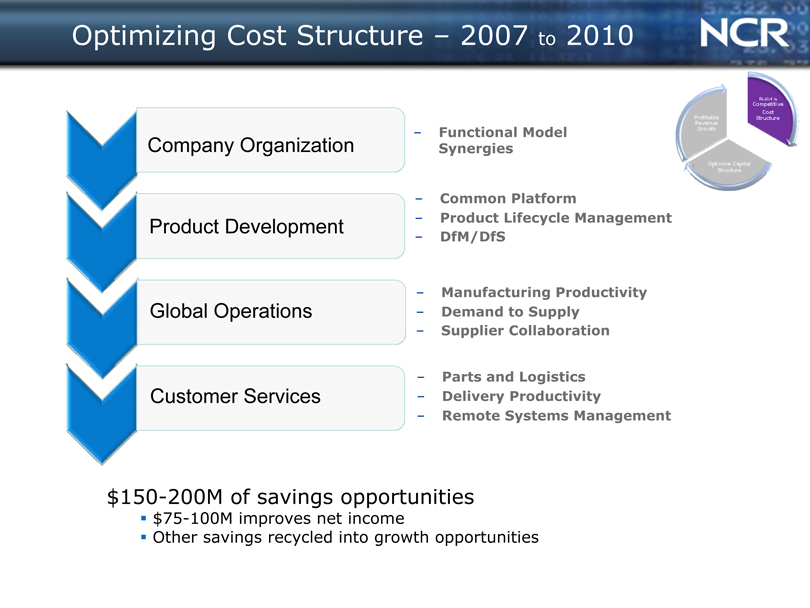

Optimizing Cost Structure—2007 to 2010

Company Organization Product Development Global Operations Customer Services

Functional Model Synergies

Common Platform

Product Lifecycle Management

DfM/DfS

Manufacturing Productivity Demand to Supply Supplier Collaboration

Parts and Logistics Delivery Productivity Remote Systems Management

$150-200M of savings opportunities

$75-100M improves net income

Other savings recycled into growth opportunities

|

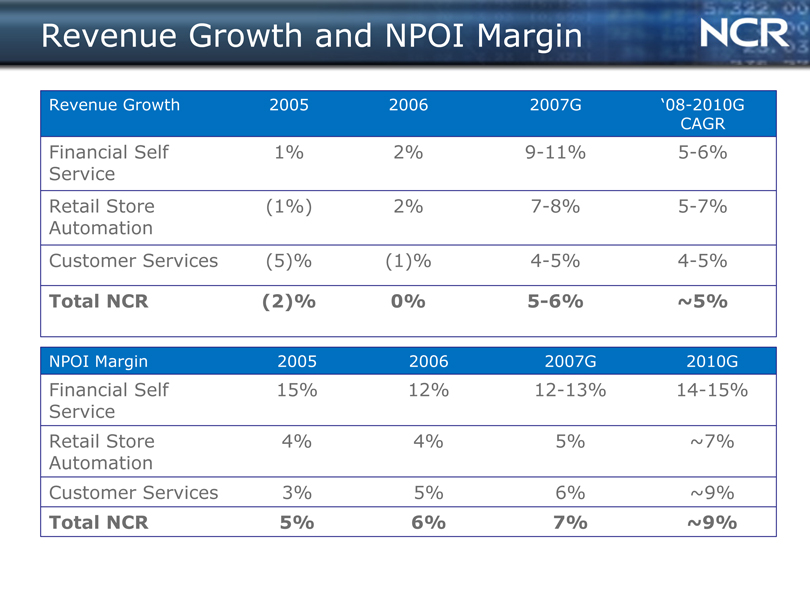

Revenue Growth and NPOI Margin

EJflBffRBPHil Efiffll EBBIM KiBflSI BIBSBBBCI

Service

Retail Store (1%) 2% 7-8% 5-7%

Automation

Customer Services (5)% (1)% 4-5% 4-5%

Total NCR (2)% 5-6% ~5%

Service

Retail Store 4% 4% 5% ~7%

Automation

Customer Services 3% 5% 6% ~9%

Total NCR 5% 6% 7% ~9%

|

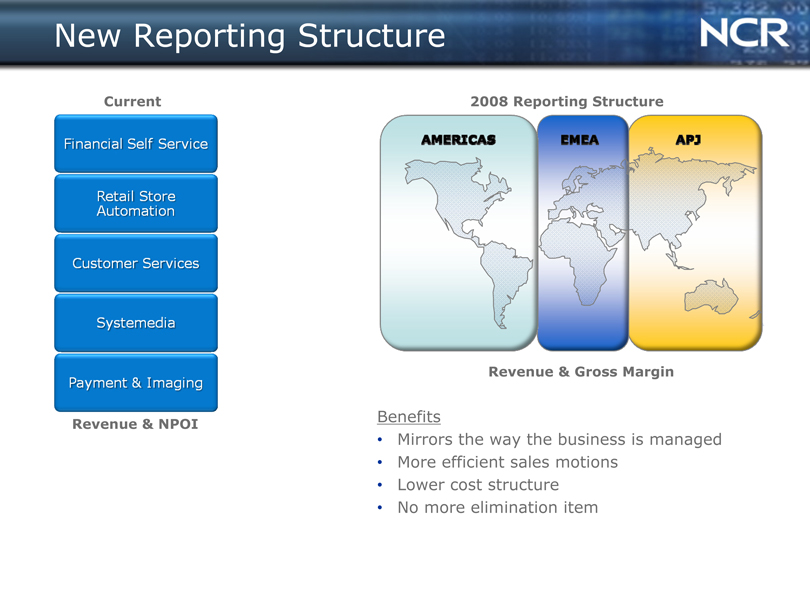

New Reporting Structure

Current

2008 Reporting Structure

Revenue & NPOI

Benefits

Mirrors the way the business is managed

More efficient sales motions

Lower cost structure

No more elimination item

|

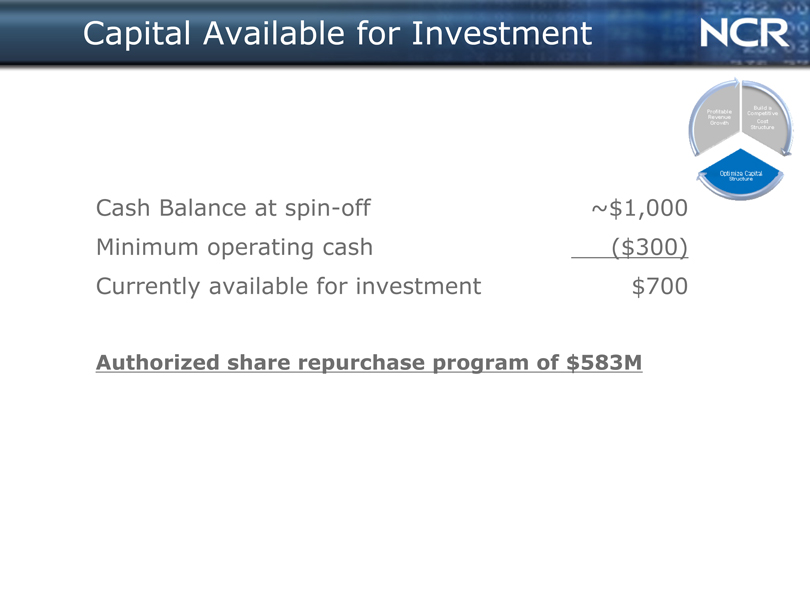

Capital Available for Investment

Cash Balance at spin-off ~$1,000

Minimum operating cash ($300)

Currently available for investment $700

Authorized share repurchase program of $583M

|

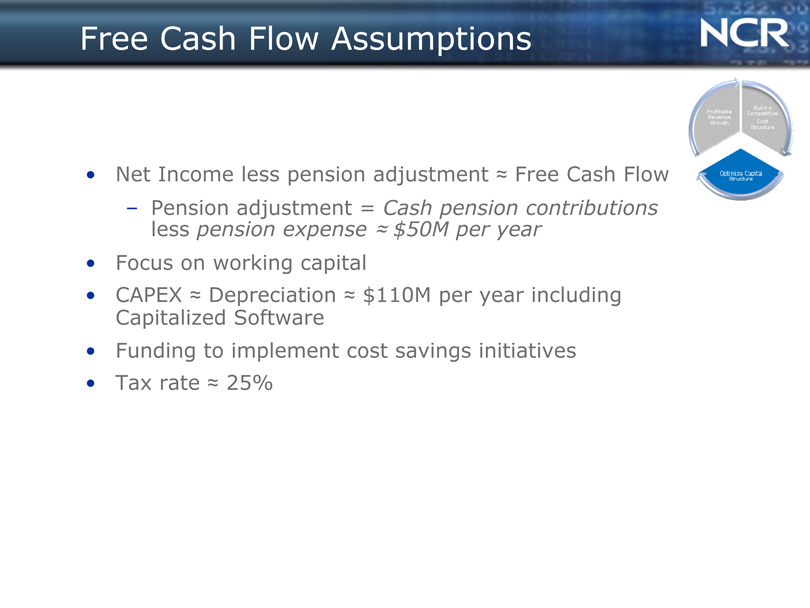

Free Cash Flow Assumptions

• Net Income less pension adjustment ~ Free Cash Flow

- Pension adjustment = Cash pension contributions less pension expense ? $50M per year

Focus on working capital

CAPEX ? Depreciation ? $110M per year including Capitalized Software

Funding to implement cost savings initiatives

Tax rate ? 25%

|

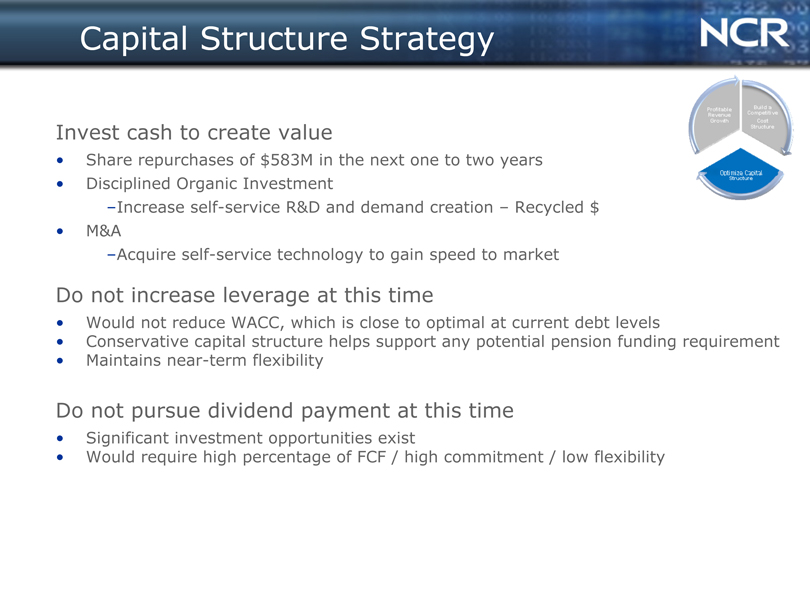

Capital Structure Strategy

Invest cash to create value

Share repurchases of $583M in the next one to two years

Disciplined Organic Investment

-Increase self-service R&D and demand creation—Recycled $

• M&A

-Acquire self-service technology to gain speed to market

Do not increase leverage at this time

Would not reduce WACC, which is close to optimal at current debt levels

Conservative capital structure helps support any potential pension funding requirement

Maintains near-term flexibility

Do not pursue dividend payment at this time

Significant investment opportunities exist

Would require high percentage of FCF / high commitment / low flexibility

|

Creating Shareholder Value

INCREASE IN EPS 2007 VERSUS 2010

$0.15—0.25/share

$0.35—0.45/share

$0.15—0.20/share

|

Continued EPS Expansion

EPS Excluding Special Items

Non-GAAP results; see NCR.com for GAAP to non-GAAP reconciliation

|

Questions