Exhibit 99.1

McDERMOTT INTERNATIONAL, INC.

The Oil Service Conference III

February 18, 2005

Cautionary Statements / Safe Harbor

Statements in this presentation which express a forecast, expectation or estimate, as well as those which are not historical fact, are forward looking. They involve a number of risks and uncertainties, including audit risks, which may cause actual results to differ materially from such forward-looking statements. These risks and uncertainties include factors detailed in McDermott International’s filings with the U.S. Securities & Exchange Commission, including its Form 10-K for the year ended December 31, 2003 and its Form 10-Q’s which are filed quarterly.

Enercom 2005 Oil Service Conference III February 18, 2005 2

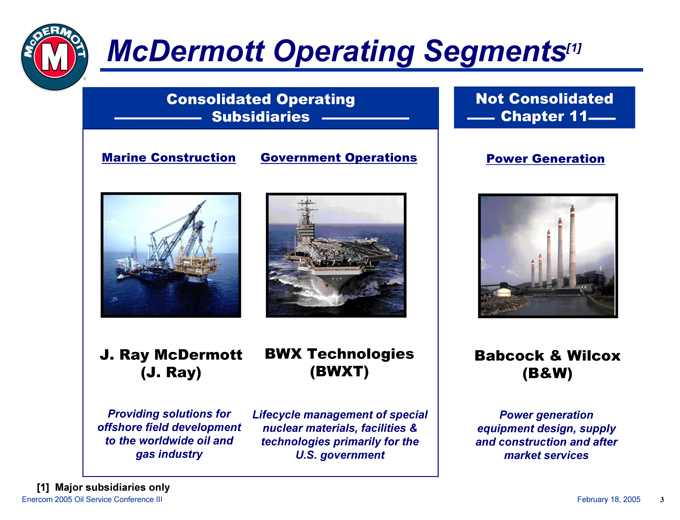

McDermott Operating Segments[1]

Consolidated Operating Subsidiaries

Marine Construction Government Operations

J. Ray McDermott BWX Technologies (J. Ray) (BWXT)

Providing solutions for offshore field development to the worldwide oil and gas industry

Lifecycle management of special nuclear materials, facilities & technologies primarily for the U.S. government

Not Consolidated Chapter 11

Power Generation

Babcock & Wilcox (B&W)

Power generation equipment design, supply and construction and after market services

[1] Major subsidiaries only

Enercom 2005 Oil Service Conference III February 18, 2005 3

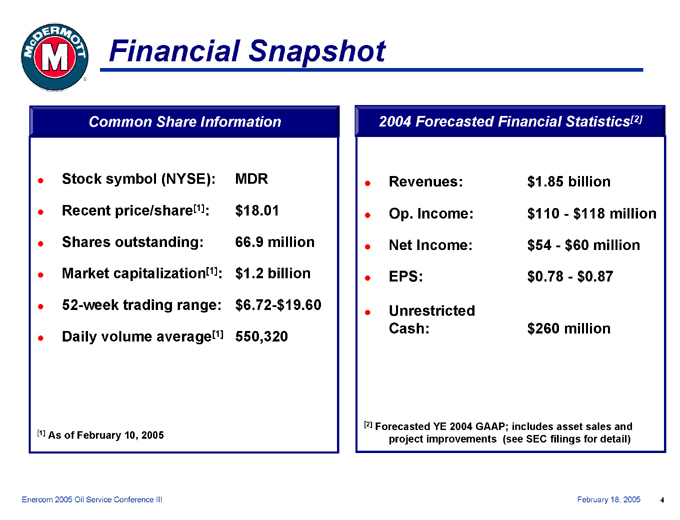

Financial Snapshot

Common Share Information

Stock symbol (NYSE): MDR

Recent price/share[1]: $18.01

Shares outstanding: 66.9 million

Market capitalization[1]: $1.2 billion

52-week trading range: $6.72-$19.60

Daily volume average[1] 550,320

[1] As of February 10, 2005

2004 Forecasted Financial Statistics[2]

Revenues: $1.85 billion

Op. Income: $110 - $118 million

Net Income: $54 - $60 million

EPS: $0.78 - $0.87

Unrestricted

Cash: $260 million

[2] Forecasted YE 2004 GAAP; includes asset sales and project improvements (see SEC filings for detail)

Enercom 2005 Oil Service Conference III February 18, 2005 4

Investment Highlights

Industry-leading, franchise-name businesses Valued supplier to our customers Improved bidding discipline at J. Ray Solid, predictable backlog at BWXT

B&W Chapter 11 bankruptcy resolution in sight Financial restructuring complete, liquidity improved Experienced, shareholder-focused management team

Enercom 2005 Oil Service Conference III February 18, 2005 5

McDERMOTT INTERNATIONAL, INC.

J. Ray’s Core Capabilities

Providing solutions for offshore field developments worldwide

Engineering and Procurement

Fabrication:

Jackets, Hulls, FPSOs, TLP’s and Topsides

Installation:

Platforms, Hulls, FPSOs, TLP’s, Topsides and Pipelines

Subsea/Deepwater Technology

Enercom 2005 Oil Service Conference III February 18, 2005 7

J. Ray McDermott Snapshot

Long, established track record as a pioneer in the marine construction industry

Worldwide operations

Location Facility Vessels

Asia Pacific (Batam) Fab 3

Caspian (Baku) Fab 1 (Operate only)

Gulf of Mexico (Morgan City) Fab 3

Middle East (Dubai) Fab 1

Mexico (Veracruz) Ship Repair 5 (Joint Venture)

9,100 employees

Enercom 2005 Oil Service Conference III February 18, 2005 8

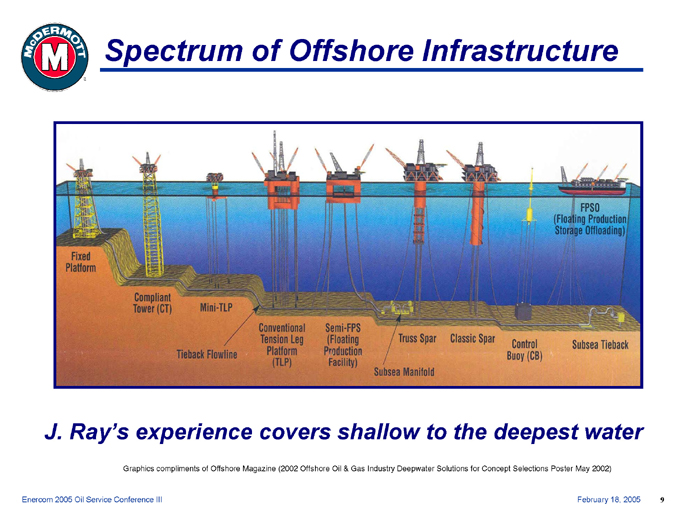

Spectrum of Offshore Infrastructure

J. Ray’s experience covers shallow to the deepest water

Graphics compliments of Offshore Magazine (2002 Offshore Oil & Gas Industry Deepwater Solutions for Concept Selections Poster May 2002)

Fixed Platform Compliant Tower (CT) Mini-TLP Conventional Tension Leg Platform (TLP)

Semi-FPS (Floating Production Facility) Truss Spar Classic Spar Classic Spar Control Buoy (CB) Subsea Tieback

Tieback Flowline FPSO (Floating Production Storage Offloading)

Enercom 2005 Oil Service Conference III February 18, 2005 9

Strong Relationships with Major Offshore Operators

Enercom 2005 Oil Service Conference III February 18, 2005 10

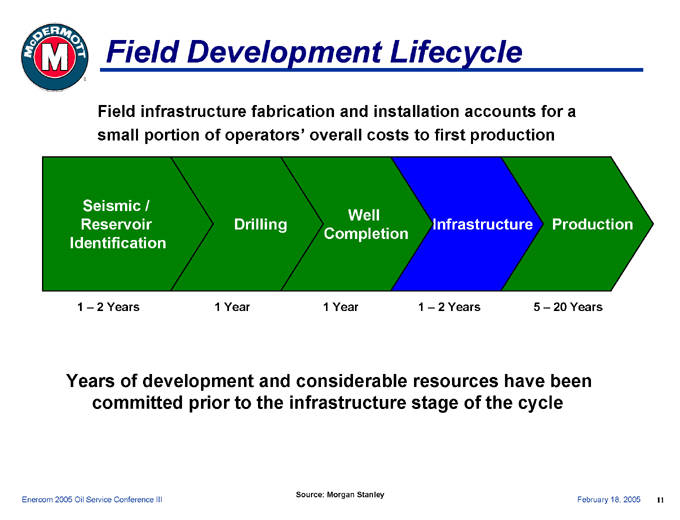

Field Development Lifecycle

Field infrastructure fabrication and installation accounts for a small portion of operators’ overall costs to first production

Seismic / Reservoir Identification

Well Completion

Drilling

Infrastructure

Production

1 – 2 Years 1 Year 1 Year 1 – 2 Years 5 – 20 Years

Years of development and considerable resources have been committed prior to the infrastructure stage of the cycle

Source: Morgan Stanley

Enercom 2005 Oil Service Conference III February 18, 2005 11

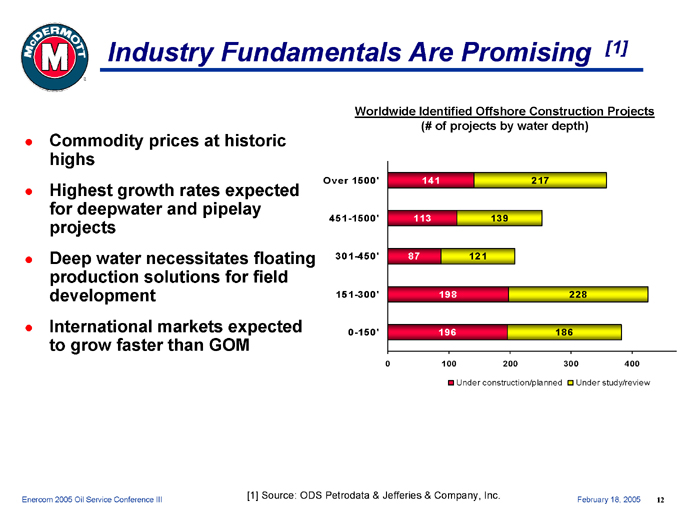

Industry Fundamentals Are Promising [1]

Commodity prices at historic highs

Highest growth rates expected for deepwater and pipelay projects

Deep water necessitates floating production solutions for field development

International markets expected to grow faster than GOM

Worldwide Identified Offshore Construction Projects (# of projects by water depth)

Over 1500’

451-1500’

301-450’

151-300’

0-150’

141 217

113 139

87 121

198 228

196 186

0 100 200 300 400

Under construction/planned Under study/review

Enercom 2005 Oil Service Conference III [1] Source: ODS Petrodata & Jefferies & Company, Inc. February 18, 2005 12

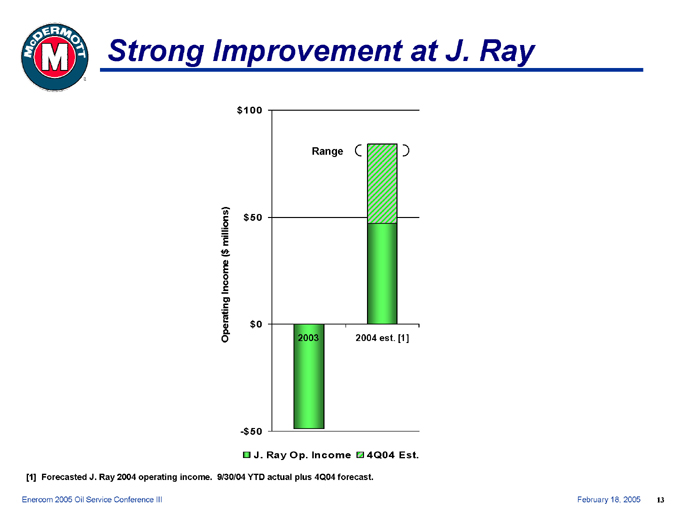

Strong Improvement at J. Ray

Range

2003 2004 est. [1]

J. Ray Op. Income 4Q04 Est.

$100 $50 $0 -$50 Operating Income ($ millions)

[1] Forecasted J. Ray 2004 operating income. 9/30/04 YTD actual plus 4Q04 forecast.

Enercom 2005 Oil Service Conference III February 18, 2005 13

J. Ray Turnaround in Progress

Recruited and built new leadership organization

Substantial improvements in business development, bidding, execution, and planning processes

Maintain strong historical relationships with key customers

Expect to successfully execute current backlog; approximately $1.2 billion at 12/31/04

Our challenge is to turn $1.2 billion of bids into profitable orders

Enercom 2005 Oil Service Conference III February 18, 2005 14

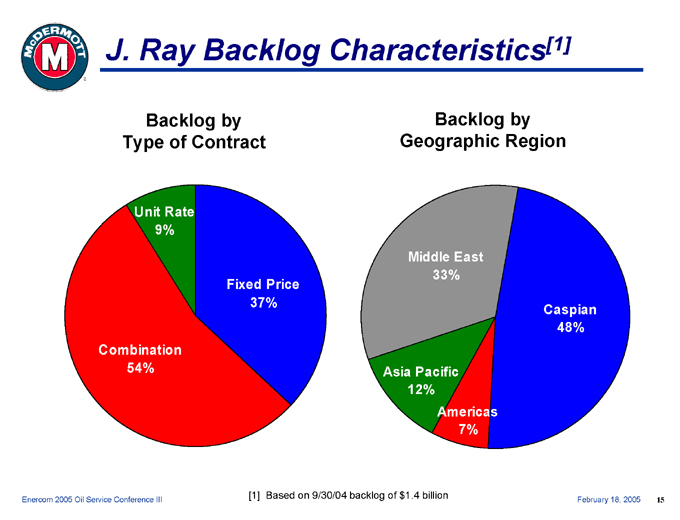

J. Ray Backlog Characteristics[1]

Backlog by Type of Contract

Unit Rate 9%

Fixed Price 37%

Combination 54%

Backlog by Geographic Region

Middle East 33%

Caspian 48%

Americas 7%

Asia Pacific 12%

Enercom 2005 Oil Service Conference III [1] Based on 9/30/04 backlog of $1.4 billion February 18, 2005 15

J. Ray Summary

Well positioned to capture industry growth

Strong franchise in strategic geographical locations

New management team leading change in all areas

$1.2 billion backlog and good growth prospects

Turnaround is underway but not yet complete

Enercom 2005 Oil Service Conference III February 18, 2005 16

BWXT is the premier manager of complex, high-consequence nuclear and national security operations. We are disciplined operators and managers of nuclear production facilities, who deliver value and customer confidence.

McDERMOTT INTERNATIONAL, INC.

BWXT Serves Two Key Roles

Manufactures, and is the premier supplier of, nuclear components for the U.S. Navy

2 divisions: Nuclear products & nuclear equipment

Provide the critical skills and resources that produce propulsion systems for the U.S. Navy

Financial results are in consolidated statements

Manage and operate sites for Dept. of Energy

12 sites managed primarily by LLCs with JV partners

Primarily equity method accounting, income from investees

Enercom 2005 Oil Service Conference III February 18, 2005 18

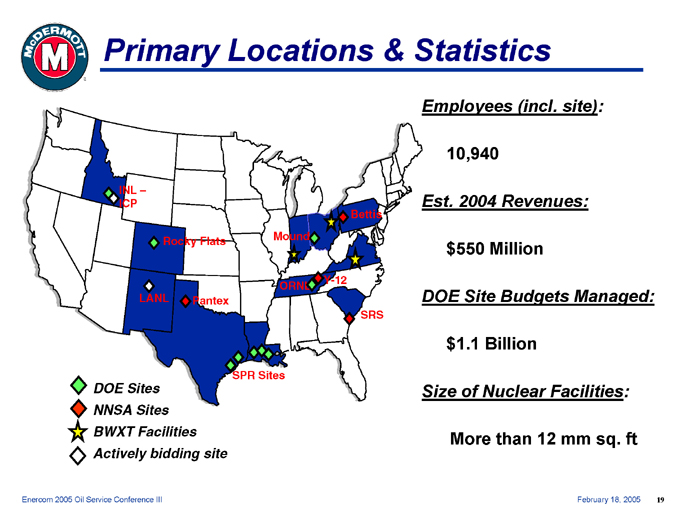

Primary Locations & Statistics

Employees (incl. site):

10,940

Est. 2004 Revenues:

$550 Million

DOE Site Budgets Managed:

$1.1 Billion

Size of Nuclear Facilities:

More than 12 mm sq. ft

INL – ICP

Bettis Rocky Flats Mound

Y-12 ORNL

LANL Pantex

SRS

SPR Sites

DOE Sites NNSA Sites BWXT Facilities Actively bidding site

Enercom 2005 Oil Service Conference III February 18, 2005 19

BWXT Growth Drivers

Ship & submarine building rates

Refuel

New M&O opportunities

Space reactor programs

Down-blending services

Funding of strategic & environmental programs

Regulatory and policy changes

Enercom 2005 Oil Service Conference III February 18, 2005 20

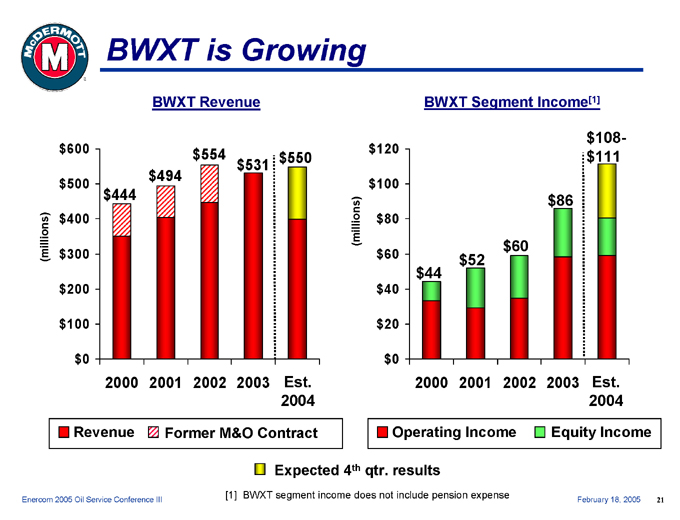

BWXT is Growing

BWXT Revenue $600

$500

(millions) $400 $300 $200 $100 $0 $554 $550 $531 $494 $444

2000 2001 2002 2003 Est.

2004 $120

$100

(millions) $80

$60 $40 $20 $0 $108-$111

$86

$60 $52 $44

2000 2001 2002 2003 Est.

2004

Revenue Former M&O Contract Operating Income Equity Income

Expected 4th qtr. results

[1] BWXT segment income does not include pension expense

Enercom 2005 Oil Service Conference III February 18, 2005 21

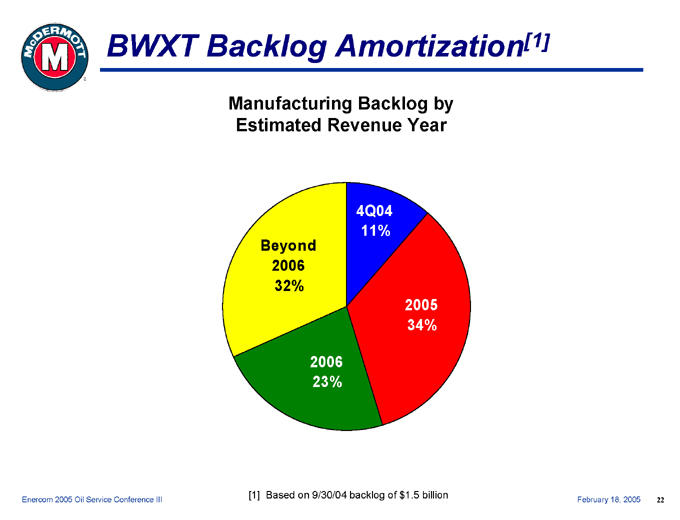

BWXT Backlog Amortization[1]

Manufacturing Backlog by Estimated Revenue Year

Beyond 2006 32%

4Q04 11%

2005 34%

2006 23%

[1] Based on 9/30/04 backlog of $1.5 billion

Enercom 2005 Oil Service Conference III February 18, 2005 22

BWXT’s Strategy

Maintain leadership position

Maintain customer confidence

Generate cost reductions

Explore opportunities selectively outside the U.S.

Continue strong operational and financial performance

Enercom 2005 Oil Service Conference III February 18, 2005 23

McDERMOTT INTERNATIONAL, INC.

B&W Snapshot

The Babcock & Wilcox Company was incorporated in 1881

Premier coal-fired boiler manufacturer for electricity generation

Today’s key products and services

OEM boilers and related equipment to generate steam and power

Environmental and emission reduction equipment

Upgrades, service and replacement parts

EPIC coal-fired power plants & projects

Field engineering and construction services

Replacement nuclear steam generators (US and Canada)

Nuclear service and parts (Canada)

World-wide locations

Approximately 10,700 employees

Enercom 2005 Oil Service Conference III February 18, 2005 25

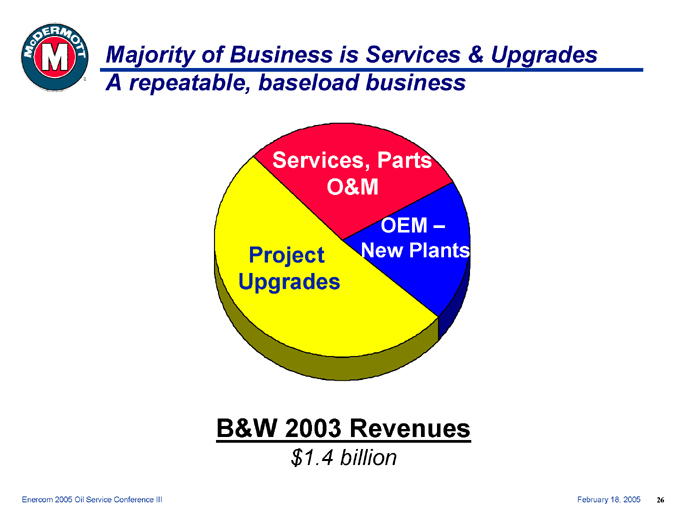

Majority of Business is Services & Upgrades A repeatable, baseload business

Services, Parts O&M

Project Upgrades

OEM – New Plants

B&W 2003 Revenues

$1.4 billion

Enercom 2005 Oil Service Conference III February 18, 2005 26

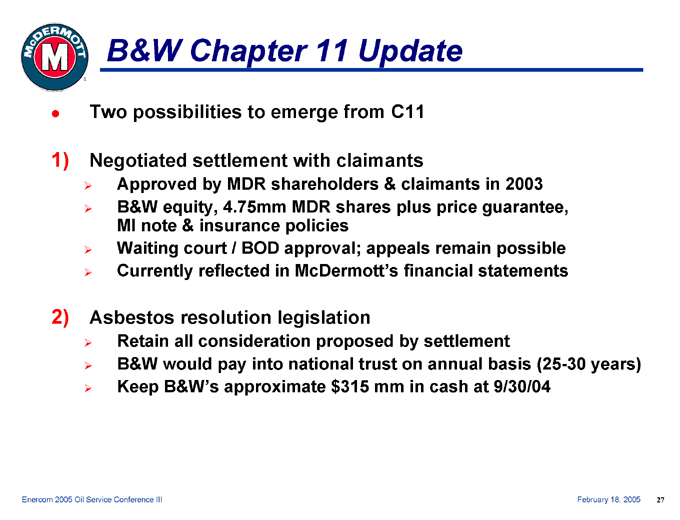

B&W Chapter 11 Update

Two possibilities to emerge from C11

1) Negotiated settlement with claimants

Approved by MDR shareholders & claimants in 2003

B&W equity, 4.75mm MDR shares plus price guarantee, MI note & insurance policies

Waiting court / BOD approval; appeals remain possible

Currently reflected in McDermott’s financial statements

2) Asbestos resolution legislation

Retain all consideration proposed by settlement

B&W would pay into national trust on annual basis (25-30 years)

Keep B&W’s approximate $315 mm in cash at 9/30/04

Enercom 2005 Oil Service Conference III February 18, 2005 27

Financial Review

McDERMOTT INTERNATIONAL, INC.

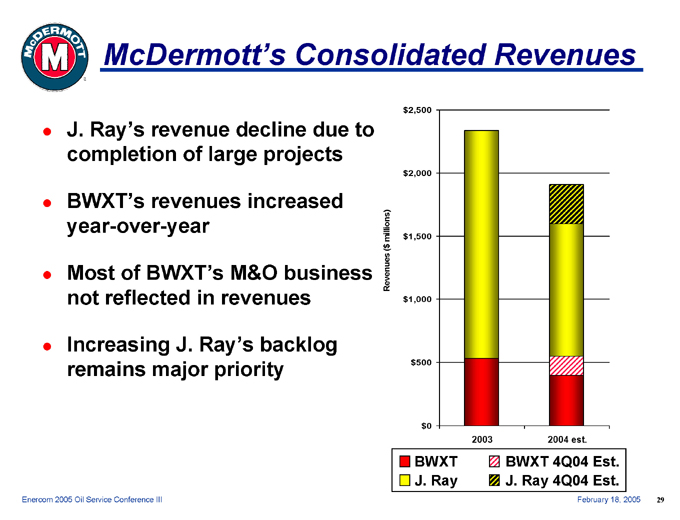

McDermott’s Consolidated Revenues

J. Ray’s revenue decline due to completion of large projects

BWXT’s revenues increased year-over-year

Most of BWXT’s M&O business not reflected in revenues

Increasing J. Ray’s backlog remains major priority $2,500

$2,000

$1,500 Revenues ($ millions)

$1,000 $500 $0

2003 2004 est.

BWXT BWXT 4Q04 Est. J. Ray J. Ray 4Q04 Est.

Enercom 2005 Oil Service Conference III February 18, 2005 29

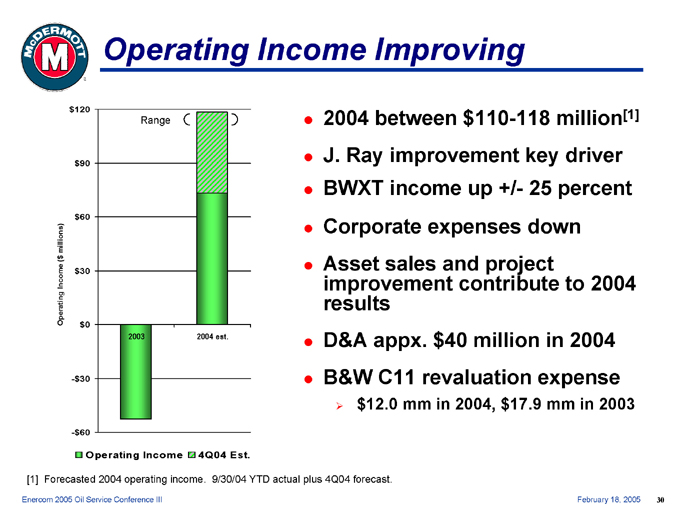

Operating Income Improving $120

$90

$60

Operating Income ($ millions)

$30

$0

-$30

-$60

Range 2003 2004 est.

Operating Income 4Q04 Est.

2004 between $110-118 million[1]

J. Ray improvement key driver

BWXT income up +/- 25 percent

Corporate expenses down

Asset sales and project improvement contribute to 2004 results

D&A appx. $40 million in 2004

B&W C11 revaluation expense

$12.0 mm in 2004, $17.9 mm in 2003

[1] Forecasted 2004 operating income. 9/30/04 YTD actual plus 4Q04 forecast.

Enercom 2005 Oil Service Conference III February 18, 2005 30

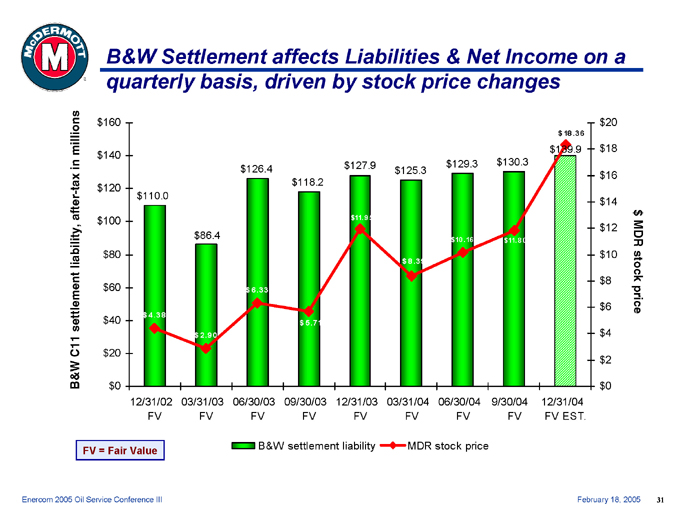

B&W Settlement affects Liabilities & Net Income on a quarterly basis, driven by stock price changes

B&W C11 settlement liability, after-tax in millions $160 $140 $120 $100 $80 $60 $40 $20 $0 $110.0

$4.38

12/31/02 FV

$86.4

$2.90

03/31/03 FV

$126.4

$6.33

06/30/03 FV

$118.2

$5.71

09/30/03 FV

$127.9

$11.95

12/31/03 FV

$125.3

$8.39

03/31/04 FV

$129.3

$10 .16

06/30/04 FV

$130.3

$11.80

9/30/04 FV

$18.36

$139.9

12/31/04 FV EST.

$20

$18

$16

$14

$ MDR stock price

$12

$10

$8

$6

$4

$2

$0

FV = Fair Value

B&W settlement liability MDR stock price

Enercom 2005 Oil Service Conference III February 18, 2005 31

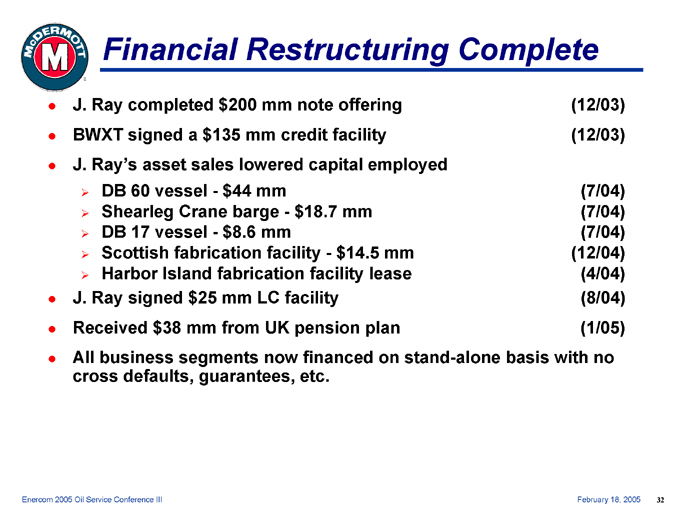

Financial Restructuring Complete

J. Ray completed $200 mm note offering (12/03)

BWXT signed a $135 mm credit facility (12/03)

J. Ray’s asset sales lowered capital employed

DB 60 vessel - $44 mm (7/04)

Shearleg Crane barge - $18.7 mm (7/04)

DB 17 vessel - $8.6 mm (7/04)

Scottish fabrication facility - $14.5 mm (12/04)

Harbor Island fabrication facility lease (4/04)

J. Ray signed $25 mm LC facility (8/04)

Received $38 mm from UK pension plan (1/05)

All business segments now financed on stand-alone basis with no cross defaults, guarantees, etc.

Enercom 2005 Oil Service Conference III February 18, 2005 32

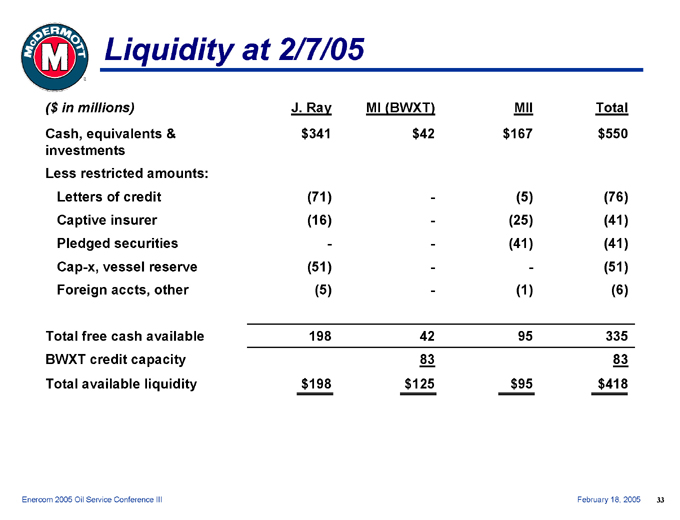

Liquidity at 2/7/05

($ in millions) J. Ray MI (BWXT) MII Total

Cash, equivalents & investments $341 $42 $167 $550

Less restricted amounts:

Letters of credit (71) - (5) (76)

Captive insurer (16) - (25) (41)

Pledged securities - - (41) (41)

Cap-x, vessel reserve (51) - - (51)

Foreign accts, other (5) - (1) (6)

Total free cash available 198 42 95 335

BWXT credit capacity 83 83

Total available liquidity $198 $125 $95 $418

Enercom 2005 Oil Service Conference III February 18, 2005 33

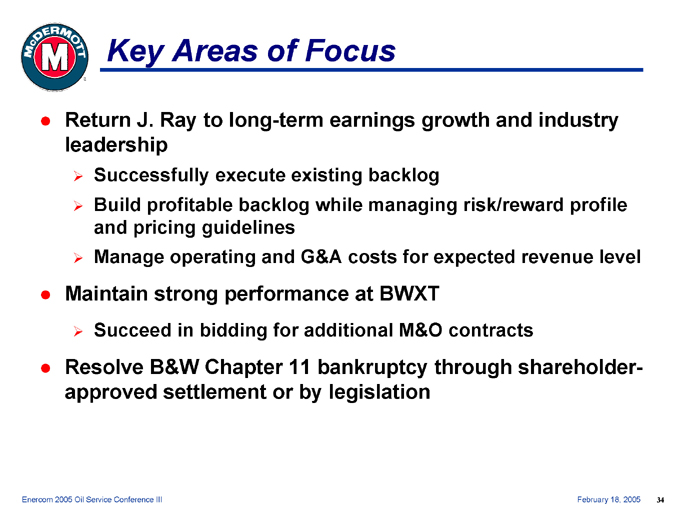

Key Areas of Focus

Return J. Ray to long-term earnings growth and industry leadership

Successfully execute existing backlog

Build profitable backlog while managing risk/reward profile and pricing guidelines

Manage operating and G&A costs for expected revenue level

Maintain strong performance at BWXT

Succeed in bidding for additional M&O contracts

Resolve B&W Chapter 11 bankruptcy through shareholder-approved settlement or by legislation

Enercom 2005 Oil Service Conference III February 18, 2005 34

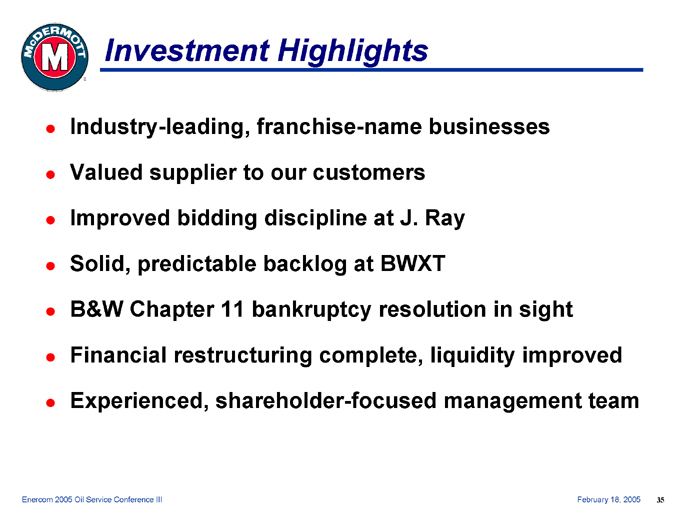

Investment Highlights

Industry-leading, franchise-name businesses

Valued supplier to our customers

Improved bidding discipline at J. Ray

Solid, predictable backlog at BWXT

B&W Chapter 11 bankruptcy resolution in sight

Financial restructuring complete, liquidity improved

Experienced, shareholder-focused management team

Enercom 2005 Oil Service Conference III February 18, 2005 35

McDERMOTT INTERNATIONAL, INC.

(NYSE: MDR)

For more information contact:

Jay Roueche

Director of Investor Relations 281-870-5462