EXHIBIT 13

2013 Annual Report 1863 ➔ 2013 YEARS 150 Here. Now.

2013 Annual Report 1863 ➔ 2013 YEARS 150 Here. Now.First Financial Bancorp

2013 Performance KEY FINANCIAL RESULTS AND TRENDS Return on Average Assets Return on Average Shareholders’ Equity 1.0% .8% .6% .4% .2% 0% 93 consecutive quarters of profitability Total uncovered loans of $3.5 billion, an increase of $326.6 million, or 10.3%, compared to December 31, 2012 Total nonperforming loans declined $23.2 million, or 30.6%, compared to December 31, 2012 10% 8% 6% 4% 2% 0% 16% 12% 8% 4% 0% Capital Ratios 9. 2 0 % 8. 56 % 14 .1 8 % 15 .8 8 % 12 .9 9 % 14 .6 1 % First Financial Tangible Common Equity Ratio First Financial Tier 1 Capital Ratio First Financial Total Capital Ratio KBW Regional Bank Index Components - Median Value 1. 0 4 % 0. 7 7 % 0 .9 7 % 8. 35 % 9 .3 2 % 6. 89 % For Full Year 2013 For Full Year 2013 Net Interest Margin Dividend Yield *Adjusted to exclude Pension Settlement Charges and FDIC Indemnification Impairment 4% 3% 2% 1% 0% 4% 3% 2% 1% 0% 3. 97 % 3. 58 % 3. 4 4 % 2 .1 6 % First Financial, as reported First Financial, as adjusted* KBW Regional Bank Index Components - Median Value At December 31, 2013For Full Year 2013

2013 Performance KEY FINANCIAL RESULTS AND TRENDS Return on Average Assets Return on Average Shareholders’ Equity 1.0% .8% .6% .4% .2% 0% 93 consecutive quarters of profitability Total uncovered loans of $3.5 billion, an increase of $326.6 million, or 10.3%, compared to December 31, 2012 Total nonperforming loans declined $23.2 million, or 30.6%, compared to December 31, 2012 10% 8% 6% 4% 2% 0% 16% 12% 8% 4% 0% Capital Ratios 9. 2 0 % 8. 56 % 14 .1 8 % 15 .8 8 % 12 .9 9 % 14 .6 1 % First Financial Tangible Common Equity Ratio First Financial Tier 1 Capital Ratio First Financial Total Capital Ratio KBW Regional Bank Index Components - Median Value 1. 0 4 % 0. 7 7 % 0 .9 7 % 8. 35 % 9 .3 2 % 6. 89 % For Full Year 2013 For Full Year 2013 Net Interest Margin Dividend Yield *Adjusted to exclude Pension Settlement Charges and FDIC Indemnification Impairment 4% 3% 2% 1% 0% 4% 3% 2% 1% 0% 3. 97 % 3. 58 % 3. 4 4 % 2 .1 6 % First Financial, as reported First Financial, as adjusted* KBW Regional Bank Index Components - Median Value At December 31, 2013For Full Year 2013

Here. Now. ALwAYS GRowING. 2013 was an eventful year for First Financial. We saw continued loan growth and positive momentum in our financial results, strategic priorities, brand awareness and geographic presence. It was a year of carrying our vision forward for the benefit of our clients, associates, shareholders and business partners. We’ve gained momentum from a wide variety of initiatives and the hard work that our associates do every day. Our market expansion into Columbus, Ohio and Fort Wayne, Indiana will provide many new opportunities to serve clients and grow our business. New products and investments in banking centers and technology are making it easier to meet client needs and serve them in more ways. The sales teams achieved significant progress in growing loan balances, which fuels our success. Achievement of our efficiency objectives, while difficult, happened thanks to the efforts of associates across the organization who found ways to work smarter and save money. Effective credit discipline and asset resolution activities led to meaningful improvement in asset quality metrics. Continued enhancement of our enterprise risk management program to further align activities with line of business strategies. It was also a year of reflection, celebration and remembering our roots. 2013 marked First Financial’s 150th anniversary. Since 1863 the bank has maintained a consistent mission and focus. It’s amazing how our heritage has prepared us to make strategic decisions here, now and for the future. It is true that our roots have given us strong wings. The story of First Financial and our ability to survive and thrive for fifteen decades is compelling and sets the stage for our continuing success. We hope you will take some time to read more about our story that begins on the back cover. It’s worth the read! This year First Financial reached a company milestone by celebrating its 150th anniversary

First Financial Bancorp 2013 Annual Report 1

*Excludes covered loans Commercial Banking First Financial offers the same sophisticated products as the larger regional banks, but our size allows us to make decisions at the local level and support our clients’ success. This high-quality service, delivered by experienced bankers, deepens client relationships and has helped us build a solid reputation in the communities we serve. Traditional commercial and industrial balances, including owner-occupied commercial real estate loans, increased $170.3 million, or 26.6 percent.* Specialty finance balances, comprised of asset-based lending and equipment finance, increased $81.3 million, or 73.3 percent. Franchise finance, a lender in the franchise restaurant segment, grew its balances $80.3 million, or 26.0 percent.* Average commercial deposit balances increased $70.8 million, or 9.3 percent. wealth Management During 2013, our wealth management group continued to refine and improve its investment management process. The team utilizes a holistic approach with the objective of growing, preserving and ultimately transferring our clients’ wealth with services delivered in a solutions-based, rather than a product-based, manner. Implementation of our flagship core strategic portfolios built to comprehensively address portfolio needs across the classic risk spectrum. Significant product and technology investments in our Retirement Plan Services business to assist employers in providing competitive retirement benefit packages. Total client assets under management and administration increased 6.7 percent. Total investment advisory, trust administration and retirement plan services revenues increased 2.6 percent. Capitalizing on our competitive advantages to BUILD STRoNGER

2 First Financial Bancorp 2013 Annual Report

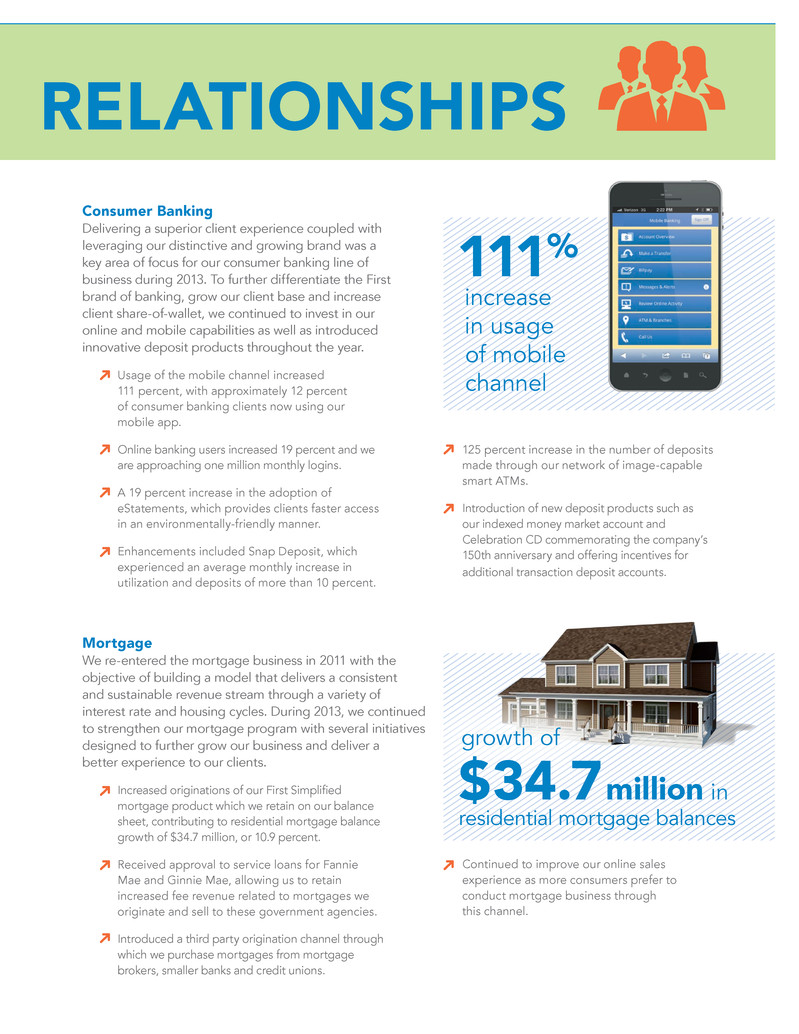

Mortgage We re-entered the mortgage business in 2011 with the objective of building a model that delivers a consistent and sustainable revenue stream through a variety of interest rate and housing cycles. During 2013, we continued to strengthen our mortgage program with several initiatives designed to further grow our business and deliver a better experience to our clients. Increased originations of our First Simplified mortgage product which we retain on our balance sheet, contributing to residential mortgage balance growth of $34.7 million, or 10.9 percent. Received approval to service loans for Fannie Mae and Ginnie Mae, allowing us to retain increased fee revenue related to mortgages we originate and sell to these government agencies. Introduced a third party origination channel through which we purchase mortgages from mortgage brokers, smaller banks and credit unions. Continued to improve our online sales experience as more consumers prefer to conduct mortgage business through this channel. Consumer Banking Delivering a superior client experience coupled with leveraging our distinctive and growing brand was a key area of focus for our consumer banking line of business during 2013. To further differentiate the First brand of banking, grow our client base and increase client share-of-wallet, we continued to invest in our online and mobile capabilities as well as introduced innovative deposit products throughout the year. Usage of the mobile channel increased 111 percent, with approximately 12 percent of consumer banking clients now using our mobile app. Online banking users increased 19 percent and we are approaching one million monthly logins. A 19 percent increase in the adoption of eStatements, which provides clients faster access in an environmentally-friendly manner. Enhancements included Snap Deposit, which experienced an average monthly increase in utilization and deposits of more than 10 percent. 125 percent increase in the number of deposits made through our network of image-capable smart ATMs. Introduction of new deposit products such as our indexed money market account and Celebration CD commemorating the company’s 150th anniversary and offering incentives for additional transaction deposit accounts. RELATIoNSHIPS 111% increase in usage of mobile channel growth of $34.7 million in residential mortgage balance

First Financial Bancorp 2013 Annual Report 3

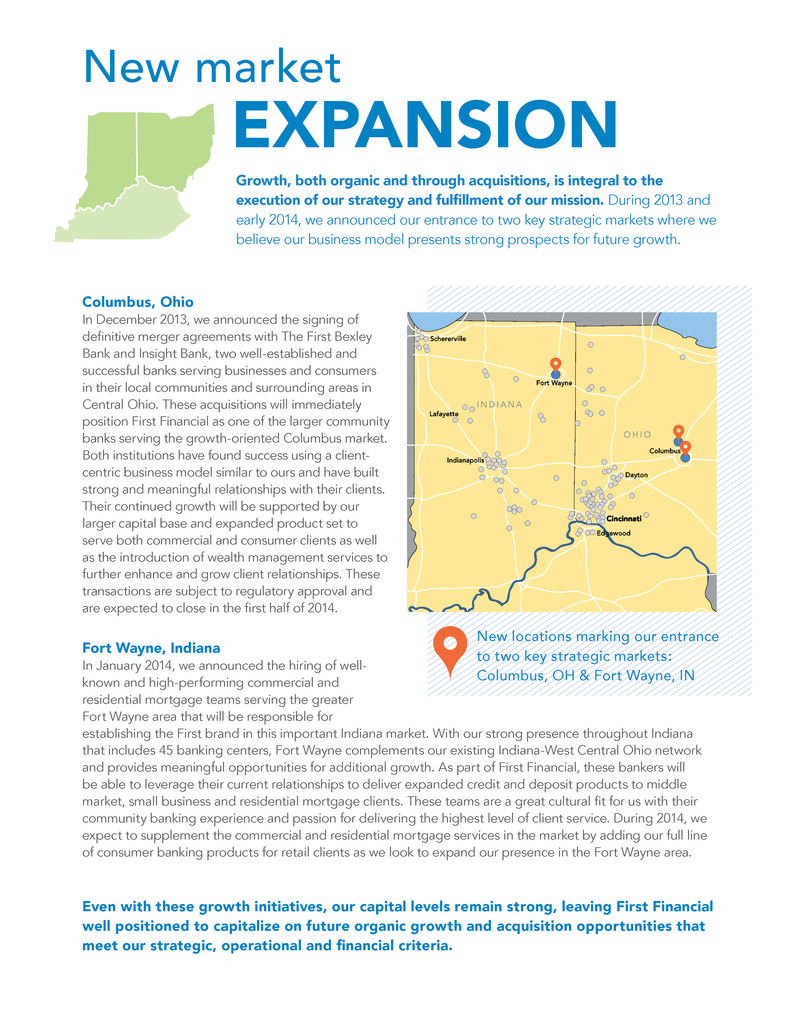

New market EXPANSIoN Growth, both organic and through acquisitions, is integral to the execution of our strategy and fulfillment of our mission. During 2013 and early 2014, we announced our entrance to two key strategic markets where we believe our business model presents strong prospects for future growth. New market EXPANSIoN Even with these growth initiatives, our capital levels remain strong, leaving First Financial well positioned to capitalize on future organic growth and acquisition opportunities that meet our strategic, operational and financial criteria. Columbus, Ohio In December 2013, we announced the signing of definitive merger agreements with The First Bexley Bank and Insight Bank, two well-established and successful banks serving businesses and consumers in their local communities and surrounding areas in Central Ohio. These acquisitions will immediately position First Financial as one of the larger community banks serving the growth-oriented Columbus market. Both institutions have found success using a client-centric business model similar to ours and have built strong and meaningful relationships with their clients. Their continued growth will be supported by our larger capital base and expanded product set to serve both commercial and consumer clients as well as the introduction of wealth management services to further enhance and grow client relationships. These transactions are subject to regulatory approval and are expected to close in the first half of 2014. Fort Wayne, Indiana In January 2014, we announced the hiring of well- known and high-performing commercial and residential mortgage teams serving the greater Fort Wayne area that will be responsible for establishing the First brand in this important Indiana market. With our strong presence throughout Indiana that includes 45 banking centers, Fort Wayne complements our existing Indiana-West Central Ohio network and provides meaningful opportunities for additional growth. As part of First Financial, these bankers will be able to leverage their current relationships to deliver expanded credit and deposit products to middle market, small business and residential mortgage clients. These teams are a great cultural fit for us with their community banking experience and passion for delivering the highest level of client service. During 2014, we expect to supplement the commercial and residential mortgage services in the market by adding our full line of consumer banking products for retail clients as we look to expand our presence in the Fort Wayne area. Traverse City Dayton Schererville Lafayette Indianapolis Edgewood Columbus Fort Wayne New locations marking our entrance to two key strategic markets: Columbus, OH & Fort Wayne, IN

4 First Financial Bancorp 2013 Annual Report

Introducing Focus. We remain client focused by putting our clients at the center of everything we do. True to our mission, we strive to put our clients at the center of everything we do. Our goal is to make a lasting impression in every interaction with every client. This lasting impression creates a legacy for our brand and differentiates us from our competitors. In 2013, we introduced Focus within the company. Focus defines our client-centric business model and provides all associates with a stronger framework for living our mission every day. Introducing Building a great team: This means hiring the right people who are committed to uniting associates across all markets, departments and lines of business to do what’s best for our client. Providing needs-based solutions: A client-centric sales approach that fully uncovers the basic financial needs of each client today and also uncovers their future aspirations. Doing the right thing: We exist because of our clients, so we should make decisions with all the facts, be fair and client-centered. Never losing a client: Each associate plays a role in creating a superior service experience for clients and being an ambassador for the company. Knowing our clients: This means developing a deep relationship with all of our clients so we can offer proactive solutions to help them be more successful. Making a difference: From our processes, programs, ongoing communications and continuing interactions with clients, associates are empowered to make a difference for our clients every day. 1 2 3 4 5 6

First Financial Bancorp 2013 Annual Report 5

Positioned for GRowTH 2013 was a year of significant change, transition and improvement for First Financial. Remaining relevant to our clients in a highly competitive industry is critical as we constantly strive to improve the client experience of banking with First Financial across all lines of business. To successfully fulfill our mission, we implemented organizational changes that better integrate our line of business strategies and the market-based approach in which our products and services are delivered by local decision makers responsible for the client experience in their markets. We made several key steps to position First Financial for continued growth. This includes our expansion into the Columbus, Ohio and Fort Wayne, Indiana markets, adding high-quality sales personnel across all lines of business and further investment in new products, services and technologies. We are well positioned to take advantage of our competitive strengths and remain focused on organic growth across all business lines and markets. Our strong capital base also provides the ability to capitalize on additional strategic opportunities to supplement this growth. Effective execution across all aspects of our business will be the key to our success. During 2013, we delivered on the execution of our efficiency plan which identified more than $17 million in annual cost savings and formed the basis of a culture dedicated to process improvement and more efficient client service. Through the unwavering commitment of our associates, we exceeded our original goal and realized 100 percent of the annual target in the year’s financial results with future annual savings expected to exceed $17 million. The culture of process improvement took hold as we identified an additional $5 million of savings beyond the original initiatives. As we enter 2014, we have made significant strides toward right-sizing our operating structure with a healthy balance between operating in a responsible, cost-effective manner while having the capacity to effectively handle future growth without compromising safety and soundness. As we reflect on our 150 year history and look towards the future, we want to thank our shareholders, associates and clients for their ongoing commitment to First Financial. Our success would not be possible without you and we look forward to a prosperous 2014. Here. Now. Always Growing. Strategic Priorities for 2014 Sustain our commitment to the collaborative and team-oriented culture and business model we are building that is focused on growth and client service. Maintain our organic growth momentum as well as continue to evaluate franchise-enhancing acquisition opportunities. Continued discipline in our operating efficiency and dedication to continual process improvements. Remain vigilant in our enterprise risk management processes, especially in light of increased regulations and threats, such as cyber fraud. Capitalize on 2013 accomplishments to deliver positive operating leverage and earnings growth. Claude E. Davis, President and CEO

6 First Financial Bancorp 2013 Annual Report

Directors and Officers

|

| | | | |

| Board of Directors | | | | Senior Management |

| | | | | |

| Murph Knapke | | Corinne R. Finnerty | | Claude E. Davis |

| Chairman of the Board, | | Partner, | | President and |

| First Financial Bancorp; | | McConnell Finnerty PC | | Chief Executive Officer |

| Partner, | | | | |

| Knapke Law Office, | | Susan L. Knust | | Matthew B. Burgess |

| | | Managing Partner, | | Executive Vice President and |

| J. Wickliffe Ach | | K.P. Properties and | | Chief Internal Auditor |

| President and | | Omega Warehouse Services | | |

| Chief Executive Officer, | | | | Kevin T. Langford |

| Hixson, Inc. | | William J. Kramer | | President, Consumer Banking |

| | | Vice President of Operations, | | President, Western Markets |

| David S. Barker | | Valco Companies, Inc. | | |

| President and | | | | C. Douglas Lefferson |

| Chief Executive Officer, | | Richard E. Olszewski | | President, Commercial Banking |

| SIHO Insurance Services | | Owner/Operator | | and Wealth Management |

| | | 7 Eleven Food Stores | | President, Eastern Markets |

| Cynthia O. Booth | | | | |

| President and | | Maribeth S. Rahe | | Alisa E. Poe |

| Chief Executive Officer, | | President and | | Executive Vice President, |

| COBCO Enterprises | | Chief Executive Officer, | | Chief Talent Officer and |

| | | Fort Washington Investment | | Chief of Staff |

| Donald M. Cisle, Sr. | | Advisors, Inc. | | |

| Managing Member, | | | | Jill A. Stanton |

| The Cisle Co. LLC | | | | President, Mortgage Banking |

| | | | | |

| Mark A. Collar | | | | Anthony M. Stollings |

| Retired Executive, | | | | Executive Vice President, |

| Procter & Gamble Company | | | | Chief Financial Officer and |

| | | | | Chief Administrative Officer |

| Claude E. Davis | | | | |

| President and | | | | Holly M. Foster |

| Chief Executive Officer, | | | | Senior Vice President and |

| First Financial Bancorp; | | | | Chief Risk Officer |

| Chairman of the Board | | | | |

| and Chief Executive Officer, | | | | John M. Gavigan |

| First Financial Bank, N.A. | | | | First Vice President and |

| | | | | Corporate Controller |

| | | | | |

| | | | | |

| | | | | |

First Financial Bancorp 2013 Annual Report 7

|

| | | | | | | | | | | |

| FINANCIAL HIGHLIGHTS |

| | | | | | | |

| (Dollars in thousands, except per share data) | | 2013 | | 2012 | | % Change |

| Earnings | | | | | | |

| Net interest income | | $ | 228,320 |

| | $ | 253,341 |

| | (9.9 | )% |

| Net income | | 48,349 |

| | 67,303 |

| | (28.2 | )% |

| | | | | | | |

| Per Share | | | | | | |

| Net income per common share-basic | | $ | 0.84 |

| | $ | 1.16 |

| | (27.6 | )% |

| Net income per common share-diluted | | 0.83 |

| | 1.14 |

| | (27.2 | )% |

| Cash dividends declared per common share | | 0.94 |

| | 1.18 |

| | (20.3 | )% |

| Tangible book value per common share (end of year) | | 10.10 |

| | 10.47 |

| | (3.5 | )% |

| Market price (end of year) | | 17.43 |

| | 14.62 |

| | 19.2 | % |

| | | | | | | |

| Balance Sheet - End of Year | | | | | | |

| Total assets | | $ | 6,417,213 |

| | $ | 6,497,048 |

| | (1.2 | )% |

| Deposits | | 4,837,507 |

| | 4,955,840 |

| | (2.4 | )% |

| Loans, including covered loans | | 3,963,514 |

| | 3,927,180 |

| | 0.9 | % |

| Investment securities | | 1,798,300 |

| | 1,874,343 |

| | (4.1 | )% |

| Shareholders' equity | | 682,161 |

| | 710,425 |

| | (4.0 | )% |

| | | | | | | |

| Ratios | | | | | | |

| Return on average assets | | 0.77 | % | | 1.07 | % | | |

| Return on average shareholders' equity | | 6.89 | % | | 9.43 | % | | |

| Return on average tangible shareholders' equity | | 8.05 | % | | 11.01 | % | | |

| Net interest margin | | 3.97 | % | | 4.37 | % | | |

| Net interest margin (fully tax equivalent) | | 4.01 | % | | 4.39 | % | | |

8 First Financial Bancorp 2013 Annual Report

|

| |

| | 2013 Financial Information |

First Financial Bancorp 2013 Annual Report 9

Management’s Discussion And Analysis Of Financial Condition And Results Of Operations

This annual report contains forward-looking statements. See the Forward-Looking Statements section that follows for further information on the risks and uncertainties associated with forward-looking statements. The following discussion and analysis is presented to facilitate the understanding of the financial position and results of operations of First Financial Bancorp. (First Financial or the Company). It identifies trends and material changes that occurred during the reporting periods and should be read in conjunction with the Statistical Data, Consolidated Financial Statements and accompanying Notes.

EXECUTIVE SUMMARY

First Financial is a $6.4 billion bank holding company headquartered in Cincinnati, Ohio. As of December 31, 2013, First Financial, through its subsidiaries, operated primarily in Ohio, Indiana and Kentucky. These subsidiaries include a commercial bank, First Financial Bank, N.A. (First Financial Bank or the Bank) with 110 banking centers and 137 ATMs. First Financial provides banking and financial services products through its four lines of business: commercial, consumer, wealth management and mortgage. The commercial, consumer and mortgage business lines provide credit-based products, deposit accounts, retail brokerage, corporate cash management support and other services to commercial and consumer clients. First Financial Wealth Management provides wealth planning, portfolio management, trust and retirement plan services and had approximately $2.5 billion in assets under management as of December 31, 2013. Additionally, the Bank provides franchise lending products, primarily equipment, real estate and leasehold improvement financing, for select concepts and franchisees in the quick service and casual dining restaurant sector located throughout the United States.

First Financial acquired the banking operations of Peoples Community Bank (Peoples), and Irwin Union Bank and Trust Company and Irwin Union Bank, F.S.B. (collectively, Irwin), through Federal Deposit Insurance Corporation (FDIC)-assisted transactions in 2009. In connection with these FDIC-assisted transactions, First Financial entered into loss sharing agreements with the FDIC. Under the terms of these agreements the FDIC reimburses First Financial for a percentage of losses with respect to certain loans (covered loans) and other real estate owned (covered OREO) (collectively, covered assets). These agreements provide for loss protection on single-family, residential loans for a period of ten years and First Financial is required to share any recoveries of previously charged-off amounts for the same time period, on the same pro-rata basis with the FDIC. All other loans are provided loss protection for a period of five years and recoveries of previously charged-off amounts must be shared with the FDIC for an additional three year period, on the same pro-rata basis. First Financial must follow specific servicing and resolution procedures, as outlined in the loss sharing agreements, in order to receive reimbursement from the FDIC for losses on covered assets.

The major components of First Financial’s operating results for the past five years are summarized in Table 1 – Financial Summary and discussed in greater detail on subsequent pages.

MARKET STRATEGY AND BUSINESS COMBINATIONS

First Financial serves a combination of metropolitan and non-metropolitan markets in Ohio, Indiana and Kentucky through its full-service banking centers, while providing franchise lending services to borrowers throughout the United States. First Financial’s market selection process includes a number of factors, but markets are primarily chosen for their potential for growth and long-term profitability. First Financial’s goal is to develop a competitive advantage utilizing a local market focus, building long-term relationships with clients to help them reach greater levels of success in their financial life and providing a superior level of service. First Financial intends to continue focusing plans for future growth and capital investments within its current metropolitan markets and evaluating other growth opportunities in metropolitan markets located within, or in close proximity to, the Company's current geographic footprint. Smaller markets have historically provided stable, low-cost funding sources to First Financial and remain an important part of its funding base. First Financial believes its historical strength in these markets should enable it to retain or improve its market share.

On December 17, 2013, First Financial and First Financial Bank entered into a definitive merger agreement with The First Bexley Bank (First Bexley or Bexley). Founded in 2006 and conducting operations out of one full service branch location in Bexley, Ohio, First Bexley serves commercial and consumer clients throughout central Ohio. Under the merger agreement, First Financial will acquire Bexley in a cash and stock transaction in which Bexley will merge with and into First Financial Bank. Shareholders of First Bexley will receive $30.50 for each share of First Bexley common stock consisting of $24.40 in the Company’s common stock and $6.10 in cash, subject to certain adjustment depending upon changes in the price of the Company’s common stock. Including outstanding options on First Bexley common stock, the transaction is valued at approximately $44.5 million. As of September 30, 2013, First Bexley had total assets of $295.4 million, total deposits of $271.1 million, and total common shareholders’ equity of $22.7 million.

10 First Financial Bancorp 2013 Annual Report

On December 19, 2013, First Financial and First Financial Bank signed a definitive merger agreement with Insight Bank (Insight). Founded in 2006 and conducting operations out of one full service location in Worthington, Ohio, and a mortgage origination office in Newark, Ohio, Insight provides commercial and consumer banking services to clients throughout central Ohio. Under the merger agreement, First Financial will acquire Insight in a cash and stock transaction in which Insight will merge with and into First Financial Bank. Shareholders of Insight will receive $20.50 for each share of Insight common stock consisting of $16.40 in the Company’s common stock and $4.10 in cash, subject to certain adjustment depending upon changes in the price of the Company’s common stock. Including outstanding options on Insight common stock, the transaction is valued at approximately $36.6 million. As of September 30, 2013, Insight had total assets of $200.2 million, total deposits of $165.4 million, and total common shareholders’ equity of $20.1 million.

The Bexley and Insight transactions are subject to approval by both regulators and their respective shareholders, and are expected to close in the first half of 2014.

While the Bexley and Insight acquisitions will provide First Financial entrance into the Columbus, Ohio metropolitan market, First Financial also entered the Fort Wayne, Indiana market through the hiring of experienced and well-established commercial and residential mortgage lending teams in January of 2014. On a combined basis, these actions provide First Financial entrance into two new metropolitan markets that it believes have attractive demographics and future growth prospects.

Efficiency. During the third quarter 2012, First Financial completed a comprehensive efficiency study across all business lines and support functions in an effort to mitigate earnings growth challenges related to the current interest rate and economic environment as well as declining balances in the Company's high-yielding covered loan portfolio. As a result, the Company identified approximately $17.1 million of annualized cost savings impacting several expense categories. Realization of the identified cost savings began late in 2012, however the Company did not recognize net savings during 2012 as costs associated with implementing the efficiency plan offset initial savings. Based on 2013 operating performance, the Company surpassed its original realization goal and achieved 100% of its annual target of $17.1 million during the year.

All initiatives related to the original plan are fully implemented and annualized cost savings are expected to exceed the original target. Ultimately, the achievement of these cost savings will be contingent upon management's continued ability to maintain efficiency plans while managing external factors, such as regulatory changes and a dynamic business environment, without impacting client service levels throughout the Company.

As part of the on-going evaluation of its banking center network and the efficiency plans discussed above, First Financial consolidated 17 banking centers located in Ohio and Indiana in 2013. Additionally, during 2012, the Company consolidated 11 banking centers located in Ohio and Indiana and closed 5 other banking centers in areas of Indiana where the Company had a limited presence. Customer relationships related to the consolidated banking centers were transferred to the nearest First Financial location where those customers continue to receive the same high level of service.

These banking center actions allow First Financial to focus additional resources in core markets, such as Cincinnati, Dayton and Columbus, Ohio and Indianapolis, Fort Wayne, Southern and Northwest Indiana, that the Company believes provide a higher level of potential overall growth and improve the efficiency of its operations.

First Financial Bancorp 2013 Annual Report 11

Management’s Discussion And Analysis Of Financial Condition And Results Of Operations

|

| | | | | | | | | | | | | | | | | | | |

| Table 1 • Financial Summary | | | | | | | | | |

| | December 31, |

| (Dollars in thousands, except per share data) | 2013 | | 2012 | | 2011 | | 2010 | | 2009 |

| Summary of operations | | | | | | | | | |

| Interest income | $ | 245,208 |

| | $ | 280,930 |

| | $ | 308,817 |

| | $ | 343,502 |

| | $ | 233,228 |

|

Tax equivalent adjustment (1) | 2,142 |

| | 1,055 |

| | 979 |

| | 866 |

| | 1,265 |

|

Interest income tax – equivalent (1) | 247,350 |

| | 281,985 |

| | 309,796 |

| | 344,368 |

| | 234,493 |

|

| Interest expense | 16,888 |

| | 27,589 |

| | 44,921 |

| | 67,992 |

| | 57,245 |

|

Net interest income tax – equivalent (1) | $ | 230,462 |

| | $ | 254,396 |

| | $ | 264,875 |

| | $ | 276,376 |

| | $ | 177,248 |

|

| Interest income | $ | 245,208 |

| | $ | 280,930 |

| | $ | 308,817 |

| | $ | 343,502 |

| | $ | 233,228 |

|

| Interest expense | 16,888 |

| | 27,589 |

| | 44,921 |

| | 67,992 |

| | 57,245 |

|

| Net interest income | 228,320 |

| | 253,341 |

| | 263,896 |

| | 275,510 |

| | 175,983 |

|

| Provision for loan and lease losses – uncovered | 8,714 |

| | 19,117 |

| | 19,210 |

| | 33,564 |

| | 56,084 |

|

| Provision for loan and lease losses – covered | 195 |

| | 30,903 |

| | 64,081 |

| | 63,144 |

| | 0 |

|

| Noninterest income | 73,647 |

| | 122,421 |

| | 142,531 |

| | 146,831 |

| | 404,715 |

|

| Noninterest expenses | 225,475 |

| | 221,997 |

| | 218,097 |

| | 233,680 |

| | 170,638 |

|

| Income before income taxes | 67,583 |

| | 103,745 |

| | 105,039 |

| | 91,953 |

| | 353,976 |

|

| Income tax expense | 19,234 |

| | 36,442 |

| | 38,300 |

| | 32,702 |

| | 132,639 |

|

| Net income | 48,349 |

| | 67,303 |

| | 66,739 |

| | 59,251 |

| | 221,337 |

|

| Dividends on preferred stock | 0 |

| | 0 |

| | 0 |

| | 1,865 |

| | 3,578 |

|

| Income available to common shareholders | $ | 48,349 |

| | $ | 67,303 |

| | $ | 66,739 |

| | $ | 57,386 |

| | $ | 217,759 |

|

| | | | | | | | | | |

| Per share data | | | | | | | | | |

| Earnings per common share | | | | | | | | | |

| Basic | $ | 0.84 |

| | $ | 1.16 |

| | $ | 1.16 |

| | $ | 1.01 |

| | $ | 4.84 |

|

| Diluted | $ | 0.83 |

| | $ | 1.14 |

| | $ | 1.14 |

| | $ | 0.99 |

| | $ | 4.78 |

|

| Cash dividends declared per common share | $ | 0.94 |

| | $ | 1.18 |

| | $ | 0.78 |

| | $ | 0.40 |

| | $ | 0.40 |

|

| Average common shares outstanding–basic (in thousands) | 57,270 |

| | 57,877 |

| | 57,692 |

| | 56,969 |

| | 45,029 |

|

| Average common shares outstanding–diluted (in thousands) | 58,073 |

| | 58,869 |

| | 58,693 |

| | 57,993 |

| | 45,557 |

|

| | | | | | | | | | |

| Selected year-end balances | | | | | | | | | |

| Total assets | $ | 6,417,213 |

| | $ | 6,497,048 |

| | $ | 6,671,511 |

| | $ | 6,250,225 |

| | $ | 6,657,593 |

|

| Earning assets | 5,840,849 |

| | 5,961,727 |

| | 6,110,934 |

| | 5,741,683 |

| | 5,964,853 |

|

Investment securities (2) | 1,798,300 |

| | 1,874,343 |

| | 1,516,002 |

| | 1,015,205 |

| | 579,147 |

|

| Loans, excluding covered loans | 3,505,641 |

| | 3,179,064 |

| | 2,968,447 |

| | 2,816,093 |

| | 2,895,129 |

|

| Covered loans | 457,873 |

| | 748,116 |

| | 1,053,244 |

| | 1,481,493 |

| | 1,934,740 |

|

| Total loans | 3,963,514 |

| | 3,927,180 |

| | 4,021,691 |

| | 4,297,586 |

| | 4,829,869 |

|

| FDIC indemnification asset | 45,091 |

| | 119,607 |

| | 173,009 |

| | 222,648 |

| | 287,407 |

|

| Interest-bearing demand deposits | 1,125,723 |

| | 1,160,815 |

| | 1,317,339 |

| | 1,111,877 |

| | 1,060,383 |

|

| Savings deposits | 1,612,005 |

| | 1,623,614 |

| | 1,724,659 |

| | 1,534,045 |

| | 1,231,081 |

|

| Time deposits | 952,327 |

| | 1,068,637 |

| | 1,654,662 |

| | 1,794,843 |

| | 2,229,500 |

|

| Noninterest-bearing demand deposits | 1,147,452 |

| | 1,102,774 |

| | 946,180 |

| | 705,484 |

| | 829,676 |

|

| Total deposits | 4,837,507 |

| | 4,955,840 |

| | 5,642,840 |

| | 5,146,249 |

| | 5,350,640 |

|

| Short-term borrowings | 748,749 |

| | 624,570 |

| | 99,431 |

| | 59,842 |

| | 37,430 |

|

| Long-term debt | 60,780 |

| | 75,202 |

| | 76,544 |

| | 128,880 |

| | 404,716 |

|

| Other long-term debt | 0 |

| | 0 |

| | 0 |

| | 20,620 |

| | 20,620 |

|

| Shareholders’ equity | 682,161 |

| | 710,425 |

| | 712,221 |

| | 697,394 |

| | 649,958 |

|

| | | | | | | | | | |

| Select Financial Ratios | | | | | | | | | |

Average loans to average deposits (3) | 82.12 | % | | 75.66 | % | | 78.53 | % | | 86.43 | % | | 92.56 | % |

| Net charge-offs to average loans, excluding covered loans | 0.38 | % | | 0.79 | % | | 0.84 | % | | 1.27 | % | | 1.16 | % |

| Average shareholders’ equity to average total assets | 11.17 | % | | 11.30 | % | | 11.33 | % | | 10.53 | % | | 9.85 | % |

| Average common shareholders’ equity to average total assets | 11.17 | % | | 11.30 | % | | 11.33 | % | | 10.35 | % | | 8.20 | % |

| Return on average assets | 0.77 | % | | 1.07 | % | | 1.06 | % | | 0.91 | % | | 4.67 | % |

| Return on average common equity | 6.89 | % | | 9.43 | % | | 9.37 | % | | 8.55 | % | | 56.07 | % |

| Return on average equity | 6.89 | % | | 9.43 | % | | 9.37 | % | | 8.68 | % | | 47.44 | % |

| Net interest margin | 3.97 | % | | 4.37 | % | | 4.55 | % | | 4.66 | % | | 4.05 | % |

Net interest margin (tax equivalent basis) (1) | 4.01 | % | | 4.39 | % | | 4.57 | % | | 4.68 | % | | 4.08 | % |

| Dividend payout | 111.90 | % | | 101.72 | % | | 67.24 | % | | 39.60 | % | | 8.26 | % |

(1) Tax equivalent basis was calculated using a 35.00% tax rate in all years presented.

(2) Includes investment securities held-to-maturity, investment securities available-for-sale, investment securities trading, and other investments.

(3) Includes covered loans and loans held for sale.

12 First Financial Bancorp 2013 Annual Report

OVERVIEW OF OPERATIONS

The primary source of First Financial’s revenue is net interest income, or the excess of interest received from earning assets over interest paid on interest-bearing liabilities, plus fees for financial services provided to clients. First Financial’s business results are influenced by overall economic factors and conditions, including market interest rates, competition within the marketplace, business spending, consumer confidence and regulatory changes.

Net interest income in 2013 declined 9.9% from 2012, compared to a 4.0% decrease in 2012 compared to 2011. The decline in 2013 was attributable to a 32.8% decrease in average covered loan balances and lower yields on the FDIC indemnification asset and uncovered loans, partially offset by a decline in the cost of interest bearing liabilities, during the year. The net interest margin was 3.97% for 2013 compared with 4.37% in 2012 and 4.55% in 2011.

Noninterest income declined $48.8 million during the year, from $122.4 million in 2012 to $73.6 million in 2013. The decline in noninterest income was primarily due to lower FDIC loss sharing income and income from the accelerated discount on covered loans that prepay during the year. FDIC loss sharing income represents reimbursements due from the FDIC under loss sharing agreements for losses and resolution expenses on covered assets.

Noninterest expense increased $3.5 million during the year, from $222.0 million in 2012 to $225.5 million in 2013. The increase was primarily due to a valuation adjustment to the FDIC indemnification asset and pension settlement charges incurred in 2013, partially offset by lower salaries and benefits, loss sharing expenses and losses on noncovered and covered OREO during the year.

Net income for the year ended December 31, 2013 was $48.3 million, resulting in basic earnings per share of $0.84, and $0.83 of earnings per diluted common share. This represented a 28.2% decrease in net income from $67.3 million in 2012. Basic and diluted earnings per share for the year ended December 31, 2012 were $1.16 and $1.14, respectively. First Financial’s return on average shareholders’ equity for 2013 was 6.89%, which compares to 9.43% for 2012. First Financial’s return on average assets for 2013 was 0.77%, which compares to a return on average assets of 1.07% for 2012.

Total loans increased $36.3 million from $3.9 billion at December 31, 2012 to $4.0 billion at December 31, 2013. Total uncovered loans increased $326.6 million, from $3.2 billion at December 31, 2012 to $3.5 billion at December 31, 2013 while total covered loans decreased $290.2 million, from $748.1 million at December 31, 2012 to $457.9 million at December 31, 2013.

First Financial experienced a $118.3 million or 2.4% decline in total deposits during 2013, from $5.0 billion at December 31, 2012 to $4.8 billion as of December 31, 2013, as a result of a continued focus on core deposit relationships and lowering the Company's funding costs. Noninterest bearing deposits increased by $44.7 million, while interest-bearing checking deposits decreased by $35.1 million, savings deposits decreased by $11.6 million and time deposits declined by $116.3 million during the period. The decline in deposits during 2013 was offset by a $124.2 million or 19.9% increase in lower cost, short-term borrowings from $624.6 million as of December 31, 2012 to $748.7 million as of December 31, 2013. The Company's total cost of funds declined to 0.31% in 2013 from 0.50% in 2012.

The uncovered allowance for loan and lease losses at December 31, 2013, was $43.8 million, or 1.25%, of uncovered loans compared to $47.8 million, or 1.50% of uncovered loans at December 31, 2012. The Company's credit quality performance improved moderately in 2012 and more notably in 2013, reflecting the continued recovery in the U.S. economy from the period of sustained weakness and falling real estate values experienced from 2007 to 2010. First Financial's lower levels of nonaccrual loans and classified assets in 2013 reflect improving economic conditions, including lower unemployment rates and higher levels of business and consumer spending.

For a more detailed discussion of the above topics, please refer to the sections that follow.

First Financial Bancorp 2013 Annual Report 13

Management’s Discussion And Analysis Of Financial Condition And Results Of Operations

NET INCOME

2013 vs. 2012. First Financial’s net income decreased $19.0 million or 28.2% to $48.3 million in 2013, compared to net income of $67.3 million in 2012. The decrease was primarily related to declines in net interest income of $25.0 million, or 9.9%, and noninterest income of $48.8 million or 39.8%, partially offset by a $30.7 million, or 99.4% reduction in provision for loan and lease losses on covered loans, a $10.4 million, or 54.4% reduction in provision for loan and lease losses on uncovered loans and a $17.2 million, or 47.2% decrease in income tax expense. For more detail, refer to the Net interest income, Noninterest income and Noninterest expense sections that follow.

2012 vs. 2011. First Financial’s net income increased $0.6 million or 0.8% to $67.3 million in 2012, compared to net income of $66.7 million in 2011. The increase was primarily related to a $33.2 million or 51.8% reduction in provision for loan and lease losses on covered loans, offset by a related $20.1 million or 14.1% decline in noninterest income as well as a $10.6 million or 4.0% decline in net interest income in 2012. The decline in net interest income during 2012 was primarily driven by a 27.7% decrease in average covered loan balances. Noninterest expenses increased $3.9 million or 1.8% in 2012.

NET INTEREST INCOME

First Financial’s net interest income for the years 2009 through 2013 is shown in Table 1 – Financial Summary. Net interest income, First Financial’s principal source of income, is the excess of interest received from earning assets over interest paid on interest-bearing liabilities, plus fees for financial services provided to clients. The amount of net interest income is determined by the volume and mix of earning assets, the rates earned on such earning assets and the volume, mix and rates paid for the deposits and borrowed money that support the earning assets. Table 2 – Volume/Rate Analysis describes the extent to which changes in interest rates and changes in the volume of earning assets and interest-bearing liabilities have affected First Financial’s net interest income on a tax equivalent basis during the years presented. Nonaccrual loans and loans held for sale, were included in the daily average loan balances used to determine the yields in Table 2 – Volume/Rate Analysis. Table 2 – Volume/Rate Analysis should be read in conjunction with the Statistical Information table.

Interest income on a tax equivalent basis is presented in Table 1 – Financial Summary. The tax equivalent adjustment recognizes the income tax savings when comparing taxable and tax-exempt assets and assumes a 35.0% tax rate for all years presented. First Financial's tax equivalent net interest margin was 4.01%, 4.39% and 4.57% for 2013, 2012 and 2011, respectively.

Loan fees included in the interest income computation for 2013, 2012 and 2011 were $6.7 million, $9.4 million and $5.6 million, respectively. The decrease in loan fees in 2013 was primarily due to lower prepayment fee income as a result of reduced levels of payoffs and loan refinancings. Loan fee income in 2012 included a $2.2 million fee related to the early payoff of a single commercial relationship.

2013 vs. 2012. Net interest income decreased $25.0 million or 9.9%, from $253.3 million in 2012 to $228.3 million in 2013, primarily due to lower yields on earning assets partially offset by a decline in the cost of interest-bearing liabilities during 2013. While average earning assets were relatively unchanged, the yield on earning assets declined 58 basis points from 4.84% in 2012 to 4.26% in 2013.

Interest income was $245.2 million in 2013, a $35.7 million or 12.7% decrease from 2012. The decline in interest income and the lower yield on earning assets in 2013 were primarily the result of a $290.2 million or 38.8% decrease in covered loans, which generally accrete a yield above market interest rates, as well as declines in the yields on uncovered loans and investment securities in 2013.

Interest expense was $16.9 million in 2013, a $10.7 million or 38.8% decrease from 2012. The total cost of funds declined 24 basis points to 0.38% in 2013 from 0.62% in 2012, primarily due to a 24 basis point decrease in the cost of interest-bearing deposits to 0.35% in 2013 from 0.59% in 2012. The lower cost of funds in 2013 was primarily a result of the lower interest rate environment as well as deposit pricing and rationalization strategies executed by the Company in recent years.

2012 vs. 2011. Net interest income decreased $10.6 million, or 4.0%, primarily due to lower yields on earning assets during 2012. Average earning assets declined $105.3 million, or 1.8%, during 2011. While average earning assets were relatively unchanged, the yield on earning assets declined 48 basis points from 5.32% in 2012 to 4.84% in 2012.

Interest income was $280.9 million in 2012, a $27.9 million or 9.0% decrease from 2011. The decline in interest income and the lower yield on earning assets in 2012 are primarily the result of a $305.1 million or 29.0% decrease in covered loans, which generally accrete a yield above market interest rates. The decline in interest income on covered loans was partially offset by

14 First Financial Bancorp 2013 Annual Report

higher interest income on investment securities in 2012 related to a $358.3 million or 23.6% increase in investment securities during the period.

Interest expense was $27.6 million in 2012, a $17.3 million or 38.6% decrease from 2011. The total cost of funds declined 34 basis points to 0.62% in 2012 from 0.96% in 2011, primarily due to a 32 basis point decrease in the cost of interest-bearing deposits to 0.59% in 2012 from 0.91% in 2011. The lower cost of funds in 2012 was primarily a result of the lower interest rate environment as well as deposit pricing and rationalization strategies the Company implemented in 2011 and continued throughout 2012.

|

| | | | | | | | | | | | | | | | | | | | | | | | |

Table 2 • Volume/Rate Analysis - Tax Equivalent Basis (1) | | | | |

| | | 2013 change from 2012 due to | | 2012 change from 2011 due to |

| (Dollars in thousands) | | Volume | Rate | | Total | | Volume | Rate | | Total |

| Interest income | | | | | | | | | | | | |

Loans (2) | | $ | 13,894 |

| | $ | (9,862 | ) | | $ | 4,032 |

| | $ | 8,652 |

| | $ | (9,715 | ) | | $ | (1,063 | ) |

| Covered loans and indemnification asset | | (30,427 | ) | | (7,200 | ) | | (37,627 | ) | | (37,357 | ) | | 2,251 |

| | (35,106 | ) |

Investment securities (3) | | | | | | | | | | | | |

| Taxable | | (1,270 | ) | | (2,247 | ) | | (3,517 | ) | | 11,873 |

| | (2,448 | ) | | 9,425 |

|

| Tax-exempt | | 2,731 |

| | (170 | ) | | 2,561 |

| | 470 |

| | (518 | ) | | (48 | ) |

Total investment securities interest (3) | | 1,461 |

| | (2,417 | ) | | (956 | ) | | 12,343 |

| | (2,966 | ) | | 9,377 |

|

| Interest-bearing deposits with other banks | | (126 | ) | | 42 |

| | (84 | ) | | (983 | ) | | (36 | ) | | (1,019 | ) |

| Total | | (15,198 | ) | | (19,437 | ) | | (34,635 | ) | | (17,345 | ) | | (10,466 | ) | | (27,811 | ) |

| | | | | | | | | | | | | |

| Interest expense | | | | | | | | | | | | |

| Interest-bearing demand deposits | | (92 | ) | | 42 |

| | (50 | ) | | 7 |

| | (1,455 | ) | | (1,448 | ) |

| Savings deposits | | (5 | ) | | (191 | ) | | (196 | ) | | 7 |

| | (3,807 | ) | | (3,800 | ) |

| Time deposits | | (3,602 | ) | | (7,530 | ) | | (11,132 | ) | | (4,722 | ) | | (6,186 | ) | | (10,908 | ) |

| Short-term borrowings | | 780 |

| | 135 |

| | 915 |

| | 135 |

| | (36 | ) | | 99 |

|

| Long-term debt | | (205 | ) | | (33 | ) | | (238 | ) | | (811 | ) | | (73 | ) | | (884 | ) |

| Other long-term debt | | N/M |

| | N/M |

| | N/M |

| | (391 | ) | | 0 |

| | (391 | ) |

| Total | | (3,124 | ) | | (7,577 | ) | | (10,701 | ) | | (5,775 | ) | | (11,557 | ) | | (17,332 | ) |

| Net interest income | | $ | (12,074 | ) | | $ | (11,860 | ) | | $ | (23,934 | ) | | $ | (11,570 | ) | | $ | 1,091 |

| | $ | (10,479 | ) |

(1) Tax equivalent basis was calculated using a 35.00% tax rate.

(2) Includes nonaccrual loans and loans held-for-sale.

(3) Includes investment securities held-to-maturity, investment securities available-for-sale and other investments.

N/M = Not meaningful.

NONINTEREST INCOME AND NONINTEREST EXPENSES

Noninterest income and noninterest expenses for 2013, 2012 and 2011 are shown in Table 3 – Noninterest Income and Noninterest Expenses.

NONINTEREST INCOME

2013 vs. 2012. Noninterest income decreased $48.8 million or 39.8% from $122.4 million in 2012 to $73.6 million in 2013 primarily related to lower FDIC loss sharing income, income from the accelerated discount on covered loans that prepay, gains on sales of securities and mortgages and other income. FDIC loss sharing income declined $31.6 million or 89.5% from 2012 to 2013 as a result of improvement in future expected cash flows on covered loans and declining losses on covered assets during the year. FDIC loss sharing income represents the proportionate share of credit losses on covered assets that First Financial expects to receive from the FDIC. Income from the accelerated discount on covered loans decreased $6.5 million or 47.6%, while other income declined $7.9 million or 39.7%. Accelerated discounts on covered loans that prepay result from the accelerated recognition of a component of the covered loan discount that would have been recognized over the expected life of the loan had it not prepaid. Income from the sale of mortgages declined $1.4 million, or 31.1% due to lower mortgage demand as a result of rising interest rates during 2013. The decrease in other noninterest income was primarily related to a $5.0 million legal settlement received in 2012 as well as lower income from bank owned life insurance and client derivative fees in 2013.

First Financial Bancorp 2013 Annual Report 15

Management’s Discussion And Analysis Of Financial Condition And Results Of Operations

2012 vs. 2011. Noninterest income decreased $20.1 million, or 14.1%, from $142.5 million in 2011 to $122.4 million in 2012 primarily related to lower FDIC loss sharing income and income from the accelerated discount on covered loans that prepay. FDIC loss sharing income declined $25.5 million or 41.9% from 2011 to 2012. Net of the FDIC loss sharing income described above, noninterest income increased $5.4 million, or 6.7%, in 2012 as compared with 2011, primarily due to higher service charges on deposits, bankcard income and other noninterest income partially offset by lower income from the accelerated discount on covered loans that prepay. The increases in service charges on deposits and bankcard income during 2012 were primarily a result of the Company's banking center acquisitions late in 2011. The increase in other noninterest income was primarily related to a $5.0 million legal settlement received in the second quarter as well as increased rental income on OREO properties, both covered and uncovered, as well as the credit valuation adjustment applied to the derivative portfolio.

|

| | | | | | | | | | | | | | | | | |

| Table 3 • Noninterest Income and Noninterest Expense |

| | 2013 | | 2012 | | 2011 |

| | | % Change | | | % Change | | | % Change |

| | | Increase | | | Increase | | | Increase |

| (Dollars in thousands) | Total | (Decrease) | | Total | (Decrease) | | Total | (Decrease) |

| Noninterest income | | | | | | | | |

| Service charges on deposit accounts | $ | 20,595 |

| (2.9 | )% | | $ | 21,215 |

| 10.5 | % | | $ | 19,206 |

| (13.4 | )% |

| Trust and wealth management fees | 14,319 |

| 2.6 | % | | 13,951 |

| (2.7 | )% | | 14,340 |

| 3.4 | % |

| Bankcard income | 10,914 |

| 8.8 | % | | 10,028 |

| 7.9 | % | | 9,291 |

| 9.1 | % |

| Net gains from sales of loans | 3,150 |

| (31.1 | )% | | 4,570 |

| 7.3 | % | | 4,258 |

| (8.1 | )% |

| FDIC loss sharing income | 3,720 |

| (89.5 | )% | | 35,346 |

| (41.9 | )% | | 60,888 |

| 17.4 | % |

| Accelerated discount on covered loans | 7,153 |

| (47.6 | )% | | 13,662 |

| (33.4 | )% | | 20,521 |

| (29.4 | )% |

| Other | 12,072 |

| (39.7 | )% | | 20,021 |

| 74.3 | % | | 11,486 |

| (31.4 | )% |

| Subtotal | 71,923 |

| (39.5 | )% | | 118,793 |

| (15.1 | )% | | 139,990 |

| (4.7 | )% |

| Gains on sales of investment securities | 1,724 |

| (52.5 | )% | | 3,628 |

| 42.8 | % | | 2,541 |

| N/M |

|

| Total | $ | 73,647 |

| (39.8 | )% | | $ | 122,421 |

| (14.1 | )% | | $ | 142,531 |

| (2.9 | )% |

| | | | | | | | | |

| Noninterest expenses | | | | | | | | |

| Salaries and employee benefits | $ | 101,402 |

| (10.4 | )% | | $ | 113,154 |

| 5.8 | % | | $ | 106,914 |

| (8.9 | )% |

| Pension settlement charges | 6,174 |

| N/M |

| | 0 |

| N/M |

| | 0 |

| N/M |

|

| Net occupancy | 21,207 |

| 2.5 | % | | 20,682 |

| (3.4 | )% | | 21,410 |

| (5.1 | )% |

| Furniture and equipment | 8,970 |

| (2.4 | )% | | 9,190 |

| (7.6 | )% | | 9,945 |

| (3.4 | )% |

| Data processing | 10,229 |

| 15.8 | % | | 8,837 |

| 54.6 | % | | 5,716 |

| 10.9 | % |

| Marketing | 4,270 |

| (23.1 | )% | | 5,550 |

| (4.2 | )% | | 5,794 |

| 8.2 | % |

| Communication | 3,207 |

| (5.9 | )% | | 3,409 |

| 6.4 | % | | 3,203 |

| (18.0 | )% |

| Professional services | 6,876 |

| (5.4 | )% | | 7,269 |

| (24.6 | )% | | 9,636 |

| 5.1 | % |

| State intangible tax | 3,929 |

| 0.8 | % | | 3,899 |

| 8.8 | % | | 3,583 |

| (26.0 | )% |

| FDIC assessments | 4,501 |

| (3.9 | )% | | 4,682 |

| (17.5 | )% | | 5,676 |

| (31.7 | )% |

| Loss-other real estate owned | 1,250 |

| (61.5 | )% | | 3,250 |

| (18.2 | )% | | 3,971 |

| 241.4 | % |

| Loss-covered other real estate owned | (1,219 | ) | (149.8 | )% | | 2,446 |

| (73.5 | )% | | 9,224 |

| 907.0 | % |

| Loss sharing expense | 7,083 |

| (34.0 | )% | | 10,725 |

| 197.9 | % | | 3,600 |

| 485.4 | % |

| FDIC indemnification impairment | 22,417 |

| N/M |

| | 0 |

| N/M |

| | 0 |

| N/M |

|

| Other | 25,179 |

| (12.9 | )% | | 28,904 |

| (1.8 | )% | | 29,425 |

| (18.3 | )% |

| Total | $ | 225,475 |

| 1.6 | % | | $ | 221,997 |

| 1.8 | % | | $ | 218,097 |

| (6.7 | )% |

N/M = Not meaningful

NONINTEREST EXPENSES

16 First Financial Bancorp 2013 Annual Report

2013 vs. 2012. Noninterest expenses increased $3.5 million or 1.6% in 2013 compared to 2012, primarily due to a $22.4 million FDIC indemnification valuation adjustment and $6.2 million of pension settlement charges incurred during 2013 as well as a $1.4 million, or 15.8% increase in data processing expenses. These increases were partially offset by an $11.8 million, or 10.4% decrease in salaries and employee benefits, a $3.6 million, or 34.0% decline in loss sharing expenses, a $2.0 million, or 61.5% decline in losses on OREO, a $3.7 million, or 149.8% decrease in losses on covered OREO and a $3.7 million, or 12.9% decline in other noninterest expense during 2013. Excluding the FDIC indemnification valuation adjustment and pension settlement charges, noninterest expenses declined $25.1 million or 11.3% during 2013 primarily as a result of the Company's ongoing efficiency efforts.

The FDIC indemnification valuation adjustment was primarily a result of improvement in future expected cash flows on covered loans, a meaningful decline in loss claims filed with the FDIC, higher reimbursements to the FDIC related to positive asset resolutions in recent periods and the significantly shorter remaining life of the indemnification asset in comparison to the weighted average life of the related covered loans.

The accounting and valuation for the FDIC indemnification asset is closely related to the accounting and valuation for covered loans. Improvement in expected cash flows related to covered loans is driven primarily by their actual or estimated credit performance and is generally reflected in changes in the yield on the loans. There is an opposite effect on the FDIC indemnification asset and those changes in estimated credit performance are reflected by a change in its yield as well. The Company continues to amortize the FDIC indemnification asset over the remaining life of the loss sharing agreements, a significantly shorter period than the remaining life of the covered loans as required by the related accounting guidance, causing a meaningful increase in the negative yield of the FDIC indemnification asset in the fourth quarter of 2013.

Also contributing to the FDIC indemnification valuation adjustment was improvement in the expected credit performance of the commercial covered loan portfolio compared to earlier estimates as criticized and classified covered loan balances have declined substantially and actual credit losses to date have been lower than First Financial originally estimated. In addition to this improved credit outlook, the Company experienced both an increase in recoveries related to covered loans, 80% of which are required to be shared back to the FDIC, as well as a significant decline in loss sharing claims filed with the FDIC late in 2013.

Given these factors and the significant negative yield that would have been required to amortize the commercial portion of the FDIC indemnification asset to zero at its expiration date, management concluded during the fourth quarter of 2013 that the FDIC indemnification asset was impaired. As a result, the Company recorded a $22.4 million pre-tax non-cash valuation adjustment to reduce the value of the FDIC indemnification asset as of December 31, 2013.

During 2013, First Financial recognized $6.2 million of pension settlement charges as a result of the level of lump sum distributions from the Company's pension plan. Consistent with FASB ASC Topic 715, Compensation - Retirement Benefits, pension settlement charges are an acceleration of previously deferred costs that would have been recognized in future periods and are triggered when lump sum distributions exceed an annual accounting threshold for the plan. First Financial incurred these pension settlement charges as a result of employee-related changes, including staff retirements and reductions due to recent efficiency initiatives, and the resulting lump sum distributions from the plan. The annual threshold for recognizing lump-sum distributions as pension settlement charges reset on January 1, 2014.

The decrease in salaries and benefits during 2013 was primarily attributable to staffing reductions associated with ongoing efficiency initiatives. The increase in data processing expense in 2013 was the full year effect of various software and system implementations in 2012, including new internet and mobile banking platforms. The decline in noninterest expenses related to OREO and covered OREO reflect continued stabilization and improvement in real estate values in 2013.

The decrease in loss sharing expense relates primarily to lower collection costs incurred to resolve problem covered loans. First Financial views the combination of provision expense on covered loans, losses on covered OREO and loss sharing expense, net of the related reimbursements due under loss sharing agreements recorded as FDIC loss sharing income, as the net credit costs associated with covered assets during the period. For additional discussion of the credit costs associated with covered assets, see "Allowance for loan and lease losses, covered loans."

The decline in other noninterest expenses is primarily attributable to a $1.1 million, or 43.3% decline in amortization expense related to core deposit intangibles due to accelerated amortization in conjunction with branch consolidation activities in 2012, a $0.6 million pension administration expense during 2012 and a decline in the reserve for off-balance sheet commitments during 2013.

First Financial Bancorp 2013 Annual Report 17

Management’s Discussion And Analysis Of Financial Condition And Results Of Operations

2012 vs. 2011. Noninterest expenses increased $3.9 million or 1.8% in 2012 compared to 2011, due primarily to a $6.2 million or 5.8% increase in salaries and employee benefits, a $3.1 million or 54.6% increase in data processing expense and a $7.1 million or 197.9% increase in loss sharing expense. These increases were partially offset by a $2.4 million or 24.6% decrease in professional services expense, a $1.0 million or 17.5% decrease in FDIC assessments and a $6.8 million or 73.5% decrease in losses incurred on the sale of covered OREO properties during 2012.

The increase in salaries and benefits during 2012 was primarily attributable to the banking center acquisitions late in 2011 as well as higher incentive payments related to elevated loan originations in 2012. The increase in data processing expense in 2012 was due to various software and system implementations finalized during the year, including new internet and mobile banking platforms introduced late in 2012. The increase in loss sharing expense related primarily to collection costs incurred to resolve problem covered loans. The decline in professional services expense in 2012 was primarily attributable to lower legal costs during the year while the decline in FDIC assessments was related to reduced assessment rates that took effect mid-2011.

INCOME TAXES

First Financial’s tax expense in 2013 totaled $19.2 million compared to $36.4 million in 2012 and $38.3 million in 2011, resulting in effective tax rates of 28.5%, 35.1% and 36.5% in 2013, 2012 and 2011, respectively. The decrease in the effective tax rate in 2013 compared to 2012 was a result of state tax planning strategies implemented during 2013, including formation of a captive real estate investment trust, a favorable adjustment to deferred tax liabilities relating to a change in state tax laws, favorable tax reversals related to an intercompany tax obligation associated with an unconsolidated former Irwin subsidiary and higher income earned on tax exempt securities during the year. The decrease in the effective tax rate in 2012 compared to 2011 was primarily due to a one-time provision to return adjustment related to state income taxes at the subsidiary level as well as the marginal impact of 2011's higher pre-tax earnings. A normalized effective tax rate in future periods is estimated to be 34.0%.

Further information on income taxes is presented in Note 14 of the Notes to Consolidated Financial Statements.

LENDING PRACTICES

First Financial remains dedicated to meeting the financial needs of individuals and businesses through its client-focused business model. The loan portfolio is comprised of a broad range of borrowers primarily in the Ohio, Indiana and Kentucky markets; however, the franchise finance business serves a national client base. All loans acquired in the Peoples and Irwin acquisitions during 2009 were acquired under loss sharing agreements whereby the FDIC reimburses First Financial for the majority of losses incurred in accordance with the agreements.

First Financial’s loan portfolio is composed of commercial loan types, including commercial and industrial (commercial), real estate construction, commercial real estate and equipment leasing (lease financing), as well as consumer loan types, including residential real estate, home equity, installment and credit card loans.

Commercial – Commercial loans include revolving lines of credit and term loans to commercial customers for use in normal business operations to finance working capital needs, equipment purchases, leasehold improvements or other projects. Commercial loans are generally underwritten individually and secured with the assets of the Company and/or the personal guarantee of the business owners. Commercial loans also include asset based lending (ABL), as well as equipment and leasehold improvement financing for select concepts and franchisees in the quick service and casual dining restaurant sector. ABL transactions typically involve larger commercial clients and are secured by specific assets, such as inventory, accounts receivable, machinery and equipment. In the franchise lending space, First Financial focuses on a limited number of restaurant concepts that have sound economics, low closure rates and strong brand awareness within specified local, regional or national markets. First Financial's franchise lending portfolio is managed to a risk-appropriate level so as not to create an industry, geographic or franchisee concept concentration.

While economic trends continued to improve during 2013, the slow and uneven pace of recovery remains a challenge. First Financial maintains vigorous underwriting processes to assess prospective commercial borrowers' credit worthiness prior to origination and actively monitors commercial relationships subsequent to funding in order to ensure adequate oversight of the portfolio.

Real Estate Construction – Real estate construction loans are term loans to individuals, companies or developers used for the construction of a commercial or residential property for which repayment will be generated by the sale or permanent financing of the property. Generally, these loans are for construction projects that have been either pre-sold, pre-leased or have secured permanent financing, as well as loans to real estate companies with significant equity invested in the project. Real estate

18 First Financial Bancorp 2013 Annual Report

construction loans are underwritten by an independent credit team, managed by experienced lending officers and monitored through the construction phase by a centralized funding desk that manages loan disbursements.

First Financial actively monitors industry and portfolio-specific credit trends affecting the Company's construction real estate loan portfolio and continues to restrict real estate construction lending to select opportunities due to excess supply and declines in property values in recent years.

Commercial Real Estate – Commercial real estate loans consist of term loans secured by a mortgage lien on real estate properties such as apartment buildings, office and industrial buildings and retail shopping centers. Additionally, the Company's franchise lending activities discussed in the "Commercial" section above often include the financing of real estate as well as equipment. The credit underwriting for both owner-occupied and investor income producing real estate loans includes detailed market analysis, historical and projected cash flow analysis, appropriate equity margins, assessment of lessees and lessors, type of real estate and other analysis.

While the commercial real estate sector continues to experience residual stress as a result of elevated vacancy levels, lower rents and depressed property values in recent years, First Financial believes the sector is improving and that its current underwriting criteria coupled with active credit monitoring of loan relationships provides adequate oversight of the commercial real estate loan portfolio. The type, age, condition and location of commercial real estate properties, as well as any environmental risks associated with the properties, are considered in the underwriting process for both owner-occupied and investment properties. Credit risk is mitigated by limiting total credit exposure to individual borrowers or groups of borrowers and by requiring borrowers to have adequate down payments or cash equity, thereby limiting the loan balance in relation to the market value of the property. First Financial also regularly reviews borrowers' financial performance, makes periodic site visits to financed properties and monitors factors in the Company's markets that influence real estate collateral values such as rental rates, occupancy trends and capitalization rates.

Lease Financing – Lease financing consists of lease transactions for the purchase of both new and used business equipment for commercial clients. Lease products may include tax leases, finance leases, lease lines of credit and interim funding. The credit underwriting for lease transactions includes detailed analysis of the lessee's industry and business model, nature of the equipment, equipment resale values, historical and projected cash flow analysis, secondary sources of repayment and guarantor analysis as well as other considerations.

Residential Real Estate – Residential real estate loans represent loans to consumers for the financing of a residence.

These loans generally have a 15 to 30 year term and a fixed interest rate, but may have a shorter term to maturity with an adjustable interest rate, and in most cases, are extended to borrowers to finance their primary residence. First Financial sells the majority of residential real estate loan originations into the secondary market on a servicing released basis. Residential real estate loans are generally underwritten to secondary market lending standards, utilizing underwriting systems that rely on empirical data to assess credit risk as well as analysis of the borrowers’ ability to repay their obligations, credit history, the amount of any down payment and the market value or other characteristics of the property. First Financial also offers a residential mortgage product that features similar borrower credit characteristics but a more streamlined underwriting process than typically required to sell to the government-sponsored enterprises and thus is retained on the Consolidated Balance Sheets.

While First Financial continues to sell the majority of residential real estate originations into the secondary market, the Company believes its current underwriting criteria coupled with the monitoring of a number of portfolio metrics, including credit scores and loan-to-value ratios, provides adequate oversight in light of depressed residential property values in recent years.

Home Equity – Home equity lending includes both home equity loans and revolving lines of credit secured by a first or second lien on the borrower’s residence. First Financial's origination practices for home equity lending keep both the credit decision and the documentation under the control of First Financial associates. Home equity lending underwriting includes consideration of the borrowers' credit history as well as to debt-to-income and loan-to-value policy limits.

From an industry perspective, it is likely home equity lending will continue to experience stress as borrowers remain under pressure and property values, while improving, remain depressed in many areas. However, First Financial believes its current underwriting criteria coupled with the monitoring of a number of portfolio metrics including credit scores, loan-to-value ratios, line size and usage provides adequate oversight. At December 31, 2013, approximately 95.0% and 83.7% of the Company's outstanding home equity lines had credit line sizes of less than $100,000 and $50,000 respectively, and had an average outstanding balance of approximately $30,000.

First Financial Bancorp 2013 Annual Report 19

Management’s Discussion And Analysis Of Financial Condition And Results Of Operations

Installment – Installment lending consists of consumer loans not secured by real estate, including loans secured by automobiles and personal unsecured loans.

Credit Card – Credit card lending consists of secured and unsecured revolving lines of credit to consumer and business customers. Credit card lines are generally available for an indefinite period of time as long as the borrower's credit characteristics do not materially or adversely change, but may be canceled by the Company under certain circumstances.

Underwriting for installment and credit card lending focuses on the borrowers’ ability to repay their obligations, including debt-to-income analysis, prior credit history and other information.

Credit Management. Subject to First Financial’s credit policy and guidelines, credit underwriting and approval occur within the region originating the loan and/or the centralized line of business. First Financial has delegated to each market president and line of business manager a lending limit sufficient to handle the majority of client requests in a timely manner. Loan requests for amounts greater than those limits require the approval of a senior credit committee and can include additional approval(s) from the chief credit officer, the chief executive officer and the board of directors as necessary. This allows First Financial to manage the initial credit risk exposure through a standardized, disciplined and strategically focused loan approval process, but with an increasingly higher level of authority. Plans to purchase or sell a participation in a loan or a group of loans require the approval of certain senior lending and administrative officers, and in some cases could include the board of directors.

Credit management practices are dependent on the type and nature of the loan. First Financial monitors all significant

exposures on an on-going basis. Commercial loans are assigned internal risk ratings reflecting the risk of loss inherent in the loan. These internal risk ratings are assigned upon initial approval of credit to borrowers and updated periodically thereafter. First Financial reviews and adjusts its risk rating criteria based on actual experience, which provides the Company with an assessment of the current risk level in the portfolio and is the basis for determining an appropriate allowance for loan and lease losses. First Financial's commercial risk ratings of pass, special mention, substandard and doubtful are derived from standard regulatory rating definitions and facilitate the monitoring of credit quality across the commercial loan portfolio. For further information regarding these risk ratings, see Note 9 in the Notes to the Consolidated Financial Statements.

Commercial loans rated as special mention, substandard or doubtful are considered criticized. Commercial loans rated as substandard or doubtful are considered classified. Commercial loans may be designated as criticized based on individual borrower performance or industry and environmental factors. Criticized loans are subject to additional reviews to adequately assess the borrower’s credit status and develop appropriate action plans.

Classified loans are managed by the Special Assets Division (Special Assets) of the Company. Special Assets is a credit group whose primary focus is to handle the day-to-day management of workouts, commercial recoveries and problem loan resolutions. Special Assets ensures that First Financial has appropriate oversight, improved communication and timely resolution of issues throughout the loan portfolio, including those loans covered by FDIC loss sharing agreements. Additionally, the Credit Risk Management group within First Financial's Risk Management function provides objective oversight and assessment of commercial credit quality and processes using an independent credit risk review approach.

Consumer lending credit approvals are based on, among other factors, the financial strength and payment history of the borrower, type of exposure and the transaction structure. Consumer loans are generally smaller dollar amounts than other types of lending and are made to a large number of customers which provides diversification within the portfolio. Credit risk in the consumer loan portfolio is managed by loan type. Consumer loan types are continuously monitored for changes in delinquency trends and other asset quality indicators. The Credit Risk Management group performs product-level reviews of portfolio performance and assesses credit quality and compliance with underwriting and loan administration guidelines across the consumer loan portfolio.

20 First Financial Bancorp 2013 Annual Report

LOANS, EXCLUDING COVERED LOANS

2013 vs. 2012. First Financial experienced strong loan demand in 2013 as a result of focused sales efforts across the portfolio, as well as success from the investments made in the lease financing and mortgage origination platforms in recent years. While the earnings impact of this loan demand remains muted due to the low interest rate environment, sales efforts across the loan product suite and investments in new and existing markets continue to position the Company for sustained success in generating future earning asset growth. Uncovered loans increased $326.6 million, or 10.3%, from $3.2 billion at December 31, 2012 to $3.5 billion at December 31, 2013, primarily due to growth in the commercial, commercial real estate, lease financing and residential real estate portfolios. Average loan balances increased $320.8 million, or 10.7%, from $3.0 billion at December 31, 2012 to $3.3 billion at December 31, 2013.