Success

doesn’t come overnight. It is the culmination of good planning, many small steps and the occasional giant leap. It requires a solid foundation and constant attention. And when a big success is achieved, there is the realization that many challenging steps lie ahead. 2009 was a successful year for First Financial in many ways. Building upon that foundation will take us to new levels of success. | |

2009 was a year of challenge and

The biggest story in 2009 for First Financial was nearly doubling the size of the company by acquiring the banking operations of Peoples Community Bank, Irwin Union Bank and Trust Company, and Irwin Union Bank, F.S.B.

Having built a strong foundation based on a clear strategic plan, First Financial was ready with the capital and management resources necessary to bid on and acquire the banking operations of these three entities from the Federal Deposit Insurance Corporation (FDIC). Our selection by the FDIC to acquire these companies recognized our solid operating fundamentals, including our strong capital, liquidity and reserve levels.

Since the acquisitions, teams of associates have worked relentlessly on the integration of the new banking centers. Systems have been converted; we have consolidated duplicate locations; and new associates have quickly adapted to their new environment.

Remained profitable in 2009. Throughout the year, First Financial continued to hold its strong financial position by maintaining healthy capital and liquidity levels, controlling expenses, and focusing on core deposit growth.

These metrics highlight this success at our legacy banking centers:

· 14% growth in transaction and savings deposits

· 9% growth in commercial loans

· 8% growth in wealth resource assets under management

· 10% growth in commercial deposit balances

Our sales teams and Compass, our aggressive new retail sales process that was introduced in 2009 and will expand in 2010, contributed to our growth.

January 2009 Entered the year with a strong | February 2009 Expanded our Cincinnati |

| loan loss reserve to prepare for continuing | market with the opening of a new prototype |

| economic stress that was expected in 2009. This | banking center in the suburb of Madeira. Visual |

| prudent action helped manage credit risk and | merchandising as well as engaging retail graphics |

| protect the company. | “take the client on a journey” that reminds them of |

| | defining moments of success in their lives. |

| | |

2 First Financial Bancorp 2009 Annual Report | |

opportunity for First Financial.

Grew our assets. Our acquisitions brought us good facilities, established clients, and knowledgeable associates.

First Financial now has the fourth largest banking center network in the greater Cincinnati market and is the first or second largest in many of the Indiana communities where we have a presence.†

| December 31, 2008 | | | | |

Banking Centers‡ | | | 81 | |

| Associates | | | 1,061 | |

| Total Loans | | $2.7 billion | |

| Total Deposits | | $2.8 billion | |

| Total Assets | | $3.7 billion | |

| December 31, 2009 | | | | |

Banking Centers# | | | 118 | |

| Associates | | | 1,390 | |

| Total Loans | | $4.8 billion | |

| Total Deposits | | $5.4 billion | |

| Total Assets | | $6.7 billion | |

† Based on deposits in the market at June 30, 2009; source FDIC and SNL Financial

‡ Banking centers in operation in Ohio, Indiana and Kentucky

# Banking centers in operation in Ohio, Indiana, Kentucky and Michigan

March 2009 Completed the first quarter of | April 2009 First Financial Bancorp was honored with |

| 2009 profitably and with strong loan and deposit | Ernst & Young’s Entrepreneur of the Year award in the |

| growth. | financial services category. The annual awards recognize |

| | the best innovators and visionary thinkers in South |

| | Central Ohio and Kentucky. An independent panel |

| | judges candidates on financial performance, creativity, |

| | community involvement, and capacity for overcoming |

| | obstacles. |

| | |

| | First Financial Bancorp 2009 Annual Report 3 |

Invested in our franchise and our future. We are adding banking centers that will leverage the First Financial brand to increase market share in key areas, complement existing locations, and provide entry into new markets. In 2009, we built prototype banking centers in Cincinnati and St. Marys, Ohio, and in Edgewood, Kentucky. In addition, eight banking centers were remodeled or refreshed as a continuation of the company’s multi-year plan for improving facilities.

During 2009, our new prototype design for banking centers won two awards for retail design – one national and one international.

Moved our corporate headquarters. To support expansion needs and to further boost visibility and proximity to other companies’ corporate headquarters in the Cincinnati market, we moved our corporate headquarters with a staff of 75 associates to downtown Cincinnati in January of 2010.

May 2009 Began a public offering of 13.8 million | June 2009 Purchased $145 million in performing |

| common shares at $7.50 per share resulting in net | commercial loans with strategic client relationships |

| proceeds of $98 million. This additional capital | from Irwin Union Bank and Trust Company. We |

| positioned us to continue to take advantage of | also announced the purchase of three banking |

| market opportunities. | centers from Irwin – a move that significantly |

| | expanded First Financial’s presence in strategic |

| | locations in central and southeastern Indiana. |

| | |

4 First Financial Bancorp 2009 Annual Report | |

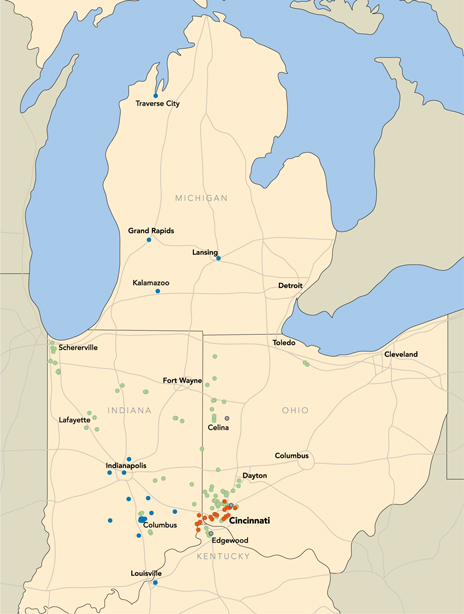

Grew our footprint.

This map shows First Financial’s base at the beginning of 2009 and the expansion of our banking center network within our strategic operating markets of Ohio, Indiana, Kentucky, and Michigan as a result of the acquisitions of the Peoples and Irwin banking centers.

• First Financial’s legacy locations

• Banking centers acquired from Peoples

• Banking centers acquired from Irwin

• New prototype banking centers opened in 2009

Strengthened our brand. After three years of developing and strengthening our brand, we commissioned a quantitative study of the brand’s impact on clients and the public in 2009. Overall awareness of our brand has increased by over 20% compared to baseline research conducted in late 2005.

Client satisfaction also showed improvement in 2009 and was a key element in our success. We continue to bring the First Financial brand of banking to new areas of our footprint.

Working swiftly to further culturalize First Financial’s brand and be sure that we are unified and consistent across all markets, we gain momentum for the challenges ahead.

July 2009 Purchased 19 banking centers, $521 | August 2009 Completed the conversion of |

| million in deposits and $335 million in loans and | client accounts from the three Indiana banking |

| other assets from Peoples Community Bank in | centers acquired from Irwin Union Bank and Trust |

| an FDIC-assisted transaction. This significantly | Company, which included total deposits of $85 |

| strengthened First Financial’s base in Greater | million and total loans of $41 million. This was |

| Cincinnati. | accomplished in record time with the extreme |

| | dedication and hard work of associates across |

| | the company. |

| | |

| | First Financial Bancorp 2009 Annual Report 5 |

Maintained our strong capital position. A strong capital level continued to support the company throughout 2009. At year-end, the total risk-based capital ratio was 18% — far exceeding the regulatory “well-capitalized” minimum requirement of 10%. In addition, our total regulatory capital exceeded the “minimum” requirement amount by $391 million. First Financial is in an excellent position to continue to take advantage of additional market opportunities.

Completed common equity offerings. We successfully completed two common equity offerings — issuing 13.8 million shares of First Financial’s common stock in June of 2009 and 6.4 million shares in February of 2010. Net proceeds from both offerings totaled approximately $190 million. The proceeds from the offering in February of 2010 allowed us to repay in full the $80 million investment made by the U.S. Treasury under the Troubled Asset Relief Program/Capital Purchase Program in December of 2008.

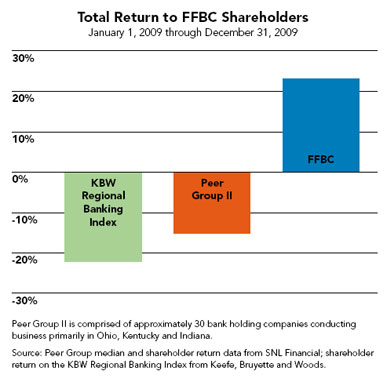

Peer Group II, comprised of approximately 30 bank holding companies conducting business primarily in Ohio, Kentucky and Indiana.

Source: Peer Group median and shareholder return data from SNL Financial; shareholder return on the KBW Regional Banking Index from Keefe, Bruyette and Woods.

Continued shareholder focus. Total return to First Financial shareholders in 2009 was 23.17%. By comparison, total return for Peer Group II was -15.70%, and total return for the KBW Regional Banking Index was -22.13%. First Financial was added to this index in November of 2009.

Managed risks successfully. Following industry trends, credit quality in our commercial and commercial real estate construction loan portfolios continued to weaken throughout 2009. However, our historically conservative underwriting practices, market discipline and proactive management of resolution strategies for problem credits produced asset quality ratios that continue to be better than industry peers.

September 2009 Purchased 27 banking centers, | October 2009 Reported record earnings for the |

| $2.5 billion in deposits and $1.8 billion in loans | third quarter. Net income was $225.6 million and |

| from Irwin Union Bank and Trust Company and | earnings per diluted common share were $4.36. |

| Irwin Union Bank, F.S.B. in an FDIC-assisted | |

| transaction. The purchase expanded First | |

| Financial’s banking center network to 49 locations | |

| in Indiana. | |

| | |

6 First Financial Bancorp 2009 Annual Report | |

2010 Outlook. First and foremost, we will continue to execute our strategic plan. This will fully prepare us to meet new opportunities where we can apply the experiences and processes our teams developed in 2009.

• As a result of the current stress commercial and commercial real estate and construction borrowers are experiencing, we expect to focus more on opportunities for growth in retail and commercial deposits and small business banking in 2010.

• As we move forward, we intend to improve the client experience at every touch point. By striving to be more positive, client-focused, and brand consistent, we will improve our service quality and deliver on our brand promises.

• We will expand our focus on risk management in 2010. We plan to learn from our weaknesses and from experts in the industry to improve our risk management systems and embed them in every aspect of our business.

• We also have plans to improve our position as an “employer of choice.” In 2009, our valued associates worked at a faster pace than ever before and stretched …sometimes more than we thought possible… to accommodate the new clients who came to us from Peoples and Irwin. We appreciate their sacrifice.

In 2010, we expect to move forward, rise to extraordinary results, and take bold new steps on our path to success.

Claude E. Davis, President and CEO

November 2009 Expanded our Northern | December 2009 In order to focus on our |

| Kentucky Market with the opening of a prototype | strategic markets, we began a series of closings |

| banking center in Edgewood, Kentucky. | of the Western states locations obtained in the |

| | acquisition of Irwin Union Bank, F.S.B. These |

| | locations do not fit the company’s strategy of |

| | Midwestern community banking. |

| | |

| | First Financial Bancorp 2009 Annual Report 7 |

| Board of Directors | | Senior Management |

| | | |

| Murph Knapke | | Claude E. Davis |

| Chairman of the Board, | | President and |

| First Financial Bancorp; | | Chief Executive Officer |

| Owner, | | |

| Knapke Law Office, | | C. Douglas Lefferson |

| Attorney-at-Law | | Executive Vice President and |

| | | Chief Operating Officer |

| J. Wickliffe Ach | | |

| President and | | J. Franklin Hall |

| Chief Executive Officer, | | Executive Vice President and |

| Hixson, Inc. | | Chief Financial Officer |

| | | |

| Donald M. Cisle, Sr. | | Samuel J. Munafo |

| President, | | Executive Vice President and |

| Seward-Murphy, Inc. | | Chief Commercial Banking Officer |

| | | |

| Mark A. Collar | | Richard Barbercheck |

| Partner, | | Senior Vice President and |

| Triathlon Medical Ventures; | | Chief Credit Officer |

| Retired President, | | |

| Global Pharmaceuticals & | | Michael J. Cassani |

| Personal Health, | | Senior Vice President and |

| Procter & Gamble Company | | Wealth Resource Group Chief |

| | | Administrative Officer |

| Claude E. Davis | | |

| President and | | Gregory A. Gehlmann |

| Chief Executive Officer, | | Senior Vice President, |

| First Financial Bancorp; | | General Counsel |

| Chairman of the Board, President, | | |

| and Chief Executive Officer, | | Kevin T. Langford |

| First Financial Bank, N.A. | | Senior Vice President and |

| | | Chief Information Officer |

| Corinne R. Finnerty | | |

| Partner, | | Alisa E. Poe |

| McConnell Finnerty Waggoner PC | | Senior Vice President and |

| | | Chief Human Resources Officer |

| Susan L. Knust | | |

| Managing Partner, | | Al Roszczyk |

| K.P. Properties and | | Senior Vice President for the |

| Omega Warehouse Services | | Commercial Banking Regions |

| | | |

| William J. Kramer | | John J. Sabath |

| Vice President of Operations, | | Senior Vice President and |

| Valco Companies, Inc. | | Chief Risk Officer |

| | | |

| Richard E. Olszewski | | Jill A. Stanton |

| Owner, | | Senior Vice President and |

| 7 Eleven Food Stores | | Co-Chief Retail Banking Officer |

| | | |

| | | Anthony M. Stollings |

| | | Senior Vice President, Controller, and |

| Internal Audit | | Chief Accounting Officer |

| James W. Manning | | |

| Senior Vice President and | | Jill L. Wyman |

| Chief Internal Auditor | | Senior Vice President and |

| | | Co-Chief Retail Banking Officer |

8 First Financial Bancorp 2009 Annual Report

Financial Highlights

| (Dollars in thousands, except per share data) | | 2009 | | | 2008 | | | % Change | |

| Earnings | | | | | | | | | |

| Net interest income | | $ | 175,983 | | | $ | 116,202 | | | | 51.45 | % |

| Net income | | | 246,546 | | | | 22,962 | | | | 973.71 | % |

| Income available to common shareholders | | | 242,968 | | | | 22,962 | | | | 958.13 | % |

| | | | | | | | | | | | | |

| Per Share | | | | | | | | | | | | |

| Net income per common share–basic | | $ | 5.40 | | | $ | 0.62 | | | | 770.97 | % |

| Net income per common share–diluted | | | 5.33 | | | | 0.61 | | | | 773.77 | % |

| Cash dividends declared per common share | | | 0.40 | | | | 0.68 | | | | (41.18 | )% |

| Book value per common share (end of year) | | | 11.59 | | | | 7.21 | | | | 60.75 | % |

| Market price (end of year) | | | 14.56 | | | | 12.39 | | | | 17.51 | % |

| | | | | | | | | | | | | |

| Average | | | | | | | | | | | | |

| Total assets | | $ | 4,741,514 | | | $ | 3,426,275 | | | | 38.39 | % |

| Deposits | | | 3,710,832 | | | | 2,797,403 | | | | 32.65 | % |

| Loans, including covered loans | | | 3,432,463 | | | | 2,661,546 | | | | 28.97 | % |

| Investment securities | | | 667,843 | | | | 452,921 | | | | 47.45 | % |

| Shareholders’ equity | | | 473,793 | | | | 279,709 | | | | 69.39 | % |

| | | | | | | | | | | | | |

| Ratios | | | | | | | | | | | | |

| Return on average assets | | | 5.20 | % | | | 0.67 | % | | | 676.12 | % |

| Return on average shareholders’ equity | | | 52.04 | % | | | 8.21 | % | | | 533.86 | % |

| Average shareholders’ equity to average assets | | | 9.99 | % | | | 8.16 | % | | | 22.43 | % |

| Net interest margin | | | 4.05 | % | | | 3.71 | % | | | 9.16 | % |

| Net interest margin (fully tax equivalent) | | | 4.08 | % | | | 3.77 | % | | | 8.22 | % |

First Financial Bancorp 2009 Annual Report 9

Management’s Discussion And Analysis Of Financial Condition And Results Of Operations

This annual report contains forward-looking statements. See Page 26 for further information on the risks and uncertainties associated with forward-looking statements.

The following discussion and analysis is presented to facilitate the understanding of the financial position and results of operations of First Financial Bancorp (First Financial or the Company). It identifies trends and material changes that occurred during the reporting periods and should be read in conjunction with the statistical data, Consolidated Financial Statements, and accompanying Notes on Pages 27 through 56.

EXECUTIVE SUMMARY

First Financial is a $6.7 billion bank holding company headquartered in Cincinnati, Ohio. As of December 31, 2009, First Financial, through its subsidiaries, operated mainly in Ohio, Indiana, Kentucky, and Michigan. These subsidiaries include a commercial bank, First Financial Bank, N.A. (Bank), with 127 banking centers and 149 ATMs, and a registered investment advisory company, First Financial Capital Advisors LLC (Capital Advisors). Within these two subsidiaries, First Financial conducts two primary activities: banking and wealth management. The Bank operates in 10 distinct markets under the First Financial Bank name and provides lending products, deposit accounts, cash management, and other services to commercial and retail clients. The wealth management activities include a full range of services including trust services, brokerage, investment, and other related services. Additionally, the Bank acquired a specialty, franchise lending subsidiary as part of a business combination in 2009 described below. The franchise finance business provides equipment and leasehold improvement financing for franchisees, in the quick service and casual dining restaurant sector, throughout the United States. Loans to franchisees often include the financing of real estate as well as equipment.

In the first quarter of 2010, First Financial’s corporate headquarters was relocated to downtown Cincinnati, Ohio. The Bank subsidiary remains headquartered in Hamilton, Ohio.

First Financial’s return on average shareholders’ equity for 2009 was 52.0%, which compares to 8.21% and 12.73% for 2008 and 2007, respectively. First Financial’s return on average assets for 2009 was 5.20%. This compares to return on average assets of 0.67% and 1.08% for 2008 and 2007, respectively.

The major components of First Financial’s operating results for the past five years are summarized in Table 1 — Financial Summary and discussed in greater detail on subsequent pages.

First Financial serves a combination of metropolitan and non-metropolitan markets in Ohio, Indiana, Kentucky, and Michigan through its full-service banking centers. Market selection is based upon a number of factors, but markets are primarily chosen for their potential for growth, and long-term profitability. First Financial’s goal is to develop a competitive advantage utilizing a local market focus; building long-term relationships with clients and helping them reach greater levels of success in their financial life. During the third quarter of 2009, First Financial assumed the banking operations of Peoples Community Bank (Peoples), Irwin Union Bank and Trust Company (Irwin Union Bank) and Irwin Union Bank, F.S.B. (Irwin FSB) (collectively, Irwin) through Federal Deposit Insurance Corporation (FDIC) assisted transactions. Also during the third quarter of 2009, in a separate and unrelated transaction, First Financial purchased three banking centers including related deposits and loans, from Irwin. First Financial intends to continue to concentrate future growth plans and capital investments in its metropolitan markets. However, the acquired franchise finance subsidiary is a national business. Smaller markets have historically provided stable, low-cost funding sources to First Financial and they remain an important part of its funding base. First Financial believes its historical strength in these markets should enable it to retain or improve its market share.

BUSINESS COMBINATIONS

All references to acquired balances reflect the fair value unless stated otherwise.

During the third quarter of 2009, through FDIC-assisted transactions, First Financial acquired the banking operations of Peoples and Irwin. The company also acquired 3 Indiana banking centers, including related deposits and loans, from Irwin in a separate and unrelated transaction. The acquisitions of the Peoples and Irwin franchises significantly expands the First Financial footprint, opens new markets and strengthens the company through the generation of additional capital. Through these three transactions, the company added a total of 49 banking centers, including 39 banking centers within the company’s primary markets.

In connection with the Peoples and Irwin FDIC-assisted transactions, First Financial entered into loss sharing agreements with the FDIC. Under the terms of these agreements the FDIC will reimburse First Financial for a percentage of losses with respect to certain loans (covered loans) and other real estate owned (OREO) (collectively, covered assets) beginning with the first dollar of loss. These agreements provide for loss protection on single-family, residential loans for a period of ten years and First Financial is required to share any recoveries of previously charged-off amounts for the same time period, on the same pro-rata basis with the FDIC. All other loans are provided loss protection for a period of five years and recoveries of previously charged-off loans must be shared with the FDIC for a period of eight years, again on the same pro-rata basis. Covered loans now represent nearly half of First Financial’s loans.

First Financial must follow specific servicing and resolution procedures, as outlined in the loss share agreements, in order to receive reimbursement from the FDIC for losses on covered assets. The company has established separate and dedicated teams of legal, finance, credit and technology staff to execute and monitor all activity related to each agreement, including the required periodic reporting to the FDIC. First Financial intends to service all covered assets with the same resolution practices and diligence as it does for the assets that are not subject to a loss share agreement.

During the fourth quarter of 2009, initial estimates of loan carrying values and other related balance sheet items were revised and resulted in adjustments to the estimated carrying values of the acquired assets and liabilities previously recorded in the third quarter of 2009. In accordance with FASB ASC Topic 805, previously reported third quarter 2009 results were adjusted to reflect the impact of this additional information. These adjustments resulted in an increase in goodwill and other intangibles of $6.0 million, a net decrease in total assets of $2.2 million, a net decrease in total shareholders’ equity of $0.6 million and a net decrease in after-tax net income of $0.6 million.

An overview of the transactions and their respective loss share agreements are discussed below.

Peoples Community Bank

Including cash received from the FDIC, First Financial acquired $566.0 million in assets, including $336.1 million in loans and other real estate, and assumed $584.7 million in liabilities, including $520.8 million in deposits. All assets and liabilities were recorded at their estimated fair market value resulting in recorded goodwill of $18.1 million as the estimated fair value of liabilities assumed exceeded the estimated fair value of assets acquired.

Covered assets totaling $324.4 million in fair value are subject to a stated loss threshold of $190.0 million whereby the FDIC will reimburse First Financial for 80% of covered asset losses up to $190.0 million, and 95% of losses beyond $190.0 million. The FDIC’s obligation to reimburse First Financial for losses with respect to covered assets begins with the first dollar of loss incurred.

First Financial holds a purchase option from the FDIC for each of Peoples bank properties and their associated contents. First Financial completed a review of the former Peoples locations and notified the FDIC of the company’s intent to purchase certain properties for a combined purchase price of $7.9 million. The acquisition date for these properties has not been determined at this time.

Early in the fourth quarter of 2009, First Financial successfully completed the technology conversion and operational integration of Peoples. In conjunction with these efforts, two former Peoples banking centers were consolidated into First Financial locations and one First Financial banking center was consolidated into a former Peoples location. In addition, of the approximately 115 associates who were employed at Peoples on the acquisition date, 102 have accepted full-time positions at First Financial. The positions are primarily located within the banking center network.

Irwin

Including cash received from the FDIC, First Financial acquired $3.3 billion in assets, including $1.8 billion in loans, and assumed $2.9 billion in liabilities, including $2.5 billion in deposits, with all assets and liabilities recorded at their estimated fair market value.

The loans were acquired under a modified transaction structure with the FDIC whereby certain non-performing loans, foreclosed real estate, acquisition, development and construction loans, and residential and commercial land loans were excluded from the acquired portfolio. The estimated fair value for loans acquired was based upon the FDIC’s estimated data for acquired loans. The company and the FDIC continue to evaluate the total loan portfolio of Irwin to determine if, based on the exclusion criteria, there are additional loans that should be excluded from the portfolio acquired by First Financial. We anticipate the final determination of the excluded loans will be completed by the end of the first quarter of 2010.

Covered assets acquired from Irwin Union Bank totaling $1.5 billion in fair value are subject to a stated loss threshold of $526.0 million whereby the FDIC will reimburse First Financial for 80% of covered asset losses up to $526.0 million, and 95% of losses beyond $526.0 million. The FDIC’s obligation to reimburse First Financial for losses with respect to covered assets begins with the first dollar of loss incurred.

Covered assets acquired from Irwin FSB totaling $259.4 million in fair value are subject to a stated loss threshold of $110.0 million whereby the FDIC will reimburse First Financial for 80% of covered asset losses up to $110.0 million, and 95% of losses beyond $110.0 million. The FDIC’s obligation to reimburse First Financial for losses with respect to covered assets begins with the first dollar of loss incurred.

As the estimated fair value of assets acquired exceeded the estimated fair value of liabilities assumed, First Financial recorded a pre-tax bargain purchase gain of $379.1 million, as required by Financial Accounting Standards Board (FASB) Accounting Standards Codification (ASC) Topic 805, Business Combinations.

Conversion of Irwin’s technology and operational systems was completed in the first quarter of 2010.

10 First Financial Bancorp 2009 Annual Report

Table 1 · Financial Summary

| | | December 31, | |

| (Dollars in thousands, except per share data) | | 2009 | | | 2008 | | | 2007 | | | 2006 | | | 2005 | |

| Summary of operations | | | | | | | | | | | | | | | |

| Interest income | | $ | 233,228 | | | $ | 183,305 | | | $ | 206,442 | | | $ | 205,525 | | | $ | 200,697 | |

Tax equivalent adjustment (1) | | | 1,265 | | | | 1,808 | | | | 2,281 | | | | 2,655 | | | | 2,983 | |

Interest income tax – equivalent (1) | | | 234,493 | | | | 185,113 | | | | 208,723 | | | | 208,180 | | | | 203,680 | |

| Interest expense | | | 57,245 | | | | 67,103 | | | | 87,942 | | | | 80,452 | | | | 67,730 | |

Net interest income tax – equivalent (1) | | $ | 177,248 | | | $ | 118,010 | | | $ | 120,781 | | | $ | 127,728 | | | $ | 135,950 | |

| Interest income | | $ | 233,228 | | | $ | 183,305 | | | $ | 206,442 | | | $ | 205,525 | | | $ | 200,697 | |

| Interest expense | | | 57,245 | | | | 67,103 | | | | 87,942 | | | | 80,452 | | | | 67,730 | |

| Net interest income | | | 175,983 | | | | 116,202 | | | | 118,500 | | | | 125,073 | | | | 132,967 | |

| Provision for loan and lease losses | | | 56,084 | | | | 19,410 | | | | 7,652 | | | | 9,822 | | | | 5,571 | |

| Noninterest income | | | 441,307 | | | | 51,749 | | | | 63,588 | | | | 67,984 | | | | 46,191 | |

| Noninterest expenses | | | 170,638 | | | | 115,176 | | | | 120,747 | | | | 152,515 | | | | 130,165 | |

| Income from continuing operations before income taxes | | | 390,568 | | | | 33,365 | | | | 53,689 | | | | 30,720 | | | | 43,422 | |

| Income tax expense | | | 144,022 | | | | 10,403 | | | | 18,008 | | | | 9,449 | | | | 12,614 | |

| Income from continuing operations | | | 246,546 | | | | 22,962 | | | | 35,681 | | | | 21,271 | | | | 30,808 | |

| Discontinued operations | | | | | | | | | | | | | | | | | | | | |

| Other operating income (loss) | | | 0 | | | | 0 | | | | 0 | | | | 0 | | | | 583 | |

| Gain on sale of discontinued operations | | | 0 | | | | 0 | | | | 0 | | | | 0 | | | | 10,366 | |

| Income (loss) from discontinued operations before income taxes | | | 0 | | | | 0 | | | | 0 | | | | 0 | | | | 10,949 | |

| Income tax expense (benefit) | | | 0 | | | | 0 | | | | 0 | | | | 0 | | | | 3,824 | |

| Income from discontinued operations | | | 0 | | | | 0 | | | | 0 | | | | 0 | | | | 7,125 | |

| Net income | | | 246,546 | | | | 22,962 | | | | 35,681 | | | | 21,271 | | | | 37,933 | |

| Dividends on preferred stock | | | 3,578 | | | | 0 | | | | 0 | | | | 0 | | | | 0 | |

| Income available to common shareholders | | $ | 242,968 | | | $ | 22,962 | | | $ | 35,681 | | | $ | 21,271 | | | $ | 37,933 | |

| | | | | | | | | | | | | | | | | | | | | |

| Per share data | | | | | | | | | | | | | | | | | | | | |

| Earnings per common share from continuing operations: | | | | | | | | | | | | | | | | | | | | |

| Basic | | $ | 5.40 | | | $ | 0.62 | | | $ | 0.93 | | | $ | 0.54 | | | $ | 0.72 | |

| Diluted | | $ | 5.33 | | | $ | 0.61 | | | $ | 0.93 | | | $ | 0.54 | | | $ | 0.71 | |

| Earnings per common share from discontinued operations: | | | | | | | | | | | | | | | | | | | | |

| Basic | | $ | 0.00 | | | $ | 0.00 | | | $ | 0.00 | | | $ | 0.00 | | | $ | 0.17 | |

| Diluted | | $ | 0.00 | | | $ | 0.00 | | | $ | 0.00 | | | $ | 0.00 | | | $ | 0.17 | |

| Earnings per common share | | | | | | | | | | | | | | | | | | | | |

| Basic | | $ | 5.40 | | | $ | 0.62 | | | $ | 0.93 | | | $ | 0.54 | | | $ | 0.89 | |

| Diluted | | $ | 5.33 | | | $ | 0.61 | | | $ | 0.93 | | | $ | 0.54 | | | $ | 0.88 | |

| Cash dividends declared per common share | | $ | 0.40 | | | $ | 0.68 | | | $ | 0.65 | | | $ | 0.64 | | | $ | 0.64 | |

| Average common shares outstanding–basic (in thousands) | | | 45,029 | | | | 37,112 | | | | 38,455 | | | | 39,539 | | | | 43,084 | |

| Average common shares outstanding–diluted (in thousands) | | | 45,557 | | | | 37,484 | | | | 38,459 | | | | 39,562 | | | | 43,173 | |

| | | | | | | | | | | | | | | | | | | | | |

| Selected year-end balances | | | | | | | | | | | | | | | | | | | | |

| Total assets | | $ | 6,681,123 | | | $ | 3,699,142 | | | $ | 3,369,316 | | | $ | 3,301,599 | | | $ | 3,690,808 | |

| Earning assets | | | 5,988,295 | | | | 3,379,873 | | | | 3,054,128 | | | | 2,956,881 | | | | 3,333,406 | |

Investment securities (2) | | | 579,147 | | | | 692,759 | | | | 346,536 | | | | 366,223 | | | | 607,983 | |

| Loans, excluding covered loans | | | 2,893,490 | | | | 2,683,260 | | | | 2,599,087 | | | | 2,479,834 | | | | 2,627,423 | |

| Covered loans | | | 1,929,549 | | | | 0 | | | | 0 | | | | 0 | | | | 0 | |

| FDIC indemnification asset | | | 316,040 | | | | 0 | | | | 0 | | | | 0 | | | | 0 | |

| Interest-bearing demand deposits | | | 1,356,249 | | | | 636,945 | | | | 603,870 | | | | 667,305 | | | | 733,880 | |

| Savings deposits | | | 1,010,469 | | | | 583,081 | | | | 596,636 | | | | 526,663 | | | | 503,297 | |

| Time deposits | | | 2,229,400 | | | | 1,150,208 | | | | 1,227,954 | | | | 1,179,852 | | | | 1,247,274 | |

| Noninterest-bearing demand deposits | | | 754,522 | | | | 413,283 | | | | 465,731 | | | | 424,138 | | | | 440,988 | |

| Total deposits | | | 5,350,640 | | | | 2,783,517 | | | | 2,894,191 | | | | 2,797,958 | | | | 2,925,439 | |

| Short-term borrowings | | | 37,430 | | | | 354,533 | | | | 98,289 | | | | 96,701 | | | | 111,634 | |

| Long-term debt | | | 404,716 | | | | 148,164 | | | | 45,896 | | | | 63,762 | | | | 286,655 | |

| Other long-term debt | | | 20,620 | | | | 20,620 | | | | 20,620 | | | | 30,930 | | | | 30,930 | |

Shareholders’ equity (3) | | | 675,167 | | | | 348,327 | | | | 276,583 | | | | 285,479 | | | | 299,881 | |

| | | | | | | | | | | | | | | | | | | | | |

| Ratios based on average balances | | | | | | | | | | | | | | | | | | | | |

Loans to deposits (4) | | | 92.50 | % | | | 95.14 | % | | | 90.03 | % | | | 89.39 | % | | | 94.81 | % |

| Net charge-offs to loans, excluding covered loans | | | 1.16 | % | | | 0.47 | % | | | 0.24 | % | | | 0.97 | % | | | 0.30 | % |

| Total shareholders’ equity to total assets | | | 9.99 | % | | | 8.16 | % | | | 8.47 | % | | | 8.69 | % | | | 9.57 | % |

| Common shareholders’ equity to total assets | | | 8.34 | % | | | 8.11 | % | | | 8.47 | % | | | 8.69 | % | | | 9.57 | % |

| Return on assets | | | 5.20 | % | | | 0.67 | % | | | 1.08 | % | | | 0.62 | % | | | 1.00 | % |

| Return on common equity | | | 61.43 | % | | | 8.27 | % | | | 12.73 | % | | | 7.13 | % | | | 10.40 | % |

| Return on equity | | | 52.04 | % | | | 8.21 | % | | | 12.73 | % | | | 7.13 | % | | | 10.40 | % |

| Net interest margin | | | 4.05 | % | | | 3.71 | % | | | 3.94 | % | | | 4.01 | % | | | 3.87 | % |

Net interest margin (tax equivalent basis) (1) | | | 4.08 | % | | | 3.77 | % | | | 4.01 | % | | | 4.09 | % | | | 3.96 | % |

| Dividend payout | | | 7.41 | % | | | 109.68 | % | | | 69.89 | % | | | 118.52 | % | | | 71.91 | % |

| (1) | Tax equivalent basis was calculated using a 35.00% tax rate in all years presented. |

| (2) | Includes investment securities held-to-maturity, investment securities available-for-sale, investment securities trading, and other investments. |

| (3) | 2008 Shareholders’ equity was reduced by $2,499 due to the impact of a pension-related accounting pronouncement effective January 1, 2008. |

| | For further information, refer to Note 17 in the Notes to Consolidated Financial Statements. |

| (4) | Includes covered loans |

First Financial Bancorp 2009 Annual Report 11

Management’s Discussion And Analysis Of Financial Condition And Results Of Operations

Irwin Banking Centers

Separate and unrelated to the previously mentioned FDIC-assisted transactions, the company purchased 3 banking centers located in Indiana from Irwin Union Bank, including $84.6 million in deposits and $41.1 million in performing loans. Assets acquired in this transaction are not subject to a loss share agreement. Loans were acquired at par value and there was no premium paid on assumed deposits. The technology conversion and operational integration of all assets acquired and liabilities assumed was complete at the acquisition date. The purchased assets and assumed liabilities were recorded at their estimated fair value resulting in recorded goodwill of $5.4 million as the estimated fair value of liabilities assumed exceeded the estimated fair value of assets acquired. Fair values are preliminary and subject to refinement for up to one year after the closing date of the acquisition, as additional information relative to closing date fair values becomes available.

Strategic Decisions

Management has concluded that the markets previously operated by Irwin in the western United States do not align with the long-term strategic plans for the company. Each of these markets pursued an exit strategy whereby the market presidents worked with an institution of their choosing to refer existing client relationships. If a suitable financial institution was not identified, an exit date was selected for each market and the office closed in compliance with the applicable regulatory requirements. Exit strategies coincided with the conversion and operational integration process. In the fourth quarter of 2009, the company elected to close the St. Louis, Missouri location and sold $43.0 million in western market loans, at their unpaid principal balances.

At December 31, 2009, the nine remaining western offices combined had $684.3 million in unpaid principal balances in loans and $347.0 million in deposits. First Financial will continue to service the loans and deposits in these markets in compliance with the terms of the purchase agreements with the FDIC and FDIC as receiver and related loss share agreements. Additionally, in the first quarter of 2010, First Financial closed 7 of the remaining 9 western market offices and sold an additional $22.6 million in western market loans at their unpaid principal balances.

First Financial also acquired, as part of the Irwin transaction, a franchise finance business. This national business is a specialty lender in the quick service and casual dining segments of the restaurant industry. It is led by a seasoned management team with strong underwriting, credit management and loss mitigation experience. There were outstanding principal balances of approximately $621.6 million in franchise finance loans at December 31, 2009, all of which are covered under a loss share agreement with the FDIC except for $16.9 million of loans originated subsequent to the acquisition.

This business offers First Financial the ability to diversify its earning assets and will be supported as part of the company’s ongoing strategy. The overall portfolio size will be managed to a risk-appropriate level so as not to create an industry concentration.

OVERVIEW OF OPERATIONS

The primary source of First Financial’s revenue is net interest income, the excess of interest received from earning assets over interest paid on interest-bearing liabilities, and the fees for financial services provided to clients. First Financial’s business results tend to be influenced by overall economic factors and conditions, including market interest rates, price competition within the marketplace, business spending, and consumer confidence.

Net interest income in 2009 increased 51.4% from 2008, compared to a 1.9% decline from 2007 to 2008. The increase in 2009, primarily during the second half of the year, was attributable to the Peoples and Irwin acquisitions which occurred in the third quarter. This resulted in an increase in the earning asset base, as well as the repricing of the assumed deposit portfolios. Average earning assets increased $1.2 billion, or 38.8%, during 2009. The net interest margin was 4.05% for 2009, compared with 3.71% in 2008, and 3.94% in 2007.

Loan growth during 2009 was primarily driven by the Peoples and Irwin acquisitions. First Financial continues to expand its commercial lending sales force and deepen its market presence, primarily in metropolitan markets. Total loans increased from $2.7 billion in the fourth quarter of 2008 to $4.8 billion in the fourth quarter of 2009, a $2.1 billion increase. The mix shift from certain lower yielding consumer loans to higher yielding commercial loans continues. Excluding covered loans, period-end commercial, commercial real estate, and construction loans increased from $1.9 billion in the fourth quarter of 2008 to $2.1 billion in the fourth quarter of 2009, an increase of $244.1 million or 12.9%.

The competitive landscape remained intense during 2009 and continues to be impacted by increased liquidity pressure being exhibited by a number of banks in our markets. First Financial experienced significant deposit growth as a result of the acquisitions described above while Compass, the company’s aggressive new retail sales process that was introduced in 2009, also contributed to deposit growth during the year. Average total deposits increased $913.4 million or 32.7% from 2008 to 2009, while, average transaction and savings deposits increased $414.3 million, or 34.0%, during this time.

Noninterest income was positively impacted by a number of factors, primarily driven by the $379.1 million bargain purchase gain recognized in the third quarter due to the Irwin acquisition as well as income earned on covered loans that prepay or that pay according to their contractual obligation. Noninterest expense increased by $55.5 million through 2009 due to higher FDIC assessment costs and higher expenses related to incentive compensation, general growth and market expansion. Acquisition related costs, which were primarily legal, professional, technology, and other integration costs also contributed to the increase in noninterest expense. Staffing, occupancy, and marketing expenses also increased due to the additional banking centers in operation during the second half of 2009.

Credit quality began to deteriorate in the second half of 2008 and this deterioration continued throughout 2009 due to sustained weakness in the economy. First Financial continued to experience significant stress in its commercial and commercial real estate portfolios as borrowers with previously sufficient capital levels struggled to withstand the protracted economic strain. The elevated levels of net charge-offs and nonperforming assets and higher provision expense recorded in 2009 reflected the weak economic conditions, including persistent high unemployment rates, lower consumer spending, higher vacancy rates, lower rents and depressed property values. Management expects credit quality trends to remain volatile until economic conditions exhibit considerable improvement.

The allowance for loan and lease losses (allowance) as a percent of nonperforming loans was 76.3% at December 31, 2009, compared with 197.3% at December 31, 2008. Coverage ratios decreased in 2009 due to growth in nonperforming loans outpacing growth in the allowance. As nonperforming loans increase, more loans are reviewed for specific valuations and these valuations are often less than 100% of loan value resulting in lower coverage ratios. While credit costs trended higher throughout 2009, management believes First Financial’s coverage ratios represent an appropriate level of reserves for the remaining risk in the portfolio. First Financial believes that its credit costs in 2009, although higher than previous levels, remain favorable relative to industry and peer levels and are a reflection of its strong credit management policies and practices.

Actions taken by the FDIC had a negative impact on First Financial’s operating results in 2009, as compared to 2008. In December 2008, the FDIC approved a final rule on deposit assessment rates for the first quarter of 2009. The rule raised assessment rates uniformly by 7 basis points, annually, beginning in the first quarter of 2009. The increase in assessment rates effective January 1, 2009 increased First Financial’s regular assessment to $4.3 million for 2009 from $0.4 million for 2008.

In addition to the change in general assessment rates discussed above, the FDIC board announced an emergency special assessment on all banks that was paid in the second quarter of 2009. The purpose of the special assessment was to restore the Deposit Insurance Fund to an acceptable level. The emergency special assessment resulted in an additional $1.7 million expense for First Financial. FDIC expense for 2009 increased $6.5 million to $6.8 million in 2009, compared to $0.4 million in 2008. We also prepaid an estimated 3 year insurance assessment of $17.1 million on December 30, 2009.

For a more detailed discussion of the above topics, please refer to the sections that follow.

NET INCOME

2009 vs. 2008. First Financial’s net income increased $223.6 million or 973.7% to $246.5 million in 2009, compared to net income of $23.0 million in 2008. Net income in 2009 included a $238.4 million bargain purchase gain, net of taxes, related to the Irwin acquisition in the third quarter. First Financial’s 2008 net income included a $3.7 million loss related to the decline in market value of 200,000 FHLMC perpetual preferred series V shares and a $1.6 million gain associated with the partial redemption of Visa Inc. common shares in the second quarter of 2008. Net interest income increased $59.8 million or 51.4% in 2009 from 2008 primarily due to the Peoples and Irwin acquisitions in the third quarter. Net interest income in 2009 was positively impacted by the increased earning asset base resulting from acquisitions as well as by the repricing of the assumed deposit portfolios. Average earning assets increased $1.2 billion, or 38.8%, during 2009. For more detail, refer to Table 2 — Volume/Rate Analysis and the Net Interest Income section.

2008 vs. 2007. First Financial’s net income decreased $12.7 million or 35.6% to $23.0 million in 2008, compared to net income of $35.7 million in 2007. The 2008 pre-tax income included a $3.7 million loss related to the decline in market value of 200,000 FHLMC perpetual preferred series V shares and a $1.6 million gain associated with the partial redemption of Visa Inc. common shares in the second quarter of 2008. First Financial’s 2007 net income included $5.5 million from the gain on the sale of its merchant payment processing portfolio, $1.1 million from the gain on the sale of residential mortgage servicing rights, and $0.4 million from the gain on the redemption of Mastercard Incorporated common shares, offset by $2.2 million in pension settlement charges and $1.6 million in severance costs. Net interest income decreased $2.3 million or 1.9% in 2008 from 2007 primarily due to the decline in market interest rates partially offset by the continued shift in the mix of deposits from higher-cost certificates of deposit to lower-cost transaction-based accounts and a $124.2 million, or 4.1%, increase in average earning assets during 2008. For more detail, refer to Table 2 — Volume/Rate Analysis and the Net Interest Income section.

12 First Financial Bancorp 2009 Annual ReportNET INTEREST INCOME

First Financial’s net interest income for the years 2005 through 2009 is shown in Table 1 — Financial Summary. Net interest income, First Financial’s principal source of income, is the excess of interest received from earning assets over interest paid on interest-bearing liabilities. The amount of net interest income is determined by the volume and mix of earning assets, the rates earned on such earning assets, and the volume, mix, and rates paid for the deposits and borrowed money that support the earning assets. Table 2 — Volume/Rate Analysis describes the extent to which changes in interest rates and changes in volume of earning assets and interest-bearing liabilities have affected First Financial’s net interest income on a tax equivalent basis during the years indicated. Table 2 — Volume/Rate Analysis should be read in conjunction with the Statistical Information shown on Page 27.

Interest income on a tax equivalent basis is presented in Table 1 — Financial Summary. The tax equivalent adjustment recognizes the income tax savings when comparing taxable and tax-exempt assets and assumes a 35.0% tax rate for all years presented. The tax equivalent net interest margin was 4.08%, 3.77%, and 4.01% for the years 2009, 2008, and 2007, respectively.

Nonaccruing loans and loans held for sale, excluding covered loans, were included in the daily average loan balances used in determining the yields in Table 2 — Volume/Rate Analysis.

Interest foregone on nonaccruing loans is disclosed in Note 10 of the Notes to Consolidated Financial Statements and is not considered to have a material effect on these presentations. The amount of loan fees included in the interest income computation for 2009, 2008, and 2007 was $1.4 million, $1.7 million, and $1.8 million, respectively. The decline in loan fees in 2009 and 2008 is primarily due to First Financial’s decision to sell residential real estate loan originations, resulting in loan fees associated with those loans being owned by the acquirer.

2009 vs. 2008. Interest income was $233.2 million in 2009, a $49.9 million or 27.2% increase from 2008. The yield on earning assets decreased 49 basis points from 5.85% in 2008 to 5.36% in 2009, as market interest rates declined throughout the year. Interest expense was $57.2 million in 2009, a decrease of $9.9 million or 14.7% from 2008. The total cost of funds increased 2 basis points to 2.49% in 2009, from 2.47% in 2008, primarily due to the impact of intense pricing competition for deposit products.

Net interest income increased $59.8 million or 51.4% primarily due to the increased level of earnings assets, including covered loans and their accretable yield. The increase was also positively impacted by the repricing of the assumed deposit portfolio. Average earning assets increased $1.2 billion, or 38.8%, during 2009.

2008 vs. 2007. Interest income was $183.3 million in 2008, a $23.1 million or 11.2% decline from 2007. The yield on earning assets decreased 109 basis points from 6.94% in 2007 to 5.85% in 2008, as market interest rates declined throughout the year. Interest expense was $67.1 million in 2008, a decrease of $20.8 million or 23.7% from 2007. The total cost of funds decreased 90 basis points to 2.47% in 2008, from 3.37% in 2007, primarily due to the decline in market interest rates which were partially offset by the impact of intense pricing competition for deposit products.

Net interest income decreased $2.3 million or 1.9% primarily due to a decline in market interest rates partially offset by the continued shift in the mix of deposits from higher-cost certificates of deposit to lower-cost transaction-based accounts and a $124.2 million, or 4.1%, increase in average earning assets during 2008.

NONINTEREST INCOME AND NONINTEREST EXPENSES

Noninterest income and noninterest expenses for 2009, 2008, and 2007 are shown in Table 3 — Noninterest Income and Noninterest Expenses.

NONINTEREST INCOME

2009 vs. 2008. Noninterest income increased $389.6 million or 752.8% from 2008. Noninterest income in 2009 included a $379.1 million bargain purchase gain on the Irwin acquisition. Noninterest income in 2008 included a $3.7 million loss related to the decline in market value of 200,000 FHLMC perpetual preferred series V shares offset by a $1.6 million gain associated with the partial redemption of Visa Inc. common shares in the second quarter of 2008. Net of the 2009 and 2008 transactions described above, noninterest income increased $6.7 million or 12.1% in 2009 as compared with 2008, primarily due to noninterest income earned on covered loans, higher service charges on deposits, and trust and wealth management fees. The increase in service charges on deposits is a result of the increase in transaction-based deposits from acquisitions.

2008 vs. 2007. Noninterest income decreased $11.8 million or 18.6% from 2007. Net of the 2008 and 2007 transactions described below, overall noninterest income in 2008 declined $2.8 million or 4.3% as compared with 2007, primarily due to lower service charges on deposits, trust and wealth management fees and earnings on bank-owned life insurance. First Financial believes that the economic downturn negatively impacted the spending habits of U.S. consumers and U.S. retail sales in the second half of 2008, also negatively affected First Financial’s client transaction volumes and led to lower deposit service charges compared to 2007. The decline related to trust and wealth management fees are attributable to decreases in investment advisory and trust fees that are a result of lower asset valuations given overall market declines in late 2007 and throughout 2008. Noninterest income in 2008 included a $3.7 million loss related to the decline in market value of 200,000 FHLMC perpetual preferred series V shares and a $1.6 million gain associated with the partial redemption of Visa Inc. common shares in the second quarter of 2008. In 2007, noninterest income included a $5.5 million gain on the sale of the merchant payment processing portfolio in the fourth quarter of 2007, the gain on the sales of investment securities of $0.4 million in the third quarter of 2007, and the gain on the sale of mortgage servicing rights of $1.1 million in the first quarter of 2007.

Table 2 · Volume/Rate Analysis – Tax Equivalent Basis (1)

| | | 2009 change from 2008 due to | | | 2008 change from 2007 due to | |

| (Dollars in thousands) | | VOLUME | | | RATE | | | TOTAL | | | VOLUME | | | RATE | | | TOTAL | |

| Interest income | | | | | | | | | | | | | | | | | | |

Loans (2) | | $ | 8,121 | | | $ | (24,089 | ) | | $ | (15,968 | ) | | $ | 6,906 | | | $ | (29,629 | ) | | $ | (22,723 | ) |

| Covered loans and indemnification asset | | | 58,271 | | | | 0 | | | | 58,271 | | | | N/M | | | | N/M | | | | N/M | |

Investment securities (3) | | | | | | | | | | | | | | | | | | | | | | | | |

| Taxable | | | 10,934 | | | | (1,512 | ) | | | 9,422 | | | | 5,739 | | | | (746 | ) | | | 4,993 | |

| Tax-exempt | | | (1,787 | ) | | | (133 | ) | | | (1,920 | ) | | | (1,634 | ) | | | 390 | | | | (1,244 | ) |

Total investment securities interest (3) | | | 9,147 | | | | (1,645 | ) | | | 7,502 | | | | 4,105 | | | | (356 | ) | | | 3,749 | |

| Interest-bearing deposits with other banks | | | 208 | | | | 0 | | | | 208 | | | | N/M | | | | N/M | | | | N/M | |

| Federal funds sold | | | (633 | ) | | | 0 | | | | (633 | ) | | | (2,911 | ) | | | (1,725 | ) | | | (4,636 | ) |

| Total | | | 75,114 | | | | (25,734 | ) | | | 49,380 | | | | 8,100 | | | | (31,710 | ) | | | (23,610 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | |

| Interest expense | | | | | | | | | | | | | | | | | | | | | | | | |

| Interest-bearing demand deposits | | | 912 | | | | (2,890 | ) | | | (1,978 | ) | | | (120 | ) | | | (7,318 | ) | | | (7,438 | ) |

| Savings deposits | | | 720 | | | | (2,888 | ) | | | (2,168 | ) | | | 298 | | | | (5,685 | ) | | | (5,387 | ) |

| Time deposits | | | 9,525 | | | | (15,796 | ) | | | (6,271 | ) | | | (1,953 | ) | | | (6,409 | ) | | | (8,362 | ) |

| Short-term borrowings | | | 118 | | | | (3,628 | ) | | | (3,510 | ) | | | 2,813 | | | | (2,217 | ) | | | 596 | |

| Long-term debt | | | 4,638 | | | | (385 | ) | | | 4,253 | | | | 783 | | | | 10 | | | | 793 | |

| Other long-term debt | | | 0 | | | | (184 | ) | | | (184 | ) | | | (509 | ) | | | (532 | ) | | | (1,041 | ) |

| Total | | | 15,913 | | | | (25,771 | ) | | | (9,858 | ) | | | 1,312 | | | | (22,151 | ) | | | (20,839 | ) |

| Net interest income | | $ | 59,201 | | | $ | 37 | | | $ | 59,238 | | | $ | 6,788 | | | $ | (9,559 | ) | | $ | (2,771 | ) |

(1) Tax equivalent basis was calculated using a 35.00% tax rate.

(2) Includes loans held-for-sale.

(3) Includes investment securities held-to-maturity, investment securities available-for-sale, and other investments.

N/M=Not meaningful

First Financial Bancorp 2009 Annual Report 13

Management’s Discussion And Analysis Of Financial Condition And Results Of Operations

Table 3 · Noninterest Income And Noninterest Expenses

| | | 2009 | | | 2008 | | | 2007 | |

| | | | | | % CHANGE | | | | | | % CHANGE | | | | | | % CHANGE | |

| | | | | | INCREASE | | | | | | INCREASE | | | | | | INCREASE | |

| (Dollars in thousands) | | TOTAL | | | (DECREASE) | | | TOTAL | | | (DECREASE) | | | TOTAL | | | (DECREASE) | |

| Noninterest income | | | | | | | | | | | | | | | | | | |

| Service charges on deposit accounts | | $ | 19,662 | | | | 0.02 | % | | $ | 19,658 | | | | (5.34 | )% | | $ | 20,766 | | | | (5.43 | )% |

| Trust and wealth management fees | | | 13,465 | | | | (22.66 | )% | | | 17,411 | | | | (5.35 | )% | | | 18,396 | | | | 13.11 | % |

| Bankcard income | | | 5,961 | | | | 5.45 | % | | | 5,653 | | | | 7.66 | % | | | 5,251 | | | | 18.35 | % |

| Net gains from sales of loans | | | 1,196 | | | | 8.33 | % | | | 1,104 | | | | 30.81 | % | | | 844 | | | | (73.67 | )% |

| Gain on sale of merchant payment processing portfolio | | | 0 | | | | N/M | | | | 0 | | | | (100.00 | )% | | | 5,501 | | | | N/M | |

| Gain on sale of mortgage servicing rights | | | 0 | | | | N/M | | | | 0 | | | | (100.00 | )% | | | 1,061 | | | | N/M | |

| Gain on acquisition | | | 379,086 | | | | N/M | | | | 0 | | | | N/M | | | | 0 | | | | N/M | |

| Income (loss) on preferred securities | | | 139 | | | | (103.72 | )% | | | (3,738 | ) | | | N/M | | | | 0 | | | | N/M | |

| Other | | | 18,449 | | | | 83.10 | % | | | 10,076 | | | | (11.63 | )% | | | 11,402 | | | | 13.45 | % |

| Subtotal | | | 437,958 | | | | 773.05 | % | | | 50,164 | | | | (20.65 | )% | | | 63,221 | | | | (7.65 | )% |

| Gains on sales of investment securities | | | 3,349 | | | | 111.29 | % | | | 1,585 | | | | 331.88 | % | | | 367 | | | | (177.10 | )% |

| Total | | $ | 441,307 | | | | 752.78 | % | | $ | 51,749 | | | | (18.62 | )% | | $ | 63,588 | | | | (6.47 | )% |

| | | | | | | | | | | | | | | | | | | | | | | | | |

| Noninterest expenses | | | | | | | | | | | | | | | | | | | | | | | | |

| Salaries and employee benefits | | $ | 86,068 | | | | 28.72 | % | | $ | 66,862 | | | | (4.33 | )% | | $ | 69,891 | | | | (14.31 | )% |

| Pension settlement charges | | | 0 | | | | N/M | | | | 0 | | | | (100.00 | )% | | | 2,222 | | | | (25.16 | )% |

| Net occupancy | | | 16,202 | | | | 52.35 | % | | | 10,635 | | | | (2.08 | )% | | | 10,861 | | | | (1.60 | )% |

| Furniture and equipment | | | 8,054 | | | | 20.07 | % | | | 6,708 | | | | (0.78 | )% | | | 6,761 | | | | 20.58 | % |

| Data processing | | | 3,475 | | | | 7.32 | % | | | 3,238 | | | | (7.43 | )% | | | 3,498 | | | | (64.91 | )% |

| Marketing | | | 3,494 | | | | 37.13 | % | | | 2,548 | | | | 4.38 | % | | | 2,441 | | | | (30.06 | )% |

| Communication | | | 3,246 | | | | 13.54 | % | | | 2,859 | | | | (11.49 | )% | | | 3,230 | | | | (3.12 | )% |

| Professional services | | | 6,032 | | | | 74.18 | % | | | 3,463 | | | | (16.39 | )% | | | 4,142 | | | | (47.13 | )% |

| State intangible tax | | | 2,508 | | | | 0.08 | % | | | 2,506 | | | | 21.06 | % | | | 2,070 | | | | (11.88 | )% |

| FDIC expense | | | 6,847 | | | | 1786.23 | % | | | 363 | | | | 10.00 | % | | | 330 | | | | (9.59 | )% |

| Other | | | 34,712 | | | | 117.03 | % | | | 15,994 | | | | 4.53 | % | | | 15,301 | | | | (36.24 | )% |

| Total | | $ | 170,638 | | | | 48.15 | % | | $ | 115,176 | | | | (4.61 | )% | | $ | 120,747 | | | | (20.83 | )% |

N/M = Not meaningful

NONINTEREST EXPENSES

2009 vs. 2008. Noninterest expenses increased $55.5 million or 48.2% for 2009 compared to 2008 due to higher FDIC costs, general growth and expansion, including acquisition related costs. Salaries and employee benefits increased $19.2 million or 28.7% from 2008 primarily due to higher expenses related to incentive compensation and acquisition related costs, as well as the additional banking centers in operation during the second half of 2009. Professional service fees increased $2.6 million or 74.2% due to acquisition-related services. A $6.5 million increase in FDIC expense due to elevated assessment rates, special assessments and increased deposits, a $0.2 million or 7.3% increase in data processing expense, and a $5.6 million or 52.3% increase in net occupancy expense related to additional banking centers contributed to the increase in noninterest expense in 2009. The increase in other noninterest expense during 2009 was primarily due to other acquisition and integration related costs of $13.4 million.

2008 vs. 2007. Noninterest expenses decreased $5.6 million or 4.6% for 2008 compared to 2007. Salaries and employee benefits decreased $3.0 million or 4.3% from 2007 primarily due to the $1.4 million reduction in salaries and other performance and incentive-based compensation resulting from an overall reduction in staffing levels and the $1.6 million reduction in retirement-related and other benefits expense. Professional fees decreased $0.7 million or 16.4% due to lower employment placement fees and both internal and external audit related expenses during 2008. There were no pension settlement charges in 2008. The $2.2 million of pension settlement charges in 2007 were due to staff reductions and an acceleration of costs that were previously deferred under pension accounting rules that would have been recognized in future periods. A $0.4 million or 11.5% decline in communication expense, a $0.3 million or 7.4% decline in data processing expense, and a $0.2 million or 2.1% decline in net occupancy expense were offset by a $1.1 million or 6.6% increase in other noninterest expense in 2008. The increase in other noninterest expense during 2008 was primarily due to a $0.4 million or 21.1% increase in state intangible tax expense and a $0.3 million or 173.5% increase in other real estate owned expense.

INCOME TAXES

First Financial’s tax expense in 2009 totaled $144.0 million compared to $10.4 million in 2008 and $18.0 million in 2007, resulting in effective tax rates of 36.9%, 31.2%, and 33.5%, in 2009, 2008, and 2007, respectively. The increase in 2009’s effective tax rate as compared to 2008 is primarily due to the tax impact from the bargain purchase gain and other changes resulting from the FDIC-assisted transactions. The lower effective tax rate in 2008 was due to the marginal impact of the year’s lower pre-tax earnings.

Further analysis of income taxes is presented in Note 14 of the Notes to Consolidated Financial Statements.

LOANS

First Financial, primarily through its banking subsidiary, is dedicated to meeting the financial needs of individuals and businesses through its high touch, high service business model. The loan portfolio is comprised of a broad range of borrowers primarily in the Ohio, Kentucky, Michigan, and Indiana markets; however, the acquired franchise finance business markets its services to a national client base. First Financial’s loan portfolio is composed of commercial, commercial real estate, real estate construction, residential real estate, and other consumer financing loans. All loans acquired in the Peoples and Irwin acquisitions were acquired under loss share agreements whereby the FDIC reimburses First Financial for losses incurred in accordance with the loss sharing agreements.

Subject to First Financial’s credit policy and guidelines, credit underwriting and approval occur within the market originating the loan. First Financial has delegated to each market president a lending limit sufficient to handle the majority of client requests in a timely manner. Loan requests for amounts greater than the market limit require the approval of the regional credit officer. The required additional approvals for greater loan amounts include the approval(s) of the chief credit officer, the chief executive officer, and the board of directors as necessary. This allows First Financial to manage the initial credit risk exposure through a standardized, disciplined, and strategically focused loan approval process, but with an increasingly higher level of authority. Plans to purchase or sell a participation in a loan or a group of loans require the approval of certain senior lending and administrative officers, and in some cases could include the board of directors.

Enhanced processes have improved management’s understanding of the loan portfolios and the value of the continuing businesses and relationships. Active use of a Special Assets Division allows First Financial to ensure appropriate oversight, improved communication, and timely resolution of issues throughout the loan portfolio. Additionally, Commercial Credit Risk provides objective oversight and assessment of commercial credit quality and credit processes using an independent, market-based credit risk review approach. Retail/Small Business Credit Risk performs product-level reviews of portfolio performance, assessment of credit quality, and compliance with underwriting and loan administration guidelines. First Financial’s analytical and reporting capability provides timely and valuable portfolio information to aid in credit management.

14 First Financial Bancorp 2009 Annual Report

LOANS (EXCLUDING COVERED LOANS)

2009 vs. 2008. Excluding covered loans, total loans increased $210.2 million or 7.8% during 2009, with average balances increasing $157.0 million or 5.9%. Period-end commercial, commercial real estate and real estate construction loans increased from $1.9 billion at December 31, 2008, to $2.1 billion at December 31, 2009, an increase of $244.1 million or 12.9%. The overall period-end increase in the loan portfolio as compared to 2008 was primarily due to growth in the commercial portfolio, partially offset by declines in consumer-related loan categories. First Financial purchased $145.1 million and $41.1 million in select, performing commercial and consumer loans from Irwin Union Bank on June 30 and August 28, 2009, respectively. None of the loans purchased were residential development, land acquisition or development loans and at the time of purchase, none were 30 days or more delinquent or considered substandard or criticized. The loans were purchased at par and were not purchased under a loss share agreement. Home equity loans increased $42.8 million or 15.0%, from $286.1 million at December 31, 2008 to $328.9 million at December 31, 2009 while residential real estate loans declined by $62.6 million or 16.3%, from $383.6 million at December 31, 2008 to $321.0 million at December 31, 2009.

At December 31, 2009, commercial, commercial real estate, and real estate construction loans comprised 73.7% of First Financial’s total loan portfolio, excluding covered loans. Residential real estate loans at 11.1%, home equity loans at 11.4%, with installment and credit card lending at 3.8%, comprised the remainder of the portfolio.

At December 31, 2009, residential development loans composed 2.9% of First Financial’s total loan portfolio.

In the third and fourth quarters of 2008, First Financial took steps to further manage the risk profile of its balance sheet by securitizing a total of $89.0 million in residential mortgage loans into agency guaranteed, mortgage-backed securities collateralized by those loans. The fourth quarter securitization consisted of $30.5 million in loans and the third quarter securitization consisted of $58.5 million in loans. These securitizations resulted in a reduction in credit risk on the balance sheet and a lower regulatory risk weighting for those assets. The assets remain on the balance sheet, but are now accounted for as investment securities available-for-sale rather than residential real estate loans.

Table 5 — Loan Maturity/Rate Sensitivity indicates the contractual maturity of commercial loans and real estate construction loans outstanding at December 31, 2009. Loans due after one year are classified according to their sensitivity to changes in interest rates.

COVERED LOANS

First Financial purchased $324.5 million and $1.8 billion of loans in conjunction with the FDIC-assisted acquisitions of Peoples and Irwin, respectively. All loans acquired in the Peoples and Irwin acquisitions were acquired under loss share agreements and are referred to as “covered loans,” whereby the FDIC reimburses First Financial for the majority of any losses incurred.

First Financial evaluated loans purchased in conjunction with the acquisitions of Peoples and Irwin for impairment in accordance with the provisions of FASB ASC Topic 310-30, Loans and Debt Securities Acquired with Deteriorated Credit Quality. Purchased loans are considered impaired if there is evidence of credit deterioration since origination and if it is probable that not all contractually required payments will be collected. First Financial elected to account for all covered loans under FASB ASC Topic 310-30, regardless of the impairment determination with the exception of $98.5 million of loans with revolving privileges, which were determined to be outside the scope of FASB ASC Topic 310-30, and other consumer loans which the Company elected to treat under the cost recovery method as expected cash flows could not be reasonably estimated.

Covered loans were recorded at fair value as of the respective acquisition dates. Generally the determination of the fair value of the loans resulted in a significant write-down in the value of the loans, which was assigned to an accretable or nonaccretable balance, with the accretable balance being recognized as interest income over the remaining term of the loan. The nonaccretable portion of the write-down in the value of the loans represents expected credit impairment on the loans and is only recognized in income if the payments on the loan exceed the recorded fair value of the loan.

Table 4 · Loan Portfolio

| | | December 31, | |

| (Dollars in thousands) | | 2009 | | | 2008 | | | 2007 | | | 2006 | | | 2005 | |

| Commercial | | $ | 798,622 | | | $ | 807,720 | | | $ | 785,143 | | | $ | 673,445 | | | $ | 582,594 | |

| Real estate – construction | | | 253,223 | | | | 232,989 | | | | 151,432 | | | | 101,688 | | | | 86,022 | |

| Real estate – commercial | | | 1,079,628 | | | | 846,673 | | | | 706,409 | | | | 623,603 | | | | 646,079 | |

| Real estate – residential | | | 321,047 | | | | 383,599 | | | | 539,332 | | | | 628,579 | | | | 772,334 | |

| Installment | | | 411,929 | | | | 384,691 | | | | 389,783 | | | | 427,009 | | | | 515,200 | |

| Credit card | | | 29,027 | | | | 27,538 | | | | 26,610 | | | | 24,587 | | | | 22,936 | |

| Lease financing | | | 14 | | | | 50 | | | | 378 | | | | 923 | | | | 2,258 | |

| Total loans, excluding covered loans | | | 2,893,490 | | | | 2,683,260 | | | | 2,599,087 | | | | 2,479,834 | | | | 2,627,423 | |

| Covered loans | | | 1,929,549 | | | | 0 | | | | 0 | | | | 0 | | | | 0 | |

| Total | | $ | 4,823,039 | | | $ | 2,683,260 | | | $ | 2,599,087 | | | $ | 2,479,834 | | | $ | 2,627,423 | |

Table 5 · Loan Maturity/Rate Sensitivity (Excluding Covered Loans)

| | | December 31, 2009 | | |

| | | Maturity | | |

| �� | | | | | After one | | | | | | | | |

| | | Within | | | but within | | | After | | | | | |

| (Dollars in thousands) | | one year | | | five years | | | five years | | | Total | | |

| Commercial | | $ | 442,361 | | | $ | 296,759 | | | $ | 59,502 | | | $ | 798,622 | | |

| Real estate – construction | | | 180,754 | | | | 60,380 | | | | 12,089 | | | | 253,223 | | |

| Total | | $ | 623,115 | | | $ | 357,139 | | | $ | 71,591 | | | $ | 1,051,845 | | |

| | | | Sensitivity to changes in interest rates | | | |

| | | | Predetermined | | | Variable | | | |

| (Dollars in thousands) | | | rate | | | rate | | | |

| Due after one year but within five years | | | $ | 138,927 | | | $ | 218,212 | | | |

| Due after five years | | | | 13,926 | | | | 57,665 | | | |

| Total | | | $ | 152,853 | | | $ | 275,877 | | | |

First Financial Bancorp 2009 Annual Report 15

Management’s Discussion And Analysis Of Financial Condition And Results Of Operations

Table 6 · Covered Loan Portfolio

| | | December 31, | |

| (Dollars in thousands) | | 2009 | |

| Commercial | | $ | 509,727 | |

Real estate – construction | | | 86,810 | |

Real estate – commercial | | | 1,012,173 | |

Real estate – residential | | | 291,210 | |

| Installment | | | 9,979 | |

| Other covered loans | | | 19,650 | |

| Total covered loans | | $ | 1,929,549 | |

Table 7 · Covered Loan Maturity

| | | December 31, 2009 | |

| | | Maturity | |

| | | | | | After one | | | | | | | |

| | | Within | | | but within | | | After | | | | |

| (Dollars in thousands) | | one year | | | five years | | | five years | | | Total | |

| Commercial | | $ | 110,964 | | | $ | 155,840 | | | $ | 242,923 | | | $ | 509,727 | |

| Real Estate – construction | | | 65,836 | | | | 15,621 | | | | 5,353 | | | | 86,810 | |

| Total | | $ | 176,800 | | | $ | 171,461 | | | $ | 248,276 | | | $ | 596,537 | |

In addition to the accretion income described above, covered loans impact noninterest income as described in the following two scenarios:

For covered loans that prepay, this income is a result of the net effect of:

| | · | The recovery of the remaining yield-based fair value adjustment, or accretable yield |

| | · | The recovery of the value adjustment associated with assumed credit impairment offset by the corresponding valuation adjustment on the FDIC indemnification asset |

This scenario can occur either through a strategic loan sale or ordinary prepayments that are typical in a loan portfolio.

For covered loans that pay according to their contractual obligation, this income is a result of the net effect of:

| | · | The value adjustment associated with assumed credit impairment offset by the corresponding valuation adjustment on the FDIC indemnification asset |

As First Financial’s experience with the acquired portfolios increases, greater predictability will emerge on the timing of the recognition of the economic value of the transaction. First Financial will consider income associated with strategic loan sales as non-core and will highlight sales when they occur. All other income associated with prepayments or contractual performance will be considered core as it arises from the expected behavior of the purchased portfolios.

First Financial and the FDIC are engaged in on-going discussions that may impact which assets and liabilities are ultimately acquired or assumed by First Financial and/or the purchase prices. The estimated fair values for the purchased impaired and nonimpaired loans were based upon the FDIC’s estimated data for excluded loans. First Financial anticipates the final determination of the excluded loans will be completed in the first quarter of 2010 and expects to finalize its analysis of these loans when this occurs.

Expected reimbursements from the FDIC under the loss sharing agreements were recorded as indemnification assets at their estimated fair value of $316.7 million on the acquisition date. These loss sharing assets are measured separately from the related covered assets as they are not contractually embedded in the assets and are not transferable with the assets should the Bank choose to dispose of them. Fair value was estimated using projected cash flows related to the loss sharing agreements based on the expected reimbursements for losses and the applicable loss sharing percentages. These expected reimbursements do not include reimbursable amounts related to future covered expenditures. These cash flows were discounted to reflect the uncertainty of the timing and receipt of the loss sharing reimbursement from the FDIC.

Reimbursement requests are submitted to the FDIC on a monthly basis for single family residential covered loans and on a quarterly basis for all other covered loans. As of December 31, 2009, none of the reimbursement claims submitted by First Financial had been denied by the FDIC.

CREDIT RISK (EXCLUDING COVERED LOANS)

First Financial records a provision for loan and lease losses (provision) in the Consolidated Statements of Income to provide for expected credit losses. Actual losses on loans and leases are charged against the allowance, which is a reserve accumulated on the Consolidated Balance Sheets through the provision. The recorded values of the loans and leases actually removed from the Consolidated Balance Sheets due to credit deterioration are referred to as charge-offs. Any subsequent recovery of a previously charged off loan is credited back to the allowance. First Financial’s policy is to charge-off loans when, in management’s opinion, full collectibility of principal and interest based upon the contractual terms of the loan is unlikely. All loans charged-off are subject to continuous review and concerted efforts are made to maximize any recovery. In most cases, the borrower’s debt obligation is not cancelled even though the balance may have been charged off.

Management maintains the allowance at a level that is considered sufficient to absorb inherent risks in the loan portfolio. Management’s evaluation in establishing the adequacy of the allowance includes evaluation of the loan and lease portfolios, past loan and lease loss experience, known and inherent risks in the portfolio, adverse situations that may affect the borrower’s ability to repay (including the timing of future payments), the estimated value of any underlying collateral, composition of the loan portfolio, economic conditions, and other pertinent factors, such as periodic internal and external evaluations of delinquent, nonaccrual, and classified loans. The evaluation is inherently subjective as it requires utilizing material estimates, including the amounts and timing of future cash flows expected to be received on impaired loans. The evaluation of these factors is the responsibility of the Allowance for Loan and Lease Losses Committee, which is comprised of senior officers from the risk management, credit administration, finance, and lending areas.