EXHIBIT 13

2010 Annual Report

True commitment involves action – carrying out plans to achieve goals. It unites teams to create new opportunities. It is most tested and most readily proven during tough times. And it is the most important factor to achieving success.

In 2010, First Financial’s strongest commitment was to the execution of our strategic plan. Our plan not only defines our company and how we do business today, but drives our decisions and direction to achieve tomorrow’s success.

commitment

to our values, principles and beliefs

| | Executing Our Strategy in 2010 With our remarkable growth in 2009 came an array of challenges and opportunities – in 2010, First Financial met those challenges successfully and focused on strategic opportunities for future growth. Careful execution of our strategic plan was fundamental throughout 2010, as we integrated the operations we acquired in 2009 while continuing to grow our core businesses. Our steadfast commitment to the plan has also allowed us to avoid some of the issues that have plagued other institutions, and remain focused on making sound business decisions that build shareholder value. |

2 First Financial Bancorp 2010 Annual Report

Achieving Solid Financial Results

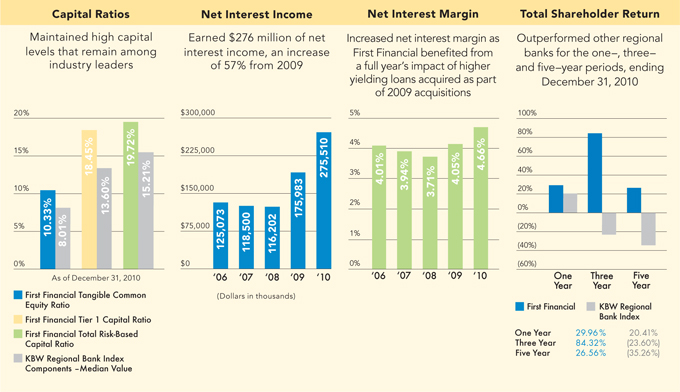

Through the most challenging economic environment in decades, we demonstrated strength and resilience by achieving solid financial results in 2010. Most notably, First Financial completed a common stock offering, generating $91.2 million in common equity, which led to our repayment of $80 million to the U.S. Treasury in February 2010. This ended our participation in the Troubled Asset Relief Program (“TARP”), and with the subsequent auction of the warrants by the U.S. Treasury in June 2010, ended any government ownership in First Financial Bancorp.

Our financial achievements for the year include the following:

| Achieved 81 consecutive quarters of profitability |

| Maintained low-risk balance sheet as 34.5% of loan portfolio enjoys loss share coverage from the FDIC |

| Growth in strategic transaction and savings deposits of 14.5% |

| Continued strong profitability, including 0.91% return on average assets and 8.68% return on average shareholders’ equity |

| Maintained stable credit quality with nonperforming assets representing 1.57% of total assets (excluding covered assets acquired in FDIC-assisted transactions) |

| Announced 20% increase in quarterly dividend effective in 2011 |

| Prepaid $232 million of FHLB advances assumed as part of our 2009 acquisitions |

First Financial Bancorp 2010 Annual Report 3

building

on our solid corporate foundation

2010 was a very active year across First Financial as we aligned resources to maximize growth and efficiency opportunities.

Increased Our Market Presence Throughout the year, we increased visibility in our strategic markets, by: · Establishing a new corporate headquarters in downtown Cincinnati with greater access to clients, partners and professional organizations. · Announcing a new regional hub in Columbus, Indiana that will drive efficiency and create a prototypical facility that fully supports our brand and client experience. · Opening new prototype banking centers in Shelbyville and downtown Indianapolis. Seven banking centers were remodeled or refreshed as part of our facilities improvement plan. · Finalizing our new Corporate Administration Center in Northern Cincinnati, which will unite nearly 400 associates. | | |

4 First Financial Bancorp 2010 Annual Report

Refined Our Business Model and Footprint We focused on increased growth and improved efficiency within our core businesses and footprint by: · Realigning our business model from a regional approach to strategic business lines: commercial, retail/small business and wealth management. · Evaluating market share and growth potential throughout our business. As a result, we announced the planned exit of the Michigan and Louisville, Kentucky markets and sold the property and casualty insurance business gained through acquisition. | | |

| | | |

Broadened Our Product Offerings To achieve our revenue and earnings goals, we invested resources

to expand our product offerings, including: · Increasing our focus on mortgage lending by hiring seasoned originators, building a new origination support team and refining risk and compliance controls. · Expanding our business banking strategy, with new product and service offerings to grow future business opportunities. | | |

| | | |

Inward Focus With our sights on consistent top quartile performance, we have identified new areas of improvement, including: · Peer benchmarking of key metrics and identifying areas to implement company-wide efficiency, business integration and process improvement. · Improving associate engagement in partnership with Gallup to support our goal of becoming an “Employer of Choice.” We expect this to positively impact our financial performance over time. | | |

First Financial Bancorp 2010 Annual Report 5

expectations

for a positive future

6 First Financial Bancorp 2010 Annual Report

Focusing on 2011

To remain strong and well positioned, First Financial plans to capitalize on strategic opportunities to grow our business.

We Will:

| · | Increase proactive sales across our retail and commercial business lines and continue momentum from 2010. Our strong, ambitious sales culture will drive future revenue and increase market share. |

| · | Accelerate growth within our Wealth Management business. This includes refining our strategy and targeting current and prospective clients to increase assets and drive higher revenue. |

| · | Expand our presence within the key growth markets of Greater Cincinnati in Ohio and strategic locations in Indiana. |

| · | Execute efficiency improvement plans. This includes identifying underperforming areas, managing costs and risks and streamlining processes while supporting a high level of client service. |

| · | Continue investing in technology to deliver secure and convenient electronic services that meet our clients’ expectations. |

Challenges and Opportunities

While we see signs of improvement, economic conditions remain challenging and recovery will occur over the long term. We expect new regulatory requirements and financial services reform to provide challenges on all fronts, including increased operating and compliance costs. We are already beginning to experience the impact of such reform on our revenue.

First Financial is well positioned to meet these challenges while delivering value to our shareholders. Our strong capital position will allow us to take advantage of new opportunities. We also continue to balance organic growth while watching for acquisition and other strategic growth opportunities. Finally, we are confident that our client-centered focus will support our ability to grow and maintain long-term client relationships.

We are proud of the successes we’ve achieved in 2010 and look forward to the opportunities that lie ahead.

Claude E. Davis, President and CEO

First Financial Bancorp 2010 Annual Report 7

Directors and Officers

| Board of Directors | | Senior Management |

| Murph Knapke | | Claude E. Davis |

| Chairman of the Board, | | President and |

| First Financial Bancorp; | | Chief Executive Officer |

| Owner, | | |

| Knapke Law Office, | | Richard Barbercheck |

| Attorney-at-Law | | Executive Vice President and |

| | | Chief Credit Officer |

| J. Wickliffe Ach | | |

| President and | | Michael J. Cassani |

| Chief Executive Officer, | | Executive Vice President, |

| Hixson, Inc. | | Wealth Management |

| | | |

| David S. Barker | | Gregory A. Gehlmann |

| President and | | Executive Vice President, |

| Chief Executive Officer, | | General Counsel |

| SIHO Insurance Services | | |

| | | J. Franklin Hall |

| Cynthia O. Booth | | Executive Vice President and |

| President and | | Chief Financial Officer |

| Chief Executive Officer, | | |

| COBCO Enterprises | | Kevin T. Langford |

| | | Senior Vice President and |

| Donald M. Cisle, Sr. | | Chief Administrative Officer |

| President, | | |

| Seward-Murphy, Inc. | | C. Douglas Lefferson |

| | | Executive Vice President and |

| Mark A. Collar | | Chief Banking Officer |

| Partner, | | |

| Triathlon Medical Ventures; | | Samuel J. Munafo |

| Retired President, | | Executive Vice President and |

| Global Pharmaceuticals & | | Chief Commercial Banking Officer |

| Personal Health, | | |

| Procter & Gamble Company | | Alisa E. Poe |

| | | Senior Vice President and |

| Claude E. Davis | | Chief Human Resources Officer |

| President and | | |

| Chief Executive Officer, | | Al Roszczyk |

| First Financial Bancorp; | | Senior Vice President, |

| Chairman of the Board, President, | | Commercial Banking Regions |

| and Chief Executive Officer, | | |

| First Financial Bank, N.A. | | John J. Sabath |

| | | Senior Vice President and |

| Corinne R. Finnerty | | Chief Risk Officer |

| Partner, | | |

| McConnell Finnerty Waggoner PC | | Jill A. Stanton |

| | | Executive Vice President and |

| Susan L. Knust | | Co-Chief Retail Banking Officer |

| Managing Partner, | | |

| K.P. Properties and | | Anthony M. Stollings |

| Omega Warehouse Services | | Senior Vice President, Controller, and |

| | | Chief Accounting Officer |

| William J. Kramer | | |

| Vice President of Operations, | | Jill L. Wyman |

| Valco Companies, Inc. | | Executive Vice President and |

| | | Co-Chief Retail Banking Officer |

| Richard E. Olszewski | | |

| Owner, | | |

| 7 Eleven Food Stores | | |

| | | |

| Maribeth S. Rahe | | |

| President and | | |

| Chief Executive Officer, | | |

| Fort Washington Investment | | |

| Advisors, Inc. | | |

8 First Financial Bancorp 2010 Annual Report

Financial Highlights

| | | | | | | | | | |

| (Dollars in thousands, except per share data) | | 2010 | | | 2009(1) | | | % Change | |

| Earnings | | | | | | | | | |

| Net interest income | | $ | 275,510 | | | $ | 175,983 | | | | 56.55 | % |

| Net income | | | 59,251 | | | | 221,337 | | | | (73.23 | )% |

| Income available to common shareholders | | | 57,386 | | | | 217,759 | | | | (73.65 | )% |

| | | | | | | | | | | | | |

| Per Share | | | | | | | | | | | | |

| Net income per common share–basic | | $ | 1.01 | | | $ | 4.84 | | | | (79.13 | )% |

| Net income per common share–diluted | | | 0.99 | | | | 4.78 | | | | (79.29 | )% |

| Cash dividends declared per common share | | | 0.40 | | | | 0.40 | | | | 0.00 | % |

| Book value per common share (end of year) | | | 12.01 | | | | 11.10 | | | | 8.20 | % |

| Market price (end of year) | | | 18.48 | | | | 14.56 | | | | 26.92 | % |

| | | | | | | | | | | | | |

| Average | | | | | | | | | | | | |

| Total assets | | $ | 6,485,632 | | | $ | 4,734,809 | | | | 36.98 | % |

| Deposits | | | 5,244,347 | | | | 3,710,832 | | | | 41.33 | % |

| Loans, including covered loans | | | 4,520,975 | | | | 3,430,652 | | | | 31.78 | % |

| Investment securities | | | 662,344 | | | | 667,843 | | | | (0.82 | )% |

| Shareholders’ equity | | | 682,987 | | | | 466,610 | | | | 46.37 | % |

| | | | | | | | | | | | | |

| Ratios | | | | | | | | | | | | |

| Return on average assets | | | 0.91 | % | | | 4.67 | % | | | | |

| Return on average shareholders’ equity | | | 8.68 | % | | | 47.44 | % | | | | |

| Average shareholders’ equity to average assets | | | 10.53 | % | | | 9.85 | % | | | | |

| Net interest margin | | | 4.66 | % | | | 4.05 | % | | | | |

| Net interest margin (fully tax equivalent) | | | 4.68 | % | | | 4.08 | % | | | | |

(1) Includes after-tax bargain purchase gain of $213.2 million resulting from business combinations.

First Financial Bancorp 2010 Annual Report 9

Management’s Discussion And Analysis Of Financial Condition And Results Of Operations

This annual report contains forward-looking statements. See Page 28 for further information on the risks and uncertainties associated with forward-looking statements.

The following discussion and analysis is presented to facilitate the understanding of the financial position and results of operations of First Financial Bancorp (First Financial or the Company). It identifies trends and material changes that occurred during the reporting periods and should be read in conjunction with the statistical data, Consolidated Financial Statements, and accompanying Notes on Pages 29 through 63.

EXECUTIVE SUMMARY

First Financial is a $6.3 billion bank holding company headquartered in Cincinnati, Ohio. As of December 31, 2010, First Financial, through its subsidiaries, operated mainly in Ohio, Indiana, Kentucky, and Michigan. These subsidiaries include a commercial bank, First Financial Bank, N.A. (Bank), with 114 banking centers and 138 ATMs, and an investment advisory company, First Financial Capital Advisors LLC (Capital Advisors). Within these two subsidiaries, First Financial conducts two primary activities: banking and wealth management. First Financial expects to execute a dissolution strategy of Capital Advisors, which should be completed in 2011. The Bank operates in 70 communities under the First Financial Bank name and provides credit based products, deposit accounts, corporate cash management support, and other services to commercial and retail clients. The wealth management activities include a full range of services including trust services, brokerage, investment, and other related services. Additionally, the Bank conducts specialty, franchise lending providing equipment and leasehold improvement financing for franchisees, in the quick service and casual dining restaurant sector, throughout the United States. Loans to franchisees often include the financing of real estate as well as equipment. The Company is managing the franchise portfolio to a risk-appropriate level so as not to create an industry, geographic or franchisee concept concentration.

First Financial’s corporate headquarters are located in downtown Cincinnati, Ohio while the Bank subsidiary remains headquartered in Hamilton, Ohio.

First Financial’s return on average shareholders’ equity for 2010 was 8.68%, which compares to 47.44% and 8.21% for 2009 and 2008, respectively. First Financial’s return on average assets for 2010 was 0.91%. This compares to return on average assets of 4.67% and 0.67% for 2009 and 2008, respectively.

The major components of First Financial’s operating results for the past five years are summarized in Table 1 – Financial Summary and discussed in greater detail on subsequent pages.

First Financial serves a combination of metropolitan and non-metropolitan markets in Ohio, Indiana, Kentucky, and Michigan through its full-service banking centers while the franchise finance lending activity serves borrowers throughout the United States. First Financial’s market selection process includes a number of factors, but markets are primarily chosen for their potential for growth, and long-term profitability. First Financial’s goal is to develop a competitive advantage utilizing a local market focus; building long-term relationships with clients, helping them reach greater levels of success in their financial life and providing a superior level of service. First Financial intends to continue to concentrate future growth plans and capital investments in its metropolitan markets. Smaller markets have historically provided stable, low-cost funding sources to First Financial and remain an important part of its funding base. First Financial believes its historical strength in these markets should enable it to retain or improve its market share.

Late in 2010, through an internal review process that included analyzing growth opportunities, brand awareness and penetration within its markets, First Financial announced its decision to exit the four banking center locations comprising its Michigan geographic market as well as its single banking center in Louisville, Kentucky. First Financial decided to shift resources towards core markets such as Cincinnati and Dayton, Ohio and Indianapolis, Southern and Northwest Indiana that it believes will provide a higher level of potential overall growth while improving the efficiency of its operations. The five banking centers in Michigan and Louisville were acquired during 2009 as part of First Financial’s Federal Deposit Insurance Corporation (FDIC)-assisted transactions under which the Company assumed the banking operations of Irwin Union Bank and Trust Company and Irwin Union Bank, F.S.B. (collectively, Irwin).

As of December 31, 2010, First Financial had total loans of $296.6 million and total deposits of $187.9 million in the four banking centers located in Michigan and the Louisville banking center combined. In total, the loans and deposits in these five markets represented 6.9% and 3.7% of First Financial’s total loans and deposits, respectively.

In exiting these markets, First Financial may conduct the sale of loans associated with these locations if market conditions are favorable for such transactions. Otherwise, the loans will be retained and serviced in accordance with their contractual terms and conditions. Deposit clients have been notified of the decision and the related deposit balances are expected to decline as a result of the announcement.

BUSINESS COMBINATIONS

All references to acquired balances reflect the fair value unless stated otherwise.

During the third quarter of 2009, through FDIC-assisted transactions, First Financial acquired the banking operations of Peoples Community Bank (Peoples) and Irwin. The Company also acquired 3 Indiana banking centers, including related deposits and loans, from Irwin in a separate and unrelated transaction prior to the FDIC-assisted transactions. The acquisitions of the Peoples and Irwin franchises significantly expanded the First Financial footprint, opened new markets and strengthened the Company through the generation of additional capital. At the time of their acquisition, these three transactions added a total of 49 banking centers, including 34 banking centers within the Company’s primary markets.

In connection with the Peoples and Irwin FDIC-assisted transactions, First Financial entered into loss sharing agreements with the FDIC. Under the terms of these agreements the FDIC will reimburse First Financial for a percentage of losses with respect to certain loans (covered loans) and other real estate owned (OREO) (collectively, covered assets) beginning with the first dollar of loss. These agreements provide for loss protection on single-family, residential loans for a period of ten years and First Financial is required to share any recoveries of previously charged-off amounts for the same time period, on the same pro-rata basis with the FDIC. All other loans are provided loss protection for a period of five years and recoveries of previously charged-off loans must be shared with the FDIC for a period of eight years, again on the same pro-rata basis. Covered loans represent 34.5% of First Financial’s loans at December 31, 2010.

First Financial must follow specific servicing, resolution and reporting procedures, as outlined in the loss share agreements, in order to receive reimbursement from the FDIC for losses on covered assets. The Company has established separate and dedicated teams of legal, finance, credit and technology staff to execute and monitor all activity related to each agreement, including the required periodic reporting to the FDIC. First Financial services all covered assets with the same resolution practices and diligence as it does for its assets that are not subject to a loss share agreement.

Late in 2009 and again in 2010, initial estimates of loan carrying values and other related balance sheet items were revised and resulted in adjustments to the estimated carrying values of the acquired assets and liabilities previously recorded in the third quarter of 2009. In accordance with FASB ASC Topic 805, Business Combinations, previously reported third quarter 2009 results were adjusted to reflect the impact of this additional information. These adjustments resulted in a $40.8 million pre-tax decline in the originally reported bargain purchase gain on the Irwin acquisitions and a $0.7 million decline in the originally reported goodwill related to the Peoples acquisition. The adjusted pre-tax gain on the Irwin acquisition was $342.5 million and the adjusted goodwill related to the Peoples acquisition was $18.0 million.

An overview of the transactions and their respective loss share agreements are discussed below.

Peoples Community Bank

Including cash received from the FDIC, First Financial acquired $566.6 million in assets, including $341.5 million in loans and other real estate, and assumed $584.7 million in liabilities, including $520.8 million in deposits. All assets and liabilities were recorded at their estimated fair market value resulting in recorded goodwill of $18.0 million as the estimated fair value of liabilities assumed exceeded the estimated fair value of assets acquired.

Covered loans totaling $421.0 million in unpaid principal balance are subject to a stated loss threshold of $190.0 million whereby the FDIC will reimburse First Financial for 80% of covered asset losses up to $190.0 million, and 95% of losses beyond $190.0 million. The FDIC’s obligation to reimburse First Financial for losses with respect to covered assets began with the first dollar of loss incurred.

First Financial did not acquire the real estate, banking facilities, furniture and equipment of Peoples as part of the purchase and assumption agreement but had the option to purchase these assets at fair market value from the FDIC. This purchase option expired 90 days after acquisition date, but was extended by the FDIC. First Financial completed a review of the former Peoples locations and notified the FDIC during the first quarter of 2010 of the Company’s intent to purchase certain properties for a combined purchase price of $7.9 million. First Financial completed the acquisition of these properties from the FDIC in the third quarter of 2010, concluding its last material financial settlement with the FDIC related to the acquisition of Peoples.

Early in the fourth quarter of 2009, First Financial successfully completed the technology conversion and operational integration of Peoples.

10 First Financial Bancorp 2010 Annual Report

| Table 1 • Financial Summary |

| | | December 31, | |

| (Dollars in thousands, except per share data) | | 2010 | | | 2009 | | | 2008 | | | 2007 | | | 2006 | |

| Summary of operations | | | | | | | | | | | | | | | |

| Interest income | | $ | 343,502 | | | $ | 233,228 | | | $ | 183,305 | | | $ | 206,442 | | | $ | 205,525 | |

Tax equivalent adjustment (1) | | | 866 | | | | 1,265 | | | | 1,808 | | | | 2,281 | | | | 2,655 | |

Interest income tax – equivalent (1) | | | 344,368 | | | | 234,493 | | | | 185,113 | | | | 208,723 | | | | 208,180 | |

| Interest expense | | | 67,992 | | | | 57,245 | | | | 67,103 | | | | 87,942 | | | | 80,452 | |

Net interest income tax – equivalent (1) | | $ | 276,376 | | | $ | 177,248 | | | $ | 118,010 | | | $ | 120,781 | | | $ | 127,728 | |

| Interest income | | $ | 343,502 | | | $ | 233,228 | | | $ | 183,305 | | | $ | 206,442 | | | $ | 205,525 | |

| Interest expense | | | 67,992 | | | | 57,245 | | | | 67,103 | | | | 87,942 | | | | 80,452 | |

| Net interest income | | | 275,510 | | | | 175,983 | | | | 116,202 | | | | 118,500 | | | | 125,073 | |

| Provision for loan and lease losses – uncovered | | | 33,564 | | | | 56,084 | | | | 19,410 | | | | 7,652 | | | | 9,822 | |

| Provision for loan and lease losses – covered | | | 63,144 | | | | 0 | | | | 0 | | | | 0 | | | | 0 | |

| Noninterest income | | | 146,831 | | | | 404,715 | | | | 51,749 | | | | 63,588 | | | | 67,984 | |

| Noninterest expenses | | | 233,680 | | | | 170,638 | | | | 115,176 | | | | 120,747 | | | | 152,515 | |

| Income before income taxes | | | 91,953 | | | | 353,976 | | | | 33,365 | | | | 53,689 | | | | 30,720 | |

| Income tax expense | | | 32,702 | | | | 132,639 | | | | 10,403 | | | | 18,008 | | | | 9,449 | |

| Net income | | | 59,251 | | | | 221,337 | | | | 22,962 | | | | 35,681 | | | | 21,271 | |

| Dividends on preferred stock | | | 1,865 | | | | 3,578 | | | | 0 | | | | 0 | | | | 0 | |

| Income available to common shareholders | | $ | 57,386 | | | $ | 217,759 | | | $ | 22,962 | | | $ | 35,681 | | | $ | 21,271 | |

| | | | | | | | | | | | | | | | | | | | | |

| Per share data | | | | | | | | | | | | | | | | | | | | |

| Earnings per common share | | | | | | | | | | | | | | | | | | | | |

| Basic | | $ | 1.01 | | | $ | 4.84 | | | $ | 0.62 | | | $ | 0.93 | | | $ | 0.54 | |

| Diluted | | $ | 0.99 | | | $ | 4.78 | | | $ | 0.61 | | | $ | 0.93 | | | $ | 0.54 | |

| | | | | | | | | | | | | | | | | | | | | |

| Cash dividends declared per common share | | $ | 0.40 | | | $ | 0.40 | | | $ | 0.68 | | | $ | 0.65 | | | $ | 0.64 | |

| Average common shares outstanding–basic (in thousands) | | | 56,969 | | | | 45,029 | | | | 37,112 | | | | 38,455 | | | | 39,539 | |

| Average common shares outstanding–diluted (in thousands) | | | 57,993 | | | | 45,557 | | | | 37,484 | | | | 38,459 | | | | 39,562 | |

| | | | | | | | | | | | | | | | | | | | | |

| Selected year-end balances | | | | | | | | | | | | | | | | | | | | |

| Total assets | | $ | 6,250,225 | | | $ | 6,657,593 | | | $ | 3,699,142 | | | $ | 3,369,316 | | | $ | 3,301,599 | |

| Earning assets | | | 5,741,683 | | | | 5,964,853 | | | | 3,379,873 | | | | 3,054,128 | | | | 2,956,881 | |

Investment securities (2) | | | 1,015,205 | | | | 579,147 | | | | 692,759 | | | | 346,536 | | | | 366,223 | |

| Loans, excluding covered loans | | | 2,816,093 | | | | 2,895,129 | | | | 2,683,260 | | | | 2,599,087 | | | | 2,479,834 | |

| Covered loans | | | 1,481,493 | | | | 1,934,740 | | | | 0 | | | | 0 | | | | 0 | |

| Total loans | | | 4,297,586 | | | | 4,829,869 | | | | 2,683,260 | | | | 2,599,087 | | | | 2,479,834 | |

| FDIC indemnification asset | | | 222,648 | | | | 287,407 | | | | 0 | | | | 0 | | | | 0 | |

| Interest-bearing demand deposits | | | 1,111,877 | | | | 1,060,383 | | | | 636,945 | | | | 603,870 | | | | 667,305 | |

| Savings deposits | | | 1,534,045 | | | | 1,231,081 | | | | 583,081 | | | | 596,636 | | | | 526,663 | |

| Time deposits | | | 1,794,843 | | | | 2,229,500 | | | | 1,150,208 | | | | 1,227,954 | | | | 1,179,852 | |

| Noninterest-bearing demand deposits | | | 705,484 | | | | 829,676 | | | | 413,283 | | | | 465,731 | | | | 424,138 | |

| Total deposits | | | 5,146,249 | | | | 5,350,640 | | | | 2,783,517 | | | | 2,894,191 | | | | 2,797,958 | |

| Short-term borrowings | | | 59,842 | | | | 37,430 | | | | 354,533 | | | | 98,289 | | | | 96,701 | |

| Long-term debt | | | 128,880 | | | | 404,716 | | | | 148,164 | | | | 45,896 | | | | 63,762 | |

| Other long-term debt | | | 20,620 | | | | 20,620 | | | | 20,620 | | | | 20,620 | | | | 30,930 | |

Shareholders’ equity (3) | | | 697,394 | | | | 649,958 | | | | 348,327 | | | | 276,583 | | | | 285,479 | |

| | | | | | | | | | | | | | | | | | | | | |

| Ratios based on average balances | | | | | | | | | | | | | | | | | | | | |

Loans to deposits (4) | | | 86.43 | % | | | 92.56 | % | | | 95.14 | % | | | 90.03 | % | | | 89.39 | % |

| Net charge-offs to loans, excluding covered loans | | | 1.27 | % | | | 1.16 | % | | | 0.47 | % | | | 0.24 | % | | | 0.97 | % |

| Total shareholders’ equity to total assets | | | 10.53 | % | | | 9.85 | % | | | 8.16 | % | | | 8.47 | % | | | 8.69 | % |

| Common shareholders’ equity to total assets | | | 10.35 | % | | | 8.20 | % | | | 8.11 | % | | | 8.47 | % | | | 8.69 | % |

| Return on assets | | | 0.91 | % | | | 4.67 | % | | | 0.67 | % | | | 1.08 | % | | | 0.62 | % |

| Return on common equity | | | 8.55 | % | | | 56.07 | % | | | 8.27 | % | | | 12.73 | % | | | 7.13 | % |

| Return on equity | | | 8.68 | % | | | 47.44 | % | | | 8.21 | % | | | 12.73 | % | | | 7.13 | % |

| Net interest margin | | | 4.66 | % | | | 4.05 | % | | | 3.71 | % | | | 3.94 | % | | | 4.01 | % |

Net interest margin (tax equivalent basis) (1) | | | 4.68 | % | | | 4.08 | % | | | 3.77 | % | | | 4.01 | % | | | 4.09 | % |

| Dividend payout | | | 39.60 | % | | | 8.26 | % | | | 109.68 | % | | | 69.89 | % | | | 118.52 | % |

(1) Tax equivalent basis was calculated using a 35.00% tax rate in all years presented.

(2) Includes investment securities held-to-maturity, investment securities available-for-sale, investment securities trading, and other investments.

(3) 2008 Shareholders’ equity was reduced by $2.5 million due to the impact of a pension-related accounting pronouncement effective January 1, 2008. For further information, refer to Note 18 in the Notes to Consolidated Financial Statements.

(4) Includes covered loans

First Financial Bancorp 2010 Annual Report 11

Management’s Discussion And Analysis Of Financial Condition And Results Of Operations

Irwin

Including cash received from the FDIC, First Financial acquired $3.2 billion in assets, including $1.8 billion in loans, and assumed $2.9 billion in liabilities, including $2.5 billion in deposits, with all assets and liabilities recorded at their estimated fair market value.

The loans were acquired under a modified transaction structure with the FDIC whereby certain non-performing loans, foreclosed real estate, acquisition, development and construction loans, and residential and commercial land loans were excluded from the acquired portfolio. The estimated fair value for the loans acquired was based upon the FDIC’s estimated data for acquired loans.

Covered loans acquired from Irwin Union Bank totaling $1.9 billion in unpaid principal balance are subject to a stated loss threshold of $526.0 million whereby the FDIC will reimburse First Financial for 80% of covered asset losses up to $526.0 million, and 95% of losses beyond $526.0 million. The FDIC’s obligation to reimburse First Financial for losses with respect to covered assets began with the first dollar of loss incurred.

Covered loans acquired from Irwin FSB totaling $368.1 million in unpaid principal balance are subject to a stated loss threshold of $110.0 million whereby the FDIC will reimburse First Financial for 80% of covered asset losses up to $110.0 million, and 95% of losses beyond $110.0 million. The FDIC’s obligation to reimburse First Financial for losses with respect to covered assets began with the first dollar of loss incurred.

As the estimated fair value of assets acquired exceeded the estimated fair value of liabilities assumed, First Financial recorded a pre-tax bargain purchase gain of $342.5 million, as required by Financial Accounting Standards Board (FASB) Accounting Standards Codification (ASC) Topic 805, Business Combinations.

Conversion of Irwin’s technology and operational systems was completed in the first quarter of 2010.

Strategic Decisions

Management concluded that the markets previously operated by Irwin in the western United States did not align with the long-term strategic plans for the Company. Each of these markets pursued an exit strategy whereby the market presidents worked with an institution of their choosing to refer existing client relationships. If a suitable financial institution was not identified, an exit date was selected for each market and the office closed in compliance with the applicable regulatory requirements. Exit strategies coincided with the conversion and operational integration process. In the fourth quarter of 2009, the Company elected to close the St. Louis, Missouri location and sold $42.9 million in western market loans, at their unpaid principal balances.

In the first quarter of 2010, First Financial closed 7 of the remaining 9 western market offices and sold an additional $24.5 million in western market loans at their unpaid principal balances. The two remaining western offices were closed in the third quarter of 2010.

As discussed previously, in the fourth quarter of 2010, First Financial announced its decision to exit four banking centers located in Michigan and the single banking center located in Louisville, Kentucky that were acquired in 2009 as part of the Irwin acquisition.

OVERVIEW OF OPERATIONS

The primary source of First Financial’s revenue is net interest income, the excess of interest received from earning assets over interest paid on interest-bearing liabilities, plus the fees for financial services provided to clients. First Financial’s business results tend to be influenced by overall economic factors and conditions, including market interest rates, price competition within the marketplace, business spending, consumer confidence and regulatory changes.

Net interest income in 2010 increased 56.6% from 2009, compared to a 51.4% increase from 2008 to 2009. The increase in 2010 was attributable to the full year impact of the Peoples and Irwin acquisitions which occurred in the third quarter of 2009. This resulted in an increase in the earning asset base, as well as the repricing of the assumed deposit portfolios. Average earning assets increased $1.6 billion, or 36.0%, during 2010. The net interest margin was 4.66% for 2010, compared with 4.05% in 2009, and 3.71% in 2008.

Loan growth during 2010 was negatively impacted by the runoff of acquired covered loans, the sale of loans in markets previously operated by Irwin in the western United States as well as lower origination volume due to the prolonged weakness in the U.S. economy. Total loans decreased from $4.8 billion at December 31, 2009 to $4.3 billion at December 31, 2010, a $532.3 million decrease. Total loans, excluding covered loans, decreased $79.0 million, from $2.9 billion at December 31, 2009 to $2.8 billion at December 31, 2010. First Financial began to see signs of improving loan demand in the fourth quarter of 2010. Excluding covered loans, period-end commercial, commercial real estate, and construction loans remained relatively flat at $2.1 billion at December 31, 2010 and December 31, 2009, respectively. Several years ago the Company elected to discontinue any material activity in consumer and residential lending for its own portfolio, and continued that strategy throughout 2010.

First Financial experienced moderate net deposit runoff in 2010 as a result of exiting the markets previously operated by Irwin in the western United States as well as continued planned runoff of retail and brokered certificates of deposit. Total deposits decreased $204.4 million or 3.8% from 2009 to 2010. Total time deposits decreased $434.7 million or 19.5% from 2009 to 2010, while total transaction and savings deposits increased $354.5 million, or 15.5%, during this time.

Noninterest income declined by $257.9 million in 2010 but 2009 included a $342.5 million bargain purchase gain related to the Irwin acquisition. Noninterest income during 2010 was positively impacted by higher service charges on deposits and fee income, gains from sales of loans, as well as income earned on covered loans that prepay.

Noninterest expense increased by $63.0 million in 2010 primarily due to higher costs associated with the Company’s expanded operations, debt extinguishment expense, and higher FDIC assessment costs. Acquisition related costs, which were primarily legal, professional, technology, and other integration costs also contributed to the increase in noninterest expense.

Credit quality began to deteriorate early in 2009 and continued through much of 2010 due to sustained weakness in the economy and falling real estate values in all sectors. First Financial continued to experience significant stress in its commercial and commercial real estate portfolios as borrowers with previously sufficient capital levels struggled to withstand the protracted economic strain. The elevated levels of net charge-offs, nonperforming assets and higher provision expense recorded in 2010 reflected the weak economic conditions, including persistent high unemployment rates, lower consumer spending, higher vacancy rates, lower rents and depressed property values. While some positive signs emerged late in 2010 with respect to credit performance of the loan portfolio, management expects credit quality trends to remain volatile until economic conditions exhibit considerable improvement. The key driver in any potential economic improvement remains the overall level of unemployment and while positive downward trends have been experienced recently, it has been at a very slow pace.

The allowance for loan and lease losses (allowance) as a percent of nonperforming loans was 71.6% at December 31, 2010, compared with 76.3% at December 31, 2009. This allowance coverage ratio declined in 2010 as the allowance remained relatively flat while nonperforming loans increased by 2.7%. Larger nonperforming loans are reviewed for specific valuation allowances and these valuation allowances are often less than 100% of loan value resulting in lower coverage ratios. While credit costs remained elevated throughout 2010, management believes First Financial’s coverage ratios represent an appropriate level of reserves for the remaining risk in the portfolio. First Financial believes that its credit costs in 2010, although higher than previous levels, remain favorable relative to industry and peer levels and are a reflection of its strong credit management policies and practices.

For a more detailed discussion of the above topics, please refer to the sections that follow.

NET INCOME

2010 vs. 2009. First Financial’s net income decreased $162.1 million or 73.2% to $59.3 million in 2010, compared to net income of $221.3 million in 2009. Net income in 2009 included a $213.2 million bargain purchase gain, net of taxes, related to the Irwin acquisition. Net interest income increased $99.5 million or 56.6% in 2010 from 2009 primarily due to the full year impact of First Financial’s expanded operations as a result of the Peoples and Irwin acquisitions in 2009. Net interest income in 2010 was positively impacted by the increased earning asset base resulting from acquisitions as well as continued runoff of retail and brokered certificates of deposit and disciplined pricing strategies. Average earning assets increased $1.6 billion, or 36.0%, during 2010. For more detail, refer to Table 2 – Volume/Rate Analysis and the Net Interest Income section.

12 First Financial Bancorp 2010 Annual Report

2009 vs. 2008. First Financial’s net income increased $198.4 million or 863.9% to $221.3 million in 2009, compared to net income of $23.0 million in 2008. Net income in 2009 included a $213.2 million bargain purchase gain, net of taxes, related to the Irwin acquisition. First Financial’s 2008 net income included a $3.7 million loss related to the decline in market value of 200,000 Federal Home Loan Mortgage Corporation (FHLMC) perpetual preferred series V shares and a $1.6 million gain associated with the partial redemption of Visa Inc. common shares in the second quarter of 2008. Net interest income increased $59.8 million or 51.4% in 2009 from 2008 primarily due to the Peoples and Irwin acquisitions in the third quarter. Net interest income in 2009 was positively impacted by the increased earning asset base resulting from acquisitions as well as by the repricing of the assumed deposit portfolios. Average earning assets increased $1.2 billion, or 38.6%, during 2009. For more detail, refer to Table 2 – Volume/Rate Analysis and the Net Interest Income section.

NET INTEREST INCOME

First Financial’s net interest income for the years 2006 through 2010 is shown in Table 1 – Financial Summary. Net interest income, First Financial’s principal source of income, is the excess of interest received from earning assets over interest paid on interest-bearing liabilities. The amount of net interest income is determined by the volume and mix of earning assets, the rates earned on such earning assets, and the volume, mix, and rates paid for the deposits and borrowed money that support the earning assets. Table 2 – Volume/Rate Analysis describes the extent to which changes in interest rates and changes in volume of earning assets and interest-bearing liabilities have affected First Financial’s net interest income on a tax equivalent basis during the years indicated. Table 2 – Volume/Rate Analysis should be read in conjunction with the Statistical Information table.

Interest income on a tax equivalent basis is presented in Table 1 – Financial Summary. The tax equivalent adjustment recognizes the income tax savings when comparing taxable and tax-exempt assets and assumes a 35.0% tax rate for all years presented. The tax equivalent net interest margin was 4.68%, 4.08%, and 3.77% for the years 2010, 2009, and 2008, respectively.

Nonaccruing loans and loans held for sale, excluding covered loans, were included in the daily average loan balances used in determining the yields in Table 2 – Volume/Rate Analysis.

Interest foregone on nonaccruing loans is disclosed in Note 10 of the Notes to Consolidated Financial Statements and is not considered to have a material effect on these presentations. The amount of loan fees included in the interest income computation for 2010, 2009, and 2008 was $4.4 million, $1.4 million, and $1.7 million, respectively. The increase in loan fees in 2010 is primarily due to First Financial’s decision to increase its efforts in residential mortgage lending after scaling back in this area in previous years.

2010 vs. 2009. Interest income was $343.5 million in 2010, a $110.3 million or 47.3% increase from 2009. The yield on earning assets increased 44 basis points from 5.37% in 2009 to 5.81% in 2010, reflecting the positive full year impact of the acquired, covered loan portfolio which generally accreted a yield above market interest rates. Interest expense was $68.0 million in 2010, an increase of $10.7 million or 18.8% from 2009. The total cost of funds decreased 16 basis points to 1.40% in 2010, from 1.56% in 2009, primarily due to the continued runoff of higher priced retail and brokered certificates of deposit.

Net interest income increased $99.5 million or 56.6% primarily due to the increased level of earnings assets, including covered loans and their accretable yield. The increase was also positively impacted by the repricing of the assumed deposit portfolio. Average earning assets increased $1.6 billion, or 36.0%, during 2010.

2009 vs. 2008. Interest income was $233.2 million in 2009, a $49.9 million or 27.2% increase from 2008. The yield on earning assets decreased 48 basis points from 5.85% in 2008 to 5.37% in 2009, as overall market interest rates declined throughout the year, primarily as a result of the Federal Reserve Board’s actions to manage the recessionary environment. Interest expense was $57.2 million in 2009, a decrease of $9.9 million or 14.7% from 2008. The total cost of funds decreased 91 basis points to 1.56% in 2009, from 2.47% in 2008, primarily due to the impact from our aggressive pricing strategies for deposit products.

Net interest income increased $59.8 million or 51.4% primarily due to the increased level of earnings assets, including covered loans and their accretable yield. The increase was also positively impacted by the repricing of the assumed deposit portfolio. Average earning assets increased $1.2 billion, or 38.6%, during 2009.

NONINTEREST INCOME AND NONINTEREST EXPENSES

Noninterest income and noninterest expenses for 2010, 2009, and 2008 are shown in Table 3 – Noninterest Income and Noninterest Expenses.

NONINTEREST INCOME

2010 vs. 2009. Noninterest income decreased $257.9 million or 63.7% from 2009. Noninterest income in 2009 included a $342.5 million bargain purchase gain on the Irwin acquisition. Noninterest income in 2010 also included $51.8 million related to the proportionate share of credit losses on covered loans that First Financial expects to receive from the FDIC. Net of the bargain purchase gain on acquisitions and the FDIC loss sharing income described above, noninterest income increased $32.8 million or 52.7% in 2010 as compared with 2009, primarily due to higher service charges on deposits, fee income and gains from sales of loans reflecting the full year impact of the residential originate and sell strategy. The full year impact of income earned on covered loans that prepay was a significant factor as well. This income results from the immediate or accelerated recognition of a component of the covered loan discount that would have been recognized over the expected life of the loan, had it not prepaid.

Table 2 • Volume/Rate Analysis – Tax Equivalent Basis (1) |

| | | 2010 change from 2009 due to | | | 2009 change from 2008 due to | |

(Dollars in thousands) | | VOLUME | | | RATE | | | TOTAL | | | VOLUME | | | RATE | | | TOTAL | |

| Interest income | | | | | | | | | | | | | | | | | | |

Loans (2) | | $ | (190 | ) | | $ | 1,719 | | | $ | 1,529 | | | $ | 8,121 | | | $ | (24,089 | ) | | $ | (15,968 | ) |

| Covered loans and indemnification asset | | | 111,652 | | | | 3,810 | | | | 115,462 | | | | 58,271 | | | | 0 | | | | 58,271 | |

Investment securities (3) | | | | | | | | | | | | | | | | | | | | | | | | |

| Taxable | | | 140 | | | | (7,768 | ) | | | (7,628 | ) | | | 10,934 | | | | (1,512 | ) | | | 9,422 | |

| Tax-exempt | | | (710 | ) | | | (138 | ) | | | (848 | ) | | | (1,787 | ) | | | (133 | ) | | | (1,920 | ) |

Total investment securities interest (3) | | | (570 | ) | | | (7,906 | ) | | | (8,476 | ) | | | 9,147 | | | | (1,645 | ) | | | 7,502 | |

| Interest-bearing deposits with other banks | | | 1,052 | | | | 308 | | | | 1,360 | | | | 208 | | | | 0 | | | | 208 | |

| Federal funds sold | | | N/M | | | | N/M | | | | N/M | | | | (633 | ) | | | 0 | | | | (633 | ) |

| Total | | | 111,944 | | | | (2,069 | ) | | | 109,875 | | | | 75,114 | | | | (25,734 | ) | | | 49,380 | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

| Interest expense | | | | | | | | | | | | | | | | | | | | | | | | |

| Interest-bearing demand deposits | | | 855 | | | | 355 | | | | 1,210 | | | | 912 | | | | (2,890 | ) | | | (1,978 | ) |

| Savings deposits | | | 3,711 | | | | 1,157 | | | | 4,868 | | | | 720 | | | | (2,888 | ) | | | (2,168 | ) |

| Time deposits | | | 11,132 | | | | (6,454 | ) | | | 4,678 | | | | 9,525 | | | | (15,796 | ) | | | (6,271 | ) |

| Short-term borrowings | | | (389 | ) | | | (835 | ) | | | (1,224 | ) | | | 118 | | | | (3,628 | ) | | | (3,510 | ) |

| Long-term debt | | | 2,083 | | | | (887 | ) | | | 1,196 | | | | 4,638 | | | | (385 | ) | | | 4,253 | |

| Other long-term debt | | | 0 | | | | 19 | | | | 19 | | | | 0 | | | | (184 | ) | | | (184 | ) |

| Total | | | 17,392 | | | | (6,645 | ) | | | 10,747 | | | | 15,913 | | | | (25,771 | ) | | | (9,858 | ) |

| Net interest income | | $ | 94,552 | | | $ | 4,576 | | | $ | 99,128 | | | $ | 59,201 | | | $ | 37 | | | $ | 59,238 | |

(1) Tax equivalent basis was calculated using a 35.00% tax rate.

(2) Includes loans held-for-sale.

(3) Includes investment securities held-to-maturity, investment securities available-for-sale, and other investments.

N/M=Not meaningful

First Financial Bancorp 2010 Annual Report 13

Management’s Discussion And Analysis Of Financial Condition And Results Of Operations

| Table 3 • Noninterest Income And Noninterest Expense |

| | | 2010 | | | 2009 | | | 2008 | |

| | | | | | % CHANGE | | | | | | % CHANGE | | | | | | % CHANGE | |

| | | | | | INCREASE | | | | | | INCREASE | | | | | | INCREASE | |

(Dollars in thousands) | | TOTAL | | | (DECREASE) | | | TOTAL | | | (DECREASE) | | | TOTAL | | | (DECREASE) | |

| Noninterest income | | | | | | | | | | | | | | | | | | |

| Service charges on deposit accounts | | $ | 22,188 | | | | 12.85 | % | | $ | 19,662 | | | | 0.02 | % | | $ | 19,658 | | | | (5.34 | )% |

| Trust and wealth management fees | | | 13,862 | | | | 2.95 | % | | | 13,465 | | | | (22.66 | )% | | | 17,411 | | | | (5.35 | )% |

| Bankcard income | | | 8,518 | | | | 42.90 | % | | | 5,961 | | | | 5.45 | % | | | 5,653 | | | | 7.66 | % |

| Net gains from sales of loans | | | 4,632 | | | | 287.29 | % | | | 1,196 | | | | 8.33 | % | | | 1,104 | | | | 30.81 | % |

| Gain on acquisition | | | 0 | | | | (100.00 | )% | | | 342,494 | | | | N/M | | | | 0 | | | | N/M | |

| FDIC loss sharing income | | | 51,844 | | | | N/M | | | | 0 | | | | N/M | | | | 0 | | | | N/M | |

| Accelerated discount on covered loans | | | 29,067 | | | | 237.95 | % | | | 8,601 | | | | N/M | | | | 0 | | | | N/M | |

| (Loss) Income on preferred securities | | | (30 | ) | | | (121.58 | )% | | | 139 | | | | 103.72 | % | | | (3,738 | ) | | | N/M | |

| Other | | | 16,750 | | | | 70.09 | % | | | 9,848 | | | | (2.26 | )% | | | 10,076 | | | | (43.91 | )% |

| Subtotal | | | 146,831 | | | | (63.42 | )% | | | 401,366 | | | | 700.11 | % | | | 50,164 | | | | (20.65 | )% |

| Gains (losses) on sales of investment securities | | | 0 | | | | (100.00 | )% | | | 3,349 | | | | 111.29 | % | | | 1,585 | | | | 331.88 | % |

| Total | | $ | 146,831 | | | | (63.72 | )% | | $ | 404,715 | | | | 682.07 | % | | $ | 51,749 | | | | (18.62 | )% |

| | | | | | | | | | | | | | | | | | | | | | | | | |

| Noninterest expenses | | | | | | | | | | | | | | | | | | | | | | | | |

| Salaries and employee benefits | | $ | 117,363 | | | | 36.36 | % | | $ | 86,068 | | | | 28.72 | % | | $ | 66,862 | | | | (4.33 | )% |

| Net occupancy | | | 22,555 | | | | 39.21 | % | | | 16,202 | | | | 52.35 | % | | | 10,635 | | | | (2.08 | )% |

| Furniture and equipment | | | 10,299 | | | | 27.87 | % | | | 8,054 | | | | 20.07 | % | | | 6,708 | | | | (0.78 | )% |

| Data processing | | | 5,152 | | | | 48.26 | % | | | 3,475 | | | | 7.32 | % | | | 3,238 | | | | (7.43 | )% |

| Marketing | | | 5,357 | | | | 53.32 | % | | | 3,494 | | | | 37.13 | % | | | 2,548 | | | | 4.38 | % |

| Communication | | | 3,908 | | | | 20.39 | % | | | 3,246 | | | | 13.54 | % | | | 2,859 | | | | (11.49 | )% |

| Professional services | | | 9,169 | | | | 52.01 | % | | | 6,032 | | | | 74.18 | % | | | 3,463 | | | | (16.39 | )% |

| Debt extinguishment | | | 8,029 | | | | N/M | | | | 0 | | | | N/M | | | | 0 | | | | N/M | |

| State intangible tax | | | 4,843 | | | | 93.10 | % | | | 2,508 | | | | 0.08 | % | | | 2,506 | | | | 21.06 | % |

| FDIC assessments | | | 8,312 | | | | 21.40 | % | | | 6,847 | | | | 1786.23 | % | | | 363 | | | | 10.00 | % |

| Other | | | 38,693 | | | | 11.47 | % | | | 34,712 | | | | 117.03 | % | | | 15,994 | | | | (8.73 | )% |

| Total | | $ | 233,680 | | | | 36.94 | % | | $ | 170,638 | | | | 48.15 | % | | $ | 115,176 | | | | (4.61 | )% |

N/M = Not meaningful

2009 vs. 2008. Noninterest income increased $353.0 million or 682.1% from 2008. Noninterest income in 2009 included a $342.5 million bargain purchase gain on the Irwin acquisition. Noninterest income in 2008 included a $3.7 million loss related to the decline in market value of 200,000 FHLMC perpetual preferred series V shares offset by a $1.6 million gain associated with the partial redemption of Visa Inc. common shares in the second quarter of 2008. Net of the 2009 and 2008 transactions described above, noninterest income increased $8.3 million or 15.4% in 2009 as compared with 2008, primarily due to noninterest income earned on covered loans, higher service charges on deposits, and trust and wealth management fees. The increase in service charges on deposits is a result of the increase in transaction-based deposits from acquisitions.

NONINTEREST EXPENSES

2010 vs. 2009. Noninterest expenses increased $63.0 million or 36.9% for 2010 compared to 2009 due to higher FDIC costs, debt prepayment charges, and general growth and expansion, including acquisitions. Salaries and employee benefits increased $31.3 million or 36.4% from 2009 primarily due to higher expenses related to acquisitions, greater staffing levels as well as the additional banking centers in operation during 2010.

Noninterest expenses in 2010 included an $8.0 million charge related to the prepayment of long term debt assumed in the 2009 acquisitions. Professional service fees increased $3.1 million or 52.0% primarily due to higher legal costs and other professional services directly related to the Company’s growth as well as continued costs related to the acquisitions in 2009. A $1.5 million increase in FDIC expense due to elevated assessment rates and increased deposits, as well as a combined $10.3 million or 37.1% increase in net occupancy, furniture and equipment, and data processing expenses related to additional banking centers contributed to the increase in noninterest expense in 2010. The $4.0 million increase in other noninterest expense during 2010 was primarily due to amortization of intangible assets related to FDIC-assisted transactions, losses on OREO property sales, and higher credit origination costs and regulatory assessment fees.

2009 vs. 2008. Noninterest expenses increased $55.5 million or 48.2% for 2009 compared to 2008 due to higher FDIC costs, general growth and expansion, including acquisition related costs. Salaries and employee benefits increased $19.2 million or 28.7% from 2008 primarily due to higher expenses related to incentive compensation and acquisition related costs, as well as the additional banking centers in operation during the second half of 2009. Professional service fees increased $2.6 million or 74.2% due to acquisition-related services. A $6.5 million increase in FDIC expense due to elevated assessment rates, special assessments and increased deposits, a $0.2 million or 7.3% increase in data processing expense, and a $5.6 million or 52.3% increase in net occupancy expense related to additional banking centers contributed to the increase in noninterest expense in 2009. The increase in other noninterest expense during 2009 was primarily due to other acquisition and integration related costs of $13.4 million.

INCOME TAXES

First Financial’s tax expense in 2010 totaled $32.7 million compared to $132.6 million in 2009 and $10.4 million in 2008, resulting in effective tax rates of 35.6%, 37.5%, and 31.2%, in 2010, 2009, and 2008, respectively. The decrease in the effective tax rate in 2010 from 2009 was due to the marginal impact of 2010’s lower pre-tax earnings. The increase in 2009’s effective tax rate as compared to 2008 is primarily due to the tax impact from the bargain purchase gain and other implications from the FDIC-assisted transactions.

Further analysis of income taxes is presented in Note 15 of the Notes to Consolidated Financial Statements.

LOANS

First Financial, primarily through its banking subsidiary, remains dedicated to meeting the financial needs of individuals and businesses through its high touch, high service business model. The loan portfolio is comprised of a broad range of borrowers primarily in the Ohio, Kentucky, Michigan, and Indiana markets; however, the franchise finance lending activity represents a national client base. First Financial’s loan portfolio is composed of commercial, commercial real estate, real estate construction, residential real estate, and other consumer financing loans. All loans acquired in the Peoples and Irwin acquisitions during 2009 were acquired under loss share agreements whereby the FDIC reimburses First Financial for losses incurred in accordance with those loss sharing agreements.

14 First Financial Bancorp 2010 Annual Report

| | | December 31, | |

| (Dollars in thousands) | | 2010 | | | 2009 | | | 2008 | | | 2007 | | | 2006 | |

| Commercial | | $ | 800,253 | | | $ | 800,261 | | | $ | 807,720 | | | $ | 785,143 | | | $ | 673,445 | |

| Real estate – construction | | | 163,543 | | | | 253,223 | | | | 232,989 | | | | 151,432 | | | | 101,688 | |

| Real estate – commercial | | | 1,139,931 | | | | 1,079,628 | | | | 846,673 | | | | 706,409 | | | | 623,603 | |

| Real estate – residential | | | 269,173 | | | | 321,047 | | | | 383,599 | | | | 539,332 | | | | 628,579 | |

| Installment | | | 69,711 | | | | 82,989 | | | | 98,581 | | | | 138,895 | | | | 198,881 | |

| Home equity | | | 341,310 | | | | 328,940 | | | | 286,110 | | | | 250,888 | | | | 228,128 | |

| Credit card | | | 29,563 | | | | 29,027 | | | | 27,538 | | | | 26,610 | | | | 24,587 | |

| Lease financing | | | 2,609 | | | | 14 | | | | 50 | | | | 378 | | | | 923 | |

| Total loans, excluding covered loans | | | 2,816,093 | | | | 2,895,129 | | | | 2,683,260 | | | | 2,599,087 | | | | 2,479,834 | |

| Covered loans | | | 1,481,493 | | | | 1,934,740 | | | | 0 | | | | 0 | | | | 0 | |

| Total | | $ | 4,297,586 | | | $ | 4,829,869 | | | $ | 2,683,260 | | | $ | 2,599,087 | | | $ | 2,479,834 | |

| Table 5 • Loan Maturity/Rate Sensitivity (Excluding Covered Loans) |

| | | December 31, 2010 | |

| | | Maturity | |

| (Dollars in thousands) | | Within one year | | | After one but within five years | | | After five years | | | Total | |

| Commercial | | $ | 386,040 | | | $ | 316,828 | | | $ | 97,385 | | | $ | 800,253 | |

| Real estate – construction | | | 120,410 | | | | 42,285 | | | | 848 | | | | 163,543 | |

| Total | | $ | 506,450 | | | $ | 359,113 | | | $ | 98,233 | | | $ | 963,796 | |

| | | Sensitivity to changes in interest rates | |

| (Dollars in thousands) | | Predetermined rate | | | Variable rate | |

| Due after one year but within five years | | $ | 177,383 | | | $ | 181,730 | |

| Due after five years | | | 49,244 | | | | 48,989 | |

| Total | | $ | 226,627 | | | $ | 230,719 | |

| Table 6 • Covered Loan Portfolio |

| (Dollars in thousands) | | December 31, 2010 | | | December 31, 2009 | |

| Commercial | | $ | 334,039 | | | $ | 506,887 | |

| Real estate – construction | | | 42,743 | | | | 97,560 | |

| Real estate – commercial | | | 855,725 | | | | 1,008,104 | |

| Real estate – residential | | | 147,052 | | | | 206,371 | |

| Installment | | | 21,071 | | | | 8,235 | |

| Home equity | | | 73,695 | | | | 87,933 | |

| Other covered loans | | | 7,168 | | | | 19,650 | |

| Total covered loans | | $ | 1,481,493 | | | $ | 1,934,740 | |

Subject to First Financial’s credit policy and guidelines, credit underwriting and approval occur within the market originating the loan. First Financial has delegated to each market president a lending limit sufficient to handle the majority of client requests in a timely manner. Loan requests for amounts greater than the market limit require the approval of the regional credit officer. The required additional approvals for greater loan amounts include the approval(s) of the chief credit officer, the chief executive officer, and the board of directors as necessary. This allows First Financial to manage the initial credit risk exposure through a standardized, disciplined, and strategically focused loan approval process, but with an increasingly higher level of authority. Plans to purchase or sell a participation in a loan or a group of loans require the approval of certain senior lending and administrative officers, and in some cases could include the board of directors.

Enhanced processes have improved management’s understanding of the loan portfolios and the value of the continuing businesses and relationships. Active use of a Special Assets Division allows First Financial to ensure appropriate oversight, improved communication, and timely resolution of issues throughout the loan portfolio, including those loans covered by FDIC loss sharing agreements. Additionally, Commercial Credit Risk provides objective oversight and assessment of commercial credit quality and credit processes using an independent, market-based credit risk review approach. Retail/Small Business Credit Risk performs product-level reviews of portfolio performance, assessment of credit quality, and compliance with underwriting and loan administration guidelines. First Financial believes its analytical and reporting capability provides timely and valuable portfolio information to aid in credit management.

First Financial Bancorp 2010 Annual Report 15

Management’s Discussion And Analysis Of Financial Condition And Results Of Operations

| Table 7 • Covered Loan Maturity |

| | | December 31, 2010 | |

| | | Maturity | |

| (Dollars in thousands) | | Within one year | | | After one year but within five years | | | After five years | | | Total | |

| Commercial | | $ | 94,682 | | | $ | 209,744 | | | $ | 29,613 | | | $ | 334,039 | |

| Real estate – construction | | | 34,012 | | | | 7,988 | | | | 743 | | | | 42,743 | |

| Total | | $ | 128,694 | | | $ | 217,732 | | | $ | 30,356 | | | $ | 376,782 | |

| | | Sensitivity to changes in interest rates | |

| (Dollars in thousands) | | Predetermined rate | | | Variable rate | |

| Due after one year but within five years | | $ | 171,787 | | | $ | 45,945 | |

| Due after five years | | | 15,366 | | | | 14,990 | |

| Total | | $ | 187,153 | | | $ | 60,935 | |

LOANS – EXCLUDING COVERED LOANS

2010 vs. 2009. Excluding covered loans, total loans decreased $79.0 million or 2.7% during 2010, with average balances decreasing $11.1 million or 0.4%. The overall decline in the loan portfolio as compared to 2009 was primarily driven by weak loan demand as a result of difficult economic conditions throughout 2010 and intense competition for the limited lending opportunities that did exist. Period-end commercial, commercial real estate and real estate construction loans declined by $29.4 million or 1.4% from December 31, 2009, to December 31, 2010. The decline in the commercial portfolio was due primarily to an $89.7 million, or 35.4%, decline in real estate construction loans during 2010 as a result of the Company’s decision to limit lending in this segment given economic conditions. The decline in real estate construction loans was partially offset by a $60.3 million, or 5.6%, increase in commercial real estate loans during 2010. Additionally, consumer-related loan categories declined by $49.7 million or 6.5% during 2010, primarily related to a $51.9 million or 16.2% decline in residential real estate loans during the year. The runoff of residential real estate loans during 2010 reflects the continued impact of First Financial’s strategic decision to discontinue the origination of residential real estate loans for retention on its balance sheet.

At December 31, 2010, commercial, commercial real estate, and real estate construction loans comprised 74.7% of First Financial’s total loan portfolio, excluding covered loans. Residential real estate loans at 9.6%, home equity loans at 12.1%, with installment, credit card and other lending at 3.6%, comprised the remainder of the portfolio.

At December 31, 2010, residential development loans composed 2.3% of First Financial’s total loan portfolio.

Table 5 – Loan Maturity/Rate Sensitivity indicates the contractual maturity of commercial loans and real estate construction loans outstanding at December 31, 2010. Loans due after one year are classified according to their sensitivity to changes in interest rates.

LOANS – COVERED

Acquired loans subject to loss share agreements whereby the FDIC reimburses First Financial for the majority of any losses incurred are referred to as covered loans.

First Financial evaluated loans purchased in conjunction with the acquisitions of Peoples and Irwin for impairment in accordance with the provisions of FASB ASC Topic 310-30, Loans and Debt Securities Acquired with Deteriorated Credit Quality. Acquired loans are considered impaired if there is evidence of credit deterioration since origination and if it is probable that not all contractually required payments will be collected. First Financial accounts for the majority of covered loans under FASB ASC Topic 310-30 with the exception of loans with revolving privileges, which were determined to be outside the scope of FASB ASC Topic 310-30, and other consumer loans for which expected cash flows could not be reasonably estimated. For further information around the accounting for covered loans, see the Critical Accounting Policies section included in Management’s Discussion and Analysis as well as the Notes to the Consolidated Financial Statements.

2010 vs. 2009. Total covered loans decreased $453.2 million or 23.4% during 2010. The decline in the covered loan portfolio is to be expected as there were no new acquisitions of loans subject to loss share agreements during 2010. The covered loan portfolio will continue to decline, through payoffs, charge-offs, termination or expiration of loss share coverage, unless First Financial acquires additional loans subject to loss share agreements in the future.

INVESTMENTS

First Financial’s investments at December 31, 2010 totaled $1.0 billion, a $436.1 million or 75.3% increase from the $579.1 million balance at December 31, 2009. The increase in the investment portfolio represents a redeployment of the Company’s liquidity position as loan demand was muted throughout the year. First Financial purchased primarily agency debentures and fixed and floating rate agency-backed mortgage backed securities (MBSs) utilizing the same discipline and portfolio management philosophy as with past investment purchases including, but not limited to, avoidance of material credit risk and geographic concentration risk within the MBSs. The investment portfolio, which is managed to minimize extension or maturity risk, provides a pool of assets eligible as a source of collateral for pledging to secure Federal, state and local depository funds, while also balancing overall asset/liability management objectives.

The other investments category in the Consolidated Balance Sheets reflects First Financial’s investment in the stock of the Federal Reserve Bank and the FHLB.

The majority of the investment portfolio is comprised of lower-risk investment securities, primarily treasury, government agency and agency residential MBSs. The December 31, 2010 investment securities portfolio included a net unrealized pre-tax gain of $15.2 million representing the difference between fair value and amortized cost. This compares with a net unrealized pre-tax gain of $16.5 million at December 31, 2009. The total investment portfolio represented 16.2% and 8.7% of total assets at December 31, 2010 and December 31, 2009, respectively.

Security debentures issued by the U.S. government, U.S. government agencies and corporations, primarily the Federal Home Loan Bank (FHLB), FHLMC, Federal National Mortgage Association (FNMA), and Federal Farm Credit Bank represented 11.8% and 7.0% of the investment portfolio at December 31, 2010, and 2009 respectively. All U.S. government agencies and corporations’ securities were classified as available-for-sale at December 31, 2010, and 2009. Due to the government guarantees, either expressed or implied, U.S. government agency and corporation obligations are considered to have a lower credit risk and high liquidity profile.

Investments in MBSs, including collateralized mortgage obligations (CMOs), represented 77.7% and 86.3% of the investment portfolio at December 31, 2010, and 2009, respectively. MBSs represent participations in pools of residential real estate loans, the principal and interest payments of which are passed through to the security investors. MBSs are subject to prepayment risk, particularly during periods of falling interest rates, and duration is prone to extend during periods of rising interest rates. Prepayments of the underlying residential real estate loans may shorten the lives of the securities, thereby affecting yields to maturity and market values. First Financial invests primarily in MBSs issued by U.S. government agencies and corporations, such as Government National Mortgage Association (GNMA), FHLMC, and FNMA. Such securities, because of government agency guarantees, are considered to have a low credit risk and high liquidity profile.

CMOs totaled $336.5 million at December 31, 2010, and $58.2 million at December 31, 2009, all of which were classified as available-for-sale. All CMOs held by First Financial are AAA rated by Standard & Poor’s Corporation or similar rating agencies, and First Financial does not own any interest-only securities, principal-only securities, or other securities considered high risk.

16 First Financial Bancorp 2010 Annual Report

Tax exempt securities of states, municipalities and other political subdivisions comprised only 1.7% and 4.5% of the investment portfolio at December 31, 2010, and 2009, respectively. The securities are diversified as to states and issuing authorities within states, thereby decreasing portfolio risk. First Financial continues to monitor the risk associated with this sector as we review the underlying ratings for possible downgrades. First Financial does not own any currently impaired state or other political subdivision securities and has not added to this component of the portfolio in more than five years.

Other securities totaled 1.0% and 2.0% of First Financial’s investment portfolio at December 31, 2010, and 2009, respectively, and were primarily comprised of taxable obligations of state and other political subdivisions, Community Reinvestment Act qualified funds, and other small holdings.

| Table 8 • Investment Securities |

| | | 2010 | | | 2009 | |

| (Dollars in thousands) | | Amount | | | Percent of Portfolio | | | Amount | | | Percent of Portfolio | |

| U.S. Treasuries | | $ | 13,959 | | | | 1.49 | % | | $ | 13,857 | | | | 2.83 | % |

| Securities of U.S. Government agencies and corporations | | | 105,985 | | | | 11.32 | % | | | 20,621 | | | | 4.21 | % |

| Mortgage-backed securities | | | 788,868 | | | | 84.23 | % | | | 422,408 | | | | 86.34 | % |

| Obligations of state and other political subdivisions | | | 17,153 | | | | 1.83 | % | | | 22,231 | | | | 4.54 | % |

| Other securities | | | 10,551 | | | | 1.13 | % | | | 10,200 | | | | 2.08 | % |

| Total | | $ | 936,516 | | | | 100.00 | % | | $ | 489,317 | | | | 100.00 | % |

The estimated maturities and weighted-average yields of the held-to-maturity and available-for-sale investment securities are shown in Table 9 – Investment Securities as of December 31, 2010. Tax-equivalent adjustments, using a 35.0% rate, have been made in calculating yields on tax-exempt obligations of state and other political subdivisions.

At December 31, 2010 and 2009, 98.1% and 96.3%, respectively, of investment securities were classified as available-for-sale. The available-for-sale investment securities are reported at their market value of $919.1 million at December 31, 2010 and $471.0 million at December 31, 2009. The market value of First Financial’s held-to-maturity investment securities portfolio exceeded the carrying value by $0.7 million and $0.5 million at December 31, 2010 and December 31, 2009, respectively. See Note 9 of the Notes to Consolidated Financial Statements for additional information.

First Financial adopted FASB ASC Topic 825-10, Financial Instruments, effective January 1, 2008. This statement permits the initial and subsequent measurement of many financial instruments and certain other assets and liabilities at fair value on an instrument-by-instrument, irrevocable basis. First Financial applied the fair value option to its equity securities of government sponsored entities (GSE), specifically 200,000 FHLMC perpetual preferred series V shares. Throughout 2009 and early in 2010, these securities were classified as trading investment securities in First Financial’s Consolidated Balance Sheets. The fair value accounting treatment discussed above requires First Financial to recognize in its income statement both the market value increases and decreases in future periods. The value of the FHLMC securities fluctuated moderately throughout 2009, resulting in a $0.1 million net realized gain for the twelve months ended December 31, 2009. First Financial sold all 200,000 FHLMC securities in the first quarter of 2010 for $0.2 million, resulting in a realized loss of less than $0.1 million.

First Financial held cash on deposit with the Federal Reserve of $141.7 million and $252.0 million at December 31, 2010 and 2009, respectively. Beginning in 2009 and during the first half of 2010, First Financial held cash on deposit with the Federal Reserve rather than investing excess cash overnight in federal funds sold when the Federal Reserve began paying interest on bank deposits. The increase in cash experienced throughout 2010 is primarily a result of the $967.4 million of cash received from the FDIC in the Irwin and Peoples acquisitions in the third quarter 2009, the muted loan demand experienced throughout most of 2010 and strong net deposit inflows. Beginning in the third quarter 2010, First Financial initiated strategies to redeploy a portion of its cash by investing in agency backed securities and prepaying $232 million of long term FHLB debt acquired during the Irwin and Peoples acquisitions. First Financial continually monitors its liquidity position as part of its enterprise risk management framework, specifically its asset/liability management process.

See Note 22 of the Notes to Consolidated Financial Statements for additional information on how First Financial determines the fair value of investment securities.

DERIVATIVES

The use of derivative instruments allows First Financial to meet the needs of its clients while managing the interest-rate risk associated with certain transactions. First Financial’s board of directors has authorized the use of certain derivative products, including interest rate caps, floors, and swaps. First Financial does not use derivatives for speculative purposes and currently does not have any derivatives that are not designated as hedges.

In accordance with FASB ASC Topic 815, Derivatives and Hedging, the accounting for changes in the fair value of derivatives depends on the intended use of the derivative and the resulting designation. Derivatives used to hedge the exposure to changes in the fair value of an asset, liability, or firm commitment attributable to a particular risk, such as interest rate risk, are considered fair value hedges. Derivatives used to hedge the exposure to variability in expected future cash flows, or other types of forecasted transactions, are considered cash flow hedges.

| Table 9 • Investment Securities As Of December 31, 2010 |

| | | Maturity | |

| | | Within one year | | | After one but within five years | | | After five but within ten years | | | After ten years | |

(Dollars in thousands) | | Amount | | | Yield(1) | | | Amount | | | Yield(1) | | | Amount | | | Yield(1) | | | Amount | | | Yield(1) | |

| Held-to-Maturity | | | | | | | | | | | | | | | | | | | | | | | | |

| U.S. Treasuries | | $ | 2,303 | | | | 1.85 | % | | $ | 11,656 | | | | 2.06 | % | | $ | 0 | | | | 0.00 | % | | $ | 0 | | | | 0.00 | % |

| Mortgage-backed securities | | | 5 | | | | 12.86 | % | | | 113 | | | | 4.38 | % | | | 0 | | | | 0.00 | % | | | 0 | | | | 0.00 | % |

| Obligations of state and other political subdivisions | | | 278 | | | | 6.06 | % | | | 1,915 | | | | 7.01 | % | | | 265 | | | | 7.53 | % | | | 871 | | | | 7.69 | % |

| Total | | $ | 2,586 | | | | 2.32 | % | | $ | 13,684 | | | | 2.77 | % | | $ | 265 | | | | 7.53 | % | | $ | 871 | | | | 7.69 | % |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Available-for-Sale | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Securities of other U.S. government agencies and corporations | | $ | 0 | | | | 0.00 | % | | $ | 100,729 | | | | 2.63 | % | | $ | 5,256 | | | | 5.50 | % | | $ | 0 | | | | 0.00 | % |

| Mortgage-backed securities | | | 41,489 | | | | 1.41 | % | | | 610,534 | | | | 2.66 | % | | | 125,836 | | | | 3.01 | % | | | 10,891 | | | | 3.86 | % |

| Obligations of state and other political subdivisions | | | 1,984 | | | | 7.28 | % | | | 8,016 | | | | 7.66 | % | | | 3,824 | | | | 6.91 | % | | | 0 | | | | 0.00 | % |

| Other securities | | | 127 | | | | 6.13 | % | | | 0 | | | | 0.00 | % | | | 0 | | | | 0.00 | % | | | 10,424 | | | | 6.30 | % |

| Total | | $ | 43,600 | | | | 1.68 | % | | $ | 719,279 | | | | 2.71 | % | | $ | 134,916 | | | | 3.22 | % | | $ | 21,315 | | | | 5.03 | % |

(1) Tax equivalent basis was calculated using a 35.00% tax rate and yields were based on amortized cost.

First Financial Bancorp 2010 Annual Report 17

Management’s Discussion And Analysis Of Financial Condition And Results Of Operations