UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORMN-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number:811-3618

BRIGHTHOUSE FUNDS TRUST II

(Exact name of registrant as specified in charter)

One Financial Center

Boston, MA 02111

(Address of principal executive offices)(Zip code)

| | |

| (Name and Address of Agent for Service) | | Copy to: |

| |

Michael Lawlor, Esq. -------------------------- c/o Brighthouse Investment Advisers, LLC One Financial Center Boston, MA 02111 | | Brian D. McCabe, Esq. ------------------------------- Ropes & Gray LLP Prudential Tower 800 Boylston Street Boston MA, 02199 |

Registrant’s telephone number, including area code:980-949-5130

Date of fiscal year end: December 31

Date of reporting period: December 31, 2018

1

Item 1: Report to Shareholders.

The following is a copy of the report transmitted to stockholders pursuant to Rule30e-1 under the Investment Company Act of 1940 (the “Act”):

2

Brighthouse Funds Trust II

Baillie Gifford International Stock Portfolio

Managed by Baillie Gifford Overseas Limited

Portfolio Manager Commentary*

PERFORMANCE

For the 12 months ended December 31, 2018, the Class A, B, and E shares of the Baillie Gifford International Stock Portfolio returned-17.01%,-17.19%, and-17.09%, respectively. The Portfolio’s benchmark, the MSCI All Country World (“ACWI”)ex-U.S. Index1, returned-14.20%.

MARKET ENVIRONMENT / CONDITIONS

2018 proved to be a turbulent year and one of the worst years for equity performance in a decade. Market weakness was widespread with most regions posting double digit declines. There was similarly indiscriminate write downs across all sectors and industries. Against this backdrop, the MSCI ACWIex-U.S. Index declined 14.20%. While it is often difficult to explain short-term swings in equity prices, the main reasons cited for the weakness over the year have tended to focus on factors such as an economic slowdown or threats to future growth from rising interest rates and trade wars, as opposed to specific issues at the corporate level.

Market confidence was fragile, with the first sharp fall in global stock prices in February. This coincided with the beginning in earnest of a trade war between the U.S. and China, with President Trump’s administration aiming an opening salvo at $60 billion worth of Chinese imports. The dispute moved to focus on the theft of intellectual property and the forced transfer of expertise from U.S. companies. Nervousness around what this might mean for global trade spilled into other markets, with sharpmid-year declines in emerging markets. European markets have also faced their share of woes with continued wrangling around Brexit (U.K. amendment to leave the European Union), weakness in the Italian economy and a disheartened electorate in France combining to weaken sentiment further.

PORTFOLIO REVIEW /PERIOD-END POSITIONING

The Portfolio underperformed its benchmark during 2018. As we would expect given our style of investing, performance was driven by the results of our stock picking approach as opposed to macro-economic considerations or asset allocation decisions. A number of holdings within the Portfolio made a significant contribution to relative performance, either negatively or positively.

ASOS (U.K.), the fast fashion retailer, was the largest detractor from relative performance. A profit warning in December saw a sharp decline in the ASOS share price. Issues at ASOS have centred on the company’s “Black Friday” strategy, where heavy discounting from competitors has proved a challenge whilst the company failed to realise the impact of the event in overseas markets such as Australia. Additionally, a strategic move to try to sell a narrower range of its own products proved unsuccessful, at a time when the company has been investing heavily in two new distribution centres in Atlanta and Berlin to drive growth. The company has revised down its guidance and margins are expected to be substantially impacted.

Naspers (South Africa) the media holdings company, invests in more than 100 companies but its largest holding is Tencent (in which it owns a 30% stake). Tencent (China) is an investment holding conglomerate, well known for online gaming and its WeChat social ecosystem. Chinese government gaming regulation and scrutiny of gaming addiction caused significant share price falls in Tencent over the year (which Naspers tends to move in line with). However, operationally, both companies have been performing well. Having had such negative pronouncements from the gaming regulator in the past, which passed without implication, our view currently is that Tencent is well placed to navigate the impact of any regulatory tightening. At year end, we continued to believe the long-term investment case remained strong for both companies. We took advantage of the short-term weakness in Tencent to buy a new holding for the Portfolio, which was funded by a partial reduction in Naspers.

On a more positive note, Edenred (France), the employee benefits vouchers business, has been executing on a transformation strategy focusing onde-risking its operational profile, which is starting to reap rewards and led to a sharp rise in the company’s share price. Gradual improvements in Brazil, which represents more than one third of revenues, are expected to sustain the recently accelerated earnings growth path. Ongoing developments in the digital payment world, where Edenred has an established foothold, open the doors to meaningful growth opportunities.

Constellation Software (Canada), a software company, was also amongst the strongest contributors. The company has reported strong earnings and growth results over the past twelve-months. Most recently, the company announced organic revenue growth was 5%year-on-year with the contribution of recurring revenue increasing to close to 70%. The company grows primarily through acquisitions, buying small software businesses that have a strong position in niche markets. Capital allocation discipline is notable with the founder Mark Leonard at the helm.

A number of new holdings were added to the Portfolio over the course of 2018. These included Spotify (Sweden), the online music streaming platform; HDFC (India), the largest mortgage lender in its domestic market; Tencent Music (China), the dominant music platform in China; and Danone (France), the world’s largest producer of organic foods. As discussed above, the Portfolio also took a holding in Tencent (China), the investment holding company. These new holdings were funded by sales made for fundamental stock-specific reasons such as that of Bureau Veritas (France), a testing and inspection company; Rakuten (Japan), thee-commerce company; and Baidu (China), an internet search provider.

The regional, sector, and industry positioning of the Portfolio are the product of such stock decisions made by the Portfolio managers rather than expressed views on international markets. At year end, the Portfolio remained relatively balanced at a regional level in comparison to the benchmark index, with an underweight to Japan being the most marked position at the close of the year in country terms.

BHFTII-1

Brighthouse Funds Trust II

Baillie Gifford International Stock Portfolio

Managed by Baillie Gifford Overseas Limited

Portfolio Manager Commentary*—(Continued)

At the sector level, deviations from the benchmark index remained more marked at year end, not changing significantly over the year. The Portfolio remained underweight in Health Care, Financials, Telecommunication Services, and Energy. At year end, the most significant overweights were the Industrials, Information Technology, and Consumer Discretionary sectors.

In industry terms, the most significant overweights for the Portfolio relative to the benchmark index at year end were in capital markets, internet & direct marketing retail, and machinery. We retained a significant underweight in oil, gas and consumable fuels, banks, and pharmaceuticals.

Jonathan Bates

Angus Franklin

Portfolio Managers

Baillie Gifford Overseas Limited

* This commentary may include statements that constitute “forward-looking statements” under the U.S. securities laws. Forward-looking statements include, among other things, projections, estimates, and information about possible or future results related to the Portfolio, market or regulatory developments. The views expressed above are not guarantees of future performance or economic results and involve certain risks, uncertainties and assumptions that could cause actual outcomes and results to differ materially from the views expressed herein. The views expressed above are subject to change at any time based upon economic, market, or other conditions and the subadvisory firm undertakes no obligation to update the views expressed herein. Any discussions of specific securities should not be considered a recommendation to buy or sell those securities. The views expressed above (including any forward-looking statement) may not be relied upon as investment advice or as an indication of the Portfolio’s trading intent. Information about the Portfolio’s holdings, asset allocation or country diversification is historical and is not an indication of future Portfolio composition, which may vary. Direct investment in any index is not possible. The performance of any index mentioned in this commentary has not been adjusted for ongoing management, distribution and operating expenses, and sales charges applicable to mutual fund investments. In addition, the returns do not reflect additional fees charged by separate accounts or variable insurance contracts that an investor in the Portfolio may pay. If these additional fees were reflected, performance would have been lower.

BHFTII-2

Brighthouse Funds Trust II

Baillie Gifford International Stock Portfolio

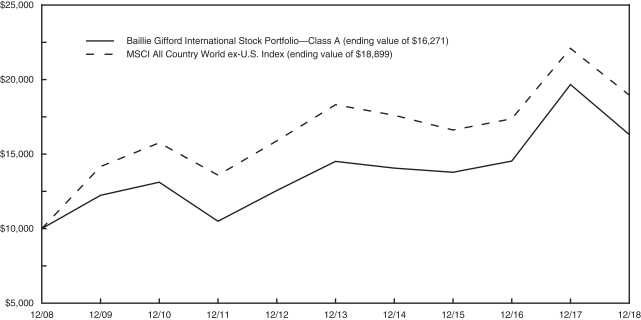

A $10,000 INVESTMENT COMPARED TO THE MSCI ALL COUNTRY WORLD EX-U.S. INDEX

AVERAGE ANNUAL RETURNS (%) (FOR THE YEAR ENDED DECEMBER 31, 2018)

| | | | | | | | | | | | |

| | | | |

| | | 1 Year | | | 5 Year | | | 10 Year | |

| Baillie Gifford International Stock Portfolio | | | | | | | | | | | | |

Class A | | | -17.01 | | | | 2.34 | | | | 4.99 | |

Class B | | | -17.19 | | | | 2.10 | | | | 4.72 | |

Class E | | | -17.09 | | | | 2.20 | | | | 4.84 | |

| MSCI All Country Worldex-U.S. Index | | | -14.20 | | | | 0.68 | | | | 6.57 | |

1 The MSCI All Country World ex-U.S. Index is an unmanaged free float-adjusted market capitalization index that is designed to measure equity market performance in the global developed and emerging markets, excluding the U.S. The Index returns shown above were calculated with net dividends: they reflect the reinvestment of dividends after the deduction of the maximum possible withholding taxes.

Portfolio performance is calculated including reinvestment of all income and capital gain distributions. Performance numbers are net of all Portfolio expenses but do not include any insurance, sales, separate account or administrative charges of variable annuity or life insurance contracts or any additional expenses that participants may bear relating to the operations of their plans. If these charges were included, the returns would be lower. The performance of any index referenced above has not been adjusted for ongoing management, distribution and operating expenses, and sales charges applicable to mutual fund investments. Direct investment in any index is not possible. The performance of Class A shares, as set forth in the line graph above, will differ from that of other classes because of the difference in expenses paid by policyholders investing in the different share classes.

This information represents past performance and is not indicative of future results. Investment return and principal value may fluctuate so that shares, upon redemption, may be worth more or less than the original cost.

PORTFOLIO COMPOSITION AS OF DECEMBER 31, 2018

Top Holdings

| | | | |

| | | % of

Net Assets | |

| Taiwan Semiconductor Manufacturing Co., Ltd. | | | 3.4 | |

| SAP SE | | | 2.7 | |

| MercadoLibre, Inc. | | | 2.7 | |

| AIA Group, Ltd. | | | 2.5 | |

| Rio Tinto plc | | | 2.4 | |

| Deutsche Boerse AG | | | 2.4 | |

| Samsung Electronics Co., Ltd. | | | 2.2 | |

| Nestle S.A. | | | 2.1 | |

| Fairfax Financial Holdings, Ltd. | | | 1.9 | |

| Edenred | | | 1.9 | |

Top Countries

| | | | |

| | | % of

Net Assets | |

| United Kingdom | | | 13.9 | |

| Japan | | | 11.5 | |

| Germany | | | 8.7 | |

| Switzerland | | | 5.5 | |

| Ireland | | | 5.0 | |

| France | | | 4.9 | |

| Canada | | | 4.3 | |

| Taiwan | | | 4.2 | |

| Hong Kong | | | 4.1 | |

| Sweden | | | 4.1 | |

BHFTII-3

Brighthouse Funds Trust II

Baillie Gifford International Stock Portfolio

Understanding Your Portfolio’s Expenses

Shareholder Expense Example

As a shareholder of the Portfolio, you incur ongoing costs, including management fees; distribution and service(12b-1) fees; and other Portfolio expenses. This example is intended to help you understand your ongoing costs (in dollars) (referred to as “expenses”) of investing in the Portfolio and compare these costs with the ongoing costs of investing in other mutual funds. The example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period, July 1, 2018 through December 31, 2018.

Actual Expenses

The first line for each share class of the Portfolio in the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested in the particular share class of the Portfolio, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second line for each share class of the Portfolio in the table below provides information about hypothetical account values and hypothetical expenses based on the Portfolio’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Portfolio’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Portfolio and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any fees or charges of your variable insurance product or any additional expenses that participants in certain eligible qualified plans may bear relating to the operations of their plan. Therefore, the second line for each share class in the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these other costs were included, your costs would have been higher.

| | | | | | | | | | | | | | | | | | |

Baillie Gifford International Stock Portfolio

| | | | Annualized

Expense

Ratio | | | Beginning

Account Value

July 1,

2018 | | | Ending

Account Value

December 31,

2018 | | | Expenses Paid

During Period**

July 1, 2018

to

December 31,

2018 | |

Class A (a) | | Actual | | | 0.71 | % | | $ | 1,000.00 | | | $ | 857.60 | | | $ | 3.32 | |

| | Hypothetical* | | | 0.71 | % | | $ | 1,000.00 | | | $ | 1,021.63 | | | $ | 3.62 | |

| | | | | |

Class B (a) | | Actual | | | 0.96 | % | | $ | 1,000.00 | | | $ | 857.00 | | | $ | 4.49 | |

| | Hypothetical* | | | 0.96 | % | | $ | 1,000.00 | | | $ | 1,020.37 | | | $ | 4.89 | |

| | | | | |

Class E (a) | | Actual | | | 0.86 | % | | $ | 1,000.00 | | | $ | 857.70 | | | $ | 4.03 | |

| | Hypothetical* | | | 0.86 | % | | $ | 1,000.00 | | | $ | 1,020.87 | | | $ | 4.38 | |

| * | Hypothetical assumes a rate of return of 5% per year before expenses. |

| ** | Expenses paid are equal to the Portfolio’s annualized expense ratio for the most recent six month period, as shown above, multiplied by the average account value over the period, multiplied by the number of days (184 days) in the most recent fiscal half-year, divided by 365 (to reflect theone-half year period). |

| (a) | The annualized expense ratio shown reflects the impact of the management fee waiver as described in Note 5 of the Notes to Financial Statements. |

BHFTII-4

Brighthouse Funds Trust II

Baillie Gifford International Stock Portfolio

Schedule of Investments as of December 31, 2018

Common Stocks—98.2% of Net Assets

| | | | | | | | |

| Security Description | | Shares | | | Value | |

|

| Argentina—2.7% | |

MercadoLibre, Inc. (a) | | | 155,633 | | | $ | 45,577,124 | |

| | | | | | | | |

|

| Australia—1.0% | |

Cochlear, Ltd. | | | 140,697 | | | | 17,096,483 | |

| | | | | | | | |

|

| Brazil—1.6% | |

Itau Unibanco Holding S.A. (ADR) | | | 1,853,662 | | | | 16,942,471 | |

Kroton Educacional S.A. | | | 4,164,500 | | | | 9,503,629 | |

| | | | | | | | |

| | | | | | | 26,446,100 | |

| | | | | | | | |

|

| Canada—4.3% | |

Constellation Software, Inc. | | | 44,429 | | | | 28,438,856 | |

Fairfax Financial Holdings, Ltd. | | | 74,426 | | | | 32,763,359 | |

Ritchie Bros. Auctioneers, Inc. (b) | | | 370,516 | | | | 12,123,283 | |

| | | | | | | | |

| | | | | | | 73,325,498 | |

| | | | | | | | |

|

| China—4.0% | |

Alibaba Group Holding, Ltd. (ADR) (a) (b) | | | 227,071 | | | | 31,124,622 | |

Tencent Holdings, Ltd. | | | 736,800 | | | | 29,206,035 | |

Tencent Music Entertainment Group (ADR) (a) (b) | | | 558,923 | | | | 7,388,962 | |

| | | | | | | | |

| | | | | | | 67,719,619 | |

| | | | | | | | |

|

| Denmark—2.5% | |

DSV A/S | | | 379,662 | | | | 25,034,829 | |

Novozymes A/S - B Shares | | | 372,104 | | | | 16,632,513 | |

| | | | | | | | |

| | | | | | | 41,667,342 | |

| | | | | | | | |

|

| Finland—2.4% | |

Kone Oyj - Class B | | | 558,025 | | | | 26,582,810 | |

Sampo Oyj - A Shares | | | 307,017 | | | | 13,496,822 | |

| | | | | | | | |

| | | | | | | 40,079,632 | |

| | | | | | | | |

|

| France—4.9% | |

Danone S.A. | | | 240,476 | | | | 16,948,612 | |

Edenred | | | 859,539 | | | | 31,508,269 | |

EssilorLuxottica S.A. | | | 121,889 | | | | 15,391,189 | |

Legrand S.A. | | | 331,017 | | | | 18,630,821 | |

| | | | | | | | |

| | | | | | | 82,478,891 | |

| | | | | | | | |

|

| Germany—8.7% | |

Brenntag AG | | | 229,696 | | | | 9,913,489 | |

Continental AG | | | 69,354 | | | | 9,590,153 | |

Deutsche Boerse AG | | | 333,728 | | | | 40,133,211 | |

MTU Aero Engines AG | | | 97,682 | | | | 17,742,118 | |

SAP SE | | | 459,355 | | | | 45,756,204 | |

Scout24 AG | | | 556,173 | | | | 25,597,936 | |

| | | | | | | | |

| | | | | | | 148,733,111 | |

| | | | | | | | |

|

| Hong Kong—4.1% | |

AIA Group, Ltd. | | | 5,262,200 | | | | 43,288,216 | |

Hong Kong Exchanges and Clearing, Ltd. | | | 948,000 | | | | 27,204,687 | |

| | | | | | | | |

| | | | | | | 70,492,903 | |

| | | | | | | | |

|

| India—1.8% | |

Housing Development Finance Corp., Ltd. | | | 1,109,992 | | | | 31,250,657 | |

| | | | | | | | |

|

| Ireland—5.0% | |

CRH plc | | | 779,090 | | | | 20,445,999 | |

James Hardie Industries plc | | | 838,564 | | | | 8,930,013 | |

Kingspan Group plc | | | 606,914 | | | | 25,994,443 | |

Ryanair Holdings plc (ADR) (a) | | | 417,048 | | | | 29,752,204 | |

| | | | | | | | |

| | | | | | | 85,122,659 | |

| | | | | | | | |

|

| Japan—11.5% | |

Denso Corp. | | | 408,500 | | | | 18,129,261 | |

FANUC Corp. | | | 83,500 | | | | 12,553,196 | |

Japan Exchange Group, Inc. | | | 1,894,800 | | | | 30,430,060 | |

Nidec Corp. | | | 197,200 | | | | 22,600,054 | |

Shimano, Inc. | | | 174,100 | | | | 24,750,766 | |

SMC Corp. | | | 80,300 | | | | 23,985,629 | |

Sony Corp. | | | 408,000 | | | | 19,648,013 | |

Sumitomo Mitsui Trust Holdings, Inc. | | | 585,300 | | | | 21,304,281 | |

Toyota Tsusho Corp. | | | 750,000 | | | | 22,058,095 | |

| | | | | | | | |

| | | | | | | 195,459,355 | |

| | | | | | | | |

|

| Netherlands—1.5% | |

Heineken Holding NV | | | 304,540 | | | | 25,631,201 | |

| | | | | | | | |

|

| Panama—1.1% | |

Copa Holdings S.A. - Class A | | | 242,804 | | | | 19,111,103 | |

| | | | | | | | |

|

| Peru—1.3% | |

Credicorp, Ltd. | | | 102,148 | | | | 22,643,147 | |

| | | | | | | | |

|

| Russia—0.6% | |

Magnit PJSC (GDR) | | | 854,138 | | | | 10,873,546 | |

| | | | | | | | |

|

| Singapore—1.6% | |

United Overseas Bank, Ltd. | | | 1,513,864 | | | | 27,134,190 | |

| | | | | | | | |

|

| South Africa—2.4% | |

Discovery, Ltd. | | | 1,702,346 | | | | 18,779,093 | |

Naspers, Ltd. - N Shares | | | 114,443 | | | | 22,732,658 | |

| | | | | | | | |

| | | | | | | 41,511,751 | |

| | | | | | | | |

|

| South Korea—3.0% | |

NAVER Corp. | | | 130,234 | | | | 14,190,006 | |

Samsung Electronics Co., Ltd. | | | 1,074,146 | | | | 37,166,173 | |

| | | | | | | | |

| | | | | | | 51,356,179 | |

| | | | | | | | |

|

| Spain—2.9% | |

Bankinter S.A. | | | 2,097,742 | | | | 16,765,775 | |

Grifols S.A. | | | 469,966 | | | | 12,275,643 | |

Industria de Diseno Textil S.A. | | | 790,927 | | | | 20,163,153 | |

| | | | | | | | |

| | | | | | | 49,204,571 | |

| | | | | | | | |

|

| Sweden—4.1% | |

Atlas Copco AB - B Shares | | | 1,173,440 | | | | 25,727,757 | |

Epiroc AB - Class B (a) | | | 2,067,087 | | | | 18,503,294 | |

See accompanying notes to financial statements.

BHFTII-5

Brighthouse Funds Trust II

Baillie Gifford International Stock Portfolio

Schedule of Investments as of December 31, 2018

Common Stocks—(Continued)

| | | | | | | | |

| Security Description | |

Shares | | | Value | |

|

| Sweden—(Continued) | |

Svenska Handelsbanken AB - A Shares (b) | | | 2,295,488 | | | $ | 25,428,716 | |

| | | | | | | | |

| | | | | | | 69,659,767 | |

| | | | | | | | |

|

| Switzerland—5.5% | |

Cie Financiere Richemont S.A. | | | 225,742 | | | | 14,507,859 | |

Credit Suisse Group AG (a) | | | 1,477,754 | | | | 16,285,060 | |

Nestle S.A. | | | 432,234 | | | | 35,140,990 | |

Panalpina Welttransport Holding AG (b) | | | 76,588 | | | | 10,192,032 | |

SGS S.A. | | | 7,859 | | | | 17,706,357 | |

| | | | | | | | |

| | | | | | | 93,832,298 | |

| | | | | | | | |

|

| Taiwan—4.2% | |

Hon Hai Precision Industry Co., Ltd. | | | 5,382,067 | | | | 12,422,462 | |

Taiwan Semiconductor Manufacturing Co., Ltd. | | | 8,020,000 | | | | 58,219,406 | |

| | | | | | | | |

| | | | | | | 70,641,868 | |

| | | | | | | | |

|

| United Kingdom—13.9% | |

ASOS plc (a) (b) | | | 299,662 | | | | 8,648,148 | |

boohoo Group plc (a) | | | 6,934,394 | | | | 14,205,122 | |

Burberry Group plc | | | 529,921 | | | | 11,658,854 | |

Experian plc | | | 1,111,686 | | | | 27,019,224 | |

Hargreaves Lansdown plc (b) | | | 1,126,766 | | | | 26,548,328 | |

Howden Joinery Group plc | | | 2,000,642 | | | | 11,064,734 | |

Just Eat plc (a) (b) | | | 3,003,763 | | | | 22,468,152 | |

Prudential plc | | | 1,485,688 | | | | 26,544,883 | |

Rio Tinto plc | | | 863,199 | | | | 41,158,081 | |

Rolls-Royce Holdings plc (a) | | | 773,191 | | | | 8,136,700 | |

St. James’s Place plc | | | 1,105,135 | | | | 13,241,127 | |

Unilever NV | | | 479,004 | | | | 26,026,673 | |

| | | | | | | | |

| | | | | | | 236,720,026 | |

| | | | | | | | |

|

| United States—1.6% | |

Pricesmart, Inc. (b) | | | 130,472 | | | | 7,710,895 | |

Spotify Technology S.A. (a) | | | 177,146 | | | | 20,106,071 | |

| | | | | | | | |

| | | | | | | 27,816,966 | |

| | | | | | | | |

Total Common Stocks

(Cost $1,505,827,225) | | | | | | | 1,671,585,987 | |

| | | | | | | | |

|

| Preferred Stock—0.3% | |

|

| Spain—0.3% | |

Grifols S.A. - Class B

(Cost $6,362,013) | | | 261,847 | | | | 4,827,692 | |

| | | | | | | | |

| Short-Term Investment—1.3% | |

| Security Description | |

Principal

Amount* | | | Value | |

|

| Repurchase Agreement—1.3% | |

Fixed Income Clearing Corp.

Repurchase Agreement dated 12/31/18 at 1.200%, due on 01/02/19 with a maturity value of $22,700,466; collateralized by U.S. Treasury Notes with rates ranging from 2.125% - 2.500%, maturity dates ranging from 03/31/24 - 05/15/24, and an aggregate market value of $23,153,469. | | | 22,698,953 | | | | 22,698,953 | |

| | | | | | | | |

Total Short-Term Investments

(Cost $22,698,953) | | | | | | | 22,698,953 | |

| | | | | | | | |

|

| Securities Lending Reinvestments (c)—6.4% | |

|

| Certificates of Deposit—0.1% | |

Banco Del Estado De Chile New York

2.820%, 1M LIBOR + 0.350%, 05/20/19 (d) | | | 1,000,000 | | | | 999,979 | |

Natixis New York

2.810%, 1M LIBOR + 0.370%, 02/14/19 (d) | | | 1,000,000 | | | | 1,000,187 | |

| | | | | | | | |

| | | | | | | 2,000,166 | |

| | | | | | | | |

|

| Commercial Paper—0.2% | |

HSBC Bank plc

2.842%, 1M LIBOR + 0.320%, 07/30/19 (d) | | | 1,000,000 | | | | 1,000,000 | |

ING Funding LLC

2.707%, 1M LIBOR + 0.320%, 02/08/19 (d) | | | 1,500,000 | | | | 1,500,139 | |

| | | | | | | | |

| | | | | | | 2,500,139 | |

| | | | | | | | |

|

| Repurchase Agreements—5.8% | |

Citigroup Global Markets, Ltd.

Repurchase Agreement dated 12/31/18 at 2.490%, due on 01/02/19 with a maturity value of $10,662,087; collateralized by U.S. Treasury Obligations with rates ranging from 0.375%- 1.875%, maturity dates ranging from 12/15/20 - 01/15/27, and an aggregate market value of $10,873,832. | | | 10,660,612 | | | | 10,660,612 | |

Repurchase Agreement dated 12/31/18 at 2.490%, due on 01/02/19 with a maturity value of $3,500,484; collateralized by U.S. Treasury Obligations with rates ranging from 1.625% - 2.875%, maturity dates ranging from 06/30/20 - 11/15/46, and an aggregate market value of $3,570,000. | | | 3,500,000 | | | | 3,500,000 | |

Deutsche Bank AG, London

Repurchase Agreement dated 12/31/18 at 2.750%, due on 01/02/19 with a maturity value of $10,001,528; collateralized by U.S. Treasury and Foreign Obligations with rates ranging from 1.000% - 2.590%, maturity dates ranging from 03/31/19 - 12/29/26, and an aggregate market value of $10,200,000. | | | 10,000,000 | | | | 10,000,000 | |

Deutsche Bank Securities, Inc.

Repurchase Agreement dated 12/31/18 at 3.200%, due on 01/02/19 with a maturity value of $8,685,588; collateralized by U.S. Treasury Obligations at 0.000%, maturity dates ranging from 08/15/30 - 08/15/39, and an aggregate market value of $8,857,725. | | | 8,684,044 | | | | 8,684,044 | |

See accompanying notes to financial statements.

BHFTII-6

Brighthouse Funds Trust II

Baillie Gifford International Stock Portfolio

Schedule of Investments as of December 31, 2018

Securities Lending Reinvestments (c)—(Continued)

| | | | | | | | |

| Security Description | |

Principal

Amount* | | | Value | |

|

| Repurchase Agreements—(Continued) | |

NBC Global Finance, Ltd.

Repurchase Agreement dated 12/31/18 at 2.560%, due on 01/02/19 with a maturity value of $5,500,782; collateralized by various Common Stock with an aggregate market value of $6,122,667. | | | 5,500,000 | | | $ | 5,500,000 | |

Repurchase Agreement dated 12/31/18 at 2.560%, due on 01/02/19 with a maturity value of $3,500,498; collateralized by various Common Stock with an aggregate market value of $3,896,243. | | | 3,500,000 | | | | 3,500,000 | |

Repurchase Agreement dated 12/31/18 at 2.560%, due on 01/02/19 with a maturity value of $14,001,991; collateralized by various Common Stock with an aggregate market value of $15,584,972. | | | 14,000,000 | | | | 14,000,000 | |

Nomura Securities International, Inc.

Repurchase Agreement dated 12/31/18 at 2.950%, due on 01/02/19 with a maturity value of $20,003,278; collateralized by U.S. Treasury Obligations with rates ranging from 0.000% - 6.500%, maturity dates ranging from 02/15/19 - 08/15/48, and an aggregate market value of $20,400,000. | | | 20,000,000 | | | | 20,000,000 | |

Societe Generale

Repurchase Agreement dated 12/31/18 at 2.530%, due on 01/02/19 with a maturity value of $3,800,534; collateralized by U.S. Treasury Obligations with rates ranging from 0.750% - 8.000%, maturity dates ranging from 09/30/19 - 08/15/46, and various Common Stock with an aggregate market value of $4,162,808. | | | 3,800,000 | | | | 3,800,000 | |

Repurchase Agreement dated 12/31/18 at 2.530%, due on 01/02/19 with a maturity value of $10,001,406; collateralized by U.S. Treasury Obligations with rates ranging from 0.750% - 8.000%, maturity dates ranging from 09/30/19 - 08/15/46, and various Common Stock with an aggregate market value of $10,954,759. | | | 10,000,000 | | | | 10,000,000 | |

Repurchase Agreement dated 12/31/18 at 2.530%, due on 01/02/19 with a maturity value of $7,501,054; collateralized by U.S. Treasury Obligations with rates ranging from 0.750% - 8.000%, maturity dates ranging from 09/30/19 - 08/15/46, and various Common Stock with an aggregate market value of $8,216,069. | | | 7,500,000 | | | | 7,500,000 | |

Repurchase Agreement dated 12/31/18 at 2.560%, due on 01/07/19 with a maturity value of $1,000,498; collateralized by U.S. Treasury Obligations with rates ranging from 0.750% - 8.000%, maturity dates ranging from 09/30/19 - 08/15/46, and various Common Stock with an aggregate market value of $1,095,476. | | | 1,000,000 | | | | 1,000,000 | |

Repurchase Agreement dated 12/31/18 at 2.560%, due on 01/07/19 with a maturity value of $500,249; collateralized by U.S. Treasury Obligations with rates ranging from 0.750% - 8.000%, maturity dates ranging from 09/30/19 - 08/15/46, and various Common Stock with an aggregate market value of $547,738. | | | 500,000 | | | | 500,000 | |

| | | | | | | | |

| | | | | | | 98,644,656 | |

| | | | | | | | |

|

| Time Deposit—0.3% | |

Royal Bank of Canada

2.420%, 01/02/19 | | | 5,000,000 | | | | 5,000,000 | |

| | | | | | | | |

Total Securities Lending Reinvestments

(Cost $108,144,656) | | | | | | | 108,144,961 | |

| | | | | | | | |

Total Investments—106.2%

(Cost $1,643,032,847) | | | | | | | 1,807,257,593 | |

Other assets and liabilities (net)—(6.2)% | | | | | | | (105,663,916 | ) |

| | | | | | | | |

| Net Assets—100.0% | | | | | | $ | 1,701,593,677 | |

| | | | | | | | |

| | | | |

| * | | Principal amount stated in U.S. dollars unless otherwise noted. |

| (a) | | Non-income producing security. |

| (b) | | All or a portion of the security was held on loan. As of December 31, 2018, the market value of securities loaned was $106,751,656 and the collateral received consisted of cash in the amount of $108,144,656 andnon-cash collateral with a value of $3,088,187. The cash collateral investments are disclosed in the Schedule of Investments and categorized as Securities Lending Reinvestments. Thenon-cash collateral received consists of U.S. government securities that are held in safe-keeping by the lending agent, or a third-party custodian, and cannot be sold or repledged by the Portfolio. As such, this non-cash collateral is excluded from the Statement of Assets and Liabilities. |

| (c) | | Represents investment of cash collateral received from securities on loan as of December 31, 2018. |

| (d) | | Variable or floating rate security. The stated rate represents the rate at December 31, 2018. Maturity date shown for callable securities reflects the earliest possible call date. For securities based on a published reference index and spread, the index and spread are indicated in the description above. For certain variable rate securities, the coupon rate is determined by the issuer/agent based on current market conditions. For certain asset- and mortgage-backed securities, the coupon rate may fluctuate based on changes of the underlying collateral or prepayments of principal. These securities do not indicate a reference index and spread in their description above. |

| (ADR)— | | American Depositary Receipt |

| (GDR)— | | Global Depositary Receipt |

| (LIBOR)— | | London Interbank Offered Rate |

| | | | |

Ten Largest Industries as of December 31, 2018 (Unaudited) | | % of

Net Assets | |

Capital Markets | | | 9.0 | |

Insurance | | | 7.9 | |

Banks | | | 7.6 | |

Internet & Direct Marketing Retail | | | 7.2 | |

Machinery | | | 6.3 | |

Software | | | 4.4 | |

Interactive Media & Services | | | 4.1 | |

Semiconductors & Semiconductor Equipment | | | 3.4 | |

Food Products | | | 3.1 | |

Airlines | | | 2.9 | |

See accompanying notes to financial statements.

BHFTII-7

Brighthouse Funds Trust II

Baillie Gifford International Stock Portfolio

Schedule of Investments as of December 31, 2018

Fair Value Hierarchy

Accounting principles generally accepted in the United States of America (“GAAP”) define fair market value as the price that the Portfolio would receive to sell an asset or pay to transfer a liability in an orderly transaction between market participants at the measurement date. It establishes a fair value hierarchy that prioritizes inputs to valuation methods and requires disclosure of the fair value hierarchy, separately for each major category of assets and liabilities, that segregates fair value measurements into three levels. Levels 1, 2 and 3 of the fair value hierarchy are defined as follows:

Level 1 - unadjusted quoted prices in active markets for identical investments

Level 2 - other significant observable inputs (including, but not limited to, quoted prices for similar assets or liabilities in markets that are either active or inactive; inputs other than quoted prices that are observable such as interest rates, yield curves, volatilities, prepayment speeds, loss severities, credit risks, default rates, or other market corroborated inputs)

Level 3 - significant unobservable inputs based on the best information available in the circumstances, to the extent observable inputs are unavailable (including the Portfolio’s own assumptions used in determining the fair value of investments and derivative financial instruments)

The inputs or methodologies used for valuing investments are not necessarily an indication of the risk associated with investing in them. Changes to the inputs or methodologies used may result in transfers between levels. A reconciliation of Level 3 securities, if any, will be disclosed following the fair value hierarchy table. For more information about the Portfolio’s policy regarding the valuation of investments, please refer to the Notes to Financial Statements.

The following table summarizes the fair value hierarchy of the Portfolio’s investments as of December 31, 2018:

| | | | | | | | | | | | | | | | |

| Description | | Level 1 | | | Level 2 | | | Level 3 | | | Total | |

| Common Stocks | |

Argentina | | $ | 45,577,124 | | | $ | — | | | $ | — | | | $ | 45,577,124 | |

Australia | | | — | | | | 17,096,483 | | | | — | | | | 17,096,483 | |

Brazil | | | 16,942,471 | | | | 9,503,629 | | | | — | | | | 26,446,100 | |

Canada | | | 73,325,498 | | | | — | | | | — | | | | 73,325,498 | |

China | | | 38,513,584 | | | | 29,206,035 | | | | — | | | | 67,719,619 | |

Denmark | | | — | | | | 41,667,342 | | | | — | | | | 41,667,342 | |

Finland | | | — | | | | 40,079,632 | | | | — | | | | 40,079,632 | |

France | | | — | | | | 82,478,891 | | | | — | | | | 82,478,891 | |

Germany | | | — | | | | 148,733,111 | | | | — | | | | 148,733,111 | |

Hong Kong | | | — | | | | 70,492,903 | | | | — | | | | 70,492,903 | |

India | | | — | | | | 31,250,657 | | | | — | | | | 31,250,657 | |

Ireland | | | 29,752,204 | | | | 55,370,455 | | | | — | | | | 85,122,659 | |

Japan | | | — | | | | 195,459,355 | | | | — | | | | 195,459,355 | |

Netherlands | | | — | | | | 25,631,201 | | | | — | | | | 25,631,201 | |

Panama | | | 19,111,103 | | | | — | | | | — | | | | 19,111,103 | |

Peru | | | 22,643,147 | | | | — | | | | — | | | | 22,643,147 | |

Russia | | | — | | | | 10,873,546 | | | | — | | | | 10,873,546 | |

Singapore | | | — | | | | 27,134,190 | | | | — | | | | 27,134,190 | |

South Africa | | | — | | | | 41,511,751 | | | | — | | | | 41,511,751 | |

South Korea | | | — | | | | 51,356,179 | | | | — | | | | 51,356,179 | |

Spain | | | — | | | | 49,204,571 | | | | — | | | | 49,204,571 | |

Sweden | | | — | | | | 69,659,767 | | | | — | | | | 69,659,767 | |

Switzerland | | | — | | | | 93,832,298 | | | | — | | | | 93,832,298 | |

Taiwan | | | — | | | | 70,641,868 | | | | — | | | | 70,641,868 | |

United Kingdom | | | — | | | | 236,720,026 | | | | — | | | | 236,720,026 | |

United States | | | 27,816,966 | | | | — | | | | — | | | | 27,816,966 | |

Total Common Stocks | | | 273,682,097 | | | | 1,397,903,890 | | | | — | | | | 1,671,585,987 | |

Total Preferred Stock* | | | — | | | | 4,827,692 | | | | — | | | | 4,827,692 | |

Total Short-Term Investment* | | | — | | | | 22,698,953 | | | | — | | | | 22,698,953 | |

Total Securities Lending Reinvestments* | | | — | | | | 108,144,961 | | | | — | | | | 108,144,961 | |

Total Investments | | $ | 273,682,097 | | | $ | 1,533,575,496 | | | $ | — | | | $ | 1,807,257,593 | |

| | | | | | | | | | | | | | | | | |

Collateral for Securities Loaned (Liability) | | $ | — | | | $ | (108,144,656 | ) | | $ | — | | | $ | (108,144,656 | ) |

| | | | |

| * | | See Schedule of Investments for additional detailed categorizations. |

See accompanying notes to financial statements.

BHFTII-8

Brighthouse Funds Trust II

Baillie Gifford International Stock Portfolio

Statement of Assets and Liabilities

December 31, 2018

| | | | |

Assets | |

Investments at value (a) (b) | | $ | 1,807,257,593 | |

Cash denominated in foreign currencies (c) | | | 716,305 | |

Receivable for: | |

Investments sold | | | 39,422 | |

Fund shares sold | | | 588,759 | |

Dividends and interest | | | 3,035,936 | |

Prepaid expenses | | | 5,250 | |

| | | | |

Total Assets | | | 1,811,643,265 | |

Liabilities | |

Collateral for securities loaned | | | 108,144,656 | |

Payables for: | |

Fund shares redeemed | | | 128,903 | |

Accrued Expenses: | |

Management fees | | | 990,233 | |

Distribution and service fees | | | 61,882 | |

Deferred trustees’ fees | | �� | 138,370 | |

Other expenses | | | 585,544 | |

| | | | |

Total Liabilities | | | 110,049,588 | |

| | | | |

Net Assets | | $ | 1,701,593,677 | |

| | | | |

Net Assets Consist of: | |

Paid in surplus | | $ | 1,406,018,918 | |

Distributable earnings (Accumulated losses) | | | 295,574,759 | |

| | | | |

Net Assets | | $ | 1,701,593,677 | |

| | | | |

Net Assets | |

Class A | | $ | 1,407,777,427 | |

Class B | | | 277,596,456 | |

Class E | | | 16,219,794 | |

Capital Shares Outstanding* | |

Class A | | | 127,690,302 | |

Class B | | | 25,589,404 | |

Class E | | | 1,486,833 | |

Net Asset Value, Offering Price and Redemption Price Per Share | |

Class A | | $ | 11.02 | |

Class B | | | 10.85 | |

Class E | | | 10.91 | |

| | | | |

| * | | The Portfolio is authorized to issue an unlimited number of shares. |

| (a) | | Identified cost of investments was $1,643,032,847. |

| (b) | | Includes securities loaned at value of $106,751,656. |

| (c) | | Identified cost of cash denominated in foreign currencies was $711,314. |

Statement of Operations

Year Ended December 31, 2018

| | | | |

Investment Income | |

Dividends (a) | | $ | 37,062,613 | |

Interest | | | 148,267 | |

Securities lending income | | | 317,442 | |

| | | | |

Total investment income | | | 37,528,322 | |

Expenses | |

Management fees | | | 14,766,331 | |

Administration fees | | | 67,179 | |

Custodian and accounting fees | | | 525,985 | |

Distribution and service fees—Class B | | | 824,654 | |

Distribution and service fees—Class E | | | 28,920 | |

Audit and tax services | | | 55,145 | |

Legal | | | 45,317 | |

Trustees’ fees and expenses | | | 33,732 | |

Shareholder reporting | | | 108,621 | |

Insurance | | | 12,210 | |

Miscellaneous | | | 133,886 | |

| | | | |

Total expenses | | | 16,601,980 | |

Less management fee waiver | | | (2,298,266 | ) |

| | | | |

Net expenses | | | 14,303,714 | |

| | | | |

Net Investment Income | | | 23,224,608 | |

| | | | |

Net Realized and Unrealized Gain (Loss) | |

| Net realized gain (loss) on: | |

Investments | | | 111,160,399 | |

Foreign currency transactions | | | (761,365 | ) |

| | | | |

Net realized gain | | | 110,399,034 | |

| | | | |

| Net change in unrealized depreciation on: | |

Investments | | | (473,003,808 | ) |

Foreign currency transactions | | | (122,236 | ) |

| | | | |

Net change in unrealized depreciation | | | (473,126,044 | ) |

| | | | |

Net realized and unrealized loss | | | (362,727,010 | ) |

| | | | |

Net Decrease in Net Assets From Operations | | $ | (339,502,402 | ) |

| | | | |

| | | | |

| (a) | | Net of foreign withholding taxes of $3,918,483. |

See accompanying notes to financial statements.

BHFTII-9

Brighthouse Funds Trust II

Baillie Gifford International Stock Portfolio

Statements of Changes in Net Assets

| | | | | | | | |

| | | Year Ended

December 31,

2018 | | | Year Ended

December 31,

2017 | |

Increase (Decrease) in Net Assets: | |

From Operations | |

Net investment income | | $ | 23,224,608 | | | $ | 21,464,894 | |

Net realized gain | | | 110,399,034 | | | | 109,990,740 | |

Net change in unrealized appreciation (depreciation) | | | (473,126,044 | ) | | | 407,661,229 | |

| | | | | | | | |

Increase (decrease) in net assets from operations | | | (339,502,402 | ) | | | 539,116,863 | |

| | | | | | | | |

From Distributions to Shareholders (a) | |

Class A | | | (18,443,225 | ) | | | (17,587,214 | ) |

Class B | | | (3,023,120 | ) | | | (3,469,294 | ) |

Class E | | | (196,972 | ) | | | (232,526 | ) |

| | | | | | | | |

Total distributions | | | (21,663,317 | ) | | | (21,289,034 | ) |

| | | | | | | | |

Increase (decrease) in net assets from capital share transactions | | | 214,440,920 | | | | (321,838,239 | ) |

| | | | | | | | |

Total increase (decrease) in net assets | | | (146,724,799 | ) | | | 195,989,590 | |

|

Net Assets | |

Beginning of period | | | 1,848,318,476 | | | | 1,652,328,886 | |

| | | | | | | | |

End of period | | $ | 1,701,593,677 | | | $ | 1,848,318,476 | (b) |

| | | | | | | | |

Other Information:

Capital Shares

Transactions in capital shares were as follows:

| | | | | | | | | | | | | | | | |

| | | Year Ended

December 31, 2018 | | | Year Ended

December 31, 2017 | |

| | | Shares | | | Value | | | Shares | | | Value | |

Class A | |

Sales | | | 23,146,832 | | | $ | 301,855,134 | | | | 431,646 | | | $ | 5,060,048 | |

Reinvestments | | | 1,382,551 | | | | 18,443,225 | | | | 1,487,920 | | | | 17,587,214 | |

Redemptions | | | (6,247,029 | ) | | | (85,040,301 | ) | | | (23,217,031 | ) | | | (280,691,731 | ) |

| | | | | | | | | | | | | | | | |

Net increase (decrease) | | | 18,282,354 | | | $ | 235,258,058 | | | | (21,297,465 | ) | | $ | (258,044,469 | ) |

| | | | | | | | | | | | | | | | |

Class B | |

Sales | | | 2,251,320 | | | $ | 28,354,279 | | | | 967,341 | | | $ | 11,333,315 | |

Reinvestments | | | 230,070 | | | | 3,023,120 | | | | 297,794 | | | | 3,469,294 | |

Redemptions | | | (3,877,975 | ) | | | (50,053,323 | ) | | | (6,445,066 | ) | | | (75,960,334 | ) |

| | | | | | | | | | | | | | | | |

Net decrease | | | (1,396,585 | ) | | $ | (18,675,924 | ) | | | (5,179,931 | ) | | $ | (61,157,725 | ) |

| | | | | | | | | | | | | | | | |

Class E | |

Sales | | | 155,694 | | | $ | 1,929,102 | | | | 85,936 | | | $ | 979,935 | |

Reinvestments | | | 14,911 | | | | 196,972 | | | | 19,874 | | | | 232,526 | |

Redemptions | | | (328,351 | ) | | | (4,267,288 | ) | | | (324,586 | ) | | | (3,848,506 | ) |

| | | | | | | | | | | | | | | | |

Net decrease | | | (157,746 | ) | | $ | (2,141,214 | ) | | | (218,776 | ) | | $ | (2,636,045 | ) |

| | | | | | | | | | | | | | | | |

Increase (decrease) derived from capital shares transactions | | | | | | $ | 214,440,920 | | | | | | | $ | (321,838,239 | ) |

| | | | | | | | | | | | | | | | |

| | | | |

| (a) | | Distributions from net investment income and realized gains are no longer required to be separately disclosed. The presentation for the year ended December 31, 2018 has been adjusted for this change (See Note 8). At December 31, 2017 the distributions were from net investment income. |

| (b) | | As part of the update in (a), it is also no longer required to disclose the Undistributed net investment income (Accumulated losses) which was $21,306,719 as of December 31, 2017. |

See accompanying notes to financial statements.

BHFTII-10

Brighthouse Funds Trust II

Baillie Gifford International Stock Portfolio

Financial Highlights

| | | | | | | | | | | | | | | | | | | | |

| Selected per share data | |

| | | Class A | |

| | | Year Ended December 31, | |

| | | 2018 | | | 2017 | | | 2016 | | | 2015 | | | 2014 | |

Net Asset Value, Beginning of Period | | $ | 13.43 | | | $ | 10.06 | | | $ | 9.71 | | | $ | 10.07 | | | $ | 10.54 | |

| | | | | | | | | | | | | | | | | | | | |

Income (Loss) from Investment Operations | |

Net investment income (a) | | | 0.16 | | | | 0.15 | | | | 0.15 | (b) | | | 0.16 | | | | 0.16 | |

Net realized and unrealized gain (loss) | | | (2.42 | ) | | | 3.37 | | | | 0.36 | | | | (0.34 | ) | | | (0.48 | ) |

| | | | | | | | | | | | | | | | | | | | |

Total income (loss) from investment operations | | | (2.26 | ) | | | 3.52 | | | | 0.51 | | | | (0.18 | ) | | | (0.32 | ) |

| | | | | | | | | | | | | | | | | | | | |

Less Distributions | |

Distributions from net investment income | | | (0.15 | ) | | | (0.15 | ) | | | (0.16 | ) | | | (0.18 | ) | | | (0.15 | ) |

| | | | | | | | | | | | | | | | | | | | |

Total distributions | | | (0.15 | ) | | | (0.15 | ) | | | (0.16 | ) | | | (0.18 | ) | | | (0.15 | ) |

| | | | | | | | | | | | | | | | | | | | |

Net Asset Value, End of Period | | $ | 11.02 | | | $ | 13.43 | | | $ | 10.06 | | | $ | 9.71 | | | $ | 10.07 | |

| | | | | | | | | | | | | | | | | | | | |

Total Return (%) (c) | | | (17.01 | ) | | | 35.15 | | | | 5.38 | | | | (1.97 | ) | | | (3.10 | ) |

|

Ratios/Supplemental Data | |

Gross ratio of expenses to average net assets (%) | | | 0.85 | | | | 0.85 | | | | 0.85 | | | | 0.87 | | | | 0.87 | |

Net ratio of expenses to average net assets (%) (d) | | | 0.72 | | | | 0.73 | | | | 0.73 | | | | 0.74 | | | | 0.75 | |

Ratio of net investment income to average net assets (%) | | | 1.28 | | | | 1.24 | | | | 1.49 | (b) | | | 1.56 | | | | 1.58 | |

Portfolio turnover rate (%) | | | 23 | | | | 8 | | | | 11 | | | | 12 | | | | 8 | |

Net assets, end of period (in millions) | | $ | 1,407.8 | | | $ | 1,469.7 | | | $ | 1,315.2 | | | $ | 1,361.8 | | | $ | 1,490.0 | |

| |

| | | Class B | |

| | | Year Ended December 31, | |

| | | 2018 | | | 2017 | | | 2016 | | | 2015 | | | 2014 | |

Net Asset Value, Beginning of Period | | $ | 13.22 | | | $ | 9.90 | | | $ | 9.56 | | | $ | 9.91 | | | $ | 10.38 | |

| | | | | | | | | | | | | | | | | | | | |

Income (Loss) from Investment Operations | |

Net investment income (a) | | | 0.14 | | | | 0.12 | | | | 0.12 | (b) | | | 0.13 | | | | 0.14 | |

Net realized and unrealized gain (loss) | | | (2.39 | ) | | | 3.32 | | | | 0.35 | | | | (0.33 | ) | | | (0.48 | ) |

| | | | | | | | | | | | | | | | | | | | |

Total income (loss) from investment operations | | | (2.25 | ) | | | 3.44 | | | | 0.47 | | | | (0.20 | ) | | | (0.34 | ) |

| | | | | | | | | | | | | | | | | | | | |

Less Distributions | |

Distributions from net investment income | | | (0.12 | ) | | | (0.12 | ) | | | (0.13 | ) | | | (0.15 | ) | | | (0.13 | ) |

| | | | | | | | | | | | | | | | | | | | |

Total distributions | | | (0.12 | ) | | | (0.12 | ) | | | (0.13 | ) | | | (0.15 | ) | | | (0.13 | ) |

| | | | | | | | | | | | | | | | | | | | |

Net Asset Value, End of Period | | $ | 10.85 | | | $ | 13.22 | | | $ | 9.90 | | | $ | 9.56 | | | $ | 9.91 | |

| | | | | | | | | | | | | | | | | | | | |

Total Return (%) (c) | | | (17.19 | ) | | | 34.89 | | | | 5.05 | | | | (2.17 | ) | | | (3.34 | ) |

|

Ratios/Supplemental Data | |

Gross ratio of expenses to average net assets (%) | | | 1.10 | | | | 1.10 | | | | 1.10 | | | | 1.12 | | | | 1.12 | |

Net ratio of expenses to average net assets (%) (d) | | | 0.97 | | | | 0.98 | | | | 0.98 | | | | 0.99 | | | | 1.00 | |

Ratio of net investment income to average net assets (%) | | | 1.09 | | | | 0.99 | | | | 1.25 | (b) | | | 1.31 | | | | 1.32 | |

Portfolio turnover rate (%) | | | 23 | | | | 8 | | | | 11 | | | | 12 | | | | 8 | |

Net assets, end of period (in millions) | | $ | 277.6 | | | $ | 356.7 | | | $ | 318.6 | | | $ | 336.0 | | | $ | 387.3 | |

Please see following page for Financial Highlights footnote legend.

See accompanying notes to financial statements.

BHFTII-11

Brighthouse Funds Trust II

Baillie Gifford International Stock Portfolio

Financial Highlights

| | | | | | | | | | | | | | | | | | | | |

| Selected per share data | |

| | | Class E | |

| | | Year Ended December 31, | |

| | | 2018 | | | 2017 | | | 2016 | | | 2015 | | | 2014 | |

Net Asset Value, Beginning of Period | | $ | 13.29 | | | $ | 9.96 | | | $ | 9.61 | | | $ | 9.97 | | | $ | 10.43 | |

| | | | | | | | | | | | | | | | | | | | |

Income (Loss) from Investment Operations | |

Net investment income (a) | | | 0.15 | | | | 0.13 | | | | 0.13 | (b) | | | 0.14 | | | | 0.15 | |

Net realized and unrealized gain (loss) | | | (2.40 | ) | | | 3.33 | | | | 0.36 | | | | (0.34 | ) | | | (0.48 | ) |

| | | | | | | | | | | | | | | | | | | | |

Total income (loss) from investment operations | | | (2.25 | ) | | | 3.46 | | | | 0.49 | | | | (0.20 | ) | | | (0.33 | ) |

| | | | | | | | | | | | | | | | | | | | |

Less Distributions | |

Distributions from net investment income | | | (0.13 | ) | | | (0.13 | ) | | | (0.14 | ) | | | (0.16 | ) | | | (0.13 | ) |

| | | | | | | | | | | | | | | | | | | | |

Total distributions | | | (0.13 | ) | | | (0.13 | ) | | | (0.14 | ) | | | (0.16 | ) | | | (0.13 | ) |

| | | | | | | | | | | | | | | | | | | | |

Net Asset Value, End of Period | | $ | 10.91 | | | $ | 13.29 | | | $ | 9.96 | | | $ | 9.61 | | | $ | 9.97 | |

| | | | | | | | | | | | | | | | | | | | |

Total Return (%) (c) | | | (17.09 | ) | | | 34.92 | | | | 5.24 | | | | (2.15 | ) | | | (3.19 | ) |

|

Ratios/Supplemental Data | |

Gross ratio of expenses to average net assets (%) | | | 1.00 | | | | 1.00 | | | | 1.00 | | | | 1.02 | | | | 1.02 | |

Net ratio of expenses to average net assets (%) (d) | | | 0.87 | | | | 0.88 | | | | 0.88 | | | | 0.89 | | | | 0.90 | |

Ratio of net investment income to average net assets (%) | | | 1.19 | | | | 1.08 | | | | 1.34 | (b) | | | 1.42 | | | | 1.43 | |

Portfolio turnover rate (%) | | | 23 | | | | 8 | | | | 11 | | | | 12 | | | | 8 | |

Net assets, end of period (in millions) | | $ | 16.2 | | | $ | 21.9 | | | $ | 18.6 | | | $ | 19.8 | | | $ | 22.8 | |

| | | | |

| (a) | | Per share amounts based on average shares outstanding during the period. |

| (b) | | Net investment income per share and the ratio of net investment income to average net assets include anon-recurring refund for overbilling of prior years’ custodianout-of-pocket fees which amounted to less than $0.01 per share and 0.05% of average net assets, respectively. |

| (c) | | Total return does not reflect any insurance, sales, separate account or administrative charges of variable annuity or life insurance contracts or any additional expenses that contract owners may bear under their variable contracts. If these charges were included, the returns would be lower. |

| (d) | | Includes the effects of management fee waivers (see Note 5 of the Notes to Financial Statements). |

See accompanying notes to financial statements.

BHFTII-12

Brighthouse Funds Trust II

Baillie Gifford International Stock Portfolio

Notes to Financial Statements—December 31, 2018

1. Organization

Brighthouse Funds Trust II (the “Trust”) is organized as a Delaware statutory trust and registered under the Investment Company Act of 1940, as amended (the “1940 Act”), as anopen-end management investment company. The Trust, which is managed by Brighthouse Investment Advisers, LLC (“Brighthouse Investment Advisers” or the “Adviser”), currently offers twenty-nine series, each of which operates as a distinct investment vehicle of the Trust. The series included in this report is Baillie Gifford International Stock Portfolio (the “Portfolio”), which is diversified. Shares of the Portfolio are not offered directly to the general public and are currently available only to separate accounts of insurance companies, including insurance companies affiliated with the Adviser (together, the “Insurance Companies”).

The Portfolio has registered and offers three classes of shares: Class A, B and E shares. Shares of each Class of the Portfolio represent an equal pro rata interest in the Portfolio and generally give the shareholder the same voting, dividend, liquidation, and other rights. Investment income, realized and unrealized capital gains and losses, the common expenses of the Portfolio, and certain Portfolio-level expense reductions, if any, are allocated on a pro rata basis to each Class based on the relative net assets of each Class to the net assets of the Portfolio. Each Class of shares differs in its respective distribution plan and such distribution expenses are allocated to the corresponding Class of shares.

2. Significant Accounting Policies

The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America (“GAAP”) requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities as of the date of the financial statements and the reported amounts of income and expenses during the reporting period. Actual results could differ from those estimates. In the preparation of these financial statements, management has evaluated events and transactions subsequent to December 31, 2018 through the date the financial statements were issued.

The Portfolio is an investment company and follows the accounting and reporting guidance of the Financial Accounting Standards Board (“FASB”) Accounting Standards Codification Topic946- Financial Services- Investment Companies. The following is a summary of significant accounting policies consistently followed by the Portfolio in the preparation of its financial statements.

Investment Valuation and Fair Value Measurements - The Portfolio values its portfolio investments for purposes of calculating its net asset value (“NAV”) using procedures approved by the Board of Trustees of the Trust (the “Board” or “Trustees”). Those procedures allow for a variety of methodologies to be used to value the Portfolio’s investments. The specific methodologies used for a particular investment may vary based on the market data available for a specific investment at the time the Portfolio calculates its NAV or based on other considerations. The procedures also permit a level of judgment to be used in the valuation process. The Portfolio follows the accounting and reporting guidance of FASB Accounting Standards Codification Topic820- Fair Value Measurement.

Domestic and foreign equity securities, such as common stock, exchange-traded funds, rights, warrants, and preferred stock, that are traded on a securities exchange on a valuation date are generally valued at their last quoted sale price or official closing price on the primary exchange for such security, or, if no sales occurred on that day, at the last reported bid price. Equity securities tradedover-the-counter (“OTC”) are generally valued at the last reported bid price. In the event of a major exchange closing during the trading day, the Adviser may use other market information obtained from quotation reporting systems, established market makers, or pricing services in valuing the securities. Valuation adjustments may be applied to certain foreign equity securities that are traded solely on foreign exchanges that close before the time as of which the Portfolio determines its NAV to account for the market movement between the close of the foreign exchanges and the time as of which the Portfolio determines its NAV. The Portfolio may use a systematic fair valuation model provided by a pricing service to value securities principally traded in these foreign markets in order to adjust for possible market movements or other changes that may occur between the close of the foreign exchanges and the time as of which the Portfolio determines its NAV. Foreign equity securities valued using these valuation adjustments are generally categorized as Level 2 within the fair value hierarchy. Equity securities that are actively traded, and have no valuation adjustments applied, are categorized as Level 1 within the fair value hierarchy. Other equity securities traded on inactive markets, or valued in reference to similar instruments traded on active markets, are generally categorized as Level 2 within the fair value hierarchy.

Investments in registeredopen-end management investment companies are valued at reported NAV per share on the valuation date and are categorized as Level 1 within the fair value hierarchy.

Debt securities, including corporate, convertible and municipal bonds and notes; obligations of the U.S. Treasury and U.S. government agencies; foreign sovereign issues; andnon-U.S. bonds, are generally valued on the basis of evaluated or composite bid quotations obtained from independent pricing services and/or brokers and dealers selected by the Adviser (each a “pricing service”), pursuant to the authorization of and subject to general oversight by the Board. Such pricing services may use matrix pricing, which considers observable inputs including, among other things, issuer details, maturity dates, interest rates, yield curves, rates of prepayment, credit risks/spreads, default rates, reported trades, broker-dealer quotes and quoted prices for similar assets. Short-term obligations with a

BHFTII-13

Brighthouse Funds Trust II

Baillie Gifford International Stock Portfolio

Notes to Financial Statements—December 31, 2018—(Continued)

remaining maturity of sixty days or less may be valued at amortized cost in the absence of market quotes, so long as the amortized cost value of such short-term debt instrument is approximately the same as the fair value of the instrument as determined without the use of amortized cost valuation. Floating rate loans are generally valued on the basis of an evaluated or composite average of aggregate bid and ask quotations supplied by brokers or dealers, as obtained from the pricing service. Securities that use similar valuation techniques and inputs as described above are generally categorized as Level 2 within the fair value hierarchy.

Foreign currency forward contracts are valued through an independent pricing service by interpolating between forward and spot currency rates in the London foreign exchange markets as of a designated hour on a valuation day. These contracts are generally categorized as Level 2 within the fair value hierarchy.

Options, whether on securities, indices, futures contracts, or otherwise, traded on exchanges are valued at the last sale price available as of the close of business on a valuation day or, if there is no such price available, at the last reported bid price. These types of options are categorized as Level 1 within the fair value hierarchy. Futures contracts that are traded on commodity exchanges are valued at their settlement prices established by the exchanges on which they are traded as of the close of such exchanges and are categorized as Level 1 within the fair value hierarchy.

Options, including options on swaps (“swaptions”), currencies, and futures contracts that are traded OTC are generally valued on the basis of interdealer bid and ask prices or prices provided by pricing service providers who use a series of techniques, including simulation pricing models, to determine the value of the contracts. The pricing models use inputs that are observed from actively quoted markets such as issuer details, indices, spreads, interest rates, yield curves, credit curves, measures of volatility and exchange rates. These contracts are generally categorized as Level 2 within the fair value hierarchy.

If no current market value quotation or other observable inputs are readily available or market value quotations are deemed to be unreliable for an investment, the fair value of the investment will be determined in accordance with procedures approved by, and under the general supervision of, the Board. In such a circumstance, the Board will be assisted in its responsibility to determine the fair value of an investment by the Valuation Committee (“Committee”) of Brighthouse Investment Advisers. The Committee provides general pricing oversight and fair value pricing determinations related to portfolio securities and meets on a regular basis to review reports relating to the valuation of the securities in the Portfolio. The Board has delegated to State Street Bank and Trust Company, the Trust’s custodian (“Custodian”), the responsibility for calculating the NAVs of the Trust’s Portfolios. The Committee is responsible for overseeing the calculation of the NAVs of the Portfolios by the custodian. The Committee also periodically reviews pricing services, including the pricing services providing fair value pricing for the Portfolio’s foreign securities, and is responsible for overseeing the correction of pricing errors and addressing other pricing issues that arise in the ordinary course of business, such as making real-time fair value determinations, as necessary.

No single standard for determining the fair value of an investment can be set forth because fair value depends upon the facts and circumstances with respect to each investment. Information relating to any relevant factors may be obtained by the Committee from any appropriate source, including the subadviser of the Portfolio, the custodian, a pricing service, market maker and/or broker for such security or the issuer. Appropriate methodologies for determining fair value under particular circumstances may include: matrix pricing, a discounted cash flow analysis, comparisons of securities with comparable characteristics, value based on multiples of earnings, discount from market price of similar marketable securities, or a combination of these and other methods.

Investment Transactions and Related Investment Income - Portfolio security transactions are recorded on the trade date. Dividend income is recorded on theex-dividend date or, for certain foreign securities, when notified. Interest income, which includes amortization of premium and accretion of discount on debt securities, is recorded on the accrual basis. Realized gains and losses on investments are determined on the identified cost basis, which is the same basis used for federal income tax purposes. Foreign income and foreign capital gains on some foreign securities may be subject to foreign taxes, which are accrued as applicable. These foreign taxes have been provided for in accordance with the Portfolio’s understanding of the applicable countries’ tax rules and rates.

Foreign Currency Translation -The books and records of the Portfolio are maintained in U.S. dollars. The values of securities, currencies, and other assets and liabilities denominated in currencies other than the U.S. dollar are translated into U.S. dollars based upon foreign exchange rates prevailing at the end of the period. Purchases and sales of investment securities, income, and expenses are translated on the respective dates of such transactions. Because the values of investment securities are translated at the foreign exchange rates prevailing at the end of the period, that portion of the results of operations arising from changes in exchange rates and that portion of the results of operations reflecting fluctuations arising from changes in market prices of the investment securities are not separated. Such fluctuations are included in the net realized and unrealized gain or loss on investments.

Net realized foreign exchange gains or losses arise from activity in forward foreign currency exchange contracts, sales of foreign currency, currency gains or losses realized between the trade and settlement dates on securities transactions, and the difference between the amounts of dividends, interest, and foreign withholding taxes recorded by the Portfolio and the U.S. dollar-equivalent of the amounts actually received or paid by the Portfolio. Net unrealized foreign exchange gains and losses arise from changes in the value of assets and liabilities, other than investment securities, resulting from changes in foreign exchange rates.

BHFTII-14

Brighthouse Funds Trust II

Baillie Gifford International Stock Portfolio

Notes to Financial Statements—December 31, 2018—(Continued)

Dividends and Distributions to Shareholders -The Portfolio records dividends and distributions on theex-dividend date. Net realized gains from securities transactions (if any) are generally distributed annually to shareholders. The timing and characterization of certain income and capital gains distributions are determined in accordance with federal tax regulations that may differ from GAAP. Permanent book and tax basis differences relating to shareholder distributions will result in reclassification between distributable earnings (accumulated losses) andpaid-in surplus.Book-tax differences are primarily due to adjustments to prior period accumulated balances. These adjustments have no impact on net assets or the results of operations.

Income Taxes -It is the Portfolio’s policy to comply with the requirements of the Internal Revenue Code of 1986, as amended, and regulations thereunder, applicable to regulated investment companies, and to distribute, with respect to each taxable year, all of its taxable income to shareholders. Therefore, no federal income tax provision is required. The Portfolio files U.S. federal tax returns. No income tax returns are currently under examination. The Portfolio’s federal tax returns for the prior three fiscal years remain subject to examination by the Internal Revenue Service. As of December 31, 2018, the Portfolio had no uncertain tax positions that would require financial statement recognition, or derecognition or disclosure.

Repurchase Agreements -The Portfolio may enter into repurchase agreements, under the terms of a Master Repurchase Agreement (“MRA”), with selected commercial banks and broker-dealers, under which the Portfolio acquires securities as collateral and agrees to resell the securities at an agreed-upon time and at an agreed-upon price. The Portfolio, through the Custodian or a subcustodian, under atri-party repurchase agreement, receives delivery of the underlying securities collateralizing any repurchase agreements. It is the Portfolio’s policy that the market value of the collateral be equal to at least 100% of the repurchase price in the case of a repurchase agreement ofone-day duration and equal to at least 102% of the repurchase price in the case of all other repurchase agreements. In the event of default or failure by a party to perform an obligation in connection with any repurchase transaction, the MRA gives thenon-defaulting party the right toset-off claims and to apply property held by it in connection with any repurchase transaction against obligations owed to it.

At December 31, 2018, the Portfolio had direct investments in repurchase agreements with a gross value of $22,698,953. Additionally, the Portfolio invested cash collateral for loans of portfolio securities in repurchase agreements with a gross value of $98,644,656. The combined value of all repurchase agreements is included as part of investments at value on the Statement of Assets and Liabilities. The value of the related collateral exceeded the value of the repurchase agreements at December 31, 2018.

Securities Lending - The Portfolio may lend its portfolio securities to certain qualified brokers who borrow securities in order to complete certain securities transactions. By lending its portfolio securities, the Portfolio attempts to increase its net investment income through the receipt of income on collateral held from securities on loan. Any gain or loss in the market price of the loaned securities that might occur and any interest earned or dividends declared during the term of the loan would accrue to the account of the Portfolio.

The Trust has entered into aNon-Custodial Securities Lending Agreement with JPMorgan Chase Bank, N.A. (the “Lending Agent”). Under the agreement, the Lending Agent is authorized to loan portfolio securities on the Portfolio’s behalf. In exchange, the Portfolio receives either cash or U.S. government securities as collateral against the loaned securities. The Portfolio receives collateral equal to at least 102% of the market value for loans secured by government securities or cash in the same currency as the loaned shares and 105% for all other loaned securities at each loan’s inception. Collateral representing at least 100% of the market value of the loaned securities is maintained for the duration of the loan. Any cash collateral received by the Portfolio is generally invested by the Lending Agent in short-term investments, which may include certificates of deposit, commercial paper, repurchase agreements, time deposits, master demand notes and money market funds. The market value of investments made with cash collateral received are disclosed in the Schedule of Investments and the valuation techniques are described in Note 2. If the market value of the collateral at the close of trading on a business day is less than 100% of the market value of the loaned securities at the close of trading on that day, the borrower is required to deliver, by the close of business on the following business day, an additional amount of collateral, so that the total amount of posted collateral is equal to at least 100% of the market value of all the loaned securities as of such preceding day. A portion of the income earned on the collateral is rebated to the borrower of the securities and the remainder is split between the Lending Agent and the Portfolio. On loans collateralized by U.S. government securities, a fee is received from the borrower and is allocated between the Portfolio and the Lending Agent.

Income received by the Portfolio in securities lending transactions during the year ended December 31, 2018 is reflected as securities lending income on the Statement of Operations. The values of any securities loaned by the Portfolio and the related collateral at December 31, 2018 are disclosed in the footnotes to the Schedule of Investments. The value of the related collateral received by the Portfolio exceeded the value of the securities out on loan at December 31, 2018.

The risks associated with lending portfolio securities include, but are not limited to, possible delays in receiving additional collateral or in the recovery of the loaned securities, possible loss of rights in the collateral should the borrower fail financially, as well as risk of loss in the value of the collateral or the value of the investments made with the collateral. The Lending Agent shall indemnify the Portfolio in the case of default of any securities borrower, subject to the terms of theNon-Custodial Securities Lending Agreement.

BHFTII-15

Brighthouse Funds Trust II

Baillie Gifford International Stock Portfolio

Notes to Financial Statements—December 31, 2018—(Continued)

All securities on loan are classified as Common Stocks in the Portfolio’s Schedule of Investments as of December 31, 2018, with a contractual maturity of overnight and continuous.

3. Certain Risks

In the normal course of business, the Portfolio invests in securities and enters into transactions where risks exist. Those risks include:

Market Risk:The value of securities held by the Portfolio may decline in response to certain events, including those directly involving the issuers whose securities are owned by the Portfolio; conditions affecting the general economy; overall market changes; local, regional or global political, social or economic instability; and currency, interest rate, and price fluctuations.

Credit and Counterparty Risk: The Portfolio may be exposed to counterparty risk, or the risk that an entity with which the Portfolio has unsettled or open transactions may default. The potential loss could exceed the value of the financial assets and liabilities recorded in the financial statements. Financial assets that potentially expose the Portfolio to credit and counterparty risk consist principally of cash due from counterparties and investments. The Portfolio manages counterparty risk by entering into agreements only with counterparties that it believes have the financial resources to honor their obligations and by monitoring the financial stability of those counterparties. The Adviser attempts to mitigate counterparty risk by (i) periodically assessing the creditworthiness of its trading partners, (ii) monitoring and/or limiting the amount of its net exposure to each individual counterparty based on its assessment, and (iii) requiring collateral from the counterparty for certain transactions. In order to preserve certain safeguards fornon-standard settlement trades, the Portfolio restricts its exposure to credit and counterparty losses by entering into master netting agreements (“Master Agreements”) with counterparties (approved brokers) with whom it undertakes a significant volume of transactions. Master Agreements govern the terms of certain transactions, and reduce the counterparty risk associated with relevant transactions by specifying credit protection mechanisms and providing standardization that improves legal certainty. Master Agreements can also help limit counterparty risk by specifying collateral posting arrangements atpre-arranged exposure levels.

Repurchase and reverse repurchase agreements are primarily executed under Global Master Repurchase Agreements (“GMRAs”) or Master Repurchase Agreements (“MRAs”), which provide the rights toset-off. Each repurchase and reverse repurchase agreement is initially collateralized at the transaction level. In the event of default, the total market value exposure will be offset against collateral exchanged to date, which would result in a net receivable/(payable) that would be due from/to the counterparty.

Foreign Investment Risk:The investments by the Portfolio in foreign securities may involve risks not present in domestic investments. Because securities may be denominated in foreign currencies, may require settlement in foreign currencies and may pay interest or dividends in foreign currencies, changes in the relationship of these foreign currencies to the U.S. dollar can significantly affect the value of the investments and earnings of the Portfolio. Foreign investments may also subject the Portfolio to foreign government exchange restrictions, expropriation, taxation or other political, social or economic developments, all of which could affect the market and/or credit risk of the investments. In addition to the risks described above, risks may arise from forward foreign currency contracts with respect to the potential inability of counterparties to meet the terms of their contracts.