PROSPECTUS

May 1, 2010

Madison Mosaic Income Trust

Government Fund (Ticker Symbol: MADTX)

Core Bond Fund (Ticker Symbol: MADBX)

The Securities and Exchange Commission has not approved or disapproved these

securities or passed upon the adequacy of this prospectus. Any representation to the

contrary is a criminal offense.

Madison Mosaic Funds ®

www.mosaicfunds.com

TABLE OF CONTENTS

Summary Data: Government Fund 1

Investment Objectives/Goals 1

Fees and Expenses 1

Portfolio Turnover 1

Principal Investment Strategies 2

Principal Risks 2

Risk/Return Bar Chart and Performance Table 2

Management 3

Purchase and Sale of Fund Shares 3

Tax Information 4

Payments to Broker-Dealers and Other Financial Intermediaries 4

Summary Data: Core Bond 5

Investment Objectives/Goals 5

Fees and Expenses 5

Portfolio Turnover 5

Principal Investment Strategies 6

Principal Risks 6

Risk/Return Bar Chart and Performance Table 7

Management 8

Purchase and Sale of Fund Shares 8

Tax Information 8

Payments to Broker-Dealers and Other Financial Intermediaries 8

Investment Objectives 9

Implementation of Investment Objectives 9

All Funds 9

Government Fund 10

Core Bond Fund 10

Risks 12

All Funds 12

Core Bond Fund 13

Portfolio Holdings 14

Management 14

Investment Adviser 14

Compensation 15

Pricing of Fund Shares 15

Shareholder Information 16

Purchase and Redemption Procedures 16

Dividends and Distributions 16

Frequent Purchases and Redemptions of Fund Shares 16

Taxes 18

Federal Taxes 18

State and Local Taxes 18

Taxability of Transactions 18

Certification of Tax Identification Number 18

Financial Highlights 19

SUMMARY DATA: GOVERNMENT FUND

Investment Objectives/Goals

The investment objective of the Government Fund is to receive income from bonds and to distribute that income to its investors as dividends.

Fees and Expenses

This table describes the fees and expenses that you may pay if you buy and hold shares of the Government Fund.

Shareholder Fees:

(fees paid directly from your investment)

| Maximum sales charge (load) | None |

| Redemption fee | None |

| Exchange fee | None |

Annual Fund Operating Expenses:

(expenses that you pay each year as a percentage of the value of your investment)

| Management fee | 0.40% |

| Distribution (12b-1) fees | None |

| Other expenses | 0.28% |

| Total annual fund operating expenses | 0.68% |

Example:

This example is intended to help you compare the cost of investing in the Government Fund with the cost of investing in other mutual funds.

The example assumes that you invest $10,000 in the Government Fund for the time periods indicated and then redeem all of your shares at the end of those periods. The example also assumes that your investment has a 5% return each year and that the Fund’s operating expenses remain the same. Although your actual costs may be higher or lower, based on these assumptions, your costs would be:

| 1 Year | 3 Years | 5 Years | 10 Years |

| $69 | $218 | $379 | $847 |

Portfolio Turnover

The Government Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover may indicate higher transaction costs and may result in higher taxes when Fund shares are held in a taxable account. These costs, which are not reflected in annual fund operating expenses or in the example, affect the Fund’s performance. During the most recent fiscal year, the Government Fund’s portfolio turnover rate was 38% of the average value of its portfolio.

1

Principal Investment Strategies

The Government Fund seeks to achieve its investment objective through diversified investments in bonds and other debt securities. The Fund invests only in investment grade U.S. Government securities and, which include a variety of securities issued or guaranteed by the U.S. Treasury and various agencies of the federal government. They also include securities issued by various instrumentalities that were established or sponsored by the U.S. Government and certain interests in these types of securities (e.g., mortgage-backed securities issued by Ginnie Mae and Fannie Mae). The Fund emphasizes the safety of principal and interest for its portfolio investments. The maturities of such investments may range from long-term (20 years or more) to short-term (less than 10 years).

Principal Risks

Interest Rate Risk. The share price of the Government Fund reflects the value of the bonds held by it. When interest rates or general demand for municipal securities change, the value of these bonds change. If the value of these bonds falls, the share price of the Fund will go down. What might cause bonds to lose value? One reason is because interest rates went up. When this happens, existing bonds that pay a lower rate become less attractive and their prices tend to go down. If the share price falls below the price you paid for your shares, you could lose money when you redeem your shares. The longer the maturity of any bond, the greater the effect will be on its price when interest rates change.

Call Risk. If a bond issuer “calls” a bond held by the Fund (i.e., pays it off at a specified price before it matures), the Fund could have to reinvest the proceeds at a lower interest rate. It may also experience a loss if the bond is called at a price lower than what the Fund paid for the bond.

Risk of Default. Although the Fund’s investment adviser monitors the condition of bond issuers, it is still possible that unexpected events could cause the issuer to be unable to pay either principal or interest on its bond. This could cause the bond to go into default and lose value. Some federal agency securities are not backed by the full faith and credit of the United States, so in the event of default, the Fund would have to look to the agency issuing the bond for ultimate repayment.

Tax-Related Risk. You can receive a taxable distribution of capital gain from the Fund. You may also owe taxes if you sell your shares at a price that is higher than the price you paid for them.

Mortgage-Backed Securities Risk. The Fund may own obligations backed by mortgages, such as those issued by Ginnie Mae and Fannie Mae. If the mortgage holders prepay them during a period of falling interest rates, the Fund could be exposed to prepayment risk. In that case, the Fund would have to reinvest the proceeds at a lower interest rate. The security itself may not increase in value with the corresponding drop in rates since the prepayment acts to shorten the maturity of the security.

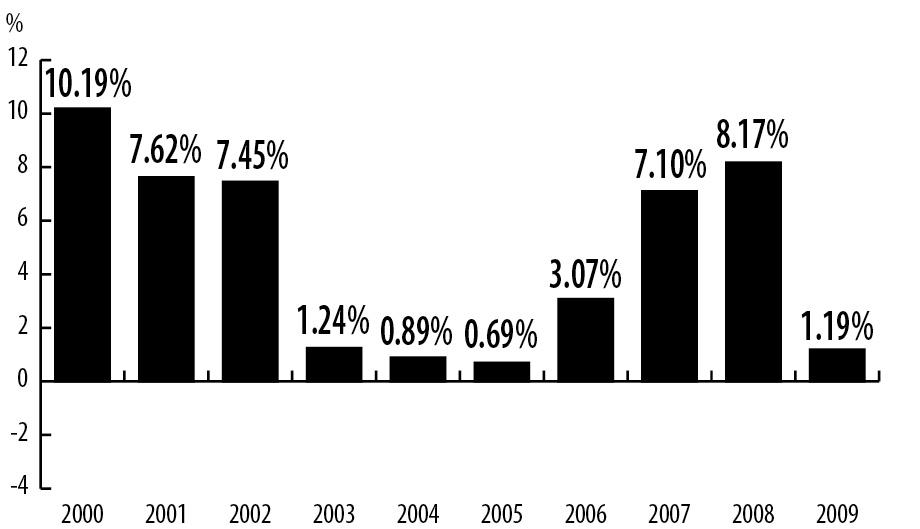

Risk/Return Bar Chart and Performance Table

The bar chart and table below demonstrate the variability of the Government Fund’s returns by showing changes in the Fund’s performance from year to year over a 10-year period. This information provides some indication of the risks of investing in the Fund. After the bar chart is a table that compares the Fund’s average annual total returns with those of a broad-based securities market index. Remember, however, that past performance (before and after taxes) does not necessarily indicate how the Fund will perform in the future.

2

Government Fund Calendar Year Returns

Highest/lowest quarterly results during the period shown in the bar chart were:

Highest: 4.91% (quarter ended September 30, 2001)

Lowest: -1.79% (quarter ended June 30, 2004)

Government Fund Average Annual Total Returns (for the period ended December 31, 2009) | |||

| One Year | Five Years | Ten Years | |

| Return before taxes | 1.19% | 4.00% | 4.70% |

| Return after taxes on distributions | 0.24% | 2.92% | 3.37% |

| Return after taxes on distributions and sale of fund shares | 0.83% | 2.78% | 3.23% |

| Barclays Capital Intermediate Government Bond Index (reflects no deduction for fees, expenses or taxes) | -0.32% | 4.74% | 5.65% |

After-tax returns are calculated using the historical highest individual federal marginal income tax rates and do not reflect the impact of state and local taxes. Also, actual after-tax returns depend on an investor’s tax situation and may differ from those shown. After-tax returns shown are not relevant to investors who hold their shares through tax-deferred arrangements, such as 401(k) plans or individual retirement accounts (IRAs).

Updated performance information is available by calling the Fund’s shareholder service department toll-free at 888-670-3600 or the toll-free 24-hour automated information line at 800-336-3063.

Management

Investment Adviser. The investment adviser to the Government Fund is Madison Investment Advisors, Inc. (“MIA”) and Madison Mosaic, LLC, a wholly owned subsidiary of MIA (collectively referred to herein as “Madison”).

Portfolio Managers. Paul Lefurgey (Managing Director and Head of Fixed Income) and Chris Nisbit (Vice President) co-manage the Government Fund. Mr. Lefurgey has served in this capacity since 2006 and Mr. Nisbit has served in this capacity since 1996.

Purchase and Sale of Fund Shares

3

Purchase minimums

To establish an account:

$1,000 for a regular account

$500 for an IRA account

$100 for an Education Savings Account with automatic monthly investments of at

least $100

To add to an account:

$50 for all account types

You may purchase, redeem or exchange shares of the Fund on any day the New York Stock Exchange is open for business. You may purchase, redeem or exchange shares of the Fund either through a financial advisor or directly from the Fund.

Tax Information

Dividends and capital gains distributions you receive from the Fund are subject to federal income taxes and will also generally be considered taxable income at the state and local level as well.

Payments to Broker-Dealers and Other Financial Intermediaries

If you purchase shares of the Government Fund through a broker-dealer or other financial intermediary (such as a financial advisor), the Fund’s investment adviser may pay the intermediary for the sale of Fund shares and related services. These payments may create a conflict of interest by influencing the broker-dealer or other financial intermediary to recommend the Fund over another investment. Ask your financial advisor or visit your financial intermediary’s website for more information.

4

SUMMARY DATA: CORE BOND FUND

Investment Objectives/Goals

The investment objective of the Core Bond Fund is to receive income from bonds and to distribute that income to its investors as dividends.

Fees and Expenses

This table describes the fees and expenses that you may pay if you buy and hold shares of the Core Bond Fund.

Shareholder Fees:

(fees paid directly from your investment)

| Maximum sales charge (load) | None |

| Redemption fee | None |

| Exchange fee | None |

Annual Fund Operating Expenses:

(expenses that you pay each year as a percentage of the value of your investment)

| Management fee | 0.40% |

| Distribution (12b-1) fees | None |

| Other expenses | 0.30% |

| Total annual fund operating expenses | 0.70% |

Example:

This example is intended to help you compare the cost of investing in the Core Bond Fund with the cost of investing in other mutual funds.

The example assumes that you invest $10,000 in the Core Bond Fund for the time periods indicated and then redeem all of your shares at the end of those periods. The example also assumes that your investment has a 5% return each year and that the Fund’s operating expenses remain the same. Although your actual costs may be higher or lower, based on these assumptions, your costs would be:

| 1 Year | 3 Years | 5 Years | 10 Years |

| $72 | $224 | $390 | $871 |

Portfolio Turnover

The Core Bond Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover may indicate higher transaction costs and may result in higher taxes when Fund shares are held in a taxable account. These costs, which are not reflected in annual fund operating expenses or in the example, affect the Fund’s performance. During the most recent fiscal year, the Core Bond Fund’s portfolio turnover rate was 16% of the average value of its portfolio.

5

Principal Investment Strategies

The Core Bond Fund seeks to achieve its investment objective through diversified investments in bonds and other debt securities. The Fund invests in a broad range of corporate debt securities, obligations of the U.S. Government and its agencies and money market instruments. It invests at least 80% of its total assets in bonds, with the total portfolio having a dollar weighted average maturity of ten years or less. Also, at least 65% of the Fund’s net assets will be invested in investment grade bonds. Finally, up to 35% of the Fund’s total assets may be invested in securities rated as low as B, including those commonly referred to as “high yield,” “high risk” or “junk” bonds.

Principal Risks

Interest Rate Risk. The share price of the Core Bond Fund reflects the value of the bonds held by it. When interest rates or general demand for municipal securities change, the value of these bonds change. If the value of these bonds falls, the share price of the Fund will go down. What might cause bonds to lose value? One reason is because interest rates went up. When this happens, existing bonds that pay a lower rate become less attractive and their prices tend to go down. If the share price falls below the price you paid for your shares, you could lose money when you redeem your shares. The longer the maturity of any bond, the greater the effect will be on its price when interest rates change.

Call Risk. If a bond issuer “calls” a bond held by the Fund (i.e., pays it off at a specified price before it matures), the Fund could have to reinvest the proceeds at a lower interest rate. It may also experience a loss if the bond is called at a price lower than what the Fund paid for the bond.

Risk of Default. Although the Fund’s investment adviser monitors the condition of bond issuers, it is still possible that unexpected events could cause the issuer to be unable to pay either principal or interest on its bond. This could cause the bond to go into default and lose value.

Tax-Related Risk. You can receive a taxable distribution of capital gain from the Fund. You may also owe taxes if you sell your shares at a price that is higher than the price you paid for them.

Mortgage-Backed Securities Risk. The Fund may own obligations backed by mortgages, such as those issued by Ginnie Mae and Fannie Mae. If the mortgage holders prepay them during a period of falling interest rates, the Fund could be exposed to prepayment risk. In that case, the Fund would have to reinvest the proceeds at a lower interest rate. The security itself may not increase in value with the corresponding drop in rates since the prepayment acts to shorten the maturity of the security.

High-Yield Bond Risk. Because the Fund may invest up to 35% of its total assetsThe risks of investing in high-yield bonds rated below investment grade, you should understand the risks associated with these bonds, which include the following:

| · | The Youth and Growth of the High Yield Bond Market. The high yield (junk) bond market is relatively young and supply is limited. |

Sensitivity to Interest Rates and Economic Changes. Prices of high yield (junk) bonds may be less sensitive to interest rate changes than other bonds, but more sensitive to adverse economic changes or individual corporate developments. |

Market Expectations. High yield (junk) bond values are very sensitive to market expectations about the credit worthiness of the issuing companies. |

Liquidity and Valuation. There may be “thin” trading during times of market distress. |

6

Taxation. Interest income may be recognized as taxable even though payment of such interest is not received in cash. |

Credit Ratings. Changes in credit ratings by the major credit rating agencies may lag changes in the credit worthiness of the issuer. |

Risk/Return Bar Chart and Performance Table

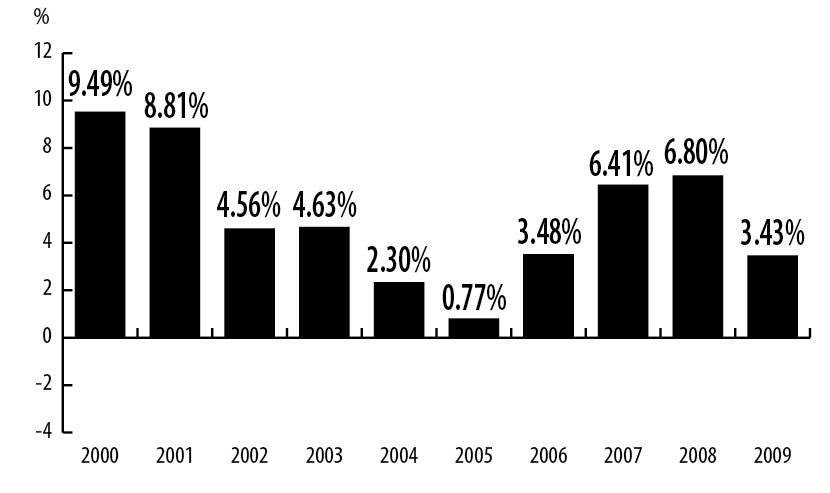

The bar chart and table below demonstrate the variability of the Core Bond Fund’s returns by showing changes in the Fund’s performance from year to year over a 10-year period. This information provides some indication of the risks of investing in the Fund. After the bar chart is a table that compares the Fund’s average annual total returns with those of a broad-based securities market index. Remember, however, that past performance (before and after taxes) does not necessarily indicate how the Fund will perform in the future.

Core Bond Fund Calendar Year Returns

Highest/lowest quarterly results during the period shown in the bar chart were:

Highest: 5.29% (quarter ended December 31, 2008)

Lowest: -1.83% (quarter ended June 30, 2004)

Core Bond Fund Average Annual Total Returns (for the period ended December 31, 2009) | |||

| One Year | Five Years | Ten Years | |

| Return before taxes | 3.43% | 4.15% | 5.03% |

| Return after taxes on distributions | 2.32% | 2.81% | 3.42% |

| Return after taxes on distributions and sale of fund shares | 2.22% | 2.75% | 3.33% |

| Barclays Capital Aggregate Bond Index (reflects no deduction for fees, expenses or taxes) | 5.93% | 4.97% | 6.33% |

After-tax returns are calculated using the historical highest individual federal marginal income tax rates and do not reflect the impact of state and local taxes. Also, actual after-tax returns depend on an investor’s tax situation and may differ from those shown. After-tax returns shown are not relevant to investors who hold their shares through tax-deferred arrangements, such as 401(k) plans or individual retirement accounts (IRAs).

Updated performance information is available by calling the Fund’s shareholder service department toll-free at 888-670-3600 or the toll-free 24-hour automated information line at 800-336-3063.

7

Management

Investment Adviser. The investment adviser to the Core Bond Fund is Madison Investment Advisors, Inc. (“MIA”) and Madison Mosaic, LLC, a wholly owned subsidiary of MIA (collectively referred to herein as “Madison”).

Portfolio Managers. Paul Lefurgey (Managing Director and Head of Fixed Income) and Chris Nisbit (Vice President) co-manage the Government Fund. Mr. Lefurgey has served in this capacity since 2006 and Mr. Nisbit has served in this capacity since 1996.

Purchase and Sale of Fund Shares

Purchase minimums

To establish an account:

$1,000 for a regular account

$500 for an IRA account

$100 for an Education Savings Account with automatic monthly investments of at

least $100

To add to an account:

$50 for all account types

You may purchase, redeem or exchange shares of the Fund on any day the New York Stock Exchange is open for business. You may purchase, redeem or exchange shares of the Fund either through a financial advisor or directly from the Fund.

Tax Information

Dividends and capital gains distributions you receive from the Fund are subject to federal income taxes and will also generally be considered taxable income at the state and local level as well.

Payments to Broker-Dealers and Other Financial Intermediaries

If you purchase shares of the Core Bond Fund through a broker-dealer or other financial intermediary (such as a financial advisor), the Fund’s investment adviser may pay the intermediary for the sale of Fund shares and related services. These payments may create a conflict of interest by influencing the broker-dealer or other financial intermediary to recommend the Fund over another investment. Ask your financial advisor or visit your financial intermediary’s website for more information.

8

INVESTMENT OBJECTIVES

Madison Mosaic Income Trust (the “Trust”) offers two portfolios for investment through this prospectus: the Government Fund and the Core Bond Fund (each, a “Fund” and collectively, the “Funds”). The Funds share a common objective: to receive income from bonds and to distribute that income to its investors as dividends.

The Funds’ Board of Trustees may change either Fund’s investment objective without shareholder approval. However, you will receive prior written notice of any material change. There is no assurance that either Fund’s investment objective will be achieved.

IMPLEMENTATION OF INVESTMENT OBJECTIVES

All Funds

General Selection Criteria. Madison selects bonds for each Fund that Madison believes provide the best combination of yield (i.e., the interest rate the bond pays in relation to its price), credit risk and diversification for the respective Fund. To a lesser extent, Madison also considers whether a particular bond may increase in value from its price at the time of purchase.

Portfolio Trading Activity - Taxable Capital Gains Potential. Madison may alter the composition of any Fund with regard to quality and maturity and may sell securities prior to maturity. Under normal circumstances, however, turnover for each Fund is generally not expected to exceed 100%. Sales of Fund securities may result in capital gains. This can occur any time Madison sells a bond at a price that was higher than the price paid for it, even if Madison does not engage in active or frequent trading. Under normal circumstances, no Fund will engage in active or frequent trading of its bonds. However, it is possible that Madison will determine that market conditions require a significant change to the composition of a Fund’s portfolio. For example, if interest rates rise or fall significantly, Madison may attempt to sell bonds before they lose much value. Also, if a Fund experiences large swings in shareholder purchases and redemptions, Madison may be required to sell bonds more frequently in order to generate the cash needed to pay redeeming shareholders. Under these circumstances, the Fund could make a taxable capital gain distribution.

Temporary Defensive Position. Madison reserves the right to invest a portion of any Fund’s total assets in short-term debt securities (i.e., those with maturities of one year or less) and to maintain a portion of Fund assets in uninvested cash. However, Madison does not intend to hold more than 35% of any Fund’s total assets in such investments unless Madison determines that market conditions warrant a temporary defensive investment position. Under such circumstances, up to 100% of any Fund may be so invested. To the extent that a Fund is so invested, it is not invested in accordance with policies designed to achieve its stated investment objective. Short-term investments may include investment grade certificates of deposit, commercial paper and repurchase agreements. Madison might hold substantial cash reserves in seeking to reduce a Fund’s exposure to bond price depreciation during a period of rising interest rates and to maintain desired liquidity while awaiting more attractive investment conditions in the bond market.

9

Government Fund

Selection. Madison limits investments in the Government Fund to investment grade U.S. Government securities, which include a variety of securities issued or guaranteed by the U.S. Treasury and various agencies of the federal government. They also include various instrumentalities that were established or sponsored by the U.S. Government and certain interests in these types of securities. It is the Fund’s policy to invest at least 80% of its assets in these types of securities.

Treasury securities include notes, bills and bonds. Obligations of the Government National Mortgage Association (Ginnie Mae), the Federal Home Loan Banks, the Federal Farm Credit System, Freddie Mac, Fannie Mae, the Small Business Association and the Student Loan Marketing Association are also considered to be U.S. Government securities. Except for Treasury securities, these obligations may not be backed by the “full faith and credit” of the United States. Government agency obligations are generally guaranteed as to principal and interest by agencies and instrumentalities of the U.S. government. In sum, all U.S. Treasury securities and Government National Mortgage Association (Ginnie Mae) securities are backed by the “full faith and credit” of the United States. Securities issued by Freddie Mac, Fannie Mae and the Federal Home Loan Banks are not.

In addition to the credit of the issuing agency, securities issued by Fannie Mae, Freddie Mac and the Federal Home Loan Banks are supported by the ability of these agencies to borrow from the Federal Treasury. In particular, on September 7, 2008, Fannie Mae and Freddie Mac were placed under the conservatorship of the Federal Housing Finance Agency (“FHFA”). The takeover permits Fannie Mae and Freddie Mac to grow their mortgage backed security books without limits and continue to purchase replacement securities for their portfolios, about $20 billion per month, without capital constraints. As part of this takeover, there will be a financing and investing relationship with the U.S. Treasury via three different financing facilities to provide critically needed support to Freddie Mac and Fannie Mae for purposes of promoting liquidity in the mortgage market. One of the three facilities is a secured liquidity facility which will be not only for Fannie Mae and Freddie Mac, but also for the 12 Federal Home Loan Banks that the FHFA also regulates. This new secured lending credit facility available to Fannie Mae, Freddie Mac, and the Federal Home Loan Banks is intended to serve as an ultimate liquidity backstop, essentially implementing the temporary liquidity backstop authority granted by Congress in July 2008. It is designed to be available until those authorities expire in December 2012.

Maturity. Madison buys bonds for the Government Fund with maturities that, in its judgment, will provide the best yields available from debt securities over the life of the investment. This means that the dollar weighted average maturity of the Government Fund may be 20 years or more, depending on market conditions. Madison may adjust this maturity, however, and sell securities prior to maturity. Madison does not intend, however, to engage in extensive short-term trading on behalf of the Fund.

Core Bond Fund

Selection. The Core Bond Fund seeks to achieve its objectives by investing in corporate debt securities, obligations of the U.S. Government and its agencies and instrumentalities, and money market instruments. The percentage of the Core Bond Fund’s assets that may be invested at any particular time in a particular type of security and the dollar weighted average maturity of the t0otaltotal portfolio will depend on Madison’s judgment regarding the risks in the general market (although the dollar weighted average maturity of the total portfolio will never exceed 10 years).

10

To gauge the risks of the general market, Madison monitors many factors, including economic, monetary and interest rate trends, market momentum, institutional psychology and historical similarities to current conditions. Below is a description of the specific types of securities in which the Fund will invest.

Corporate Debt Securities. Madison will primarily buy corporate debt securities accorded one of the four highest quality ratings by Standard & Poor’s or Moody’s or, if unrated, judged by Madison to be a comparable quality. These are generally referred to as “investment grade” securities and are rated AAA, AA, A and BBB by Standard & Poor’s or Aaa, Aa, A or Baa by Moody’s. Although all of the corporate debt securities the Fund holds may be investment grade at any time, the Fund may up to 35% of its total assets in lower grade corporate debt securities, commonly known as “high yield,” “high risk” or “junk” bonds. The lowest-grade securities the Fund will purchase are those rated “B”. Madison will only invest in lower-grade securities when it believes that the creditworthiness of the issuer is stable or improving, and when the potential return of investing in such securities justifies the higher level of risk. Although the Fund may invest in securities with ratings as low as “B”, Madison follows certain policies intended to lessen some of the risks associated with investment in such securities. Included among such policies are the following: |

| Bonds acquired at the time of their initial public offering must be rated at least “B” by either Standard & Poor’s Corporation or Moody’s Investors Services, Inc.; |

| Bonds rated “BB” or “Ba” or lower must have more than one market maker at the time of acquisition; |

| Madison does not purchase unrated bonds issued by an unrated company, privately placed bonds or bonds of issuers in bankruptcy; |

| Madison does not purchase zero coupon bonds or bonds having interest paid in the form of additional securities (commonly called “payment-in-kind” or “PIK” bonds) if immediately after the investment more than 15% of the value of the Fund would be invested in such bonds; and |

| Madison will sell, as soon as practical, any security owned by the Fund that is downgraded below B. |

Madison applies the foregoing investment selection criteria at the time an investment is made. Except as described in item (5) above, Madison might not sell a bond because of an adverse change in its quality rating or other characteristics because the impact of such change is often already reflected in its market price before the bond can be sold.

U.S. Government Securities. Madison may also buy the same type of Government securities for the Core Bond Fund as are purchased for the Government Fund described above, including mortgage backed securities pools from U.S. government agencies. |

Money Market Securities. Finally, Madison may invest in money market securities. Money market securities are subject to the limitation that they mature within one year of the date of their purchase. These include: |

11

| Commercial paper (including variable rate master demand notes) rated at least A-2 by Standard and Poor’s Corporation or Prime-2 by Moody’s, or if not so rated, issued by a corporation which has outstanding debt obligations rated at least in the top two ratings by Standard and Poor’s and Moody’s; |

| Debt obligations (other than commercial paper) of corporate issuers which obligations are rated at least AA by Standard & Poor’s or Aa by Moody’s; and |

| Short-term obligations of or guaranteed by the U.S. government, its agencies or instrumentalities. |

Maturity. Madison will normally invest the Core Bond Fund so that the Fund has a dollar weighted average maturity of 10 years or less. If Madison believes that market risks are high and bond prices in general are vulnerable to decline, Madison may reduce the dollar weighted average maturity of the Fund’s bonds and increase its cash reserves and money market holdings. Madison does not, however, intend to engage in extensive short-term trading on behalf of the Fund.

RISKS

All Funds

Interest Rate Risk. The value of shares purchased in each Fund will fluctuate due to changes in the value of securities held by such Fund. At the time an investor sells his or her shares, they may be worth more or less than their original cost. Bonds tend to increase in value when prevailing interest rates fall, and to decrease in value when prevailing interest rates rise. The longer the maturities of the bonds held in the Fund, the greater the magnitude of these changes. Investments with the highest yields may have longer maturities or lower quality ratings than other investments, increasing the possibility of fluctuations in value per share.

Tax-Related Risk. In addition to dividends from interest (which will be paid monthly), shareholders in each Fund can recognize taxable income in two ways:

| If you sell your shares at a price that is higher than when you bought them, you will have a taxable capital gain. On the other hand, if you sell your shares at a price that is lower than the price when you bought them, you will have a capital loss. |

| In the event a Fund sells more securities at prices higher than when they were bought by the Fund, the Fund may pass through the profit it makes from these transactions by making a taxable capital gain distribution. The discussion regarding “Portfolio Trading Activity - Taxable Capital Gains Potential” in the previous section above explains what circumstances can produce taxable capital gains. |

Call Risk. Madison may buy “callable bonds” for the Funds. This means that the issuer can redeem the bond before maturity. An issuer may want to call a bond after interest rates have gone down. If an issuer calls a bond a Fund owns, the Fund could have to reinvest the proceeds at a lower interest rate. Also, if the price paid for the bond was higher than the call price, the effect is the same as if the affected Fund sold the bond at a loss.

12

Mortgage Backed Securities Risk. Each Fund may own securities that are backed by mortgages such as, for example, Ginnie Mae or Fannie Mae securities in the Government Fund, and similar government or corporate securities in the Core Bond Fund. Normally, the payments the Fund will receive on such securities represent interest and a portion of the principal on each mortgage. However, mortgage holders may refinance their properties when interest rates fall. This has the effect of prepaying large amounts of the principal on these types of securities. If this happens, the affected Fund must reinvest the proceeds at a lower interest rate than it was able to obtain when the Fund purchased the security. Another aspect of this “prepayment risk” is that prepayments have the effect of shortening maturity. As a result, when bonds with longer maturities are becoming more valuable as interest rates fall, these types of securities may not enjoy the full benefit of this interest rate movement.

Risk of Default. Even for bonds that are rated investment grade, it is still possible that unexpected events (for example, a disaster or unforeseen economic developments, fraud or corruption at the company or its suppliers or clients, or unanticipated costs resulting from government legislation) could cause the issuer of a bond to be unable to pay either principal or interest on its bond. This could cause the bond to go into default and lose value.

Government Fund

Some federal agencies have authority to borrow from the U.S. Treasury while others do not. In the case of securities not backed by the full faith and credit of the United States, Madison must look principally to the agency issuing or guaranteeing the obligation for ultimate repayment. Madison may not be able to assess a claim against the United States itself in the event the agency or instrumentality does not meet its commitments.

Core Bond Fund

The Core Bond Fund may invest in securities rated as low as B (anything rated below BBB is considered below “investment grade”). These bonds are generally deemed to lack desirable investment characteristics. There may be only small assurance of payment of interest and principal or adherence to the original terms of issue over any long period. Although the Core Bond Fund can only invest up to 35% of its total assets in securities rated below investment grade, you should consider certain risks associated with below investment grade securities. These risks include the following:

Youth and Growth of the High Yield Bond Market. The high yield bond market is relatively young and its major growth occurred during a long period of economic expansion. Past economic downturns resulted in large price swings in the value of high yield bonds. This also adversely affected the value of outstanding bonds and the ability of the issuers to repay principal and interest. |

Sensitivity to Interest Rates and Economic Changes. Changes in the economy and interest rates may affect high yield securities differently from other securities. Prices of high yield bonds may be less sensitive to interest rate fluctuations than investment grade securities, but more sensitive to adverse economic changes or individual corporate developments. An economic downturn or a period of rising interest rates could adversely affect the ability of highly leveraged issuers to make required principal and interest payments, meet financial projections or obtain additional financing. Periods of economic decline or uncertainty may increase the price volatility of high yield bonds and, therefore, magnify changes in the fund’s net asset value. Zero coupon bonds and payment-in-kind securities |

13

| may be affected to a greater extent by such developments and thereby tend to be more volatile than securities that pay interest periodically in cash. |

Market Expectations. High yield bond values are very sensitive to market expectations about the credit worthiness of the issuing companies. If events produce a sudden concern in the marketplace about the ability of high yield bond issuers to service their debts, investors might try to liquidate significant amounts of high yield bonds within a short period of time. If shareholders in the Fund made significant redemptions at the same time, Madison might be forced to sell some of the Fund’s holdings under adverse market conditions. Madison would have to do this without regard to their investment merits. If this happened, the Fund could realize capital losses and decrease the asset base upon which expenses can be spread. Rising interest rates can adversely affect the value of high yield bonds, both by lowering the perceived credit worthiness of the issuers and by lowering bond prices generally. However, when interest rates are falling or the credit worthiness of the issuer improves, early redemption or call features of the bonds may limit their potential for increased value. |

Liquidity and Valuation. Adverse publicity about or public perceptions of high yield securities and their market, whether or not based on fundamental analysis, may cause these bonds to lose value and liquidity. Since the high yield market is an over-the-counter market, there may be “thin” trading during times of market distress. This means there is a limited number of buyers and sellers in the market. |

Taxation. Interest income is recognized on zero coupon and payment-in-kind securities. This income is passed through to shareholders for income tax purposes, even though payment of such interest is not received in cash. |

Credit Ratings. Madison considers quality ratings of debt securities when investments are selected. However, changes in credit ratings by the major credit rating agencies may lag changes in the credit worthiness of the issuer. Madison monitors the issuers of high yield bonds to anticipate whether the issuer will have sufficient cash flow to meet required principal and interest payments and to assess the bonds’ liquidity, but Madison may not always be able to foresee adverse developments. Furthermore, credit ratings attempt to evaluate the safety of principal and interest payments and may not accurately reflect the market value risks of high yield bonds. |

PORTFOLIO HOLDINGS

Portfolio holdings information is available on the Funds’ website at www.mosaicfunds.com. In addition, a complete description of the Funds’ policies and procedures with respect to the disclosure of portfolio holdings is available in the Funds’ SAI. Please see the back cover of this prospectus for information about the SAI.

MANAGEMENT

Investment Adviser

The investment adviser to the Funds is Madison Investment Advisors, Inc. (“MIA”) and Madison Mosaic, LLC, a wholly-owned subsidiary of MIA (collectively referred to herein as “Madison”), both located at 550 Science Drive, Madison, Wisconsin 53711. As of December 31, 2009,

14

Madison Investment Advisors, Inc., which was founded in 1974, and its subsidiary organizations, including Madison Mosaic, LLC, managed approximately $15 billion in assets, including open-end mutual funds, closed-end mutual funds, separately managed accounts and wrap accounts. Madison is responsible for the day-to-day administration of the Funds’ activities.

Investment decisions regarding the Funds can be influenced in various manners by a number of individuals. Generally, all decisions regarding a Fund’s average maturity, duration and investment considerations concerning interest rate and market risk are the primary responsibility of Madison’s investment policy committee. The investment policy committee is made up of the top officers and managers of Madison.

Day-to-day decisions regarding the selection of individual bonds and other management functions for the Funds are primarily the responsibilities of Paul Lefurgey and Chris Nisbet.

Paul Lefurgey. Mr. Lefurgey, managing director and head of fixed income of Madison since joining Madison in October 2005, was formerly Vice President for MEMBERS Capital Advisors, Inc. from 2003 until joining Madison. Mr. Lefurgey became involved in the management of the Funds in 2006. |

Chris Nisbet. Mr. Nisbet is a Vice President of Madison and has been a member of the team managing the Funds since 1996. He has been a member of the firm’s fixed income team since 1992. |

Information regarding the portfolio managers’ compensation, their ownership of securities in the Funds and the other accounts they manage can be found in the SAI.

Compensation

Investment Advisory Fee. Madison receives a fee for its services under an investment advisory agreement with the Funds. The annual fee is 0.40% of the average daily net assets of each Fund. This fee is deducted automatically from all accounts and is reflected in the daily share price of each Fund. A discussion regarding the basis for approval of the Funds’ investment advisory agreement with Madison is contained in the Funds’ annual report to shareholders for the fiscal year ended December 31, 2009.

Other Expenses. Under a separate services agreement with the Funds, Madison provides or arranges for the Funds to have all other operational and support services needed by the Funds. Madison receives a fee calculated as a percentage of the average daily net assets of each Fund for these services. At the end of the Funds’ most recent fiscal year, this fee was set at 0.28% for the Government Fund and 0.30% for the Core Bond Fund. Because of this services arrangement with Madison, Madison is responsible for paying all of the Funds’ fees and expenses, other than the investment advisory fee (discussed above), fees related to the Fund’s portfolio holdings (such as brokerage commissions, interest on loans, etc.), and extraordinary or non-recurring fees of the Fund (such as fees and costs relating to any temporary line of credit the Funds maintain for emergency or extraordinary purposes).

15

PRICING OF FUND SHARES

The price of each Fund’s shares is based on the net asset value (“NAV”) per share. NAV per share equals the total daily value of a Fund’s assets, minus its liabilities, divided by the total number of shares. NAV is calculated at the close of the New York Stock Exchange (typically 3:00 p.m., Central Time) each day it is open for trading. The New York Stock Exchange is closed on New Year’s Day, Martin Luther King, Jr. Day, President’s Day, Good Friday, Memorial Day, Independence Day, Labor Day, Thanksgiving Day, and Christmas Day.

When you purchase or redeem shares, your transaction will be priced based on the next calculation of NAV after your order is placed. This may be higher, lower or the same as the NAV from the previous day.

Madison uses the market value of the securities in each Fund to calculate NAV. Madison obtains the market value from one or more established pricing services. The Funds maintain a pricing committee to review market value of portfolio securities to determine whether or not prices obtained from the pricing services are fair. In accordance with policies approved by the Board of Trustees of the Funds, the pricing committee may determine that the “fair value” of a particular security is different than the market value provided by the pricing service. Although this would be an unusual occurrence for the types of securities held by the Funds, this may occur, for example, due to events or information not known to the pricing service or due to events occurring in other parts of the world. In using fair value pricing, the Funds’ goal is to prevent share transactions from occurring at a price that is unrealistically high or low based on information known but not reflected in the “market” price of portfolio securities calculated at the close of the New York Stock Exchange.

SHAREHOLDER INFORMATION

Purchase and Redemption Procedures

Information regarding how to purchase and sell shares in any Madison Mosaic Fund (including the Funds) is provided in a separate brochure entitled, “Madison Mosaic’s Guide to Doing Business,” which is incorporated by reference into this prospectus.

Dividends and Distributions

The Funds’ net income is declared as dividends monthly. Dividends are paid in the form of additional shares credited to your account at the end of each calendar month, unless you elect in writing to receive a monthly dividend check or payment by electronic funds transfer. Any net realized capital gains would be distributed at least annually and like dividends, are paid in the form of additional shares credited to your account, unless you elect otherwise. Please refer to “Madison Mosaic’s Guide to Doing Business” for more information about dividend distribution options.

Frequent Purchases and Redemptions of Fund Shares

General Rule. Madison Mosaic Funds discourage investors from using the Funds to frequently trade or otherwise attempt to “time” the market. As a result, the Funds reserve the right to reject a purchase or exchange request for any reason.

16

Market Timing. It is the policy of Madison Mosaic Funds to block shareholders or potential shareholders from engaging in harmful trading behavior, as described below, in any Madison Mosaic Fund (including the Funds). To accomplish this, the Funds reserve the right to reject a purchase or exchange request for any reason, without notice. This policy does not affect a shareholder’s right to redeem an account.

Identifiable Harmful Frequent Trading and Market-Timing Activity. Madison Mosaic Funds defines harmful trading activity as that activity having a negative effect on portfolio management or Fund expenses. For example, a Fund subject to frequent trading or “market-timing” must maintain a large cash balance in order to permit the frequent purchases and redemptions caused by market-timing activity. Cash balances must be over and above the “normal” cash requirements the Fund keeps to handle redemption requests from long-term shareholders, to buy and sell portfolio securities, etc. By forcing a Fund’s portfolio manager to keep greater cash balances to accommodate market timing, the Fund may be unable to invest its assets in accordance with the Fund’s investment objectives. Alternatively, harmful trading activity may require frequent purchase and sale of portfolio securities to satisfy cash requirements. To the extent market-timing activity of this sort requires the affected Fund to continually purchase and sell securities, the Fund’s transaction costs will increase in the form of brokerage commissions and custody fees. Finally, frequent trading activity results in a greater burden on the affected Fund’s transfer agent, increasing transfer agent expenses and, if not actually raising Fund expenses, at least preventing them from being lowered.

For all of the above reasons, the Funds monitor cash flows and transfer agent activity in order to identify harmful activity. Furthermore, when approached by firms or individuals who request access for market timing activities, the Funds decline such requests; when trades are attempted without such courtesy, the Funds make every effort to block them and prohibit any future investments from the source of such trades. The Funds do not define market-timing by the frequency or amount of trades during any particular time period. Rather, the Funds seek to prevent market-timing of any type that harms the Funds in the manner described above.

The Funds do not currently impose additional fees on market timing activity, nor do they restrict the number of exchanges shareholders can make, although the right to do so is reserved upon notice in the future. The Funds do not specifically define the frequency of trading that will be considered “market timing” because the goal is to prevent any harm to long-term investors that is caused by any out-of-the-ordinary trading or account activity. As a result, when the Funds identify any shareholder activity that causes or is expected to cause the negative results described above, the Funds will block the shareholder from making future investments. In effect, the Funds allow harmful market-timers to leave Madison Mosaic Funds and shut the doors to their return.

The Funds use their discretion to determine whether transaction activity is harmful based on the criteria described above. Except as described below, the Funds do not distinguish between shareholders that invest directly with a Fund or shareholders that invest with Madison Mosaic Funds through a broker (either directly or through an intermediary account), an investment adviser or other third party as long as the account is engaging in harmful activity as described above.

Other Risks Associated with Market Timing. Moving money in and out of Funds on short notice is a strategy employed by certain investors who hope to reap profits from short-term market fluctuation. This is not illegal, but is discouraged by many funds since it can complicate fund management and, if successfully employed, have a negative impact on performance. In particular, a successful “market-timer” could, over time, dilute the value of fund shares held by long-term investors by essentially “siphoning off” cash by frequently buying fund shares at an

17

NAV lower than the NAV at which the same shares are redeemed. Nevertheless, the success of any market-timer is not considered by Madison Mosaic Funds. Rather, the Funds will block ALL identifiable harmful frequent trading and market-timing activity described above regardless of whether the market-timer is successful or unsuccessful. In any event, investors in any of the Madison Mosaic Funds should be aware that dilution caused by successful market timing by some shareholders is a risk borne by the remaining shareholders.

Exceptions or Other Arrangements. It is possible that a Fund will not detect certain frequent trading or market timing activity in small amounts that, because of the relatively small size of such activity, is subsumed by the normal day-to-day cash flow of the Fund (see the section above entitled “Other Risks Associated with Market Timing”). However, the Funds believe their procedures are adequate to identify any market timing activity having the harmful effects identified in the section entitled “Identifiable Harmful Frequent Trading and Market-Timing Activity” regardless of the nature of the shareholder or method of investment in Madison Mosaic Funds.

Because the Funds discourage market timing in general, Madison Mosaic Funds does not currently, nor does it intend to, have any arrangements or agreements, formal or informal, to permit any shareholders or potential shareholders to directly or indirectly engage in any type of market-timing activities, harmful or otherwise.

Although the Funds believe reasonable efforts are made to block shareholders that engage in or attempt to engage in harmful trading activities, the Funds cannot guarantee that such efforts will successfully identify and block every shareholder that does or attempts to do this.

TAXES

Federal Taxes

Each Fund will distribute to shareholders 100% of its net income and net capital gains, if any. The capital gains distribution is determined as of October 31st each year and distributed annually.

Dividends and capital gains distributions will be taxable to you. In January each year, the Funds will send you an annual notice of dividends and other distributions paid during the prior year. Capital gain distributions can be taxed at different rates depending on the length of time the securities were held.

When a Fund makes a distribution, the Fund’s NAV decreases by the amount of the payment. If you purchase shares shortly before a distribution, you will, nonetheless, be subject to income taxes on the distribution, even though the value of your investment (plus cash received, if any) remains the same.

Fund distributions are expected to be primarily distributions of net income.

State and Local Taxes

In most states, the dividends and any capital gains you receive from the Funds will be subject to state and local taxation.

Taxability of Transactions

Your redemption of Fund shares may result in a taxable gain or loss to you, depending on whether the redemption proceeds are more or less than what you paid for the redeemed shares.

18

An exchange of Fund shares for shares in any other Madison Mosaic Fund generally will have similar tax consequences.

Certification of Tax Identification Number

Account applications without a social security number will not be accepted. If you do not provide a valid social security or tax identification number, you may be subject to federal withholding at a rate of 28% of your Fund distributions. Any fine assessed against the Funds that results from your failure to provide a valid social security or tax identification number will be charged to your account. You should retain all statements received from the Funds to maintain accurate records of your investments.

This section is not intended to be a full discussion of federal, state or local income tax laws and the effect of such laws on you. There may be other tax considerations applicable to a particular investor. You are urged to consult with your own tax advisor. In addition, please see the SAI for more information about taxes.

FINANCIAL HIGHLIGHTS

The following financial highlights tables are intended to help you understand each Fund’s financial performance for the past five years. Certain information reflects financial results for a single Fund share. The total returns in the table represent the rate that an investor would have earned (or lost) on an investment in each Fund, assuming reinvestment of all dividends and distributions. This information has been derived from financial statements audited by Grant Thornton LLP, whose report dated February 25, 2010, along with the Funds’ financial statements, is included in the annual report which is available upon request.

GOVERNMENT FUND

| Year Ended December 31, | |||||

2009 | 2008 | 2007 | 2006 | 2005 | |

| Net asset value, beginning of period | $10.81 | $10.30 | $9.94 | $9.95 | $10.16 |

| Investment operations: | |||||

| Net investment income | 0.27 | 0.32 | 0.33 | 0.31 | 0.28 |

| Net realized and unrealized gain (loss) on investments | (0.15) | 0.51 | 0.36 | (0.01) | (0.21) |

| Total from investment operations | 0.12 | 0.83 | 0.69 | 0.30 | 0.07 |

| Less distributions: | �� | ||||

| From net investment income | (0.27) | (0.32) | (0.33) | (0.31) | (0.28) |

| From net capital gains | (0.03) | -- | -- | -- | -- |

| Total distribution | (0.30) | (0.32) | (0.33) | (0.31) | (0.28) |

| Net asset value, end of period | $10.63 | $10.81 | $10.30 | $9.94 | $9.95 |

Total return (%) | 1.19 | 8.17 | 7.10 | 3.07 | 0.69 |

| Ratios and supplemental data | |||||

Net assets, end of period (in thousands) | $4,300 | $5,071 | $2,986 | $3,055 | $3,248 |

| Ratio of expenses to average net assets (%) | 0.69 | 0.78 | 1.15 | 1.19 | 1.19 |

| Ratio of net investment income to average net assets (%) | 2.55 | 3.00 | 3.30 | 3.11 | 2.75 |

| Portfolio turnover (%) | 38 | 67 | 18 | 41 | 43 |

19

ORE BOND FUND

| Year Ended December 31, | |||||

2009 | 2008 | 2007 | 2006 | 2005 | |

| Net asset value, beginning of period | $6.74 | $6.58 | $6.44 | $6.46 | $6.64 |

Investment operations: | |||||

| Net investment income | 0.21 | 0.27 | 0.26 | 0.24 | 0.23 |

| Net realized and unrealized gain (loss) on investments | 0.02 | 0.16 | 0.14 | (0.02) | (0.18) |

| Total from investment operations | 0.23 | 0.43 | 0.40 | 0.22 | 0.05 |

| Less distributions from net investment income | (0.21) | (0.27) | (0.26) | (0.24) | (0.23) |

| Net asset value, end of period | $6.76 | $6.74 | $6.58 | $6.44 | $6.46 |

Total return (%) | 3.43 | 6.80 | 6.41 | 3.48 | 0.77 |

| Ratios and supplemental data | |||||

Net assets, end of period (in thousands) | $12,501 | $5,188 | $4,523 | $4,610 | $5,602 |

| Ratio of expenses to average net assets (%) | 0.70 | 0.80 | 1.12 | 1.10 | 1.08 |

| Ratio of net investment income to average net assets (%) | 3.13 | 4.18 | 4.05 | 3.70 | 3.49 |

| Portfolio turnover (%) | 16 | 36 | 41 | 60 | 60 |

20

Madison Mosaic Income Trust has a statement of additional information (“SAI”), which is incorporated by reference into this prospectus, that includes additional information about each Fund. Additional information about each Fund’s investments is available in the Funds’ annual and semi-annual reports to shareholders. In the Funds’ annual report, you will find a discussion of the market conditions and investment strategies that significantly affected the performance of the Funds during their last fiscal year. The SAI, the Funds’ annual and semi-annual reports and other information about the Funds are available without charge by calling 1-800-368-3195, or by visiting the Funds’ Internet site at http://www.mosaicfunds.com. Use the shareholder service number below to make shareholder inquiries.

You may also review and copy information about the Funds (including the SAI) at the SEC’s Public Reference Room in Washington, DC. Information about the operation of the Public Reference Room may be obtained by calling the SEC at 1-202-551-8090.

Reports and other information about the Funds are also available on the EDGAR Database on the SEC’s Internet site at http://www.sec.gov. Copies of this information may also be obtained, upon payment of a duplicating fee, by electronic request at the following email address: publicinfo@sec.gov, or by writing the SEC’s Public Reference Section, Washington, DC 20549-1520.

In addition to the SAI, “Madison Mosaic’s Guide to Doing Business,” which provides information on how to purchase and sell shares in any Madison Mosaic Fund, is incorporated by reference into this prospectus.

Transfer Agent

Madison Mosaic Funds

c/o U.S. Bancorp Fund Services, LLC

P.O. Box 701

Milwaukee, WI 53201-0701

www.mosaicfunds.com

Telephone Numbers

Shareholder Service

Toll-free nationwide: (888) 670 3600

Mosaic Tiles (24 hour automated information)

Toll-free nationwide: (800) 336 3063

SEC File Number 811-03616

Document comparison by Workshare Professional on Thursday, April 15, 2010 1:48:21 PM

| Input: | |

| Document 1 ID | |

| Description | |

| Document 2 ID | |

| Description | |

| Rendering set | |

| Legend: | |

| Inserted cell | |

| Deleted cell | |

| Moved cell | |

| Split/Merged cell | |

| Padding cell | |

| Statistics: | |

| Count | |

| Insertions | |

| Deletions | |

| Moved from | |

| Moved to | |

| Style change | |

| Format changed | |

| Total changes | |