EXHIBIT 99.1

INVESTOR PRESENTATION SEPTEMBER 2017 onelibertyproperties.com

2 TABLE OF CONTENTS DESCRIPTION PAGE Table of Contents 2 Safe Harbor Disclosure 3 Company Overview 4 Experienced Management Team 5 Attractive Portfolio Fundamentals 6 Portfolio Detail 7 Diversified Portfolio 8 Diversified Tenant Base 9 Financial Summary 10 Targeting Long Term Total Return 11 Growth in Operations 12 Growth Oriented Balance Sheet 13 Mortgage Debt Maturities 14 Lease Maturity Profile 15 Consistent Operational Performance 16 - 17 Acquisition Track Record 18 Recent Acquisitions 19 Recent Dispositions 20 Recent Mortgages 21 DESCRIPTION PAGE Case Studies: Acquisition – Nashville, TN 22 Disposition – Greenwood Village, CO 23 Acquisition – Baltimore, MD 24 Summary 25 APPENDIX Case Studies: Acquisition – Cleveland, OH 27 Acquisition – El Paso, TX 28 Blend and Extend – Office Depot 29 Releasing Case Study – Atlanta, GA 30 Top Tenant Profiles: Havertys Furniture 32 LA Fitness 33 Northern Tool & Equipment 34 Regal Entertainment Group 35 Office Depot 36 GAAP Reconciliation to FFO & AFFO 37

3 SAFE HARBOR The statements in this presentation , including targets and assumptions, state the Company’s and management’s hopes, intentions, beliefs, expectations or projections of the future and are forward - looking statements. It is important to note that the Company’s actual results could differ materially from those projected in such forward - looking statements. Factors that could cause actual results to differ materially from current expectations include the key assumptions contained within this presentation, general economic conditions, local real estate conditions, increases in interest rates, tenant defaults, non - renewals, and/or bankruptcies, and increases in operating costs and real estate taxes. Additional information concerning factors that could cause actual results to differ materially from those forward - looking statements is contained in the Company’s SEC filings , and in particular the sections of such documents captioned “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations”. Copies of the SEC filings may be obtained from the Company or the SEC. The Company does not undertake to publicly update or revise any forward - looking statements included in this presentation, whether as a result of new information, future events or otherwise.

4 COMPANY OVERVIEW Fundamentals – focused real estate company Disciplined track record through economic cycles Active net lease strategy Experienced management team Alignment of interests through significant insider ownership

5 EXPERIENCED MANAGEMENT TEAM Patrick J. Callan, Jr. President & CEO Chief Executive Officer since 2008, President since 2006, Director since 2002 Senior Vice President of First Washington Realty Inc. from 2004 to 2005. A joint venture with CalPERS that controlled 100 shopping centers (13 million square feet) which was sold for $2.6 billion to Regency Centers/Macquarie Vice President of Kimco Realty Corporation (NYSE: KIM) from 1998 to 2004, joined in 1987. Responsible for a $3 billion, 200+ shopping center portfolio Lawrence G. Ricketts, Jr. COO & EVP Chief Operating Officer since 2008 and Executive Vice President since 2006 (Vice President since 1999) Over $3 billion of transaction experience in acquisitions, dispositions and financings David W. Kalish, CPA SVP & CFO Senior Vice President and Chief Financial Officer since 1990 Senior Vice President, Finance of BRT Apartments Corp. (NYSE: BRT) since 1998 and Senior Vice President and Chief Financial Officer of the managing general partner of Gould Investors L.P. since 1990 Matthew J. Gould Chairman Chairman of the Board since June 2013 and Vice Chairman from 2011 through 2013. President and Chief Executive Officer from 1989 to 1999; Senior Vice President from 1999 to 2011 Senior Vice President of BRT Apartments Corp. (NYSE: BRT) since 1993 and Director since 2004 Chairman of the managing general partner of Gould Investors L.P. since January 2013 and President and CEO from 1997 to 2012 Fredric H. Gould Vice Chairman Vice Chairman of the Board since June 2013. Chairman of the Board from 1989 to 2013 Chairman of BRT Apartments Corp. (NYSE: BRT) from 1984 to April 2013 and Director since 1984 Chairman Emeritus of the managing general partner of Gould Investors L.P. since January 2013 and Chairman from 1997 to 2013 Director of EastGroup Properties, Inc. (NYSE: EGP) since 1998

6 ATTRACTIVE PORTFOLIO FUNDAMENTALS (1) Total Square Footage 10.6 M Number of Properties 121 Current Occupancy 97.2% Contractual Rental income (2) $69.5 M Lease Term Remaining 8.2 Years Northern Tool – Fort Mill, SC (Charlotte, MSA) Regal Cinemas (d/b/a United Artists) – Indianapolis, IN (1) Information presented as of June 30 ,2017, including five properties owned by unconsolidated joint ventures (2) Our contractual rental income represents, after giving effect to any abatements, concessions or adjustments, the base rent payable to us for the twelve months ending June 30, 2018 under leases in effect at June 30, 2017 and excludes ( i ) approximately $283,000 of straight - line rent and $1.1 million of amortization of intangibles; (ii) approximately $310,000 of aggregate contractual rental income from properties tenanted by Payless ShoeSource and Joe’s Crab Shack, which filed for Chapter 11 bankruptcy protection during the three months ended June 30, 2017; and (iii) approximately $783,000 of contractual rental income from our Kansas City, Missouri property, tenanted by Kohls, which was sold in July 2017. In addition, we have included our $2.8 million share of the base rent payable to our unconsolidated joint ventures for the twelve months ending June 30, 2018.

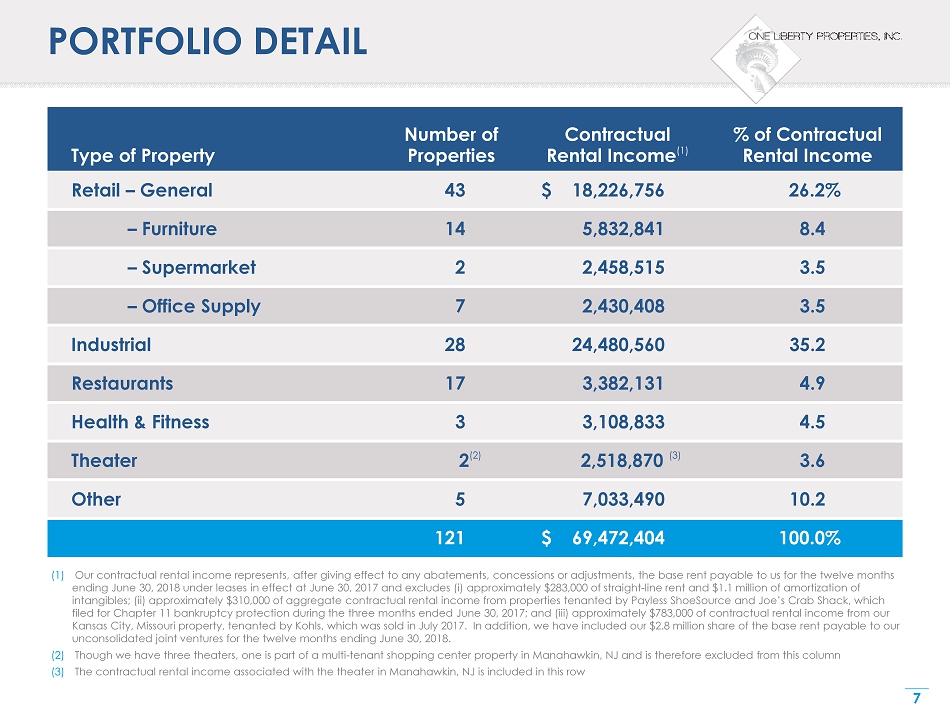

7 PORTFOLIO DETAIL Type of Property Number of Properties Contractual Rental Income (1) % of Contractual Rental Income Retail – General 43 $ 18,226,756 26.2% – Furniture 14 5,832,841 8.4 – Supermarket 2 2,458,515 3.5 – Office Supply 7 2,430,408 3.5 Industrial 28 24,480,560 35.2 Restaurants 17 3,382,131 4.9 Health & Fitness 3 3,108,833 4.5 Theater 2 (2) 2,518,870 (3) 3.6 Other 5 7,033,490 10.2 121 $ 69,472,404 100.0% (1) Our contractual rental income represents, after giving effect to any abatements, concessions or adjustments, the base rent pa yab le to us for the twelve months ending June 30, 2018 under leases in effect at June 30, 2017 and excludes ( i ) approximately $283,000 of straight - line rent and $1.1 million of amortization of intangibles; (ii) approximately $310,000 of aggregate contractual rental income from properties tenanted by Payless ShoeSourc e a nd Joe’s Crab Shack, which filed for Chapter 11 bankruptcy protection during the three months ended June 30, 2017; and (iii) approximately $783,000 of c ont ractual rental income from our Kansas City, Missouri property, tenanted by Kohls, which was sold in July 2017. In addition, we have included our $2.8 milli on share of the base rent payable to our unconsolidated joint ventures for the twelve months ending June 30, 2018. (2) Though we have three theaters, one is part of a multi - tenant shopping center property in Manahawkin, NJ and is therefore exclude d from this column (3) The contractual rental income associated with the theater in Manahawkin, NJ is included in this row

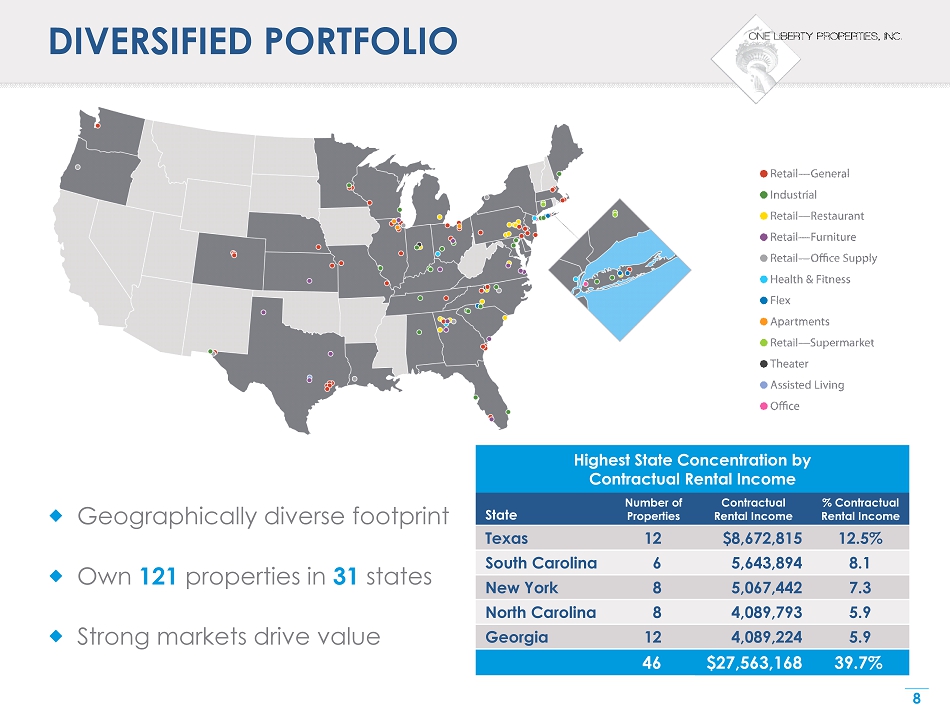

8 DIVERSIFIED PORTFOLIO Geographically diverse footprint Own 121 properties in 31 states Strong markets drive value Highest State Concentration by Contractual Rental Income State Number of Properties Contractual Rental Income % Contractual Rental Income Texas 12 $8,672,815 12.5% South Carolina 6 5,643,894 8.1 New York 8 5,067,442 7.3 North Carolina 8 4,089,793 5.9 Georgia 12 4,089,224 5.9 46 $27,563,168 39.7%

9 DIVERSIFIED TENANT BASE Top Tenants Number of Locations Contractual Rental Income % of Contractual Rental Income Haverty Furniture Companies, Inc. (NYSE: HVT) 11 $ 4,809,684 6.9% LA Fitness International , LLC 3 3,108,833 4.5 Northern Tool & Equipment 1 2,799,409 4.0 Regal Entertainment Group (NYSE: RGC) 3 2,518,870 3.6 Office Depot, Inc. (NYSE: ODP) 7 2,430,408 3.5 25 $15,667,204 22.5%

10 FINANCIAL SUMMARY Market Cap (1) $445.4 M Shares Outstanding (1) 18.6 M Insider Ownership (2) 23.3% Current Annualized Dividend $1.72 Dividend Yield (3) 7.2% FedEx Ground & Chep USA – St. Louis, MO JCI/ Yanfeng (Johnson Controls Guarantee) – McCalla , AL (1) Market cap is calculated using the shares outstanding and the closing OLP stock price of $23.91 at September 13, 2017 (2) Calculated as of September 13, 2017 (3) Based on closing stock price of $23.91 at September 13, 2017

11 TARGETING LONG TERM TOTAL RETURN (1) Performance period ended June 30, 2017 Consistent driver of long term stockholder value 11.5% 10.1% 8.5% 0% 2% 4% 6% 8% 10% 12% OLP NAREIT Equity Index S&P 500 15 - Year Annualized Total Return (1)

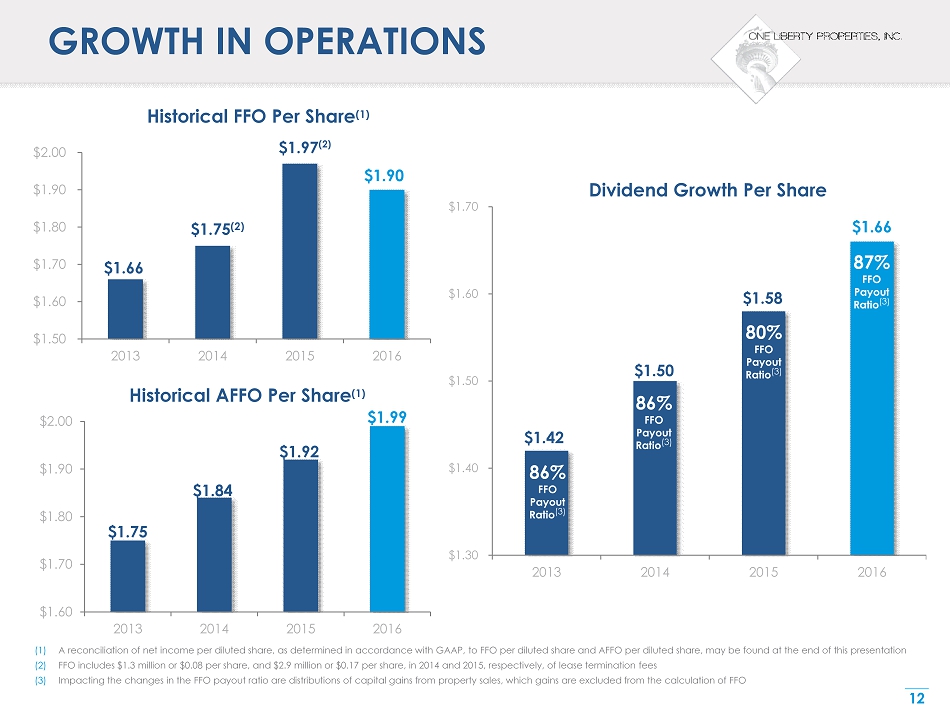

12 GROWTH IN OPERATIONS (1) A reconciliation of net income per diluted share, as determined in accordance with GAAP, to FFO per diluted share and AFFO pe r d iluted share, may be found at the end of this presentation (2) FFO includes $1.3 million or $0.08 per share, and $2.9 million or $0.17 per share, in 2014 and 2015, respectively, of lease t erm ination fees (3) Impacting the changes in the FFO payout ratio are distributions of capital gains from property sales, which gains are exclude d f rom the calculation of FFO $1.66 $1.75 (2) $1.97 (2) $1.90 $1.50 $1.60 $1.70 $1.80 $1.90 $2.00 2013 2014 2015 2016 Historical FFO Per Share (1) $1.75 $1.84 $1.92 $1.99 $1.60 $1.70 $1.80 $1.90 $2.00 2013 2014 2015 2016 Historical AFFO Per Share (1) $1.42 $1.50 $1.58 $1.66 $1.30 $1.40 $1.50 $1.60 $1.70 2013 2014 2015 2016 Dividend Growth Per Share 86% FFO Payout Ratio (3) 86% FFO Payout Ratio (3) 87% FFO Payout Ratio (3) 80% FFO Payout Ratio (3)

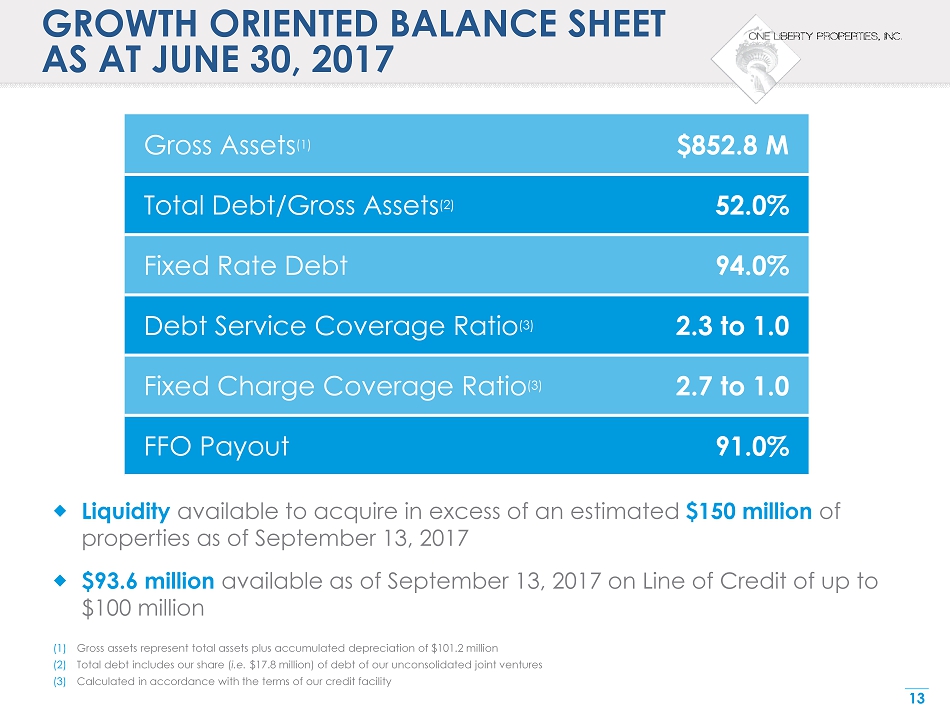

13 GROWTH ORIENTED BALANCE SHEET AS AT JUNE 30, 2017 Gross Assets (1) $852.8 M Total Debt/Gross Assets (2) 52.0% Fixed Rate Debt 94.0% Debt Service Coverage Ratio (3) 2.3 to 1.0 Fixed Charge Coverage Ratio (3) 2.7 to 1.0 FFO Payout 91.0% (1) Gross assets represent total assets plus accumulated depreciation of $101.2 million (2) Total debt includes our share ( i.e. $17.8 million) of debt of our unconsolidated joint ventures (3) Calculated in accordance with the terms of our credit facility Liquidity available to acquire in excess of an estimated $150 million of properties as of September 13, 2017 $93.6 million available as of September 13, 2017 on Line of Credit of up to $100 million

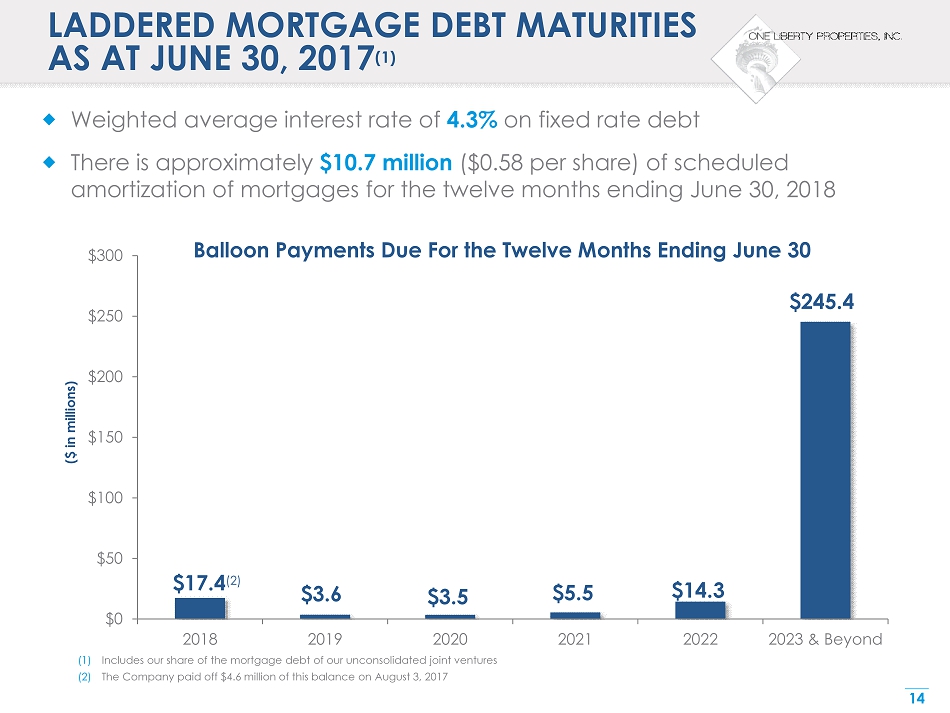

14 LADDERED MORTGAGE DEBT MATURITIES AS AT JUNE 30, 2017 (1) (1) Includes our share of the mortgage debt of our unconsolidated joint ventures (2) The Company paid off $4.6 million of this balance on August 3, 2017 Weighted average interest rate of 4.3% on fixed rate debt There is approximately $10.7 million ($0.58 per share) of scheduled amortization of mortgages for the twelve months ending June 30, 2018 $17.4 (2) $3.6 $3.5 $5.5 $14.3 $245.4 $0 $50 $100 $150 $200 $250 $300 2018 2019 2020 2021 2022 2023 & Beyond ($ in millions) Balloon Payments Due For the Twelve Months Ending June 30

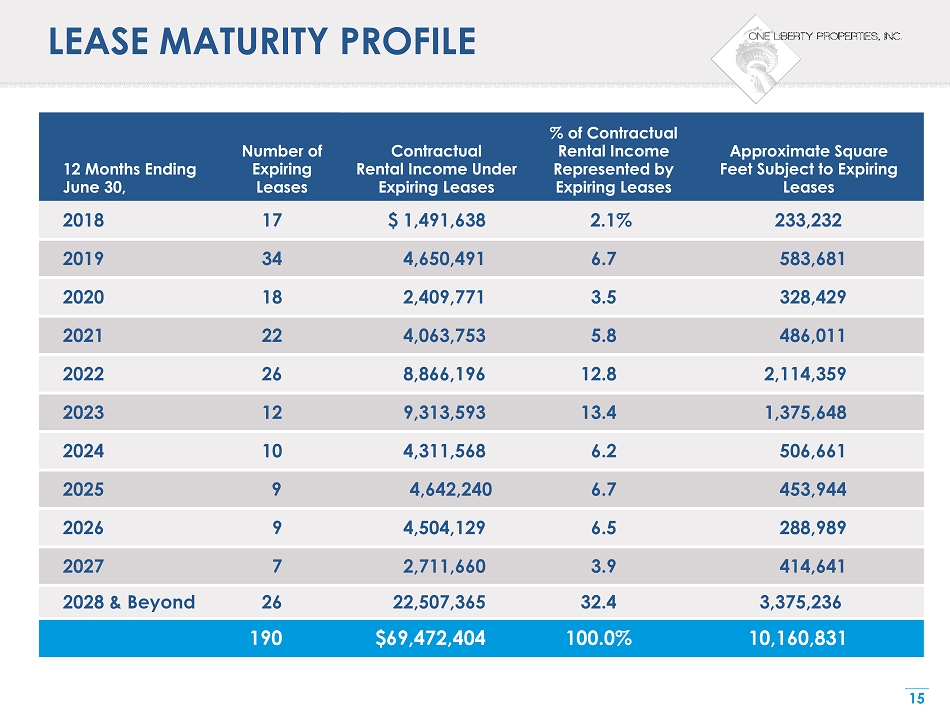

15 LEASE MATURITY PROFILE 12 Months Ending June 30, Number of Expiring Leases Contractual Rental Income Under Expiring Leases % of Contractual Rental Income Represented by Expiring Leases Approximate Square Feet Subject to Expiring Leases 2018 17 $ 1,491,638 2.1% 233,232 2019 34 4,650,491 6.7 583,681 2020 18 2,409,771 3.5 328,429 2021 22 4,063,753 5.8 486,011 2022 26 8,866,196 12.8 2,114,359 2023 12 9,313,593 13.4 1,375,648 2024 10 4,311,568 6.2 506,661 2025 9 4,642,240 6.7 453,944 2026 9 4,504,129 6.5 288,989 2027 7 2,711,660 3.9 414,641 2028 & Beyond 26 22,507,365 32.4 3,375,236 190 $69,472,404 100.0% 10,160,831

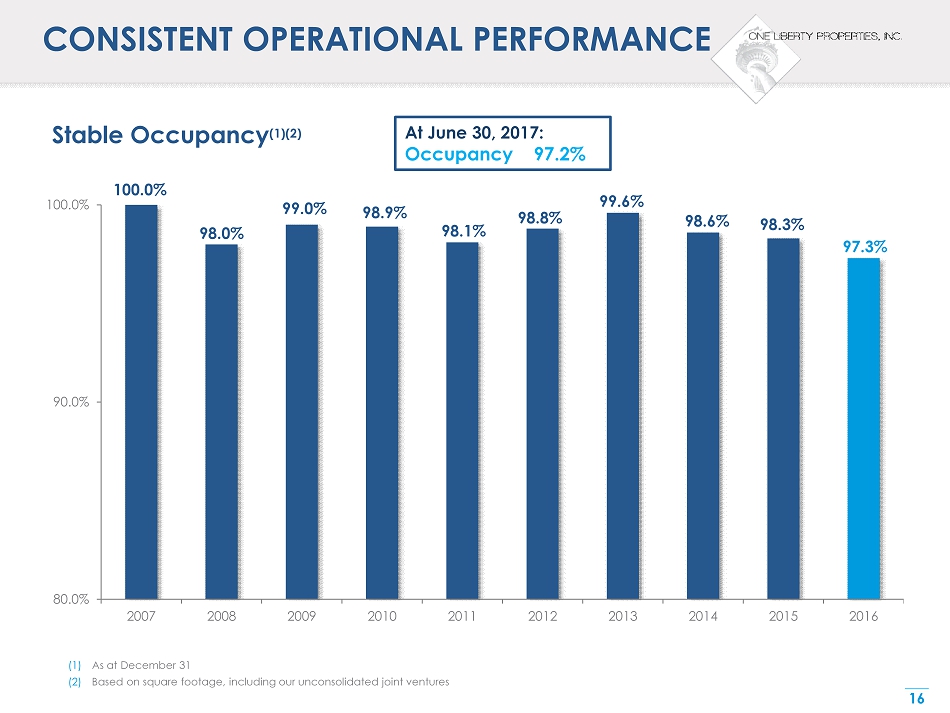

16 CONSISTENT OPERATIONAL PERFORMANCE (1) As at December 31 (2) Based on square footage, including our unconsolidated joint ventures 100.0% 98.0% 99.0% 98.9% 98.1% 98.8% 99.6% 98.6% 98.3% 97.3% 80.0% 90.0% 100.0% 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 Stable Occupancy (1)(2) At June 30, 2017: Occupancy 97.2%

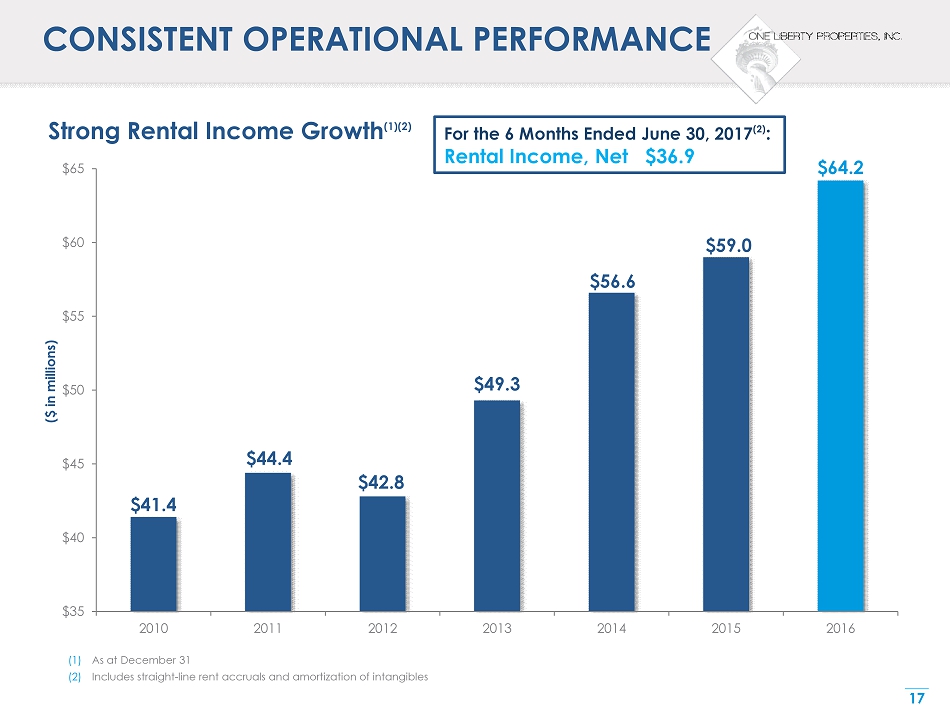

17 CONSISTENT OPERATIONAL PERFORMANCE (1) As at December 31 (2) Includes straight - line rent accruals and amortization of intangibles $41.4 $44.4 $42.8 $49.3 $56.6 $59.0 $64.2 $35 $40 $45 $50 $55 $60 $65 2010 2011 2012 2013 2014 2015 2016 ($ in millions) Strong Rental Income Growth (1)(2) For the 6 Months Ended June 30, 2017 (2) : Rental Income, Net $36.9

18 ACQUISITION TRACK RECORD (1) Includes our 50% share of an unconsolidated joint venture property in (a) Savannah, GA acquired in 2011 and (b) Manahawkin, N J a cquired in 2015 Acquired $35.2 million of properties through June 30, 2017 Current pipeline of diverse opportunities in excess of $225.0 million $72.3 $29.6 (1) $44.6 $107.5 $56.8 $95.2 (1) $118.6 $0 $20 $40 $60 $80 $100 $120 2010 2011 2012 2013 2014 2015 2016 ($ in millions) Acquisitions per Year

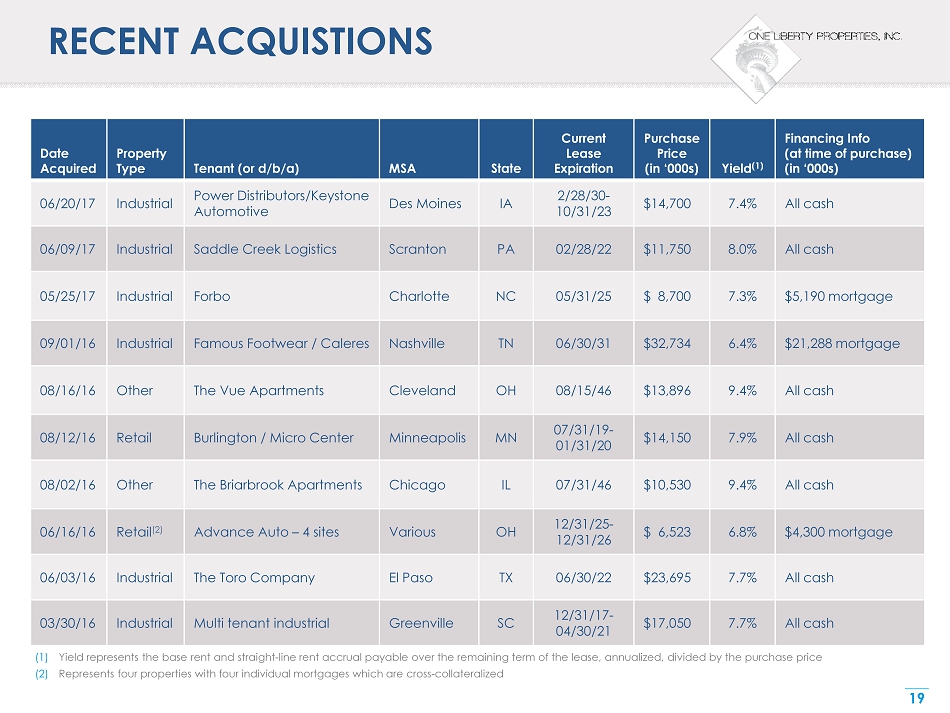

19 RECENT ACQUISTIONS Date Acquired Property Type Tenant (or d/b/a) MSA State Current Lease Expiration Purchase Price (in ‘000s) Yield (1) Financing Info (at time of purchase) (in ‘000s) 06/20/17 Industrial Power Distributors/Keystone Automotive Des Moines IA 2/28/30 - 10/31/23 $14,700 7.4% All cash 06/09/17 Industrial Saddle Creek Logistics Scranton PA 02/28/22 $11,750 8.0% All cash 05/25/17 Industrial Forbo Charlotte NC 05/31/25 $ 8,700 7.3% $5,190 mortgage 09/01/16 Industrial Famous Footwear / Caleres Nashville TN 06/30/31 $32,734 6.4% $21,288 mortgage 08/16/16 Other The Vue Apartments Cleveland OH 08/15/46 $13,896 9.4% All cash 08/12/16 Retail Burlington / Micro Center Minneapolis MN 07/31/19 - 01/31/20 $14,150 7.9% All cash 08/02/16 Other The Briarbrook Apartments Chicago IL 07/31/46 $10,530 9.4% All cash 06/16/16 Retail (2) Advance Auto – 4 sites Various OH 12/31/25 - 12/31/26 $ 6,523 6.8% $4,300 mortgage 06/03/16 Industrial The Toro Company El Paso TX 06/30/22 $23,695 7.7% All cash 03/30/16 Industrial Multi tenant industrial Greenville SC 12/31/17 - 04/30/21 $17,050 7.7% All cash (1) Yield represents the base rent and straight - line rent accrual payable over the remaining term of the lease, annualized, divided by the purchase price (2) Represents four properties with four individual mortgages which are cross - collateralized

20 RECENT DISPOSITIONS Date Acquired Date Sold Property Type Tenant (or d/b/a) MSA State Gross Sales Price (in ‘000s) Net Gain (in ‘000s) 06/30/2010 07/14/2017 Retail Kohls Kansas City MO $10,250 $2,181 04/08/1996 05/08/2017 Retail Former Sports Authority Denver CO $ 9,500 $6,568 12/22/2010 12/22/2016 Restaurant Ruby Tuesday Long Island NY $ 2,702 $ 213 02/18/2005 06/30/2016 Industrial Sweet Ovations Philadelphia PA $14,800 $5,660 06/07/2014 06/15/2016 Other The River Crossing Apartments Atlanta GA $ 8,858 $2,331 07/30/2013 05/19/2016 Restaurant Texas Land & Cattle Killeen - Temple - Fort Hood TX $ 3,100 $ 980 11/14/2006 02/01/2016 Retail Portfolio of 8 Pantry stores Various LA/MS $13,750 $ 787

21 RECENT MORTGAGES Date Financed Property Type Tenant (or d/b/a) MSA State Amount (in ‘000s) Mortgage Maturity Interest Rate 08/11/17 Industrial Saddle Creek Logistics Scranton PA $ 7,200 08/10/42 3.75% 07/10/17 Industrial Power Distributors/Keystone Automotive Des Moines IA $ 8,820 08/01/27 3.61% 05/25/17 Industrial Forbo Charlotte NC $ 5,190 06/01/27 3.72% 12/12/16 (1) Industrial Ferguson Enterprises, Inc. Baltimore MD $21,000 01/01/27 3.75% 11/14/16 Retail Bed Bath & Beyond Kennesaw GA $ 5,525 11/01/41 3.50% 09/01/16 Industrial Famous Footwear / Caleres Nashville TN $21,288 10/01/31 3.70% 08/24/16 Industrial The Toro Company El Paso TX $15,000 09/01/22 3.50% 07/29/16 Industrial Iron Mountain, Anixter & Softbox Systems Greenville SC $ 5,850 08/01/26 4.00% 07/29/16 Industrial Hartness Int’l, Imperial Pools & Minileit Greenville SC $ 5,265 08/01/26 4.00% 06/30/16 Retail Ross Stores, Hobby Lobby, Tuesday Morning & Mattress Firm El Paso TX $11,500 07/01/26 4.00% 06/28/16 Furniture LaZBoy Naples FL $ 2,150 11/05/24 3.24% 06/28/16 Industrial FedEx Durham NC $ 2,900 11/05/23 3.02% 06/16/16 (2) Retail Advance Auto – 4 sites Various OH $ 4,300 07/01/26 3.24% 05/20/16 Industrial US Lumber Baltimore MD $10,000 06/01/28 3.65% 04/20/16 Retail Carmax Knoxville TN $ 9,500 07/31/28 3.80% 03/11/16 (1) Supermarket Whole Foods West Hartford CT $18,000 04/01/28 3.38% 01/21/16 Industrial FedEx Tampa FL $ 2,500 12/05/25 3.57% 01/14/16 (1) Retail Avalon Carpet & Tile Store Deptford NJ $ 2,850 02/01/41 3.95% (1) These mortgages were refinanced or modified (2) Represents four individual loans on four Advance Auto properties which are cross - collateralized

22 ACQUISITION CASE STUDY - INDUSTRIAL In September 2016, acquired a distribution facility in Lebanon, TN (Nashville MSA) net leased to Famous Footwear and guaranteed by Caleres , Inc (NYSE: CAL) » Global footwear retailer and wholesaler with annual sales of $2.6 billion. This mission critical facility provides distribution to over 1,200 retail stores and their e - commerce website » Building is situated on 43 acres of land and was expanded in 2016 by 213,000 SF to a total of 541,024 SF . It has 40’ clear height, 54 dock doors and is 100% climate controlled » Distribution companies see Nashville as an ideal location as it is within 650 miles of 50% of the US population Purchase Price $32,734,000 Mortgage (1) (21,287,500) Net Equity Invested $11,446,500 Year 1 Base Rent $2,014,946 Interest Expense – 3.70% (1) (787,638) Net Cash to OLP $1,227,308 Return on Equity 10.72% (1) Mortgage with an interest rate of 3.70% closed simultaneously with the acquisition Famous Footwear / Caleres – Lebanon, TN (Nashville MSA)

23 DISPOSITION CASE STUDY Purchase Price $ 4,040,000 Sales Price 9,500,000 Internal Rate of Return to OLP 19.57% In April 1996, acquired a net leased retail property in Greenwood Village (Denver MSA), CO leased to Gart Bros. Sporting Goods Company for $4.0 million » 11 miles southeast of downtown Denver » The building is 45,000 SF on 3.5 acres of land Financed the asset at closing and refinanced the asset in July 2006. Paid off the loan balance in November 2015. Gart Bros merged with Sports Authority in August 2003. Sports Authority filed bankruptcy on March 2, 2016. Property was sold to Recreational Equipment, Inc. (REI) in May 2017 for $9.2 million , net of closing costs, resulting in a gain to OLP of approximately $6.6 million , net of all costs Former Sports Authority – Greenwood Village, CO

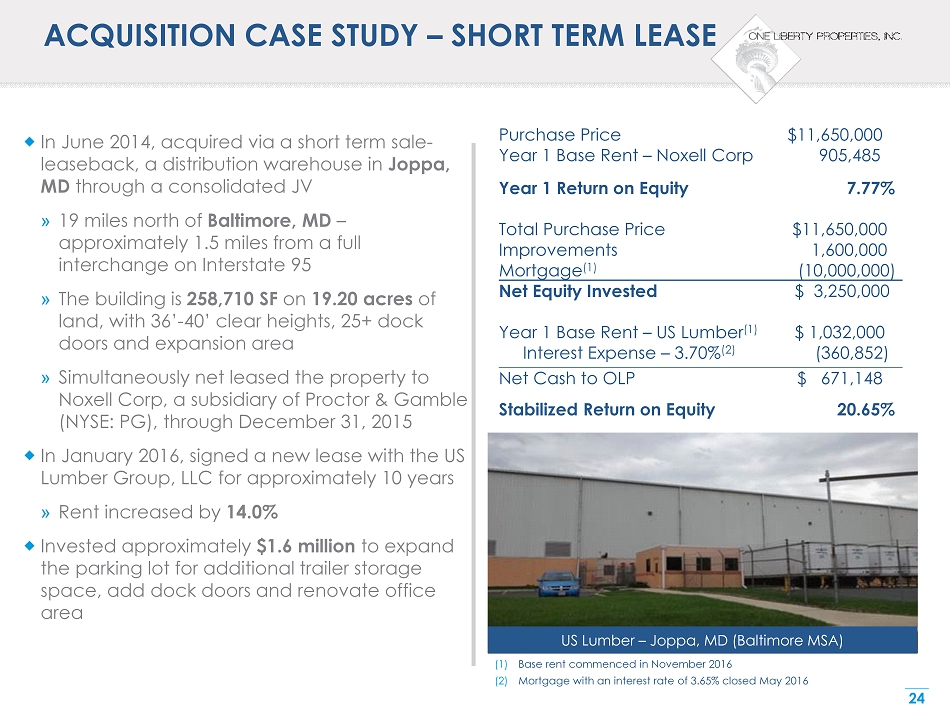

24 ACQUISITION CASE STUDY – SHORT TERM LEASE In June 2014, acquired via a short term sale - leaseback, a distribution warehouse in Joppa, MD through a consolidated JV » 19 miles north of Baltimore, MD – approximately 1.5 miles from a full interchange on Interstate 95 » The building is 258,710 SF on 19.20 acres of land, with 36’ - 40’ clear heights, 25+ dock doors and expansion area » Simultaneously net leased the property to Noxell Corp, a subsidiary of Proctor & Gamble (NYSE: PG), through December 31, 2015 In January 2016, signed a new lease with the US Lumber Group, LLC for approximately 10 years » Rent increased by 14.0% Invested approximately $1.6 million to expand the parking lot for additional trailer storage space, add dock doors and renovate office area Purchase Price $11,650,000 Year 1 Base Rent – Noxell Corp 905,485 Year 1 Return on Equity 7.77% Total Purchase Price $11,650,000 Improvements 1,600,000 Mortgage (1) (10,000,000) Net Equity Invested $ 3,250,000 Year 1 Base Rent – US Lumber (1) $ 1,032,000 Interest Expense – 3.70% (2) (360,852) Net Cash to OLP $ 671,148 Stabilized Return on Equity 20.65% (1) Base rent commenced in November 2016 (2) Mortgage with an interest rate of 3.65% closed May 2016 US Lumber – Joppa, MD (Baltimore MSA)

25 SUMMARY – WHY OLP ? Fundamentals – focused real estate company Disciplined track record through economic cycles Active net lease strategy Experienced management team Alignment of interests through significant insider ownership

APPENDIX

27 ACQUISITION CASE STUDY – GROUND LEASE In August 2016, acquired 8 acres of land in Beachwood, OH , a wealthy suburb of Cleveland » Simultaneously ground leased to an experience multi - family operator » Land is improved by a class A 348 unit mid - rise multi - family complex » Building and improvements constructed in 2015 feature the market’s best modern amenities including: – Underground parking and storage – Heated saltwater pool – Two story fitness center – Yoga room – Art gallery Purchase Price $13,896,000 Year 1 Base Rent 1,450,633 Return on Equity 10.44% The Vue Apartments – Beachwood, OH (Cleveland MSA)

28 ACQUISITION CASE STUDY – INDUSTRIAL In June 2016, acquired a distribution facility in El Paso, TX , net leased to Toro Co (NYSE: TTC) » Toro is global developer , manufacturer and distributor of lawn and landscape equipment » Toro has a market cap of approximately $6.6 billion (as of 3/15/2017) and a BBB investment grade credit per Standard & Poors » Building is 419,821 SF on 24.09 acres of land with 24’ clear heights and 69 dock doors. Building features a depth of 240’ and provides in - place flexibility to be converted into a multi - tenant facility Purchase Price $23,695,000 Mortgage (1) (15,000,000) Net Equity Invested $ 8,695,000 Year 1 Base Rent $ 1,657,600 Interest Expense – 3.70% (1) (519,000) Net Cash to OLP $ 1,138,600 Return on Equity 13.09% The Toro Company – El Paso, TX

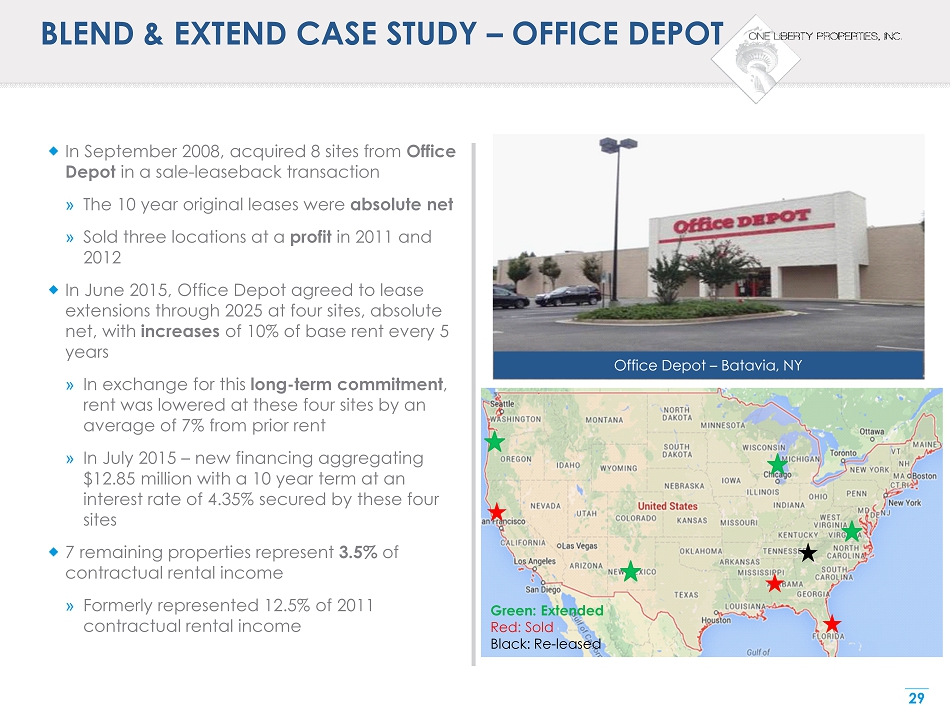

29 BLEND & EXTEND CASE STUDY – OFFICE DEPOT In September 2008, acquired 8 sites from Office Depot in a sale - leaseback transaction » The 10 year original leases were absolute net » Sold three locations at a profit in 2011 and 2012 In June 2015, Office Depot agreed to lease extensions through 2025 at four sites, absolute net, with increases of 10% of base rent every 5 years » In exchange for this long - term commitment , rent was lowered at these four sites by an average of 7% from prior rent » In July 2015 – new financing aggregating $12.85 million with a 10 year term at an interest rate of 4.35% secured by these four sites 7 remaining properties represent 3.5% of contractual rental income » Formerly represented 12.5% of 2011 contractual rental income Green: Extended Red: Sold Black: Re - leased Office Depot – Batavia, NY

30 RELEASING CASE STUDY – OFFICE DEPOT Dark and paying Office Depot site located in Kennesaw, GA (Atlanta MSA) » Building is 32,138 SF on 3.3 acres of land In December 2015, simultaneously negotiated a lease termination with Office Depot (obtaining a $950,000 early termination fee) and entered into a new 10 year lease with Bed Bath & Beyond Store Operates as Bed Bath & Beyond’s new andThat ! Concept » Tenant credit rating increased to BBB+ from B » Rent increased by 3.4% andThat ! – Kennesaw, GA (Atlanta MSA)

TOP TENANTS’ PROFILES

32 HAVERTYS FURNITURE – TENANT PROFILE Tenant: Haverty Furniture Companies, Inc. (NYSE: HVT) (Source: Tenant’s website) » Full service home furnishing retailer founded in 1885 » Public company since 1929 » 124 showrooms in 15 states in the Southern and Midwestern regions » Weathered economic cycles, from recessions to depressions to boom times » Total assets of $455 million and stockholders’ equity of $290 million at 6/30/2017 Represents 6.9% of contractual rental income 11 properties aggregating 611,930 SF – Duluth (Atlanta), GA – Fayetteville (Atlanta), GA – Wichita, KS – Lexington, KY – Bluffton (Hilton Head), SC – Amarillo, TX – Cedar Park (Austin), TX – Tyler, TX – Richmond, VA – Newport News, VA – Virginia Beach, VA Properties subject to a unitary lease which expires in 2022 Rent per square foot on the portfolio is $7.86 Havertys – Cedar Park, TX (Austin MSA)

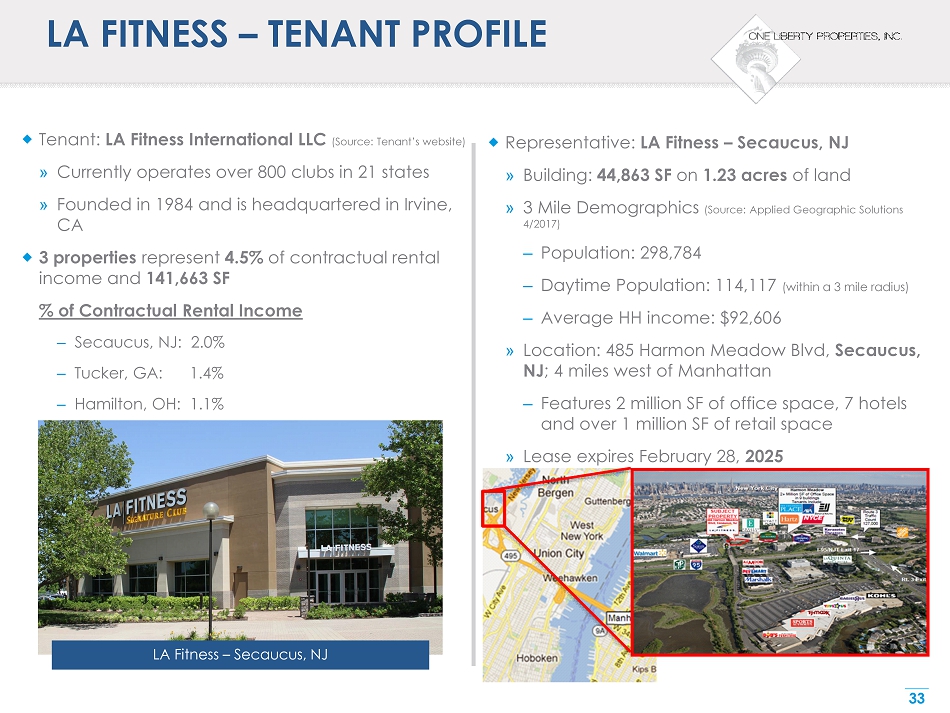

33 LA FITNESS – TENANT PROFILE Tenant: LA Fitness International LLC (Source: Tenant’s website) » Currently operates over 800 clubs in 21 states » Founded in 1984 and is headquartered in Irvine, CA 3 properties represent 4.5% of contractual rental income and 141,663 SF % of Contractual Rental Income – Secaucus, NJ: 2.0% – Tucker, GA: 1.4% – Hamilton, OH: 1.1% Representative: LA Fitness – Secaucus, NJ » Building: 44,863 SF on 1.23 acres of land » 3 Mile Demographics (Source: Applied Geographic Solutions 4/2017) – Population: 298,784 – Daytime Population: 114,117 (within a 3 mile radius) – Average HH income: $92,606 » Location: 485 Harmon Meadow Blvd, Secaucus, NJ ; 4 miles west of Manhattan – Features 2 million SF of office space, 7 hotels and over 1 million SF of retail space » Lease expires February 28, 2025 LA Fitness – Secaucus, NJ

34 NORTHERN TOOL & EQUIPMENT – TENANT PROFILE Tenant: Northern Tool & Equipment (Source: Tenant’s website) » Distributor and retailer of industrial grade and personal use power tools and equipment » 95 retail stores in the U.S. » Acquired The Sportsman’s Guide and The Golf Warehouse to sell outdoor sports and leisure goods through their distribution chain » Class A, 30’ clearance building is situated 18 miles south of downtown Charlotte, NC off Interstate - 77 Represent 4.0% of contractual rental income Location: 1850 Banks Road, Fort Mill, SC » Building: 701,595 SF on 40.0 acres of land » 3 Mile Demographics (Source: Applied Geographic Solutions 4/2017) – Population: 24,098 – Average HH income: $70,476 » Lease expires April 30, 2029 Northern Tool & Equipment – Fort Mill, SC

35 REGAL ENTERTAINMENT GROUP – TENANT PROFILE Tenant: Regal Entertainment Group (NYSE: RGC) (Source: Tenant’s website) » Brands include: Regal Cinemas, Edward Theaters and United Artists Theaters » 7,379 screens and 566 theaters in America » Currently the largest American theater chain. The second largest chain, AMC, bought Carmike (4 th largest chain) which will make AMC the largest American chain » $2.6 billion market cap (as of 8/16/2017) 3 locations represent 3.6% of contractual rental income and 150,250 SF % of Contractual Rental Income – Indianapolis, IN: 1.0% – Manahawkin, NJ (1) : 0.3% – Greensboro, NC: 2.3% Regal Cinemas (d/b/a United Artists) – Indianapolis, IN Sample Regal Luxury Seating Conversion (1) Represents one tenant at a multi - tenant shopping center

36 OFFICE DEPOT – TENANT PROFILE Tenant: Office Depot, Inc. (NYSE: ODP) (Source: Tenant’s website) » Leading global provider of office products and services » Operates more than 1,400 retail stores » Revenues of $11.0 billion (as of 12/31/2016) » $2.1 billion market cap (as of 8/16/2017) 7 properties represent 3.5% of contractual rental income and 174,431 SF % of Contractual Rental Income – Chicago, IL: 0.8% – Cary (Raleigh), NC: 0.6% – El Paso, TX: 0.5% – Eugene, OR: 0.5% – Athens, GA: 0.4% – Lake Charles, LA: 0.4% – Batavia, NY: 0.3% » The first 4 locations listed above are subject to similar leases which expire in 2025 and were all part of the original sale - leaseback transaction in 2008 Office Depot – Batavia, NY

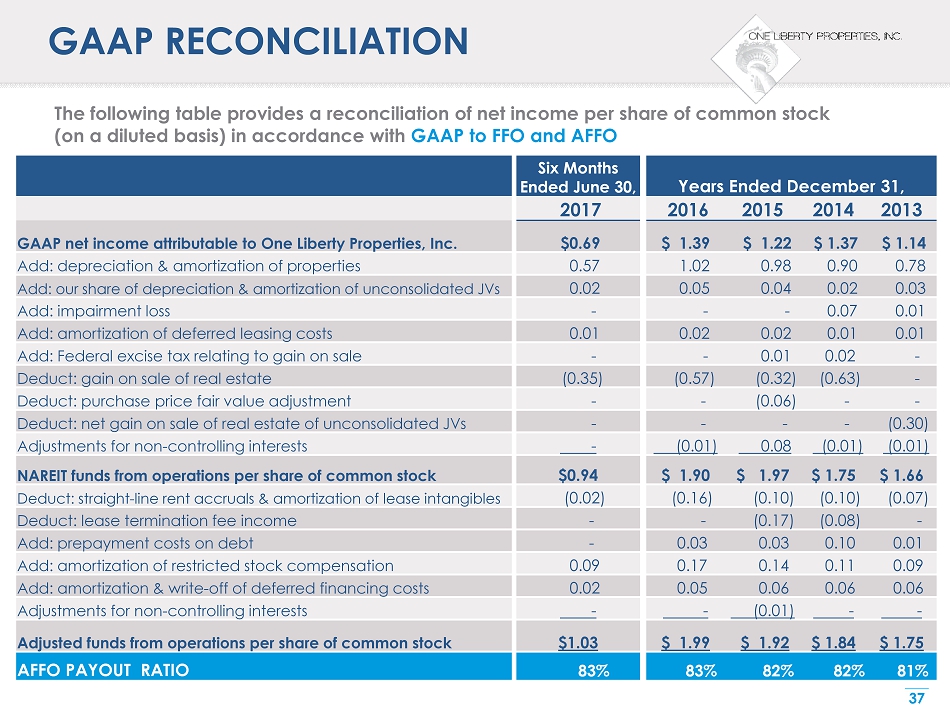

37 GAAP RECONCILIATION The following table provides a reconciliation of net income per share of common stock (on a diluted basis) in accordance with GAAP to FFO and AFFO Six Months Ended June 30, Years Ended December 31, 2017 2016 2015 2014 2013 GAAP n et income attributable to One Liberty Properties, Inc. $0.69 $ 1.39 $ 1.22 $ 1.37 $ 1.14 Add: depreciation

& amortization of properties 0.57 1.02 0.98 0.90 0.78 Add: our share of depreciation & amortization of unconsolidated JVs 0.02 0.05 0.04 0.02 0.03 Add: impairment loss - - - 0.07 0.01 Add: amortization of deferred leasing costs 0.01 0.02 0.02 0.01 0.01 Add: Federal excise tax relating to gain on sale - - 0.01 0.02 - Deduct: gain on sale of real estate (0.35) (0.57) (0.32) (0.63) - Deduct: purchase price fair value adjustment - - (0.06) - - Deduct: net gain on sale of real estate of unconsolidated JVs - - - - (0.30) Adjustments for non - controlling interests - (0.01) 0.08 (0.01) (0.01) NAREIT f unds from operations per share of common stock $0.94 $ 1.90 $ 1.97 $ 1.75 $ 1.66 Deduct: straight - line rent accruals & amortization of lease intangibles (0.02) (0.16) (0.10) (0.10) (0.07) Deduct: lease termination fee income - - (0.17) (0.08) - Add: prepayment costs on debt - 0.03 0.03 0.10 0.01 Add: amortization of restricted stock compensation 0.09 0.17 0.14 0.11 0.09 Add: amortization & write - off of deferred financing costs 0.02 0.05 0.06 0.06 0.06 Adjustments for non - controlling interests - - (0.01) - - Adjusted funds from operations per share of common stock $1.03 $ 1.99 $ 1.92 $ 1.84 $ 1.75 AFFO PAYOUT RATIO 83% 83% 82% 82% 81%