Investor Presentation PNC Announces Agreement to Buy RBC Bank (USA) June 20, 2011 Exhibit 99.2 * * * * * * * * * * * * * |

2 Cautionary Statement Regarding Forward-Looking Information This presentation contains forward-looking statements regarding our outlook or expectations with respect to the planned acquisition of RBC Bank (USA), the expected costs to be incurred in connection with the acquisition, RBC Bank (USA)’s future performance and consequences of its integration into PNC, and the impact of the transaction on PNC’s future performance. Forward-looking statements are subject to numerous assumptions, risks and uncertainties, which change over time. The forward-looking statements in this presentation speak only as of the date of the presentation, and PNC assumes no duty, and does not undertake, to update them. Actual results or future events could differ, possibly materially, from those that we anticipated in these forward-looking statements. These forward-looking statements are subject to the principal risks and uncertainties applicable to PNC’s businesses generally that are disclosed in PNC’s 2010 Form 10-K and 2011 Form 10-Qs, including in the Risk Factors and Risk Management sections of those reports, and in PNC’s subsequent SEC filings (accessible on the SEC’s website at www.sec.gov and on PNC’s corporate website at www.pnc.com/secfilings). We have included these web addresses as inactive textual references only. Information on these websites is not part of this document. Any annualized, proforma, estimated, third party or consensus numbers in this presentation are used for illustrative or comparative purposes only and may not reflect actual results. Any consensus earnings estimates are calculated based on the earnings projections made by analysts who cover that company. The analysts’ opinions, estimates or forecasts (and therefore the consensus earnings estimates) are theirs alone, are not those of PNC or its management, and may not reflect PNC’s, RBC Bank (USA)’s, or other company’s actual or anticipated results. In addition, forward-looking statements in this presentation are subject to the following risks and uncertainties related both to the acquisition transaction itself and to the integration of the acquired business into PNC after closing: • Completion of the transaction is dependent on, among other things, receipt of regulatory and other applicable approvals, the timing of which cannot be predicted with precision at this point and which may not be received at all. The impact of the completion of the transaction on PNC’s financial statements will be affected by the timing of the transaction. • The transaction may be substantially more expensive to complete (including the integration of RBC Bank (USA)’s businesses) and the anticipated benefits, including anticipated cost savings and strategic gains, may be significantly harder or take longer to achieve than expected or may not be achieved in their entirety as a result of unexpected factors or events. • Our ability to achieve anticipated results from this transaction is dependent on the state of the economic and financial markets going forward, which have been under significant stress recently. Specifically, we may incur more credit losses from RBC Bank (USA)’s loan portfolio than expected. Other issues related to achieving anticipated financial results include the possibility that deposit attrition may be greater than expected. Litigation and governmental investigations that may be filed or commenced, as a result of this transaction or otherwise, could impact the timing or realization of anticipated benefits to PNC. • The integration of RBC Bank (USA)’s business and operations into PNC, which will include conversion of RBC Bank (USA)’s different systems and procedures, may take longer than anticipated or be more costly than anticipated or have unanticipated adverse results relating to RBC Bank (USA)’s or PNC’s existing businesses. PNC’s ability to integrate RBC Bank (USA) successfully may be adversely affected by the fact that this transaction will result in PNC entering several markets where PNC does not currently have any meaningful retail presence. |

3 Strategic Rationale Opportunity to deliver PNC’s products and services to new commercial, wealth management and retail customers Fairly priced market expansion into demographically attractive growth markets Demonstrated ability to successfully integrate and grow underperforming franchises RBC Bank (USA) has quality branch network and human capital to leverage PNC’s sales and service model |

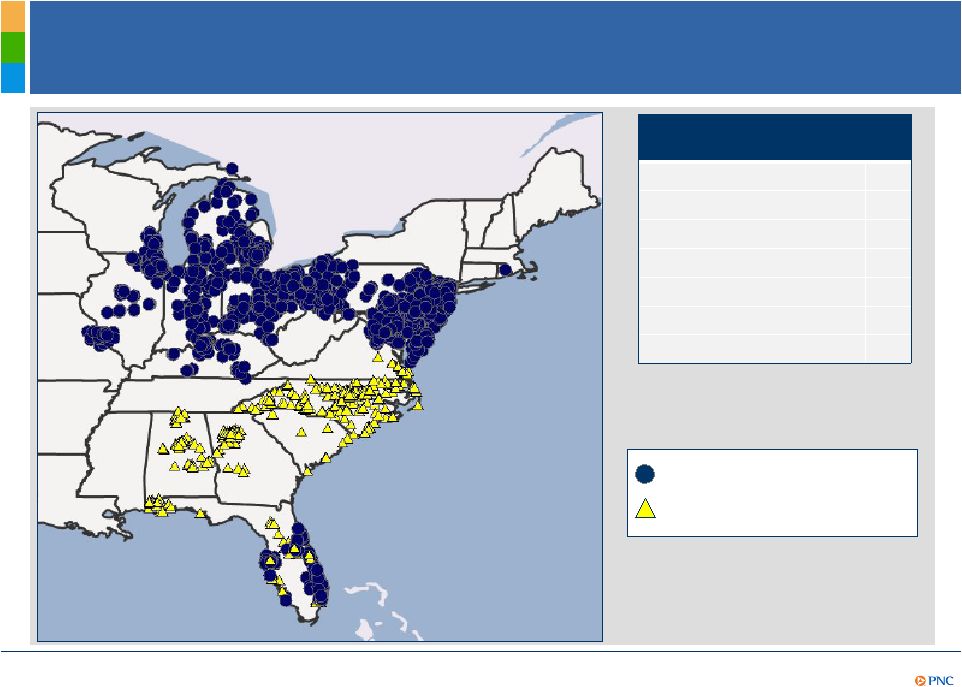

4 Extends East Coast Branch Network into Faster Growing Markets Source: SNL Financial, as of June 2010. RBC Bank (USA) branches by state North Carolina 180 Florida 83 Alabama 78 Georgia 61 Virginia 13 South Carolina 9 Total 424 PNC branches RBC Bank (USA) branches |

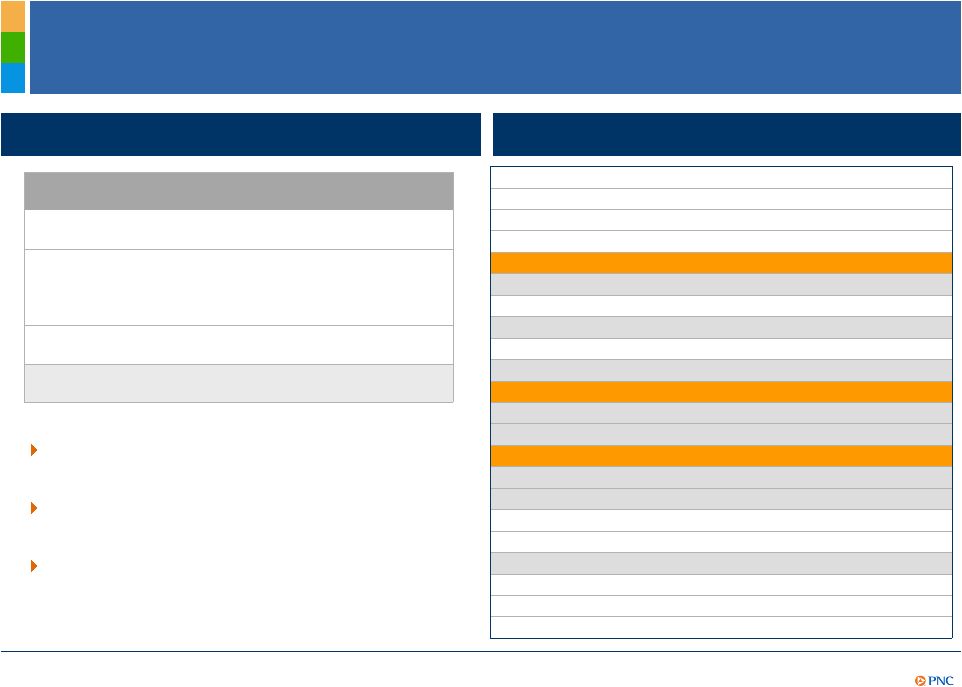

5 Opportunity to Capture More Deposit Share in Demographically Attractive Markets (1) Source: SNL DataSource. (2) Top 20 states based on wealth holders with >$1.5 million in net worth. Source: IRS Statistics of Income Division, August 2008. (3) Deposit rank based on share of deposits in state. Source: SNL DataSource as of June 30, 2010. …wealthy markets Projected 5-year growth¹ Population HH income PNC 1.2% 13.3% RBC Bank (USA) 6.5% 12.6% Proforma PNC 1.7% 13.2% U.S. average 3.9% 12.4% PNC’s proforma retail footprint covers 11 of the top 20 wealthiest states² PNC has demonstrated the ability to grow and attract customers in all its markets PNC continues to leverage its suite of innovative products and services to deepen customer relationships Proforma State² Branches Deposits( $bn) Rank³ California New York Florida 216 $8.0 10 Illinois 198 $15.7 4 Texas Pennsylvania 510 $58.2 1 Massachusetts New Jersey 334 $19.0 5 Georgia 61 $2.8 8 Michigan 244 $15.3 3 Ohio 418 $25.6 2 North Carolina 180 $8.9 5 Virginia 96 $2.6 11 Maryland 230 $10.2 3 Connecticut Washington Wisconsin 25 $1.4 11 Colorado Wyoming Arizona RBC Bank (USA) brings high growth and… |

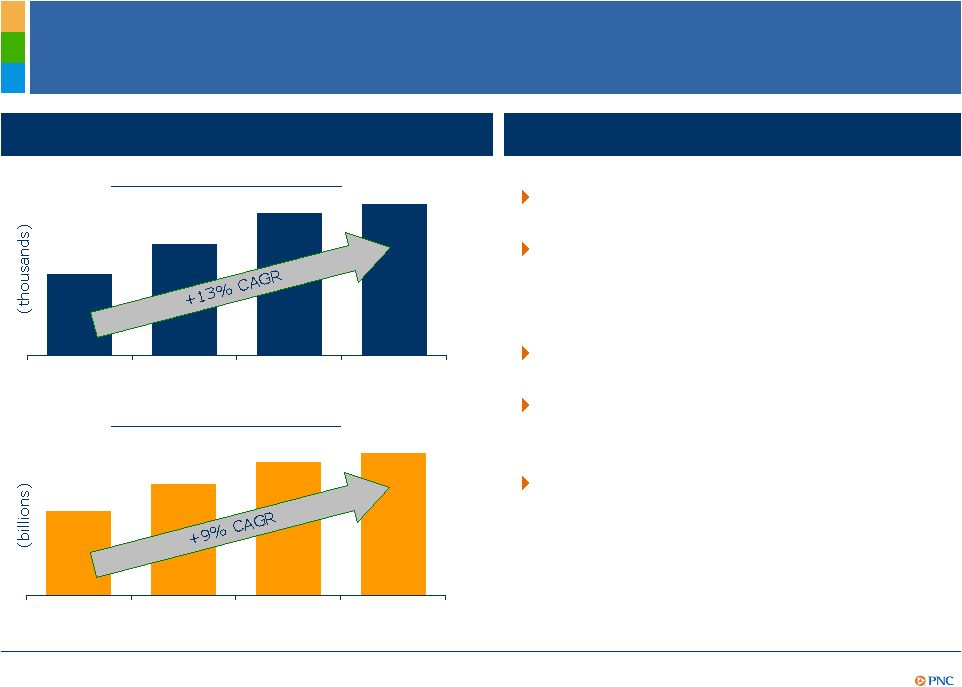

6 PNC’s Proven Capabilities to Grow Retail Banking Relationships in Acquired Markets Greater Maryland/Washington, D.C. market growth Growth strategies Increase brand awareness Introduce innovative products- Virtual Wallet, University and Workplace Banking Increase share of wallet Expand branch distribution network and channels Deliver exceptional customer service (1)Total retail deposits adjusted to exclude CDs and IRAs. (2) 2011 reflects amounts as of March 31, 2011. 497 483 430 382 2008 2009 2010 2011 Total DDA Households 2 Total Retail Deposits¹ $10.6 $10.3 $9.6 $8.7 2008 2009 2010 2011 2 |

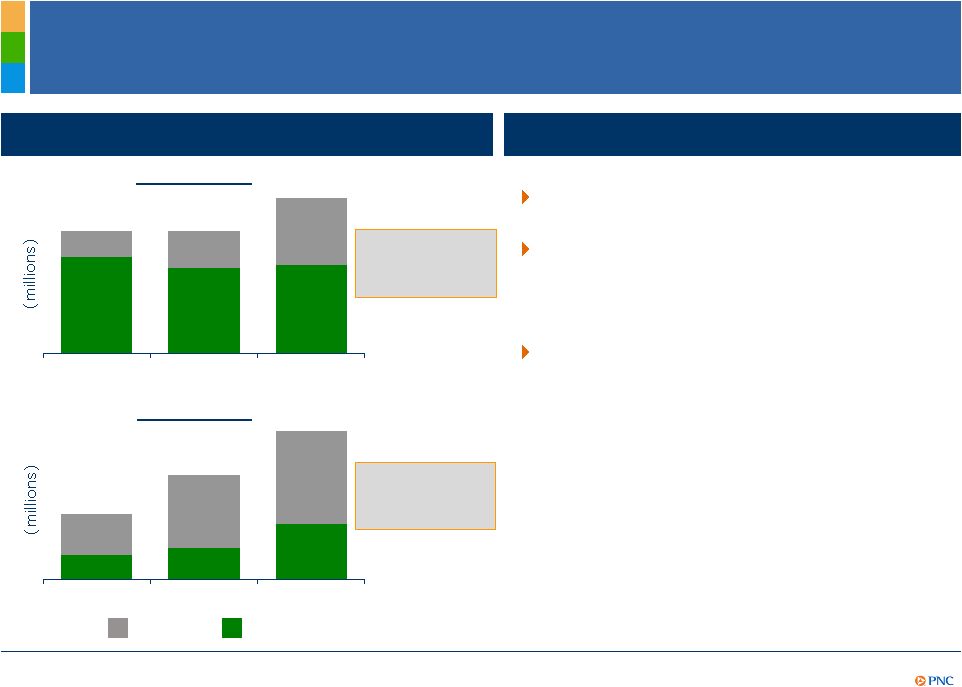

7 Demonstrated Ability to Grow C&IB and AMG in New Markets and Cross-Sell Innovative Products (1) Year over year market revenue growth. (2) Year over year total new primary client growth. (3) 2011 represents revenue growth for the five months ended May 31, 2011, annualized. $14 $20 $35 $46 $44 $50 2009 2010 2011³ Total market revenue growth¹ for C&IB and AMG Chicago Fee NII $64 $64 $81 New clients up 48% over YTD10² $12 $21 $27 $16 $9 $7 2009 2010 2011 Florida $19 $30 $43 New clients up 24% over YTD10² Growth strategies Leverage cross-sell opportunities Expand PNC’s loan syndication capabilities as a differentiated leader in middle market Deliver innovative treasury management and capital markets products 3 |

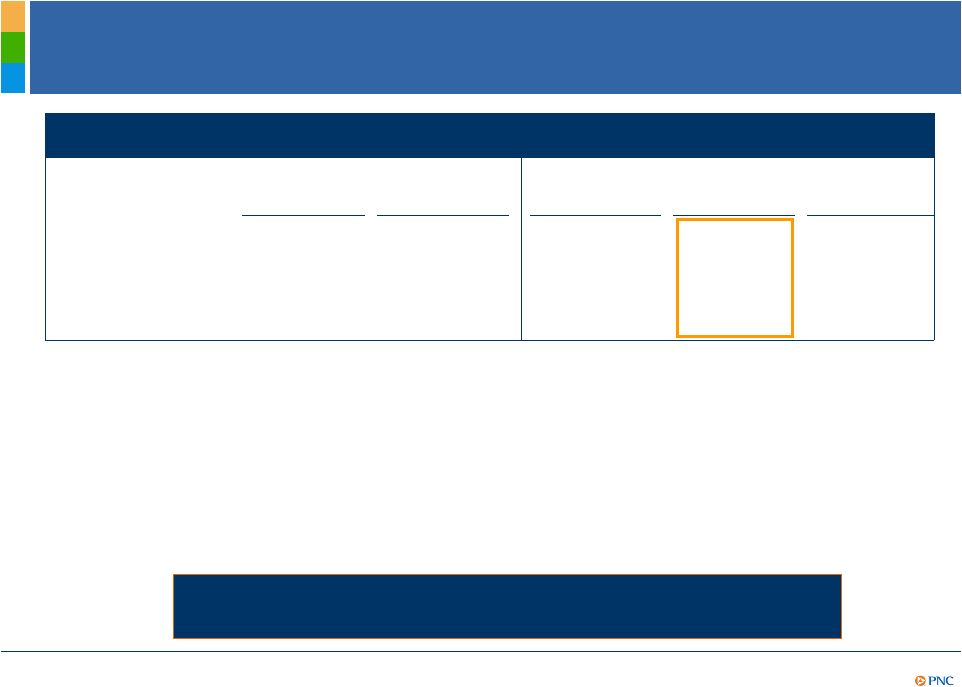

8 Significant New Commercial Market Opportunity (1) Top 10 MSAs ranked by deposit size. Small businesses defined as businesses with sale up to $20 million, Mid-market defined as businesses with sale between $20 million and $50 million, and Corporate defined as businesses with sale greater than $50 million. (2) Small Businesses total sales is unavailable. Source: SNL Financial and OneSource. PNC’s Top 10 MSAs¹ RBC Bank (USA)’s Top 10 MSAs¹ # of Businesses Total Sales ($ billions) # of Businesses % of PNC’s Top 10 Total Sales ($ billions) Small Businesses 1,373,556 NA² 506,749 37% NA² Mid-Market 14,013 $435 3,922 28% $123 Corporate 6,687 $6,092 1,999 30% $1,046 RBC Bank (USA) substantially increases target commercial clients RBC Bank (USA) substantially increases target commercial clients |

9 Compelling Transaction (1) The total consideration is comprised of a fixed dollar amount (subject to adjustment at close for net tangible asset value delivered), including cash and, at PNC’s option, common stock. The amount of PNC stock will not exceed $1 billion or cause Royal Bank of Canada’s ownership of PNC common stock to exceed 4.9%. (2) As of April 30, 2011. (3) Gross of allowance for loan losses of $755 million, therefore incremental mark of $1,488 million. As of April 30, 2011. (4) Estimated. (5) As of April 2011. Excludes $150 million for goodwill expense. Transaction Summary Transaction total value $3.45 billion 1 Internal rate of return 4 19%+ Accretion 4 End of year 2013 or sooner Compelling Financial Terms: – Price to tangible book 2 Discount to tangible book of $112 million; currently 97% – Deposit premium 2 (0.6%) Annual expense reduction 4 $230 million (27% of RBC Bank (USA)’s annualized expense base 5 ) Merger and integration costs 4 $322 million Due diligence Completed Loan marks 3,4 Total loan marks: 12.5%, 48% of NPLs Closing conditions Regulatory approvals and customary conditions Anticipated closing March 2012 |

10 Value-Added Acquisition Positions PNC Well for the Future PNC remains core funded with a proforma loan to deposit ratio of 82% Credit risk remains manageable given loan marks of 12.5% and demonstrated distressed loan management capabilities PNC remains well positioned regarding Basel III implementation Drawing upon our NCC branch conversion experience, all conversions will occur simultaneously with closing Expense savings achievable |

11 Summary PNC Continues to Build a Great Company. PNC Continues to Build a Great Company. Opportunity to deliver PNC’s products and services to new commercial, wealth management and retail customers Fairly priced market expansion into demographically attractive growth markets Demonstrated ability to successfully integrate and grow underperforming franchises RBC Bank (USA) has quality branch network and human capital to leverage PNC’s sales and service model |

12 Combined Balance Sheet (1) Gives effect to excluded assets and liabilities and estimated purchase accounting adjustments. Source: Royal Bank of Canada. (2) Assumes $1.0 billon of PNC common stock issued to the Royal Bank of Canada and $1 billion preferred stock issuance. (3) Includes loans held for sale. Appendix 1 2 3 ($ billions) PNC RBC Bank (USA) Proforma PNC ASSETS 3/31/2011 4/30/2011 3/31/2011 Investments 66.8 4.7 71.5 Loans, net 147.6 15.7 163.3 Other Assets 35.9 3.4 39.3 Intangible Assets, excluding MSRs 9.0 1.0 10.0 Total Assets 259.4 24.8 284.1 LIABILITIES Deposits 182.0 19.4 201.4 Funding 35.0 3.0 38.0 Other Liabilities 8.7 0.3 9.0 Total Liabilities 225.7 22.8 248.4 EQUITY Equity 33.7 2.0 35.7 Total Liabilities & Equity 259.4 24.8 284.1 |

13 RBC Bank (USA) Loan Portfolio Assessment (1) Gross of allowance for loan losses of $755 million, therefore incremental mark of $1,488 million. (2) Source: Royal Bank of Canada. Appendix 1 2 Estimated ($ in millions) Balance as of Credit Mark Rate Mark Total Mark Loan Category 4/30/2011 $ % $ % $ % Performing: Commercial: C&I 3,477 125 3.6% 35 1.0% 159 4.6% Owner Occupied 2,973 137 4.6% 1 0.0% 137 4.6% CRE & Construction 3,202 167 5.2% 68 2.1% 235 7.4% Consumer: Mortgage 1,855 122 6.6% 0 0.0% 122 6.6% Home Equity 3,670 496 13.5% -9 -0.2% 487 13.3% Other 806 171 21.2% -30 -3.7% 141 17.5% Total Performing 15,983 1,218 7.6% 64 0.4% 1,283 8.0% Non Accrual: Commercial: C&I 165 66 40.0% 13 8.1% 79 48.1% Owner Occupied 460 162 35.3% 40 8.7% 203 44.0% CRE & Construction 1,101 402 36.5% 94 8.6% 496 45.0% Consumer: Mortgage 137 71 52.3% 9 6.4% 80 58.7% Home Equity 68 48 71.0% 3 3.9% 51 74.9% Other 69 48 69.2% 3 4.1% 51 73.3% Total Non Accural 2,000 798 39.9% 162 8.1% 960 48.0% Total Loan Mark 17,984 2,016 11.2% 226 1.3% 2,242 12.5% |

14 Valuation Comparables Based on Recent Transactions Appendix (1) Includes repayment of target’s TARP outstanding where applicable. (2) TBV adjusted by tax adjusted credit mark net of reserves (35% tax rate). (3) As reported by company where available, otherwise core deposit amounts per SNL Financial. (4) Includes transaction expense. (5) Assumes midpoint mark. Source: SNL Financial and company filings. Buyer Target Announce Date Announced Deal Value ($M) P/TBV P/ Adj. TBV Core Deposit Premium Valley National Bancorp State Bancorp Inc. 4/28/11 $259 216% 252% 11.7% Brookline Bancorp Inc. Bancorp Rhode Island Inc. 4/20/11 $234 201% NA 11.8% Susquehanna Bancshares, Inc. Abington Bancorp, Inc. 1/26/11 $268 122% 133% 8.2% People's United Financial Inc. Danvers Bancorp Inc. 1/21/11 $493 186% 190% 13.9% Comerica Inc. Sterling Bancshares Inc. 1/18/11 $1,027 234% 374% 17.0% Hancock Holding Co. Whitney Holding Corp. 12/22/10 $1,796 200% 239% 11.6% BMO Financial Group Marshall & Ilsley Corp. 12/17/10 $5,803 138% 285% 4.9% M&T Bank Corp. Wilmington Trust Corp. 11/1/10 $681 192% 2,613% 4.7% First Niagara Financial Group NewAlliance Bancshares Inc. 8/19/10 $1,500 163% 176% 14.0% Median 192% 245% 11.7% PNC RBC Bank (USA) 6/20/11 $3,450 97% 126% (0.6%) 2 3 1 5 4 |