Exhibit 99.1

Ryan Beck & Co.

2005 Financial Institutions Investor Conference November 2, 2005

Information For Investors And Shareholders

This presentation contains forward looking statements concerning Valley’s future business outlook, financial condition and operating results. Generally, the words “will,” “may,” “should,” “continue,” “believes,” “expects,” “anticipates” or similar expressions identify forward looking statements. Readers are advised not to place undue reliance on these forward looking statements as they are influenced by certain risk factors and unpredictable events. Factors that could cause actual results to differ materially from those predicted by the forward looking statements include among others:

Increased competitive pressure among banking and/or financial services companies Adverse changes in the interest rate environment, causing reduced interest margins Unexpected changes in the debt securities market Decline in general economic conditions, whether nationally or in the market areas where Valley operates New legislation or regulatory changes that may disrupt the course of business The disallowance of prior tax strategies and changes in the effective income tax rate

NOTE: Valley disclaims any obligation to update or revise forward looking statements for any reason.

Overview of Valley National Bancorp

78 Year Commercial Banking History

Listed on the NYSE: VLY (eleven years as of December 5, 2004) Consistent Shareholder Returns Strong Financial Performance Sound Asset Quality Management Longevity/Ownership Marketplace Marketing Opportunity Business Lending Initiative

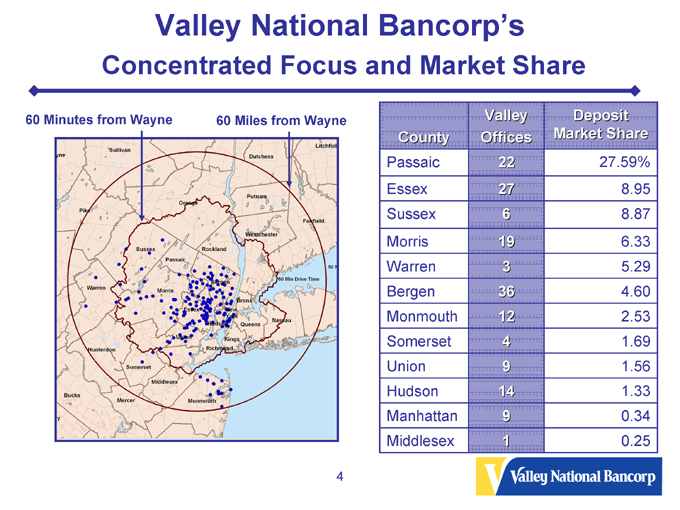

Valley National Bancorp’s

Concentrated Focus and Market Share

60 Minutes from Wayne

60 Miles from Wayne

Valley Deposit

County Offices Market Share

Passaic 22 27.59%

Essex 27 8.95

Sussex 6 8.87

Morris 19 6.33

Warren 3 5.29

Bergen 36 4.60

Monmouth 12 2.53

Somerset 4 1.69

Union 9 1.56

Hudson 14 1.33

Manhattan 9 0.34

Middlesex 1 0.25

Acquisition Strategy

Target Total

Closing Assets

Target Date ($ 000)

NorCrown Bank 6/3/2005 621,966

Shrewsbury Bancorp 3/31/2005 424,588

Merchants New York Bancorp, Inc 1/19/2001 1,369,676

Ramapo Financial Corporation 6/11/1999 327,779

Wayne Bancorp, Inc 10/16/1998 272,007

Midland Bancorporation, Inc 2/28/1997 405,027

Lakeland First Financial Group, Inc 6/30/1995 661,393

American Union Bank 2/28/1995 53,695

Rock Financial Corporation 11/30/1994 187,378

Peoples Bank 6/18/1993 217,161

Mayflower Financial Corporation 12/31/1990 122,760

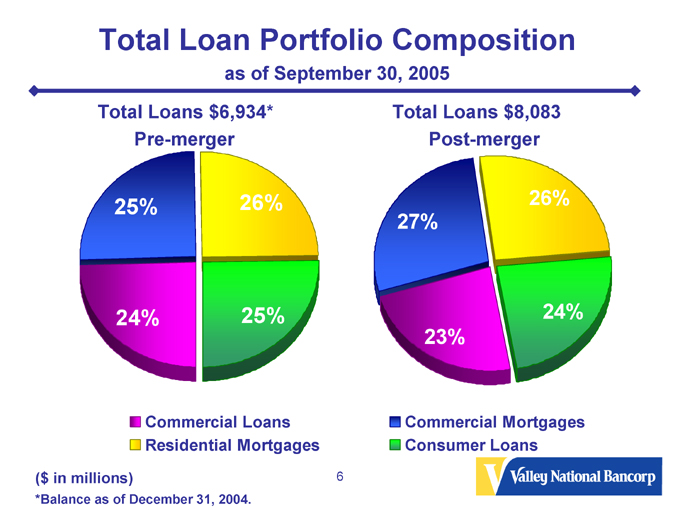

Total Loan Portfolio Composition

as of September 30, 2005

Total Loans $6,934* Pre-merger

25%

26%

24%

25%

Commercial Loans Residential Mortgages

Total Loans $8,083 Post-merger

27%

26%

23%

24%

Commercial Mortgages Consumer Loans

($ in millions)

*Balance as of December 31, 2004.

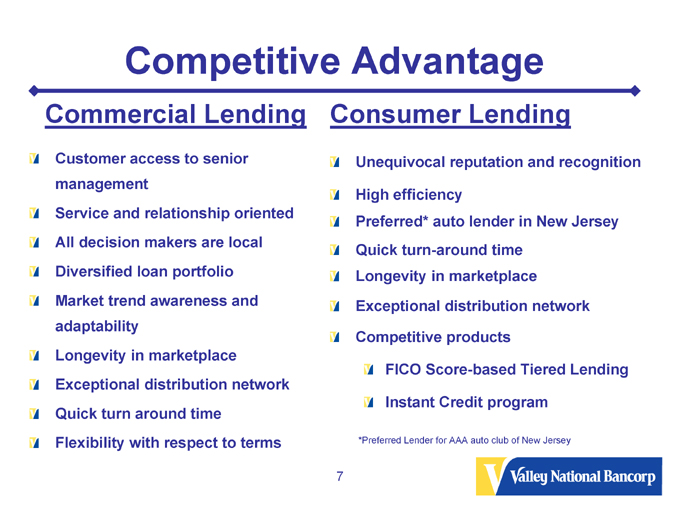

Competitive Advantage

Commercial Lending

Customer access to senior management Service and relationship oriented All decision makers are local Diversified loan portfolio Market trend awareness and adaptability Longevity in marketplace Exceptional distribution network Quick turn around time Flexibility with respect to terms

Consumer Lending

Unequivocal reputation and recognition

High efficiency

Preferred* auto lender in New Jersey Quick turn-around time Longevity in marketplace Exceptional distribution network

Competitive products

FICO Score-based Tiered Lending

Instant Credit program

*Preferred Lender for AAA auto club of New Jersey

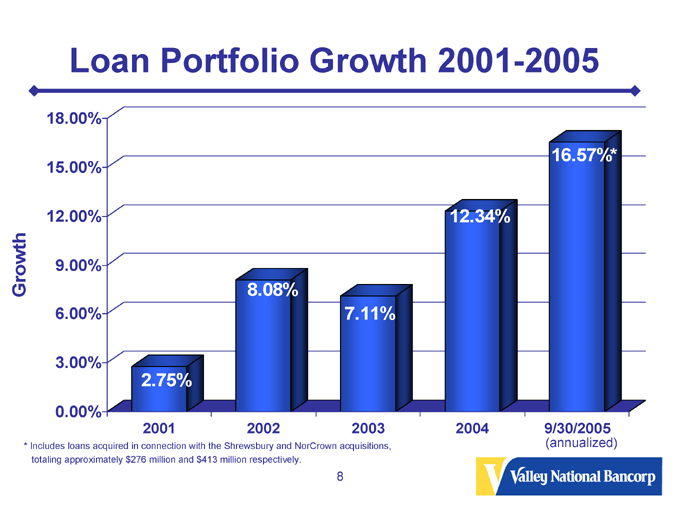

Loan Portfolio Growth 2001-2005

Growth

18.00% 15.00% 12.00% 9.00% 6.00% 3.00% 0.00%

2.75%

8.08%

7.11%

12.34%

16.57%*

2001 2002 2003 2004

9/30/2005

(annualized)

* Includes loans acquired in connection with the Shrewsbury and NorCrown acquisitions, totaling approximately $276 million and $413 million respectively.

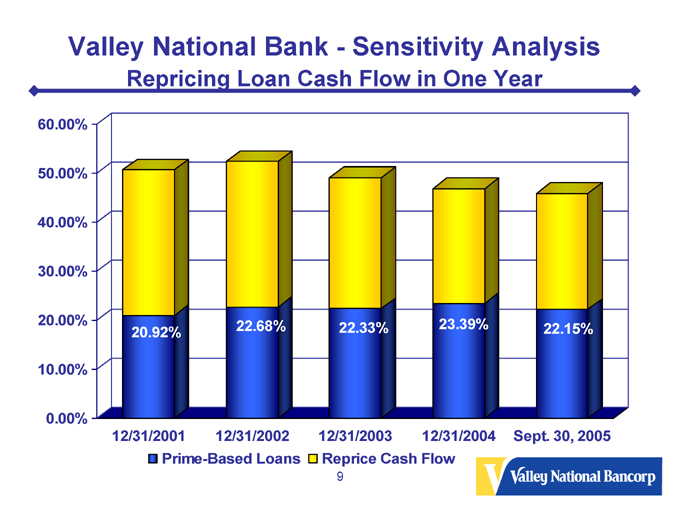

Valley National Bank—Sensitivity Analysis

Repricing Loan Cash Flow in One Year

60.00% 50.00% 40.00% 30.00% 20.00% 10.00% 0.00%

20.92%

22.68%

22.33%

23.39%

22.15%

12/31/2001 12/31/2002 12/31/2003 12/31/2004 Sept. 30, 2005

Prime-Based Loans

Reprice Cash Flow

9

Non-Performing Loans as a % of Loans 2000-2005

2.00%

1.50% Delinquency 1.00%

0.50%

0.00%

0.07%

0.35%

0.37%

0.36%

0.44%

0.30%

2000 2001 2002 2003 2004 9/30/2005

Year

10

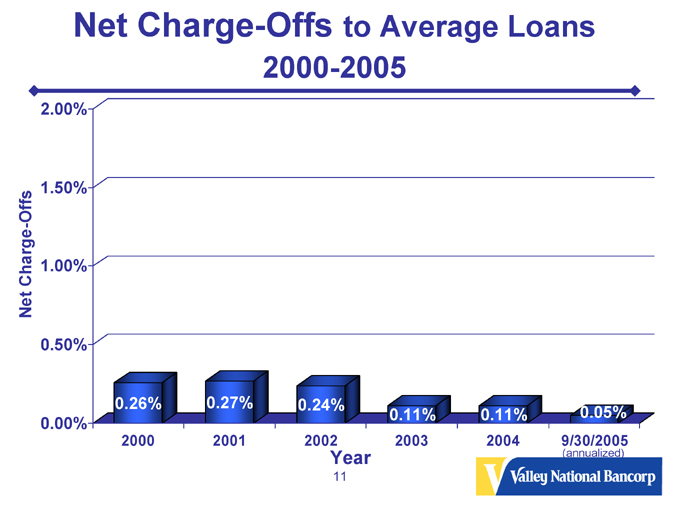

Net Charge-Offs to Average Loans

2000-2005

Net Charge-Offs

2.00% 1.50% 1.00% 0.50% 0.00%

0.26%

0.27%

0.24%

0.11%

0.11%

0.05%

2000 2001 2002 2003 2004

9/30/2005

(annualized)

Year

11

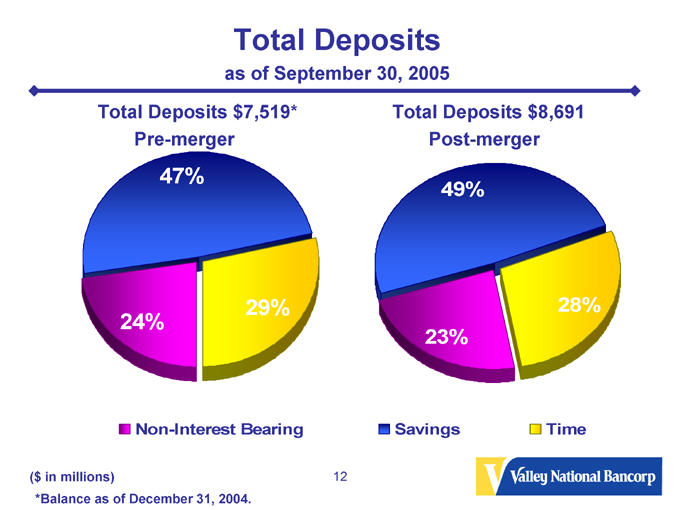

Total Deposits

as of September 30, 2005

Total Deposits $7,519* Pre-merger

47%

24%

29%

Non-Interest Bearing

Total Deposits $8,691 Post-merger

49%

23%

28%

Savings

Time

($ in millions)

*Balance as of December 31, 2004.

12

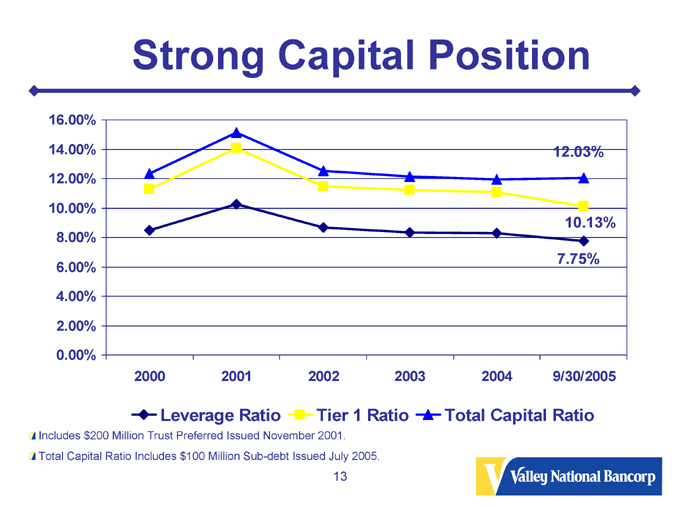

Strong Capital Position

16.00% 14.00% 12.00% 10.00% 8.00% 6.00% 4.00% 2.00% 0.00%

12.03%

10.13%

7.75%

2000 2001 2002 2003 2004 9/30/2005

Leverage Ratio

Tier 1 Ratio

Total Capital Ratio

Includes $200 Million Trust Preferred Issued November 2001. Total Capital Ratio Includes $100 Million Sub-debt Issued July 2005.

13

Unrealized Capital Position

(as of September 30, 2005)

Marked-to-Market Facilities

Number of facilities owned—73

Book value of facilities owned – $82 Million

Approximate Market Value of

Facilities owned—$280 Million

14

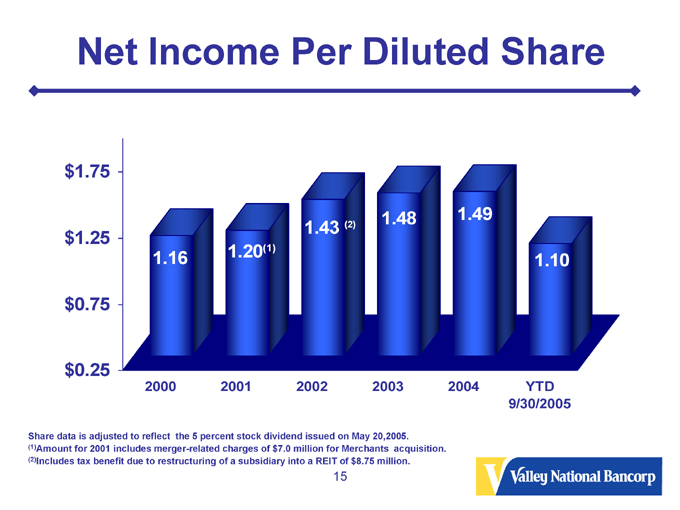

Net Income Per Diluted Share $1.75 $1.25 $0.75 $0.25

1.16

1.20(1)

1.43 (2)

1.48

1.49

1.10

2000 2001 2002 2003 2004 YTD

9/30/2005

Share data is adjusted to reflect the 5 percent stock dividend issued on May 20,2005. (1)Amount for 2001 includes merger-related charges of $7.0 million for Merchants acquisition. (2)Includes tax benefit due to restructuring of a subsidiary into a REIT of $8.75 million.

15

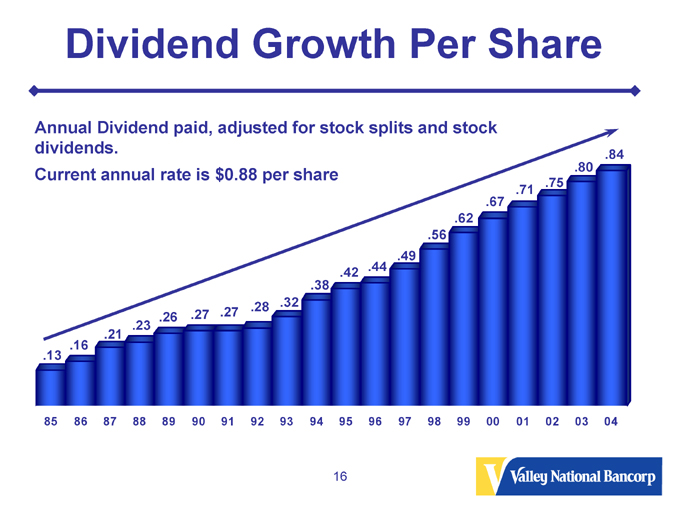

Dividend Growth Per Share

Annual Dividend paid, adjusted for stock splits and stock dividends.

Current annual rate is $0.88 per share

.13

.16

.21

.23

.26

.27

.27

.28

.32

.38

.42

.44

.49

.56

.62

.67

.71

.75

.80

.84

85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04

16

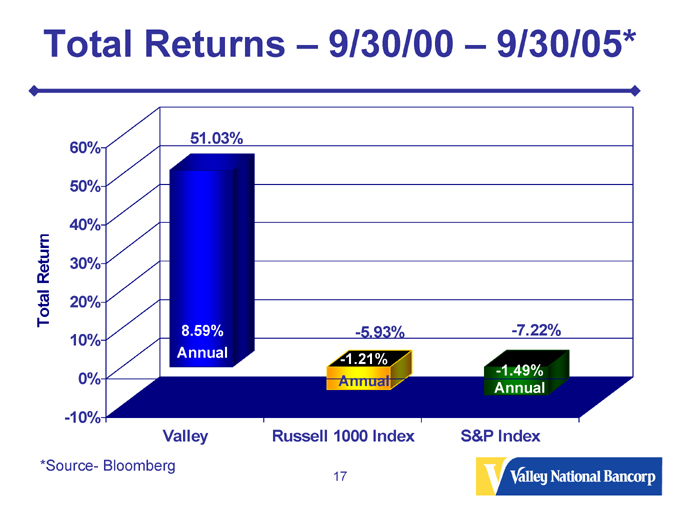

Total Returns – 9/30/00 – 9/30/05*

Total Return

60% 50% 40% 30% 20% 10% 0% -10%

8.59% Annual

51.03%

-1.21% Annual

-5.93%

-1.49% Annual

-7.22%

Valley Russell 1000 Index S&P Index

*Source- Bloomberg

17

Valley National Bancorp

Growth Strategy

18

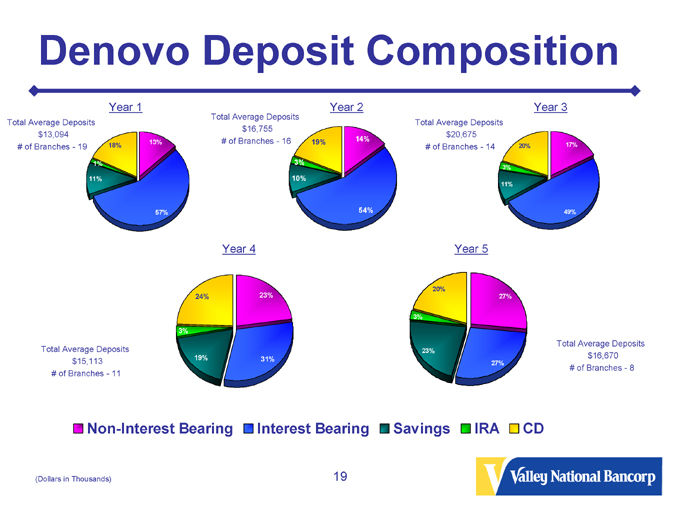

Denovo Deposit Composition

Year 1

Total Average Deposits $13,094 # of Branches—19

18%

13%

1%

11%

57%

Year 2

Total Average Deposits $16,755 # of Branches—16

19%

14%

3%

10%

54%

Year 3

Total Average Deposits $20,675 # of Branches—14

20%

17%

3%

11%

49%

Year 4

Total Average Deposits $15,113 # of Branches—11

24%

23%

3%

19%

31%

Year 5

Total Average Deposits $16,670 # of Branches—8

20%

27%

3%

23%

27%

Non-Interest Bearing

Interest Bearing

Savings

IRA

CD

(Dollars in Thousands)

19

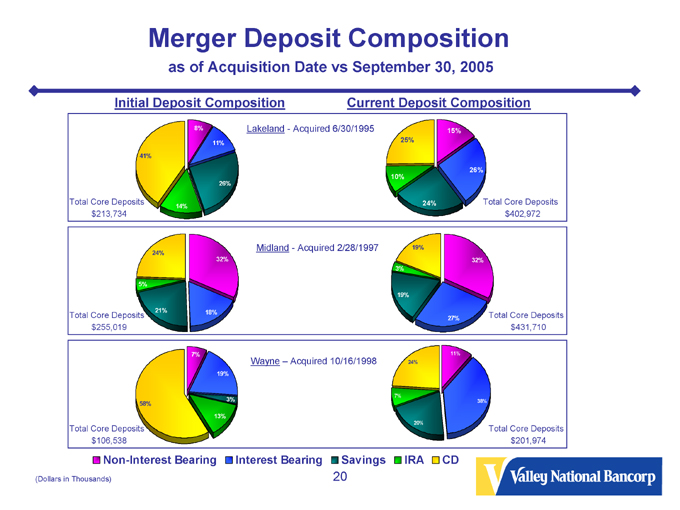

Merger Deposit Composition

as of Acquisition Date vs September 30, 2005

Initial Deposit Composition

Lakeland—Acquired 6/30/1995

8%

11%

26%

14%

41%

Total Core Deposits $213,734

Midland—Acquired 2/28/1997

24%

32%

18%

21%

5%

Total Core Deposits $255,019

Wayne – Acquired 10/16/1998

7%

19%

3%

13%

58%

Total Core Deposits $106,538

Current Deposit Composition

15%

25%

10%

24%

26%

Total Core Deposits $402,972

19%

3%

19%

32%

27%

Total Core Deposits $431,710

11%

24%

7%

20%

38%

Total Core Deposits $201,974

Non-Interest Bearing

Interest Bearing

Savings

IRA

CD

(Dollars in Thousands)

20

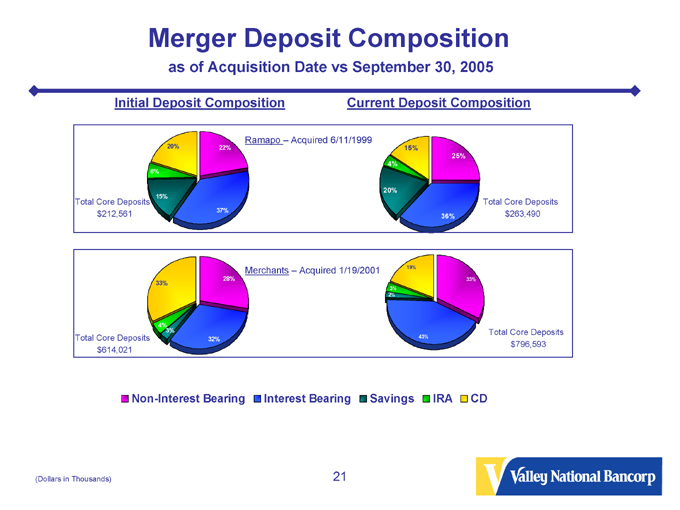

Merger Deposit Composition

as of Acquisition Date vs September 30, 2005

Initial Deposit Composition

Current Deposit Composition

Ramapo – Acquired 6/11/1999

22%

20%

6%

15%

37%

Total Core Deposits $212,561

25%

15%

4%

20%

36%

Total Core Deposits $263,490

Merchants – Acquired 1/19/2001

28%

33%

4% 3%

32%

Total Core Deposits $614,021

19%

3% 2%

33%

43%

Total Core Deposits $796,593

Non-Interest Bearing

Interest Bearing

Savings

IRA

CD

(Dollars in Thousands)

21

Valley National Bancorp

Average Life Distribution of Nonmaturity Deposits (as of September 30, 2005)

Account Life (in years)

25.00 20.00 15.00 10.00 5.00 0.00

11.57

1.48

13.02

3.20

6.63

1.38

5.92

3.20

23.81

3.20

Commercial DDA Retail DDA Money Market Savings NOW

Deposit Types

Valley

Regulatory FDICIA 305 Guidelines

22

Future Goals

Maintain exceptional asset quality

Remain aggressive and active in the lending community Emphasize business lending Take advantage of changing market in the Tri-State area Focused growth within sixty miles of Valley’s headquarters through new branches and acquisitions of other financial institutions with a similar customer culture

23

For More Information

Log onto our web site: www.valleynationalbank.com Visit our kids site: www.vnbkids.com E-mail requests to: dgrenz@valleynationalbank.com Call Shareholder Relations at: (973) 305-3380

Write to: Valley National Bank

1455 Valley Road

Wayne, New Jersey 07470

Attn: Dianne M. Grenz, Senior Vice President Director of Shareholder & Public Relations

Log onto www.sec.gov to obtain free copies of documents filed by Valley with the SEC

24