Filed Pursuant to Rule 424(b)(5)

Registration File No. 333-181718

This preliminary prospectus supplement relates to an effective registration statement under the Securities Act of 1933, as amended, but it is not complete and may be changed. This preliminary prospectus supplement is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

Subject to Completion, Dated April 10, 2013

Prospectus Supplement to Prospectus dated May 25, 2012.

$819,613,000

2013-1 Pass Through Trusts

Pass Through Certificates, Series 2013-1

Two classes of the US Airways Pass Through Certificates, Series 2013-1, are being offered under this prospectus supplement: Class A and Class B. US Airways may subsequently offer a single additional class of US Airways Pass Through Certificates, Series 2013-1: Class C, after the date of this prospectus supplement. Class C certificates are not being offered under this prospectus supplement. A separate trust will be established for each class of certificates that are issued. The proceeds from the sale of certificates will initially be held in escrow, and interest on the escrowed funds will be payable semiannually on May 15 and November 15, commencing November 15, 2013. The trusts will use the escrowed funds to acquire equipment notes. The equipment notes will be issued by US Airways and will be secured by eighteen (18) new Airbus aircraft scheduled for delivery from September 2013 to June 2014. Payments on the equipment notes held in each trust will be passed through to the holders of certificates of such trust.

Interest on the equipment notes will be payable semiannually on each May 15 and November 15 after issuance. Principal payments on the equipment notes are scheduled on May 15 and November 15 of each year, beginning on November 15, 2014.

The Class A certificates will rank senior to the other certificates. The Class B certificates will rank junior to the Class A certificates and will rank senior to the Class C certificates, if issued. The Class C certificates, if issued, will rank junior to the other certificates.

Natixis S.A., acting through its New York Branch, will provide a liquidity facility for the Class A certificates and the Class B certificates, in each case, in an amount sufficient to make three semiannual interest payments.

The payment obligations of US Airways under the equipment notes will be fully and unconditionally guaranteed by US Airways Group, Inc.

The certificates will not be listed on any national securities exchange.

Investing in the certificates involves risks. See “Risk Factors” beginning on page S-19.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus supplement or the accompanying prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

| | | | | | | | | | | | | | | | |

Pass Through Certificates | | Face

Amount | | | Interest

Rate | | | Final Expected

Distribution Date | | | Price to

Public(1) | |

Class A | | $ | 620,095,000 | | | | | % | | | November 15, 2025 | | | | 100 | % |

Class B | | $ | 199,518,000 | | | | | % | | | November 15, 2021 | | | | 100 | % |

| (1) | Plus accrued interest, if any, from the date of issuance. |

The underwriters will purchase all of the Class A and Class B certificates if any are purchased. The aggregate proceeds from the sale of the certificates will be $819,613,000. US Airways will pay the underwriters a commission of $ . Delivery of the certificates in book-entry form only will be made on or about , 2013.

Joint Bookrunners

| | | | |

| Goldman, Sachs & Co. | | Citigroup | | Morgan Stanley |

| Structuring Agent | | | | |

Co-Managers

| | | | |

| | |

| Barclays | | BofA Merrill Lynch | | Natixis |

Prospectus Supplement dated , 2013

TABLE OF CONTENTS

Prospectus Supplement

S-i

S-ii

Prospectus

You should rely only on the information contained in this document or to which this document refers you. We have not authorized anyone to provide you with information that is different. This document may be used only where it is legal to sell these securities. The information in this document may be accurate only on the date of this document.

S-iii

ABOUT THIS PROSPECTUS SUPPLEMENT

This document is in two parts. The first part is this prospectus supplement, which describes the specific terms of this offering (the “Offering”). The second part, the accompanying prospectus, gives more general information about our pass through certificates, some of which may not apply to this Offering. You should read both this prospectus supplement and the accompanying prospectus, together with the additional information described in this prospectus and the base prospectus under the headings “Incorporation of Certain Documents by Reference” and “Where You Can Find More Information.”

If the description of this offering varies between this prospectus supplement and the accompanying prospectus, you should rely on the information in this prospectus supplement.

Information contained on our website does not constitute part of this prospectus supplement or the accompanying prospectus.

In this prospectus supplement, all references to “we,” “us,” “our,” “US Airways Group,” the “Company” and similar designations refer to US Airways Group, Inc. and its consolidated subsidiaries, unless the context indicates otherwise. References to “US Airways” refer to US Airways, Inc.

S-iv

SPECIAL NOTE ABOUT FORWARD-LOOKING STATEMENTS

Certain statements in this prospectus supplement and in the accompanying prospectus and other materials filed or to be filed with the Securities and Exchange Commission (“SEC”) (or otherwise made by US Airways Group, US Airways or on our behalf) should be considered “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). These forward-looking statements may be identified by words such as “may,” “will,” “expect,” “intend,” “anticipate,” “believe,” “estimate,” “plan,” “project,” “could,” “should,” “would,” “continue” and similar terms used in connection with statements regarding, among others, our outlook, expected fuel costs, the revenue and pricing environment, and our expected financial performance and liquidity position. These statements include, but are not limited to, statements about future financial and operating results, our plans, objectives, expectations and intentions and other statements that are not historical facts. These statements are based upon the current beliefs and expectations of management and are subject to significant risks and uncertainties that could cause our actual results and financial position to differ materially from these statements. These risks and uncertainties include, but are not limited to, those described below under “Risk Factors” and the following:

| | Ÿ | | the impact of significant operating losses in the future; |

| | Ÿ | | downturns in economic conditions and their impact on passenger demand, booking practices and related revenues; |

| | Ÿ | | the impact of the price and availability of fuel and significant disruptions in the supply of aircraft fuel; |

| | Ÿ | | competitive practices in the industry, including the impact of industry consolidation; |

| | Ÿ | | increased costs of financing, a reduction in the availability of financing and fluctuations in interest rates; |

| | Ÿ | | our high level of fixed obligations and our ability to fund general corporate requirements, obtain additional financing and respond to competitive developments; |

| | Ÿ | | any failure to comply with the liquidity covenants contained in our financing arrangements; |

| | Ÿ | | provisions in our credit card processing and other commercial agreements that may affect our liquidity; |

| | Ÿ | | the impact of union disputes, employee strikes and other labor-related disruptions; |

| | Ÿ | | our inability to maintain labor costs at competitive levels; |

| | Ÿ | | interruptions or disruptions in service at one or more of our hub airports; |

| | Ÿ | | regulatory changes affecting the allocation of slots; |

| | Ÿ | | our reliance on third-party regional operators or third-party service providers; |

| | Ÿ | | our reliance on and costs, rights and functionality of third-party distribution channels, including those provided by global distribution systems, conventional travel agents and online travel agents; |

| | Ÿ | | changes in government regulation; |

| | Ÿ | | the impact of changes to our business model; |

| | Ÿ | | the loss of key personnel or our ability to attract and retain qualified personnel; |

| | Ÿ | | the impact of conflicts overseas or terrorist attacks, and the impact of ongoing security concerns; |

S-v

| | Ÿ | | our ability to operate and grow our route network; |

| | Ÿ | | the impact of environmental regulation; |

| | Ÿ | | our reliance on technology and automated systems and the impact of any failure or disruption of, or delay in, these technologies or systems; |

| | Ÿ | | costs of ongoing data security compliance requirements and the impact of any significant data security breach; |

| | Ÿ | | the impact of any accident involving our aircraft or the aircraft of our regional operators; |

| | Ÿ | | delays in scheduled aircraft deliveries or other loss of anticipated fleet capacity; |

| | Ÿ | | our dependence on a limited number of suppliers for aircraft, aircraft engines and parts; |

| | Ÿ | | our ability to operate profitably out of Philadelphia International Airport; |

| | Ÿ | | the impact of weather conditions and seasonality of airline travel; |

| | Ÿ | | the impact of possible future increases in insurance costs or reductions in available insurance coverage; |

| | Ÿ | | the impact of global events that affect travel behavior, such as an outbreak of a contagious disease; |

| | Ÿ | | the impact of foreign currency exchange rate fluctuations; |

| | Ÿ | | our ability to use NOLs and certain other tax attributes; |

| | Ÿ | | risks relating to our anticipated merger with AMR Corporation (“AMR”); and |

| | Ÿ | | other risks and uncertainties listed from time to time in our reports to and filings with the SEC. |

All of the forward-looking statements are qualified in their entirety by reference to the risks and uncertainties discussed in the “Risk Factors” section and elsewhere in this prospectus supplement and in the accompanying prospectus and other materials filed or to be filed with the SEC (or otherwise made by US Airways Group, US Airways or on our behalf). There may be other factors not identified above, or in the “Risk Factors” section, of which we are not currently aware, that may affect matters discussed in the forward-looking statements and may also cause actual results to differ materially from those discussed. We assume no obligation to publicly update or supplement any forward-looking statement to reflect actual results, changes in assumptions or changes in other factors affecting these estimates other than as required by law. Any forward-looking statements speak only as of the date of this prospectus supplement or the accompanying prospectus or as of the dates indicated in the statements.

S-vi

PROSPECTUS SUPPLEMENT SUMMARY

This summary highlights selected information from this prospectus supplement and the accompanying prospectus and may not contain all of the information that is important to you. For more complete information about the Certificates and us, you should read this entire prospectus supplement and the accompanying prospectus, as well as the materials filed with the SEC that are considered to be part of this prospectus supplement and the accompanying prospectus. See “Incorporation of Certain Documents by Reference” in this prospectus supplement and “Where You Can Find More Information” in the accompanying prospectus.

US Airways Group

US Airways Group is a holding company whose primary business activity is the operation of a major network air carrier through its wholly owned subsidiaries US Airways, Piedmont Airlines, Inc. (“Piedmont”), PSA Airlines, Inc. (“PSA”), Material Services Company, Inc. and Airways Assurance Limited. We operate the fifth largest airline in the United States as measured by domestic revenue passenger miles and available seat miles. We have hubs in Charlotte, Philadelphia, Phoenix and Washington, D.C. We offer scheduled passenger service on more than 3,000 flights daily to 198 communities in the United States, Canada, Mexico, Europe, the Middle East, the Caribbean, and Central and South America. We also have an established East Coast route network, including the US Airways Shuttle service. We had approximately 54 million passengers boarding our mainline flights in 2012. During 2012, our mainline operation provided regularly scheduled service or seasonal service at 130 airports while the US Airways Express network served 157 airports in the United States, Canada, Mexico and the Caribbean, including 78 airports also served by our mainline operation. US Airways Express air carriers had approximately 28 million passengers boarding their planes in 2012. As of December 31, 2012, we operated 340 mainline jets and were supported by our regional airline subsidiaries and affiliates operating as US Airways Express under capacity purchase agreements, which operated 238 regional jets and 44 turboprops. Our prorate carriers operated four regional jets at December 31, 2012.

US Airways Group is a Delaware corporation formed in 1982 whose origins trace back to the formation of All American Aviation in 1939. Our principal executive offices are located at 111 West Rio Salado Parkway, Tempe, Arizona 85281. Our telephone number is (480) 693-0800, and our internet address is www.usairways.com. Our wholly owned subsidiary, US Airways, is also a Delaware corporation. Information contained on our website does not constitute part of this prospectus supplement or the accompanying prospectus.

Recent Developments

On February 13, 2013, we entered into an Agreement and Plan of Merger (the “Merger Agreement”) with AMR and a wholly owned subsidiary of AMR (“Merger Sub”), which provides for a business combination of AMR and US Airways Group. The Merger Agreement provides that, upon the terms and subject to the conditions set forth in the Merger Agreement, Merger Sub will merge with and into US Airways Group (the “Merger”), with US Airways Group as the surviving corporation and as a wholly owned subsidiary of AMR. The Merger Agreement and the transactions contemplated thereby, including the Merger, are subject to the approval of the United States Bankruptcy Court for the Southern District of New York (the “Bankruptcy Court”), and are to be effected pursuant to a plan of reorganization (the “Reorganization Plan”) of AMR and certain of its direct and indirect domestic subsidiaries (the “Debtors”) in connection with their currently pending cases under Chapter 11 of Title 11 of the United States Code, 11 U.S.C.

S-1

Sections 101 et seq. (the “Bankruptcy Code”). The Reorganization Plan is subject to confirmation and consummation in accordance with the requirements of the Bankruptcy Code. Consummation of the Merger is subject to customary conditions, including approval of our stockholders and certain regulatory approvals. For additional information on the Merger and the Merger Agreement, see Part I, Item 1, “Business—Recent Developments” in our most recent Annual Report on Form 10-K.

Summary of Terms of Certificates

| | | | |

| | | Class A Certificates | | Class B Certificates |

Aggregate Face Amount | | $620,095,000 | | $199,518,000 |

Interest Rate | | % | | % |

Initial Loan to Aircraft Value (cumulative)(1) | | 54.3% | | 72.1% |

Highest Loan to Aircraft Value (cumulative)(2) | | 54.3% | | 72.1% |

Expected Principal Distribution Window (in years) | | 1.6-12.6 | | 1.6-8.6 |

Initial Average Life (in years from Issuance Date) | | 8.5 | | 7.2 |

Regular Distribution Dates | | May 15 and

November 15 | | May 15 and

November 15 |

Final Expected Distribution Date | | November 15, 2025 | | November 15, 2021 |

Final Maturity Date | | May 15, 2027 | | May 15, 2023 |

Minimum Denomination | | $1,000 | | $1,000 |

Section 1110 Protection | | Yes | | Yes |

Liquidity Facility Coverage | | 3 semiannual

interest payments | | 3 semiannual

interest payments |

| (1) | These percentages are determined as of November 15, 2014, the first Regular Distribution Date after all Aircraft are expected to have been financed pursuant to the Offering. In calculating these percentages, we have assumed that the financings of all Aircraft hereunder are completed prior to such date and that the aggregate appraised value of such Aircraft is $1,108,725,575 as of such date. The appraised value is only an estimate and reflects certain assumptions. See “Description of the Aircraft and the Appraisals—The Appraisals.” |

| (2) | See “—Loan to Aircraft Value Ratios.” |

S-2

Equipment Notes and the Aircraft

The eighteen (18) Aircraft to be financed pursuant to this Offering will consist of fourteen (14) new Airbus A321-231 aircraft and four (4) new Airbus A330-243 aircraft, all of which are scheduled to be delivered from September 2013 to June 2014. See “Description of the Aircraft and the Appraisals” for a description of the fourteen (14) new Airbus A321-231 aircraft and four (4) new Airbus A330-243 aircraft to be financed pursuant to this Offering. Set forth below is certain information about the Equipment Notes expected to be held in the Trusts and the Aircraft expected to secure such Equipment Notes:

| | | | | | | | | | | | | | | | | | |

Aircraft Type | | Registration

Number(1) | | | Manufacturer’s

Serial Number(1) | | | Delivery Month(1) | | Principal

Amount of

Equipment

Notes | | | Appraised

Value(2) | |

A321-231 | | | N568UW | | | | 5751 | | | September 2013 | | $ | 38,290,000 | | | $ | 52,960,000 | |

A321-231 | | | N569UW | | | | 5763 | | | September 2013 | | | 38,290,000 | | | | 52,960,000 | |

A321-231 | | | N570UW | | | | 5795 | | | October 2013 | | | 38,355,000 | | | | 53,050,000 | |

A321-231 | | | N571UW | | | | 5800 | | | October 2013 | | | 38,355,000 | | | | 53,050,000 | |

A321-231 | | | N572UW | | | | TBD | | | December 2013 | | | 38,478,000 | | | | 53,220,000 | |

A321-231 | | | N573UW | | | | TBD | | | January 2014 | | | 38,543,000 | | | | 53,310,000 | |

A321-231 | | | N575UW | | | | TBD | | | February 2014 | | | 38,608,000 | | | | 53,400,000 | |

A321-231 | | | N576UW | | | | TBD | | | March 2014 | | | 38,673,000 | | | | 53,490,000 | |

A321-231 | | | N578UW | | | | TBD | | | March 2014 | | | 38,673,000 | | | | 53,490,000 | |

A321-231 | | | N579UW | | | | TBD | | | April 2014 | | | 38,738,000 | | | | 53,580,000 | |

A321-231 | | | N580UW | | | | TBD | | | May 2014 | | | 38,796,000 | | | | 53,660,000 | |

A321-231 | | | N581UW | | | | TBD | | | May 2014 | | | 38,796,000 | | | | 53,660,000 | |

A321-231 | | | N582UW | | | | TBD | | | June 2014 | | | 38,861,000 | | | | 53,750,000 | |

A321-231 | | | N583UW | | | | TBD | | | June 2014 | | | 38,861,000 | | | | 53,750,000 | |

A330-243 | | | N290AY | | | | TBD | | | December 2013 | | | 69,480,000 | | | | 96,100,000 | |

A330-243 | | | N291AY | | | | TBD | | | March 2014 | | | 69,770,000 | | | | 96,500,000 | |

A330-243 | | | N292AY | | | | TBD | | | April 2014 | | | 70,023,000 | | | | 96,850,000 | |

A330-243 | | | N293AY | | | | TBD | | | May 2014 | | | 70,023,000 | | | | 96,850,000 | |

| (1) | The indicated registration number, manufacturer’s serial number and delivery month for each aircraft reflect our current expectations, although these may differ for the actual aircraft financed hereunder. The financing of each newly delivered Airbus aircraft is expected to be effected at delivery of such aircraft from Airbus to US Airways. The actual delivery date for any new Airbus aircraft may be subject to delay or acceleration. The deadline for purposes of financing an Aircraft pursuant to this Offering is August 31, 2014. See “Description of the Aircraft and the Appraisals—Timing of Financing the Aircraft.” US Airways has certain rights to substitute other Airbus aircraft if the scheduled delivery date of any of the new Airbus aircraft eligible to be financed pursuant to this Offering is delayed for more than 30 days after the month scheduled for delivery or beyond the delivery deadline. See “Description of the Aircraft and the Appraisals—Substitute Aircraft.” |

| (2) | The appraised value of each Aircraft set forth above is the lesser of the average and median values of such Aircraft as appraised by three independent appraisal and consulting firms. Such appraisals indicate appraised base value, projected as of the scheduled delivery month of the applicable aircraft. These appraisals are based upon varying assumptions and methodologies. An appraisal is only an estimate of value and should not be relied upon as a measure of realizable value. See “Risk Factors—Risk Factors Relating to the Certificates and the Offering—The Appraisals are only Estimates of Aircraft Value.” |

S-3

Loan to Aircraft Value Ratios

The following table sets forth loan to Aircraft value ratios (“LTVs”) for each Class of Certificates as of November 15, 2014 the first Regular Distribution Date after all Aircraft are expected to have been financed pursuant to the Offering, and each Regular Distribution Date thereafter. The LTVs for any Class of Certificates for the period prior to November 15, 2014, are not meaningful because during such period all of the Equipment Notes expected to be acquired by the Trusts and the related Aircraft will not be included in the calculation. The table should not be considered a forecast or prediction of expected or likely LTVs but simply a mathematical calculation based on one set of assumptions. See “Risk Factors—Risk Factors Relating to the Certificates and the Offering—The Appraisals are only Estimates of Aircraft Value.”

| | | | | | | | | | | | | | | | | | | | |

Regular Distribution Date | | Assumed

Aggregate

Aircraft Value(1) | | | Outstanding Balance(2) | | | LTV(3) | |

| | | Class A

Certificates | | | Class B

Certificates | | | Class A

Certificates | | | Class B

Certificates | |

November 15, 2014 | | $ | 1,108,725,575 | | | $ | 602,038,000 | | | $ | 197,354,000 | | | | 54.3 | % | | | 72.1 | % |

May 15, 2015 | | | 1,091,721,125 | | | | 581,061,888 | | | | 192,915,122 | | | | 53.2 | % | | | 70.9 | % |

November 15, 2015 | | | 1,074,716,675 | | | | 560,949,599 | | | | 186,686,217 | | | | 52.2 | % | | | 69.6 | % |

May 15, 2016 | | | 1,057,712,225 | | | | 540,439,187 | | | | 180,894,675 | | | | 51.1 | % | | | 68.2 | % |

November 15, 2016 | | | 1,040,707,775 | | | | 520,302,896 | | | | 174,508,999 | | | | 50.0 | % | | | 66.8 | % |

May 15, 2017 | | | 1,023,703,325 | | | | 499,516,994 | | | | 167,512,615 | | | | 48.8 | % | | | 65.2 | % |

November 15, 2017 | | | 1,006,698,875 | | | | 479,139,188 | | | | 162,716,665 | | | | 47.6 | % | | | 63.8 | % |

May 15, 2018 | | | 989,694,425 | | | | 461,148,878 | | | | 157,988,734 | | | | 46.6 | % | | | 62.6 | % |

November 15, 2018 | | | 972,689,975 | | | | 445,444,050 | | | | 153,328,809 | | | | 45.8 | % | | | 61.6 | % |

May 15, 2019 | | | 955,685,525 | | | | 426,188,547 | | | | 148,736,905 | | | | 44.6 | % | | | 60.2 | % |

November 15, 2019 | | | 938,681,075 | | | | 404,525,103 | | | | 143,274,343 | | | | 43.1 | % | | | 58.4 | % |

May 15, 2020 | | | 921,676,625 | | | | 382,450,113 | | | | 138,835,486 | | | | 41.5 | % | | | 56.6 | % |

November 15, 2020 | | | 904,672,175 | | | | 360,014,594 | | | | 134,464,648 | | | | 39.8 | % | | | 54.7 | % |

May 15, 2021 | | | 887,667,725 | | | | 338,157,224 | | | | 129,274,161 | | | | 38.1 | % | | | 52.7 | % |

November 15, 2021 | | | 870,663,275 | | | | 316,007,352 | | | | 0 | | | | 36.3 | % | | | 0.0 | % |

May 15, 2022 | | | 853,658,825 | | | | 295,323,303 | | | | 0 | | | | 34.6 | % | | | 0.0 | % |

November 15, 2022 | | | 836,654,375 | | | | 275,217,394 | | | | 0 | | | | 32.9 | % | | | 0.0 | % |

May 15, 2023 | | | 819,649,925 | | | | 254,869,984 | | | | 0 | | | | 31.1 | % | | | 0.0 | % |

November 15, 2023 | | | 802,645,475 | | | | 235,134,749 | | | | 0 | | | | 29.3 | % | | | 0.0 | % |

May 15, 2024 | | | 785,641,025 | | | | 216,011,665 | | | | 0 | | | | 27.5 | % | | | 0.0 | % |

November 15, 2024 | | | 768,636,575 | | | | 196,732,101 | | | | 0 | | | | 25.6 | % | | | 0.0 | % |

May 15, 2025 | | | 751,632,125 | | | | 178,098,708 | | | | 0 | | | | 23.7 | % | | | 0.0 | % |

November 15, 2025 | | | 734,627,675 | | | | 0 | | | | 0 | | | | 0.0 | % | | | 0.0 | % |

| (1) | In calculating the assumed aggregate aircraft values above, we assumed that the initial appraised value of each Aircraft, determined as described under “—Equipment Notes and the Aircraft,” declines by approximately 3% per year for the first fifteen (15) years after the year of delivery of such Aircraft, in each case prior to the final expected Regular Distribution Date. Other rates or methods of depreciation may result in materially different LTVs. We cannot assure you that the depreciation rate and method used for purposes of the table will occur or predict the actual future value of any Aircraft. See “Risk Factors—Risk Factors Relating to the Certificates and the Offering—The Appraisals are only Estimates of Aircraft Value.” |

| (2) | In calculating the outstanding balances of each Class of Certificates, we have assumed that the Trusts will acquire the Equipment Notes for all Aircraft. Outstanding balances as of each Regular Distribution Date are shown after giving effect to distributions expected to be made on such distribution date. |

S-4

| (3) | The LTVs for each Class of Certificates were obtained for each Regular Distribution Date by dividing (i) the expected outstanding balance of such Class together with the expected outstanding balance of each other class senior in right of payment to such class after giving effect to the distributions expected to be made on such distribution date, by (ii) the assumed value of all of the Aircraft on such date based on the assumptions described above. The outstanding balances and LTVs of each Class of Certificates will change if the Trusts do not acquire Equipment Notes with respect to all the Aircraft. |

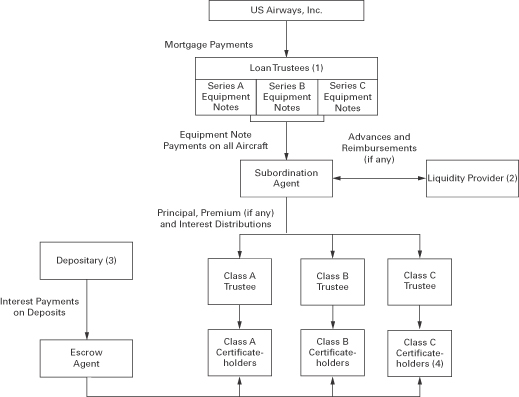

Cash Flow Structure

Set forth below is a diagram illustrating the structure for the offering of the Certificates and certain cash flows.

| (1) | The Equipment Notes with respect to each Aircraft will be issued under a separate Indenture. |

| (2) | The Liquidity Facility for each of the Class A Certificates and the Class B Certificates will be sufficient to cover up to three consecutive semiannual interest payments with respect to such Class, except that the Liquidity Facilities will not cover interest on the Deposits. There will be no liquidity facility for the Class C Certificates if any Class C Certificates are issued. |

| (3) | The proceeds of the offering of each Class of Certificates will initially be held in escrow and deposited with the Depositary, pending financing of each Aircraft. The Depositary will hold such funds as interest-bearing Deposits. Each Trust will withdraw funds from the Deposits relating to such Trust to purchase Equipment Notes from time to time as each Aircraft is financed. The scheduled payments of interest on the Equipment Notes and on the Deposits relating to a Trust, taken together, will be sufficient to pay accrued interest on the outstanding Certificates of such |

S-5

| | Trust. If any funds remain as Deposits with respect to a Trust at the Delivery Period Termination Date, such funds will be withdrawn by the Escrow Agent and distributed to the holders of the Certificates issued by such Trust, together with accrued and unpaid interest thereon. No interest will accrue with respect to the Deposits after they have been fully withdrawn. |

| (4) | Class C Certificates are not being offered under this prospectus supplement, but Class C Certificates may be offered at any time after the date of this prospectus supplement. |

The Offering

| | |

Certificates Offered | | Ÿ Class A Pass Through Certificates, Series 2013-1. |

| |

| | Ÿ Class B Pass Through Certificates, Series 2013-1. |

| |

| | If US Airways elects to offer Class C Certificates after the date of this prospectus supplement, a Class C pass through trust will be formed in order to issue such Class C Pass Through Certificates. Class C Pass Through Certificates are not being offered under this prospectus supplement. Each Class of Certificates will represent a fractional undivided interest in a related Trust. |

| |

Use of Proceeds | | The proceeds from the sale of the Certificates of each Trust will initially be held in escrow and deposited with the Depositary, pending financing of each Aircraft under this Offering. Each Trust will withdraw funds from the Deposits relating to such Trust to acquire Equipment Notes as these Aircraft are financed. The Equipment Notes will be issued to finance the purchase by US Airways of eighteen (18) new Airbus aircraft. |

| |

Subordination Agent, Trustee, Paying Agent and Loan Trustee | |

Wilmington Trust Company. |

| |

Escrow Agent | | Wilmington Trust, National Association. |

| |

Depositary | | Natixis S.A., acting through its New York Branch. |

| |

Liquidity Provider | | Natixis S.A., acting through its New York Branch. |

| |

Trust Property | | The property of each Trust will include: |

| |

| | Ÿ Equipment Notes acquired by such Trust. |

| |

| | Ÿ The UAG Guarantee (as defined below) with respect to such Equipment Notes. |

| | Ÿ With respect to the Class A Trust and the Class B Trust, all monies receivable under the Liquidity Facility for such Trust. |

| |

| | Ÿ Funds from time to time deposited with the applicable Trustee in accounts relating to such Trust, including payments made by US Airways on the Equipment Notes held in such Trust. |

S-6

| | |

UAG Guarantee | | US Airways Group, Inc. will unconditionally guarantee the payment obligations of US Airways under each Equipment Note issued by US Airways pursuant to a guarantee agreement (the “UAG Guarantee”). |

| |

Regular Distribution Dates | | May 15 and November 15, commencing on November 15, 2013. |

| |

Record Dates | | The fifteenth day preceding the related Distribution Date. |

| |

Distributions | | The Trustee will distribute all payments of principal, premium (if any) and interest received on the Equipment Notes held in each Trust to the holders of the Certificates of such Trust, subject to the subordination provisions applicable to the Certificates. |

| |

| | Scheduled payments of principal and interest made on the Equipment Notes will be distributed on the applicable Regular Distribution Dates. |

| |

| | Payments of principal, premium (if any) and interest made on the Equipment Notes resulting from any early redemption of such Equipment Notes will be distributed on a special distribution date after not less than 15 days’ notice from the Trustee to the applicable Certificateholders. |

| |

Subordination | | Distributions on the Certificates will be made in the following order: |

| |

| | Ÿ First, to the holders of the Class A Certificates to pay interest on the Class A Certificates. Ÿ Second, to the holders of Class B Certificates to pay interest on the Preferred B Pool Balance. Ÿ Third, if any Class C Certificates have been issued, to the holders of the Class C Certificates to pay interest on the Preferred C Pool Balance. Ÿ Fourth, to the holders of the Class A Certificates to make distributions in respect of the Pool Balance of the Class A Certificates. Ÿ Fifth, to the holders of the Class B Certificates to pay interest on the Pool Balance of the Class B Certificates not previously distributed under clause “Second” above. Ÿ Sixth, to the holders of the Class B Certificates to make distributions in respect of the Pool Balance of the Class B Certificates. Ÿ Seventh, if any Class C Certificates have been issued, to the holders of the Class C Certificates to pay interest on the Pool Balance |

S-7

| | |

| |

| | of the Class C Certificates not previously distributed under clause “Third” above. Ÿ Eighth, if any Class C Certificates have been issued, to the holders of the Class C Certificates to make distributions in respect of the Pool Balance of the Class C Certificates. |

| |

Control of Loan Trustee | | The holders of at least a majority of the outstanding principal amount of Equipment Notes issued under each Indenture will be entitled to direct the Loan Trustee under such Indenture in taking action as long as no Indenture Default is continuing thereunder. If an Indenture Default is continuing, subject to certain conditions, the “Controlling Party” will direct the Loan Trustee under such Indenture (including in exercising remedies, such as accelerating such Equipment Notes or foreclosing the lien on the Aircraft securing such Equipment Notes). |

| |

| | The Controlling Party will be: |

| |

| | Ÿ The Class A Trustee. Ÿ Upon payment of final distributions to the holders of Class A Certificates, the Class B Trustee. Ÿ If any Class C Certificates have been issued, upon payment of final distributions to the holders of Class B Certificates, the Class C Trustee. Ÿ Under certain circumstances, and notwithstanding the foregoing, the Liquidity Provider with the largest amount owed to it. |

| |

| | In exercising remedies during the nine months after the earlier of (a) the acceleration of the Equipment Notes issued pursuant to any Indenture or (b) the bankruptcy of US Airways, the Equipment Notes and the Aircraft subject to the lien of such Indenture may not be sold for less than certain specified minimums. |

| |

Right to Purchase Other Classes of Certificates | | If US Airways is in bankruptcy and certain specified circumstances then exist: |

| |

| | Ÿ The Class B Certificateholders (other than US Airways or any of its affiliates) will have the right to purchase all but not less than all of the Class A Certificates. Ÿ If any Class C Certificates have been issued, the Class C Certificateholders (other than US Airways or any of its affiliates) will have the right to purchase all but not less than all of the Class A Certificates and the Class B Certificates. |

S-8

| | |

| | The purchase price will be the outstanding balance of the applicable Class or Classes of Certificates plus accrued and unpaid interest and other amounts due to the applicable Certificateholders. |

| |

Liquidity Facilities | | Under the Liquidity Facility for each of the Class A Trust and the Class B Trust, the Liquidity Provider will, if necessary, make advances in an aggregate amount sufficient to pay interest on the applicable Certificates on up to three successive semiannual Regular Distribution Dates at the applicable interest rate for such Certificates. Drawings under the Liquidity Facilities cannot be used to pay any amount in respect of the Certificates other than interest and will not cover interest payable on amounts held in escrow as Deposits with the Depositary. |

| |

| | Notwithstanding the subordination provisions applicable to the Certificates, the holders of the Certificates to be issued by the Class A Trust or the Class B Trust will be entitled to receive and retain the proceeds of drawings under the Liquidity Facility for such Trust. |

| |

| | Upon each drawing under any Liquidity Facility to pay interest on the Certificates, the Subordination Agent will reimburse the applicable Liquidity Provider for the amount of such drawing. Such reimbursement obligation and all interest, fees and other amounts owing to the Liquidity Provider under each Liquidity Facility and certain other agreements will rank equally with comparable obligations relating to the other Liquidity Facility and will rank senior to the Certificates in right of payment. |

| |

Escrowed Funds | | Funds in escrow for the Certificateholders of each Trust will be held by the Depositary as Deposits relating to such Trust. The Trustees may withdraw these funds from time to time to purchase Equipment Notes prior to the deadline established for purposes of this Offering. On each Regular Distribution Date, the Depositary will pay interest accrued on the Deposits relating to such Trust at a rate per annum equal to the interest rate applicable to the Certificates issued by such Trust. The Deposits relating to each Trust and interest paid thereon will not be subject to the subordination provisions applicable to the Certificates. The Deposits cannot be used to pay any other amount in respect of the Certificates. |

S-9

| | |

Unused Escrowed Funds | | All of the Deposits held in escrow might not be used to purchase Equipment Notes by the deadline established for purposes of this Offering. This may occur because of delays in the financing of Aircraft or other reasons. See “Description of the Certificates—Obligation to Purchase Equipment Notes.” If any funds remain as Deposits with respect to any Trust after such deadline, such funds will be withdrawn by the Escrow Agent for such Trust and distributed, with accrued and unpaid interest, to the Certificateholders of such Trust after at least 15 days’ prior written notice. See “Description of the Deposit Agreements—Unused Deposits.” |

| |

Obligation to Purchase Equipment Notes | | The Trustees will be obligated to purchase the Equipment Notes issued with respect to each Aircraft pursuant to the Note Purchase Agreement. US Airways will enter into a secured debt financing with respect to each Aircraft pursuant to financing agreements substantially in the forms attached to the Note Purchase Agreement. The terms of such financing agreements must not vary the Required Terms set forth in the Note Purchase Agreement. In addition, US Airways must certify to the Trustees that any substantive modifications do not materially and adversely affect the Certificateholders. US Airways must also obtain written confirmation from each Rating Agency that the use of financing agreements modified in any material respect from the forms attached to the Note Purchase Agreement will not result in a withdrawal, suspension or downgrading of the rating of any Class of Certificates. The Trustees will not be obligated to purchase Equipment Notes if, at the time of issuance, US Airways is in bankruptcy or certain other specified events have occurred. See “Description of the Certificates—Obligation to Purchase Equipment Notes.” |

Issuance of Class C Certificates | | After the Issuance Date, Class C Certificates, which will evidence fractional undivided ownership interests in equipment notes secured by Aircraft, may be issued. If Class C Certificates are issued, holders of Class C Certificates will have the right to purchase all, but not less than all, of the Class A Certificates and the Class B Certificates under certain circumstances after a bankruptcy of US Airways at the outstanding principal balance of the Certificates plus accrued and unpaid interest and other amounts due to Certificateholders, but without a premium. |

S-10

| | |

| | Consummation of the issuance of Class C Certificates will be subject to satisfaction of certain conditions, including receipt of confirmation from the Rating Agencies that it will not result in a withdrawal, suspension or downgrading of any Class of Certificates that remains outstanding. In addition, US Airways may elect to redeem and re-issue Series B Equipment Notes and Series C Equipment Notes, if any, in respect of all (but not less than all) of the Aircraft. In such case, US Airways will fund the sale of such Equipment Notes through the sale of pass through certificates issued by a US Airways pass through trust. See “Possible Issuance of Class C Certificates and Refinancing of Certificates.” |

| |

Equipment Notes | | |

| |

(a) Issuer | | US Airways, Inc. |

| |

(b) Interest | | The Equipment Notes held in each Trust will accrue interest at the rate per annum for the Certificates issued by such Trust set forth on the cover page of this prospectus supplement. Interest will be payable on May 15 and November 15 of each year, commencing on the first such date after issuance of such Equipment Notes. Interest is calculated on the basis of a 360-day year consisting of twelve 30-day months. |

| |

(c) Principal | | Principal payments on the Equipment Notes are scheduled on May 15 and November 15 of each year, commencing on November 15, 2014. |

| |

(d) Redemption | | Aircraft Event of Loss. If an Event of Loss occurs with respect to an Aircraft, all of the Equipment Notes issued with respect to such Aircraft will be redeemed, unless US Airways replaces such Aircraft under the related financing agreements. The redemption price in such case will be the unpaid principal amount of such Equipment Notes, together with accrued interest, but without any premium. |

| |

| | Optional Redemption. US Airways may elect to redeem all of the Equipment Notes issued with respect to an Aircraft prior to maturity;provided that all outstanding Equipment Notes with respect to all other Aircraft are simultaneously redeemed. In addition, US Airways may elect to redeem the Series B Equipment Notes or Series C Equipment Notes, if any, in connection with a refinancing of such Series. The redemption price in such case will be the unpaid principal amount of such Equipment Notes, together with accrued interest and Make-Whole Premium. |

S-11

| | |

(e) Security | | The Equipment Notes issued with respect to each Aircraft will be secured by a security interest in such Aircraft. |

| |

(f) Cross-collateralization | | The Equipment Notes held in the Trusts will be cross-collateralized. This means that any proceeds from the exercise of remedies with respect to an Aircraft will be available to cover shortfalls then due under Equipment Notes issued with respect to the other Aircraft. In the absence of any such shortfall, excess proceeds will be held by the relevant Loan Trustee as additional collateral for such other Equipment Notes. |

| |

(g) Cross-default | | There will be cross-default provisions in the Indentures. This means that if the Equipment Notes issued with respect to one Aircraft are in default and remedies are exercisable with respect to such aircraft, the Equipment Notes issued with respect to the remaining Aircraft will also be in default, and remedies will be exercisable with respect to all Aircraft. |

| |

(h) Section 1110 Protection | | US Airways’ outside counsel will provide its opinion to the Trustees that the benefits of Section 1110 of the U.S. Bankruptcy Code will be available with respect to the Equipment Notes. |

| |

Material U.S. Federal Income Tax Consequences | |

No Trust will be treated as a corporation or other entity taxable as a corporation for United States federal income tax purposes. Each person acquiring an interest in Certificates generally should report on its federal income tax return its pro rata share of income from the relevant Deposits and income from the Equipment Notes and other property held by the relevant Trust. See “Material U.S. Federal Income Tax Consequences.” |

| |

Certain ERISA Considerations | | Each person who acquires a Certificate will be deemed to have (i) represented that either (a) no employee benefit plan assets have been used to purchase or hold such Certificate or (b) the purchase and holding of such Certificate are exempt from the prohibited transaction restrictions of ERISA and the Code pursuant to one or more prohibited transaction statutory or administrative exemptions, and (ii) directed the relevant Trustee to invest in the assets held in the relevant Trust pursuant to the terms and conditions described herein. See “Certain ERISA Considerations.” |

S-12

| | | | | | |

| | | |

| | | Fitch | | Moody’s | | S&P |

Threshold Rating for the Depositary | | Long Term A- | | Short Term

P-1 | | Long Term

A- |

| | |

| |

Depositary Rating | | The Depositary meets the Depositary Threshold Rating requirement. |

| | | | | | |

| | | |

| | | Fitch | | Moody’s | | S&P |

Threshold Rating for the Liquidity Provider | | Long Term BBB- | | Long Term Unsecured

Baa2 | | Long Term

BBB |

| | |

| |

Liquidity Provider Rating | | The Liquidity Provider meets the Liquidity Threshold Rating requirement. |

S-13

Summary Historical Consolidated Financial and Operating Data

The following tables summarize certain consolidated financial data and certain operating data with respect to US Airways Group. The selected consolidated financial data presented below under the captions “Consolidated statements of operations data” and “Consolidated balance sheet data” as of and for the years ended December 31, 2008 to 2012 are derived from the consolidated financial statements of US Airways Group, which have been audited by KPMG LLP, an independent registered public accounting firm. The selected consolidated financial data should be read in conjunction with the consolidated financial statements for the respective periods, the related notes and the related reports of US Airways Group’s independent registered public accounting firm incorporated by reference in this prospectus supplement and the accompanying prospectus.

| | | | | | | | | | | | | | | | | | | | |

| | | Year Ended December 31, | |

| | | 2012 | | | 2011 | | | 2010 | | | 2009 | | | 2008 | |

Consolidated statements of operations data: | | | | | | | | | | | | | | | | | | | | |

Operating revenues | | $ | 13,831 | | | $ | 13,055 | | | $ | 11,908 | | | $ | 10,458 | | | $ | 12,118 | |

Operating expenses | | | 12,975 | | | | 12,629 | | | | 11,127 | | | | 10,340 | | | | 13,918 | |

| | | | | | | | | | | | | | | | | | | | |

Operating income (loss) | | | 856 | | | | 426 | | | | 781 | | | | 118 | | | | (1,800 | ) |

Net income (loss) | | | 637 | | | | 71 | | | | 502 | | | | (205 | ) | | | (2,215 | ) |

Earnings (loss) per common share: | | | | | | | | | | | | | | | | | | | | |

Basic | | | 3.92 | | | | 0.44 | | | | 3.11 | | | | (1.54 | ) | | | (22.11 | ) |

Diluted | | | 3.28 | | | | 0.44 | | | | 2.61 | | | | (1.54 | ) | | | (22.11 | ) |

Shares used for computation (in thousands): | | | | | | | | | | | | | | | | | | | | |

Basic | | | 162,331 | | | | 162,028 | | | | 161,412 | | | | 133,000 | | | | 100,168 | |

Diluted | | | 203,978 | | | | 163,743 | | | | 201,131 | | | | 133,000 | | | | 100,168 | |

Ratio of earnings to fixed charges(a) | | | 1.83 | | | | 1.11 | | | | 1.68 | | | | (a | ) | | | (a | ) |

| | | | | |

Consolidated balance sheet data (at end of period): | | | | | | | | | | | | | | | | | | | | |

Total assets | | $ | 9,396 | | | $ | 8,335 | | | $ | 7,819 | | | $ | 7,454 | | | $ | 7,214 | |

Long-term obligations, less current maturities(b) | | | 5,013 | | | | 4,718 | | | | 4,559 | | | | 4,643 | | | | 4,281 | |

Current maturities of long-term obligations | | | 417 | | | | 436 | | | | 397 | | | | 502 | | | | 362 | |

Total stockholders’ equity (deficit) | | | 790 | | | | 150 | | | | 84 | | | | (355 | ) | | | (494 | ) |

| | | | | |

Consolidated statements of operations data excluding special items(c): | | | | | | | | | | | | | | | | | | | | |

Operating income (loss) excluding special items | | $ | 893 | | | $ | 452 | | | $ | 785 | | | $ | (199 | ) | | $ | (606 | ) |

Net income (loss) excluding special items | | | 537 | | | | 111 | | | | 447 | | | | (499 | ) | | | (808 | ) |

Earnings (loss) per common share excluding special items: | | | | | | | | | | | | | | | | | | | | |

Basic | | | 3.31 | | | | 0.69 | | | | 2.77 | | | | (3.75 | ) | | | (8.06 | ) |

Diluted | | | 2.79 | | | | 0.68 | | | | 2.34 | | | | (3.75 | ) | | | (8.06 | ) |

| (a) | Earnings for the years ended December 31, 2009 and 2008 were not sufficient to cover fixed charges by $253 million and $2.22 billion, respectively. |

| (b) | Includes debt, capital leases, postretirement benefits other than pensions and employee benefit liabilities and other. |

| (c) | See “—Reconciliation of GAAP to Non-GAAP Financial Measures” below. |

S-14

Reconciliation of GAAP to Non-GAAP Financial Measures

We are providing disclosure of the reconciliation of reported non-GAAP financial measures to their comparable financial measures on a GAAP basis. We believe that the non-GAAP financial measures provide investors the ability to measure financial performance excluding special items, which is more indicative of our ongoing performance and is more comparable to measures reported by other major airlines.

| | | | | | | | | | | | | | | | | | | | |

| | | Year Ended December 31, | |

| | | 2012 | | | 2011 | | | 2010 | | | 2009 | | | 2008 | |

| | | (In millions) | |

Operating income (loss)—GAAP | | $ | 856 | | | $ | 426 | | | $ | 781 | | | $ | 118 | | | $ | (1,800 | ) |

Operating special items, net(a) | | | 37 | | | | 26 | | | | 4 | | | | (317 | ) | | | 1,194 | |

| | | | | | | | | | | | | | | | | | | | |

Operating income (loss) excluding special items | | | 893 | | | | 452 | | | | 785 | | | | (199 | ) | | | (606 | ) |

| | | | | |

Net income (loss)—GAAP | | | 637 | | | | 71 | | | | 502 | | | | (205 | ) | | | (2,215 | ) |

Operating special items, net(a) | | | 37 | | | | 26 | | | | 4 | | | | (317 | ) | | | 1,194 | |

Nonoperating special items, net(b) | | | (137 | ) | | | (7 | ) | | | (59 | ) | | | 61 | | | | 213 | |

Income tax special items(c) | | | 0 | | | | 21 | | | | 0 | | | | (38 | ) | | | 0 | |

| | | | | | | | | | | | | | | | | | | | |

Net income (loss) excluding special items | | $ | 537 | | | $ | 111 | | | $ | 447 | | | $ | (499 | ) | | $ | (808 | ) |

| (a) | Includes the following operating special charges (credits): |

The 2012 period included $34 million of charges primarily related to corporate transaction and auction rate securities arbitration costs as well as $3 million of express special charges related to ratification of a new Piedmont fleet and passenger services contract.

The 2011 period included $24 million of charges primarily related to corporate transaction and auction rate securities arbitration costs as well as $2 million in express other special charges.

The 2010 period included a $6 million non-cash charge related to the decline in value of certain spare parts, $5 million in aircraft costs related to capacity reductions and other net special charges of $10 million, which included a settlement and corporate transaction costs. These costs were offset in part by a $16 million refund of Aviation Security Infrastructure Fee (“ASIF”) and a $1 million refund of ASIF for our express subsidiaries previously paid to the TSA during the years 2005 to 2009.

The 2009 period included $375 million of net unrealized gains on fuel hedging instruments, offset in part by $22 million in aircraft costs as a result of capacity reductions, $16 million in non-cash impairment charges due to the decline in fair value of certain indefinite lived intangible assets associated with international routes, $11 million in severance and other charges, $6 million in costs incurred related to the 2009 liquidity improvement program and $3 million in non-cash charges related to the decline in value of certain express spare parts.

The 2008 period included a $622 million non-cash charge to write off all of the goodwill created by the merger of US Airways Group and America West Holdings in September 2005, as well as $496 million of net unrealized losses on fuel hedging instruments. In addition, the 2008 period included $35 million of merger-related transition expenses, $18 million in non-cash charges related to the decline in value of certain spare parts associated with our Boeing 737 aircraft fleet and, as a result of capacity reductions, $14 million in aircraft costs and $9 million in severance charges.

S-15

| (b) | Includes the following nonoperating special charges (credits): |

The 2012 period primarily included a $142 million gain related to the slot transaction with Delta Air Lines, Inc., offset in part by $3 million in debt prepayment penalties and non-cash write offs of certain debt issuance costs related to the refinancing of two Airbus aircraft.

The 2011 period included a $15 million credit in connection with an award received in an arbitration involving investments in auction rate securities, offset in part by $6 million in debt prepayment penalties and non-cash write offs of certain debt issuance costs related to the refinancing of five Airbus aircraft as well as $2 million of losses related to investments in auction rate securities.

The 2010 period included $53 million of net realized gains related to the sale of certain investments in auction rate securities as well as an $11 million settlement gain, offset in part by $5 million in non-cash charges related to the write off of debt issuance costs.

The 2009 period included $49 million in non-cash charges associated with the sale of 10 Embraer 190 aircraft and write off of related debt discount and issuance costs, $10 million in other-than-temporary non-cash impairment charges for investments in auction rate securities and a $2 million non-cash asset impairment charge.

The 2008 period included $214 million in other-than-temporary non-cash impairment charges for investments in auction rate securities as well as $7 million in write offs of debt discount and debt issuance costs in connection with the refinancing of certain aircraft equipment notes and certain loan prepayments, offset in part by $8 million in gains on forgiveness of debt.

| (c) | Includes the following income tax special charges (credits): |

The 2011 period included a non-cash tax charge of $21 million as a result of the sale of our final remaining investment in auction rate securities in July 2011. This charge recognized in the statement of operations the tax provision that was recorded in other comprehensive income, a subset of stockholders’ equity, in the fourth quarter of 2009 as described below.

The 2009 period included a tax benefit of $38 million. Of this amount, $21 million was due to a non-cash income tax benefit related to gains recorded within other comprehensive income during 2009. In addition, we recorded a $14 million tax benefit related to a legislation change allowing us to carry back 100% of 2008 Alternative Minimum Tax liability (“AMT”) net operating losses, resulting in the recovery of AMT amounts paid in prior years. We also recognized a $3 million tax benefit related to the reversal of the deferred tax liability associated with the indefinite lived intangible assets that were impaired during 2009.

S-16

Operating Data

The table below sets forth our selected mainline and express operating data:

| | | | | | | | | | | | |

| | | Year Ended December 31, | |

| | | 2012 | | | 2011 | | | 2010 | |

Mainline: | | | | | | | | | | | | |

Revenue passenger miles (millions)(a) | | | 62,435 | | | | 60,779 | | | | 58,977 | |

Available seat miles (millions)(b) | | | 74,211 | | | | 72,603 | | | | 71,588 | |

Passenger load factor (percent)(c) | | | 84.1 | | | | 83.7 | | | | 82.4 | |

Yield (cents)(d) | | | 14.38 | | | | 13.99 | | | | 12.96 | |

Passenger revenue per available seat mile (cents)(e) | | | 12.10 | | | | 11.71 | | | | 10.68 | |

Operating cost per available seat mile (cents)(f) | | | 13.22 | | | | 13.09 | | | | 11.73 | |

Passenger enplanements (thousands)(g) | | | 54,277 | | | | 52,959 | | | | 51,853 | |

Departures (thousands) | | | 449 | | | | 452 | | | | 451 | |

Aircraft at end of period | | | 340 | | | | 340 | | | | 339 | |

Block hours (thousands)(h) | | | 1,209 | | | | 1,217 | | | | 1,199 | |

Average stage length (miles)(i) | | | 1,004 | | | | 991 | | | | 981 | |

Average passenger journey (miles)(j) | | | 1,704 | | | | 1,691 | | | | 1,674 | |

Fuel consumption (gallons in millions) | | | 1,102 | | | | 1,095 | | | | 1,073 | |

Average aircraft fuel price including related taxes (dollars per gallon) | | | 3.17 | | | | 3.11 | | | | 2.24 | |

Full time equivalent employees at end of period | | | 31,236 | | | | 31,548 | | | | 30,871 | |

Express:(k) | | | | | | | | | | | | |

Revenue passenger miles (millions)(a) | | | 10,883 | | | | 10,542 | | | | 10,616 | |

Available seat miles (millions)(b) | | �� | 14,214 | | | | 14,070 | | | | 14,230 | |

Passenger load factor (percent)(c) | | | 76.6 | | | | 74.9 | | | | 74.6 | |

Yield (cents)(d) | | | 30.56 | | | | 29.03 | | | | 26.57 | |

Passenger revenue per available seat mile (cents)(e) | | | 23.40 | | | | 21.75 | | | | 19.83 | |

Operating cost per available seat mile (cents)(f) | | | 22.24 | | | | 22.23 | | | | 19.18 | |

Passenger enplanements (thousands)(g) | | | 28,269 | | | | 27,613 | | | | 27,707 | |

Aircraft at end of period | | | 282 | | | | 283 | | | | 281 | |

Fuel consumption (gallons in millions) | | | 345 | | | | 338 | | | | 336 | |

Average aircraft fuel price including related taxes (dollars per gallon) | | | 3.19 | | | | 3.12 | | | | 2.29 | |

Total Mainline and Express: | | | | | | | | | | | | |

Revenue passenger miles (millions)(a) | | | 73,318 | | | | 71,321 | | | | 69,593 | |

Available seat miles (millions)(b) | | | 88,425 | | | | 86,673 | | | | 85,818 | |

Passenger load factor (percent)(c) | | | 82.9 | | | | 82.3 | | | | 81.1 | |

Yield (cents)(d) | | | 16.78 | | | | 16.21 | | | | 15.04 | |

Passenger revenue per available seat mile (cents)(e) | | | 13.92 | | | | 13.34 | | | | 12.20 | |

Total revenue per available seat mile (cents)(l) | | | 15.64 | | | | 15.06 | | | | 13.88 | |

Passenger enplanements (thousands)(g) | | | 82,546 | | | | 80,572 | | | | 79,560 | |

Aircraft at end of period | | | 622 | | | | 623 | | | | 620 | |

Fuel consumption (gallons in millions) | | | 1,447 | | | | 1,433 | | | | 1,409 | |

Average aircraft fuel price including related taxes (dollars per gallon) | | | 3.17 | | | | 3.11 | | | | 2.25 | |

| (a) | Revenue passenger mile (RPM)—A basic measure of sales volume. One RPM represents one passenger flown one mile. |

| (b) | Available seat mile (ASM)—A basic measure of production. One ASM represents one seat flown one mile. |

| (c) | Passenger load factor—The percentage of available seats that are filled with revenue passengers. |

| (d) | Yield—A measure of airline revenue derived by dividing passenger revenue by RPMs. |

S-17

| (e) | Passenger revenue per available seat mile—Passenger revenues divided by ASMs. |

| (f) | Operating cost per available seat mile—Operating expenses divided by ASMs. |

| (g) | Passenger enplanements—The number of passengers on board an aircraft, including local, connecting and through passengers. |

| (h) | Block hours—The hours measured from the moment an aircraft first moves under its own power, including taxi time, for the purposes of flight until the aircraft is docked at the next point of landing and its power is shut down. |

| (i) | Average stage length—The average of the distances flown on each segment of every route. |

| (j) | Average passenger journey—The average one-way trip measured in miles for one passenger origination. |

| (k) | Express statistics include Piedmont and PSA, as well as operating and financial results from capacity purchase agreements with Air Wisconsin Airlines Corporation, Republic Airline Inc., Mesa Airlines, Inc., Chautauqua Airlines, Inc. and SkyWest Airlines, Inc. |

| (l) | Total revenue per available seat mile—Total revenues divided by total mainline and express ASMs. |

S-18

RISK FACTORS

An investment in the certificates involves certain risks. You should carefully consider the risks described below, as well as the other information included or incorporated by reference in this prospectus supplement and the accompanying prospectus, before making an investment decision. Our business, financial condition or results of operations could be materially adversely affected by any of these risks. The market or trading price of the certificates could decline due to any of these risks, and you may lose all or part of your investment. In addition, please read “Special Note About Forward-Looking Statements” in this prospectus supplement, where we describe additional uncertainties associated with our business and the forward-looking statements included or incorporated by reference in this prospectus supplement and the accompanying prospectus. Please note that additional risks not presently known to us or that we currently deem immaterial may also impair our business, financial condition or results of operations.

Risk Factors Relating to the Company and Industry Related Risks

Certain risks relating to us and our business are described below and under the heading “Risk Factors” in our reports filed with the SEC that are incorporated by reference in this prospectus supplement, which you should carefully review and consider.

US Airways Group could experience significant operating losses in the future.

For a number of reasons, including those addressed in these risk factors, US Airways Group might fail to achieve profitability and might experience significant losses. In particular, the condition of the economy and the high volatility of fuel prices have had and continue to have an impact on our operating results, and increase the risk that we will experience losses.

Downturns in economic conditions adversely affect our business.

Due to the discretionary nature of business and leisure travel spending, airline industry revenues are heavily influenced by the condition of the U.S. economy and economies in other regions of the world. Unfavorable conditions in these broader economies have resulted, and may result in the future, in decreased passenger demand for air travel and changes in booking practices, both of which in turn have had, and may have in the future, a strong negative effect on our revenues. In addition, during challenging economic times, actions by our competitors to increase their revenues can have an adverse impact on our revenues. See “The airline industry is intensely competitive and dynamic” below. Certain labor agreements to which we are a party limit our ability to reduce the number of aircraft in operation, and the utilization of such aircraft, below certain levels. As a result, we may not be able to optimize the number of aircraft in operation in response to a decrease in passenger demand for air travel.

Our business is dependent on the price and availability of aircraft fuel. Continued periods of high volatility in fuel costs, increased fuel prices and significant disruptions in the supply of aircraft fuel could have a significant negative impact on our operating results and liquidity.

Our operating results are materially impacted by changes in the availability, price volatility and cost of aircraft fuel, which represents one of the largest single cost items in our business. Jet fuel market prices have fluctuated substantially over the past several years with market spot prices ranging from a low of approximately $1.87 per gallon to a high of approximately $3.38 per gallon during the period from January 1, 2010 to December 31, 2012.

S-19

Because of the amount of fuel needed to operate our airline, even a relatively small increase in the price of fuel can have a material adverse aggregate effect on our costs and liquidity. Due to the competitive nature of the airline industry and unpredictability of the market, we can offer no assurance that we may be able to increase our fares, impose fuel surcharges or otherwise increase revenues sufficiently to offset fuel price increases.

Although we are currently able to obtain adequate supplies of aircraft fuel, we cannot predict the future availability, price volatility or cost of aircraft fuel. Natural disasters, political disruptions or wars involving oil-producing countries, changes in fuel-related governmental policy, the strength of the U.S. dollar against foreign currencies, changes in access to petroleum product pipelines and terminals, speculation in the energy futures markets, changes in aircraft fuel production capacity, environmental concerns and other unpredictable events may result in fuel supply shortages, additional fuel price volatility and cost increases in the future.

Historically, we have from time to time entered into hedging arrangements designed to protect against rising fuel costs. Currently, we are not a party to any transactions to hedge our fuel consumption. Our ability to hedge in the future may be limited, particularly if our financial condition provides insufficient liquidity to meet counterparty collateral requirements. Our future fuel hedging arrangements, if any, may not completely protect us against price increases and may be limited in both volume of fuel and duration. Also, a rapid decline in the projected price of fuel at a time when we have fuel hedging contracts in place could adversely impact our short-term liquidity, because hedge counterparties could require that we post collateral in the form of cash or letters of credit. See also the discussion in Part II, Item 7A, “Quantitative and Qualitative Disclosures About Market Risk” in our most recent Annual Report on Form 10-K.

The airline industry is intensely competitive and dynamic.

Our competitors include other major domestic airlines and foreign, regional and new entrant airlines, many of which have more financial resources or lower cost structures than ours, as well as other forms of transportation, including rail and private automobiles. In many of our markets we compete with at least one low-cost air carrier. Our revenues are sensitive to the actions of other carriers in many areas including pricing, scheduling, capacity and promotions, which can have a substantial adverse impact not only on our revenues, but on overall industry revenues. These factors may become even more significant in periods when the industry experiences large losses, as airlines under financial stress, or in bankruptcy, may institute pricing structures intended to achieve near-term survival rather than long-term viability. In addition, because a significant portion of our traffic is short-haul travel, we are more susceptible than other major airlines to competition from surface transportation such as automobiles and trains.

Low-cost carriers have a profound impact on industry revenues. Using the advantage of low unit costs, these carriers offer lower fares in order to shift demand from larger, more-established airlines. Some low-cost carriers, which have cost structures lower than ours, have better financial performance and significant numbers of aircraft on order for delivery in the next few years. These low-cost carriers are expected to continue to increase their market share through growth and, potentially, consolidation, and could continue to have an impact on our overall performance.

Additionally, as mergers and other forms of industry consolidation, including antitrust immunity grants, take place, we might or might not be included as a participant. Depending on which carriers combine and which assets, if any, are sold or otherwise transferred to other carriers in connection with such combinations, our competitive position relative to the post-combination carriers or other carriers that acquire such assets could be harmed. In addition, as carriers combine through traditional mergers or antitrust immunity grants, their route networks will grow, and that growth will result in greater overlap

S-20

with our network, which in turn could result in lower overall market share and revenues for us. Such consolidation is not limited to the U.S., but could include further consolidation among international carriers in Europe and elsewhere.

Also see the risk factors provided under the caption “Risk Factors Relating to the Merger and the Combined Company.”

Increased costs of financing, a reduction in the availability of financing and fluctuations in interest rates could adversely affect our liquidity, operating expenses and results.

Concerns about the systemic impact of inflation, the availability and cost of credit, energy costs and geopolitical issues, combined with continued changes in business activity levels and consumer confidence, increased unemployment and volatile oil prices, have contributed to unprecedented levels of volatility in the capital markets. As a result of these market conditions, the cost and availability of credit have been and may continue to be adversely affected by illiquid credit markets and wider credit spreads. These changes in the domestic and global financial markets may increase our costs of financing and adversely affect our ability to obtain financing needed for the acquisition of aircraft that we have contractual commitments to purchase and for other types of financings we may seek in order to refinance debt maturities, raise capital or fund other types of obligations. Any downgrades to our credit rating may likewise increase the cost and reduce the availability of financing.

In addition, we have substantial non-cancelable commitments for capital expenditures, including the acquisition of new aircraft and related spare engines. We have not yet secured financing commitments for four Airbus aircraft scheduled for delivery after November 2013, and cannot assure you of the availability or cost of that financing. If we are not able to arrange financing for such aircraft at customary advance rates and on terms and conditions acceptable to us, we expect we would seek to negotiate deferrals of aircraft deliveries with the manufacturer or financing at lower than customary advance rates, or, if required, use cash from operations or other sources to purchase the aircraft.

Further, a substantial portion of our indebtedness bears interest at fluctuating interest rates, primarily based on the London interbank offered rate for deposits of U.S. dollars (“Libor”). Libor tends to fluctuate based on general economic conditions, general interest rates, Federal Reserve rates and the supply of and demand for credit in the London interbank market. We have not hedged our interest rate exposure and, accordingly, our interest expense for any particular period may fluctuate based on Libor and other variable interest rates. To the extent these interest rates increase, our interest expense will increase, in which event we may have difficulties making interest payments and funding our other fixed costs, and our available cash flow for general corporate requirements may be adversely affected. See also the discussion of interest rate risk in Part II, Item 7A, “Quantitative and Qualitative Disclosures About Market Risk” in our most recent Annual Report on Form 10-K.

Our high level of fixed obligations limits our ability to fund general corporate requirements and obtain additional financing, limits our flexibility in responding to competitive developments and increases our vulnerability to adverse economic and industry conditions.

We have a significant amount of fixed obligations, including debt, aircraft leases and financings, aircraft purchase commitments, leases and developments of airport and other facilities and other cash obligations. We also have certain guaranteed costs associated with our express operations. Our existing indebtedness is secured by substantially all of our assets.

As a result of the substantial fixed costs associated with these obligations:

| | Ÿ | | a decrease in revenues results in a disproportionately greater percentage decrease in earnings; |

S-21

| | Ÿ | | we may not have sufficient liquidity to fund all of these fixed costs if our revenues decline or costs increase; and |

| | Ÿ | | we may have to use our working capital to fund these fixed costs instead of funding general corporate requirements, including capital expenditures. |

These obligations also impact our ability to obtain additional financing, if needed, and our flexibility in the conduct of our business.

Any failure to comply with the liquidity covenants contained in our financing arrangements would likely have a material adverse effect on our business, financial condition and results of operations.

The terms of our Citicorp credit facility and certain of our other financing arrangements require us to maintain consolidated unrestricted cash and cash equivalents of not less than $850 million, with not less than $750 million (subject to partial reductions upon certain reductions in the outstanding principal amount of the loan) of that amount held in accounts subject to control agreements.

Our ability to comply with these covenants while paying the fixed costs associated with our contractual obligations and our other expenses, including payments in respect of the Certificates, will depend on our operating performance and cash flow, which are seasonal, as well as factors including fuel costs and general economic and political conditions.

The factors affecting our liquidity (and our ability to comply with related covenants) will remain subject to significant fluctuations and uncertainties, many of which are outside our control. Any breach of our liquidity covenants or failure to timely pay our obligations could result in a variety of adverse consequences, including the acceleration of our indebtedness, the withholding of credit card proceeds by our credit card processors and the exercise of remedies by our creditors and lessors. In such a situation, it is unlikely that we would be able to fulfill our contractual obligations, repay the accelerated indebtedness, make required lease payments or otherwise cover our fixed costs.

If our financial condition worsens, provisions in our credit card processing and other commercial agreements may adversely affect our liquidity.

We have agreements with companies that process customer credit card transactions for the sale of air travel and other services. These agreements allow these processing companies, under certain conditions, to hold an amount of our cash (referred to as a “holdback”) equal to some or all of the advance ticket sales that have been processed by that company, but for which we have not yet provided the air transportation. We are currently subject to certain holdback requirements. These holdback requirements can be modified at the discretion of the processing companies upon the occurrence of specific events, including material adverse changes in our financial condition. An increase in the current holdback balances to higher percentages up to and including 100% of relevant advanced ticket sales could materially reduce our liquidity. Likewise, other of our commercial agreements contain provisions that allow other entities to impose less favorable terms, including the acceleration of amounts due, in the event of material adverse changes in our financial condition.

Union disputes, employee strikes and other labor-related disruptions may adversely affect our operations.

Relations between air carriers and labor unions in the United States are governed by the Railway Labor Act (“RLA”). Under the RLA, collective bargaining agreements generally contain “amendable dates” rather than expiration dates, and the RLA requires that a carrier maintain the existing terms and conditions of employment following the amendable date through a multi-stage and usually lengthy series of bargaining processes overseen by the National Mediation Board (“NMB”).

S-22

If no agreement is reached during direct negotiations between the parties, either party may request that the NMB appoint a federal mediator. The RLA prescribes no timetable for the direct negotiation and mediation processes, and it is not unusual for those processes to last for many months or even several years. If no agreement is reached in mediation, the NMB in its discretion may declare that an impasse exists and proffer binding arbitration to the parties. Either party may decline to submit to arbitration, and if arbitration is rejected by either party, a 30-day “cooling off” period commences. During or after that period, a Presidential Emergency Board (“PEB”) may be established, which examines the parties’ positions and recommends a solution. The PEB process lasts for 30 days and is followed by another 30-day “cooling off” period. At the end of a “cooling off” period, unless an agreement is reached or action is taken by Congress, the labor organization may exercise “self-help”, such as a strike, which could materially adversely affect our ability to conduct our business and our financial performance.