UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 6-K

REPORT OF FOREIGN PRIVATE ISSUER

PURSUANT TO RULE 13a-16 OR 15d-16 UNDER

THE SECURITIES EXCHANGE ACT OF 1934

Report on Form 6-K dated December 12, 2005

Commission File Number 0-10906

The BOC Group plc

(Translation of registrant’s name into English)

Chertsey Road, Windlesham

Surrey, GU20 6HJ England

(Address of principal executive offices)

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F.

Form 20-F: ![]() Form 40-F:

Form 40-F: ![]()

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1).

Yes: ![]() No:

No: ![]()

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7).

Yes: ![]() No:

No: ![]()

Indicate by check mark whether the registrant by furnishing the information contained in this Form is also thereby furnishing the information to the Commission pursuant to Rule 12g3-2(b) under the Securities Exchange Act of 1934.

Yes: ![]() No:

No: ![]()

Enclosure: The BOC Group plc Report and Accounts 2005.

This report contains the Report and Accounts 2005 of The BOC Group plc (the “Company”) for the financial year ended 30 September 2005. The Report and Accounts 2005 comprises the annual report and accounts of the Company in accordance with United Kingdom requirements and the information required to be set out in the Company’s annual report on Form 20-F for the financial year ended 30 September 2005 (the “Form 20-F”) to the Securities and Exchange Commission. The information in the Report and Accounts 2005 that is referenced in the “Cross reference to Form 20-F” table on page 146 shall be deemed to be filed with the Securities and Exchange Commission for all purposes, including incorporation by reference into the Company’s annual report on Form 20-F filed with the Securities and Exchange Commission on 12 December 2005.

| BOC Report and accounts 2005 | ||

| The BOC Group plc Annual report and accounts 2005 |

The Group’s objectives

Over a sustained period, consistently to outperform our peers in terms of safety, customer service, revenue growth, earnings and cash generation.

We will be the employer of choice for all existing and future employees.

Who we are

BOC employs over 30,000 people and earns a living in some 50 countries. Over 80 per cent of our revenue comes from industrial gases and we serve customers in fields as diverse as electronics, chemicals and medical. We are organised into three lines of business and a specialist logistics business, Gist.

| 01 | |

The BOC Group plc is a public limited company listed on the London and New York Stock Exchanges and registered in England. This is the report and accounts for the year ended 30 September 2005.

It complies with UK regulations and incorporates the annual report on Form 20-F for the Securities and Exchange Commission to meet US regulations. An annual review and summary financial statements for the year ended 30 September 2005 has been issued to all shareholders who have not elected to receive this report and accounts.

Cautionary Statement

Forward-looking information, within the meaning of section 27A of the US Securities Act of 1933, as amended, and section 21E of the US Securities Exchange Act of 1934, as amended, is given throughout this annual report and accounts including in the chairman’s statement, the chief executive’s review, the Group profile, strategy, research, development and information technology, the operating review and the financial review. Such forward-looking statements include, without limitation, those concerning the company’s operations, economic performance and financial condition, namely (i) the company’s strategies, (ii) the company’s research and development and information technology activities, (iii) the company’s investments, (iv) the commencement of operations of new plants and other facilities, (v) the company’s restructuring plans, (vi) efficiencies, including cost savings, for the company resulting from business reviews and reorganisations, (vii) management’s view of the general development of, and competition in, the economies and markets in which it does, or plans to do, business, (viii) management’s view of the competitiveness of its products and services, and (ix) the company’s liquidity, capital resources and capital expenditure. Although the company believes that the expectations reflected in such forward-looking statements are reasonable, no assurance can be given that such expectations will prove to have been correct. By their nature, forward-looking statements involve risks and uncertainties because they relate to events and depend on circumstances that will or may occur in the future. Accordingly, actual results could differ materially from those set out in the forward-looking statements, as a result of a variety of factors, including changes in economic conditions, changes in the level of capital investment by the semiconductor industry, success of business and operating initiatives and restructuring objectives, customers’ strategies and stability, changes in the regulatory environment, fluctuations in interest and exchange rates, the outcome of litigation, government actions and natural phenomena such as floods, earthquakes and hurricanes. Other unknown or unpredictable factors could cause the company’s actual results to differ materially from those in the forward-looking statements.

Financial year

Throughout the report and accounts, reference to ‘2005’ in the text means the financial year ended 30 September 2005. Similarly, references to other years, eg ‘2006’,‘2004’ and ‘2003’, also mean the financial years to 30 September unless stated otherwise.

| 02 | The BOC Group plc Annual report and accounts 2005 |

Financial highlights

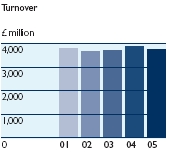

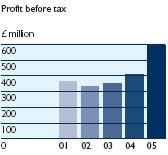

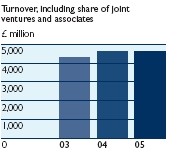

| Turnover – subsidiary companies | Operating profit | Profit before tax | Earnings per share | |||

| 2005 | 2005 | 2005 | 2005 | |||

| £3,754.7m | £543.5m | £593.6m | 74.1p | |||

| 2004 £3,885.4m | 2004 £559.5m | 2004 £412.3m | 2004 53.5p | |||

| 2003 £3,718.3m | 2003 £438.6m | 2003 £351.9m | 2003 44.5p | |||

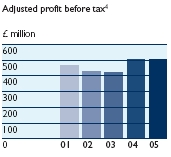

| Turnover – including share of | ||||||

| joint ventures and associates | Adjusted operating profit | Adjusted profit before tax | Adjusted earnings per share | |||

| 2005 | 2005 | 2005 | 2005 | |||

| £4,605.0m | £564.2m | £505.7m | 67.5p | |||

| 2004 £4,599.3m | 2004 £576.9m | 2004 £504.3m | 2004 63.2p | |||

| 2003 £4,323.2m | 2003 £505.6m | 2003 £418.9m | 2003 52.9p | |||

2005 results

| Analysis by business | |||||

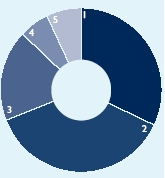

| Turnover (including share of joint ventures and associates) | £ million | % |  | ||

| 1. Process Gas Solutions | 1,466.3 | 32 | |||

| 2. Industrial and Special Products | 1,721.7 | 37 | |||

| 3. BOC Edwards | 826.0 | 18 | |||

| 4. Afrox hospitals | 275.1 | 6 | |||

| 5. Gist | 315.9 | 7 | |||

| Total | 4,605.0 | 100 | |||

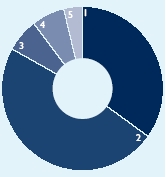

| Adjusted operating profit | £ million | % |  | ||

| 1. Process Gas Solutions | 207.2 | 37 | |||

| 2. Industrial and Special Products | 289.4 | 51 | |||

| 3. BOC Edwards | 38.1 | 7 | |||

| 4. Afrox hospitals | 37.2 | 7 | |||

| 5. Gist | 24.5 | 4 | |||

| Corporate | (32.2 | ) | (6 | ) | |

| Total | 564.2 | 100 | |||

| Financial highlights | 03 | |

| Dividends per share | Return on capital employed | Figures shown as ‘adjusted’ exclude exceptional items. Other figures shown are prepared under UK Generally Accepted Accounting Principles (GAAP) and include all exceptional items. | ||||

| 2005 | 2005 | |||||

| 41.2p | 15.6% | |||||

| 2004 40.0p | 2004 14.9% | |||||

| 2003 39.0p | 2003 10.9% | |||||

| Adjusted return | ||||||

| on capital employed | ||||||

| 2005 | ||||||

| 16.2% | ||||||

| 2004 15.4% | ||||||

| 2003 12.6% | ||||||

| Analysis by region | |||||

| Turnover (including share of joint ventures and associates) | £ million | % |  | ||

| 1. Europe | 1,300.8 | 28 | |||

| 2. Americas | 1,222.1 | 27 | |||

| 3. Africa | 586.0 | 13 | |||

| 4. Asia/Pacific | 1,496.1 | 32 | |||

| Total | 4,605.0 | 100 | |||

| Adjusted operating profit | £ million | % |  | ||

| 1. Europe | 143.7 | 25 | |||

| 2. Americas | 100.0 | 18 | |||

| 3. Africa | 91.3 | 16 | |||

| 4. Asia/Pacific | 229.2 | 41 | |||

| Total | 564.2 | 100 | |||

| 04 | The BOC Group plc Annual report and accounts 2005 |

Implementing our

strategy effectively

Chairman’s statement

Your board has again fully reviewed and approved BOC’s strategy, which is being effectively implemented by Tony Isaac and his management team. The strategy has seen BOC confirm its leading position in Asia, develop a strong base in China and invest strongly in other growth markets. It has seen a continuing commitment to safety and to improve the efficiency and environmental performance of our operations. It has seen the divestment of underperforming businesses allied to a well implemented acquisition strategy.

Rewarding our shareholders

In 2005 BOC raised its first interim dividend to 15.9p. Combined with the second interim dividend of 25.3p, this represents an increase of three per cent on the previous year as we continue to build our dividend cover towards two-times over the medium term. Your board has decided to raise the first interim dividend to be paid on 1 February 2006 by 2.5 per cent to 16.3p.

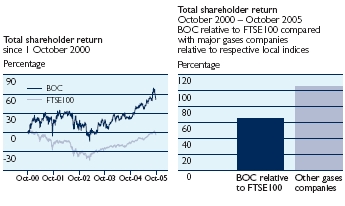

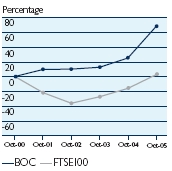

I have updated the graphs I have shown here every year since 2001. They show BOC’s total shareholder return since October 2000 compared with the FTSE100 and our major gases competitors. We have continued to outperform the FTSE100. Industrial gases companies have proved to be a rewarding investment over recent years and in the last year or so we have matched our competitors’ performance, although a gap remains from earlier years. In his review,Tony Isaac will explain in more detail how we have progressed this year.

Corporate Governance

This year your company has completed its work to comply with one new set of requirements, the Combined Code on Corporate Governance, and has made good progress on two others, namely changing over to International Financial Reporting Standards (IFRS) and meeting the provisions of the US Sarbanes-Oxley Act. The quarterly results to be announced in February 2006 will be the first in accordance with IFRS. We estimate that meeting the requirements of Sarbanes-Oxley cost your company some £10 million this year. We are likely to spend the same next year before the costs reduce somewhat. BOC has to comply with these provisions because we are registered in the US, but being a complex and diverse business working globally means that the cost of such compliance is very high.

Next year we will, in common with all UK companies, publish an operating and financial review (OFR) as part of our annual report. The intention of the OFR is to help you, our shareholders, assess our strategies and the likelihood of their success.

External checks and reporting requirements may help but I believe the best assurance for shareholders is to ensure high standards of integrity and transparency throughout the organisation, overseen by a strong and independent group of non-executive directors. BOC has both of these. It has a strong and well-implemented Code of

| Chairman’s statement | 05 |

Conduct and a management team committed to the principles of accountability, collaboration, transparency and stretch, known in BOC as ACTS.

Your board regularly reviews the management of our social, environmental and ethical risks. These have now been integrated into the company’s overall risk management programme. Each year our performance is judged against criteria set by the UK’s Business in the Community (BiTC). To be as transparent as possible we publish on our website, boc.com, both our comprehensive submission to BiTC and its independent assessment of our performance.

An important feature of BOC’s corporate responsibility programme is to enable people at all levels of the organisation to become involved and support things that matter to them. Our joint giving scheme is an example. This year countries around the Indian Ocean suffered from the appalling effects of the tsunami. Our businesses in the countries affected responded immediately with medical oxygen and with other practical help. BOC extended its joint giving scheme to match two-to-one our employees’ donations to the relief effort for both the tsunami and hurricane Katrina. BOC again responded when the Pakistan earthquake struck in October 2005. In total the community of BOC gave over £570,000 to the tsunami appeal and we await the final totals for hurricane Katrina and the Pakistan earthquake.

One of our US subsidiaries, along with other companies in the welding products industry, has been the subject of allegations that manganese in welding fumes causes Parkinson’s disease or symptoms similar to Parkinson’s. Again this year there were no adverse jury verdicts; the only adverse jury verdict was in 2003 and this is the subject of appeal in the Illinois court system.

Board of Directors

We appointed two new executive directors this year: Kent Masters, chief executive for Industrial and Special Products, joined the board in March, replacing John Walsh who resigned to return to his native United States; and Alan Ferguson joined in September as Group finance director in place of René Médori who resigned to take up a similar role at Anglo American. Rebecca McDonald was appointed as a non-executive director in July. Rebecca is president, gas and power, for BHP Billiton. During the year two non-executive directors resigned: Iain Napier, following his appointment as deputy chairman of Imperial Tobacco, and Julie Baddeley because of increasing demands on her time. John Walsh and René Médori each served BOC for some 20 years, Iain Napier and Julie Baddeley for a somewhat shorter time, and I would like to thank them all for their contributions.

Every year we review the performance of the board and each individual director. In alternate years, which included 2005, we conduct these reviews with external facilitation. They confirmed that each director contributes effectively and is committed to his or her role at BOC.

Thanks

BOC’s 30,000 people around the world provide products and services that are essential to everyday life. I thank them for their dedication and professionalism. I thank the customers they serve for entrusting their business to BOC. I thank all those with whom we work and in the communities where we operate for their support. And I thank you, our shareholders, for your continuing support.

| 06 | The BOC Group plc Annual report and accounts 2005 | |

Chief executive’s review

2005 was a year of underlying strong performance punctuated by events that challenged and brought out the best in BOC and its people. We continue to see an accelerating rise in energy prices, the move of manufacturing activity from higher- to lower-cost economies and relatively slow growth in an historical context for the semiconductor industry. Faced with these long-term trends we have responded by investing for growth while concentrating on energy efficiency, cost containment and high levels of customer service.

In the year, the biggest structural change in the Group was the reduction in our ownership of Afrox hospitals. Elsewhere, among the highlights, we continued our penetration of the north American refinery market with a string of new hydrogen orders, maintained the pace of our developments in China, and saw BOC Edwards enter into an important customer relationship in Korea. In contrast, events such as the Asian tsunami, the London bombings, hurricane Katrina and most recently the Pakistan earthquake saw BOC businesses helping where they could, notably with medical gases, and BOC people giving freely of their time and money.

Against this background BOC produced good results, with turnover similar to last year at £4,605 million, adjusted operating profit down three per cent to £564.2 million, adjusted profit before tax down one per cent at £505.7 million and record adjusted earnings per share of 67.5p. Adjusted figures eliminate exceptional items. Year-on-year comparisons at constant currency show the performance of our businesses in the markets where they operate without any distortions from changes in the sterling exchange rate. Our statutory results include exceptional items and reflect currency movements and on this basis turnover was similar to last year with operating profit down by three per cent and profit before tax up by 44 per cent.

Our two gases lines of business, Process Gas Solutions and Industrial and Special Products, contribute over 80 per cent of Group operating profit and both of them made good progress. Process Gas Solutions continues to increase the percentage of its business that comes from long-term tonnage schemes, with the emphasis recently on winning hydrogen contracts and building on our strong position in Asia, and particularly in China. There has been a steady flow of new orders with some £500 million of new plant due to enter service over the next couple of years. Our Process Systems team works closely with customers to identify and deliver solutions for their industrial gases needs. This approach has seen us win a disproportionate share of the new business available. In China our success has been founded on our willingness to enter joint ventures with our key customers, enabling us to share the risks and rewards of China’s industrial growth. Our joint venture plant building operation, Linde BOC Process Plants, gives us reliable and cost-effective plant to fulfil our customers’ needs. This year Process Gas Solutions grew turnover by 16 per cent and adjusted operating profit by nine per cent.

| |

| Chief executive’s review | 07 | |

Industrial and Special Products continues to extract value from its extensive distribution network and its high standards of product stewardship. The core industrial business continues to evolve as manufacturing processes change. We now offer a wider range of products and services to our industrial customers. We have developed sizeable businesses based on liquefied petroleum gas (LPG) and in several of our markets we are taking advantage of similar opportunities for safety products. Our medical business, which serves hospitals and delivers oxygen therapy to patients in their homes, is continuing to grow, particularly in Asia. The special products portfolio is also developing well, serving growth markets with products such as helium, packaged chemicals, refrigerants and propellants. Industrial and Special Products saw turnover decline by four per cent following the sale of the US packaged gas business last year, while adjusted operating profit rose by six per cent as profitability improved in the US.

BOC Edwards’ core semiconductor market remained broadly stable without returning to the activity levels seen last year. Despite this, BOC Edwards continued to improve its market position and embarked on a restructuring programme to achieve cost savings. It saw an increase in turnover of two per cent with adjusted operating profit down 21 per cent.

Gist saw some organic growth from new and existing customers and towards the end of the year it expanded into Europe with the acquisition of Van Dongen, a temperature-controlled transport business operating in a number of countries. In November 2005 it extended until 2011 its contract to manage the distribution of Marks & Spencer’s chilled and ambient food. This provides long-term security for a significant portion of Gist’s business. Gist’s turnover for the year rose eight per cent while adjusted operating profit fell by two per cent, impacted by higher pension and compliance costs.

In March we disposed of most of our shareholding in Afrox Healthcare Limited to a consortium led by two major black empowerment investors. Our African Oxygen Limited subsidiary retains a 20 per cent interest in the business. We received the disposal proceeds in March. Afrox Healthcare was a large employer and its disposal has reduced the number of Group employees by over 10,000. The disposal also had the effect of reducing the Group’s earnings per share by approximately one penny this year and an expected further one penny in 2006.

We had another good year for cash generation, helped by the Afrox Healthcare disposal. With our strong balance sheet we are in a good position to fund our growth projects, notably the ones already won by Process Gas Solutions and those still in the pipeline.

Safety remains our number one priority. It is unacceptable that anyone is hurt in the course of our business and we continue to emphasise that safety must be 100 per cent of our behaviour, 100 per cent of the time. At the start of this report we set out our objectives as a Group. We intend to outperform our competitors and to do this we must be the employer of choice for talented people. We are working hard on all aspects of our business to achieve these objectives.

Three members of the executive management board resigned this year. René Médori became group finance director for Anglo American plc while John Walsh and Rob Lourey returned with their families to new jobs in their home countries of the United States and Australia respectively. I wish all of them success in their new careers and thank them for their contributions to BOC. Kent Masters was appointed chief executive, Industrial and Special Products, in March and James Cullens joined the executive management board in April as Group human resources director. Alan Ferguson joined us as Group finance director in September from Inchcape plc.

I thank our employees for their hard work over the past year and for their continued emphasis on high standards of customer service. I thank our customers, our shareholders, our suppliers and those with whom we work on a daily basis. BOC contributes to the economic life of many countries around the world and I thank you all for helping us to do so.

Tony Isaac

Chief executive

| Strong underlying |

| performance |

| 08 | The BOC Group plc Annual report and accounts 2005 |

|

Board of directors

Rob Margetts CBE ![]()

![]() (01)

(01)

59, chairman.

Appointed chairman in January 2002. He is chairman of Legal & General Group plc, a non-executive director of Anglo American plc and chairman of the Natural Environment Research Council. Previously he was with ICI PLC for 31 years, becoming a main board director in 1992 and vice chairman in 1998. He is a fellow of both the Royal Academy of Engineering and the Institution of Chemical Engineers.

Tony Isaac ![]()

![]()

![]()

![]() (02)

(02)

64, chief executive.

Appointed an executive director in October 1994 and became chief executive in May 2000. He was previously finance director of Arjo Wiggins Appleton plc, which he joined shortly before the demerger from BAT Industries p.l.c. in 1990. Prior to that he had been finance director of GEC Plessey Telecommunications Ltd since its formation in 1988. He is a non-executive director of International Power plc and Schlumberger Ltd.

John Bevan ![]()

![]() (03)

(03)

48, chief executive, Process Gas Solutions.

Appointed an executive director in December 2002. He joined BOC in 1978 in Australia and has held various positions in general management in Australia, Korea,Thailand and the UK. He was formerly chief executive Asia, responsible for BOC's operations in 15 countries. He has a degree in commerce (marketing) from the University of New South Wales.

Andrew Bonfield ![]()

![]()

![]() (04)

(04)

43, non-executive director.

Appointed in July 2003. He is chief financial officer of Bristol-Myers Squibb Company. He qualified as a chartered accountant in South Africa, working for Price Waterhouse, before joining SmithKline Beecham in 1990 and rising to become chief financial officer in 1999. He joined BG Group plc in 2001 as executive director, finance, before assuming his current role at Bristol-Myers Squibb Company in September 2002.

Guy Dawson ![]()

![]()

![]()

![]() (05)

(05)

52, non-executive director.

Appointed in March 2004. He was chairman of European investment banking at Merrill Lynch until 2003. Before joining Merrill Lynch in 1995 he held senior positions in Morgan Grenfell and Deutsche Bank. He is a founding partner in Tricorn, an independent corporate advisory business that he co-founded in 2003, and he is also a non-executive director of Boots Group PLC.

Alan Ferguson ![]()

![]()

![]() (06)

(06)

47, group finance director.

Appointed an executive director in September 2005. Prior to joining BOC as group finance director he held a similar role with Inchcape plc, which he joined in 1983 having qualified as a chartered accountant with KPMG. He has a degree in business economics from Southampton University.

Kent Masters ![]()

![]() (07)

(07)

44, chief executive,Industrial and Special Products.

Appointed an executive director in March 2005. He joined BOC in 1985 and has held positions of increasing responsibility in engineering, marketing and general management, most recently, president, Process Gas Solutions, north America. He holds an engineering degree from Georgia Institute of Technology and an MBA from New York University.

| Board of directors | 09 |

Rebecca McDonald ![]()

![]()

![]() (08)

(08)

53, non-executive director.

Appointed in July 2005. She is president, gas and power, for BHP Billiton and is a member of the BHP Billiton executive committee. She is a director of Granite Construction Company in California.

Matthew Miau ![]()

![]()

![]() (09)

(09)

59, non-executive director.

Appointed in January 2002. He is chairman of MiTAC-Synnex Group, one of Taiwan's leading high-tech industrial groups. He is also a Convenor of Civil Advisory Committee of National Information and Communications Initiatives (NICI) and on the Board of Directors of the Institute for Information Industry (III),Taiwan. He obtained a BS in electronic engineering and computer science from U.C. Berkeley, an MBA from Santa Clara University and holds an honorary doctorate degree from the National Chiao Tung University,Taiwan.

Sir Christopher O’Donnell ![]()

![]()

![]() (10)

(10)

59, non-executive director.

Appointed in March 2001. He is chief executive of Smith & Nephew plc. Previously he held senior positions with Davy Ashmore, Vickers Limited and C R Bard Inc. He has an honours degree in mechanical engineering from Imperial College, London and an MBA from the London Business School. He is a chartered engineer and a member of the Institution of Mechanical Engineers.

Anne Quinn CBE ![]()

![]()

![]() (11)

(11)

54, non-executive director.

Appointed in May 2004. She is group vice president of BP's gas, power and renewables business. Previously she was managing director of BP Gas Marketing Ltd, managing director of Alliance Gas Ltd and an executive with Standard Oil of Ohio. She has a Bachelor of Commerce degree from Auckland University and a Masters in management science from the Massachusetts Institute of Technology. She serves on the President's Advisory Committee to the Sloan School, Massachusetts Institute of Technology.

Dr ‘Raj’ Rajagopal ![]()

![]() (12)

(12)

52, chief executive, BOC Edwards.

Appointed an executive director in July 2000. He joined BOC in 1981 and has held several positions in BOC Edwards including manufacturing systems manager, director of manufacturing and managing director, being appointed chief executive in 1998. He was appointed a non-executive director of Foseco plc in May 2005 and joined the Council of Cranfield University in July 2005. He was appointed to The Council of Science and Technology in March 2004 and has chaired the Institution of Electrical Engineers Manufacturing Sector Panel since 2003. He is a Fellow of the Royal Academy of Engineers as well as the Institution of Mechanical Engineers, the Institution of Electrical Engineers and the Chartered Management Institute. He has an MSc in manufacturing technology and a PhD in mechanical engineering both from Manchester University and an honorary degree from Cranfield University received in May 2004. He was awarded the Sir Eric Mensforth Manufacturing Gold Medal in March 2003. He resigned as a non-executive director of FSI International Inc in May 2005 and resigned from the board of the business support organisation, Sussex Enterprise, in February 2005.

| Board committees | |

| Audit committee | |

| Remuneration committee | |

| Nomination committee | |

| Pensions committee | |

| Executive management board | |

| Investment committee | |

| 10 | The BOC Group plc Annual report and accounts 2005 |

|

Executive management board

John Bevan (01)

48, chief executive, Process Gas Solutions since January 2003.

Appointed to the executive management board in June 2000. See page 08 for biographical details.

James Cullens (02)

42, group human resources director since April 2005.

Appointed to the executive management board in April 2005. He joined BOC in July 2003 and most recently was human resources director for BOC Edwards. Prior to joining BOC, he held a variety of senior, international HR roles in organisations including Mars Incorporated, Asda and PA Consulting Group. He has an MA from Cambridge University, an MLitt from Otago University, New Zealand and an MSc from Thames Valley University.

Nick Deeming (03)

51, group legal director and company secretary since May 2001.

Appointed to the executive management board in May 2001. He has over 18 years in-house counsel experience, including Schlumberger SEMA and Axa PPP Healthcare, specialising in corporate and commercial law. He has a degree in law from Guildhall University, an MBA from Cranfield University and qualified as a solicitor in 1980.

Stephen Dempsey (04)

54, group director, corporate relations since February 1999.

Appointed to the executive management board in October 1999. He joined BOC in 1990 as director of marketing services for the UK gases business and has held various communications roles in the Group. He has an MA in geography from Oxford University and an MBA from Cranfield University.

Peter Dew (05)

45, group director, information management since February 1998.

Appointed to the executive management board in October 1999. He joined BOC in 1986. He has held information technology roles in the Group’s businesses in South Africa, the UK and most recently as information management director for the Group’s businesses in Asia/Pacific.

| Executive management board | 11 |

Alan Ferguson (06)

47, group finance director since September 2005.

Appointed to the executive management board in September 2005. See page 08 for biographical details.

Tony Isaac (07)

64, chief executive since May 2000.

Appointed to the executive management board in July 1996. See page 08 for biographical details.

Kent Masters (08)

44, chief executive,Industrial and Special Products since March 2005.

Appointed to the executive management board in December 2002. See page 08 for biographical details.

Mark Nichols (09)

48, group director,business development since January 2004.

Appointed to the executive management board in January 2004. He joined BOC in February 1988 and held senior financial roles in the UK and US before moving into general management, most recently as managing director, Industrial and Special Products, east Asia. Before joining BOC he worked for Total Oil and Merck. He is a Fellow of the Association of Chartered Certified Accountants.

Dr ‘Raj’ Rajagopal (10)

52, chief executive,BOC Edwards since June 1998.

Appointed to the executive management board in July 1996. See page 09 for biographical details.

| 12 | The BOC Group plc Annual report and accounts 2005 |

| Group five year record | |

| 2001 | 2002 | 2003 | 2004 | 2005 | |||||||

| Profit and loss | £ million | £ million | £ million | £ million | £ million | ||||||

| Turnover1 | 3,772.9 | 3,657.7 | 3,718.3 | 3,885.4 | 3,754.7 | ||||||

| Total operating profit before | |||||||||||

| exceptional items2 | 530.6 | 500.1 | 505.6 | 576.9 | 564.2 | ||||||

| Exceptional items | (108.3 | ) | (74.5 | ) | (67.0 | ) | (17.4 | ) | (20.7 | ) | |

| Total operating profit2 | 422.3 | 425.6 | 438.6 | 559.5 | 543.5 | ||||||

| Profit/(loss) on termination/disposal | |||||||||||

| of businesses | – | (20.2 | ) | – | (79.5 | ) | 98.1 | ||||

| Profit on disposal of fixed assets | 3.6 | – | – | 4.9 | 10.5 | ||||||

| Profit before interest | 425.9 | 405.4 | 438.6 | 484.9 | 652.1 | ||||||

| Interest on net debt | (123.4 | ) | (103.1 | ) | (96.1 | ) | (88.4 | ) | (76.7 | ) | |

| Interest on pension scheme liabilities | (107.2 | ) | (106.1 | ) | (110.2 | ) | (117.4 | ) | (128.9 | ) | |

| Expected return on pension scheme assets | 166.9 | 139.1 | 119.6 | 133.2 | 147.1 | ||||||

| Other net financing income | 59.7 | 33.0 | 9.4 | 15.8 | 18.2 | ||||||

| Profit before tax | 362.2 | 335.3 | 351.9 | 412.3 | 593.6 | ||||||

| Tax on profit on ordinary activities | (104.6 | ) | (106.2 | ) | (96.4 | ) | (101.7 | ) | (159.9 | ) | |

| Profit after tax | 257.6 | 229.1 | 255.5 | 310.6 | 433.7 | ||||||

| Minority interests | (33.5 | ) | (26.2 | ) | (36.4 | ) | (46.6 | ) | (66.7 | ) | |

| Profit for the financial year | 224.1 | 202.9 | 219.1 | 264.0 | 367.0 | ||||||

| Earnings per 25p Ordinary share | |||||||||||

| Basic: | |||||||||||

| – on profit for the financial year | 46.0 | p | 41.4 | p | 44.5 | p | 53.5 | p | 74.1 | p | |

| – before exceptional items | 57.5 | p | 55.9 | p | 52.9 | p | 63.2 | p | 67.5 | p | |

| Diluted: | |||||||||||

| – on profit for the financial year | 45.9 | p | 41.2 | p | 44.5 | p | 53.5 | p | 73.9 | p | |

| – before exceptional items | 57.3 | p | 55.7 | p | 52.9 | p | 63.1 | p | 67.3 | p | |

| Ordinary dividends per share3 | |||||||||||

| Actual | 37.0 | p | 38.0 | p | 39.0 | p | 40.0 | p | 41.2 | p | |

| Number of fully paid Ordinary shares | |||||||||||

| in issue at the year end (million) | 494.4 | 497.3 | 497.7 | 498.8 | 502.5 | ||||||

| 1. | Subsidiary undertakings only. |

| 2. | Including share of operating profit of joint ventures and associates. |

| 3. | Dividends paid in the calendar year. |

| 4. | Excludes exceptional items. A fuller explanation of the term ‘adjusted’, and the reasons for presenting such a measure, is given in the operating review on pages 40 and 41. A reconciliation of adjusted profit before tax to profit before tax is given in the profit and loss account on page 86. A reconciliation of adjusted return on capital employed to return on capital employed is given in the operating review on page 41. |

All turnover and operating profit arose from continuing operations.

| Group five year record | 13 |

| 2001 | 2002 | 2003 | 2004 | 2005 | |||||||

| Balance sheet | £ million | £ million | £ million | £ million | £ million | ||||||

| Fixed assets | |||||||||||

| – intangible assets | 48.1 | 150.7 | 206.1 | 174.9 | 142.6 | ||||||

| – tangible assets | 3,168.6 | 3,027.4 | 2,913.4 | 2,618.4 | 2,639.9 | ||||||

| – joint ventures, associates and other | |||||||||||

| investments | 390.3 | 426.1 | 608.6 | 548.2 | 613.9 | ||||||

| Working capital | |||||||||||

| (excluding bank balances and short-term loans) | 257.0 | 203.1 | 220.1 | 154.5 | 151.8 | ||||||

| Deferred tax provisions | (294.3 | ) | (291.8 | ) | (279.2 | ) | (253.0 | ) | (241.9 | ) | |

| Other non current liabilities and provisions | (184.3 | ) | (173.7 | ) | (145.8 | ) | (126.9 | ) | (149.7 | ) | |

| Net borrowings and finance leases | (1,272.1 | ) | (1,325.6 | ) | (1,368.1 | ) | (962.4 | ) | (839.7 | ) | |

| Net assets excluding pension assets | |||||||||||

| and liabilities | 2,113.3 | 2,016.2 | 2,155.1 | 2,153.7 | 2,316.9 | ||||||

| Pension assets5 | 107.0 | 54.3 | 50.7 | 68.9 | 88.7 | ||||||

| Pension liabilities5 | (56.0 | ) | (311.0 | ) | (341.8 | ) | (344.5 | ) | (352.5 | ) | |

| Net assets including pension assets | |||||||||||

| and liabilities | 2,164.3 | 1,759.5 | 1,864.0 | 1,878.1 | 2,053.1 | ||||||

| Shareholders’ capital and reserves | 2,026.7 | 1,641.6 | 1,686.7 | 1,675.3 | 1,942.0 | ||||||

| Minority shareholders’ interests | 137.6 | 117.9 | 177.3 | 202.8 | 111.1 | ||||||

| Total capital and reserves | 2,164.3 | 1,759.5 | 1,864.0 | 1,878.1 | 2,053.1 | ||||||

| Other selected financial information | |||||||||||

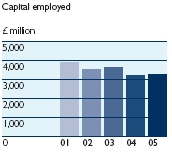

| Capital employed6 | |||||||||||

| Total capital and reserves | 2,164.3 | 1,759.5 | 1,864.0 | 1,878.1 | 2,053.1 | ||||||

| Non current liabilities and provisions | 478.6 | 465.5 | 425.0 | 379.9 | 391.6 | ||||||

| Net borrowings and finance leases7 | 1,272.1 | 1,325.6 | 1,368.1 | 962.4 | 839.7 | ||||||

| 3,915.0 | 3,550.6 | 3,657.1 | 3,220.4 | 3,284.4 | |||||||

| Total assets | 5,000.5 | 4,904.9 | 4,883.7 | 4,665.7 | 4,726.2 | ||||||

| Long-term liabilities and provisions | 1,554.5 | 1,897.5 | 1,851.5 | 1,652.9 | 1,515.6 | ||||||

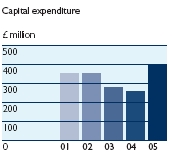

| Capital expenditure1 | 352.6 | 354.3 | 281.2 | 256.1 | 397.3 | ||||||

| Depreciation and amortisation1 | 329.5 | 330.9 | 333.4 | 324.0 | 301.9 | ||||||

| Employees | |||||||||||

| UK | 10,597 | 11,266 | 10,414 | 10,682 | 11,014 | ||||||

| Overseas | 32,574 | 35,014 | 34,093 | 32,701 | 19,558 | ||||||

| Continuing operations | 43,171 | 46,280 | 44,507 | 43,383 | 30,572 | ||||||

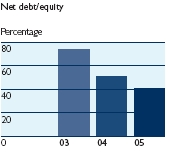

| Ratios | |||||||||||

| Return on capital employed8 | 10.4% | 10.6% | 10.9% | 14.9% | 15.6% | ||||||

| Adjusted return on capital employed4, 9 | 13.1% | 12.5% | 12.6% | 15.4% | 16.2% | ||||||

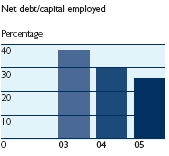

| Net debt/capital employed | 32.5% | 37.3% | 37.4% | 29.9% | 25.6% | ||||||

| Net debt/equity | 58.8% | 75.3% | 73.4% | 51.2% | 40.9% | ||||||

| 5. | Pension assets represents the excess of pension assets over pension liabilities in countries where pension assets exceed pension liabilities. Pension liabilities represents the excess of pension liabilities over pension assets in countries where pension liabilities exceed pension assets. |

| 6. | As defined in note 1 b) to the financial statements. |

| 7. | Analysed for 2005 and 2004 in note 20 to the financial statements. |

| 8. | Operating profit as a percentage of the average capital employed excluding net pension liabilities. The average is calculated on a monthly basis. |

| 9. | Operating profit before exceptional items as a percentage of the average capital employed excluding net pension liabilities. The average is calculated on a monthly basis. |

| 14 | The BOC Group plc Annual report and accounts 2005 |

| Group profile | |

Introduction

The BOC Group began its business life over 100 years ago as the Brin’s Oxygen Company. The company was incorporated in England in 1886 and adopted its present name on 1 March 1982.

A technology to extract oxygen from the air in commercial quantities had just been developed and in 1886 the Brin brothers started production at a factory in Westminster, London. Two uses had already been found for oxygen. One was to intensify limelight, which was then used in theatres. The other was to assist patients’ breathing during and after surgery. New technology was soon developed that allowed air to be separated into all its major components - nitrogen, oxygen and argon. By 1960, industrial gases were in widespread use and BOC’s business was firmly established. Tonnage plants were supplying steelworks with oxygen and the customer base had been broadened to extend from metal cutting and welding to food and medicine. The business had also spread overseas with subsidiaries or associated companies as far away as Australia and South Africa. During the 1980s, BOC’s South African subsidiary began to invest in private hospitals. This diversification was the basis of the Afrox hospitals segment.

BOC acquired the vacuum equipment company Edwards High Vacuum International Limited in 1968 and this formed the basis of what was to become the BOC Edwards line of business today.

The BOC Distribution Services business (now called Gist) was first established in 1970, initially providing a chilled food distribution service for Marks & Spencer and relying upon distribution skills and liquid nitrogen chilling technology, acquired as a result of BOC’s involvement in gases.

In 1978, BOC completed the acquisition of Airco Inc in America, a predominantly gases business that doubled the Group’s size and brought BOC for the first time into the US gases market. In the period from 1970 to 1990 The BOC Group significantly increased its presence in the Asia/Pacific region through participation in several joint ventures or associated companies. BOC established strong market positions in Thailand, Indonesia,Taiwan, the Philippines, China and Korea.

An investment in 1982 gave BOC effective management control of the Japanese gases company Osaka Sanso Kogyo KK (OSK). BOC’s holding in OSK was raised to 97 per cent before BOC and Air Liquide merged their industrial and medical gases businesses in Japan in January 2003. BOC’s subsidiary in Japan has retained a 45 per cent interest in the joint venture company, which is called Japan Air Gases Ltd.

In the period from 1998 to 2001, BOC increased investments in its gases companies in Thailand, Indonesia and the Philippines by acquiring the interests of joint venture partners or minority shareholders.

The BOC Group has an international portfolio of companies operating and reporting as three lines of business. These are Process Gas Solutions (PGS), Industrial and Special Products (ISP) and BOC Edwards. In addition two separately managed specialist businesses,Afrox hospitals and Gist, are reported as business segments. Until a disposal in March 2005, results for Afrox hospitals were fully consolidated. Since then BOC has reported its 20 per cent share of this business.

BOC Process Plants was combined with Linde Engineering in the US with effect from September 2002. BOC retains an interest in the manufacture of industrial gas equipment through its Cryostar business based in France. Cryostar makes specialist cryogenic pumps and expansion turbines that are used by most manufacturers of industrial gas plant. In recent years Cryostar has also developed a strong position in the market for shipboard compressors and heat exchangers used aboard liquefied natural gas (LNG) tankers. Management believes that Cryostar is the leading manufacturer of its product range worldwide.

The main exports of the Group in 2005 were special products from the UK, helium from the US and vacuum equipment and semiconductor manufacturing equipment from the UK, the US and Japan. Trade between Group undertakings is conducted at fair market prices.

Analysis of results by business

(including share of joint ventures and associates)

| Turnover | Operating profit | Adjusted operating profit | |||||||||||

| £ million | % | £ million | % | £ million | % | ||||||||

| Process Gas Solutions | 1,466.3 | 32 | 207.2 | 38 | 207.2 | 37 | |||||||

| Industrial and Special Products | 1,721.7 | 37 | 289.4 | 53 | 289.4 | 51 | |||||||

| BOC Edwards | 826.0 | 18 | 17.4 | 3 | 38.1 | 7 | |||||||

| Afrox hospitals | 275.1 | 6 | 37.2 | 7 | 37.2 | 7 | |||||||

| Gist | 315.9 | 7 | 24.5 | 5 | 24.5 | 4 | |||||||

| Corporate | – | – | (32.2 | ) | (6 | ) | (32.2 | ) | (6 | ) | |||

| 4,605.0 | 100 | 543.5 | 100 | 564.2 | 100 | ||||||||

| Adjusted operating profit excludes exceptional items. See also pages 40 and 41 of the operating review. | |||||||||||||

The BOC Group contributes to the economies of some 50 countries throughout the world. The UK is the largest single source of sales revenue for the Group’s products and services, followed by the US. Other major geographic areas for the Group are Australia, South Africa, Japan and other markets in the Asia/Pacific region. The business therefore operates from a broad geographical base with local manufacturing in most of the key overseas markets.

| Group profile | 15 |

Analysis of results by region

(including share of joint ventures and associates)

| Turnover | Operating profit | Adjusted operating profit | |||||||||||

| £ million | % | £ million | % | £ million | % | ||||||||

| Europe | 1,300.8 | 28 | 138.6 | 25 | 143.7 | 25 | |||||||

| Americas | 1,222.1 | 27 | 84.4 | 16 | 100.0 | 18 | |||||||

| Africa | 586.0 | 13 | 91.3 | 17 | 91.3 | 16 | |||||||

| Asia/Pacific | 1,496.1 | 32 | 229.2 | 42 | 229.2 | 41 | |||||||

| 4,605.0 | 100 | 543.5 | 100 | 564.2 | 100 | ||||||||

| Adjusted operating profit excludes exceptional items. See also pages 40 and 41 of the operating review. | |||||||||||||

The UK accounts for the largest part of the Group’s activities in Europe but BOC has significant gases subsidiaries in Ireland and Poland, vacuum products manufacturing in France and a pharmaceutical packaging machinery operation in the Netherlands.

Gist, BOC’s supply chain solutions business, operates principally in the UK but also has operations in other countries.

Subsidiaries in the US are engaged in the Group’s three lines of business. The Group’s other principal subsidiaries, joint ventures and associates in the Americas are located in Canada,Venezuela, Colombia, Chile and Mexico.

The largest Group subsidiary in Africa is African Oxygen Limited (Afrox), a South African public company in which the Group owns 56 per cent of the equity. The largest shareholder, other than BOC, holds less than 15 per cent of the equity. Afrox, primarily through wholly-owned subsidiaries, is engaged in the manufacture and sale of products within the PGS and ISP lines of business. Afrox also has a 20 per cent interest in private hospitals, clinics and other health care services in southern Africa.

There are other Group or Afrox subsidiary companies in Africa located in Botswana, Kenya, Malawi, Mozambique, N amibia, Nigeria, Swaziland,Tanzania, Uganda, Zambia and Zimbabwe. These companies are engaged primarily in the manufacture and/or sale of products in the ISP line of business.

BOC has businesses in most of the Asia/Pacific markets, including Japan, Korea,Thailand,Taiwan, Indonesia, Malaysia, Singapore, China, the Philippines, India, Pakistan, Bangladesh,Australia and New Zealand. In Australia, the Group’s business is conducted by BOC Limited. This company, as well as its subsidiaries, joint ventures and associates, is engaged in the manufacture and sale of products in the PGS and ISP lines of business. BOC participates in the liquefied petroleum gas market in Australia through a 50 per cent shareholding in Elgas Limited. Elsewhere in the Pacific region, the Group conducts its business through subsidiaries, joint ventures and associated companies.

Management organisation

BOC’s management structure is based on three global lines of business and, throughout the period 2003 to 2005, on two specialist businesses. Each line of business serves a clearly defined type of customer and each pursues its own strategy for growth and performance at a local level. The organisation is designed to maximise BOC’s global as well as local strengths. The lines of business have global responsibility to set strategy and prioritise investment. They include operational business units and these local units are responsible to the Group chief executive for delivering financial, safety and operational performance. The business units contribute to the development of the strategies of the lines of business and customise and implement them in local markets. The business unit heads collaborate in order to share best practice and to maximise growth and profit opportunities wherever they may appear.

Process Gas Solutions (PGS) manages all aspects of BOC’s business with customers requiring bulk supplies of industrial gases from on-site plants or by pipeline as well as deliveries of liquefied gases. Typical customers are found in the oil and chemicals, food and beverage, metals, and glass sectors all round the world. Marketing, business development and the execution of investments to provide customer specific solutions for the supply of industrial gases are handled by Process Systems, which forms part of PGS.

Industrial and Special Products (ISP) covers BOC’s business with customers in the fabrication, medical and leisure sectors as well as the special products and liquefied petroleum gases businesses.

BOC Edwards embraces all aspects of business with semiconductor industry customers worldwide including the supply of bulk gases and electronic materials, vacuum and abatement technology, chemical management systems and semiconductor-related services. BOC Edwards also serves general vacuum markets around the world and manufactures pharmaceutical freeze-drying and packaging machinery.

The segment reported as Afrox hospitals operated through Afrox Healthcare Limited up to the end of March 2005. It owned and managed private hospitals and clinics in southern Africa. BOC’s majority-owned subsidiary, African Oxygen Limited (Afrox), held 69 per cent of Afrox Healthcare Limited (AHealth) when the company was sold to a consortium led by two major black economic empowerment investors in March 2005. Afrox has retained a significant interest in the hospitals business through a 20 per cent holding in the new company.

In 2001, BOC Distribution Services was re-named Gist to reflect the changing nature of its business. Gist operates as a separate business unit outside the lines of business structure. It remains focused on developing business with major customers, including Marks & Spencer, and has developed capability in supply chain consultancy and end-to-end supply chain solutions.

| 16 | The BOC Group plc Annual report and accounts 2005 | Group profile |

Corporate development

Over the last three years BOC has continued to invest in its core businesses at the same time as divesting assets and businesses that were no longer consistent with its strategy.

In October 2002, BOC acquired Environmental Management Corporation (EMC), a privately owned water services company based in St Louis, Missouri. EMC manages water and wastewater treatment facilities for both industrial and local municipal customers around the US. EMC forms part of the PGS line of business, which is expanding the range of solutions offered to its industrial customer base.

BOC and Air Liquide merged their industrial and medical gases businesses in Japan in January 2003 and BOC’s subsidiary in Japan has retained a 45 per cent interest in the combined company called Japan Air Gases Ltd.

At the end of January 2003, BOC acquired the partial oxidation syngas plant at Clear Lake,Texas, from Celanese. Under the agreement BOC fulfils a significant proportion of the industrial gas requirements for the Celanese chemical facility at Clear Lake.

In March 2003 BOC announced an agreement to purchase the Canadian packaged gas and related welding equipment business of Air Products. The acquisition was completed in April 2003 following approval from the Canadian regulatory authority.

In June 2003, BOC announced an agreement to obtain half the output of a new helium extraction facility to be constructed in Qatar. Deliveries from the new source are now scheduled to commence during 2006.

In May 2004 BOC agreed to buy Duke Energy’s 30 per cent ownership interest in the Cantarell joint venture company for US$59.7 million in cash. This increased BOC’s overall stake to 65 per cent on completion in September 2004. This company supplies Pemex with nitrogen for the pressurisation of its oilfields in the Gulf of Mexico.

BOC completed the disposal of the packaged gas part of its US ISP business to Airgas Inc on 30 July 2004. The initial consideration received was US$175 million in cash and a final payment of US$20 million that had been subject to performance conditions was recognised in 2005. These funds were received in November 2005. All packaged gases and associated hardgoods were included in the sale. This comprised compressed industrial, speciality (excluding electronic) and medical gases in the US, sold through BOC retail and distributor channels. The sale did not include BOC’s bulk liquid helium, bulk medical gases and distributor businesses.

In October 2004, BOC purchased a 50 per cent holding in Asia Union Electronic Chemical Corporation (AUECC). This acquisition expanded BOC Edwards’ electronic materials offering to include the purification, blending, packaging and distribution of wet chemicals for flat panel display, semiconductor and solar cell manufacturers throughout Asia.

In December 2004, BOC sold its shares in Unique Gas and Petrochemicals thereby divesting interests in the LPG and bulk ammonia businesses in Thailand but the cylinder and aqueous ammonia business was retained.

At the end of January 2005, BOC acquired Calor Gas Limited’s UK aerosol propellants business. This includes the sales, marketing and distribution of bulk and packaged propane, isobutene and butane blends in the UK. The acquisition also included Calor’s CARE range of hydrocarbon refrigerants.

The segment reported as Afrox hospitals operated through Afrox Healthcare Limited up to the end of March 2005. It owned and managed private hospitals and clinics in southern Africa. BOC’s majority-owned subsidiary, African Oxygen Limited (Afrox), held 69 per cent of Afrox Healthcare Limited (AHealth) when the company was sold to a consortium led by two major black economic empowerment investors in March 2005. Afrox has retained a significant interest in the hospitals business through a 20 per cent holding in the new company.

In September2005, Gist acquired G Van Dongen Holding BV, a European temperature-controlled transport operator. The business, which had an annual turnover of some 46 million euros, expands Gist’s existing primary food business into continental Europe by providing fresh chill and ambient transport services to food manufacturers in the Netherlands, Spain, Germany, Portugal and France.

Industrial gases

The BOC Group is one of the major producers of industrial gases in the world. Its products include the atmospheric gases (nitrogen, oxygen and argon) produced by air separation plants as well as hydrogen, carbon monoxide and syngas (a mixture of hydrogen and carbon monoxide) made by technologies including steam-reforming or partial oxidation of hydrocarbons. The Group also markets carbon dioxide, helium and liquefied petroleum gas. These are generally derived as by-products from chemical processes or from natural sources and are also purchased from other producers. In addition, the Group markets dissolved acetylene and a wide range of special gases, medical gases, gas mixtures and gaseous chemicals.

Industry structure and consolidation The industrial gases business is capital-intensive, with increasing demand, together with economies of scale, leading to the need for large production units and distribution networks. The need for fixed asset investments, the trend towards global customers and the benefits from the transfer of applications technology worldwide have resulted in the business being handled by a relatively small number of companies internationally.

One or more of the other major international producers compete in each of the industrial gases markets served by the Group, and in many of the markets there are smaller local producers as well. International competitors include Air Liquide, Praxair, Air Products and Chemicals, Linde and Nippon Sanso. The world market for gases and related products is estimated to be some £25 billion a year.

| Group profile | 17 |

Principal industrial gas products Nitrogen possesses two key characteristics that make it the world’s most widely used and versatile industrial gas. Nitrogen is almost inert and when liquefied it is intensely cold. This makes liquid nitrogen a highly effective, versatile and non-polluting agent for freezing and chilling.

Under normal conditions nitrogen is chemically inactive. This makes it an important purging and blanketing gas in the chemical and refining industry as well as in the electronics industry.

Oxygen, in contrast to nitrogen, is useful for its reactivity. It supports combustion and it supports life. Oxygen has been used in welding and medicine for over 100 years and in steel production since the 1950s.

Iron and steel producers use oxygen to accelerate melting and to improve metal quality during the refining process. It is also used by the oil and chemicals industries and many others for a variety of oxidation processes. Mixed with fuel gases, oxygen provides a heat source for many welding, cutting and metal fabrication processes.

Argon makes up less than one per cent of the atmosphere but it is the most abundant truly inert gas. It is used to provide a shielding atmosphere in welding, metal fabrication, aluminium processing, microelectronics, glass coating, advanced ceramics and other industrial processes. It is also used in the steel industry, principally in the production of stainless steel.

Hydrogen is typically produced by steam reforming or partial oxidation of natural gas, petroleum gas, or liquid or solid hydrocarbon feedstocks. Hydrogen may also be recovered from by-products purchased by BOC from external suppliers. Hydrogen is used primarily in the oil and chemicals industries for applications aimed at upgrading crude oil through hydrocracking to form lighter fractions and to remove sulphur in the production of cleaner fuels. The chemicals industry also uses hydrogen where it is required as an active ingredient in many large-scale processes.

Helium is extracted from natural gas deposits. Only a few sources in the world contain a sufficient proportion of helium to justify its separation. The Group’s supplies now come from the US, Poland and Russia and are secured by long-term contracts. In June 2003, BOC announced an agreement to obtain half the output from a new helium extraction facility to be constructed in Qatar. Deliveries from this new source are now expected to begin in 2006. Due to its high value, helium is the only major industrial gas to be extensively traded internationally. Helium is used in welding, leak detection, hospital MRI scanners and in the production of optical fibres. Helium gas mixtures are used in balloons.

Carbon dioxide supplied by BOC is obtained as a by-product from other companies’ manufacturing processes, from natural sources or recovered in the generation process for hydrogen or syngas and put to constructive use. Solid carbon dioxide is, like liquid nitrogen, used for chilling and freezing in the food industry. As a gas it is used to carbonate and dispense beverages of all kinds.

Acetylene is normally supplied in cylinders and used together with oxygen in metal cutting and welding applications. BOC is a major manufacturer of dissolved acetylene.

Liquefied petroleum gas (LPG) is a fuel gas with a wide variety of domestic, industrial and transport applications. BOC is a major distributor of LPG in South Africa, and its joint venture company Elgas Limited is a major distributor in Australia. BOC has smaller market positions in several other countries.

Production of industrial gases Oxygen was first extracted from the atmosphere by a chemical process. This was superseded over 80 years ago by the cryogenic (low temperature) process involving the liquefaction and distillation of air. The cryogenic process is still by far the most widely used, but non-cryogenic techniques (pressure swing adsorption and membrane diffusion), which were first developed during the 1970s, are becoming increasingly significant for smaller or less demanding on-site applications.

Cryogenic air separation is a mature and stable technology, although incremental technical advances are still yielding improvements in capital cost, operating cost, ease of operation and reliability. The only significant ‘raw material’, apart from the air itself, is electricity, which is used in large quantities to drive compressors, pumps and other equipment. The production process in modern air separation plants is highly automated, and remote operation of BOC’s plants from control centres is becoming increasingly common.

The production of hydrogen and syngas uses steam reforming or partial oxidation of hydrocarbon feedstocks such as natural gas, petroleum or coal to separate the hydrogen and carbon compounds. The choice of feedstock is related to their prices in local markets.

Distribution of industrial gases Industrial gases may be supplied to customers in a variety of ways; through pipelines from on-site or nearby cryogenic or non-cryogenic plants, by deliveries of liquefied gases in road or rail tankers, in portable cryogenic containers or in cylinders (also called compressed or packaged gases).

Distribution is an important competitive factor in the industrial gases business and the methods of distribution vary according to the nature of the products themselves and the customer’s volume requirements. Most gases have to be stored and distributed either under great pressure, which requires them to be carried in heavy and bulky cylinders, or at extremely low temperatures in specially insulated tankers, which limits how far they can be transported before carriage costs become unacceptable. Pipeline delivery involves high capital costs and the routing is inflexible. As a result, there is little international trade in industrial gases. Production has to occur in or near the market being served and there is a trend towards production at customers’ own sites.

Business segments

The BOC Group reports financial results for the three lines of business and for Afrox hospitals and Gist separately.

| 18 | The BOC Group plc Annual report and accounts 2005 | Group profile |

Process Gas Solutions (PGS)

This line of business covers BOC’s business with larger-scale industrial customers worldwide, typically in the oil and chemicals, food and beverage, metals, and glass sectors. Gases and services are supplied as part of customer-specific solutions that create the most value for customers at the lowest cost to BOC. These range from supply by pipeline or from dedicated on-site plants to the largest users, to supply by road tanker in liquefied form to others.

Tonnage (pipeline) customers are usually supplied on the basis of long-term contracts, typically containing a fixed facility charge together with a variable charge for product supplied in excess of a set minimum quantity. Revenues from these contracts thus have a measure of stability with respect to changes in demand for product. Tonnage plants are often built to produce merchant gases in addition to those required by the tonnage customer and these gases can be sold to other customers. The BOC Group has substantial positions in the tonnage markets of the UK, the US,Australia, South Africa and Asia as well as in some smaller markets. The products supplied to tonnage customers have traditionally been the atmospheric gases oxygen, nitrogen and argon. More recently, hydrogen and syngas are becoming significant tonnage products as are associated utilities including steam and power.

The delivery of liquefied gases by road or rail to the customer’s site is normally limited by transport costs to a radius of about 200 miles. Product for this market is supplied either from merchant plants or from tonnage plants incorporating liquefiers. Larger users are typically supplied with product in liquid form delivered in cryogenic tankers into special storage vessels installed at customer premises. Tankers and vessels are often BOC Group owned. Liquefied gases are usually supplied on the basis of contracts with terms of one to five years. Revenues are generally based upon the actual quantity of gas consumed, with an additional fixed charge for the use of storage equipment.

The growth of sales and profit in this line of business is driven by investment in new production facilities. Such investment is predominantly the result of opportunities to satisfy long-term supply contracts with one or more heavy industrial customers for each plant.

Marketing, business development and the execution of investments to provide customer-specific solutions for the supply of industrial gases are handled by Process Systems, which forms part of PGS.

Business development In October 2002, BOC acquired Environmental Management Corporation (EMC), a privately owned water services company based in St Louis, Missouri. EMC manages water and wastewater treatment facilities for both industrial and local municipal customers around the US. EMC’s management services extend to steam systems, cold and chilled water systems and wastewater treatment. Customers include small to medium-sized municipalities and industrial customers, many of which are in the food sector. EMC forms part of the PGS line of business and BOC’s strategy is to expand the range of solutions offered to its industrial customer base.

At the end of January 2003, BOC acquired the partial oxidation syngas plant at Clear Lake,Texas, from Celanese. Under the agreement BOC fulfils a significant proportion of the industrial gas requirements for the Celanese chemical facility at Clear Lake. The Celanese facility is located on the Houston ship canal, and includes a world scale vinyl acetate monomer plant and the world’s largest acetic acid plant. These require large quantities of oxygen and nitrogen as well as carbon monoxide.

A new hydrogen and carbon monoxide (HyCO) plant supplying the Thai Polycarbonate Company for the manufacture of plastic resins began production in 2003.

In October 2003, BOC commissioned a new hydrogen plant supplying Citgo’s oil refinery at Lemont, Illinois. The hydrogen is used in the removal of sulphur to produce clean fuels.

In the same month BOC, and its joint venture partners, announced plans to invest over US$100 million in developing three schemes in China, at Taiyuan, Suzhou and in the Pearl River region.

BOC-TISCO, the joint venture between BOC Gases and Taiyuan Iron and Steel Corporation (TISCO), has under construction two new air separation units (ASUs) to supply 1,400 tonnes a day of oxygen each to TISCO’s plant in Shanxi province in north-central China. The new ASUs represent an investment of US$82 million and they are scheduled to begin coming on stream during 2006. This investment is in response to strong demand for stainless steel in China and will support TISCO’s vigorous expansion plans.

Pearl River Gases (PRG), a joint venture between Guangzhou Iron & Steel (GIS) and BOC’s joint venture, Hong Kong Oxygen, invested in two further ASU’s during 2005. These add some 400 tonnes a day of oxygen capacity to support the expansion of steelmaking in southern China.

Also in 2005, BOC’s wholly owned subsidiaries in Suzhou constructed new on-site supply scheme pipelines to meet increasing demand for industrial gases from key customers in Suzhou Industrial Park and the Suzhou New District Industrial Park.

A new hydrogen plant to supply both a Sunoco refinery, and a nearby BP refinery is under construction at Toledo, Ohio. The hydrogen will be used by both BP and Sunoco in the production of ultra-low sulphur gasoline and diesel fuels. The complex will be capable of supplying over 120 million standard cubic feet a day of hydrogen. BOC’s partner for engineering and construction is Linde BOC Process Plants of Tulsa, Oklahoma. BOC is investing more than US$100 million in the facility.

In May 2004 BOC agreed to buy Duke Energy’s 30 per cent ownership interest in the Cantarell joint venture company for US$59.7 million in cash. This increased BOC’s overall stake to 65 per cent on completion in September 2004. This company supplies Pemex with nitrogen for the pressurisation of its oilfields in the Gulf of Mexico.

In December 2004, BOC announced a new, 20-year agreement to supply an additional 300 million standard cubic feet a day (scf/d) of nitrogen to be used at the Cantarell and Ku Maalob Zaap oil fields. The additional supply will lift the total nitrogen output by 25 per cent to 1.5 billion scf/d at the site. Construction of a fifth production module has commenced and the new facility is scheduled to begin production in 2007.

| Group profile | 19 |

In China, significant new business was won in the chemical sector. BOC has agreed to form a joint venture with the Sinopec Shanghai Petrochemical Company (SPC) at Jinshan, near the Caojing chemical complex, to invest in existing assets and then add further air separation capacity to satisfy the industrial gases requirements of SPC in the region. This follows the establishment in 2003 of a similar joint venture with Sinopec YPC to supply the Sinopec and BASF joint venture petrochemical complex at Nanjing.

BOC’s subsidiary in Thailand is investing in a venture establishing a 1,300 tonnes-a-day plant to supply TOC Glycol Co. Ltd. (TOCGC) in Map Ta Phut and to increase merchant capacity in the area. When completed in 2006, this will be the largest air separation unit in Thailand. It will be owned and operated by a joint venture between BOC’s Thai subsidiary,TIG, and Bangkok Industrial Gas Company.

In January 2005 BOC formed a joint venture with Maanshan Iron & Steel Company (Ma Steel) to invest initially in the construction of two large air separation units. Each will be capable of supplying 1,400 tonnes a day of oxygen to meet the growing needs of Ma Steel in Maanshan City, China. Total production of oxygen, nitrogen and argon is expected to total some 5,000 tonnes a day when commissioned during 2007.

At the same time BOC India Ltd announced that it had been awarded a contract to supply gases requirements of approximately 1,400 tonnes a day for an expansion programme by Jindal Vijaynagar Steel Limited at Bellary in southern India. A plant with an oxygen capacity of 855 tonnes a day will be constructed and is expected to be commissioned in 2006.

In April 2005, BOC agreed to invest approximately US$40 million in equipment and pipelines in order to supply hydrogen to Valero’s 170,000 barrel a day refinery at Lima, Ohio and to supply other customers in the area. Construction of the plant has begun and it is expected to start supplying hydrogen during 2006.

In June 2005, BOC announced further refinery hydrogen business in the US with the proposed investment of nearly US$50 million at Salt Lake City to supply Chevron and Holly Corporation’s Utah subsidiary with hydrogen for cleaner fuels production at their refineries. The refiners are upgrading their facilities in accordance with the US Environmental Protection Agency’s lower-sulphur requirements for gasoline and diesel fuels.

Chevron is installing additional hydrotreating capacity at its 49,000 barrel per day (bpd) refinery and will take hydrogen and steam from BOC’s plant, which will be located on the Chevron site. Holly will also receive hydrogen for new hydrotreating capacity at its nearby 26,000 bpd Woods Cross refinery through a five-mile pipeline connection from the BOC facility.

Construction of the hydrogen plant has started and production is expected to begin in 2006.

Industrial and Special Products (ISP)

Gases for cutting and welding, hospitality, laboratory applications and a variety of medical purposes are mainly distributed under pressure in cylinders. The ISP line of business covers products and services provided to this section of the market together with sales of packaged chemicals and liquefied petroleum gas (LPG). Customers are typically in the fabrication, engineering, automotive, refrigeration, hospitality or medical sectors. The customer base is therefore broad and varied. The number of separate customers served by ISP is much greater than the other two lines of business and the quality of service is often the key factor in securing existing or obtaining new customers. In order to raise service standards at the same time as reducing costs, national customer service centres have been successfully established in all the major markets.

In addition to supplying gases, BOC also supplies a range of associated equipment in many of its major markets. This includes cutting and welding products and, in some markets, associated safety equipment.

BOC has devoted considerable attention over the last few years to understand the requirements of different types of customer in its major markets and to provide the required service at an appropriate price. Such customer segmentation programmes have been implemented in the UK, South Africa,Australia,Asia, Latin America and are in progress elsewhere.

The cutting and welding applications are a relatively mature part of the industrial gases business and growth opportunities are principally in other segments of the market such as medical applications, safety products, packaged chemicals, hospitality and services. BOC is pursuing these opportunities by the development of new products, packages and services as well as by marketing initiatives to take advantage of BOC’s global capabilities by introducing existing products to new regions. Electronic commerce has also become an important tool for sustaining and growing sales by making it easier for customers to manage their business with BOC as a supplier.

BOC is a leading supplier of helium and has liquid helium distribution centres, or transfills, in many markets around the world. With 48 helium transfills in its global network, management believes that this is the largest of its kind. Helium has a broad range of applications, including welding and the refrigeration of medical scanner magnets, and is vital to the production of optical fibres, semiconductors and special alloys. It is also used for leak detection, underwater breathing mixtures and lifting.

Business development In April 2002, BOC acquired Matheson Gas Products Canada Inc, one of Canada’s leading providers of special gases and equipment. Unique Gas and Petrochemicals Public Company Limited (UGP), a leading distributor of liquefied petroleum gas (LPG) and ammonia in Thailand, was acquired in May 2002. BOC’s associated company in Malaysia acquired 35.6 per cent of the gases company Nissan Industrial Oxygen Inc (NIOI) in March 2002 and, following a tender offer, increased its holding to 100 per cent in September 2002. At the end of August 2002, BOC announced an agreement to purchase Praxair’s Polish gases business. The transaction was completed in January 2003 following approval by the Polish competition authority. The business acquired includes a high proportion of ISP sales.

Since 2002, BOC has continued its global roll-out of a light-weight medical cylinder with an integrated valve and regulator for homecare patients and emergency services. Heliox, a helium and oxygen mixture formulated to ease the respiratory effort associated with airway obstruction, was launched in the UK and in some other markets.

| 20 | The BOC Group plc Annual report and accounts 2005 | Group profile |

Capacity at BOC’s Otis, Kansas, helium plant was expanded in 2002 to match market demands. In addition, BOC has access to helium produced by other US plants, as well as to product from Poland and Russia. In 2003 BOC and KRIO, a division of the Polish Oil and Gas Company, entered into a new helium supply agreement. BOC will purchase for export all of KRIO’s helium that is not sold to its domestic customers in Poland. BOC has been KRIO’s sole customer for bulk liquid helium since the original agreement was signed in 1972. In June 2003, BOC announced an agreement to obtain half the output from a new helium extraction facility to be constructed in Qatar. Deliveries from this new source are now expected to begin in 2006.

Magnetic resonance imaging (MRI) systems use liquid helium to cool superconducting magnets. BOC provides helium as well as a liquid nitrogen filling service to meet MRI operators’ total requirements. In 2002, ISP signed a major helium supply scheme with Oxford Magnet Technology (now Siemens) in the UK.

BOC continued to invest in refrigerant filling facilities and in 2003 new filling facilities were installed in Hong Kong, Malaysia and the Philippines. Each of these was built to a standardised global design. BOC now supplies refrigerants in 19 countries compared with six countries in 1999. In June 2003, BOC announced a global alliance with Hudson Technologies to promote technology for cleaning and recycling used refrigerants.

Significant progress in developing web-based customer portals has been made. Amongst others, ISP has launched customer portals in the UK,Australia and New Zealand. Thousands of customers are now able to access detailed material on BOC’s product service offers, manage and settle their accounts and place orders on-line.

BOC acquired the Canadian packaged gas and related welding equipment business of Air Products in April 2003.

BOC completed the disposal of the packaged gas part of its US ISP business to Airgas Inc on 30 July 2004. The initial consideration was US$175 million in cash and a final payment of US$20 million that had been subject to performance conditions was received in November 2005. All packaged gases and associated hardgoods were included in the sale. This comprised compressed industrial, speciality (excluding electronic) and medical gases in the US, sold through BOC retail and distributor channels. The sale did not include BOC’s bulk liquid helium, bulk medical gases and distributor businesses.