UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM 10-Q

(Mark One)

☒ QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended March 31, 2024

OR

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from _______ to _______

Commission file number 1-35015

ACNB CORPORATION

(Exact name of Registrant as specified in its charter)

| | | | | | | | |

| Pennsylvania | | 23-2233457 |

| (State or other jurisdiction of | | (I.R.S. Employer |

| incorporation or organization) | | Identification No.) |

| | | | | | | | |

| 16 Lincoln Square, Gettysburg, Pennsylvania | | 17325 |

| (Address of principal executive offices) | | (Zip Code) |

Registrant’s telephone number, including area code: (717) 334-3161

Securities registered pursuant to Section 12(b) of the Act:

| | | | | | | | | | | | | | |

| Title of each class | | Trading Symbol | | Name of each exchange on which registered |

| Common Stock, $2.50 par value per share | | ACNB | | The NASDAQ Stock Market, LLC |

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the Registrant has submitted electronically every Interactive Data File required to be submitted and pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the Registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer”, “accelerated filer”, “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| | | | | | | | | | | | | | | | | |

| Large accelerated filer | ☐ | | Accelerated filer | | ☒ |

| Non-accelerated filer | ☐ | | Smaller reporting company | ☐ |

| Emerging growth company | ☐ | | | | |

If an emerging growth company, indicate by check mark if the Registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐

No ☒

The number of shares of the Registrant’s Common Stock outstanding on May 1, 2024, was 8,539,575.

ACNB CORPORATION

Table of Contents

| | | | | | | | |

| | Page |

| | |

| Part I - Financial Information | |

| Item 1. | | |

| | |

| | |

| | |

| | |

| | |

| Item 2. | | |

| Item 3. | | |

| Item 4. | | |

| Part II - Other Information | |

| Item 1. | | |

| Item 1A. | | |

| Item 2. | | |

| Item 3. | | |

| Item 4. | | |

| Item 5. | | |

| Item 6. | | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

ACNB CORPORATION

Glossary of Defined Acronyms and Terms

| | | | | |

| ACL | Allowance for Credit Losses |

| ACNB Insurance Services | ACNB Insurance Services, Inc. |

| ACNB, Corporation or Company | ACNB Corporation |

| AFS | Available for Sale |

| |

| ALCO | Asset Liability Committee |

| ASC | Accounting Standard Codification |

| ASU | Accounting Standard Update |

| ATM | Automatic Teller Machine |

| Bank | ACNB Bank |

| Basel III | Risk-based requirements and rules issued by federal banking agencies |

| bp or bps | Basis point(s) |

| |

| |

| |

| CECL | Current Expected Credit Loss |

| |

| CME | Chicago Mercantile Exchange |

| |

| CRA | Community Reinvestment Act of 1977 |

| |

| |

| |

| ETR | Effective Tax Rate |

| Exchange Act | Securities Exchange Act of 1934 |

| FASB | Financial Accounting Standards Board |

| FCA | Financial Conduct Authority |

| |

| FCBI | Frederick County Bancorp, Inc. |

| FDIC | Federal Deposit Insurance Corporation |

| |

| |

| |

| FOMC | Federal Open Market Committee |

| FTE | Fully Taxable Equivalent |

| GAAP | U.S. Generally Accepted Accounting Principles |

| |

| |

| |

| HTM | Held to Maturity |

| |

| |

| LIBOR | London Inter-Bank Offered Rate |

| |

| Market Area | Southcentral Pennsylvania and Northern Maryland |

| |

| |

| |

| |

| |

| |

| |

| PPP | Paycheck Protection Program |

| Purchase Agreements | Subordinated Note Purchase Agreements |

| Purchasers | Institutional accredited investors and qualified institutional buyers |

| |

| SBIC | Small Business Investment Company |

| SEC | Securities and Exchange Commission |

| |

| SOFR | Secured Overnight Financing Rate |

| Subordinated Notes | 4.00% fixed-to-floating rate subordinated notes due March 31, 2031 |

| |

| |

PART I - FINANCIAL INFORMATION

ACNB CORPORATION

ITEM 1 - FINANCIAL STATEMENTS

CONSOLIDATED STATEMENTS OF CONDITION (UNAUDITED)

| | | | | | | | | | | |

| (Dollars in thousands, except per share data) | March 31,

2024 | | December 31,

2023 |

| ASSETS | | | |

| Cash and due from banks | $ | 17,395 | | | $ | 21,442 | |

| Interest-bearing deposits with banks | 35,740 | | | 44,516 | |

| Total Cash and Cash Equivalents | 53,135 | | | 65,958 | |

| Equity securities with readily determinable fair values | 918 | | | 928 | |

| Investment securities available for sale, at estimated fair value | 425,114 | | | 451,693 | |

| Investment securities held to maturity, at amortized cost (fair value $58,084, $59,057) | 64,594 | | | 64,600 | |

| Loans held for sale | 88 | | | 280 | |

| Total loans, net of unearned income | 1,664,980 | | | 1,627,988 | |

| Less: Allowance for credit losses | (20,172) | | | (19,969) | |

| Loans, net | 1,644,808 | | | 1,608,019 | |

| | | |

| Premises and equipment, net | 25,916 | | | 26,283 | |

| Right of use asset | 2,447 | | | 2,615 | |

| Restricted investment in bank stocks | 10,877 | | | 9,677 | |

| Investment in bank-owned life insurance | 80,348 | | | 79,871 | |

| Investments in low-income housing partnerships | 971 | | | 1,003 | |

| Goodwill | 44,185 | | | 44,185 | |

| Intangible assets, net | 8,761 | | | 9,082 | |

| Foreclosed assets held for resale | 467 | | | 467 | |

| Other assets | 51,659 | | | 54,186 | |

| Total Assets | $ | 2,414,288 | | | $ | 2,418,847 | |

| | | |

| LIABILITIES AND STOCKHOLDERS’ EQUITY | | | |

| Deposits: | | | |

| Noninterest-bearing | $ | 499,583 | | | $ | 500,332 | |

| Interest-bearing | 1,335,641 | | | 1,361,481 | |

| Total Deposits | 1,835,224 | | | 1,861,813 | |

| Short-term borrowings | 17,303 | | | 56,882 | |

| Long-term borrowings | 255,302 | | | 195,292 | |

| Lease liability | 2,447 | | | 2,615 | |

| Allowance for unfunded commitments | 1,569 | | | 1,719 | |

| Other liabilities | 22,523 | | | 23,065 | |

| Total Liabilities | 2,134,368 | | | 2,141,386 | |

| | | |

| Stockholders’ Equity: | | | |

| Preferred stock, $2.50 par value; 20,000,000 shares authorized; no shares outstanding at March 31, 2024 and December 31, 2023, respectively | — | | | — | |

| Common stock, $2.50 par value; 20,000,000 shares authorized; 8,928,441 and 8,896,119 shares issued; 8,539,575 and 8,511,453 shares outstanding at March 31, 2024 and December 31, 2023, respectively | 22,315 | | | 22,231 | |

| Treasury stock, at cost; 388,866 and 384,666 shares at March 31, 2024 and December 31, 2023, respectively | (11,101) | | | (10,954) | |

| Additional paid-in capital | 97,818 | | | 97,602 | |

| Retained earnings | 217,712 | | | 213,491 | |

| Accumulated other comprehensive loss | (46,824) | | | (44,909) | |

| Total Stockholders’ Equity | 279,920 | | | 277,461 | |

| Total Liabilities and Stockholders’ Equity | $ | 2,414,288 | | | $ | 2,418,847 | |

The accompanying notes are an integral part of the Consolidated Financial Statements.

ACNB CORPORATION | | | | | | | | | | | | | | | |

| CONSOLIDATED STATEMENTS OF INCOME (UNAUDITED) | Three Months Ended March 31, | | |

| (Dollars in thousands, except per share data) | 2024 | | 2023 | | | | |

| INTEREST AND DIVIDEND INCOME | | | | | | | |

| Loans, including fees | | | | | | | |

| Taxable | $ | 21,470 | | | $ | 18,898 | | | | | |

| Tax-exempt | 319 | | | 356 | | | | | |

| Securities: | | | | | | | |

| Taxable | 2,911 | | | 3,286 | | | | | |

| Tax-exempt | 284 | | | 314 | | | | | |

| Dividends | 240 | | | 41 | | | | | |

| Other | 750 | | | 1,014 | | | | | |

| Total Interest and Dividend Income | 25,974 | | | 23,909 | | | | | |

| INTEREST EXPENSE | | | | | | | |

| Deposits | 2,160 | | | 473 | | | | | |

| Short-term borrowings | 339 | | | 17 | | | | | |

| Long-term borrowings | 2,882 | | | 327 | | | | | |

| Total Interest Expense | 5,381 | | | 817 | | | | | |

| Net Interest Income | 20,593 | | | 23,092 | | | | | |

| Provision for credit losses | 223 | | | 97 | | | | | |

| (Reversal of) provision for unfunded commitments | (151) | | | 276 | | | | | |

| Net Interest Income after Provisions for Credit Losses and Unfunded Commitments | 20,521 | | | 22,719 | | | | | |

| NONINTEREST INCOME | | | | | | | |

| Insurance commissions | 2,115 | | | 1,902 | | | | | |

| Service charges on deposits | 991 | | | 962 | | | | | |

| Wealth management | 962 | | | 840 | | | | | |

| ATM debit card charges | 819 | | | 823 | | | | | |

| Earnings on investment in bank-owned life insurance | 477 | | | 442 | | | | | |

| Gain from mortgage loans held for sale | 48 | | | 17 | | | | | |

| | | | | | | |

| Net gains (losses) on sales or calls of investment securities | 69 | | | (193) | | | | | |

| Net (losses) gains on equity securities | (10) | | | 20 | | | | | |

| | | | | | | |

| | | | | | | |

| Other | 196 | | | 171 | | | | | |

| Total Noninterest Income | 5,667 | | | 4,984 | | | | | |

| NONINTEREST EXPENSES | | | | | | | |

| Salaries and employee benefits | 11,168 | | | 10,442 | | | | | |

| Equipment | 1,729 | | | 1,607 | | | | | |

| Net occupancy | 1,130 | | | 1,037 | | | | | |

| Professional services | 616 | | | 382 | | | | | |

| FDIC and regulatory | 375 | | | 249 | | | | | |

| Other tax | 370 | | | 337 | | | | | |

| Intangible assets amortization | 321 | | | 360 | | | | | |

| Supplies and postage | 191 | | | 206 | | | | | |

| Marketing and corporate relations | 88 | | | 154 | | | | | |

| | | | | | | |

| | | | | | | |

| Other | 1,674 | | | 1,508 | | | | | |

| Total Noninterest Expenses | 17,662 | | | 16,282 | | | | | |

| Income before Income Taxes | 8,526 | | | 11,421 | | | | | |

| Provision for income taxes | 1,758 | | | 2,398 | | | | | |

| Net Income | $ | 6,768 | | | $ | 9,023 | | | | | |

| PER SHARE DATA | | | | | | | |

| Basic and diluted earnings | $ | 0.80 | | | $ | 1.06 | | | | | |

| | | | | | | |

The accompanying notes are an integral part of the Consolidated Financial Statements.

ACNB CORPORATION

CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME (UNAUDITED)

| | | | | | | | | | | | | | | | | | |

| | | Three Months Ended March 31, | | |

| (Dollars in thousands) | | 2024 | | 2023 | | | | |

| NET INCOME | | $ | 6,768 | | | $ | 9,023 | | | | | |

| | | | | | | | |

| OTHER COMPREHENSIVE (LOSS) INCOME | | | | | | | | |

| INVESTMENT SECURITIES | | | | | | | | |

| Unrealized (losses) gains arising during the period, net of income tax (benefit) expense of $(644) and $558, respectively | | (2,198) | | | 5,136 | | | | | |

Reclassification adjustment for net AFS investment securities gains (losses) included in net income, net of income tax expense (benefit) of $16 and $(45), respectively | | 53 | | | (146) | | | | | |

| Total unrealized (loss) gain on AFS investment securities | | (2,145) | | | 4,990 | | | | | |

| Amortization of unrealized losses on AFS investment securities transferred to HTM, net of income taxes of $63 and $223, respectively | | 215 | | | 1,014 | | | | | |

| | | | | | | | |

| PENSION | | | | | | | | |

| Amortization of pension net loss, transition liability, and prior service cost, net of income taxes of $4 and $50, respectively | | 15 | | | 48 | | | | | |

| | | | | | | | |

| | | | | | | | |

| TOTAL OTHER COMPREHENSIVE (LOSS) INCOME | | (1,915) | | | 6,052 | | | | | |

| TOTAL COMPREHENSIVE INCOME | | $ | 4,853 | | | $ | 15,075 | | | | | |

The accompanying notes are an integral part of the Consolidated Financial Statements.

ACNB CORPORATION

CONSOLIDATED STATEMENTS OF CHANGES IN STOCKHOLDERS’ EQUITY (UNAUDITED)

Three Months Ended March 31, 2024 and 2023

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| (Dollars in thousands, except per share data) | | | Common Stock | | Treasury Stock | | Additional Paid-in Capital | | Retained

Earnings | | Accumulated

Other

Comprehensive

Loss | | Total

Stockholders’

Equity |

| BALANCE – January 1, 2024 | | | $ | 22,231 | | | $ | (10,954) | | | $ | 97,602 | | | $ | 213,491 | | | $ | (44,909) | | | $ | 277,461 | |

| Net income | | | — | | | — | | | — | | | 6,768 | | | — | | | 6,768 | |

| Other comprehensive loss, net of taxes | | | — | | | — | | | — | | | — | | | (1,915) | | | (1,915) | |

| Common stock shares issued (4,898 shares) | | | 13 | | | — | | | 161 | | | — | | | — | | | 174 | |

| Repurchase shares (4,200 shares) | | | — | | | (147) | | | — | | | — | | | — | | | (147) | |

| Restricted stock grants, net of forfeitures and withheld for taxes (27,424 shares) | | | 71 | | | — | | | (479) | | | — | | | — | | | (408) | |

| Compensation expense for restricted shares | | | — | | | — | | | 534 | | | — | | | — | | | 534 | |

| Cash dividends declared ($0.30 per share) | | | — | | | — | | | — | | | (2,547) | | | — | | | (2,547) | |

| BALANCE – March 31, 2024 | | | $ | 22,315 | | | $ | (11,101) | | | $ | 97,818 | | | $ | 217,712 | | | $ | (46,824) | | | $ | 279,920 | |

| | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| (Dollars in thousands, except per share data) | Common Stock | | Treasury Stock | | Additional Paid-in Capital | | Retained

Earnings | | Accumulated

Other

Comprehensive

Loss | | Total

Stockholders’

Equity |

| BALANCE – January 1, 2023 | $ | 22,086 | | | $ | (8,927) | | | $ | 96,022 | | | $ | 193,873 | | | $ | (58,012) | | | $ | 245,042 | |

| Cumulative effect for adoption of Topic 326, net of tax | — | | | — | | | — | | | (2,368) | | | — | | | (2,368) | |

| Net income | — | | | — | | | — | | | 9,023 | | | — | | | 9,023 | |

| Other comprehensive income, net of taxes | — | | | — | | | — | | | — | | | 6,052 | | | 6,052 | |

| Common stock shares issued (5,889 shares) | 15 | | | — | | | 173 | | | — | | | — | | | 188 | |

| Repurchase shares (850 shares) | — | | | (29) | | | — | | | — | | | — | | | (29) | |

| Restricted stock grants, net of forfeitures and withheld for taxes (43,074 shares) | 97 | | | — | | | (97) | | | — | | | — | | | — | |

| Compensation expense for restricted shares | — | | | — | | | 317 | | | — | | | — | | | 317 | |

| Cash dividends declared ($0.28 per share) | — | | | — | | | — | | | (2,384) | | | — | | | (2,384) | |

| BALANCE – March 31, 2023 | $ | 22,198 | | | $ | (8,956) | | | $ | 96,415 | | | $ | 198,144 | | | $ | (51,960) | | | $ | 255,841 | |

| | | | | | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

The accompanying notes are an integral part of the Consolidated Financial Statements.

ACNB CORPORATION

CONSOLIDATED STATEMENTS OF CASH FLOWS (UNAUDITED)

| | | | | | | | | | | |

| | Three Months Ended March 31, |

| (In thousands) | 2024 | | 2023 |

| CASH FLOWS FROM OPERATING ACTIVITIES | | | |

| Net income | $ | 6,768 | | | $ | 9,023 | |

| Adjustments to reconcile net income to net cash provided by operating activities: | | | |

| Gain on sales of loans originated for sale | (48) | | | (17) | |

| | | |

| | | |

| Earnings on investment in bank-owned life insurance | (477) | | | (442) | |

| | | |

| (Gain) loss on sales or calls of securities | (69) | | | 193 | |

| Loss (gain) on equity securities | 10 | | | (20) | |

| Restricted stock compensation expense | 534 | | | 317 | |

| | | |

| Depreciation and amortization | 766 | | | 883 | |

| Provision for credit losses and provision for unfunded commitments | 72 | | | 373 | |

| Net amortization of investment securities premiums | 414 | | | 446 | |

| (Increase) decrease in interest receivable | (60) | | | 18 | |

| Increase in interest payable | 682 | | | 72 | |

| Mortgage loans originated for sale | (1,820) | | | (8,375) | |

| Proceeds from sales of loans originated for sale | 2,060 | | | 8,348 | |

| Decrease in other assets | 3,589 | | | 606 | |

| Increase in deferred tax asset | (222) | | | (972) | |

| (Decrease) increase in other liabilities | (1,381) | | | 4,466 | |

| Net Cash Provided by Operating Activities | 10,818 | | | 14,919 | |

| CASH FLOWS FROM INVESTING ACTIVITIES | | | |

| Proceeds from calls/maturities of investment securities held to maturity | 184 | | | 205 | |

| Proceeds from calls/maturities of investment securities available for sale | 9,225 | | | 10,912 | |

| Proceeds from sales of investment securities available for sale | 14,336 | | | 46,612 | |

| Proceeds from sale of equity securities | — | | | 369 | |

| | | |

| | | |

| Redemption of equity securities | — | | | 40 | |

| Purchase of restricted investment in bank stocks | (1,200) | | | (923) | |

| Net (increase) decrease in loans | (37,012) | | | 5,867 | |

| | | |

| | | |

| | | |

| | | |

| | | |

| Capital expenditures | (78) | | | (58) | |

| | | |

| | | |

| Net Cash Provided by (Used in) Investing Activities | (14,545) | | | 63,024 | |

| CASH FLOWS FROM FINANCING ACTIVITIES | | | |

| Net decrease in noninterest-bearing deposits | (749) | | | (694) | |

| Net decrease in interest-bearing deposits | (25,840) | | | (142,459) | |

| Net decrease in short-term borrowings | (39,579) | | | (11,660) | |

| Proceeds from long-term borrowings | 60,000 | | | 25,000 | |

| | | |

| Dividends paid | (2,547) | | | (2,384) | |

| Common stock repurchased | (147) | | | (29) | |

| Common stock issued, net of restricted stock forfeitures and withheld for taxes | (234) | | | 188 | |

| Net Cash Used In Financing Activities | (9,096) | | | (132,038) | |

| Net Decrease in Cash and Cash Equivalents | (12,823) | | | (54,095) | |

| CASH AND CASH EQUIVALENTS — BEGINNING | 65,958 | | | 168,161 | |

| CASH AND CASH EQUIVALENTS — ENDING | $ | 53,135 | | | $ | 114,066 | |

| Supplemental disclosures of cash flow information: | | | |

| Cash paid for interest | $ | 5,321 | | | $ | 745 | |

| Cash paid for income taxes | — | | | — | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

The accompanying notes are an integral part of the Consolidated Financial Statements.

ACNB CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

Note 1 - Basis of Presentation and Nature of Operations

ACNB Corporation, headquartered in Gettysburg, Pennsylvania, provides banking, insurance, and financial services to businesses and consumers through its wholly-owned subsidiaries, ACNB Bank and ACNB Insurance Services. The Bank engages in full-service commercial and consumer banking and wealth management services, including trust and retail brokerage, through its 26 community banking offices, including 17 community banking office locations in Adams, Cumberland, Franklin and York Counties, Pennsylvania, and nine community banking office locations in Carroll and Frederick Counties, Maryland. There are also loan production offices in Lancaster and York, Pennsylvania, and Hunt Valley, Maryland.

ACNB Insurance Services is a full-service insurance agency based in Westminster, Maryland, with additional locations in Jarrettsville, Maryland, and Gettysburg, Pennsylvania. The agency offers a broad range of property, casualty, health, life and disability insurance to both individual and commercial clients.

The accompanying unaudited Consolidated Financial Statements have been prepared in accordance with GAAP for interim financial information and with the instructions to Form 10-Q and Article 10 of Regulation S-X. The preparation of financial statements in accordance with GAAP requires management to make estimates and assumptions that affect the amounts of assets and liabilities as of the date of the financial statements as well as revenues and expenses during the period. Actual results could differ from those estimates. In the opinion of management, the accompanying unaudited Consolidated Financial Statements contain all adjustments necessary for a fair presentation. All such adjustments are of a normal recurring nature. These Consolidated Financial Statements should be read in conjunction with the audited Consolidated Financial Statements and the notes included in the Corporation’s Annual Report on Form 10-K for the year ended December 31, 2023. The Corporation evaluates subsequent events through the filing date of this From 10-Q with the SEC. The results of operations for the three month period ended March 31, 2024, are not necessarily indicative of the results to be expected for the full year.

Certain reclassifications have been made to the prior period financial statements to conform to the current period presentation. Reclassifications had no material effect on prior year net income or stockholders’ equity.

Significant Accounting Policies

The significant accounting policies used in preparation of the Consolidated Financial Statements are disclosed in the Corporation’s 2023 Annual Report on Form 10-K. Those significant accounting policies are unchanged at March 31, 2024.

Recently Issued Accounting Standards

In December 2022, the FASB issued ASU 2022-06, “Deferral of the Sunset Date of Reference Rate Reform (Topic 848)”. This ASU extends the sunset date of ASC Topic 848 (Reference Rate Reform) to December 31, 2024, in response to the United Kingdom’s FCA extension of the intended cessation date of LIBOR in the United States. The Corporation evaluated the impact of this standard, and believes that its adoption will not have a material impact on the Corporation’s Consolidated Financial Statements.

In November 2023, the FASB issued ASU 2023-07, “Segment Reporting (Topic 280)”. The amendments in this ASU are expected to improve financial reporting by requiring disclosure of incremental segment information on an annual and interim basis for all public entities to enable investors to develop more decision-useful financial analyses. The amendments of ASU 2023-07 are effective for fiscal years beginning after December 15, 2023, and for interim periods within fiscal years beginning after December 15, 2024, with early adoption permitted. The amendments in ASU 2023-07 should be applied retrospectively to all periods presented on the financial statements. The Corporation adopted the amendments of ASU 2023-07 related to annual disclosure requirements effective January 1, 2024, and will present any newly required annual disclosures in its Annual Report on Form 10-K for the year ending December 31, 2024 and intends to adopt the amendments of ASU 2023-07 related to interim disclosure requirements effective January 1, 2025, and will present any newly required interim disclosures beginning with its Quarterly Report on Form 10-Q for the period ending March 31, 2025. Adoption of this standard is not expected to have a material impact on the Corporation’s Consolidated Financial Statements.

In December 2023, the FASB issued ASU 2023-09, “Income Taxes (Topic 740)”. This ASU is intended to improve the disclosures for income taxes to address requests from investors, lenders, creditors and other allocators of capital that use the financial statements to make capital allocation decisions. The amendments in ASU 2023-09 will require consistent categories and greater disaggregation of information in the rate reconciliation disclosure as well as disclosure of income taxes paid disaggregated by jurisdiction. The amendments of ASU 2023-09 are effective for annual periods beginning after December 15, 2024, and early adoption is permitted for annual financial statements that have not yet been issued or made available for issuance. The Corporation intends to adopt the amendments of ASU 2023-09 effective January 1, 2025, and will include the required disclosures in its Annual Report on Form 10-K for the year ending December 31, 2025. The Corporation is currently evaluating the impact of this standard, and believes that its adoption will not have a material impact on the Corporation’s Consolidated Financial Statements.

Note 2 - Earnings Per Share and Restricted Stock

The Corporation has a simple capital structure. Basic earnings per share of common stock is calculated as net income available to common shareholders divided by the weighted average number of shares outstanding less unvested restricted stock at the end of the period. Diluted earnings per share is calculated as net income available to common shareholders divided by the weighted average number of shares outstanding.

| | | | | | | | | | | | | | | |

| Three Months Ended March 31, | | |

| 2024 | | 2023 | | | | |

| Weighted average shares outstanding (basic) | 8,493,104 | | | 8,511,244 | | | | | |

| Dilutive effect of unvested shares | 18,544 | | | 11,732 | | | | | |

| Weighted average shares outstanding (diluted) | 8,511,648 | | | 8,522,976 | | | | | |

| Per share: | | | | | | | |

| Basic | $ | 0.80 | | | $ | 1.06 | | | | | |

| Diluted | 0.80 | | | 1.06 | | | | | |

There were no antidilutive instruments at March 31, 2024 and 2023.

Stock Incentive Plan

On May 1, 2018, shareholders approved and ratified the ACNB Corporation 2018 Omnibus Stock Incentive Plan, effective as of March 20, 2018, in which awards shall not exceed, in the aggregate, 400,000 shares of common stock, plus any shares that were authorized, but not issued, under the ACNB Corporation 2009 Restricted Stock Plan. The ACNB Corporation 2009 Restricted Stock Plan expired by its own terms after 10 years on February 24, 2019. No further shares may be issued under this plan. The remaining 174,055 shares were transferred to the ACNB Corporation 2018 Omnibus Stock Incentive Plan.

As of March 31, 2024, 138,019 shares were issued under this plan, of which 38,438 were unvested. Plan expense is recognized over the vesting period of the stock issued and resulted in $534 thousand and $495 thousand of compensation expense during the three months ended March 31, 2024 and 2023, respectively.

Share Repurchase Plan

On October 24, 2022, the Corporation announced that the Board of Directors approved on October 18, 2022, a plan to repurchase, in open market and privately negotiated transactions, up to 255,575, or approximately 3%, of the outstanding shares of the Corporation’s common stock. This new common stock repurchase program replaces and supersedes any and all earlier announced repurchase plans. There were 65,266 treasury shares purchased under this plan through March 31, 2024.

Note 3 - Investment Securities

Fair value of equity securities with readily determinable fair values at March 31, 2024 and December 31, 2023, are as follows:

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| (In thousands) | Fair Value at Beginning of Period | | | Sales/reclassification | | (Losses) Gains | | Losses on sales of securities | | Fair Value at End of Period |

| Three Months Ended March 31, 2024 | | | | | | | | | | |

| CRA Mutual Fund | $ | 928 | | | | $ | — | | | $ | (10) | | | $ | — | | | $ | 918 | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

| Twelve Months Ended December 31, 2023 | | | | | | | | | | |

| CRA Mutual Fund | $ | 915 | | | | $ | — | | | $ | 13 | | | $ | — | | | $ | 928 | |

| Canapi Ventures SBIC Fund | 206 | | | | 206 | | | — | | | — | | | — | |

| Stock in other banks | 598 | | | | 592 | | | 5 | | | (11) | | | — | |

| $ | 1,719 | | | | $ | 798 | | | $ | 18 | | | $ | (11) | | | $ | 928 | |

Amortized cost and fair value of securities were as follows:

| | | | | | | | | | | | | | | | | | | | | | | |

| (In thousands) | Amortized

Cost | | Gross

Unrealized

Gains | | Gross

Unrealized

Losses | | Fair

Value |

| March 31, 2024 | | | | | | | |

| Available for Sale | | | | | | | |

| U.S. Government and agencies | $ | 176,049 | | | $ | — | | | $ | 20,228 | | | $ | 155,821 | |

| Collateralized mortgage obligations | 43,892 | | | — | | | 4,386 | | | 39,506 | |

| Residential mortgage-backed securities | 173,920 | | | — | | | 21,340 | | | 152,580 | |

| Commercial mortgage-backed securities | 66,136 | | | 3 | | | 4,485 | | | 61,654 | |

| | | | | | | |

| Corporate bonds | 18,109 | | | — | | | 2,556 | | | 15,553 | |

| $ | 478,106 | | | $ | 3 | | | $ | 52,995 | | | $ | 425,114 | |

| | | | | | | |

| Held to Maturity | | | | | | | |

| | | | | | | |

| State and municipal | $ | 62,310 | | | $ | — | | | $ | 6,387 | | | $ | 55,923 | |

| Residential mortgage-backed securities | 2,284 | | | — | | | 123 | | | 2,161 | |

| $ | 64,594 | | | $ | — | | | $ | 6,510 | | | $ | 58,084 | |

| | | | | | | |

| December 31, 2023 | | | | | | | |

| Available for Sale | | | | | | | |

| U.S. Government and agencies | $ | 176,458 | | | $ | — | | | $ | 19,663 | | | $ | 156,795 | |

| Collateralized mortgage obligations | 45,189 | | | — | | | 4,105 | | | 41,084 | |

| Residential mortgage-backed securities | 178,441 | | | 19 | | | 19,630 | | | 158,830 | |

| Commercial mortgage-backed securities | 69,498 | | | 344 | | | 4,552 | | | 65,290 | |

| | | | | | | |

| Corporate bonds | 32,326 | | | 202 | | | 2,834 | | | 29,694 | |

| | $ | 501,912 | | | $ | 565 | | | $ | 50,784 | | | $ | 451,693 | |

| | | | | | | |

| Held to Maturity | | | | | | | |

| | | | | | | |

| State and municipal | $ | 62,133 | | | $ | — | | | $ | 5,419 | | | $ | 56,714 | |

| Residential mortgage-backed securities | 2,467 | | | — | | | 124 | | | 2,343 | |

| $ | 64,600 | | | $ | — | | | $ | 5,543 | | | $ | 59,057 | |

The following table shows the Corporation’s investments’ gross unrealized losses and fair value, aggregated by investment category and length of time that individual securities have been in a continuous unrealized loss position, at March 31, 2024, and December 31, 2023:

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Less than 12 Months | | 12 Months or More | | Total |

| (In thousands) | Fair

Value | | Unrealized

Losses | | Fair

Value | | Unrealized

Losses | | Fair

Value | | Unrealized

Losses |

| March 31, 2024 | | | | | | | | | | | |

| Available for Sale | | | | | | | | | | | |

| U.S. Government and agencies | $ | — | | | $ | — | | | $ | 155,821 | | | $ | 20,228 | | | $ | 155,821 | | | $ | 20,228 | |

| Collateralized mortgage obligations | — | | | — | | | 39,506 | | | 4,386 | | | 39,506 | | | 4,386 | |

| Residential mortgage-backed securities | 2,737 | | | 6 | | | 149,843 | | | 21,334 | | | 152,580 | | | 21,340 | |

| Commercial mortgage-backed securities | 26,850 | | | 92 | | | 29,847 | | | 4,393 | | | 56,697 | | | 4,485 | |

| | | | | | | | | | | |

| Corporate bonds | — | | | — | | | 15,553 | | | 2,556 | | | 15,553 | | | 2,556 | |

| $ | 29,587 | | | $ | 98 | | | $ | 390,570 | | | $ | 52,897 | | | $ | 420,157 | | | $ | 52,995 | |

| | | | | | | | | | | |

| Held to Maturity | | | | | | | | | | | |

| State and municipal | $ | — | | | $ | — | | | $ | 55,923 | | | $ | 6,387 | | | $ | 55,923 | | | $ | 6,387 | |

| Residential mortgage-backed securities | — | | | — | | | 2,161 | | | 123 | | | 2,161 | | | 123 | |

| $ | — | | | $ | — | | | $ | 58,084 | | | $ | 6,510 | | | $ | 58,084 | | | $ | 6,510 | |

| | | | | | | | | | | |

| December 31, 2023 | | | | | | | | | | | |

| Available for Sale | | | | | | | | | | | |

| U.S. Government and agencies | $ | — | | | $ | — | | | $ | 156,795 | | | $ | 19,663 | | | $ | 156,795 | | | $ | 19,663 | |

| Collateralized mortgage obligations | — | | | — | | | 41,085 | | | 4,104 | | | 41,085 | | | 4,104 | |

| Residential mortgage-backed securities | — | | | — | | | 156,295 | | | 19,630 | | | 156,295 | | | 19,630 | |

| Commercial mortgage-backed securities | — | | | — | | | 33,063 | | | 4,553 | | | 33,063 | | | 4,553 | |

| | | | | | | | | | | |

| Corporate bonds | — | | | — | | | 15,279 | | | 2,834 | | | 15,279 | | | 2,834 | |

| | $ | — | | | $ | — | | | $ | 402,517 | | | $ | 50,784 | | | $ | 402,517 | | | $ | 50,784 | |

| | | | | | | | | | | |

| Held to Maturity | | | | | | | | | | | |

| | | | | | | | | | | |

| State and municipal | $ | — | | | $ | — | | | $ | 56,713 | | | $ | 5,419 | | | $ | 56,713 | | | $ | 5,419 | |

| Residential mortgage-backed securities | — | | | — | | | 2,344 | | | 124 | | | 2,344 | | | 124 | |

| $ | — | | | $ | — | | | $ | 59,057 | | | $ | 5,543 | | | $ | 59,057 | | | $ | 5,543 | |

All mortgage-backed security investments are government sponsored enterprise pass-through instruments issued by the Federal National Mortgage Association or Federal Home Loan Mortgage Corporation or they are issued by Government National Mortgage Association which is backed by the U.S. government.

The Company evaluates AFS debt securities for impairment in unrealized loss positions at each measurement date to determine whether the decline in the fair value below the amortized cost basis is due to credit-related factors or noncredit-related factors. The Company evaluates HTM debt securities for expected credit losses at each measurement date to determine if an ACL is required. In estimating credit events management considers whether it intends to sell the security, or if it is more likely than not that it will be required to sell the security before anticipated recovery, or if it does not expect to recover the entire amortized cost basis. The Corporation does not have an ACL for HTM investment securities as of March 31, 2024 and December 31, 2023.

Amortized cost and fair value at March 31, 2024, by contractual maturity, where applicable, are shown below. Expected maturities will differ from contractual maturities because issuers may have the right to call or prepay with or without penalties. Securities not due at a single maturity date are shown separately.

| | | | | | | | | | | | | | | | | | | | | | | |

| | Available for Sale | | Held to Maturity |

| (In thousands) | Amortized

Cost | | Fair

Value | | Amortized

Cost | | Fair

Value |

| 1 year or less | $ | 15,609 | | | $ | 15,265 | | | $ | — | | | $ | — | |

| Over 1 year through 5 years | 117,054 | | | 105,401 | | | 1,960 | | | 1,732 | |

| Over 5 years through 10 years | 59,495 | | | 49,245 | | | 23,643 | | | 23,572 | |

| Over 10 years | 2,000 | | | 1,463 | | | 36,707 | | | 30,619 | |

| Mortgage-backed securities | 283,948 | | | 253,740 | | | 2,284 | | | 2,161 | |

| | $ | 478,106 | | | $ | 425,114 | | | $ | 64,594 | | | $ | 58,084 | |

The proceeds from sales and calls of securities and the associated gains and losses are listed below:

| | | | | | | | | | | | | | | |

| Three Months Ended March 31, | | |

| (In thousands) | 2024 | | 2023 | | | | |

| Proceeds | $ | 23,561 | | | $ | 57,524 | | | | | |

| Gross gains | 87 | | | 228 | | | | | |

| Gross losses | 18 | | | 421 | | | | | |

At March 31, 2024, and December 31, 2023, securities with a carrying value of $186.1 million and $233.7 million, respectively, were pledged as collateral as required by law on public and trust deposits, repurchase agreements, and for other purposes.

Note 4 - Loans and Allowance for Credit Losses

The following table presents the composition of the loan portfolio:

| | | | | | | | | | | |

| (In thousands) | March 31, 2024 | | December 31, 2023 |

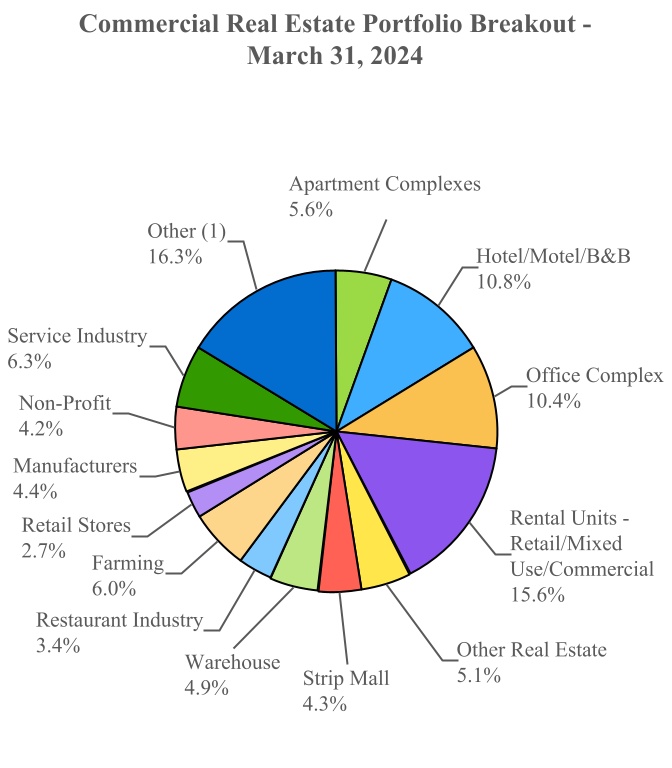

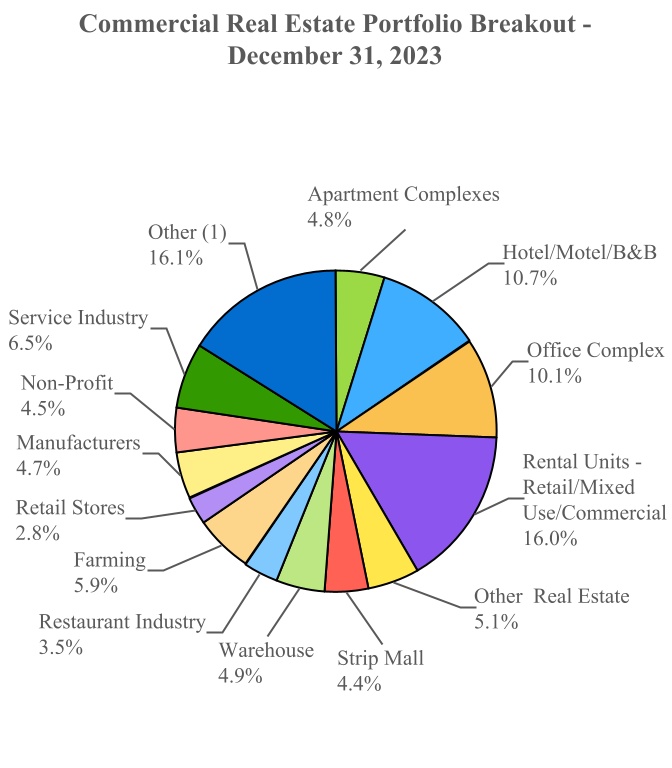

| Commercial real estate | $ | 930,109 | | | $ | 898,709 | |

| Residential mortgage | 391,864 | | | 394,189 | |

| Commercial and industrial | 157,085 | | | 152,344 | |

| Home equity lines of credit | 87,475 | | | 90,163 | |

| Real estate construction | 90,331 | | | 84,341 | |

| Consumer | 9,789 | | | 9,954 | |

| Gross loans | 1,666,653 | | | 1,629,700 | |

| Unearned income | (1,673) | | | (1,712) | |

| Total loans, net of unearned income | $ | 1,664,980 | | | $ | 1,627,988 | |

One of the factors used to monitor the performance and credit quality of the loan portfolio is to analyze the age of the loans receivable as determined by the length of time a recorded payment is past due. The following tables present the classes of the loan portfolio summarized by the past due status:

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| (In thousands) | | 30–59 Days Past Due | | 60–89 Days

Past Due | | ≥ 90 Days

Past Due | | Total Past

Due | | Current | | Total Loans

Receivable | | Loans

Receivable

≥ 90 Days

and

Accruing |

| March 31, 2024 | | | | | | | | | | | | | | |

| Commercial real estate | | $ | 1,927 | | | $ | — | | | $ | 347 | | | $ | 2,274 | | | $ | 927,835 | | | $ | 930,109 | | | $ | 32 | |

| Residential mortgage | | 1,704 | | | — | | | 711 | | | 2,415 | | | 389,449 | | | 391,864 | | | 535 | |

| Commercial and industrial | | 52 | | | — | | | 158 | | | 210 | | | 156,875 | | | 157,085 | | | — | |

| Home equity lines of credit | | 257 | | | 23 | | | 652 | | | 932 | | | 86,543 | | | 87,475 | | | 652 | |

| Real estate construction | | 97 | | | 12 | | | — | | | 109 | | | 90,222 | | | 90,331 | | | — | |

| Consumer | | — | | | — | | | — | | | — | | | 9,789 | | | 9,789 | | | — | |

| Gross Loans | | $ | 4,037 | | | $ | 35 | | | $ | 1,868 | | | $ | 5,940 | | | $ | 1,660,713 | | | $ | 1,666,653 | | | $ | 1,219 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| (In thousands) | | 30–59 Days Past Due | | 60–89 Days

Past Due | | ≥ 90 Days

Past Due | | Total Past

Due | | Current | | Total Loans

Receivable | | Loans

Receivable

≥ 90 Days

and

Accruing |

| December 31, 2023 | | | | | | | | | | | | | | |

| Commercial real estate | | $ | 150 | | | $ | 347 | | | $ | — | | | $ | 497 | | | $ | 898,212 | | | $ | 898,709 | | | $ | — | |

| Residential mortgage | | 1,293 | | | 388 | | | 849 | | | 2,530 | | | 391,659 | | | 394,189 | | | 505 | |

| Commercial and industrial | | 50 | | | — | | | 159 | | | 209 | | | 152,135 | | | 152,344 | | | — | |

| Home equity lines of credit | | 414 | | | — | | | 654 | | | 1,068 | | | 89,095 | | | 90,163 | | | 654 | |

| Real estate construction | | 12 | | | — | | | — | | | 12 | | | 84,329 | | | 84,341 | | | — | |

| Consumer | | 8 | | | — | | | 3 | | | 11 | | | 9,943 | | | 9,954 | | | 3 | |

| Gross Loans | | $ | 1,927 | | | $ | 735 | | | $ | 1,665 | | | $ | 4,327 | | | $ | 1,625,373 | | | $ | 1,629,700 | | | $ | 1,162 | |

Nonaccrual and Nonperforming Loans

Loans individually evaluated consist of nonaccrual loans, presented in the following table:

| | | | | | | | | | | | | | | | | |

| (In thousands) | With a Related Allowance | | Without a Related Allowance | | Total |

| March 31, 2024 | | | | | |

| Commercial real estate | $ | 315 | | | $ | 1,107 | | | $ | 1,422 | |

| Residential mortgage | — | | | 176 | | | 176 | |

| Commercial and industrial | 937 | | | — | | | 937 | |

| Home equity lines of credit | — | | | 181 | | | 181 | |

| | | | | |

| | $ | 1,252 | | | $ | 1,464 | | | $ | 2,716 | |

| December 31, 2023 | | | | | |

| Commercial real estate | $ | 315 | | | $ | 1,164 | | | $ | 1,479 | |

| Residential mortgage | — | | | 343 | | | 343 | |

| Commercial and industrial | 1,004 | | | — | | | 1,004 | |

| Home equity lines of credit | — | | | 185 | | | 185 | |

| | | | | |

| $ | 1,319 | | | $ | 1,692 | | | $ | 3,011 | |

During the three months ended March 31, 2024, no material amount of interest income was recognized on nonaccrual loans subsequent to their classification as nonaccrual.

Total nonperforming loans are as follows:

| | | | | | | | | | | | | | |

| (In thousands) | | March 31, 2024 | | December 31, 2023 |

| Nonaccrual loans | | $ | 2,716 | | | $ | 3,011 | |

| Greater than or equal to 90 days past due and still accruing | | 1,219 | | | 1,162 | |

| Total nonperforming loans | | $ | 3,935 | | | $ | 4,173 | |

Collateral-Dependent Loans

A loan is considered to be collateral-dependent when the debtor is experiencing financial difficulty and repayment is expected to be provided substantially through the sale or operation of the collateral. For all classes of loans deemed collateral-dependent, the Corporation elected the practical expedient to estimate expected credit losses based on the collateral’s fair value less cost to sell. In most cases, the Corporation records a partial charge-off to reduce the collateral-dependent loan’s carrying value to the collateral’s fair value less cost to sell. Substantially all of the collateral supporting collateral-dependent loans consists of various types of real estate, including residential properties, commercial properties, such as retail centers, office buildings, and lodging, agriculture land, and vacant land.

Changes in the fair value of the collateral for individually evaluated loans are reported as provision for credit losses or a reversal of provision for credit losses in the period of change. The following table presents the amortized cost basis of individually evaluated loans as of the periods presented:

| | | | | | | | | | | | | | |

| | Type of Collateral |

| (In thousands) | | Business Assets | | Real Estate |

| March 31, 2024 | | | | |

| Commercial real estate | | $ | — | | | $ | 1,422 | |

| Residential mortgage | | — | | | 176 | |

| Commercial and industrial | | 937 | | | — | |

| Home equity lines of credit | | — | | | 181 | |

| | | | |

| | | | |

| Total | | $ | 937 | | | $ | 1,779 | |

| | | | |

| December 31, 2023 | | | | |

| Commercial real estate | | $ | — | | | $ | 1,479 | |

| Residential mortgage | | — | | | 343 | |

| Commercial and industrial | | 1,004 | | | — | |

| Home equity lines of credit | | — | | | 185 | |

| | | | |

| | | | |

| Total | | $ | 1,004 | | | $ | 2,007 | |

Consumer residential mortgages and home equity lines of credit which are well secured by residential real estate properties and are in the process of collection are not considered nonaccrual, however, formal foreclosure proceedings are in process. These loans totaled $1.3 million at both March 31, 2024 and December 31, 2023 and are included in nonperforming loans if they are greater than or equal to 90 days past due.

Loan Modifications

The Corporation evaluates all loan restructurings according to the accounting guidance for loan modifications to determine if the restructuring results in a new loan or a continuation of the existing loan. Loan modifications to borrowers experiencing financial difficulty that result in a direct change in the timing or amount of contractual cash flows include situations where there is principal forgiveness, interest rate reductions, other-than-insignificant payment delays, term extensions, and combinations of the above. Therefore, the disclosures related to loan restructurings are only for modifications that directly affect cash flows.

During both the three months ended March 31, 2024 and 2023, the Corporation did not modify any loans nor were there any commitments to lend any additional funds on existing modified loans.

The following presents the performance of loans modified in the previous twelve months as of March 31, 2024:

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| (In thousands) | | Current | | | | 30-89 Days Past Due | | ≥ 90 Days

Past Due | | Total Past Due |

| Commercial and industrial | | $ | 292 | | | | | $ | — | | | $ | — | | | $ | — | |

As of March 31, 2024, the Corporation had no loans that defaulted during the period that had been modified preceding the payment default when the borrower was experiencing financial difficulty at the time of modification. For purposes of this disclosure, a default occurs when, within 12 months of the original modification, either a full or partial charge-off occurs or the loan becomes 90 days or more past due.

Allowance for Credit Losses

The Corporation maintains an ACL at a level determined to be adequate to absorb expected credit losses associated with the Corporation’s financial instruments over the life of those instruments as of the balance sheet date. The ACL consists of loans evaluated collectively and individually for expected credit losses. The Corporation considers the performance of the loan portfolio and its impact on the ACL and does not assign internal risk ratings to smaller balance, homogeneous loans such as certain residential mortgage, home equity lines of credit, construction loans to individuals secured by residential real estate and consumer loans. For these loans, the Corporation evaluates credit quality based on the aging status of the loan and designates as performing and nonperforming.

The following summarizes designated internal risk categories by portfolio segment for loans assigned a risk rating and those evaluated based on the performance status:

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | March 31, 2024 |

| | Term Loans Amortized Cost Basis by Origination Year | | Revolving Loans Amortized Cost Basis | | |

| (In thousands) | | 2024 | | 2023 | | 2022 | | 2021 | | 2020 | | Prior | | | Total |

| Internally Risk Rated: | | | | | | | | | | | | | | | | |

| Commercial real estate | | | | | | | | | | | | | | | | |

| Pass | | $ | 45,462 | | | $ | 135,864 | | | $ | 154,328 | | | $ | 129,033 | | | $ | 58,625 | | | $ | 343,722 | | | $ | 13,858 | | | $ | 880,892 | |

| Special Mention | | — | | | 1,960 | | | 5,082 | | | 6,422 | | | 2,220 | | | 23,578 | | | 1,530 | | | 40,792 | |

| Substandard | | — | | | — | | | — | | | — | | | 1,518 | | | 6,907 | | | — | | | 8,425 | |

| Total Commercial real estate | | $ | 45,462 | | | $ | 137,824 | | | $ | 159,410 | | | $ | 135,455 | | | $ | 62,363 | | | $ | 374,207 | | | $ | 15,388 | | | $ | 930,109 | |

| | | | | | | | | | | | | | | | |

| Residential mortgage | | | | | | | | | | | | | | | | |

| Pass | | $ | 4,161 | | | $ | 39,225 | | | $ | 25,230 | | | $ | 40,049 | | | $ | 14,573 | | | $ | 35,849 | | | $ | 339 | | | $ | 159,426 | |

| Special Mention | | — | | | 584 | | | 82 | | | 587 | | | 389 | | | 3,211 | | | 78 | | | 4,931 | |

| Substandard | | — | | | — | | | — | | | — | | | — | | | 245 | | | — | | | 245 | |

| Total Residential Mortgage | | $ | 4,161 | | | $ | 39,809 | | | $ | 25,312 | | | $ | 40,636 | | | $ | 14,962 | | | $ | 39,305 | | | $ | 417 | | | $ | 164,602 | |

| | | | | | | | | | | | | | | | |

| Commercial and industrial | | | | | | | | | | | | | | | | |

| Pass | | $ | 2,286 | | | $ | 11,844 | | | $ | 23,167 | | | $ | 33,374 | | | $ | 15,172 | | | $ | 30,579 | | | $ | 31,721 | | | $ | 148,143 | |

| Special Mention | | 37 | | | 167 | | | 297 | | | 268 | | | 480 | | | 547 | | | 1,812 | | | 3,608 | |

| Substandard | | — | | | 432 | | | 109 | | | 472 | | | 16 | | | 1,463 | | | 2,842 | | | 5,334 | |

| Total Commercial and industrial | | $ | 2,323 | | | $ | 12,443 | | | $ | 23,573 | | | $ | 34,114 | | | $ | 15,668 | | | $ | 32,589 | | | $ | 36,375 | | | $ | 157,085 | |

| | | | | | | | | | | | | | | | |

| Home equity lines of credit | | | | | | | | | | | | | | | | |

| Pass | | $ | — | | | $ | 299 | | | $ | 97 | | | $ | — | | | $ | — | | | $ | 128 | | | $ | 5,832 | | | $ | 6,356 | |

| Special Mention | | — | | | — | | | — | | | — | | | — | | | — | | | 742 | | | 742 | |

| Substandard | | — | | | — | | | — | | | — | | | — | | | 355 | | | — | | | 355 | |

| Total Home equity lines of credit | | $ | — | | | $ | 299 | | | $ | 97 | | | $ | — | | | $ | — | | | $ | 483 | | | $ | 6,574 | | | $ | 7,453 | |

| | | | | | | | | | | | | | | | |

| Real estate construction | | | | | | | | | | | | | | | | |

| Pass | | $ | 1,310 | | | $ | 25,096 | | | $ | 43,661 | | | $ | 2,353 | | | $ | 329 | | | $ | 1,155 | | | $ | 6,103 | | | $ | 80,007 | |

| Special Mention | | — | | | — | | | 459 | | | — | | | — | | | 706 | | | — | | | 1,165 | |

| Substandard | | — | | | — | | | — | | | — | | | — | | | 67 | | | — | | | 67 | |

| Total Real estate construction | | $ | 1,310 | | | $ | 25,096 | | | $ | 44,120 | | | $ | 2,353 | | | $ | 329 | | | $ | 1,928 | | | $ | 6,103 | | | $ | 81,239 | |

| | | | | | | | | | | | | | | | |

| Performance Rated: | | | | | | | | | | | | | | | | |

| Residential mortgage | | | | | | | | | | | | | | | | |

| Performing | | $ | 2,376 | | | $ | 36,651 | | | $ | 44,113 | | | $ | 14,262 | | | $ | 15,728 | | | $ | 113,526 | | | $ | 71 | | | $ | 226,727 | |

| Nonperforming | | — | | | — | | | — | | | — | | | — | | | 535 | | | — | | | 535 | |

| Total Residential Mortgage | | $ | 2,376 | | | $ | 36,651 | | | $ | 44,113 | | | $ | 14,262 | | | $ | 15,728 | | | $ | 114,061 | | | $ | 71 | | | $ | 227,262 | |

| Home equity lines of credit | | | | | | | | | | | | | | | | |

| Performing | | $ | — | | | $ | 22 | | | $ | 37 | | | $ | — | | | $ | 13 | | | $ | 3,746 | | | $ | 75,552 | | | $ | 79,370 | |

| Nonperforming | | — | | | — | | | — | | | — | | | — | | | 1 | | | 651 | | | 652 | |

| Total Home equity lines of credit | | $ | — | | | $ | 22 | | | $ | 37 | | | $ | — | | | $ | 13 | | | $ | 3,747 | | | $ | 76,203 | | | $ | 80,022 | |

| Consumer | | | | | | | | | | | | | | | | |

| Performing | | $ | 512 | | | $ | 2,085 | | | $ | 2,471 | | | $ | 677 | | | $ | 460 | | | $ | 1,180 | | | $ | 2,404 | | | $ | 9,789 | |

| | | | | | | | | | | | | | | | |

| Total Consumer | | $ | 512 | | | $ | 2,085 | | | $ | 2,471 | | | $ | 677 | | | $ | 460 | | | $ | 1,180 | | | $ | 2,404 | | | $ | 9,789 | |

| Year-to-date gross charge-offs | | $ | — | | | $ | — | | | $ | 5 | | | $ | — | | | $ | — | | | $ | — | | | $ | 55 | | | $ | 60 | |

| Real estate construction | | | | | | | | | | | | | | | | |

| Performing | | $ | 1,561 | | | $ | 5,400 | | | $ | 748 | | | $ | 172 | | | $ | 204 | | | $ | 1,005 | | | $ | 2 | | | $ | 9,092 | |

| | | | | | | | | | | | | | | | |

| Total Real estate construction | | $ | 1,561 | | | $ | 5,400 | | | $ | 748 | | | $ | 172 | | | $ | 204 | | | $ | 1,005 | | | $ | 2 | | | $ | 9,092 | |

| Total Portfolio loans: | | | | | | | | | | | | | | | | |

| Pass | | $ | 53,219 | | | $ | 212,328 | | | $ | 246,483 | | | $ | 204,809 | | | $ | 88,699 | | | $ | 411,433 | | | $ | 57,853 | | | $ | 1,274,824 | |

| Special Mention | | 37 | | | 2,711 | | | 5,920 | | | 7,277 | | | 3,089 | | | 28,042 | | | 4,162 | | | 51,238 | |

| Substandard | | — | | | 432 | | | 109 | | | 472 | | | 1,534 | | | 9,037 | | | 2,842 | | | 14,426 | |

| Performing | | 4,449 | | | 44,158 | | | 47,369 | | | 15,111 | | | 16,405 | | | 119,457 | | | 78,029 | | | 324,978 | |

| Nonperforming | | — | | | — | | | — | | | — | | | — | | | 536 | | | 651 | | | 1,187 | |

| Total Portfolio loans | | $ | 57,705 | | | $ | 259,629 | | | $ | 299,881 | | | $ | 227,669 | | | $ | 109,727 | | | $ | 568,505 | | | $ | 143,537 | | | $ | 1,666,653 | |

| Year-to-date gross charge-offs | | $ | — | | | $ | — | | | $ | 5 | | | $ | — | | | $ | — | | | $ | — | | | $ | 55 | | | $ | 60 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | December 31, 2023 |

| | Term Loans Amortized Cost Basis by Origination Year | | Revolving Loans Amortized Cost Basis | | |

| (In thousands) | | 2023 | | 2022 | | 2021 | | 2020 | | 2019 | | Prior | | | Total |

| Internally Risk Rated: | | | | | | | | | | | | | | | | |

| Commercial real estate | | | | | | | | | | | | | | | | |

| Pass | | $ | 136,158 | | | $ | 152,767 | | | $ | 130,994 | | | $ | 60,918 | | | $ | 65,856 | | | $ | 287,026 | | | $ | 13,636 | | | $ | 847,355 | |

| Special Mention | | 1,927 | | | 6,385 | | | 5,920 | | | 1,904 | | | 8,222 | | | 16,244 | | | 1,994 | | | 42,596 | |

| Substandard | | — | | | — | | | — | | | 1,530 | | | 704 | | | 6,524 | | | — | | | 8,758 | |

| Total Commercial real estate | | $ | 138,085 | | | $ | 159,152 | | | $ | 136,914 | | | $ | 64,352 | | | $ | 74,782 | | | $ | 309,794 | | | $ | 15,630 | | | $ | 898,709 | |

| | | | | | | | | | | | | | | | |

| Residential mortgage | | | | | | | | | | | | | | | | |

| Pass | | $ | 39,146 | | | $ | 27,612 | | | $ | 41,031 | | | $ | 14,758 | | | $ | 10,492 | | | $ | 27,274 | | | $ | 402 | | | $ | 160,715 | |

| Special Mention | | 588 | | | 82 | | | 593 | | | 397 | | | 826 | | | 2,457 | | | 62 | | | 5,005 | |

| Substandard | | — | | | — | | | — | | | — | | | — | | | 218 | | | — | | | 218 | |

| Total Residential Mortgage | | $ | 39,734 | | | $ | 27,694 | | | $ | 41,624 | | | $ | 15,155 | | | $ | 11,318 | | | $ | 29,949 | | | $ | 464 | | | $ | 165,938 | |

| | | | | | | | | | | | | | | | |

| Commercial and industrial | | | | | | | | | | | | | | | | |

| Pass | | $ | 12,319 | | | $ | 24,259 | | | $ | 34,830 | | | $ | 15,614 | | | $ | 13,922 | | | $ | 17,780 | | | $ | 25,147 | | | $ | 143,871 | |

| Special Mention | | 128 | | | 303 | | | 290 | | | 529 | | | 140 | | | 459 | | | 2,014 | | | 3,863 | |

| Substandard | | 7 | | | 135 | | | 499 | | | 91 | | | 9 | | | 1,597 | | | 2,272 | | | 4,610 | |

| Total Commercial and industrial | | $ | 12,454 | | | $ | 24,697 | | | $ | 35,619 | | | $ | 16,234 | | | $ | 14,071 | | | $ | 19,836 | | | $ | 29,433 | | | $ | 152,344 | |

| Year-to-date gross charge-offs | | $ | — | | | $ | — | | | $ | — | | | $ | — | | | $ | — | | | $ | 110 | | | $ | — | | | $ | 110 | |

| Home equity lines of credit | | | | | | | | | | | | | | | | |

| Pass | | $ | 300 | | | $ | 99 | | | $ | — | | | $ | — | | | $ | — | | | $ | 131 | | | $ | 5,235 | | | $ | 5,765 | |

| Special Mention | | — | | | — | | | — | | | — | | | — | | | — | | | 727 | | | 727 | |

| Substandard | | — | | | — | | | — | | | — | | | — | | | 362 | | | — | | | 362 | |

| Total Home equity lines of credit | | $ | 300 | | | $ | 99 | | | $ | — | | | $ | — | | | $ | — | | | $ | 493 | | | $ | 5,962 | | | $ | 6,854 | |

| | | | | | | | | | | | | | | | |

| Real estate construction | | | | | | | | | | | | | | | | |

| Pass | | $ | 19,766 | | | $ | 39,758 | | | $ | 3,953 | | | $ | 1,160 | | | $ | — | | | $ | 2,604 | | | $ | 8,003 | | | $ | 75,244 | |

| Special Mention | | — | | | 465 | | | — | | | 92 | | | — | | | 725 | | | — | | | 1,282 | |

| Substandard | | — | | | — | | | — | | | — | | | — | | | 69 | | | — | | | 69 | |

| Total Real estate construction | | $ | 19,766 | | | $ | 40,223 | | | $ | 3,953 | | | $ | 1,252 | | | $ | — | | | $ | 3,398 | | | $ | 8,003 | | | $ | 76,595 | |

| | | | | | | | | | | | | | | | |

| Performance Rated: | | | | | | | | | | | | | | | | |

| Residential mortgage | | | | | | | | | | | | | | | | |

| Performing | | $ | 33,884 | | | $ | 45,221 | | | $ | 14,878 | | | $ | 16,184 | | | $ | 9,059 | | | $ | 108,021 | | | $ | 156 | | | $ | 227,403 | |

| Nonperforming | | — | | | — | | | — | | | — | | | — | | | 848 | | | — | | | 848 | |

| Total Residential Mortgage | | $ | 33,884 | | | $ | 45,221 | | | $ | 14,878 | | | $ | 16,184 | | | $ | 9,059 | | | $ | 108,869 | | | $ | 156 | | | $ | 228,251 | |

| Home equity lines of credit | | | | | | | | | | | | | | | | |

| Performing | | $ | 23 | | | $ | 38 | | | $ | — | | | $ | 13 | | | $ | 94 | | | $ | 4,742 | | | $ | 77,745 | | | $ | 82,655 | |

| Nonperforming | | — | | | — | | | — | | | — | | | — | | | 92 | | | 562 | | | 654 | |

| Total Home equity lines of credit | | $ | 23 | | | $ | 38 | | | $ | — | | | $ | 13 | | | $ | 94 | | | $ | 4,834 | | | $ | 78,307 | | | $ | 83,309 | |

| Consumer | | | | | | | | | | | | | | | | |

| Performing | | $ | 2,351 | | | $ | 2,685 | | | $ | 778 | | | $ | 522 | | | $ | 271 | | | $ | 1,085 | | | $ | 2,259 | | | $ | 9,951 | |

| Nonperforming | | — | | | — | | | — | | | — | | | — | | | — | | | 3 | | | 3 | |

| Total Consumer | | $ | 2,351 | | | $ | 2,685 | | | $ | 778 | | | $ | 522 | | | $ | 271 | | | $ | 1,085 | | | $ | 2,262 | | | $ | 9,954 | |

| Year-to-date gross charge-offs | | $ | 48 | | | $ | 83 | | | $ | 42 | | | $ | 55 | | | $ | 23 | | | $ | 78 | | | $ | 67 | | | $ | 396 | |

| Real estate construction | | | | | | | | | | | | | | | | |

| Performing | | $ | 5,571 | | | $ | 753 | | | $ | 175 | | | $ | 210 | | | $ | 170 | | | $ | 867 | | | $ | — | | | $ | 7,746 | |

| | | | | | | | | | | | | | | | |

| Total Real estate construction | | $ | 5,571 | | | $ | 753 | | | $ | 175 | | | $ | 210 | | | $ | 170 | | | $ | 867 | | | $ | — | | | $ | 7,746 | |

| Total Portfolio loans | | | | | | | | | | | | | | | | |

| Pass | | $ | 207,689 | | | $ | 244,495 | | | $ | 210,808 | | | $ | 92,450 | | | $ | 90,270 | | | $ | 334,815 | | | $ | 52,423 | | | $ | 1,232,950 | |

| Special Mention | | 2,643 | | | 7,235 | | | 6,803 | | | 2,922 | | | 9,188 | | | 19,885 | | | 4,797 | | | 53,473 | |

| Substandard | | 7 | | | 135 | | | 499 | | | 1,621 | | | 713 | | | 8,770 | | | 2,272 | | | 14,017 | |

| Performing | | 41,829 | | | 48,697 | | | 15,831 | | | 16,929 | | | 9,594 | | | 114,715 | | | 80,160 | | | 327,755 | |

| Nonperforming | | — | | | — | | | — | | | — | | | — | | | 940 | | | 565 | | | 1,505 | |

| Total Portfolio loans | | $ | 252,168 | | | $ | 300,562 | | | $ | 233,941 | | | $ | 113,922 | | | $ | 109,765 | | | $ | 479,125 | | | $ | 140,217 | | | $ | 1,629,700 | |

| Year-to-date gross charge-offs | | $ | 48 | | | $ | 83 | | | $ | 42 | | | $ | 55 | | | $ | 23 | | | $ | 188 | | | $ | 67 | | | $ | 506 | |

The following table presents the activity in the ACL by loan portfolio segment:

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| (In thousands) | Commercial

Real Estate | | Residential

Mortgage | | Commercial

and

Industrial | | Home Equity

Lines of

Credit | | Real Estate

Construction | | Consumer | | Unallocated | | Total |

| Three Months Ended March 31, 2024 | | | | | | | | | | | | |

| Beginning balance - January 1, 2024 | $ | 12,010 | | | $ | 3,303 | | | $ | 2,048 | | | $ | 397 | | | $ | 2,070 | | | $ | 141 | | | $ | — | | | $ | 19,969 | |

| Charge-offs | — | | | — | | | — | | | — | | | — | | | (60) | | | — | | | (60) | |

| Recoveries | — | | | — | | | 15 | | | — | | | — | | | 25 | | | — | | | 40 | |

| Provisions (credits) | 230 | | | (76) | | | (103) | | | (83) | | | 243 | | | 12 | | | — | | | 223 | |

| Ending balance - March 31, 2024 | $ | 12,240 | | | $ | 3,227 | | | $ | 1,960 | | | $ | 314 | | | $ | 2,313 | | | $ | 118 | | | $ | — | | | $ | 20,172 | |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| Three Months Ended March 31, 2023 | | | | | | | | | | | | |

| Beginning balance - January 1, 2023 | $ | 10,016 | | | $ | 3,029 | | | $ | 2,848 | | | $ | 347 | | | $ | 1,000 | | | $ | 376 | | | $ | 245 | | | $ | 17,861 | |

| Impact of CECL adoption | 1,106 | | | 297 | | | (762) | | | 17 | | | 1,347 | | | (142) | | | (245) | | | 1,618 | |

| Charge-offs | — | | | — | | | (29) | | | — | | | — | | | (88) | | | — | | | (117) | |

| Recoveries | — | | | — | | | 1 | | | — | | | — | | | 25 | | | — | | | 26 | |

| Provisions | (90) | | | 40 | | | 47 | | | 15 | | | 118 | | | (33) | | | — | | | 97 | |

| Ending balance - March 31, 2023 | $ | 11,032 | | | $ | 3,366 | | | $ | 2,105 | | | $ | 379 | | | $ | 2,465 | | | $ | 138 | | | $ | — | | | $ | 19,485 | |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

Note 5 - Deposits

Deposits were comprised of the following for the periods presented:

| | | | | | | | | | | |

| (In thousands) | March 31, 2024 | | December 31, 2023 |

| Noninterest-bearing demand deposits | $ | 499,583 | | | $ | 500,332 | |

| Interest-bearing demand deposits | 493,783 | | | 524,289 | |

| Money market | 252,363 | | | 264,907 | |

| Savings | 332,213 | | | 340,134 | |

| Total demand and savings | 1,577,942 | | | 1,629,662 | |

| Time | 257,282 | | | 232,151 | |

| Total deposits | $ | 1,835,224 | | | $ | 1,861,813 | |

Scheduled maturities of time certificates of deposit at March 31, 2024 are as follows:

| | | | | | | | | | | |

| Time Deposits |

| Year | Less than $250,000 | | $250,000 or more |

| Less than 1 year | $ | 176,531 | | | $ | 46,675 | |

| 1 through 2 years | 20,264 | | | 1,495 | |

| 2 through 3 years | 6,231 | | | 254 | |

| 3 through 4 years | 3,946 | | | — | |

| 4 through 5 years | 1,874 | | | — | |

| Thereafter | 12 | | | — | |

| Total time deposits | $ | 208,858 | | | $ | 48,424 | |

Note 6 - Borrowings

Short-term borrowings were comprised of the following for the periods presented:

| | | | | | | | | | | |

| (In thousands) | March 31, 2024 | | December 31, 2023 |

| | | |

| Securities sold under repurchase agreements | $ | 17,303 | | | $ | 26,882 | |

| FHLB advance | — | | | 30,000 | |

| $ | 17,303 | | | $ | 56,882 | |

Borrowings with original maturities of one year or less are classified as short-term. Securities sold under repurchase agreements are comprised of customer repurchase agreements, which are sweep accounts with next-day maturities utilized by larger commercial customers to earn interest on their funds. Securities are pledged to these customers in an amount at least equal to the outstanding balance. Under an agreement with the FHLB, the Bank has short-term borrowing capacity included within its maximum borrowing capacity. All FHLB advances are collateralized by a security agreement covering qualifying loans. In addition, all FHLB advances are secured by the FHLB capital stock owned by the Bank having a par value of $10.6 million at March 31, 2024. The Bank also has lines of credit that total $192.0 million with correspondent banks for overnight federal funds borrowings. There were no advances on these lines at March 31, 2024 and December 31, 2023.

Long-term borrowings were comprised of the following for the periods presented:

| | | | | | | | | | | |

| (In thousands) | March 31, 2024 | | December 31, 2023 |

| FHLB fixed-rate advances maturing: | | | |

| 2026 | $ | 80,000 | | | $ | 80,000 | |

| 2027 | 90,000 | | | 60,000 | |

| 2028 | 35,000 | | | 35,000 | |

| 2029 | 30,000 | | | — | |

| | | |

| | | |

| | | |

| Trust preferred subordinated debt | 5,302 | | | 5,292 | |

| Subordinated debt | 15,000 | | | 15,000 | |

| $ | 255,302 | | | $ | 195,292 | |

The long-term FHLB advances have a weighted average rate of 4.52%, and are collateralized by the assets defined in the security agreement and FHLB capital stock described previously. Based on this collateral and ACNB’s holding of FHLB stock, ACNB is eligible to borrow up to $883.2 million, of which $647.1 million was available at March 31, 2024.

The trust preferred subordinated debt is comprised of debt securities issued by FCBI in December 2006 and assumed by ACNB Corporation through the acquisition of FCBI. FCBI completed the private placement of an aggregate of $6.0 million of trust preferred securities. The interest rate on the subordinated debentures is adjusted quarterly to 163 bps over the three-month CME Term SOFR plus applicable tenor spread adjustment. On March 15, 2024, the most recent interest rate reset date, the interest rate was adjusted to 7.22% for the period ending June 16, 2024. The trust preferred securities mature on December 15, 2036, and may be redeemed at par, at the Corporation’s option, on any interest payment date. The trust preferred subordinated debt is considered Tier 1 capital for the consolidated capital ratios.

On March 30, 2021, the Company entered into Purchase Agreements with the Purchasers pursuant to which the Company sold and issued $15.0 million in aggregate principal amount of its 4.00% fixed-to-floating rate subordinated notes due March 31, 2031. The Subordinated Notes bear interest at a fixed rate of 4.00% per year, from and including March 30, 2021 to, but excluding, March 31, 2026 or earlier redemption date. From and including March 31, 2026 to, but excluding the maturity date or earlier redemption date, the interest rate will reset quarterly at a variable rate equal to the then current 90-day average SOFR plus 329 bps. As provided in the Subordinated Notes, the interest rate on the Subordinated Notes during the applicable floating rate period may be determined based on a rate other than the 90-day average SOFR. The Subordinated Notes were issued by the Corporation to the Purchasers at a price equal to 100% of their face amount. The Subordinated Notes have a stated maturity of March 31, 2031, are redeemable by the Company at its option, in whole or in part, on or after March 30, 2026, and at any time upon the occurrences of certain events. The Subordinated Notes are considered Tier 2 capital for the consolidated capital ratios.

Note 7 - Fair Value Measurements

Fair value is the exchange price that would be received to sell the asset or transfer the liability in an orderly transaction (that is, not a forced liquidation or distressed sale) between market participants at the measurement date under current market conditions.

Fair value measurement establishes a fair value hierarchy that prioritizes the inputs to valuation methods used to measure fair value. The hierarchy gives the highest priority to unadjusted quoted prices in active markets for identical assets or liabilities (Level 1 measurements) and the lowest priority to unobservable inputs (Level 3 measurements). The three levels of the fair value hierarchy are as follows:

Level 1 - Unadjusted quoted prices in active markets that are accessible at the measurement date for identical, unrestricted assets or liabilities.

Level 2 - Quoted prices for similar assets or liabilities in markets that are not active, or inputs that are observable, either directly or indirectly, for substantially the full term of the asset or liability.

Level 3 - Prices or valuation techniques that require inputs that are both significant to the fair value measurement and unobservable (i.e., supported with little or no market activity).

An asset or liability’s level within the fair value hierarchy is based on the lowest level of input that is significant to the fair value measurement.

The following tables present assets measured at fair value and the basis of measurement used at the periods presented:

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| March 31, 2024 |

| (In thousands) | Basis | | Level 1 | | Level 2 | | Level 3 | | Total |

| Equity securities with readily determinable fair values | Recurring | | $ | 918 | | | $ | — | | | $ | — | | | $ | 918 | |

| AFS Investment Securities: | | | | | | | | | |

| U.S. Government and agencies | | | — | | | 155,821 | | | — | | | 155,821 | |

| Collateralized mortgage obligations | | | — | | | 39,506 | | | — | | | 39,506 | |

| Residential mortgage-backed securities | | | — | | | 152,580 | | | — | | | 152,580 | |

| Commercial mortgage-backed securities | | | — | | | 61,654 | | | — | | | 61,654 | |

| | | | | | | | | |

| Corporate bonds | | | — | | | 15,553 | | | — | | | 15,553 | |

| | | | | | | | | |

| | | | | | | | | |

| Total AFS Investment Securities | Recurring | | — | | | 425,114 | | | — | | | 425,114 | |

| Loans held for sale | Recurring | | — | | | 88 | | | — | | | 88 | |

| Individually evaluated loans | Non-recurring | | — | | | — | | | 294 | | | 294 | |

| Foreclosed assets held for resale | Non-recurring | | — | | | — | | | 467 | | | 467 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| December 31, 2023 |

| (In thousands) | Basis | | Level 1 | | Level 2 | | Level 3 | | Total |

| Equity securities with readily determinable fair values | Recurring | | $ | 928 | | | $ | — | | | $ | — | | | $ | 928 | |

| AFS Investment Securities: | | | | | | | | | |

| U.S. Government and agencies | | | — | | | 156,795 | | | — | | | 156,795 | |

| Collateralized mortgage obligations | | | — | | | 41,084 | | | — | | | 41,084 | |

| Residential mortgage-backed securities | | | — | | | 158,830 | | | — | | | 158,830 | |

| Commercial mortgage-backed securities | | | — | | | 65,290 | | | — | | | 65,290 | |

| | | | | | | | | |

| Corporate bonds | | | — | | | 29,694 | | | — | | | 29,694 | |

| | | | | | | | | |

| | | | | | | | | |

| Total AFS Investment Securities | Recurring | | — | | | 451,693 | | | — | | | 451,693 | |

| Loans held for sale | Recurring | | — | | | 280 | | | — | | | 280 |

| Individually evaluated loans | Non-recurring | | — | | | — | | | 242 | | | 242 | |

| Foreclosed assets held for resale | Non-recurring | | — | | | — | | | 467 | | | 467 | |

The valuation techniques used to measure fair value for the items in the preceding tables are as follows:

Equity securities - The fair value of equity securities with readily determinable fair values is recorded on the Consolidated Balance Sheet, with realized and unrealized gains and losses reported in other expense on the Consolidated Statements of Income.

Available for sale investment securities – Included in this asset category are debt securities. Level 2 investment securities are valued by a third-party pricing service. The pricing service uses pricing models that vary based on asset class and incorporate available market information, including quoted prices of investment securities with similar characteristics. Because many fixed income securities do not trade on a daily basis, pricing models use available information, as applicable, through processes such as benchmark yield curves, benchmarking of like securities, sector groupings and matrix pricing. Standard market inputs include: benchmark yields, reported trades, broker/dealer quotes, issuer spreads, two-sided markets, benchmark securities, bids, offers and reference data, including market research publications. For certain security types, additional inputs may be used, or some of the standard market inputs may not be applicable.

• U.S. Government and agencies – These debt securities are classified as Level 2. Fair values are determined by a third-party pricing service, as detailed above.

• Mortgage-backed securities – These debt securities are classified as Level 2. Fair values are determined by a third-party pricing service, as detailed above.

• Corporate bonds – This category consists of subordinated and senior debt issued by financial institutions and are classified as Level 2 investments. The fair values for these corporate debt securities are determined by a third-party pricing service, as detailed above.

Loans held for sale – This category includes mortgage loans held for sale that are measured at fair value. Fair values as of March 31, 2024 and December 31, 2023, were measured as the price that secondary market investors were offering for loans with similar characteristics. See “Note 1 - Summary of Significant Accounting Policies” for details related to the Corporation’s election to measure assets and liabilities at fair value.

Individually evaluated loans – This category consists of loans that were individually evaluated for impairment and have a specific reserve. They are classified as Level 3 assets.

Foreclosed assets held for resale – This category consists of foreclosed assets that are held for resale and classified as Level 3 assets, for which the fair values were based on estimated selling prices less estimated selling costs for similar assets in active markets.

The following table presents additional quantitative information about assets measured at fair value on a nonrecurring basis for which the Corporation has utilized Level 3 inputs to determine fair value:

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| (Dollars in thousands) | | Fair Value Estimate | | Valuation Technique(1) | | Unobservable Input(2) | | Range | | Weighted Average |

| March 31, 2024 | | | | | | | | | | |

| Individually evaluated loans | | $ | 294 | | | Appraisal of collateral | | Appraisal adjustments | | (33) – (100)% | | (93)% |

| Foreclosed assets held for resale | | 467 | | | Appraisal of collateral | | Appraisal adjustments | | (56) | | (56) |

| | | | | | | | | | |

| December 31, 2023 | | | | | | | | | | |

| Individually evaluated loans | | $ | 242 | | | Appraisal of collateral | | Appraisal adjustments | | (33) – (100)% | | (94)% |

| Foreclosed assets held for resale | | 467 | | | Appraisal of collateral | | Appraisal adjustments | | (56) | | (56) |

_______________________________

(1) Fair value is generally determined through management’s estimate or independent third-party appraisals of the underlying collateral, which generally includes various Level 3 inputs which are not observable.

(2) Appraisals may be adjusted downward by management for qualitative factors such as economic conditions and estimated liquidation expenses. The range of liquidation expenses and other appraisal adjustments are presented as a percentage of the appraisal. Higher downward adjustments are caused by negative changes to the collateral or conditions in the real estate market, actual offers or sales contracts received, and/or age of the appraisal.

The following information should not be interpreted as an estimate of the fair value of the entire Corporation since a fair value calculation is only provided for a limited portion of the Corporation’s assets and liabilities. Due to a wide range of valuation techniques and the degree of subjectivity used in making the estimates, comparisons between the Corporation’s disclosures and those of other companies may not be meaningful.

The following tables present the carrying amount and the estimated fair value of the Corporation’s financial instruments:

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| March 31, 2024 |

| | | Estimated Fair Value |

| (In thousands) | Carrying Amount | | Total | | Level 1 | | Level 2 | | Level 3 |

| Financial assets: | | | | | | | | | |