Investor Presentation

May 2009

May 2009

2

This presentation contains forward-looking statements, including, in particular, statements about

Interface’s plans, strategies and prospects. These are based on the Company’s current assumptions,

expectations and projections about future events.

Interface’s plans, strategies and prospects. These are based on the Company’s current assumptions,

expectations and projections about future events.

Although Interface believes that the expectations reflected in these forward-looking statements are

reasonable, the Company can give no assurance that these expectations will prove to be correct or that

savings or other benefits anticipated in the forward-looking statements will be achieved. Important

factors, some of which may be beyond the Company’s control, that could cause actual results to differ

materially from management’s expectations are discussed under the heading “Risk Factors” included

in Item 1A of the Company’s most recent Annual Report on Form 10-K, filed with the Securities and

Exchange Commission, which discussion is hereby incorporated by reference. Forward-looking

statements speak only as of the date made. The Company assumes no responsibility to update or

revise forward-looking statements and cautions listeners and conference attendees not to place undue

reliance on any such statements.

reasonable, the Company can give no assurance that these expectations will prove to be correct or that

savings or other benefits anticipated in the forward-looking statements will be achieved. Important

factors, some of which may be beyond the Company’s control, that could cause actual results to differ

materially from management’s expectations are discussed under the heading “Risk Factors” included

in Item 1A of the Company’s most recent Annual Report on Form 10-K, filed with the Securities and

Exchange Commission, which discussion is hereby incorporated by reference. Forward-looking

statements speak only as of the date made. The Company assumes no responsibility to update or

revise forward-looking statements and cautions listeners and conference attendees not to place undue

reliance on any such statements.

Forward Looking Statements

3

Daniel Hendrix

§ President and Chief Executive Officer

Patrick Lynch

§ Senior Vice President and Chief Financial Officer

Presenters

Company Overview

5

Investment Highlights

§ Interface is the largest manufacturer of modular carpet in the world, with 35%

market share, and some of the most recognized brands

market share, and some of the most recognized brands

§ Interface is the only global manufacturer with a presence on four continents

§ Interface serves diversified end markets, with the non-office market representing

almost 40% of the overall business

almost 40% of the overall business

§ Interface has been focused on organic growth of its modular business and debt

paydown

paydown

§ Substantial liquidity position

- Undrawn ABL Revolver and European Credit facility utilized for LCs and working

capital needs

capital needs

§ Management committed to conservative financial policies

6

Current Realities Facing our Business

§ Our operating structure was built for a $1 billion+ revenue base, which has now been

right-sized to meet current demand

right-sized to meet current demand

§ A continued secular shift to carpet tile in non-corporate commercial markets

represents a partial hedge against the declining office market

represents a partial hedge against the declining office market

§ Our operating philosophy in the current under capitalized global carpet industry is to

take market share, particularly in Europe, through our superior global position

take market share, particularly in Europe, through our superior global position

§ Raw material pricing should continue to be favorable due to lower demand and lower

inputs costs, which will help offset margin erosion due to underabsorption

inputs costs, which will help offset margin erosion due to underabsorption

§ Foreign exchange rates are moving in an unfavorable direction, however, our local

manufacturing footprint creates a competitive advantage against importers

manufacturing footprint creates a competitive advantage against importers

7

Interface Brands - Most Recognized in the Industry

8

High Margin, Low Capital Requirements and Enhanced Liquidity

First Mover in Sustainability

Rapid Innovation, Leading Brands and Designs

Global Make-to-Order Manufacturing and Local Distribution

Leading Position

in Modular Carpet

in Modular Carpet

Global Capabilities

with Expanding

Position in

Emerging Markets

with Expanding

Position in

Emerging Markets

Broadened Reach

with Residential

Modular Carpet

with Residential

Modular Carpet

Offering

Segmented Sales

Portfolio with

Diversified End

Markets

Portfolio with

Diversified End

Markets

Strengths

Interface Strengths and Value Drivers

9

4

1

2

3

5

6

7

MODULAR carpet means NO glue,

NO pad

NO pad

MODULAR lowers the cost of

change

change

MODULAR produces less waste

MODULAR means faster and more

profitable installations for

contractor

profitable installations for

contractor

MODULAR is easier to reconfigure

and maintain

and maintain

MODULAR means creative design

freedom

freedom

MODULAR is easily recycled and

repurposed

repurposed

Modular Carpet is Becoming the Category for

Commercial Flooring - Secular Shift

Commercial Flooring - Secular Shift

Modular Core

Easy

Repairs

11

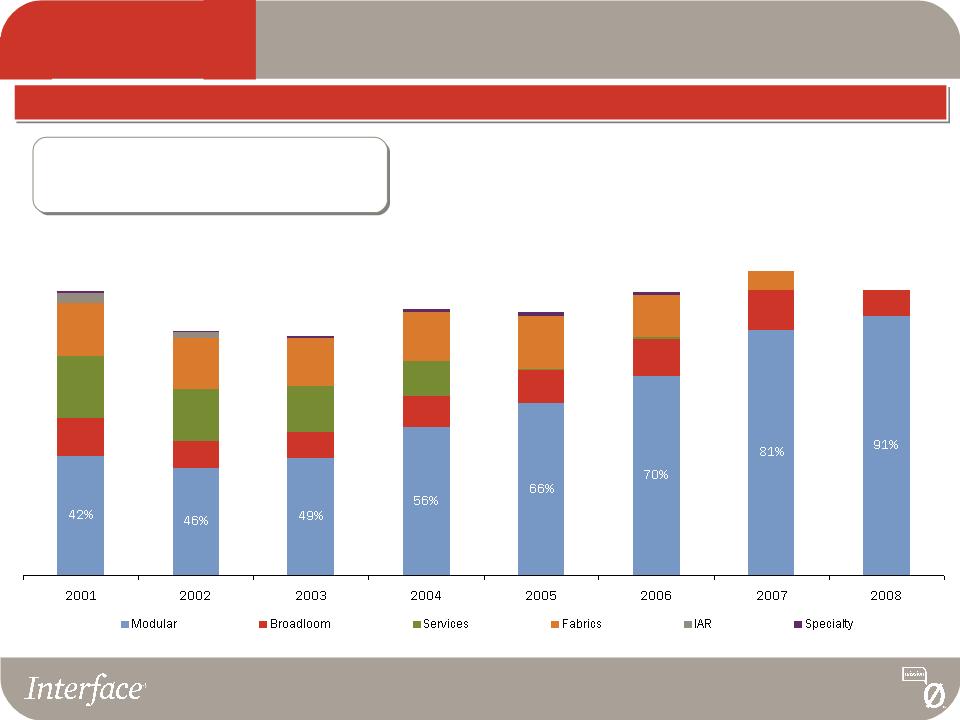

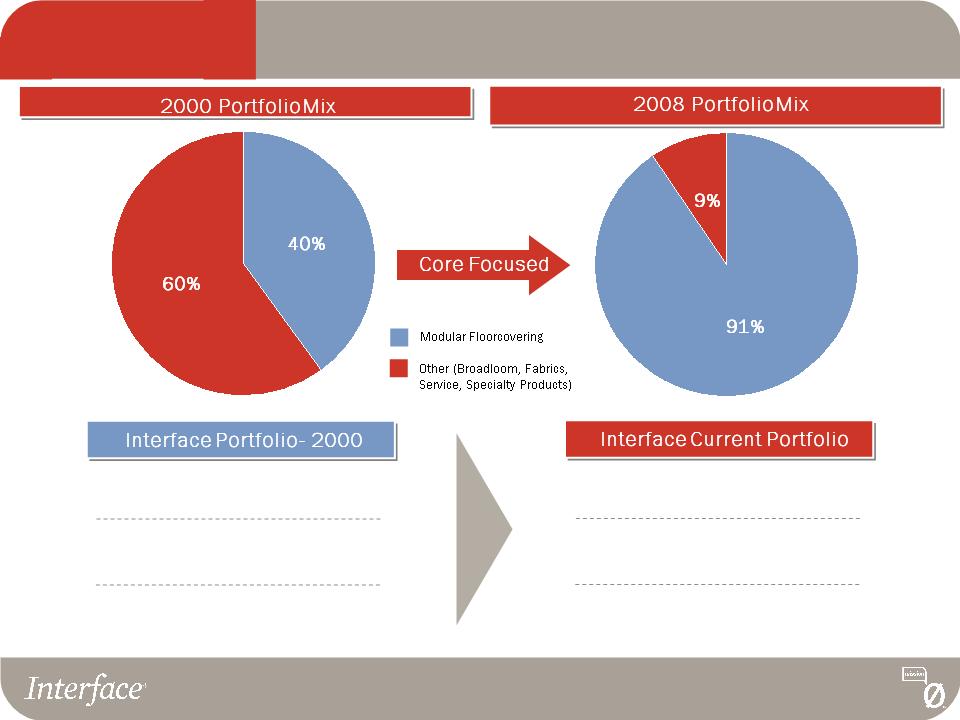

Modular Carpet Represents 91% of Interface

Divested

Raised

Access

Flooring

Raised

Access

Flooring

Divested

European

Fabrics

European

Fabrics

Divested

N. American

Fabrics

Divested

European

Broadloom

Divested

Installation &

Maintenance

Installation &

Maintenance

Sales by Business Type

Divested

Vinyl

Vinyl

Matting

Modular Core

Divested $500M in Revenue Base and

Replaced with Organic Modular Sales

Growth

Growth

12

98% Commercial

2% Residential

2% Residential

70% Corporate Office

30% Non-Corporate Office

30% Non-Corporate Office

90% Refurbishment

10% New Construction

10% New Construction

95% Commercial

5% Residential

5% Residential

60% Corporate Office

40% Non-Corporate Office

40% Non-Corporate Office

90% Refurbishment

10% New Construction

10% New Construction

Modular Core

Over the Past Five Years, Interface Has Focused

on its Core Modular Business

on its Core Modular Business

13

Source: Invista, Carpet and Rug Institute, Catalina Research Inc., U.S. Flooring Forecast and management estimates

§ Preferred interior design element

§ “Becoming the Flooring of Choice”

§ Random products merge design with

function

function

§ Sustainability drives recycled and

repurposed products

repurposed products

§ Stressed the functionality

of modular carpet

of modular carpet

§ Exploited the benefits of

modular vs. broadloom

modular vs. broadloom

§ Limited application and

design

design

§ Open office plans emerge

Pioneering Stage

Functionality Stage

Secular Shift

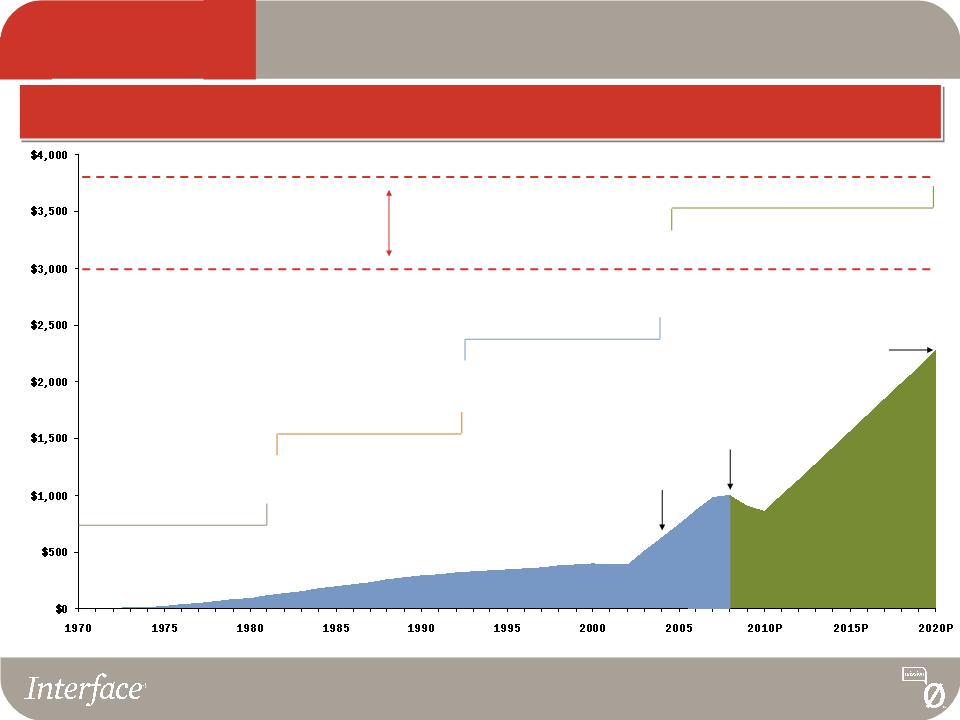

2008 Total U.S. Specified

Commercial Carpet Market = $3.0B

§ Celebrating the square

§ Sustainability is introduced

§ Pattern by tile

Liberation of Design

2020P Total U.S. Specified

Commercial Carpet Market = $3.8B

2.0%

CAGR

2008

34% Penetration

2020P

60% Penetration

U.S. Modular Carpet Sales

Specified Commercial Market

($ in millions)

What if modular

carpet reached

60% market

share of the

commercial

market by 2020?

carpet reached

60% market

share of the

commercial

market by 2020?

Modular Core

2004

26% Penetration

Functionality and Design Create a Secular Shift

From a Niche to a Category

From a Niche to a Category

14

Source: 2007 Floor Focus Magazine.

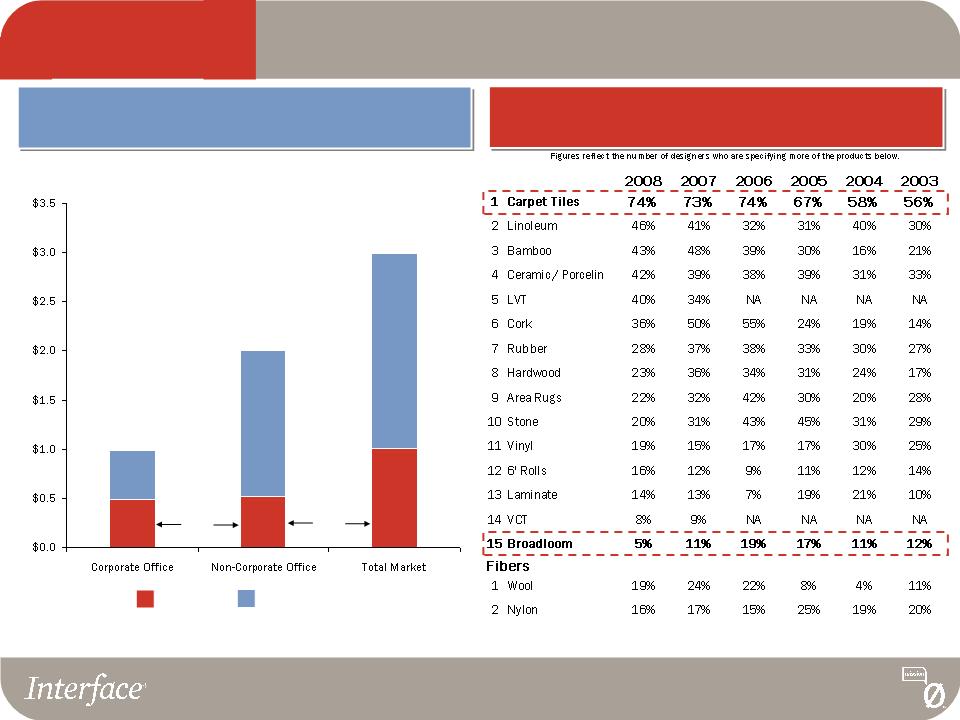

U.S. Floorcovering Opportunity

2008 Specified Commercial Market

$1B

50%

26%

Carpet

Tile

Penetration

$2B

U.S. Commercial Market Opportunity

$3B

34%

Carpet

Tile

Penetration

Carpet Tile

Other Floor Coverings

($ in Billions)

Floor Focus Top 250 Design Survey 2008:

Hot Products

Modular Core

Source: Invista, Carpet and Rug Institute, Catalina Research Inc., U.S. Flooring Forecast and management estimates

15

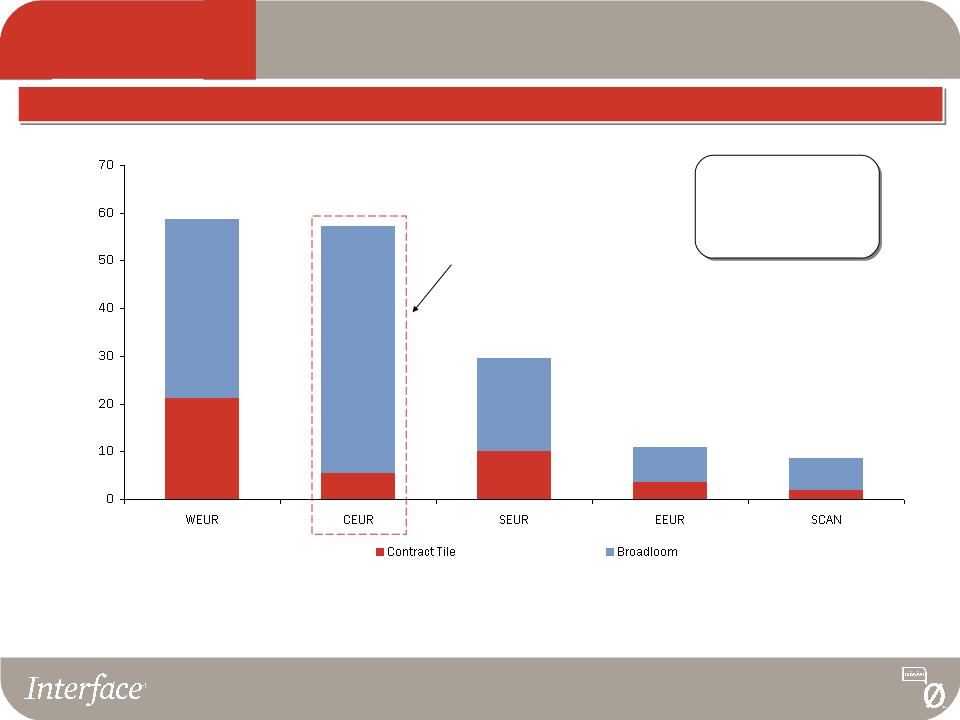

Carpet Tile Penetration of the European Contract Soft Flooring Market

There is significant opportunity for growth as Interface continues to penetrate major markets across

Europe

Europe

~26% Penetration

of the European

Commercial Market

Note: WEUR = BEN and UK/Ireland; CEUR includes Germany; SEUR includes France

Source: BMW Associates and management estimates

German market poised

for considerable carpet

tile expansion

for considerable carpet

tile expansion

European Market Opportunity

36%

9%

34%

33%

22%

(millions of square meters)

Modular Core

(millions of square meters)

German Market

16

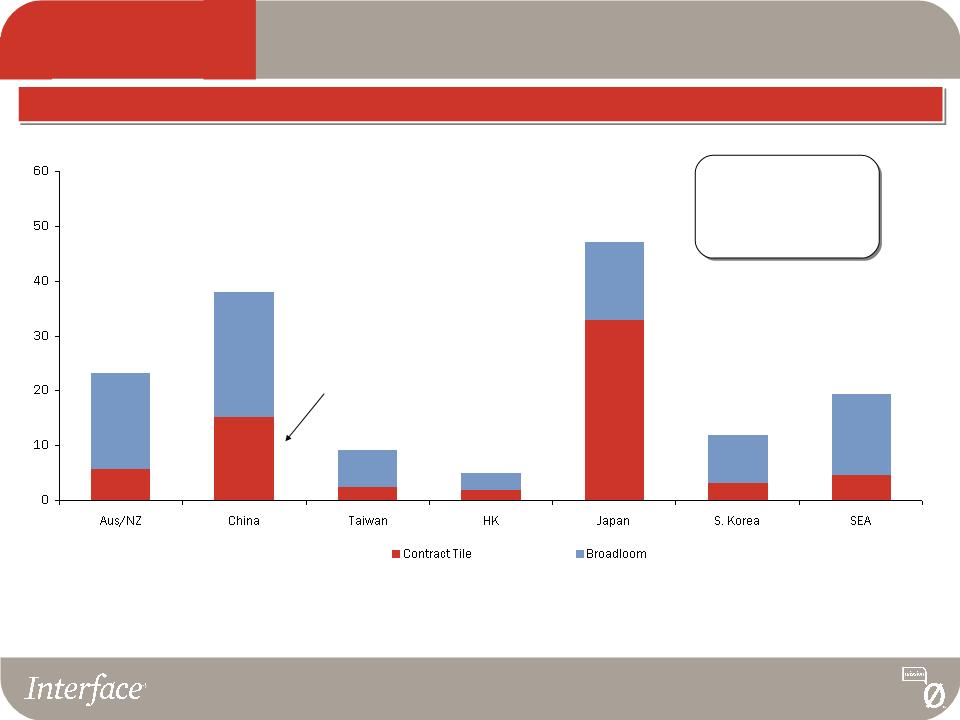

Carpet Tile Penetration of the Asia-Pacific Commercial Carpet Market

Strong penetration of Chinese and Japanese markets with significant opportunity for growth in other

major Asian and Australian markets

major Asian and Australian markets

~34% Penetration

of the Asia-Pacific

Commercial Market

(excluding Japan)

Source: BMW Associates and management estimates

Asia-Pacific Market Opportunity

(millions of square meters)

25%

40%

25%

39%

70%

26%

24%

Modular Core

Only 15% penetration of

Specified Commercial

Carpet Market in China

Specified Commercial

Carpet Market in China

17

Corporate

Office

Office

Government

Religious

Establishments

Establishments

Hospitals

Medical Office

Buildings

Buildings

Hotels/Resorts

Casinos

Stores

Malls

K-12

Colleges &

Universities

Universities

Assisted

Living

Boutique

Turnkey

Solutions

Segmented Commercial Market Approach

Institutional

Healthcare

Hospitality

Retail

Education

Commercial Segmentation

Financial

Service

Service

Fortune 1000

Main

Street

Segmentation

18

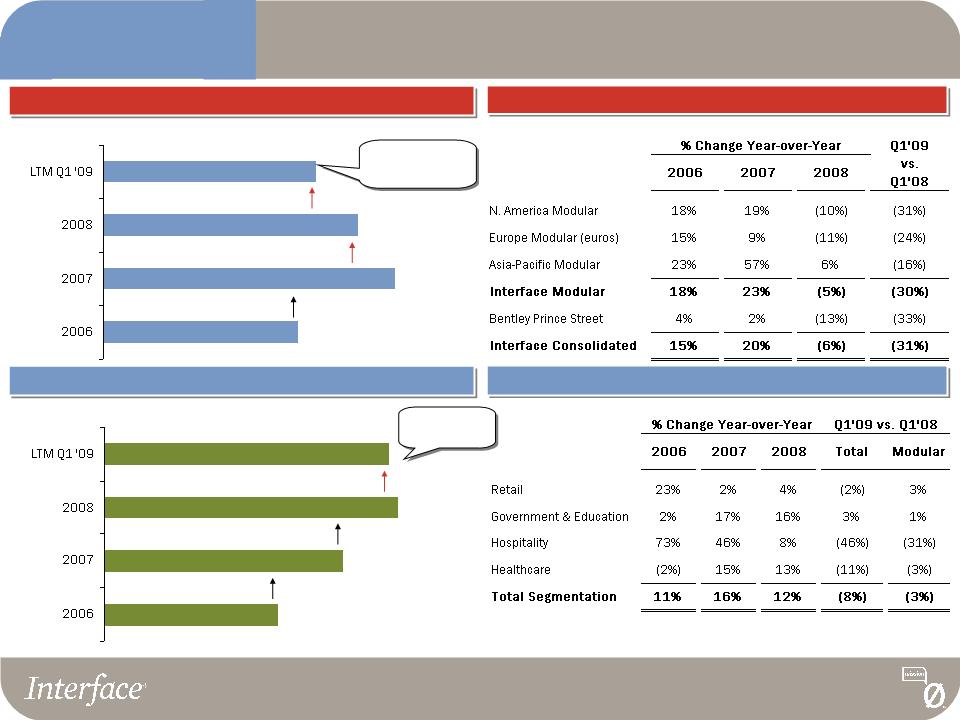

Strong Growth from Non-Corporate Segments

Segmentation

Only 50% of the

overall business

Over 35% of

our business

Gross Billings from Non-Corporate Office Segments

16% Growth

(Institutional, Healthcare, Hospitality, Retail, Education)

Non-Corporate Office Growth Comparison by Segment

Gross Billings from Mature Corporate Office

20% Growth

Mature Corporate Office Growth Comparison by Geography

6% Decline

12% Growth

(excludes Emerging Office Markets)

(excludes Emerging Office Markets)

* Growth due to CVS acquisition of Albertson’s drug

stores

stores

*

8% Decline

2% Decline

19

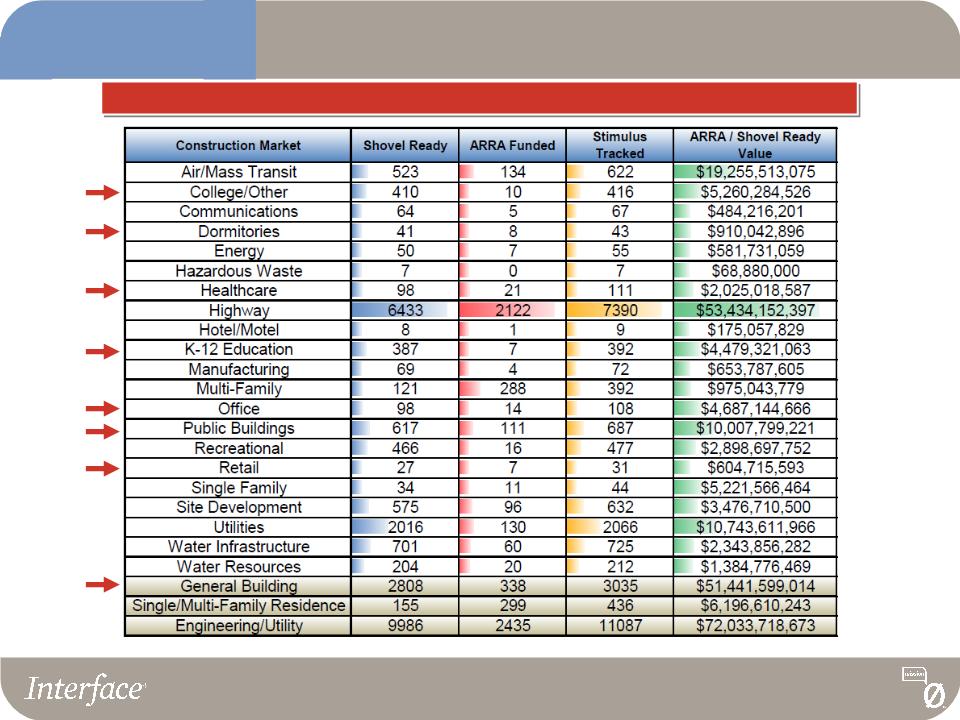

United States Stimulus Package

Reported Stimulus by Markets

Source: McGraw Hill Construction

Segmentation

20

Corporate Office Segment

Segmentation

21

Retail

Segmentation

22

Higher Education

K-12 Education

Education

Segmentation

23

Healthcare

Segmentation

24

Public Spaces

Library

Government

Segmentation

25

Hospitality

Segmentation

26

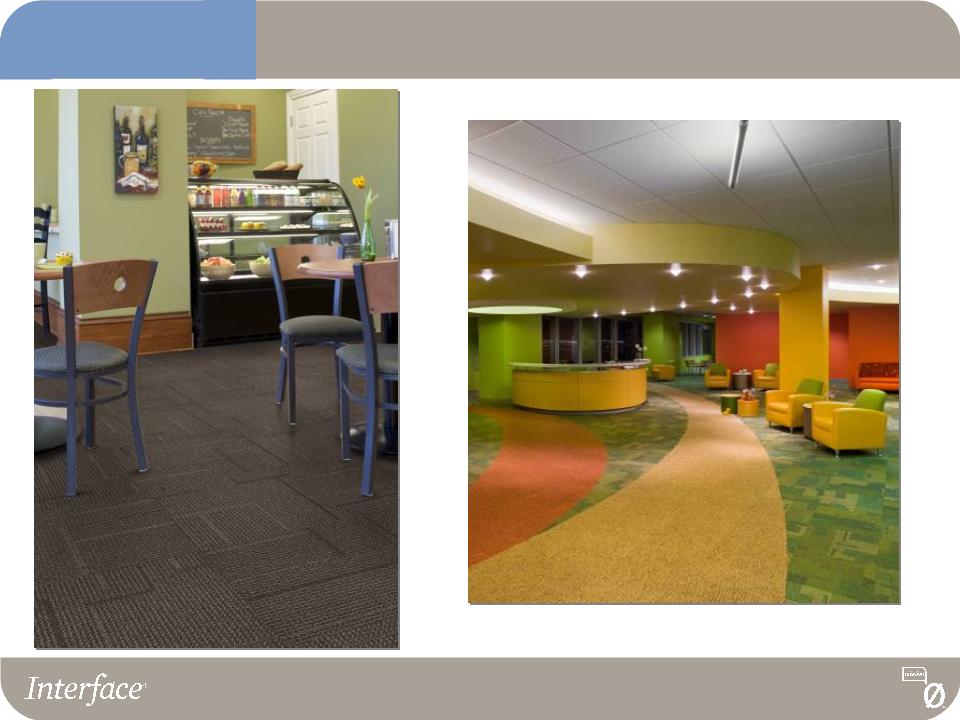

Hospitality - - Interface Hospitality Installations

Segmentation

27

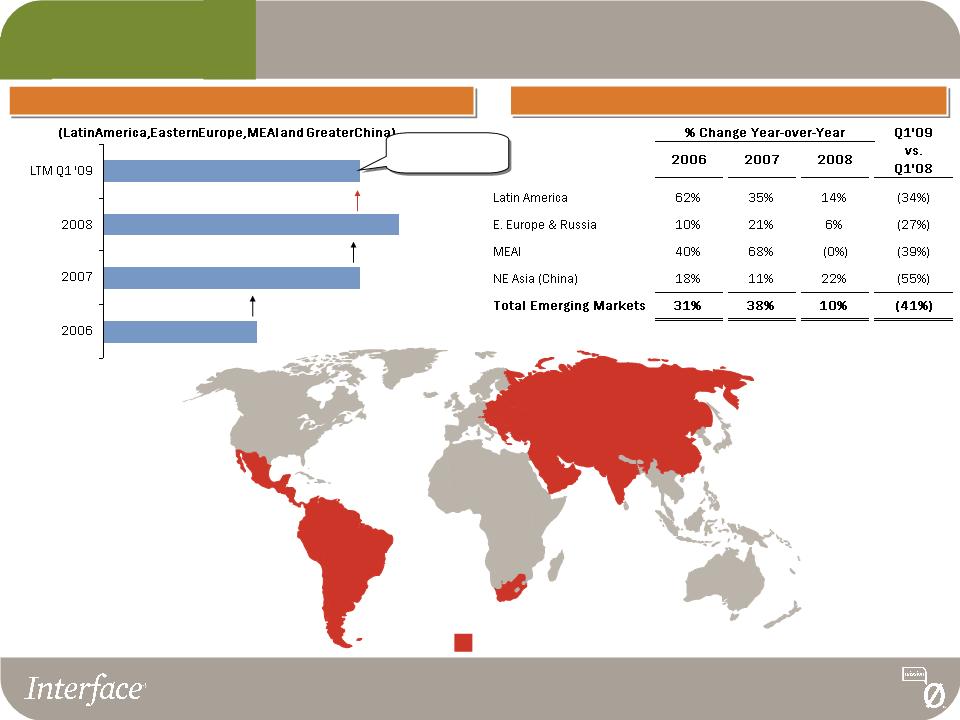

Successfully Penetrating Emerging Markets

Emerging

Markets

Markets

Emerging Markets

Gross Billings from Emerging Markets

Emerging Market Growth Comparison by Geography

38% Growth

10% Growth

9% Decline

Represents 10%

of our business

of our business

28

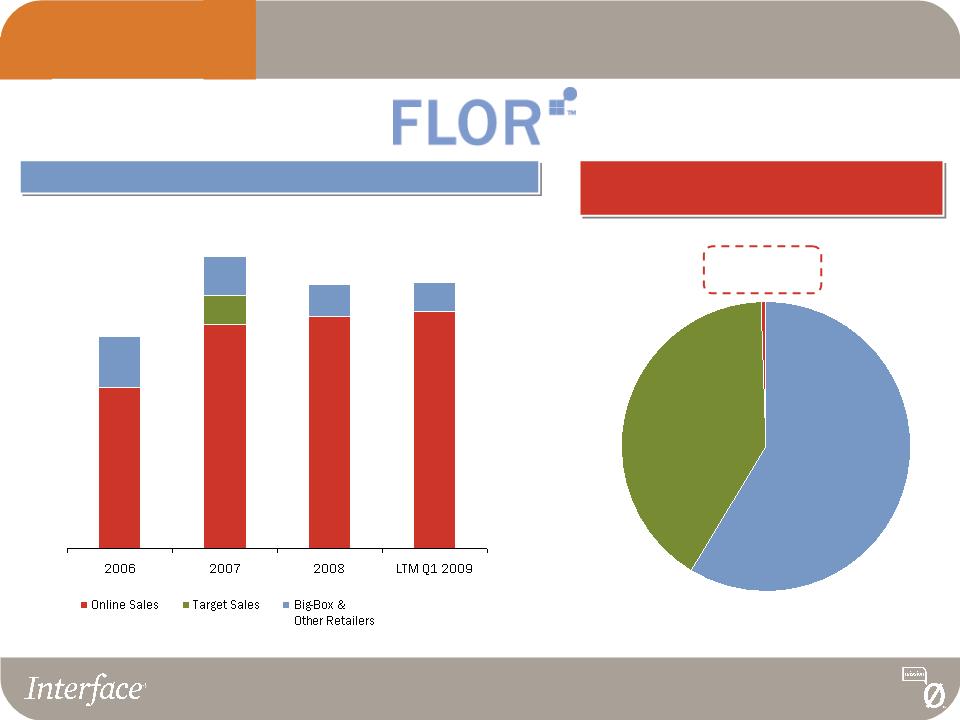

Carpet Tile

<1%

FLOR Sales by Channel

FLOR is Creating a Category:

“Modular Carpet for the Home”

“Modular Carpet for the Home”

↑ 44%

↑ 4%

↑ 39%

Carpet Tile Penetration of the $11B

U.S. Residential Floorcovering Market

↑ Online Sales

Y-o-Y Growth

Residential

Opportunity

Opportunity

Area Rugs

41%

Other

Floorcoverings

58%

↑ 2%

Online Sales up 9% in Q1 2009 vs. Q1 2008

29

FLOR is Expanding its Online and Retail Presence

Residential

Opportunity

Opportunity

FLOR Catalog and Online Sales

FLOR Retail Presence

30

Modular Goes in the Home

Residential

Opportunity

Opportunity

31

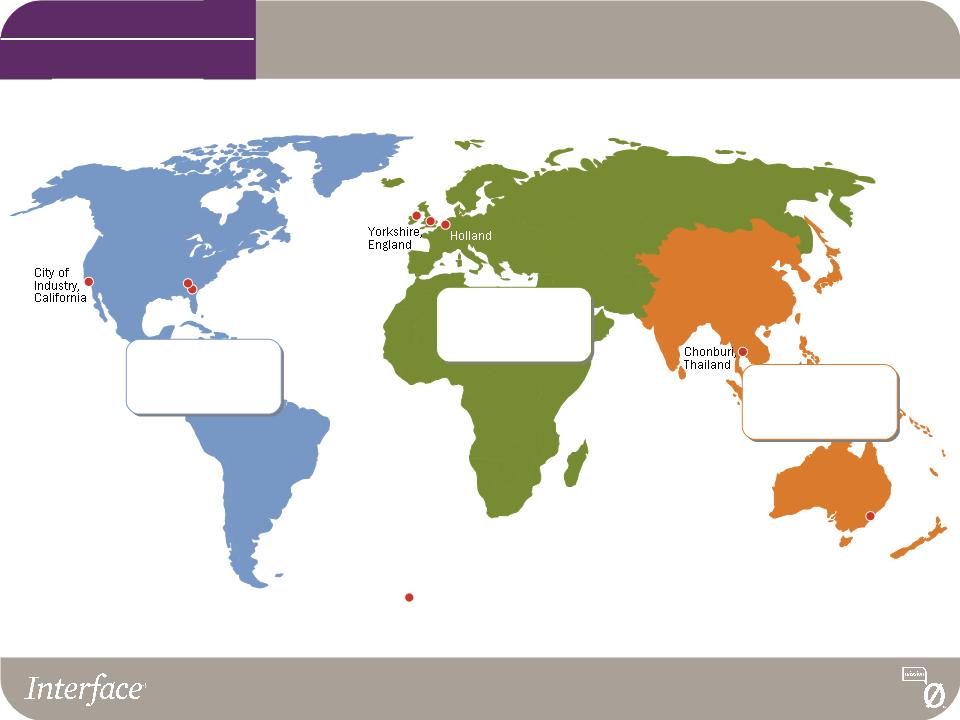

Global Manufacturing Capabilities and Local

Distribution

Distribution

N. Ireland

Picton,

Australia

Australia

Manufacturing Facility

LaGrange,

Georgia

Georgia

Americas

55% of Sales

50% of Production

Europe

34% of Sales

34% of Production

Asia-Pacific

11% of Sales

16% of Production

Note: Figures represent FYE 2008

Global Make-to-Order

Value Drivers

32

1. Increases speed to market

2. Promotes innovation

3. Offers unique custom product

capabilities

capabilities

4. Supports a constant flow of new

products

products

5. Offers sales force the opportunity to

visit the customer with new products

visit the customer with new products

6. Decreases lead time to customers

7. Increases inventory turns

The Made-to-Order ADVANTAGE

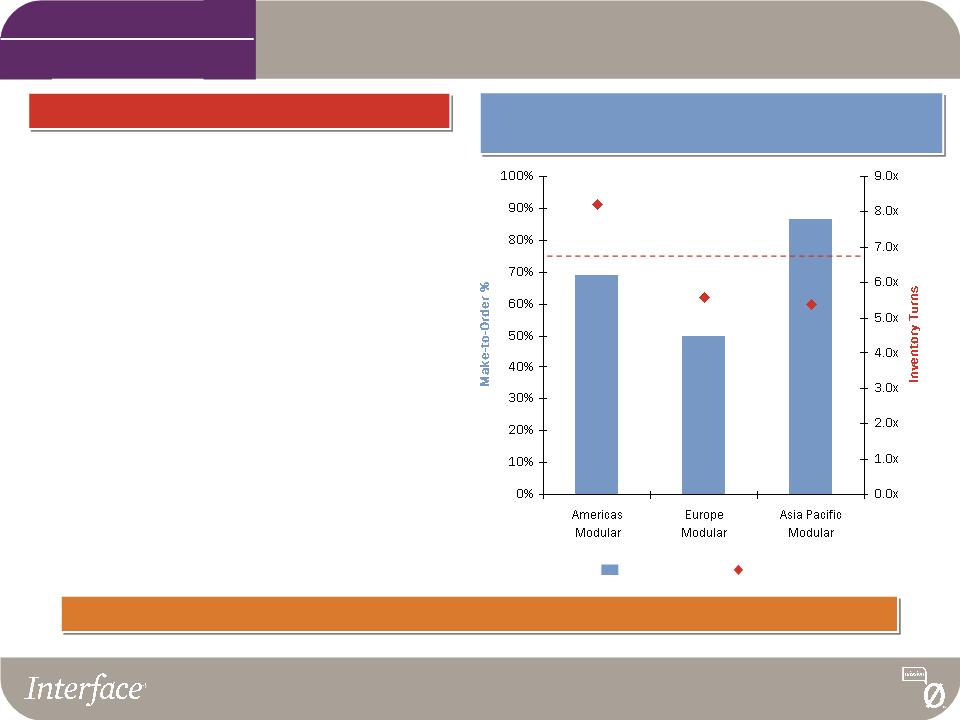

Interface Modular Businesses

2008 Make-to-Order % and Inventory Turns

Interface is the ONLY company with a “make-to-order” approach to the market

75% TARGET Level

Strong Competitive Advantage Through

Make-to-Order Philosophy

Make-to-Order Philosophy

Note: Figures represent FYE 2008

Global Make-to-Order

Value Drivers

Make-to-Order %

Inventory Turns

33

Interface Innovation

1. INVENTED carpet tile in Europe (1950s) and PIONEERED the modular concept

In the U.S. (1970s)

In the U.S. (1970s)

2. FIRST to move away from the monolithic broadloom look for carpet tile

3. FIRST to introduce a make-to-order offering

4. FIRST in the industry to recognize the importance of sustainability

5. FIRST to introduce 100% post-consumer recycled backing

6. FIRST to introduce modular products designed to be installed randomly

7. EARLY adopter in the residential market

8. FIRST to introduce a “glueless” installation - TacTiles

9. FIRST to introduce post-consumer recycled content face yarns

10. FIRST to introduce moisture vapor barrier

Interface Leads with INNOVATION

Value Drivers

Innovation & Design

34

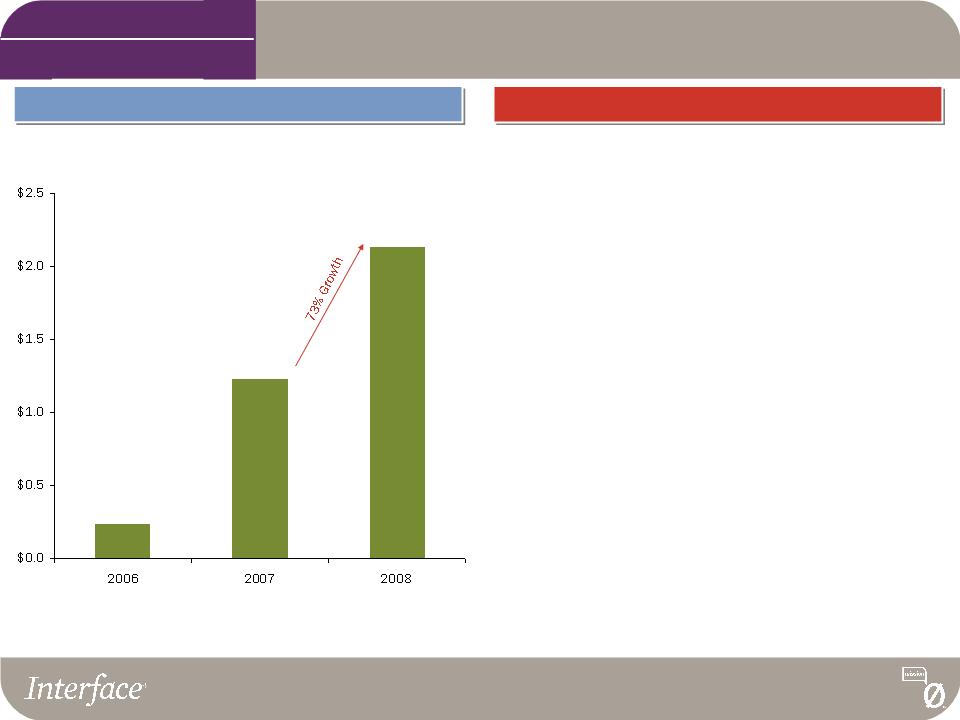

TacTiles Sales Exceed $2 Million as We Drive

“Glueless” Installation Exclusive to Interface

“Glueless” Installation Exclusive to Interface

Value Drivers

($ in mms)

* Includes TacTiles and TacTiles dispensers

$0.2

$1.2

$2.1

Sales of TacTiles

Benefits of TacTiles

§ Patented No Glue / No VOCs installation

system

system

§ 25% of current orders include TacTiles

§ High margin product

§ Leading to other new innovations - Moisture

Guard 2.0

Guard 2.0

§ Outside distribution protects our share of

new channels that switch to “glueless”

installation

new channels that switch to “glueless”

installation

Innovation & Design

35

Market Leader in Product DESIGN and FASHION

Value Drivers

Innovation & Design

36

Brands that Deliver Our Promise of High End

Functionality, Quality and Design

Functionality, Quality and Design

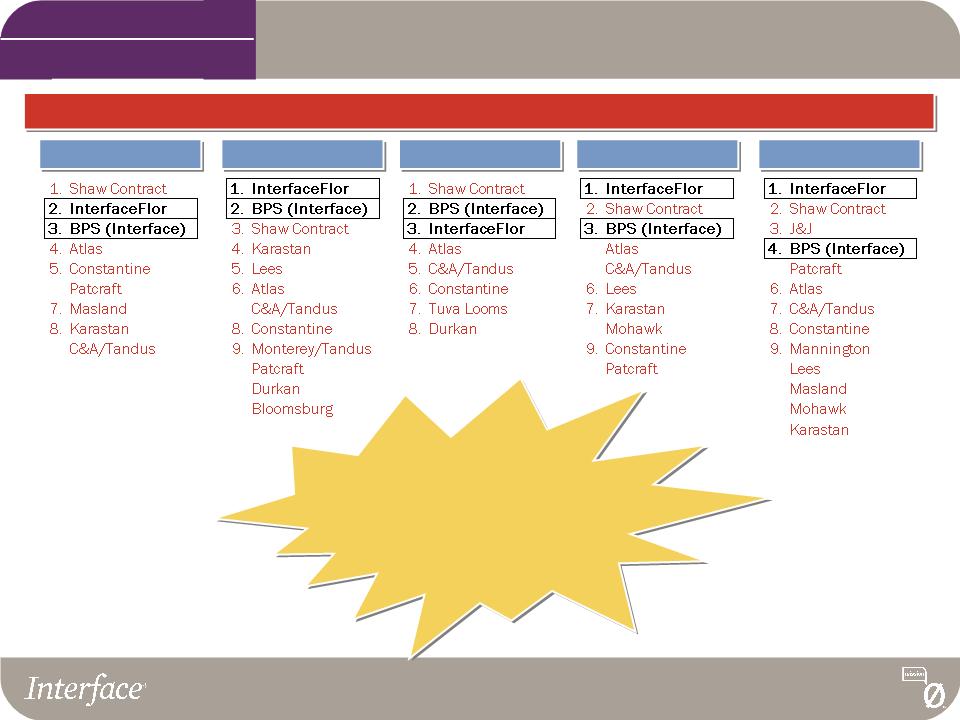

Source: 2008 Floor Focus Magazine (U.S. Market)

Interface Rated the “Best

Overall Business Experience”

for the 5th

for the 5th

Year in a Row

Favorite Carpet Manufacturers

Service

Quality

Design

Performance

Value

Value Drivers

Innovation & Design

37

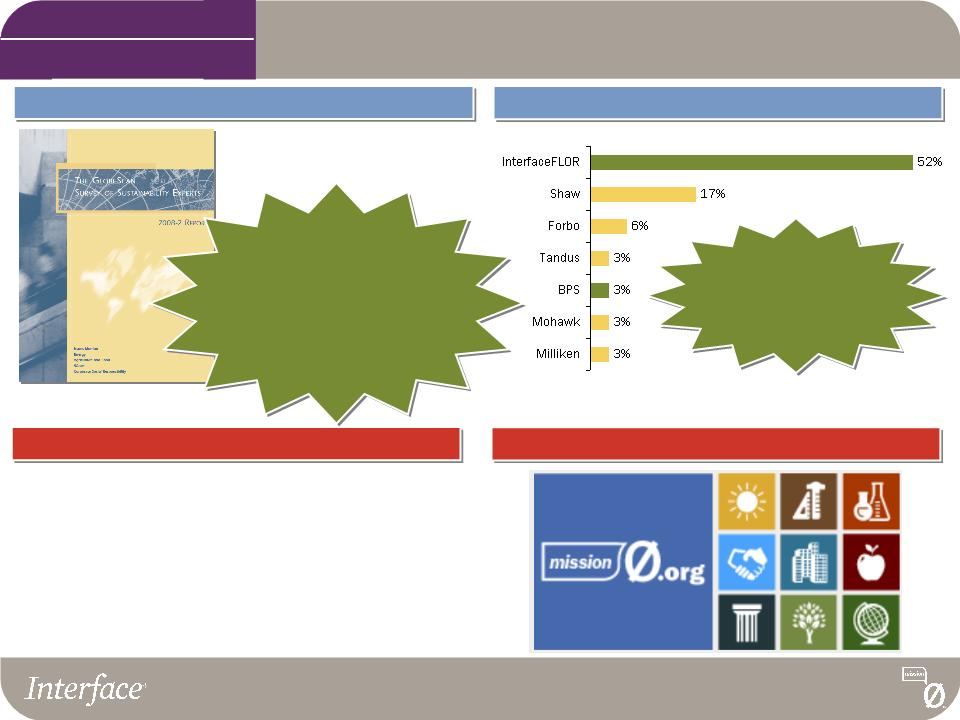

Interface Continues to be Recognized as the

Leader in Sustainability

Leader in Sustainability

Sustainability

2008 GlobeScan Survey of Sustainability Experts

Floor Focus Green Leaders 2008

Source: 2008 Floor Focus Magazine (U.S. Market)

§ Employee programs

§ NGO partnerships

§ Policy working groups

§ Standards development groups

Interface received

“Green Kudos”

for closed loop processes

and recycled content

Value Drivers

Stakeholder Engagement

MissonZero.org

Interface was again

named the top company

above companies like BP, General

Electric, Shell and Toyota

that comes to mind as fulfilling

their responsibility to society

better than others.

38

Interface Continues to be Recognized as the

Leader in Sustainability

Leader in Sustainability

Sustainability

Value Drivers

§ Product/Process Innovation:

– Random Carpet Tile Patent

– TacTiles

– Cool Blue (100% Recycled Backing)

– Cool Carpet (Climate Neutral)

– Landfill Gas Project

– LEED innovation credits

– ReEntry Process (post-consumer content

recycled face yarn)

recycled face yarn)

§ The Federal Stimulus bill will provide potential

opportunities for funding of corporate research and

development incentives for projects focused on

renewable energy and carbon reductions

opportunities for funding of corporate research and

development incentives for projects focused on

renewable energy and carbon reductions

Sustainability-Focused Innovation

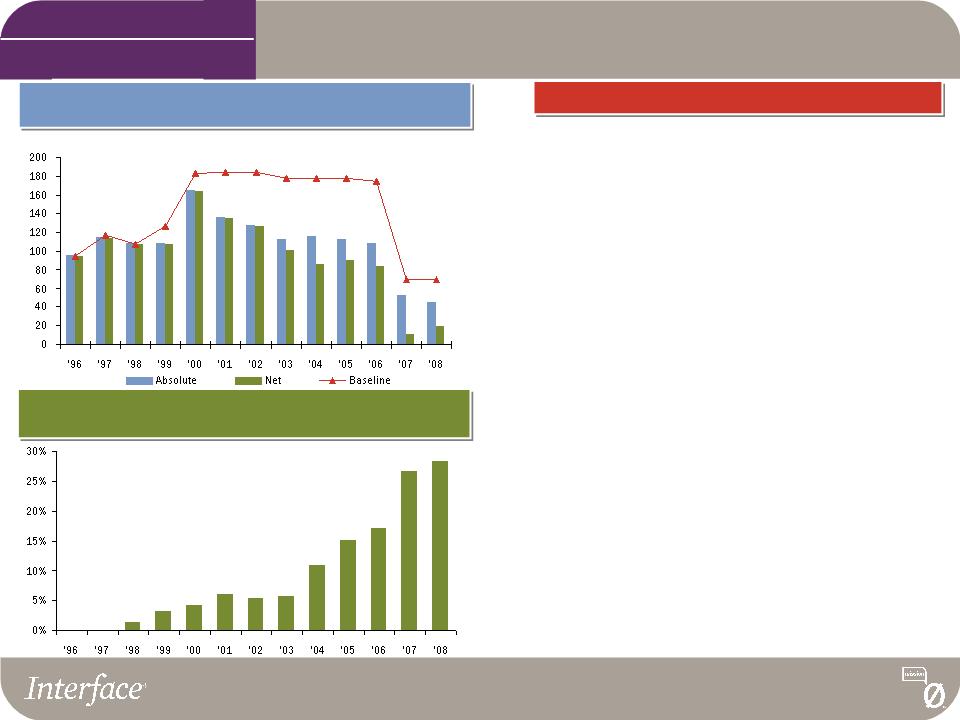

Greenhouse Gas Emissions

(metric tons of CO2 equivalent in thousands)

Energy from Renewable Resources at Carpet Manufacturing

Facilities (percent of total energy use)

Facilities (percent of total energy use)

28%

Absolute GHG emissions have been reduced by 34% and further offset by an

additional 37% as a result of company owned GHG projects.

39

ReEntry and Cool Blue

ReEntry

Cool Blue

Sustainability

Value Drivers

40

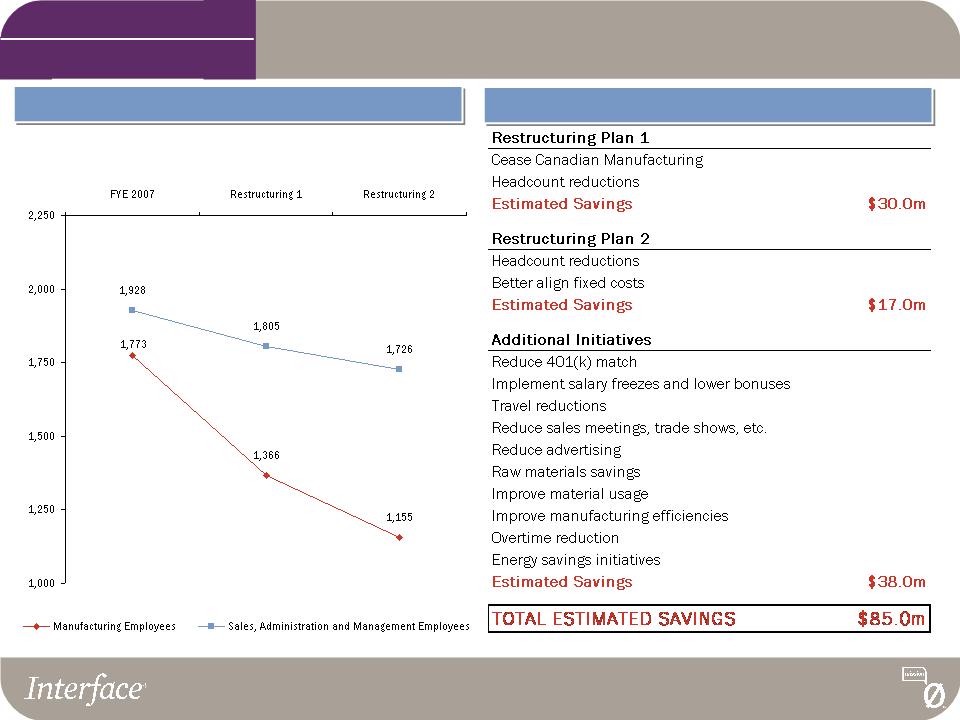

Right-sizing our Business

Profitability

Value Drivers

Interface Headcount

↓ 530

Employees

↓ 290

Employees

Cost Savings Initiatives

↓ 35%

↓ 10%

41

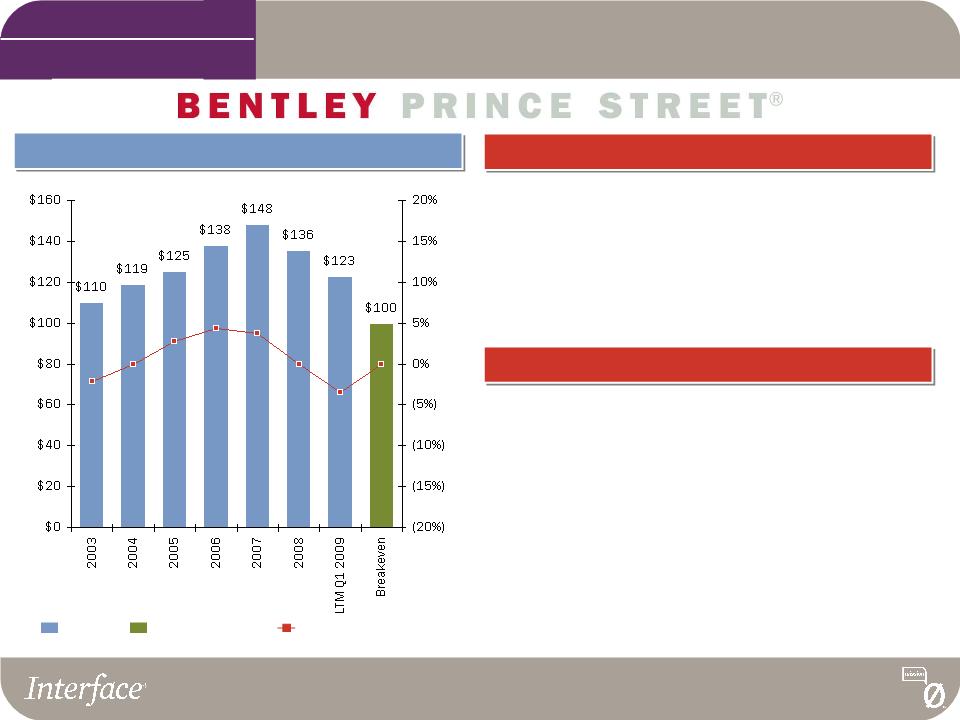

Downsizing Bentley Prince Street to Breakeven

Profitability

Value Drivers

Net Sales and Operating Income

Current Realities

Net Sales

Operating Income % of Net Sales

§ Contracting broadloom market - particularly high-end

§ Non-cash goodwill charge of $61.2 million in 2008 due to

revised projections and declining valuations of market

comparables

revised projections and declining valuations of market

comparables

§ Operating efficiency challenges resulting from declining

revenue base

revenue base

Profitability Protection

§ Realigned business to $100 million breakeven point:

- Reduced headcount by 157 employees (30%)

- Implemented expense reduction and manufacturing

efficiency initiatives that are expected to yield $7

million in annualized savings

efficiency initiatives that are expected to yield $7

million in annualized savings

- Anticipated raw materials savings of almost $3 million

- Realigned product portfolio and rationalized

manufacturing operations

manufacturing operations

Breakeven Net Sales

($ in millions)

Financial Overview

43

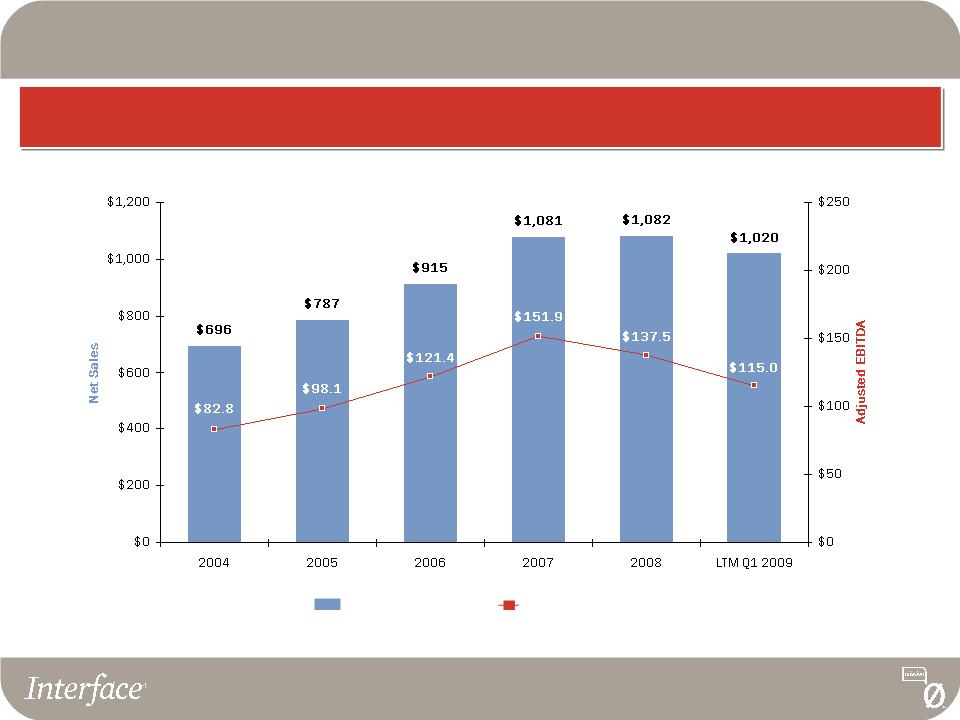

Net Sales and Adjusted EBITDA*

(Continuing Operations)

Consolidated Financial Results

($ in millions)

Adjusted EBITDA

Net Sales

* See page 48 for a reconciliation of Adjusted EBITDA

44

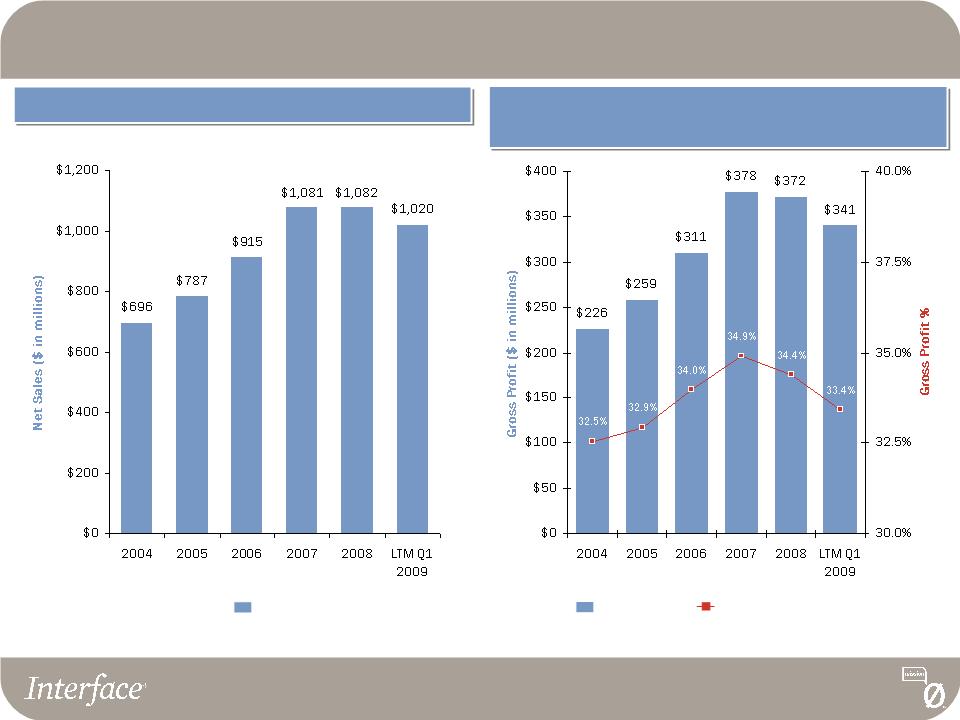

Net Sales

Gross Profit and

Gross Profit % of Net Sales

Net Sales

Gross Profit

Gross Profit % of Net Sales

Interface Financial Results From Continuing Operations

45

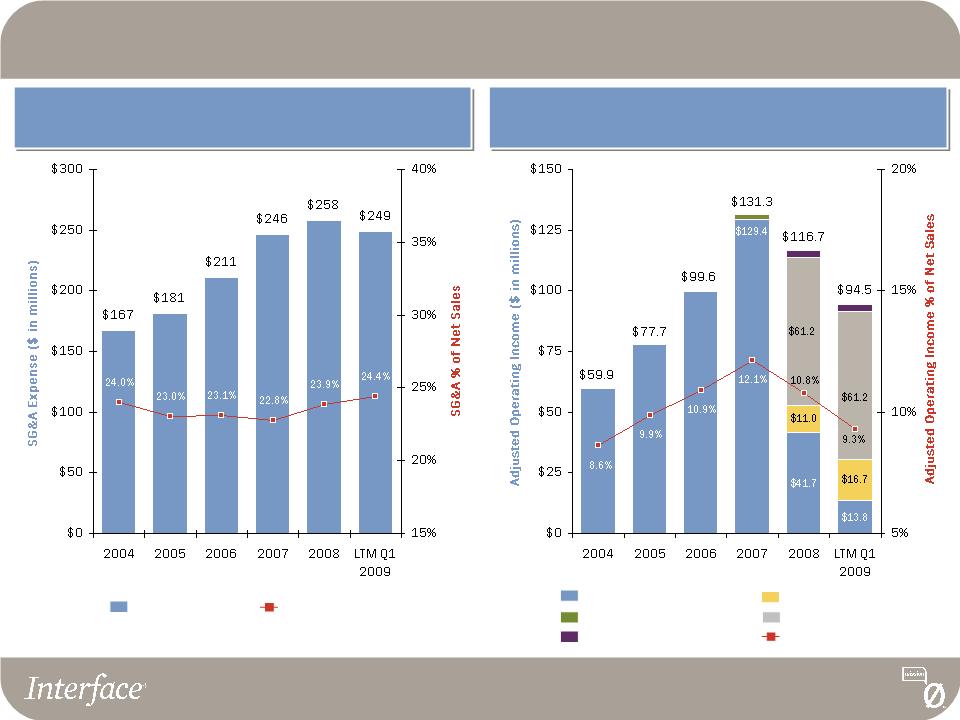

SG&A Expense and

SG&A % of Net Sales

Adjusted Operating Income* and

Adjusted Operating Income % of Net Sales

SG&A Expense

SG&A % of Net Sales

Reported Operating Income

Restructuring Charges

Loss on Disposal ($1.9m)

Operating Income % of Net Sales

Goodwill Impairment

Decline in Insurance Value ($2.8m)

* See page 48 for a reconciliation of Adjusted Operating Income

Interface Financial Results From Continuing Operations

46

§ Protect profitability - expect to generate $35-$50 million of cash

from operating activities in 2009

from operating activities in 2009

§ Reduce capital spending to $10 million - maintenance capital

expenditures only or a payback period of one year or less

expenditures only or a payback period of one year or less

§ Continue to maximize working capital including DSO contraction and

increased inventory turns

increased inventory turns

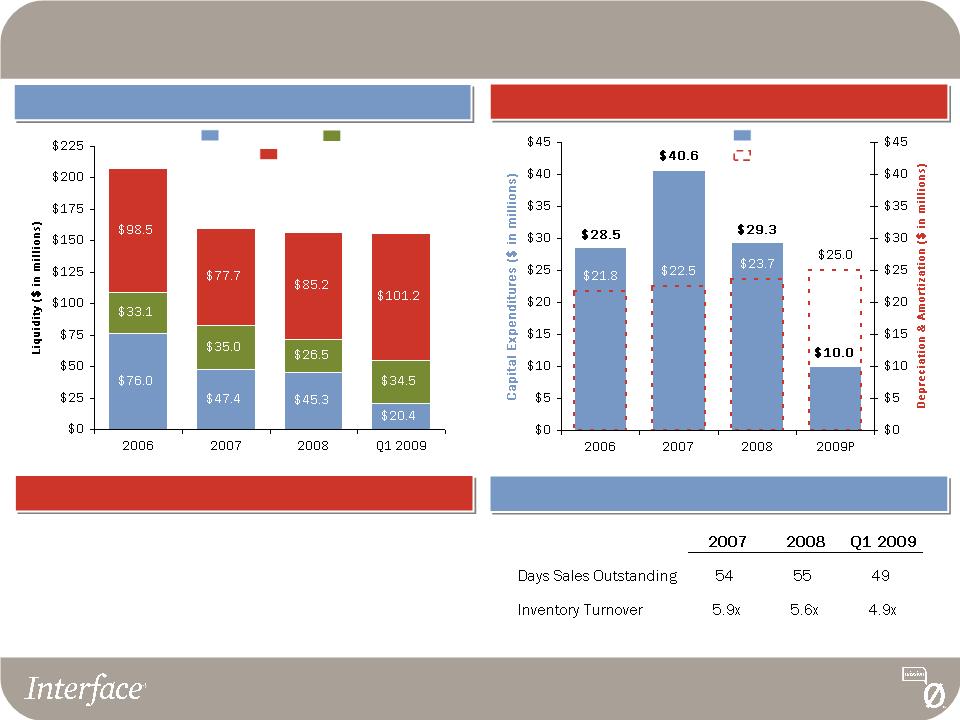

Interface Liquidity Strategy

Capital Expenditures

Working Capital Ratios

Interface Liquidity Strategy

Capital Expenditures

Depreciation &

Amortization

Liquidity Position

U.S. Cash Position

International Cash Position

Availability Under U.S. and

International Revolvers*

$207.7

$160.1

$157.0

* Q1 2009 revolver availability includes the €32 million ($42 million) European credit facility effective May 1, 2009

$156.1

47

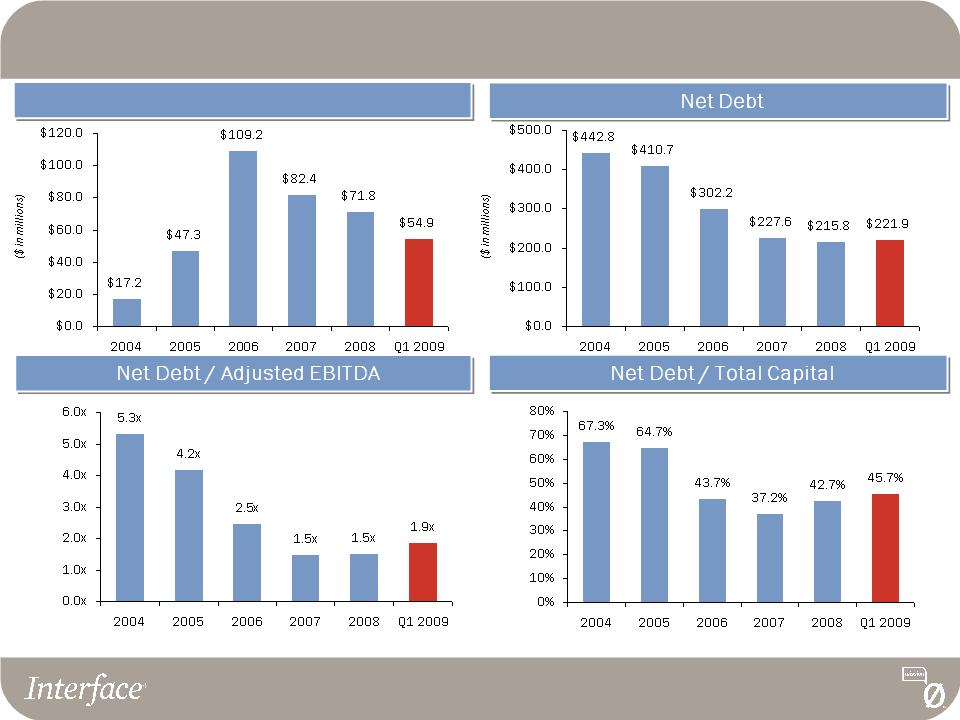

Key Credit Statistics* (All data excludes the Fabrics Division sold in 2007)

Ending Cash Balance

* See page 48 for a reconciliation of Net Debt and Adjusted EBITDA

48

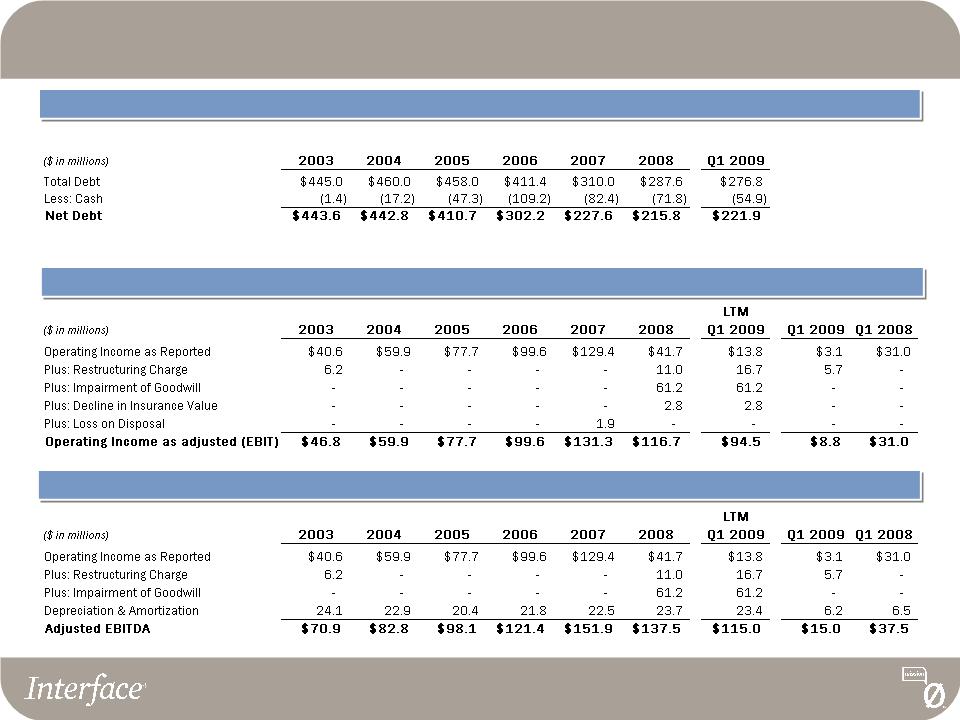

Appendix: Reconciliation of Non-GAAP Financial Measures

Net Debt (pg. 47)

Adjusted Operating Income (pg. 45)

Adjusted EBITDA (pg. 43 and 47)