2

This presentation contains forward-looking statements, including, in particular, statements about Interface’s

plans, strategies and prospects. These are based on the Company’s current assumptions, expectations and

projections about future events.

plans, strategies and prospects. These are based on the Company’s current assumptions, expectations and

projections about future events.

Although Interface believes that the expectations reflected in these forward-looking statements are

reasonable, the Company can give no assurance that these expectations will prove to be correct or that

savings or other benefits anticipated in the forward-looking statements will be achieved. Important factors,

some of which may be beyond the Company’s control, that could cause actual results to differ materially from

management’s expectations are discussed under the heading “Risk Factors” included in Item 1A of the

Company’s most recent Annual Report on Form 10-K, filed with the Securities and Exchange Commission,

which discussion is hereby incorporated by reference. Forward-looking statements speak only as of the date

made. The Company assumes no responsibility to update or revise forward-looking statements and cautions

listeners and conference attendees not to place undue reliance on any such statements.

reasonable, the Company can give no assurance that these expectations will prove to be correct or that

savings or other benefits anticipated in the forward-looking statements will be achieved. Important factors,

some of which may be beyond the Company’s control, that could cause actual results to differ materially from

management’s expectations are discussed under the heading “Risk Factors” included in Item 1A of the

Company’s most recent Annual Report on Form 10-K, filed with the Securities and Exchange Commission,

which discussion is hereby incorporated by reference. Forward-looking statements speak only as of the date

made. The Company assumes no responsibility to update or revise forward-looking statements and cautions

listeners and conference attendees not to place undue reliance on any such statements.

Forward Looking Statements

3

Daniel Hendrix

§ President and Chief Executive Officer

Patrick Lynch

§ Senior Vice President and Chief Financial Officer

Presenters

4

§ Interface is leading the secular shift to modular carpet as it moves from a niche to a

category with the leading global market share.

category with the leading global market share.

§ Interface is the largest global manufacturer of modular carpet with a presence on four

continents (United States, England, Holland, Ireland, Thailand, China, Australia).

continents (United States, England, Holland, Ireland, Thailand, China, Australia).

§ Interface has established diversified end markets including emerging markets, non-

office commercial markets, and consumer representing nearly 55% of the overall

business.

office commercial markets, and consumer representing nearly 55% of the overall

business.

§ Interface is creating a consumer brand (FLOR) as modular carpet is moving from a

concept to awareness for the home.

concept to awareness for the home.

§ Interface’s global sales and marketing capabilities have created significant growth in

emerging markets which will experience growth faster than developed countries.

emerging markets which will experience growth faster than developed countries.

§ Interface is the recognized thought leader in sustainability - the marketplace is

rewarding our leading position.

rewarding our leading position.

Investment Highlights

5

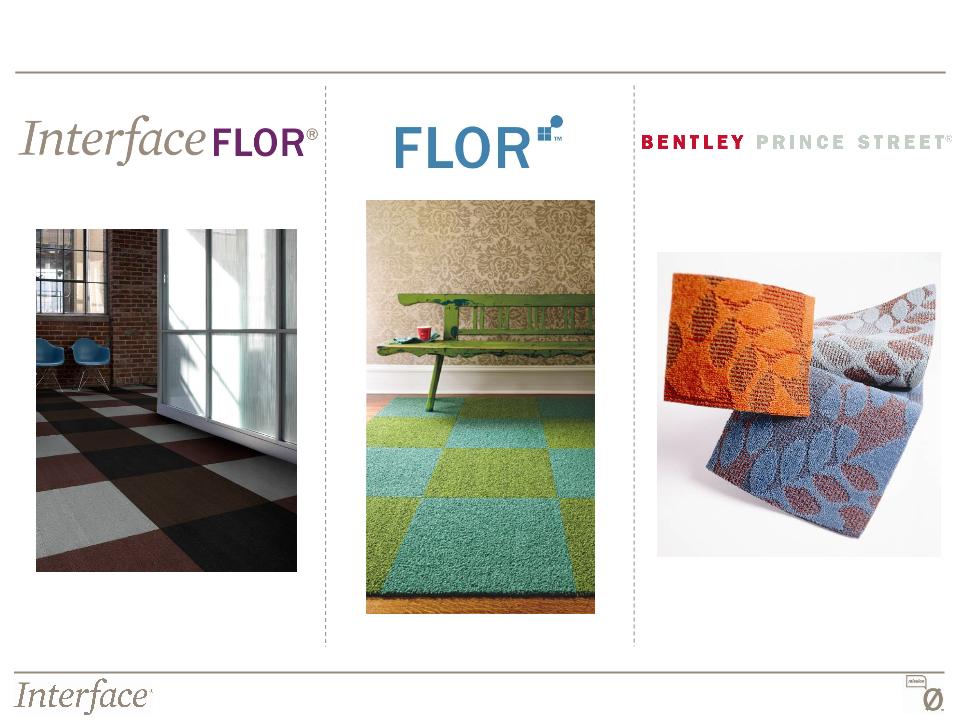

Interface Brands - Most Recognized in the Industry

6

Leadership Position in Sustainability

Global Make-to-Order Manufacturing and Local Distribution

Rapid Innovation and Designs

Invest in the Growth

of Emerging Markets

of Emerging Markets

Grow a

Consumer Brand

Diversify

End Use

Markets

Maintain Dominant

Share in the

Share in the

Office Market

§ Establish our position as

the leader in modular

carpet for the home

the leader in modular

carpet for the home

§ Drive sales through direct

channels

channels

§ Potential roll out of FLOR-

branded store network in

the U.S.

branded store network in

the U.S.

§ Drive growth of carpet tile

market in China with local

manufacturing presence

market in China with local

manufacturing presence

§ Invest in growth in Latin

America, Eastern Europe,

Middle East, Africa and

Indo-China

America, Eastern Europe,

Middle East, Africa and

Indo-China

§ Gain share in commercial

non-office segments

non-office segments

§ Establish “main street”

commercial presence in

the U.S. and Australia

commercial presence in

the U.S. and Australia

§ Pursue the airline

transportation segment in

the U.S.

transportation segment in

the U.S.

§ Capture opportunity as

the Office market

rebounds

the Office market

rebounds

§ Gain share in European

carpet tile market

carpet tile market

Lead the Secular Shift of Modular Carpet

Reduce the Cyclical Nature of our Business

Customer Intimacy

Interface Strategy: Be the Global Category Leader for Modular Carpet

7

Secular Shift

1. Creative DESIGN freedom

2. NO glue, NO pad

3. LOWER COST to change

4. Produces LESS WASTE

5. FASTER and more PROFITABLE

INSTALLATION for contractors

INSTALLATION for contractors

6. Easier to RECONFIGURE and

MAINTAIN

MAINTAIN

7. Easily RECYCLED and

REPURPOSED

REPURPOSED

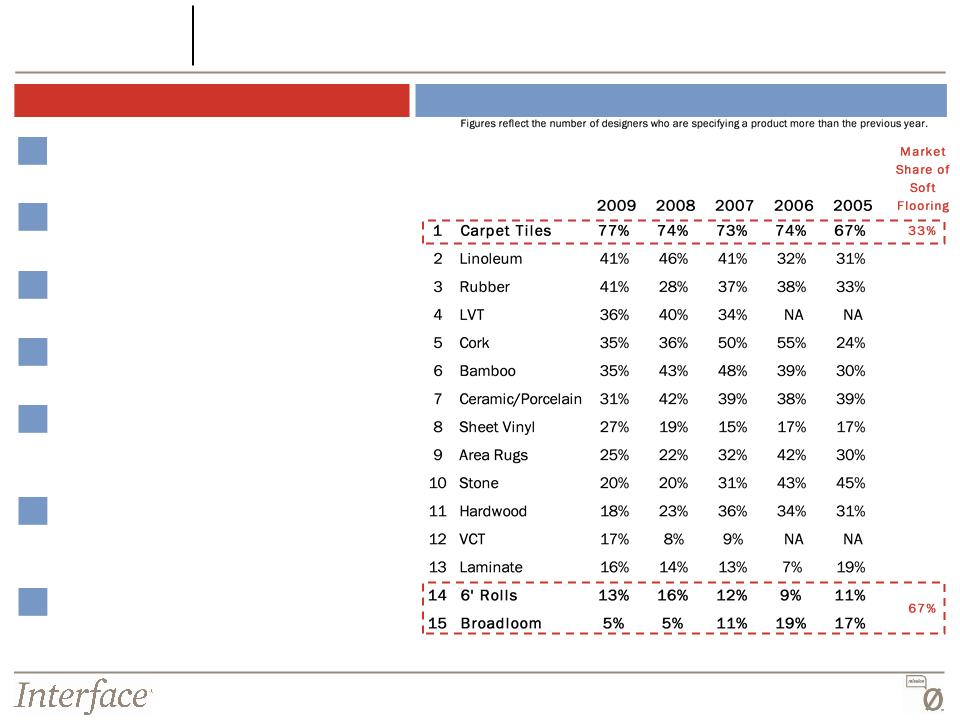

2009 Floor Focus U.S. Top 250 Design Survey: Hot Products

Benefits of Modular

Source: Floor Focus

Modular Carpet is Moving from a Niche to a Category for

Commercial Flooring

Commercial Flooring

Easy

Repairs

9

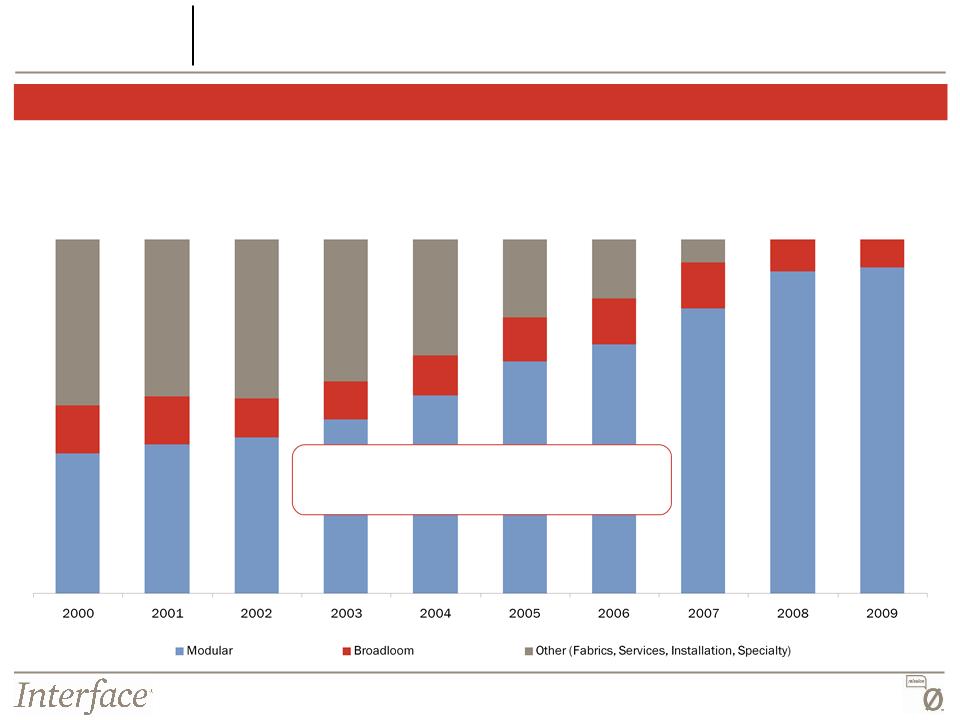

Long-Term Strategy Has Been to Focus on Organic Growth of

Modular Carpet

Modular Carpet

Sales by Business Type

Divested

Raised Access

Flooring

Raised Access

Flooring

Divested

European

Fabrics

European

Fabrics

Divested

N. American

Fabrics

Divested

European

Broadloom

Divested

Installation &

Maintenance

Installation &

Maintenance

Divested

Vinyl

Matting

Divested $500M in Revenue Base and

Replaced with Organic Modular Sales Growth

Secular Shift

40%

92%

10

Functionality and Design Create a Secular Shift in Modular

Carpet From a Niche to a Category

Carpet From a Niche to a Category

§ Preferred interior design element

§ “Becoming the Flooring of Choice”

§ Random products merge design with function

§ Sustainability drives recycled and repurposed

products

products

§ Stressed the functionality of

modular carpet

modular carpet

§ Exploited the benefits of

modular vs. broadloom

modular vs. broadloom

§ Limited application and design

§ Open office plans emerge

Pioneering Stage

Functionality Stage

Secular Shift

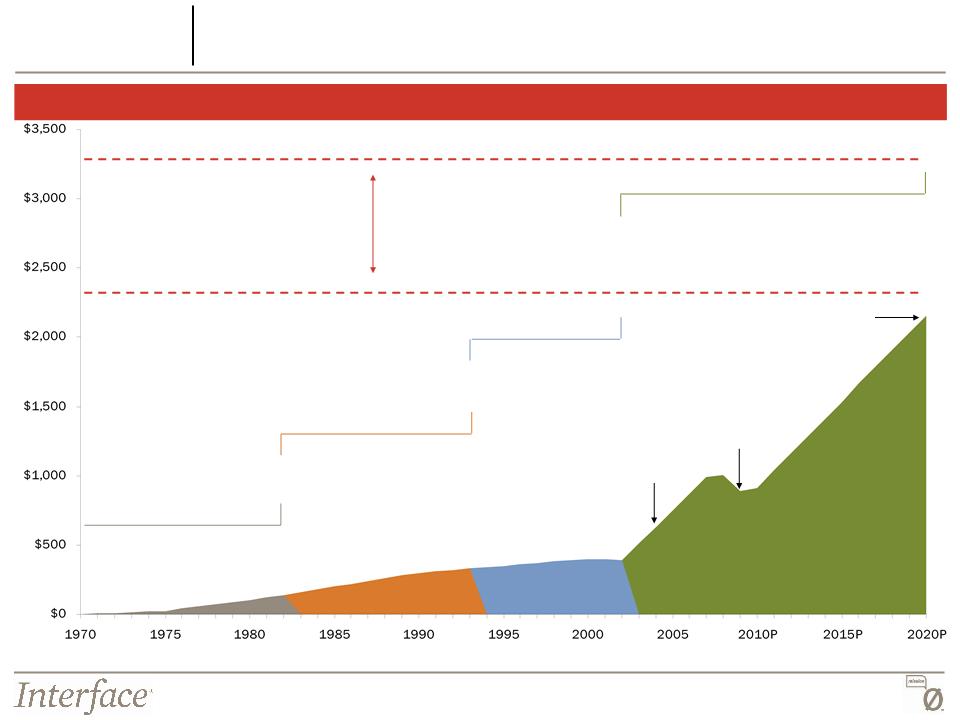

2009 Total U.S. Specified

Commercial Carpet Market = $2.3B

§ Celebrating the square

§ Sustainability introduced

§ Pattern by tile

Liberation of Design

2020P Total U.S. Specified

Commercial Carpet Market = $3.3B

3%

CAGR

CAGR

2009

38% Penetration

2020P

65% Penetration

Carpet Tile Share of U.S. Commercial Carpet Market

($ in millions)

What if modular

carpet reached

65% market share

of the commercial

market by 2020?

carpet reached

65% market share

of the commercial

market by 2020?

2004

26% Penetration

($ in millions)

Source: Invista, Floor Focus, Carpet and Rug Institute, Catalina Research Inc., U.S. Flooring Forecast and management estimates

Secular Shift

11

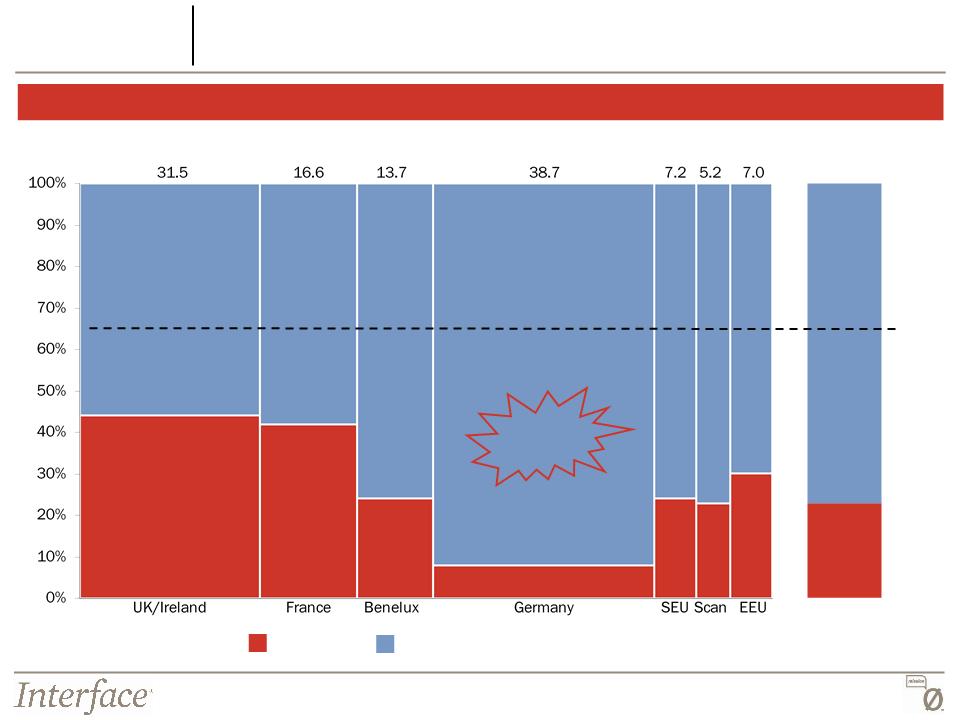

Carpet Tile Penetration of European Contract Soft Flooring Market

European Market Opportunity

(millions of square meters)

(Billions of square meters)

Significant

Opportunity

65%

Penetration

8%

44%

24%

42%

24%

30%

23%

Carpet Tile

Broadloom and Other Soft Flooring

Source: BMW Associates and management estimates

Secular Shift

23%

Total

Europe

12

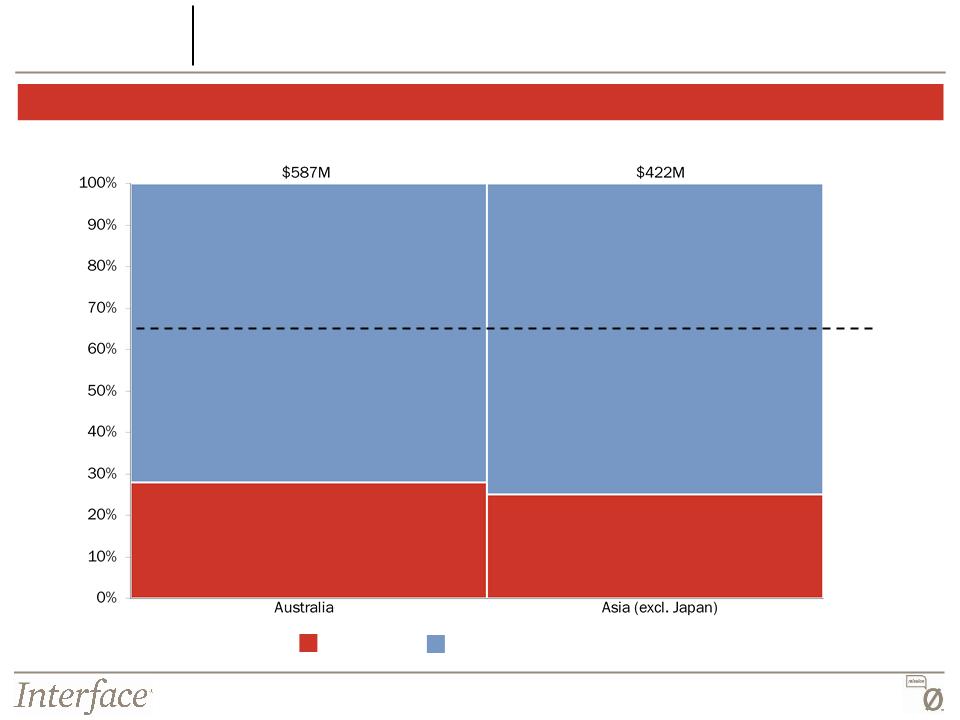

Carpet Tile Penetration of the Asia-Pacific Contract Soft Flooring Market

Asia-Pacific Market Opportunity

(millions of square meters)

28%

($ in millions)

25%

Carpet Tile

Broadloom and Other Soft Flooring

Source: BMW Associates and management estimates

Secular Shift

65%

Penetration

13

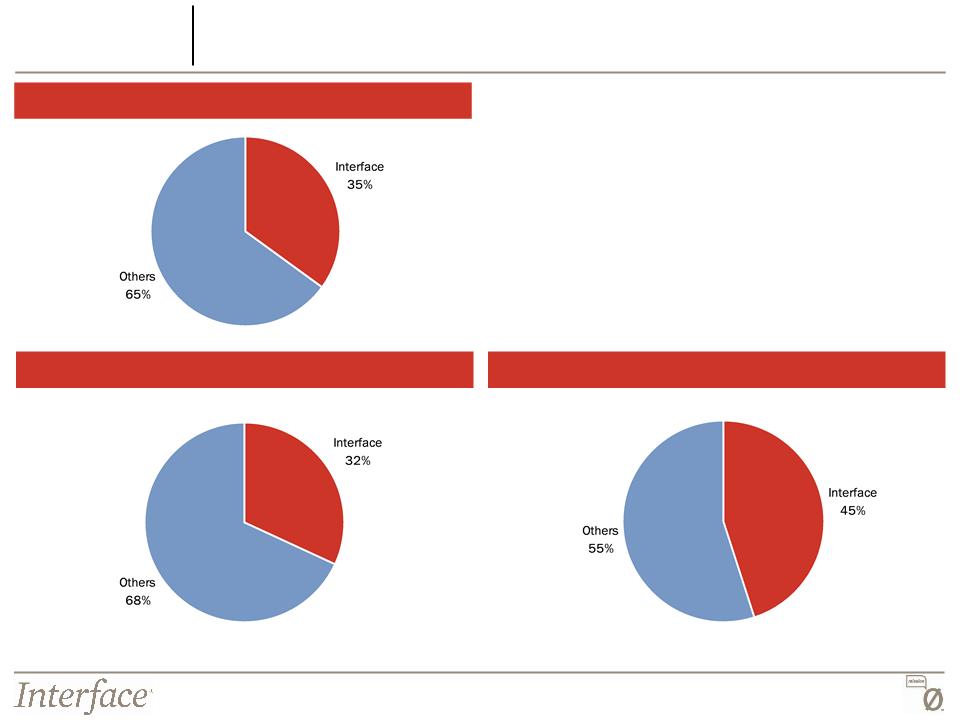

Interface has a Significant Share of the Global Carpet Tile Market

Secular Shift

Americas

Europe & MEAI

Australia/NZ

Source: BMW Associates and management estimates

§ Interface has significant market presence

in key major markets

in key major markets

§ Interface has manufacturing, sales &

marketing support on four continents

marketing support on four continents

14

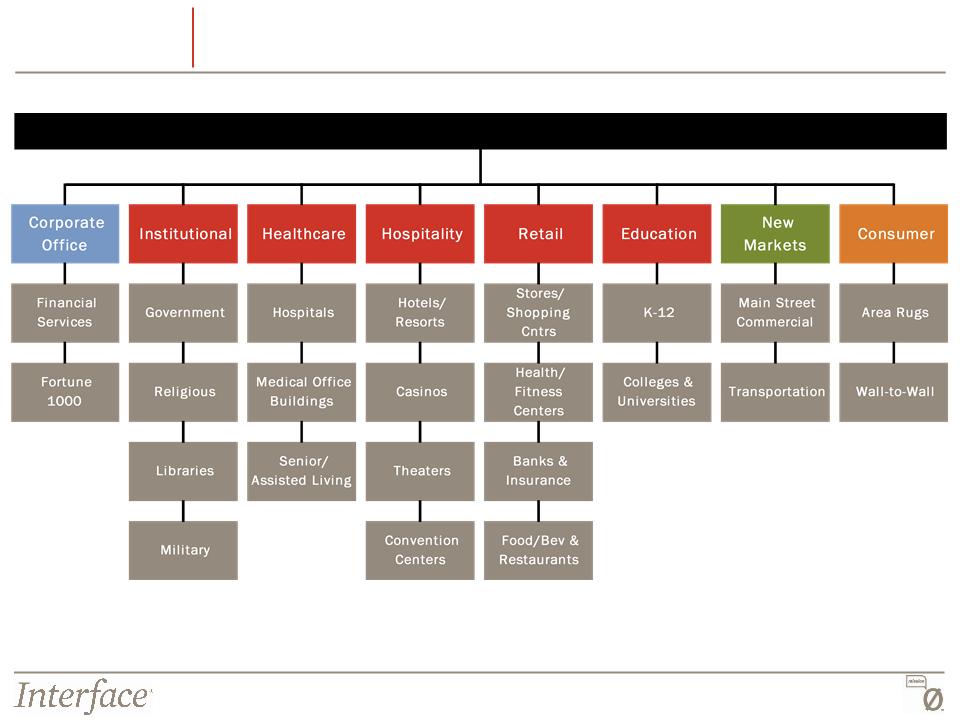

Segmented Market Approach

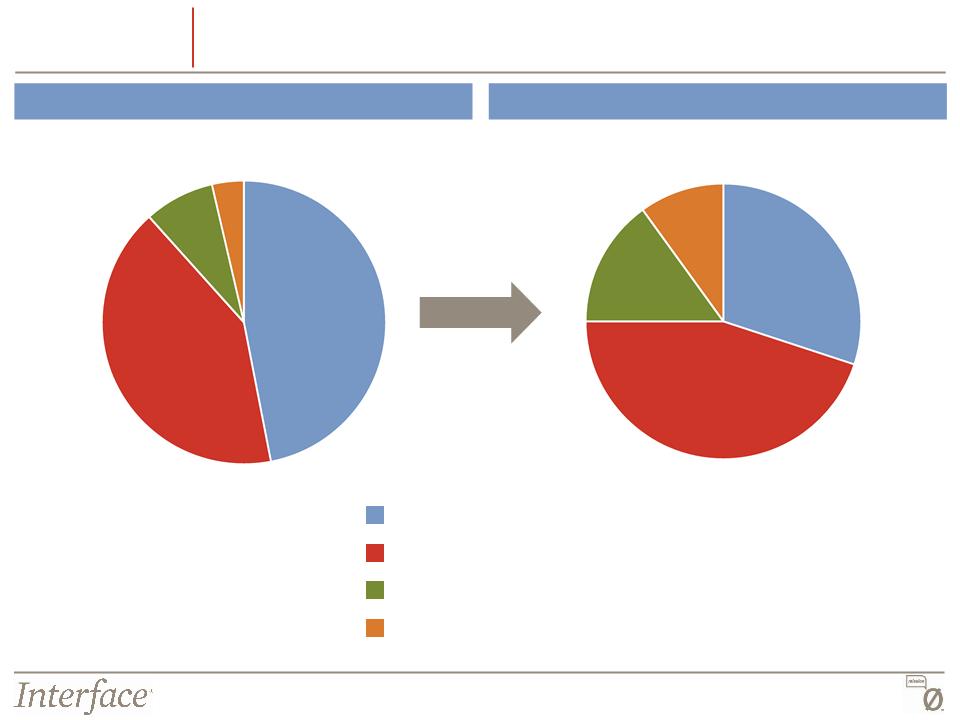

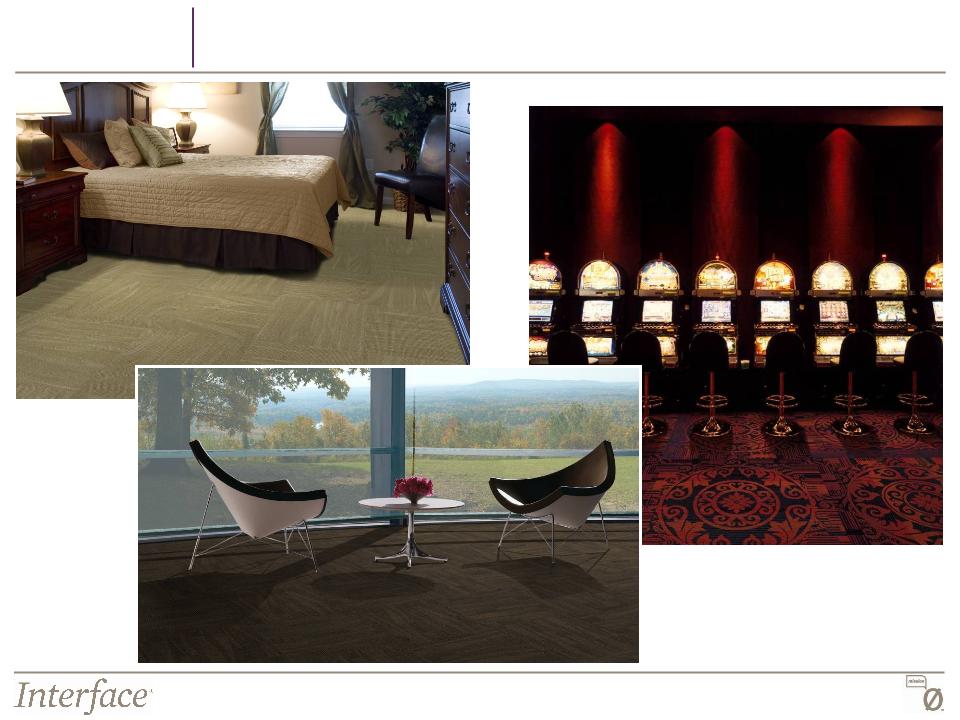

Diversified End Use Markets

Growth

Platforms

15

Diversify End Use Markets

Current Portfolio

Growth

Platforms

Target Portfolio

Mature Office Market

Non-Office Commercial Segments

Emerging Markets

Consumer

16

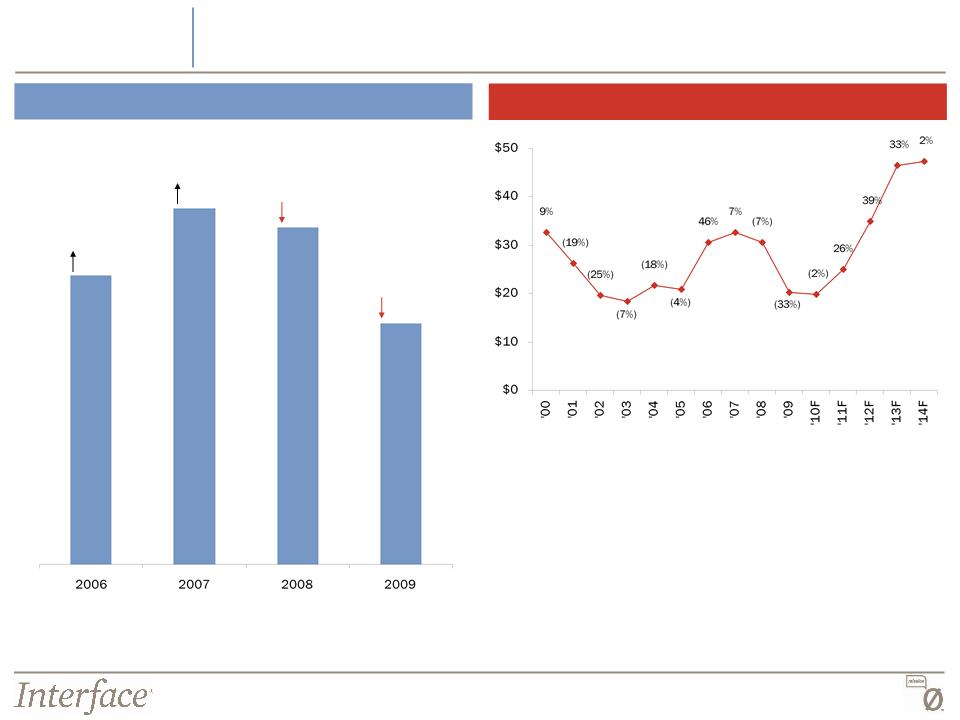

Capture the Rebound in the Corporate Office Segment

Growth

Platforms

Modular Mature Corporate Office Sales

Excludes Latin America, Eastern Europe, Russia, Middle East, Africa, India and NE Asia

23%

28%

18%

5%

U.S. Office Construction Starts

§ U.S. office construction is expected to

remain flat in 2010 and then rebound in

late 2011, returning to 2007 levels by the

end of 2012

remain flat in 2010 and then rebound in

late 2011, returning to 2007 levels by the

end of 2012

($ in Billions)

Source: McGraw-Hill

17

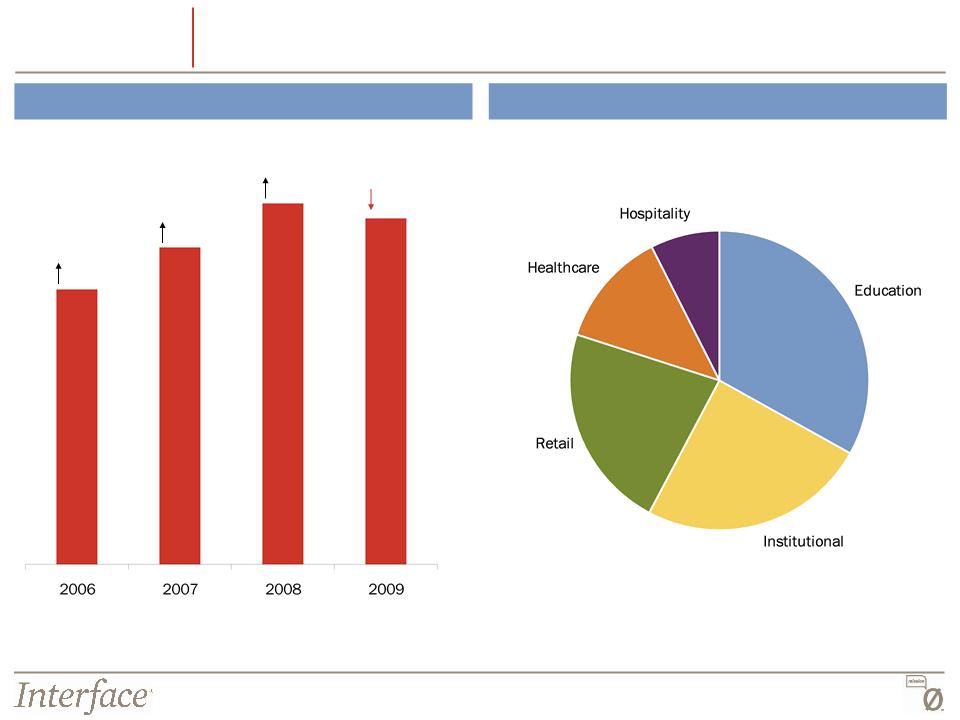

Strong Growth from Non-Corporate Segments

Modular Non-Office Commercial Sales

15%

14%

4%

10%

Non-Office Commercial Sales by Segment

Growth

Platforms

18

New Segment Opportunities - Main Street Commercial

§ Access to secondary Contract and Main

Street commercial markets in smaller rural

and suburban areas

Street commercial markets in smaller rural

and suburban areas

§ Broadened reach in primary markets

beyond specified market

beyond specified market

§ Exploring several strategies to expand

reach and distribution

reach and distribution

Opportunity

Main Street Commercial Market

U.S. Commercial Carpet Market

($ in billions)

Main Street Commercial

Contract Commercial

$3.0B

Growth

Platforms

19

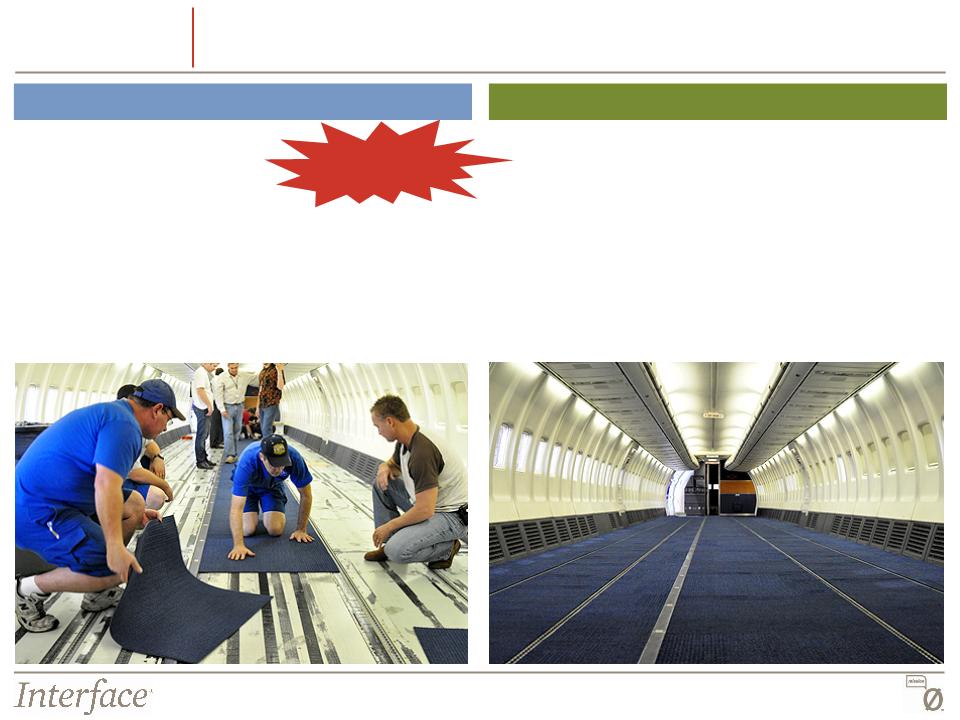

New Segment Opportunities - Transportation

§ Single tile replace-ability

§ Longer Life construction

§ Highest standards of Smoke Toxicity with Nylon

§ Lighter weight than current carpet options

§ Quick replacement - no “out of service” time

required

required

§ Recycled after use by manufacturer

Benefits of Modular for Transportation

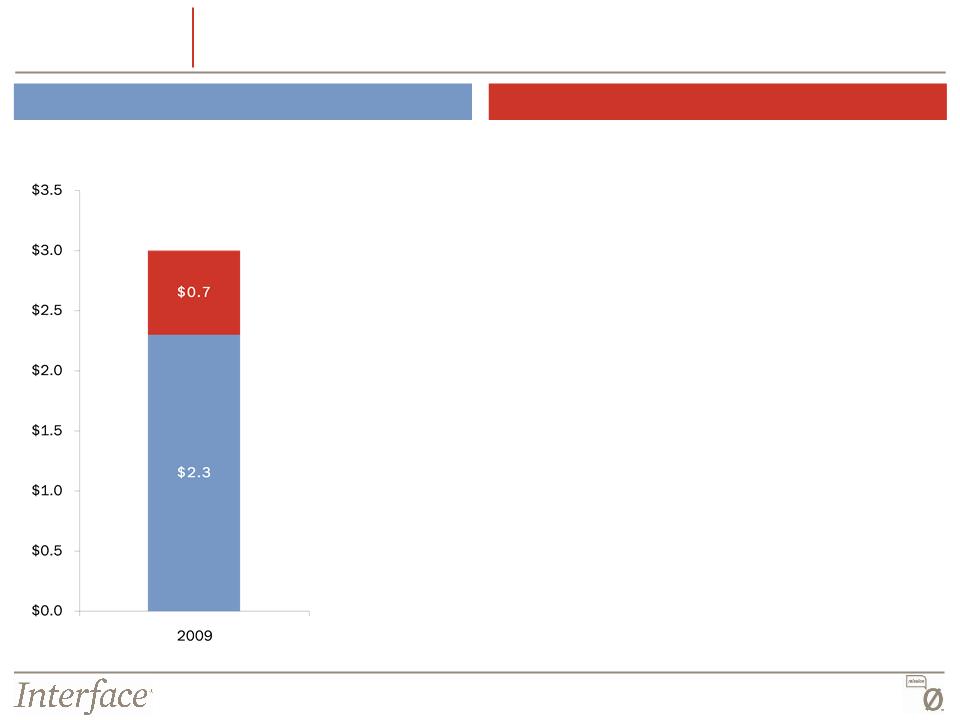

$200M

Airline Opportunity

Southwest Airlines Green Plane

§ Pilot project serving as a test for new

environmentally responsible materials

environmentally responsible materials

§ InterfaceFLOR, in collaboration with Boeing,

designed a carpet tile to meet Federal Aviation

requirements and Southwest’s environmental

expectations

designed a carpet tile to meet Federal Aviation

requirements and Southwest’s environmental

expectations

§ First ever modular carpet product used for the

airline industry

airline industry

Growth

Platforms

20

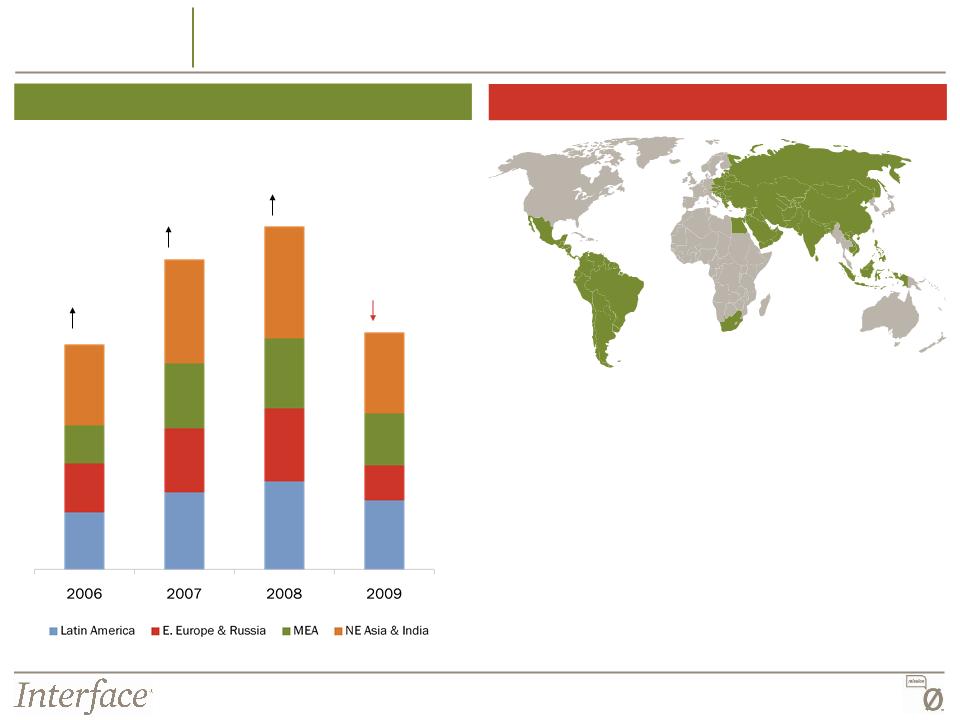

Invest in Emerging Markets

Growth

Platforms

Interface Target Emerging Markets

§ Central America

§ South America

§ Eastern Europe

§ Russia

§ Middle East

§ Africa

§ India

§ China

§ Vietnam

§ Cambodia

§ Singapore

§ Indonesia

§ Philippines

Emerging Market Sales

38%

10%

31%

31%

21

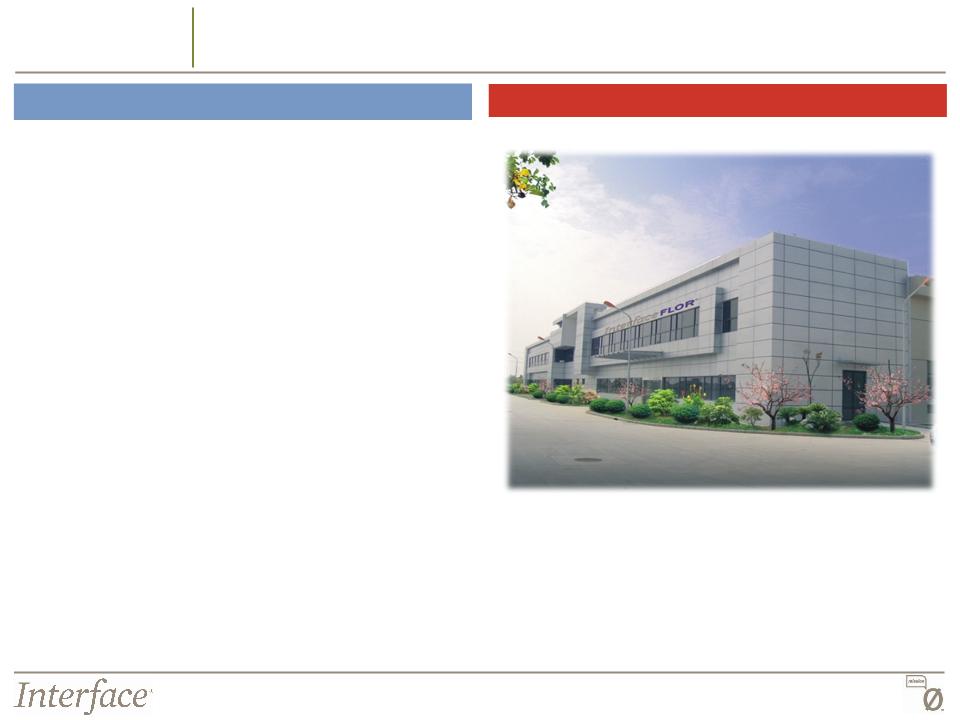

Invest in Emerging Markets: Establishing Local Manufacturing

in High Growth China Market

in High Growth China Market

Growth

Platforms

InterfaceFLOR Taicang Facility

§ Targeting LEED Silver certification for Office and

Customer spaces

Customer spaces

§ Expect to begin production by third quarter 2010

§ Greater access to Local customers -

reduced exposure to Multi-National

Corporations

reduced exposure to Multi-National

Corporations

§ Improved service speed

§ “Made in China”

§ Leading with our strengths

- Design Flexibility & Responsiveness

- Local Sustainability Position

§ Non-office segment opportunities in

Institutional and Hospitality

Institutional and Hospitality

§ Future opportunity to capitalize on

urbanization of population

urbanization of population

Benefits of China Manufacturing Plant

22

FLOR is…

§ A new way to think about floor covering

§ A new kind of customer experience

§ A new way to design for your life

§ A new standard in sustainable residential

design

design

Grow a Consumer Brand: Modular Goes in the Home

Growth

Platforms

23

2010 catalog, online and in-store experiences bring the proposition to life for consumers

Grow a Consumer Brand: FLOR Connects Directly with

Consumers

Consumers

Growth

Platforms

24

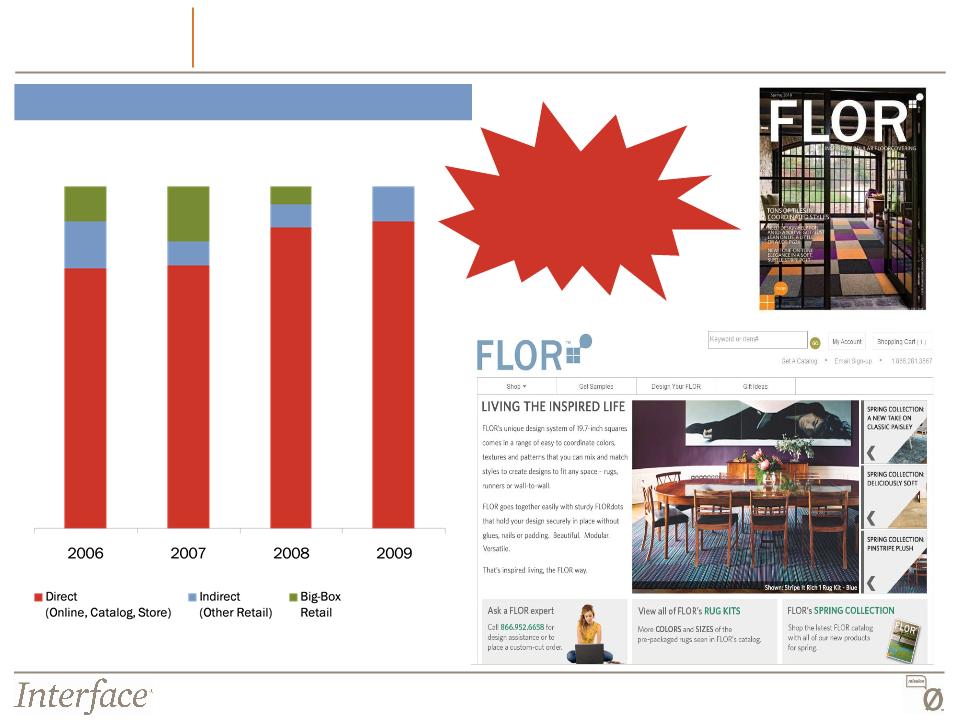

FLOR Sales by Channel

Grow a Consumer Brand: FLOR is Creating a Category:

“Modular Carpet for the Home”

“Modular Carpet for the Home”

% Direct Sales

Percent of Total

Percent of Total

75%

77%

88%

90% of FLOR

sales are

generated Online

and via Catalog

and via Catalog

90%

Growth

Platforms

25

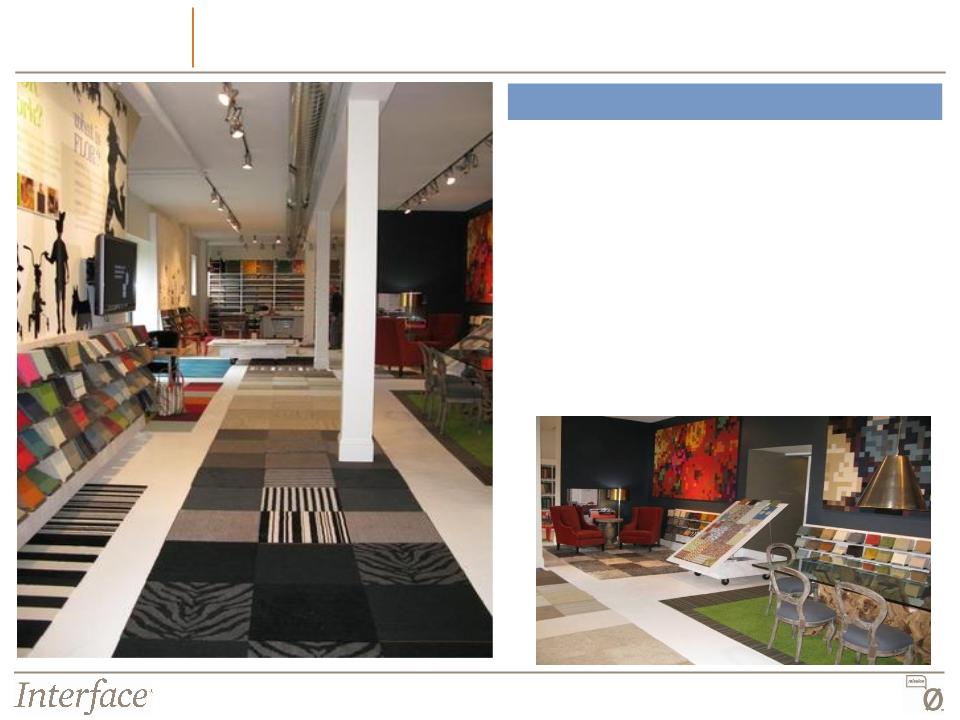

Grow a Consumer Brand: FLOR Store Opened

§ First store opened in Chicago in June 2009

§ Opportunity to interact with the customer about

the modular concept, design and sustainability

the modular concept, design and sustainability

§ 8x10 grid allowing visitors to bring design ideas

to life

to life

§ Exceeded budget in 2009

§ Exploring opportunities for future stores

FLOR Store Highlights

Growth

Platforms

26

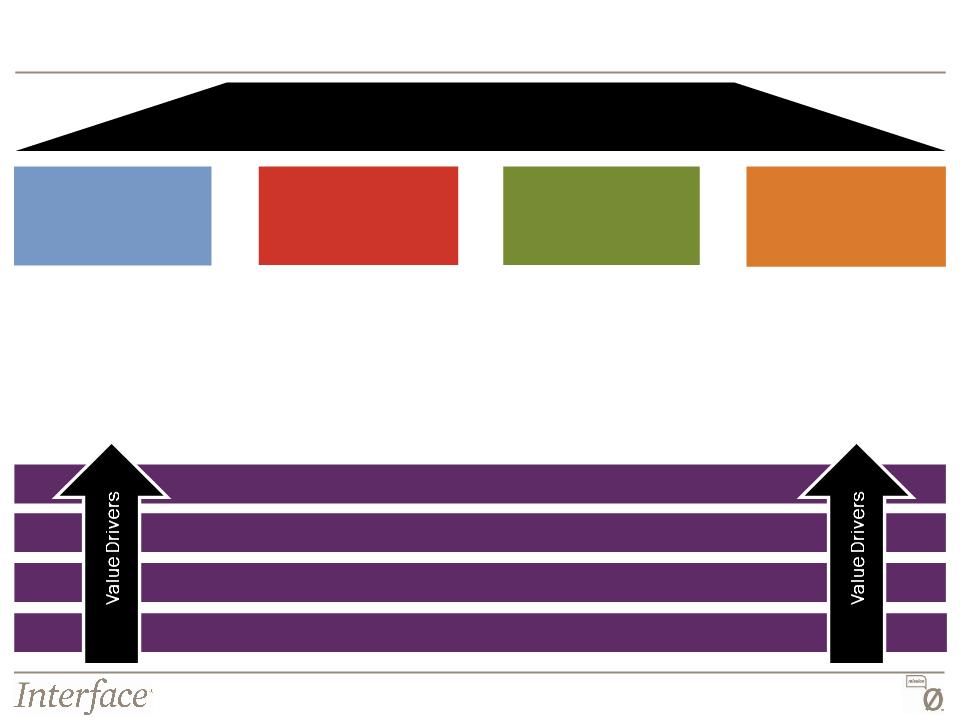

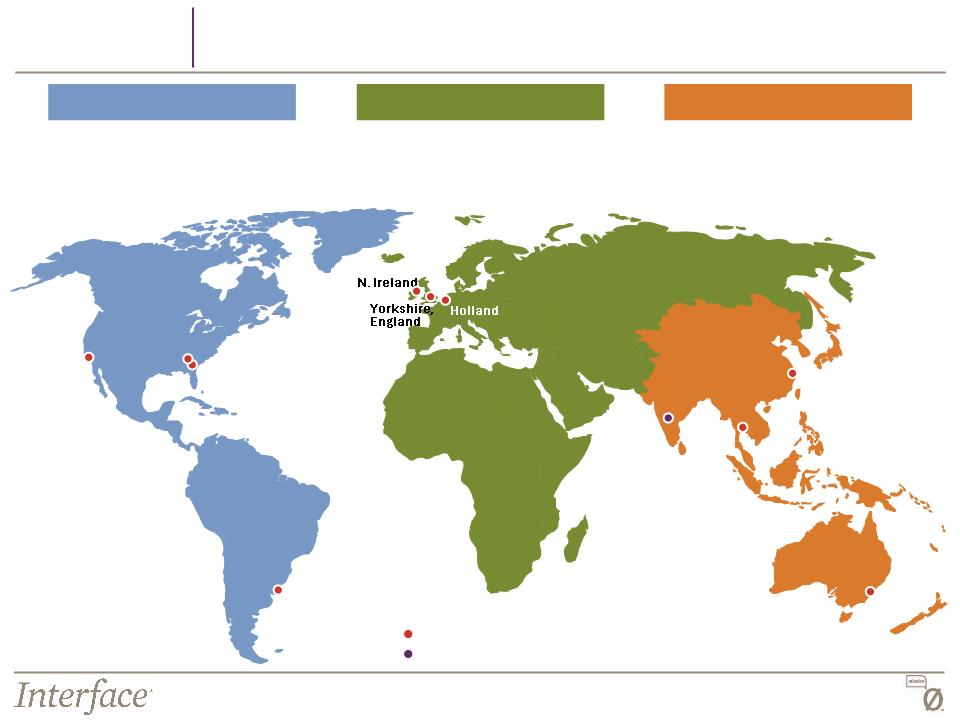

Global Manufacturing Capabilities and Local Distribution

City of

Industry,

California

Bangkok,

Thailand

Thailand

Picton,

Australia

Australia

Current Manufacturing Facility

LaGrange,

Georgia

Georgia

58% of Sales

51% of Production

30% of Sales

34% of Production

12% of Sales

15% of Production

Note: Figures represent FYE 2009

Value Drivers

Shanghai, China

Americas

Europe & MEAI

Asia-Pacific

Future Manufacturing Facility

Uruguay

(commissioned)

India

27

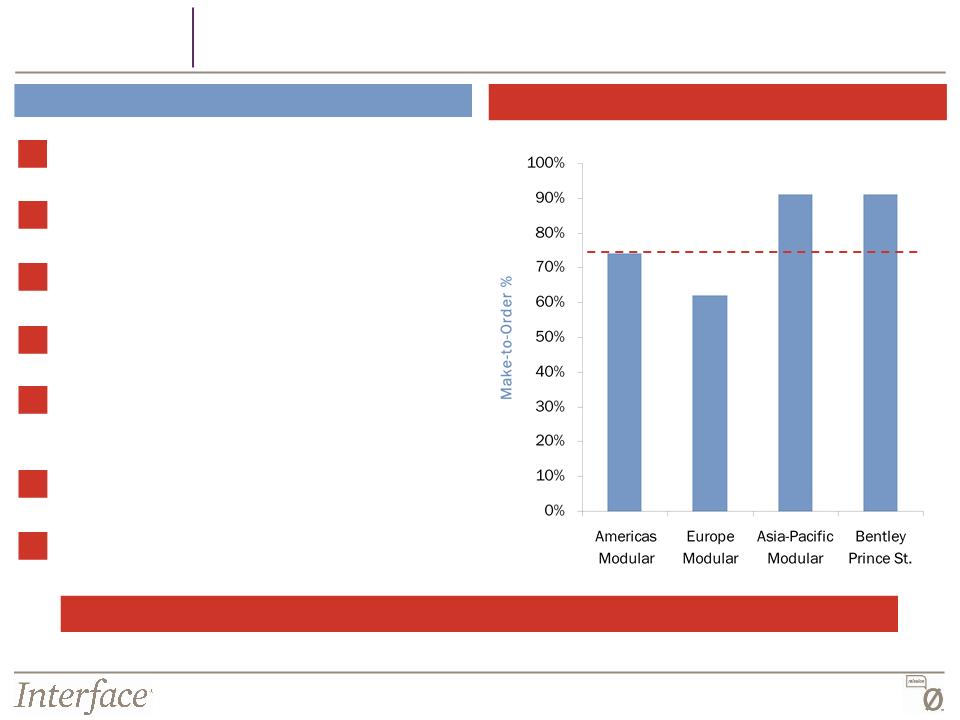

1. Increases speed to market

2. Promotes innovation

3. Offers unique custom product capabilities

4. Supports a constant flow of new products

5. Offers sales force the opportunity to visit the

customer with new products

customer with new products

6. Decreases lead time to customers

7. Increases inventory turns

The Made-to-Order Advantage

Interface Modular Percentage Make-to-Order

Interface is the ONLY company with a “make-to-order” approach to the market

75% TARGET Level

Note: Figures represent FYE 2009

Value Drivers

Strong Competitive Advantage Through Make-to-Order Philosophy

28

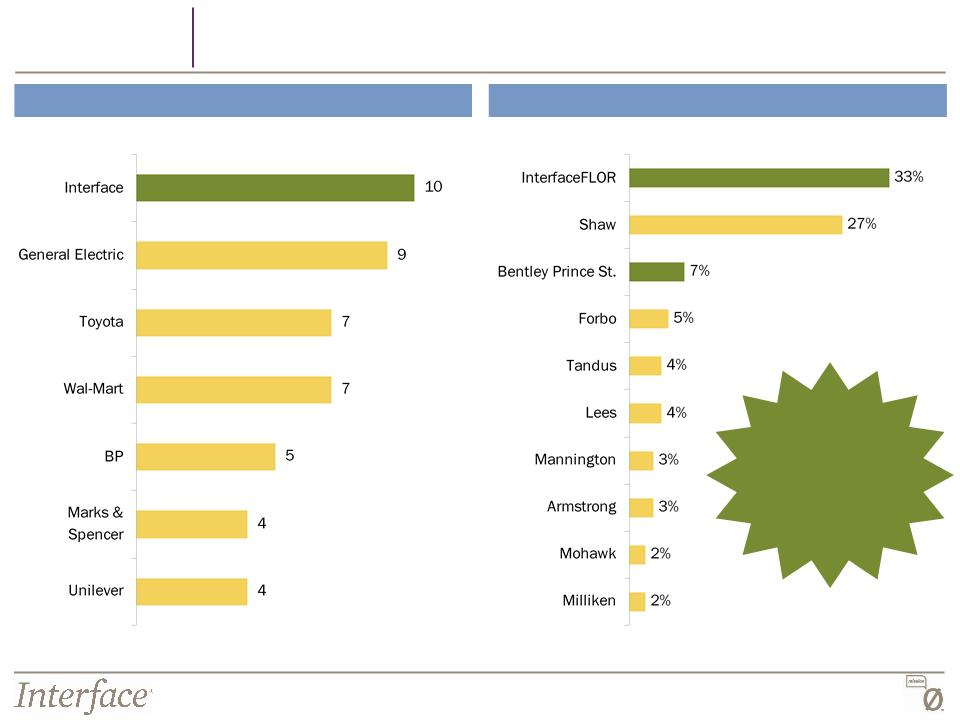

Contract Magazine 2009 Brand Report

Value Drivers

Top Modular Carpet Brands

1. InterfaceFLOR

2. Shaw Contract Group

3. Lees Carpets

4. Milliken

5. Bentley Prince Street

5. Tandus

7. Patcraft Designweave

8. C&A

8. Mannington

10. J&J/Invision

Top-ranked Modular Carpet brands for 2009

Source: Contract Magazine 10th Annual Brand Report

Market Leader in Product Design and Fashion

29

Corporate Office

Value Drivers

30

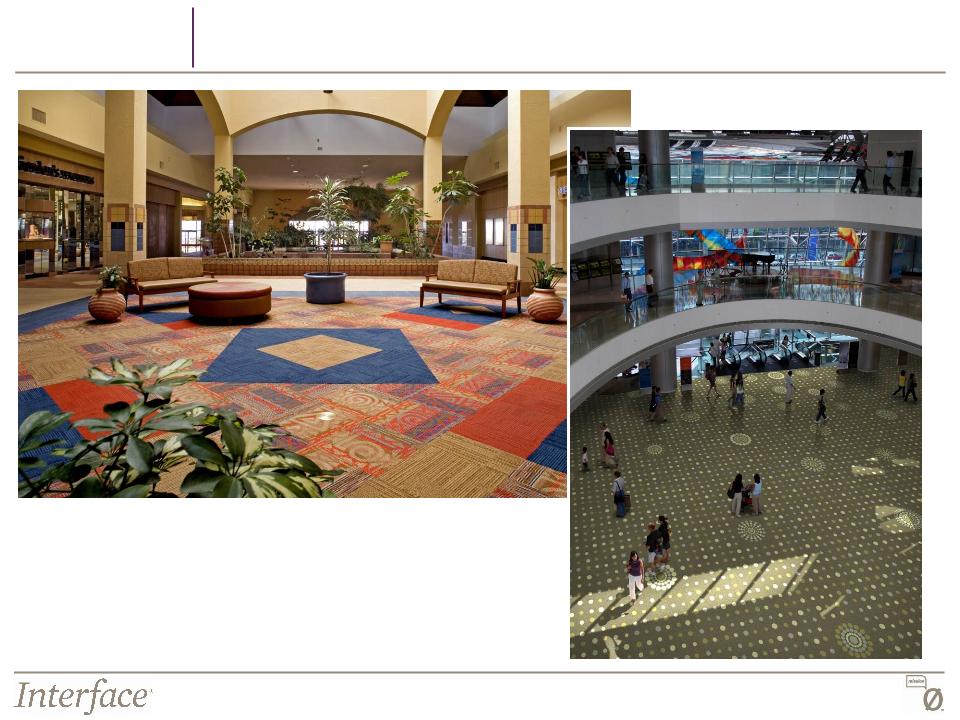

Retail

Value Drivers

31

Colleges & Universities

Value Drivers

32

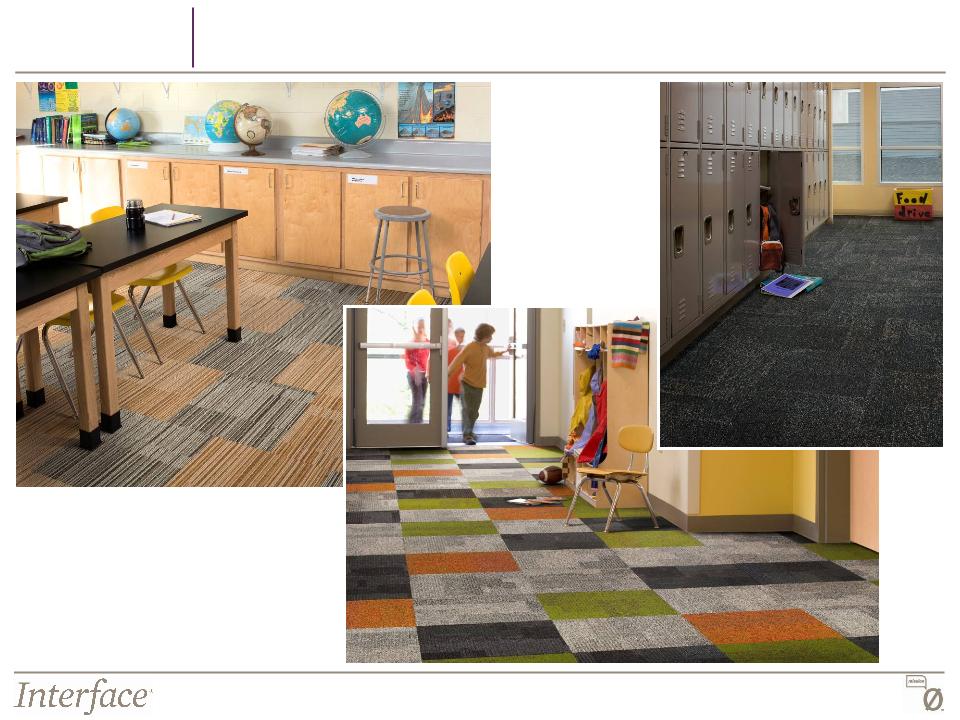

K-12 Education

Value Drivers

33

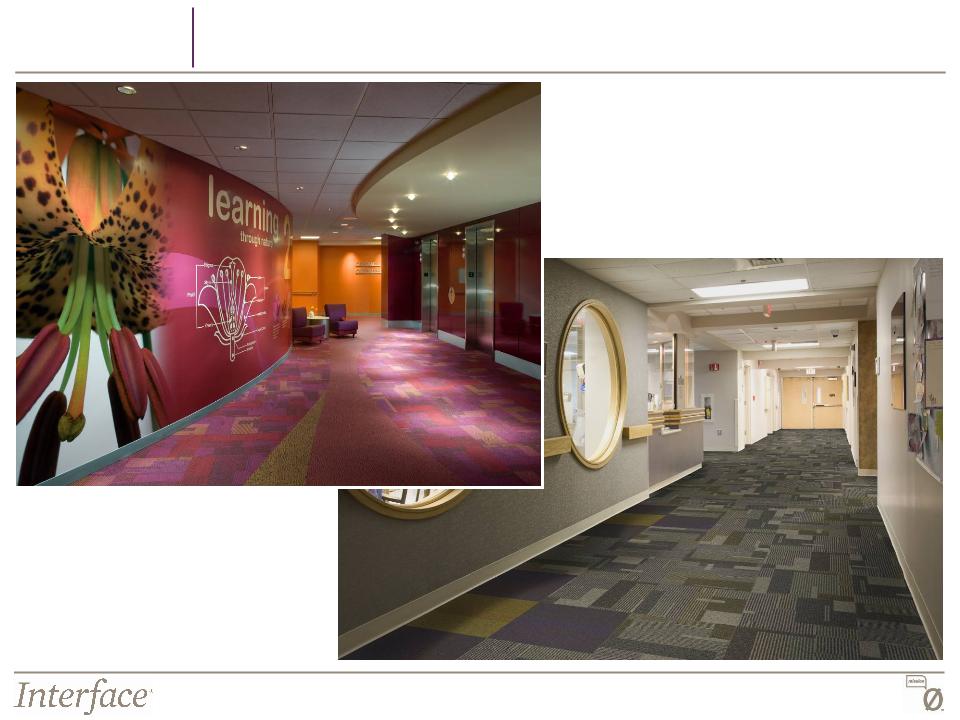

Healthcare

Value Drivers

34

Government & Public Spaces

Value Drivers

35

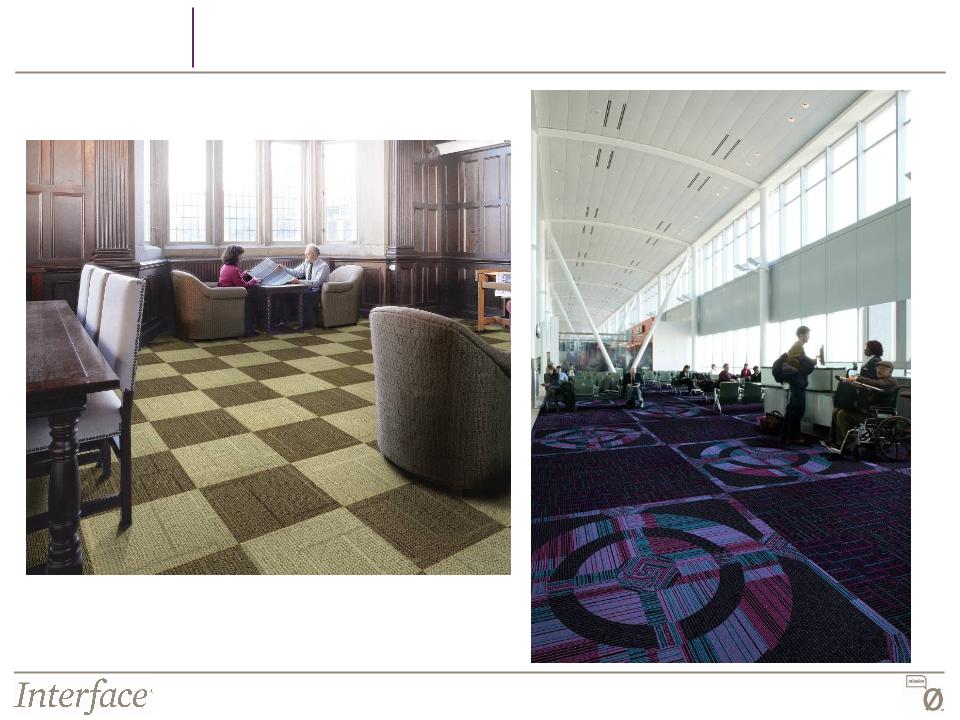

Hospitality

Value Drivers

36

Interface is the Recognized Leader in Sustainability

GlobeScan Corporate Sustainability Leaders 2009

Floor Focus Green Leaders 2009

Unprompted, Combined Mentions 2009

Value Drivers

Source: 2009 Floor Focus Top 250 Design Survey (U.S. Market)

Interface received

“Green Kudos”

for Sustainable

Products with good

Design options and

Closed Loop

Processes

Products with good

Design options and

Closed Loop

Processes

Source: The Sustainability Survey from GlobeScan

37

Sustainability Inspires Innovation

Value Drivers

§ i2 Design Platform - biomimicry inspired

random carpet tile patent

random carpet tile patent

§ TacTiles - - no glue installation

§ Cool Blue - 100% recycled backing process

§ Cool Carpet - climate neutral product

§ ReEntry 2.0 - carpet reclamation and

recycling program

recycling program

§ Convert - - post-consumer recycled content

product platform

product platform

§ Southwest Green Plane - pilot project

testing new environmentally responsible

materials for airplanes

testing new environmentally responsible

materials for airplanes

Sustainability-Focused Innovation

Cool Blue™

Greenbuild 2009

i2 Products

38

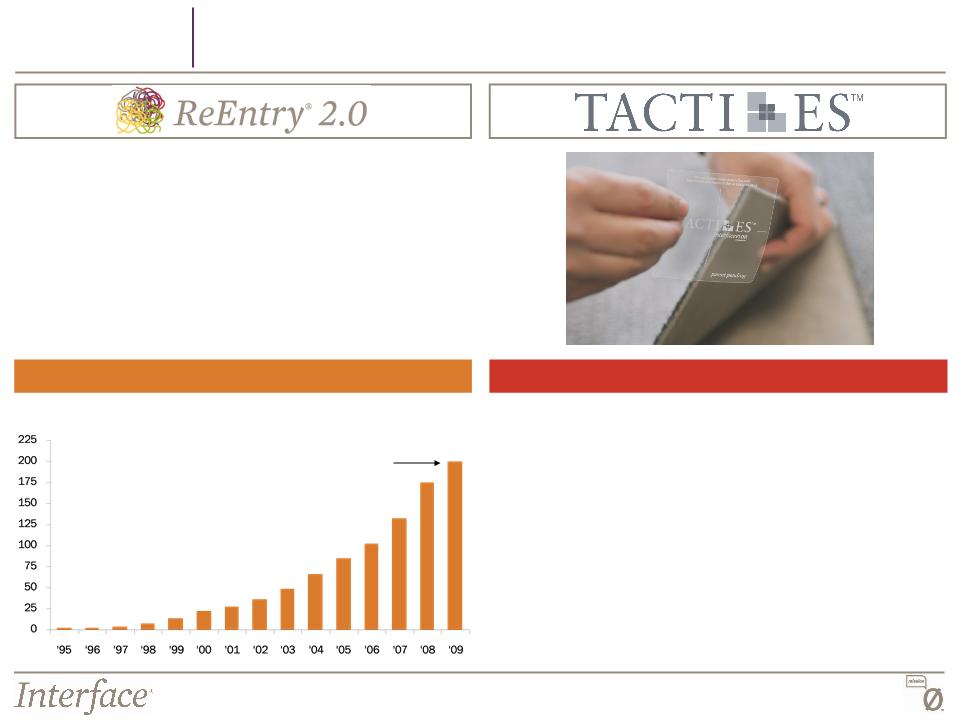

ReEntry 2.0 Brings Convert Product Platform

Value Drivers

§ Reclaiming both Interface and competitor carpet tile

and broadloom, sorting & separating

and broadloom, sorting & separating

§ Access to recycled N6 and N6,6 face fiber, boosting

post consumer recycled content in our products

post consumer recycled content in our products

§ Diverted 200 million pounds of materials from

landfills from 1995-2009

landfills from 1995-2009

ReEntry - - Cumulative Carpet Diverted from Landfill

200m pounds of

carpet diverted

(millions of lbs)

Benefits of TacTiles

§ Patented No Glue / No VOCs installation system

§ 25% of current orders include TacTiles

§ High margin product

§ Leading to other new innovations - Moisture Guard

2.0 moisture vapor barrier

2.0 moisture vapor barrier

§ Integrating TacTiles into Design - designing

installation patterns that drive TacTile demand

installation patterns that drive TacTile demand

Interface, Inc. Financials

40

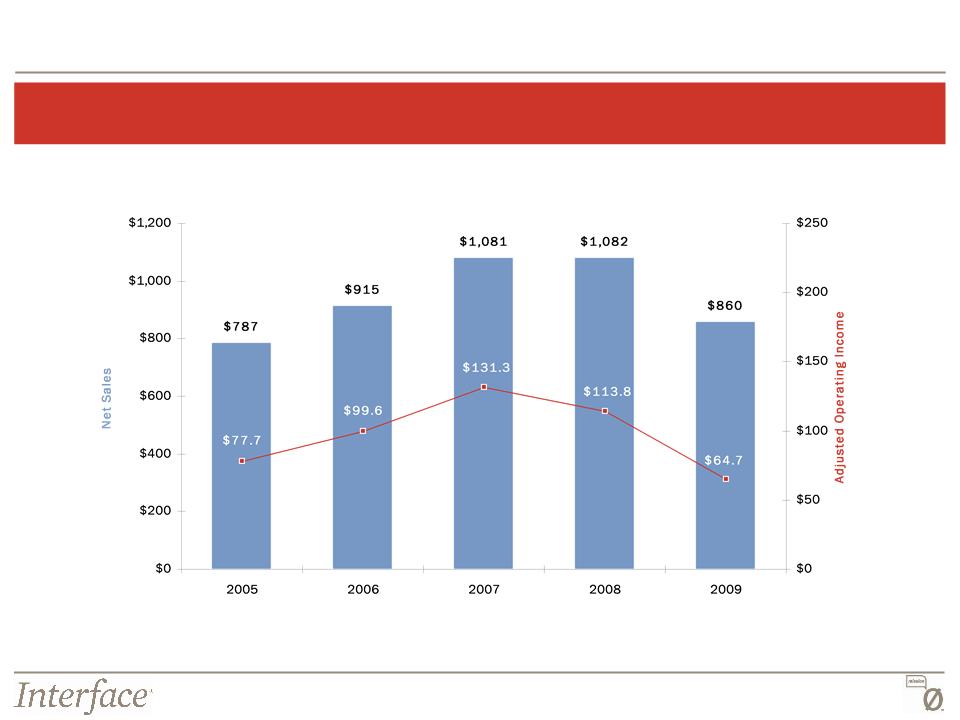

Consolidated Financial Results

Net Sales and Adjusted Operating Income

(Continuing Operations)*

* See the Appendix for a reconciliation of Adjusted Operating Income from Continuing Operations

($ in millions)

41

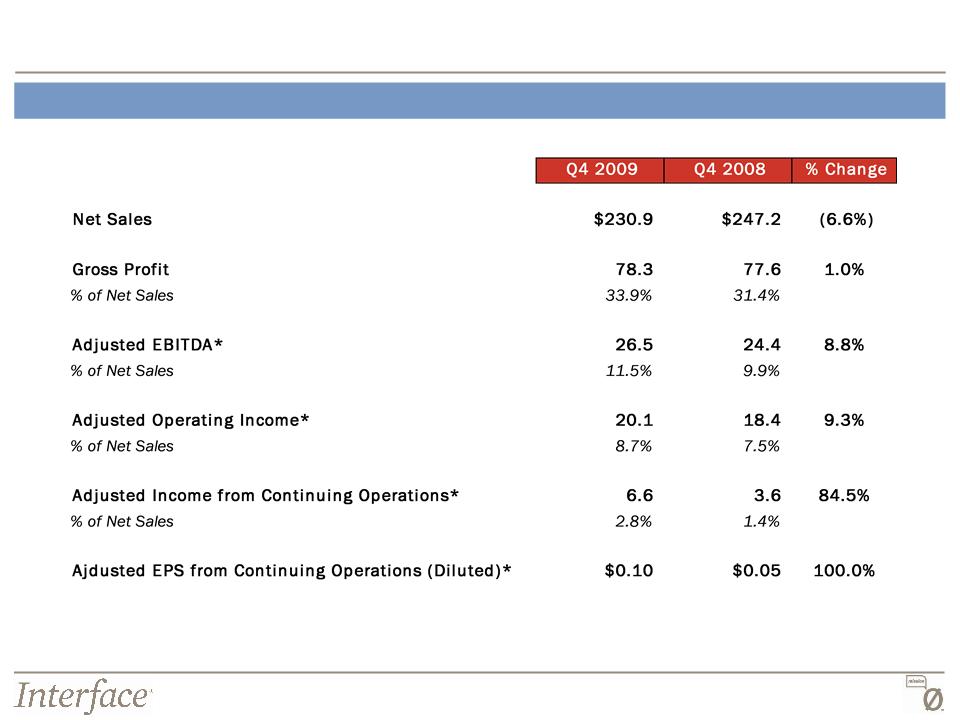

Quarterly Results

Q4 Comparison*

* See the Appendix for a reconciliation of adjusted figures

($ in millions)

42

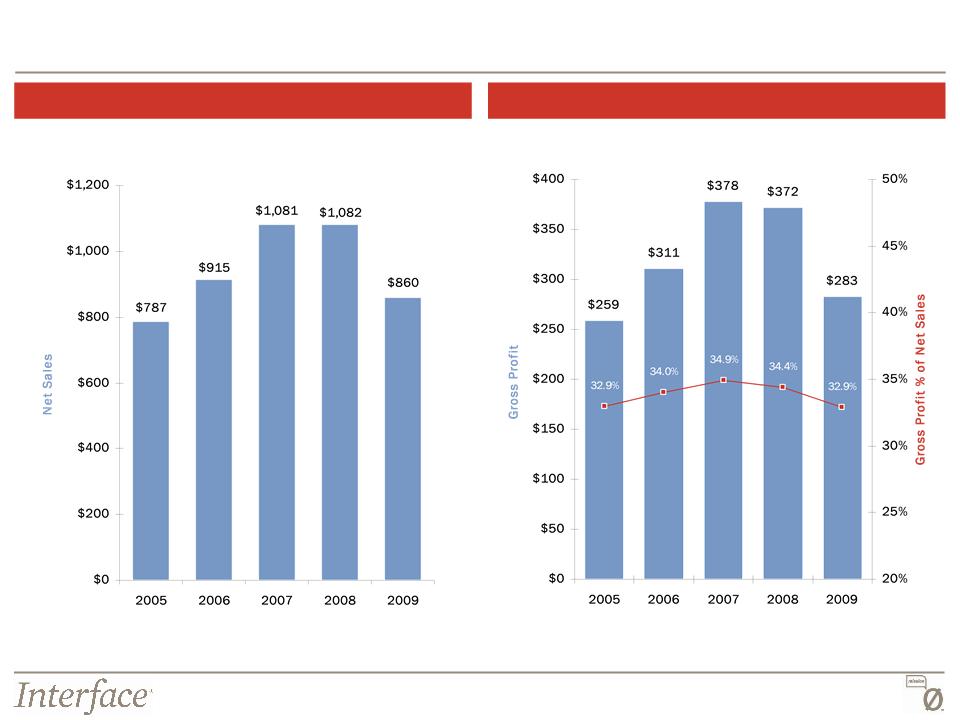

Interface Financial Results from Continuing Operations

Net Sales

Gross Profit

($ in millions)

($ in millions)

43

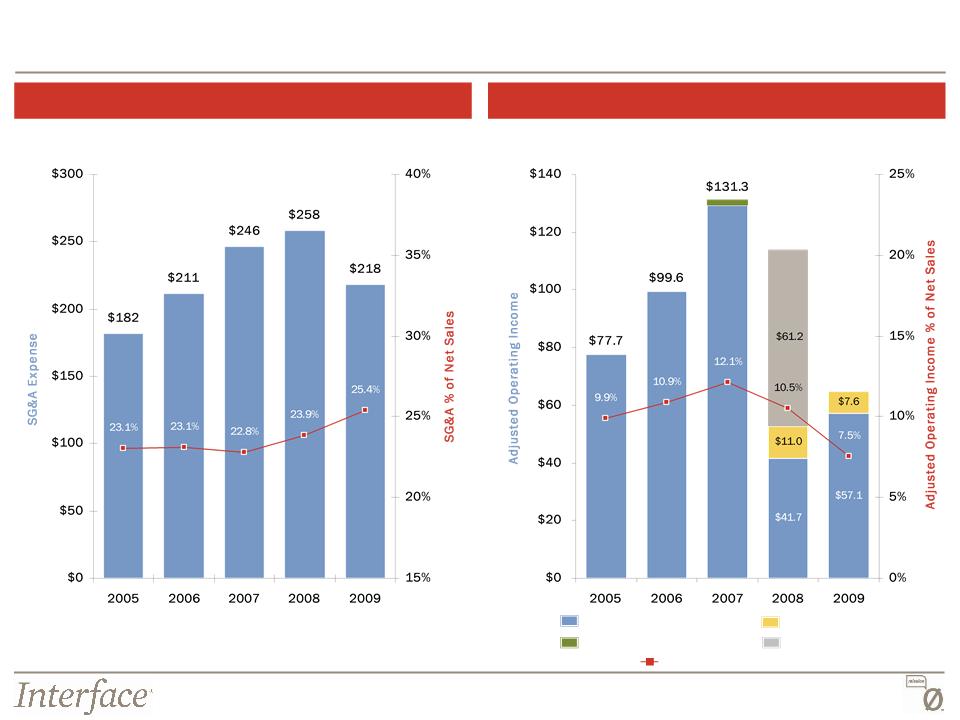

Interface Financial Results from Continuing Operations

SG&A Expense

Adjusted Operating Income*

($ in millions)

($ in millions)

(1) Reported Operating Income of $57.1M in 2009 excludes Income from Litigation Settlements of $5.9M

* See the Appendix for a reconciliation of Adjusted Operating Income

Reported Operating Income

Restructuring Charges

Loss on Disposal ($1.9m)

Operating Income % of Net Sales

Goodwill Impairment

$113.8

$64.7

(1)

44

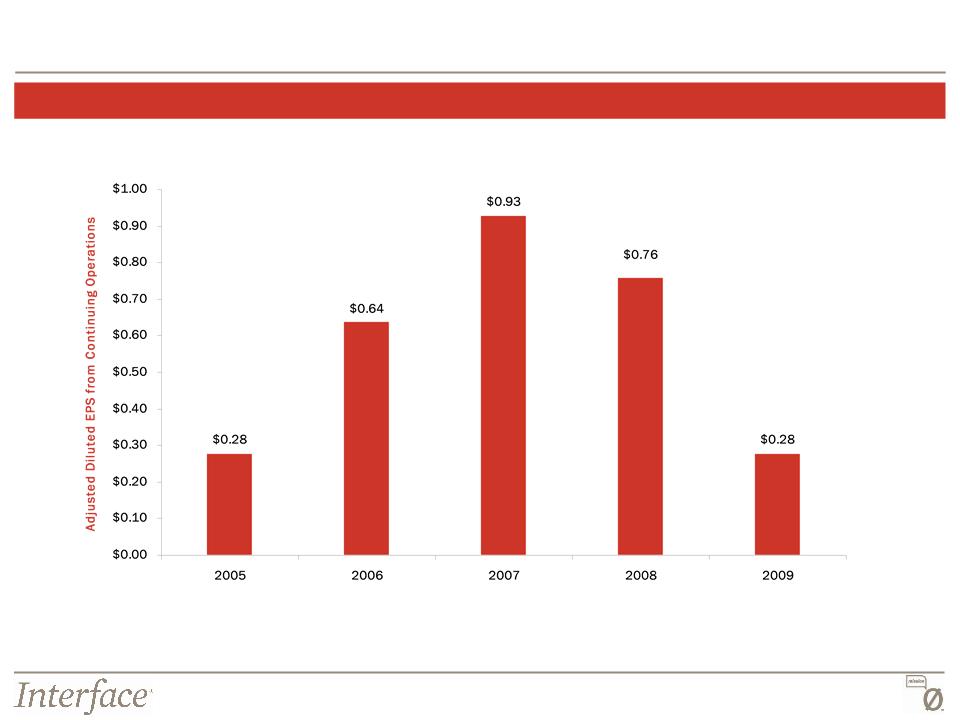

Interface Financial Results from Continuing Operations

Adjusted Diluted Earnings Per Share (Continuing Operations)*

* See the Appendix for a reconciliation of Adjusted Diluted Earnings Per Share from Continuing Operations

45

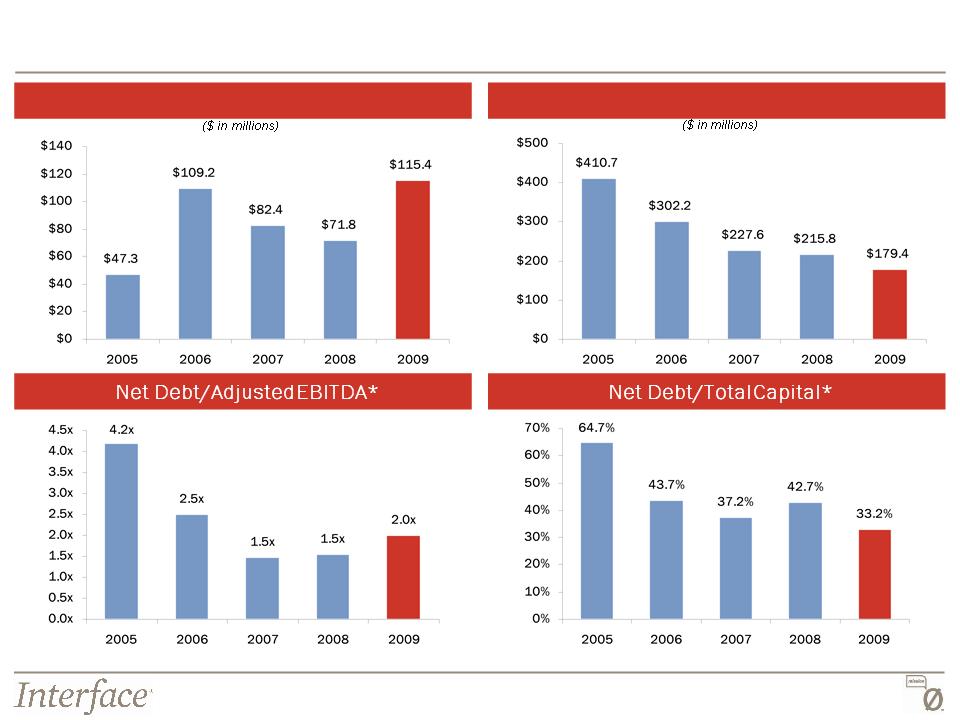

Key Leverage Statistics

Ending Cash Balance

Net Debt*

* See the Appendix for a reconciliation of Net Debt and Adjusted EBITDA

46

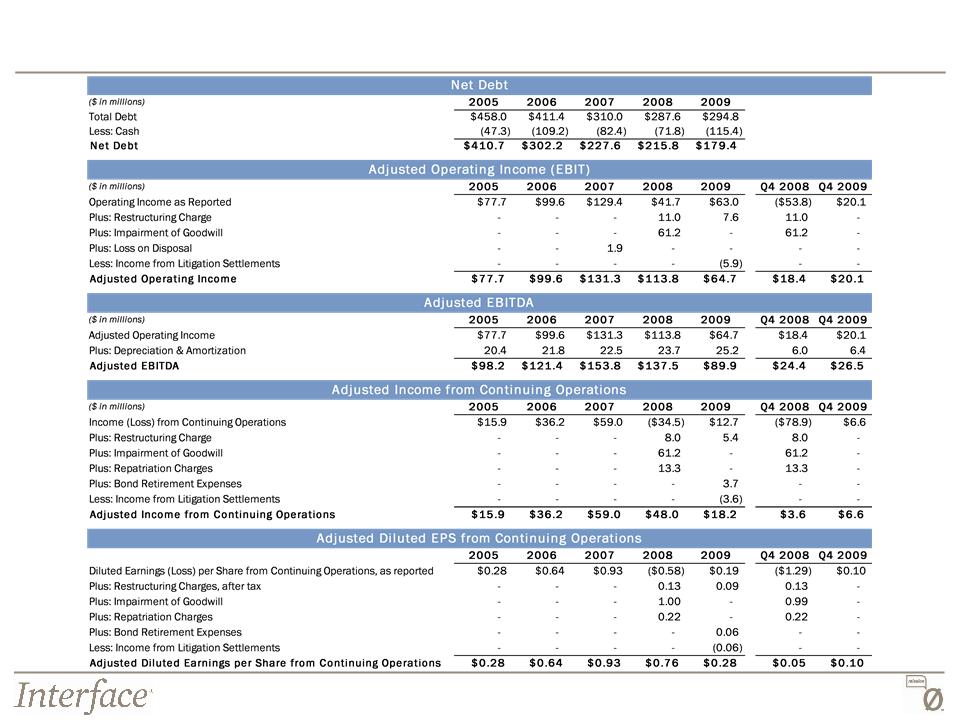

Appendix: Reconciliation of Non-GAAP Financial Measures