Free signup for more

- Track your favorite companies

- Receive email alerts for new filings

- Personalized dashboard of news and more

- Access all data and search results

Filing tables

Filing exhibits

- 8-K/A Current report

- 4.1 First Supplemental Indenture Dated Nov. 17, 2010

- 4.2 Second Supplemental Indenture Dated Nov. 17, 2010

- 99.1 Termination of Split-dollar Agreement Dated Nov. 18, 2010

- 99.2 Press Release Announcing Receipt of Requisite Consents

- 99.3 Press Release Announcing Commencement of Private Debt Offering

- 99.4 Investor Presentation Dated November 2010

TILE similar filings

- 23 Feb 11 Interface Reports Fourth Quarter and Full Year 2010 Results

- 2 Feb 11 Entry into a Material Definitive Agreement

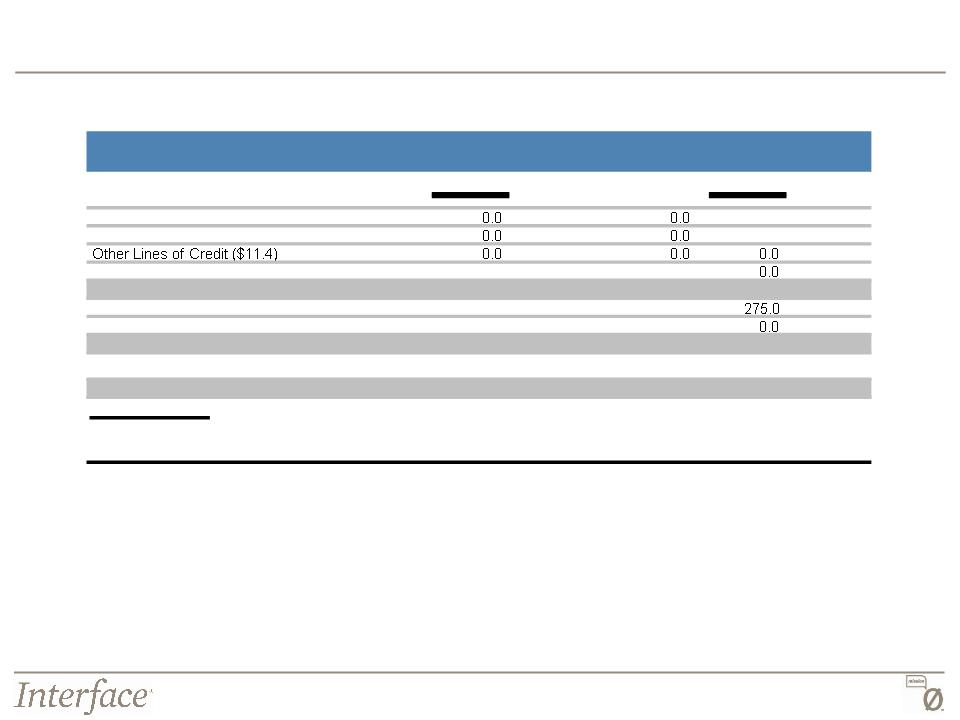

- 7 Dec 10 Interface Announces Closing of $275 Million Senior Notes Offering

- 19 Nov 10 Entry into a Material Definitive Agreement

- 18 Nov 10 Entry into a Material Definitive Agreement

- 9 Nov 10 Interface Commences Tender Offer and Consent Solicitation

- 27 Oct 10 Interface Reports Third Quarter 2010 Results

Filing view

External links