SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

__________________________________

FORM 10-Q

(Mark One)

| þ | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended: September 30, 2008

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from _____________ to ___________

Commission file number 1-8625

READING INTERNATIONAL, INC.

(Exact name of Registrant as specified in its charter)

NEVADA (State or other jurisdiction of incorporation or organization) | 95-3885184 (IRS Employer Identification No.) |

500 Citadel Drive, Suite 300 Commerce CA (Address of principal executive offices) | 90040 (Zip Code) |

Registrant’s telephone number, including area code: (213) 235-2240

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding twelve months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one): Large accelerated filer ¨ Accelerated filer þ Non-accelerated filer ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No þ

Indicate the number of shares outstanding of each of the issuer’s classes of common stock, as of the latest practicable date. As of November 5, 2008, there were 20,987,115 shares of Class A Nonvoting Common Stock, $0.01 par value per share and 1,495,490 shares of Class B Voting Common Stock, $0.01 par value per share outstanding.

READING INTERNATIONAL, INC. AND SUBSIDIARIES

TABLE OF CONTENTS

Page

PART I – Financial Information

Item 1 – Financial Statements

Reading International, Inc. and Subsidiaries

Consolidated Balance Sheets (Unaudited)

(U.S. dollars in thousands)

September 30, 2008 | December 31, 2007 | |||||||

| ASSETS | ||||||||

| Current Assets: | ||||||||

| Cash and cash equivalents | $ | 25,119 | $ | 20,783 | ||||

| Receivables | 7,220 | 5,670 | ||||||

| Inventory | 695 | 654 | ||||||

| Investment in marketable securities | 4,085 | 4,533 | ||||||

| Restricted cash | -- | 59 | ||||||

| Assets held for sale | 22,775 | 25,942 | ||||||

| Prepaid and other current assets | 2,334 | 3,799 | ||||||

| Total current assets | 62,228 | 61,440 | ||||||

| Land held for sale | -- | 1,984 | ||||||

| Property held for development | 7,304 | 9,289 | ||||||

| Property under development | 69,387 | 66,787 | ||||||

| Property & equipment, net | 179,789 | 154,011 | ||||||

| Investments in unconsolidated joint ventures and entities | 13,603 | 15,480 | ||||||

| Investment in Reading International Trust I | 1,547 | 1,547 | ||||||

| Goodwill | 23,808 | 19,100 | ||||||

| Intangible assets, net | 23,999 | 8,448 | ||||||

| Other assets | 10,483 | 7,985 | ||||||

| Total assets | $ | 392,148 | $ | 346,071 | ||||

| LIABILITIES AND STOCKHOLDERS' EQUITY | ||||||||

| Current Liabilities: | ||||||||

| Accounts payable and accrued liabilities | $ | 11,634 | $ | 12,331 | ||||

| Film rent payable | 4,326 | 3,275 | ||||||

| Notes payable – current portion | 1,533 | 395 | ||||||

| Note payable to related party – current portion | -- | 5,000 | ||||||

| Taxes payable | 6,115 | 4,770 | ||||||

| Deferred current revenue | 3,130 | 3,214 | ||||||

| Liabilities of assets held for sale | -- | -- | ||||||

| Other current liabilities | 202 | 169 | ||||||

| Total current liabilities | 26,940 | 29,154 | ||||||

| Notes payable – long-term portion | 173,774 | 111,253 | ||||||

| Notes payable to related party – long-term portion | 14,000 | 9,000 | ||||||

| Subordinated debt | 51,547 | 51,547 | ||||||

| Noncurrent tax liabilities | 6,070 | 5,418 | ||||||

| Deferred non-current revenue | 609 | 566 | ||||||

| Other liabilities | 17,654 | 14,936 | ||||||

| Total liabilities | 290,594 | 221,874 | ||||||

| Commitments and contingencies (Note 13) | ||||||||

| Minority interest in consolidated affiliates | 2,288 | 2,835 | ||||||

| Stockholders’ equity: | ||||||||

| Class A Nonvoting Common Stock, par value $0.01, 100,000,000 shares authorized, 35,564,339 issued and 20,987,115 outstanding at September 30, 2008 and at December 31, 2007 | 216 | 216 | ||||||

| Class B Voting Common Stock, par value $0.01, 20,000,000 shares authorized and 1,495,490 issued and outstanding at September 30, 2008 and at December 31, 2007 | 15 | 15 | ||||||

| Nonvoting Preferred Stock, par value $0.01, 12,000 shares authorized and no outstanding shares | -- | -- | ||||||

| Additional paid-in capital | 132,838 | 131,930 | ||||||

| Accumulated deficit | (54,676 | ) | (52,670 | ) | ||||

| Treasury shares | (4,306 | ) | (4,306 | ) | ||||

| Accumulated other comprehensive income | 25,179 | 46,177 | ||||||

| Total stockholders’ equity | 99,266 | 121,362 | ||||||

| Total liabilities and stockholders’ equity | $ | 392,148 | $ | 346,071 | ||||

See accompanying notes to consolidated financial statements.

Reading International, Inc. and Subsidiaries

Consolidated Statements of Operations (Unaudited)

(U.S. dollars in thousands, except per share amounts)

Three Months Ended September 30, | Nine Months Ended September 30, | |||||||||||||||

| 2008 | 2007 | 2008 | 2007 | |||||||||||||

| Revenue | ||||||||||||||||

| Cinema | $ | 52,909 | $ | 28,009 | $ | 135,693 | $ | 76,825 | ||||||||

| Real estate | 3,619 | 3,068 | 11,779 | 10,124 | ||||||||||||

| 56,528 | 31,077 | 147,472 | 86,949 | |||||||||||||

| Operating expense | ||||||||||||||||

| Cinema | 41,765 | 20,041 | 109,597 | 56,878 | ||||||||||||

| Real estate | 2,253 | 2,044 | 6,139 | 5,462 | ||||||||||||

| Depreciation and amortization | 4,877 | 2,647 | 13,829 | 7,970 | ||||||||||||

| General and administrative | 4,397 | 3,871 | 13,993 | 11,424 | ||||||||||||

| 53,292 | 28,603 | 143,558 | 81,734 | |||||||||||||

| Operating income | 3,236 | 2,474 | 3,914 | 5,215 | ||||||||||||

| Interest income | 221 | 329 | 829 | 558 | ||||||||||||

| Interest expense | (4,183 | ) | (2,606 | ) | (10,661 | ) | (6,536 | ) | ||||||||

| Loss on sale of assets | -- | -- | -- | (185 | ) | |||||||||||

| Other income | (1,009 | ) | 707 | 2,033 | 435 | |||||||||||

| Income (loss) before minority interest expense, discontinued operations, income tax expense, and equity earnings of unconsolidated joint ventures and entities | (1,735 | ) | 904 | (3,885 | ) | (513 | ) | |||||||||

| Minority interest expense | (85 | ) | (162 | ) | (246 | ) | (657 | ) | ||||||||

| Income (loss) before discontinued operations, income tax expense, and equity earnings of unconsolidated joint ventures and entities | (1,820 | ) | 742 | (4,131 | ) | (1,170 | ) | |||||||||

| Gain on sale of a discontinued operation, net of tax | -- | -- | -- | 1,912 | ||||||||||||

| Income (loss) from discontinued operations, net of tax | 178 | 45 | 371 | (67 | ) | |||||||||||

| Income (loss) before income tax expense and equity earnings of unconsolidated joint ventures and entities | (1,642 | ) | 787 | (3,760 | ) | 675 | ||||||||||

| Income tax expense | (689 | ) | (501 | ) | (1,513 | ) | (1,443 | ) | ||||||||

| Income (loss) before equity earnings of unconsolidated joint ventures and entities | (2,331 | ) | 286 | (5,273 | ) | (768 | ) | |||||||||

| Equity earnings of unconsolidated joint ventures and entities | 270 | 584 | 817 | 2,626 | ||||||||||||

| Gain on sale of unconsolidated entity | -- | -- | 2,450 | -- | ||||||||||||

| Net income (loss) | $ | (2,061 | ) | $ | 870 | $ | (2,006 | ) | $ | 1,858 | ||||||

| Earnings (loss) per common share – basic and diluted: | ||||||||||||||||

Earnings (loss) from continuing operations | $ | (0.10 | ) | $ | 0.04 | $ | (0.11 | ) | $ | 0.00 | ||||||

Earnings from discontinued operations | 0.01 | 0.00 | 0.02 | 0.08 | ||||||||||||

| Basic and diluted earnings (loss) per share | $ | (0.09 | ) | $ | 0.04 | $ | (0.09 | ) | $ | 0.08 | ||||||

| Weighted average number of shares outstanding – basic | 22,476,904 | 22,487,943 | 22,476,514 | 22,486,395 | ||||||||||||

| Weighted average number of shares outstanding – dilutive | 22,476,904 | 22,761,270 | 22,476,514 | 22,759,723 | ||||||||||||

See accompanying notes to consolidated financial statements.

Reading International, Inc. and Subsidiaries

Consolidated Statements of Cash Flows (Unaudited)

(U.S. dollars in thousands)

| Nine Months Ended | ||||||||

| September 30, | ||||||||

| 2008 | 2007 | |||||||

| Operating Activities | ||||||||

| Net income (loss) | $ | (2,006 | ) | $ | 1,858 | |||

| Adjustments to reconcile net income (loss) to net cash provided by operating activities: | ||||||||

| Gain recognized on foreign currency transactions | (446 | ) | (132 | ) | ||||

| Equity earnings of unconsolidated joint ventures and entities | (817 | ) | (2,626 | ) | ||||

| Distributions of earnings from unconsolidated joint ventures and entities | 731 | 4,693 | ||||||

| (Gain) loss on marketable securities | 1 | (773 | ) | |||||

| Gain on sale of an unconsolidated entity | (2,450 | ) | -- | |||||

| Gain on sale of a discontinued operation | -- | (1,912 | ) | |||||

| Loss on sale of assets | -- | 185 | ||||||

| Loss on extinguishment of debt | -- | 98 | ||||||

| Loss related to impairment of assets | 1,049 | -- | ||||||

| Gain on insurance settlement | (910 | ) | -- | |||||

| Depreciation and amortization | 14,511 | 8,933 | ||||||

| Amortization of prior service costs | 214 | 177 | ||||||

| Amortization of above and below market leases | 638 | -- | ||||||

| Stock based compensation expense | 908 | 775 | ||||||

| Minority interest | 246 | 657 | ||||||

| Changes in operating assets and liabilities: | ||||||||

| (Increase) decrease in receivables | (1,908 | ) | 2,510 | |||||

| (Increase) decrease in prepaid and other assets | 159 | (34 | ) | |||||

| Increase (decrease) in accounts payable and accrued expenses | 1,729 | (1,023 | ) | |||||

| Increase (decrease) in film rent payable | 1,225 | (1,428 | ) | |||||

| Increase in deferred revenues and other liabilities | 2,978 | 1,576 | ||||||

| Net cash provided by operating activities | 15,852 | 13,534 | ||||||

| Investing activities | ||||||||

| Acquisitions | (51,746 | ) | (20,631 | ) | ||||

| Acquisition deposit returned | 2,000 | -- | ||||||

| Purchases of and additions to property and equipment | (18,431 | ) | (17,348 | ) | ||||

| Change in restricted cash | (214 | ) | 796 | |||||

| Investment in Reading International Trust I | -- | (1,547 | ) | |||||

| Investments in unconsolidated joint ventures and entities | (381 | ) | -- | |||||

| Distributions of investment in unconsolidated joint ventures and entities | 214 | 2,186 | ||||||

| Purchase of marketable securities | -- | (15,548 | ) | |||||

| Net proceeds from the sale of an unconsolidated entity | 3,267 | -- | ||||||

| Option proceeds related to property held for sale | 1,095 | -- | ||||||

| Sale of marketable securities | -- | 19,900 | ||||||

| Proceeds from insurance settlement | 910 | -- | ||||||

| Net cash used in investing activities | (63,286 | ) | (32,192 | ) | ||||

| Financing activities | ||||||||

| Repayment of long-term borrowings | (8,670 | ) | (55,813 | ) | ||||

| Proceeds from borrowings | 66,285 | 96,098 | ||||||

| Capitalized borrowing costs | (2,498 | ) | (2,334 | ) | ||||

| Proceeds from exercise of stock options | -- | 25 | ||||||

| Minority interest distributions | (788 | ) | (3,856 | ) | ||||

| Net cash provided by financing activities | 54,329 | 34,120 | ||||||

| Effect of exchange rate changes on cash and cash equivalents | (2,559 | ) | 678 | |||||

| Increase in cash and cash equivalents | 4,336 | 16,140 | ||||||

| Cash and cash equivalents at beginning of period | 20,783 | 11,008 | ||||||

| Cash and cash equivalents at end of period | $ | 25,119 | $ | 27,148 | ||||

| Supplemental Disclosures | ||||||||

Interest paid | $ | 13,547 | $ | 8,625 | ||||

Income taxes paid | $ | 221 | $ | 252 | ||||

| Non-cash transactions | ||||||||

Note payable due to Seller issued for acquisition (Note 19) | $ | 14,750 | $ | -- | ||||

| Decrease in cost basis of Cinema 1, 2 & 3 related to the purchase price adjustment of the call option liability to related party | $ | -- | $ | (2,100 | ) | |||

| Adjustment to accumulated deficit related to adoption of FIN 48 (Note 10) | $ | -- | $ | 509 | ||||

| Decrease in deposit payable and increase in minority interest liability related to the exercise of the Cinema 1, 2 & 3 call option by a related party | $ | -- | $ | (3,000 | ) | |||

| Decrease in call option liability and increase in additional paid in capital related to the exercise of the Cinema 1, 2 & 3 call option by a related party | $ | -- | $ | (2,513 | ) | |||

| Accrued construction-in-progress costs | $ | -- | $ | (2,440 | ) | |||

See accompanying notes to consolidated financial statements.

Reading International, Inc. and Subsidiaries

Notes to Consolidated Financial Statements (Unaudited)

For the Nine Months Ended September 30, 2008

Note 1 – Basis of Presentation

Reading International, Inc., a Nevada corporation (“RDI” and collectively with our consolidated subsidiaries and corporate predecessors, the “Company,” “Reading” and “we,” “us,” or “our”), was founded in 1983 as a Delaware corporation and reincorporated in 1999 in Nevada. Our businesses consist primarily of:

| · | the development, ownership and operation of multiplex cinemas in the United States, Australia, and New Zealand and |

| · | the development, ownership, and operation of retail and commercial real estate in Australia, New Zealand, and the United States. |

The accompanying unaudited consolidated financial statements were prepared in accordance with accounting principles generally accepted in the United States of America (“US GAAP”) for interim reporting and with the instructions to Form 10-Q and Rule 10-01 of Regulation S-X of the Securities and Exchange Commission for interim reporting. As such, certain information and footnote disclosures typically required by US GAAP for complete financial statements have been condensed or omitted. There have been no material changes in the information disclosed in the notes to the consolidated financial statements contained in our Annual Report on Form 10-K for the year ended December 31, 2007 (“2007 Annual Report”). The financial information presented in this quarterly report on Form 10-Q for the period ended September 30, 2008 (the “September Report”), including the information under the heading, Management’s Discussion and Analysis of Financial Condition and Results of Operations, should be read in conjunction with our 2007 Annual Report which contains the latest audited financial statements and related footnotes.

In the opinion of management, all adjustments of a normal recurring nature considered necessary to present fairly in all material respects our financial position, results of our operations and cash flows as of and for the three months and nine months ended September 30, 2008 and 2007 have been made. The results of operations for the three months and nine months ended September 30, 2008 and 2007 are not necessarily indicative of the results of operations to be expected for the entire year.

Marketable Securities

We have investments in marketable securities of $4.1 million at September 30, 2008. These investments are accounted for as available for sale investments in accordance with Statement of Financial Accounting Standards (“SFAS”) No. 115, Accounting for Certain Investments in Debt and Equity Securities, as amended by FSP FAS 115-1/124-1, The Meaning of Other-Than-Temporary Impairment and Its Application to Certain Investments. In accordance with the Financial Accounting Standards Board’s Emerging Issues Task Force (“EITF”) 03-1, The Meaning of Other-Than-Temporary Impairment and Its Application to Certain Investments, assessments of potential impairment for these investments are performed for each applicable reporting period. We have determined that there was no impairment for these investments at September 30, 2008. These investments have a cumulative unrealized gain of $16,000 included in accumulated other comprehensive income at September 30, 2008. For the three months and nine months ended September 30, 2008 our net unrealized loss on marketable securities was $6,000 and $2,000, respectively. For the three months ended September 30, 2007, our net unrealized loss on marketable securities was $880,000 and for the nine months ended September 30, 2007 our net unrealized gain on marketable securities was $82,000. During the three and nine months ended September 30, 2007, we sold $13.4 million and $19.1 million, respectively, of our marketable securities resulting in realized gain on sale of $549,000 and $773,000, respectively, which is included in other income on our Consolidated Statements of Operations.

Other Income

Included in our nine months ended September 30, 2008 other income is $910,000 of insurance settlement proceeds related to damage caused by Hurricane George in 1998 to one of our previously owned cinemas in Puerto Rico, as well as legal settlement proceeds received on our Burstone litigation of $1.1 million and credit card dispute proceeds of $385,000 (See Note 13 – Commitments and Contingencies).

Deferred Leasing Costs

Direct costs incurred in connection with obtaining tenants are amortized over the respective term of the lease on a straight-line basis.

Deferred Financing Costs

Direct costs incurred in connection with financing are amortized over the respective term of the loan utilizing the effective interest method, or straight-line method if the result is not materially different. In addition, interest on loans with increasing interest rates and scheduled principal pre-payments is also recognized on the effective interest method.

Accounting Pronouncements Adopted on January 1, 2008

Statement of Financial Accounting Standards No. 157

Effective January 1, 2008, we adopted, on a prospective basis, SFAS No. 157, Fair Value Measurements (“SFAS 157”) as amended by FASB Staff Position SFAS 157-1, Application of FASB Statement No. 157 to FASB Statement No. 13 and Other Accounting Pronouncements That Address Fair Value Measurements for Purposes of Lease Classification or Measurement under Statement 13 (“FSP FAS 157-1”) and FASB Staff Position SFAS 157-2, Effective Date of FASB Statement No. 157 (“FSP FAS 157-2”). SFAS 157 defines fair value, establishes a framework for measuring fair value in GAAP and provides for expanded disclosure about fair value measurements. SFAS 157 applies prospectively to all other accounting pronouncements that require or permit fair value measurements. FSP FAS 157-1 amends SFAS 157 to exclude from the scope of SFAS 157 certain leasing transactions accounted for under SFAS No. 13, Accounting for Leases. FSP FAS 157-2 amends SFAS 157 to defer the effective date of SFAS 157 for all non-financial assets and non-financial liabilities except those that are recognized or disclosed at fair value in the financial statements on a recurring basis to fiscal years beginning after November 15, 2008.

The adoption of SFAS 157 did not have a material impact on our consolidated financial statements. We are evaluating the impact that SFAS 157 will have on our non-financial assets and non-financial liabilities, since the application of SFAS 157 for such items was deferred, in our case, to January 1, 2009. We believe that the impact of these items will not be material to our consolidated financial statements. Assets and liabilities, typically recorded at fair value on a non-recurring basis, but to which we have not yet applied SFAS 157 due to the deferral of SFAS 157 for such items include:

| · | Non-financial assets and liabilities initially measured at fair value in an acquisition or business combination |

| · | Long-lived assets measured at fair value due to an impairment assessment under SFAS No. 144, Accounting for the Impairment or Disposal of Long-Lived Assets |

| · | Asset retirement obligations initially measured under SFAS No. 143, Accounting for Asset Retirement Obligations |

Statement of Financial Accounting Standards No. 159

Effective January 1, 2008, we adopted, on a prospective basis, SFAS No. 159, The Fair Value Option for Financial Assets and Financial Liabilities (“SFAS 159”). SFAS 159 permits entities to choose to measure many financial instruments and certain other items at fair value. The objective of the guidance is to improve financial reporting by providing entities with the opportunity to mitigate volatility in reported earnings caused by measuring related assets and liabilities differently without having to apply complex hedge accounting provisions. The adoption of SFAS 159 did not have a material impact on our consolidated financial statements since we did not elect to apply the fair value option for any of our eligible financial instruments or other items on the January 1, 2008 effective date.

New Accounting Pronouncements

Statement of Financial Accounting Standards No. 160

In December 2007, the Financial Accounting Standards Board (“FASB”) issued SFAS No. 160, Noncontrolling Interests in Consolidated Financial Statements — an amendment of ARB No. 51 (“SFAS 160”). SFAS 160 requires (i) that noncontrolling (minority) interests be reported as a component of shareholders’ equity, (ii) that net income attributable to the parent and to the noncontrolling interest be separately identified in the consolidated statement of operations, (iii) that changes in a parent’s ownership interest while the parent retains its controlling interest be accounted for as equity transactions, (iv) that any retained noncontrolling equity investment upon the deconsolidation of a subsidiary be initially measured at fair value, and (v) that sufficient disclosures are provided that clearly identify and distinguish between the interests of the parent and the interests of the noncontrolling owners. SFAS 160 is effective for annual periods beginning after December 15, 2008, which is the year ending December 31, 2009 for the Company, and should be applied prospectively. However, the presentation and disclosure requirements of the statement shall be applied retrospectively for all periods presented. The adoption of the provisions of SFAS 160 is not anticipated to materially impact the Company’s consolidated financial position and results of operations.

Statement of Financial Accounting Standards No. 161

In March 2008, the Financial Accounting Standards Board issued SFAS No. 161, Disclosures about Derivative Instruments and Hedging Activities (“SFAS 161”). This new standard enhances disclosure requirements for derivative instruments in order to provide users of financial statements with an enhanced understanding of (i) how and why an entity uses derivative instruments, (ii) how derivative instruments and related hedged items are accounted for under SFAS 133, Accounting for Derivative Instruments and Hedging Activities and its related interpretations and (iii) how derivative instruments and related hedged items affect an entity’s financial position, financial performance, and cash flows. SFAS 161 is to be applied prospectively for the first annual reporting period beginning on or after November 15, 2008. We believe that the adoption of SFAS 161 will not have a material impact on our consolidated financial statement disclosures since we solely have interest rate swap agreements not formally designated as cash flow hedges at the inception of the derivative contract.

FASB Staff Position 142-3

In April 2008, the FASB issued FASB Staff Position 142-3, “Determination of the Useful Life of Intangible Assets” (“FSP 142-3”). FSP 142-3 is to be applied prospectively for fiscal years beginning after December 15, 2008. We are currently evaluating the impact of FSP 142-3 on our consolidated financial position, results of operations and cash flows but currently does not believe it will have a material impact on our consolidated financial statements.

Note 2 – Stock-Based and Equity Compensation

Stock Based Compensation

On August 21, 2008, as part of their executive compensation, 37,388 shares of fully vested restricted Class A Non-Voting Common Stock were granted to three of our executives as stock bonuses having a grant date fair value of $286,000. As of September 30, 2008, these shares had yet to be issued to them and the executives had the option to accept the shares or to receive a reduced cash payment in lieu of shares.

As part of his compensation package, Mr. John Hunter, our Chief Operating Officer, was granted $100,000 of restricted Class A Non-Voting Common Stock on February 12, 2008 and 2007. These stock grants have vesting periods of two years and stock grant prices of $9.70 and $8.63, respectively. On February 11, 2008, $50,000 of restricted Class A Non-Voting Common Stock vested related to Mr. Hunter’s 2007 grant. The 5,794 shares related to this vesting have yet to be issued to him. During the three months and nine months ended September 30, 2008, we recorded compensation expense of $100,000 and $296,000, respectively, and during the three months and nine months ended September 30, 2007, we recorded compensation expense of $59,000 and $178,000, respectively, for the vesting of all our restricted stock grants. In July 2008, Mr. Jay Laifman started with the Company as our Corporate General Counsel. As part of his compensation package, Mr. Laifman was granted $100,000 of Class A Non-Voting Common Stock or 10,638 shares upon acceptance of his employment agreement. This stock grant has a vesting period of two years.

The following table details the grants and vesting of restricted stock to our employees (dollars in thousands):

| Non-Vested Restricted Stock | Fair Value at Grant Date | |||||||

| Outstanding – December 31, 2007 | 61,756 | $ | 524 | |||||

Granted | 58,335 | $ | 468 | |||||

Vested | (53,820 | ) | $ | (418 | ) | |||

| Outstanding – September 30, 2008 | 66,271 | $ | 574 | |||||

Equity Compensation

In 2006, we formed two new wholly owned subsidiaries, Landplan Property Partners, Pty Ltd and Landplan Property Partners New Zealand, Ltd collectively referred to as Landplan Property Partners (“LPP”), to engage in the real estate development business. We have granted the President of LPP, Doug Osborne, as incentive compensation, a subordinated carried interest in certain property trusts, owned by LPP and formed to acquire and hold LPP’s real property investments. That incentive interest may range between 27.5% and 15%, depending on a number of factors including the amount and duration of LPP’s investment in the properties held by these property trusts. Mr. Osborne’s incentive interest is subordinated to (i) the repayment of all third party indebtedness, (ii) the repayment of all funds invested or advanced by Reading, and (iii) the realization by Reading of an 11% annual compounded preferred return on its capital. The estimated value of Mr. Osborne’s incentive interest of $269,000 at September 30, 2008 is included in the minority interest of LPP at September 30, 2008 (see Note 14 – Minority Interest). This amount is based upon a current evaluation of the properties held by these property trusts, all of which are in various stages of development, and not upon any realized or closed transaction. During the three months ended September 30, 2008, we adjusted the expense for these interests based on more current project estimates for our Lake Taupo and Indooroopilly projects resulting in a reduction of the three months expense of $6,000 and a nine months ended September 30, 2008 expense of $85,000. During the three and nine months ended September 30, 2007, we expensed $59,000 and $155,000,

respectively, associated with Mr. Osborne’s interests. At September 30, 2008, the total unrecognized compensation expense related to the LPP equity awards was $214,000, which is expected to be recognized over the remaining weighted average period of approximately 73 months. No amounts, however, will be payable unless the properties held by the property trusts, on a consolidated basis, provide returns on capital in excess of 11%, compounded annually.

Employee/Director Stock Option Plan

We have a long-term incentive stock option plan that provides for the grant to eligible employees and non-employee directors of incentive stock options and non-qualified stock options to purchase shares of the Company’s Class A Nonvoting Common Stock.

When the Company’s tax deduction from an option exercise exceeds the compensation cost resulting from the option, a tax benefit is created. SFAS No. 123(R), Accounting for Stock-Based Compensation (“SFAS 123(R)”, requires that excess tax benefits related to stock option exercises be reflected as financing cash inflows instead of operating cash inflows. For the three months ended September 30, 2008 and 2007, there was no impact to the consolidated statement of cash flows because there were no recognized tax benefits from stock option exercises during these periods.

SFAS 123(R) requires companies to estimate forfeitures. Based on our historical experience and the relative market price to strike price of the options, we do not currently estimate any forfeitures of vested or unvested options.

In accordance with SFAS 123(R), we estimate the fair value of our options using the Black-Scholes option-pricing model, which takes into account assumptions such as the dividend yield, the risk-free interest rate, the expected stock price volatility, and the expected life of the options. The dividend yield is excluded from the calculation, as it is our present intention to retain all earnings. We expense the estimated grant date fair values of options issued on a straight-line basis over the vesting period.

We granted 301,250 of options during the nine months ended September 30, 2007. Of these options, 70,000 were granted to our directors as fully vested options during the nine months ended September 30, 2007. There were no options granted to our directors or employees during the three or nine months ended September 30, 2008 or during the three months ended September 30, 2007. We estimated the fair value of the 2007 option grants at the date of grant using a Black-Scholes option-pricing model with the following weighted average assumptions:

| 2007 | |

| Stock option exercise price | $ 8.35 - $10.30 |

| Risk-free interest rate | 4.636 - 4.824% |

| Expected dividend yield | -- |

| Expected option life | 9.60 - 9.96 yrs |

| Expected volatility | 33.64 - 45.47% |

| Weighted average fair value | $4.42 - $ 4.82 |

Using the above assumptions and in accordance with the SFAS 123(R) modified prospective method, we recorded $160,000 and $480,000 in compensation expense for the total estimated grant date fair value of stock options that vested during the three and nine months ended September 30, 2008, respectively. We also recorded $177,000 and $597,000 in compensation expense for the total estimated grant date fair value of stock options that vested during the three and nine months ended September 30, 2007, respectively. At September 30, 2008, the total unrecognized estimated compensation cost related to non-vested stock options granted was $396,000, which is expected to be recognized over a weighted average vesting period of 0.86 years. No options were exercised during the three or nine months ended September 30, 2008; therefore, no cash was received and no value was realized

from the exercise of options during those periods. We recorded cash received from stock options exercised of $25,000 for the three and nine months ended September 30, 2007. The total realized value of these exercised stock options for the three and nine months ended September 30, 2007 was $37,000. There were 1,875 and 122,500 and options vested during the three and nine months ended September 30, 2008 having a current intrinsic value of $0 for the period as all the options were “out-of-the-money” at September 30, 2008. Except for the 70,000 fully vested options granted to our directors during the first quarter of 2007, 1,875 and 6,875 options vested during the three and nine months ended September 30, 2007, respectively; therefore, the grant date fair value of options vesting during the three and nine months ended September 30, 2007 was $15,000 and $55,000, respectively. The intrinsic, unrealized value of all options outstanding, vested and expected to vest, at September 30, 2008 was $1.1 million of which 100.0% are currently exercisable.

All stock options granted have a contractual life of 10 years at the grant date. The aggregate total number of shares of Class A Nonvoting Common Stock and Class B Voting Common Stock authorized for issuance under our 1999 Stock Option Plan is 1,287,150. At the time that options are exercised, at the discretion of management, we will either issue treasury shares or make a new issuance of shares to the employee or board member. Dependent on the grant letter to the employee or board member, the required service period for option vesting is between zero and four years.

We had the following stock options outstanding and exercisable as of September 30, 2008 and December 31, 2007:

| Common Stock Options Outstanding | Weighted Average Exercise Price of Options Outstanding | Common Stock Exercisable Options | Weighted Average Price of Exercisable Options | |||||||||||||||||||||||||||||

| Class A | Class B | Class A | Class B | Class A | Class B | Class A | Class B | |||||||||||||||||||||||||

| Outstanding- January 1, 2007 | 514,100 | 185,100 | $ | 5.21 | $ | 9.90 | 488,475 | 185,100 | $ | 5.06 | $ | 9.90 | ||||||||||||||||||||

| Granted | 151,250 | 150,000 | $ | 9.37 | $ | 10.24 | ||||||||||||||||||||||||||

| Exercised | (6,250 | ) | -- | $ | 4.01 | $ | -- | |||||||||||||||||||||||||

| Expired | (81,250 | ) | (150,000 | ) | $ | 10.25 | $ | 10.24 | ||||||||||||||||||||||||

| Outstanding- December 31, 2007 | 577,850 | 185,100 | $ | 5.60 | $ | 9.90 | 477,850 | 35,100 | $ | 4.72 | $ | 8.47 | ||||||||||||||||||||

No activity during the period | -- | -- | $ | -- | $ | -- | ||||||||||||||||||||||||||

| Outstanding-September 30, 2008 | 577,850 | 185,100 | $ | 5.60 | $ | 9.90 | 525,350 | 110,100 | $ | 5.19 | $ | 9.67 | ||||||||||||||||||||

The weighted average remaining contractual life of all options outstanding, vested and expected to vest, at September 30, 2008 and December 31, 2007 was approximately 4.86 and 6.22 years, respectively. The weighted average remaining contractual life of the exercisable options outstanding at September 30, 2008 and December 31, 2007 was approximately 5.47 and 4.74 years, respectively.

Note 3 – Business Segments

Our operations are organized into two reportable business segments within the meaning of SFAS No. 131, Disclosures about Segments of an Enterprise and Related Information. Our reportable segments are (1) cinema exhibition and (2) real estate. The cinema segment is engaged in the development, ownership, and operation of multiplex cinemas. The real estate segment is engaged in the development, ownership, and operation of commercial properties. Incident to our real estate operations we have acquired, and continue to hold, raw land in urban and suburban centers in Australia and New Zealand.

The tables below summarize the results of operations for each of our principal business segments for the three (“2008 Quarter”) and nine (“2008 Nine Months”) months ended September 30, 2008 and the three (“2007 Quarter”) and nine (“2007 Nine Months”) months ended September 30, 2007, respectively. Operating expense includes costs associated with the day-to-day operations of the cinemas and live theatres and the management of

rental properties. All operating results from discontinued operations are included in “Gain on sale of a discontinued operation” (dollars in thousands):

| Three months ended September 30, 2008 | Cinema | Real Estate | Intersegment Eliminations | Total | ||||||||||||

| Revenue | $ | 52,909 | $ | 5,588 | $ | (1,969 | ) | $ | 56,528 | |||||||

| Operating expense | 43,734 | 2,253 | (1,969 | ) | 44,018 | |||||||||||

| Depreciation & amortization | 3,834 | 880 | -- | 4,714 | ||||||||||||

| General & administrative expense | 1,106 | 255 | -- | 1,361 | ||||||||||||

| Segment operating income | $ | 4,235 | $ | 2,200 | $ | -- | $ | 6,435 | ||||||||

Three months ended September 30, 2007 | Cinema | Real Estate | Intersegment Eliminations | Total | ||||||||||||

| Revenue | $ | 28,009 | $ | 4,858 | $ | (1,790 | ) | $ | 31,077 | |||||||

| Operating expense | 21,831 | 2,044 | (1,790 | ) | 22,085 | |||||||||||

| Depreciation & amortization | 1,591 | 917 | -- | 2,508 | ||||||||||||

| General & administrative expense | 793 | 176 | -- | 969 | ||||||||||||

| Segment operating income | $ | 3,794 | $ | 1,721 | $ | -- | $ | 5,515 | ||||||||

| Reconciliation to consolidated net income (loss): | 2008 Quarter | 2007 Quarter | ||||||

| Total segment operating income | $ | 6,435 | $ | 5,515 | ||||

Non-segment: | ||||||||

Depreciation and amortization expense | 163 | 139 | ||||||

General and administrative expense | 3,036 | 2,902 | ||||||

| Operating income | 3,236 | 2,474 | ||||||

Interest expense, net | (3,962 | ) | (2,277 | ) | ||||

Other income | (1,009 | ) | 707 | |||||

Minority interest | (85 | ) | (162 | ) | ||||

Income from discontinued operation | 178 | 45 | ||||||

Income tax expense | (689 | ) | (501 | ) | ||||

Equity earnings of unconsolidated joint ventures and entities | 270 | 584 | ||||||

| Net income (loss) | $ | (2,061 | ) | $ | 870 | |||

| Nine months ended September 30, 2008 | Cinema | Real Estate | Intersegment Eliminations | Total | ||||||||||||

| Revenue | $ | 135,693 | $ | 16,297 | $ | (4,518 | ) | $ | 147,472 | |||||||

| Operating expense | 114,115 | 6,139 | (4,518 | ) | 115,736 | |||||||||||

| Depreciation & amortization | 10,473 | 2,833 | -- | 13,306 | ||||||||||||

| General & administrative expense | 3,005 | 851 | -- | 3,856 | ||||||||||||

| Segment operating income | $ | 8,100 | $ | 6,474 | $ | -- | $ | 14,574 | ||||||||

Nine months ended September 30, 2007 | Cinema | Real Estate | Intersegment Eliminations | Total | ||||||||||||

| Revenue | $ | 76,825 | $ | 14,205 | $ | (4,081 | ) | $ | 86,949 | |||||||

| Operating expense | 60,959 | 5,462 | (4,081 | ) | 62,340 | |||||||||||

| Depreciation & amortization | 4,909 | 2,645 | -- | 7,554 | ||||||||||||

| General & administrative expense | 2,317 | 763 | -- | 3,080 | ||||||||||||

| Segment operating income | $ | 8,640 | $ | 5,335 | $ | -- | $ | 13,975 | ||||||||

| Reconciliation to consolidated net income (loss): | 2008 Nine Months | 2007 Nine Months | ||||||

| Total segment operating income | $ | 14,574 | $ | 13,975 | ||||

Non-segment: | ||||||||

Depreciation and amortization expense | 523 | 416 | ||||||

General and administrative expense | 10,137 | 8,344 | ||||||

| Operating income | 3,914 | 5,215 | ||||||

Interest expense, net | (9,832 | ) | (5,978 | ) | ||||

Other income | 2,033 | 250 | ||||||

Minority interest | (246 | ) | (657 | ) | ||||

Gain on sale of a discontinued operation | -- | 1,912 | ||||||

Income (loss) from discontinued operation | 371 | (67 | ) | |||||

Income tax expense | (1,513 | ) | (1,443 | ) | ||||

Equity earnings of unconsolidated joint ventures and entities | 817 | 2,626 | ||||||

Gain on sale of unconsolidated entity | 2,450 | -- | ||||||

| Net income (loss) | $ | (2,006 | ) | $ | 1,858 | |||

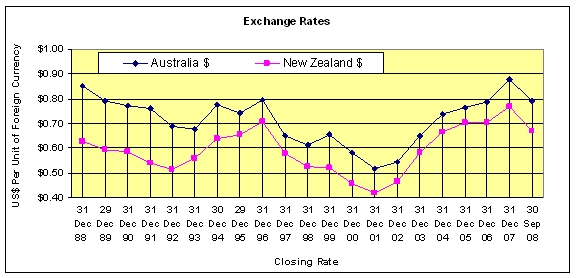

Note 4 – Operations in Foreign Currency

We have significant assets in Australia and New Zealand. To the extent possible, we conduct our Australian and New Zealand operations on a self-funding basis. The carrying value of our Australian and New Zealand assets and liabilities fluctuate due to changes in the exchange rates between the US dollar and the functional currency of Australia (Australian dollar) and New Zealand (New Zealand dollar). We have no derivative financial instruments to hedge against the risk of foreign currency exposure.

Presented in the table below are the currency exchange rates for Australia and New Zealand as of September 30, 2008 and December 31, 2007:

| US Dollar | ||||||||

| September 30, 2008 | December 31, 2007 | |||||||

| Australian Dollar | $ | 0.7904 | $ | 0.8776 | ||||

| New Zealand Dollar | $ | 0.6690 | $ | 0.7678 | ||||

Note 5 – Earnings (Loss) Per Share

Basic earnings (loss) per share is computed by dividing the net income (loss) to common stockholders by the weighted average number of common shares outstanding during the period. Diluted earnings (loss) per share is computed by dividing the net income (loss) to common stockholders by the weighted average number of common shares outstanding during the period after giving effect to all potentially dilutive common shares that would have been outstanding if the dilutive common shares had been issued. Stock options and non-vested stock awards give rise to potentially dilutive common shares. In accordance with SFAS No. 128, Earnings Per Share, these shares are included in the dilutive loss per share calculation under the treasury stock method. The following is a calculation of earnings (loss) per share (dollars in thousands, except share data):

Three Months Ended September 30, | Nine Months Ended September 30, | |||||||||||||||

| 2008 | 2007 | 2008 | 2007 | |||||||||||||

| Income (loss) from continuing operations | $ | (2,239 | ) | $ | 825 | $ | (2,377 | ) | $ | 13 | ||||||

| Income from discontinued operations | 178 | 45 | 371 | 1,845 | ||||||||||||

| Net income (loss) | $ | (2,061 | ) | $ | 870 | $ | (2,006 | ) | $ | 1,858 | ||||||

| Earnings (loss) per common share – basic and diluted: | ||||||||||||||||

Earnings (loss) from continuing operations | $ | (0.10 | ) | $ | 0.04 | $ | (0.11 | ) | $ | 0.00 | ||||||

Earnings from discontinued operations | 0.01 | 0.00 | 0.02 | 0.08 | ||||||||||||

| Basic and diluted earnings (loss) per share | $ | (0.09 | ) | $ | 0.04 | $ | (0.09 | ) | $ | 0.08 | ||||||

| Weighted average common stock – basic | 22,476,904 | 22,487,943 | 22,476,514 | 22,486,395 | ||||||||||||

| Weighted average common stock – dilutive | 22,476,904 | 22,761,270 | 22,476,514 | 22,759,723 | ||||||||||||

For the three and nine months ended September 30, 2007, the weighted average common stock – dilutive only included 273,327 of exercisable stock options. For the three and nine months ended September 30, 2008, we recorded losses from continuing operations. As such, the incremental shares of 53,820 shares of unissued Class A Non-Voting Common Stock and 263,010 of exercisable stock options in 2008 were excluded from the computation of diluted loss per share because they were anti-dilutive in those periods.

Note 6 - Property Held for Development, Property Under Development, and Property and Equipment

During the 2008 quarter we transferred land previously held for sale, into property held for development. The value of this property, relating to a New Zealand asset, was subsequently impaired by $1.0 million (NZ$1.6 million).

As of September 30, 2008 and December 31, 2007, we owned property under development summarized as follows (dollars in thousands):

| Property Under Development | September 30, 2008 | December 31, 2007 | ||||||

| Land | $ | 33,149 | $ | 36,994 | ||||

| Construction-in-progress (including capitalized interest) | 36,238 | 29,793 | ||||||

| Property Under Development | $ | 69,387 | $ | 66,787 | ||||

We recorded capitalized interest related to our properties under development for the three months ended September 30, 2008 and 2007 of $1.6 million and $1.1 million, respectively, and $3.1 million for each of the nine months ended September 30, 2008 and 2007, respectively.

As of September 30, 2008 and December 31, 2007, we owned investments in property and equipment as follows (dollars in thousands):

| Property and equipment | September 30, 2008 | December 31, 2007 | ||||||

| Land | $ | 50,101 | $ | 51,242 | ||||

| Building | 89,221 | 96,321 | ||||||

| Leasehold interests | 45,231 | 12,171 | ||||||

| Construction-in-progress | 467 | 1,318 | ||||||

| Fixtures and equipment | 63,420 | 55,657 | ||||||

| 248,440 | 216,709 | |||||||

| Less: accumulated depreciation | (68,651 | ) | (62,698 | ) | ||||

| Property and equipment, net | $ | 179,789 | $ | 154,011 | ||||

Depreciation expense for property and equipment was $4.2 million and $2.5 million for the three months ended September 30, 2008 and 2007, respectively, and $12.0 million and $7.4 million for the nine months ended September 30, 2008 and 2007, respectively.

In April 2008, we opened a newly leased 9-screen cinema in Rouse Hill, Australia. We fitted out the cinema with leasehold assets costing $1.3 million (AUS$1.4 million) and fixture and equipment costs of $3.9 million (AUS$4.1 million). Additionally, in August 2008, we opened a newly leased 6-screen cinema in Dandenong, Australia. We fitted out the cinema with leasehold assets costing $419,000 (AUS$472,000) and fixture and equipment costs of $467,000 (AUS$527,000).

Upon completion of our Lake Taupo property, we have transferred the assets related to the redeveloped property to land and building during the third quarter of 2008. These transfers resulted in an increase of our land and building balances of $994,000 (NZ$1.5 million) and $2.7 million (NZ$4.0 million), respectively.

Note 7 – Investments in Unconsolidated Joint Ventures and Entities

Except as noted below regarding our investment in Malulani Investments, Limited, investments in unconsolidated joint ventures and entities are accounted for under the equity method of accounting, and, as of September 30, 2008 and December 31, 2007, include the following (dollars in thousands):

| Interest | September 30, 2008 | December 31, 2007 | ||||||||||

| Malulani Investments, Limited | 29.3 | % | $ | 1,800 | $ | 1,800 | ||||||

| Rialto Distribution | 33.3 | % | 1,219 | 1,029 | ||||||||

| Rialto Cinemas | 50.0 | % | 4,844 | 5,717 | ||||||||

205-209 East 57th Street Associates, LLC | 25.0 | % | 1,146 | 1,059 | ||||||||

| Mt. Gravatt Cinema | 33.3 | % | 4,594 | 5,159 | ||||||||

| Berkeley Cinemas – Botany | 50.0 | % | -- | 716 | ||||||||

| Total investment | $ | 13,603 | $ | 15,480 | ||||||||

For the three months and nine months ended September 30, 2008 and 2007, we recorded our share of equity earnings (loss) from our investments in unconsolidated joint ventures and entities as follows:

Three Months Ended September 30, | Nine Months Ended September 30, | |||||||||||||||

| 2008 | 2007 | 2008 | 2007 | |||||||||||||

| Rialto Distribution | $ | 100 | $ | 3 | $ | 272 | $ | 91 | ||||||||

| Rialto Cinemas | 9 | 74 | (5 | ) | 54 | |||||||||||

205-209 East 57th Street Associates, LLC | 87 | 201 | 87 | 1,550 | ||||||||||||

| Mt. Gravatt Cinema | 222 | 184 | 680 | 610 | ||||||||||||

| Berkeley Cinema – Botany | (1 | ) | 122 | 87 | 321 | |||||||||||

| Other investments | (147 | ) | -- | (304 | ) | -- | ||||||||||

| Total equity earnings | $ | 270 | $ | 584 | $ | 817 | $ | 2,626 | ||||||||

Malulani Investments, Limited

We continue to treat this investment on a cost basis by recognizing earnings as they are distributed to us. We are currently in litigation with certain controlling shareholders and directors of Malulani Investments Limited (“MIL”).

Berkeley Cinemas

On June 6, 2008, we sold the Botany Downs Cinema to our joint venture partner for $3.3 million (NZ$4.3 million) resulting in a net gain on sale of an unconsolidated entity of $2.5 million (NZ$3.2 million). With the sale of this cinema, our unconsolidated joint venture debt decreased by $3.2 million (NZ$4.2 million) We continue to have certain outstanding, contingent claims related to interest and working capital, which may or may not increase the total sales price of the cinema.

Other Investments

From time to time, we will make investments in various activities that require equity method accounting including but not limited to investments in productions in our live theatres.

Note 8 – Goodwill and Intangible Assets

Subsequent to January 1, 2002, in accordance with SFAS No. 142, Goodwill and Other Intangible Assets, we do not amortize goodwill. Instead, we perform an annual impairment review of our goodwill and other intangible assets in the fourth quarter unless changes in circumstances indicate that an asset may be impaired. As of September 30, 2008 and December 31, 2007, we had goodwill consisting of the following (dollars in thousands):

| Cinema | Real Estate | Total | ||||||||||

| Balance as of December 31, 2007 | $ | 13,827 | $ | 5,273 | $ | 19,100 | ||||||

| Goodwill acquired during 2008 | 6,306 | -- | 6,306 | |||||||||

| Foreign currency translation adjustment | (1,493 | ) | (105 | ) | (1,598 | ) | ||||||

| Balance at September 30, 2008 | $ | 18,640 | $ | 5,168 | $ | 23,808 | ||||||

We have intangible assets other than goodwill that are subject to amortization and are being amortized over various periods. We amortize our beneficial leases over the lease period, the longest of which is 20 years, our trade name using an accelerated amortization method over its estimated useful life of 50 years, and our option fee and other intangible assets over 10 years. For the three months ended September 30, 2008 and 2007,

amortization expense totaled $653,000 and $139,000, respectively; and for the nine months ended September 30, 2008 and 2007, amortization expense totaled $1.9 million and $614,000, respectively.

Intangible assets subject to amortization consist of the following (dollars in thousands):

As of September 30, 2008 | Beneficial Leases | Trade name | Option Fee | Other Intangible Assets | Total | |||||||||||||||

| Gross carrying amount | $ | 22,131 | $ | 7,220 | $ | 2,773 | $ | 609 | $ | 32,733 | ||||||||||

| Less: Accumulated amortization | 5,587 | 480 | 2,592 | 75 | 8,734 | |||||||||||||||

| Total, net | $ | 16,544 | $ | 6,740 | $ | 181 | $ | 534 | $ | 23,999 | ||||||||||

As of December 31, 2007 | Beneficial Leases | Trade name | Option Fee | Other Intangible Assets | Total | |||||||||||||||

| Gross carrying amount | $ | 12,295 | $ | -- | $ | 2,773 | $ | 238 | $ | 15,306 | ||||||||||

| Less: Accumulated amortization | 4,311 | -- | 2,521 | 26 | 6,858 | |||||||||||||||

| Total, net | $ | 7,984 | $ | -- | $ | 252 | $ | 212 | $ | 8,448 | ||||||||||

Note 9 – Prepaid and Other Assets

Prepaid and other assets are summarized as follows (dollars in thousands):

September 30, 2008 | December 31, 2007 | |||||||

| Prepaid and other current assets | ||||||||

| Prepaid expenses | $ | 899 | $ | 569 | ||||

| Prepaid taxes | 486 | 602 | ||||||

| Deposits | 302 | 2,097 | ||||||

| Other | 647 | 531 | ||||||

Total prepaid and other current assets | $ | 2,334 | $ | 3,799 | ||||

| Other non-current assets | ||||||||

| Other non-cinema and non-rental real estate assets | $ | 1,260 | $ | 1,270 | ||||

| Deferred financing costs, net | 5,319 | 2,805 | ||||||

| Interest rate swaps | 741 | 526 | ||||||

| Other receivables | 2,470 | 1,648 | ||||||

| Pre-acquisition costs | -- | 948 | ||||||

| Other | 693 | 788 | ||||||

Total non-current assets | $ | 10,483 | $ | 7,985 | ||||

Note 10 – Income Tax

The income tax provision for the three months and nine months ended September 30, 2008 and 2007 was composed of the following amounts (dollars in thousands):

Three Months Ended September 30, | Nine Months Ended September 30, | |||||||||||||||

| 2008 | 2007 | 2008 | 2007 | |||||||||||||

| Foreign income tax provision | $ | 113 | $ | 122 | $ | 228 | $ | 282 | ||||||||

| Foreign withholding tax | 183 | 168 | 562 | 480 | ||||||||||||

| Federal tax provision | 365 | 128 | 619 | 383 | ||||||||||||

| Other income tax | 28 | 83 | 104 | 298 | ||||||||||||

| Net tax provision | $ | 689 | $ | 501 | $ | 1,513 | $ | 1,443 | ||||||||

We adopted FASB Interpretation No. 48 (“FIN 48”) on January 1, 2007. As a result, we recognized a $509,000 cumulative increase to reserves for uncertain tax positions, which was accounted for as an adjustment to the beginning balance of accumulated deficit in 2007. As of that date, we also reclassified approximately $4.0 million in reserves from current taxes liabilities to noncurrent tax liabilities. During the three and nine months ended September 30, 2008 the Company’s FIN 48 liability increased by $397,000 and $651,000, respectively, reflecting the accrual of interest for IRS matters under litigation.

Note 11 – Notes Payable and Subordinated Debt

Notes payable and subordinated debt are summarized as follows (dollars in thousands):

| Interest Rates as of | Balance as of | ||||||||||||||||

| Name of Note Payable or Security | September 30, 2008 | December 31, 2007 | Maturity Date | September 30, 2008 | December 31, 2007 | ||||||||||||

| Australian Corporate Credit Facility | 8.69% | 7.75% | June 30, 2011 | $ | 79,435 | $ | 85,772 | ||||||||||

| Australian Shopping Center Loans | -- | -- | 2007-2013 | 881 | 1,066 | ||||||||||||

| Australian Construction Loan | 9.28% | -- | January 1, 2015 | 1,855 | -- | ||||||||||||

| New Zealand Corporate Credit Facility | 8.90% | 10.10% | November 23, 2010 | 2,168 | 2,488 | ||||||||||||

| Trust Preferred Securities | 9.22% | 9.22% | April 30, 2027 | 51,547 | 51,547 | ||||||||||||

| US Euro-Hypo Loan | 6.73% | 6.73% | June 30, 2012 | 15,000 | 15,000 | ||||||||||||

| US GE Capital Term Loan | 6.90% | -- | February 21, 2013 | 41,625 | -- | ||||||||||||

| US Liberty Theatres Term Loans | 6.20% | -- | April 1, 2013 | 7,020 | -- | ||||||||||||

| US Nationwide Loans 1 | 6.50% - 7.50% | -- | February 21, 2013 | 18,627 | -- | ||||||||||||

| US Nationwide Loans 2 | 8.50% | -- | February 21, 2011 | 1,527 | -- | ||||||||||||

| US Sutton Hill Capital Note 1 – Related Party | 10.34% | 9.91% | December 31, 2010 | 5,000 | 5,000 | ||||||||||||

| US Sutton Hill Capital Note 2 – Related Party | 8.25% | 8.25% | December 31, 2010 | 9,000 | 9,000 | ||||||||||||

| US Union Square Theatre Term Loan | 6.26% | 6.26% | January 1, 2010 | 7,169 | 7,322 | ||||||||||||

Total | $ | 240,854 | $ | 177,195 | |||||||||||||

Australian Corporate Credit Facility

During June 2008, we extended the term of our $86.9 million (AUS$110.0 million) Australian facility to June 30, 2011. This facility will continue to roll to a 3-year term, following an annual bank review. Besides the extended term, the only other changes to the original agreement was that the loan requires interest only payments and our interest margin over BBSY (Bank Bill Swap Bid Rate) increased from 1.00% to 1.25%. The drawn balance of this loan was $79.4 million (AUS$100.5 million) at September 30, 2008.

Australian Construction Loan

We have negotiated with an Australia bank a construction line of credit on our Indooroopilly property of $6.9 million (AUS$8.7 million) which, upon completion of the development project, converts to a term loan of up to $8.3 million (AUS$10.5 million). As of September 30, 2008, we have drawn $1.9 million (AUS$2.3 million) on this credit facility.

GE Capital Term Loan

In connection with the Consolidated Entertainment acquisition described in Note 19 - - Acquisitions, on February 21, 2008, Consolidated Amusement Theatres, Inc., (now renamed Consolidated Entertainment, Inc.) as borrower (“Borrower”), and Consolidated Amusement Holdings, Inc. (“Holdings”) entered into a Credit Agreement with General Electric Capital Corporation (“GE”) as lender and administrative agent, and GE Capital Markets, Inc. as lead arranger, which provides Borrower with a senior secured credit facility of up to $55.0 million in the aggregate, including a revolving credit facility of up to $5.0 million and a $1.0 million sub-limit for letters of credit (the “Credit Facility”). The initial borrowings under the Credit Facility were used to finance, in part, our acquisition of the theaters and other assets described in Note 17 - Acquisitions. We may borrow additional amounts under the Credit Facility for other acquisitions as permitted under the Credit Facility (and to pay any related transaction expenses), and for ordinary working capital and general corporate needs of Borrower, subject to the terms of the Credit Facility. We incurred deferred financing costs of $2.6 million related to our borrowings under this Credit Facility. The Credit Facility expires on February 21, 2013 and is secured by substantially all the assets of Borrower and Holdings.

Borrowings under the Credit Facility bear interest at a rate equal to either (i) the Index Rate (defined as the higher of the Wall Street Journal prime rate and the federal funds rate plus 50 basis points), or (ii) LIBOR (as defined in the Credit Facility), at the election of Borrower, plus, in each case, a margin determined by reference to Borrower's Leverage Ratio (as defined in the Credit Facility) that ranges between prime rate plus 2.00% and prime rate plus 2.75%, and between LIBOR plus 3.25% and LIBOR plus 4.00%, respectively.

Borrowings under the Credit Facility may be prepaid at any time without penalty, subject to certain minimums and payment of any LIBOR funding breakage costs. Borrower will be required to pay an unused commitment fee equal to 0.50% per annum on the actual daily-unused portion of the revolving loan facility, payable quarterly in arrears. Outstanding letters of credit under the Credit Facility are subject to a fee of the applicable LIBOR rate in effect per annum on the face amount of such letters of credit, payable quarterly in arrears. Borrower will be required to pay standard fees with respect to the issuance, negotiation, and amendment of letters of credit issued under the letter of credit facility. In accordance with the prepayment provisions of the credit agreement, during 2008, we paid down on the facility by $8.0 million. This includes a prepayment of the annual cash flow draw of $5.0 million and a pay down of the overall facility by an additional $3.0 million.

The Credit Facility contains other customary terms and conditions, including representations and warranties, affirmative and negative covenants, events of default and indemnity provisions. Such covenants, among other things, limit Borrower's ability to incur indebtedness, incur liens or other encumbrances, make capital expenditures, enter into mergers, consolidations and asset sales, engage in transactions with affiliates, pay dividends or other distributions and change the nature of the business conducted by Borrower.

The Credit Agreement contains financial covenants requiring the Borrower to maintain minimum fixed charge and interest coverage ratios and not to exceed specified maximum leverage ratios. The compliance levels for the maximum leverage and minimum interest coverage covenants become stricter over the term of the Credit Facility.

The Credit Facility provides for customary events of default, including payment defaults, covenant defaults, cross-defaults to certain other indebtedness, certain bankruptcy events, judgment defaults, invalidity of any loan documents or liens created under the Credit Agreement, change of control of Borrower, termination of certain theater leases and material inaccuracies in representations and warranties.

Liberty Theatres Term Loan

On March 17, 2008, we entered into a $7.1 million loan agreement with a financial institution, secured by our Royal George Theatre in Chicago, Illinois and our Minetta and Orpheum Theatres in New York. The loan has a 5-year term loan that accrues a 6.20% interest rate payable monthly in arrears. We incurred deferred financing costs of $527,000 related to our borrowings of this loan. The loan agreement requires only monthly principal and interest payments along with self-reported annual financial statements.

US Nationwide Loan 1

As described in greater detail in Note 19 – Acquisitions, on February 22, 2008, we acquired 15 motion picture theaters and theater-related assets from Pacific Theatres Exhibition Corp. and its affiliates (collectively, the “Sellers”) for $70.2 million. The Seller’s affiliate, Nationwide Theatres Corp (“Nationwide”), provided $21.0 million of acquisition financing evidenced by a five-year promissory note (the “Nationwide Note 1”) of Reading Consolidated Holdings, Inc., our wholly owned subsidiary (“RCHI”), maturing on February 21, 2013. The Nationwide Note 1 bears interest (i) as to $8.0 million of principal at the annual rates of 7.50% for the first three years and 8.50% thereafter and (ii) as to $13.0 million of principal at the annual rates of 6.50% through July 31, 2009 and 8.50% thereafter. Accrued interest is due and payable on February 21, 2011 and thereafter on the last day of each calendar quarter, commencing on June 30, 2011. The entire principal amount is due and payable upon maturity, subject to our right to prepay at any time without premium or penalty and to the requirement that, under certain circumstances, we make mandatory prepayments equal to a portion of free cash flow generated by the acquired theaters. The loan is recourse only to RCHI and its assets, which include all of the Hawaii theaters and certain of the California theaters acquired from the Sellers and our Manville and Dallas Angelika Theaters.

The Nationwide Note 1 is subject to certain adjustments. To date, these adjustments have resulted in a net reduction of $3.3 million in the principal amount of the $8.0 million portion of the note, comprised of a reduction in the amount of $6.3 million and an additional advance of $3.0 million (such advance being used to pay down the GE Capital Term Loan discussed above).

US Nationwide Loan 2

In connection with the acquisition, the Sellers also committed to loan to RDI up to $3.0 million in two draws of $1.5 million each, one of which was drawn on July 21, 2008 and the other of which may be drawn on or before July 31, 2009. This loan bears an interest rate of 8.50%, compounded annually, and is due and payable, in full, on February 21, 2011, subject to our right to prepay the loan without premium or penalty.

Note 12 – Other Liabilities

Other liabilities are summarized as follows (dollars in thousands):

September 30, 2008 | December 31, 2007 | |||||||

| Current liabilities | ||||||||

Security deposit payable | $ | 202 | $ | 175 | ||||

Other | -- | (6 | ) | |||||

Other current liabilities | $ | 202 | $ | 169 | ||||

| Other liabilities | ||||||||

Foreign withholding taxes | $ | 5,681 | $ | 5,480 | ||||

Straight-line rent liability | 5,135 | 3,783 | ||||||

Option liability | 948 | -- | ||||||

Environmental reserve | 1,656 | 1,656 | ||||||

Accrued pension | 2,915 | 2,626 | ||||||

Other | 1,319 | 1,391 | ||||||

Other liabilities | $ | 17,654 | $ | 14,936 | ||||

Included in our other liabilities are accrued pension costs of $2.9 million. Associated with our pension plans, for the three and nine months ended September 30, 2008, we recognized $63,000 and $289,000, respectively, of interest cost and $71,000 and $214,000, respectively, of amortized prior service cost. For the three and nine months ended September 30, 2007, we recognized $39,000 and $91,000, respectively, of interest cost and $76,000 and $177,000, respectively, of amortized prior service cost.

Note 13 – Commitments and Contingencies

Unconsolidated Debt and Construction Commitments

Total debt of unconsolidated joint ventures and entities was $3.0 million and $4.2 million as of September 30, 2008 and December 31, 2007, respectively. Our share of unconsolidated debt, based on our ownership percentage, was $989,000 and $2.0 million as of September 30, 2008 and December 31, 2007, respectively. This debt is without recourse to Reading as of September 30, 2008 and December 31, 2007.

Associated with the development of our Indooroopilly, Brisbane, Australia property, we have entered into a construction agreement related to its redevelopment. Obligations under this agreement are contingent upon the completion of the services within the guidelines specified in the agreement. At September 30, 2008, we had $3.6 million (AU$4.6 million) in outstanding obligations for this contract, which we believe will be settled in the next twelve months.

Litigation

Whitehorse Center Litigation

On May 10, 2005, a mixed judgment was entered by the trial court in Reading Entertainment Australia Pty Ltd vs. Burstone Victoria Pty Ltd. Appeal rights have been exhausted and the net result of that judgment has been the payment to us by the defendants during the 2008 first quarter of $830,000 (AUS$901,000) and $314,000 (AUS$333,000) during the 2008 second quarter which are each included in other income.

Botany Downs Cinema Litigation

This litigation was resolved by our sale, on June 6, 2008, of the Botany Downs Cinema to our joint venture partner for $3.3 million (NZ$4.3 million) resulting in a gain of $2.5 million (NZ$3.2 million) (see Note 7 - Investments in Unconsolidated Joint Ventures and Entities).

Condrens Litigation

On May 13, 2008, the High Court of Wellington rendered a decision against the liquidators of Condrens Parking Limited and in favor of Aeneas Edward O’Sullivan, Mark Gerard McKinley, and Clifford Joseph Condrens in the matter titled Palmer and Petterson v. O’Sullivan et al. Reading New Zealand Ltd was the majority creditor of Condrens Parking Ltd, and, as such, financially supported the liquidator, Palmer and Petterson, in this case. Because of this determination, the defendants are claiming costs of approximately $290,000 (NZ$381,000). No amount has been accrued for this as of September 30, 2008. We have appealed this decision, and are contesting the defendants’ cost claims.

Tax Audit/Litigation

On September 11, 2008, we advised the Internal Revenue Service (the “IRS”) that we would no longer be contesting the $349,000 deficiency assessment made with respect to Reading Entertainment, Inc (one of our wholly owned subsidiaries) for the tax years 1997, 1998, and 1999. As one of the results of this decision will be a refund of $760,000 of alternative minimum tax paid in 1996, the net result of this conclusion will be a net refund to us of previously paid Federal Income Taxes. The major portion of the currently outstanding litigation between Craig Corporation (another of our wholly owned subsidiaries) remains ongoing, and is in the discovery phase. This portion of the litigation relates to the treatment of the contribution to Reading Entertainment, Inc. by Craig Corporation of Stater Bros. Stock, the contribution of those shares to our Australian subsidiary and the eventual repurchase of those shares by Stater Bros. This litigation is described in greater detail in our Annual Report of Form 10K for the year ended December 31, 2007.

Note 14 – Minority Interest

Minority interest is composed of the following enterprises:

| · | 50% of membership interest in Angelika Film Centers LLC (“AFC LLC”) owned by a subsidiary of iDNA, Inc.; |

| · | 25% minority interest in Australia Country Cinemas Pty Ltd (“ACC”) owned by Panorama Cinemas for the 21st Century Pty Ltd.; |

| · | 33% minority interest in the Elsternwick Joint Venture owned by Champion Pictures Pty Ltd.; |

| · | Up to 27.5% incentive interest in certain property holding trusts established by LPP (see Note 2, above); |

| · | 25% minority interest in the Sutton Hill Properties, LLC owned by Sutton Hill Capital, L.L.C.; and |

| · | 20% minority interest in Big 4 Farming, LLC by Cecelia Packing Corporation. |

The components of minority interest are as follows (dollars in thousands):

| September 30, | December 31, | |||||||

| 2008 | 2007 | |||||||

| AFC LLC | $ | 1,956 | $ | 2,256 | ||||

| Australian Country Cinemas | 174 | 232 | ||||||

| Elsternwick Unincorporated Joint Venture | 131 | 145 | ||||||

| LPP Property Trusts | 112 | 237 | ||||||

| Sutton Hill Properties | (85 | ) | (36 | ) | ||||

| Other (Big 4 Farming) | -- | 1 | ||||||

Minority interest in consolidated subsidiaries | $ | 2,288 | $ | 2,835 | ||||

Expense for the Three Months Ended September 30, | Expense for the Nine Months Ended September 30, | |||||||||||||||

| 2008 | 2007 | 2008 | 2007 | |||||||||||||

| AFC LLC | $ | 198 | $ | 130 | $ | 300 | $ | 458 | ||||||||

| Australian Country Cinemas | 58 | 18 | 116 | 71 | ||||||||||||

| Elsternwick Unincorporated Joint Venture | 8 | 16 | 27 | 34 | ||||||||||||

| LPP Property Trusts | (165 | ) | 59 | (74 | ) | 155 | ||||||||||

| Sutton Hill Properties | (14 | ) | (61 | ) | (124 | ) | (61 | ) | ||||||||

| Other (Big 4 Farming) | -- | -- | 1 | -- | ||||||||||||

Minority interest | $ | 85 | $ | 162 | $ | 246 | $ | 657 | ||||||||

Note 15 – Common Stock

Employee Stock Grants

On August 21, 2008, as part of their executive compensation, 37,388 shares of fully vested restricted Class A Non-Voting Common Stock was granted to three of our executives as stock bonuses having a grant date fair value of $286,000. As of September 30, 2008, these shares have yet to be issued to them and the executives have the option to accept the shares or to receive a reduced cash payment in lieu of shares.

As part of his compensation package, Mr. John Hunter, our Chief Operating Officer, was granted $100,000 of restricted Class A Non-Voting Common Stock on February 12, 2008 and 2007. These stock grants have vesting periods of two years and stock grant prices of $9.70 and $8.63, respectively. On February 11, 2008, $50,000 of restricted Class A Non-Voting Common Stock vested related to Mr. Hunter’s 2007 grant. The 5,794 shares related to this vesting have yet to be issued to him. As part of his compensation package, Mr. Laifman was granted $100,000 of Class A Non-Voting Common Stock or 10,638 shares upon acceptance of his employment agreement. This stock grant has a vesting period of two years.

Note 16 - Comprehensive Income (Loss)

U.S. GAAP requires that the effect of foreign currency translation adjustments and unrealized gains and/or losses on securities that are available-for-sale (“AFS”) be classified as comprehensive income (loss). The following table sets forth our comprehensive income (loss) for the periods indicated (dollars in thousands):

Three Months Ended September 30, | Nine Months Ended September 30, | |||||||||||||||

| 2008 | 2007 | 2008 | 2007 | |||||||||||||

| Net income (loss) | $ | (2,061 | ) | $ | 870 | $ | (2,006 | ) | $ | 1,858 | ||||||

| Foreign currency translation gain (loss) | (27,978 | ) | 1,948 | (21,210 | ) | 14,365 | ||||||||||

| Accrued pension | 71 | 76 | 214 | (2,524 | ) | |||||||||||

| Realized gain on AFS securities | -- | (549 | ) | -- | (773 | ) | ||||||||||

| Unrealized gain (loss) on AFS securities | (6 | ) | (880 | ) | (2 | ) | 82 | |||||||||

| Comprehensive income (loss) | $ | (29,974 | ) | $ | 1,465 | $ | (23,004 | ) | $ | 13,008 | ||||||

Note 17 – Derivative Instruments

The following table sets forth the terms of our interest rate swap derivative instruments at September 30, 2008:

| Type of Instrument | Notional Amount | Pay Fixed Rate | Receive Variable Rate | Maturity Date | |||||||||

| Interest rate swap | $ | 21,736,000 | 6.4400% | 7.8883% | December 31, 2008 | ||||||||

| Interest rate swap | $ | 12,903,000 | 6.6800% | 7.8883% | December 31, 2008 | ||||||||

| Interest rate swap | $ | 9,623,000 | 5.8800% | 7.8883% | December 31, 2008 | ||||||||

| Interest rate swap | $ | 2,766,000 | 6.3600% | 7.8883% | December 31, 2008 | ||||||||

| Interest rate swap | $ | 2,766,000 | 6.9600% | 7.8883% | December 31, 2008 | ||||||||

| Interest rate swap | $ | 2,213,000 | 7.0000% | 7.8883% | December 31, 2008 | ||||||||

| Interest rate swap | $ | 1,098,000 | 7.1900% | 7.8883% | December 31, 2008 | ||||||||

| Interest rate swap | $ | 2,221,000 | 7.5900% | 7.8883% | December 31, 2008 | ||||||||

| Interest rate swap | $ | 44,000,000 | 6.8540% | 6.6975% | April 1, 2011 | ||||||||

| Interest rate swap | $ | 1,186,000 | 8.2500% | 7.8883% | December 31, 2008 | ||||||||

In accordance with SFAS No. 133, Accounting for Derivative Instruments and Hedging Activities (“SFAS 133”), we marked our interest rate swap instruments to market on the consolidated balance sheet resulting in a $601,000 increase and a $215,000 decrease to interest expense during the three and nine months ended September 30, 2008, respectively, and a $76,000 and $186,000 increase to interest expense during the three and nine months ended September 30, 2007, respectively. At September 30, 2008 and December 31, 2007, we have recorded the fair market value of our interest rate swaps of $741,000 and $526,000, respectively, as an other noncurrent asset. In accordance with SFAS 133, we have not designated any of our current interest rate swap positions as financial reporting hedges.

As part of our GE Capital loan, we are required to swap 50% of our variable rate loan to fixed rate terms for a minimum period of two years. During April 2008, we entered into a swap contract starting with a maximum notional amount of $49.0 million to comply with this requirement. This notional swap balance is currently $44.0 million and is scheduled to reduce incrementally over the next two years until the balance reaches $28.0 million on January 1, 2011. The swap contract terminates on April 1, 2011.

Note 18 – Fair Value of Financial Instruments

| Book Value | Fair Value | |||||||||||

| Financial Instrument | Level | September 30, 2008 | September 30, 2008 | |||||||||

| Investment in marketable securities | 1 | $ | 4,085 | $ | 4,085 | |||||||

| Interest rate swaps asset | 2 | $ | 741 | $ | 741 | |||||||

SFAS 157 (see Note 1 – Basis of Presentation) establishes a fair value hierarchy that prioritizes the inputs to valuation techniques used to measure fair value. As presented in the table above, the statement requires that assets and liabilities carried at fair value be classified and disclosed in one of the following three categories:

Level 1: Quoted market prices in active markets for identical assets or liabilities.

Level 2: Observable market based inputs or unobservable inputs that are corroborated by market data.

Level 3: Unobservable inputs that are not corroborated by market data.

We use appropriate valuation techniques based on the available inputs to measure the fair values of our assets and liabilities. When available, we measure fair value using Level 1 inputs because they generally provide the most reliable evidence of fair value.

We used the following methods and assumptions to estimate the fair values of the assets and liabilities in the table above.

Level 1 Fair Value Measurements – are based on market quotes of our marketable securities.

Level 2 Fair Value Measurements – Interest Rate Swaps – The fair value of interest rate swaps are estimated using internal discounted cash flow calculations based upon forward interest rate curves, which are corroborated by market data, and quotes obtained from counterparties to the agreements.

Level 3 Fair Value Measurements – we do not have any assets or liabilities that fall into this category.

Note 19 – Acquisitions

Consolidated Entertainment Cinemas Acquisitions

In keeping with our business plan of being opportunistic in adding to our existing cinema portfolio, on February 22, 2008, we acquired 15 cinemas with 181 screens in Hawaii and California (the “Consolidated Entertainment” acquisition) from Pacific Theatres Exhibition Corp. and its affiliates (collectively, the “Sellers”) for $70.2 million. The purchase price was subsequently adjusted to $63.9 million as described below under post closing adjustments, which were applied to reduce the principal amount owed under financing provided by an affiliate of the Sellers (the “Nationwide Note 1”). The financing of the transaction included $48.4 million of debt from GE Capital, net of deferred financing costs of $1.6 million, a loan of $21.0 million as evidenced by the Nationwide Note 1, and $800,000 of cash from Reading (see Note 11 – Notes Payable for a more complete explanation of the GE debt and the Nationwide Note 1).