2019 Annual Stockholders Meeting May 7, 2019 Reading International 1

Reading International Disclaimers Our comments today may contain forward-looking statements and management may make additional forward-looking statements in response to your questions. Such written and oral disclosures are made pursuant to the Safe Harbor provision of the Private Securities Litigation Reform Act of 1995. Although we believe our expectations expressed in such forward- looking statements are reasonable, we cannot assure you that they will be realized. Investors are cautioned that such forward-looking statements involve risks and uncertainties that could cause actual results to differ materially from the anticipated results, and therefore we refer you to a more detailed discussion of the risks and uncertainties in the Company’s filings with the Securities & Exchange Commission. This presentation is intended to summarize the projects on which we are working and our plan for moving our Company forward. Many of the projects are in their early stages and will be subject to various Governmental and Board approvals. Accordingly, no assurances can be given that the plans discussed herein will be achieved. Further, some of the design concepts included in this presentation include proposed architectural renderings that represent works in progress. 2

Financial Reconciliations We use EBITDA in the evaluation of our Company’s performance since we believe that EBITDA provides a useful measure of financial performance and value. We believe this principally for the following reasons: We believe that EBITDA is an accepted industry-wide comparative measure of financial performance. It is, in our experience, a measure commonly adopted by analysts and financial commentators who report upon the cinema exhibition and real estate industries, and it is also a measure used by financial institutions in underwriting the creditworthiness of companies in these industries. Accordingly, our management monitors this calculation as a method of judging our performance against our peers, market expectations and our creditworthiness. It is widely accepted that analysts, financial commentators and persons active in the cinema exhibition and real estate industries typically value enterprises engaged in these businesses at various multiples of EBITDA. Accordingly, we find EBITDA valuable as an indicator of the underlying value of our businesses. We expect that investors may use EBITDA to judge our ability to generate cash, as a basis of comparison to other companies engaged in the cinema exhibition and real estate businesses and as a basis to value our company against such other companies. EBITDA is not a measurement of financial performance under generally accepted accounting principles in the United States of America and it should not be considered in isolation or construed as a substitute for net income or other operations data or cash flow data prepared in accordance with generally accepted accounting principles in the United States for purposes of analyzing our profitability. The exclusion of various components, such as interest, taxes, depreciation and amortization, limits the usefulness of these measures when assessing our financial performance, as not all funds depicted by EBITDA are available for management’s discretionary use. For example, a substantial portion of such funds may be subject to contractual restrictions and functional requirements to service debt, to fund necessary capital expenditures and to meet other commitments from time to time. EBIT and EBITDA also fail to take into account the cost of interest and taxes. Interest is clearly a real cost that for us is paid periodically as accrued. Taxes may or may not be a current cash item but are nevertheless real costs that, in most situations, must eventually be paid. A company that realizes taxable earnings in high tax jurisdictions may, ultimately, be less valuable than a company that realizes the same amount of taxable earnings in a low tax jurisdiction. EBITDA fails to take into account the cost of depreciation and amortization and the fact that assets will eventually wear out and have to be replaced. In addition to EBIT and EBITDA, we also use Adjusted EBITDA. Adjusted EBITDA – using the principles we consistently apply to determine our EBIDTA, we further adjusted the EBIDTA for certain items we believe to be external to our business and not reflective of our costs of doing business or results of operation. Specifically, we have adjusted for (i) gains on insurance recoveries, (ii) legal expenses relating to extraordinary litigation, (iii) adjustments for gains/losses relating to property sales, and (iv) any other items that can be considered non-recurring in accordance with the 2-year SEC requirement for determining an item is non-recurring, infrequent or unusual in nature. 3

Our Mission Cinema & Real Estate THROUGH CURATION AND CUSTOMIZATION, OUR MISSION IS TO CREATE ENGAGING EXPERIENCES THAT ENRICH AND GROW OUR COMMUNITIES. 4

Cinema Portfolio 60 Theaters 484 screens in US, AU & NZ 4 Brands Reading Cinemas (US, AU & NZ) Consolidated Theatres (Hawaii) Angelika Film Centers (US) City Cinemas (NYC) Geographic Footprint United States: 27 theaters in 6 states & DC 10th largest US exhibitor Australia: 22 theaters in 6 states 4th largest AU exhibitor New Zealand: 11 theaters in North & South Island 3rd largest NZ exhibitor Diversified Programming US - Leading exhibitor in both commercial and specialty film and curated content LEADING CINEMA AND READ ESTATE COMPANY DIERSIFIED OWNER/OPERATOR OF ENTERTAINMENT & REAL ESTATE ASSETS REAL ESTATE PORTFOLIO 7 Value Creation Projects US, AU & NZ11 Operating Properties US, AU & NZ, including 2 Off Broadway Live Theatres in NYC & 1 in Chicago3 Future Long-Term Value Creation Projects US & NZ *As of March 31, 2019 5

WELL POSITIONS TO CREATE LONG-TERM STOCKHOLDER VALUE Complementary Cinema & Real Estate portfolios offer compelling strategic and financial benefits. Cinemas provide steady cash flow to support real estate development focused on driving long-term stockholder value. Continue to grow that cash flow by elevating the cinema guest experience and further grow our audience by improving customization. State-of-the-art presentation and sound exhibit our well curated programming in venues where our guests can also enjoy the comforts of luxury recliner seating and the tastes of crafted food & drinks. At the same time, our engaging digital platforms create customized and enhanced guest experiences. Maximize the value in our existing real estate by creating centres offering a curated mix of tenants and events in spaces that build community and, at the same time, allow for engaging personalized experiences. Disciplined focus on elements of risk in existing opportunities and pursuit of new opportunities builds both cash flow and long term tangible value. 6

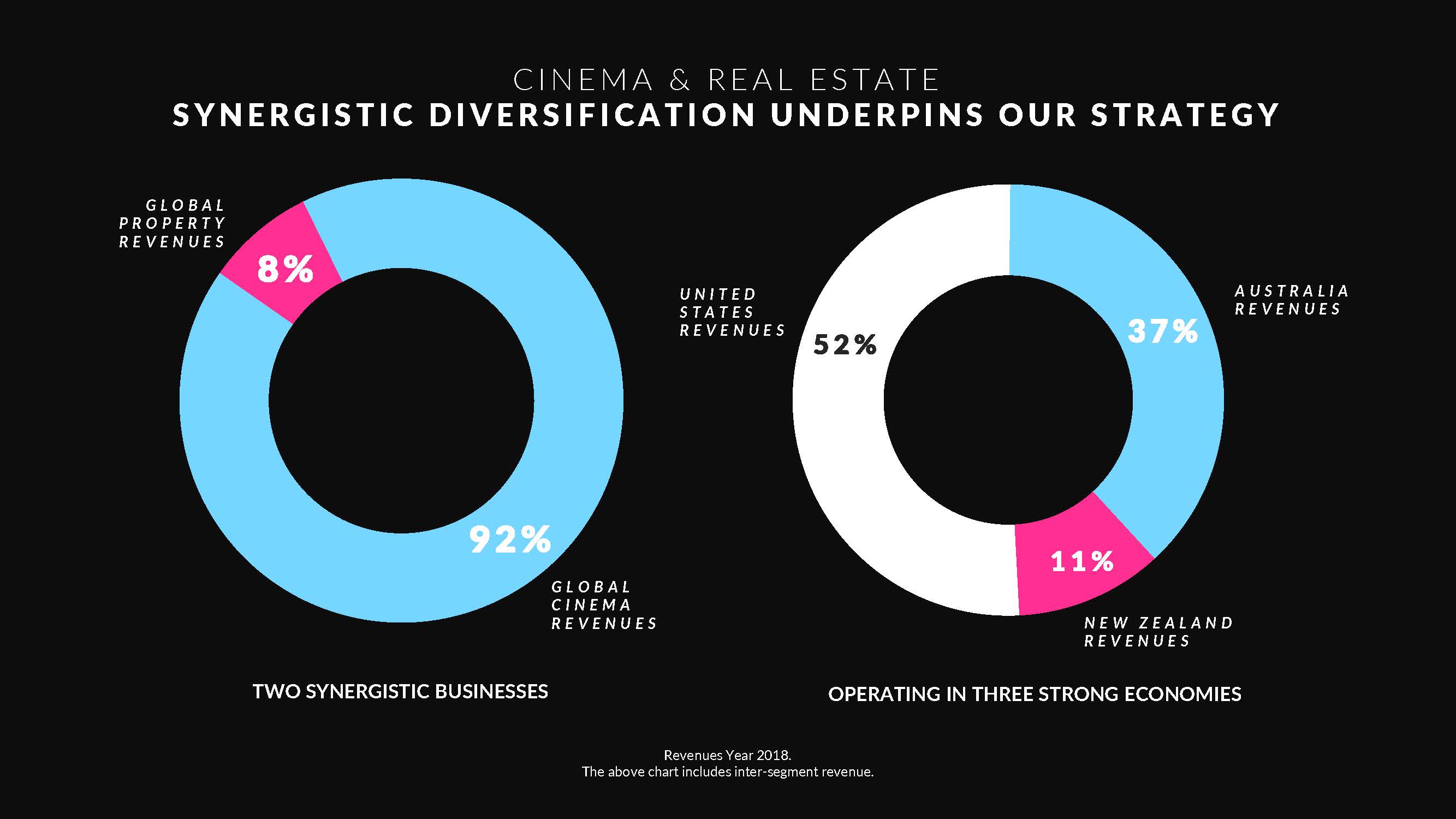

CINEMA & REAL ESTATE SYNERGISTIC DIVERSIFICATION UNDERPINS OUR STRATEGY Global Property Revenues 8% Global Cinema Revenues 92% Two Synergistic Businesses United States Revenues 52% Australia Revues 37% New Zealand Revenues 11% Operating in Three Strong Economies Revenues Year 2018. The above chart includes inter-segment revenue. 7

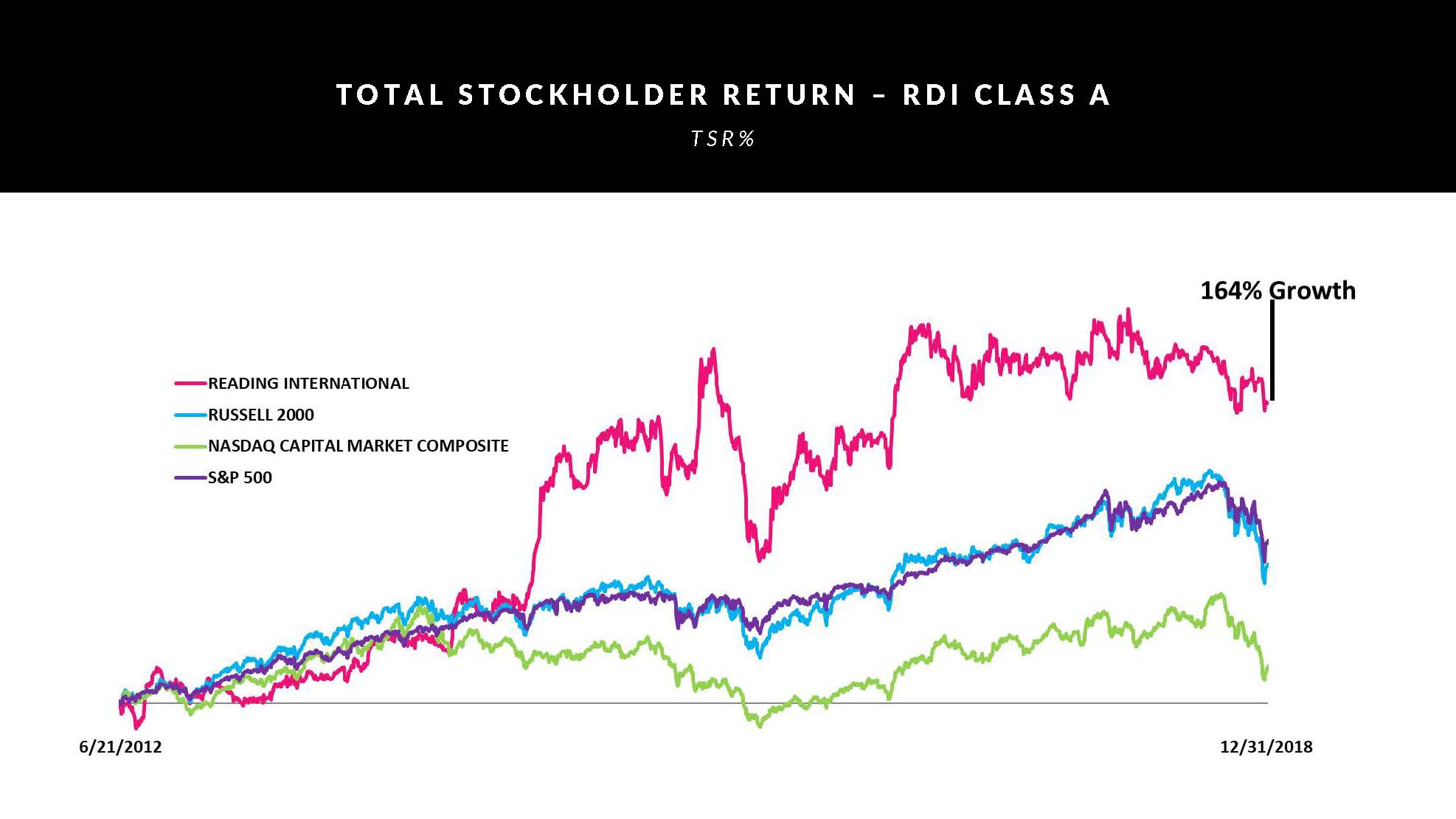

TOTAL STOCKHOLDER RETURN – RDI CLASS A TSR% Reading International Russell 2000 Nasdaq Capital Market Composite S&P 500 164% Growth 6/21/2012 12/31/2018 8

Core Values & Guiding Principals Inspired By Our Founder ENTREPRENEURIAL approach to our business EDUCATED analysis underpins our strategies ENGAGING our guests is paramount to our success EXECUTION is a focus of our three-year strategy EXTENDED VIEW means pursuing a long-term value strategy EMPATHETIC approach to our stakeholders James J. Cotter, Sr. 9

2018 Record Operational Year Financial Highlights 11% Revenue Growth 16% Operating Income Growth 10

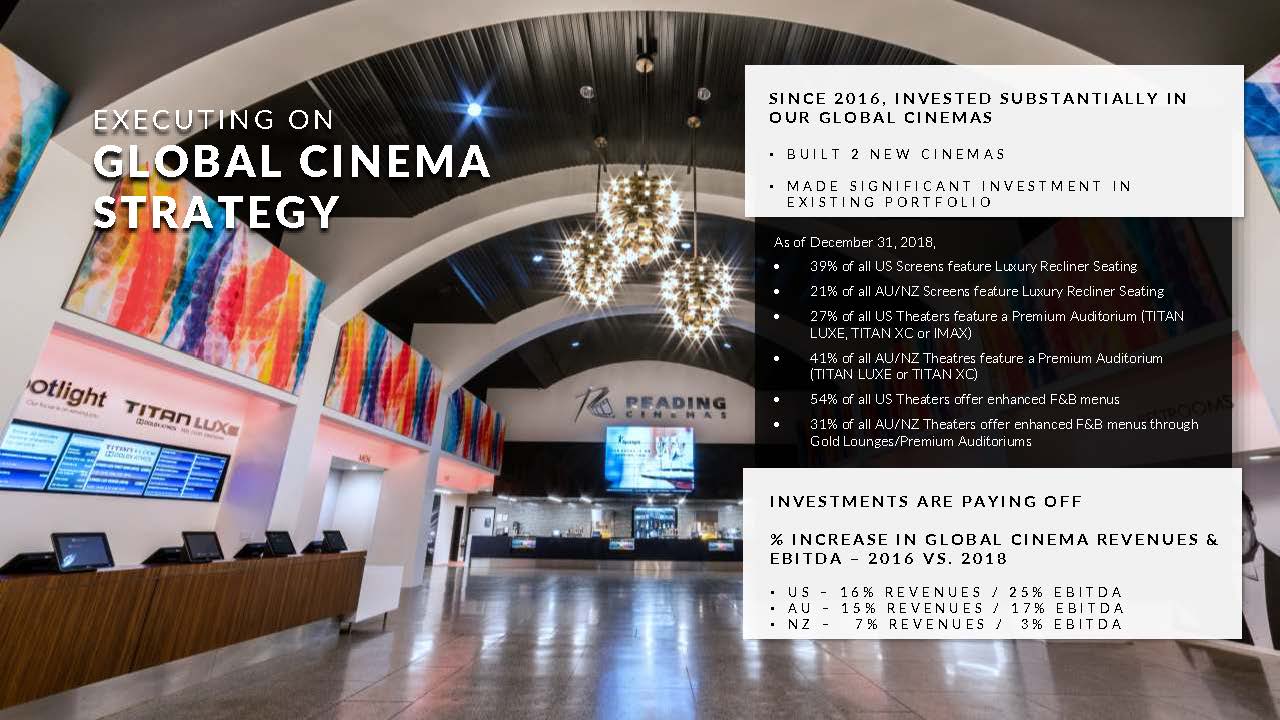

Executing on Global Cinema Strategy Since 2016, Invested Substantially In Our Global Cinemas Built 2 New Cinemas Made Significant Investment in Existing Portfolio As of December 31, 2018, 39% of all US Screens feature Luxury Recliner Seating 21% of all AU/NZ Screens feature Luxury Recliner Seating 27% of all US Theaters feature a Premium Auditorium (TITAN LUXE, TITAN XC or IMAX) 41% of all AU/NZ Theatres feature a Premium Auditorium (TITAN LUXE or TITAN XC) 54% of all US Theaters offer enhanced F&B menus 31% of all AU/NZ Theaters offer enhanced F&B menus through Gold Lounges/Premium Auditoriums Investments Are Paying Off & Increase in Global Cinema Revenues & EBITDA – 2016 VS. 2018 US – 16% REVENUES/ 25% EBITDA AU- 15% REVENUES/ 17% EBITDA NZ- 7% REVENUES/ 3% EBITDA 11

Executing on Global Real Estate Strategy Completed expansion of Newmarket Village in Brisbane in Q1 2018, which added 52,668 leaseable SF inclusive of a new 8 screen Reading Cinema and 10,355 SF of third party space Acquired the strategically located Telstra property that directly abuts Redyard in Auburn (NSW) Increased total leasable area in the Australia Real Estate Portfolio by 41,904 SF (not including the Newmarket cinema) since Jan 2017 Rationalized our landholding at Cannon Park, by acquiring ownership and control of shared title property Invested roughly $3M upgrading existing centers to ensure long term sustainable value Completing the redevelopment of 44 Union Square, an iconic property in New York City 12

GLOBAL CINEMA DIVISION 13

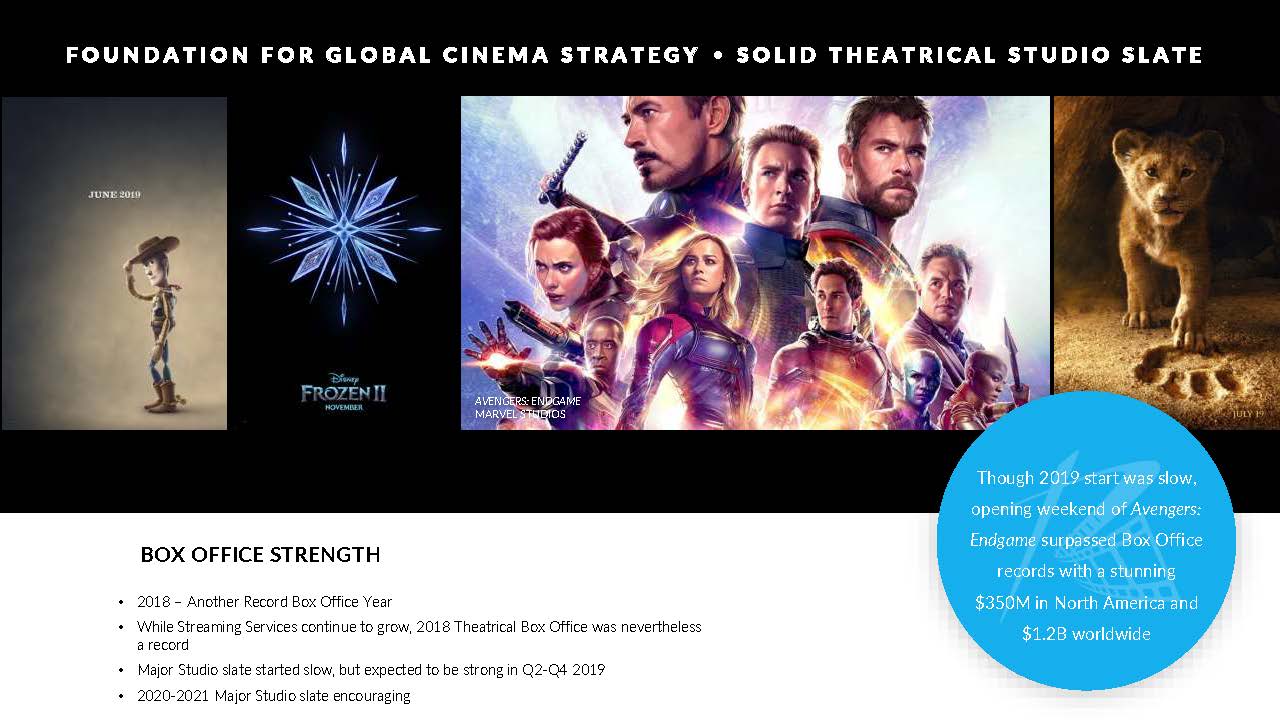

FOUNDATION FOR GLOBAL CINEMA STRATEGY SOLID THEATRICAL STUDIO SLATE BOX OFFICE STRENGTH 2018 – Another Record Box Office Year While Streaming Services continue to grow, 2018 Theatrical Box Office was nevertheless a record Major Studio slate started slow, but expected to be strong in Q2-Q4 2019 2020-2021 Major Studio slate encouraging Though 2019 start was slow, opening weekend of Avengers: Endgame surpassed Box Office records with a stunning $350M in North America and $1.2B worldwide 14

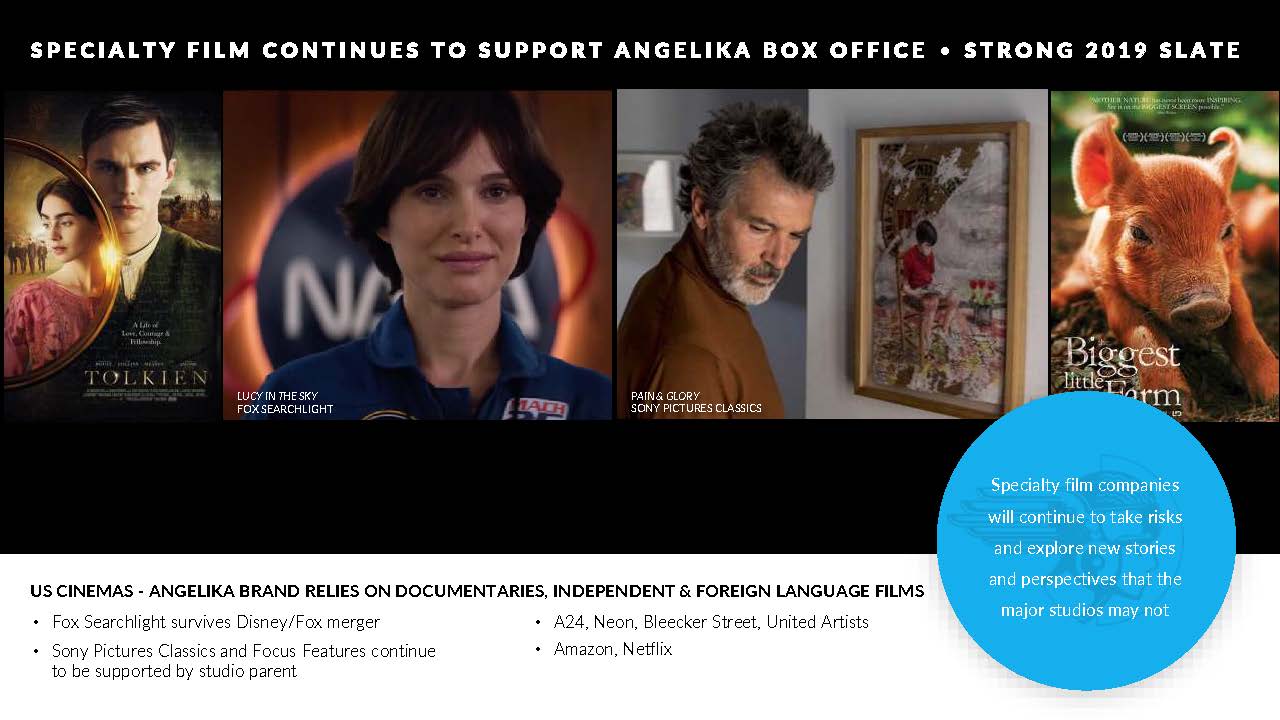

Specialty Film Continues to Support Angelika Box Office Strong 2019 Slate US Cinemas – Angelika Brand Relies on Documentaries, Independent & Foreign Language Films Fox Searchlight survives Disney/Fox merger Sony Pictures Classics and Focus Features continue to be supported by studio parent A24, Neon, Bleecker Street, United Artists Amazon, Netflix Specialty film companies will continue to take risks and explore new stories and perspectives that the major studios may not 15

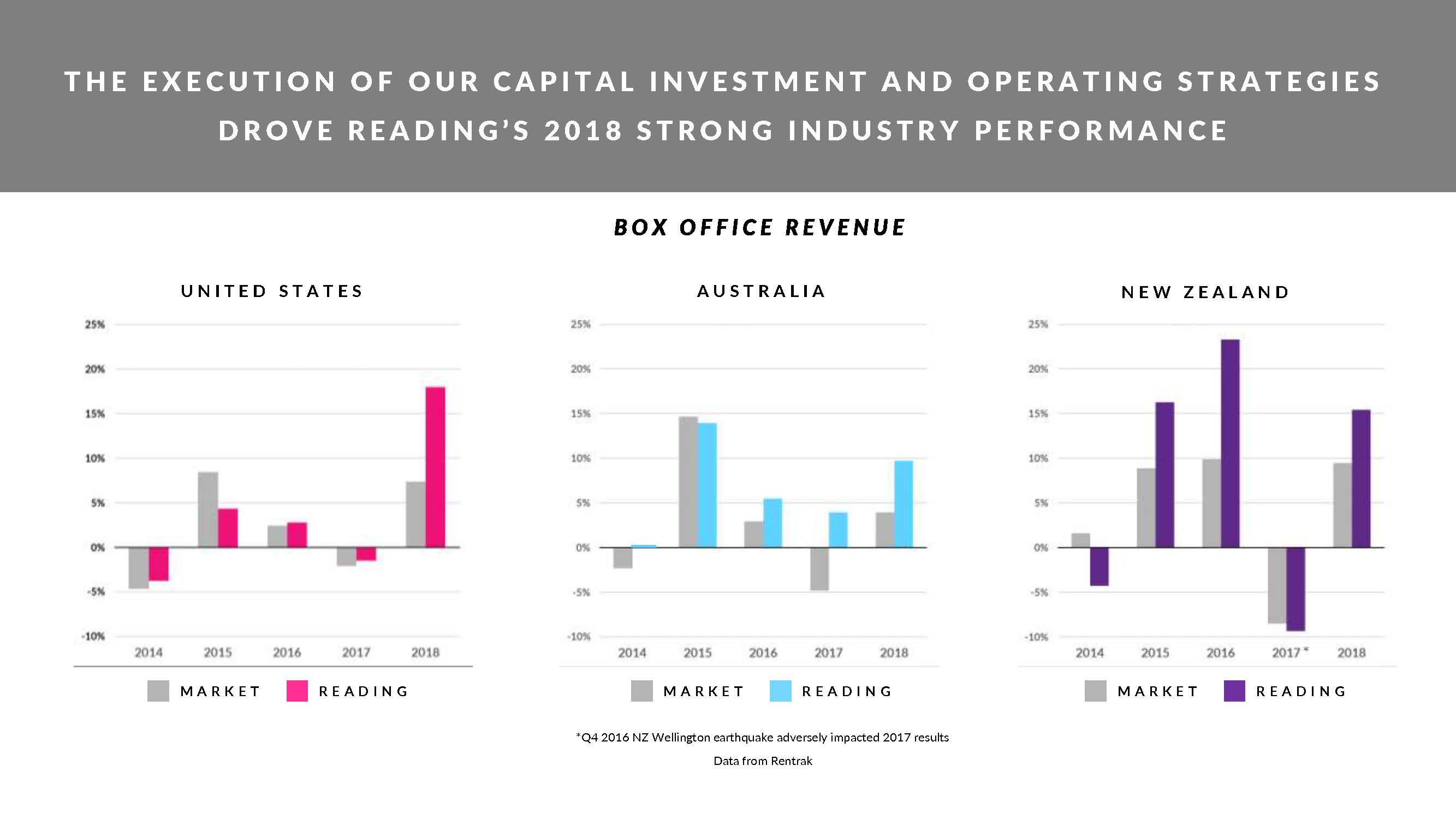

The Execution Of Our Capital Investment And Operating Strategies Drove Reading’s 2018 Strong Industry Performance United States 25% 20% 15% 10% 5% 0% -5% -10% 2014 2015 2016 2017 2018 Market Reading Australia 25% 20% 15% 10% 5% 0% -5% -10% 2014 2015 2016 2017 2018 Market Reading New Zealand 25% 20% 15% 10% 5% 0% -5% -10% 2014 2015 2016 2017 2018 Market Reading *Q4 2016 NZ Wellington earthquake adversely impacted 2017 results Data from Rentrak 16

Reading Cinemas Consolidated Theaters Angelika Film Center & Café City Cinemas Global Cinema Strategy Re-invest in existing portfolio Pursue Company growth through new developments and financially sound acquisitions Improve Theater Level Cash Flow 17

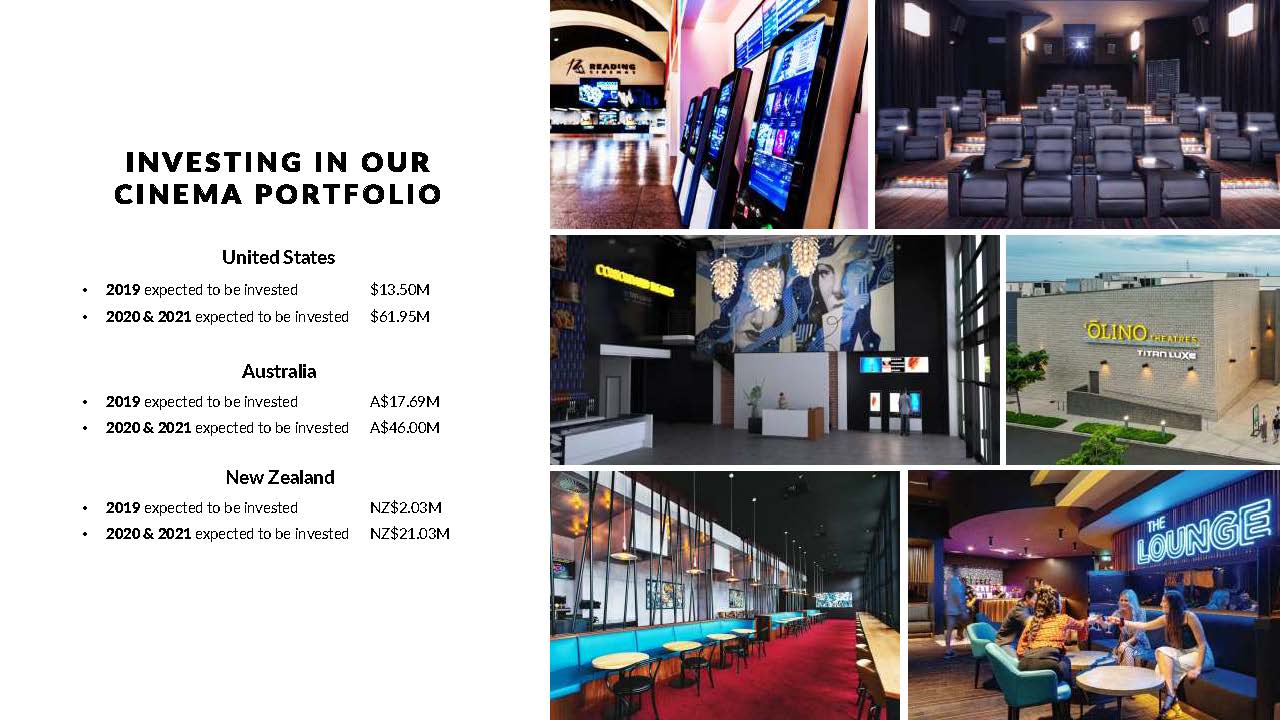

Investing in Our Cinema Portfolio United States 2019 expected to be invested $13.50M 2020 & 2021 expected to be invested $61.95M Australia 2019 expected to be invested A$17.69M 2020 & 2021 expected to be invested A%46.00M New Zealand 2019 expected to be invested NZ$2.03M 2020 & 2021 expected to be invested NZ$21.03M 18

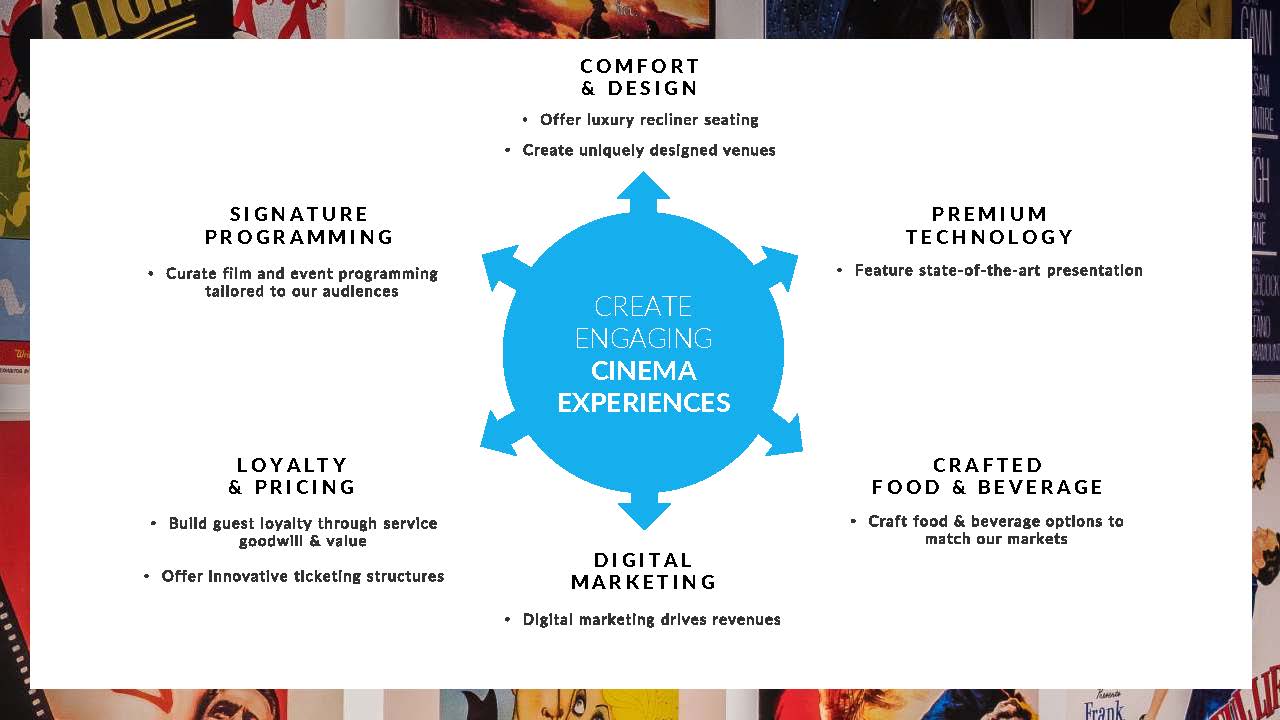

CREATE ENGAGING CINEMA EXPERIENCES Comfort and Design Offer luxury recliner seating Create uniquely designed venues Premium Technology Feature state-of-the-art presentation Crafted Food and Beverage Craft food & beverage options to match our markets Digital Marketing Digital marketing dries revenues Loyalty & Pricing Build guest loyalty through service goodwill & value Offer innovative ticketing structure Signature Programming Curate film and event programming tailored to our audiences 19

Recliner Seating Continues to Drive Attendance & Ticket Price PERCENTAGE OF US SCREENS WITH LUXURY RECLINERS TODAY 39% By end of 2019 42% By end of 2020 59% By end of 2021 81% Percentage of AU/NZ Screes with Luxury Reclines Today 21% By end of 2019 27% By end of 2020 32% By end of 2021 40% 20

PREMIUM PRESENTATION CONTINUES TO DRIVE ATTENDANCE & TICKET PRICE PERCENTAGE OF US CINEMAS WITH AT LEAST ONE PREMIUM SCREEN Today 27% By end of 2019 31% By end of 2020 42% By end of 2021 46% PERCENTAGE OF AU/NZ CINEMAS WITH AT LEAST ONE PREMIUM SCREEN Today 41% By end of 2019 55% By end of 2020 64% By end of 2021 72% 21

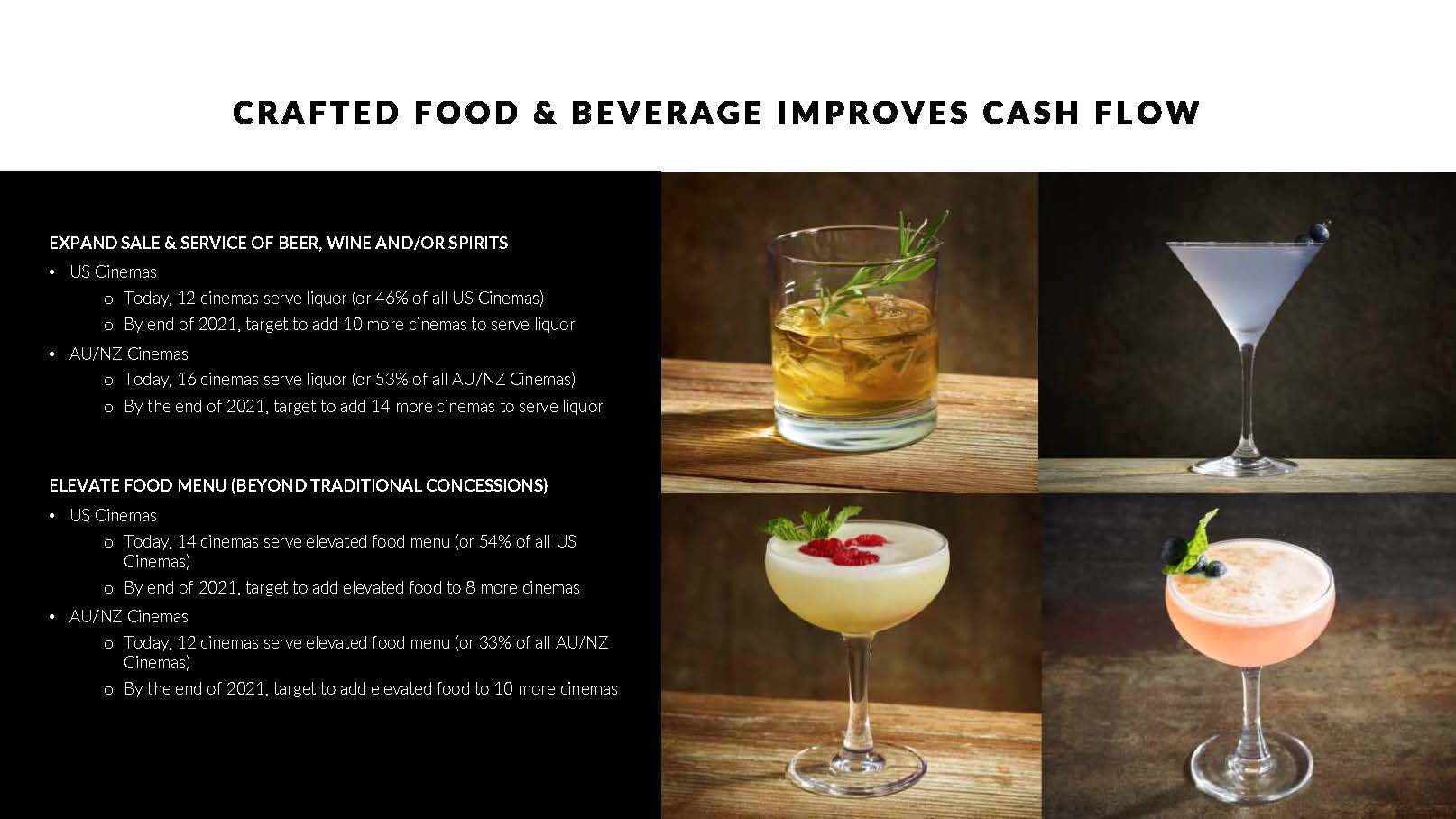

CRAFTED FOOD AND BEVERAGE IMPROVES CASH FLOW Expand Sale and Service of Beer, Wine And/ Or Spirits US Cinemas Today, 12 cinemas serve liquor (or 46% of all US Cinemas) By end of 2021, target to add 10 more cinemas to serve liquor AU/NZ Cinemas Today, 16 cinemas serve liquor (or 53% of all AU/NZ Cinemas) By the end of 2021, target to add 14 more cinemas to serve liquor Elevate Food Menu (Beyond Traditional Concessions) US Cinemas Today, 14 cinemas serve elevated food menu (or 54% of all US Cinemas) By end of 2021, target to add elevated food to 8 more cinemas AU/NZ Cinemas Today, 12 cinemas serve elevated food menu (or 33% of all AU/NZ Cinemas) By the end of 2021, target to add elevated food to 10 more cinemas 22

US Cinemas Per Cap Continue Improving US Cinema SF&BPERCAPITA 2008 $3.16 2009 $3.28 2010$3.31 2011 $3.38 2012 $3.55 2013 $3.69 2014 $3.78 2015 $4.08 2016 $4.49 2017 $4.78 2018 $4.99 2018 Laser focus on Food Quality & Consistency lead to the Angelika Film Center Carmel Mountain hamburger being voted a “Favorite” by Readers of the San Diego Union Tribune San Diego’s Favorite Union-Tribune Readers Poll 2018 23

DINE-IN SERVICES DRIVES REVENUE US CINEMAS Today, only one US Cinema features SPOTLIGHT service (waiters serve elevated food & liquor in intimately sized auditoriums) Throughout 2019-2021, evaluate other US cinemas/new builds for SPOTLIGHT opportunities AU/NZ CINEMAS Today, 9 cinemas (or 30% of all AU/NZ Cinemas) feature GOLD LOUNGE service (waiters serving elevated food & liquor in intimately sized auditoriums) GOLD LOUNGE in AU/NZ drives not only F&B per caps, but also ticket prices, are typically more than double the general admission price By the end of 2021, target to feature GOLD LOUNGE service in 11 cinemas Gold Lounge Cinema Spotlight 24

INNOVATIVE PRICING CONTINUES TO DRIVE ATTENDANCE In AU/NZ, a compelling value-based ticket pricing structure, with a simple, clear marketing plan, continues to be the foundation for circuit distinction and strength Continue monitoring cinema competition for Value Pricing matching Value Price is specific to amenity and market-by- market US pricing decisions made market-by-market due to US circuit’s geographic and programming diversity Attendance improved significantly at select US Cinemas where we launched reasonably priced general admission ticket structure, coupled with concession discounts Adding Value Pricing to other US Cinemas by end of 2019 Exploring Subscription Service Model and expected to launch US test cinema by end of 2019 ‘OHANA SUNDAYS FAMILY SNACK PACK ENDLESS.. KAPOLE! KOKO MARINA KOOLAU $6 ENDLESS POPCORN ALL AGES. ALL MOVES. $8.50 TICKETS 25

DIGITAL MARKETING DRIVES INCREASED REVENUES Online Convenience Fee Revenue F&B Revenue Other Revenue Organic Audience Growth 26

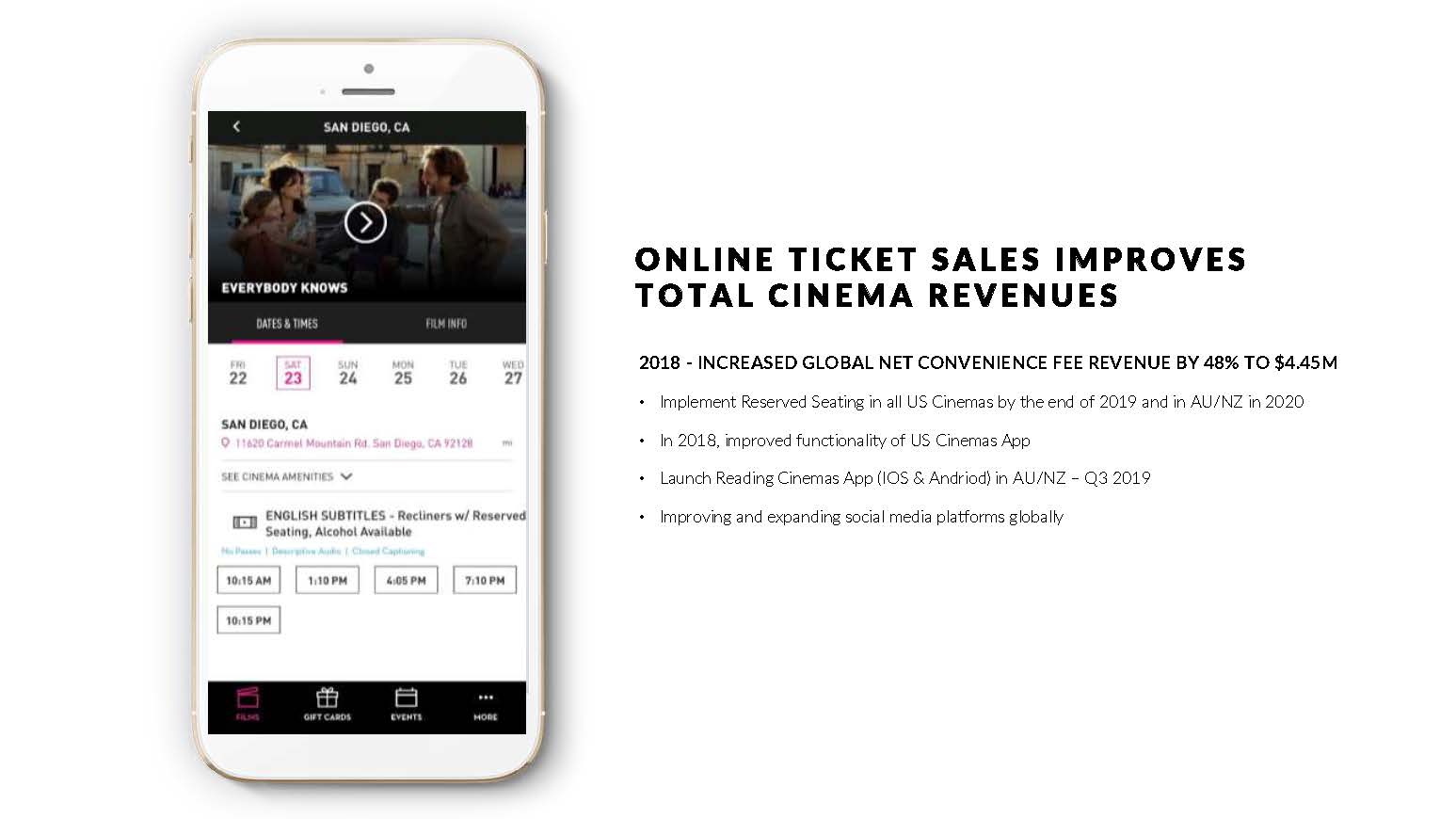

ONLINE TICKET SALES IMPROVES TOTAL CINEMA REVENUES 2018 – Increased Global Net Convenience Fee Revenue by 48% TO $4.45M Implement Reserved Seating in all US Cinemas by the end of 2019 and in AU/NZ in 2020 In 2018, improved functionality of US Cinemas App Launch Reading Cinemas App (IOS & Andriod) in AU/NZ – Q3 2019 Improving and expanding social media platforms globally 27

DIGITAL MARKETING DRIVES OTHER REVEUES Online Gift Card Sales (Email & Mail) Launch AU/NZ E-Cards in 2019 Launch some form of F&B online sales by Q1 2020 Ensure that entire F&B menu available for online purchase by 2021 With global cinema attendance over 21M and an expanding global digital infrastructure, we are exploring development of another revenue stream - third party advertising/sponsorship Elevate AngelikaBlog.com with a view to improving the quality of content focused on the independent theatrical experience, our films, food & drink and in-theater events (i.e. Q&As) 28

CURATE FILM & EVENT PROGRAMMING TAILORED TO OUR AUDIENCES Continue to generate incremental revenues through the curation of signature programming Alternative Content emphasis Japanese anime, foreign language films, music movies, cultural events Exclusively programmed repertory series, coupled with events or engagements Executed by our global programming and marketing teams Our simple marketing formulas are easily overlaid across our programs, series, titles & events Booked in advance and marketed across our own platforms, with no incremental advertising spend Increase Revenues through Theater Rentals (Film Festivals, Premieres, Screenings, Corporate Presentations) 29

CONTINUED DISCIPLINED APPROACH TO PURSUING NEW OPPORTUNITIES – AUSTRALIA FOUR NEW READING CINEMAS ARE UNDER CONTRACT IN AUSTRALIA Burwood Brickworks developed by Frasers – Expected to open late 2019 Our first AU cinema with recliners in all 6 screens Melbourne’s first premium TITAN LUXE with DOLBY ATMOS Our first cinema to feature all laser projection Enhanced F&B throughout cinema In the world’s first retail development to achieve Living Building Challenge™ certification (it will generate more energy than it consumes annually). Direct Factory Outlets at Jindalee (QLD) – Expected to open late 2020 6 screens Include one TITAN LUXE and 3 GOLD LOUNGE Traralgon, outside of Melbourne – Expected to open mid 2020 5 screens South City Square, Brisbane – Expected to open 2021 8 screens 3 GOLD LOUNGE 30

GLOBAL REAL ESTATE DIVISION 31

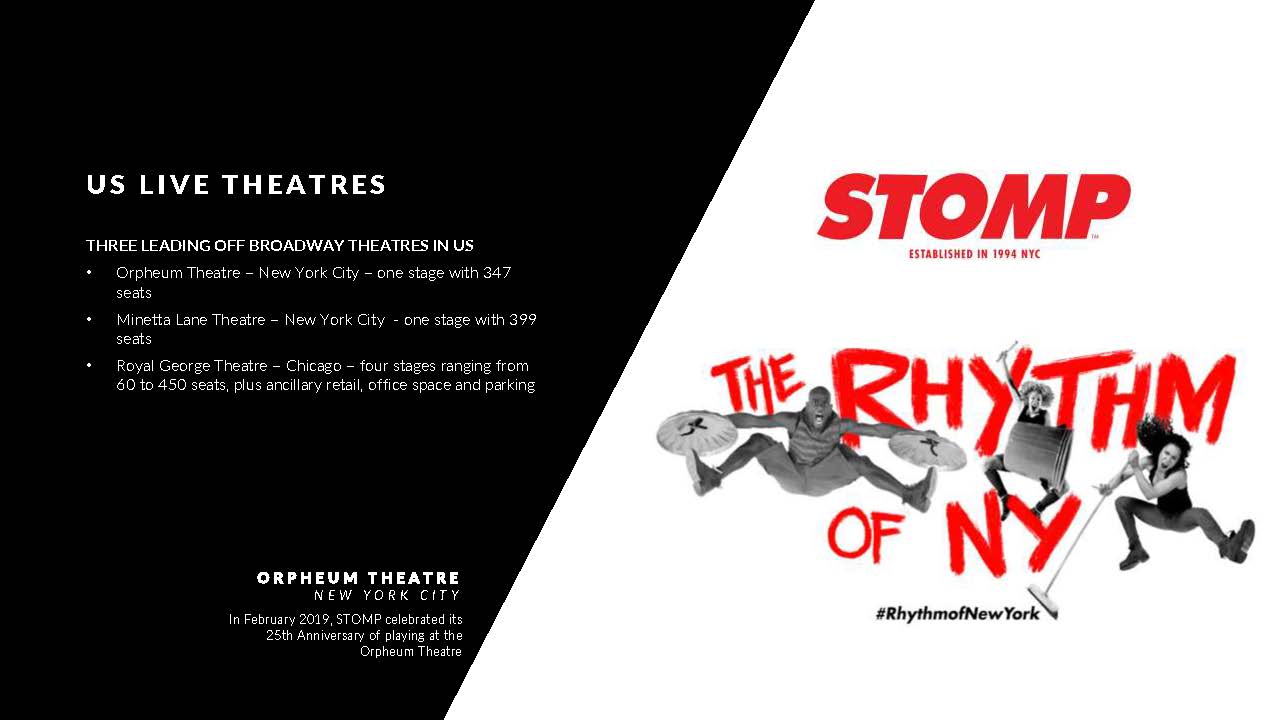

US LIVE THEATRES Three Leading Off Broadway Theatres In US Orpheum Theatre – New York City – one stage with 347 seats Minetta Lane Theatre – New York City - one stage with 399 seats Royal George Theatre – Chicago – four stages ranging from 60 to 450 seats, plus ancillary retail, office space and parking STOMP ESTABLISHED IN 1994 NYC THE RHYTHM OF NY #RhythmofNewYork ORPHEUM THEATRE NEW YORK CITY In February 2019, STOMP celebrated its 25th Anniversary of playing at the Orpheum Theatre 32

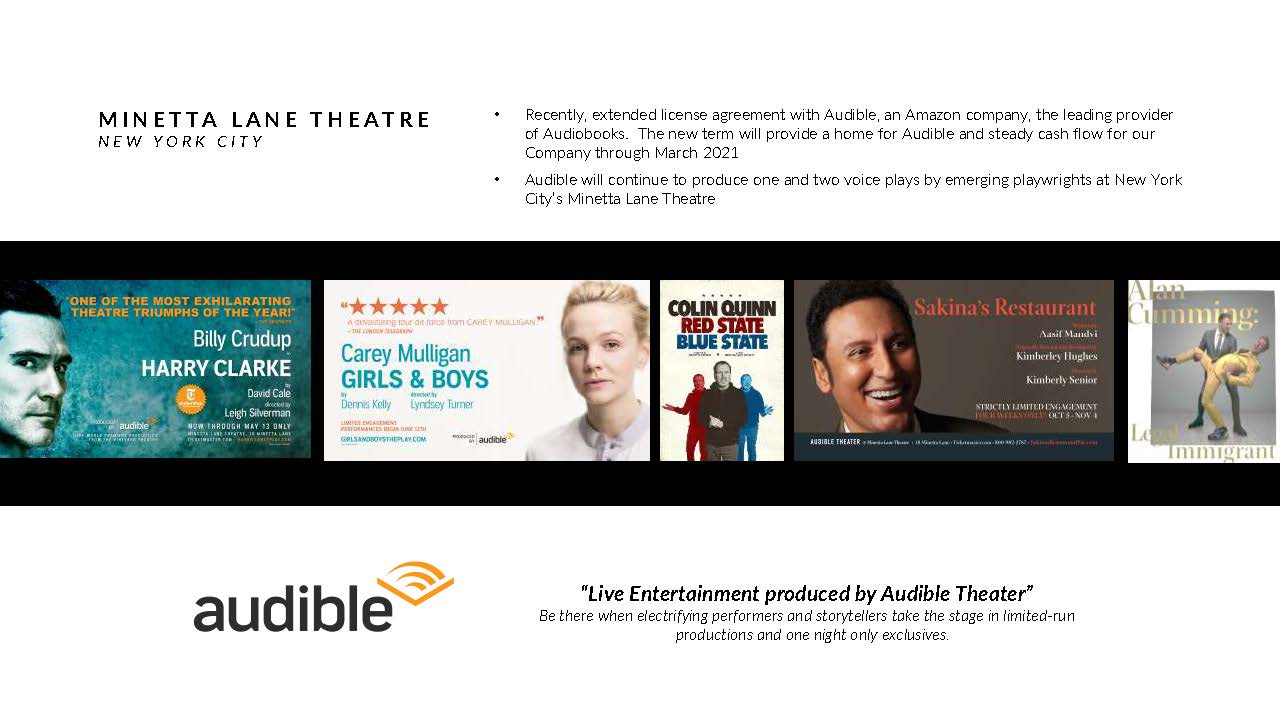

MINETTA LANE THEATRE NEW YORK CITY Recently, extended license agreement with Audible, an Amazon company, the leading provider of Audiobooks. The new term will provide a home for Audible and steady cash flow for our Company through March 2021 Audible will continue to produce one and two voice plays by emerging playwrights at New York City’s Minetta Lane Theatre audible “Live Entertainment produced by Audible Theater” Be there when electrifying performers and storytellers take the stage in limited-run productions and one night only exclusives. 33

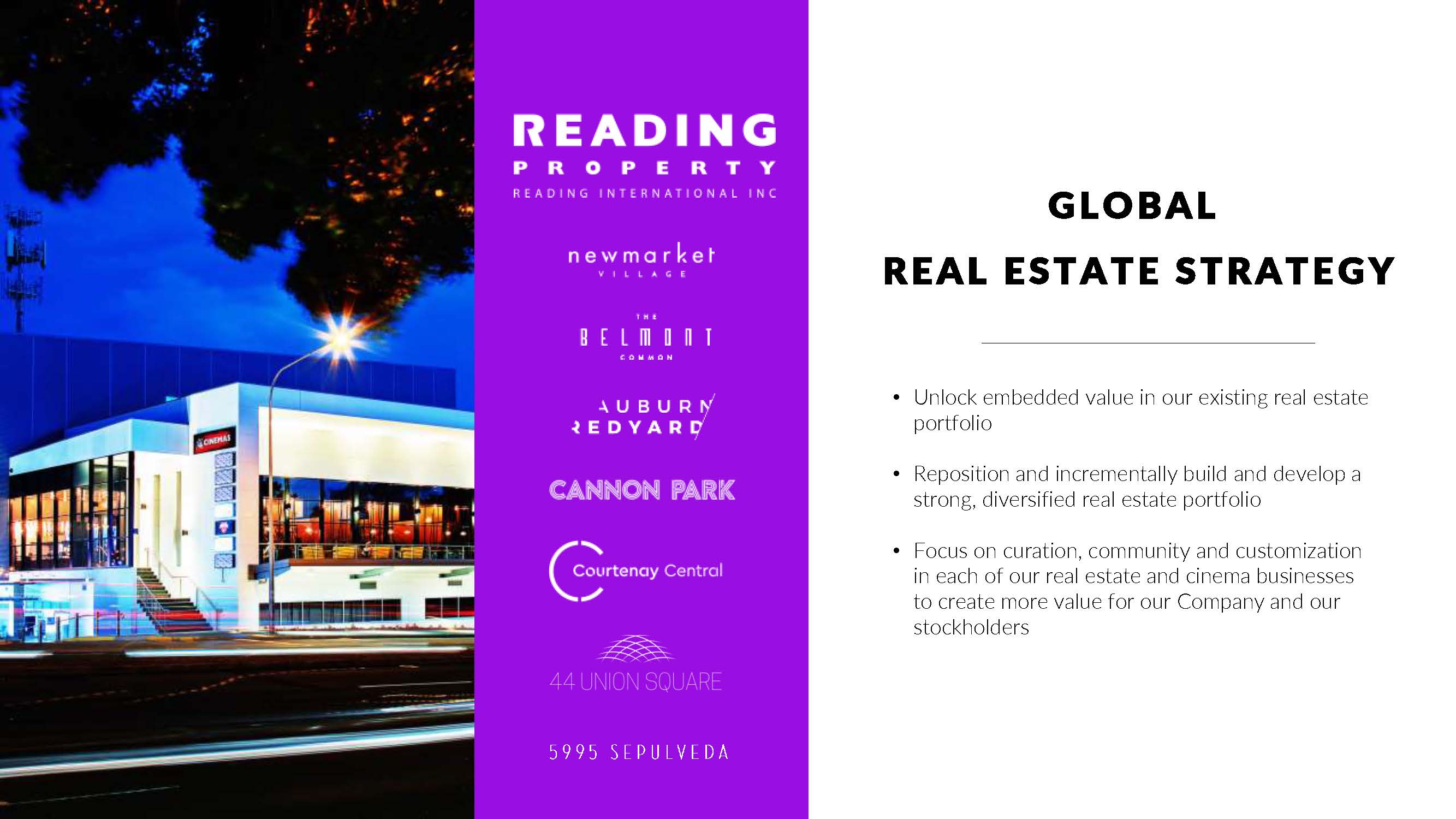

GLOBAL REAL ESTATE STRATEGY Unlock embedded value in our existing real estate portfolio Reposition and incrementally build and develop a strong, diversified real estate portfolio Focus on curation, community and customization in each of our real estate and cinema businesses to create more value for our Company and our stockholders Reading Property Reading International, Inc newmarket Village The Belmont Common Auburn Redyard Cannon Park Courtenay Central 44 Union Square 5995 Sepulveda 34

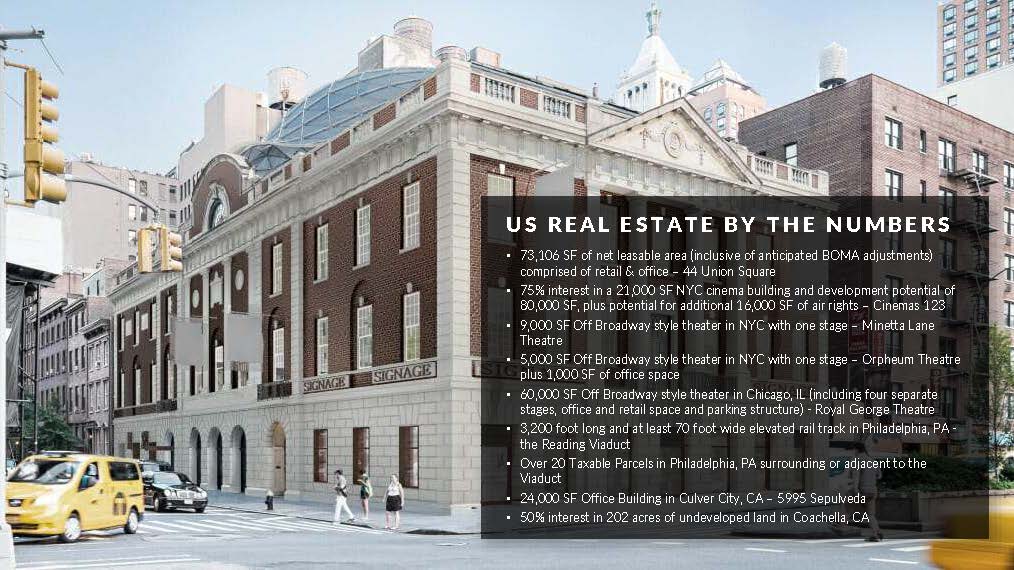

US REAL ESTATE BY THE NUMBERS 73,106 SF of net leasable area (inclusive of anticipated BOMA adjustments) comprised of retail & office – 44 Union Square 75% interest in a 21,000 SF NYC cinema building and development potential of 80,000 SF, plus potential for additional 16,000 SF of air rights – Cinemas 123 9,000 SF Off Broadway style theater in NYC with one stage – Minetta Lane Theatre 5,000 SF Off Broadway style theater in NYC with one stage – Orpheum Theatre plus 1,000 SF of office space 60,000 SF Off Broadway style theater in Chicago, IL (including four separate stages, office and retail space and parking structure) - Royal George Theatre 3,200 foot long and at least 70 foot wide elevated rail track in Philadelphia, PA - the Reading Viaduct Over 20 Taxable Parcels in Philadelphia, PA surrounding or adjacent to the Viaduct 24,000 SF Office Building in Culver City, CA – 5995 Sepulveda 50% interest in 202 acres of undeveloped land in Coachella, CA 35

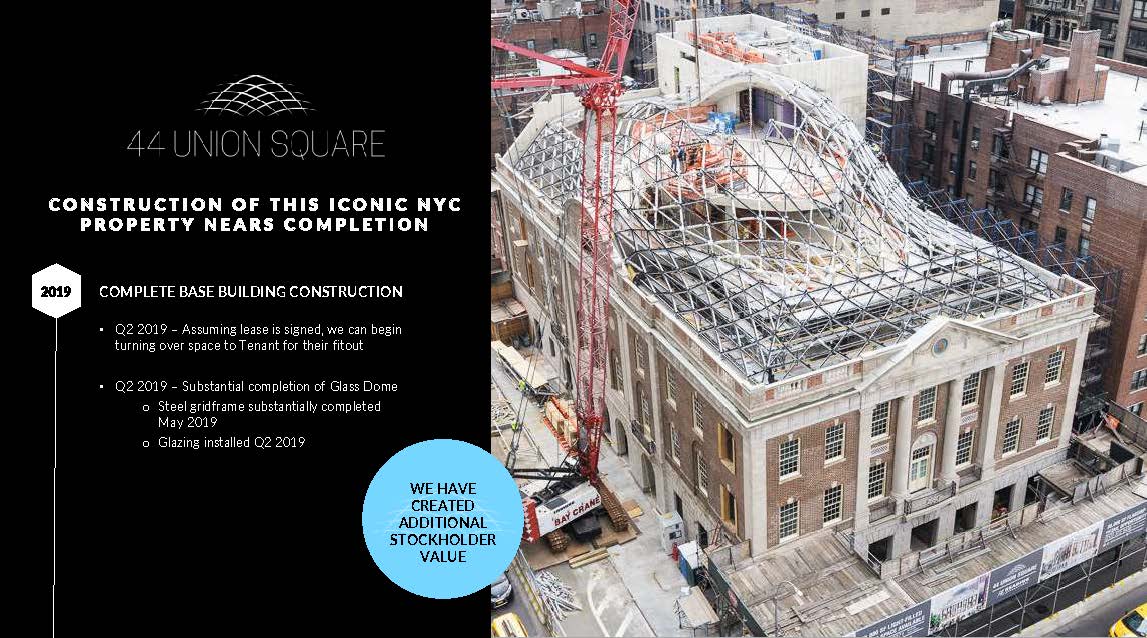

44 UNION SQUARE CONSTRUCTION OF THIS ICONIC NYC PROPERTY NEARS COMPLETION 2019 Complete Base Building ConstructionQ2 2019 – Assuming lease is signed, we can begin turning over space to Tenant for their fitout Q2 2019 – Substantial completion of Glass Dome Steel gridframe substantially completed May 2019 Glazing installed Q2 2019 We have created additional stockholder value 36

44 UNION SQUARE LEASING OF THIS ICONIC NYC PROPERTY UNDERWAY 2019 cont’d Approx. 90% of net leasable area Executed Letter of Intent with credit tenant Currently in lease negotiation Remaining 7,200 SF on ground floor will be retail 2020-2021 Expected completion of “rent concession” period Replace construction financing with permanent financing We are Creating Even More Stockholder Value 37

CINEMAS 123 “GO IT ALONE” STRATEGY – 2021 IRREPLACEBLA PROPERTY ACROSS FROM BLOOMINGDALES IN NYC Complete evaluation of major foundational issues Subway Excavation and ability to create below grade floors Pursue and potentially buy inclusionary air rights to maximize development potential With inclusionary rights, we can build maximum of approximately 96,000 RSF File re-zoning application for a best-in-class cinema as a part of redevelopment (estimated two year process) IKEA Metro Store opened next door to the Cinemas 123 38

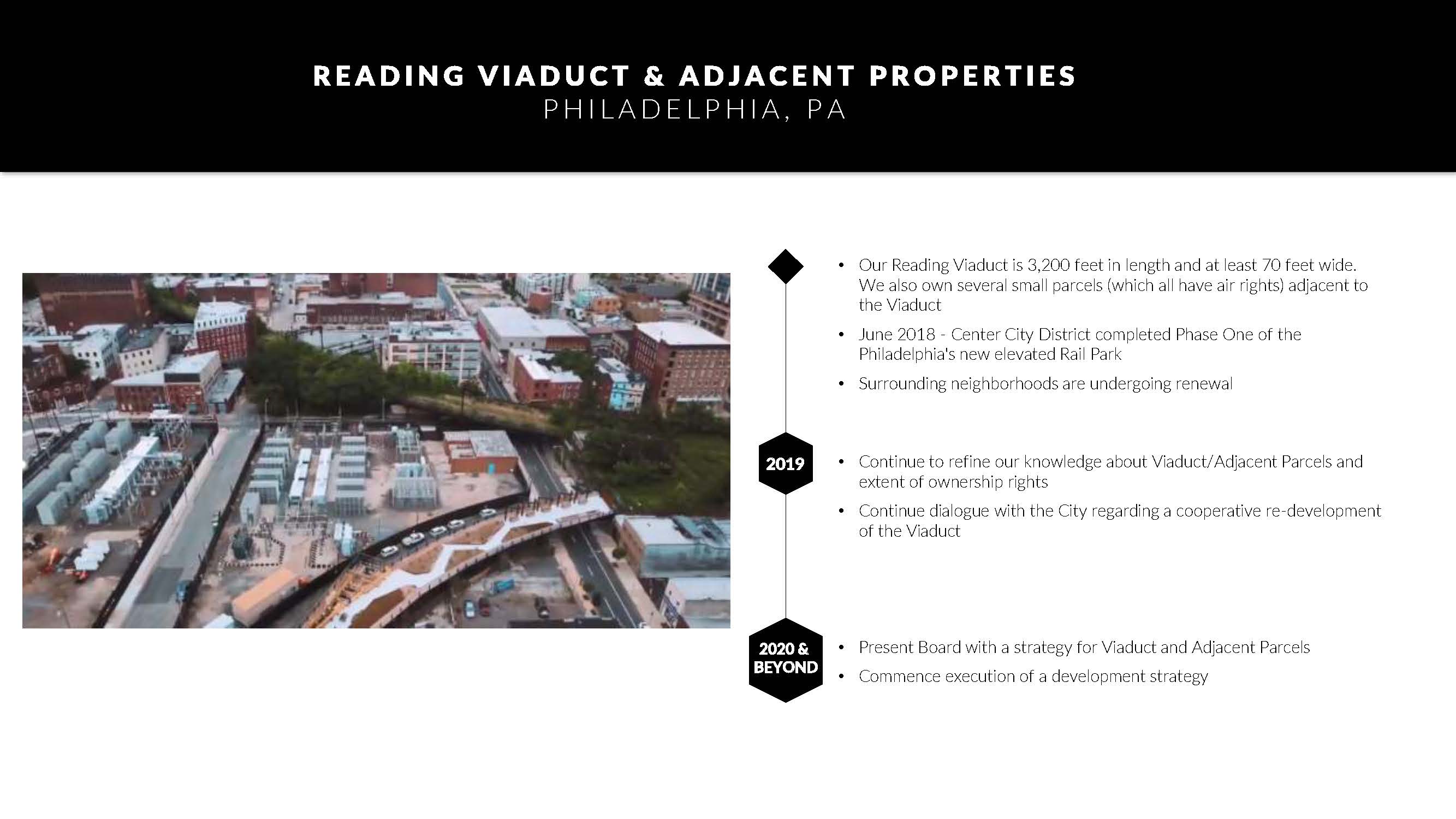

READING VIADUCT & ADJACENT PROPERTIES PHILADELPHIA, PA Our Reading Viaduct is 3,200 feet in length and at least 70 feet wide. We also own several small parcels (which all have air rights) adjacent to the Viaduct June 2018 - Center City District completed Phase One of the Philadelphia's new elevated Rail Park Surrounding neighborhoods are undergoing renewal 2019 Continue to refine our knowledge about Viaduct/Adjacent Parcels and extent of ownership rights Continue dialogue with the City regarding a cooperative re-development of the Viaduct 2020 AND BEYOND Present Board with a strategy for Viaduct and Adjacent Parcels Commence execution of a development strategy 39

COACHELLA 50% MANAGING MEMBER INTEREST IN 202 ACRES OF UNDEVELOPED LAND Located immediately south of Interstate 10 and east of Highway 86 in Coachella Valley Current zoning for 50 acres of high density mixed-use and 150 acres of single family residences As we maintain the 202 acres, we monitor the market for meaningful opportunities to monetize legacy investment for RDI and its partner Holding costs and management time are minimal CALIFORNIA PROPERTIES 5995 SEPULVEDA CREATIVE OFFICE SPACE Exploring conversion of second floor to co-working venue to take advantage of growth in Playa Vista and Culver City sub-market Evaluating both leased and managed co-working opportunities Exclusive third party leasing agreement terminated 40

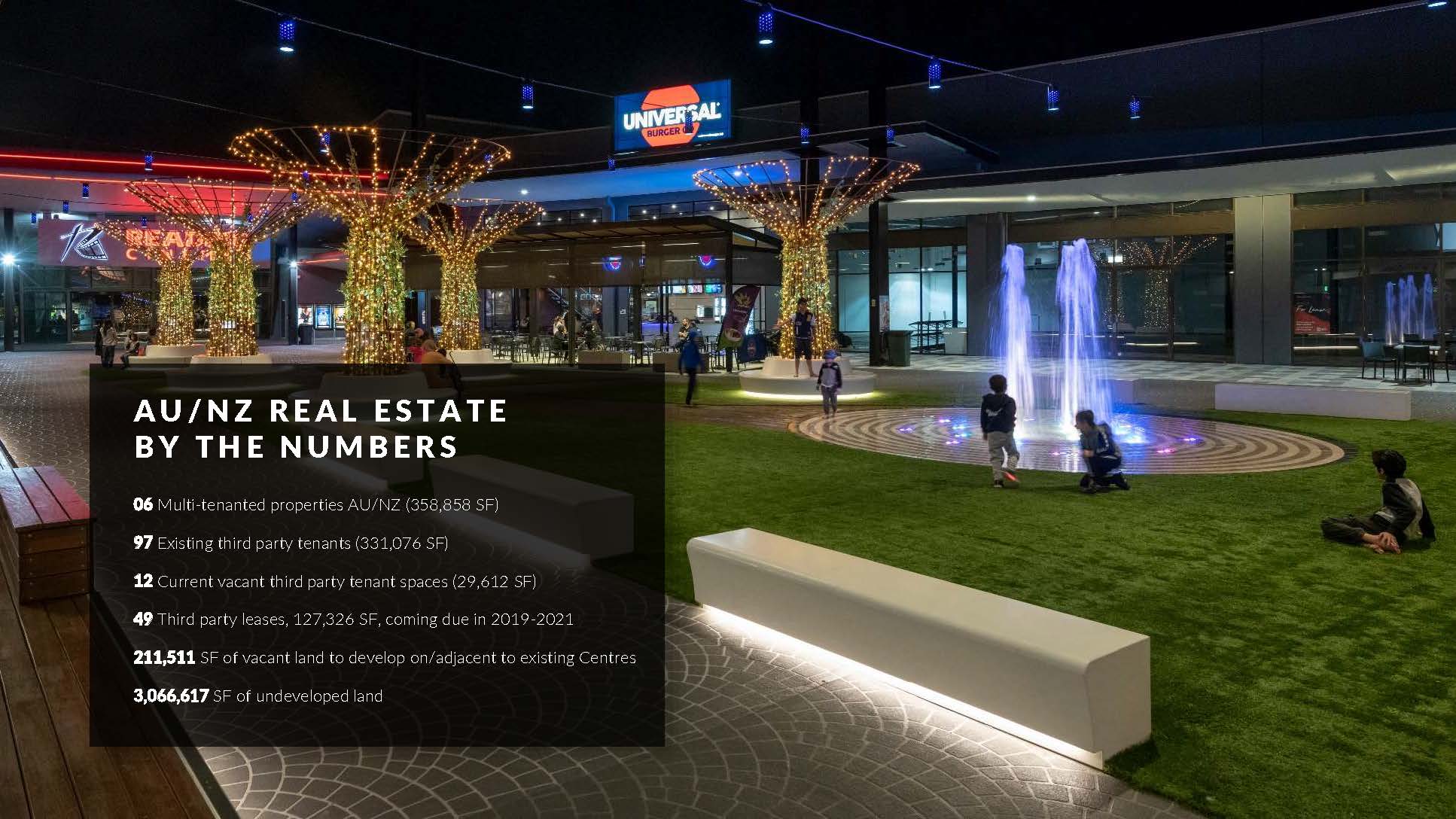

AU/NZ REAL ESTATE BY THE NUMBERS 06 Multi-tenanted properties AU/NZ (358,858 SF) 97 Existing third party tenants (331,076 SF) 12 Current vacant third party tenant spaces (29,612 SF) 49 Third party leases, 127,326 SF, coming due in 2019-2021 211,511 SF of vacant land to develop on/adjacent to existing Centres 3,066,617 SF of undeveloped land 41

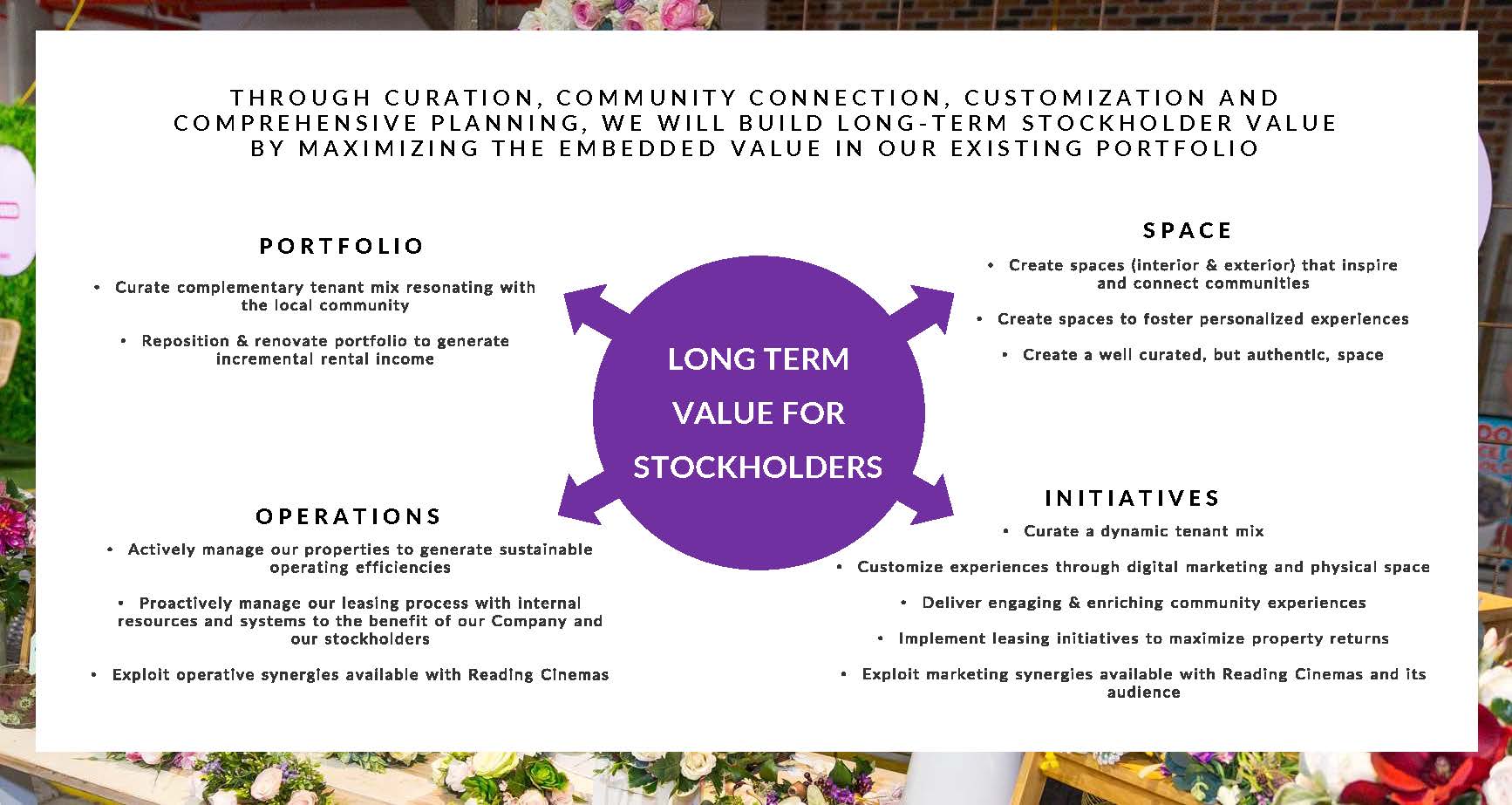

THROUGH CURATION, COMMUNITY CONNECTION, CUSTOMIZATION AND COMPREHENSIVE PLANNING, WE WILL BUILD LONG-TERM STOCKHOLDER VALUE BY MAXIMIZING THE EMBEDDED VALUE IN OUR EXISTING PORTFOLIO LONG TERM VALUE FOR STOCKHOLERS PORTFOLIO Curate complementary tenant mix resonating with the local community Reposition & renovate portfolio to generate incremental rental income SPACE Create spaces (interior & exterior) that inspire and connect communities Create spaces to foster personalized experiences Create a well curated, but authentic, space OPERATIONS Actively manage our properties to generate sustainable operating efficiencies Proactively manage our leasing process with internal resources and systems to the benefit of our Company and our stockholders Exploit operative synergies available with Reading Cinemas INITIATIVES Curate a dynamic tenant mix Customize experience through digital marketing and physical space Deliver engaging & enriching community experiences Implement leasing initiatives to maximize property returns Exploit marketing synergies available with Reading Cinemas and its audience 42

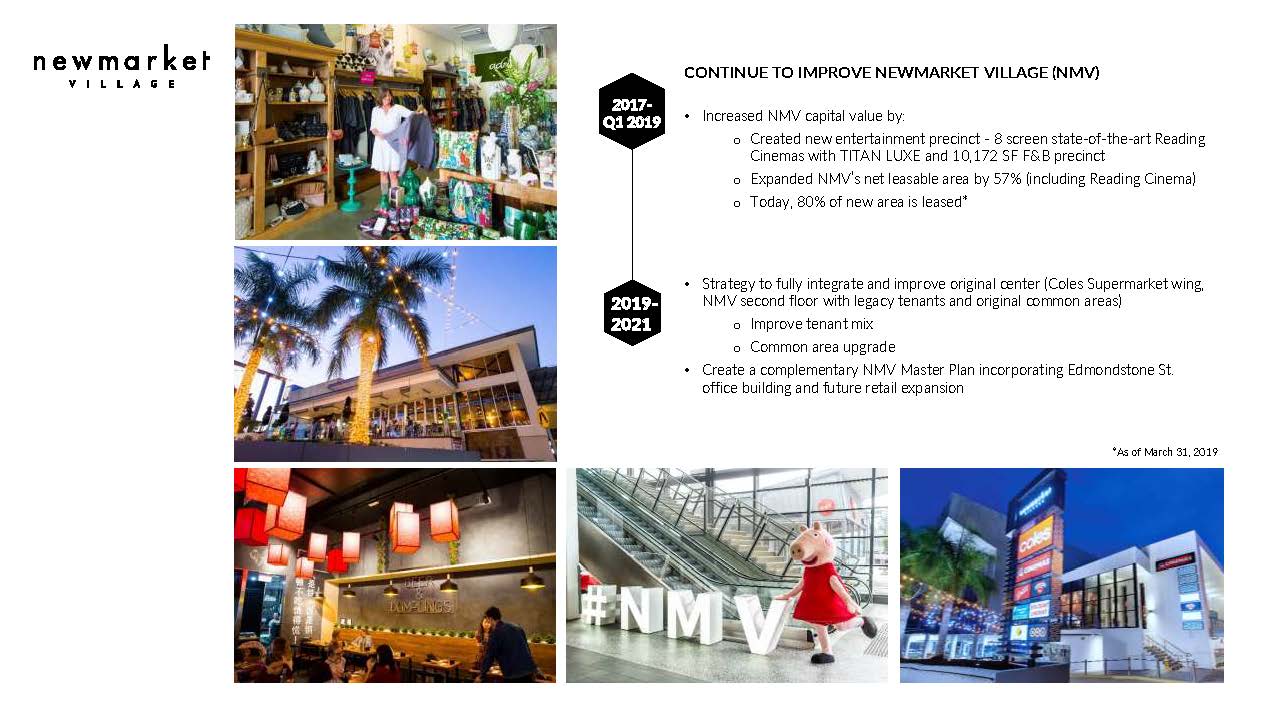

newmarket village CONTINUE TO IMRPOVE NEWMARKET VILLAGE (NMV) 2017-Q1 2019 Increased NMV capital value by: Created new entertainment precinct - 8 screen state-of-the-art Reading Cinemas with TITAN LUXE and 10,172 SF F&B precinct Expanded NMV’s net leasable area by 57% (including Reading Cinema) Today, 80% of new area is leased* 2019-2021 Strategy to fully integrate and improve original center (Coles Supermarket wing, NMV second floor with legacy tenants and original common areas) Improve tenant mix Common area upgrade Create a complementary NMV Master Plan incorporating Edmondstone St. office building and future retail expansion *As of March 31, 2019 43

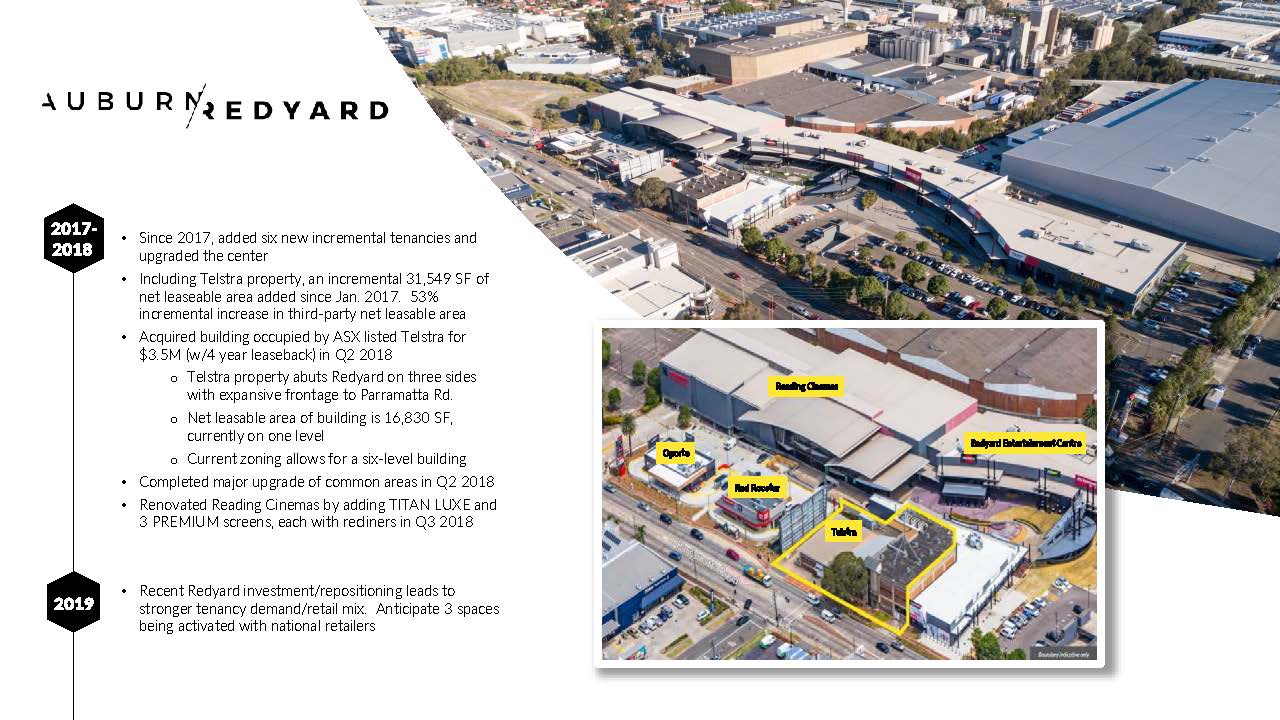

Auburn Redyard 2017-2018 Since 2017, added six new incremental tenancies and upgraded the center Including Telstra property, an incremental 31,549 SF of net leaseable area added since Jan. 2017. 53% incremental increase in third-party net leasable area Acquired building occupied by ASX listed Telstra for $3.5M (w/4 year leaseback) in Q2 2018 Telstra property abuts Redyard on three sides with expansive frontage to Parramatta Rd. Net leasable area of building is 16,830 SF, currently on one level Current zoning allows for a six-level building Completed major upgrade of common areas in Q2 2018 Renovated Reading Cinemas by adding TITAN LUXE and 3 PREMIUM screens, each with recliners in Q3 2018 2019 Recent Redyard investment/repositioning leads to stronger tenancy demand/retail mix. Anticipate 3 spaces being activated with national retailers 44

Auburn Redyard 2020-2021 Future Value Opportunities Complete Redyard Master Plan, taking into account the opportunity and potential Eastern Pad (129,167 SF), Western Pad (21,528 SF) and integration of the Telstra building 45

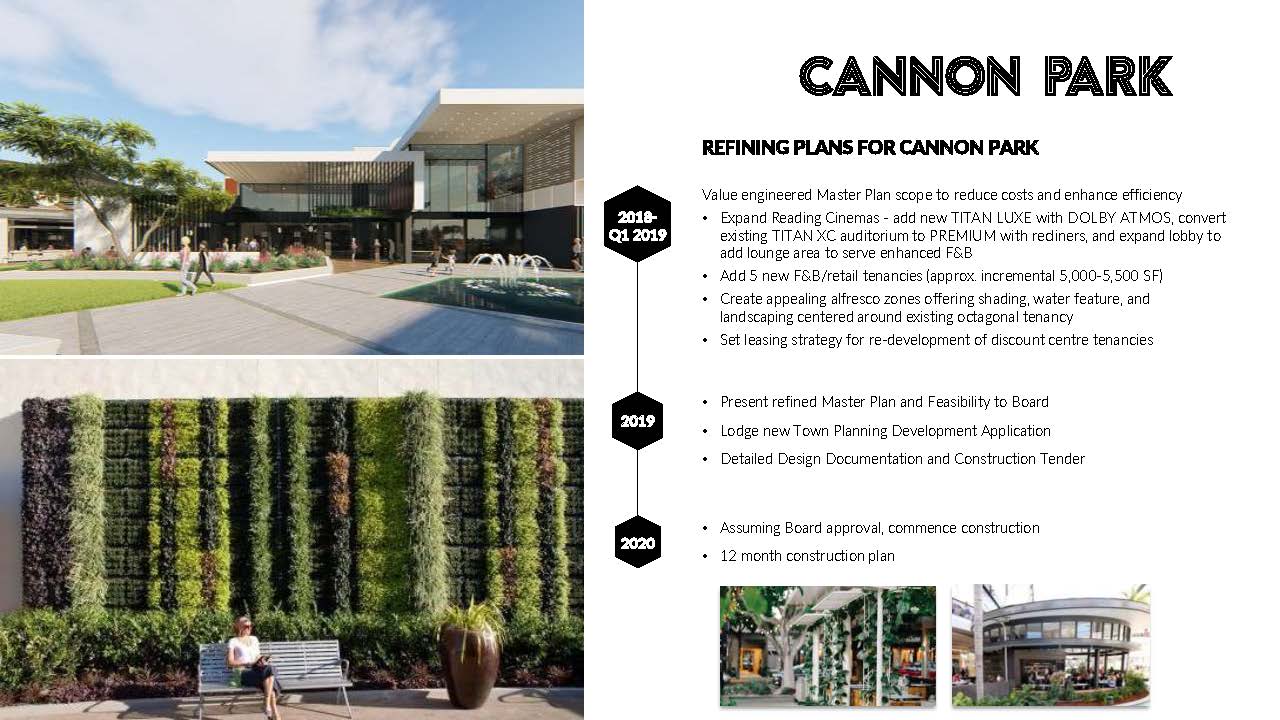

CANNON PARK Refining Plans for Cannon Park 2018-Q1 2019 Value engineered Master Plan scope to reduce costs and enhance efficiency Expand Reading Cinemas - add new TITAN LUXE with DOLBY ATMOS, convert existing TITAN XC auditorium to PREMIUM with recliners, and expand lobby to add lounge area to serve enhanced F&B Add 5 new F&B/retail tenancies (approx. incremental 5,000-5,500 SF) Create appealing alfresco zones offering shading, water feature, and landscaping centered around existing octagonal tenancy Set leasing strategy for re-development of discount centre tenancies 2019 Present refined Master Plan and Feasibility to Board Lodge new Town Planning Development Application Detailed Design Documentation and Construction Tender 2020 Assuming Board approval, commence construction 12 month construction plan 46

Courtenay Central Wellington Is A Thriving Capital City & New Zealand’s Ultimate Creative Urban Destination Wellington City Council’s Convention & Exhibition Centre being built across the street from Courtenay NZ$179M project Consent Application filed ~300,000 visitors expected annually No parking planned in development Let’s Get Wellington Moving Again – Government engaging with public on developing plans to complete major upgrade to City’s infrastructure. Te Papa, NZ’s National Museum (one block from Courtenay), rated as one of the world’s best museums, attracts over 1.5 million annual visitors Tourism is integral to Wellington’s economy, resulting in NZ$2.6B in expenditure per year Wellington Ranked “the most livable city in the world” by Deutsche Bank – 2017 & 2018 Branded as “one of the coolest little capitals in the World” by Lonely Planet - 2018 Expects 50,000-80,000 more people to move to the city over the next 30 years 47

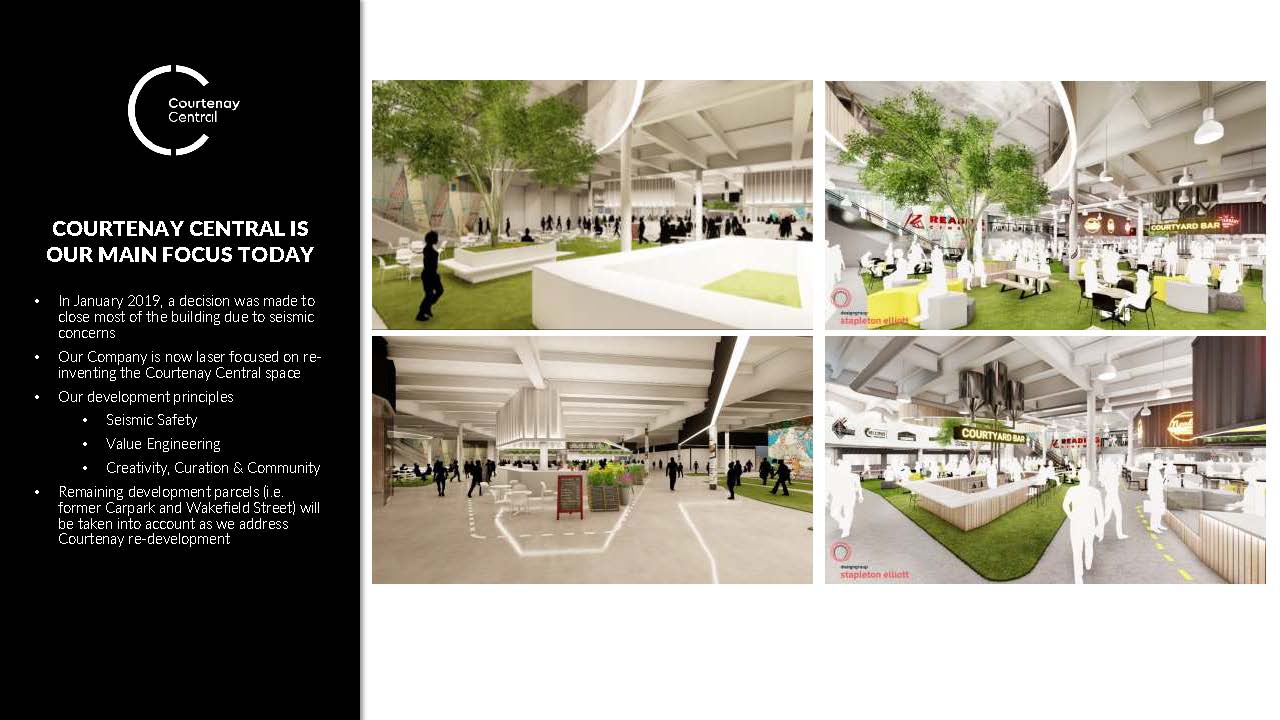

Courtenay Central Courtenay Central is our Main Focus Today In January 2019, a decision was made to close most of the building due to seismic concerns Our Company is now laser focused on re- inventing the Courtenay Central space Our development principles Seismic Safety Value Engineering Creativity, Curation & Community Remaining development parcels (i.e. former Carpark and Wakefield Street) will be taken into account as we address Courtenay re-development 48

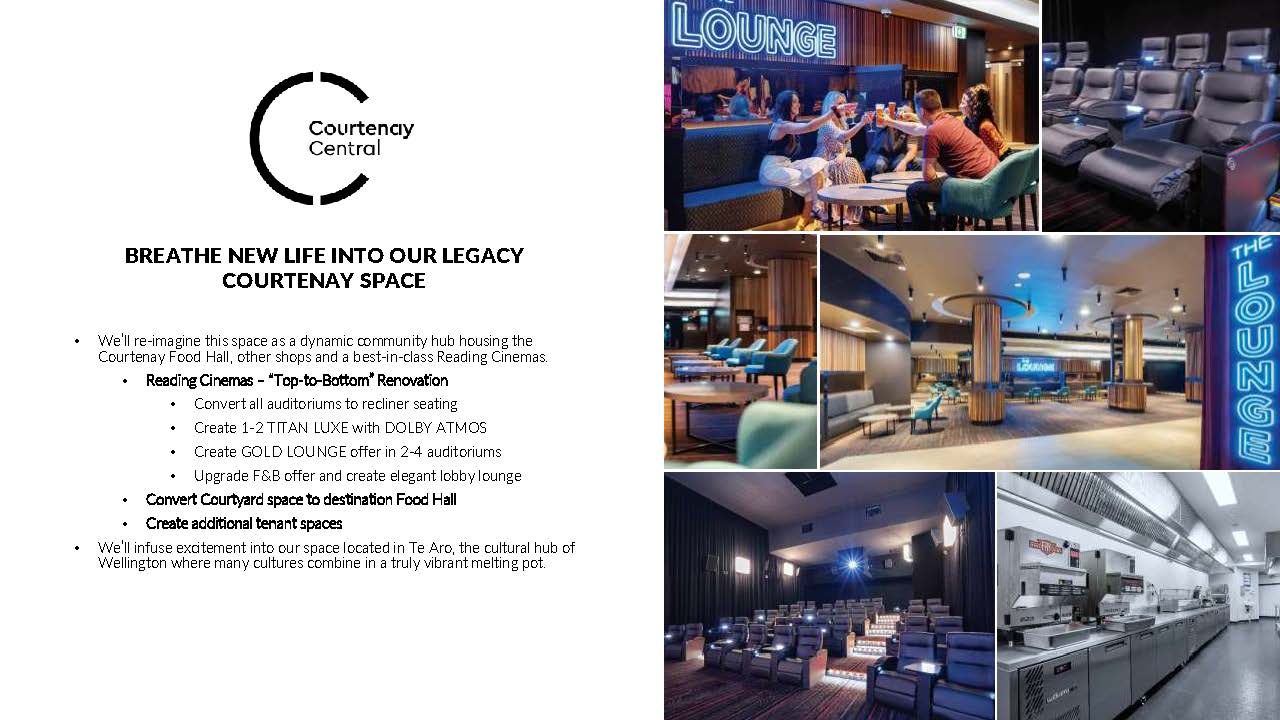

Courtenay Central Breathe New Life Into Our Legacy Courtenay Space We’ll re-imagine this space as a dynamic community hub housing the Courtenay Food Hall, other shops and a best-in-class Reading Cinemas. Reading Cinemas – “Top-to-Bottom” Renovation Convert all auditoriums to recliner seating Create 1-2 TITAN LUXE with DOLBY ATMOS Create GOLD LOUNGE offer in 2-4 auditoriums Upgrade F&B offer and create elegant lobby lounge Convert Courtyard space to destination Food Hall Create additional tenant spaces We’ll infuse excitement into our space located in Te Aro, the cultural hub of Wellington where many cultures combine in a truly vibrant melting pot. 49

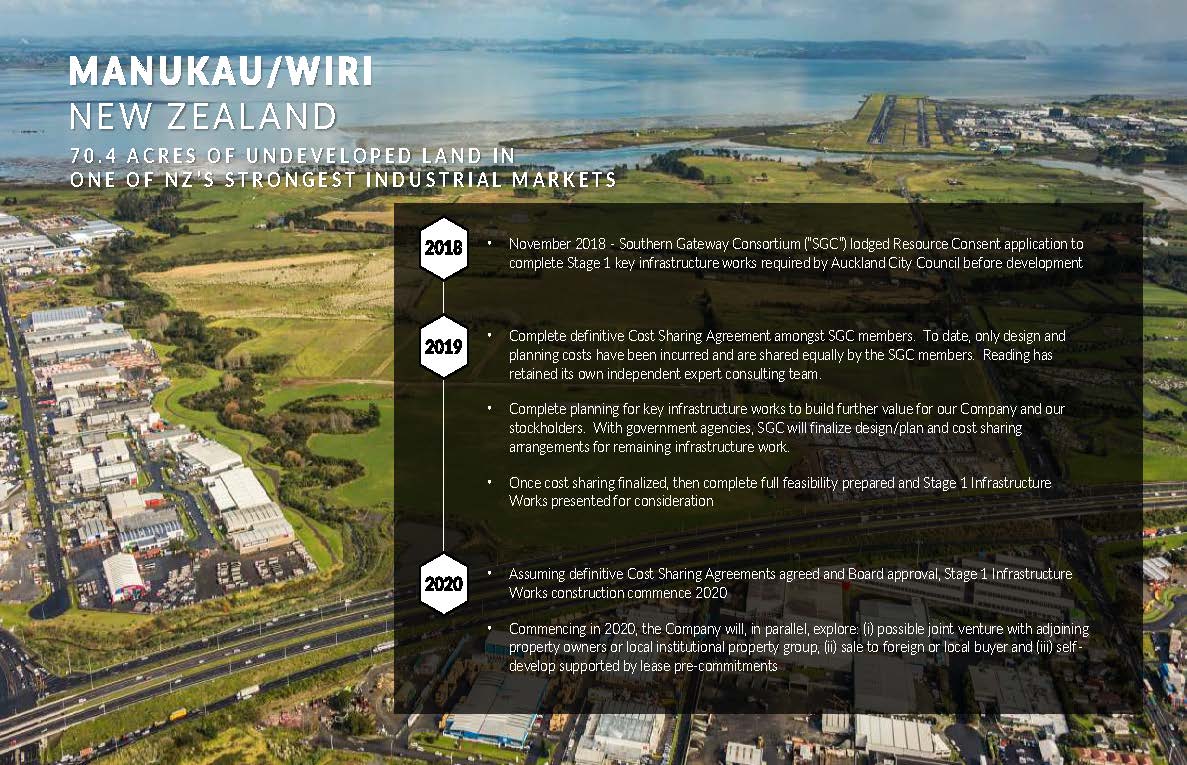

MANUKAU/WIRI NEW ZEALAND 70.4 ACRES OF UNDEVELOPED LAND IN ONE OF NZ’S STRONGESTED INDUSTRIAL MARKETS 2018 November 2018 - Southern Gateway Consortium (“SGC”) lodged Resource Consent application to complete Stage 1 key infrastructure works required by Auckland City Council before development 2019 Complete definitive Cost Sharing Agreement amongst SGC members. To date, only design and planning costs have been incurred and are shared equally by the SGC members. Reading has retained its own independent expert consulting team. Complete planning for key infrastructure works to build further value for our Company and our stockholders. With government agencies, SGC will finalize design/plan and cost sharing arrangements for remaining infrastructure work. Once cost sharing finalized, then complete full feasibility prepared and Stage 1 Infrastructure Works presented for consideration 2020 Assuming definitive Cost Sharing Agreements agreed and Board approval, Stage 1 Infrastructure Works construction commence 2020 Commencing in 2020, the Company will, in parallel, explore: (i) possible joint venture with adjoining property owners or local institutional property group, (ii) sale to foreign or local buyer and (iii) self- develop supported by lease pre-commitments 50

Financial Revenue Presented by Gilbert Avanes Interim Chief Financial Officer & Treasurer 51

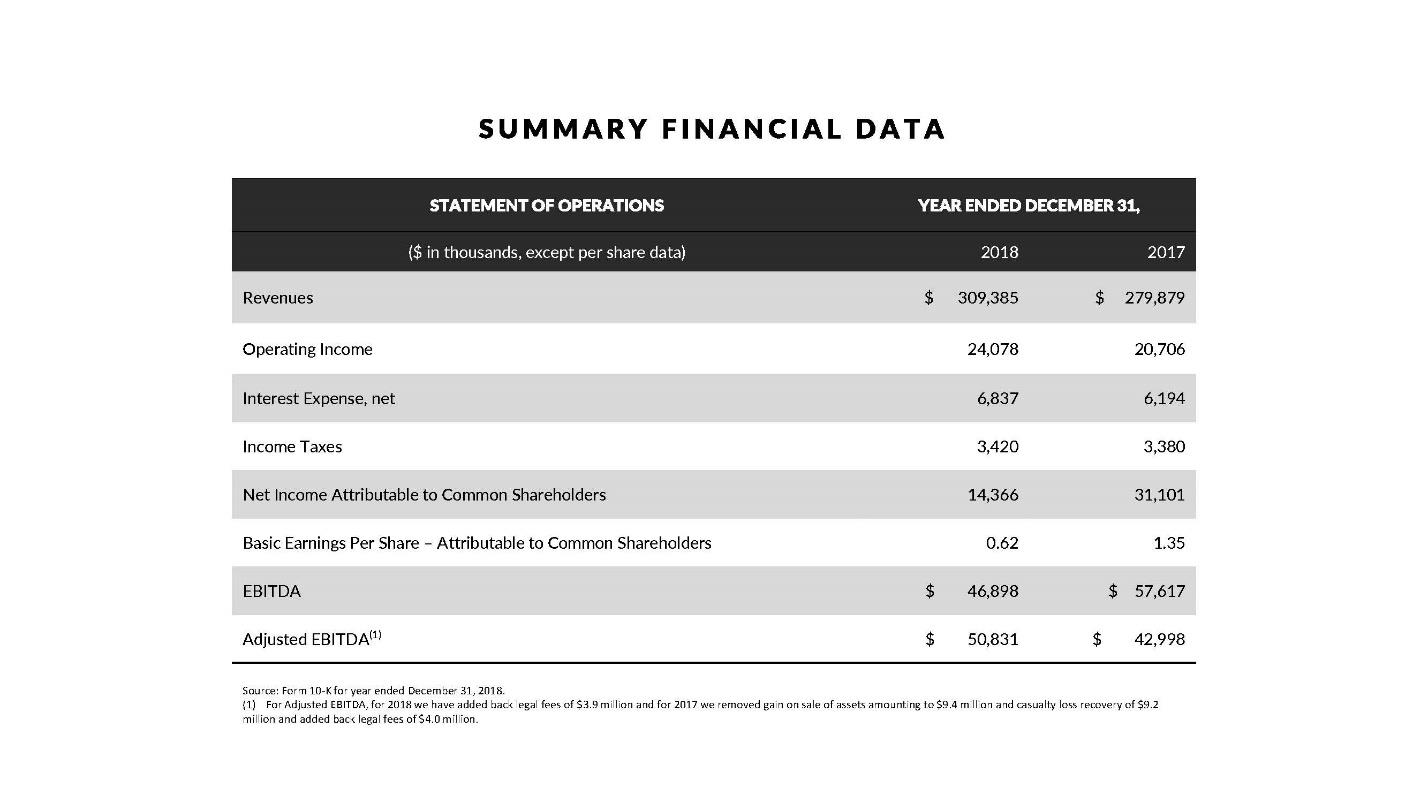

SUMMARY FINANCIAL DATA Statement of Operations ($ in thousands, except per share data) Year ended December 31, 2018 2017 Revenues $309,385 $279,879 Operating Income 24,078 20,706 Interest Expense, net 6,837 6,194 Income Taxes 3,420 3,380 Net Income Attributable to Common Shareholders 14,366 31,101 Basic Earnings Per Share – Attributable to Common Shareholders 0.62 1.35 EBITDA $46,898 $57,617 Adjusted EBITDA(1) $50,831 $42,998 Source: Form 10-K for year ended December 31, 2018. (1) For Adjusted EBITDA, for 2018 we have added back legal fees of $3.9 million and for 2017 we removed gain on sale of assets amounting to $9.4 million and casualty loss recovery of $9.2 million and added back legal fees of $4.0 million. 52

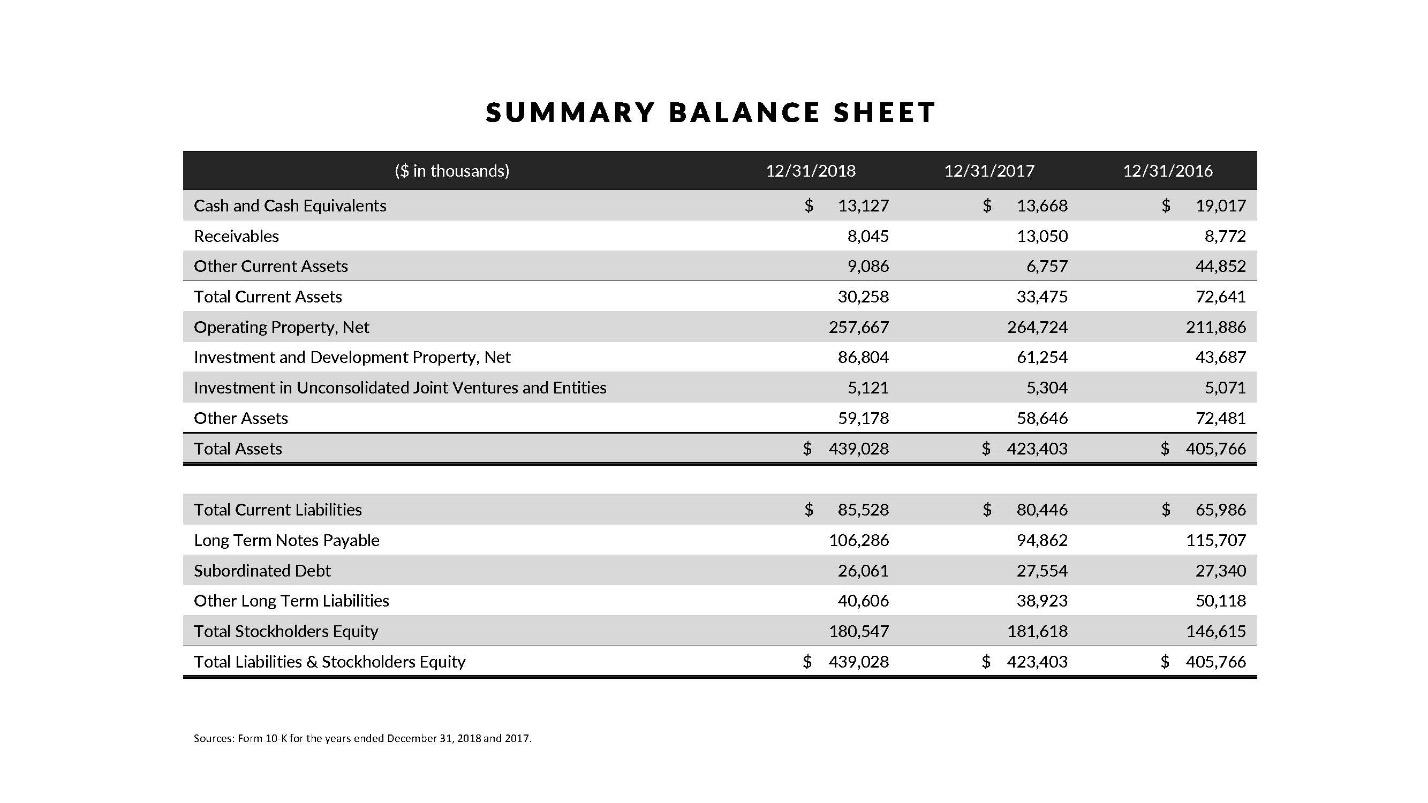

SUMMARY BALANCE SHEET ($ in thousands) 12/31/2018 12/31/2017 12/31/2016 Cash and Cash Equivalents $13,127 $13,338 $19,017 Receivables 8,045 13,050 8,772 Other Current Assets 9,086 6,757 44,852 Total Current Assets 30,258 33,475 72,641 Operating Property, Net 257,667 264,724 211,886 Investment and Development Property, Net 86,804 61,254 43,687 Investment in Unconsolidated Joint Ventures and Entities 5,121 5,304 5,071 Other Assets 59,178 58,646 72,481 Total Assets $439,028 $423,403 $405,766 Total Current Liabilities $85,528 $80,446 $65,986 Long Term Notes Payable 106,286 94,862 115,707 Subordinated Debt 26,061 27,554 27,640 Other Long Term Liabilities 40,606 38,923 50,118 Total Stockholders Equity 180,547 181,618 146,615 Total Liabilities & Stockholders Equity $439,028 $423,403 $405,766 Sources: Form 10-K for the years ended December 31, 2018 and 2017. 53

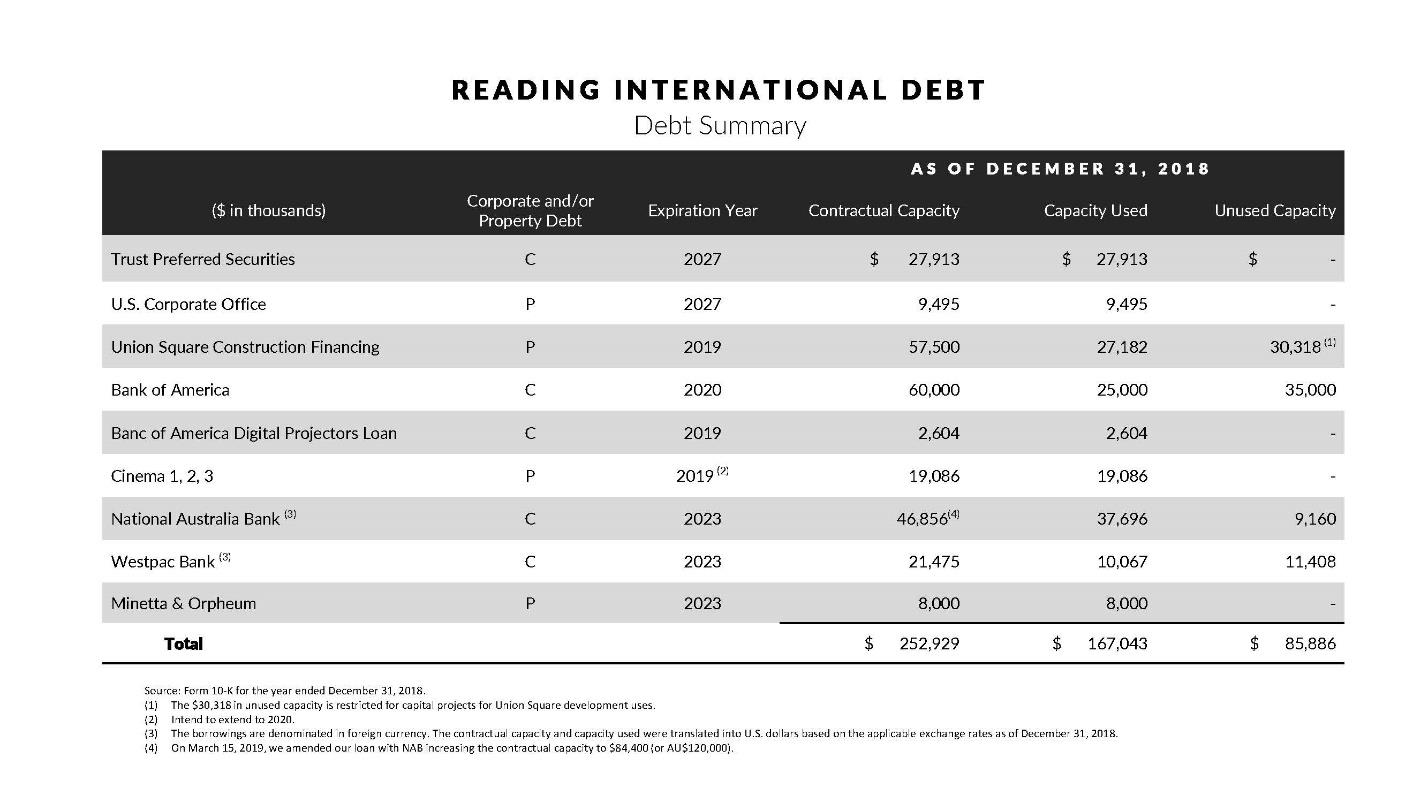

READING INTERNATIONAL DEBT DEBT SUMMARY ($ in thousands) Corporate and/or Property Debt Expiration Year Contractual Capacity Capacity Used Unused Capacity As of December 31, 2018 Trust Preferred Securities C 2027 $27,913 $27,913 $ - U.S Corporate Office P 2027 9,495 9,495 – Union Square Construction Financing P 2019 57,500 27,182 30,318(1) Bank of America C 2020 60,000 25,000, 35,000 Banc of America Digital Projects Loan C 2019 2,604 2,604 – Cinema 1, 2, 3 P 2019(2) 19,086 19,086 – National Australia Bank(3) C 2023 46,856(4) 37,696 9,160 Westpac Bank(3) C 2023 21,475, 10,067 11,408 Minetta & Orpheum P 2023 8,000 8,000 – Total $252,929 $167,043 $85,886 Source: Form 10-K for the year ended December 31, 2018. (1) The $30,318 in unused capacity is restricted for capital projects for Union Square development uses. (2) Intend to extend to 2020. (3) The borrowings are denominated in foreign currency. The contractual capacity and capacity used were translated into U.S. dollars based on the applicable exchange rates as of December 31, 2018. (4) On March 15, 2019, we amended our loan with NAB increasing the contractual capacity to $84,400 (or AU$120,000). 54

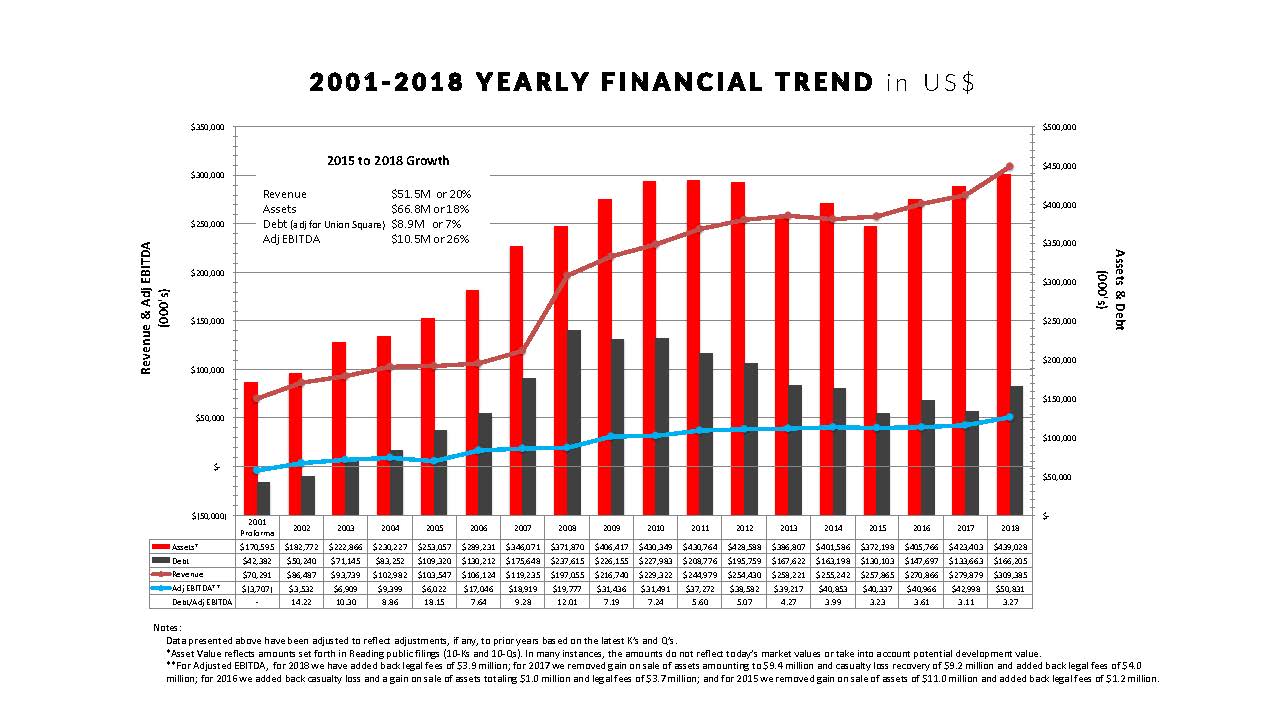

2001-2018 Yearly Financial Trend in US$ Revenue & Adj. EBITA (000’s) $(50,000) $ $50,000 $100,000 $150,000 $200,000 $250,000 $300,000 $350,000 2015 to 2018 Growth Revenue $51.5M or 20% Assets $66.8M or 18% Debt (Adj for Union Square) $8.9M or 9% Adj EBITDA $10.5M or 26% Assets & Debt (000’s) $ $50,000 $100,000 $150,000 $200,000 $250,000 $300,000 $350,000 $400,000 $450,000 $500,000 2001 Proforma 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 Assets* Debt Revenue Adj EBITDA** Debt/Adj EBITDA $170,595 $42,382 $70,291 $(3,707) $182,772 $50,240 $86,487 $3,532 14.22 $222,866 $71,145 $93,739 $6,909 10.30 $230,277 $83,252 $102,982 $9,399 8.86 $253,057 $109,320 $103,547 $6,022 18.15 $289,231 $130,212 $106,124 $17,046 7.64 $346,071 $175,648 $119,235 $18,919 9.28 $371,870 $237,615 $197,055 $19,777 12.01 $406,417 $226,155$216,740 $31,436 7.19 $430,349 $277,983 $299,322 #31,491 7.24 $430,764 $208,776 $244,979 $37,272 5.60 $428,588 $195,759 $254,430 $38,582 5.07 $386,807 $167,622 $258,221 $39,217 4.27 $401,586 $163,198 $255,242 $40,853 3.99 $372,198 $130,103 $257,865 $40,337 3.23 $405,766 $147,697 $270,866 $40,966 3.61 $423,403 $133,663 $279,879 $42,998 3.11 $439,028 $166,205 $309,385 $50,831 3.27 Notes: Data presented above have been adjusted to reflect adjustments, if any, to prior years based on the latest K’s and Q’s. *Asset Value reflects amounts set forth in Reading public filings (10-Ks and 10-Qs). In many instances, the amounts do not reflect today’s market values or take into account potential development value. **For Adjusted EBITDA, for 2018 we have added back legal fees of $3.9 million; for 2017 we removed gain on sale of assets amounting to $9.4 million and casualty loss recovery of $9.2 million and added back legal fees of $4.0 million; for 2016 we added back casualty loss and a gain on sale of assets totaling $1.0 million and legal fees of $3.7 million; and for 2015 we removed gain on sale of assets of $11.0 million and added back legal fees of $1.2 million. 55

STATUS OF READING INTERNATIONAL, INC. AS AN INDEPENDENT COMPAY In March, the Board reviewed and approved our three-year strategy and resolved that it has no current intention to engage in a sales process. The Board believes that Reading’s prospects for creating long term value offer the best course of action for our Company and our stockholders generally. This is a perspective also shared by the controlling stockholders. 56

Reading International Thank You