UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number | 811-3700 |

| |

| The Dreyfus/Laurel Tax-Free Municipal Funds | |

| (Exact name of Registrant as specified in charter) | |

| | |

| c/o The Dreyfus Corporation 200 Park Avenue New York, New York 10166 | |

| (Address of principal executive offices) (Zip code) | |

| | |

| John Pak, Esq. 200 Park Avenue New York, New York 10166 | |

| (Name and address of agent for service) | |

|

Registrant's telephone number, including area code: | (212) 922-6000 |

| |

Date of fiscal year end: | 06/30 | |

Date of reporting period: | 06/30/2013 | |

| | | | | | | |

FORM N-CSR

Item 1. Reports to Stockholders.

The views expressed in this report reflect those of the portfolio manager only through the end of the period covered and do not necessarily represent the views of Dreyfus or any other person in the Dreyfus organization. Any such views are subject to change at any time based upon market or other conditions and Dreyfus disclaims any responsibility to update such views.These views may not be relied on as investment advice and, because investment decisions for a Dreyfus fund are based on numerous factors, may not be relied on as an indication of trading intent on behalf of any Dreyfus fund.

| | Contents |

| | THE FUND |

| 2 | A Letter from the President |

| 3 | Discussion of Fund Performance |

| 6 | Understanding Your Fund’s Expenses |

| 6 | Comparing Your Fund’s Expenses With Those of Other Funds |

| 7 | Statement of Investments |

| 14 | Statement of Assets and Liabilities |

| 15 | Statement of Operations |

| 16 | Statement of Changes in Net Assets |

| 17 | Financial Highlights |

| 18 | Notes to Financial Statements |

| 24 | Report of Independent Registered Public Accounting Firm |

| 25 | Important Tax Information |

| 26 | Information About the Renewal of the Fund’s Investment Management Agreement |

| 31 | Board Members Information |

| 33 | Officers of the Fund |

| | FOR MORE INFORMATION |

| | Back Cover |

Dreyfus BASIC

New York Municipal

Money Market Fund

The Fund

A LETTER FROM THE PRESIDENT

Dear Shareholder:

We are pleased to present this annual report for Dreyfus BASIC NewYork Municipal Money Market Fund, covering the 12-month period from July 1, 2012, through June 30, 2013. For information about how the fund performed during the reporting period, as well as general market perspectives, we provide a Discussion of Fund Performance on the pages that follow.

After more than 30 years of declining interest rates, it appears that the secular downtrend may be over. Improvements in U.S. housing and labor markets so far in 2013 prompted the Federal Reserve Board (the “Fed”) to signal its intent to back away from its quantitative easing program later this year, a development that sparked heightened bond market volatility and rising bond yields during the second quarter.

These developments suggest to us that a new phase of the economic cycle is about to begin.The U.S. economic recovery appears poised to accelerate later this year in advance of a multi-year expansion. Stronger economic growth and the Fed’s widely anticipated shift to a more moderately stimulative monetary policy stance are likely to presage a gradual, upward drift in longer term interest rates as the relationship between rates and economic conditions normalizes. However, a tapering off of quantitative easing does not necessarily herald imminent increases in short-term interest rates, and we continue to expect any short-term interest-rate hikes to be postponed until 2015.As always, we urge you to discuss our observations with your financial adviser.

Thank you for your continued confidence and support.

Sincerely,

J. Charles Cardona

President

The Dreyfus Corporation

July 15, 2013

2

DISCUSSION OF FUND PERFORMANCE

For the period of July 1, 2012, through June 30, 2013, as provided by Bill Vasiliou, Portfolio Manager

Fund and Market Performance Overview

For the 12-month period ended June 30, 2013, Dreyfus BASIC NewYork Municipal Money Market Fund produced a yield of 0.00%.Taking into account the effects of compounding, the fund produced an effective yield of 0.00%.1

Yields of tax-exempt money market instruments stayed near historical lows throughout the reporting period, as short-term interest rates remained anchored by an overnight federal funds rate between 0% and 0.25% despite rising long-term interest rates amid evidence of more robust economic growth.

The Fund’s Investment Approach

The fund seeks to provide a high level of current income exempt from federal, New York state and New York city income taxes to the extent consistent with the preservation of capital and the maintenance of liquidity. To pursue this objective, the fund normally invests substantially all of its assets in short-term high-quality municipal obligations that provide income exempt from federal, New York state and New York city personal income taxes. We also actively manage the fund’s weighted average maturity in anticipation of interest-rate and supply-and-demand changes in New York’s short-term municipal marketplace.

The management of the fund’s weighted average maturity uses a more tactical approach. If we expect the supply of securities to increase temporarily, we may reduce the fund’s weighted average maturity to make cash available for the purchase of higher yielding securities, if such securities become available.This is due to the fact that yields tend to rise temporarily if issuers are competing for investor interest. If we expect demand to surge at a time when we anticipate little issuance and therefore lower yields, we may increase the fund’s weighted average maturity to maintain current yields for as long as we deem practical. At other times, we try to maintain a neutral weighted average maturity.

The Fund 3

DISCUSSION OF FUND PERFORMANCE (continued)

Gradual Economic Recovery Continues

Despite releases of mixed economic data throughout the reporting period, the economic recovery appeared to gain a degree of traction. U.S. GDP growth increased from a 0.4% annualized rate during the fourth quarter of 2012 to 1.8% over the first quarter of 2013. In addition, the unemployment rate declined from 8.2% at the start of the reporting period to 7.6% at the end of June 2013. Meanwhile, U.S. housing markets have exhibited long-awaited signs of recovery, including rebounding home sales and prices. In light of these developments, the Federal Reserve Board (the “Fed”) signaled in late May that it is likely to begin backing away from its ongoing quantitative easing program later this year. However, the Fed has continued to indicate that short-term interest rates are likely to stay near historically low levels at least until the unemployment rate reaches 6.5%.

In this low interest-rate environment, investors focused on higher yielding securities in the longer term municipal bond market. Demand for securities issued by municipalities also remained strong among nontraditional buyers, such as separately managed accounts and intermediate bond funds, due to attractive tax-exempt yields compared to taxable securities and narrow yield differences across the one- to three-year maturity spectrum. Nonetheless, yields on high-quality, one-year municipal notes remained near historical lows over the reporting period, and increased investor demand for variable rate demand notes (“VRDNs”) has kept yields of shorter term securities steady.

Like many other states, New York’s credit quality continued to improve over the reporting period as its economy has proved resilient and lawmakers have cooperated in producing a balanced budget.

Credit Selection Remains Paramount

Due to narrow yield differences along the maturity spectrum, as well as ongoing regulatory uncertainty, most tax-exempt money market funds have maintained relatively short weighted average maturities compared to historical averages.The fund was no exception, and we maintained its weighted average maturity in a range that was consistent with industry averages.

4

Moreover, well-researched credit selection has remained paramount.As we have for some time, we favored state general obligation bonds; essential service revenue bonds backed by revenues from water, sewer, and electric facilities; certain local credits with strong financial positions and stable tax bases; and health care and education issuers with stable credit characteristics.We generally continued to shy away from instruments issued by localities that depend heavily on state aid.

Low Rates Likely to Persist

We have remained cautiously optimistic regarding U.S. economic prospects over the foreseeable future. Despite the likelihood that the Fed will begin to taper off its ongoing, open-ended quantitative easing program later this year, the central bank also has made clear that short-term interest rates are likely to remain low for some time to come. Consequently, we believe that the prudent course continues to be an emphasis on preservation of capital and liquidity.

July 15, 2013

An investment in the fund is not insured or guaranteed by the FDIC or any other government agency. Although the fund seeks to preserve the value of your investment at $1.00 per share, it is possible to lose money by investing in the fund.

Short-term municipal securities holdings involve credit and liquidity risks and risk of principal loss.

| |

| 1 | Effective yield is based upon dividends declared daily and reinvested monthly. Past performance is no guarantee of future |

| | results.Yields fluctuate. Income may be subject to state and local taxes for non-NewYork residents, and some income |

| | may be subject to the federal alternative minimum tax (AMT) for certain investors.Yields provided reflect the absorption |

| | of certain fund expenses by The Dreyfus Corporation pursuant to a voluntary undertaking that may be extended, |

| | terminated or modified at any time. Had these expenses not been absorbed, fund yields would have been lower. |

The Fund 5

UNDERSTANDING YOUR FUND’S EXPENSES (Unaudited)

As a mutual fund investor, you pay ongoing expenses, such as management fees and other expenses. Using the information below, you can estimate how these expenses affect your investment and compare them with the expenses of other funds.You also may pay one-time transaction expenses, including sales charges (loads) and redemption fees, which are not shown in this section and would have resulted in higher total expenses. For more information, see your fund’s prospectus or talk to your financial adviser.

Review your fund’s expenses

The table below shows the expenses you would have paid on a $1,000 investment in Dreyfus BASIC New York Municipal Money Market Fund from January 1, 2013 to June 30, 2013. It also shows how much a $1,000 investment would be worth at the close of the period, assuming actual returns and expenses.

|

| Expenses and Value of a $1,000 Investment |

| assuming actual returns for the six months ended June 30, 2013 |

| | |

| Expenses paid per $1,000† | $ | 1.24 |

| Ending value (after expenses) | $ | 1,000.00 |

COMPARING YOUR FUND’S EXPENSES

WITH THOSE OF OTHER FUNDS (Unaudited)

Using the SEC’s method to compare expenses

The Securities and Exchange Commission (SEC) has established guidelines to help investors assess fund expenses. Per these guidelines, the table below shows your fund’s expenses based on a $1,000 investment, assuming a hypothetical 5% annualized return. You can use this information to compare the ongoing expenses (but not transaction expenses or total cost) of investing in the fund with those of other funds.All mutual fund shareholder reports will provide this information to help you make this comparison. Please note that you cannot use this information to estimate your actual ending account balance and expenses paid during the period.

Expenses and Value of a $1,000 Investment

assuming a hypothetical 5% annualized return for the six months ended June 30, 2013

| | |

| Expenses paid per $1,000† | $ | 1.25 |

| Ending value (after expenses) | $ | 1,023.55 |

|

| † Expenses are equal to the fund’s annualized expense ratio of .25%, multiplied by the average account value over the |

| period, multiplied by 181/365 (to reflect the one-half year period). |

6

STATEMENT OF INVESTMENTS

June 30, 2013

| | | | | |

| Short-Term | Coupon | Maturity | Principal | | |

| Investments—100.9% | Rate (%) | Date | Amount ($) | | Value ($) |

| Albany Industrial Development | | | | | |

| Agency, Civic Facility Revenue | | | | | |

| (Albany Medical Center | | | | | |

| Hospital Project) (LOC; | | | | | |

| Bank of America) | 0.13 | 7/7/13 | 6,315,000 | a | 6,315,000 |

| Cooperstown, | | | | | |

| GO Notes, BAN | 1.25 | 8/28/13 | 1,750,000 | | 1,751,520 |

| Deutsche Bank Spears/Lifers Trust | | | | | |

| (Series DBE-1152) (TSASC, | | | | | |

| Inc., Tobacco Settlement | | | | | |

| Asset-Backed Bonds) (Liquidity | | | | | |

| Facility: Deutsche Bank AG and | | | | | |

| LOC; Deutsche Bank AG) | 0.16 | 7/7/13 | 3,000,000 | a,b,c | 3,000,000 |

| Deutsche Bank Spears/Lifers Trust | | | | | |

| (Series DBE-1162) (Westchester | | | | | |

| County Industrial Development | | | | | |

| Agency, IDR (Ardsley Housing | | | | | |

| Associates, LLC Facility)) (Liquidity | | | | | |

| Facility; Deutsche Bank AG and | | | | | |

| LOC; Deutsche Bank AG) | 0.26 | 7/7/13 | 7,000,000 | a,b,c | 7,000,000 |

| East Rochester Housing Authority, | | | | | |

| Housing Revenue (Park Ridge | | | | | |

| Nursing Home, Inc. Project) | | | | | |

| (LOC; JPMorgan Chase Bank) | 0.09 | 7/7/13 | 4,070,000 | a | 4,070,000 |

| Erie County Industrial Development | | | | | |

| Agency, IDR (Luminescent | | | | | |

| System, Inc. Project) (LOC; | | | | | |

| HSBC Bank USA) | 0.40 | 7/7/13 | 1,895,000 | a | 1,895,000 |

| Hamburg Central School District, | | | | | |

| GO Notes, BAN | 2.00 | 6/13/14 | 4,600,000 | | 4,666,122 |

| Hamburg Village, | | | | | |

| GO Notes, BAN | 1.00 | 7/18/13 | 2,480,000 | | 2,480,459 |

| Holley Central School District, | | | | | |

| GO Notes, BAN | 1.25 | 6/19/14 | 1,300,000 | | 1,308,788 |

| LaGrange, | | | | | |

| GO Notes, BAN | 1.50 | 1/3/14 | 1,964,926 | | 1,973,380 |

| Metropolitan Transportation | | | | | |

| Authority, Transportation | | | | | |

| Revenue, CP (LOC; | | | | | |

| Royal Bank of Canada) | 0.09 | 7/11/13 | 3,000,000 | | 3,000,000 |

| Middletown, | | | | | |

| GO Notes, BAN | 1.00 | 2/21/14 | 1,400,000 | | 1,404,930 |

The Fund 7

STATEMENT OF INVESTMENTS (continued)

| | | | | |

| Short-Term | Coupon | Maturity | Principal | | |

| Investments (continued) | Rate (%) | Date | Amount ($) | | Value ($) |

| Monroe County Industrial | | | | | |

| Development Agency, Civic | | | | | |

| Facility Revenue (YMCA of | | | | | |

| Greater Rochester Project) | | | | | |

| (LOC; M&T Trust) | 0.11 | 7/7/13 | 2,200,000 | a | 2,200,000 |

| Monroe County Industrial | | | | | |

| Development Agency, Civic | | | | | |

| Facility Revenue (YMCA of | | | | | |

| Greater Rochester Project) | | | | | |

| (LOC; M&T Trust) | 0.11 | 7/7/13 | 4,600,000 | a | 4,600,000 |

| Monroe County Industrial | | | | | |

| Development Corporation, | | | | | |

| Revenue (Saint Ann’s Home | | | | | |

| for the Aged Project) (LOC; | | | | | |

| HSBC Bank USA) | 0.08 | 7/7/13 | 1,605,000 | a | 1,605,000 |

| Nassau County Industrial | | | | | |

| Development Agency, Housing | | | | | |

| Revenue (Rockville Centre | | | | | |

| Housing Associates, L.P. | | | | | |

| Project) (LOC; M&T Trust) | 0.16 | 7/7/13 | 4,600,000 | a | 4,600,000 |

| Nassau County Interim Finance | | | | | |

| Authority, Sales Tax | | | | | |

| Secured Revenue (Liquidity | | | | | |

| Facility; Sumitomo Mitsui | | | | | |

| Banking Corporation) | 0.05 | 7/7/13 | 4,000,000 | a | 4,000,000 |

| New York City, | | | | | |

| GO Notes (SBPA; | | | | | |

| Wells Fargo Bank) | 0.03 | 7/1/13 | 1,900,000 | a | 1,900,000 |

| New York City Capital Resource | | | | | |

| Corporation, Recovery Zone | | | | | |

| Facility Revenue (Arverne by | | | | | |

| the Sea Project) (LOC; TD Bank) | 0.06 | 7/7/13 | 3,000,000 | a | 3,000,000 |

| New York City Capital Resource | | | | | |

| Corporation, Revenue (Loan | | | | | |

| Enhanced Assistance Program— | | | | | |

| Cobble Hill Health Center, Inc. | | | | | |

| Project) (LOC; Bank of America) | 0.17 | 7/7/13 | 5,500,000 | a | 5,500,000 |

| New York City Housing Development | | | | | |

| Corporation, Multi-Family | | | | | |

| Rental Housing Revenue | | | | | |

| (Queenswood Apartments | | | | | |

| Project) (Liquidity Facility; | | | | | |

| FHLMC and LOC; FHLMC) | 0.06 | 7/7/13 | 1,800,000 | a | 1,800,000 |

8

| | | | | |

| Short-Term | Coupon | Maturity | Principal | | |

| Investments (continued) | Rate (%) | Date | Amount ($) | | Value ($) |

| New York City Industrial | | | | | |

| Development Agency, Civic | | | | | |

| Facility Revenue (Birch | | | | | |

| Wathen Lenox School | | | | | |

| Project) (LOC; TD Bank) | 0.13 | 7/7/13 | 2,800,000 | a | 2,800,000 |

| New York City Industrial | | | | | |

| Development Agency, IDR | | | | | |

| (Novelty Crystal Corporation | | | | | |

| Project) (LOC; TD Bank) | 0.20 | 7/7/13 | 2,745,000 | a | 2,745,000 |

| New York City Industrial | | | | | |

| Development Agency, IDR | | | | | |

| (Super-Tek Products, Inc. | | | | | |

| Project) (LOC; Citibank NA) | 0.39 | 7/7/13 | 3,760,000 | a | 3,760,000 |

| New York City Municipal Water | | | | | |

| Finance Authority, Water and | | | | | |

| Sewer System Second General | | | | | |

| Resolution Revenue (Liquidity | | | | | |

| Facility; Bank of Nova Scotia) | 0.07 | 7/1/13 | 2,170,000 | a | 2,170,000 |

| New York City Municipal Water | | | | | |

| Finance Authority, Water | | | | | |

| and Sewer System Second | | | | | |

| General Resolution Revenue | | | | | |

| (Liquidity Facility; Bank of | | | | | |

| Nova Scotia) | 0.07 | 7/1/13 | 6,900,000 | a | 6,900,000 |

| New York City Transitional Finance | | | | | |

| Authority, Future Tax Secured | | | | | |

| Subordinate Revenue (Liquidity | | | | | |

| Facility; California State | | | | | |

| Teachers Retirement System) | 0.05 | 7/1/13 | 2,700,000 | a | 2,700,000 |

| New York City Trust for Cultural | | | | | |

| Resources, Revenue (Alvin | | | | | |

| Ailey Dance Foundation) | | | | | |

| (LOC; Citibank NA) | 0.09 | 7/7/13 | 5,660,000 | a | 5,660,000 |

| New York City Trust for Cultural | | | | | |

| Resources, Revenue, Refunding | | | | | |

| (American Museum of Natural | | | | | |

| History) (Liquidity Facility; | | | | | |

| Wells Fargo Bank) | 0.03 | 7/7/13 | 4,500,000 | a | 4,500,000 |

| New York Liberty Development | | | | | |

| Corporation, Liberty Revenue, | | | | | |

| Refunding (3 World Trade | | | | | |

| Center Project) (LOC; | | | | | |

| JPMorgan Chase Bank) | 0.09 | 7/7/13 | 6,005,000 | a | 6,005,000 |

The Fund 9

STATEMENT OF INVESTMENTS (continued)

| | | | | |

| Short-Term | Coupon | Maturity | Principal | | |

| Investments (continued) | Rate (%) | Date | Amount ($) | | Value ($) |

| New York Liberty Development | | | | | |

| Corporation, Recovery Zone | | | | | |

| Revenue (3 World Trade Center | | | | | |

| Project) (LOC; JPMorgan | | | | | |

| Chase Bank) | 0.09 | 7/7/13 | 1,490,000 | a | 1,490,000 |

| New York State Energy Research | | | | | |

| and Development Authority, | | | | | |

| Facilities Revenue (Consolidated | | | | | |

| Edison Company of New York, Inc. | | | | | |

| Project) (LOC; Mizuho Corporate | | | | | |

| Bank Ltd.) | 0.06 | 7/7/13 | 650,000 | a | 650,000 |

| New York State Housing Finance | | | | | |

| Agency, Housing Revenue | | | | | |

| (Baisley Park Gardens) (LOC; | | | | | |

| Citibank NA) | 0.10 | 7/7/13 | 5,000,000 | a | 5,000,000 |

| Otsego County Industrial | | | | | |

| Development Agency, Civic | | | | | |

| Facility Revenue (Saint James | | | | | |

| Retirement Community Project) | | | | | |

| (LOC; M&T Trust) | 0.11 | 7/7/13 | 1,555,000 | a | 1,555,000 |

| Port Authority of New York and | | | | | |

| New Jersey, Equipment Notes | 0.11 | 7/7/13 | 4,000,000 | a | 4,000,000 |

| Rensselaer Industrial Development | | | | | |

| Agency, Senior Housing Revenue | | | | | |

| (Brunswick Senior Housing | | | | | |

| Project) (LOC; FHLB) | 0.07 | 7/1/13 | 2,600,000 | a | 2,600,000 |

| Rockland County Industrial | | | | | |

| Development Agency, IDR | | | | | |

| (Intercos America, Inc. | | | | | |

| Project) (LOC; HSBC Bank USA) | 0.40 | 7/7/13 | 2,500,000 | a | 2,500,000 |

| Rockland County Industrial | | | | | |

| Development Authority, Revenue | | | | | |

| (Northern Manor Multicare | | | | | |

| Center, Inc. Project) | | | | | |

| (LOC; M&T Trust) | 0.16 | 7/7/13 | 2,300,000 | a | 2,300,000 |

10

| | | | | | |

| Short-Term | Coupon | Maturity | Principal | | | |

| Investments (continued) | Rate (%) | Date | Amount ($) | | Value ($) | |

| Triborough Bridge and Tunnel | | | | | | |

| Authority, General Revenue | | | | | | |

| (MTA Bridges and Tunnels) | | | | | | |

| (LOC; California State | | | | | | |

| Teachers Retirement System) | 0.06 | 7/1/13 | 1,150,000 | a | 1,150,000 | |

| |

| Total Investments (cost $126,555,199) | | | 100.9 | % | 126,555,199 | |

| Liabilities, Less Cash and Receivables | | | (.9 | %) | (1,175,722 | ) |

| Net Assets | | | 100.0 | % | 125,379,477 | |

|

| a Variable rate demand note—rate shown is the interest rate in effect at June 30, 2013. Maturity date represents the |

| next demand date, or the ultimate maturity date if earlier. |

| b Securities exempt from registration pursuant to Rule 144A under the Securities Act of 1933.These securities may be |

| resold in transactions exempt from registration, normally to qualified institutional buyers.At June 30, 2013, these |

| securities amounted to $10,000,000 or 8.0% of net assets. |

| c The fund does not directly own the municipal security indicated; the fund owns an interest in a special purpose entity |

| that, in turn, owns the underlying municipal security.The special purpose entity permits the fund to own interests in |

| underlying assets, but in a manner structured to provide certain advantages not inherent in the underlying bonds (e.g., |

| enhanced liquidity, yields linked to short-term rates). |

The Fund 11

STATEMENT OF INVESTMENTS (continued)

| | | |

| Summary of Abbreviations | | |

| |

| ABAG | Association of Bay Area | ACA | American Capital Access |

| | Governments | | |

| AGC | ACE Guaranty Corporation | AGIC | Asset Guaranty Insurance Company |

| AMBAC | American Municipal Bond | ARRN | Adjustable Rate |

| | Assurance Corporation | | Receipt Notes |

| BAN | Bond Anticipation Notes | BPA | Bond Purchase Agreement |

| CIFG | CDC Ixis Financial Guaranty | COP | Certificate of Participation |

| CP | Commercial Paper | DRIVERS | Derivative Inverse |

| | | | Tax-Exempt Receipts |

| EDR | Economic Development | EIR | Environmental Improvement |

| | Revenue | | Revenue |

| FGIC | Financial Guaranty | FHA | Federal Housing |

| | Insurance Company | | Administration |

| FHLB | Federal Home | FHLMC | Federal Home Loan Mortgage |

| | Loan Bank | | Corporation |

| FNMA | Federal National | GAN | Grant Anticipation Notes |

| | Mortgage Association | | |

| GIC | Guaranteed Investment | GNMA | Government National Mortgage |

| | Contract | | Association |

| GO | General Obligation | HR | Hospital Revenue |

| IDB | Industrial Development Board | IDC | Industrial Development Corporation |

| IDR | Industrial Development | LIFERS | Long Inverse Floating |

| | Revenue | | Exempt Receipts |

| LOC | Letter of Credit | LOR | Limited Obligation Revenue |

| LR | Lease Revenue | MERLOTS | Municipal Exempt Receipts |

| | | | Liquidity Option Tender |

| MFHR | Multi-Family Housing Revenue | MFMR | Multi-Family Mortgage Revenue |

| PCR | Pollution Control Revenue | PILOT | Payment in Lieu of Taxes |

| P-FLOATS | Puttable Floating Option | PUTTERS | Puttable Tax-Exempt Receipts |

| | Tax-Exempt Receipts | | |

| RAC | Revenue Anticipation Certificates | RAN | Revenue Anticipation Notes |

| RAW | Revenue Anticipation Warrants | ROCS | Reset Options Certificates |

| RRR | Resources Recovery Revenue | SAAN | State Aid Anticipation Notes |

| SBPA | Standby Bond Purchase Agreement | SFHR | Single Family Housing Revenue |

| SFMR | Single Family Mortgage Revenue | SONYMA | State of New York Mortgage Agency |

| SPEARS | Short Puttable Exempt | SWDR | Solid Waste Disposal Revenue |

| | Adjustable Receipts | | |

| TAN | Tax Anticipation Notes | TAW | Tax Anticipation Warrants |

| TRAN | Tax and Revenue Anticipation Notes | XLCA | XL Capital Assurance |

12

| | | | | | |

| Summary of Combined Ratings (Unaudited) | |

| |

| Fitch | | or | Moody’s | or | Standard & Poor’s | Value (%)† |

| F1 | +,F1 | | VMIG1,MIG1,P1 | | SP1+,SP1,A1+,A1 | 67.8 |

| F2 | | | VMIG2,MIG2,P2 | | SP2, A2 | 16.3 |

| Not Ratedd | | | Not Ratedd | | Not Ratedd | 15.9 |

| | | | | | | 100.0 |

|

| † Based on total investments. |

| d Securities which, while not rated by Fitch, Moody’s and Standard & Poor’s, have been determined by the Manager to |

| be of comparable quality to those rated securities in which the fund may invest. |

See notes to financial statements.

The Fund 13

STATEMENT OF ASSETS AND LIABILITIES

June 30, 2013

| | |

| | Cost | Value |

| Assets ($): | | |

| Investments in securities—See Statement of Investments | 126,555,199 | 126,555,199 |

| Cash | | 73,856 |

| Interest receivable | | 80,249 |

| | | 126,709,304 |

| Liabilities ($): | | |

| Due to The Dreyfus Corporation and affiliates—Note 2(a) | | 21,036 |

| Payable for investment securities purchased | | 1,308,788 |

| Payable for shares of Beneficial Interest redeemed | | |

| Dividend payable | | |

| | | 1,329,827 |

| Net Assets ($) | | 125,379,477 |

| Composition of Net Assets ($): | | |

| Paid-in capital | | 125,379,477 |

| Net Assets ($) | | 125,379,477 |

| Shares Outstanding | | |

| (unlimited number of shares of Beneficial Interest authorized) | | 125,379,487 |

| Net Asset Value, offering and redemption price per share ($) | | 1.00 |

|

| See notes to financial statements. |

14

STATEMENT OF OPERATIONS

Year Ended June 30, 2013

| | |

| Investment Income ($): | | |

| Interest Income | 365,236 | |

| Expenses: | | |

| Management fee—Note 2(a) | 593,027 | |

| Trustees’ fees—Note 2(a,b) | 8,079 | |

| Total Expenses | 601,106 | |

| Less—reduction in expenses due to undertaking—Note 2(a) | (227,862 | ) |

| Less—Trustees’ fees reimbursed by the Manager—Note 2(a) | (8,079 | ) |

| Net Expenses | 365,165 | |

| Investment Income—Net, representing net increase | | |

| in net assets resulting from operations | 71 | |

| |

| See notes to financial statements. | | |

The Fund 15

STATEMENT OF CHANGES IN NET ASSETS

| | | | |

| | | | Year Ended June 30, | |

| | 2013 | | 2012 | |

| Operations ($): | | | | |

| Investment income—net | 71 | | 24 | |

| Net realized gain (loss) on investments | — | | 4,605 | |

| Net Increase (Decrease) in Net Assets | | | | |

| Resulting from Operations | 71 | | 4,629 | |

| Dividends to Shareholders from ($): | | | | |

| Investment income—net | (4,676 | ) | (24 | ) |

| Beneficial Interest Transactions ($1.00 per share): | | | | |

| Net proceeds from shares sold | 140,800,977 | | 201,818,149 | |

| Dividends reinvested | 3,417 | | 16 | |

| Cost of shares redeemed | (168,361,711 | ) | (218,373,946 | ) |

| Increase (Decrease) in Net Assets from | | | | |

| Beneficial Interest Transactions | (27,557,317 | ) | (16,555,781 | ) |

| Total Increase (Decrease) in Net Assets | (27,561,922 | ) | (16,551,176 | ) |

| Net Assets ($): | | | | |

| Beginning of Period | 152,941,399 | | 169,492,575 | |

| End of Period | 125,379,477 | | 152,941,399 | |

|

| See notes to financial statements. |

16

FINANCIAL HIGHLIGHTS

The following table describes the performance for the fiscal periods indicated. Total return shows how much your investment in the fund would have increased (or decreased) during each period, assuming you had reinvested all dividends and distributions.These figures have been derived from the fund’s financial statements.

| | | | | | | | | | |

| | | | Year Ended June 30, | | | |

| | 2013 | | 2012 | | 2011 | | 2010 | | 2009 | |

| Per Share Data ($): | | | | | | | | | | |

| Net asset value, beginning of period | 1.00 | | 1.00 | | 1.00 | | 1.00 | | 1.00 | |

| Investment Operations: | | | | | | | | | | |

| Investment income—net | .000 | a | .000 | a | .000 | a | .001 | | .013 | |

| Distributions: | | | | | | | | | | |

| Dividends from investment income—net | (.000 | )a | (.000 | )a | (.000 | )a | (.001 | ) | (.013 | ) |

| Net asset value, end of period | 1.00 | | 1.00 | | 1.00 | | 1.00 | | 1.00 | |

| Total Return (%) | .00 | b | .00 | b | .00 | b | .07 | | 1.35 | |

| Ratios/Supplemental Data (%): | | | | | | | | | | |

| Ratio of total expenses | | | | | | | | | | |

| to average net assets | .46 | | .46 | | .46 | | .47 | | .49 | |

| Ratio of net expenses | | | | | | | | | | |

| to average net assets | .28 | | .27 | | .42 | | .43 | | .48 | |

| Ratio of net investment income | | | | | | | | | | |

| to average net assets | .00 | b | .00 | b | .00 | b | .07 | | 1.37 | |

| Net Assets, end of period ($ x 1,000) | 125,379 | | 152,941 | | 169,493 | | 221,622 | | 303,439 | |

| |

| a | Amount represents less than $.001 per share. |

| b | Amount represents less than .01%. |

See notes to financial statements.

The Fund 17

NOTES TO FINANCIAL STATEMENTS

NOTE 1—Significant Accounting Policies:

Dreyfus BASIC New York Municipal Money Market Fund (the “fund”) is the sole series of The Dreyfus/Laurel Tax-Free Municipal Funds (the “Trust”), which is registered under the Investment Company Act of 1940, as amended (the “Act”), as an open-end management investment company.The fund seeks to provide a high level of current income exempt from federal, NewYork state and NewYork city income taxes to the extent consistent with the preservation of capital and the maintenance of liquidity.The Dreyfus Corporation (the “Manager” or “Dreyfus”), a wholly-owned subsidiary of The Bank of NewYork Mellon Corporation (“BNY Mellon”), serves as the fund’s investment adviser. MBSC Securities Corporation (the “Distributor”), a wholly-owned subsidiary of the Manager, is the distributor of the fund’s shares, which are sold without a sales charge.

It is the fund’s policy to maintain a continuous net asset value per share of $1.00; the fund has adopted certain investment, portfolio valuation and dividend and distribution policies to enable it to do so.There is no assurance, however, that the fund will be able to maintain a stable net asset value per share of $1.00.

The Financial Accounting Standards Board (“FASB”) Accounting Standards Codification is the exclusive reference of authoritative U.S. generally accepted accounting principles (“GAAP”) recognized by the FASB to be applied by nongovernmental entities. Rules and interpretive releases of the Securities and Exchange Commission (“SEC”) under authority of federal laws are also sources of authoritative GAAP for SEC registrants. The fund’s financial statements are prepared in accordance with GAAP, which may require the use of management estimates and assumptions.Actual results could differ from those estimates.

(a) Portfolio valuation: Investments in securities are valued at amortized cost in accordance with Rule 2a-7 under the Act. If amortized cost is determined not to approximate market value, the fair value of

18

the portfolio securities will be determined by procedures established by and under the general supervision of the Trust’s Board of Trustees (the “Board”).

The fair value of a financial instrument is the amount that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date (i.e., the exit price). GAAP establishes a fair value hierarchy that prioritizes the inputs of valuation techniques used to measure fair value.This hierarchy gives the highest priority to unadjusted quoted prices in active markets for identical assets or liabilities (Level 1 measurements) and the lowest priority to unobservable inputs (Level 3 measurements).

Additionally, GAAP provides guidance on determining whether the volume and activity in a market has decreased significantly and whether such a decrease in activity results in transactions that are not orderly. GAAP requires enhanced disclosures around valuation inputs and techniques used during annual and interim periods.

Various inputs are used in determining the value of the fund’s investments relating to fair value measurements.These inputs are summarized in the three broad levels listed below:

Level 1—unadjusted quoted prices in active markets for identical investments.

Level 2—other significant observable inputs (including quoted prices for similar investments, interest rates, prepayment speeds, credit risk, etc.).

Level 3—significant unobservable inputs (including the fund’s own assumptions in determining the fair value of investments).

The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities. For example, money market securities are valued using amortized

The Fund 19

NOTES TO FINANCIAL STATEMENTS (continued)

cost, in accordance with rules under the Act. Generally, amortized cost approximates the current fair value of a security, but since the value is not obtained from a quoted price in an active market, such securities are reflected within Level 2 of the fair value hierarchy.

The following is a summary of the inputs used as of June 30, 2013 in valuing the fund’s investments:

| |

| | Short-Term |

| Valuation Inputs | Investments ($)† |

| Level 1—Unadjusted Quoted Prices | — |

| Level 2—Other Significant Observable Inputs | 126,555,199 |

| Level 3—Significant Unobservable Inputs | — |

| Total | 126,555,199 |

| † See Statement of Investments for additional detailed categorizations. | |

At June 30, 2013, there were no transfers between Level 1 and Level 2 of the fair value hierarchy.

(b) Securities transactions and investment income: Securities transactions are recorded on a trade date basis. Interest income, adjusted for accretion of discount and amortization of premium on investments, is earned from settlement date and is recognized on the accrual basis. Realized gains and losses from securities transactions are recorded on the identified cost basis. Cost of investments represents amortized cost.

The fund follows an investment policy of investing primarily in municipal obligations of one state. Economic changes affecting the state and certain of its public bodies and municipalities may affect the ability of issuers within the state to pay interest on, or repay principal of, municipal obligations held by the fund.

(c) Dividends to shareholders: It is the policy of the fund to declare dividends daily from investment income-net. Such dividends are paid monthly. Dividends from net realized capital gains, if any, are normally declared and paid annually, but the fund may make distributions on a more frequent basis to comply with the distribution requirements of the Internal Revenue Code of 1986, as amended, (the “Code”).To the

20

extent that net realized capital gains can be offset by capital loss carryovers, it is the policy of the fund not to distribute such gains.

(d) Federal income taxes: It is the policy of the fund to continue to qualify as a regulated investment company, which can distribute tax-exempt dividends, by complying with the applicable provisions of the Code, and to make distributions of income and net realized capital gain sufficient to relieve it from substantially all federal income and excise taxes.

As of and during the period ended June 30, 2013, the fund did not have any liabilities for any uncertain tax positions.The fund recognizes interest and penalties, if any, related to uncertain tax positions as income tax expense in the Statement of Operations. During the period, the fund did not incur any interest or penalties.

Each tax year in the four-year period ended June 30, 2013 remains subject to examination by the Internal Revenue Service and state taxing authorities.

At June 30, 2013, the components of accumulated earnings on a tax basis were substantially the same as the cost for financial reporting purposes.

The tax character of distributions paid to shareholders during the fiscal periods ended June 30, 2013 and June 30, 2012 were as follows: tax-exempt income $71 and $24 and ordinary income $4,605 and $0, respectively.

During the period ended June 30, 2013, as a result of permanent book to tax differences, primarily due to dividend reclassification, the fund increased accumulated undistributed investment income-net by $4,605 and decreased accumulated net realized gain (loss) on investments by the same amount. Net assets and net asset value per share were not affected by this reclassification.

At June 30, 2013, the cost of investments for federal income tax purposes was substantially the same as the cost for financial reporting purposes (see the Statement of Investments).

The Fund 21

NOTES TO FINANCIAL STATEMENTS (continued)

NOTE 2—Investment Management Fee and Other Transactions with Affiliates:

(a) Pursuant to an investment management agreement with the Manager, the Manager provides or arranges for one or more third parties and/or affiliates to provide investment advisory, administrative, custody, fund accounting and transfer agency services to the fund.The Manager also directs the investments of the fund in accordance with its investment objective, policies and limitations. For these services, the fund is contractually obligated to pay the Manager a fee, calculated daily and paid monthly, at the annual rate of .45% of the value of the fund’s average daily net assets. Out of its fee, the Manager pays all of the expenses of the fund excluding brokerage fees, taxes, interest, fees and expenses of non-interested Trustees (including counsel fees) and extraordinary expenses. In addition, the Manager is required to reduce its fee in an amount equal to the fund’s allocable portion of fees and expenses of the non-interested Trustees (including counsel fees). During the period ended June 30, 2013, fees reimbursed by the Manager amounted to $8,079.

The Manager has undertaken to waive receipt of the management fee and/or reimburse operating expenses in order to facilitate a daily yield at or above a certain level which may change from time to time.This undertaking is voluntary and not contractual, and may be terminated at any time. The reduction in expenses, pursuant to the undertaking, amounted to $227,862 during the period ended June 30, 2013.

The components of “Due to The Dreyfus Corporation and affiliates” in the Statement of Assets and Liabilities consist of: management fees $46,479, which are offset against an expense reimbursement currently in effect in the amount of $25,443.

22

(b) Each Board member also serves as a Board member of other funds within the Dreyfus complex. Annual retainer fees and attendance fees are allocated to each fund based on net assets.

NOTE 3—Securities Transactions:

The fund is permitted to purchase or sell securities from or to certain affiliated funds under specified conditions outlined in procedures adopted by the Board. The procedures have been designed to ensure that any purchase or sale of securities by the fund from or to another fund or portfolio that are, or could be, considered an affiliate by virtue of having a common investment adviser (or affiliated investment adviser), common Trustees and/or common officers, complies with Rule 17a-7 under the Act. During the period ended June 30, 2013, the fund engaged in purchases and sales of securities pursuant to Rule 17a-7 under the Act amounting to $35,400,000 and $66,265,000, respectively.

The Fund 23

REPORT OF INDEPENDENT REGISTERED

PUBLIC ACCOUNTING FIRM

The Board of Trustees and Shareholders of

Dreyfus BASIC New York Municipal Money Market Fund

We have audited the accompanying statement of assets and liabilities of Dreyfus BASIC New York Municipal Money Market Fund (the “Fund”), a series of The Dreyfus/Laurel Tax-Free Municipal Funds, including the statement of investments, as of June 30, 2013, and the related statement of operations for the year then ended, the statements of changes in net assets for each of the years in the two-year period then ended and the financial highlights for each of the years in the five-year period then ended. These financial statements and financial highlights are the responsibility of the Fund’s management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States).Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement.An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. Our procedures included confirmation of securities owned as of June 30, 2013, by correspondence with the custodian and brokers or by other appropriate auditing procedures where replies from brokers were not received. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation.We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of Dreyfus BASIC New York Municipal Money Market Fund as of June 30, 2013, and the results of its operations for the year then ended, the changes in its net assets for each of the years in the two-year period then ended and the financial highlights for each of the years in the five-year period then ended, in conformity with U.S. generally accepted accounting principles.

New York, New York

August 14, 2013

24

IMPORTANT TAX INFORMATION (Unaudited)

In accordance with federal tax law, the fund hereby designates $71 as dividends paid from investment income-net during the fiscal year ended June 30, 2013 as “exempt-interest dividends” (not subject to regular federal and, for individuals who are New York residents, New York state and NewYork city personal income taxes), and $4,605 as an ordinary income distribution for reporting purposes. Where required by federal tax law rules, shareholders will receive notification of their portion of the fund’s exempt-interest dividends paid for the 2013 calendar year on Form 1099-DIV, which will be mailed in early 2014.

The Fund 25

INFORMATION ABOUT THE RENEWAL OF THE FUND’S

INVESTMENT MANAGEMENT AGREEMENT (Unaudited)

At a meeting of the fund’s Board of Trustees held on February 13-14, 2013, the Board considered the renewal of the fund’s Investment Management Agreement pursuant to which Dreyfus provides the fund with investment advisory and administrative services (the “Agreement”).The Board members, none of whom are “interested persons” (as defined in the Investment Company Act of 1940, as amended) of the fund, were assisted in their review by independent legal counsel and met with counsel in executive session separate from Dreyfus representatives. In considering the renewal of the Agreement, the Board considered all factors that it believed to be relevant, including those discussed below.The Board did not identify any one factor as dispositive, and each Board member may have attributed different weights to the factors considered.

Analysis of Nature, Extent, and Quality of Services Provided to the Fund. The Board considered information provided to them at the meeting and in previous presentations from Dreyfus representatives regarding the nature, extent, and quality of the services provided to funds in the Dreyfus fund complex. Dreyfus provided the number of open accounts in the fund, the fund’s asset size and the allocation of fund assets among distribution channels. Dreyfus also had previously provided information regarding the diverse intermediary relationships and distribution channels of funds in the Dreyfus fund complex (such as retail direct or intermediary, in which intermediaries typically are paid by the fund and/or Dreyfus) and Dreyfus’ corresponding need for broad, deep, and diverse resources to be able to provide ongoing shareholder services to each intermediary or distribution channel, as applicable to the fund.

The Board also considered research support available to, and portfolio management capabilities of, the fund’s portfolio management personnel and that Dreyfus also provides oversight of day-to-day fund operations, including fund accounting and administration and assistance in meeting legal and regulatory requirements.The Board also considered Dreyfus’ extensive administrative, accounting, and compliance infrastructures.

26

Comparative Analysis of the Fund’s Performance and Management Fee and Expense Ratio.The Board reviewed reports prepared by Lipper, Inc. (“Lipper”), an independent provider of investment company data, which included information comparing (1) the fund’s performance with the performance of a group of comparable funds (the “Performance Group”) and with a broader group of funds (the “Performance Universe”), all for various periods ended December 31, 2012, and (2) the fund’s actual and contractual management fees and total expenses with those of a group of comparable funds (the “Expense Group”) and with a broader group of funds (the “Expense Universe”), the information for which was derived in part from fund financial statements available to Lipper as of the date of its analysis. Dreyfus previously had furnished the Board with a description of the methodology Lipper used to select the Performance Group and Performance Universe and the Expense Group and Expense Universe.

Dreyfus representatives stated that the usefulness of performance comparisons may be affected by a number of factors, including different investment limitations that may be applicable to the fund and comparison funds. The Board discussed the results of the comparisons and noted that the fund’s total return performance was above or one or two basis points below the Performance Group and Performance Universe medians for the various periods.

The Board also reviewed the range of actual and contractual management fees and total expenses of the Expense Group and Expense Universe funds and discussed the results of the comparisons. Taking into account the fund’s “unitary” fee structure, the Board noted that the fund’s contractual management fee was at the Expense Group median, the fund’s actual management fee was above the Expense Group and Expense Universe medians (were the highest in the Expense Group and Expense Universe) and the fund’s total expenses were at the Expense Group median and slightly above the Expense

The Fund 27

INFORMATION ABOUT THE RENEWAL OF THE FUND’S INVESTMENT

MANAGEMENT AGREEMENT (Unaudited) (continued)

Universe median. The Board also considered the current fee waiver and expense reimbursement arrangement undertaken by Dreyfus.

Dreyfus representatives reviewed with the Board the management or investment advisory fees paid by funds advised or administered by Dreyfus that are in the same Lipper category as the fund (the “Similar Clients”), and explained the nature of the Similar Clients.They discussed differences in fees paid and the relationship of the fees paid in light of any differences in the services provided and other relevant factors, noting the fund’s “unitary” fee structure. The Board considered the relevance of the fee information provided for the Similar Clients to evaluate the appropriateness and reasonableness of the fund’s management fee.

Analysis of Profitability and Economies of Scale. Dreyfus representatives reviewed the expenses allocated and profit received by Dreyfus and the resulting profitability percentage for managing the fund and the aggregate profitability percentage to Dreyfus of managing the funds in the Dreyfus fund complex, and the method used to determine the expenses and profit. The Board concluded that the profitability results were not unreasonable, given the services rendered and service levels provided by Dreyfus. The Board also noted the fee waiver and expense reimbursement arrangement and its effect on Dreyfus’ prof-itability.The Board also had been provided with information prepared by an independent consulting firm regarding Dreyfus’ approach to allocating costs to, and determining the profitability of, individual funds and the entire Dreyfus fund complex.The consulting firm also had analyzed where any economies of scale might emerge in connection with the management of a fund.

The Board’s counsel stated that the Board should consider the profitability analysis (1) as part of the evaluation of whether the fees under the Agreement bear a reasonable relationship to the mix of services provided by Dreyfus, including the nature, extent and quality of such services, and (2) in light of the relevant circumstances for the fund and the extent to which economies of scale would be realized if the fund grows

28

and whether fee levels reflect these economies of scale for the benefit of fund shareholders. Dreyfus representatives noted that a discussion of economies of scale is predicated on a fund having achieved a substantial size with increasing assets and that, if a fund’s assets had been stable or decreasing, the possibility that Dreyfus may have realized any economies of scale would be less. Dreyfus representatives also noted that, as a result of shared and allocated costs among funds in the Dreyfus fund complex, the extent of economies of scale could depend substantially on the level of assets in the complex as a whole, so that increases and decreases in complex-wide assets can affect potential economies of scale in a manner that is disproportionate to, or even in the opposite direction from, changes in the fund’s asset level.The Board also considered potential benefits to Dreyfus from acting as investment adviser and noted that there were no soft dollar arrangements in effect for trading the fund’s investments.

At the conclusion of these discussions, the Board agreed that it had been furnished with sufficient information to make an informed business decision with respect to the renewal of the Agreement. Based on the discussions and considerations as described above, the Board concluded and determined as follows.

The Board concluded that the nature, extent and quality of the services provided by Dreyfus are adequate and appropriate.

The Board was satisfied with the fund’s relative performance.

The Board concluded that the fee paid to Dreyfus was reasonable in light of the considerations described above.

The Board determined that the economies of scale which may accrue to Dreyfus and its affiliates in connection with the management of the fund had been adequately considered by Dreyfus in connection with the fee rate charged to the fund pursuant to the Agreement and that, to the extent in the future it were determined that material economies of scale had not been shared with the fund, the Board would seek to have those economies of scale shared with the fund.

The Fund 29

INFORMATION ABOUT THE RENEWAL OF THE FUND’S INVESTMENT

MANAGEMENT AGREEMENT (Unaudited) (continued)

In evaluating the Agreement, the Board considered these conclusions and determinations and also relied on its previous knowledge, gained through meetings and other interactions with Dreyfus and its affiliates, of the fund and the services provided to the fund by Dreyfus.The Board also relied on information received on a routine and regular basis throughout the year relating to the operations of the fund and the investment management and other services provided under the Agreement, including information on the investment performance of the fund in comparison to similar mutual funds and benchmark performance indices; general market outlook as applicable to the fund; and compliance reports. In addition, it should be noted that the Board’s consideration of the contractual fee arrangements for this fund had the benefit of a number of years of reviews of prior or similar agreements during which lengthy discussions took place between the Board and Dreyfus representatives. Certain aspects of the arrangements may receive greater scrutiny in some years than in others, and the Board’s conclusions may be based, in part, on their consideration of the same or similar arrangements in prior years. The Board determined that renewal of the Agreement was in the best interests of the fund and its shareholders.

30

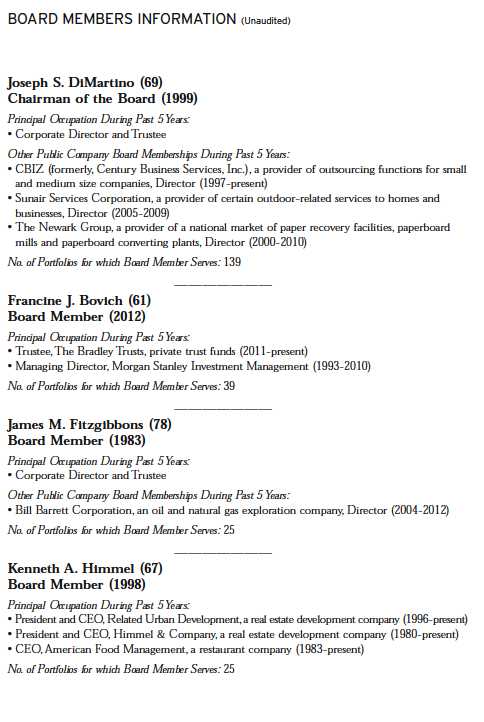

The Fund 31

32

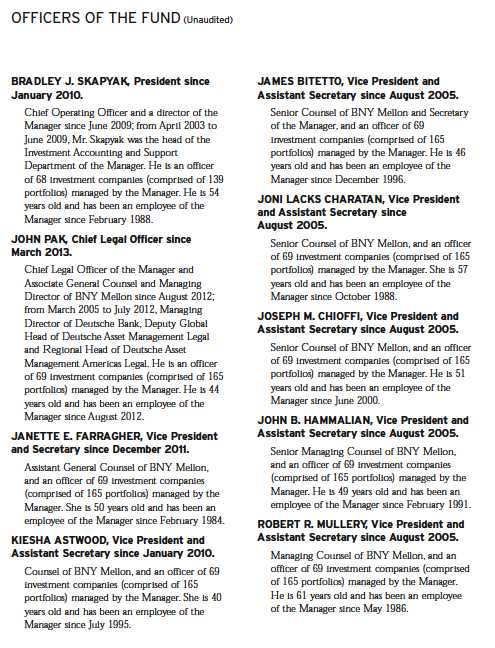

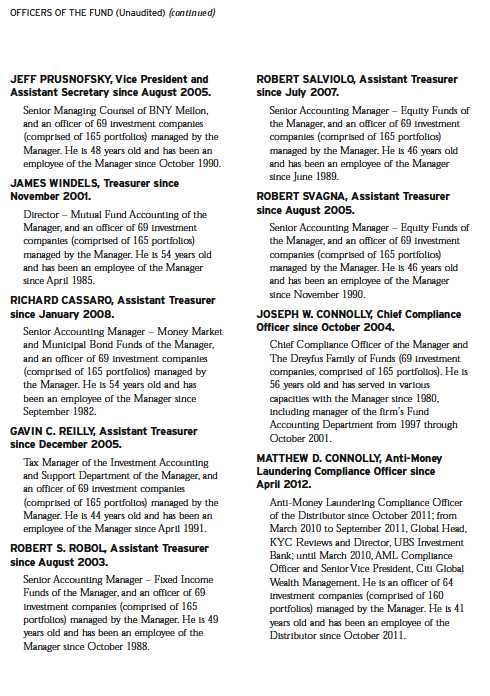

TheFund 33

34

Item 2. Code of Ethics.

The Registrant has adopted a code of ethics that applies to the Registrant's principal executive officer, principal financial officer, principal accounting officer or controller, or persons performing similar functions. There have been no amendments to, or waivers in connection with, the Code of Ethics during the period covered by this Report.

Item 3. Audit Committee Financial Expert.

The Registrant's Board has determined that Joseph S. DiMartino, a member of the Audit Committee of the Board, is an audit committee financial expert as defined by the Securities and Exchange Commission (the "SEC"). Joseph S. DiMartino is "independent" as defined by the SEC for purposes of audit committee financial expert determinations.

Item 4. Principal Accountant Fees and Services.

(a) Audit Fees. The aggregate fees billed for each of the last two fiscal years (the "Reporting Periods") for professional services rendered by the Registrant's principal accountant (the "Auditor") for the audit of the Registrant's annual financial statements, or services that are normally provided by the Auditor in connection with the statutory and regulatory filings or engagements for the Reporting Periods, were $81,090 in 2012 and $27,880 in 2013.

(b) Audit-Related Fees. The aggregate fees billed in the Reporting Periods for assurance and related services by the Auditor that are reasonably related to the performance of the audit of the Registrant's financial statements and are not reported under paragraph (a) of this Item 4 were $6,930 in 2012 and $2,340 in 2013. These services consisted of one or more of the following: (i) agreed upon procedures related to compliance with Internal Revenue Code section 817(h), (ii) security counts required by Rule 17f-2 under the Investment Company Act of 1940, as amended, (iii) advisory services as to the accounting or disclosure treatment of Registrant transactions or events and (iv) advisory services to the accounting or disclosure treatment of the actual or potential impact to the Registrant of final or proposed rules, standards or interpretations by the Securities and Exchange Commission, the Financial Accounting Standards Boards or other regulatory or standard-setting bodies.

The aggregate fees billed in the Reporting Periods for non-audit assurance and related services by the Auditor to the Registrant's investment adviser (not including any sub-investment adviser whose role is primarily portfolio management and is subcontracted with or overseen by another investment adviser), and any entity controlling, controlled by or under common control with the investment adviser that provides ongoing services to the Registrant ("Service Affiliates"), that were reasonably related to the performance of the annual audit of the Service Affiliate, which required pre-approval by the Audit Committee were $0 in 2012 and $0 in 2013.

(c) Tax Fees. The aggregate fees billed in the Reporting Periods for professional services rendered by the Auditor for tax compliance, tax advice and tax planning ("Tax Services") were $6,930 in 2012 and $2,340 in 2013. These services consisted of review or preparation of U.S. federal, state, local and excise tax returns. The aggregate fees billed in the Reporting Periods for Tax Services by the Auditor to Service Affiliates which required pre-approval by the Audit Committee were $0 in 2012 and $0 in 2013.

(d) All Other Fees. The aggregate fees billed in the Reporting Periods for products and services provided by the Auditor, other than the services reported in paragraphs (a) through (c) of this Item, were $0 in 2012 and $0 in 2013.

The aggregate fees billed in the Reporting Periods for Non-Audit Services by the Auditor to Service Affiliates, other than the services reported in paragraphs (b) through (c) of this Item, which required pre-approval by the Audit Committee were $0 in 2012 and $0 in 2013.

(e)(1) Audit Committee Pre-Approval Policies and Procedures. The Registrant's Audit Committee has established policies and procedures (the "Policy") for pre-approval (within specified fee limits) of the Auditor's engagements for non-audit services to the Registrant and Service Affiliates without specific case-by-case consideration. The pre-approved services in the Policy can include pre-approved audit services, pre-approved audit-related services, pre-approved tax services and pre-approved all other services. Pre-approval considerations include whether the proposed services are compatible with maintaining the Auditor's independence. Pre-approvals pursuant to the Policy are considered annually.

(e)(2) Note: None of the services described in paragraphs (b) through (d) of this Item 4 were approved by the Audit Committee pursuant to paragraph (c)(7)(i)(C) of Rule 2-01 of Regulation S-X.

(f) None of the hours expended on the principal accountant's engagement to audit the registrant's financial statements for the most recent fiscal year were attributed to work performed by persons other than the principal account's full-time, permanent employees.

Non-Audit Fees. The aggregate non-audit fees billed by the Auditor for services rendered to the Registrant, and rendered to Service Affiliates, for the Reporting Periods were $11,724,170 in 2012 and $14,767,243 in 2013.

Auditor Independence. The Registrant's Audit Committee has considered whether the provision of non-audit services that were rendered to Service Affiliates which were not pre-approved (not requiring pre-approval) is compatible with maintaining the Auditor's independence.

Item 5. Audit Committee of Listed Registrants.

Not applicable.

Item 6. Investments.

(a) Not applicable.

Item 7. Disclosure of Proxy Voting Policies and Procedures for Closed-End Management Investment Companies.

Not applicable.

Item 8. Portfolio Managers of Closed-End Management Investment Companies.

Not applicable.

Item 9. �� Purchases of Equity Securities by Closed-End Management Investment Companies and Affiliated Purchasers.

Not applicable.

Item 10. Submission of Matters to a Vote of Security Holders.

There have been no material changes to the procedures applicable to Item 10.

Item 11. Controls and Procedures.

(a) The Registrant's principal executive and principal financial officers have concluded, based on their evaluation of the Registrant's disclosure controls and procedures as of a date within 90 days of the filing date of this report, that the Registrant's disclosure controls and procedures are reasonably designed to ensure that information required to be disclosed by the Registrant on Form N-CSR is recorded, processed, summarized and reported within the required time periods and that information required to be disclosed by the Registrant in the reports that it files or submits on Form N-CSR is accumulated and communicated to the Registrant's management, including its principal executive and principal financial officers, as appropriate to allow timely decisions regarding required disclosure.

(b) There were no changes to the Registrant's internal control over financial reporting that occurred during the second fiscal quarter of the period covered by this report that have materially affected, or are reasonably likely to materially affect, the Registrant's internal control over financial reporting.

Item 12. Exhibits.

(a)(1) Code of ethics referred to in Item 2.

(a)(2) Certifications of principal executive and principal financial officers as required by Rule 30a-2(a) under the Investment Company Act of 1940.

(a)(3) Not applicable.

(b) Certification of principal executive and principal financial officers as required by Rule 30a-2(b) under the Investment Company Act of 1940.

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment Company Act of 1940, the Registrant has duly caused this Report to be signed on its behalf by the undersigned, thereunto duly authorized.

The Dreyfus/Laurel Tax-Free Municipal Funds

By: /s/ Bradley J. Skapyak |

Bradley J. Skapyak, President |

Date: | 08/15/2013 |

|

Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment Company Act of 1940, this Report has been signed below by the following persons on behalf of the Registrant and in the capacities and on the dates indicated. |

|

By: /s/ Bradley J. Skapyak |

Bradley J. Skapyak, President |

Date: | 08/15/2013 |

|

By: /s/ James Windels |

James Windels, Treasurer |

Date: | 08/15/2013 |

|

EXHIBIT INDEX

(a)(1) Code of ethics referred to in Item 2.

(a)(2) Certifications of principal executive and principal financial officers as required by Rule 30a-2(a) under the Investment Company Act of 1940. (EX-99.CERT)

(b) Certification of principal executive and principal financial officers as required by Rule 30a-2(b) under the Investment Company Act of 1940. (EX-99.906CERT)