UNITED STATES SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

(Mark One)

|

| |

| ☒ | Annual Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

| | For the Fiscal Year Ended August 26, 2017 |

|

| |

| ☐ | Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

| | Commission file number 001-08504

|

UNIFIRST CORPORATION

(Exact Name of Registrant as Specified in Its Charter)

|

| |

| Massachusetts | 04-2103460 |

| (State or Other Jurisdiction of Incorporation or Organization) | (IRS Employer Identification No.) |

68 Jonspin Road

Wilmington, Massachusetts 01887

(Address of Principal Executive Offices)(Zip Code)

Registrant’s telephone number, including area code: (978) 658-8888

Securities registered pursuant to Section 12(b) of the Act:

|

| | |

| Title of Class | | Name of Each Exchange on Which Registered |

| Common Stock, | | New York Stock Exchange |

| $0.10 par value per share | | |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark whether the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes ✔ No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes No ✔

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes ✔ No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes ✔ No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer”, “accelerated filer”, “smaller reporting company” and "emerging growth company" in Rule 12b-2 of the Exchange Act (Check one):

Large accelerated filer ✔ Accelerated filer Smaller Reporting Company Non-accelerated filer

Emerging Growth Company

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes No ✔

The number of outstanding shares of the Registrant’s Common Stock and Class B Common Stock as of October 13, 2017 were 15,460,082 and 4,815,519, respectively. The aggregate market value of the voting stock of the Registrant held by non-affiliates as of February 24, 2017 (the last business day of the Registrant’s most recently completed second fiscal quarter), computed by reference to the closing sale price of such shares on such date, was approximately $1,999,318,504.

Documents Incorporated By Reference

The Registrant intends to file a Definitive Proxy Statement pursuant to Regulation 14A promulgated under the Securities Exchange Act of 1934, as amended, for its 2018 Annual Meeting of Shareholders within 120 days of the end of the fiscal year ended August 26, 2017. Portions of such Proxy Statement are incorporated by reference in Part III of this Annual Report on Form 10-K.

UniFirst Corporation

Annual Report on Form 10-K

For the Fiscal Year Ended August 26, 2017

|

| |

Table of Contents |

| | |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| Ex-21 List of Subsidiaries | |

| Ex-23.1 Consent of Ernst & Young LLP, Independent Registered Public Accounting Firm | |

| Ex-31.1 Section 302 Certification of CEO | |

| Ex-31.2 Section 302 Certification of CFO | |

| Ex-32.1 Section 906 Certification of CEO | |

| Ex-32.2 Section 906 Certification of CFO | |

PART I

This Annual Report on Form 10-K contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. Our actual results could differ materially from those set forth in the forward-looking statements. Certain factors that might cause such a difference are discussed in “Management’s Discussion and Analysis of Financial Condition and Results of Operations”; “Safe Harbor for Forward Looking Statements” and “Risk Factors” included elsewhere in this Annual Report on Form 10-K.

ITEM 1. BUSINESS

GENERAL

UniFirst Corporation, a corporation organized under the laws of the Commonwealth of Massachusetts in 1950, together with its subsidiaries, hereunder referred to as “we”, “our”, the “Company”, or “UniFirst”, is one of the largest providers of workplace uniforms and protective work wear clothing in the United States. We design, manufacture, personalize, rent, clean, deliver, and sell a wide range of uniforms and protective clothing, including shirts, pants, jackets, coveralls, lab coats, smocks, aprons and specialized protective wear, such as flame resistant and high visibility garments. We also rent and sell industrial wiping products, floor mats, facility service products and other non-garment items, and provide restroom and cleaning supplies and first aid cabinet services and other safety supplies, to a variety of manufacturers, retailers and service companies. We serve businesses of all sizes in numerous industry categories. At certain specialized facilities, we also decontaminate and clean work clothes and other items that may have been exposed to radioactive materials and service special cleanroom protective wear and facilities.

Our principal services include providing customers with uniforms and other non-garment items, picking up soiled uniforms or other items on a periodic basis (usually weekly), and delivering, at the same time, cleaned and processed items. We offer uniforms in a wide variety of styles, colors, sizes and fabrics and with personalized emblems selected by the customer. Our centralized services, specialized equipment and economies of scale generally allow us to be more cost effective in providing garment services than customers could be themselves, particularly those customers with high employee turnover rates. During the fiscal year ended August 26, 2017 ("fiscal 2017"), we manufactured approximately 69% of the garments we placed in service. These were primarily work pants and shirts manufactured at three of our plants located in San Luis Potosi, Mexico, one plant located in Managua, Nicaragua, as well as at subcontract manufacturers that we utilize to supplement our manufacturing capacity in periods of high demand. Because we design and manufacture a majority of our own uniforms and protective clothes, we can produce custom garment programs for our larger customers, offer a diverse range of such designs within our standard line of garments and better control the quality, price and speed at which we produce such garments. In addition, among our competitors, we believe we have the largest in-house digital image processing capability, allowing us to convert an image provided by a customer into customized, mass producible embroidered emblems, typically within two days.

We have six operating segments: US Rental and Cleaning, Canadian Rental and Cleaning, Manufacturing (“MFG”), Specialty Garments Rental and Cleaning (“Specialty Garments”), First Aid and Corporate. The US Rental and Cleaning and Canadian Rental and Cleaning operating segments have been combined to form the US and Canadian Rental and Cleaning reporting segment. The US and Canadian Rental and Cleaning reporting segment purchases, rents, cleans, delivers and sells, uniforms and protective clothing and non-garment items in the United States and Canada. The Corporate operating segment consists of costs associated with our distribution center, sales and marketing, information systems, engineering, materials management, manufacturing planning, finance, budgeting, human resources, other general and administrative costs and interest expense. The revenues generated from the Corporate operating segment represent certain direct sales made directly from our distribution center. The products sold by this operating segment are the same products rented and sold by the US and Canadian Rental and Cleaning reporting segments. The MFG operating segment designs and manufactures uniforms and non-garment items primarily for the purpose of providing these goods to the US and Canadian Rental and Cleaning reporting segment. The Specialty Garments operating segment purchases, rents, cleans, delivers and sells, specialty garments and non-garment items primarily for nuclear and cleanroom applications and provides cleanroom cleaning services at limited customer locations. The First Aid operating segment sells first aid cabinet services and other safety supplies as well as maintains wholesale distribution and pill packaging operations. Refer to Note 15, “Segment Reporting”, of our Consolidated Financial Statements for our disclosure of segment information.

In fiscal 2017, we generated $1.591 billion in revenue, of which approximately 91% was derived from the US and Canadian Rental and Cleaning and Corporate segments. Specialty Garments and First Aid accounted for approximately 6% and 3% of our 2017 revenues, respectively.

On May 24, 2017, we announced the passing of Ronald D. Croatti, our Chairman, Chief Executive Officer and President. Mr. Croatti had been our Chief Executive Officer since 1991 and had been with the Company since 1965. Following Mr. Croatti’s death, on July 27, 2017, the Board of Directors (the “Board”) of the Company unanimously approved the appointment of Steven S. Sintros, the Corporation’s Senior Vice President and Chief Financial Officer, as President and Chief Executive Officer of the Company effective as of July 31, 2017. The Board also voted unanimously to elect Mr. Sintros to the Board as a Class II Director to fill the vacancy created by the passing of Mr. Croatti. Mr. Sintros will continue to serve as the Company’s Chief Financial Officer and its principal accounting officer until the Board appoints a new Chief Financial Officer and principal accounting officer.

PRODUCTS AND SERVICES

We provide our customers with personalized workplace uniforms and protective work clothing in a broad range of styles, colors, sizes and fabrics. Our uniform products include shirts, pants, jackets, coveralls, lab coats, smocks, aprons and specialized protective wear, such as flame resistant and high visibility garments. At certain specialized facilities, we also decontaminate and clean clothes and other items which may have been exposed to radioactive materials and service special cleanroom protective wear and facilities. We also offer non-garment items and services, such as industrial wiping products, floor mats, dry and wet mops, restroom and cleaning supplies and other textile products.

We offer our customers a range of garment service options, including full-service rental programs in which garments are cleaned and serviced by us, lease programs in which garments are cleaned and maintained by individual employees and purchase programs to buy garments and related items directly. As part of our rental business, we pick up a customer’s soiled uniforms and/or other items on a periodic basis (usually weekly) and deliver back cleaned and processed replacement items. We believe our centralized services, specialized equipment and economies of scale generally allow us to be more cost effective in providing garment and related services than customers would be themselves, particularly those customers with high employee turnover rates. Our uniform program is intended not only to help our customers foster greater company identity, but to enhance their corporate image and improve employee safety, productivity and morale. We primarily serve our customers pursuant to written service contracts that range in duration from three to five years.

CUSTOMERS

We serve businesses of all sizes in numerous industry categories. During each of the past five years, no single customer in our Core Laundry Operations accounted for more than 1% of our revenues. Our typical customers include automobile service centers and dealers, delivery services, food and general merchandise retailers, food processors and service operations, light manufacturers, maintenance facilities, restaurants, service companies, soft and durable goods wholesalers, transportation companies, and others who require employee clothing for image, identification, protection or utility purposes. Among our largest customers of our conventional uniform rental business are divisions, units, regional operations or franchised agencies of major, nationally recognized organizations. With respect to our Specialty Garment segment, typical customers include government agencies, research and development laboratories, high technology companies and utilities operating nuclear reactors. We currently service over 300,000 customer locations in the United States, Canada and Europe from over 250 customer service, distribution and manufacturing facilities.

MARKETING, SALES, AND CUSTOMER SERVICE

We market our products and services to a diverse customer base and to prospects that range across virtually all industry segments. Marketing contact is made through print advertising, direct mail, publicity, trade shows, catalogs, telemarketing, multiple web sites and direct field sales representation. We have built and maintain an extensive, proprietary database of prescreened and qualified business prospects that have been sourced from our various promotional initiatives, including mailers, web site contacts, advertising responses, sales calls and lists purchased from third-party providers. These prospect records serve as a primary targeting resource for our professional sales organization and are constantly updated, expanded and maintained by an in-house team of specialist database qualifiers and managers. To aid in the effective marketing of products and services, we supply sales representatives with an extensive selection of sales aids, brochures, presentation materials and vertical market communications tools. We also provide representatives with detailed on-line profiles of high opportunity markets to educate them to the typical issues, needs and concerns of those markets. This helps establish credibility and aids their ability to deliver value-based solutions.

We employ a large team of trained professional sales representatives whose sole function is to market our services to potential customers and develop new accounts. While most of our sales representatives are capable of presenting a full range of service solutions, some are dedicated to developing business for a limited range of products and services or have a specific market focus.

For example, in select geographic markets we employ teams of dedicated facility services sales representatives who focus exclusively on developing business for our floor care, restroom and related service programs. We employ specialist executive-level salespeople in our National Account Organization—some who specialize in rental programs and some who specialize in direct sale programs—to target the very largest national companies with known uniform and/or facility services program needs. We believe that effective customer service is the most important element in developing and maintaining our market position. Our commitment to service excellence is reflected throughout our organization. Our route sales representatives are the first line of continuing customer contact, who are supported by local customer service representatives, local service management staff and local operations management leaders, all of whom are focused on addressing the ongoing needs of customers, constantly delivering high-value service and pursuing total customer satisfaction. Our proprietary information systems enable us to respond to customer inquiries or issues within 24 hours, and our service personnel are specially trained to handle the daily contact work necessary to effectively manage customer relations.

We measure the speed and accuracy of our customer service efforts on a weekly basis and, through our “Customers for Life’’ program, we continuously survey, record and report satisfaction levels as a means of evaluating current performance and highlighting areas for improvement.

COMPETITION

The uniform rental and sales industry is highly competitive. The principal methods of competition in the industry are the quality of products, the quality of service and price. Our principal competitors include Cintas Corporation and Aramark Corporation. The remainder of the market, however, is divided among more than 600 smaller businesses, many of which serve one or a limited number of markets or geographic service areas. In addition to our traditional rental competitors, we may increasingly compete in the future with businesses that focus on selling uniforms and other related items. We also compete with industry competitors for acquisitions.

MANUFACTURING AND SOURCING

We manufactured approximately 69% of all garments which we placed in service during fiscal 2017. These garments were primarily work pants and shirts manufactured at three of our plants located in San Luis Potosi, Mexico, one plant located in Managua, Nicaragua, as well as at subcontract manufacturers that we utilize to supplement our manufacturing capacity in periods of high demand. The balance of the garments used in our programs are purchased from a variety of industry suppliers. While we currently acquire the raw materials with which we produce our garments from a limited number of suppliers, we believe that such materials are readily available from other sources. To date, we have experienced no significant difficulty in obtaining any of our raw materials or supplies. Currently, we also manufacture approximately 88% of the mats we place in service at our plant in Cave City, Arkansas.

EMPLOYEES

As of August 26, 2017, we employed approximately 14,000 persons and approximately 1% of our United States employees are represented by a union pursuant to a collective bargaining agreement. We consider our employee relations to be good.

EXECUTIVE OFFICERS

Our executive officers are as follows:

|

| | | | |

| NAME | | AGE | | POSITION |

| Steven S. Sintros | | 44 | | President, Chief Executive Officer and Chief Financial Officer |

| Cynthia Croatti | | 62 | | Executive Vice President and Treasurer |

| David A. DiFillippo | | 60 | | Senior Vice President, Operations |

| David M. Katz | | 54 | | Senior Vice President, Sales and Marketing |

| Michael A. Croatti | | 48 | | Senior Vice President, Operations |

| William M. Ross | | 56 | | Senior Vice President, Operations |

The principal occupation and positions for the past five years of our executive officers named above are as follows:

Steven S. Sintros joined our Company in 2004. Mr. Sintros has served as our President and Chief Executive Officer and a Director since July 2017. He also has served as our Chief Financial Officer since January 2009. He has overall responsibility

for management of the Company including oversight of the financial functions. Mr. Sintros served as a Finance Manager in 2004 and Corporate Controller from 2005 until January 2009.

Cynthia Croatti joined our Company in 1980. Ms. Croatti has served as Director since 1995, Treasurer since 1982 and Executive Vice President since 2001. In addition, she has primary responsibility for overseeing the human resources and purchasing functions of our Company.

David A. DiFillippo joined our Company in 1979. Mr. DiFillippo has served as Senior Vice President, Operations since 2002 and has primary responsibility for overseeing the operations of certain regions in the United States and Canada. From 2000 through 2002, Mr. DiFillippo served as Vice President, Central Rental Group and, prior to 2000, he served as a Regional General Manager.

David M. Katz joined our Company in 2009. Mr. Katz is a Senior Vice President and has primary responsibility for overseeing the sales and marketing functions of our Company. Prior to joining our Company, Mr. Katz worked for DHL Express where he served as the Northeast Vice President of Field Sales, from 2003 to 2007, the Northeast Vice President of National Account Sales from 2007 to 2008 and the Senior Vice President and General Manager of the Northeast from 2008 until 2009.

Michael A. Croatti joined our Company in 1987. Mr. Croatti became Senior Vice President, Operations in 2015 and has primary responsibility for overseeing specified regions in the United States and the Company’s overall service operations. From 2012 through 2015, he served as Senior Vice President, Service; from 2002 through 2012, he served as Vice President, Central Rental Group; and prior to 2002, he held various operating positions within the Company.

William M. Ross joined our Company in 1989. Mr. Ross became Senior Vice President of Operations in 2016 and has primary responsibility for overseeing specified regions in the United States. From 2002 to 2016, Mr. Ross served as Regional Vice President of the Company. Prior to 2002, Mr. Ross held several sales and operations management positions at the Company.

Michael A. Croatti is the nephew of Cynthia Croatti.

ENVIRONMENTAL MATTERS

We, like our competitors, are subject to various federal, state and local laws and regulations governing, among other things, air emissions, wastewater discharges, and the generation, handling, storage, transportation, treatment and disposal of hazardous wastes and other substances. In particular, industrial laundries currently use and must dispose of detergent waste water and other residues, and, in the past, used perchloroethylene and other dry cleaning solvents. We are attentive to the environmental concerns surrounding the disposal of these materials and have through the years taken measures to avoid their improper disposal. Over the years, we have settled, or contributed to the settlement of, actions or claims brought against us relating to the disposal of hazardous materials and there can be no assurance that we will not have to expend material amounts to remediate the consequences of any such disposal in the future. Further, under environmental laws, an owner or lessee of real estate may be liable for the costs of removal or remediation of certain hazardous or toxic substances located on or in or emanating from such property, as well as related costs of investigation and property damage. Such laws often impose liability without regard to whether the owner or lessee knew of or was responsible for the presence of such hazardous or toxic substances. There can be no assurance that acquired or leased locations have been operated in compliance with environmental laws and regulations or that future uses or conditions will not result in the imposition of liability upon us under such laws or expose us to third-party actions such as tort suits. We continue to address environmental conditions under terms of consent orders negotiated with the applicable environmental authorities or otherwise with respect to sites located in, or related to, Woburn, Massachusetts, Somerville, Massachusetts, Springfield, Massachusetts, Uvalde, Texas, Stockton, California, three sites related to former operations in Williamstown, Vermont, as well as sites located in Goldsboro, North Carolina, Wilmington, North Carolina, Landover, Maryland and Syracuse, New York. For additional discussion refer to “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the risk factors set forth in this Annual Report on Form 10-K.

Our nuclear garment decontamination facilities in the United States are licensed by the Nuclear Regulatory Commission, or in certain cases, by the applicable state agency, and are subject to regulation by federal, state and local authorities. We also have nuclear garment decontamination facilities in the United Kingdom and the Netherlands. These facilities are licensed and regulated by the respective country’s applicable federal agency. In the past, scrutiny and regulation of nuclear facilities and related services have resulted in the suspension of operations at certain nuclear facilities served by us or disruptions in our ability to service such facilities. There can be no assurance that such scrutiny and regulation will not lead to the shut-down of such facilities or otherwise cause material disruptions in our garment decontamination business.

AVAILABLE INFORMATION

We make available free of charge our Proxy Statement, Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, including exhibits and any amendments to those reports, as soon as reasonably practicable after we electronically file such material with, or furnish it to, the Securities and Exchange Commission. These reports are available on our website at www.unifirst.com. In addition, you may request a copy of our filings, excluding exhibits, by contacting our Investor Relations group at (978) 658-8888 or at UniFirst Corporation, 68 Jonspin Road, Wilmington, MA 01887. Information included on our website is not deemed to be incorporated into this Annual Report on Form 10-K or the documents incorporated by reference into this Annual Report on Form 10-K.

ITEM 1A. RISK FACTORS

The statements in this section, as well as statements described elsewhere in this Annual Report on Form 10-K, or in other SEC filings, describe risks that could materially and adversely affect our business, financial condition and results of operations and the trading price of our securities. These risks are not the only risks that we face. Our business, financial condition and results of operations could also be materially affected by additional factors that are not presently known to us or that we currently consider to be immaterial to our operations.

SAFE HARBOR FOR FORWARD LOOKING STATEMENTS

This Annual Report on Form 10-K and any documents incorporated by reference may contain forward looking statements within the meaning of the federal securities laws. Forward looking statements contained in this Annual Report on Form 10-K and any documents incorporated by reference are subject to the safe harbor created by the Private Securities Litigation Reform Act of 1995. Forward looking statements may be identified by words such as “estimates,” “anticipates,” “projects,” “plans,” “expects,” “intends,” “believes,” “seeks,” “could,” “should,” “may,” “will,” or the negative versions thereof, and similar expressions and by the context in which they are used. Such forward looking statements are based upon our current expectations and speak only as of the date made. Such statements are highly dependent upon a variety of risks, uncertainties and other important factors that could cause actual results to differ materially from those reflected in such forward looking statements. Such factors include, but are not limited to, the performance and success of our new Chief Executive Officer, uncertainties caused by adverse economic conditions and their impact on our customers’ businesses and workforce levels, uncertainties regarding our ability to consummate and successfully integrate acquired businesses, our ability to maintain and grow Arrow Uniform’s customer base and enhance its operating margins, uncertainties regarding any existing or newly-discovered expenses and liabilities related to environmental compliance and remediation, any adverse outcome of pending or future contingencies or claims, our ability to compete successfully without any significant degradation in our margin rates, seasonal and quarterly fluctuations in business levels, our ability to preserve positive labor relationships and avoid becoming the target of corporate labor unionization campaigns that could disrupt our business, the effect of currency fluctuations on our results of operations and financial condition, our dependence on third parties to supply us with raw materials, any loss of key management or other personnel, increased costs as a result of any future changes in federal or state laws, rules and regulations or governmental interpretation of such laws, rules and regulations, uncertainties regarding the price levels of natural gas, electricity, fuel and labor, the negative effect on our business from sharply depressed oil prices, the continuing increase in domestic healthcare costs, including the ultimate impact of the Affordable Care Act, our ability to retain and grow our customer base, demand and prices for our products and services, fluctuations in our Specialty Garments business, rampant criminal activity and instability in Mexico where our principal garment manufacturing plants are located, our ability to properly and efficiently design, construct, implement and operate a new customer relationship management (“CRM”) computer system, interruptions or failures of our information technology systems, including as a result of cyber-attacks, additional professional and internal costs necessary for compliance with recent and proposed future changes in Securities and Exchange Commission, New York Stock Exchange and accounting rules, strikes and unemployment levels, our efforts to evaluate and potentially reduce internal costs, economic and other developments associated with the war on terrorism and its impact on the economy and general economic conditions. We undertake no obligation to update any forward looking statements to reflect events or circumstances arising after the date on which they are made.

RISKS RELATING TO OUR BUSINESS AND INDUSTRY

We face intense competition within our industry, which may adversely affect our results of operations and financial condition.

The uniform rental and sales industry is highly competitive. The principal methods of competition in the industry are quality of products, quality of service and price. Our leading competitors include Cintas Corporation and Aramark Corporation. The remainder of the market, however, is divided among more than 600 smaller businesses, many of which serve one or a limited

number of markets or geographic service areas. In addition to our traditional rental competitors, we may increasingly compete in the future with businesses that focus on selling uniforms and other related items, including single-use disposable garments for use in the nuclear industry. Increased competition may result in price reductions, reduced gross margins and loss of market share, any of which could have a material effect on our results of operations and financial condition. We also compete with industry competitors for acquisitions, which has the effect of increasing the price for acquisitions and reducing the number of acquisition candidates available to us. If we pay higher prices for businesses we acquire, our returns on investment and profitability may be reduced.

Adverse economic and business conditions or geopolitical events may affect our customer base and negatively impact our sales and operating results.

We supply uniform services to many industries that have been in the past, and may be in the future, subject to adverse economic and business conditions resulting in shifting employment levels, workforce reductions, changes in worker productivity, uncertainty regarding the impacts of rehiring and shifts to offshore manufacturing. In addition, geopolitical conflicts, calamities or other events may disrupt domestic and global business and financial markets and conditions. Any conditions or events that adversely affect our current customers or sales prospects may cause such customers or prospects to restrict expenditures, reduce workforces or even to cease to conduct their businesses. Any of these circumstances would have the effect of reducing the number of employees utilizing our uniform services, which adversely affects our sales and results of operations.

The expenses we incur to comply with environmental regulations, including costs associated with potential environmental remediation, may prove to be significant and could have a material adverse effect on our results of operations and financial condition.

We, like our competitors, are subject to various federal, state and local laws and regulations governing, among other things, air emissions, wastewater discharges, and the generation, handling, storage, transportation, treatment and disposal of hazardous wastes and other substances. In particular, industrial laundries currently use and must dispose of detergent waste water and other residues, and, in the past, used perchloroethylene and other dry cleaning solvents. We are attentive to the environmental concerns surrounding the disposal of these materials and have, through the years, taken measures to avoid their improper disposal. Over the years, we have settled, or contributed to the settlement of, actions or claims brought against us relating to the disposal of hazardous materials and there can be no assurance that we will not have to expend material amounts to remediate the consequences of any such disposal in the future. Further, under environmental laws, an owner or lessee of real estate may be liable for the costs of removal or remediation of certain hazardous or toxic substances located on or in or emanating from such property, as well as related costs of investigation and property damage. Such laws often impose liability without regard to whether the owner or lessee knew of or was responsible for the presence of such hazardous or toxic substances. There can be no assurance that acquired or leased locations have been operated in compliance with environmental laws and regulations or that future uses or conditions will not result in the imposition of liability upon us under such laws or expose us to third-party actions such as tort suits.

We continue to address environmental conditions under terms of consent orders negotiated with the applicable environmental authorities or otherwise with respect to sites located in or related to Woburn, Massachusetts, Somerville, Massachusetts, Springfield, Massachusetts, Uvalde, Texas, Stockton, California, three sites related to former operations in Williamstown, Vermont, as well as sites located in Goldsboro, North Carolina, Wilmington, North Carolina, Landover, Maryland and Syracuse, New York.

We have accrued certain costs related to the sites described above as it has been determined that the costs are probable and can be reasonably estimated. We have potential exposure related to a parcel of land (the “Central Area”) related to the Woburn, Massachusetts site cited above. Currently, the consent decree for the Woburn site does not define or require any remediation work in the Central Area. The United States Environmental Protection Agency (the “EPA”) has provided us and other signatories to the consent decree with comments on the design and implementation of groundwater and soil remedies at the Woburn site and investigation of environmental conditions in the Central Area. We, and other signatories, have implemented and proposed to do additional work at the Woburn site but many of EPA’s comments remain to be resolved. We have implemented mitigation measures and continue to monitor environmental conditions at the Somerville, Massachusetts site. We also have received demands from the local transit authority for reimbursement of certain costs associated with its construction of a new municipal transit station in the area of our Somerville site. This station is part of a planned extension of the transit system. Due to cost projections of the extension which substantially exceeded original estimates, the local transit authority had placed the extension on hold pending its redesign and receipt of related state and federal approvals and funding increases. It is now proceeding with the bidding process. We have reserved for costs in connection with this matter; however, in light of the uncertainties associated with this matter, these costs and the related reserve may change. We have also received notice that the

Massachusetts Department of Environmental Protection is conducting an audit of the Company’s investigation and remediation work with respect to the Somerville site.

On a quarterly basis, we assess each of our environmental sites to determine whether the costs of investigation and remediation of environmental conditions are probable and can be reasonably estimated as well as the adequacy of our accruals with respect to such costs. There can be no assurance that our accruals with respect to our environmental sites will be sufficient or that the costs of remediation and investigation will not substantially exceed our accruals as new facts, circumstances or estimates arise.

Our nuclear garment decontamination facilities are licensed by the Nuclear Regulatory Commission, or in certain cases, by the applicable state agency, and are subject to regulation by federal, state and local authorities. We also have nuclear garment decontamination facilities in the United Kingdom and the Netherlands. These facilities are licensed and regulated by the respective country’s applicable federal agency. In the past, scrutiny and regulation of nuclear facilities and related services have resulted in the suspension of operations at certain nuclear facilities served by us or disruptions in our ability to service such facilities. There can be no assurance that such scrutiny and regulation will not lead to the shut-down of such facilities or otherwise cause material disruptions in our garment decontamination business.

In addition, our nuclear garment decontamination operations are subject to asset retirement obligations related to the decommissioning of our nuclear laundry facilities. We recognize as a liability the present value of the estimated future costs to decommission these facilities. The estimated liability is based on historical experience in decommissioning nuclear laundry facilities, estimated useful lives of the underlying assets, external vendor estimates as to the cost to decommission these assets in the future, and federal and state regulatory requirements. No assurances can be given that these accruals will be sufficient or that the costs of such decommissioning will not substantially exceed such accruals, as our facts, circumstances or estimates change, including changes in the Company’s estimated useful lives of the underlying assets, estimated dates of decommissioning, changes in decommissioning costs, changes in federal or state regulatory guidance on the decommissioning of such facilities, or other changes in estimates.

In addition to contingencies and claims relating to environmental compliance matters, we may from time to time be subject to legal proceedings and claims related to our business operations which may adversely affect our financial condition and operating results.

In addition to contingencies and claims relating to environmental compliance matters, we are subject from time to time to legal proceedings and claims arising from the conduct of our business operations, including personal injury claims, customer contract matters and employment claims. Certain of these claims are typically not covered by our available insurance. In addition, claims occasionally result in significant investigation and litigation expenses and, if successful, may result in material losses to us. Certain claims may also result in significant adverse publicity against us. As a consequence, successful claims against us not covered by our available insurance coverage, or the impact of adverse publicity against us, could have a material adverse effect on our business, financial condition and results of operation.

Our failure to implement successfully our acquisition strategy and to grow our business could adversely affect our ability to increase our revenues and could negatively impact our profitability.

As part of our growth strategy, we intend to continue to actively pursue additional acquisition opportunities. However, as discussed above, we compete with others within our industry for suitable acquisition candidates. This competition may increase the price for acquisitions and reduce the number of acquisition candidates available to us. Moreover, the current economic weakness has resulted in, and may continue to result in, the sale of fewer target businesses at prices consistent with the current market weakness. As a result, acquisition candidates may not be available to us in the future on favorable terms. Even if we are able to acquire businesses on favorable terms, managing growth through acquisition is a difficult process that includes integration and training of personnel, combining plant and operating procedures and additional matters related to the integration of acquired businesses within our existing organization. Unanticipated issues related to integration may result in additional expense or in disruption to our operations, either of which could negatively impact our ability to achieve anticipated benefits. While we believe we will be able to fully integrate acquired businesses, we can give no assurance that we will be successful in this regard.

Growth of our business will likely require us to increase our work force, the scope of our operating and financial systems and the geographic area of our operations. We believe this growth will increase our operating complexity and the level of responsibility for both existing and new management personnel. Managing and sustaining our growth and expansion may require substantial enhancements to our operational and financial systems and controls, as well as additional administrative, operational and financial resources. There can be no assurance that we will be able to manage our expanding operations

successfully or that we will be able to maintain or accelerate our growth, and any failure to do so could have an adverse effect on our results of operations and financial condition.

In order to finance such acquisitions, we may need to obtain additional funds either through public or private financings, including bank and other secured and unsecured borrowings and the issuance of debt or equity securities. There can be no assurance that such financings would be available to us on reasonable terms or that any future issuances of securities in connection with acquisitions will not be dilutive to our shareholders.

On September 19, 2016, we completed an acquisition of Arrow Uniform (“Arrow”) for approximately $118.7 million. The all-cash transaction was structured as an asset acquisition, with our Company acquiring substantially all of Arrow’s assets and a limited amount of liabilities. Arrow, headquartered in Taylor, Michigan, provided uniform and facility service rental programs as well as direct sales uniform programs to a wide range of large and small customers. Arrow operated from 12 locations with nearly 700 employees in five Midwestern states.

If we are unable to preserve positive labor relationships or become the target of corporate labor unionization campaigns, the resulting labor unrest could disrupt our business by impairing our ability to produce and deliver our products.

As of August 26, 2017, we employ approximately 14,000 persons and approximately 1% of our United States employees are represented by a union pursuant to a collective bargaining agreement. Competitors within our industry have been the target of corporate unionization campaigns by multiple labor unions. While our management believes that our employee relations are good, we cannot assure you that we will not experience pressure from labor unions or become the target of campaigns similar to those faced by our competitors. The potential for unionization could increase if the United States Congress passes federal “card check” legislation. If we do encounter pressure from labor unions, any resulting labor unrest could disrupt our business by impairing our ability to produce and deliver our products. In addition, significant union representation would require us to negotiate wages, salaries, benefits and other terms with many of our employees collectively and could adversely affect our results of operations by increasing our labor costs or otherwise restricting our ability to maximize the efficiency of our operations.

We may incur unexpected cost increases due to rising healthcare costs, the Affordable Care Act and other labor costs.

The cost of healthcare that we provide to our employees has grown over the last few years at a rate in excess of our revenue growth and, as a result, has negatively impacted our operating results. In the fiscal year ended August 29, 2015 ("fiscal 2015"), the Affordable Care Act (“ACA”) required us to modify one of the healthcare plans we provided to our employees. Moreover, it is generally expected that healthcare costs in the United States will increase over the coming years at rates in excess of inflation. As a result of these factors, and depending on the effect of the modifications we have made, and may make in the future, to our employee healthcare plans and enrollment levels in those plans, we expect that our future operating results will continue to be further adversely impacted by increasing healthcare costs.

Federal, state and municipal governments are mandating increases to minimum wage and other employee benefits. In addition, we face wage pressure as the result of a low unemployment environment. We have raised, and expect to continue to raise, our wage rates and benefits to reflect these changes, which has the effect of increasing our labor costs, which in turn adversely affects our results of operation and financial condition. Our failure to comply with these regulatory requirements would expose us to applicable penalties and increase the likelihood that we would be subject to unionization campaigns. Further mandates would require additional increases to our labor costs and adversely affect our operating margin.

Our failure to retain our current customers and renew our existing customer contracts could adversely affect our results of operations and financial condition.

Our success depends on our ability to retain our current customers and renew our existing customer contracts. Our ability to do so generally depends on a variety of factors, including the quality, price and responsiveness of our services, as well as our ability to market these services effectively and to differentiate ourselves from our competitors. In addition, renewal rates are generally adversely affected by the difficult economic and business conditions. We cannot assure you that we will be able to renew existing customer contracts at the same or higher rates or that our current customers will not turn to competitors, cease operations, elect to self-operate or terminate contracts with us. The failure to renew a significant number of our existing contracts would have an adverse effect on our results of operations and financial condition.

Increases in fuel and energy costs could adversely affect our operating costs.

The price of fuel and energy needed to run our vehicles and equipment is unpredictable and fluctuates based on events outside our control, including geopolitical developments, supply and demand for oil and gas, actions by OPEC and other oil and gas producers, war and unrest in oil producing countries, regional production patterns, limits on refining capacities, natural disasters and environmental concerns. Any increase in fuel and energy costs could adversely affect our operating costs.

As a result of our significant presence in energy producing regions, the prolonged drop in energy prices has and may continue to negatively impact our financial results.

We have a substantial number of plants and conduct a significant portion of our business in energy producing regions in the US and Canada. The price of oil declined dramatically in year ended August 30, 2014 and has remained relatively low since then. This decline has directly affected our customers in the oil industry, as they have curtailed their level of operations, and has had a corresponding effect on our customers in businesses which service or supply the oil industry as well as our customers in unrelated businesses located in areas which had benefited from the economic expansion generated by the robust growth driven by the higher oil prices in prior years. As a result, our fiscal 2017 organic growth was negatively impacted by elevated headcount reductions in our wearer base, increased lost accounts and a reduction in new sales. Further declines in oil prices may exacerbate these effects.

Fluctuations in the nuclear portion of our Specialty Garments segment could disproportionately impact our revenue and net income and create volatility in the price of our Common Stock.

Our nuclear decontamination business is affected by shut-downs, outages and clean-ups of the nuclear facilities we service. We are not able to control or predict with certainty when such shut-downs, outages and clean-ups will occur. In addition, our nuclear decontamination business tends to generate more revenue in the first and third fiscal quarters, which is when nuclear power plants typically schedule their plant outages and refuelings and thereby increase nuclear garment utilization. Moreover, a significant percentage of this segment’s revenues are generated from a limited number of nuclear power plant operators. This concentration subjects this business to significant risks and may result in greater volatility in this segment’s results of operations. Fluctuations in our nuclear decontamination business could adversely affect our results of operations and financial condition.

Our international business results are influenced by currency fluctuations and other risks that could have an adverse effect on our results of operations and financial condition.

A portion of our sales is derived from international markets. Revenue denominated in currencies other than the U.S. dollar represented approximately 7.4%, 7.9% and 8.4% of total consolidated revenues for fiscal 2017, fiscal year ended August 27, 2016 ("fiscal 2016") and fiscal 2015, respectively. The operating results of our international subsidiaries are translated into U.S. dollars and such results are affected by movements in foreign currencies relative to the U.S. dollar. The strength of the U.S. dollar has generally increased recently as compared to other currencies, which has had, and may continue to have, an adverse effect on our operating results as reported in U.S. dollars. In addition, a weaker Canadian dollar increases the costs to our Canadian operations of merchandise and other operational inputs that are sourced from outside Canada, which has the effect of reducing the operating margins of our Canadian business if we are unable to recover these additional costs through price adjustments with our Canadian customers. Our international operations are also subject to other risks, including the requirement to comply with changing and conflicting national and local regulatory requirements; potential difficulties in staffing and labor disputes; managing and obtaining support and distribution for local operations; credit risk or financial condition of local customers; potential imposition of restrictions on investments; potentially adverse tax consequences, including imposition or increase of withholding and other taxes on remittances and other payments by subsidiaries; foreign exchange controls; and local political and social conditions. There can be no assurance that the foregoing factors will not have an adverse effect on our international operations or on our consolidated financial condition and results of operations. We own and operate manufacturing facilities in Mexico. Violence, crime and instability in Mexico has had, and may continue to have, an adverse effect on our operations, including the hijacking of our trucks and the implementation of security measures to protect our employees. We are not insured against such criminal attacks and there can be no assurance that losses that could result from an attack on our trucks or our personnel would not have a material adverse effect on our business, results of operations and financial condition. Operations in developing nations present several additional risks, including greater fluctuation in currencies relative to the U.S. dollar, economic and governmental instability, civil disturbances, volatility in gross domestic production, Foreign Corrupt Practice Act compliance issues and nationalization and expropriation of private assets.

Adverse global financial and economic conditions may result in impairment of our goodwill and intangibles.

Our market capitalization, from time to time, has experienced volatility due in part to turbulent economic conditions and disruption in the global equity and credit markets. Under accounting principles generally accepted in the United States (“US GAAP”), we may be required to record an impairment charge if changes in circumstances or events indicate that the carrying values of our goodwill and intangible assets exceed their fair value and are not recoverable. Any significant and other-than-temporary decrease in our market capitalization could be an indicator, when considered together with other factors, that the carrying values of our goodwill and intangible assets exceed their fair value, which may result in our recording an impairment charge. We are unable to predict economic trends, but we continue to monitor the impact of changes in economic and financial conditions on our operations and on the carrying value of our goodwill and intangible assets. Should the value of our acquired goodwill or one or more of our acquired intangibles become impaired, our consolidated earnings and net worth may be materially adversely affected.

Our failure to properly and efficiently design, construct, implement and operate a new customer relationship management computer system could materially disrupt our operations, adversely impact the servicing of our customers and have a material adverse effect on our financial performance.

We have been working on a CRM systems project ("Unity 20/20) to modernize and improve the CRM system's current capabilities. The new system was intended to combine enterprise resource planning (“ERP”) solutions and custom-built applications to address, among other areas, account management, billing and customer service. The new system was also intended to improve functionality and information flow and increase automation in servicing our customers. Through August 26, 2017, we capitalized $59.9 million related to Unity 20/20. We have been working with a well-regarded third-party contractor to develop the custom-built applications and interfaces. This project experienced repeated delays due primarily to significant quality issues with the stability and performance of the underlying code. Based on the Company’s analysis of the project together with input from outside consultants, including the lead third-party contractor, the Company determined that as of August 26, 2017 it is not probable that the current version of the CRM system that was being developed will be completed and placed into service. As a result, we recognized a non-cash impairment charge of $55.8 million in the fourth quarter of fiscal 2017, the after-tax impact of which was $34.1 million. The remaining $4.1 million of capitalized costs relate primarily to software licenses that have alternative future uses in our business.

Overall, we continue to evaluate our options to determine our best path moving forward. The failure to properly, efficiently and economically complete and operate a new system on a timely basis or at all could materially disrupt our operations, adversely impact the servicing of our customers and have a material adverse effect on our financial results.

If our information technology systems suffer interruptions or failures, including as a result of cyber-attacks, our business operations could be disrupted.

Our information technology systems serve an important role in the efficient operation of our business. The failure of these information technology systems to perform as we anticipate could disrupt our business and negatively impact our results of operations. In addition, our information technology systems could be damaged or cease to function properly due to any number of causes, such as catastrophic events, power outages, security breaches, computer viruses or cyber-based attacks. While we have contingency plans in place to prevent or mitigate the impact of these events, if such events were to occur and our disaster recovery plans do not effectively address the issues on a timely basis, we could suffer interruptions in our ability to manage our operations and service our customers, and we may be required to make a significant investment to fix or replace our information technology systems, each of which may have a material adverse effect on our business and financial results. In addition, if customer or our proprietary information is compromised by a security breach or cyber-attack, it could have a material adverse effect on our business.

Failure to comply with the other state and federal regulations to which we are subject may result in penalties or costs that could have a material adverse effect on our business.

Our business is subject to various other state and federal regulations, including employment laws and regulations, minimum wage requirements, overtime requirements, working condition requirements, citizenship requirements, healthcare insurance mandates and other laws and regulations. Any appreciable increase in the statutory minimum wage rate, income or overtime pay, costs of complying with healthcare insurance mandates, changes in OSHA requirements, changes in environmental compliance requirements, or changes to immigration laws and citizenship requirements would likely result in an increase in our labor costs and/or contribute to a shortage of available labor and such cost increase or labor shortage, or the penalties for failing to comply with such statutory minimums or regulations, could have an adverse effect on our business, liquidity and results of operations.

Our business may be subject to seasonal and quarterly fluctuations.

Historically, our revenues and operating results have varied from quarter to quarter and are expected to continue to fluctuate in the future. In addition, our operating results historically have been seasonally lower during the second and fourth fiscal quarters than during the other quarters of the fiscal year. We incur various costs in integrating or establishing newly acquired businesses or start-up operations, and the profitability of a new location is generally expected to be lower in the initial period of its operation than in subsequent periods. Start-up operations in particular lack the support of an existing customer base and require a significantly longer period to develop sales opportunities and meet targeted operating results.

These factors, among others, may cause our results of operations in some future quarters to be below the expectations of securities analysts and investors, which could have an adverse effect on the market price of our Common Stock.

Loss of our key management or other personnel, including the recent passing of our Chairman, Chief Executive Officer and President, could adversely impact our business.

Our success is largely dependent on the skills, experience and efforts of our senior management and certain other key personnel. If, for any reason, one or more senior executives or key personnel were not to remain active in our Company, our results of operations could be adversely affected. On May 24, 2017, we announced the passing of Ronald D. Croatti, our Chairman, Chief Executive Officer and President. Mr. Croatti had been our Chief Executive Officer since 1991 and had been with the Company since 1965. Following Mr. Croatti’s death, on July 27, 2017, the Board of the Company unanimously approved the appointment of Steven S. Sintros, the Corporation’s Senior Vice President and Chief Financial Officer, as President and Chief Executive Officer of the Company effective as of July 31, 2017. The Board also voted unanimously to elect Mr. Sintros to the Board as a Class II Director to fill the vacancy created by the passing of Mr. Croatti. Mr. Sintros will continue to serve as the Company’s Chief Financial Officer and its principal accounting officer until the Board appoints a new Chief Financial Officer and principal accounting officer.

Our future success also depends upon our ability to attract and retain key employees. There is competition in the market for the services of such qualified personnel and hourly workers and our failure to attract and retain such personnel or workers could adversely affect our results of operations.

We depend on third parties to supply us with raw materials and our results of operations could be adversely affected if we are unable to obtain adequate raw materials in a timely manner.

We manufactured approximately 69% of all garments which we placed in service during fiscal 2017. These were primarily work pants and shirts manufactured at three of our plants located in San Luis Potosi, Mexico, one plant located in Managua, Nicaragua, as well as at subcontract manufacturers that we utilize to supplement our manufacturing capacity in periods of high demand. The balance of the garments used in our programs are purchased from a variety of industry suppliers. While we currently acquire the raw materials with which we produce our garments from a limited number of suppliers, we believe that such materials are readily available from other sources. To date, we have experienced no significant difficulty in obtaining any of our raw materials or supplies. However, if we were to experience difficulty obtaining any of our raw materials from such suppliers and were unable to obtain new materials or supplies from other industry suppliers, it could adversely affect our results of operations.

Unexpected events could disrupt our operations and adversely affect our operating results.

Unexpected events, including, without limitation, fires at facilities, natural disasters, such as hurricanes and tornados, public health emergencies, war or terrorist activities, unplanned utility outages, supply disruptions, failure of equipment or information systems, temporary or long-term disruption of our computer systems, or changes in laws and/or regulations impacting our business, could adversely affect our operating results. These events could result in disruption of customer service, physical damage to one or more key operating facilities, the temporary closure of one or more key operating facilities or the temporary disruption of information systems. In addition, the destruction or temporary loss of our distribution facility in Owensboro, Kentucky would have a material adverse effect on our operations and financial results.

Changes in or new interpretations of the governmental regulatory framework may affect our contract terms and may reduce our sales or profits.

A portion of our total consolidated revenues is derived from business with U.S. federal, state and local governments and agencies. Changes or new interpretations in, or changes in the enforcement of, the statutory or regulatory framework applicable to services provided under governmental contracts or bidding procedures could result in fewer new contracts or contract

renewals, modifications to the methods we apply to price government contracts or in contract terms of shorter duration than we have historically experienced, any of which could result in lower sales or profits than we have historically achieved, which could have an adverse effect on our results of operations.

The price of our Common Stock may be highly volatile, which could result in significant price declines.

The price of our Common Stock may experience significant volatility. Such volatility may be caused by fluctuations in our operating results, changes in earnings estimated by investment analysts, the number of shares of our Common Stock traded each day, the degree of success we achieve in implementing our business and growth strategies, changes in business or regulatory conditions affecting us, our customers or our competitors and other factors. In addition, the New York Stock Exchange historically has experienced extreme price and volume fluctuations that often have been unrelated to, or disproportionate to, the operating performance of its listed companies. These fluctuations, as well as general economic, political and market conditions, may adversely affect the market price of our Common Stock.

We are controlled by our principal shareholders, and our other shareholders may be unable to affect the outcome of shareholder voting.

As of October 13, 2017, to the Company’s knowledge, the members of the Croatti family owned, directly or indirectly, in the aggregate approximately 293,092 shares of our Common Stock and approximately 4,815,519 shares of our Class B Common Stock, which represents approximately 25.2% of the aggregate number of outstanding shares of our Common Stock and Class B Common Stock, but approximately 76.2% of the combined voting power of the outstanding shares of our Common Stock and Class B Common Stock. As a result, the members of the Croatti family, acting with other family members, could effectively control most matters requiring approval by our shareholders, including the election of a majority of the directors. While historically the members of the Croatti family have individually voted their respective shares of Class B Common Stock in the same manner, there is no contractual understanding requiring this and there is no assurance that the family members will continue to individually vote their shares of Class B Common Stock in the same manner. This voting control by the members of the Croatti family, together with certain provisions of our by-laws and articles of organization, could have the effect of delaying, deferring or preventing a change in control of our Company that would otherwise be beneficial to our public shareholders.

Our business could be adversely impacted if we have deficiencies in our disclosure controls and procedures or internal controls over financial reporting.

The design and effectiveness of our disclosure controls and procedures and internal controls over financial reporting may not prevent all errors, misstatements or misrepresentations. While management will continue to review the effectiveness of our disclosure controls and procedures and internal controls over financial reporting, there can be no guarantee that our internal controls over financial reporting will be effective in accomplishing all control objectives all of the time. Deficiencies, including any material weakness, in our internal controls over financial reporting which may occur in the future could result in misstatements of our results of operations, restatements of our financial statements, a decline in our stock price, or otherwise materially adversely affect our business, reputation, results of operations, financial condition or liquidity.

ITEM 1B. UNRESOLVED STAFF COMMENTS

None.

ITEM 2. PROPERTIES

As of August 26, 2017, we owned or leased approximately 258 facilities containing an aggregate of approximately 7.4 million square feet located in the United States, Canada, Mexico, Europe and Nicaragua. We owned 127 of these facilities, containing approximately 5.5 million square feet. These facilities include our 325,000 square foot Owensboro, Kentucky distribution center and almost all of our industrial laundry processing plants. We believe our industrial laundry facilities are among the most modern in the industry.

We own substantially all of the machinery and equipment used in our operations. We believe that our facilities and our production, cleaning and decontamination equipment have been well maintained and are adequate for our present needs. We also own a fleet of approximately 3,600 delivery vans, trucks and other vehicles.

ITEM 3. LEGAL PROCEEDINGS

From time to time, we are subject to legal proceedings and claims arising from the current conduct of our business operations, including personal injury, customer contract, employment claims and environmental matters as described in our Consolidated Financial Statements. We maintain insurance coverage providing indemnification against many of such claims, and we do not expect that we will sustain any material loss as a result thereof.

In addition, we, like our competitors, are subject to various federal, state and local laws and regulations governing, among other things, air emissions, wastewater discharges, and the generation, handling, storage, transportation, treatment and disposal of hazardous wastes and other substances. In particular, industrial laundries currently use and must dispose of detergent waste water and other residues, and, in the past, used perchloroethylene and other dry cleaning solvents. Over the years, we have settled, or contributed to the settlement of, actions or claims brought against us relating to the disposal of hazardous materials and there can be no assurance that we will not have to expend material amounts to remediate the consequences of any such disposal in the future. Further, under environmental laws, an owner or lessee of real estate may be liable for the costs of removal or remediation of certain hazardous or toxic substances located on or in or emanating from such property, as well as related costs of investigation and property damage. Such laws often impose liability without regard to whether the owner or lessee knew of or was responsible for the presence of such hazardous or toxic substances. There can be no assurance that acquired or leased locations have been operated in compliance with environmental laws and regulations or that future uses or conditions will not result in the imposition of liability upon us under such laws or expose us to third-party actions such as tort suits. Refer to Note 11, “Commitments and Contingencies”, of our Consolidated Financial Statements for further discussion.

ITEM 4. MINE SAFETY DISCLOSURES

Not Applicable.

PART II

ITEM 5. MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

COMMON STOCK INFORMATION

Our Common Stock trades on the New York Stock Exchange under the symbol “UNF”, while our Class B Common Stock is not publicly traded. The following table sets forth, for the periods indicated, the high and low closing prices of our Common Stock on the New York Stock Exchange, and the dividends per share paid on our Common Stock and Class B Common Stock.

|

| | | | | | | | | | | | | | | |

| | Price Per Share | | Dividends Per Share |

| | High | | Low | | Common Stock | | Class B Common Stock |

| Year ended August 26, 2017 | | | | | | | |

| First Quarter | $ | 141.80 |

| | $ | 117.75 |

| | $ | 0.0375 |

| | $ | 0.0300 |

|

| Second Quarter | 146.95 |

| | 125.80 |

| | 0.0375 |

| | 0.0300 |

|

| Third Quarter | 142.30 |

| | 130.60 |

| | 0.0375 |

| | 0.0300 |

|

| Fourth Quarter | 144.80 |

| | 136.75 |

| | 0.0375 |

| | 0.0300 |

|

|

| | | | | | | | | | | | | | | |

| | Price Per Share | | Dividends Per Share |

| | High | | Low | | Common Stock | | Class B Common Stock |

| Year ended August 27, 2016 | | | | | | | |

| First Quarter | $ | 112.22 |

| | $ | 103.78 |

| | $ | 0.0375 |

| | $ | 0.0300 |

|

| Second Quarter | 110.55 |

| | 97.97 |

| | 0.0375 |

| | 0.0300 |

|

| Third Quarter | 115.85 |

| | 104.61 |

| | 0.0375 |

| | 0.0300 |

|

| Fourth Quarter | 128.07 |

| | 105.44 |

| | 0.0375 |

| | 0.0300 |

|

The approximate number of shareholders of record of our Common Stock and Class B Common Stock as of October 13, 2017 was 48 and 37, respectively. We believe that the number of beneficial owners of our Common Stock is substantially greater than the number of record holders because a large portion of our Common Stock is held of record in broker “street names”.

We have paid regular quarterly dividends since 1983 and intend to continue such policy subject to, among other factors, our earnings, financial condition, capital requirements and tax law changes. No dividends will be payable unless declared by our Board of Directors and then only to the extent funds are legally available for the payment of such dividends. In the event that our Board of Directors votes to pay a dividend, our Common Stock must receive a dividend equal to no less than 125% of any dividend paid on the Class B Common Stock. On July 7, 2017, our Board of Directors declared a quarterly dividend of $0.0375 and $0.0300 per share on our Common Stock and Class B Common Stock, respectively, which was paid on September 29, 2017 to shareholders of record on September 8, 2017.

The following table sets forth information concerning our equity compensation plans as of August 26, 2017.

|

| | | | | | | | | |

| | Equity Compensation Plan Information |

| Plan category | Number of securities to be issued upon exercise of outstanding options and stock appreciation rights | | Weighted average exercise price of outstanding options and stock appreciation rights | | Number of securities remaining available for future issuance under equity compensation plans (excluding securities referenced in column (a)) |

| | (a) | | (b) | | (c) |

| Equity compensation plans approved by security holders | 600,606 |

| | $ | 94.98 |

| | 694,870 |

|

| Equity compensation plans not approved by security holders | — |

| | N/A |

| | — |

|

| Total | 600,606 |

| | $ | 94.98 |

| | 694,870 |

|

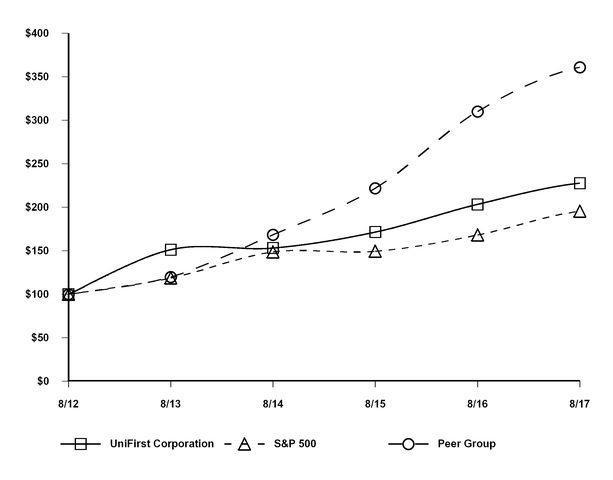

Stock Performance Graph

Set forth below is a line graph comparing the yearly percentage change in the cumulative total shareholder return on our Common Stock, based on the market price of our Common Stock, with the cumulative total shareholder return of a peer group and of companies within the Standard & Poor’s 500 Stock Index, in each case assuming reinvestment of dividends. The calculation of cumulative total shareholder return assumes a $100 investment in our Common Stock, the peer group and the S&P 500 Stock Index on August 31, 2012. The peer group is composed of Cintas Corporation.

COMPARISON OF 5 YEAR CUMULATIVE TOTAL RETURN*

Among UniFirst Corporation, the S&P 500 Index,

and a Peer Group

*$100 invested on 8/31/12 in stock or index, including reinvestment of dividends.

Fiscal year ending August 31.

Copyright© 2017 S&P, a division of McGraw Hill Financial. All rights reserved.

ITEM 6. SELECTED FINANCIAL DATA

The following selected consolidated financial data should be read in conjunction with our Consolidated Financial Statements and Notes to Consolidated Financial Statements included in Item 8.

The selected consolidated balance sheet data set forth below as of August 26, 2017 and August 27, 2016 and the selected consolidated income statement data for each of the three years in the period ended August 26, 2017 are derived from our audited Consolidated Financial Statements included in this Annual Report on Form 10-K. All other selected consolidated financial data set forth below are derived from our audited financial statements not included in this Annual Report on Form 10-K. Current accounting guidance requires the income per share for each class of common stock to be calculated assuming 100% of our earnings are distributed as dividends to each class of common stock based on their respective dividend rights. Our Common Stock has a 25% dividend preference to our Class B Common Stock. The Class B Common Stock, which has ten votes per share as opposed to one vote per share for the Common Stock, is not freely transferable but may be converted at any time on a one-for-one basis into Common Stock at the option of the holder of the Class B Common Stock.

Five Year Financial Summary

UniFirst Corporation and Subsidiaries

|

| | | | | | | | | | | | | | | | | | | |

Fiscal Year Ended August (In thousands, except per share data) | 2017(1) | | 2016(2) | | 2015 | | 2014 | | 2013 |

| Selected Balance Sheet Data: | | | | | | | | | |

| Total assets | $ | 1,819,128 |

| | $ | 1,702,007 |

| | $ | 1,533,237 |

| | $ | 1,424,161 |

| | $ | 1,374,862 |

|

| Notes payable and long-term debt | $ | — |

| | $ | — |

| | $ | 1,385 |

| | $ | 7,859 |

| | $ | 111,408 |

|

| Shareholders' equity | $ | 1,453,192 |

| | $ | 1,364,781 |

| | $ | 1,242,208 |

| | $ | 1,134,459 |

| | $ | 1,013,398 |

|

| | | | | | | | | | |

| Selected Income Statement Data: | | | | | | | | | |

| Revenues | $ | 1,590,958 |

| | $ | 1,468,046 |

| | $ | 1,456,605 |

| | $ | 1,394,897 |

| | $ | 1,355,515 |

|

| Depreciation and amortization | $ | 88,879 |

| | $ | 81,612 |

| | $ | 77,113 |

| | $ | 71,752 |

| | $ | 69,607 |

|

| Income from operations | $ | 110,283 |