Exhibit 1

| ASX Release 6 November 2023 Westpac 2023 Presentation and Investor Discussion Pack Westpac Banking Corporation (“Westpac”) today provides the attached Westpac 2023 Presentation and Investor Discussion Pack. For further information: Hayden Cooper Justin McCarthy Group Head of Media Relations General Manager, Investor Relations 0402 393 619 0422 800 321 This document has been authorised for release by Tim Hartin, Company Secretary. Level 18, 275 Kent Street Sydney, NSW, 2000 |

|

| WESTPAC 2023 FULL YEAR RESULTS INDEX 2023 Full Year Results Presentation 3 Investor Discussion Pack of 2023 Full Year Results 33 Earnings drivers 36 Credit quality and provisions 48 Non-credit risk management 69 Capital, Funding and Liquidity 76 Customer franchise 88 Sustainability 95 Segment results 106 Economics 115 Appendix 119 Contact us 133 Disclaimer 134 |

| PETER KING Chief Executive Officer |

| 4 Westpac Group 2023 Full Year Results Presentation & Investor Discussion Pack FY23 HIGHLIGHTS IMPROVED FINANCIAL RESULT BALANCE SHEET MOMENTUM ACCELERATING TECHNOLOGY SIMPLIFICATION STRENGTHENED CUSTOMER FRANCHISE COMPLETED PORTFOLIO SIMPLIFICATION |

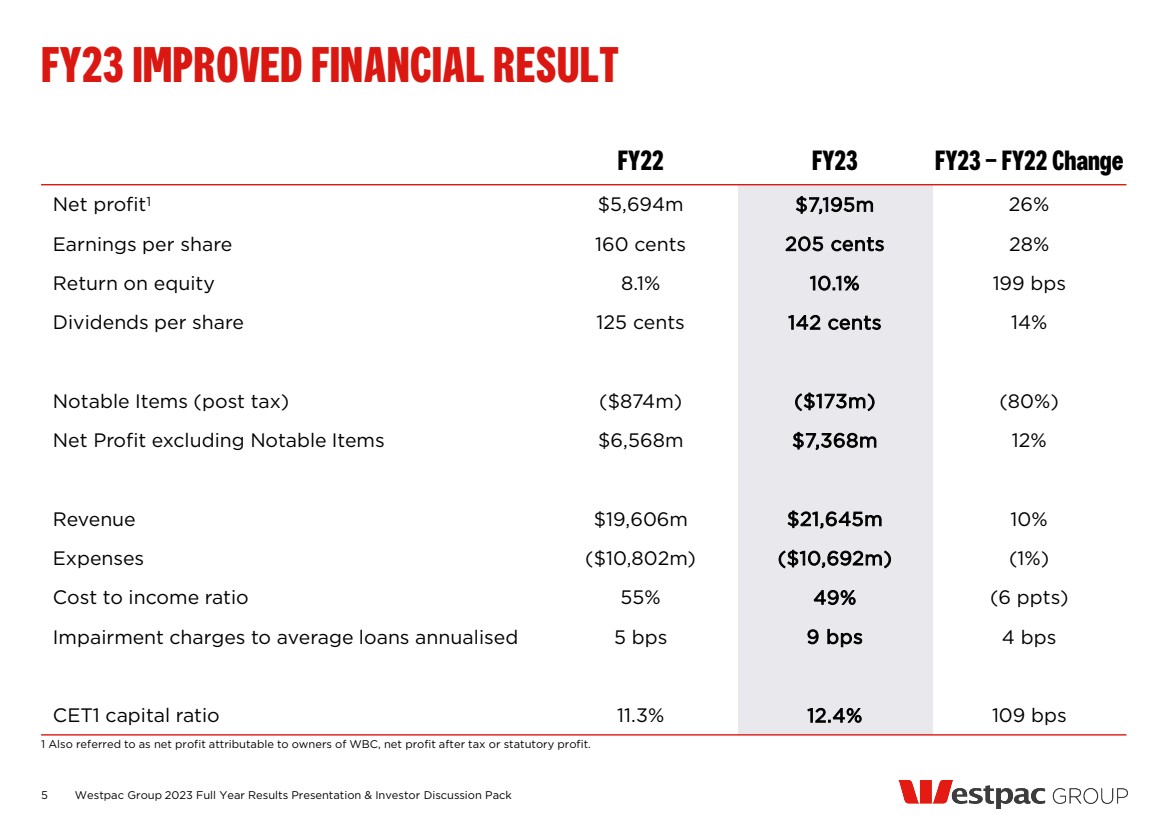

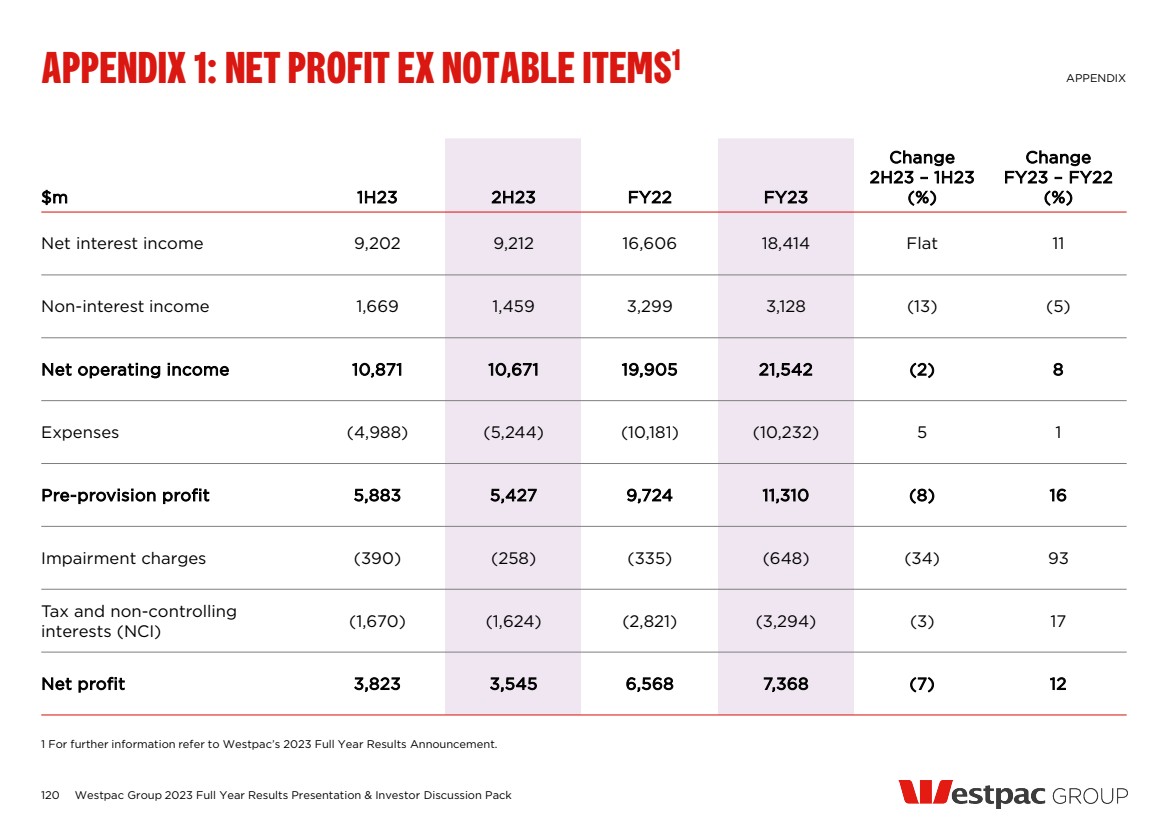

| FY22 FY23 FY23 – FY22 Change Net profit1 $5,694m $7,195m 26% Earnings per share 160 cents 205 cents 28% Return on equity 8.1% 10.1% 199 bps Dividends per share 125 cents 142 cents 14% Notable Items (post tax) ($874m) ($173m) (80%) Net Profit excluding Notable Items $6,568m $7,368m 12% Revenue $19,606m $21,645m 10% Expenses ($10,802m) ($10,692m) (1%) Cost to income ratio 55% 49% (6 ppts) Impairment charges to average loans annualised 5 bps 9 bps 4 bps CET1 capital ratio 11.3% 12.4% 109 bps FY23 IMPROVED FINANCIAL RESULT 1 Also referred to as net profit attributable to owners of WBC, net profit after tax or statutory profit. 5 Westpac Group 2023 Full Year Results Presentation & Investor Discussion Pack |

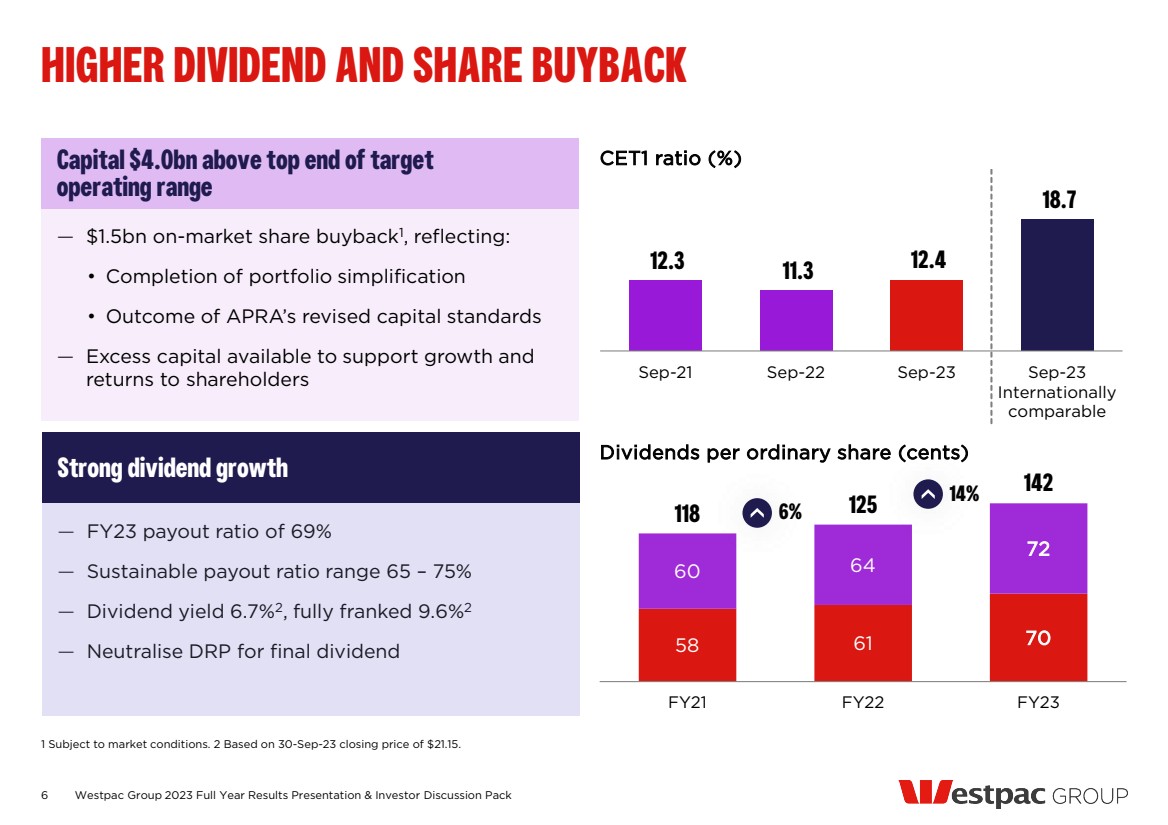

| — $1.5bn on-market share buyback1 , reflecting: • Completion of portfolio simplification • Outcome of APRA’s revised capital standards — Excess capital available to support growth and returns to shareholders Capital $4.0bn above top end of target operating range 6 CET1 ratio (%) 12.3 11.3 12.4 18.7 Sep-21 Sep-22 Sep-23 Sep-23 Internationally comparable Dividends per ordinary share (cents) 58 61 70 60 64 72 118 125 142 FY21 FY22 FY23 HIGHER DIVIDEND AND SHARE BUYBACK 1 Subject to market conditions. 2 Based on 30-Sep-23 closing price of $21.15. 14% 6% Westpac Group 2023 Full Year Results Presentation & Investor Discussion Pack — FY23 payout ratio of 69% — Sustainable payout ratio range 65 – 75% — Dividend yield 6.7%2, fully franked 9.6%2 — Neutralise DRP for final dividend Strong dividend growth |

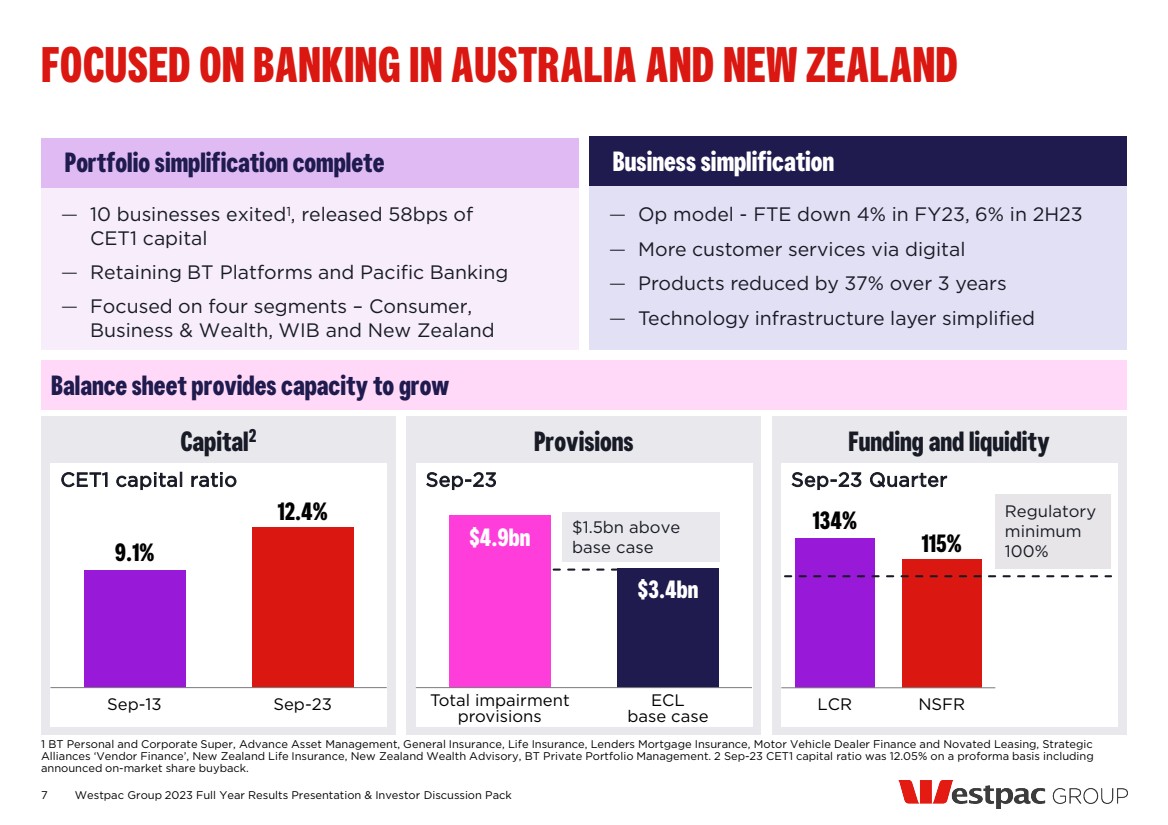

| Capital2 Provisions Funding and liquidity 7 Westpac Group 2023 Full Year Results Presentation & Investor Discussion Pack 1 BT Personal and Corporate Super, Advance Asset Management, General Insurance, Life Insurance, Lenders Mortgage Insurance, Motor Vehicle Dealer Finance and Novated Leasing, Strategic Alliances ‘Vendor Finance’, New Zealand Life Insurance, New Zealand Wealth Advisory, BT Private Portfolio Management. 2 Sep-23 CET1 capital ratio was 12.05% on a proforma basis including announced on-market share buyback. FOCUSED ON BANKING IN AUSTRALIA AND NEW ZEALAND — Op model - FTE down 4% in FY23, 6% in 2H23 — More customer services via digital — Products reduced by 37% over 3 years — Technology infrastructure layer simplified — 10 businesses exited1 , released 58bps of CET1 capital — Retaining BT Platforms and Pacific Banking — Focused on four segments – Consumer, Business & Wealth, WIB and New Zealand Portfolio simplification complete Business simplification Balance sheet provides capacity to grow CET1 capital ratio Sep-23 Sep-23 Quarter 9.1% 12.4% Sep-13 Sep-23 $4.9bn $3.4bn Total impairment provisions ECL base case 134% 115% LCR NSFR $1.5bn above base case Regulatory minimum 100% |

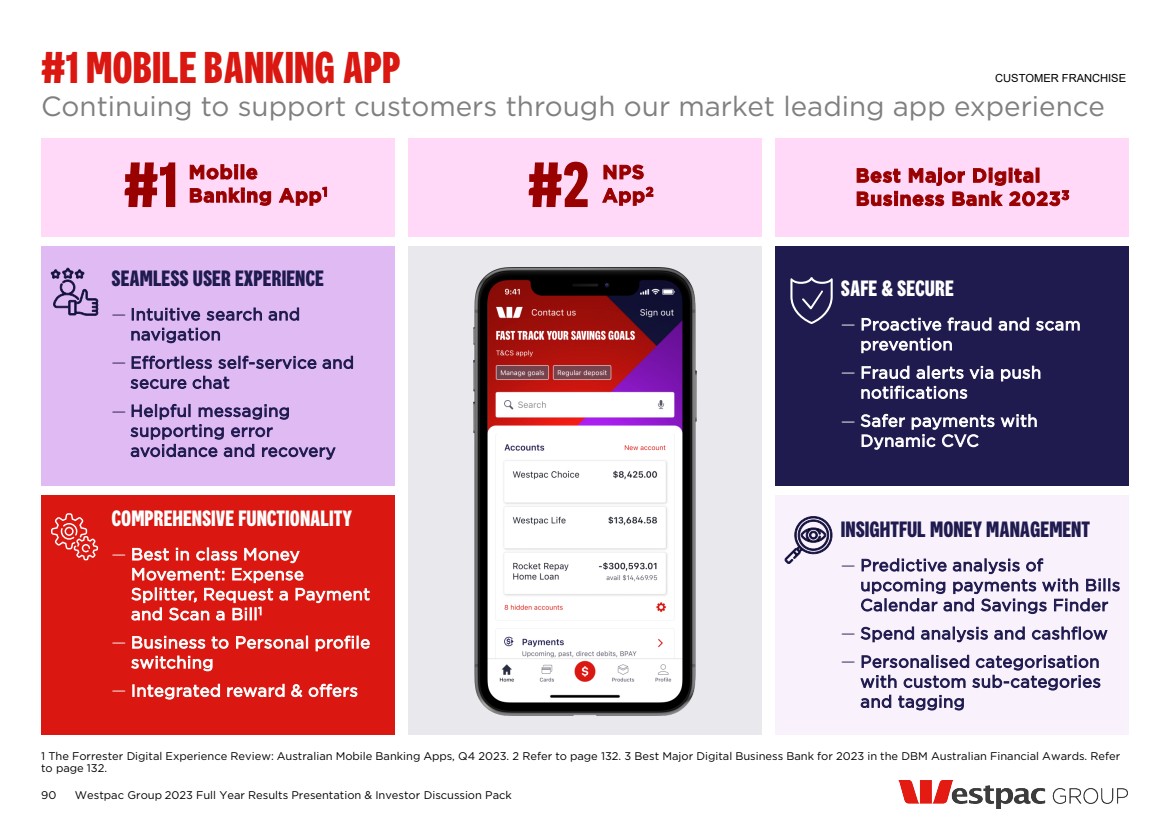

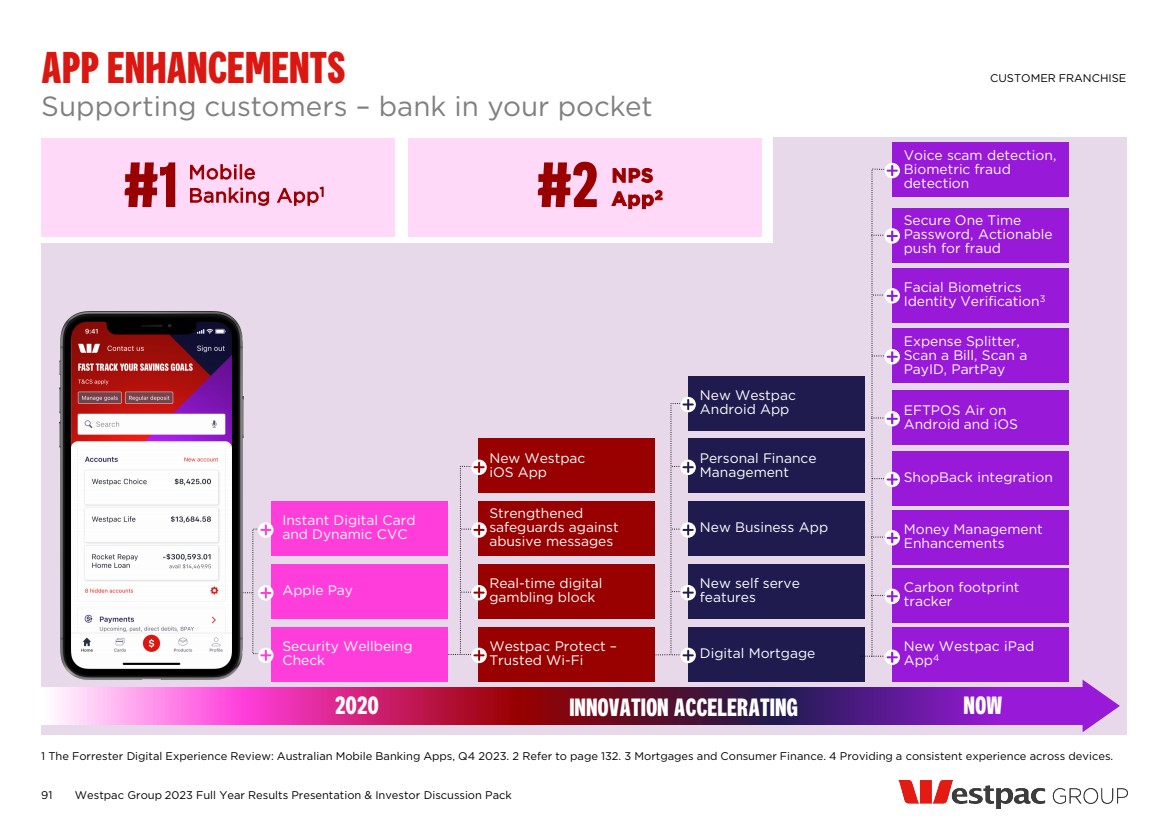

| 8 Westpac Group 2023 Full Year Results Presentation & Investor Discussion Pack 1 The Forrester Digital Experience Review: Australian Mobile Banking Apps, Q4 2023. 2 For further details on metric see page 132. 3 Average for month of Sep-23. Time to Right (TTR) is the number of days from application to unconditional approval for a new loan. 4 Since improved process was implemented in May-23 portion of customers retained in three months post expiry. 5 Main Financial Institution, refer page 132 for definition. 6 Sep-23 compared to Sep-22. 7 Based on ADI System as published in the Monthly ADI statistics by APRA. EASY AND INTUITIVE ONLINE BANKING DRIVING GROWTH #1 NPS App2 #2 Mobile Banking App1 Everyday banking — Simple design with easy search — Open a transaction account online within 3 minutes — Best in class money movement — Insightful money management — Enhanced scam protection Consumer MFI5 18% Home lending — One mortgage origination platform — Fast and automated experience — Consistent First Party TTR: 6 days3 — Third Party TTR improved: 7 days3 — Fixed rate mortgages retention rate increased to 90%4 Strong household deposit growth, 1.3x system6,7 Mortgage growth, 0.8x system6,7 #2 NPS mortgages2 Transaction accounts up 11%6 |

| 9 1 Sep-23 compared to Sep-22. 2 At Sep-23. BUSINESS BANKING OPPORTUNITY Lending growth, up 5% to $88.9bn1 Strong business deposit base, deposit to loan ratio 147%2 Transaction accounts, up 4%1 Awarded Canstar’s 2023 Banker of the Year in Agribusiness EFTPOS Air — Businesses can accept payments on iPhone or Android — Simple online application process, set-up within 15 minutes Business One Account — Competitive business transaction account — Open online within 10 minutes Business lending — Streamlined application process, saves 2hrs per deal1 — Time to decision improved 32% to 9.5 days1 Westpac Group 2023 Full Year Results Presentation & Investor Discussion Pack |

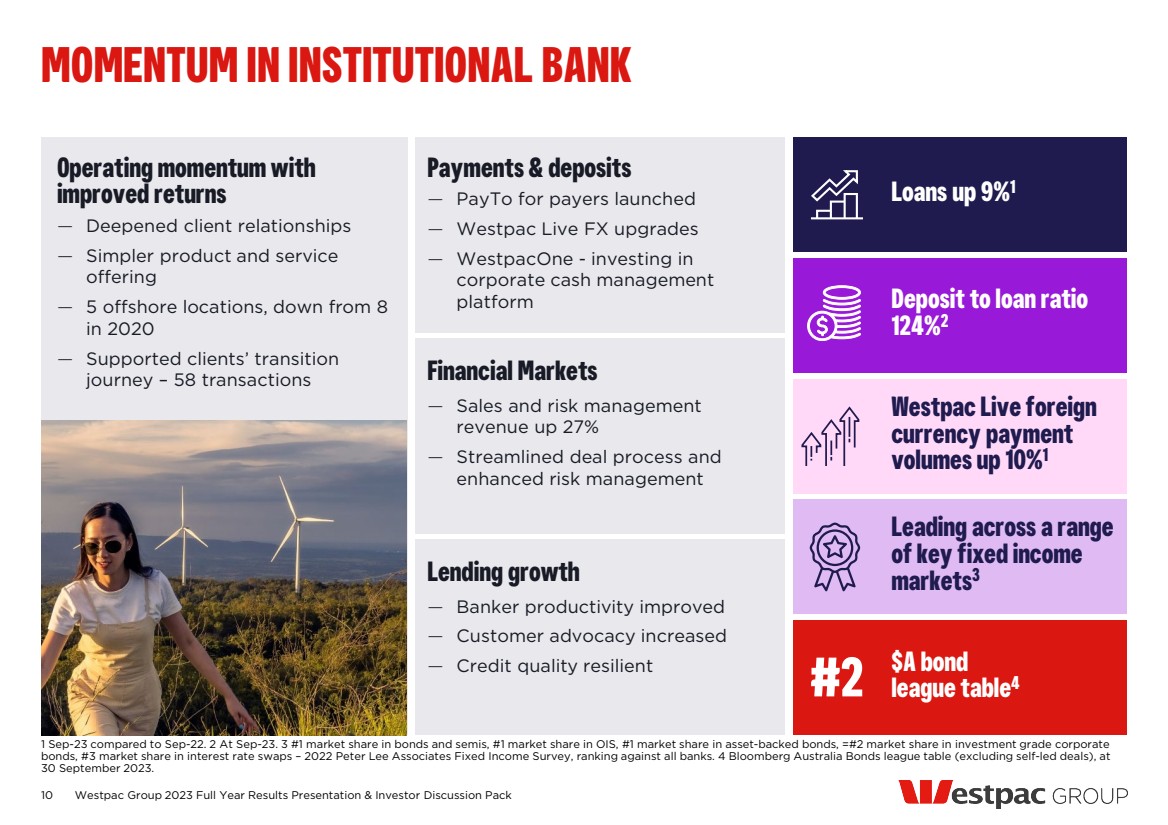

| 10 Westpac Group 2023 Full Year Results Presentation & Investor Discussion Pack 1 Sep-23 compared to Sep-22. 2 At Sep-23. 3 #1 market share in bonds and semis, #1 market share in OIS, #1 market share in asset-backed bonds, =#2 market share in investment grade corporate bonds, #3 market share in interest rate swaps – 2022 Peter Lee Associates Fixed Income Survey, ranking against all banks. 4 Bloomberg Australia Bonds league table (excluding self-led deals), at 30 September 2023. MOMENTUM IN INSTITUTIONAL BANK Operating momentum with improved returns — Deepened client relationships — Simpler product and service offering — 5 offshore locations, down from 8 in 2020 — Supported clients’ transition journey – 58 transactions Payments & deposits — PayTo for payers launched — Westpac Live FX upgrades — WestpacOne - investing in corporate cash management platform Financial Markets — Sales and risk management revenue up 27% — Streamlined deal process and enhanced risk management Lending growth — Banker productivity improved — Customer advocacy increased — Credit quality resilient Loans up 9%1 Westpac Live foreign currency payment volumes up 10%1 Leading across a range of key fixed income markets3 $A bond league table4 Deposit to loan ratio 124%2 #2 |

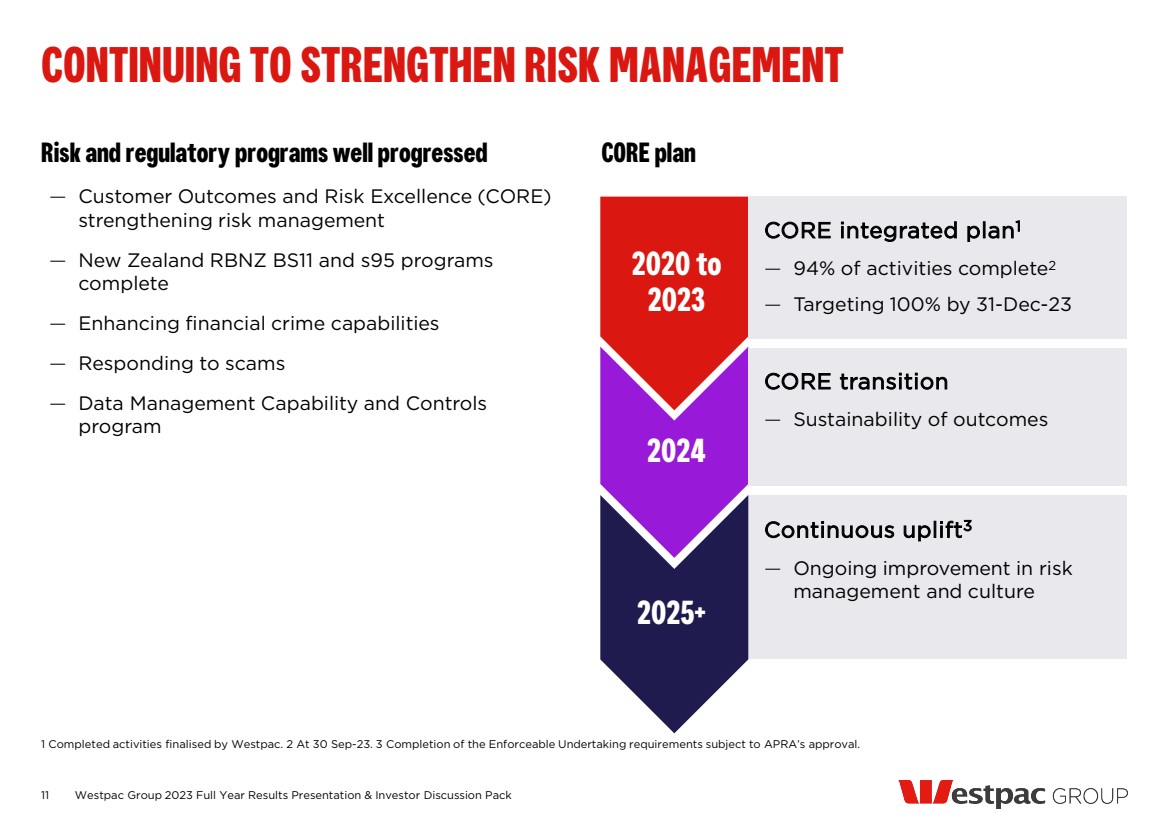

| CONTINUING TO STRENGTHEN RISK MANAGEMENT 11 Risk and regulatory programs well progressed — Customer Outcomes and Risk Excellence (CORE) strengthening risk management — New Zealand RBNZ BS11 and s95 programs complete — Enhancing financial crime capabilities — Responding to scams — Data Management Capability and Controls program CORE plan 1 Completed activities finalised by Westpac. 2 At 30 Sep-23. 3 Completion of the Enforceable Undertaking requirements subject to APRA’s approval. Continuous uplift3 — Ongoing improvement in risk management and culture 2020 to 2023 CORE integrated plan1 — 94% of activities complete2 — Targeting 100% by 31-Dec-23 2024 CORE transition — Sustainability of outcomes 2025+ Westpac Group 2023 Full Year Results Presentation & Investor Discussion Pack |

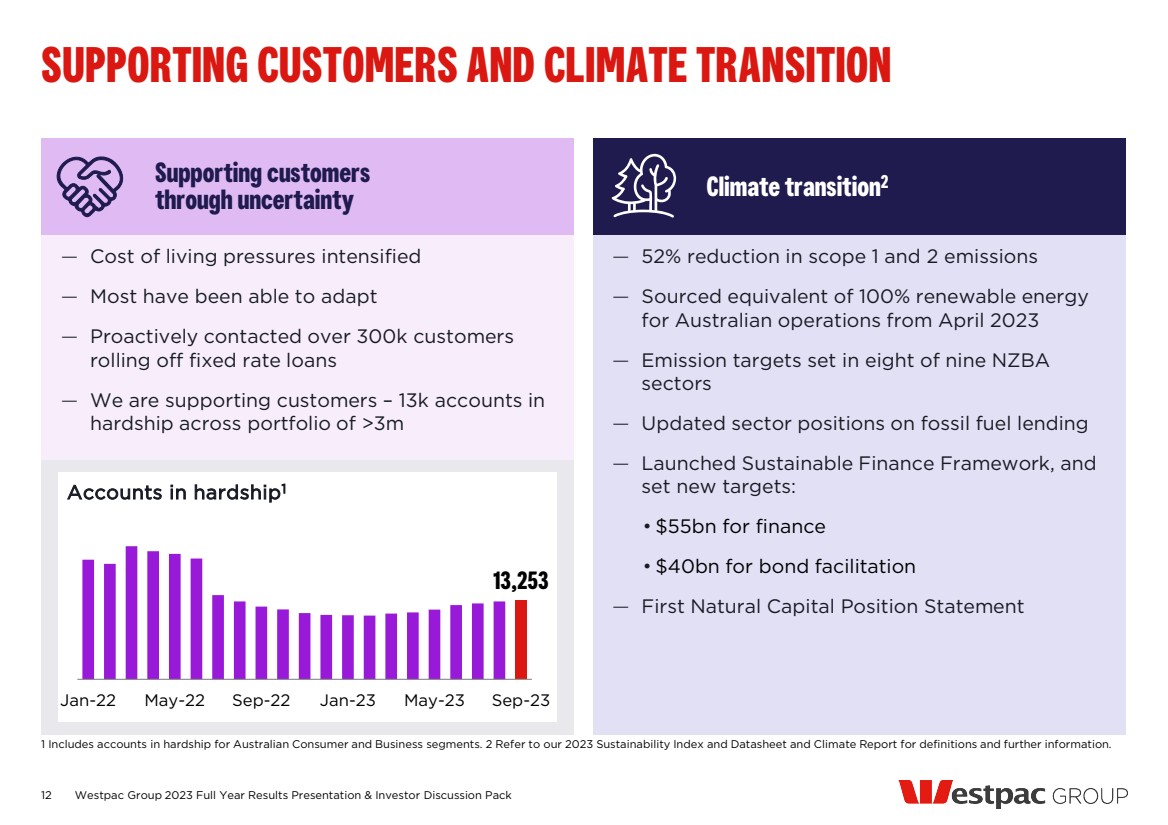

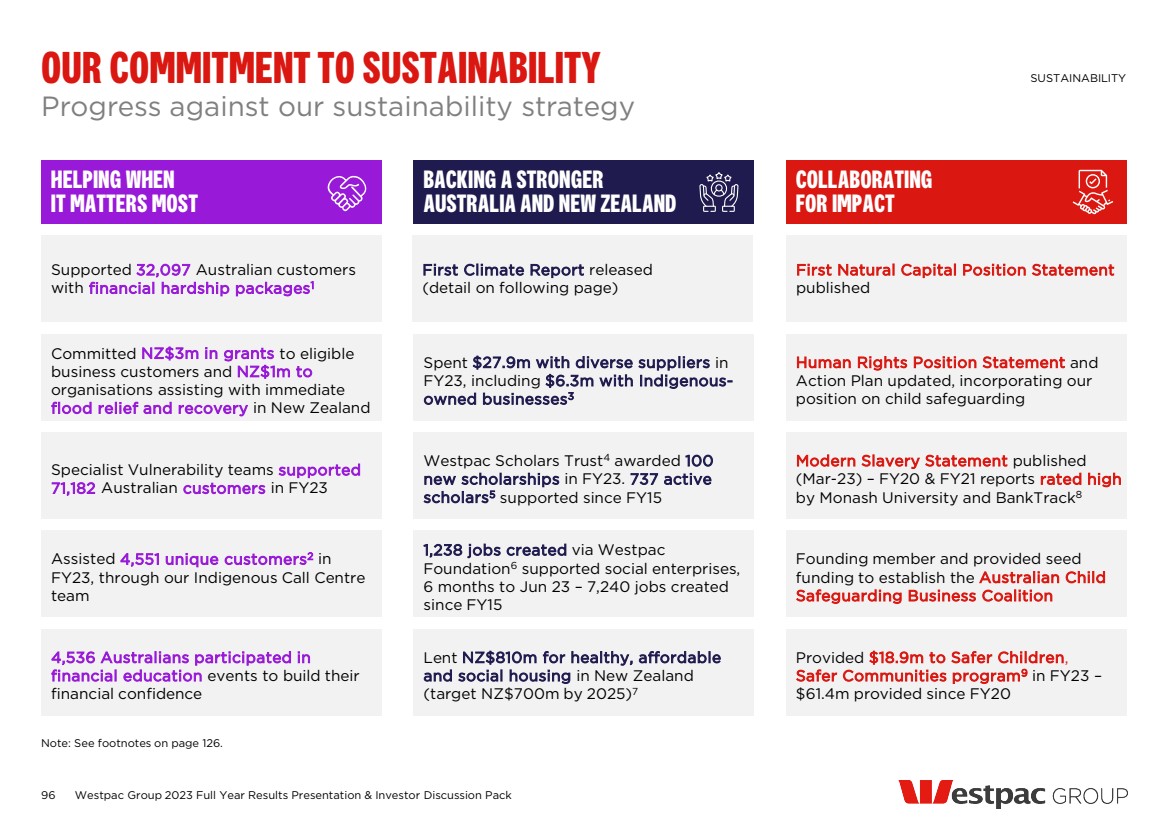

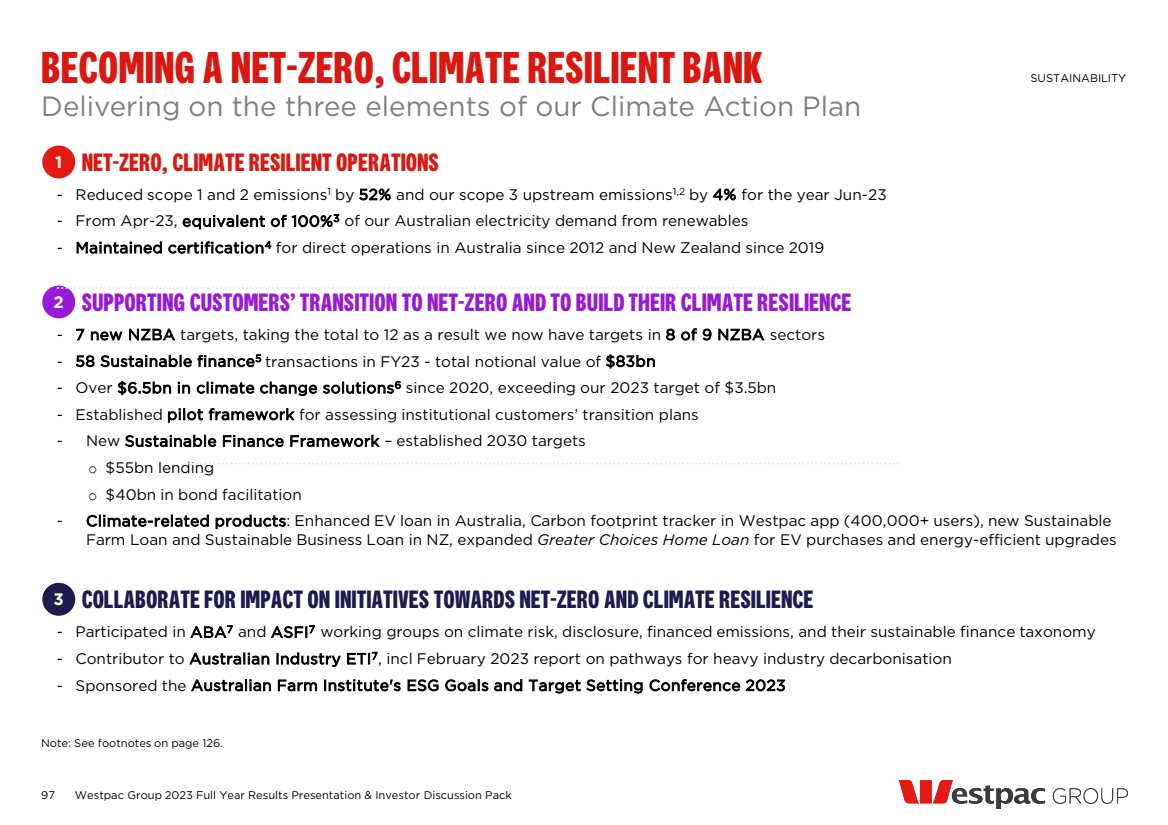

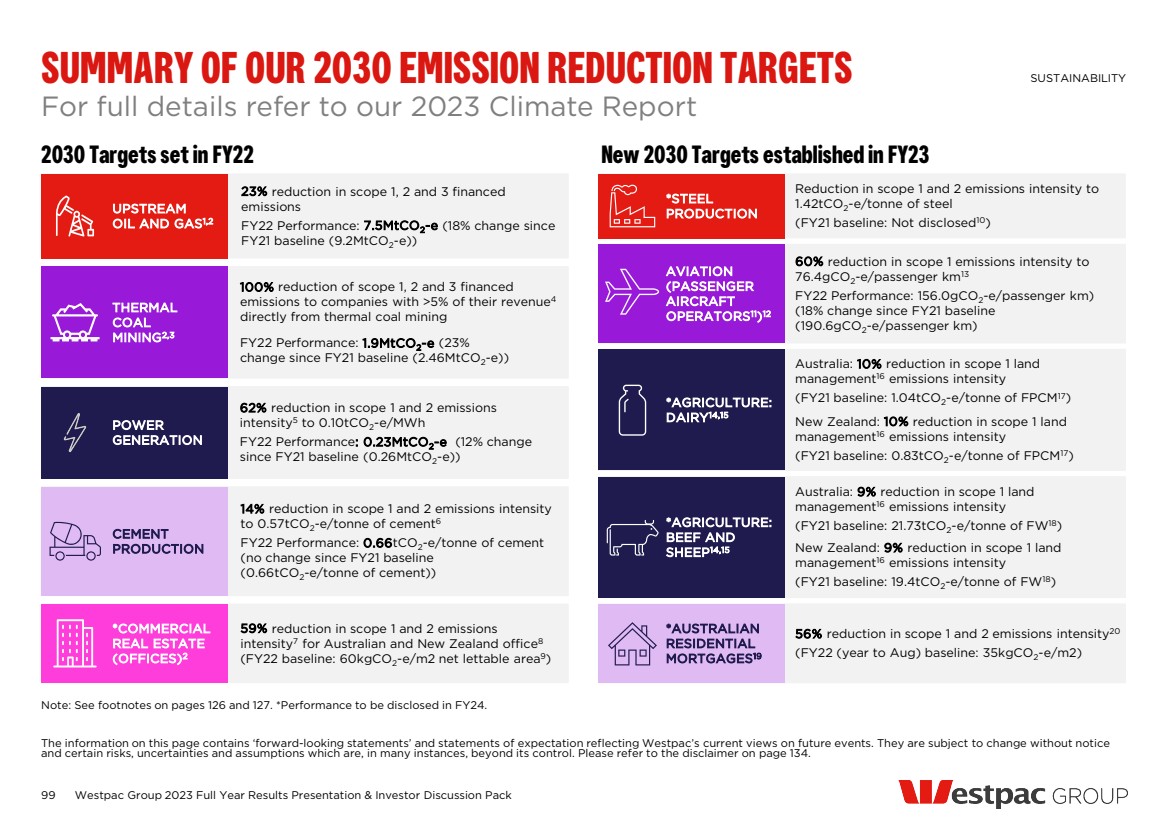

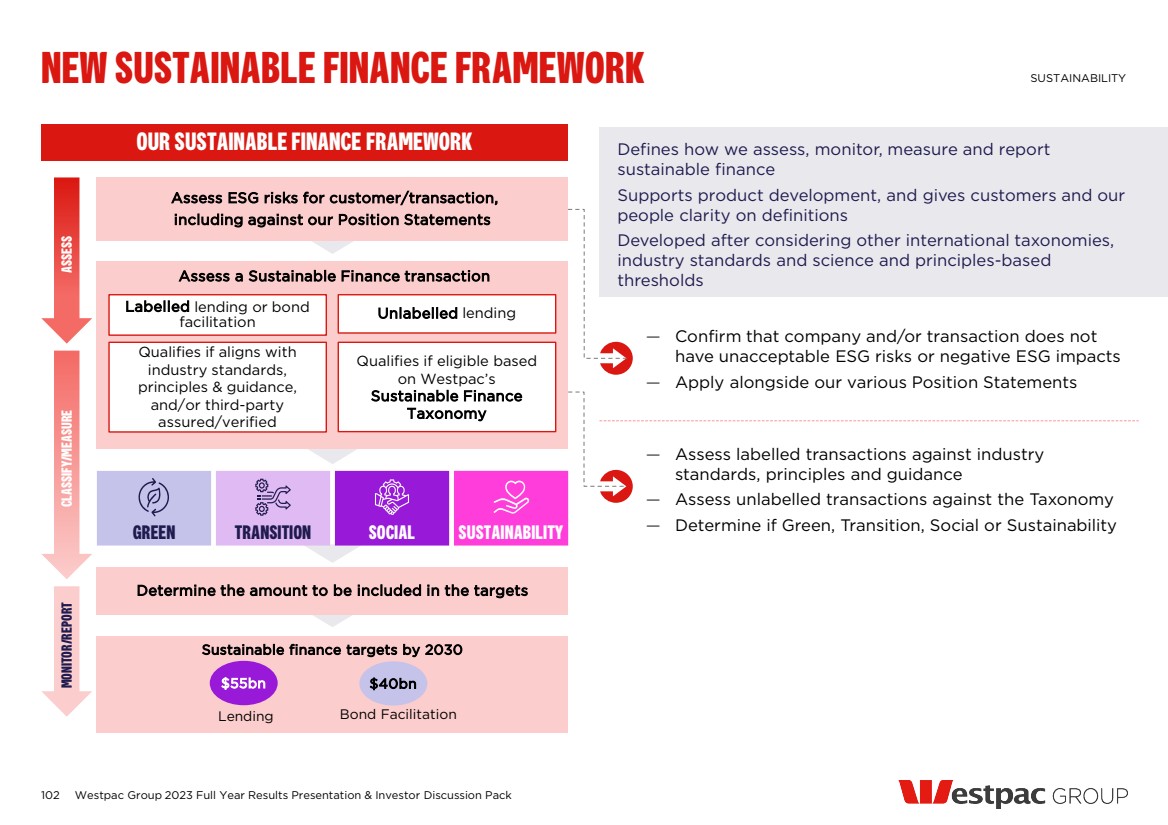

| 1 Includes accounts in hardship for Australian Consumer and Business segments. 2 Refer to our 2023 Sustainability Index and Datasheet and Climate Report for definitions and further information. 12 Westpac Group 2023 Full Year Results Presentation & Investor Discussion Pack SUPPORTING CUSTOMERS AND CLIMATE TRANSITION — 52% reduction in scope 1 and 2 emissions — Sourced equivalent of 100% renewable energy for Australian operations from April 2023 — Emission targets set in eight of nine NZBA sectors — Updated sector positions on fossil fuel lending — Launched Sustainable Finance Framework, and set new targets: • $55bn for finance • $40bn for bond facilitation — First Natural Capital Position Statement — Cost of living pressures intensified — Most have been able to adapt — Proactively contacted over 300k customers rolling off fixed rate loans — We are supporting customers – 13k accounts in hardship across portfolio of >3m Climate transition Supporting customers 2 through uncertainty 13,253 Jan-22 May-22 Sep-22 Jan-23 May-23 Sep-23 Accounts in hardship1 |

| MICHAEL ROWLAND Chief Financial Officer |

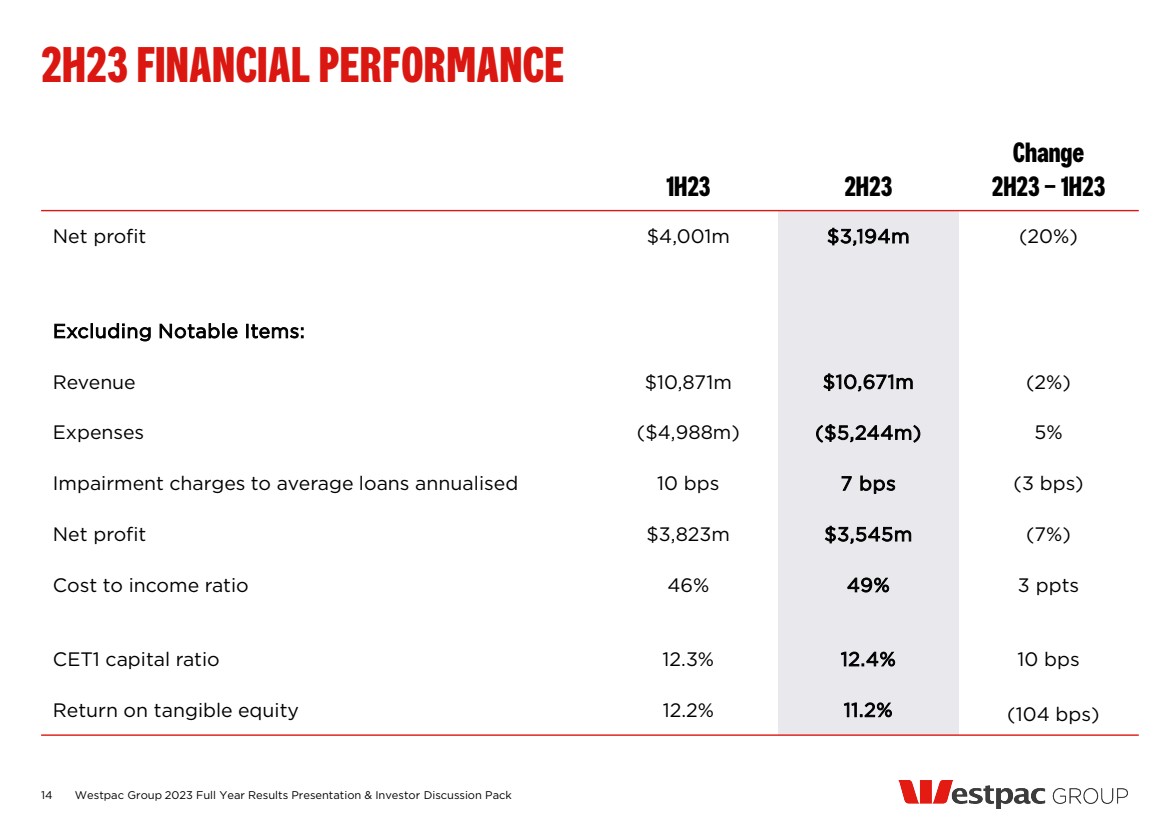

| 1H23 2H23 Change 2H23 – 1H23 Net profit $4,001m $3,194m (20%) Excluding Notable Items: Revenue $10,871m $10,671m (2%) Expenses ($4,988m) ($5,244m) 5% Impairment charges to average loans annualised 10 bps 7 bps (3 bps) Net profit $3,823m $3,545m (7%) Cost to income ratio 46% 49% 3 ppts CET1 capital ratio 12.3% 12.4% 10 bps Return on tangible equity 12.2% 11.2% (104 bps) 2H23 FINANCIAL PERFORMANCE 14 Westpac Group 2023 Full Year Results Presentation & Investor Discussion Pack |

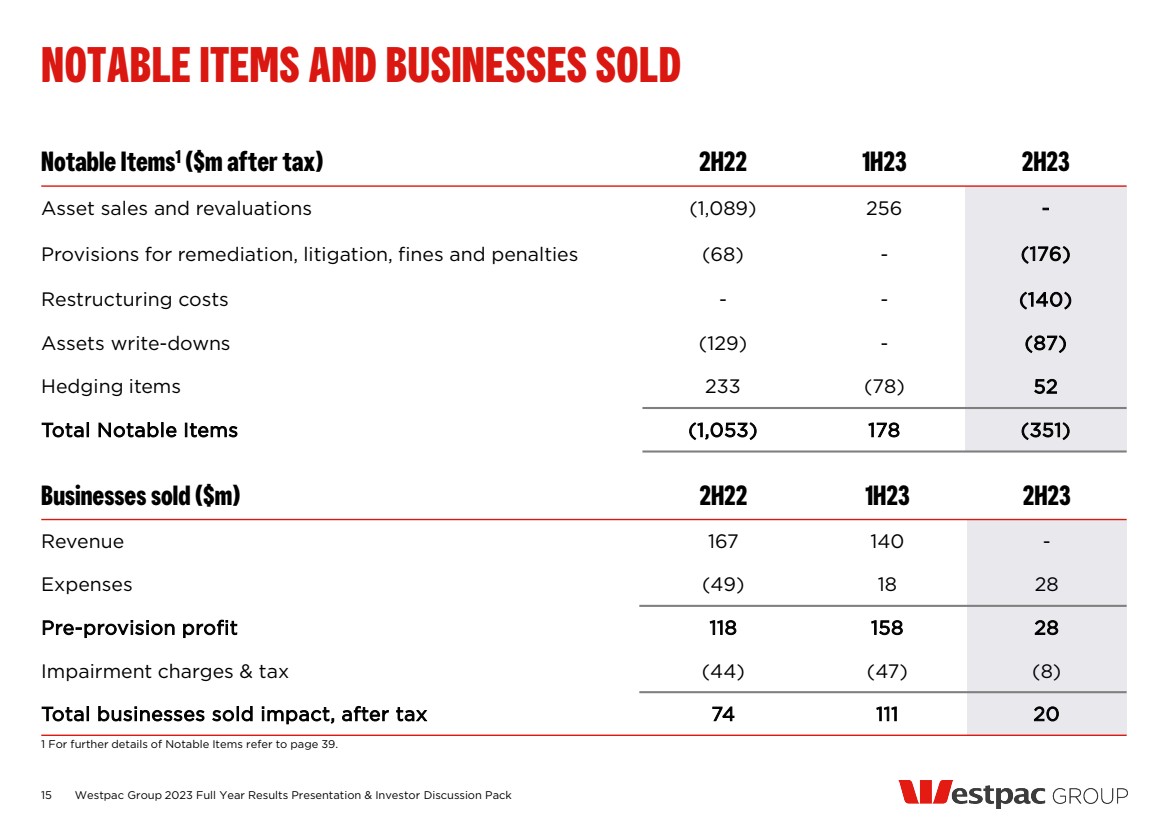

| Notable Items1 ($m after tax) 2H22 1H23 2H23 Asset sales and revaluations (1,089) 256 - Provisions for remediation, litigation, fines and penalties (68) - (176) Restructuring costs - - (140) Assets write-downs (129) - (87) Hedging items 233 (78) 52 Total Notable Items (1,053) 178 (351) 15 NOTABLE ITEMS AND BUSINESSES SOLD 1 For further details of Notable Items refer to page 39. Businesses sold ($m) 2H22 1H23 2H23 Revenue 167 140 - Expenses (49) 18 28 Pre-provision profit 118 158 28 Impairment charges & tax (44) (47) (8) Total businesses sold impact, after tax 74 111 20 Westpac Group 2023 Full Year Results Presentation & Investor Discussion Pack |

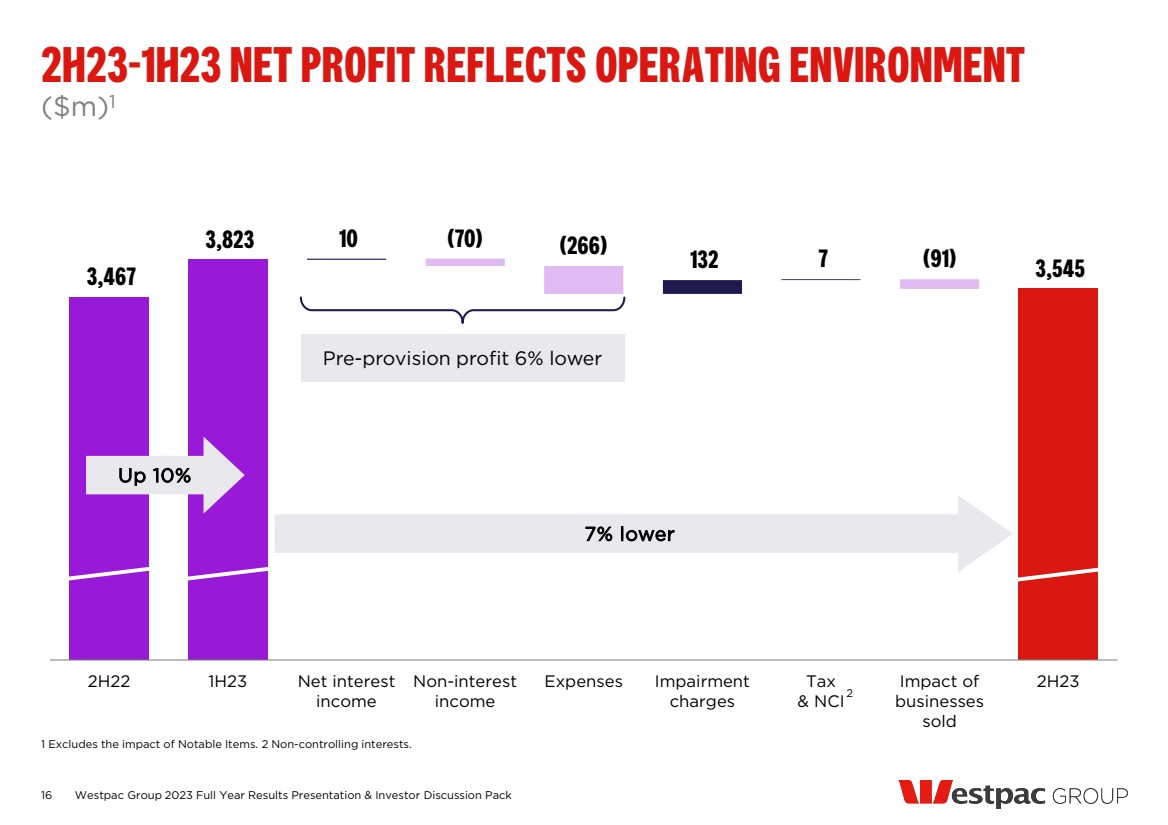

| 3,467 3,823 10 132 7 3,545 (70) (266) (91) 2H22 1H23 Net interest income Non-interest income Expenses Impairment charges Tax & NCI Impact of businesses sold 2H23 ($m)1 2H23-1H23 NET PROFIT REFLECTS OPERATING ENVIRONMENT 1 Excludes the impact of Notable Items. 2 Non-controlling interests. 2 Pre-provision profit 6% lower 7% lower Up 10% 16 Westpac Group 2023 Full Year Results Presentation & Investor Discussion Pack |

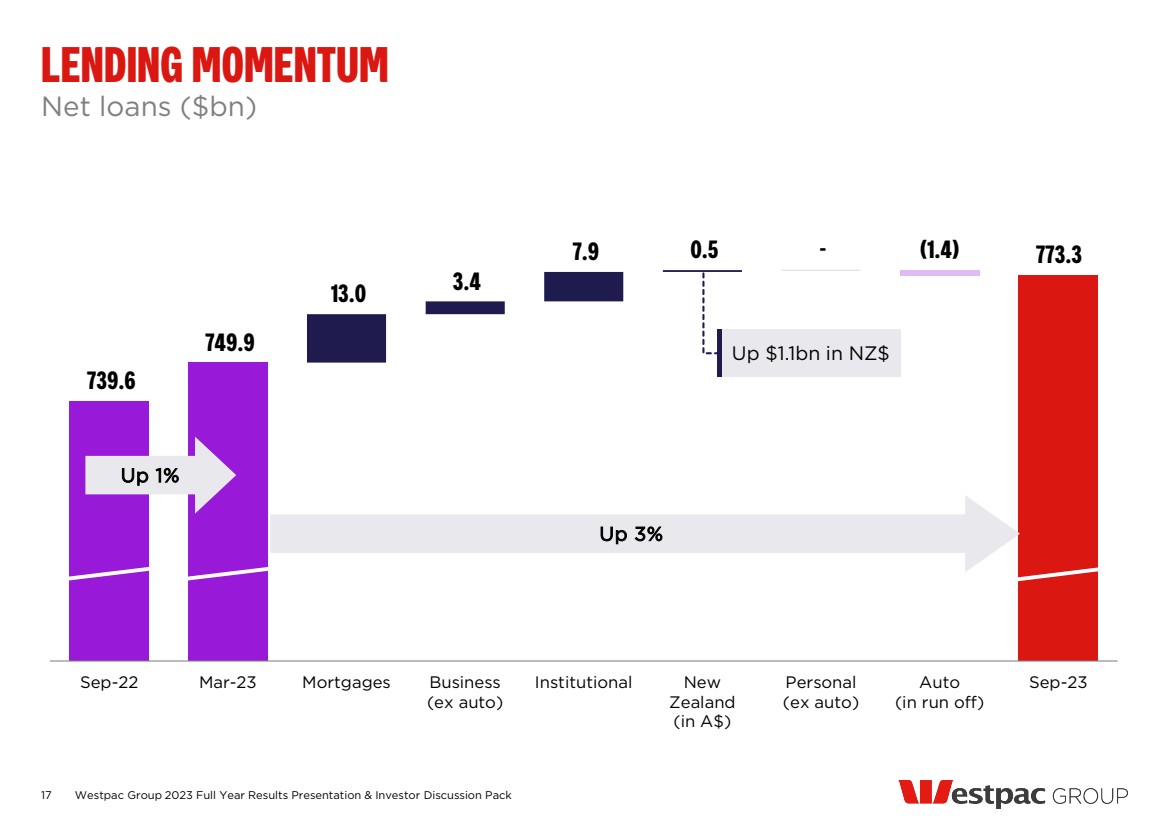

| 739.6 749.9 13.0 3.4 7.9 0.5 - 773.3 (1.4) Sep-22 Mar-23 Mortgages Business (ex auto) Institutional New Zealand (in A$) Personal (ex auto) Auto (in run off) Sep-23 Net loans ($bn) LENDING MOMENTUM Up $1.1bn in NZ$ Up 3% Up 1% 17 Westpac Group 2023 Full Year Results Presentation & Investor Discussion Pack |

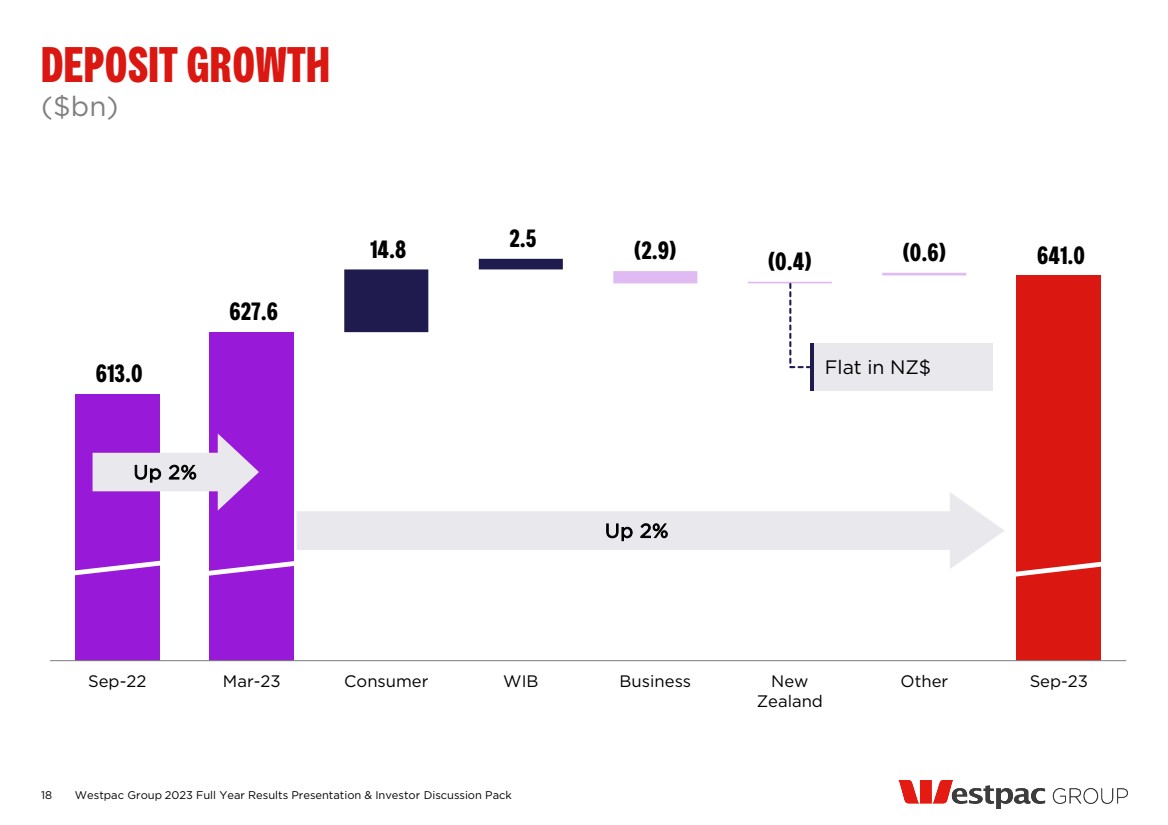

| 613.0 627.6 14.8 2.5 641.0 (2.9) (0.4) (0.6) Sep-22 Mar-23 Consumer WIB Business New Zealand Other Sep-23 ($bn) DEPOSIT GROWTH Up 2% Up 2% Flat in NZ$ 18 Westpac Group 2023 Full Year Results Presentation & Investor Discussion Pack |

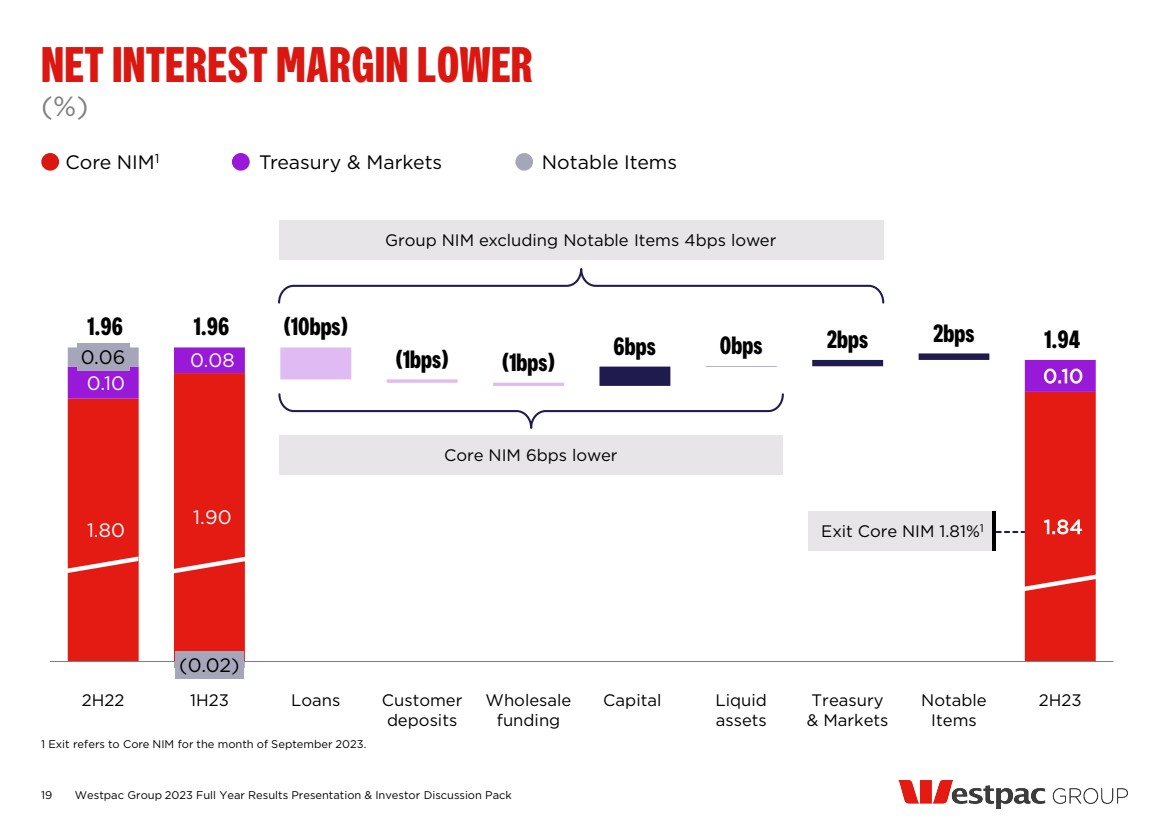

| 1.80 1.90 1.84 0.10 0.08 0.10 0.06 (0.02) 1.96 1.96 6bps 0bps 2bps 2bps 1.94 (10bps) (1bps) (1bps) 2H22 1H23 Loans Customer deposits Wholesale funding Capital Liquid assets Treasury & Markets Notable Items 2H23 (%) NET INTEREST MARGIN LOWER 1 Exit refers to Core NIM for the month of September 2023. Core NIM1 Treasury & Markets Notable Items Core NIM 6bps lower 19 Westpac Group 2023 Full Year Results Presentation & Investor Discussion Pack Exit Core NIM 1.81%1 Group NIM excluding Notable Items 4bps lower |

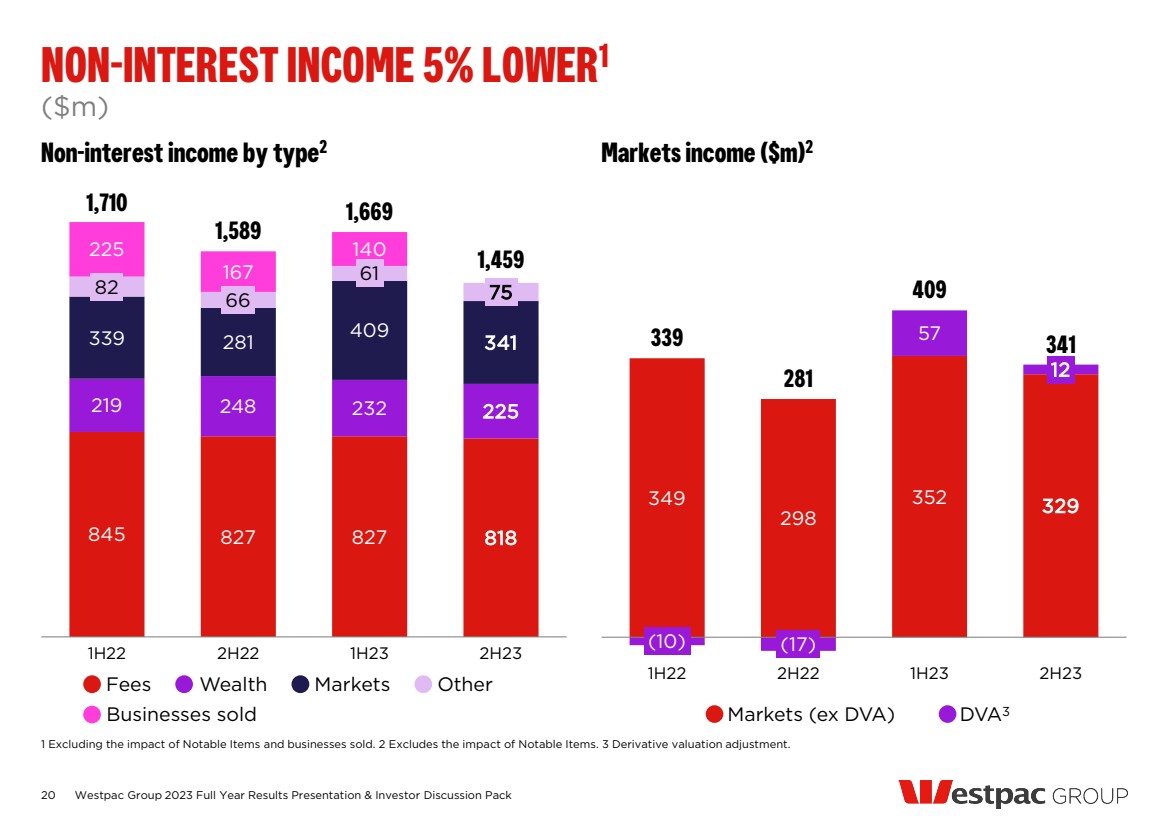

| NON-INTEREST INCOME 5% LOWER1 20 Non-interest income by type2 845 827 827 818 219 248 232 225 339 281 409 341 82 66 61 75 225 167 140 1,710 1,589 1,669 1,459 1H22 2H22 1H23 2H23 Markets income ($m)2 349 298 352 329 (10) (17) 57 12 339 281 409 341 1H22 2H22 1H23 2H23 ($m) 1 Excluding the impact of Notable Items and businesses sold. 2 Excludes the impact of Notable Items. 3 Derivative valuation adjustment. Westpac Group 2023 Full Year Results Presentation & Investor Discussion Pack Markets (ex DVA) DVA3 Fees Wealth Markets Other Businesses sold |

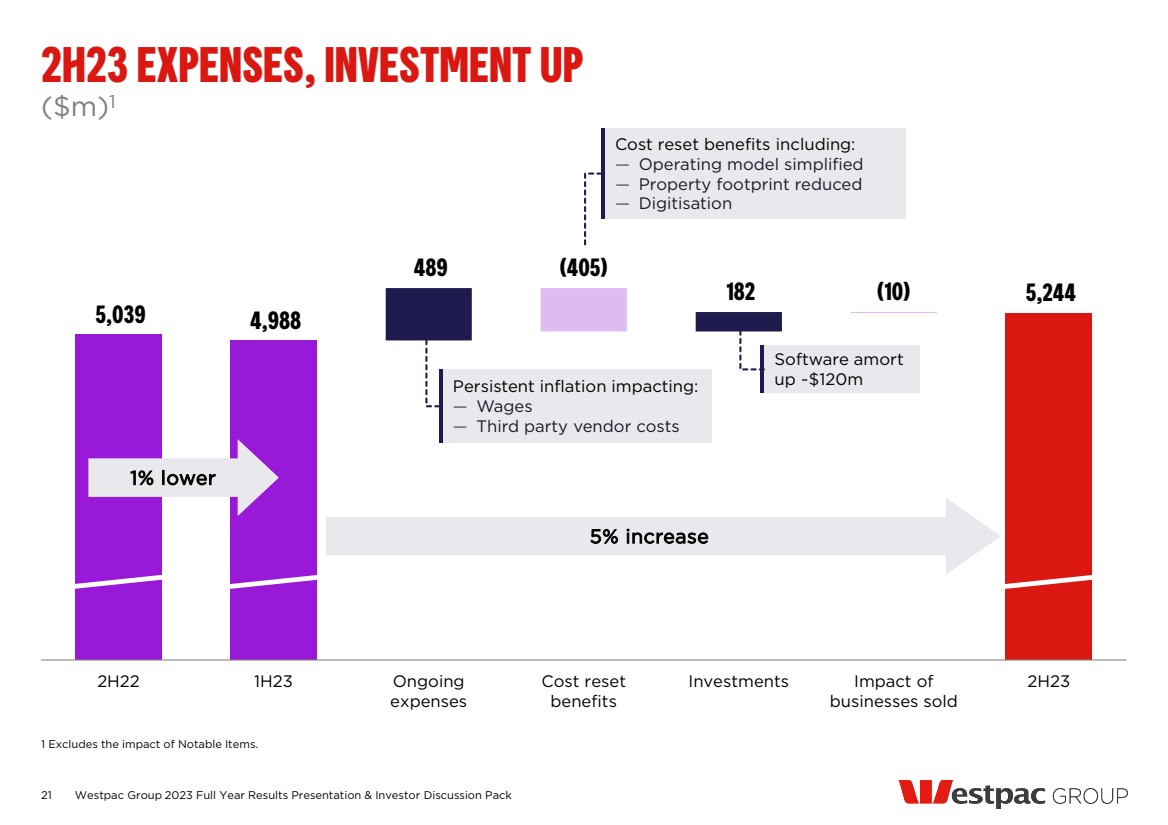

| 5,039 4,988 489 182 5,244 (405) (10) 2H22 1H23 Ongoing expenses Cost reset benefits Investments Impact of businesses sold 2H23 ($m)1 2H23 EXPENSES, INVESTMENT UP 1 Excludes the impact of Notable Items. 5% increase 1% lower Software amort up ~$120m Persistent inflation impacting: — Wages — Third party vendor costs Cost reset benefits including: — Operating model simplified — Property footprint reduced — Digitisation 21 Westpac Group 2023 Full Year Results Presentation & Investor Discussion Pack |

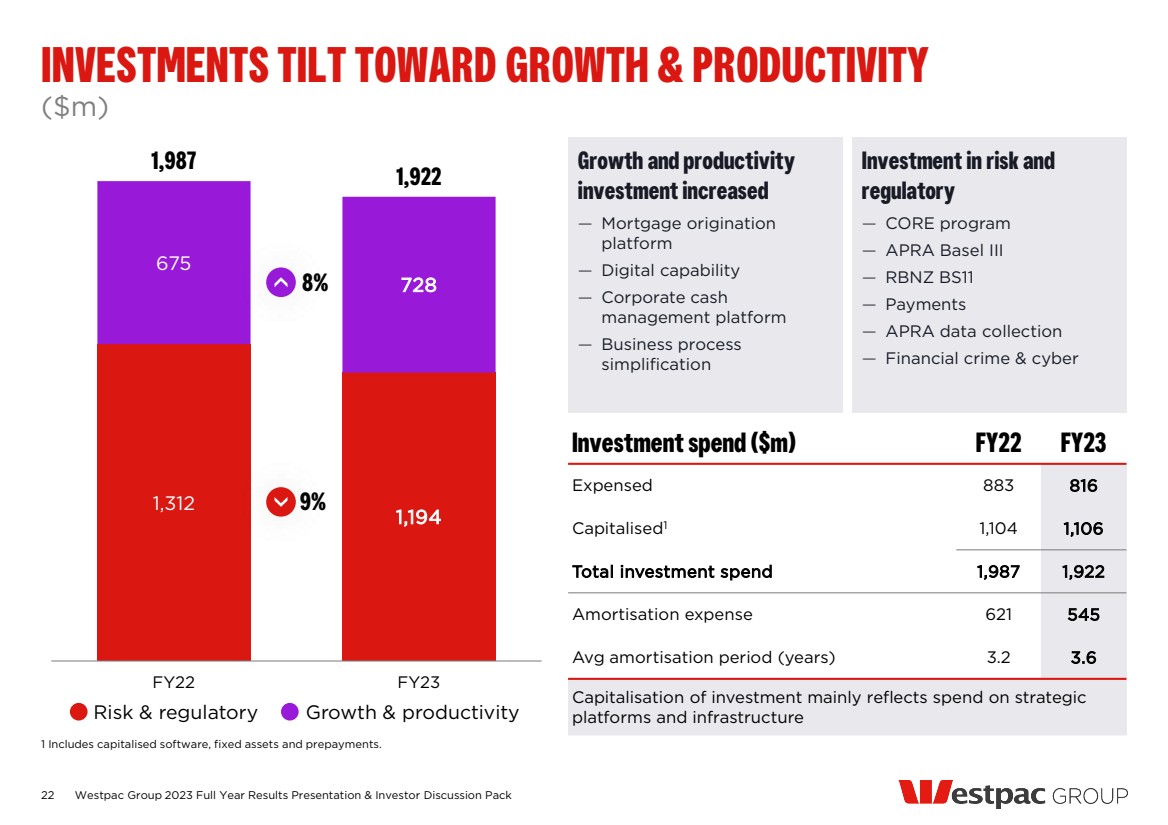

| Growth and productivity investment increased — Mortgage origination platform — Digital capability — Corporate cash management platform — Business process simplification Investment in risk and regulatory — CORE program — APRA Basel III — RBNZ BS11 — Payments — APRA data collection — Financial crime & cyber 1,312 1,194 675 728 1,987 1,922 FY22 FY23 ($m) INVESTMENTS TILT TOWARD GROWTH & PRODUCTIVITY 1 Includes capitalised software, fixed assets and prepayments. 8% 9% Investment spend ($m) FY22 FY23 Expensed 883 816 Capitalised1 1,104 1,106 Total investment spend 1,987 1,922 Amortisation expense 621 545 Avg amortisation period (years) 3.2 3.6 Capitalisation of investment mainly reflects spend on strategic platforms and infrastructure 22 Westpac Group 2023 Full Year Results Presentation & Investor Discussion Pack Risk & regulatory Growth & productivity |

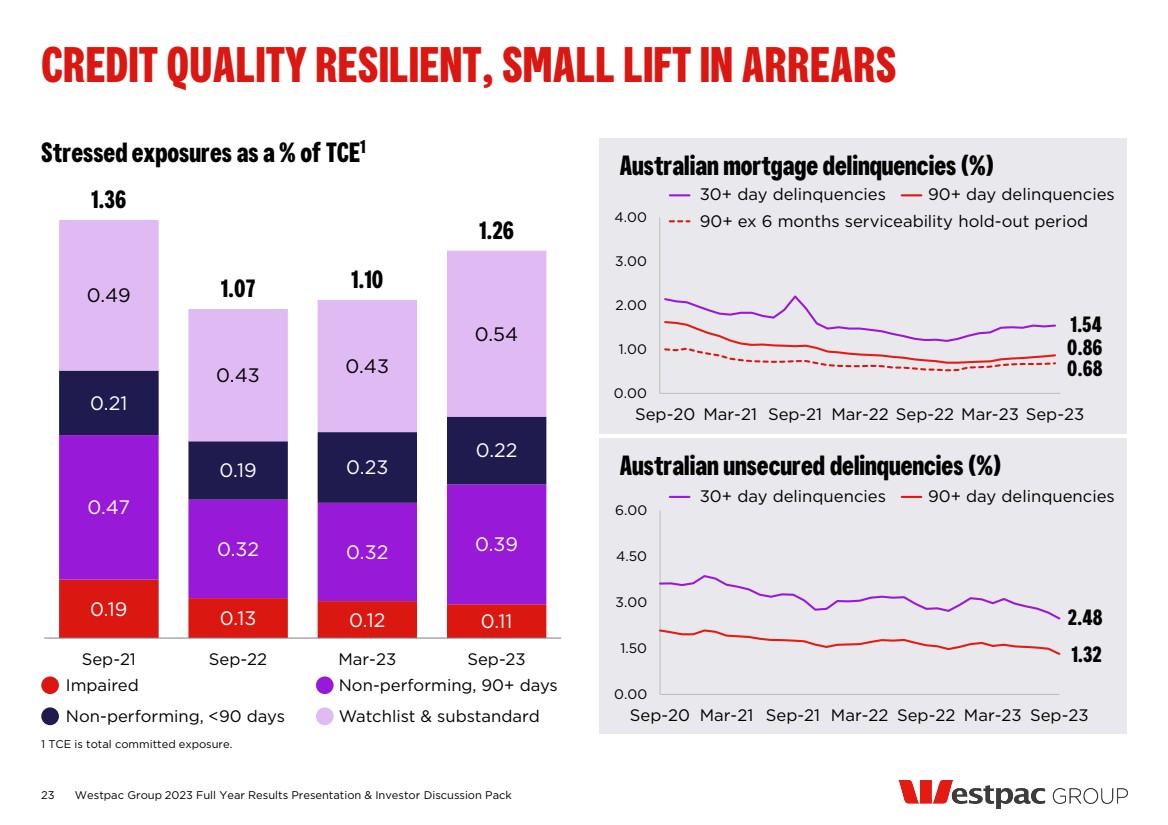

| 23 0.19 0.13 0.12 0.11 0.47 0.32 0.32 0.39 0.21 0.19 0.23 0.22 0.49 0.43 0.43 0.54 1.36 1.07 1.10 1.26 Sep-21 Sep-22 Mar-23 Sep-23 Stressed exposures as a % of TCE1 Westpac Group 2023 Full Year Results Presentation & Investor Discussion Pack CREDIT QUALITY RESILIENT, SMALL LIFT IN ARREARS 1 TCE is total committed exposure. Australian mortgage delinquencies (%) Australian unsecured delinquencies (%) 1.54 0.86 0.68 0.00 1.00 2.00 3.00 4.00 Sep-20 Mar-21 Sep-21 Mar-22 Sep-22 Mar-23 Sep-23 2.48 1.32 0.00 1.50 3.00 4.50 6.00 Sep-20 Mar-21 Sep-21 Mar-22 Sep-22 Mar-23 Sep-23 Impaired Non-performing, 90+ days Non-performing, <90 days Watchlist & substandard 30+ day delinquencies 90+ day delinquencies 90+ ex 6 months serviceability hold-out period 30+ day delinquencies 90+ day delinquencies |

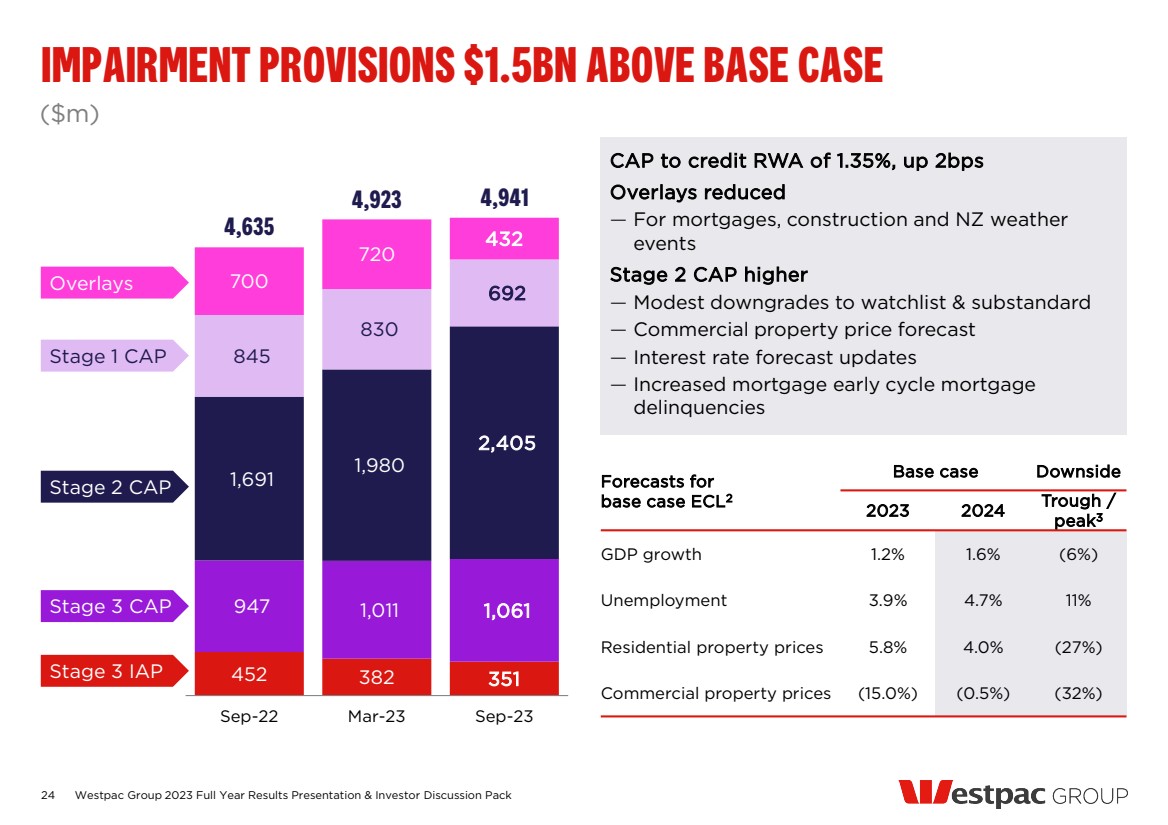

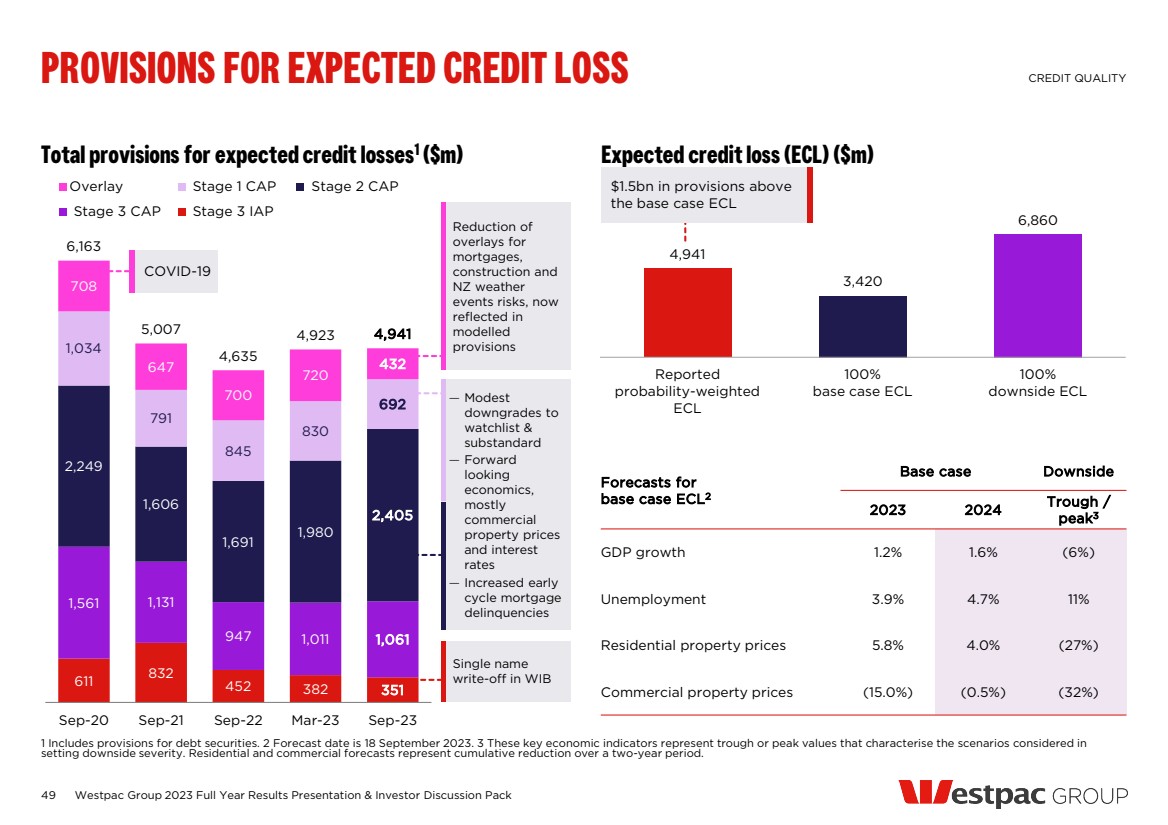

| IMPAIRMENT PROVISIONS $1.5BN ABOVE BASE CASE 24 452 382 351 947 1,011 1,061 1,691 1,980 2,405 845 830 692 700 720 432 4,635 4,923 4,941 Sep-22 Mar-23 Sep-23 ($m) Overlays Stage 3 IAP Stage 3 CAP Stage 1 CAP Stage 2 CAP CAP to credit RWA of 1.35%, up 2bps Overlays reduced — For mortgages, construction and NZ weather events Stage 2 CAP higher — Modest downgrades to watchlist & substandard — Commercial property price forecast — Interest rate forecast updates — Increased mortgage early cycle mortgage delinquencies Westpac Group 2023 Full Year Results Presentation & Investor Discussion Pack Forecasts for base case ECL2 Base case Downside 2023 2024 Trough / peak3 GDP growth 1.2% 1.6% (6%) Unemployment 3.9% 4.7% 11% Residential property prices 5.8% 4.0% (27%) Commercial property prices (15.0%) (0.5%) (32%) |

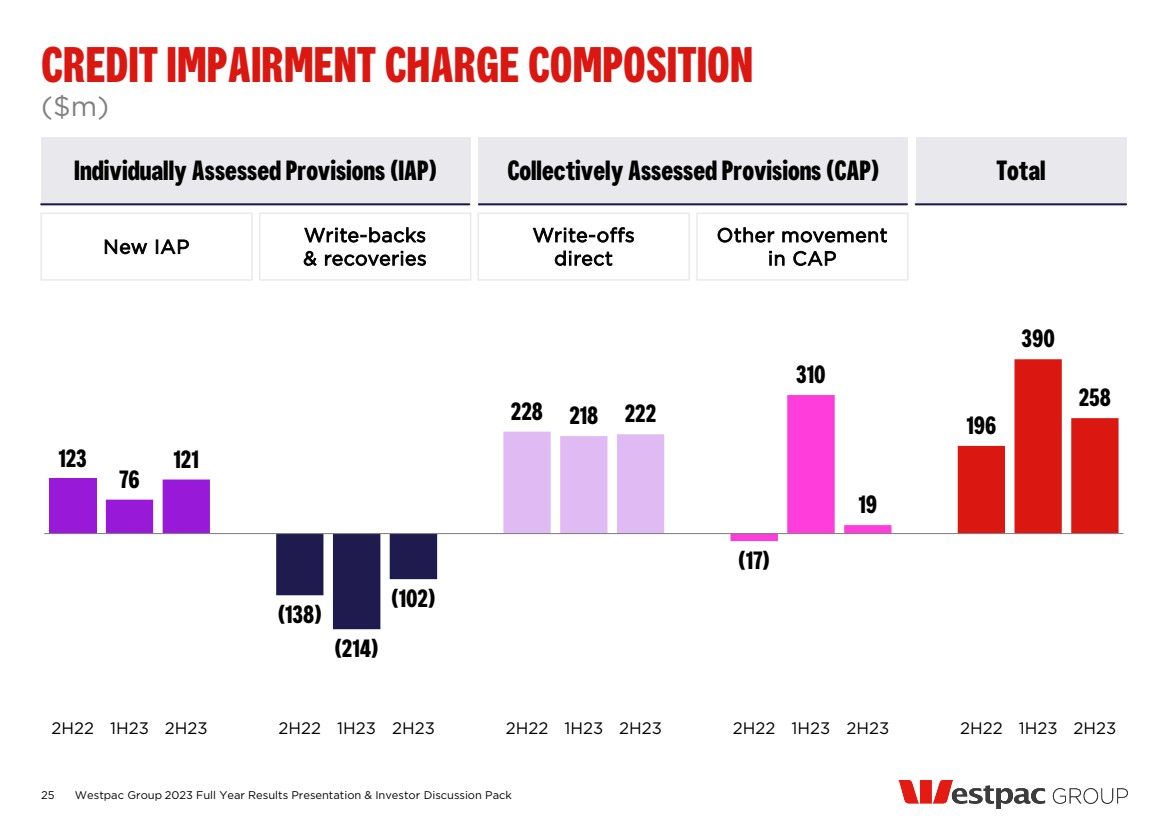

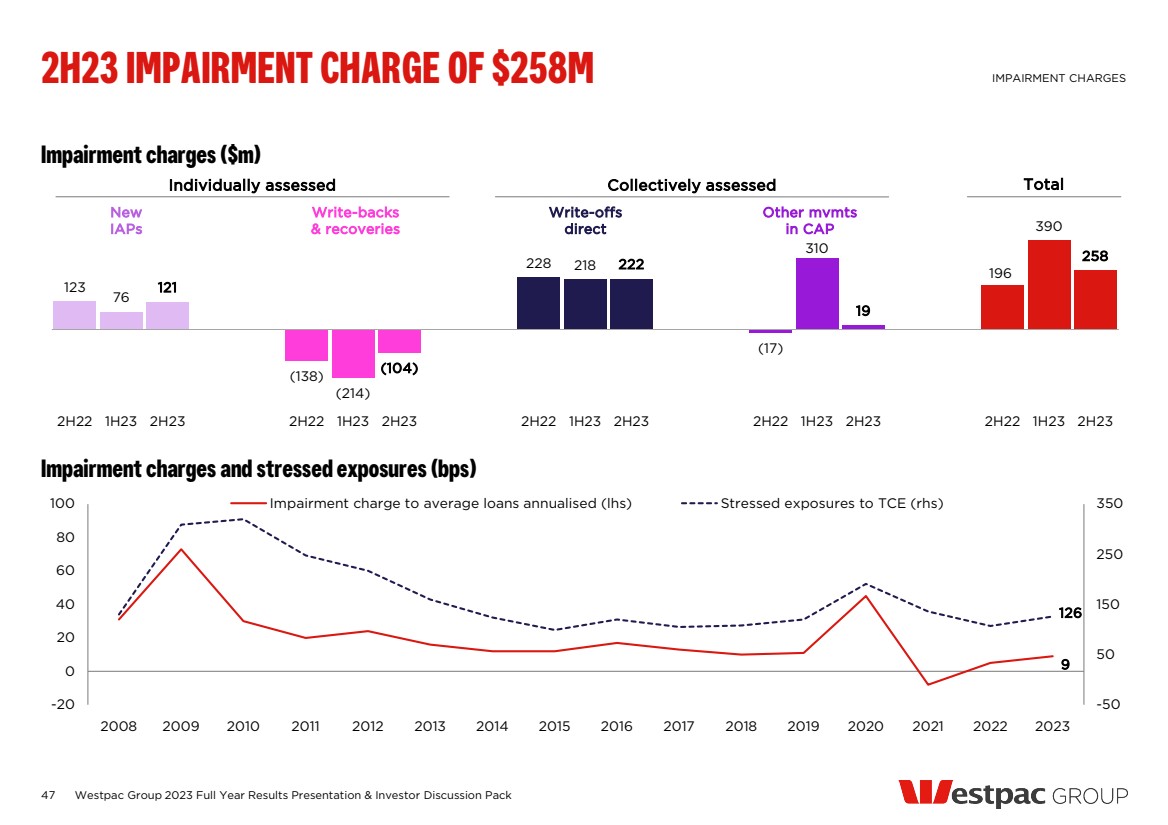

| 25 ($m) Westpac Group 2023 Full Year Results Presentation & Investor Discussion Pack CREDIT IMPAIRMENT CHARGE COMPOSITION 123 76 121 (138) (214) (102) 228 218 222 (17) 310 19 196 390 258 2H22 1H23 2H23 2H22 1H23 2H23 2H22 1H23 2H23 2H22 1H23 2H23 2H22 1H23 2H23 Individually Assessed Provisions (IAP) Collectively Assessed Provisions (CAP) Total New IAP Write-backs & recoveries Write-offs direct Other movement in CAP |

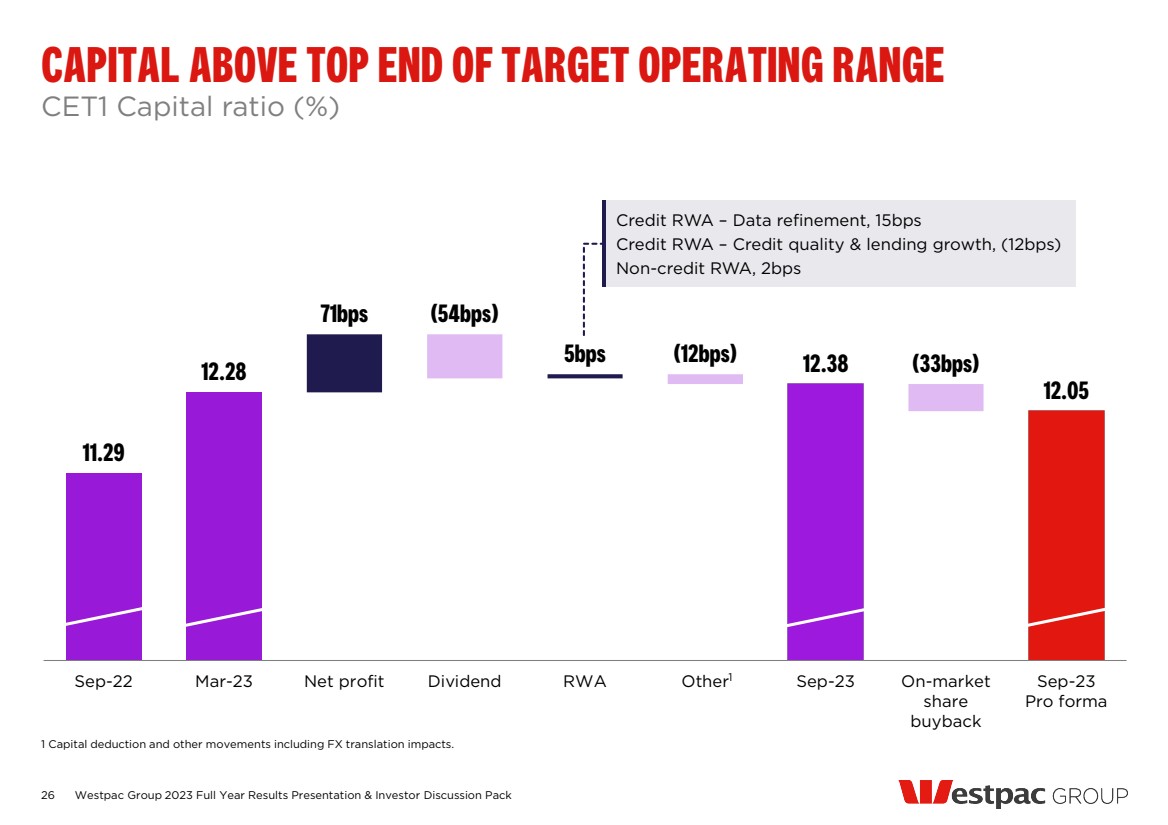

| 11.29 12.28 71bps 5bps 12.38 12.05 (54bps) (12bps) (33bps) Sep-22 Mar-23 Net profit Dividend RWA Other Sep-23 On-market share buyback Sep-23 Pro forma CET1 Capital ratio (%) CAPITAL ABOVE TOP END OF TARGET OPERATING RANGE 1 Capital deduction and other movements including FX translation impacts. 1 26 Westpac Group 2023 Full Year Results Presentation & Investor Discussion Pack Credit RWA – Data refinement, 15bps Credit RWA – Credit quality & lending growth, (12bps) Non-credit RWA, 2bps |

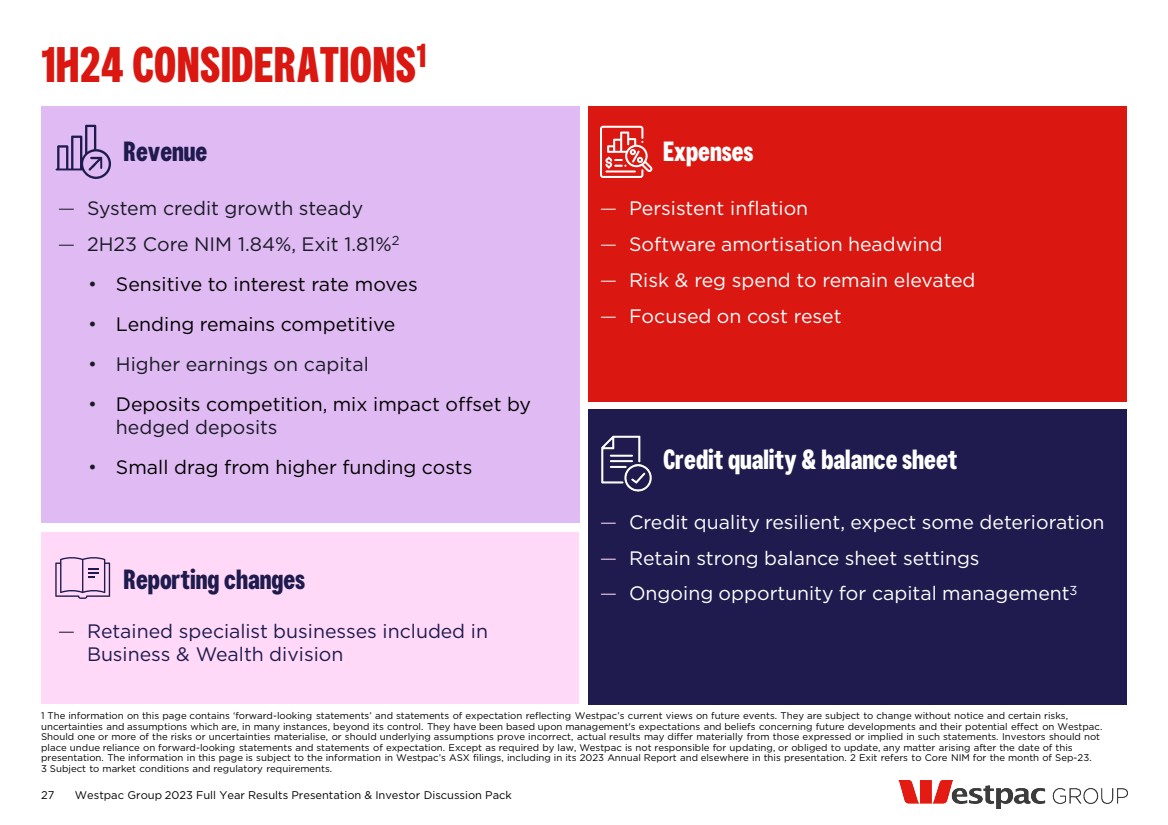

| 27 Westpac Group 2023 Full Year Results Presentation & Investor Discussion Pack 1 The information on this page contains ‘forward-looking statements’ and statements of expectation reflecting Westpac’s current views on future events. They are subject to change without notice and certain risks, uncertainties and assumptions which are, in many instances, beyond its control. They have been based upon management's expectations and beliefs concerning future developments and their potential effect on Westpac. Should one or more of the risks or uncertainties materialise, or should underlying assumptions prove incorrect, actual results may differ materially from those expressed or implied in such statements. Investors should not place undue reliance on forward-looking statements and statements of expectation. Except as required by law, Westpac is not responsible for updating, or obliged to update, any matter arising after the date of this presentation. The information in this page is subject to the information in Westpac’s ASX filings, including in its 2023 Annual Report and elsewhere in this presentation. 2 Exit refers to Core NIM for the month of Sep-23. 3 Subject to market conditions and regulatory requirements. 1H24 CONSIDERATIONS1 Revenue — System credit growth steady — 2H23 Core NIM 1.84%, Exit 1.81%2 • Sensitive to interest rate moves • Lending remains competitive • Higher earnings on capital • Deposits competition, mix impact offset by hedged deposits • Small drag from higher funding costs — Retained specialist businesses included in Business & Wealth division Reporting changes Credit quality & balance sheet — Credit quality resilient, expect some deterioration — Retain strong balance sheet settings — Ongoing opportunity for capital management3 Expenses — Persistent inflation — Software amortisation headwind — Risk & reg spend to remain elevated — Focused on cost reset |

| PETER KING Chief Executive Officer |

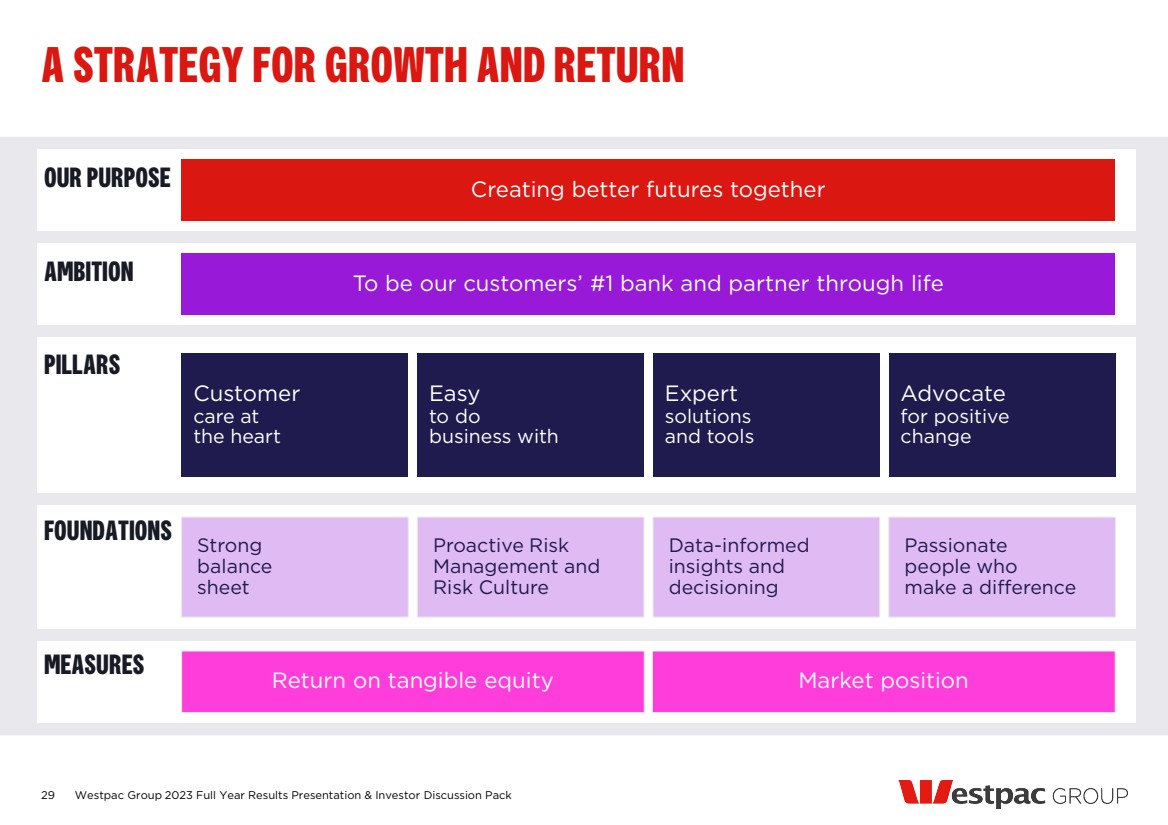

| 29 Westpac Group 2023 Full Year Results Presentation & Investor Discussion Pack A STRATEGY FOR GROWTH AND RETURN PILLARS Customer care at the heart Easy to do business with Expert solutions and tools Advocate for positive change FOUNDATIONS Strong balance sheet Proactive Risk Management and Risk Culture Data-informed insights and decisioning Passionate people who make a difference MEASURES Return on tangible equity Market position To be our customers’ #1 bank and partner through life AMBITION Creating better futures together OUR PURPOSE |

| 1 Refers to Australian banking system simplification. This page contains ‘forward looking statements’ and statements of expectation. Please refer to the disclaimer on page 134. ACCELERATING TECHNOLOGY SIMPLIFICATION1 EXPERIENCE PRODUCTS & SERVICES PLATFORMS ENTERPRISE TECHNOLOGY FOUNDATIONS Developer platforms Networks Private & Public cloud Desktop platforms Workflow systems Collections systems Data platforms Customer onboarding systems Customer masters Payment captures Product originations Product processors Staff platforms to assist customers Online customer platforms From >180 30 Westpac Group 2023 Full Year Results Presentation & Investor Discussion Pack >10 >60 >60 >20 >20 <5 <30 <20 <10 <10 To <60 |

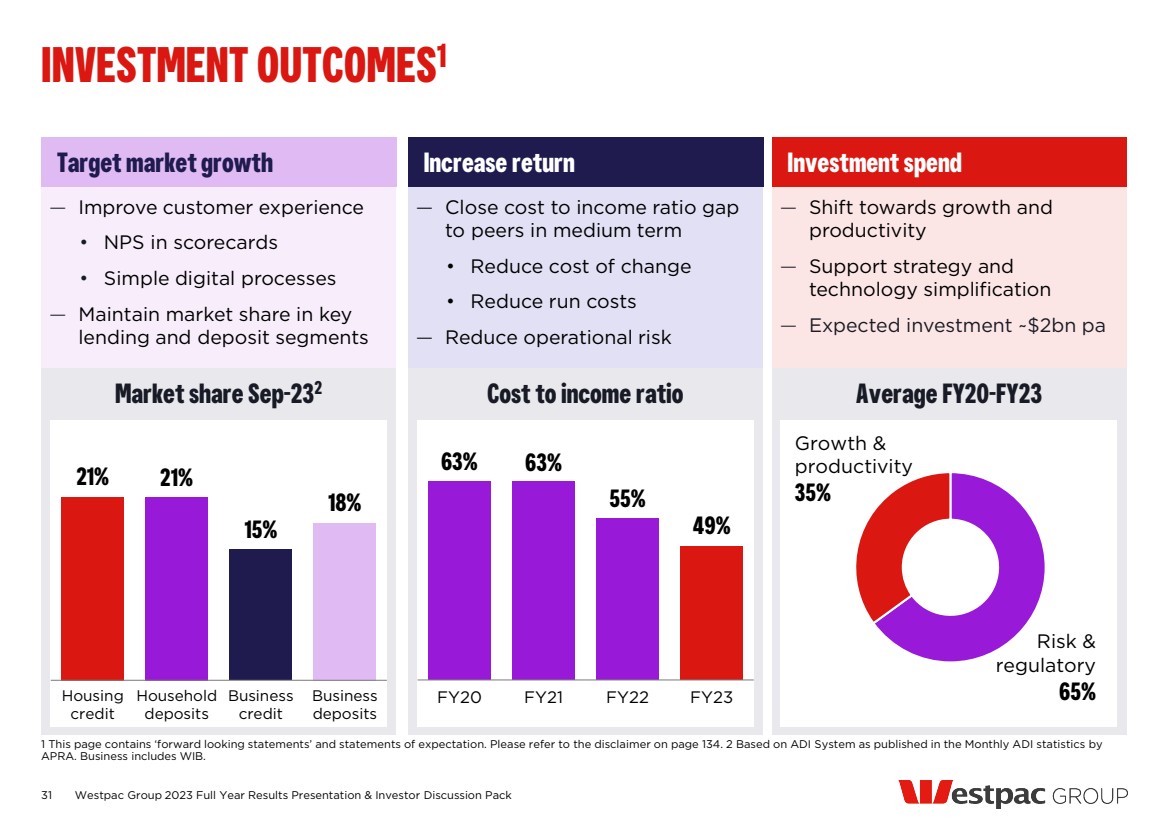

| — Improve customer experience • NPS in scorecards • Simple digital processes — Maintain market share in key lending and deposit segments — Close cost to income ratio gap to peers in medium term • Reduce cost of change • Reduce run costs — Reduce operational risk — Shift towards growth and productivity — Support strategy and technology simplification — Expected investment ~$2bn pa Market share Sep-232 31 1 This page contains ‘forward looking statements’ and statements of expectation. Please refer to the disclaimer on page 134. 2 Based on ADI System as published in the Monthly ADI statistics by APRA. Business includes WIB. INVESTMENT OUTCOMES1 Westpac Group 2023 Full Year Results Presentation & Investor Discussion Pack Cost to income ratio Average FY20-FY23 Target market growth Increase return Investment spend Growth & productivity 35% Risk & regulatory 65% 63% 63% 55% 49% FY20 FY21 FY22 FY23 21% 21% 15% 18% Housing credit Household deposits Business credit Business deposits |

| 32 Westpac Group 2023 Full Year Results Presentation & Investor Discussion Pack FY23 HIGHLIGHTS IMPROVED FINANCIAL RESULT BALANCE SHEET MOMENTUM ACCELERATING TECHNOLOGY SIMPLIFICATION STRENGTHENED CUSTOMER FRANCHISE COMPLETED PORTFOLIO SIMPLIFICATION |

| INVESTOR DISCUSSION PACK |

| OVERVIEW |

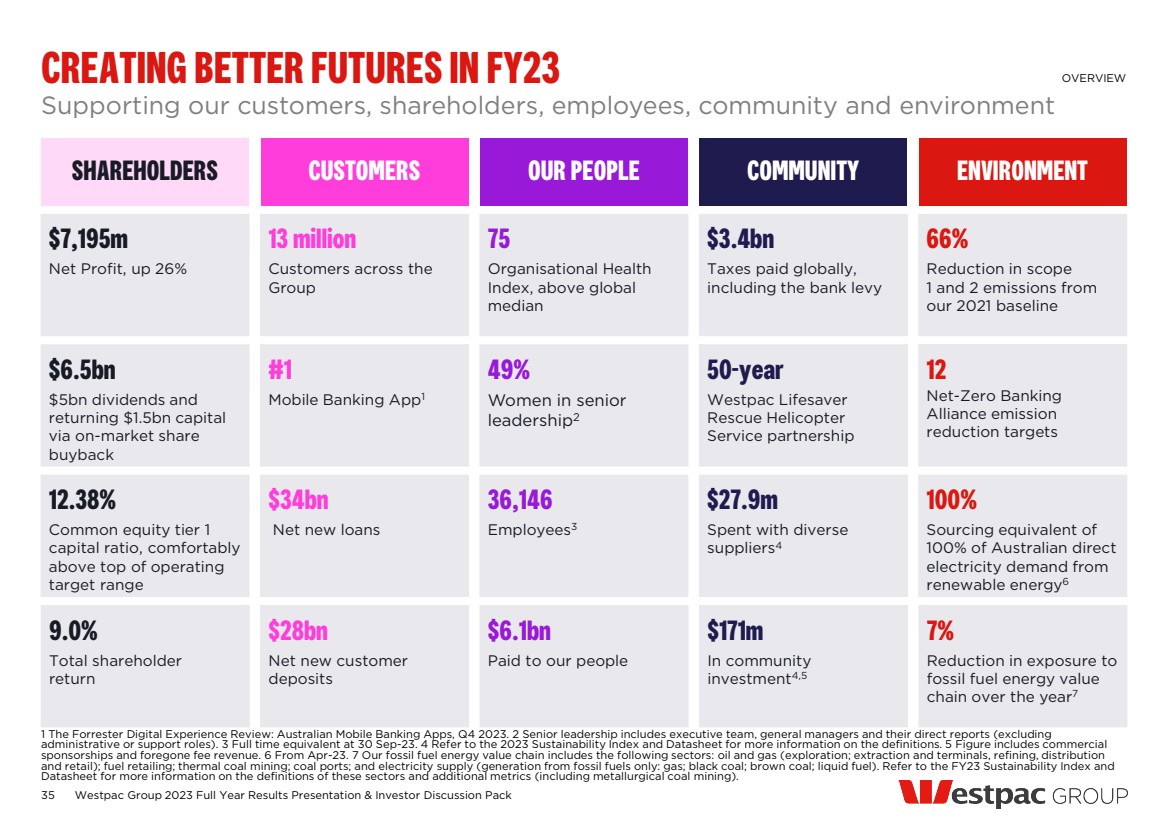

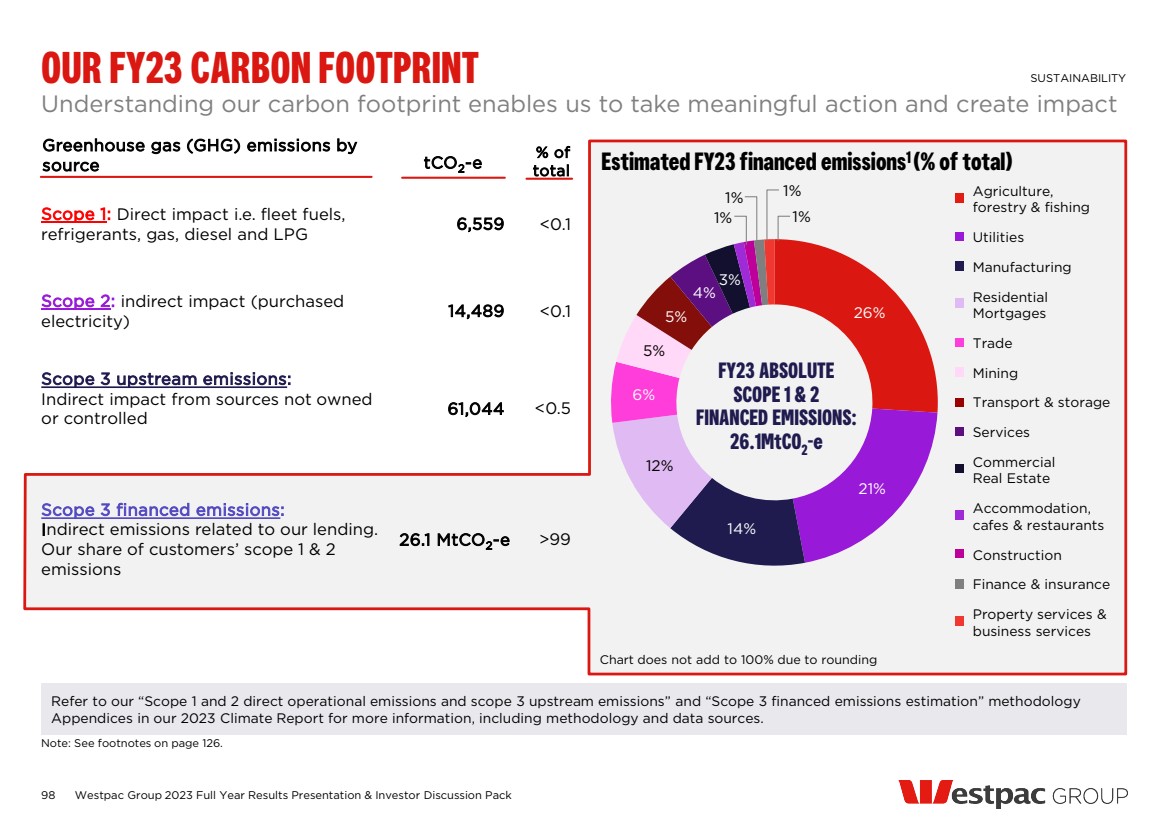

| 35 Supporting our customers, shareholders, employees, community and environment OVERVIEW 1 The Forrester Digital Experience Review: Australian Mobile Banking Apps, Q4 2023. 2 Senior leadership includes executive team, general managers and their direct reports (excluding administrative or support roles). 3 Full time equivalent at 30 Sep-23. 4 Refer to the 2023 Sustainability Index and Datasheet for more information on the definitions. 5 Figure includes commercial sponsorships and foregone fee revenue. 6 From Apr-23. 7 Our fossil fuel energy value chain includes the following sectors: oil and gas (exploration; extraction and terminals, refining, distribution and retail); fuel retailing; thermal coal mining; coal ports; and electricity supply (generation from fossil fuels only: gas; black coal; brown coal; liquid fuel). Refer to the FY23 Sustainability Index and Datasheet for more information on the definitions of these sectors and additional metrics (including metallurgical coal mining). CREATING BETTER FUTURES IN FY23 SHAREHOLDERS CUSTOMERS OUR PEOPLE COMMUNITY ENVIRONMENT $7,195m Net Profit, up 26% 13 million Customers across the Group 75 Organisational Health Index, above global median $3.4bn Taxes paid globally, including the bank levy 66% Reduction in scope 1 and 2 emissions from our 2021 baseline $6.5bn $5bn dividends and returning $1.5bn capital via on-market share buyback #1 Mobile Banking App1 49% Women in senior leadership2 50-year Westpac Lifesaver Rescue Helicopter Service partnership 12 Net-Zero Banking Alliance emission reduction targets 12.38% Common equity tier 1 capital ratio, comfortably above top of operating target range $34bn Net new loans 36,146 Employees3 $27.9m Spent with diverse suppliers4 100% Sourcing equivalent of 100% of Australian direct electricity demand from renewable energy6 9.0% Total shareholder return $28bn Net new customer deposits $6.1bn Paid to our people $171m In community investment4,5 7% Reduction in exposure to fossil fuel energy value chain over the year7 Westpac Group 2023 Full Year Results Presentation & Investor Discussion Pack |

| EARNINGS DRIVERS 2023 Full year financial results |

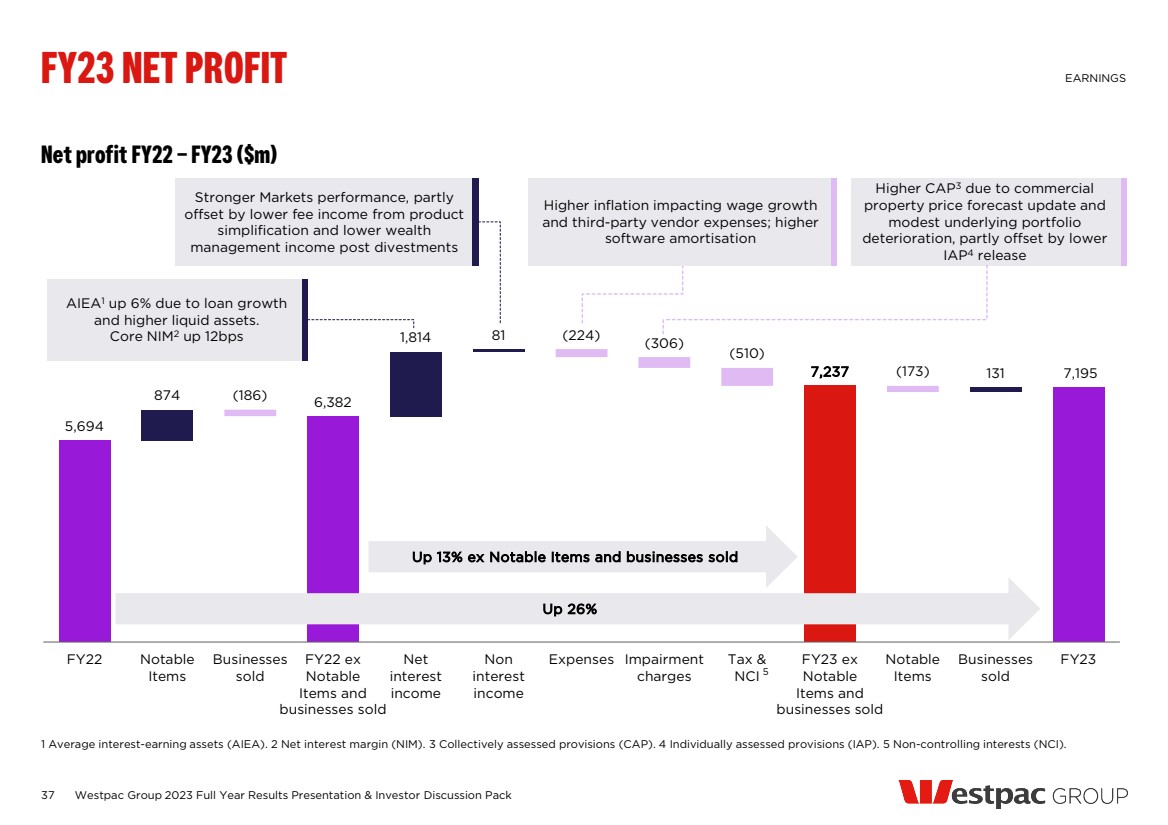

| 5,694 874 6,382 1,814 81 7,237 131 (186) (224) (306) (510) (173) 7,195 FY22 Notable Items Businesses sold FY22 ex Notable Items and businesses sold Net interest income Non interest income Expenses Impairment charges Tax & NCI FY23 ex Notable Items and businesses sold Notable Items Businesses sold FY23 37 Westpac Group 2023 Full Year Results Presentation & Investor Discussion Pack FY23 NET PROFIT EARNINGS 1 Average interest-earning assets (AIEA). 2 Net interest margin (NIM). 3 Collectively assessed provisions (CAP). 4 Individually assessed provisions (IAP). 5 Non-controlling interests (NCI). Up 26% Up 13% ex Notable Items and businesses sold 5 Net profit FY22 – FY23 ($m) AIEA1 up 6% due to loan growth and higher liquid assets. Core NIM2 up 12bps Stronger Markets performance, partly offset by lower fee income from product simplification and lower wealth management income post divestments Higher inflation impacting wage growth and third-party vendor expenses; higher software amortisation Higher CAP3 due to commercial property price forecast update and modest underlying portfolio deterioration, partly offset by lower IAP4 release |

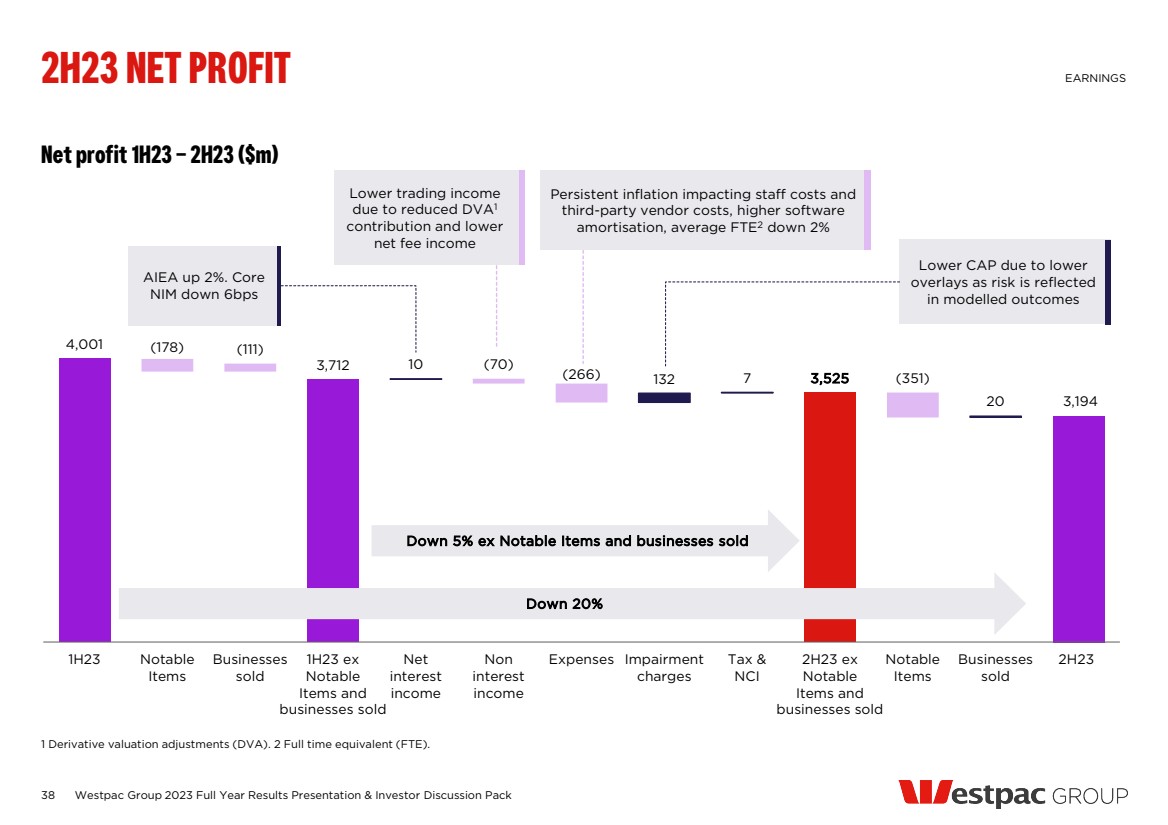

| 38 Westpac Group 2023 Full Year Results Presentation & Investor Discussion Pack Net profit 1H23 – 2H23 ($m) 2H23 NET PROFIT EARNINGS 1 Derivative valuation adjustments (DVA). 2 Full time equivalent (FTE). 4,001 3,712 10 132 7 3,525 20 (178) (111) (70) (266) (351) 3,194 1H23 Notable Items Businesses sold 1H23 ex Notable Items and businesses sold Net interest income Non interest income Expenses Impairment charges Tax & NCI 2H23 ex Notable Items and businesses sold Notable Items Businesses sold 2H23 Down 20% Down 5% ex Notable Items and businesses sold Lower trading income due to reduced DVA1 contribution and lower net fee income AIEA up 2%. Core NIM down 6bps Persistent inflation impacting staff costs and third-party vendor costs, higher software amortisation, average FTE2 down 2% Lower CAP due to lower overlays as risk is reflected in modelled outcomes |

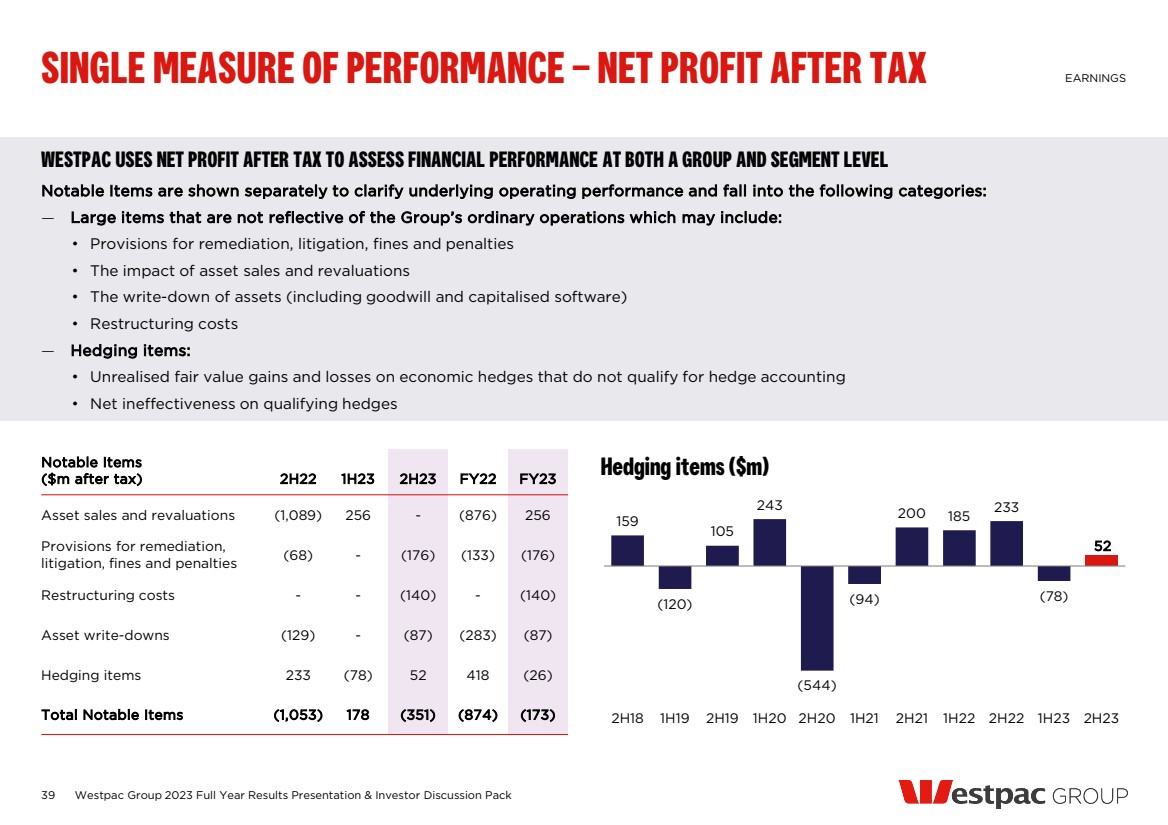

| 39 WESTPAC USES NET PROFIT AFTER TAX TO ASSESS FINANCIAL PERFORMANCE AT BOTH A GROUP AND SEGMENT LEVEL Notable Items are shown separately to clarify underlying operating performance and fall into the following categories: — Large items that are not reflective of the Group’s ordinary operations which may include: • Provisions for remediation, litigation, fines and penalties • The impact of asset sales and revaluations • The write-down of assets (including goodwill and capitalised software) • Restructuring costs — Hedging items: • Unrealised fair value gains and losses on economic hedges that do not qualify for hedge accounting • Net ineffectiveness on qualifying hedges Notable Items ($m after tax) 2H22 1H23 2H23 FY22 FY23 Asset sales and revaluations (1,089) 256 - (876) 256 Provisions for remediation, litigation, fines and penalties (68) - (176) (133) (176) Restructuring costs - - (140) - (140) Asset write-downs (129) - (87) (283) (87) Hedging items 233 (78) 52 418 (26) Total Notable Items (1,053) 178 (351) (874) (173) Hedging items ($m) Westpac Group 2023 Full Year Results Presentation & Investor Discussion Pack SINGLE MEASURE OF PERFORMANCE – NET PROFIT AFTER TAX EARNINGS 159 (120) 105 243 (544) (94) 200 185 233 (78) 52 2H18 1H19 2H19 1H20 2H20 1H21 2H21 1H22 2H22 1H23 2H23 |

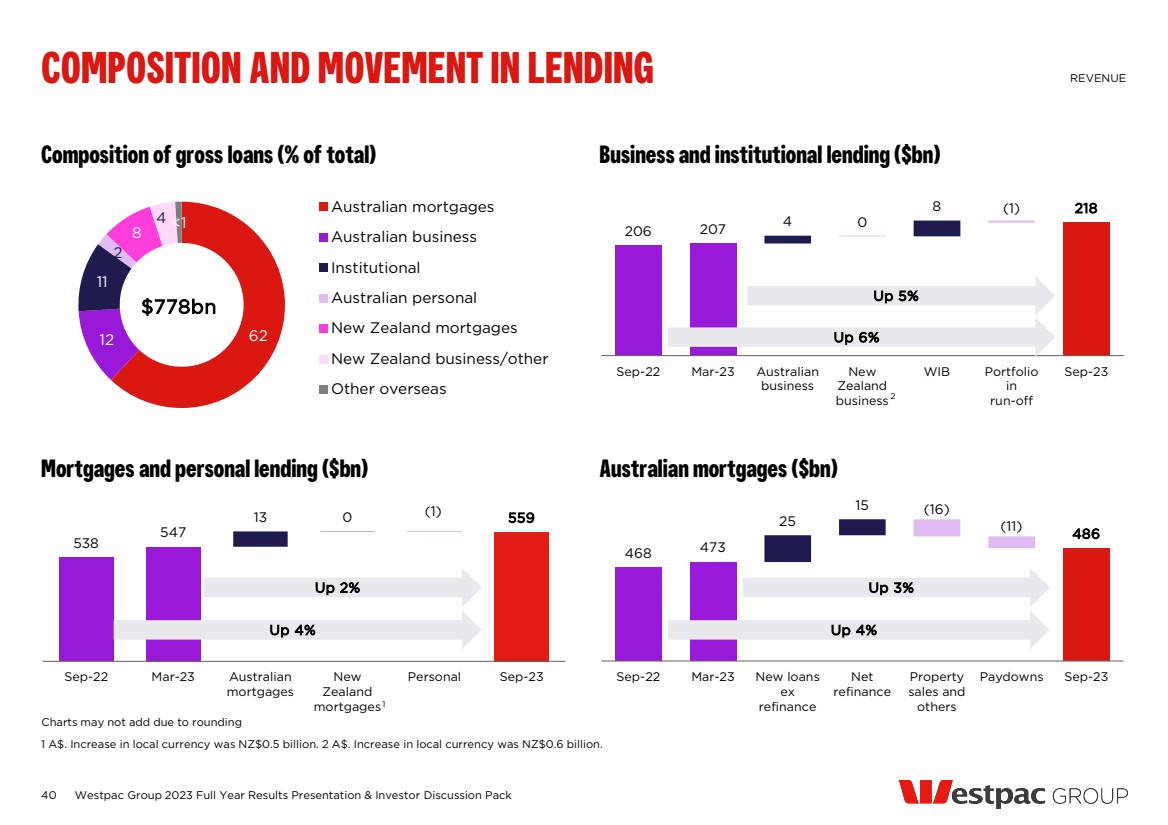

| 40 Composition of gross loans (% of total) 62 12 11 2 8 4 <1 Australian mortgages Australian business Institutional Australian personal New Zealand mortgages New Zealand business/other Other overseas Business and institutional lending ($bn) Mortgages and personal lending ($bn) Australian mortgages ($bn) Westpac Group 2023 Full Year Results Presentation & Investor Discussion Pack COMPOSITION AND MOVEMENT IN LENDING REVENUE 1 A$. Increase in local currency was NZ$0.5 billion. 2 A$. Increase in local currency was NZ$0.6 billion. $778bn 206 207 4 0 8 (1) 218 Sep-22 Mar-23 Australian business New Zealand business WIB Portfolio in run-off Sep-23 538 547 13 0 559 (1) Sep-22 Mar-23 Australian mortgages New Zealand mortgages Personal Sep-23 468 473 25 15 486 (16) (11) Sep-22 Mar-23 New loans ex refinance Net refinance Property sales and others Paydowns Sep-23 Up 6% Up 5% 2 Charts may not add due to rounding Up 4% Up 3% Up 4% Up 2% 1 |

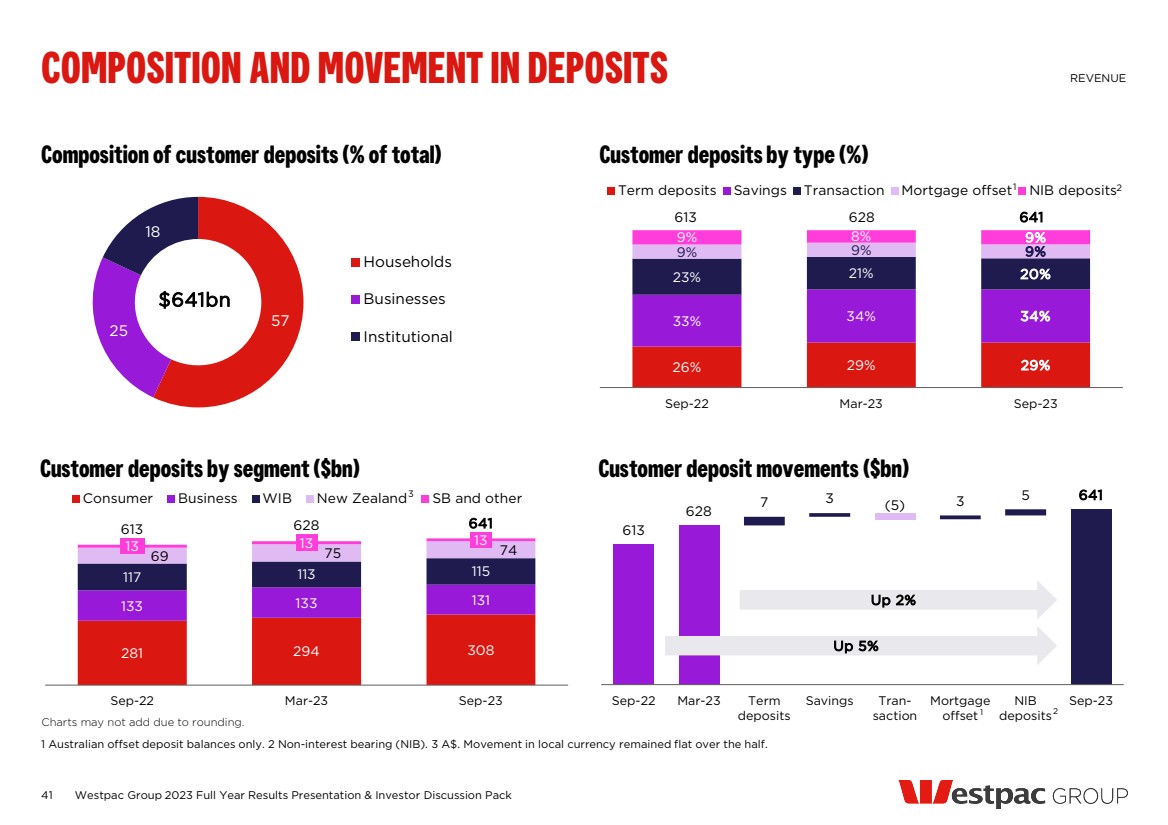

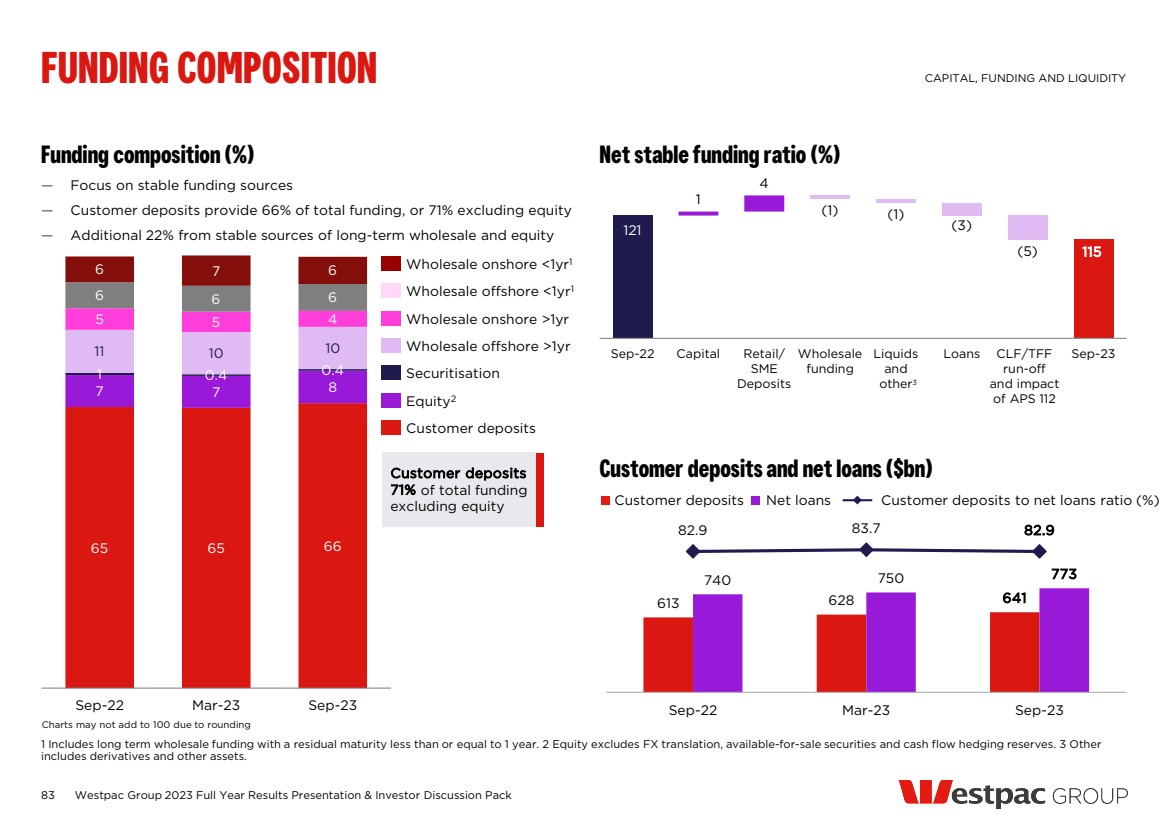

| 613 628 7 3 3 5 641 (5) Sep-22 Mar-23 Term deposits Savings Tran-saction Mortgage offset NIB deposits Sep-23 1 281 294 308 133 133 131 117 113 115 13 69 75 74 13 13 613 628 641 Sep-22 Mar-23 Sep-23 Consumer Business WIB New Zealand SB and other 41 Composition of customer deposits (% of total) 57 25 18 Households Businesses Institutional Customer deposits by type (%) 26% 29% 29% 33% 34% 34% 23% 21% 20% 9% 9% 9% 9% 8% 9% Sep-22 Mar-23 Sep-23 Term deposits Savings Transaction Mortgage offset NIB deposits Customer deposits by segment ($bn) Customer deposit movements ($bn) Westpac Group 2023 Full Year Results Presentation & Investor Discussion Pack COMPOSITION AND MOVEMENT IN DEPOSITS REVENUE 1 Australian offset deposit balances only. 2 Non-interest bearing (NIB). 3 A$. Movement in local currency remained flat over the half. $641bn Charts may not add due to rounding. 1 2 3 Up 5% Up 2% 2 613 628 641 |

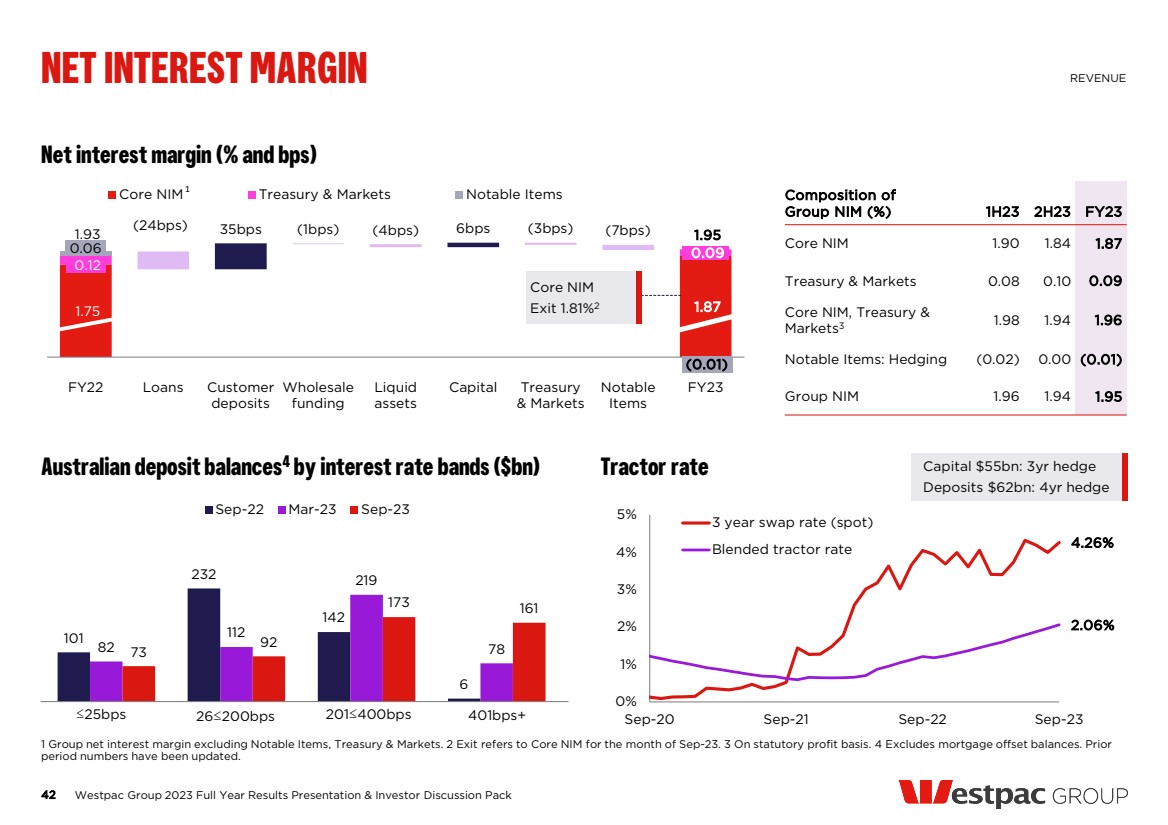

| 1.75 1.87 0.12 0.06 0.09 (0.01) 1.93 35bps 6bps 1.95 (24bps) (1bps) (4bps) (3bps) (7bps) FY22 Loans Customer deposits Wholesale funding Liquid assets Capital Treasury & Markets Notable Items FY23 Core NIM Treasury & Markets Notable Items Composition of Group NIM (%) 1H23 2H23 FY23 Core NIM 1.90 1.84 1.87 Treasury & Markets 0.08 0.10 0.09 Core NIM, Treasury & Markets3 1.98 1.94 1.96 Notable Items: Hedging (0.02) 0.00 (0.01) Group NIM 1.96 1.94 1.95 42 Net interest margin (% and bps) Australian deposit balances4 by interest rate bands ($bn) 101 232 142 6 82 112 219 73 78 92 173 161 Sep-22 Mar-23 Sep-23 Tractor rate Westpac Group 2023 Full Year Results Presentation & Investor Discussion Pack NET INTEREST MARGIN REVENUE 1 Group net interest margin excluding Notable Items, Treasury & Markets. 2 Exit refers to Core NIM for the month of Sep-23. 3 On statutory profit basis. 4 Excludes mortgage offset balances. Prior period numbers have been updated. 42 Capital $55bn: 3yr hedge Deposits $62bn: 4yr hedge 1 4.26% 2.06% 0% 1% 2% 3% 4% 5% Sep-20 Sep-21 Sep-22 Sep-23 3 year swap rate (spot) Blended tractor rate ≤25bps 26≤200bps 201≤400bps 401bps+ Core NIM Exit 1.81%2 |

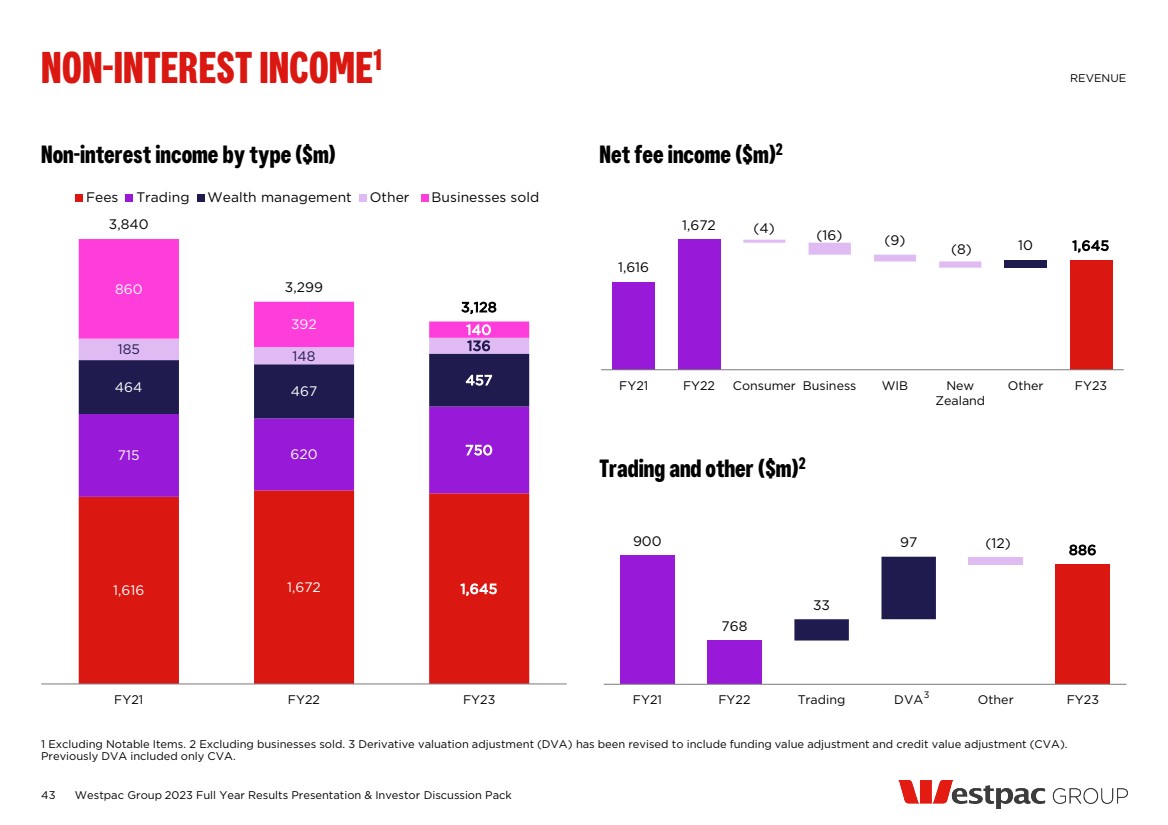

| 43 1,616 1,672 1,645 715 620 750 464 467 457 185 148 136 860 392 140 3,840 3,299 3,128 FY21 FY22 FY23 Fees Trading Wealth management Other Businesses sold Net fee income ($m)2 1,616 1,672 10 1,645 (4) (16) (9) (8) FY21 FY22 Consumer Business WIB New Zealand Other FY23 Trading and other ($m)2 900 768 33 97 886 (12) FY21 FY22 Trading DVA Other FY23 Non-interest income by type ($m) Westpac Group 2023 Full Year Results Presentation & Investor Discussion Pack NON-INTEREST INCOME1 REVENUE 1 Excluding Notable Items. 2 Excluding businesses sold. 3 Derivative valuation adjustment (DVA) has been revised to include funding value adjustment and credit value adjustment (CVA). Previously DVA included only CVA. 3 |

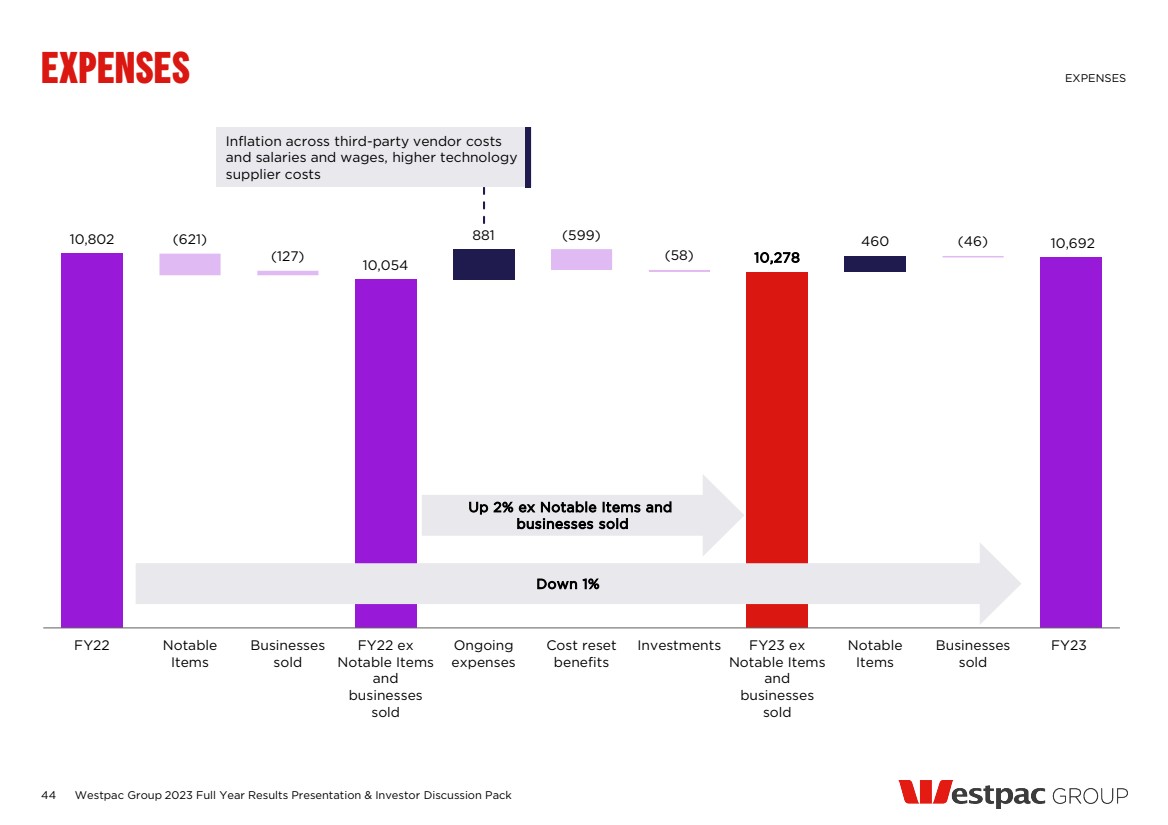

| 44 Westpac Group 2023 Full Year Results Presentation & Investor Discussion Pack EXPENSES EXPENSES 10,802 10,054 881 10,278 (621) 460 (127) (599) (58) (46) 10,692 FY22 Notable Items Businesses sold FY22 ex Notable Items and businesses sold Ongoing expenses Cost reset benefits Investments FY23 ex Notable Items and businesses sold Notable Items Businesses sold FY23 Down 1% Up 2% ex Notable Items and businesses sold Inflation across third-party vendor costs and salaries and wages, higher technology supplier costs |

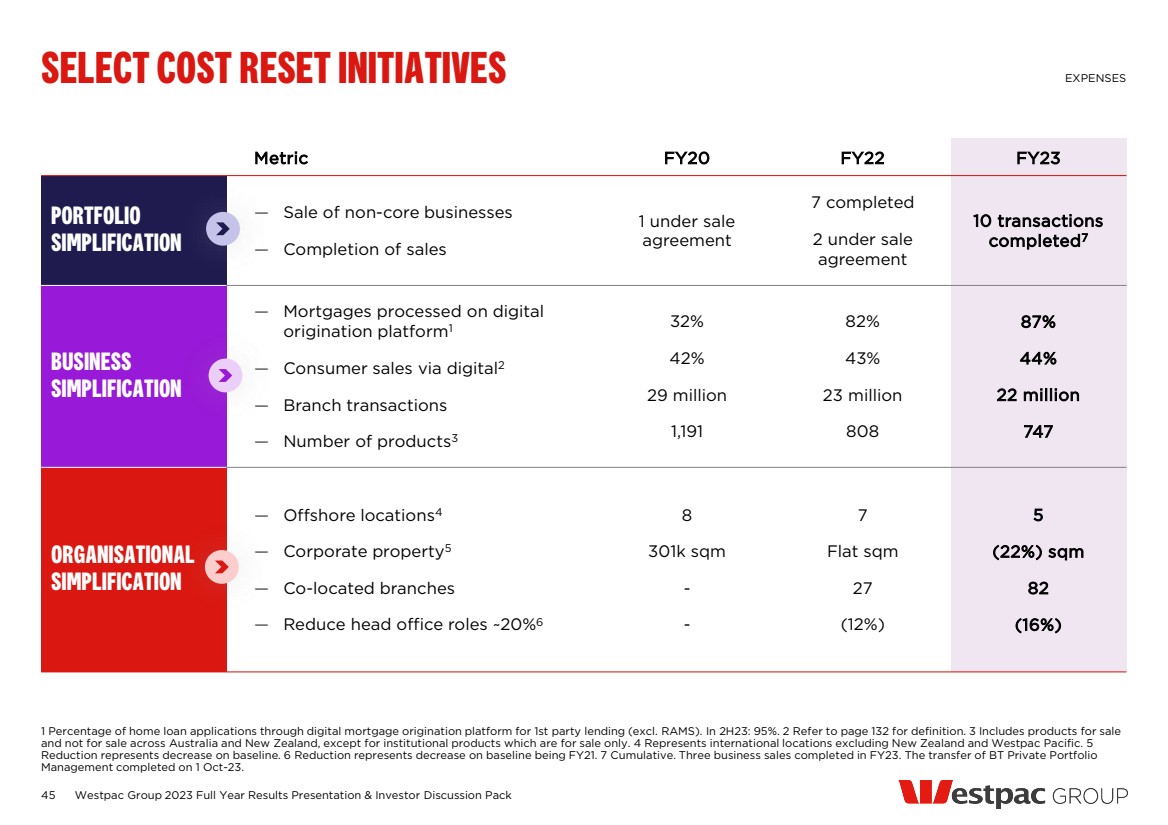

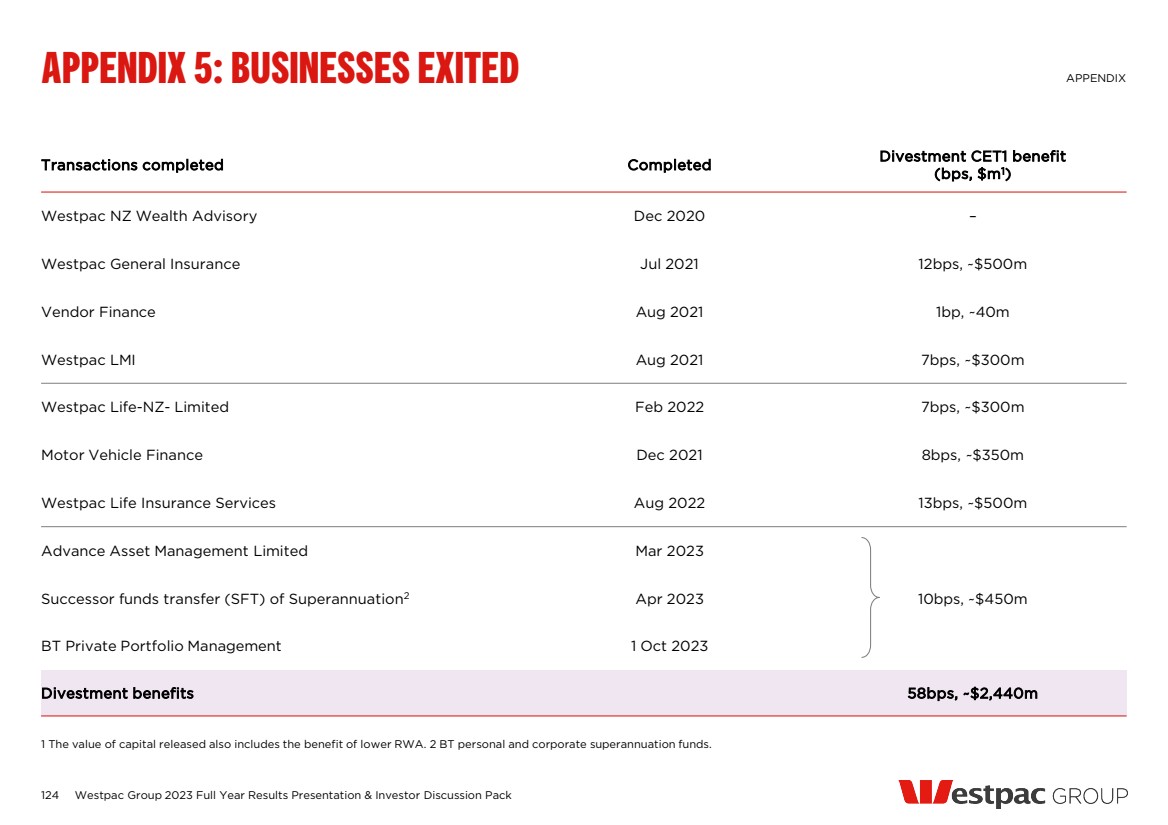

| Metric FY20 FY22 FY23 PORTFOLIO SIMPLIFICATION — Sale of non-core businesses — Completion of sales 1 under sale agreement 7 completed 2 under sale agreement 10 transactions completed7 BUSINESS SIMPLIFICATION — Mortgages processed on digital origination platform1 — Consumer sales via digital2 — Branch transactions — Number of products3 32% 42% 29 million 1,191 82% 43% 23 million 808 87% 44% 22 million 747 ORGANISATIONAL SIMPLIFICATION — Offshore locations4 — Corporate property5 — Co-located branches — Reduce head office roles ~20%6 8 301k sqm - - 7 Flat sqm 27 (12%) 5 (22%) sqm 82 (16%) 45 SELECT COST RESET INITIATIVES EXPENSES 1 Percentage of home loan applications through digital mortgage origination platform for 1st party lending (excl. RAMS). In 2H23: 95%. 2 Refer to page 132 for definition. 3 Includes products for sale and not for sale across Australia and New Zealand, except for institutional products which are for sale only. 4 Represents international locations excluding New Zealand and Westpac Pacific. 5 Reduction represents decrease on baseline. 6 Reduction represents decrease on baseline being FY21. 7 Cumulative. Three business sales completed in FY23. The transfer of BT Private Portfolio Management completed on 1 Oct-23. Westpac Group 2023 Full Year Results Presentation & Investor Discussion Pack |

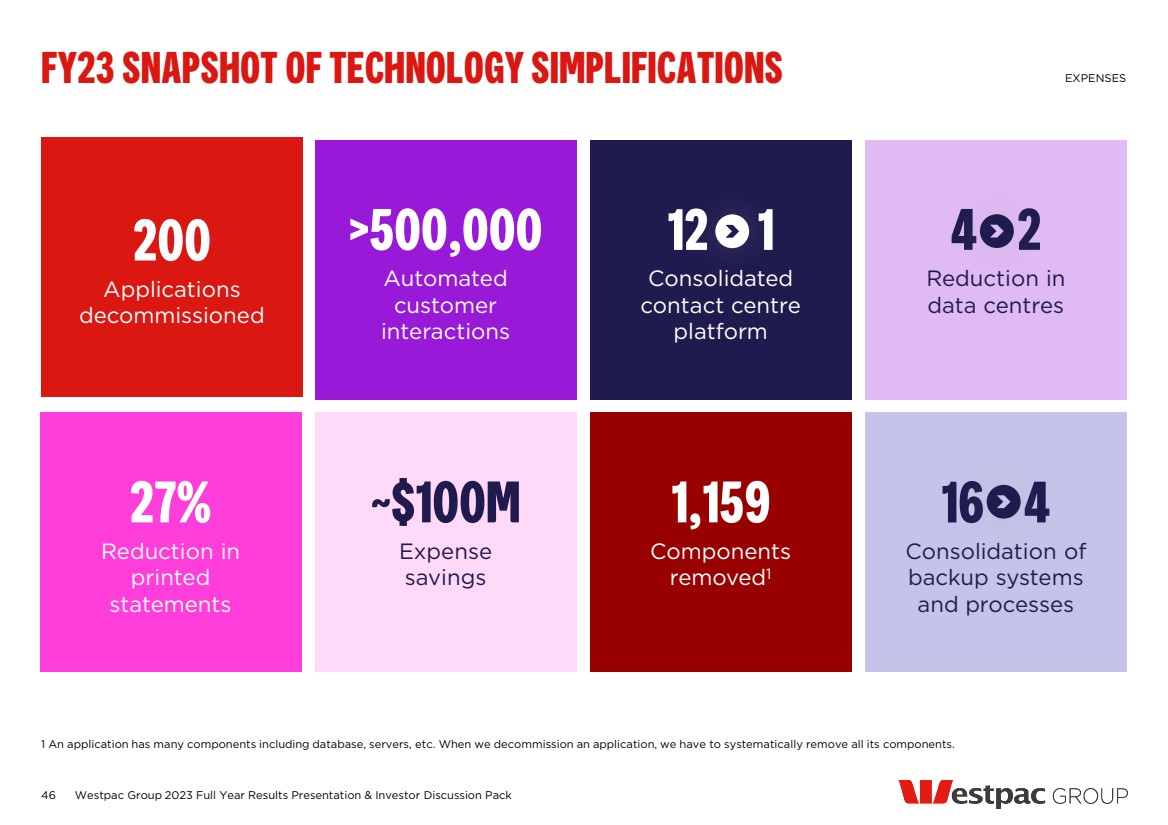

| 46 Westpac Group 2023 Full Year Results Presentation & Investor Discussion Pack FY23 SNAPSHOT OF TECHNOLOGY SIMPLIFICATIONS EXPENSES 1 An application has many components including database, servers, etc. When we decommission an application, we have to systematically remove all its components. ~$100M Expense savings >500,000 Automated customer interactions 1,159 Components removed1 12 1 Consolidated contact centre platform 200 Applications decommissioned 27% Reduction in printed statements 4 2 Reduction in data centres 16 4 Consolidation of backup systems and processes |

| Impairment charges ($m) 47 Impairment charges and stressed exposures (bps) 2H23 IMPAIRMENT CHARGE OF $258M IMPAIRMENT CHARGES 123 76 121 (138) (214) (104) 228 218 222 (17) 310 19 196 390 258 2H22 1H23 2H23 2H22 1H23 2H23 2H22 1H23 2H23 2H22 1H23 2H23 2H22 1H23 2H23 9 126 -50 50 150 250 350 -20 0 20 40 60 80 100 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 Impairment charge to average loans annualised (lhs) Stressed exposures to TCE (rhs) New IAPs Write-backs & recoveries Write-offs direct Other mvmts in CAP Individually assessed Collectively assessed Total Westpac Group 2023 Full Year Results Presentation & Investor Discussion Pack |

| CREDIT QUALITY AND PROVISIONS 2023 Full year financial results |

| 611 832 452 382 351 1,561 1,131 947 1,011 1,061 2,249 1,606 1,691 1,980 2,405 1,034 791 845 830 692 708 647 700 720 432 6,163 5,007 4,635 4,923 4,941 Sep-20 Sep-21 Sep-22 Mar-23 Sep-23 Overlay Stage 1 CAP Stage 2 CAP Stage 3 CAP Stage 3 IAP 4,941 3,420 6,860 Reported probability-weighted ECL 100% base case ECL 100% downside ECL PROVISIONS FOR EXPECTED CREDIT LOSS 49 Total provisions for expected credit losses1 ($m) Expected credit loss (ECL) ($m) Westpac Group 2023 Full Year Results Presentation & Investor Discussion Pack CREDIT QUALITY 1 Includes provisions for debt securities. 2 Forecast date is 18 September 2023. 3 These key economic indicators represent trough or peak values that characterise the scenarios considered in setting downside severity. Residential and commercial forecasts represent cumulative reduction over a two-year period. Forecasts for base case ECL2 Base case Downside 2023 2024 Trough / peak3 GDP growth 1.2% 1.6% (6%) Unemployment 3.9% 4.7% 11% Residential property prices 5.8% 4.0% (27%) Commercial property prices (15.0%) (0.5%) (32%) COVID-19 Reduction of overlays for mortgages, construction and NZ weather events risks, now reflected in modelled provisions Single name write-off in WIB $1.5bn in provisions above the base case ECL — Modest downgrades to watchlist & substandard — Forward looking economics, mostly commercial property prices and interest rates — Increased early cycle mortgage delinquencies |

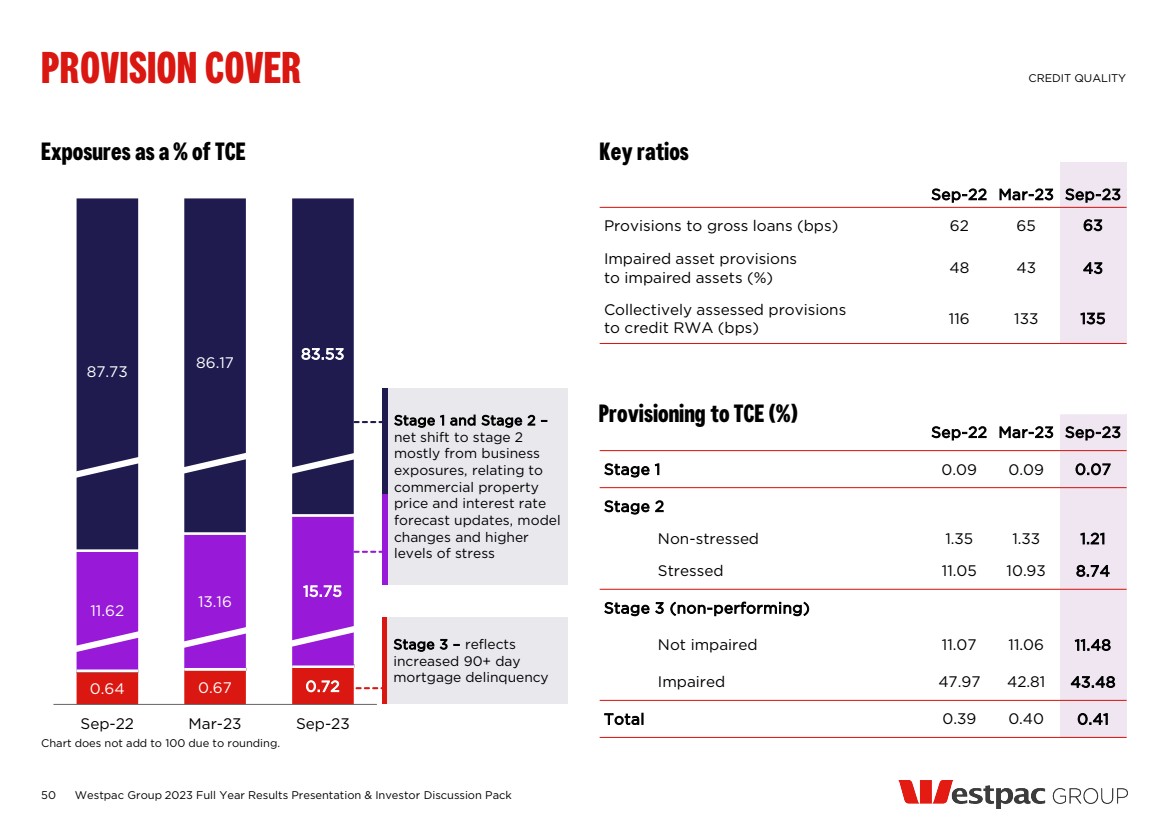

| Sep-22 Mar-23 Sep-23 Provisions to gross loans (bps) 62 65 63 Impaired asset provisions to impaired assets (%) 48 43 43 Collectively assessed provisions to credit RWA (bps) 116 133 135 0.64 0.67 0.72 11.62 13.16 15.75 87.73 86.17 83.53 Sep-22 Mar-23 Sep-23 50 Exposures as a % of TCE Key ratios Westpac Group 2023 Full Year Results Presentation & Investor Discussion Pack PROVISION COVER CREDIT QUALITY Chart does not add to 100 due to rounding. Provisioning to TCE (%) Stage 3 – reflects increased 90+ day mortgage delinquency Stage 1 and Stage 2 – net shift to stage 2 mostly from business exposures, relating to commercial property price and interest rate forecast updates, model changes and higher levels of stress Sep-22 Mar-23 Sep-23 Stage 1 0.09 0.09 0.07 Stage 2 Non-stressed 1.35 1.33 1.21 Stressed 11.05 10.93 8.74 Stage 3 (non-performing) Not impaired 11.07 11.06 11.48 Impaired 47.97 42.81 43.48 Total 0.39 0.40 0.41 |

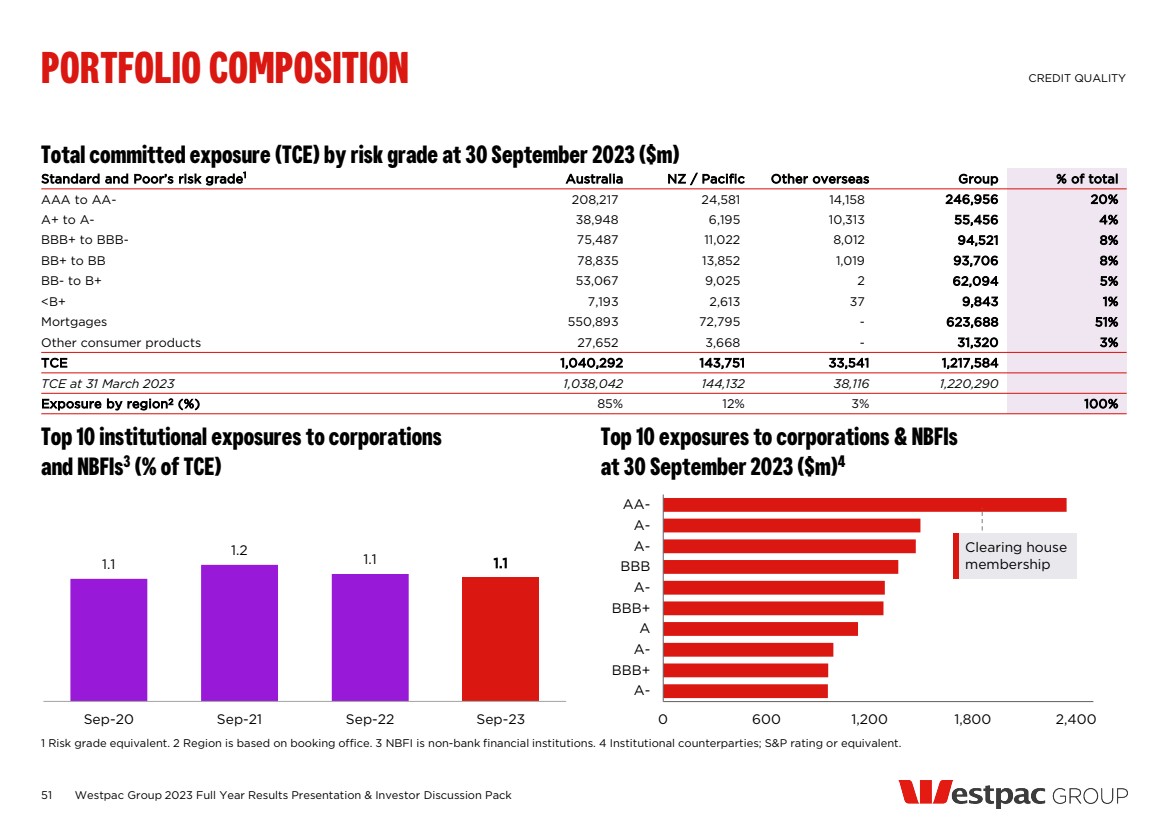

| 51 Total committed exposure (TCE) by risk grade at 30 September 2023 ($m) Top 10 institutional exposures to corporations and NBFIs3 (% of TCE) 1.1 1.2 1.1 1.1 Sep-20 Sep-21 Sep-22 Sep-23 Top 10 exposures to corporations & NBFIs at 30 September 2023 ($m)4 0 600 1,200 1,800 2,400 A-BBB+ A-A BBB+ A-BBB A-A-AA-Westpac Group 2023 Full Year Results Presentation & Investor Discussion Pack PORTFOLIO COMPOSITION CREDIT QUALITY 1 Risk grade equivalent. 2 Region is based on booking office. 3 NBFI is non-bank financial institutions. 4 Institutional counterparties; S&P rating or equivalent. Standard and Poor’s risk grade1 Australia NZ / Pacific Other overseas Group % of total AAA to AA- 208,217 24,581 14,158 246,956 20% A+ to A- 38,948 6,195 10,313 55,456 4% BBB+ to BBB- 75,487 11,022 8,012 94,521 8% BB+ to BB 78,835 13,852 1,019 93,706 8% BB- to B+ 53,067 9,025 2 62,094 5% <B+ 7,193 2,613 37 9,843 1% Mortgages 550,893 72,795 - 623,688 51% Other consumer products 27,652 3,668 - 31,320 3% TCE 1,040,292 143,751 33,541 1,217,584 TCE at 31 March 2023 1,038,042 144,132 38,116 1,220,290 Exposure by region2 (%) 85% 12% 3% 100% Clearing house membership |

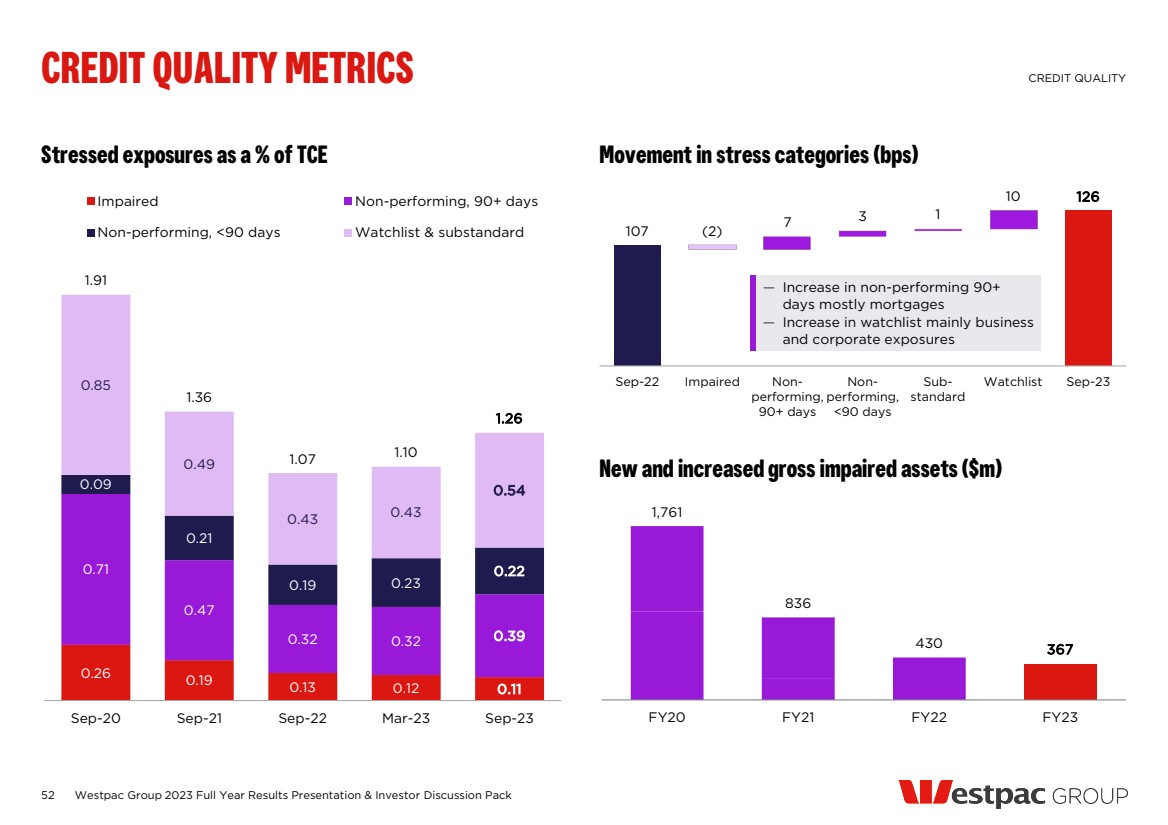

| 107 7 3 1 10 126 (2) Sep-22 Impaired Non-performing, 90+ days Non-performing, <90 days Sub-standard Watchlist Sep-23 Movement in stress categories (bps) 52 New and increased gross impaired assets ($m) 1,761 836 430 367 FY20 FY21 FY22 FY23 Stressed exposures as a % of TCE Westpac Group 2023 Full Year Results Presentation & Investor Discussion Pack CREDIT QUALITY METRICS CREDIT QUALITY — Increase in non-performing 90+ days mostly mortgages — Increase in watchlist mainly business and corporate exposures 0.26 0.19 0.13 0.12 0.11 0.71 0.47 0.32 0.32 0.39 0.09 0.21 0.19 0.23 0.22 0.85 0.49 0.43 0.43 0.54 1.91 1.36 1.07 1.10 1.26 Sep-20 Sep-21 Sep-22 Mar-23 Sep-23 Impaired Non-performing, 90+ days Non-performing, <90 days Watchlist & substandard |

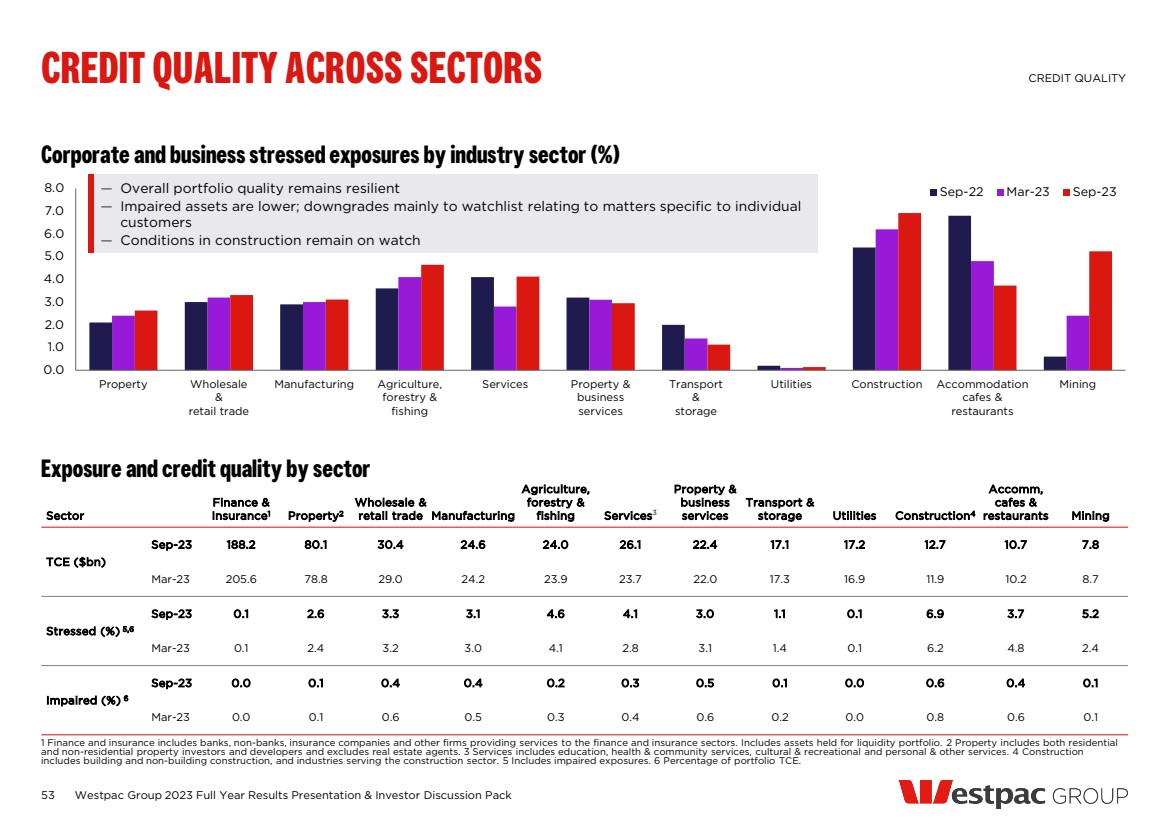

| Corporate and business stressed exposures by industry sector (%) 0.0 1.0 2.0 3.0 4.0 5.0 6.0 7.0 8.0 Property Wholesale & retail trade Manufacturing Agriculture, forestry & fishing Services Property & business services Transport & storage Utilities Construction Accommodation cafes & restaurants Mining Sep-22 Mar-23 Sep-23 53 Exposure and credit quality by sector Sector Finance & Insurance1 Property2 Wholesale & retail trade Manufacturing Agriculture, forestry & fishing Services3 Property & business services Transport & storage Utilities Construction4 Accomm, cafes & restaurants Mining TCE ($bn) Sep-23 188.2 80.1 30.4 24.6 24.0 26.1 22.4 17.1 17.2 12.7 10.7 7.8 Mar-23 205.6 78.8 29.0 24.2 23.9 23.7 22.0 17.3 16.9 11.9 10.2 8.7 Stressed (%) 5,6 Sep-23 0.1 2.6 3.3 3.1 4.6 4.1 3.0 1.1 0.1 6.9 3.7 5.2 Mar-23 0.1 2.4 3.2 3.0 4.1 2.8 3.1 1.4 0.1 6.2 4.8 2.4 Impaired (%) 6 Sep-23 0.0 0.1 0.4 0.4 0.2 0.3 0.5 0.1 0.0 0.6 0.4 0.1 Mar-23 0.0 0.1 0.6 0.5 0.3 0.4 0.6 0.2 0.0 0.8 0.6 0.1 Westpac Group 2023 Full Year Results Presentation & Investor Discussion Pack CREDIT QUALITY ACROSS SECTORS CREDIT QUALITY 1 Finance and insurance includes banks, non-banks, insurance companies and other firms providing services to the finance and insurance sectors. Includes assets held for liquidity portfolio. 2 Property includes both residential and non-residential property investors and developers and excludes real estate agents. 3 Services includes education, health & community services, cultural & recreational and personal & other services. 4 Construction includes building and non-building construction, and industries serving the construction sector. 5 Includes impaired exposures. 6 Percentage of portfolio TCE. — Overall portfolio quality remains resilient — Impaired assets are lower; downgrades mainly to watchlist relating to matters specific to individual customers — Conditions in construction remain on watch |

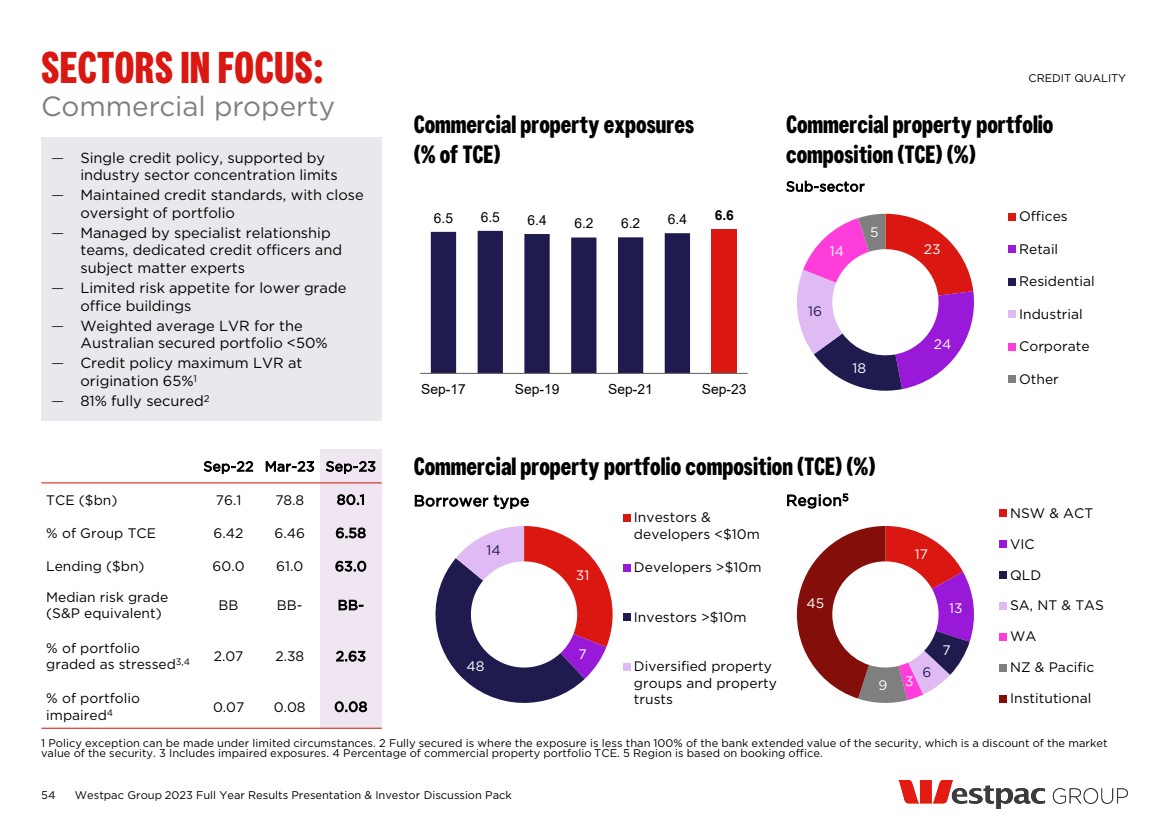

| — Single credit policy, supported by industry sector concentration limits — Maintained credit standards, with close oversight of portfolio — Managed by specialist relationship teams, dedicated credit officers and subject matter experts — Limited risk appetite for lower grade office buildings — Weighted average LVR for the Australian secured portfolio <50% — Credit policy maximum LVR at origination 65%1 — 81% fully secured2 54 Sep-22 Mar-23 Sep-23 TCE ($bn) 76.1 78.8 80.1 % of Group TCE 6.42 6.46 6.58 Lending ($bn) 60.0 61.0 63.0 Median risk grade (S&P equivalent) BB BB- BB- % of portfolio graded as stressed3,4 2.07 2.38 2.63 % of portfolio impaired4 0.07 0.08 0.08 Commercial property portfolio composition (TCE) (%) Commercial property exposures (% of TCE) Commercial property portfolio composition (TCE) (%) Westpac Group 2023 Full Year Results Presentation & Investor Discussion Pack SECTORS IN FOCUS: CREDIT QUALITY 1 Policy exception can be made under limited circumstances. 2 Fully secured is where the exposure is less than 100% of the bank extended value of the security, which is a discount of the market value of the security. 3 Includes impaired exposures. 4 Percentage of commercial property portfolio TCE. 5 Region is based on booking office. Commercial property 23 24 18 16 14 5 Offices Retail Residential Industrial Corporate Other 6.5 6.5 6.4 6.2 6.2 6.4 6.6 Sep-17 Sep-19 Sep-21 Sep-23 Sub-sector Borrower type Region5 17 13 7 6 9 3 45 NSW & ACT VIC QLD SA, NT & TAS WA NZ & Pacific Institutional 31 7 48 14 Investors & developers <$10m Developers >$10m Investors >$10m Diversified property groups and property trusts |

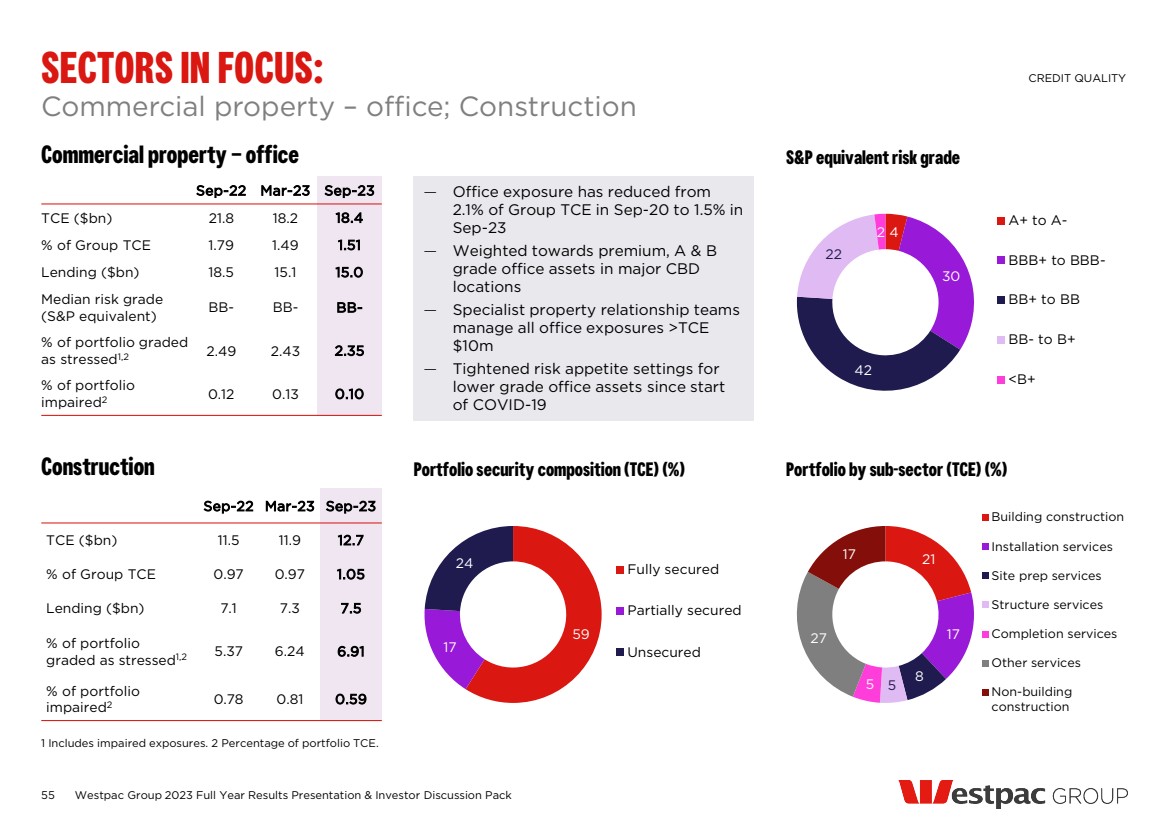

| 55 Construction Portfolio security composition (TCE) (%) Portfolio by sub-sector (TCE) (%) Commercial property – office — Office exposure has reduced from 2.1% of Group TCE in Sep-20 to 1.5% in Sep-23 — Weighted towards premium, A & B grade office assets in major CBD locations — Specialist property relationship teams manage all office exposures >TCE $10m — Tightened risk appetite settings for lower grade office assets since start of COVID-19 S&P equivalent risk grade Commercial property – office; Construction Westpac Group 2023 Full Year Results Presentation & Investor Discussion Pack SECTORS IN FOCUS: CREDIT QUALITY 1 Includes impaired exposures. 2 Percentage of portfolio TCE. Sep-22 Mar-23 Sep-23 TCE ($bn) 21.8 18.2 18.4 % of Group TCE 1.79 1.49 1.51 Lending ($bn) 18.5 15.1 15.0 Median risk grade (S&P equivalent) BB- BB- BB- % of portfolio graded as stressed1,2 2.49 2.43 2.35 % of portfolio impaired2 0.12 0.13 0.10 4 30 42 22 2 A+ to A-BBB+ to BBB-BB+ to BB BB- to B+ <B+ 59 17 24 Fully secured Partially secured Unsecured Sep-22 Mar-23 Sep-23 TCE ($bn) 11.5 11.9 12.7 % of Group TCE 0.97 0.97 1.05 Lending ($bn) 7.1 7.3 7.5 % of portfolio graded as stressed1,2 5.37 6.24 6.91 % of portfolio impaired2 0.78 0.81 0.59 21 17 8 5 5 27 17 Building construction Installation services Site prep services Structure services Completion services Other services Non-building construction |

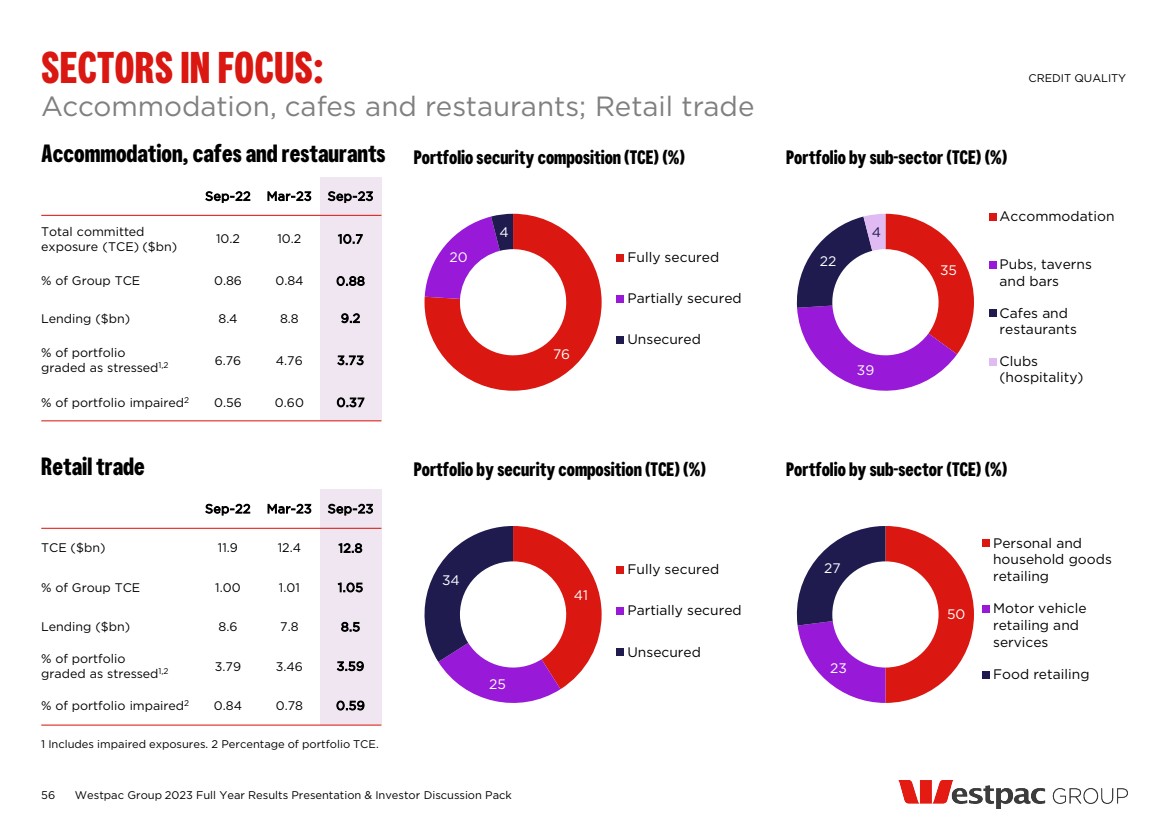

| 56 Retail trade Sep-22 Mar-23 Sep-23 TCE ($bn) 11.9 12.4 12.8 % of Group TCE 1.00 1.01 1.05 Lending ($bn) 8.6 7.8 8.5 % of portfolio graded as stressed1,2 3.79 3.46 3.59 % of portfolio impaired2 0.84 0.78 0.59 Portfolio by security composition (TCE) (%) 41 25 34 Fully secured Partially secured Unsecured Portfolio by sub-sector (TCE) (%) 50 23 27 Personal and household goods retailing Motor vehicle retailing and services Food retailing Accommodation, cafes and restaurants Sep-22 Mar-23 Sep-23 Total committed exposure (TCE) ($bn) 10.2 10.2 10.7 % of Group TCE 0.86 0.84 0.88 Lending ($bn) 8.4 8.8 9.2 % of portfolio graded as stressed1,2 6.76 4.76 3.73 % of portfolio impaired2 0.56 0.60 0.37 Portfolio security composition (TCE) (%) 76 20 4 Fully secured Partially secured Unsecured Portfolio by sub-sector (TCE) (%) 35 39 22 4 Accommodation Pubs, taverns and bars Cafes and restaurants Clubs (hospitality) Accommodation, cafes and restaurants; Retail trade Westpac Group 2023 Full Year Results Presentation & Investor Discussion Pack SECTORS IN FOCUS: CREDIT QUALITY 1 Includes impaired exposures. 2 Percentage of portfolio TCE. |

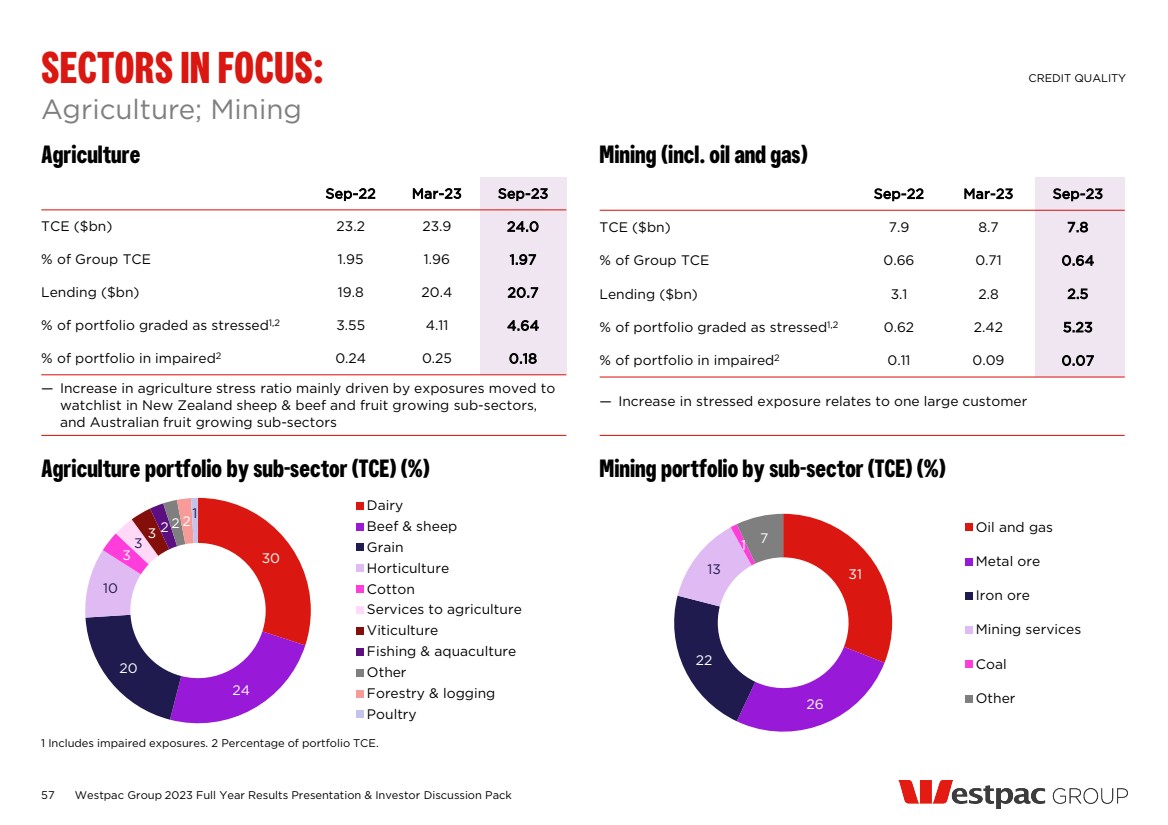

| Agriculture Mining (incl. oil and gas) Agriculture portfolio by sub-sector (TCE) (%) Mining portfolio by sub-sector (TCE) (%) Agriculture; Mining SECTORS IN FOCUS: CREDIT QUALITY 1 Includes impaired exposures. 2 Percentage of portfolio TCE. Sep-22 Mar-23 Sep-23 TCE ($bn) 23.2 23.9 24.0 % of Group TCE 1.95 1.96 1.97 Lending ($bn) 19.8 20.4 20.7 % of portfolio graded as stressed1,2 3.55 4.11 4.64 % of portfolio in impaired2 0.24 0.25 0.18 — Increase in agriculture stress ratio mainly driven by exposures moved to watchlist in New Zealand sheep & beef and fruit growing sub-sectors, and Australian fruit growing sub-sectors Sep-22 Mar-23 Sep-23 TCE ($bn) 7.9 8.7 7.8 % of Group TCE 0.66 0.71 0.64 Lending ($bn) 3.1 2.8 2.5 % of portfolio graded as stressed1,2 0.62 2.42 5.23 % of portfolio in impaired2 0.11 0.09 0.07 — Increase in stressed exposure relates to one large customer 30 24 20 10 3 3 3 2 2 21 Dairy Beef & sheep Grain Horticulture Cotton Services to agriculture Viticulture Fishing & aquaculture Other Forestry & logging Poultry 31 26 22 13 1 7 Oil and gas Metal ore Iron ore Mining services Coal Other 57 Westpac Group 2023 Full Year Results Presentation & Investor Discussion Pack |

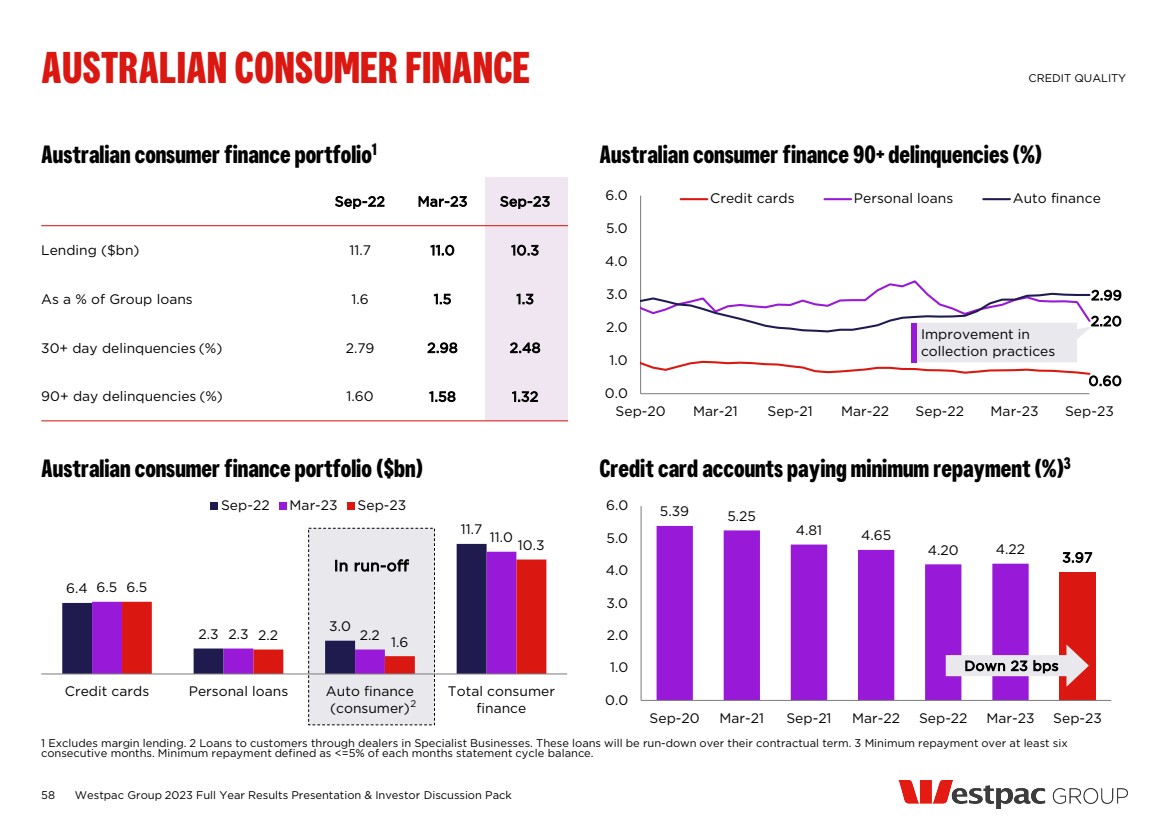

| Australian consumer finance portfolio1 Sep-22 Mar-23 Sep-23 Lending ($bn) 11.7 11.0 10.3 As a % of Group loans 1.6 1.5 1.3 30+ day delinquencies (%) 2.79 2.98 2.48 90+ day delinquencies (%) 1.60 1.58 1.32 Australian consumer finance 90+ delinquencies (%) 0.60 2.20 2.99 0.0 1.0 2.0 3.0 4.0 5.0 6.0 Sep-20 Mar-21 Sep-21 Mar-22 Sep-22 Mar-23 Sep-23 Credit cards Personal loans Auto finance Australian consumer finance portfolio ($bn) 6.4 2.3 3.0 11.7 6.5 2.3 2.2 11.0 6.5 2.2 1.6 10.3 Credit cards Personal loans Auto finance (consumer) Total consumer finance Sep-22 Mar-23 Sep-23 Credit card accounts paying minimum repayment (%)3 AUSTRALIAN CONSUMER FINANCE CREDIT QUALITY 1 Excludes margin lending. 2 Loans to customers through dealers in Specialist Businesses. These loans will be run-down over their contractual term. 3 Minimum repayment over at least six consecutive months. Minimum repayment defined as <=5% of each months statement cycle balance. Improvement in collection practices 58 Westpac Group 2023 Full Year Results Presentation & Investor Discussion Pack 2 In run-off 5.39 5.25 4.81 4.65 4.20 4.22 3.97 0.0 1.0 2.0 3.0 4.0 5.0 6.0 Sep-20 Mar-21 Sep-21 Mar-22 Sep-22 Mar-23 Sep-23 Down 23 bps |

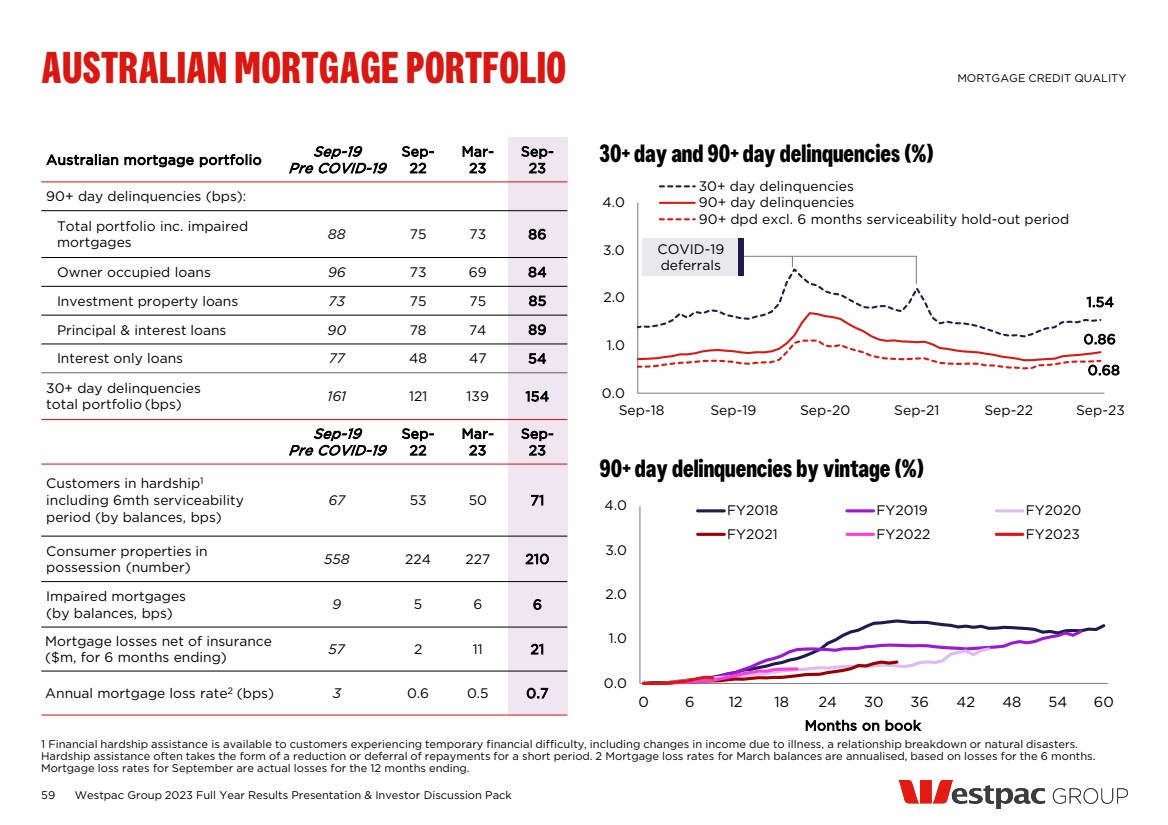

| 59 30+ day and 90+ day delinquencies (%) 1.54 0.86 0.68 0.0 1.0 2.0 3.0 4.0 Sep-18 Sep-19 Sep-20 Sep-21 Sep-22 Sep-23 30+ day delinquencies 90+ day delinquencies 90+ dpd excl. 6 months serviceability hold-out period 90+ day delinquencies by vintage (%) AUSTRALIAN MORTGAGE PORTFOLIO MORTGAGE CREDIT QUALITY 1 Financial hardship assistance is available to customers experiencing temporary financial difficulty, including changes in income due to illness, a relationship breakdown or natural disasters. Hardship assistance often takes the form of a reduction or deferral of repayments for a short period. 2 Mortgage loss rates for March balances are annualised, based on losses for the 6 months. Mortgage loss rates for September are actual losses for the 12 months ending. COVID-19 deferrals Australian mortgage portfolio Sep-19 Pre COVID-19 Sep-22 Mar-23 Sep-23 90+ day delinquencies (bps): Total portfolio inc. impaired mortgages 88 75 73 86 Owner occupied loans 96 73 69 84 Investment property loans 73 75 75 85 Principal & interest loans 90 78 74 89 Interest only loans 77 48 47 54 30+ day delinquencies total portfolio (bps) 161 121 139 154 Sep-19 Pre COVID-19 Sep-22 Mar-23 Sep-23 Customers in hardship1 including 6mth serviceability period (by balances, bps) 67 53 50 71 Consumer properties in possession (number) 558 224 227 210 Impaired mortgages (by balances, bps) 9 5 6 6 Mortgage losses net of insurance ($m, for 6 months ending) 57 2 11 21 Annual mortgage loss rate2 (bps) 3 0.6 0.5 0.7 0.0 1.0 2.0 3.0 4.0 0 6 12 18 24 30 36 42 48 54 60 FY2018 FY2019 FY2020 FY2021 FY2022 FY2023 Months on book Westpac Group 2023 Full Year Results Presentation & Investor Discussion Pack |

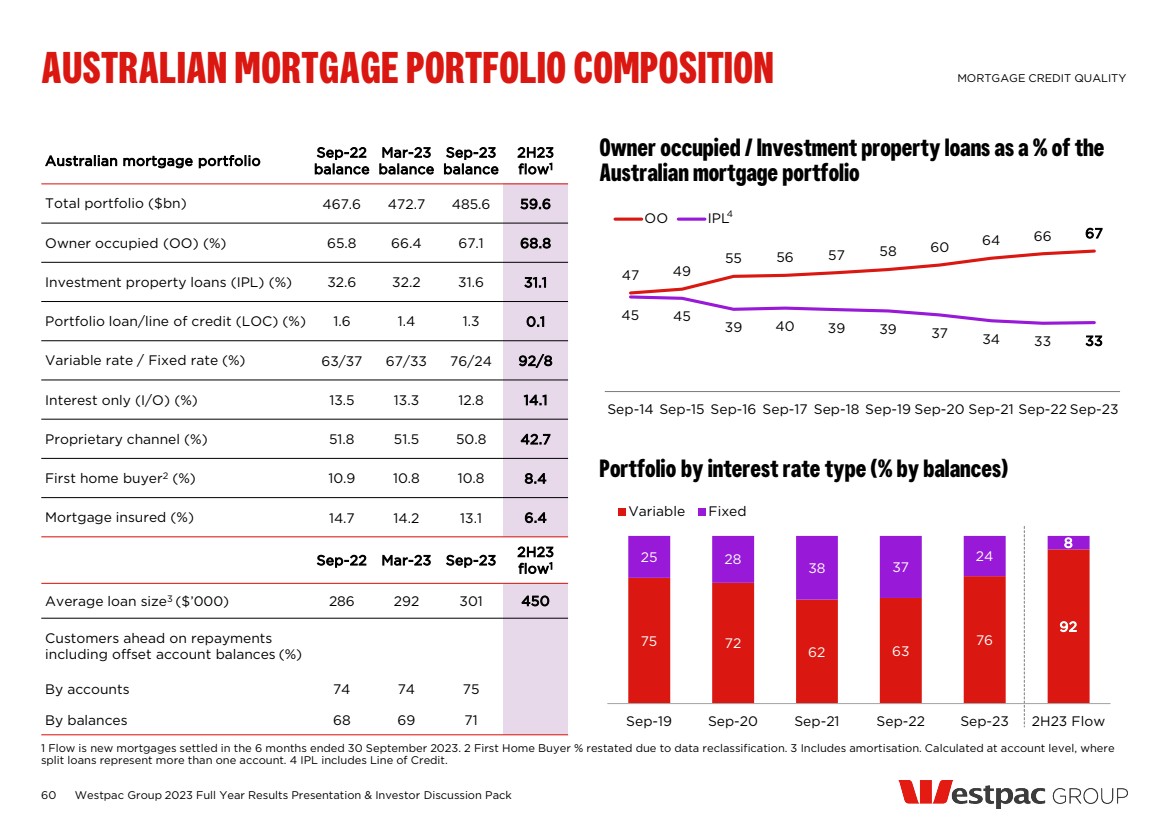

| Australian mortgage portfolio Sep-22 balance Mar-23 balance Sep-23 balance 2H23 flow1 Total portfolio ($bn) 467.6 472.7 485.6 59.6 Owner occupied (OO) (%) 65.8 66.4 67.1 68.8 Investment property loans (IPL) (%) 32.6 32.2 31.6 31.1 Portfolio loan/line of credit (LOC) (%) 1.6 1.4 1.3 0.1 Variable rate / Fixed rate (%) 63/37 67/33 76/24 92/8 Interest only (I/O) (%) 13.5 13.3 12.8 14.1 Proprietary channel (%) 51.8 51.5 50.8 42.7 First home buyer2 (%) 10.9 10.8 10.8 8.4 Mortgage insured (%) 14.7 14.2 13.1 6.4 Sep-22 Mar-23 Sep-23 2H23 flow1 Average loan size3 ($’000) 286 292 301 450 Customers ahead on repayments including offset account balances (%) By accounts 74 74 75 By balances 68 69 71 60 Owner occupied / Investment property loans as a % of the Australian mortgage portfolio Portfolio by interest rate type (% by balances) AUSTRALIAN MORTGAGE PORTFOLIO COMPOSITION MORTGAGE CREDIT QUALITY 1 Flow is new mortgages settled in the 6 months ended 30 September 2023. 2 First Home Buyer % restated due to data reclassification. 3 Includes amortisation. Calculated at account level, where split loans represent more than one account. 4 IPL includes Line of Credit. 4 47 49 55 56 57 58 60 64 66 67 45 45 39 40 39 39 37 34 33 33 Sep-14 Sep-15 Sep-16 Sep-17 Sep-18 Sep-19 Sep-20 Sep-21 Sep-22 Sep-23 OO IPL 75 72 62 63 76 92 25 28 38 37 24 8 Sep-19 Sep-20 Sep-21 Sep-22 Sep-23 2H23 Flow Variable Fixed Westpac Group 2023 Full Year Results Presentation & Investor Discussion Pack |

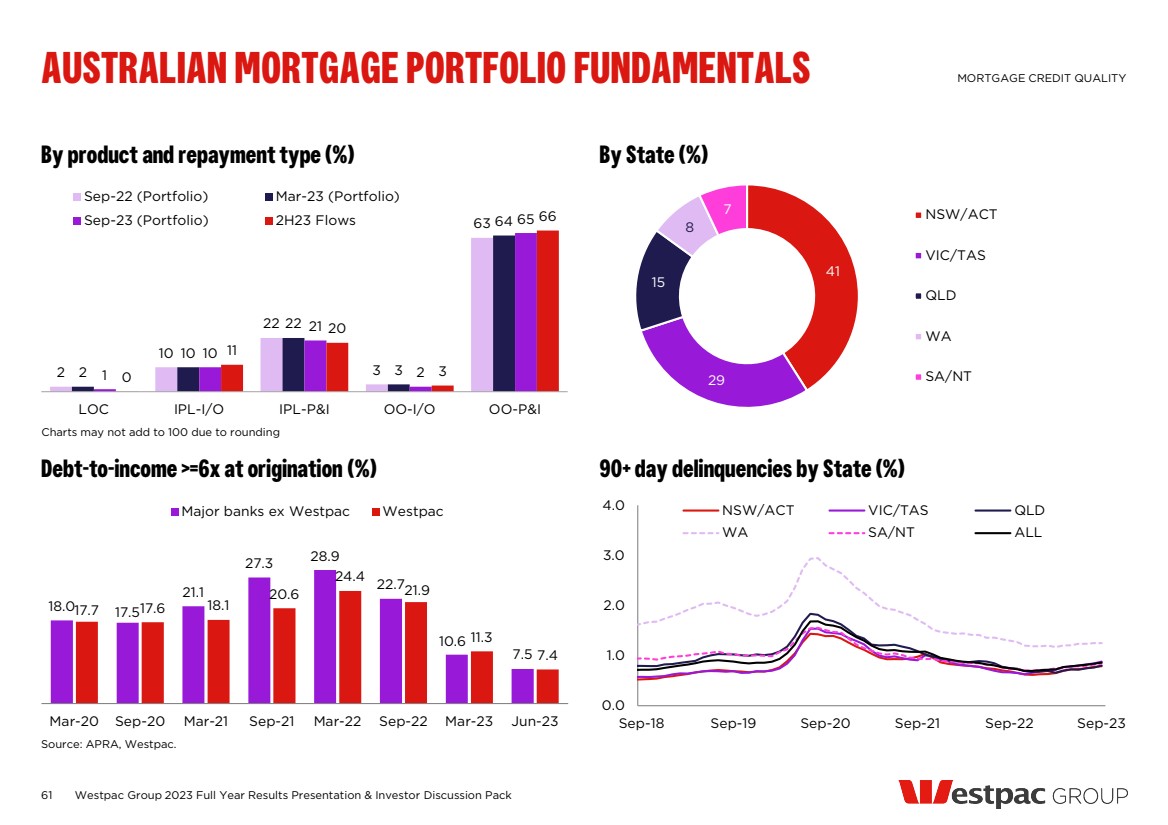

| 61 By product and repayment type (%) By State (%) Debt-to-income >=6x at origination (%) 90+ day delinquencies by State (%) Westpac Group 2023 Full Year Results Presentation & Investor Discussion Pack AUSTRALIAN MORTGAGE PORTFOLIO FUNDAMENTALS MORTGAGE CREDIT QUALITY Source: APRA, Westpac. Charts may not add to 100 due to rounding 2 10 22 3 63 2 10 22 3 64 1 10 21 2 65 0 11 20 3 66 LOC IPL-I/O IPL-P&I OO-I/O OO-P&I Sep-22 (Portfolio) Mar-23 (Portfolio) Sep-23 (Portfolio) 2H23 Flows 41 29 15 8 7 NSW/ACT VIC/TAS QLD WA SA/NT 0.0 1.0 2.0 3.0 4.0 Sep-18 Sep-19 Sep-20 Sep-21 Sep-22 Sep-23 NSW/ACT VIC/TAS QLD WA SA/NT ALL 18.0 17.5 21.1 27.3 28.9 22.7 10.6 7.5 17.7 17.6 18.1 20.6 24.4 21.9 11.3 7.4 Mar-20 Sep-20 Mar-21 Sep-21 Mar-22 Sep-22 Mar-23 Jun-23 Major banks ex Westpac Westpac |

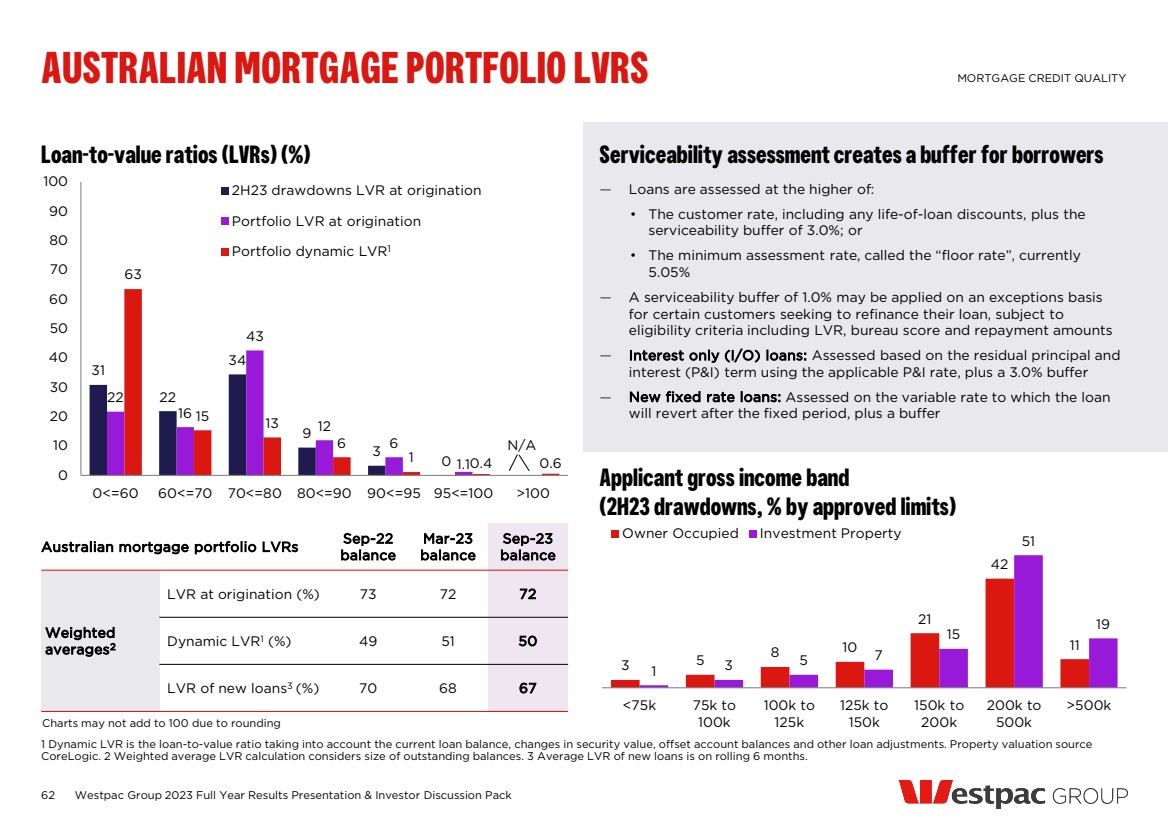

| 31 22 34 9 3 0 22 16 43 12 6 1.1 63 15 13 6 1 0.4 0.6 0 10 20 30 40 50 60 70 80 90 100 0<=60 60<=70 70<=80 80<=90 90<=95 95<=100 >100 2H23 drawdowns LVR at origination Portfolio LVR at origination Portfolio dynamic LVR 62 Loan-to-value ratios (LVRs) (%) Serviceability assessment creates a buffer for borrowers — Loans are assessed at the higher of: • The customer rate, including any life-of-loan discounts, plus the serviceability buffer of 3.0%; or • The minimum assessment rate, called the “floor rate”, currently 5.05% — A serviceability buffer of 1.0% may be applied on an exceptions basis for certain customers seeking to refinance their loan, subject to eligibility criteria including LVR, bureau score and repayment amounts — Interest only (I/O) loans: Assessed based on the residual principal and interest (P&I) term using the applicable P&I rate, plus a 3.0% buffer — New fixed rate loans: Assessed on the variable rate to which the loan will revert after the fixed period, plus a buffer Australian mortgage portfolio LVRs Sep-22 balance Mar-23 balance Sep-23 balance Weighted averages2 LVR at origination (%) 73 72 72 Dynamic LVR1 (%) 49 51 50 LVR of new loans3 (%) 70 68 67 Applicant gross income band (2H23 drawdowns, % by approved limits) Westpac Group 2023 Full Year Results Presentation & Investor Discussion Pack AUSTRALIAN MORTGAGE PORTFOLIO LVRS MORTGAGE CREDIT QUALITY 1 Dynamic LVR is the loan-to-value ratio taking into account the current loan balance, changes in security value, offset account balances and other loan adjustments. Property valuation source CoreLogic. 2 Weighted average LVR calculation considers size of outstanding balances. 3 Average LVR of new loans is on rolling 6 months. Charts may not add to 100 due to rounding N/A 1 3 5 8 10 21 42 11 1 3 5 7 15 51 19 <75k 75k to 100k 100k to 125k 125k to 150k 150k to 200k 200k to 500k >500k Owner Occupied Investment Property |

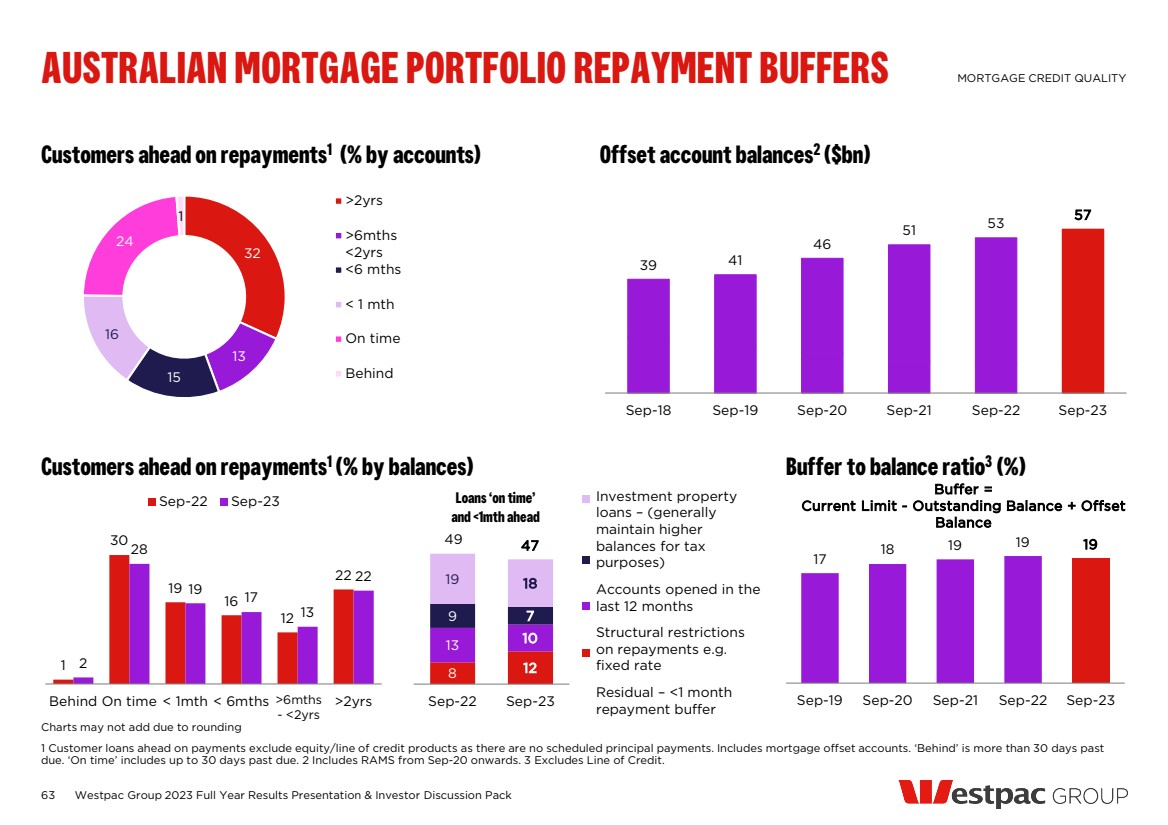

| 1 30 19 16 12 22 2 28 19 17 13 22 Behind On time < 1mth < 6mths >2yrs Sep-22 Sep-23 Loans ‘on time’ and <1mth ahead 63 Offset account balances2 Customers ahead on repayments ($bn) 1 (% by accounts) Customers ahead on repayments1 (% by balances) Buffer to balance ratio3 (%) Westpac Group 2023 Full Year Results Presentation & Investor Discussion Pack AUSTRALIAN MORTGAGE PORTFOLIO REPAYMENT BUFFERS MORTGAGE CREDIT QUALITY 1 Customer loans ahead on payments exclude equity/line of credit products as there are no scheduled principal payments. Includes mortgage offset accounts. ‘Behind’ is more than 30 days past due. ‘On time’ includes up to 30 days past due. 2 Includes RAMS from Sep-20 onwards. 3 Excludes Line of Credit. 8 12 13 10 9 7 19 18 Sep-22 Sep-23 47 49 Investment property loans – (generally maintain higher balances for tax purposes) Accounts opened in the last 12 months Structural restrictions on repayments e.g. fixed rate Residual – <1 month repayment buffer Charts may not add due to rounding Buffer = Current Limit - Outstanding Balance + Offset Balance >6mths - <2yrs 39 41 46 51 53 57 Sep-18 Sep-19 Sep-20 Sep-21 Sep-22 Sep-23 32 13 15 16 24 1 >2yrs >6mths <2yrs <6 mths < 1 mth On time Behind 17 18 19 19 19 Sep-19 Sep-20 Sep-21 Sep-22 Sep-23 |

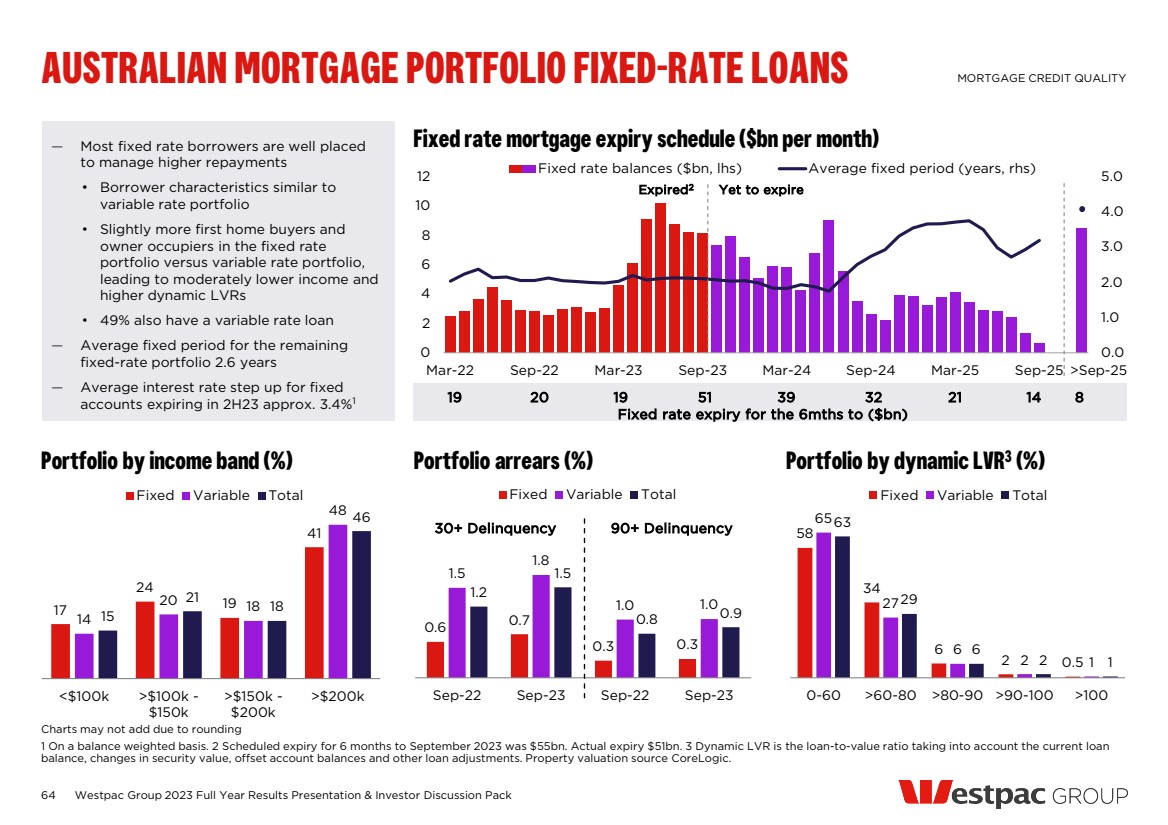

| 0.6 0.7 0.3 0.3 1.5 1.8 1.0 1.0 1.2 1.5 0.8 0.9 Sep-22 Sep-23 Sep-22 Sep-23 Fixed Variable Total 64 — Most fixed rate borrowers are well placed Fixed rate mortgage expiry schedule ($bn per month) to manage higher repayments • Borrower characteristics similar to variable rate portfolio • Slightly more first home buyers and owner occupiers in the fixed rate portfolio versus variable rate portfolio, leading to moderately lower income and higher dynamic LVRs • 49% also have a variable rate loan — Average fixed period for the remaining fixed-rate portfolio 2.6 years — Average interest rate step up for fixed accounts expiring in 2H23 approx. 3.4%1 Portfolio by income band (%) Portfolio arrears (%) Portfolio by dynamic LVR3 (%) Westpac Group 2023 Full Year Results Presentation & Investor Discussion Pack AUSTRALIAN MORTGAGE PORTFOLIO FIXED-RATE LOANS MORTGAGE CREDIT QUALITY 1 On a balance weighted basis. 2 Scheduled expiry for 6 months to September 2023 was $55bn. Actual expiry $51bn. 3 Dynamic LVR is the loan-to-value ratio taking into account the current loan balance, changes in security value, offset account balances and other loan adjustments. Property valuation source CoreLogic. 17 24 19 41 14 20 18 48 15 21 18 46 <$100k >$100k - $150k >$150k - $200k >$200k Fixed Variable Total 58 34 6 2 0.5 65 27 6 2 1 63 29 6 2 1 0-60 >60-80 >80-90 >90-100 >100 Fixed Variable Total 30+ Delinquency 90+ Delinquency 0.0 1.0 2.0 3.0 4.0 5.0 0 2 4 6 8 10 12 Mar-22 Sep-22 Mar-23 Sep-23 Mar-24 Sep-24 Mar-25 Sep-25 Fixed rate balances ($bn, lhs) Average fixed period (years, rhs) >Sep-25 19 20 19 51 39 32 21 14 8 Fixed rate expiry for the 6mths to ($bn) Expired2 Yet to expire Charts may not add due to rounding |

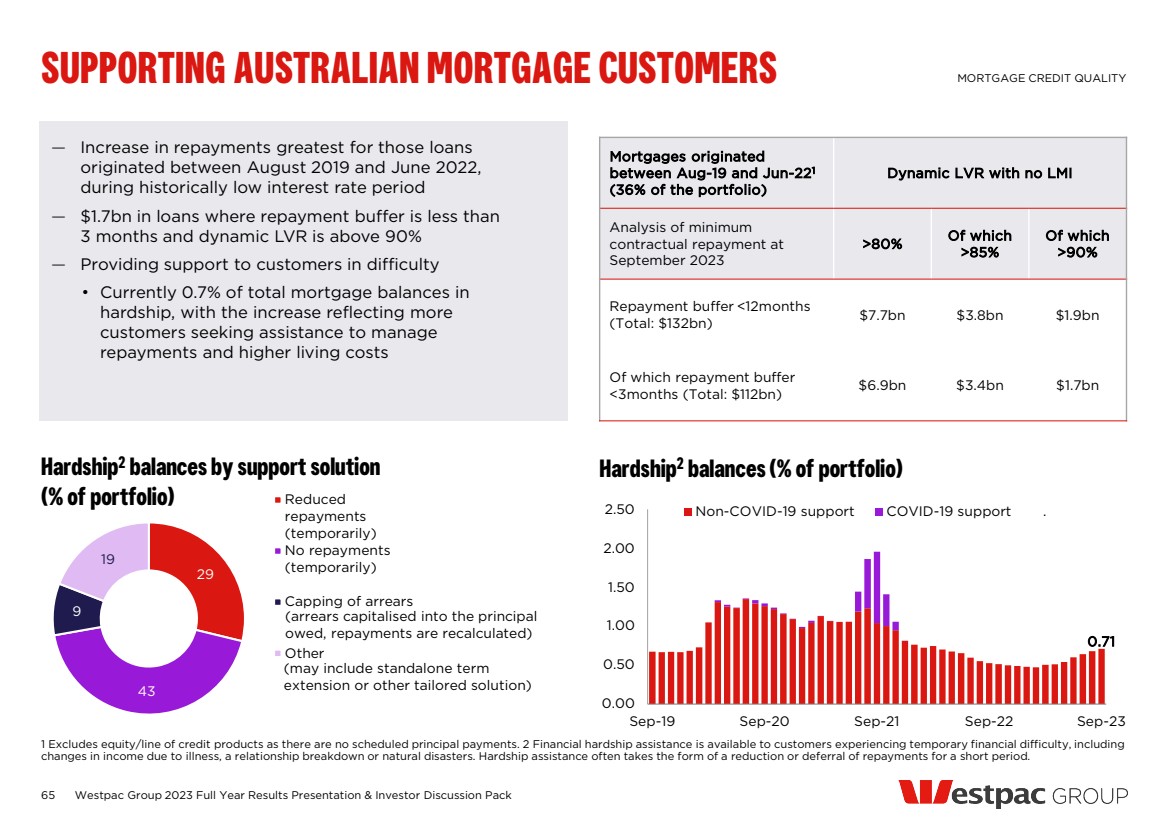

| 65 — Increase in repayments greatest for those loans originated between August 2019 and June 2022, during historically low interest rate period — $1.7bn in loans where repayment buffer is less than 3 months and dynamic LVR is above 90% — Providing support to customers in difficulty • Currently 0.7% of total mortgage balances in hardship, with the increase reflecting more customers seeking assistance to manage repayments and higher living costs Hardship2 balances by support solution (% of portfolio) Hardship2 balances (% of portfolio) Westpac Group 2023 Full Year Results Presentation & Investor Discussion Pack SUPPORTING AUSTRALIAN MORTGAGE CUSTOMERS MORTGAGE CREDIT QUALITY 1 Excludes equity/line of credit products as there are no scheduled principal payments. 2 Financial hardship assistance is available to customers experiencing temporary financial difficulty, including changes in income due to illness, a relationship breakdown or natural disasters. Hardship assistance often takes the form of a reduction or deferral of repayments for a short period. Mortgages originated between Aug-19 and Jun-221 (36% of the portfolio) Dynamic LVR with no LMI Analysis of minimum contractual repayment at September 2023 >80% Of which >85% Of which >90% Repayment buffer <12months (Total: $132bn) $7.7bn $3.8bn $1.9bn Of which repayment buffer <3months (Total: $112bn) $6.9bn $3.4bn $1.7bn 29 43 9 19 Reduced repayments (temporarily) No repayments (temporarily) Capping of arrears Other (arrears capitalised into the principal owed, repayments are recalculated) (may include standalone term extension or other tailored solution) 0.71 0.00 0.50 1.00 1.50 2.00 2.50 Sep-19 Sep-20 Sep-21 Sep-22 Sep-23 Non-COVID-19 support COVID-19 support . |

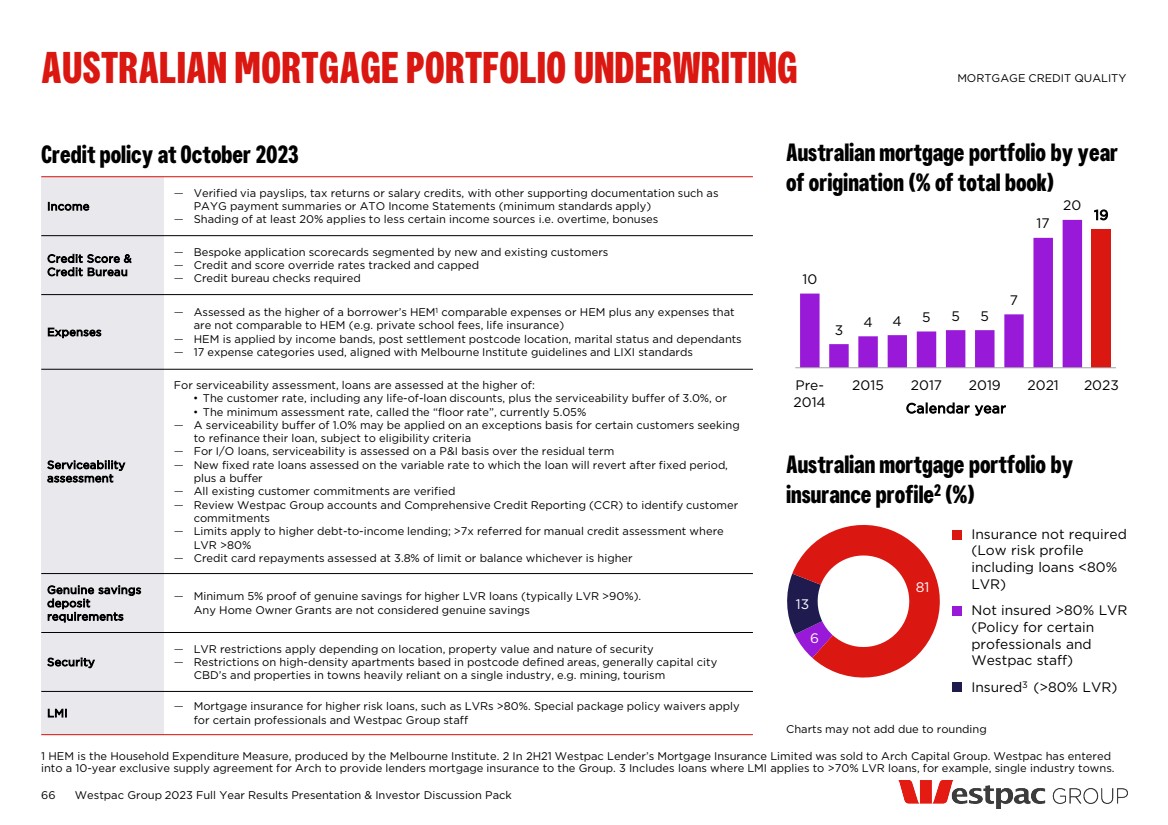

| 6 13 81 66 Australian mortgage portfolio by insurance profile2 (%) Credit policy at October 2023 Australian mortgage portfolio by year of origination (% of total book) Westpac Group 2023 Full Year Results Presentation & Investor Discussion Pack AUSTRALIAN MORTGAGE PORTFOLIO UNDERWRITING MORTGAGE CREDIT QUALITY Calendar year Charts may not add due to rounding Insurance not required (Low risk profile including loans <80% LVR) Not insured >80% LVR (Policy for certain professionals and Westpac staff) Insured3 (>80% LVR) 10 3 4 4 5 5 5 7 17 20 19 Pre-2014 2015 2017 2019 2021 2023 Income — Verified via payslips, tax returns or salary credits, with other supporting documentation such as PAYG payment summaries or ATO Income Statements (minimum standards apply) — Shading of at least 20% applies to less certain income sources i.e. overtime, bonuses Credit Score & Credit Bureau — Bespoke application scorecards segmented by new and existing customers — Credit and score override rates tracked and capped — Credit bureau checks required Expenses — Assessed as the higher of a borrower’s HEM1 comparable expenses or HEM plus any expenses that are not comparable to HEM (e.g. private school fees, life insurance) — HEM is applied by income bands, post settlement postcode location, marital status and dependants — 17 expense categories used, aligned with Melbourne Institute guidelines and LIXI standards Serviceability assessment For serviceability assessment, loans are assessed at the higher of: • The customer rate, including any life-of-loan discounts, plus the serviceability buffer of 3.0%, or • The minimum assessment rate, called the “floor rate”, currently 5.05% — A serviceability buffer of 1.0% may be applied on an exceptions basis for certain customers seeking to refinance their loan, subject to eligibility criteria — For I/O loans, serviceability is assessed on a P&I basis over the residual term — New fixed rate loans assessed on the variable rate to which the loan will revert after fixed period, plus a buffer — All existing customer commitments are verified — Review Westpac Group accounts and Comprehensive Credit Reporting (CCR) to identify customer commitments — Limits apply to higher debt-to-income lending; >7x referred for manual credit assessment where LVR >80% — Credit card repayments assessed at 3.8% of limit or balance whichever is higher Genuine savings deposit requirements — Minimum 5% proof of genuine savings for higher LVR loans (typically LVR >90%). Any Home Owner Grants are not considered genuine savings Security — LVR restrictions apply depending on location, property value and nature of security — Restrictions on high-density apartments based in postcode defined areas, generally capital city CBD’s and properties in towns heavily reliant on a single industry, e.g. mining, tourism LMI — Mortgage insurance for higher risk loans, such as LVRs >80%. Special package policy waivers apply for certain professionals and Westpac Group staff 1 HEM is the Household Expenditure Measure, produced by the Melbourne Institute. 2 In 2H21 Westpac Lender’s Mortgage Insurance Limited was sold to Arch Capital Group. Westpac has entered into a 10-year exclusive supply agreement for Arch to provide lenders mortgage insurance to the Group. 3 Includes loans where LMI applies to >70% LVR loans, for example, single industry towns. |

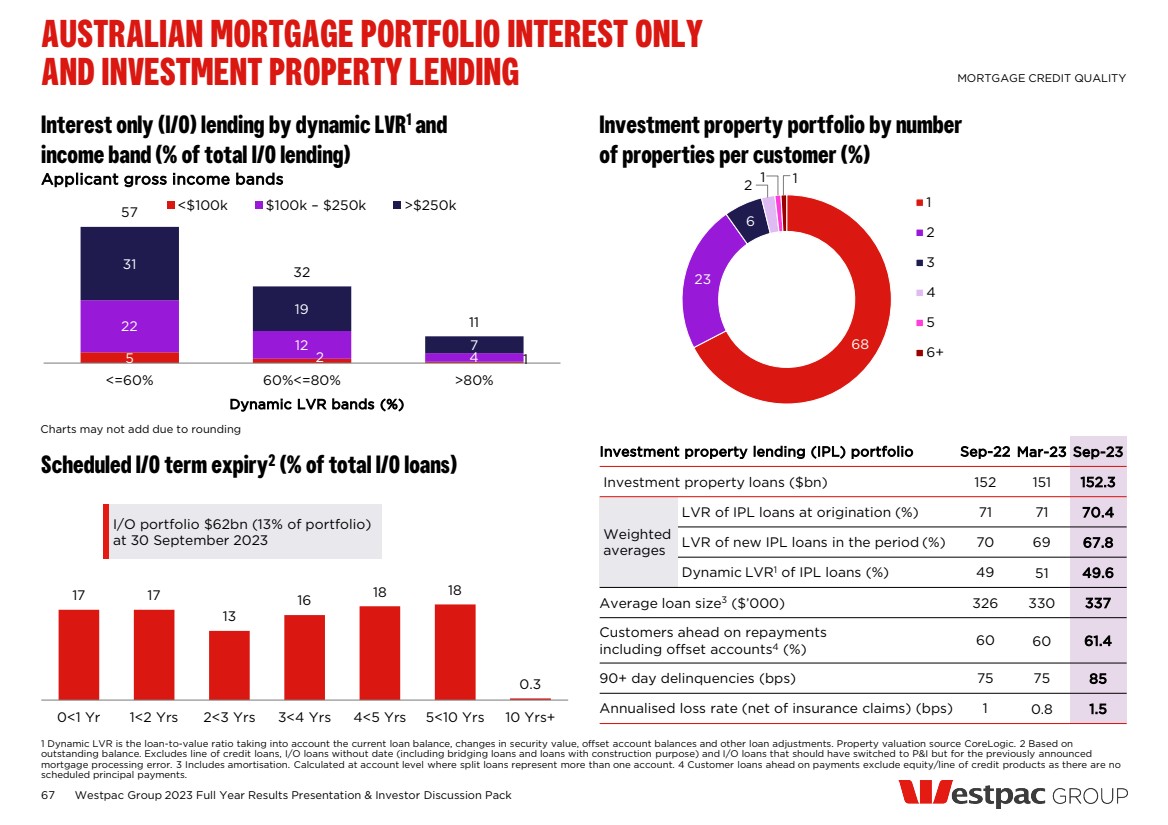

| 68 23 6 1 2 3 4 5 6+ 67 Interest only (I/O) lending by dynamic LVR1 and income band (% of total I/O lending) Investment property portfolio by number of properties per customer (%) Scheduled I/O term expiry2 (% of total I/O loans) Westpac Group 2023 Full Year Results Presentation & Investor Discussion Pack AUSTRALIAN MORTGAGE PORTFOLIO INTEREST ONLY AND INVESTMENT PROPERTY LENDING MORTGAGE CREDIT QUALITY 1 Dynamic LVR is the loan-to-value ratio taking into account the current loan balance, changes in security value, offset account balances and other loan adjustments. Property valuation source CoreLogic. 2 Based on outstanding balance. Excludes line of credit loans, I/O loans without date (including bridging loans and loans with construction purpose) and I/O loans that should have switched to P&I but for the previously announced mortgage processing error. 3 Includes amortisation. Calculated at account level where split loans represent more than one account. 4 Customer loans ahead on payments exclude equity/line of credit products as there are no scheduled principal payments. Charts may not add due to rounding 5 2 1 22 12 4 31 19 7 57 32 11 <=60% 60%<=80% >80% Dynamic LVR bands (%) <$100k $100k – $250k >$250k 17 17 13 16 18 18 0.3 0<1 Yr 1<2 Yrs 2<3 Yrs 3<4 Yrs 4<5 Yrs 5<10 Yrs 10 Yrs+ 1 Investment property lending (IPL) portfolio Sep-22 Mar-23 Sep-23 Investment property loans ($bn) 152 151 152.3 Weighted averages LVR of IPL loans at origination (%) 71 71 70.4 LVR of new IPL loans in the period (%) 70 69 67.8 Dynamic LVR1 of IPL loans (%) 49 51 49.6 Average loan size3 ($’000) 326 330 337 Customers ahead on repayments including offset accounts4 (%) 60 60 61.4 90+ day delinquencies (bps) 75 75 85 Annualised loss rate (net of insurance claims) (bps) 1 0.8 1.5 I/O portfolio $62bn (13% of portfolio) at 30 September 2023 1 Applicant gross income bands 2 |

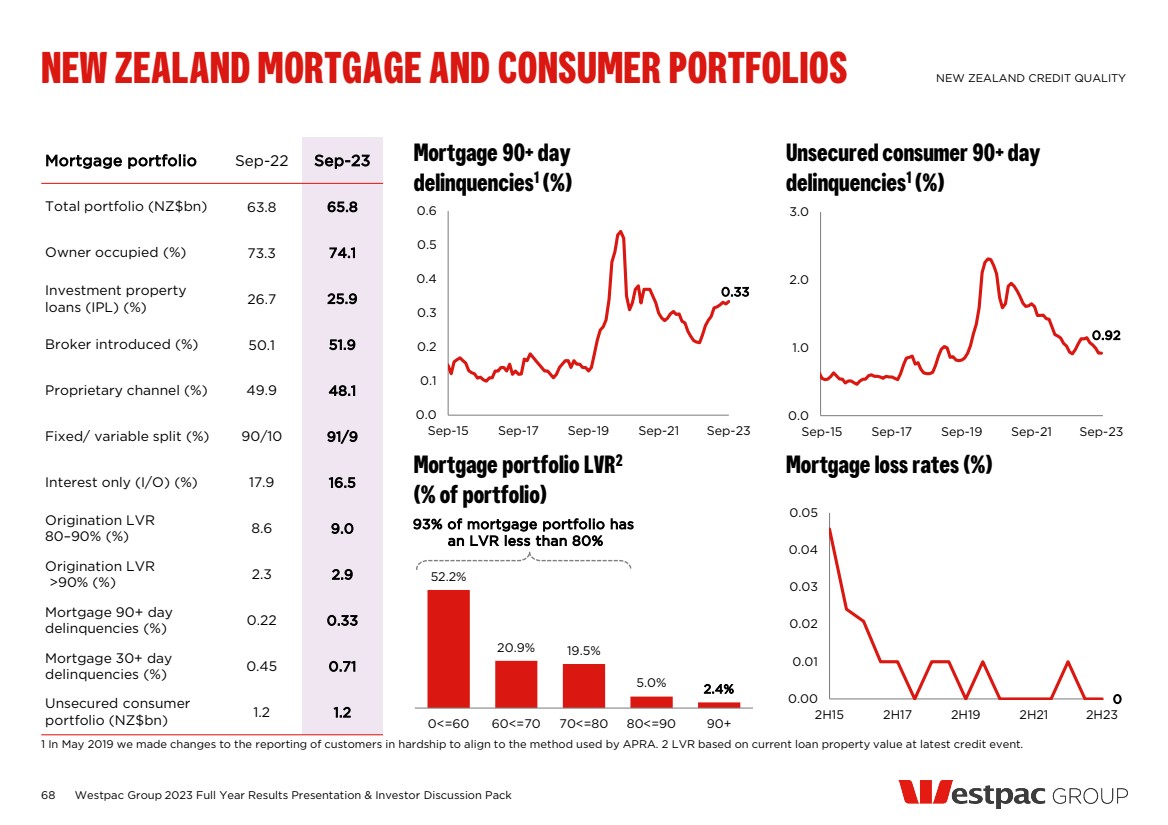

| 68 Mortgage portfolio LVR2 (% of portfolio) Mortgage loss rates (%) Mortgage 90+ day delinquencies1 (%) Unsecured consumer 90+ day delinquencies1 (%) NEW ZEALAND MORTGAGE AND CONSUMER PORTFOLIOS NEW ZEALAND CREDIT QUALITY 1 In May 2019 we made changes to the reporting of customers in hardship to align to the method used by APRA. 2 LVR based on current loan property value at latest credit event. Mortgage portfolio Sep-22 Sep-23 Total portfolio (NZ$bn) 63.8 65.8 Owner occupied (%) 73.3 74.1 Investment property loans (IPL) (%) 26.7 25.9 Broker introduced (%) 50.1 51.9 Proprietary channel (%) 49.9 48.1 Fixed/ variable split (%) 90/10 91/9 Interest only (I/O) (%) 17.9 16.5 Origination LVR 80–90% (%) 8.6 9.0 Origination LVR >90% (%) 2.3 2.9 Mortgage 90+ day delinquencies (%) 0.22 0.33 Mortgage 30+ day delinquencies (%) 0.45 0.71 Unsecured consumer portfolio (NZ$bn) 1.2 1.2 0.00 0 0.01 0.02 0.03 0.04 0.05 2H15 2H17 2H19 2H21 2H23 0.92 0.0 1.0 2.0 3.0 Sep-15 Sep-17 Sep-19 Sep-21 Sep-23 0.33 0.0 0.1 0.2 0.3 0.4 0.5 0.6 Sep-15 Sep-17 Sep-19 Sep-21 Sep-23 52.2% 20.9% 19.5% 5.0% 2.4% 0<=60 60<=70 70<=80 80<=90 90+ 93% of mortgage portfolio has an LVR less than 80% Westpac Group 2023 Full Year Results Presentation & Investor Discussion Pack |

| NON-CREDIT RISK MANAGEMENT 2023 Full year financial results |

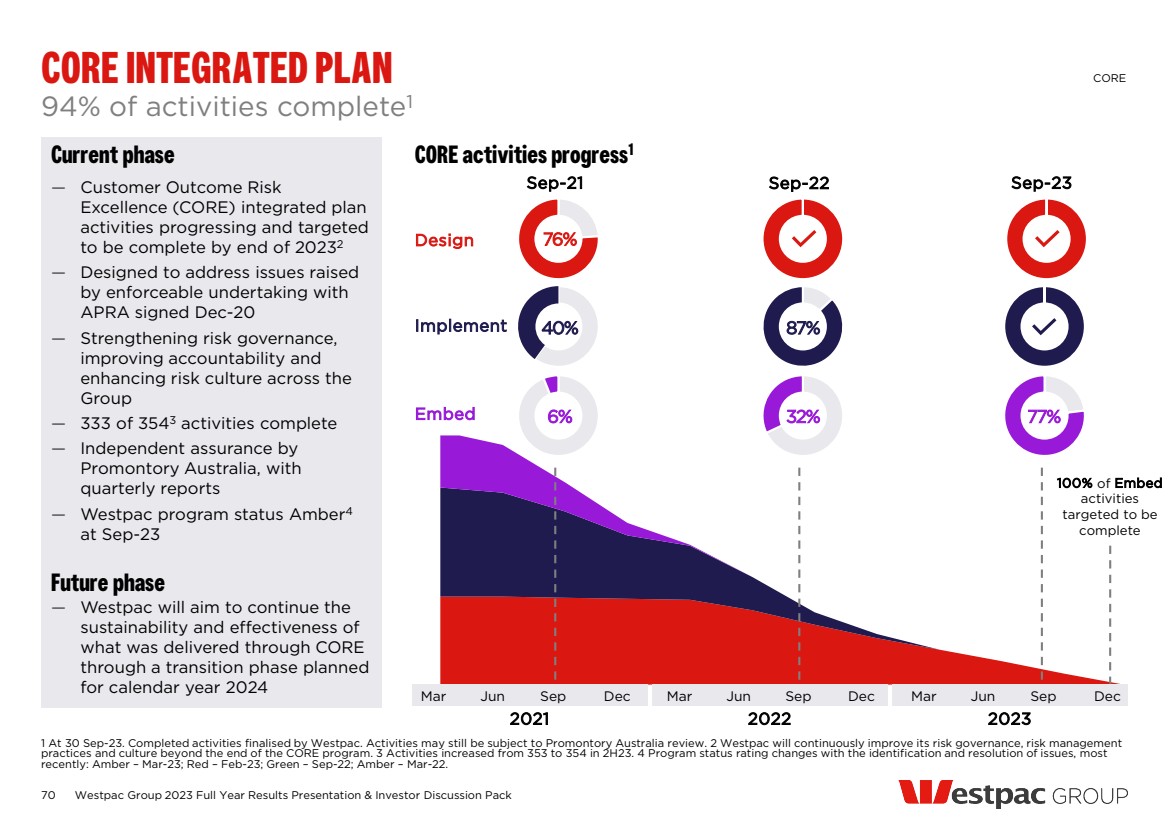

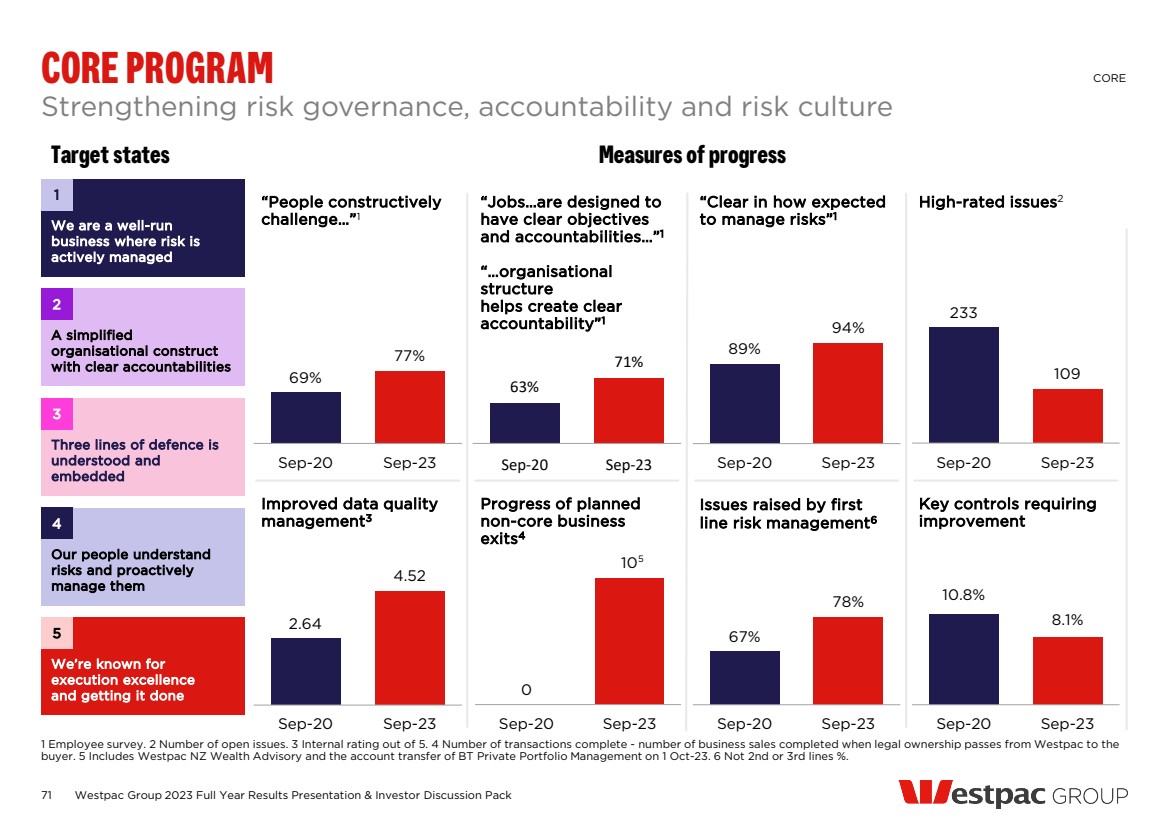

| 70 — Customer Outcome Risk Excellence (CORE) integrated plan activities progressing and targeted to be complete by end of 20232 — Designed to address issues raised by enforceable undertaking with APRA signed Dec-20 — Strengthening risk governance, improving accountability and enhancing risk culture across the Group — 333 of 3543 activities complete — Independent assurance by Promontory Australia, with quarterly reports — Westpac program status Amber4 at Sep-23 CORE activities progress1 Current phase 94% of activities complete1 Westpac Group 2023 Full Year Results Presentation & Investor Discussion Pack CORE INTEGRATED PLAN CORE 1 At 30 Sep-23. Completed activities finalised by Westpac. Activities may still be subject to Promontory Australia review. 2 Westpac will continuously improve its risk governance, risk management practices and culture beyond the end of the CORE program. 3 Activities increased from 353 to 354 in 2H23. 4 Program status rating changes with the identification and resolution of issues, most recently: Amber – Mar-23; Red – Feb-23; Green – Sep-22; Amber – Mar-22. 2021 2022 2023 Mar Jun Sep Dec Mar Jun Sep Dec Mar Jun Sep Dec Sep-23 Design Sep-21 Sep-22 Implement Embed 6% 32% 77% 40% 87% 76% 100% of Embed activities targeted to be complete Future phase — Westpac will aim to continue the sustainability and effectiveness of what was delivered through CORE through a transition phase planned for calendar year 2024 |

| We are a well-run business where risk is actively managed A simplified organisational construct with clear accountabilities Three lines of defence is understood and embedded Our people understand risks and proactively manage them We’re known for execution excellence and getting it done 71 Target states Measures of progress Strengthening risk governance, accountability and risk culture Westpac Group 2023 Full Year Results Presentation & Investor Discussion Pack CORE PROGRAM CORE 1 Employee survey. 2 Number of open issues. 3 Internal rating out of 5. 4 Number of transactions complete - number of business sales completed when legal ownership passes from Westpac to the buyer. 5 Includes Westpac NZ Wealth Advisory and the account transfer of BT Private Portfolio Management on 1 Oct-23. 6 Not 2nd or 3rd lines %. 67% 78% Sep-20 Sep-23 Issues raised by first line risk management6 233 109 Sep-20 Sep-23 High-rated issues2 2.64 4.52 Sep-20 Sep-23 Improved data quality management3 89% 94% Sep-20 Sep-23 “Clear in how expected to manage risks”1 69% 77% Sep-20 Sep-23 “People constructively challenge…”1 10.8% 8.1% Sep-20 Sep-23 Key controls requiring improvement 63% 71% Sep-20 Sep-23 “Jobs…are designed to have clear objectives and accountabilities…”1 “…organisational structure helps create clear accountability”1 0 10 Sep-20 Sep-23 Progress of planned non-core business exits4 1 2 3 4 5 5 |

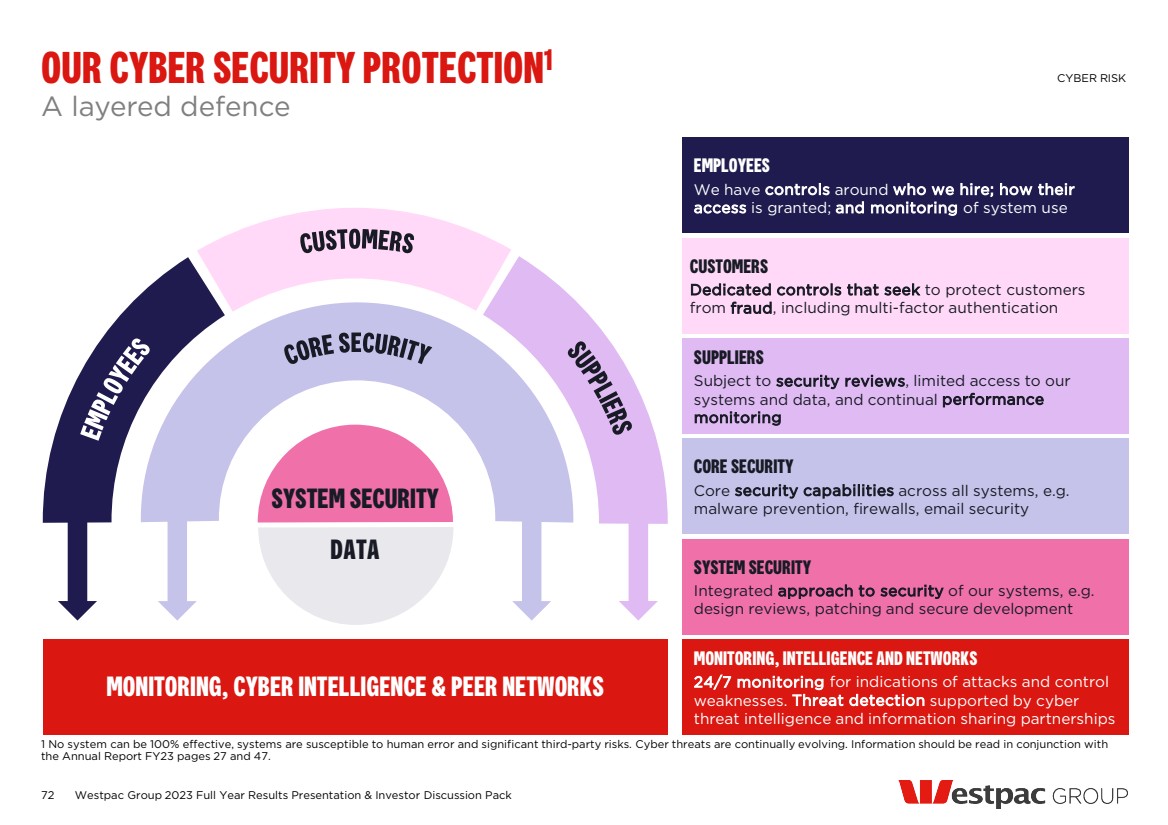

| OUR CYBER SECURITY PROTECTION1 A layered defence CYBER RISK 1 No system can be 100% effective, systems are susceptible to human error and significant third-party risks. Cyber threats are continually evolving. Information should be read in conjunction with the Annual Report FY23 pages 27 and 47. EMPLOYEES We have controls around who we hire; how their access is granted; and monitoring of system use SUPPLIERS Subject to security reviews, limited access to our systems and data, and continual performance monitoring SYSTEM SECURITY Integrated approach to security of our systems, e.g. design reviews, patching and secure development CUSTOMERS Dedicated controls that seek to protect customers from fraud, including multi-factor authentication CORE SECURITY Core security capabilities across all systems, e.g. malware prevention, firewalls, email security MONITORING, INTELLIGENCE AND NETWORKS 24/7 monitoring for indications of attacks and control weaknesses. Threat detection supported by cyber threat intelligence and information sharing partnerships MONITORING, CYBER INTELLIGENCE & PEER NETWORKS SYSTEM SECURITY DATA 72 Westpac Group 2023 Full Year Results Presentation & Investor Discussion Pack |

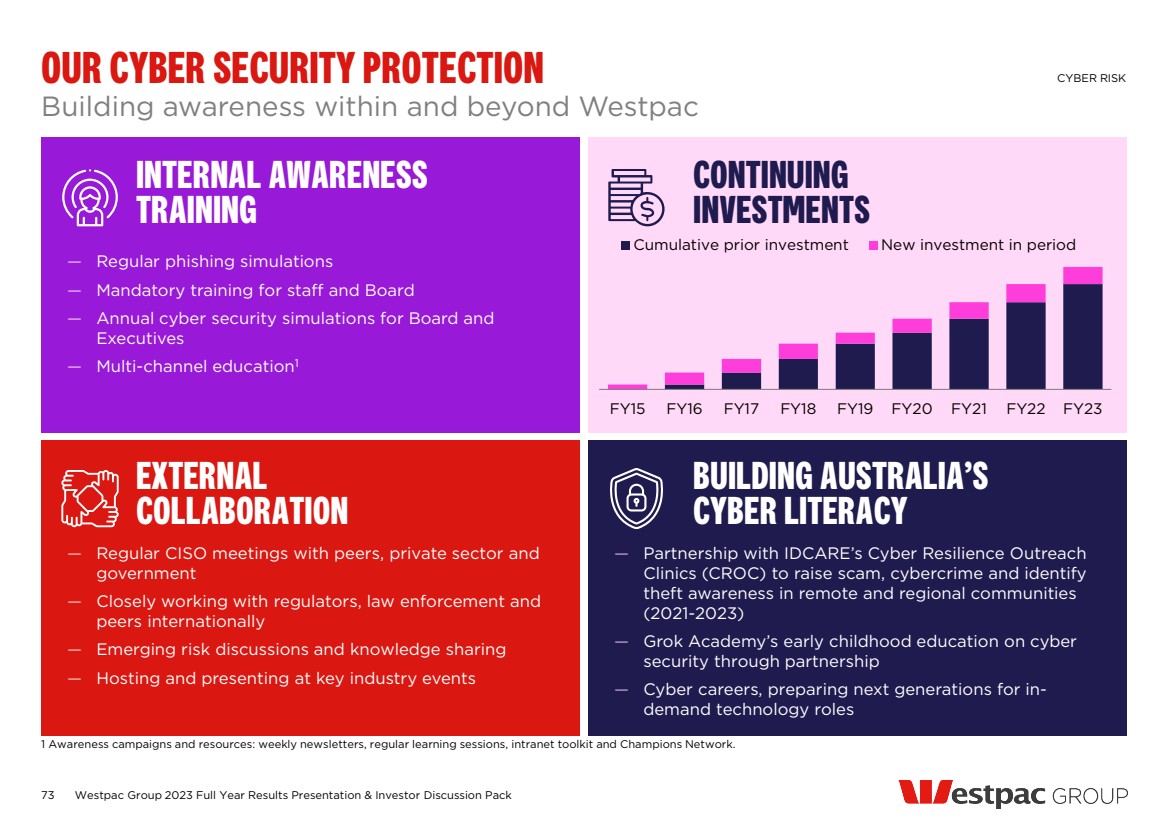

| OUR CYBER SECURITY PROTECTION Building awareness within and beyond Westpac CYBER RISK 1 Awareness campaigns and resources: weekly newsletters, regular learning sessions, intranet toolkit and Champions Network. BUILDING AUSTRALIA’S CYBER LITERACY EXTERNAL COLLABORATION — Regular CISO meetings with peers, private sector and government — Closely working with regulators, law enforcement and peers internationally — Emerging risk discussions and knowledge sharing — Hosting and presenting at key industry events — Partnership with IDCARE’s Cyber Resilience Outreach Clinics (CROC) to raise scam, cybercrime and identify theft awareness in remote and regional communities (2021-2023) — Grok Academy’s early childhood education on cyber security through partnership — Cyber careers, preparing next generations for in-demand technology roles CONTINUING INVESTMENTS INTERNAL AWARENESS TRAINING — Regular phishing simulations — Mandatory training for staff and Board — Annual cyber security simulations for Board and Executives — Multi-channel education1 FY15 FY16 FY17 FY18 FY19 FY20 FY21 FY22 FY23 Cumulative prior investment New investment in period 73 Westpac Group 2023 Full Year Results Presentation & Investor Discussion Pack |

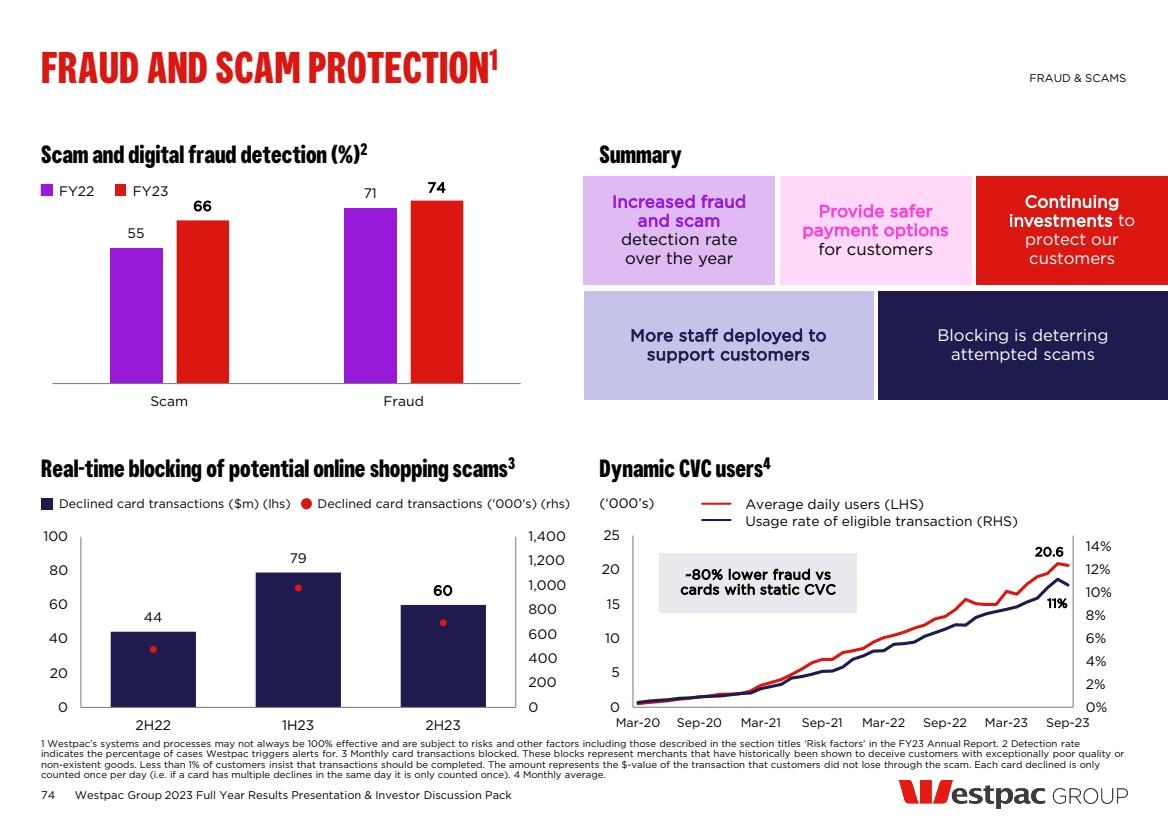

| More staff deployed to support customers Blocking is deterring attempted scams Increased fraud and scam detection rate over the year Provide safer payment options for customers Continuing investments to protect our customers 74 Scam and digital fraud detection (%)2 55 71 66 74 Scam Fraud Summary Real-time blocking of potential online shopping scams3 44 79 60 0 200 400 600 800 1,000 1,200 1,400 0 20 40 60 80 100 2H22 1H23 2H23 Dynamic CVC users4 20.6 11% 0% 2% 4% 6% 8% 10% 12% 14% 0 5 10 15 20 25 Mar-20 Sep-20 Mar-21 Sep-21 Mar-22 Sep-22 Mar-23 Sep-23 Westpac Group 2023 Full Year Results Presentation & Investor Discussion Pack FRAUD AND SCAM PROTECTION1 FRAUD & SCAMS 1 Westpac’s systems and processes may not always be 100% effective and are subject to risks and other factors including those described in the section titles ‘Risk factors’ in the FY23 Annual Report. 2 Detection rate indicates the percentage of cases Westpac triggers alerts for. 3 Monthly card transactions blocked. These blocks represent merchants that have historically been shown to deceive customers with exceptionally poor quality or non-existent goods. Less than 1% of customers insist that transactions should be completed. The amount represents the $-value of the transaction that customers did not lose through the scam. Each card declined is only counted once per day (i.e. if a card has multiple declines in the same day it is only counted once). 4 Monthly average. ~80% lower fraud vs cards with static CVC Declined card transactions ($m) (lhs) Declined card transactions ('000's) (rhs) (‘000’s) Average daily users (LHS) Usage rate of eligible transaction (RHS) FY22 FY23 |

| DIGITAL BANKING SECURITY INITIATIVES 75 Helping protect customers and reducing fraud and scams Westpac Group 2023 Full Year Results Presentation & Investor Discussion Pack FRAUD & SCAMS Westpac Verify is a risk rating security layer provided when adding new payees in digital banking, targeting business email compromise scams Dynamic CVC generates a new CVC every 24 hours; ~80% lower fraud vs cards with static CVC Westpac Prompts will be presented to customers where systems detect potential scam; expected to be available in 1H24 Real-time blocking of potentially questionable online merchants Saved $139m for 1.67m customer incidences in FY23 Biometric onboarding experience reduces identity theft, fraud and promotes digital usage; $20.1m saved in averted fraud losses Advanced customer behavioural tools saved customers $23m in FY23, combatting remote access scams, including Voice scam detection |

| CAPITAL, FUNDING AND LIQUIDITY 2023 Full year financial results |

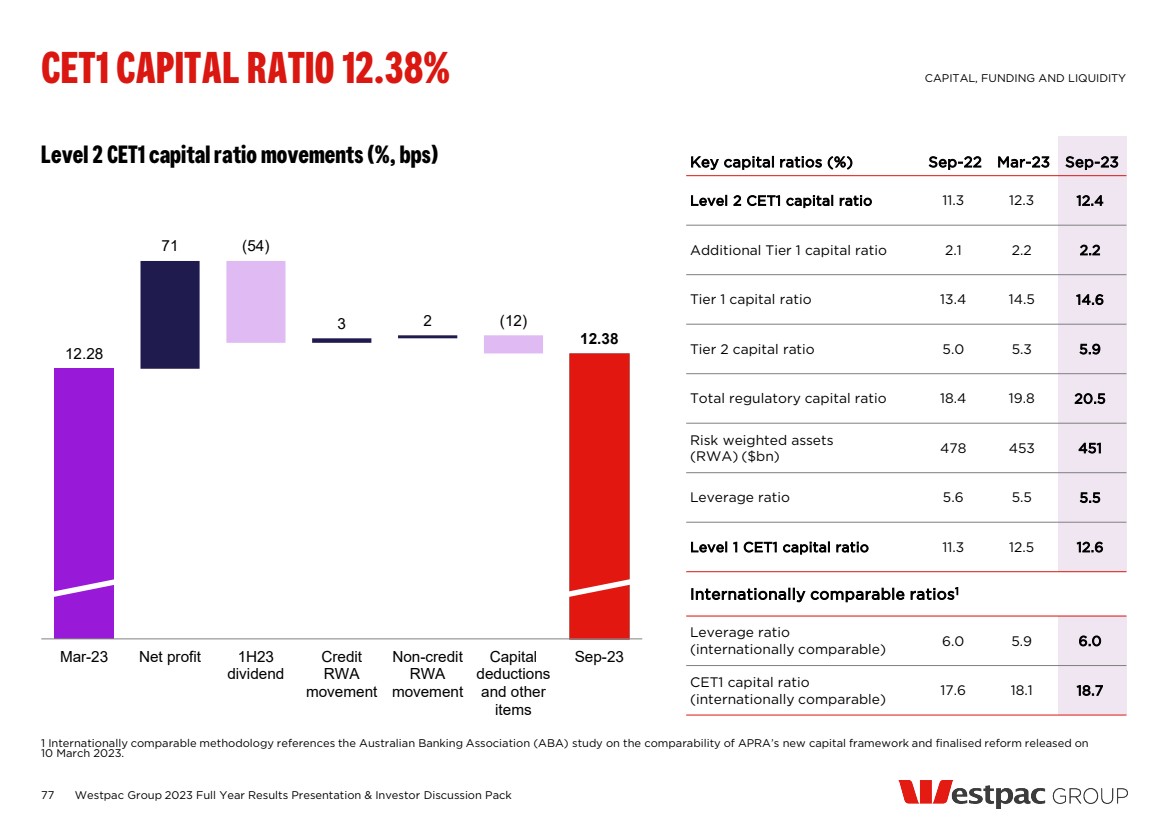

| 77 12.28 71 3 2 12.38 (54) (12) Mar-23 Net profit 1H23 dividend Credit RWA movement Non-credit RWA movement Capital deductions and other items Sep-23 Level 2 CET1 capital ratio movements (%, bps) CET1 CAPITAL RATIO 12.38% CAPITAL, FUNDING AND LIQUIDITY 1 Internationally comparable methodology references the Australian Banking Association (ABA) study on the comparability of APRA’s new capital framework and finalised reform released on 10 March 2023. Key capital ratios (%) Sep-22 Mar-23 Sep-23 Level 2 CET1 capital ratio 11.3 12.3 12.4 Additional Tier 1 capital ratio 2.1 2.2 2.2 Tier 1 capital ratio 13.4 14.5 14.6 Tier 2 capital ratio 5.0 5.3 5.9 Total regulatory capital ratio 18.4 19.8 20.5 Risk weighted assets (RWA) ($bn) 478 453 451 Leverage ratio 5.6 5.5 5.5 Level 1 CET1 capital ratio 11.3 12.5 12.6 Internationally comparable ratios1 Leverage ratio (internationally comparable) 6.0 5.9 6.0 CET1 capital ratio (internationally comparable) 17.6 18.1 18.7 Westpac Group 2023 Full Year Results Presentation & Investor Discussion Pack |

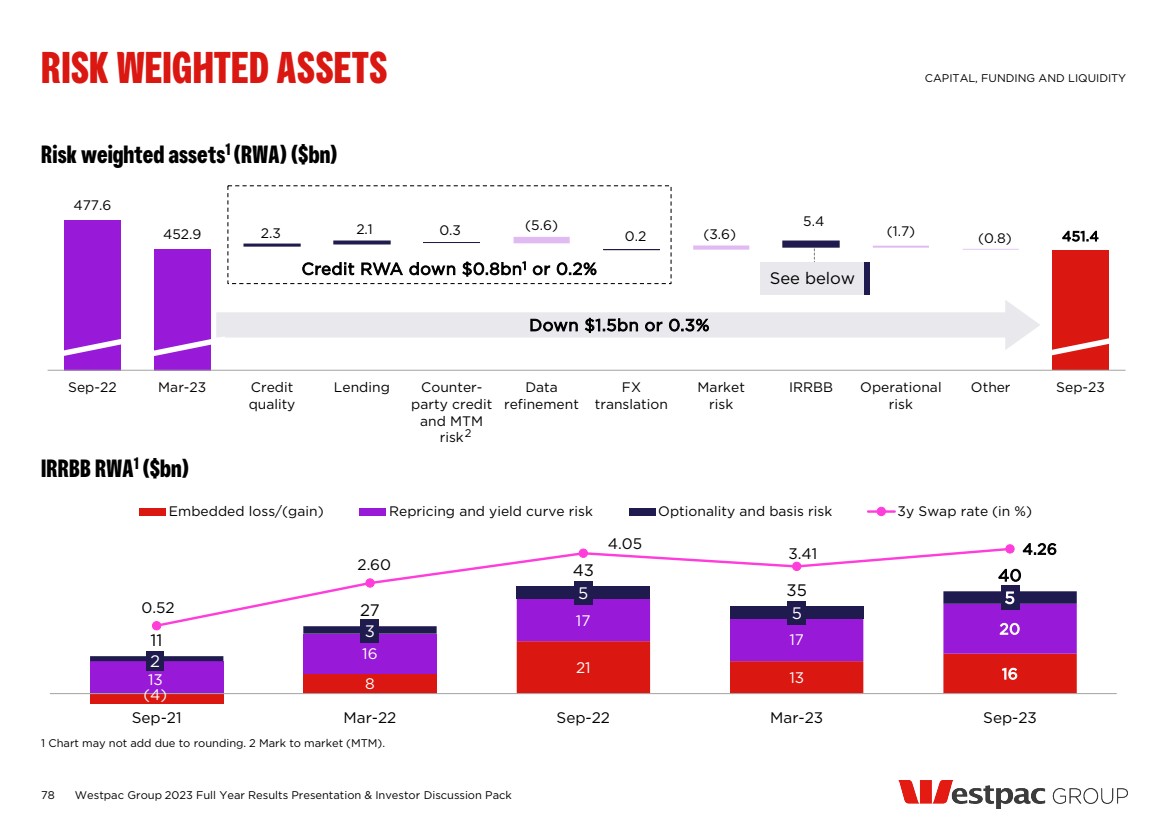

| Risk weighted assets1 (RWA) ($bn) 78 IRRBB RWA1 ($bn) RISK WEIGHTED ASSETS CAPITAL, FUNDING AND LIQUIDITY 1 Chart may not add due to rounding. 2 Mark to market (MTM). 2 2.3 2.1 0.3 0.2 (5.6) 5.4 (3.6) (1.7) (0.8) 477.6 452.9 451.4 Sep-22 Mar-23 Credit quality Lending Counter-party credit and MTM risk Data refinement FX translation Market risk IRRBB Operational risk Other Sep-23 (4) 8 21 13 16 13 16 17 17 20 2 3 5 5 5 11 27 43 35 40 0.52 2.60 4.05 3.41 4.26 -4 -3 -2 -1 0 1 2 3 4 -10 0 10 20 30 40 50 60 Sep-21 Mar-22 Sep-22 Mar-23 Sep-23 Embedded loss/(gain) Repricing and yield curve risk Optionality and basis risk 3y Swap rate (in %) Westpac Group 2023 Full Year Results Presentation & Investor Discussion Pack Down $1.5bn or 0.3% Credit RWA down $0.8bn1 or 0.2% See below |

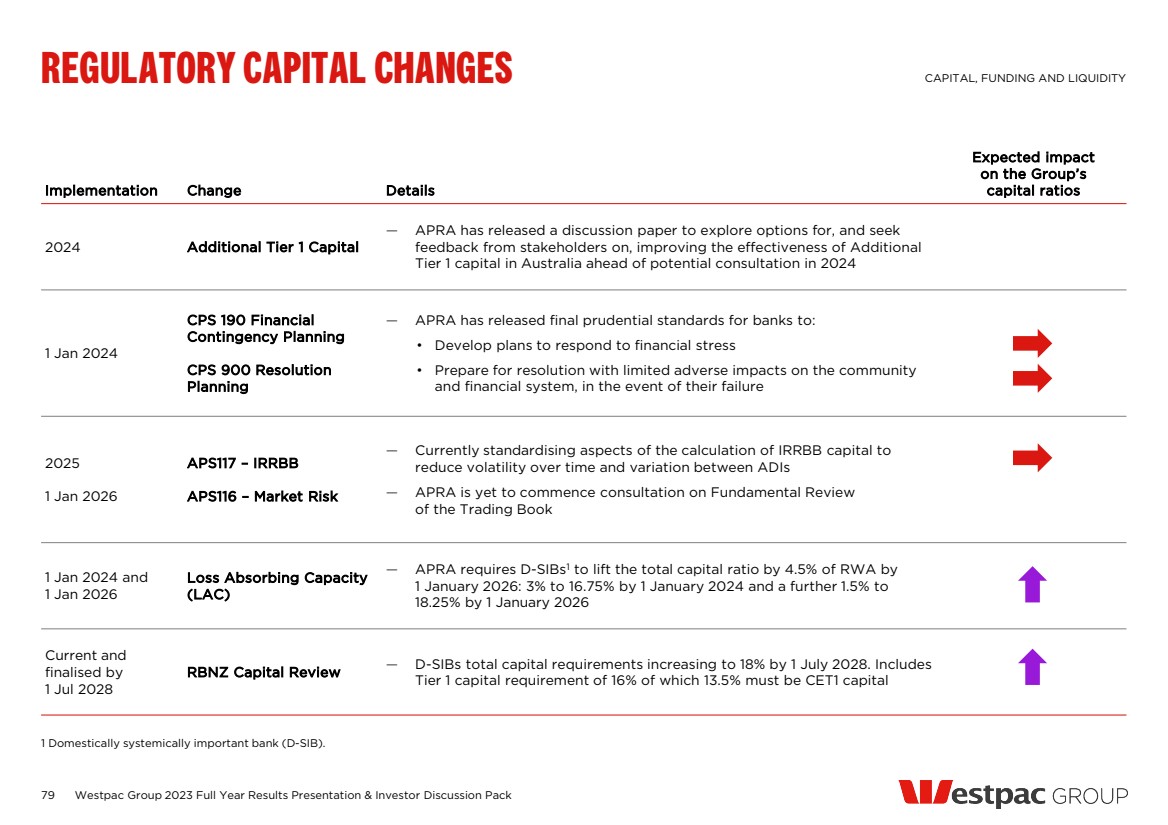

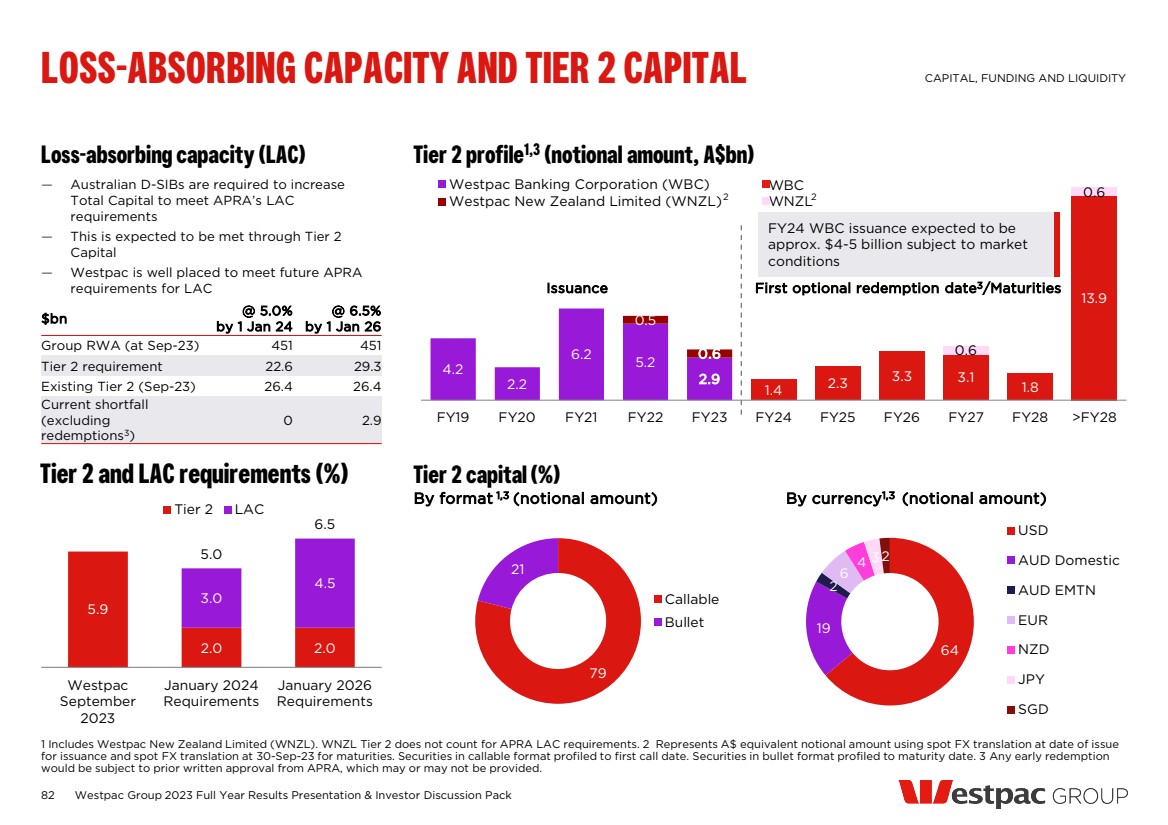

| Implementation Change Details Expected impact on the Group’s capital ratios 2024 Additional Tier 1 Capital — APRA has released a discussion paper to explore options for, and seek feedback from stakeholders on, improving the effectiveness of Additional Tier 1 capital in Australia ahead of potential consultation in 2024 1 Jan 2024 CPS 190 Financial Contingency Planning CPS 900 Resolution Planning — APRA has released final prudential standards for banks to: • Develop plans to respond to financial stress • Prepare for resolution with limited adverse impacts on the community and financial system, in the event of their failure 2025 1 Jan 2026 APS117 – IRRBB APS116 – Market Risk — Currently standardising aspects of the calculation of IRRBB capital to reduce volatility over time and variation between ADIs — APRA is yet to commence consultation on Fundamental Review of the Trading Book 1 Jan 2024 and 1 Jan 2026 Loss Absorbing Capacity (LAC) — APRA requires D-SIBs1 to lift the total capital ratio by 4.5% of RWA by 1 January 2026: 3% to 16.75% by 1 January 2024 and a further 1.5% to 18.25% by 1 January 2026 Current and finalised by 1 Jul 2028 RBNZ Capital Review — D-SIBs total capital requirements increasing to 18% by 1 July 2028. Includes Tier 1 capital requirement of 16% of which 13.5% must be CET1 capital 79 REGULATORY CAPITAL CHANGES CAPITAL, FUNDING AND LIQUIDITY 1 Domestically systemically important bank (D-SIB). Westpac Group 2023 Full Year Results Presentation & Investor Discussion Pack |

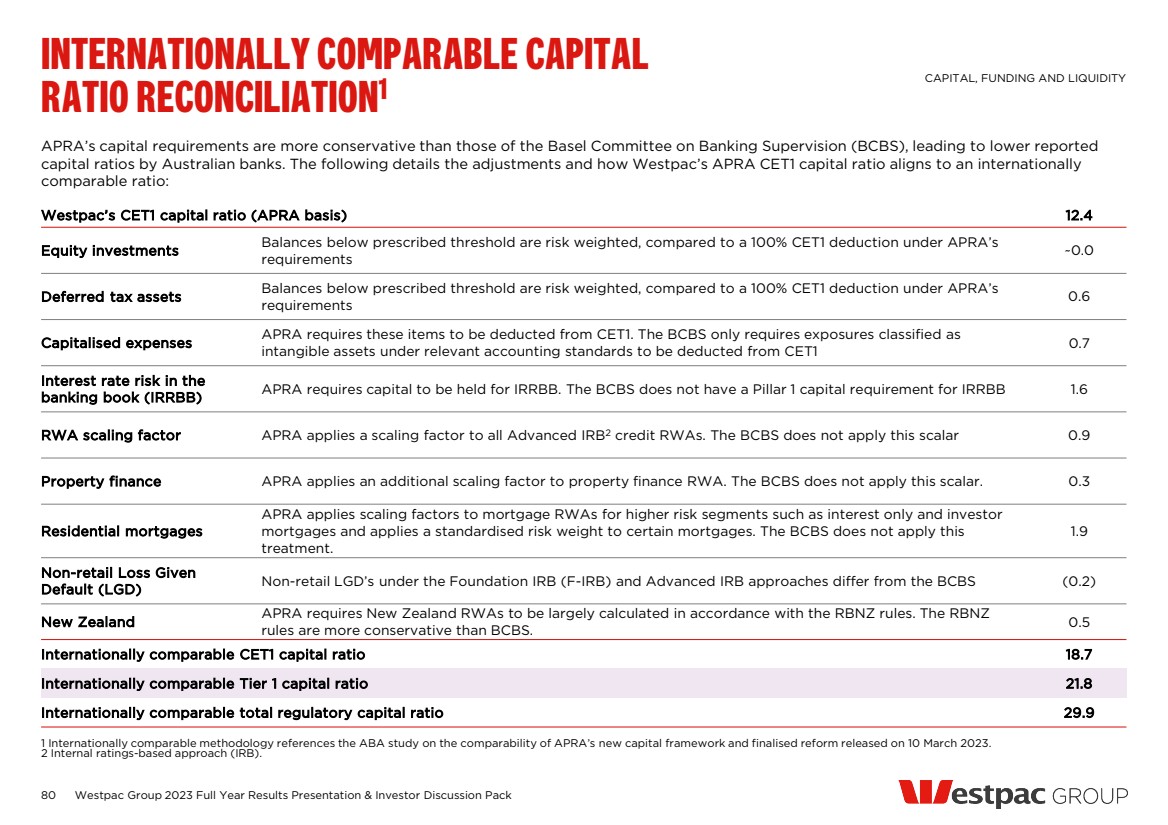

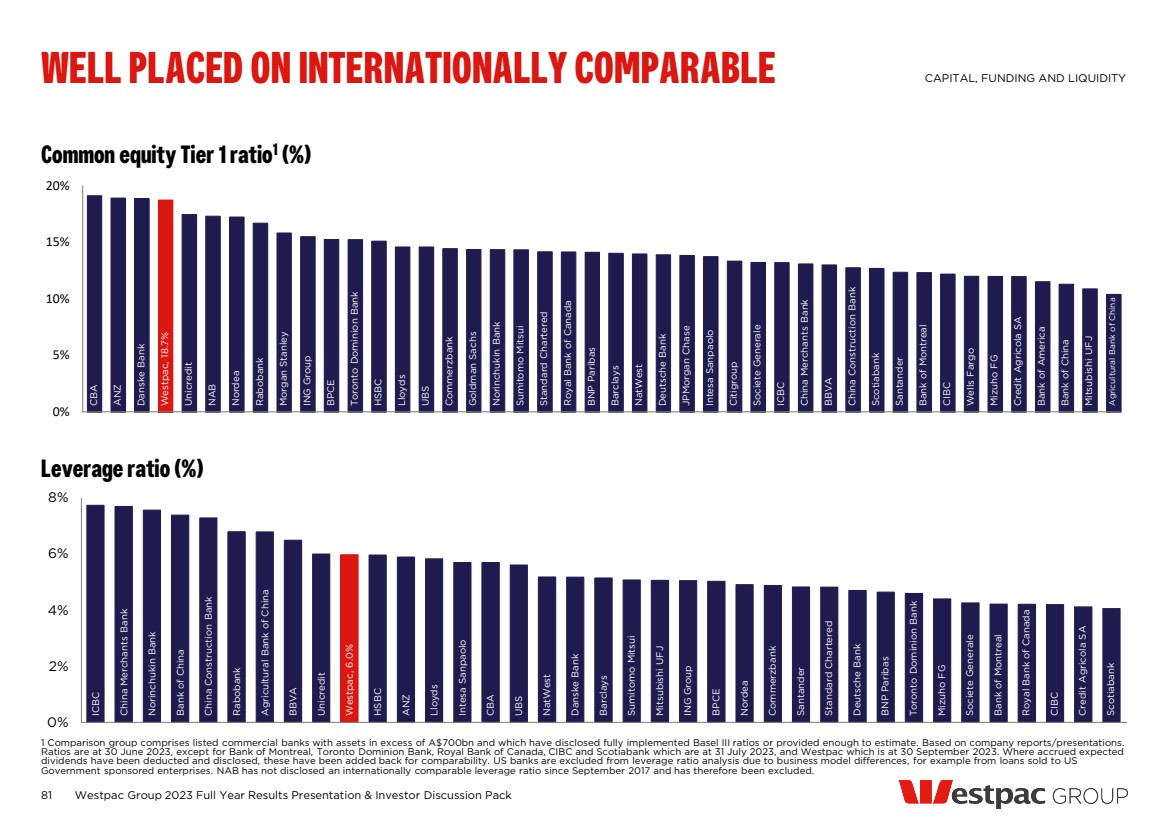

| APRA’s capital requirements are more conservative than those of the Basel Committee on Banking Supervision (BCBS), leading to lower reported capital ratios by Australian banks. The following details the adjustments and how Westpac’s APRA CET1 capital ratio aligns to an internationally comparable ratio: 80 INTERNATIONALLY COMPARABLE CAPITAL RATIO RECONCILIATION1 CAPITAL, FUNDING AND LIQUIDITY 1 Internationally comparable methodology references the ABA study on the comparability of APRA’s new capital framework and finalised reform released on 10 March 2023. 2 Internal ratings-based approach (IRB). Westpac’s CET1 capital ratio (APRA basis) 12.4 Equity investments Balances below prescribed threshold are risk weighted, compared to a 100% CET1 deduction under APRA’s requirements ~0.0 Deferred tax assets Balances below prescribed threshold are risk weighted, compared to a 100% CET1 deduction under APRA’s requirements 0.6 Capitalised expenses APRA requires these items to be deducted from CET1. The BCBS only requires exposures classified as intangible assets under relevant accounting standards to be deducted from CET1 0.7 Interest rate risk in the banking book (IRRBB) APRA requires capital to be held for IRRBB. The BCBS does not have a Pillar 1 capital requirement for IRRBB 1.6 RWA scaling factor APRA applies a scaling factor to all Advanced IRB2 credit RWAs. The BCBS does not apply this scalar 0.9 Property finance APRA applies an additional scaling factor to property finance RWA. The BCBS does not apply this scalar. 0.3 Residential mortgages APRA applies scaling factors to mortgage RWAs for higher risk segments such as interest only and investor mortgages and applies a standardised risk weight to certain mortgages. The BCBS does not apply this treatment. 1.9 Non-retail Loss Given Default (LGD) Non-retail LGD’s under the Foundation IRB (F-IRB) and Advanced IRB approaches differ from the BCBS (0.2) New Zealand APRA requires New Zealand RWAs to be largely calculated in accordance with the RBNZ rules. The RBNZ rules are more conservative than BCBS. 0.5 Internationally comparable CET1 capital ratio 18.7 Internationally comparable Tier 1 capital ratio 21.8 Internationally comparable total regulatory capital ratio 29.9 Westpac Group 2023 Full Year Results Presentation & Investor Discussion Pack |

| Common equity Tier 1 ratio1 (%) 0% 5% 10% 15% 20% 81 Leverage ratio (%) 0% 2% 4% 6% 8% Westpac Group 2023 Full Year Results Presentation & Investor Discussion Pack WELL PLACED ON INTERNATIONALLY COMPARABLE CAPITAL, FUNDING AND LIQUIDITY 1 Comparison group comprises listed commercial banks with assets in excess of A$700bn and which have disclosed fully implemented Basel III ratios or provided enough to estimate. Based on company reports/presentations. Ratios are at 30 June 2023, except for Bank of Montreal, Toronto Dominion Bank, Royal Bank of Canada, CIBC and Scotiabank which are at 31 July 2023, and Westpac which is at 30 September 2023. Where accrued expected dividends have been deducted and disclosed, these have been added back for comparability. US banks are excluded from leverage ratio analysis due to business model differences, for example from loans sold to US Government sponsored enterprises. NAB has not disclosed an internationally comparable leverage ratio since September 2017 and has therefore been excluded. CBA ANZ Danske Bank Westpac, 18.7% Unicredit NAB Nordea Rabobank Morgan Stanley ING Group BPCE Toronto Dominion Bank HSBC Lloyds UBS Commerzbank Goldman Sachs Norinchukin Bank Sumitomo Mitsui Standard Chartered Royal Bank of Canada BNP Paribas Barclays NatWest Deutsche Bank JPMorgan Chase Intesa Sanpaolo Citigroup Societe Generale ICBC China Merchants Bank BBVA China Construction Bank Scotiabank Santander Bank of Montreal CIBC Wells Fargo Mizuho FG Credit Agricola SA Bank of America Bank of China Mitsubishi UFJ Agricultural Bank of China ICBC China Merchants Bank Norinchukin Bank Bank of China China Construction Bank Rabobank Agricultural Bank of China BBVA Unicredit Westpac, 6.0% HSBC ANZ Lloyds Intesa Sanpaolo CBA UBS NatWest Danske Bank Barclays Sumitomo Mitsui Mitsubishi UFJ ING Group BPCE Nordea Commerzbank Santander Standard Chartered Deutsche Bank BNP Paribas Toronto Dominion Bank Mizuho FG Societe Generale Bank of Montreal Royal Bank of Canada CIBC Credit Agricola SA Scotiabank |