Exhibit 1

| ASX Release 4 November 2024 Westpac 2024 Second Half Financial Performance Review Westpac Banking Corporation (“Westpac”) today provides the attached Westpac 2024 Second Half Financial Performance Review. For further information: Hayden Cooper Justin McCarthy Group Head of Media Relations General Manager, Investor Relations 0402 393 619 0422 800 321 This document has been authorised for release by Tim Hartin, Company Secretary. Level 18, 275 Kent Street Sydney, NSW, 2000 |

| FINANCIAL PERFORMANCE REVIEW WESTPAC BANKING CORPORATION ABN 33 007 457 141 2024 SECOND HALF |

| 2 WESTPAC GROUP 2024 SECOND HALF FINANCIAL PERFORMANCE REVIEW Contents GROUP PERFORMANCE 3 Performance overview 3 Performance summary 4 Key financial information 5 Impact of Notable Items 6 Review of earnings 7 SEGMENT REPORTING 15 Consumer 16 Business & Wealth 18 Westpac Institutional Bank 20 Westpac New Zealand 22 Group Businesses 25 GLOSSARY OF ABBREVIATIONS AND DEFINED TERMS 27 CONTACT US 30 This report provides a discussion of the Group’s performance for the six months ended 30 September 2024 compared to the six months ended 31 March 2024, unless otherwise specified. Factors that relate primarily to a particular business segment are discussed in more detail in the Segment Reporting section. Certain amounts, measures and ratios presented in this overview are not defined by Australian Accounting Standards (AAS). These non-AAS measures include: • Performance measure excluding the impact of Notable Items; • Pre-provision profit; • Core net interest income and core net interest margin (Core NIM); and • Expense to income ratio (excluding Notable Items). These non-AAS measures and Notable Items are described in detail in the 2024 Annual Report. In this Report, a reference to 'Westpac', 'Group', 'Westpac Group', 'we', 'us' and 'our' is to Westpac Banking Corporation ABN 33 007 457 141 and its subsidiaries unless it clearly means just Westpac Banking Corporation. For certain information about the basis of preparing the financial information in this Report, see 'Reading this report' in the 2024 Annual Report. Information contained in or accessible through the websites mentioned in this Report does not form part of this report unless we specifically state that it is incorporated by reference and forms part of this report. All references in this report to websites are inactive textual references and are for information only. Westpac Banking Corporation ABN 33 007 457 141 |

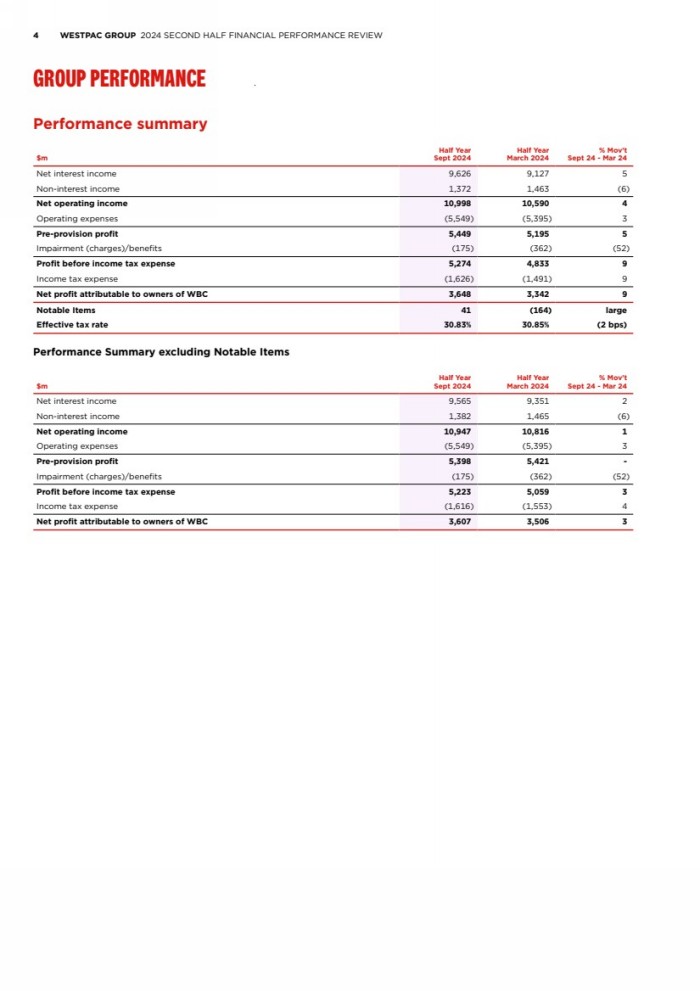

| GROUP PERFORMANCE SEGMENT REPORTING 3 GROUP PERFORMANCE Performance overview The Group's net profit for Second Half 2024 was $3,648 million, up 9% on the prior period. Excluding Notable Items, net profit increased 3% to $3,607 million. Pre-provision profit was $5,449 million, an increase of 5% on the prior period. Excluding Notable Items, pre-provision profit was little changed at $5,398 million driven by a 1% increase in operating income and a 3% increase in operating expenses. • Net interest income increased 5% to $9,626 million. Excluding Notable Items, net interest income increased 2% to $9,565 million reflecting disciplined management of net interest margins and balance sheet growth. This reflected a slight expansion of core net interest margin (NIM) and a 1% increase in average interest-earning assets. Growth in average interest-earning assets was driven by increases in owner occupied mortgages, and loans to business and institutional customers. Customer deposits increased 3% reflecting the improved strength of our customer franchise across all segments. • NIM was 1.97% and comprised: – Core NIM of 1.83% which expanded by 3 basis points with higher earnings on capital and hedged deposits partly offset by narrowing of deposit spreads as customers preferred higher yield savings and term deposits and tighter loan spreads due to lending competition, particularly in mortgages; – Treasury and Markets income of 13 basis points, down 1 basis point; and – Notable Items, related to accounting for hedges, added 6 basis points compared to detracting 5 basis points in the prior period. • Non-interest income of $1,372 million was 6% lower. Excluding Notable Items, non-interest income of $1,382 million was also down 6% mainly due to lower Markets income. • Operating expenses of $5,549 million increased 3% due to higher costs of third party technology vendors, higher wage and salary costs along with costs related to the UNITE program. Cost Reset actions provided a partial offset. Impairment charges were $175 million or 4 basis points of average loans, compared to 9 basis points of average loans in the prior half. The charge reflects lower Collectively Assessed Provisions (CAP), mainly from the reduction in overlays as the expected losses did not materialise or are now reflected in modelled outcomes. The effective tax rate of 30.8% was broadly in line with the Australian corporate tax rate of 30%. |

| 4 WESTPAC GROUP 2024 SECOND HALF FINANCIAL PERFORMANCE REVIEW GROUP PERFORMANCE Performance summary $m Half Year Sept 2024 Half Year March 2024 % Mov't Sept 24 - Mar 24 Net interest income 9,626 9,127 5 Non-interest income 1,372 1,463 (6) Net operating income 10,998 10,590 4 Operating expenses (5,549) (5,395) 3 Pre-provision profit 5,449 5,195 5 Impairment (charges)/benefits (175) (362) (52) Profit before income tax expense 5,274 4,833 9 Income tax expense (1,626) (1,491) 9 Net profit attributable to owners of WBC 3,648 3,342 9 Notable Items 41 (164) large Effective tax rate 30.83% 30.85% (2 bps) Performance Summary excluding Notable Items $m Half Year Sept 2024 Half Year March 2024 % Mov't Sept 24 - Mar 24 Net interest income 9,565 9,351 2 Non-interest income 1,382 1,465 (6) Net operating income 10,947 10,816 1 Operating expenses (5,549) (5,395) 3 Pre-provision profit 5,398 5,421 - Impairment (charges)/benefits (175) (362) (52) Profit before income tax expense 5,223 5,059 3 Income tax expense (1,616) (1,553) 4 Net profit attributable to owners of WBC 3,607 3,506 3 |

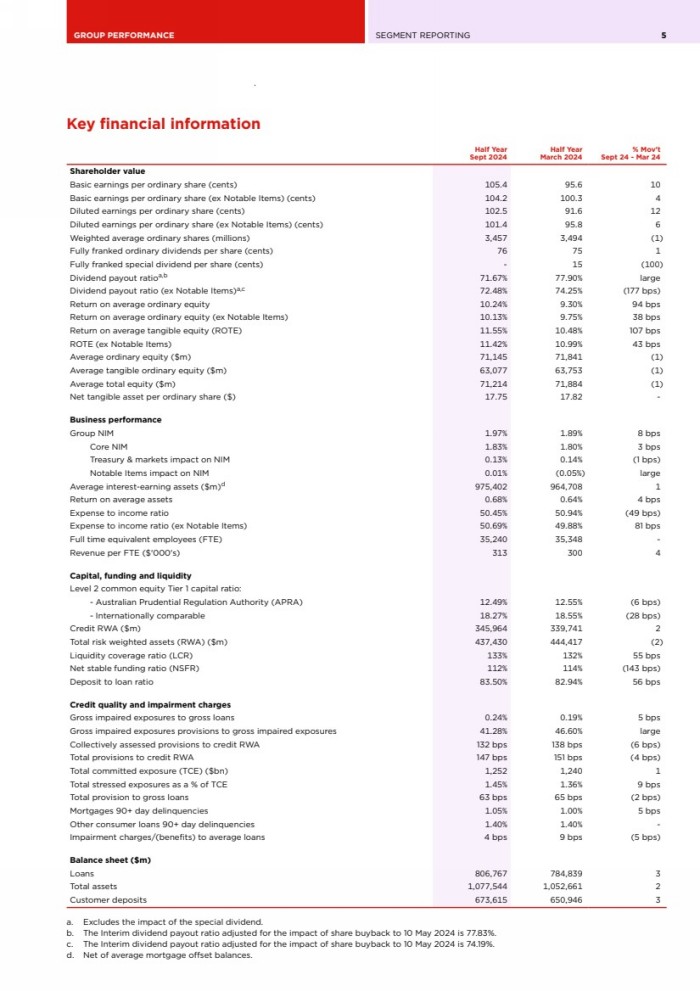

| GROUP PERFORMANCE SEGMENT REPORTING 5 Key financial information Half Year Sept 2024 Half Year March 2024 % Mov't Sept 24 - Mar 24 Shareholder value Basic earnings per ordinary share (cents) 105.4 95.6 10 Basic earnings per ordinary share (ex Notable Items) (cents) 104.2 100.3 4 Diluted earnings per ordinary share (cents) 102.5 91.6 12 Diluted earnings per ordinary share (ex Notable Items) (cents) 101.4 95.8 6 Weighted average ordinary shares (millions) 3,457 3,494 (1) Fully franked ordinary dividends per share (cents) 76 75 1 Fully franked special dividend per share (cents) - 15 (100) Dividend payout ratioa,b 71.67% 77.90% large Dividend payout ratio (ex Notable Items)a,c 72.48% 74.25% (177 bps) Return on average ordinary equity 10.24% 9.30% 94 bps Return on average ordinary equity (ex Notable Items) 10.13% 9.75% 38 bps Return on average tangible equity (ROTE) 11.55% 10.48% 107 bps ROTE (ex Notable Items) 11.42% 10.99% 43 bps Average ordinary equity ($m) 71,145 71,841 (1) Average tangible ordinary equity ($m) 63,077 63,753 (1) Average total equity ($m) 71,214 71,884 (1) Net tangible asset per ordinary share ($) 17.75 17.82 - Business performance Group NIM 1.97% 1.89% 8 bps Core NIM 1.83% 1.80% 3 bps Treasury & markets impact on NIM 0.13% 0.14% (1 bps) Notable Items impact on NIM 0.01% (0.05%) large Average interest-earning assets ($m)d 975,402 964,708 1 Return on average assets 0.68% 0.64% 4 bps Expense to income ratio 50.45% 50.94% (49 bps) Expense to income ratio (ex Notable Items) 50.69% 49.88% 81 bps Full time equivalent employees (FTE) 35,240 35,348 - Revenue per FTE ($'000's) 313 300 4 Capital, funding and liquidity Level 2 common equity Tier 1 capital ratio: - Australian Prudential Regulation Authority (APRA) 12.49% 12.55% (6 bps) - Internationally comparable 18.27% 18.55% (28 bps) Credit RWA ($m) 345,964 339,741 2 Total risk weighted assets (RWA) ($m) 437,430 444,417 (2) Liquidity coverage ratio (LCR) 133% 132% 55 bps Net stable funding ratio (NSFR) 112% 114% (143 bps) Deposit to loan ratio 83.50% 82.94% 56 bps Credit quality and impairment charges Gross impaired exposures to gross loans 0.24% 0.19% 5 bps Gross impaired exposures provisions to gross impaired exposures 41.28% 46.60% large Collectively assessed provisions to credit RWA 132 bps 138 bps (6 bps) Total provisions to credit RWA 147 bps 151 bps (4 bps) Total committed exposure (TCE) ($bn) 1,252 1,240 1 Total stressed exposures as a % of TCE 1.45% 1.36% 9 bps Total provision to gross loans 63 bps 65 bps (2 bps) Mortgages 90+ day delinquencies 1.05% 1.00% 5 bps Other consumer loans 90+ day delinquencies 1.40% 1.40% - Impairment charges/(benefits) to average loans 4 bps 9 bps (5 bps) Balance sheet ($m) Loans 806,767 784,839 3 Total assets 1,077,544 1,052,661 2 Customer deposits 673,615 650,946 3 a. Excludes the impact of the special dividend. b. The Interim dividend payout ratio adjusted for the impact of share buyback to 10 May 2024 is 77.83%. c. The Interim dividend payout ratio adjusted for the impact of share buyback to 10 May 2024 is 74.19%. d. Net of average mortgage offset balances. |

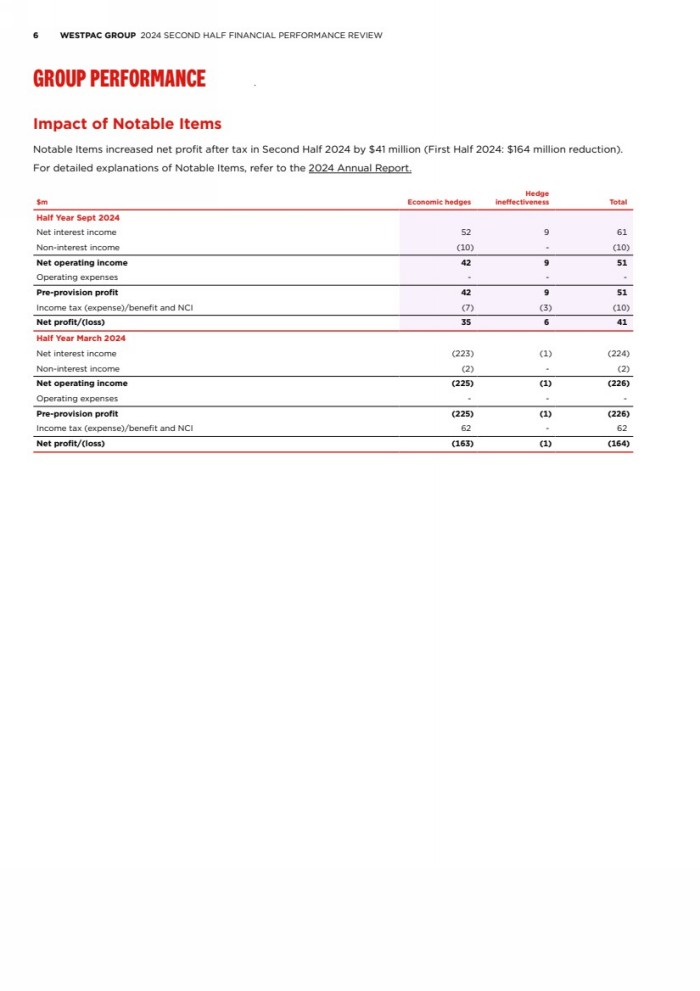

| 6 WESTPAC GROUP 2024 SECOND HALF FINANCIAL PERFORMANCE REVIEW GROUP PERFORMANCE Impact of Notable Items Notable Items increased net profit after tax in Second Half 2024 by $41 million (First Half 2024: $164 million reduction). For detailed explanations of Notable Items, refer to the 2024 Annual Report. $m Economic hedges Hedge ineffectiveness Total Half Year Sept 2024 Net interest income 52 9 61 Non-interest income (10) - (10) Net operating income 42 9 51 Operating expenses - - - Pre-provision profit 42 9 51 Income tax (expense)/benefit and NCI (7) (3) (10) Net profit/(loss) 35 6 41 Half Year March 2024 Net interest income (223) (1) (224) Non-interest income (2) - (2) Net operating income (225) (1) (226) Operating expenses - - - Pre-provision profit (225) (1) (226) Income tax (expense)/benefit and NCI 62 - 62 Net profit/(loss) (163) (1) (164) |

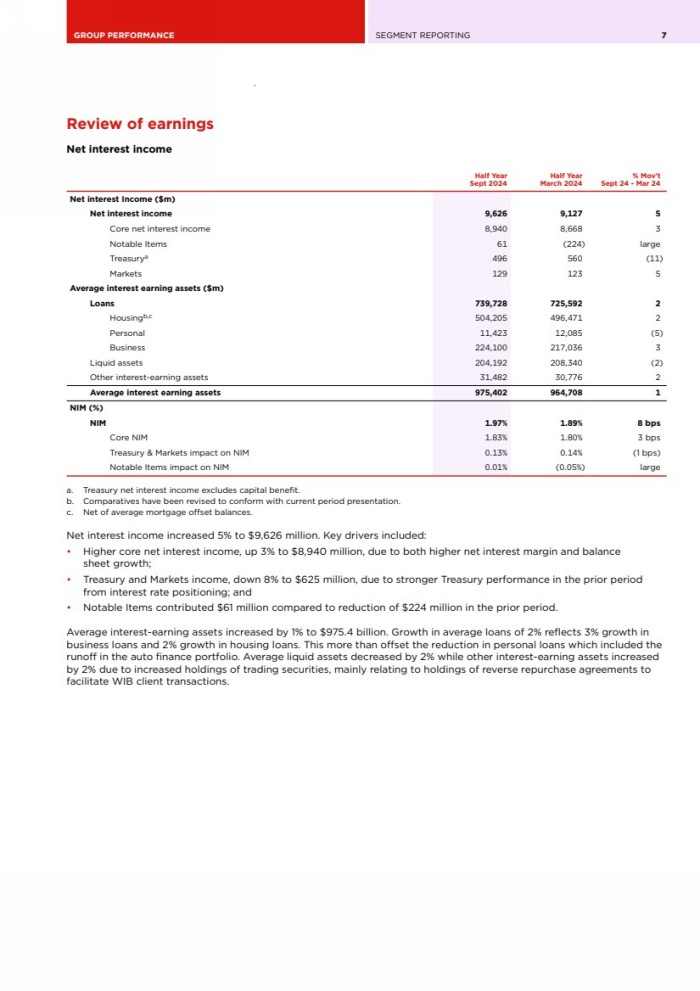

| GROUP PERFORMANCE SEGMENT REPORTING 7 Review of earnings Net interest income Half Year Sept 2024 Half Year March 2024 % Mov't Sept 24 - Mar 24 Net interest Income ($m) Net interest income 9,626 9,127 5 Core net interest income 8,940 8,668 3 Notable Items 61 (224) large Treasurya 496 560 (11) Markets 129 123 5 Average interest earning assets ($m) Loans 739,728 725,592 2 Housingb,c 504,205 496,471 2 Personal 11,423 12,085 (5) Business 224,100 217,036 3 Liquid assets 204,192 208,340 (2) Other interest-earning assets 31,482 30,776 2 Average interest earning assets 975,402 964,708 1 NIM (%) NIM 1.97% 1.89% 8 bps Core NIM 1.83% 1.80% 3 bps Treasury & Markets impact on NIM 0.13% 0.14% (1 bps) Notable Items impact on NIM 0.01% (0.05%) large a. Treasury net interest income excludes capital benefit. b. Comparatives have been revised to conform with current period presentation. c. Net of average mortgage offset balances. Net interest income increased 5% to $9,626 million. Key drivers included: • Higher core net interest income, up 3% to $8,940 million, due to both higher net interest margin and balance sheet growth; • Treasury and Markets income, down 8% to $625 million, due to stronger Treasury performance in the prior period from interest rate positioning; and • Notable Items contributed $61 million compared to reduction of $224 million in the prior period. Average interest-earning assets increased by 1% to $975.4 billion. Growth in average loans of 2% reflects 3% growth in business loans and 2% growth in housing loans. This more than offset the reduction in personal loans which included the runoff in the auto finance portfolio. Average liquid assets decreased by 2% while other interest-earning assets increased by 2% due to increased holdings of trading securities, mainly relating to holdings of reverse repurchase agreements to facilitate WIB client transactions. |

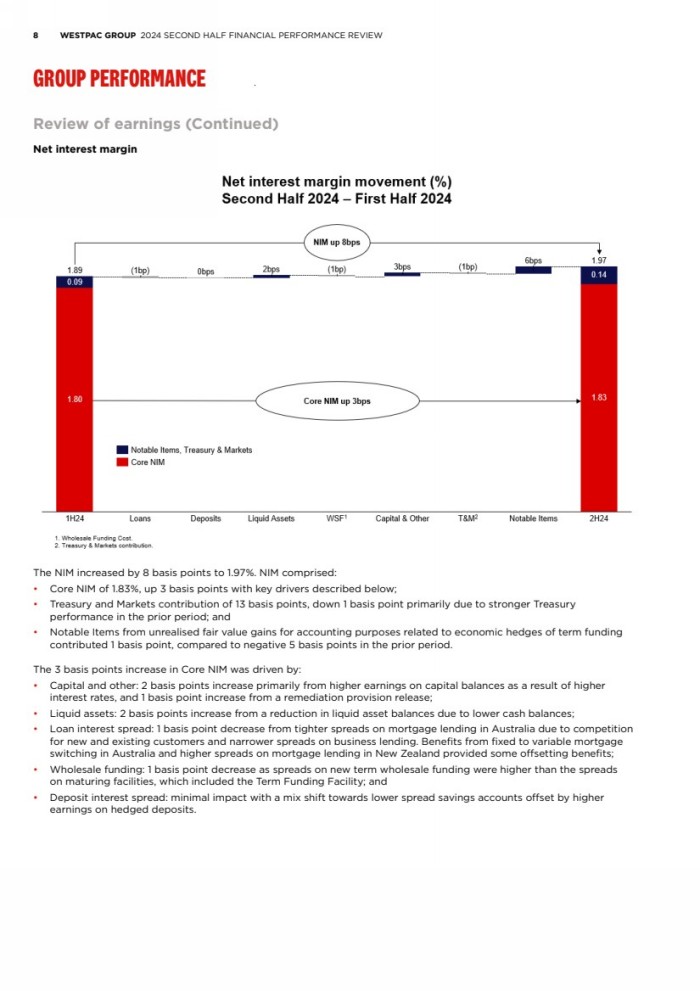

| 8 WESTPAC GROUP 2024 SECOND HALF FINANCIAL PERFORMANCE REVIEW GROUP PERFORMANCE Review of earnings (Continued) Net interest margin The NIM increased by 8 basis points to 1.97%. NIM comprised: • Core NIM of 1.83%, up 3 basis points with key drivers described below; • Treasury and Markets contribution of 13 basis points, down 1 basis point primarily due to stronger Treasury performance in the prior period; and • Notable Items from unrealised fair value gains for accounting purposes related to economic hedges of term funding contributed 1 basis point, compared to negative 5 basis points in the prior period. The 3 basis points increase in Core NIM was driven by: • Capital and other: 2 basis points increase primarily from higher earnings on capital balances as a result of higher interest rates, and 1 basis point increase from a remediation provision release; • Liquid assets: 2 basis points increase from a reduction in liquid asset balances due to lower cash balances; • Loan interest spread: 1 basis point decrease from tighter spreads on mortgage lending in Australia due to competition for new and existing customers and narrower spreads on business lending. Benefits from fixed to variable mortgage switching in Australia and higher spreads on mortgage lending in New Zealand provided some offsetting benefits; • Wholesale funding: 1 basis point decrease as spreads on new term wholesale funding were higher than the spreads on maturing facilities, which included the Term Funding Facility; and • Deposit interest spread: minimal impact with a mix shift towards lower spread savings accounts offset by higher earnings on hedged deposits. |

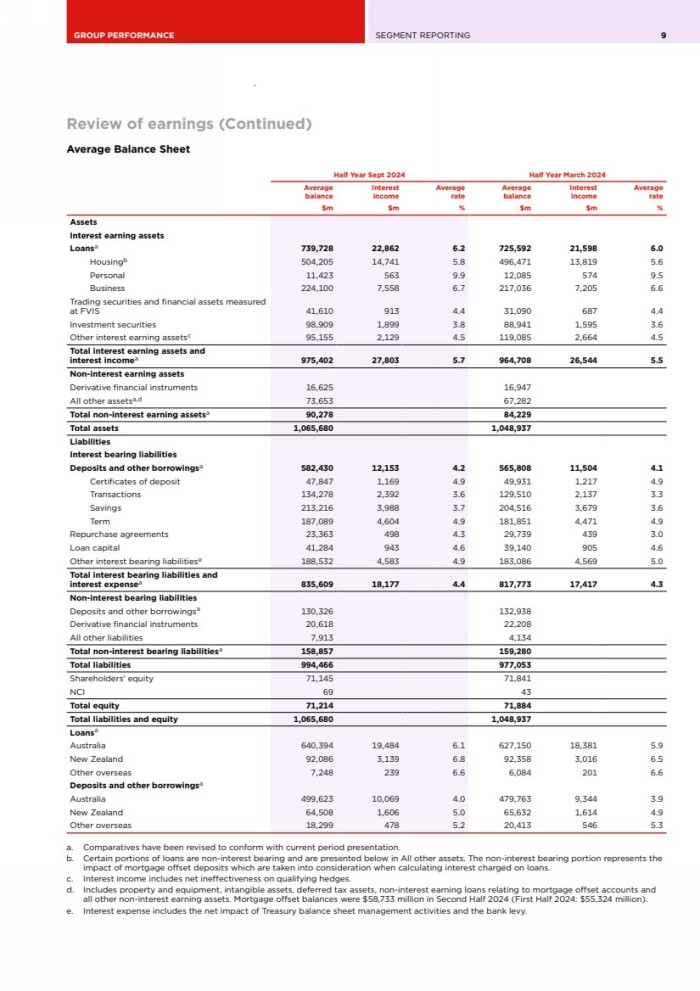

| GROUP PERFORMANCE SEGMENT REPORTING 9 Review of earnings (Continued) Average Balance Sheet Half Year Sept 2024 Half Year March 2024 Average balance Interest income Average rate Average balance Interest income Average rate $m $m % $m $m % Assets Interest earning assets Loansa 739,728 22,862 6.2 725,592 21,598 6.0 Housingb 504,205 14,741 5.8 496,471 13,819 5.6 Personal 11,423 563 9.9 12,085 574 9.5 Business 224,100 7,558 6.7 217,036 7,205 6.6 Trading securities and financial assets measured at FVIS 41,610 913 4.4 31,090 687 4.4 Investment securities 98,909 1,899 3.8 88,941 1,595 3.6 Other interest earning assetsc 95,155 2,129 4.5 119,085 2,664 4.5 Total interest earning assets and interest incomea 975,402 27,803 5.7 964,708 26,544 5.5 Non-interest earning assets Derivative financial instruments 16,625 16,947 All other assetsa,d 73,653 67,282 Total non-interest earning assetsa 90,278 84,229 Total assets 1,065,680 1,048,937 Liabilities Interest bearing liabilities Deposits and other borrowingsa 582,430 12,153 4.2 565,808 11,504 4.1 Certificates of deposit 47,847 1,169 4.9 49,931 1,217 4.9 Transactions 134,278 2,392 3.6 129,510 2,137 3.3 Savings 213,216 3,988 3.7 204,516 3,679 3.6 Term 187,089 4,604 4.9 181,851 4,471 4.9 Repurchase agreements 23,363 498 4.3 29,739 439 3.0 Loan capital 41,284 943 4.6 39,140 905 4.6 Other interest bearing liabilitiese 188,532 4,583 4.9 183,086 4,569 5.0 Total interest bearing liabilities and interest expensea 835,609 18,177 4.4 817,773 17,417 4.3 Non-interest bearing liabilities Deposits and other borrowingsa 130,326 132,938 Derivative financial instruments 20,618 22,208 All other liabilities 7,913 4,134 Total non-interest bearing liabilitiesa 158,857 159,280 Total liabilities 994,466 977,053 Shareholders' equity 71,145 71,841 NCI 69 43 Total equity 71,214 71,884 Total liabilities and equity 1,065,680 1,048,937 Loansa Australia 640,394 19,484 6.1 627,150 18,381 5.9 New Zealand 92,086 3,139 6.8 92,358 3,016 6.5 Other overseas 7,248 239 6.6 6,084 201 6.6 Deposits and other borrowingsa Australia 499,623 10,069 4.0 479,763 9,344 3.9 New Zealand 64,508 1,606 5.0 65,632 1,614 4.9 Other overseas 18,299 478 5.2 20,413 546 5.3 a. Comparatives have been revised to conform with current period presentation. b. Certain portions of loans are non-interest bearing and are presented below in All other assets. The non-interest bearing portion represents the impact of mortgage offset deposits which are taken into consideration when calculating interest charged on loans. c. Interest income includes net ineffectiveness on qualifying hedges. d. Includes property and equipment, intangible assets, deferred tax assets, non-interest earning loans relating to mortgage offset accounts and all other non-interest earning assets. Mortgage offset balances were $58,733 million in Second Half 2024 (First Half 2024: $55,324 million). e. Interest expense includes the net impact of Treasury balance sheet management activities and the bank levy. |

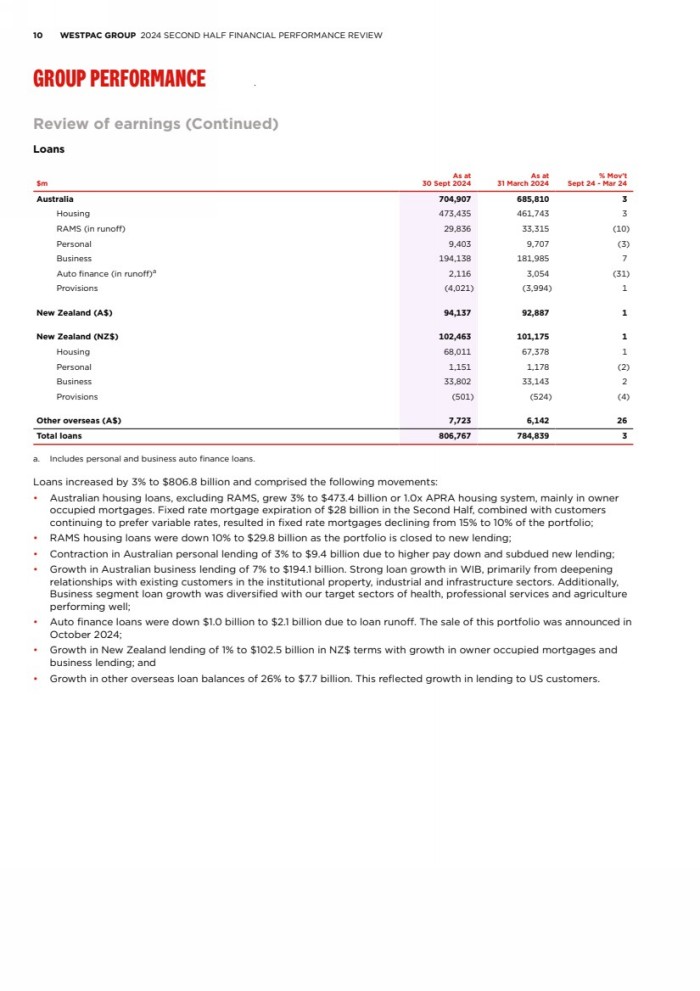

| 10 WESTPAC GROUP 2024 SECOND HALF FINANCIAL PERFORMANCE REVIEW GROUP PERFORMANCE Review of earnings (Continued) Loans $m As at 30 Sept 2024 As at 31 March 2024 % Mov't Sept 24 - Mar 24 Australia 704,907 685,810 3 Housing 473,435 461,743 3 RAMS (in runoff) 29,836 33,315 (10) Personal 9,403 9,707 (3) Business 194,138 181,985 7 Auto finance (in runoff)a 2,116 3,054 (31) Provisions (4,021) (3,994) 1 New Zealand (A$) 94,137 92,887 1 New Zealand (NZ$) 102,463 101,175 1 Housing 68,011 67,378 1 Personal 1,151 1,178 (2) Business 33,802 33,143 2 Provisions (501) (524) (4) Other overseas (A$) 7,723 6,142 26 Total loans 806,767 784,839 3 a. Includes personal and business auto finance loans. Loans increased by 3% to $806.8 billion and comprised the following movements: • Australian housing loans, excluding RAMS, grew 3% to $473.4 billion or 1.0x APRA housing system, mainly in owner occupied mortgages. Fixed rate mortgage expiration of $28 billion in the Second Half, combined with customers continuing to prefer variable rates, resulted in fixed rate mortgages declining from 15% to 10% of the portfolio; • RAMS housing loans were down 10% to $29.8 billion as the portfolio is closed to new lending; • Contraction in Australian personal lending of 3% to $9.4 billion due to higher pay down and subdued new lending; • Growth in Australian business lending of 7% to $194.1 billion. Strong loan growth in WIB, primarily from deepening relationships with existing customers in the institutional property, industrial and infrastructure sectors. Additionally, Business segment loan growth was diversified with our target sectors of health, professional services and agriculture performing well; • Auto finance loans were down $1.0 billion to $2.1 billion due to loan runoff. The sale of this portfolio was announced in October 2024; • Growth in New Zealand lending of 1% to $102.5 billion in NZ$ terms with growth in owner occupied mortgages and business lending; and • Growth in other overseas loan balances of 26% to $7.7 billion. This reflected growth in lending to US customers. |

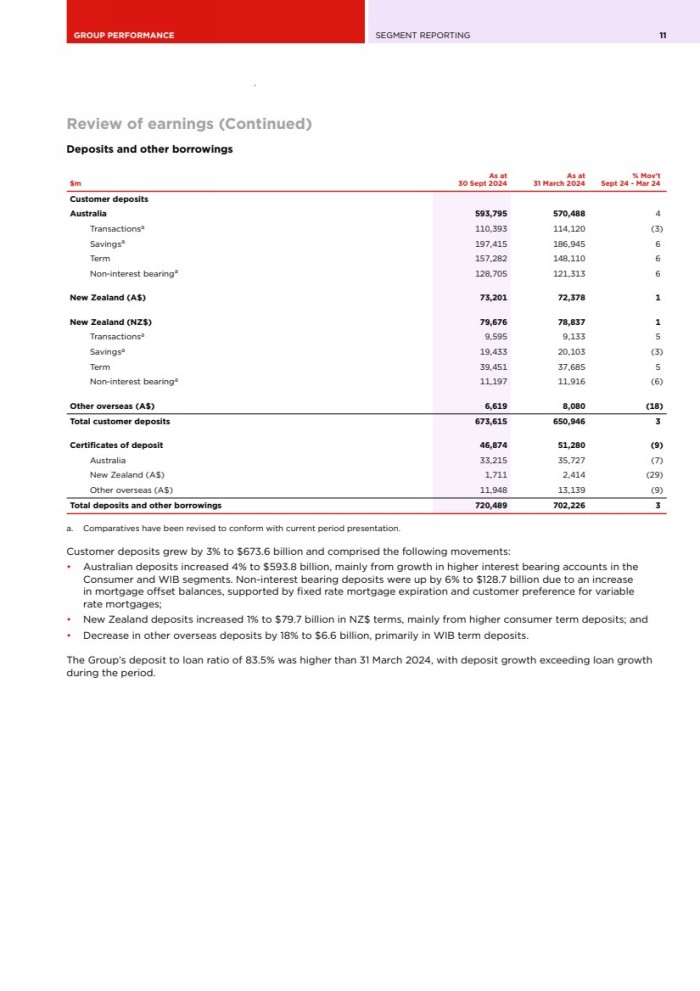

| GROUP PERFORMANCE SEGMENT REPORTING 11 Review of earnings (Continued) Deposits and other borrowings $m As at 30 Sept 2024 As at 31 March 2024 % Mov't Sept 24 - Mar 24 Customer deposits Australia 593,795 570,488 4 Transactionsa 110,393 114,120 (3) Savingsa 197,415 186,945 6 Term 157,282 148,110 6 Non-interest bearinga 128,705 121,313 6 New Zealand (A$) 73,201 72,378 1 New Zealand (NZ$) 79,676 78,837 1 Transactionsa 9,595 9,133 5 Savingsa 19,433 20,103 (3) Term 39,451 37,685 5 Non-interest bearinga 11,197 11,916 (6) Other overseas (A$) 6,619 8,080 (18) Total customer deposits 673,615 650,946 3 Certificates of deposit 46,874 51,280 (9) Australia 33,215 35,727 (7) New Zealand (A$) 1,711 2,414 (29) Other overseas (A$) 11,948 13,139 (9) Total deposits and other borrowings 720,489 702,226 3 a. Comparatives have been revised to conform with current period presentation. Customer deposits grew by 3% to $673.6 billion and comprised the following movements: • Australian deposits increased 4% to $593.8 billion, mainly from growth in higher interest bearing accounts in the Consumer and WIB segments. Non-interest bearing deposits were up by 6% to $128.7 billion due to an increase in mortgage offset balances, supported by fixed rate mortgage expiration and customer preference for variable rate mortgages; • New Zealand deposits increased 1% to $79.7 billion in NZ$ terms, mainly from higher consumer term deposits; and • Decrease in other overseas deposits by 18% to $6.6 billion, primarily in WIB term deposits. The Group’s deposit to loan ratio of 83.5% was higher than 31 March 2024, with deposit growth exceeding loan growth during the period. |

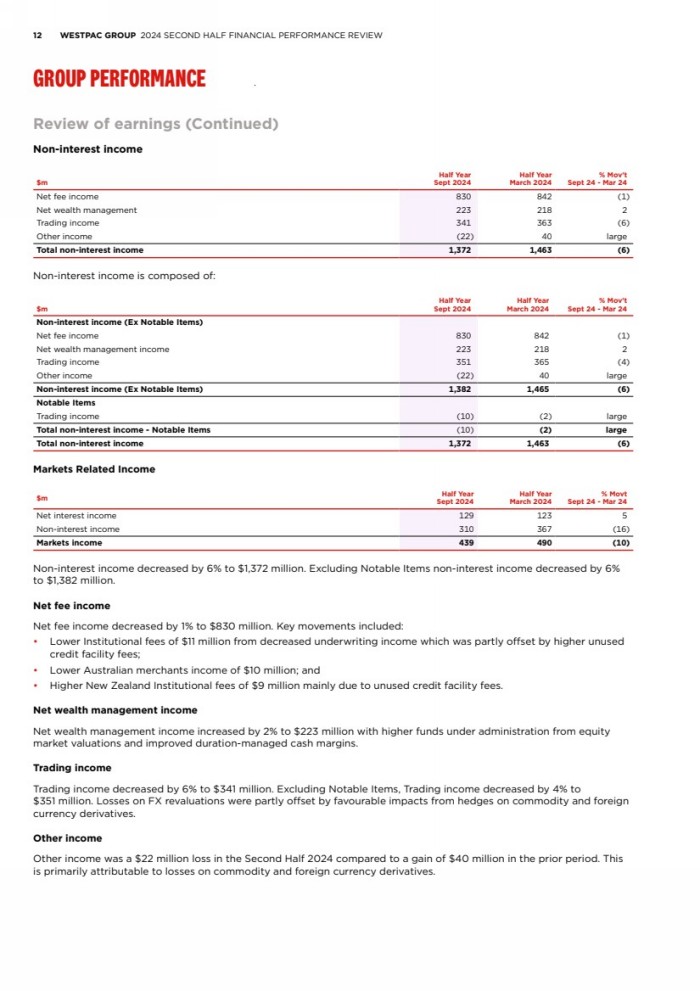

| 12 WESTPAC GROUP 2024 SECOND HALF FINANCIAL PERFORMANCE REVIEW GROUP PERFORMANCE Review of earnings (Continued) Non-interest income $m Half Year Sept 2024 Half Year March 2024 % Mov't Sept 24 - Mar 24 Net fee income 830 842 (1) Net wealth management 223 218 2 Trading income 341 363 (6) Other income (22) 40 large Total non-interest income 1,372 1,463 (6) Non-interest income is composed of: $m Half Year Sept 2024 Half Year March 2024 % Mov't Sept 24 - Mar 24 Non-interest income (Ex Notable Items) Net fee income 830 842 (1) Net wealth management income 223 218 2 Trading income 351 365 (4) Other income (22) 40 large Non-interest income (Ex Notable Items) 1,382 1,465 (6) Notable Items Trading income (10) (2) large Total non-interest income - Notable Items (10) (2) large Total non-interest income 1,372 1,463 (6) Markets Related Income $m Half Year Sept 2024 Half Year March 2024 % Movt Sept 24 - Mar 24 Net interest income 129 123 5 Non-interest income 310 367 (16) Markets income 439 490 (10) Non-interest income decreased by 6% to $1,372 million. Excluding Notable Items non-interest income decreased by 6% to $1,382 million. Net fee income Net fee income decreased by 1% to $830 million. Key movements included: • Lower Institutional fees of $11 million from decreased underwriting income which was partly offset by higher unused credit facility fees; • Lower Australian merchants income of $10 million; and • Higher New Zealand Institutional fees of $9 million mainly due to unused credit facility fees. Net wealth management income Net wealth management income increased by 2% to $223 million with higher funds under administration from equity market valuations and improved duration-managed cash margins. Trading income Trading income decreased by 6% to $341 million. Excluding Notable Items, Trading income decreased by 4% to $351 million. Losses on FX revaluations were partly offset by favourable impacts from hedges on commodity and foreign currency derivatives. Other income Other income was a $22 million loss in the Second Half 2024 compared to a gain of $40 million in the prior period. This is primarily attributable to losses on commodity and foreign currency derivatives. |

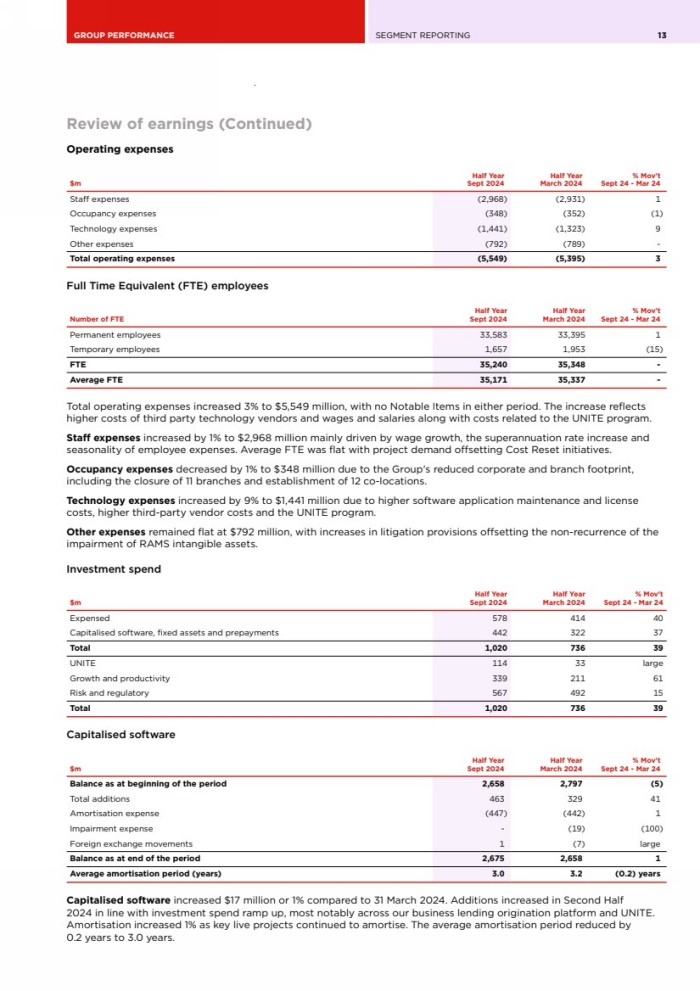

| GROUP PERFORMANCE SEGMENT REPORTING 13 Review of earnings (Continued) Operating expenses $m Half Year Sept 2024 Half Year March 2024 % Mov't Sept 24 - Mar 24 Staff expenses (2,968) (2,931) 1 Occupancy expenses (348) (352) (1) Technology expenses (1,441) (1,323) 9 Other expenses (792) (789) - Total operating expenses (5,549) (5,395) 3 Full Time Equivalent (FTE) employees Number of FTE Half Year Sept 2024 Half Year March 2024 % Mov't Sept 24 - Mar 24 Permanent employees 33,583 33,395 1 Temporary employees 1,657 1,953 (15) FTE 35,240 35,348 - Average FTE 35,171 35,337 - Total operating expenses increased 3% to $5,549 million, with no Notable Items in either period. The increase reflects higher costs of third party technology vendors and wages and salaries along with costs related to the UNITE program. Staff expenses increased by 1% to $2,968 million mainly driven by wage growth, the superannuation rate increase and seasonality of employee expenses. Average FTE was flat with project demand offsetting Cost Reset initiatives. Occupancy expenses decreased by 1% to $348 million due to the Group's reduced corporate and branch footprint, including the closure of 11 branches and establishment of 12 co-locations. Technology expenses increased by 9% to $1,441 million due to higher software application maintenance and license costs, higher third-party vendor costs and the UNITE program. Other expenses remained flat at $792 million, with increases in litigation provisions offsetting the non-recurrence of the impairment of RAMS intangible assets. Investment spend $m Half Year Sept 2024 Half Year March 2024 % Mov't Sept 24 - Mar 24 Expensed 578 414 40 Capitalised software, fixed assets and prepayments 442 322 37 Total 1,020 736 39 UNITE 114 33 large Growth and productivity 339 211 61 Risk and regulatory 567 492 15 Total 1,020 736 39 Capitalised software $m Half Year Sept 2024 Half Year March 2024 % Mov't Sept 24 - Mar 24 Balance as at beginning of the period 2,658 2,797 (5) Total additions 463 329 41 Amortisation expense (447) (442) 1 Impairment expense - (19) (100) Foreign exchange movements 1 (7) large Balance as at end of the period 2,675 2,658 1 Average amortisation period (years) 3.0 3.2 (0.2) years Capitalised software increased $17 million or 1% compared to 31 March 2024. Additions increased in Second Half 2024 in line with investment spend ramp up, most notably across our business lending origination platform and UNITE. Amortisation increased 1% as key live projects continued to amortise. The average amortisation period reduced by 0.2 years to 3.0 years. |

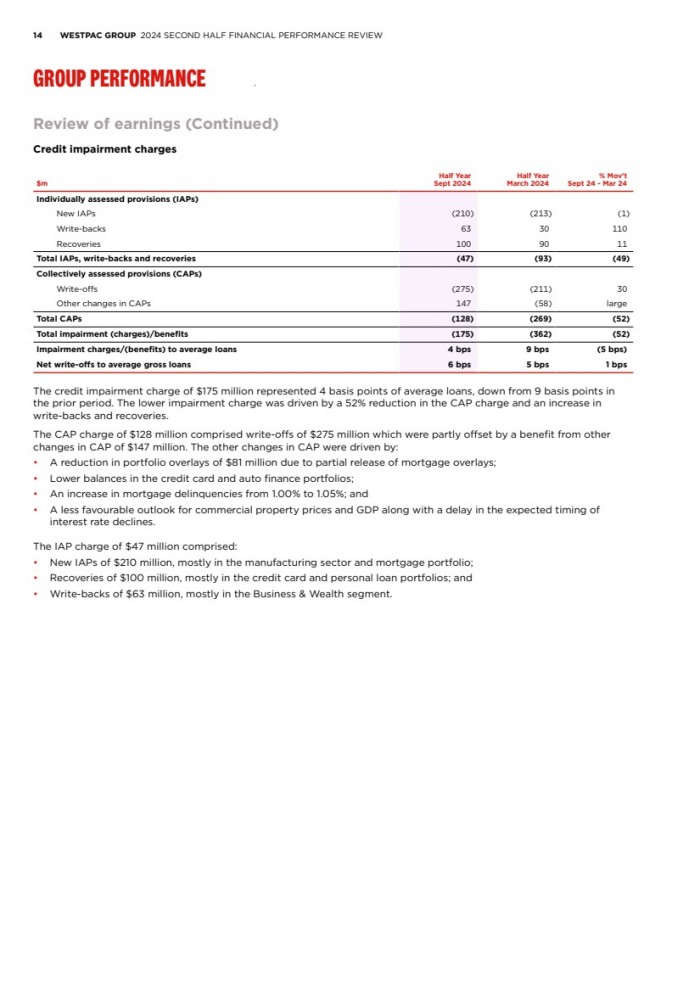

| 14 WESTPAC GROUP 2024 SECOND HALF FINANCIAL PERFORMANCE REVIEW GROUP PERFORMANCE Review of earnings (Continued) Credit impairment charges $m Half Year Sept 2024 Half Year March 2024 % Mov't Sept 24 - Mar 24 Individually assessed provisions (IAPs) New IAPs (210) (213) (1) Write-backs 63 30 110 Recoveries 100 90 11 Total IAPs, write-backs and recoveries (47) (93) (49) Collectively assessed provisions (CAPs) Write-offs (275) (211) 30 Other changes in CAPs 147 (58) large Total CAPs (128) (269) (52) Total impairment (charges)/benefits (175) (362) (52) Impairment charges/(benefits) to average loans 4 bps 9 bps (5 bps) Net write-offs to average gross loans 6 bps 5 bps 1 bps The credit impairment charge of $175 million represented 4 basis points of average loans, down from 9 basis points in the prior period. The lower impairment charge was driven by a 52% reduction in the CAP charge and an increase in write-backs and recoveries. The CAP charge of $128 million comprised write-offs of $275 million which were partly offset by a benefit from other changes in CAP of $147 million. The other changes in CAP were driven by: • A reduction in portfolio overlays of $81 million due to partial release of mortgage overlays; • Lower balances in the credit card and auto finance portfolios; • An increase in mortgage delinquencies from 1.00% to 1.05%; and • A less favourable outlook for commercial property prices and GDP along with a delay in the expected timing of interest rate declines. The IAP charge of $47 million comprised: • New IAPs of $210 million, mostly in the manufacturing sector and mortgage portfolio; • Recoveries of $100 million, mostly in the credit card and personal loan portfolios; and • Write-backs of $63 million, mostly in the Business & Wealth segment. |

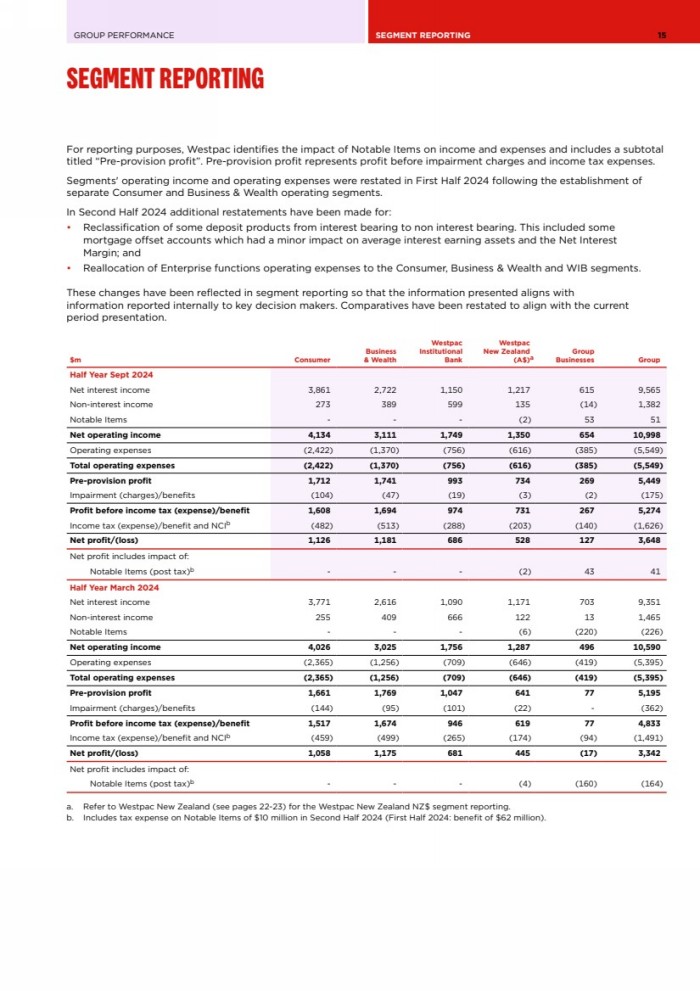

| GROUP PERFORMANCE SEGMENT REPORTING 15 SEGMENT REPORTING For reporting purposes, Westpac identifies the impact of Notable Items on income and expenses and includes a subtotal titled “Pre-provision profit”. Pre-provision profit represents profit before impairment charges and income tax expenses. Segments' operating income and operating expenses were restated in First Half 2024 following the establishment of separate Consumer and Business & Wealth operating segments. In Second Half 2024 additional restatements have been made for: • Reclassification of some deposit products from interest bearing to non interest bearing. This included some mortgage offset accounts which had a minor impact on average interest earning assets and the Net Interest Margin; and • Reallocation of Enterprise functions operating expenses to the Consumer, Business & Wealth and WIB segments. These changes have been reflected in segment reporting so that the information presented aligns with information reported internally to key decision makers. Comparatives have been restated to align with the current period presentation. $m Consumer Business & Wealth Westpac Institutional Bank Westpac New Zealand (A$)a Group Businesses Group Half Year Sept 2024 Net interest income 3,861 2,722 1,150 1,217 615 9,565 Non-interest income 273 389 599 135 (14) 1,382 Notable Items - - - (2) 53 51 Net operating income 4,134 3,111 1,749 1,350 654 10,998 Operating expenses (2,422) (1,370) (756) (616) (385) (5,549) Total operating expenses (2,422) (1,370) (756) (616) (385) (5,549) Pre-provision profit 1,712 1,741 993 734 269 5,449 Impairment (charges)/benefits (104) (47) (19) (3) (2) (175) Profit before income tax (expense)/benefit 1,608 1,694 974 731 267 5,274 Income tax (expense)/benefit and NCIb (482) (513) (288) (203) (140) (1,626) Net profit/(loss) 1,126 1,181 686 528 127 3,648 Net profit includes impact of: Notable Items (post tax)b - - - (2) 43 41 Half Year March 2024 Net interest income 3,771 2,616 1,090 1,171 703 9,351 Non-interest income 255 409 666 122 13 1,465 Notable Items - - - (6) (220) (226) Net operating income 4,026 3,025 1,756 1,287 496 10,590 Operating expenses (2,365) (1,256) (709) (646) (419) (5,395) Total operating expenses (2,365) (1,256) (709) (646) (419) (5,395) Pre-provision profit 1,661 1,769 1,047 641 77 5,195 Impairment (charges)/benefits (144) (95) (101) (22) - (362) Profit before income tax (expense)/benefit 1,517 1,674 946 619 77 4,833 Income tax (expense)/benefit and NCIb (459) (499) (265) (174) (94) (1,491) Net profit/(loss) 1,058 1,175 681 445 (17) 3,342 Net profit includes impact of: Notable Items (post tax)b - - - (4) (160) (164) a. Refer to Westpac New Zealand (see pages 22-23) for the Westpac New Zealand NZ$ segment reporting. b. Includes tax expense on Notable Items of $10 million in Second Half 2024 (First Half 2024: benefit of $62 million). |

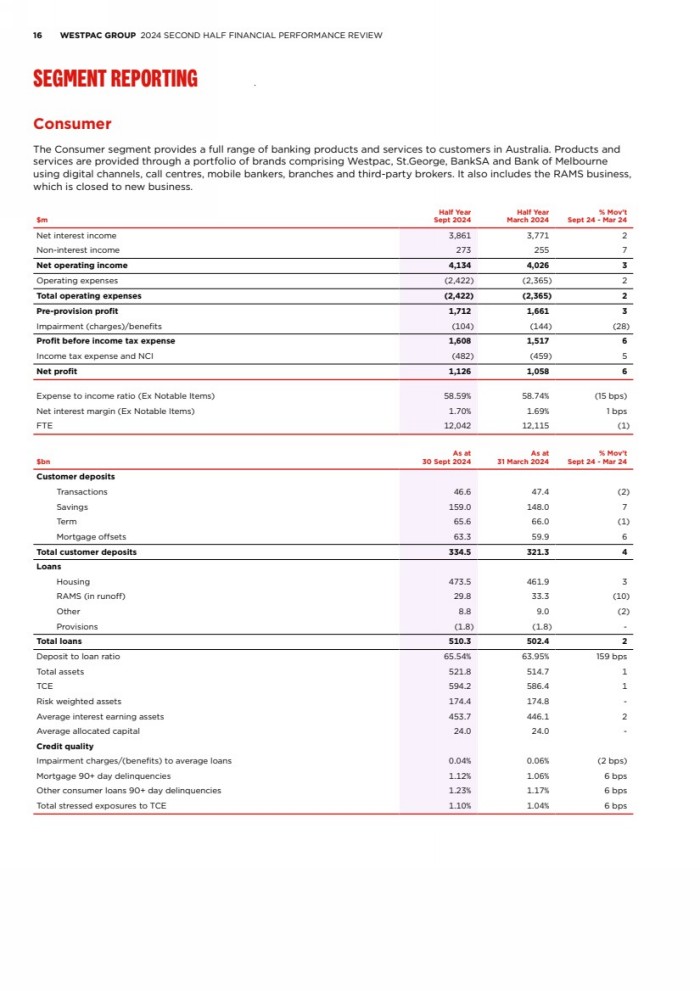

| 16 WESTPAC GROUP 2024 SECOND HALF FINANCIAL PERFORMANCE REVIEW SEGMENT REPORTING Consumer The Consumer segment provides a full range of banking products and services to customers in Australia. Products and services are provided through a portfolio of brands comprising Westpac, St.George, BankSA and Bank of Melbourne using digital channels, call centres, mobile bankers, branches and third-party brokers. It also includes the RAMS business, which is closed to new business. $m Half Year Sept 2024 Half Year March 2024 % Mov't Sept 24 - Mar 24 Net interest income 3,861 3,771 2 Non-interest income 273 255 7 Net operating income 4,134 4,026 3 Operating expenses (2,422) (2,365) 2 Total operating expenses (2,422) (2,365) 2 Pre-provision profit 1,712 1,661 3 Impairment (charges)/benefits (104) (144) (28) Profit before income tax expense 1,608 1,517 6 Income tax expense and NCI (482) (459) 5 Net profit 1,126 1,058 6 Expense to income ratio (Ex Notable Items) 58.59% 58.74% (15 bps) Net interest margin (Ex Notable Items) 1.70% 1.69% 1 bps FTE 12,042 12,115 (1) $bn As at 30 Sept 2024 As at 31 March 2024 % Mov't Sept 24 - Mar 24 Customer deposits Transactions 46.6 47.4 (2) Savings 159.0 148.0 7 Term 65.6 66.0 (1) Mortgage offsets 63.3 59.9 6 Total customer deposits 334.5 321.3 4 Loans Housing 473.5 461.9 3 RAMS (in runoff) 29.8 33.3 (10) Other 8.8 9.0 (2) Provisions (1.8) (1.8) - Total loans 510.3 502.4 2 Deposit to loan ratio 65.54% 63.95% 159 bps Total assets 521.8 514.7 1 TCE 594.2 586.4 1 Risk weighted assets 174.4 174.8 - Average interest earning assets 453.7 446.1 2 Average allocated capital 24.0 24.0 - Credit quality Impairment charges/(benefits) to average loans 0.04% 0.06% (2 bps) Mortgage 90+ day delinquencies 1.12% 1.06% 6 bps Other consumer loans 90+ day delinquencies 1.23% 1.17% 6 bps Total stressed exposures to TCE 1.10% 1.04% 6 bps |

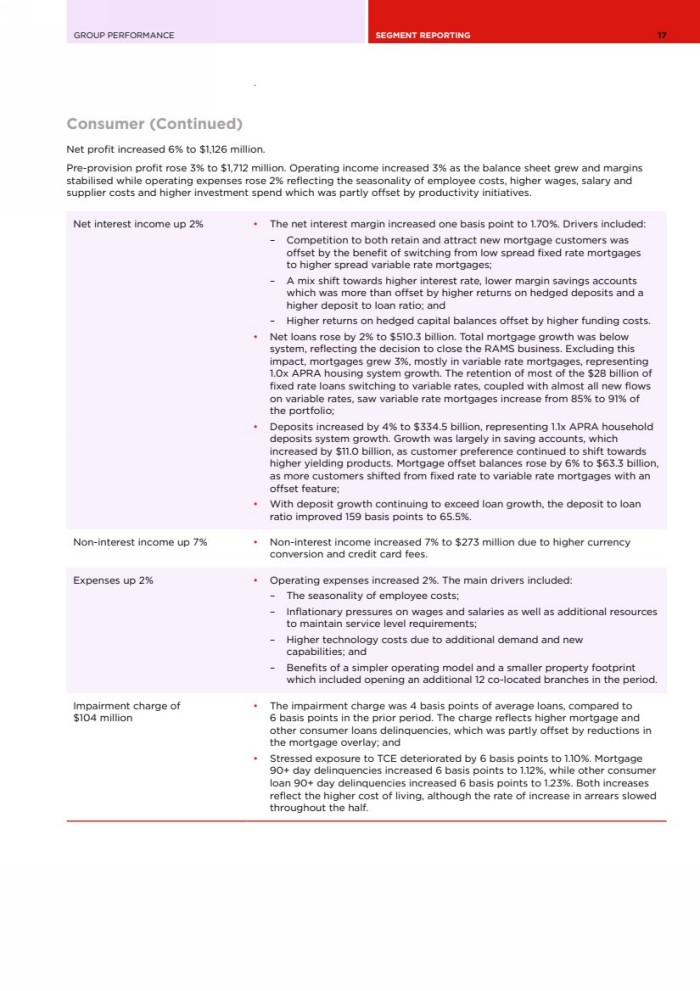

| GROUP PERFORMANCE SEGMENT REPORTING 17 Consumer (Continued) Net profit increased 6% to $1,126 million. Pre-provision profit rose 3% to $1,712 million. Operating income increased 3% as the balance sheet grew and margins stabilised while operating expenses rose 2% reflecting the seasonality of employee costs, higher wages, salary and supplier costs and higher investment spend which was partly offset by productivity initiatives. Net interest income up 2% • The net interest margin increased one basis point to 1.70%. Drivers included: – Competition to both retain and attract new mortgage customers was offset by the benefit of switching from low spread fixed rate mortgages to higher spread variable rate mortgages; – A mix shift towards higher interest rate, lower margin savings accounts which was more than offset by higher returns on hedged deposits and a higher deposit to loan ratio; and – Higher returns on hedged capital balances offset by higher funding costs. • Net loans rose by 2% to $510.3 billion. Total mortgage growth was below system, reflecting the decision to close the RAMS business. Excluding this impact, mortgages grew 3%, mostly in variable rate mortgages, representing 1.0x APRA housing system growth. The retention of most of the $28 billion of fixed rate loans switching to variable rates, coupled with almost all new flows on variable rates, saw variable rate mortgages increase from 85% to 91% of the portfolio; • Deposits increased by 4% to $334.5 billion, representing 1.1x APRA household deposits system growth. Growth was largely in saving accounts, which increased by $11.0 billion, as customer preference continued to shift towards higher yielding products. Mortgage offset balances rose by 6% to $63.3 billion, as more customers shifted from fixed rate to variable rate mortgages with an offset feature; • With deposit growth continuing to exceed loan growth, the deposit to loan ratio improved 159 basis points to 65.5%. Non-interest income up 7% • Non-interest income increased 7% to $273 million due to higher currency conversion and credit card fees. Expenses up 2% • Operating expenses increased 2%. The main drivers included: – The seasonality of employee costs; – Inflationary pressures on wages and salaries as well as additional resources to maintain service level requirements; – Higher technology costs due to additional demand and new capabilities; and – Benefits of a simpler operating model and a smaller property footprint which included opening an additional 12 co-located branches in the period. Impairment charge of $104 million • The impairment charge was 4 basis points of average loans, compared to 6 basis points in the prior period. The charge reflects higher mortgage and other consumer loans delinquencies, which was partly offset by reductions in the mortgage overlay; and • Stressed exposure to TCE deteriorated by 6 basis points to 1.10%. Mortgage 90+ day delinquencies increased 6 basis points to 1.12%, while other consumer loan 90+ day delinquencies increased 6 basis points to 1.23%. Both increases reflect the higher cost of living, although the rate of increase in arrears slowed throughout the half. |

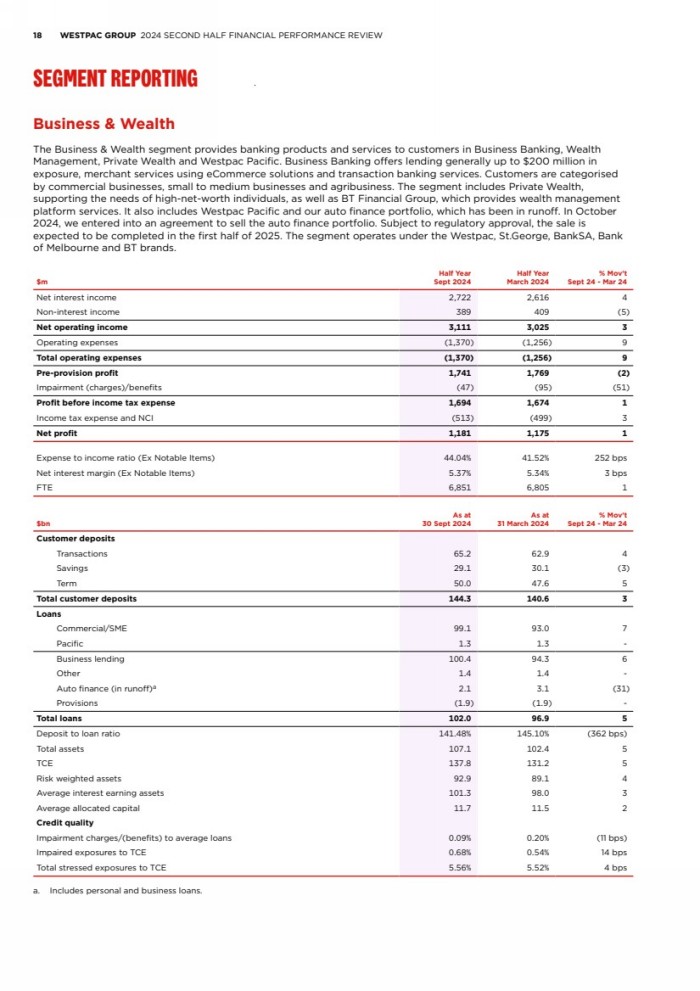

| 18 WESTPAC GROUP 2024 SECOND HALF FINANCIAL PERFORMANCE REVIEW SEGMENT REPORTING Business & Wealth The Business & Wealth segment provides banking products and services to customers in Business Banking, Wealth Management, Private Wealth and Westpac Pacific. Business Banking offers lending generally up to $200 million in exposure, merchant services using eCommerce solutions and transaction banking services. Customers are categorised by commercial businesses, small to medium businesses and agribusiness. The segment includes Private Wealth, supporting the needs of high-net-worth individuals, as well as BT Financial Group, which provides wealth management platform services. It also includes Westpac Pacific and our auto finance portfolio, which has been in runoff. In October 2024, we entered into an agreement to sell the auto finance portfolio. Subject to regulatory approval, the sale is expected to be completed in the first half of 2025. The segment operates under the Westpac, St.George, BankSA, Bank of Melbourne and BT brands. $m Half Year Sept 2024 Half Year March 2024 % Mov't Sept 24 - Mar 24 Net interest income 2,722 2,616 4 Non-interest income 389 409 (5) Net operating income 3,111 3,025 3 Operating expenses (1,370) (1,256) 9 Total operating expenses (1,370) (1,256) 9 Pre-provision profit 1,741 1,769 (2) Impairment (charges)/benefits (47) (95) (51) Profit before income tax expense 1,694 1,674 1 Income tax expense and NCI (513) (499) 3 Net profit 1,181 1,175 1 Expense to income ratio (Ex Notable Items) 44.04% 41.52% 252 bps Net interest margin (Ex Notable Items) 5.37% 5.34% 3 bps FTE 6,851 6,805 1 $bn As at 30 Sept 2024 As at 31 March 2024 % Mov't Sept 24 - Mar 24 Customer deposits Transactions 65.2 62.9 4 Savings 29.1 30.1 (3) Term 50.0 47.6 5 Total customer deposits 144.3 140.6 3 Loans Commercial/SME 99.1 93.0 7 Pacific 1.3 1.3 - Business lending 100.4 94.3 6 Other 1.4 1.4 - Auto finance (in runoff)a 2.1 3.1 (31) Provisions (1.9) (1.9) - Total loans 102.0 96.9 5 Deposit to loan ratio 141.48% 145.10% (362 bps) Total assets 107.1 102.4 5 TCE 137.8 131.2 5 Risk weighted assets 92.9 89.1 4 Average interest earning assets 101.3 98.0 3 Average allocated capital 11.7 11.5 2 Credit quality Impairment charges/(benefits) to average loans 0.09% 0.20% (11 bps) Impaired exposures to TCE 0.68% 0.54% 14 bps Total stressed exposures to TCE 5.56% 5.52% 4 bps a. Includes personal and business loans. |

| GROUP PERFORMANCE SEGMENT REPORTING 19 Business & Wealth (Continued) Net profit increased 1% to $1,181 million. Pre-provision profit declined 2% to $1,741 million with a 3% increase in operating income more than offset by a 9% rise in operating expenses. Operating expenses were higher reflecting higher salaries and wages and seasonality of employee costs, increased investment spend and an increase in litigation provisions while operating income benefited from strong lending growth and a higher net interest margin. Net interest income up 4% • The net interest margin rose 3 basis points reflecting provision releases and higher returns on hedged deposits and capital as previous interest rate rises continue to support the replicating portfolio. This was partially offset by higher wholesale funding costs, a mix shift from at call deposits to higher interest rate, lower margin term deposits and the continued runoff of the higher spread auto finance portfolio. Excluding the impact of auto finance, lending spreads were slightly down as margins were well managed, despite the competitive environment; • Net loans increased by 5% to $102.0 billion. Business lending growth of 6% was diversified with consistent growth across most industries and products. Our target industries of health, professional services and agriculture all performed well, with health growing strongly supported by the acquisition of Healthpoint. This was partly offset by the continued run down of the Auto finance portfolio to $2.1 billion. The sale of this portfolio was announced post balance date in October 2024; and • Deposits increased by 3% to $144.3 billion. Growth in term deposits of $2.4 billion and transaction accounts of $2.3 billion were partly offset by the decline in savings balances of $1.0 billion. Within the business segment, commercial and private wealth customer growth was more than offset by the reduction in balances across small and medium business customers from softer economic and trading conditions. Non-interest income down 5% • Non-interest income decreased 5% due to lower merchants income and trading activity. Expenses up 9% • Operating expenses were up 9%. Excluding the increase in litigation provisions, operating expenses increased 8% reflecting: – Higher salaries and wages and seasonality of employee costs; – Higher investment spend across the portfolio on the HealthPoint integration, UNITE and upgraded merchant terminals; and – Investment in business bankers to drive growth. Impairment charge of $47 million • The impairment charge of 9 basis points of average loans compared to 20 basis points in the prior period. The charge reflects higher new IAPs, which were partly offset by a small CAP benefit reflecting run off in the auto portfolio; and • Credit quality metrics deteriorated with stressed exposures to TCE up 4 basis points to 5.56%, mostly within the retail and wholesale trade sector. The proportion of impaired TCE increased 14 basis points to 0.68%. Platforms and Investments $bn As at 30 Sept 2024 Inflows Outflows Net Flows Other Mov't As at 31 March 2024 % Mov't Sept 24 - Mar 24 Platforms 150.8 11.4 (12.4) (1.0) 4.8 147.0 3 Total funds 150.8 11.4 (12.4) (1.0) 4.8 147.0 3 BT & Private Wealth platform funds increased 3% to $150.8 billion over the half reflecting higher equity markets and dividend distributions. |

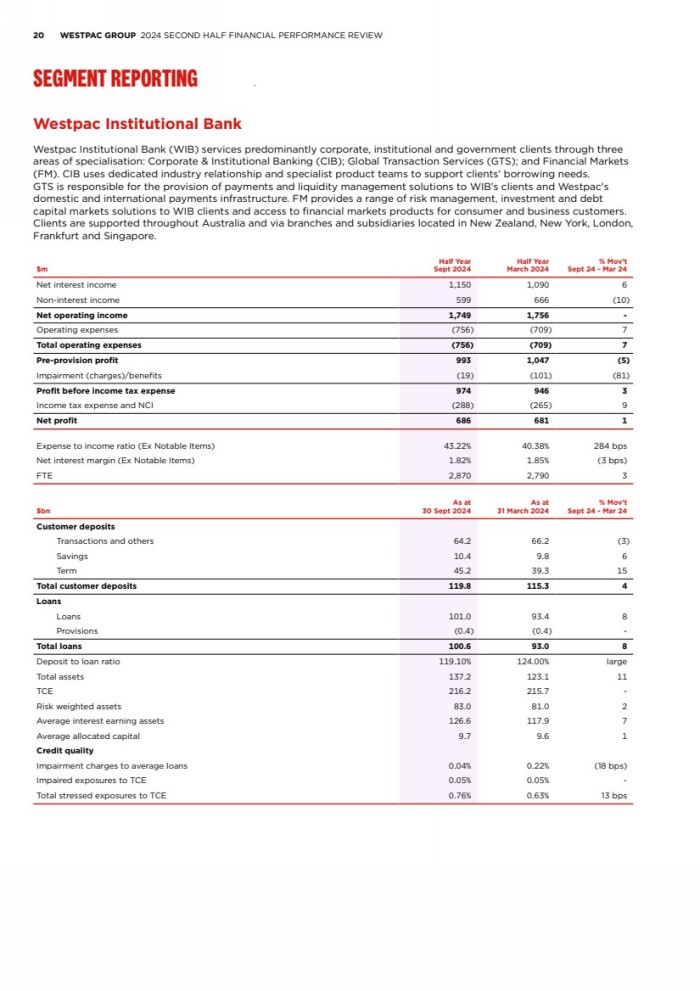

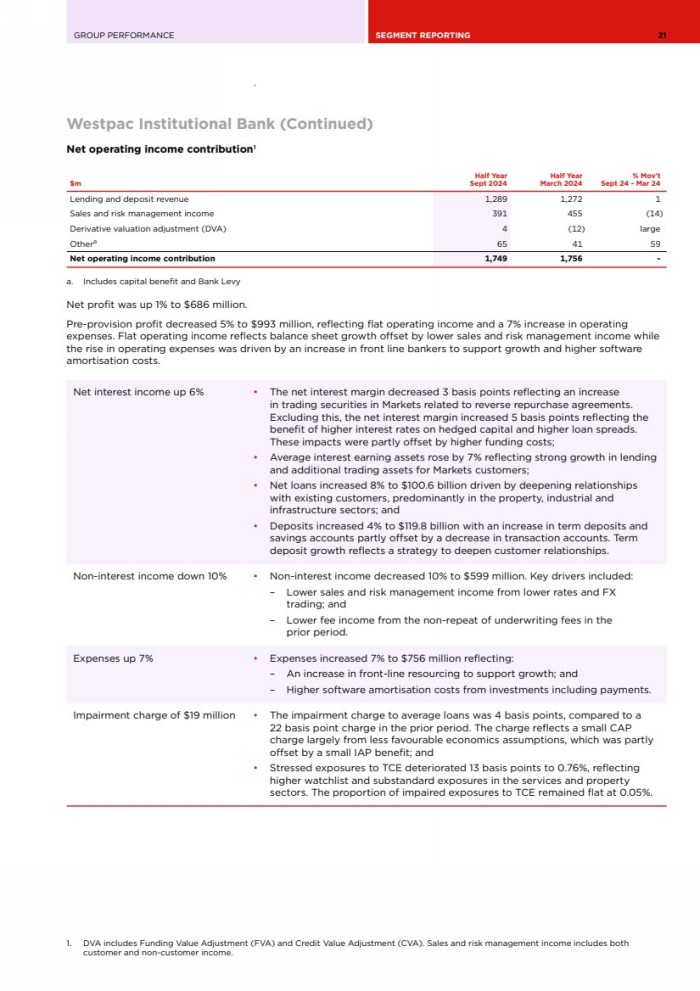

| 20 WESTPAC GROUP 2024 SECOND HALF FINANCIAL PERFORMANCE REVIEW SEGMENT REPORTING Westpac Institutional Bank Westpac Institutional Bank (WIB) services predominantly corporate, institutional and government clients through three areas of specialisation: Corporate & Institutional Banking (CIB); Global Transaction Services (GTS); and Financial Markets (FM). CIB uses dedicated industry relationship and specialist product teams to support clients’ borrowing needs. GTS is responsible for the provision of payments and liquidity management solutions to WIB’s clients and Westpac's domestic and international payments infrastructure. FM provides a range of risk management, investment and debt capital markets solutions to WIB clients and access to financial markets products for consumer and business customers. Clients are supported throughout Australia and via branches and subsidiaries located in New Zealand, New York, London, Frankfurt and Singapore. $m Half Year Sept 2024 Half Year March 2024 % Mov't Sept 24 - Mar 24 Net interest income 1,150 1,090 6 Non-interest income 599 666 (10) Net operating income 1,749 1,756 - Operating expenses (756) (709) 7 Total operating expenses (756) (709) 7 Pre-provision profit 993 1,047 (5) Impairment (charges)/benefits (19) (101) (81) Profit before income tax expense 974 946 3 Income tax expense and NCI (288) (265) 9 Net profit 686 681 1 Expense to income ratio (Ex Notable Items) 43.22% 40.38% 284 bps Net interest margin (Ex Notable Items) 1.82% 1.85% (3 bps) FTE 2,870 2,790 3 $bn As at 30 Sept 2024 As at 31 March 2024 % Mov't Sept 24 - Mar 24 Customer deposits Transactions and others 64.2 66.2 (3) Savings 10.4 9.8 6 Term 45.2 39.3 15 Total customer deposits 119.8 115.3 4 Loans Loans 101.0 93.4 8 Provisions (0.4) (0.4) - Total loans 100.6 93.0 8 Deposit to loan ratio 119.10% 124.00% large Total assets 137.2 123.1 11 TCE 216.2 215.7 - Risk weighted assets 83.0 81.0 2 Average interest earning assets 126.6 117.9 7 Average allocated capital 9.7 9.6 1 Credit quality Impairment charges to average loans 0.04% 0.22% (18 bps) Impaired exposures to TCE 0.05% 0.05% - Total stressed exposures to TCE 0.76% 0.63% 13 bps |

| GROUP PERFORMANCE SEGMENT REPORTING 21 Westpac Institutional Bank (Continued) Net operating income contribution1 $m Half Year Sept 2024 Half Year March 2024 % Mov't Sept 24 - Mar 24 Lending and deposit revenue 1,289 1,272 1 Sales and risk management income 391 455 (14) Derivative valuation adjustment (DVA) 4 (12) large Othera 65 41 59 Net operating income contribution 1,749 1,756 - a. Includes capital benefit and Bank Levy Net profit was up 1% to $686 million. Pre-provision profit decreased 5% to $993 million, reflecting flat operating income and a 7% increase in operating expenses. Flat operating income reflects balance sheet growth offset by lower sales and risk management income while the rise in operating expenses was driven by an increase in front line bankers to support growth and higher software amortisation costs. Net interest income up 6% • The net interest margin decreased 3 basis points reflecting an increase in trading securities in Markets related to reverse repurchase agreements. Excluding this, the net interest margin increased 5 basis points reflecting the benefit of higher interest rates on hedged capital and higher loan spreads. These impacts were partly offset by higher funding costs; • Average interest earning assets rose by 7% reflecting strong growth in lending and additional trading assets for Markets customers; • Net loans increased 8% to $100.6 billion driven by deepening relationships with existing customers, predominantly in the property, industrial and infrastructure sectors; and • Deposits increased 4% to $119.8 billion with an increase in term deposits and savings accounts partly offset by a decrease in transaction accounts. Term deposit growth reflects a strategy to deepen customer relationships. Non-interest income down 10% • Non-interest income decreased 10% to $599 million. Key drivers included: – Lower sales and risk management income from lower rates and FX trading; and – Lower fee income from the non-repeat of underwriting fees in the prior period. Expenses up 7% • Expenses increased 7% to $756 million reflecting: – An increase in front-line resourcing to support growth; and – Higher software amortisation costs from investments including payments. Impairment charge of $19 million • The impairment charge to average loans was 4 basis points, compared to a 22 basis point charge in the prior period. The charge reflects a small CAP charge largely from less favourable economics assumptions, which was partly offset by a small IAP benefit; and • Stressed exposures to TCE deteriorated 13 basis points to 0.76%, reflecting higher watchlist and substandard exposures in the services and property sectors. The proportion of impaired exposures to TCE remained flat at 0.05%. 1. DVA includes Funding Value Adjustment (FVA) and Credit Value Adjustment (CVA). Sales and risk management income includes both customer and non-customer income. |

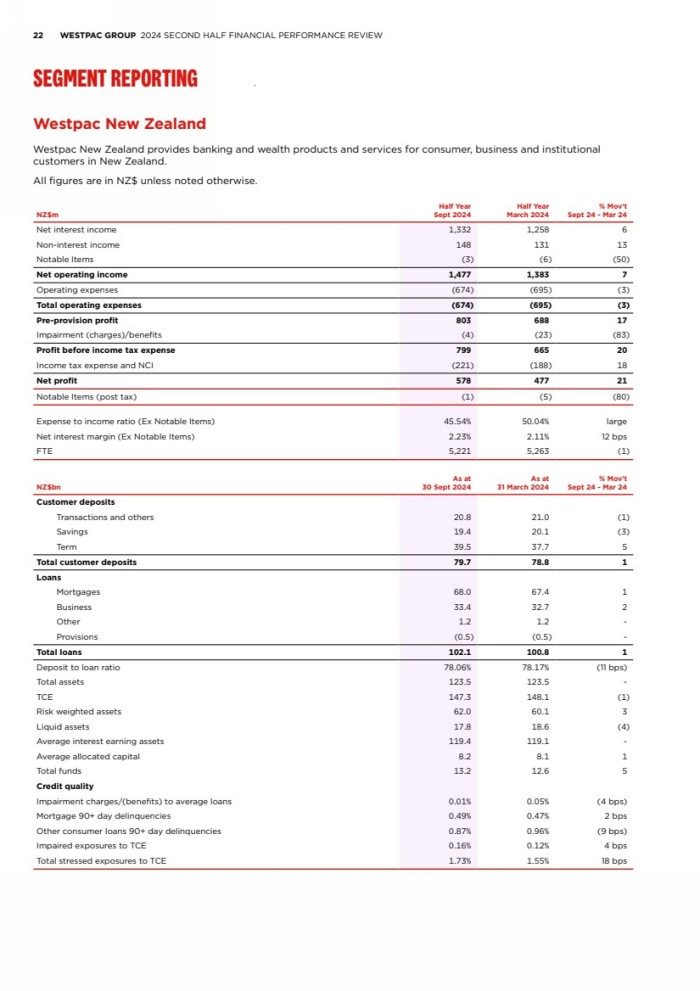

| 22 WESTPAC GROUP 2024 SECOND HALF FINANCIAL PERFORMANCE REVIEW SEGMENT REPORTING Westpac New Zealand Westpac New Zealand provides banking and wealth products and services for consumer, business and institutional customers in New Zealand. All figures are in NZ$ unless noted otherwise. NZ$m Half Year Sept 2024 Half Year March 2024 % Mov't Sept 24 - Mar 24 Net interest income 1,332 1,258 6 Non-interest income 148 131 13 Notable Items (3) (6) (50) Net operating income 1,477 1,383 7 Operating expenses (674) (695) (3) Total operating expenses (674) (695) (3) Pre-provision profit 803 688 17 Impairment (charges)/benefits (4) (23) (83) Profit before income tax expense 799 665 20 Income tax expense and NCI (221) (188) 18 Net profit 578 477 21 Notable Items (post tax) (1) (5) (80) Expense to income ratio (Ex Notable Items) 45.54% 50.04% large Net interest margin (Ex Notable Items) 2.23% 2.11% 12 bps FTE 5,221 5,263 (1) NZ$bn As at 30 Sept 2024 As at 31 March 2024 % Mov't Sept 24 - Mar 24 Customer deposits Transactions and others 20.8 21.0 (1) Savings 19.4 20.1 (3) Term 39.5 37.7 5 Total customer deposits 79.7 78.8 1 Loans Mortgages 68.0 67.4 1 Business 33.4 32.7 2 Other 1.2 1.2 - Provisions (0.5) (0.5) - Total loans 102.1 100.8 1 Deposit to loan ratio 78.06% 78.17% (11 bps) Total assets 123.5 123.5 - TCE 147.3 148.1 (1) Risk weighted assets 62.0 60.1 3 Liquid assets 17.8 18.6 (4) Average interest earning assets 119.4 119.1 - Average allocated capital 8.2 8.1 1 Total funds 13.2 12.6 5 Credit quality Impairment charges/(benefits) to average loans 0.01% 0.05% (4 bps) Mortgage 90+ day delinquencies 0.49% 0.47% 2 bps Other consumer loans 90+ day delinquencies 0.87% 0.96% (9 bps) Impaired exposures to TCE 0.16% 0.12% 4 bps Total stressed exposures to TCE 1.73% 1.55% 18 bps |

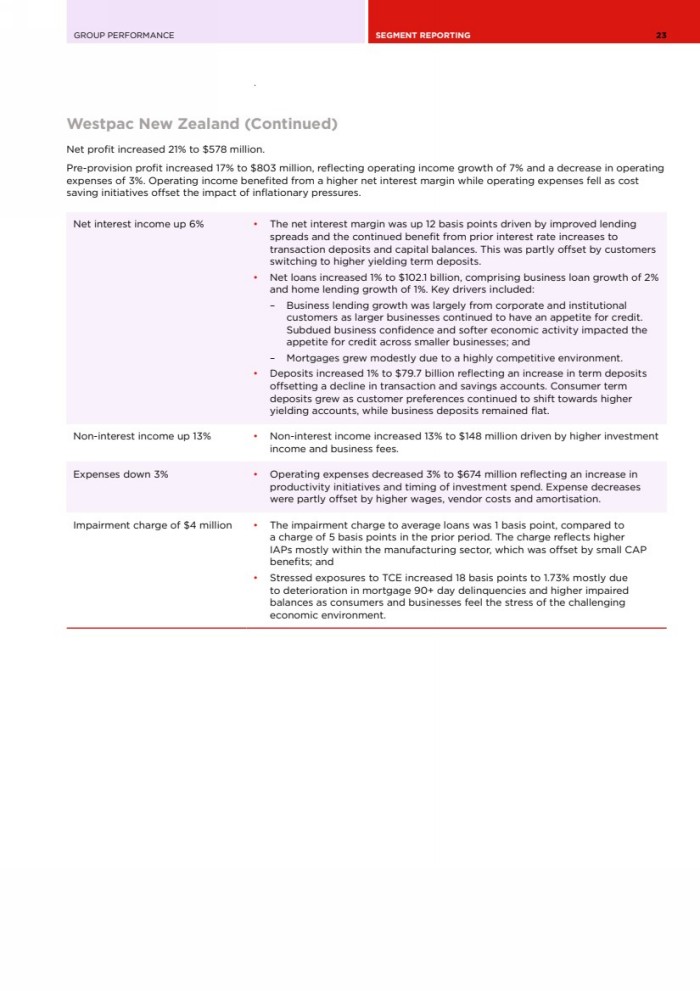

| GROUP PERFORMANCE SEGMENT REPORTING 23 Westpac New Zealand (Continued) Net profit increased 21% to $578 million. Pre-provision profit increased 17% to $803 million, reflecting operating income growth of 7% and a decrease in operating expenses of 3%. Operating income benefited from a higher net interest margin while operating expenses fell as cost saving initiatives offset the impact of inflationary pressures. Net interest income up 6% • The net interest margin was up 12 basis points driven by improved lending spreads and the continued benefit from prior interest rate increases to transaction deposits and capital balances. This was partly offset by customers switching to higher yielding term deposits. • Net loans increased 1% to $102.1 billion, comprising business loan growth of 2% and home lending growth of 1%. Key drivers included: – Business lending growth was largely from corporate and institutional customers as larger businesses continued to have an appetite for credit. Subdued business confidence and softer economic activity impacted the appetite for credit across smaller businesses; and – Mortgages grew modestly due to a highly competitive environment. • Deposits increased 1% to $79.7 billion reflecting an increase in term deposits offsetting a decline in transaction and savings accounts. Consumer term deposits grew as customer preferences continued to shift towards higher yielding accounts, while business deposits remained flat. Non-interest income up 13% • Non-interest income increased 13% to $148 million driven by higher investment income and business fees. Expenses down 3% • Operating expenses decreased 3% to $674 million reflecting an increase in productivity initiatives and timing of investment spend. Expense decreases were partly offset by higher wages, vendor costs and amortisation. Impairment charge of $4 million • The impairment charge to average loans was 1 basis point, compared to a charge of 5 basis points in the prior period. The charge reflects higher IAPs mostly within the manufacturing sector, which was offset by small CAP benefits; and • Stressed exposures to TCE increased 18 basis points to 1.73% mostly due to deterioration in mortgage 90+ day delinquencies and higher impaired balances as consumers and businesses feel the stress of the challenging economic environment. |

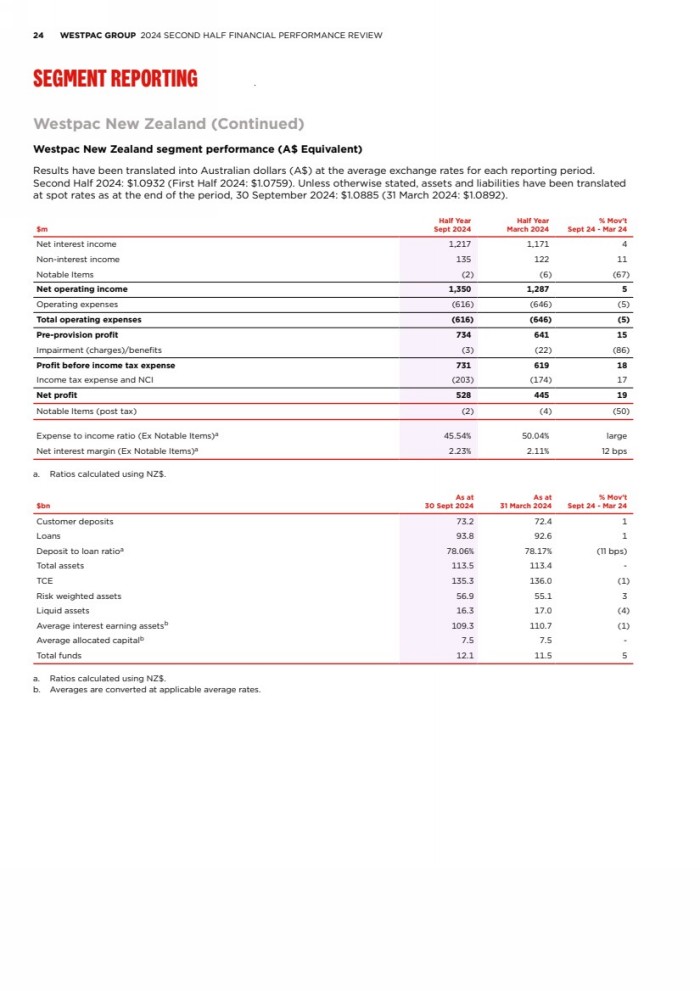

| 24 WESTPAC GROUP 2024 SECOND HALF FINANCIAL PERFORMANCE REVIEW SEGMENT REPORTING Westpac New Zealand (Continued) Westpac New Zealand segment performance (A$ Equivalent) Results have been translated into Australian dollars (A$) at the average exchange rates for each reporting period. Second Half 2024: $1.0932 (First Half 2024: $1.0759). Unless otherwise stated, assets and liabilities have been translated at spot rates as at the end of the period, 30 September 2024: $1.0885 (31 March 2024: $1.0892). $m Half Year Sept 2024 Half Year March 2024 % Mov't Sept 24 - Mar 24 Net interest income 1,217 1,171 4 Non-interest income 135 122 11 Notable Items (2) (6) (67) Net operating income 1,350 1,287 5 Operating expenses (616) (646) (5) Total operating expenses (616) (646) (5) Pre-provision profit 734 641 15 Impairment (charges)/benefits (3) (22) (86) Profit before income tax expense 731 619 18 Income tax expense and NCI (203) (174) 17 Net profit 528 445 19 Notable Items (post tax) (2) (4) (50) Expense to income ratio (Ex Notable Items)a 45.54% 50.04% large Net interest margin (Ex Notable Items)a 2.23% 2.11% 12 bps a. Ratios calculated using NZ$. $bn As at 30 Sept 2024 As at 31 March 2024 % Mov't Sept 24 - Mar 24 Customer deposits 73.2 72.4 1 Loans 93.8 92.6 1 Deposit to loan ratioa 78.06% 78.17% (11 bps) Total assets 113.5 113.4 - TCE 135.3 136.0 (1) Risk weighted assets 56.9 55.1 3 Liquid assets 16.3 17.0 (4) Average interest earning assetsb 109.3 110.7 (1) Average allocated capitalb 7.5 7.5 - Total funds 12.1 11.5 5 a. Ratios calculated using NZ$. b. Averages are converted at applicable average rates. |

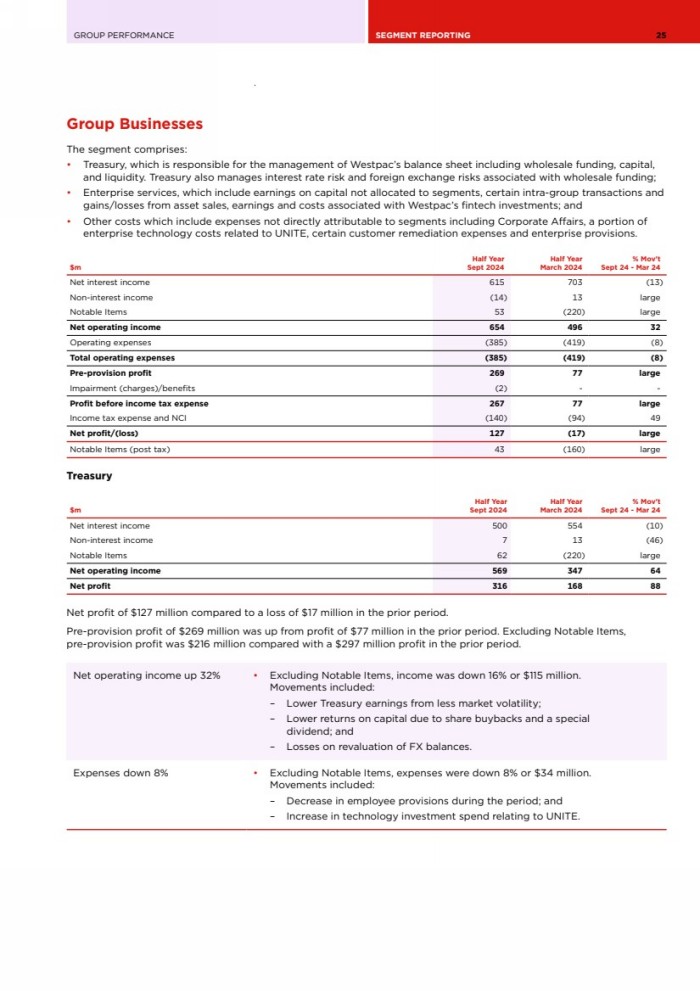

| GROUP PERFORMANCE SEGMENT REPORTING 25 Group Businesses The segment comprises: • Treasury, which is responsible for the management of Westpac’s balance sheet including wholesale funding, capital, and liquidity. Treasury also manages interest rate risk and foreign exchange risks associated with wholesale funding; • Enterprise services, which include earnings on capital not allocated to segments, certain intra-group transactions and gains/losses from asset sales, earnings and costs associated with Westpac’s fintech investments; and • Other costs which include expenses not directly attributable to segments including Corporate Affairs, a portion of enterprise technology costs related to UNITE, certain customer remediation expenses and enterprise provisions. $m Half Year Sept 2024 Half Year March 2024 % Mov't Sept 24 - Mar 24 Net interest income 615 703 (13) Non-interest income (14) 13 large Notable Items 53 (220) large Net operating income 654 496 32 Operating expenses (385) (419) (8) Total operating expenses (385) (419) (8) Pre-provision profit 269 77 large Impairment (charges)/benefits (2) - - Profit before income tax expense 267 77 large Income tax expense and NCI (140) (94) 49 Net profit/(loss) 127 (17) large Notable Items (post tax) 43 (160) large Treasury $m Half Year Sept 2024 Half Year March 2024 % Mov't Sept 24 - Mar 24 Net interest income 500 554 (10) Non-interest income 7 13 (46) Notable Items 62 (220) large Net operating income 569 347 64 Net profit 316 168 88 Net profit of $127 million compared to a loss of $17 million in the prior period. Pre-provision profit of $269 million was up from profit of $77 million in the prior period. Excluding Notable Items, pre-provision profit was $216 million compared with a $297 million profit in the prior period. Net operating income up 32% • Excluding Notable Items, income was down 16% or $115 million. Movements included: – Lower Treasury earnings from less market volatility; – Lower returns on capital due to share buybacks and a special dividend; and – Losses on revaluation of FX balances. Expenses down 8% • Excluding Notable Items, expenses were down 8% or $34 million. Movements included: – Decrease in employee provisions during the period; and – Increase in technology investment spend relating to UNITE. |

| 26 WESTPAC GROUP 2024 SECOND HALF FINANCIAL PERFORMANCE REVIEW DISCLOSURE REGARDING FORWARD-LOOKING STATEMENTS The information contained in this report contains statements that constitute “forward-looking statements” within the meaning of section 21E of the U.S. Securities Exchange Act of 1934. Forward-looking statements are statements that are not historical facts. Forward-looking statements appear in a number of places in this report and include statements regarding Westpac’s intent, belief or current expectations with respect to its business and operations, macro and micro economic and market conditions, results of operations and financial condition, capital adequacy, liquidity and risk management, including, without limitation, future loan loss provisions and financial support to certain borrowers, forecasted economic indicators and performance metric outcomes, indicative drivers, climate- and other sustainability- related statements, commitments, targets, projections and metrics, and other estimated and proxy data. Words such as ‘will’, ‘may’, ‘expect’, ‘intend’, ‘seek’, ‘would’, ‘should’, ‘could’, ‘continue’, ‘plan’, ‘estimate’, ‘anticipate’, ‘believe’, ‘probability’, ‘indicative’, ‘risk’, ‘aim’, ‘outlook’, ‘forecast’, ‘f’cast’, ‘f’, ‘assumption’, ‘projection’, ‘target,’ goal’, ‘guidance’, 'objective', ‘ambition’ or other similar words are used to identify forward-looking statements, or otherwise identify forward-looking statements. These forward-looking statements reflect Westpac’s current views on future events and are subject to change, certain known and unknown risks, uncertainties and assumptions and other factors which are, in many instances, beyond Westpac’s control (and the control of Westpac’s officers, employees, agents and advisors), and have been made based on management’s current expectations or beliefs concerning future developments and their potential effect upon Westpac. Forward-looking statements may also be made, verbally or in writing, by members of Westpac’s management or Board in connection with this report. Such statements are subject to the same limitations, uncertainties, assumptions and disclaimers set out in this report. There can be no assurance that future developments or performance will align with Westpac’s expectations or that the effect of future developments on Westpac will be those anticipated. Actual results could differ materially from those we expect or which are expressed or implied in forward-looking statements, depending on various factors including, but not limited to, those described in Risk Management in the 2024 Annual Report and the 2024 Risk Factors. When relying on forward-looking statements to make decisions with respect to Westpac, investors and others should carefully consider such factors and other uncertainties and events. Except as required by law, Westpac assumes no obligation to revise or update any forward-looking statements in this report, whether from new information, future events, conditions or otherwise, after the date of this report. |

| GROUP PERFORMANCE SEGMENT REPORTING 27 GLOSSARY OF ABBREVIATIONS AND DEFINED TERMS Shareholder value Average ordinary equity Average total equity less average non-controlling interests. Average tangible ordinary equity Average ordinary equity less intangible assets (excluding capitalised software). Average total equity The average balance of shareholders’ equity, including non-controlling interests. Dividend payout ratio Current period ordinary dividend paid/declared on issued shares (net of Treasury shares) divided by the net profit attributable to owners of WBC (adjusted for RSP dividends). Earnings per ordinary share • Basic earnings per ordinary share is calculated by dividing the net profit attributable to owners of WBC by the weighted average number of ordinary shares on issue during the period, adjusted for treasury shares. • Diluted earnings per ordinary share is calculated by adjusting the basic earnings per ordinary share by assuming all dilutive potential ordinary shares are converted. Fully franked dividends per ordinary share (cents) Dividends paid out of retained profits which carry a credit for Australian company income tax paid by Westpac. Net tangible assets per share Net tangible assets (total equity less goodwill and other intangible assets less minority interests) divided by the number of ordinary shares on issue (less Treasury shares held). Pre-provision profit Net interest income plus non-interest income less operating expenses. Return on average ordinary equity (ROE) Net profit attributable to the owners of WBC adjusted for RSP dividends (annualised where applicable) divided by average ordinary equity. Return on average tangible ordinary equity (ROTE) Net profit attributable to the owners of WBC adjusted for RSP dividends (annualised where applicable) divided by average tangible ordinary equity. Weighted average ordinary shares Weighted average number of fully paid ordinary shares listed on the Australian Stock Exchange for the relevant period less Westpac shares held by Westpac (‘Treasury shares’). Productivity and efficiency Expense to income ratio Operating expenses divided by net operating income. Expense to income ratio (ex Notable Items) Operating expenses excluding Notable Items divided by net operating income excluding Notable Items. Full time equivalent employees (FTE) A calculation based on the number of hours worked by full and part-time employees as part of their normal duties. For example, the full time equivalent of one FTE is 76 hours paid work per fortnight. Revenue per FTE Total operating income divided by the average number of FTE for the period. Business Performance Average Where possible, daily balances are used to calculate the average balance for the period. Average interest bearing liabilities The average balance of liabilities owed by Westpac that incur an interest expense. Where possible, daily balances are used to calculate the average balance for the period. Average interest earning assets The average balance of assets held by Westpac that generate interest income. Where possible, daily balances are used to calculate the average balance for the period. Core NIM Calculated by dividing net interest income excluding Notable Items and Treasury & Markets (annualised where applicable) by average interest earning assets. Group NIM/Net interest margin Calculated by dividing net interest income (annualised where applicable) by average interest earning assets. Net profit Net profit attributable to owners of WBC. TSR Total shareholder return. Capital Adequacy Australian Prudential Regulation Authority (APRA) leverage ratio Tier 1 capital divided by ‘exposure measure’ and expressed as a percentage. ‘Exposure measure’ is the sum of on balance sheet exposures, derivative exposures, securities financing transaction (SFT) exposures and non-market related off balance sheet exposures. Common equity tier 1 (CET1) capital ratio Total common equity capital divided by risk weighted assets, as defined by APRA. Internationally comparable capital ratios Internationally comparable methodology references the ABA study on the comparability of APRA’s capital framework released on 10 March 2023. Risk weighted assets (RWA) Assets (both on and off-balance sheet) are risk weighted according to each asset’s inherent potential for default and what the likely losses would be in case of default. In the case of non-asset backed risks (i.e. market, IRRBB and operational risk), RWA is determined by multiplying the capital requirements for those risks by 12.5. Credit risk weighted assets (Credit RWA) Credit risk weighted assets represent risk weighted assets (on-balance sheet and off-balance sheet) that relate to credit exposures and therefore exclude market risk, operational risk, IRRBB and other assets. Tier 1 capital ratio Total Tier 1 capital divided by risk weighted assets, as defined by APRA. Total regulatory capital ratio Total regulatory capital divided by risk weighted assets, as defined by APRA. |

| 28 WESTPAC GROUP 2024 SECOND HALF FINANCIAL PERFORMANCE REVIEW GLOSSARY OF ABBREVIATIONS AND DEFINED TERMS Funding and liquidity Deposit to loan ratio Customer deposits divided by net loans. High Quality Liquid Assets (HQLA) Assets which meet APRA’s criteria for inclusion as HQLA in the numerator of the LCR. Liquid assets HQLA and non LCR qualifying liquid assets, but excludes internally securitised assets that are eligible for a repurchase agreement with the RBA and the RBNZ. Liquidity Coverage Ratio (LCR) An APRA requirement to maintain an adequate level of unencumbered high quality liquid assets, to meet liquidity needs for a 30 calendar day period under an APRA-defined severe stress scenario. Absent a situation of financial stress, the value of the LCR must not be less than 100%. LCR is calculated as the percentage ratio of stock of HQLA, and qualifying RBNZ securities over the total net cash out-flows in a modelled 30 day defined stressed scenario. Net Stable Funding Ratio (NSFR) The NSFR is defined as the ratio of the amount of available stable funding (ASF) to the amount of required stable funding (RSF) defined by APRA. The amount of ASF is the portion of an ADI’s capital and liabilities expected to be a reliable source of funds over a one year time horizon. The amount of RSF is a function of the liquidity characteristics and residual maturities of an ADI’s assets and off-balance sheet activities. ADIs must maintain an NSFR of at least 100%. Term Funding Facility (TFF) A facility that was established by the RBA in March 2020 to provide 3 year term funding to Australian ADIs via repurchase transactions, subject to qualifying conditions, to help support lending to Australian businesses. The facility closed to new draw downs in June 2021. Wholesale funding Wholesale funding includes debt issues, loan capital, certificates of deposit, term funding from central banks and interbank placements. Credit quality Collectively assessed provisions (CAPs) Collectively assessed provisions for expected credit loss under AASB 9 represent the Expected Credit Loss (ECL) which is collectively assessed in pools of similar assets with similar risk characteristics. This incorporates forward-looking information and does not require an actual loss event to have occurred for an impairment provision to be recognised. Default Credit exposures that are non-performing. Gross impaired exposures provisions to gross impaired exposures Impairment provisions relating to impaired exposures include individually assessed provisions plus the proportion of the collectively assessed provisions that relate to impaired exposures. Impaired exposures Includes exposures that have deteriorated to the point where full collection of interest and principal is in doubt, based on an assessment of the customer’s outlook, cash flow, and the net realisation of value of assets to which recourse is held: • Facilities 90 days or more past due, and full recovery is in doubt: exposures where contractual payments are 90 or more days in arrears and the net realisable value of assets to which recourse is held may not be sufficient to allow full collection of interest and principal, including overdrafts or other revolving facilities that remain continuously outside approved limits by material amounts for 90 or more calendar days; • Non-accrual facilities: exposures with individually assessed impairment provisions held against them, excluding restructured loans; • Restructured facilities: exposures where the original contractual terms have been formally modified to provide for concessions of interest or principal for reasons related to the financial difficulties of the customer; • Other assets acquired through security enforcement (includes other real estate owned): includes the value of any other assets acquired as full or partial settlement of outstanding obligations through the enforcement of security arrangements; or • Any other facilities where the full collection of interest and principal is in doubt. Impairment charges/(benefit) to average loans Calculated as impairment charges (annualised where applicable) divided by average gross loans. Individually assessed provisions (IAPs) Provisions raised for losses on loans that are known to be impaired and are assessed on an individual basis. The estimated losses on these impaired loans is based on expected future cash flows discounted to their present value and, as this discount unwinds, interest will be recognised in the income statement. Non-performing not impaired exposures Includes those credit exposures that are in default, but where it is expected that the full value of principal and accrued interest can be collected, generally by reference to the value of security held. Performing exposures Credit exposures that are not non-performing. Stressed exposures Watchlist and substandard credit exposures plus non-performing exposures. Total committed exposure (TCE) Represents the sum of the committed portion of direct lending (including funds placement overall and deposits placed), contingent and pre-settlement risk plus the committed portion of secondary market trading and underwriting risk. |

| GROUP PERFORMANCE SEGMENT REPORTING 29 Other AASB Australian Accounting Standards Board ABA Australian Banking Association ADI Authorised Deposit-taking Institution APRA Australian Prudential Regulation Authority bps Basis points Credit Value Adjustment (CVA) CVA adjusts the fair value of over-the-counter derivatives for credit risk. CVA is employed on the majority of derivative positions and reflects the market view of the counter party credit risk. A Debit Valuation Adjustment is employed to adjust for our own credit risk. Derivative Valuation Adjustment (DVA) DVA includes CVA and FVA. First Half 2024 (1H24) Six months ended 31 March 2024 Full Year 2023 (FY23) Twelve months ended 30 September 2023 Full Year 2024 (FY24) Twelve months ended 30 September 2024 FVIS Fair value through income statement FX Foreign exchange IRRBB Interest Rate Risk in the Banking Book NCI Non-controlling interests Non-interest earning/bearing Instruments which do not carry an entitlement to interest. Prior period Refers to the six months ended 31 March 2024 RBA Reserve Bank of Australia RBNZ Reserve Bank of New Zealand RSP Restricted Share Plan Runoff Scheduled and unscheduled repayments and debt repayments, net of redraws. Second Half 2024 Six months ended 30 September 2024 Segment reporting Segment reporting is presented on a management reporting basis. Internal charges and transfer pricing adjustments are included in the performance of each segment reflecting the management structure rather than the legal entity (these results cannot be compared to results for individual legal entities). Where management reporting structures or accounting classifications have changed, financial results for comparative periods have been restated and may differ from results previously reported. Overhead costs are allocated to revenue generating segments. Westpac’s internal transfer pricing frameworks facilitate risk transfer, profitability measurement, capital allocation and segment alignment, tailored to the jurisdictions in which Westpac operates. Transfer pricing allows Westpac to measure the relative contribution of products and segments to Westpac’s interest margin and other dimensions of performance. Key components of Westpac’s transfer pricing frameworks are funds transfer pricing for interest rate and liquidity risk and allocation of basis and contingent liquidity costs, including capital allocation. UNITE program A business-led, technology-enabled simplification program. WIB Westpac Institutional Bank WNZL Westpac New Zealand Limited |

| 30 WESTPAC GROUP 2024 SECOND HALF FINANCIAL PERFORMANCE REVIEW CONTACT US Westpac Head Office 275 Kent Street, Sydney NSW 2000 Australia Tel: +61 2 9155 7713 International payments Tel: +61 2 9155 7700 Website: westpac.com.au/westpacgroup Westpac Consumer - Tel: 132 032 Business - Tel: 132 142 From outside Australia: +61 2 9155 7700 Website: westpac.com.au St.George Bank St.George House 4-16 Montgomery Street Kogarah NSW 2217 Australia Mail: Locked Bag 1 Kogarah NSW 1485 Australia Tel: 13 33 30 website: stgeorge.com.au Bank of Melbourne 150 Collins Street Melbourne VIC 3000 Australia Tel: 13 22 66 From outside Australia: +61 3 8536 7870 Website: bankofmelbourne.com.au BankSA Level 8, 97 King William Street, Adelaide SA 5000 Australia Mail: GPO Box 399, Adelaide SA 5001 Australia Tel: 13 13 76 From outside Australia: +61 2 9155 7850 Website: banksa.com.au RAMS RAMS Financial Group Pty Ltd International Towers Tower 2, Level 19, 200 Barangaroo Avenue Barangaroo NSW 2000 Australia Mail: GPO Box 4008, Sydney NSW 2001 Australia Tel: +61 2 8218 7000 Email: communications@rams.com.au Website: rams.com.au BT Level 8, Tower Two, International Towers 200 Barangaroo Avenue Barangaroo NSW 2000 Australia Mail: GPO Box 2861 Adelaide SA 5001 Tel: 1300 881 716 From outside Australia: +61 2 9155 4030 Email: support@panorama.com.au Website: bt.com.au Westpac Institutional Bank Tel: 132 032 Website: westpac.com.au Westpac NZ Limited Westpac On Takutai Square 16 Takutai Square Auckland 1010, New Zealand Tel: +64 9 912 8000 Email: customer_support@westpac.co.nz Website: westpac.co.nz Global locations Fiji Germany Papua New Guinea Republic of Singapore United States of America United Kingdom See our website at westpac.com.au for the contact details of our global locations. Share Registrar Link Market Services Limited Level 12, 680 George Street Sydney NSW 2000 Australia Mail: Locked Bag A6015, Sydney South NSW 1235 Tel: 1800 804 255 Facsimile: +61 2 9287 0303 Email: westpac@linkmarketservices.com.au Website: linkmarketservices.com.au The 2024 Westpac Annual Report is printed on PEFC certified paper. Compliance with the certification criteria set out by the Programme for the Endorsement of Forest Certification (PEFC) means that the paper fibre is sourced from sustainable forests. |

| WESTPAC.COM.AU |