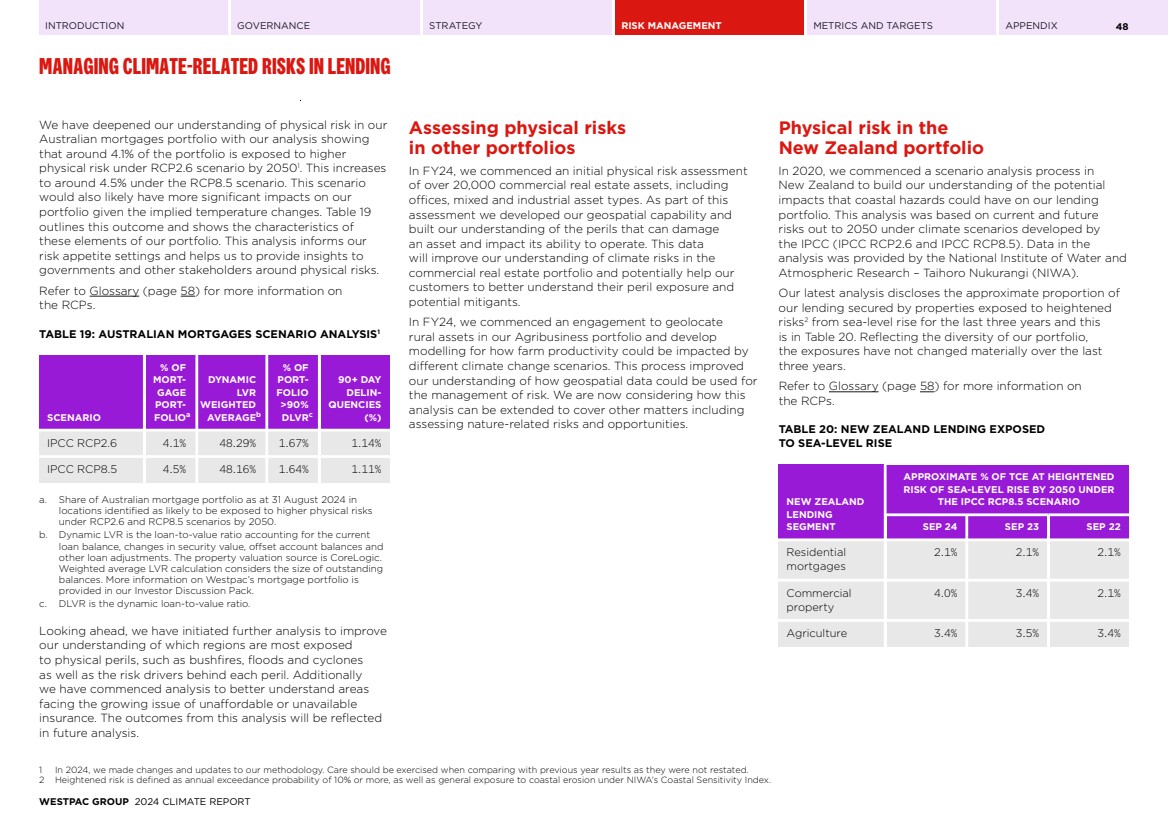

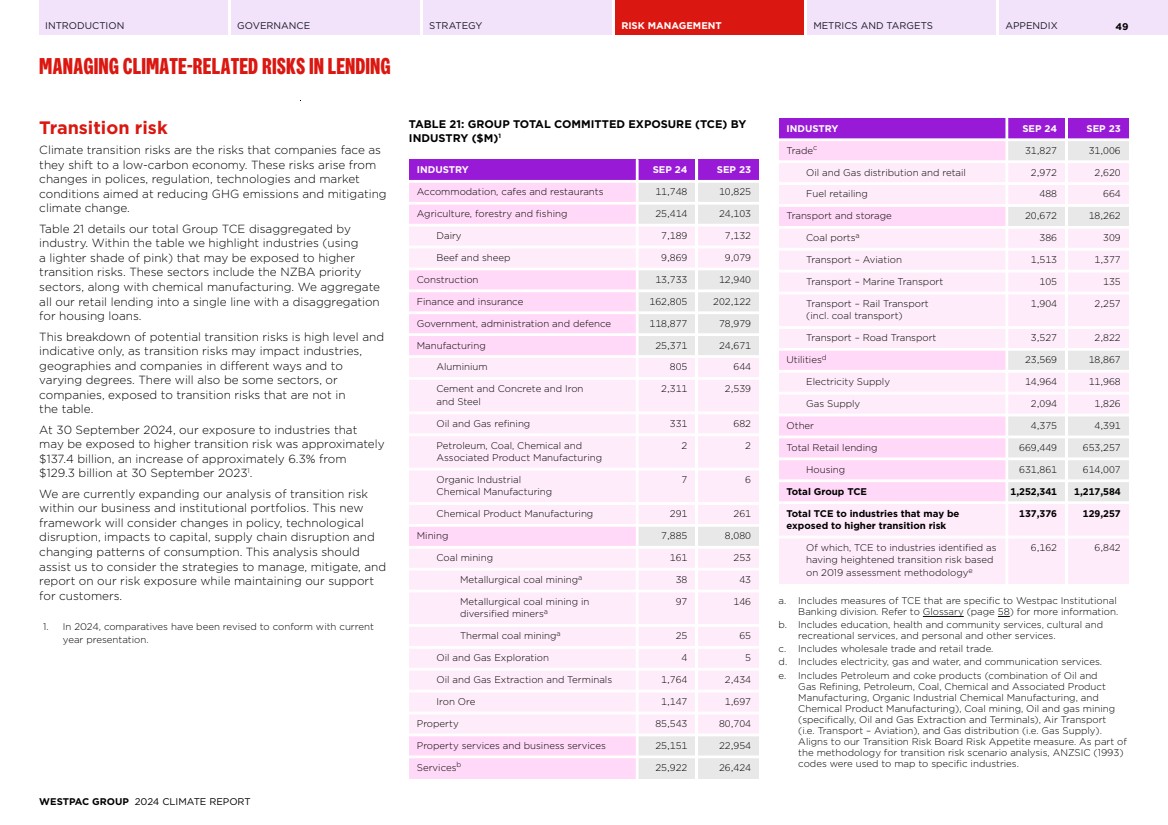

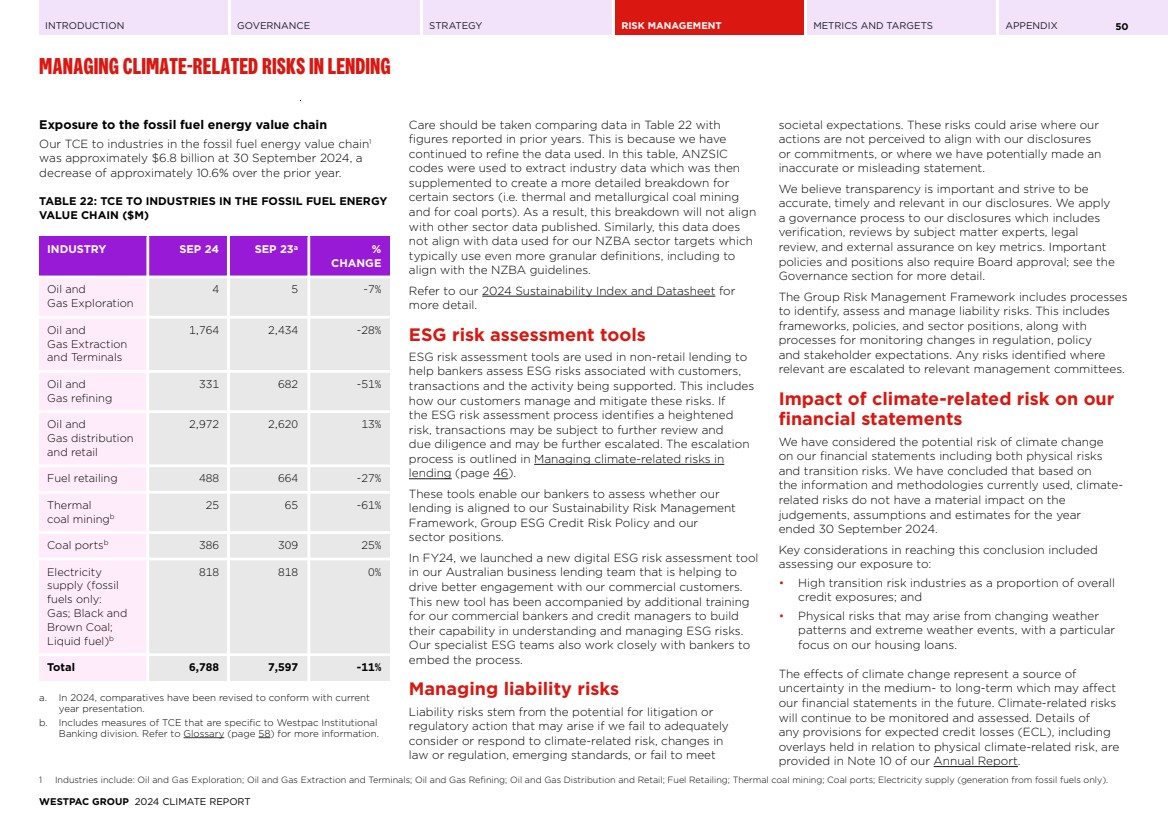

Exhibit 1

| ASX Release 4 November 2024 Westpac 2024 Climate Report Westpac Banking Corporation (“Westpac”) today provides the attached Westpac 2024 Climate Report. For further information: Hayden Cooper Justin McCarthy Group Head of Media Relations General Manager, Investor Relations 0402 393 619 0422 800 321 This document has been authorised for release by Tim Hartin, Company Secretary. Level 18, 275 Kent Street Sydney, NSW, 2000 |

| CLIMATE REPORT 2024 WESTPAC BANKING CORPORATION ABN 33 007 457 141 |

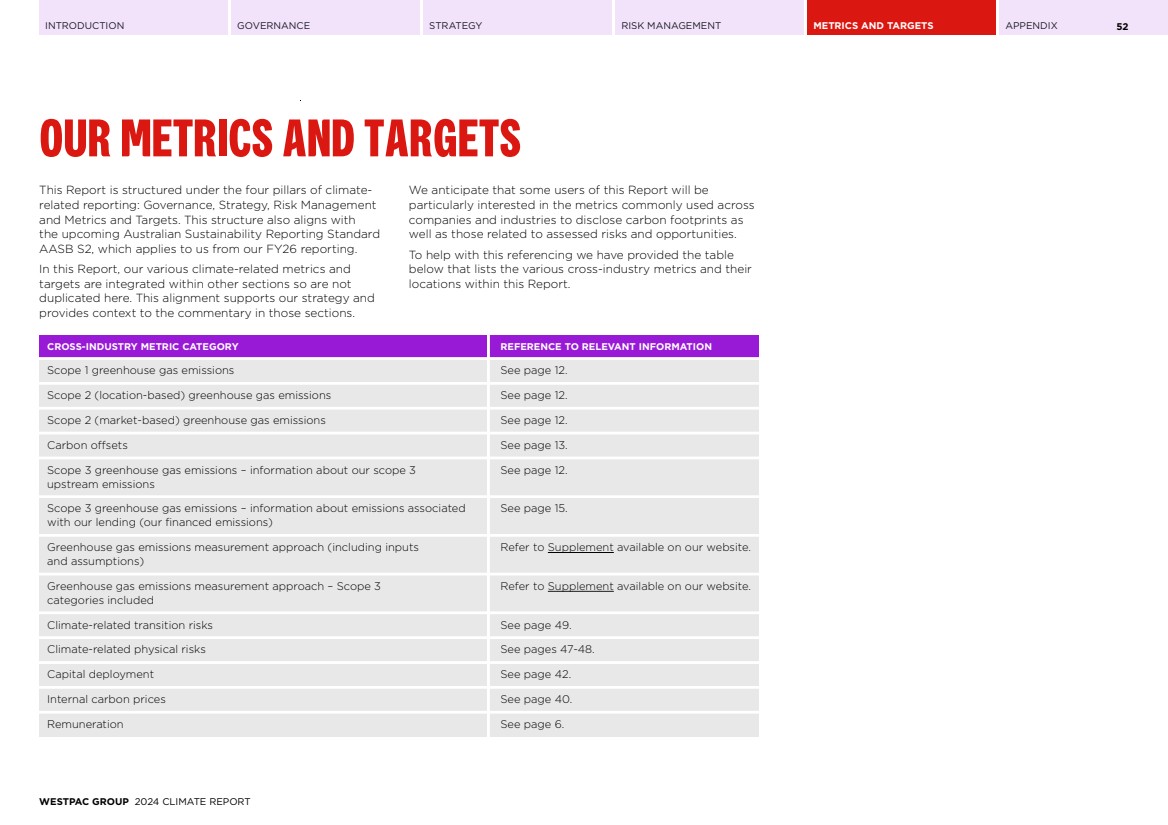

| INTRODUCTION GOVERNANCE STRATEGY RISK MANAGEMENT METRICS AND TARGETS APPENDIX 1 CONTENTS INTRODUCTION 2 Message from the CEO 3 GOVERNANCE 5 STRATEGY 7 Action area 1: Net-zero, climate resilient operations 10 Action area 2: Supporting customers’ transition to net-zero and to build their climate resilience 14 Action area 3: Collaborate for impact on initiatives towards net-zero and climate resilience 41 RISK MANAGEMENT 43 METRICS AND TARGETS 51 APPENDIX 57 I Glossary 58 II NZBA Sector Emissions Targets 61 III Climate-related positions and partnerships 66 IV Disclaimer 67 “OUR PURPOSE IS CREATING BETTER FUTURES TOGETHER. ONE WAY WE ARE DOING THIS IS THROUGH OUR AMBITION TO BECOME A NET-ZERO, CLIMATE RESILIENT BANK. IN THIS REPORT, WE SHARE OUR PROGRESS, CHALLENGES, AND ACHIEVEMENTS, AS WE WORK TOWARDS A NET-ZERO ECONOMY.” WESTPAC CEO, PETER KING Cover photo: Agribusiness customer Brendan Pattison with Margie Seale, Westpac Board member ACKNOWLEDGEMENT OF INDIGENOUS PEOPLES Westpac acknowledges the First Peoples of Australia. We recognise their ongoing role as Traditional Owners of the land and waters of this country and pay our respects to Elders, past and present. We extend our respect to Westpac’s Aboriginal and Torres Strait Islander employees, partners, and stakeholders, and to the Indigenous Peoples in the other locations where we operate. In Aotearoa New Zealand we also acknowledge tāngata whenua and the unique relationship that Indigenous Peoples share with all New Zealanders under Te Tiriti o Waitangi. WESTPAC GROUP 2024 CLIMATE REPORT |

| INTRODUCTION GOVERNANCE STRATEGY RISK MANAGEMENT METRICS AND TARGETS APPENDIX 2 INTRODUCTION Westpac Reporting Suite Our reporting suite brings together the Group’s financial, non-financial, risk and sustainability performance for the 2024 year. It includes our 2024 Annual Report, FY24 Financial Results Presentation and Investor Discussion pack, Pillar 3 report, Corporate Governance Statement, 2024 Risk Factors, 2024 Climate Report and our 2024 Sustainability Index and Datasheet. Access the full suite online at westpac.com.au/2024annualreport. About this report Our 2024 Climate Report (Report) outlines Westpac’s strategy, targets, and approach for addressing the risks and opportunities presented by climate change. It also describes our climate transition plan, outlining how we are working to reduce our carbon footprint. A Glossary (page 58) is at the end of this Report along with a list of climate-related positions and partnerships (page 66). We released our refreshed 2030 Sustainability Strategy in November 2023, outlining how we are working towards our purpose of Creating better futures together. This Climate Report focuses on our progress consistent with this strategy's climate objective. We have also published a 2024 Climate Methodologies Supplement (Supplement) on our website. This Supplement includes the details of the methodologies for estimating our operational emissions, our Net-Zero Banking Alliance sector emissions targets (NZBA sector targets), our Group financed emissions calculations, as well as details on the climate scenarios used in our climate scenario analysis. Our 2024 Sustainability Index and Datasheet provides additional detail on some metrics in this Report along with other key sustainability metrics in the 2024 Annual Report and is available on our website. This detailed spreadsheet also outlines how our reporting aligns with major reporting standards and frameworks. We recognise the intersection of climate change with other risk thematics, such as nature and human rights. These are referred to in this Report but more is also available in our Natural Capital and Human Rights Position Statements published in 2023. Westpac and its subsidiaries are covered by this Report. This includes Australia and New Zealand along with our businesses in other international locations. For certain metrics we exclude some areas of the business due to materiality and/or a lack of readily available data. In New Zealand, we are working to comply with the new External Reporting Board (XRB) climate-related standards and will publish separate climate reports for Westpac New Zealand Limited (WNZL) and our New Zealand branch (NZ Branch). For clarity, both WNZL and the NZ Branch are considered in this Report. Frameworks and standards Our reporting continues to be shaped by both global and local climate reporting standards, including the International Sustainability Standards Board (ISSB) International Financial Reporting Standards (IFRS) S1 and S2 sustainability and climate-related disclosure standards, the recently released Australian AASB S1 and S2 sustainability and climate-related disclosure standards and the New Zealand XRB climate-related disclosure standards. This Report is structured under the four major sections of Governance, Strategy, Risk Management and Metrics and Targets. This structure aligns with the ISSB IFRS S2 climate-related disclosure standards, which have absorbed the earlier recommendations of the Task Force on Climate-related Financial Disclosures (TCFD). It also aligns with the new AASB S2 Climate-related Disclosure standard. We are committed to uplift our reporting to align with the new mandatory climate-related disclosure standards and international best practice in the future. Our approach to climate reporting Outlining our approach to managing climate change risks and opportunities is challenging as measuring, reporting and the setting of targets relies on estimates, inexact data and the availability of appropriate methodologies. We strive to apply consistent principles in how we measure and report our climate metrics although these remain estimates that have inherent uncertainties. Despite the uncertainties of reported metrics and that metrics may vary over time, it is essential to estimate our impact, set targets and report on progress – so we can achieve our ambition of becoming a net-zero, climate resilient bank. We ask readers to consider these limitations and focus on our intent and our guiding principles. Over time, our climate-related data will evolve as new methodologies and technologies emerge and our stakeholders improve the measurement of their climate impacts, risks and opportunities. This Report includes forward-looking statements – such as targets, ambitions, plans, estimates, assumptions and metrics – that inherently carry uncertainty, particularly in the context of climate reporting. These risks and uncertainties need to be considered when interpreting this Report. For an explanation of forward-looking statements and the risks, uncertainties and assumptions to which they are subject, see the Disclaimer (page 67) in the Appendix. References to ‘Westpac’, ‘Group’, ‘Westpac Group’, ‘we’, ‘us’ and ‘our’ are to Westpac Banking Corporation ABN 33 007 457 141 and its subsidiaries unless stated otherwise. Operational greenhouse gas (GHG) emissions data and targets are absolute market-based greenhouse gas emissions. Unless otherwise indicated, our operational greenhouse gas emissions and energy consumption are reported for the 12-month period ended 30 June 2024. Our estimated Group portfolio financed emissions and progress of our NZBA sector targets are reported one year in arrears, for the period ended 30 September 2023, unless otherwise indicated. All other data in this Report is for the 12 months to 30 September 2024 or at 30 September 2024 and all dollar amounts are in Australian dollars, unless otherwise indicated. PricewaterhouseCoopers (PwC) provided independent reasonable assurance over our scope 1, 2 and 3 upstream emissions, and limited assurance over selected metrics and targets within this report. Their independent assurance statement is on pages 53-56 of this Report and on our website. WESTPAC GROUP 2024 CLIMATE REPORT |

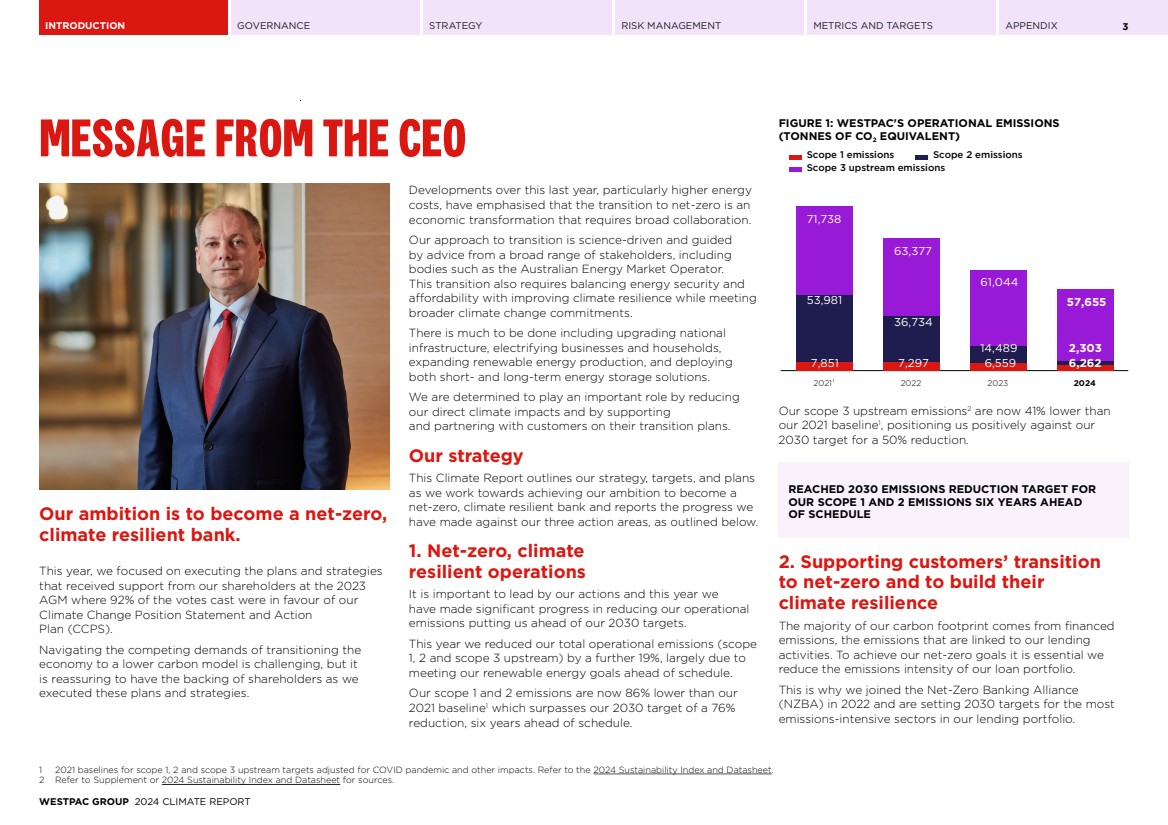

| INTRODUCTION GOVERNANCE STRATEGY RISK MANAGEMENT METRICS AND TARGETS APPENDIX 3 MESSAGE FROM THE CEO Our ambition is to become a net-zero, climate resilient bank. This year, we focused on executing the plans and strategies that received support from our shareholders at the 2023 AGM where 92% of the votes cast were in favour of our Climate Change Position Statement and Action Plan (CCPS). Navigating the competing demands of transitioning the economy to a lower carbon model is challenging, but it is reassuring to have the backing of shareholders as we executed these plans and strategies. Developments over this last year, particularly higher energy costs, have emphasised that the transition to net-zero is an economic transformation that requires broad collaboration. Our approach to transition is science-driven and guided by advice from a broad range of stakeholders, including bodies such as the Australian Energy Market Operator. This transition also requires balancing energy security and affordability with improving climate resilience while meeting broader climate change commitments. There is much to be done including upgrading national infrastructure, electrifying businesses and households, expanding renewable energy production, and deploying both short- and long-term energy storage solutions. We are determined to play an important role by reducing our direct climate impacts and by supporting and partnering with customers on their transition plans. Our strategy This Climate Report outlines our strategy, targets, and plans as we work towards achieving our ambition to become a net-zero, climate resilient bank and reports the progress we have made against our three action areas, as outlined below. 1. Net-zero, climate resilient operations It is important to lead by our actions and this year we have made significant progress in reducing our operational emissions putting us ahead of our 2030 targets. This year we reduced our total operational emissions (scope 1, 2 and scope 3 upstream) by a further 19%, largely due to meeting our renewable energy goals ahead of schedule. Our scope 1 and 2 emissions are now 86% lower than our 2021 baseline1 which surpasses our 2030 target of a 76% reduction, six years ahead of schedule. Our scope 3 upstream emissions2 are now 41% lower than our 2021 baseline1 , positioning us positively against our 2030 target for a 50% reduction. REACHED 2030 EMISSIONS REDUCTION TARGET FOR OUR SCOPE 1 AND 2 EMISSIONS SIX YEARS AHEAD OF SCHEDULE 2. Supporting customers’ transition to net-zero and to build their climate resilience The majority of our carbon footprint comes from financed emissions, the emissions that are linked to our lending activities. To achieve our net-zero goals it is essential we reduce the emissions intensity of our loan portfolio. This is why we joined the Net-Zero Banking Alliance (NZBA) in 2022 and are setting 2030 targets for the most emissions-intensive sectors in our lending portfolio. 1 2021 baselines for scope 1, 2 and scope 3 upstream targets adjusted for COVID pandemic and other impacts. Refer to the 2024 Sustainability Index and Datasheet. 2 Refer to Supplement or 2024 Sustainability Index and Datasheet for sources. FIGURE 1: WESTPAC'S OPERATIONAL EMISSIONS (TONNES OF CO2 EQUIVALENT) 7,851 7,297 6,559 6,262 53,981 36,734 14,489 2,303 71,738 63,377 61,044 57,655 Scope 1 emissions Scope 2 emissions Scope 3 upstream emissions 2021¹ 2022 2023 2024 WESTPAC GROUP 2024 CLIMATE REPORT |

| INTRODUCTION GOVERNANCE STRATEGY RISK MANAGEMENT METRICS AND TARGETS APPENDIX MESSAGE FROM THE CEO 4 After finalising our Aluminium sector target this year, we now have targets in all nine emissions-intensive sectors required under our NZBA commitment1 .. The coverage of our Group financed emissions by our NZBA sector targets is estimated in Table 1. TABLE 1: PROGRESS IN SETTING OUR NZBA SECTOR TARGETS SEP 2024 SEP 2023 SEP 2022 NZBA emissions-intensive sectors with targets set (out of nine) 9 8 5 Number of NZBA sector targets 13 12 5 Estimated % of Group scope 3 financed emissions (scope 1 and 2 customer emissions) related to customers captured in our NZBA sector targets for the prior reporting period Up to 54% Up to 48% NA We made progress in FY23 with an improved emissions profile in 11 of our 12 sectors where we have targets. Emission reductions were attributed to multiple factors including grid decarbonisation and more customers implementing their own emission reduction plans. Our focus this year has been on operationalising existing plans, improving data and modelling, integrating targets into lending processes (both reviews and new lending), refining policies and developing solutions to better support customers in achieving their climate goals. As part of this, we engaged just over 150 institutional customers on their climate transition plans and found that 84% of customers assessed had a public climate transition plan. We are committed to partnering with customers and to supporting them through the transition. In practical terms, this means we are ready to increase support to customers to reduce their emissions intensity. We have broken new ground this year with the development of our Sustainable Upgrades home and investor loans, collaborating with the Clean Energy Finance Corporation (CEFC) to enable home loan customers to invest in the energy efficiency or climate resilience of their properties and reduce their energy costs. The CEFC $1 billion Household Energy Upgrades Fund (HEUF) is a landmark program to help Australians improve energy efficiency. We are proud to be the first bank to facilitate customer support through this fund. In New Zealand, we launched a new Sustainable Equipment Finance Loan, supporting Kiwi businesses to reduce their climate impacts through a range of sustainable assets, such as electric vehicles. These products build on the success of Westpac New Zealand’s Sustainable Farm Loan and Sustainable Business Loan launched last year that now have balances of over NZ$4.1 billion. Earlier in FY24, we introduced a new framework to define and assess sustainable financing. At 30 September 2024, we had assessed a total committed exposure (TCE) of $28.7 billion and facilitated approximately $13.7 billion in bonds (cumulative) between 2021 and 2024. This puts us on track to meet our 2030 sustainable finance targets of $55 billion in TCE and $40 billion in bond facilitation. 3. Collaborating for impact Tackling climate change requires collective effort. Our third area of action is collaborating for meaningful impact with stakeholders in Australia, New Zealand, and globally, including governments, NGOs, communities, and industry bodies. Our aspiration is to support a transition that is inclusive. This is particularly important given the pressure of higher costs on both households and businesses. Recognising the need to maintain momentum on the climate transition, we have committed to invest in Virescent Ventures, a new venture capital fund focused on investing in early-stage climate-related technologies aimed at addressing these challenges. Investing alongside the CEFC and participating in the fund provides us with the opportunity to gain insights into emerging technologies and collaborate with companies within the fund where synergies exist. Beyond generating long-term returns, we aim for this initiative to support our net-zero objectives and help customers, particularly in hard-to-abate sectors, advance their own transition plans. Looking ahead We will continue to focus on supporting customers in their transition and expanding our sustainable finance, while keeping our targets in sight. New climate reporting standards in Australia have been finalised and while we have been aligning to global frameworks for some years, further work is required to fully comply by FY26. Related to these are the New Zealand climate standards already in place and APRA’s Prudential Practice Guide CPG229 focusing on prudent practices in relation to climate change financial risk management. These requirements require further reporting on the financial and strategic impacts of climate change and integrating climate risks and opportunities into how we run the Company. I would like to finish by mentioning that this is my last Climate Report, having announced my plans to retire after our AGM in December. I am immensely proud of the progress we have made on climate and sustainability during my tenure as CEO. That said, the journey has been made easier by the dedication of our people to help customers and communities to transition. As always, we welcome feedback as we continue working together towards a more sustainable future. Sincerely, Peter King CEO 1 NZBA Guidelines require sector-level targets be set for all, or a substantial majority of, carbon-intensive sectors (where data and methodologies allow) that include agriculture, aluminium, cement, coal, commercial and residential real estate, iron and steel, oil and gas, power generation and transport. WESTPAC GROUP 2024 CLIMATE REPORT |

| INTRODUCTION GOVERNANCE STRATEGY RISK MANAGEMENT METRICS AND TARGETS APPENDIX 5 GOVERNANCE Westpac has been integrating climate change risks and opportunities into its operations – this starts with governance. Highlight CLIMATE-RELATED MEASURES MORE EXPLICITLY INCLUDED IN EXECUTIVES' SHORT-TERM VARIABLE REWARD |

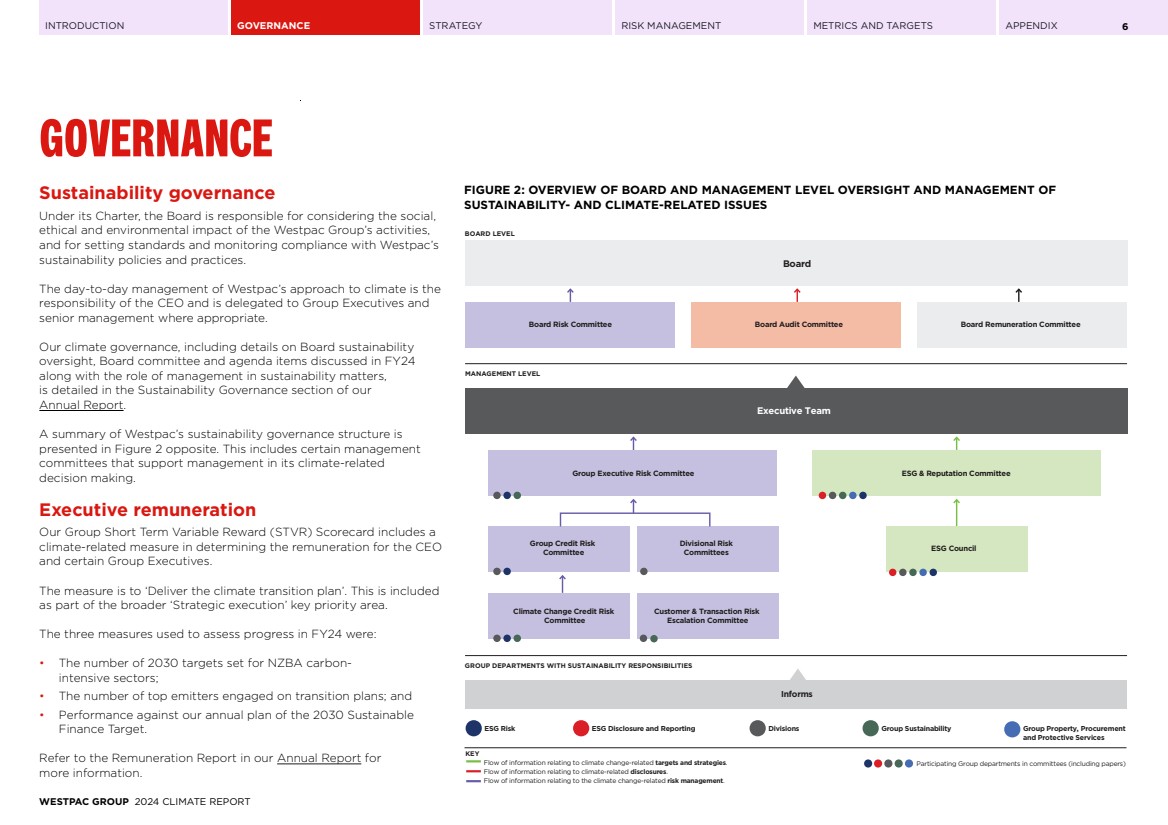

| INTRODUCTION GOVERNANCE STRATEGY RISK MANAGEMENT METRICS AND TARGETS APPENDIX 6 GOVERNANCE Sustainability governance Under its Charter, the Board is responsible for considering the social, ethical and environmental impact of the Westpac Group’s activities, and for setting standards and monitoring compliance with Westpac’s sustainability policies and practices. The day-to-day management of Westpac’s approach to climate is the responsibility of the CEO and is delegated to Group Executives and senior management where appropriate. Our climate governance, including details on Board sustainability oversight, Board committee and agenda items discussed in FY24 along with the role of management in sustainability matters, is detailed in the Sustainability Governance section of our Annual Report. A summary of Westpac’s sustainability governance structure is presented in Figure 2 opposite. This includes certain management committees that support management in its climate-related decision making. Executive remuneration Our Group Short Term Variable Reward (STVR) Scorecard includes a climate-related measure in determining the remuneration for the CEO and certain Group Executives. The measure is to ‘Deliver the climate transition plan’. This is included as part of the broader ‘Strategic execution’ key priority area. The three measures used to assess progress in FY24 were: • The number of 2030 targets set for NZBA carbon-intensive sectors; • The number of top emitters engaged on transition plans; and • Performance against our annual plan of the 2030 Sustainable Finance Target. Refer to the Remuneration Report in our Annual Report for more information. FIGURE 2: OVERVIEW OF BOARD AND MANAGEMENT LEVEL OVERSIGHT AND MANAGEMENT OF SUSTAINABILITY- AND CLIMATE-RELATED ISSUES MANAGEMENT LEVEL GROUP DEPARTMENTS WITH SUSTAINABILITY RESPONSIBILITIES ESG Risk ESG Disclosure and Reporting Divisions Group Sustainability Group Property, Procurement and Protective Services KEY Flow of information relating to climate change-related targets and strategies. Flow of information relating to climate-related disclosures. Flow of information relating to the climate change-related risk management. BOARD LEVEL Participating Group departments in committees (including papers) Informs Climate Change Credit Risk Committee Customer & Transaction Risk Escalation Committee Group Executive Risk Committee ESG & Reputation Committee ESG Council Group Credit Risk Committee Divisional Risk Committees Executive Team Board Risk Committee Board Audit Committee Board Remuneration Committee Board WESTPAC GROUP 2024 CLIMATE REPORT |

| INTRODUCTION GOVERNANCE STRATEGY RISK MANAGEMENT METRICS AND TARGETS APPENDIX 7 STRATEGY Our climate strategy is driven by our ambition to become a net-zero, climate resilient bank. Our three areas of action: 1. NET-ZERO, CLIMATE RESILIENT OPERATIONS 2. SUPPORTING CUSTOMERS’ TRANSITION TO NET-ZERO AND TO BUILD THEIR CLIMATE RESILIENCE 3. COLLABORATE FOR IMPACT ON INITIATIVES TOWARDS NET-ZERO AND CLIMATE RESILIENCE |

| INTRODUCTION GOVERNANCE STRATEGY RISK MANAGEMENT METRICS AND TARGETS APPENDIX 8 Setting our strategy and targets Our climate strategy has evolved over many years and is founded on our ambition to become a net-zero, climate resilient bank. This ambition was first set as part of our CCPS in 2022 after significant consultation with our stakeholders, including customers, our people, shareholders, governments, and the community. Our ambition is an objective within our broader sustainability strategy. That strategy also includes other sustainability objectives for customers, nature, human rights, along with inclusion and diversity, that together support our purpose of Creating better futures together. Our climate strategy is further defined by our three areas of action. See Table 2 opposite. Working towards our climate ambition means reducing the climate change impacts of our operations, and aligning our lending portfolio with net-zero financed emissions by 2050 consistent with a 1.5°C pathway in line with our NZBA commitment. The 1.5°C pathway aligns with the Paris Agreement which aims to limit the global temperature rise this century to well below 2°C above pre-industrial levels, with efforts to limit the increase at 1.5°C. This international treaty on climate change was first set in 2015 and was signed by Australia and New Zealand when it came into force in 2016. We remain committed to pursuing ambitious climate goals. This is reflected in both our operational emissions targets and our NZBA sector targets, where we have aligned our reference scenarios with the Paris Agreement. However limiting the increase in temperature to 1.5°C requires unprecedented change to our economies and as such, we will monitor sector developments, emerging science, and government policy to work with customers to tackle these challenges. Climate change and the interaction with other ESG themes Climate change has widespread effects that overlap with other environmental, social, and governance (ESG) issues, making it important to understand how these areas interact to avoid new risks and negative impacts on customers and communities. Climate change and nature are deeply connected. As natural resources decline and ecosystems we rely on for services face pressure, we are working to integrate these considerations into our plans. Last year, we launched our Natural Capital Position Statement, which defines our ambition to become a nature-positive bank. This year, we have focused on better identifying the risks and opportunities related to nature for our business and customers. We are involved in initiatives such as the United Nations Environment Programme Finance Initiative (UNEP FI) and are a member of the Taskforce on Nature-related Financial Disclosures Forum. The insights from our involvement are helping shape our plans. Physical and transition risks, such as droughts and floods, affect everyone but hit communities unequally, with developing economies being especially vulnerable. These economies often lack the resources and infrastructure to cope with climate change. Risks arising from the economic transition, like the closure of coal mines, can also impact individuals and communities. Our Human Rights Position Statement commits us to respecting human rights and helps guide our actions. We already respond quickly in times of real need when natural disasters strike, offering relief packages and on-the-ground support. We also have a Drought Assistance Package for agribusinesses to assist them to carry-on through the more challenging times. Our approach to hardship more broadly is backed by our specialist hardship support teams. Regardless of the cause of financial stress or hardship, these teams are experts at providing tailored solutions and identifying vulnerability to help customers get back on track. The convergence of these ESG themes highlights the need to deepen our understanding of the intersectionality of climate change, nature, and human rights. It is crucial to assess the long-term impacts and identify how we can best support customers though the transition. Climate change and our business model As one of Australia’s largest financial institutions, we acknowledge that climate change is a significant issue which is already impacting our business, customers and communities. While we expect that, over the longer term, the physical and transition risks arising from climate change may create further challenges for our business and stakeholders, we expect that our core business model of providing financial products and services to customers will be consistent. We will continue to adapt our strategy and operations amid the changing backdrop of climate-related risks and opportunities, and to help deliver on our purpose. TABLE 2: OUR THREE AREAS OF ACTION 1. Net-zero, climate resilient operations This involves leading by example by reducing the direct impact of our operations, setting targets for our scope 1 and 2 and scope 3 upstream emissions and developing our approach to assessing and managing physical climate risk to our operational sites. 2. Supporting customers' transition to net-zero and to build their climate resilience This is focused on reducing our portfolio financed emissions by working with customers on their transition plans, setting targets in all of the NZBA emissions-intensive sectors and having clear sector positions for specific sectors. It also includes identifying opportunities to offer products and services that facilitate customers to transition. 3. Collaborate for impact on initiatives towards net-zero and climate resilience This recognises the need to work with government, industry and business associations on initiatives that align with our principles and ambition to become a net-zero, climate resilient bank. WESTPAC GROUP 2024 CLIMATE REPORT |

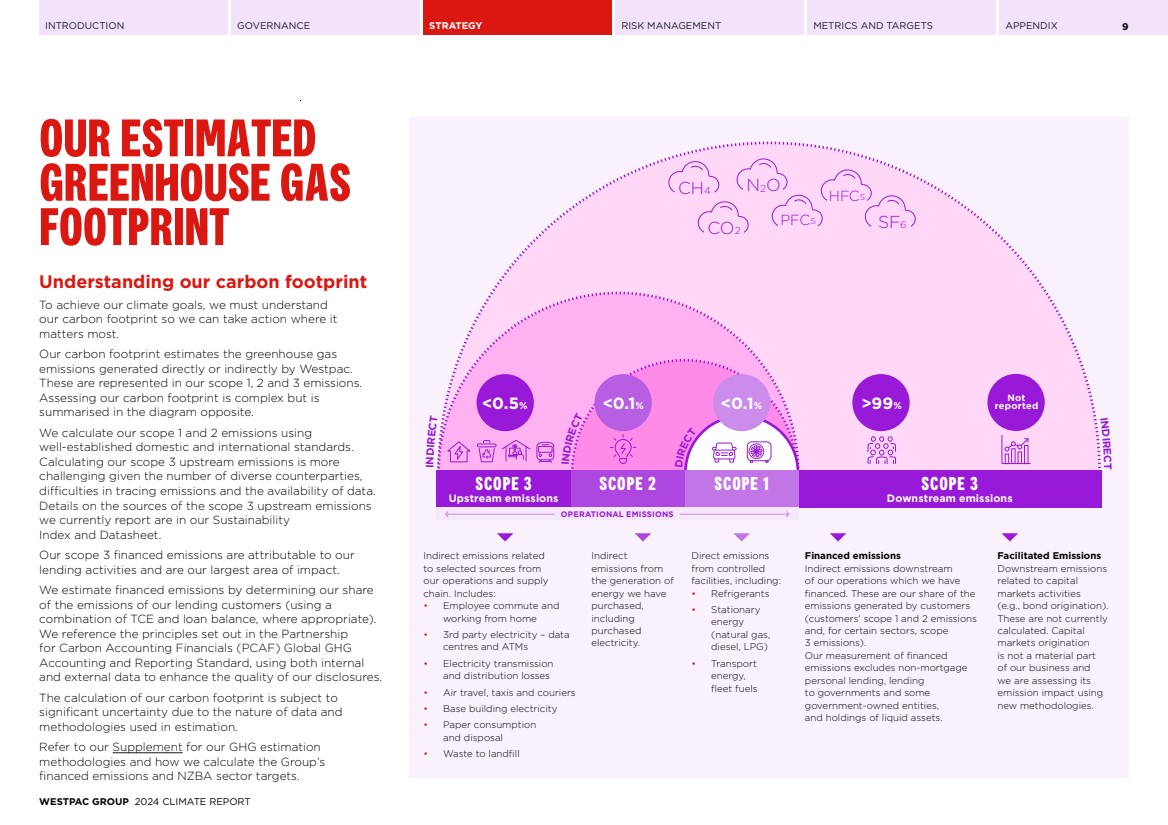

| INTRODUCTION GOVERNANCE STRATEGY RISK MANAGEMENT METRICS AND TARGETS APPENDIX 9 OUR ESTIMATED GREENHOUSE GAS FOOTPRINT Understanding our carbon footprint To achieve our climate goals, we must understand our carbon footprint so we can take action where it matters most. Our carbon footprint estimates the greenhouse gas emissions generated directly or indirectly by Westpac. These are represented in our scope 1, 2 and 3 emissions. Assessing our carbon footprint is complex but is summarised in the diagram opposite. We calculate our scope 1 and 2 emissions using well-established domestic and international standards. Calculating our scope 3 upstream emissions is more challenging given the number of diverse counterparties, difficulties in tracing emissions and the availability of data. Details on the sources of the scope 3 upstream emissions we currently report are in our Sustainability Index and Datasheet. Our scope 3 financed emissions are attributable to our lending activities and are our largest area of impact. We estimate financed emissions by determining our share of the emissions of our lending customers (using a combination of TCE and loan balance, where appropriate). We reference the principles set out in the Partnership for Carbon Accounting Financials (PCAF) Global GHG Accounting and Reporting Standard, using both internal and external data to enhance the quality of our disclosures. The calculation of our carbon footprint is subject to significant uncertainty due to the nature of data and methodologies used in estimation. Refer to our Supplement for our GHG estimation methodologies and how we calculate the Group’s financed emissions and NZBA sector targets. CH4 CO2 N2O HFCS PFCS SF6 IN DIR E C T IN DIR E CT <0.1% >99% Not <0.5% <0.1% reported SCOPE 3 SCOPE 2 SCOPE 1 SCOPE 3 Upstream emissions Downstream emissions DIRECT IN DIRECT OPERATIONAL EMISSIONS Indirect emissions related to selected sources from our operations and supply chain. Includes: • Employee commute and working from home • 3rd party electricity – data centres and ATMs • Electricity transmission and distribution losses • Air travel, taxis and couriers • Base building electricity • Paper consumption and disposal • Waste to landfill Indirect emissions from the generation of energy we have purchased, including purchased electricity. Direct emissions from controlled facilities, including: • Refrigerants • Stationary energy (natural gas, diesel, LPG) • Transport energy, fleet fuels Financed emissions Indirect emissions downstream of our operations which we have financed. These are our share of the emissions generated by customers (customers' scope 1 and 2 emissions and, for certain sectors, scope 3 emissions). Our measurement of financed emissions excludes non-mortgage personal lending, lending to governments and some government-owned entities, and holdings of liquid assets. Facilitated Emissions Downstream emissions related to capital markets activities (e.g., bond origination). These are not currently calculated. Capital markets origination is not a material part of our business and we are assessing its emission impact using new methodologies. WESTPAC GROUP 2024 CLIMATE REPORT |

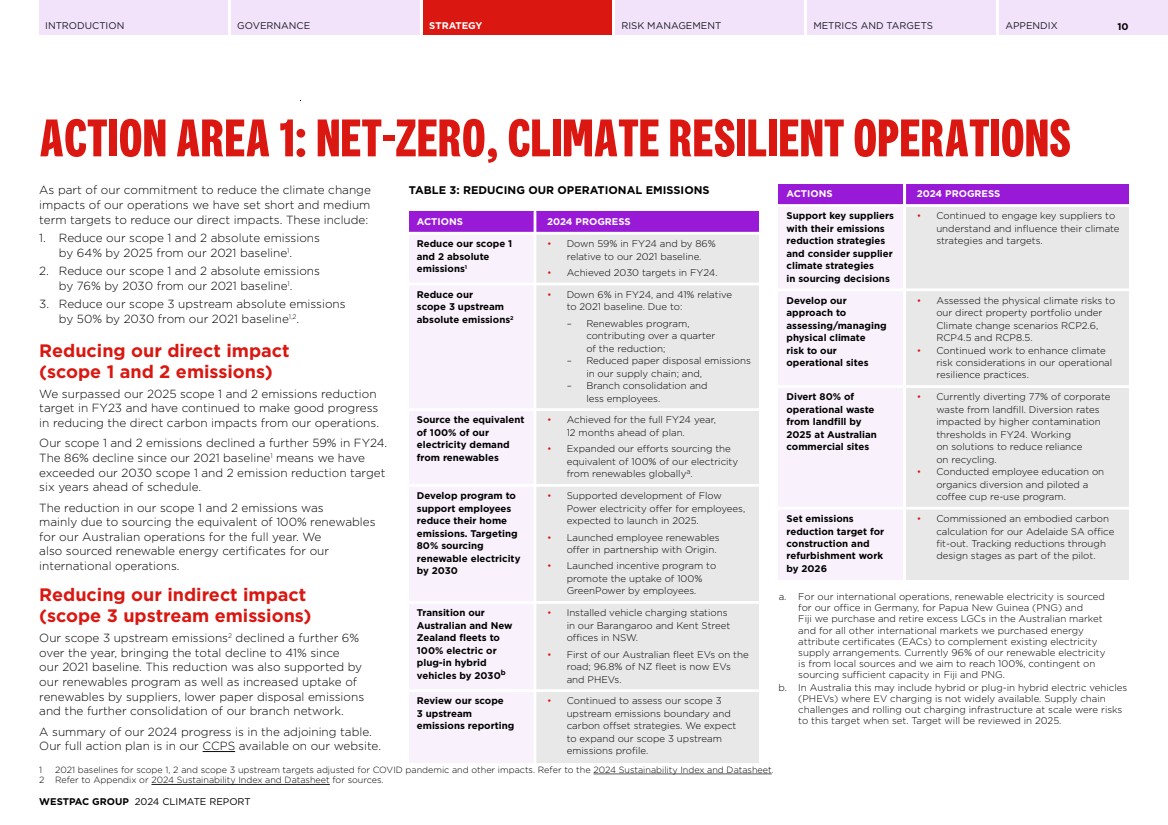

| INTRODUCTION GOVERNANCE STRATEGY RISK MANAGEMENT METRICS AND TARGETS APPENDIX 10 ACTION AREA 1: NET-ZERO, CLIMATE RESILIENT OPERATIONS As part of our commitment to reduce the climate change impacts of our operations we have set short and medium term targets to reduce our direct impacts. These include: 1. Reduce our scope 1 and 2 absolute emissions by 64% by 2025 from our 2021 baseline1 .. 2. Reduce our scope 1 and 2 absolute emissions by 76% by 2030 from our 2021 baseline1 .. 3. Reduce our scope 3 upstream absolute emissions by 50% by 2030 from our 2021 baseline1,2 .. Reducing our direct impact (scope 1 and 2 emissions) We surpassed our 2025 scope 1 and 2 emissions reduction target in FY23 and have continued to make good progress in reducing the direct carbon impacts from our operations. Our scope 1 and 2 emissions declined a further 59% in FY24. The 86% decline since our 2021 baseline1 means we have exceeded our 2030 scope 1 and 2 emission reduction target six years ahead of schedule. The reduction in our scope 1 and 2 emissions was mainly due to sourcing the equivalent of 100% renewables for our Australian operations for the full year. We also sourced renewable energy certificates for our international operations. Reducing our indirect impact (scope 3 upstream emissions) Our scope 3 upstream emissions2 declined a further 6% over the year, bringing the total decline to 41% since our 2021 baseline. This reduction was also supported by our renewables program as well as increased uptake of renewables by suppliers, lower paper disposal emissions and the further consolidation of our branch network. A summary of our 2024 progress is in the adjoining table. Our full action plan is in our CCPS available on our website. TABLE 3: REDUCING OUR OPERATIONAL EMISSIONS ACTIONS 2024 PROGRESS Reduce our scope 1 and 2 absolute emissions1 • Down 59% in FY24 and by 86% relative to our 2021 baseline. • Achieved 2030 targets in FY24. Reduce our scope 3 upstream absolute emissions2 • Down 6% in FY24, and 41% relative to 2021 baseline. Due to: – Renewables program, contributing over a quarter of the reduction; – Reduced paper disposal emissions in our supply chain; and, – Branch consolidation and less employees. Source the equivalent of 100% of our electricity demand from renewables • Achieved for the full FY24 year, 12 months ahead of plan. • Expanded our efforts sourcing the equivalent of 100% of our electricity from renewables globallya .. Develop program to support employees reduce their home emissions. Targeting 80% sourcing renewable electricity by 2030 • Supported development of Flow Power electricity offer for employees, expected to launch in 2025. • Launched employee renewables offer in partnership with Origin. • Launched incentive program to promote the uptake of 100% GreenPower by employees. Transition our Australian and New Zealand fleets to 100% electric or plug-in hybrid vehicles by 2030b • Installed vehicle charging stations in our Barangaroo and Kent Street offices in NSW. • First of our Australian fleet EVs on the road; 96.8% of NZ fleet is now EVs and PHEVs. Review our scope 3 upstream emissions reporting • Continued to assess our scope 3 upstream emissions boundary and carbon offset strategies. We expect to expand our scope 3 upstream emissions profile. ACTIONS 2024 PROGRESS Support key suppliers with their emissions reduction strategies and consider supplier climate strategies in sourcing decisions • Continued to engage key suppliers to understand and influence their climate strategies and targets. Develop our approach to assessing/managing physical climate risk to our operational sites • Assessed the physical climate risks to our direct property portfolio under Climate change scenarios RCP2.6, RCP4.5 and RCP8.5. • Continued work to enhance climate risk considerations in our operational resilience practices. Divert 80% of operational waste from landfill by 2025 at Australian commercial sites • Currently diverting 77% of corporate waste from landfill. Diversion rates impacted by higher contamination thresholds in FY24. Working on solutions to reduce reliance on recycling. • Conducted employee education on organics diversion and piloted a coffee cup re-use program. Set emissions reduction target for construction and refurbishment work by 2026 • Commissioned an embodied carbon calculation for our Adelaide SA office fit-out. Tracking reductions through design stages as part of the pilot. a. For our international operations, renewable electricity is sourced for our office in Germany, for Papua New Guinea (PNG) and Fiji we purchase and retire excess LGCs in the Australian market and for all other international markets we purchased energy attribute certificates (EACs) to complement existing electricity supply arrangements. Currently 96% of our renewable electricity is from local sources and we aim to reach 100%, contingent on sourcing sufficient capacity in Fiji and PNG. b. In Australia this may include hybrid or plug-in hybrid electric vehicles (PHEVs) where EV charging is not widely available. Supply chain challenges and rolling out charging infrastructure at scale were risks to this target when set. Target will be reviewed in 2025. 1 2021 baselines for scope 1, 2 and scope 3 upstream targets adjusted for COVID pandemic and other impacts. Refer to the 2024 Sustainability Index and Datasheet. 2 Refer to Appendix or 2024 Sustainability Index and Datasheet for sources. WESTPAC GROUP 2024 CLIMATE REPORT |

| INTRODUCTION GOVERNANCE STRATEGY RISK MANAGEMENT METRICS AND TARGETS APPENDIX ACTION AREA 1: NET-ZERO, CLIMATE RESILIENT OPERATIONS 11 Our approach to renewables We are proud to have sourced the equivalent of 100% of our direct electricity demand from renewable sources – achieving this milestone 12 months ahead of schedule. Our approach has been to support the development of new renewables capacity in the grid where possible, rather than purchasing from existing generation facilities. This effort involved years of collaboration with suppliers to support the development of the Bomen Solar Farm in Wagga Wagga, New South Wales and the Berri Solar Farm and Battery in South Australia. We reached the equivalent of 100% renewables for our national operations in April 2023, making FY24 our first full year of sourcing for our Australian business. This year we expanded our efforts to cover all our international operations, sourcing the equivalent of 100% of our electricity globally1 .. Our next goal is to source renewable electricity in the markets where it is consumed. Currently 96% of our renewable electricity is from local sources and we aim to reach 100%, contingent on sourcing sufficient capacity in Fiji and PNG. Our renewable strategy goes beyond sourcing renewable electricity, it’s also about giving back to the communities that host the facilities. We have worked with our partners to establish community funds supporting local initiatives which in FY24 supported: • Planting a further 10,000 trees and shrubs in the valley opposite the Bomen Solar Farm as part of a 50,000- planting target to re-green the valley; • Programs at Wagga Wagga’s Mount Austin High School, aimed at empowering girls to stay in school and assisting year 12 students with their next steps whether in further education or their careers; and, • Supported the launch of a 'Pathway to Electrotechnology' program in partnership with the Tauondi Aboriginal College in Adelaide to support First Nations students to gain employment in the evolving energy sector. Sharing success Our approach to sourcing renewable electricity reflects our commitment to actively participate in the transition to a cleaner energy future. Leveraging our scale and deep understanding of energy and carbon markets, we have delivered long-term benefits not only to Westpac but also for the grid and the communities in which we operate. Building on this experience, we are now extending our impact to customers, suppliers and employees. For customers we are facilitating relationships with our energy suppliers to help them access renewable energy. We are also seeking opportunities to support key suppliers with their renewables transition where needed. For employees, we have launched a renewable offer to help reduce their carbon footprint at home. As existing supply contracts mature, we are exploring opportunities to use our scale to support the underwriting of additional renewable capacity and looking to share these efficiency benefits with suppliers, employees and customers. These initiatives help to improve the emissions profile of our stakeholders, contributing to our own scope 3 upstream emissions reduction. Assessing our climate resilience Westpac undertook scenario analysis to better understand the impacts of climate change to our global operational footprint and to inform climate resilience decision making for our operations. Three climate change scenarios (IPCC Representative Concentration Pathways (RCPs)) were considered: • IPCC RCP2.6 (represents a stringent emissions reduction pathway that is likely to keep temperatures below 2°C by 2100); • IPCC RCP4.5 (represents an intermediate scenario where temperatures are likely to exceed 2°C by 2100); and, • IPCC RCP8.5 (represents a higher emissions scenario where there are no additional efforts to constrain emissions). Insights from the scenario analysis showed elevated fire, precipitation and flood risk as global temperatures rise. Refer to Glossary (page 58) for more information on the RCPs. 1 For our international operations, renewable electricity is sourced for our offices in Germany, for PNG and Fiji we purchase and retire excess LGCs in the Australian market and for all other international markets we purchased EACs to complement existing retail electricity supply arrangements. WESTPAC GROUP 2024 CLIMATE REPORT |

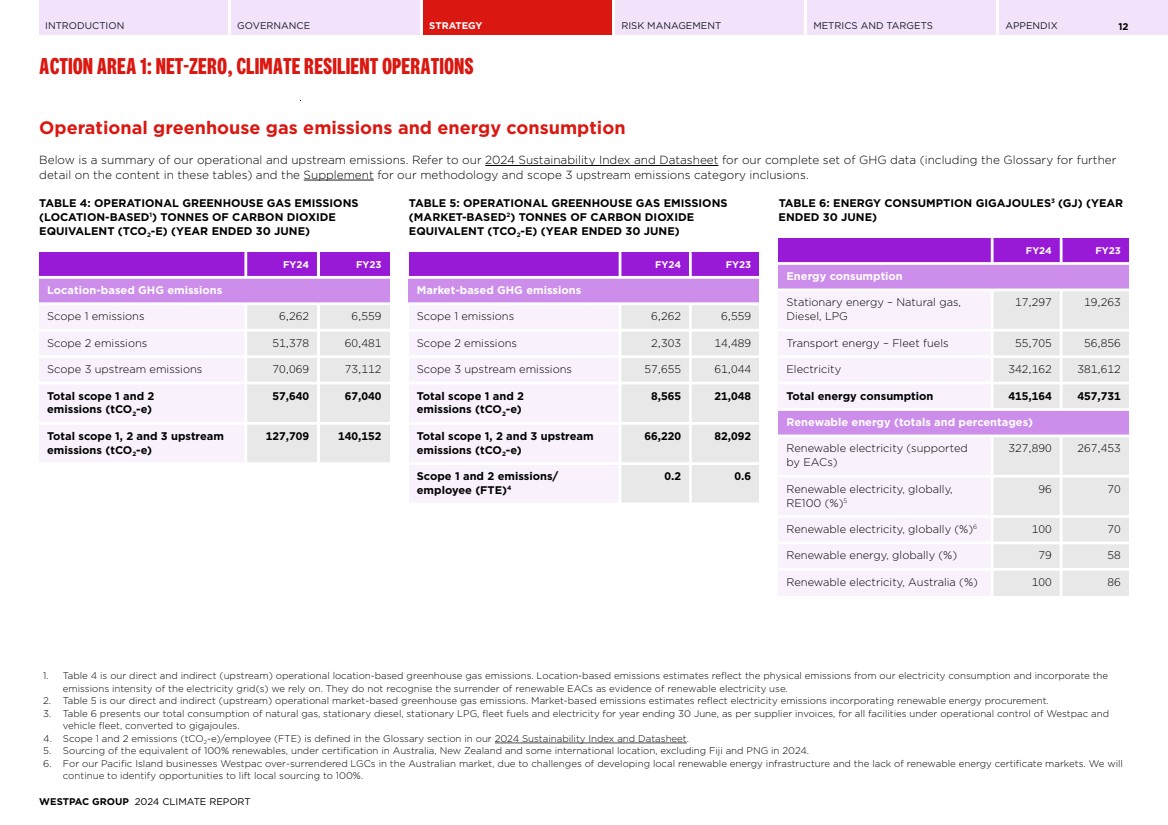

| INTRODUCTION GOVERNANCE STRATEGY RISK MANAGEMENT METRICS AND TARGETS APPENDIX ACTION AREA 1: NET-ZERO, CLIMATE RESILIENT OPERATIONS 12 Operational greenhouse gas emissions and energy consumption Below is a summary of our operational and upstream emissions. Refer to our 2024 Sustainability Index and Datasheet for our complete set of GHG data (including the Glossary for further detail on the content in these tables) and the Supplement for our methodology and scope 3 upstream emissions category inclusions. TABLE 4: OPERATIONAL GREENHOUSE GAS EMISSIONS (LOCATION-BASED1) TONNES OF CARBON DIOXIDE EQUIVALENT (TCO2-E) (YEAR ENDED 30 JUNE) FY24 FY23 Location-based GHG emissions Scope 1 emissions 6,262 6,559 Scope 2 emissions 51,378 60,481 Scope 3 upstream emissions 70,069 73,112 Total scope 1 and 2 emissions (tCO2-e) 57,640 67,040 Total scope 1, 2 and 3 upstream emissions (tCO2-e) 127,709 140,152 TABLE 5: OPERATIONAL GREENHOUSE GAS EMISSIONS (MARKET-BASED2) TONNES OF CARBON DIOXIDE EQUIVALENT (TCO2-E) (YEAR ENDED 30 JUNE) FY24 FY23 Market-based GHG emissions Scope 1 emissions 6,262 6,559 Scope 2 emissions 2,303 14,489 Scope 3 upstream emissions 57,655 61,044 Total scope 1 and 2 emissions (tCO2-e) 8,565 21,048 Total scope 1, 2 and 3 upstream emissions (tCO2-e) 66,220 82,092 Scope 1 and 2 emissions/ employee (FTE)4 0.2 0.6 TABLE 6: ENERGY CONSUMPTION GIGAJOULES3 (GJ) (YEAR ENDED 30 JUNE) FY24 FY23 Energy consumption Stationary energy – Natural gas, Diesel, LPG 17,297 19,263 Transport energy – Fleet fuels 55,705 56,856 Electricity 342,162 381,612 Total energy consumption 415,164 457,731 Renewable energy (totals and percentages) Renewable electricity (supported by EACs) 327,890 267,453 Renewable electricity, globally, RE100 (%)5 96 70 Renewable electricity, globally (%)6 100 70 Renewable energy, globally (%) 79 58 Renewable electricity, Australia (%) 100 86 1. Table 4 is our direct and indirect (upstream) operational location-based greenhouse gas emissions. Location-based emissions estimates reflect the physical emissions from our electricity consumption and incorporate the emissions intensity of the electricity grid(s) we rely on. They do not recognise the surrender of renewable EACs as evidence of renewable electricity use. 2. Table 5 is our direct and indirect (upstream) operational market-based greenhouse gas emissions. Market-based emissions estimates reflect electricity emissions incorporating renewable energy procurement. 3. Table 6 presents our total consumption of natural gas, stationary diesel, stationary LPG, fleet fuels and electricity for year ending 30 June, as per supplier invoices, for all facilities under operational control of Westpac and vehicle fleet, converted to gigajoules. 4. Scope 1 and 2 emissions (tCO2-e)/employee (FTE) is defined in the Glossary section in our 2024 Sustainability Index and Datasheet. 5. Sourcing of the equivalent of 100% renewables, under certification in Australia, New Zealand and some international location, excluding Fiji and PNG in 2024. 6. For our Pacific Island businesses Westpac over-surrendered LGCs in the Australian market, due to challenges of developing local renewable energy infrastructure and the lack of renewable energy certificate markets. We will continue to identify opportunities to lift local sourcing to 100%. WESTPAC GROUP 2024 CLIMATE REPORT |

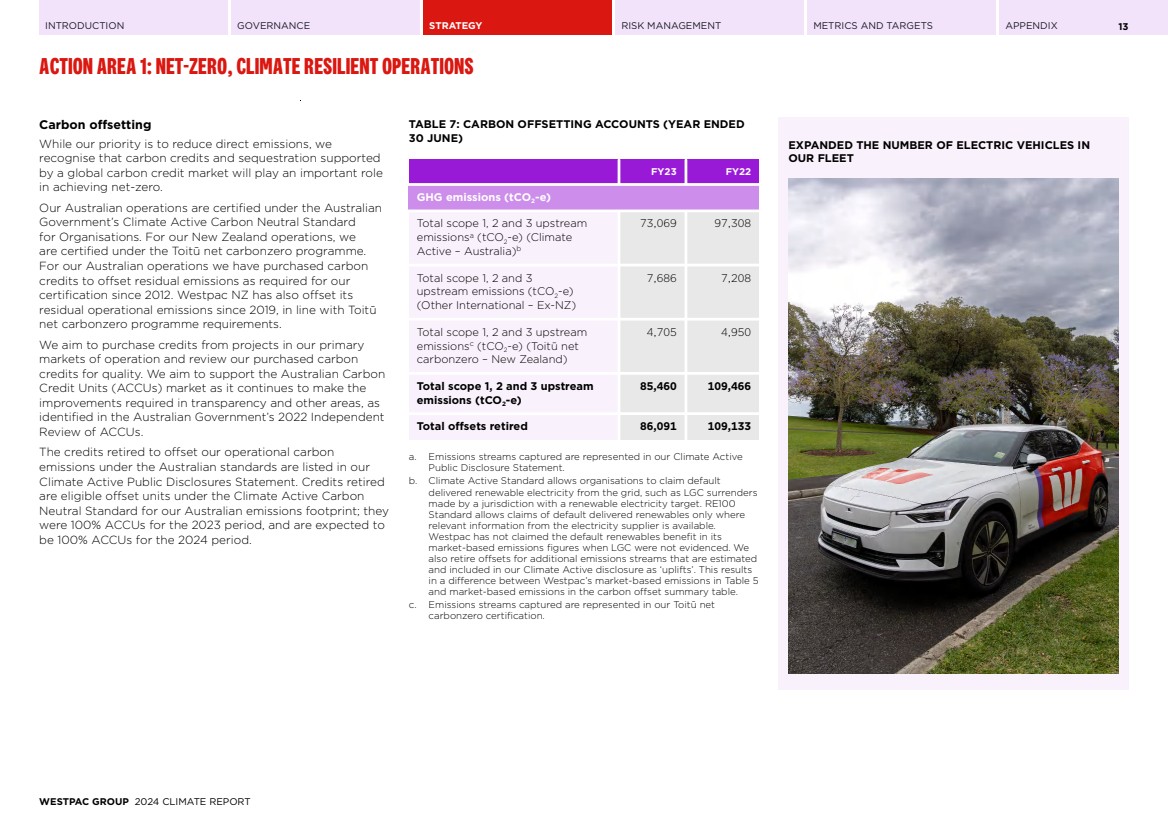

| INTRODUCTION GOVERNANCE STRATEGY RISK MANAGEMENT METRICS AND TARGETS APPENDIX ACTION AREA 1: NET-ZERO, CLIMATE RESILIENT OPERATIONS 13 Carbon offsetting While our priority is to reduce direct emissions, we recognise that carbon credits and sequestration supported by a global carbon credit market will play an important role in achieving net-zero. Our Australian operations are certified under the Australian Government’s Climate Active Carbon Neutral Standard for Organisations. For our New Zealand operations, we are certified under the Toitū net carbonzero programme. For our Australian operations we have purchased carbon credits to offset residual emissions as required for our certification since 2012. Westpac NZ has also offset its residual operational emissions since 2019, in line with Toitū net carbonzero programme requirements. We aim to purchase credits from projects in our primary markets of operation and review our purchased carbon credits for quality. We aim to support the Australian Carbon Credit Units (ACCUs) market as it continues to make the improvements required in transparency and other areas, as identified in the Australian Government’s 2022 Independent Review of ACCUs. The credits retired to offset our operational carbon emissions under the Australian standards are listed in our Climate Active Public Disclosures Statement. Credits retired are eligible offset units under the Climate Active Carbon Neutral Standard for our Australian emissions footprint; they were 100% ACCUs for the 2023 period, and are expected to be 100% ACCUs for the 2024 period. TABLE 7: CARBON OFFSETTING ACCOUNTS (YEAR ENDED 30 JUNE) FY23 FY22 GHG emissions (tCO2-e) Total scope 1, 2 and 3 upstream emissionsa (tCO2-e) (Climate Active – Australia)b 73,069 97,308 Total scope 1, 2 and 3 upstream emissions (tCO2-e) (Other International – Ex-NZ) 7,686 7,208 Total scope 1, 2 and 3 upstream emissionsc (tCO2-e) (Toitū net carbonzero – New Zealand) 4,705 4,950 Total scope 1, 2 and 3 upstream emissions (tCO2-e) 85,460 109,466 Total offsets retired 86,091 109,133 a. Emissions streams captured are represented in our Climate Active Public Disclosure Statement. b. Climate Active Standard allows organisations to claim default delivered renewable electricity from the grid, such as LGC surrenders made by a jurisdiction with a renewable electricity target. RE100 Standard allows claims of default delivered renewables only where relevant information from the electricity supplier is available. Westpac has not claimed the default renewables benefit in its market-based emissions figures when LGC were not evidenced. We also retire offsets for additional emissions streams that are estimated and included in our Climate Active disclosure as ‘uplifts’. This results in a difference between Westpac’s market-based emissions in Table 5 and market-based emissions in the carbon offset summary table. c. Emissions streams captured are represented in our Toitū net carbonzero certification. EXPANDED THE NUMBER OF ELECTRIC VEHICLES IN OUR FLEET WESTPAC GROUP 2024 CLIMATE REPORT |

| INTRODUCTION GOVERNANCE STRATEGY RISK MANAGEMENT METRICS AND TARGETS APPENDIX 14 ACTION AREA 2: SUPPORTING CUSTOMERS’ TRANSITION TO NET-ZERO AND TO BUILD THEIR CLIMATE RESILIENCE To achieve our climate change ambitions, we must reduce our financed emissions and continue to support our customers on their transition to help them enhance their climate resilience. Under this priority area, we are working to: 1. Reduce our financed emissions; 2. Become the transition partner of choice; and 3. Help customers and communities build resilience to the physical impacts of climate change. WESTPAC GROUP 2024 CLIMATE REPORT |

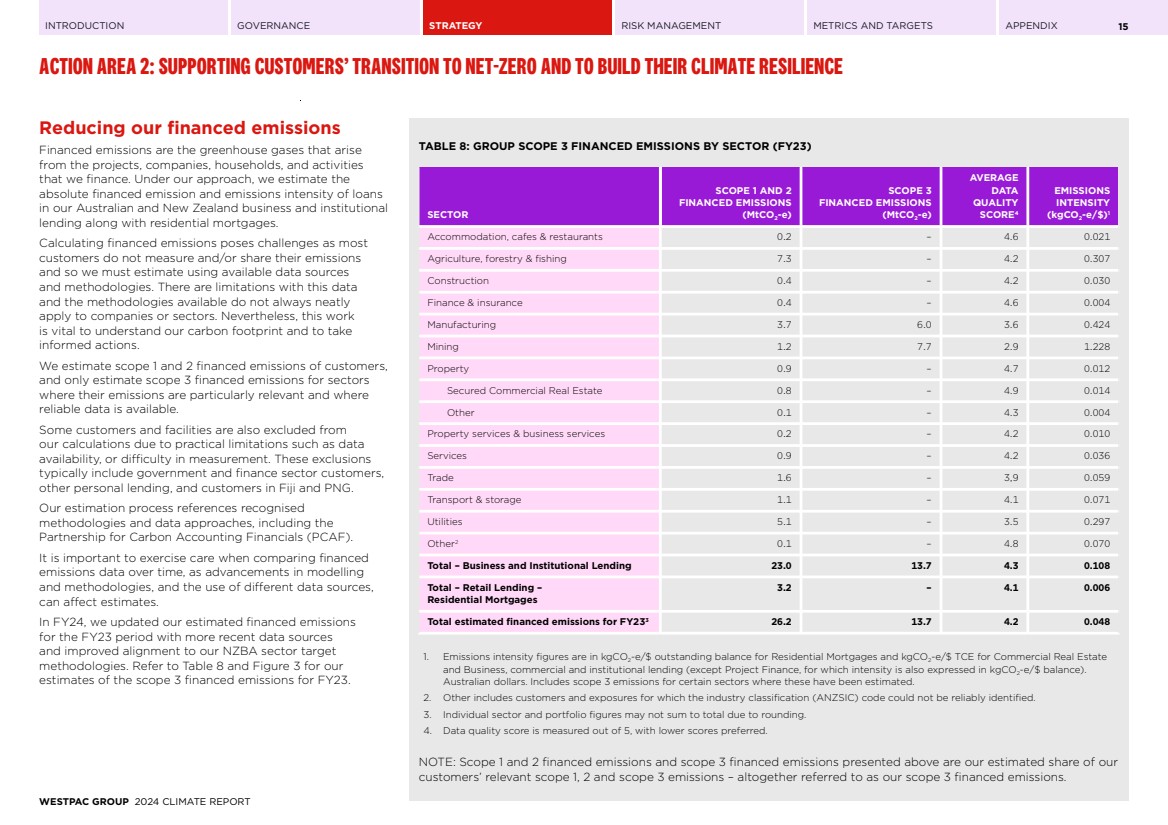

| INTRODUCTION GOVERNANCE STRATEGY RISK MANAGEMENT METRICS AND TARGETS APPENDIX ACTION AREA 2: SUPPORTING CUSTOMERS’ TRANSITION TO NET-ZERO AND TO BUILD THEIR CLIMATE RESILIENCE 15 Reducing our financed emissions Financed emissions are the greenhouse gases that arise from the projects, companies, households, and activities that we finance. Under our approach, we estimate the absolute financed emission and emissions intensity of loans in our Australian and New Zealand business and institutional lending along with residential mortgages. Calculating financed emissions poses challenges as most customers do not measure and/or share their emissions and so we must estimate using available data sources and methodologies. There are limitations with this data and the methodologies available do not always neatly apply to companies or sectors. Nevertheless, this work is vital to understand our carbon footprint and to take informed actions. We estimate scope 1 and 2 financed emissions of customers, and only estimate scope 3 financed emissions for sectors where their emissions are particularly relevant and where reliable data is available. Some customers and facilities are also excluded from our calculations due to practical limitations such as data availability, or difficulty in measurement. These exclusions typically include government and finance sector customers, other personal lending, and customers in Fiji and PNG. Our estimation process references recognised methodologies and data approaches, including the Partnership for Carbon Accounting Financials (PCAF). It is important to exercise care when comparing financed emissions data over time, as advancements in modelling and methodologies, and the use of different data sources, can affect estimates. In FY24, we updated our estimated financed emissions for the FY23 period with more recent data sources and improved alignment to our NZBA sector target methodologies. Refer to Table 8 and Figure 3 for our estimates of the scope 3 financed emissions for FY23. TABLE 8: GROUP SCOPE 3 FINANCED EMISSIONS BY SECTOR (FY23) SECTOR SCOPE 1 AND 2 FINANCED EMISSIONS (MtCO2-e) SCOPE 3 FINANCED EMISSIONS (MtCO2-e) AVERAGE DATA QUALITY SCORE4 EMISSIONS INTENSITY (kgCO2-e/$)1 Accommodation, cafes & restaurants 0.2 – 4.6 0.021 Agriculture, forestry & fishing 7.3 – 4.2 0.307 Construction 0.4 – 4.2 0.030 Finance & insurance 0.4 – 4.6 0.004 Manufacturing 3.7 6.0 3.6 0.424 Mining 1.2 7.7 2.9 1.228 Property 0.9 – 4.7 0.012 Secured Commercial Real Estate 0.8 – 4.9 0.014 Other 0.1 – 4.3 0.004 Property services & business services 0.2 – 4.2 0.010 Services 0.9 – 4.2 0.036 Trade 1.6 – 3,9 0.059 Transport & storage 1.1 – 4.1 0.071 Utilities 5.1 – 3.5 0.297 Other2 0.1 – 4.8 0.070 Total – Business and Institutional Lending 23.0 13.7 4.3 0.108 Total – Retail Lending – Residential Mortgages 3.2 – 4.1 0.006 Total estimated financed emissions for FY233 26.2 13.7 4.2 0.048 1. Emissions intensity figures are in kgCO2-e/$ outstanding balance for Residential Mortgages and kgCO2-e/$ TCE for Commercial Real Estate and Business, commercial and institutional lending (except Project Finance, for which intensity is also expressed in kgCO2-e/$ balance). Australian dollars. Includes scope 3 emissions for certain sectors where these have been estimated. 2. Other includes customers and exposures for which the industry classification (ANZSIC) code could not be reliably identified. 3. Individual sector and portfolio figures may not sum to total due to rounding. 4. Data quality score is measured out of 5, with lower scores preferred. NOTE: Scope 1 and 2 financed emissions and scope 3 financed emissions presented above are our estimated share of our customers’ relevant scope 1, 2 and scope 3 emissions – altogether referred to as our scope 3 financed emissions. WESTPAC GROUP 2024 CLIMATE REPORT |

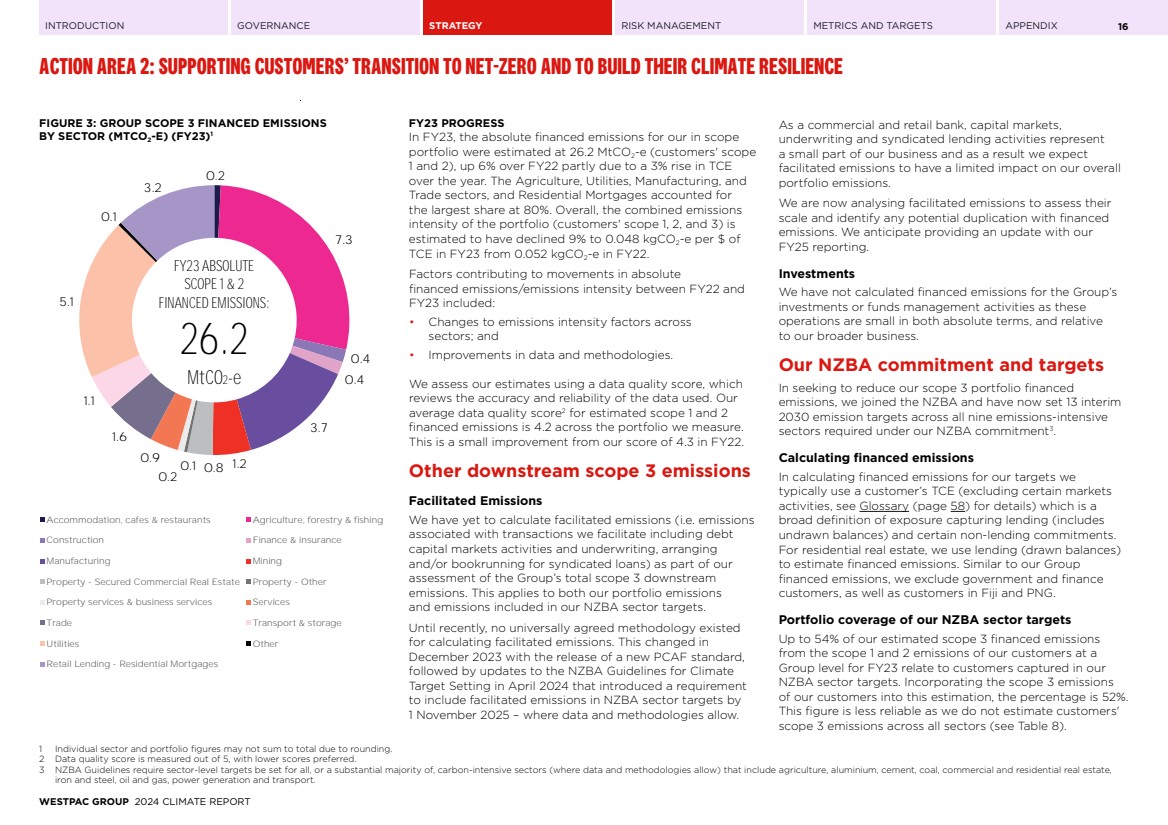

| INTRODUCTION GOVERNANCE STRATEGY RISK MANAGEMENT METRICS AND TARGETS APPENDIX ACTION AREA 2: SUPPORTING CUSTOMERS’ TRANSITION TO NET-ZERO AND TO BUILD THEIR CLIMATE RESILIENCE 16 FIGURE 3: GROUP SCOPE 3 FINANCED EMISSIONS BY SECTOR (MTCO2-E) (FY23)1 0.2 7.3 0.4 0.4 3.7 0.1 0.8 1.2 0.2 0.9 1.6 1.1 5.1 0.1 3.2 Accommodation, cafes & restaurants Agriculture, forestry & fishing Construction Finance & insurance Manufacturing Mining Property - Secured Commercial Real Estate Property - Other Property services & business services Services Trade Transport & storage Utilities Other Retail Lending - Residential Mortgages FY23 ABSOLUTE SCOPE 1 & 2 FINANCED EMISSIONS: 26.2 MtCO2-e FY23 PROGRESS In FY23, the absolute financed emissions for our in scope portfolio were estimated at 26.2 MtCO2-e (customers' scope 1 and 2), up 6% over FY22 partly due to a 3% rise in TCE over the year. The Agriculture, Utilities, Manufacturing, and Trade sectors, and Residential Mortgages accounted for the largest share at 80%. Overall, the combined emissions intensity of the portfolio (customers' scope 1, 2, and 3) is estimated to have declined 9% to 0.048 kgCO2-e per $ of TCE in FY23 from 0.052 kgCO2-e in FY22. Factors contributing to movements in absolute financed emissions/emissions intensity between FY22 and FY23 included: • Changes to emissions intensity factors across sectors; and • Improvements in data and methodologies. We assess our estimates using a data quality score, which reviews the accuracy and reliability of the data used. Our average data quality score2 for estimated scope 1 and 2 financed emissions is 4.2 across the portfolio we measure. This is a small improvement from our score of 4.3 in FY22. Other downstream scope 3 emissions Facilitated Emissions We have yet to calculate facilitated emissions (i.e. emissions associated with transactions we facilitate including debt capital markets activities and underwriting, arranging and/or bookrunning for syndicated loans) as part of our assessment of the Group’s total scope 3 downstream emissions. This applies to both our portfolio emissions and emissions included in our NZBA sector targets. Until recently, no universally agreed methodology existed for calculating facilitated emissions. This changed in December 2023 with the release of a new PCAF standard, followed by updates to the NZBA Guidelines for Climate Target Setting in April 2024 that introduced a requirement to include facilitated emissions in NZBA sector targets by 1 November 2025 – where data and methodologies allow. As a commercial and retail bank, capital markets, underwriting and syndicated lending activities represent a small part of our business and as a result we expect facilitated emissions to have a limited impact on our overall portfolio emissions. We are now analysing facilitated emissions to assess their scale and identify any potential duplication with financed emissions. We anticipate providing an update with our FY25 reporting. Investments We have not calculated financed emissions for the Group’s investments or funds management activities as these operations are small in both absolute terms, and relative to our broader business. Our NZBA commitment and targets In seeking to reduce our scope 3 portfolio financed emissions, we joined the NZBA and have now set 13 interim 2030 emission targets across all nine emissions-intensive sectors required under our NZBA commitment3 .. Calculating financed emissions In calculating financed emissions for our targets we typically use a customer’s TCE (excluding certain markets activities, see Glossary (page 58) for details) which is a broad definition of exposure capturing lending (includes undrawn balances) and certain non-lending commitments. For residential real estate, we use lending (drawn balances) to estimate financed emissions. Similar to our Group financed emissions, we exclude government and finance customers, as well as customers in Fiji and PNG. Portfolio coverage of our NZBA sector targets Up to 54% of our estimated scope 3 financed emissions from the scope 1 and 2 emissions of our customers at a Group level for FY23 relate to customers captured in our NZBA sector targets. Incorporating the scope 3 emissions of our customers into this estimation, the percentage is 52%. This figure is less reliable as we do not estimate customers' scope 3 emissions across all sectors (see Table 8). 1 Individual sector and portfolio figures may not sum to total due to rounding. 2 Data quality score is measured out of 5, with lower scores preferred. 3 NZBA Guidelines require sector-level targets be set for all, or a substantial majority of, carbon-intensive sectors (where data and methodologies allow) that include agriculture, aluminium, cement, coal, commercial and residential real estate, iron and steel, oil and gas, power generation and transport. WESTPAC GROUP 2024 CLIMATE REPORT |

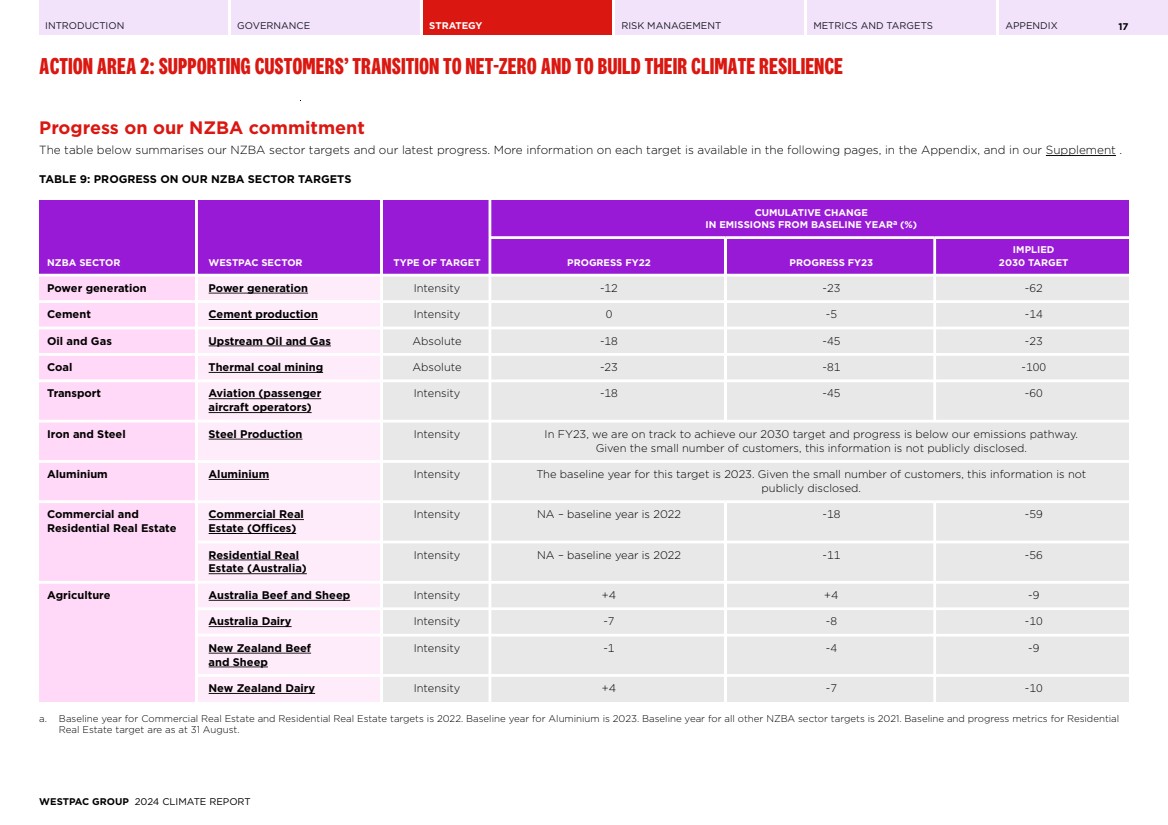

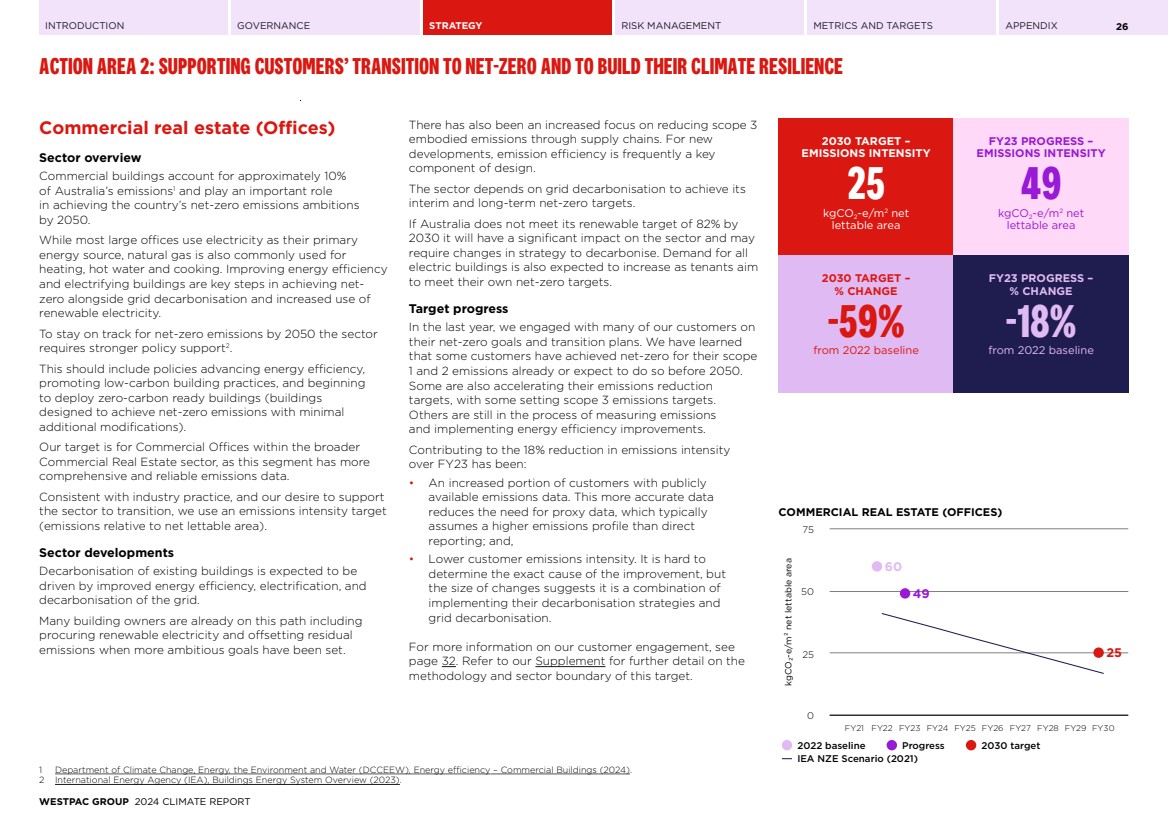

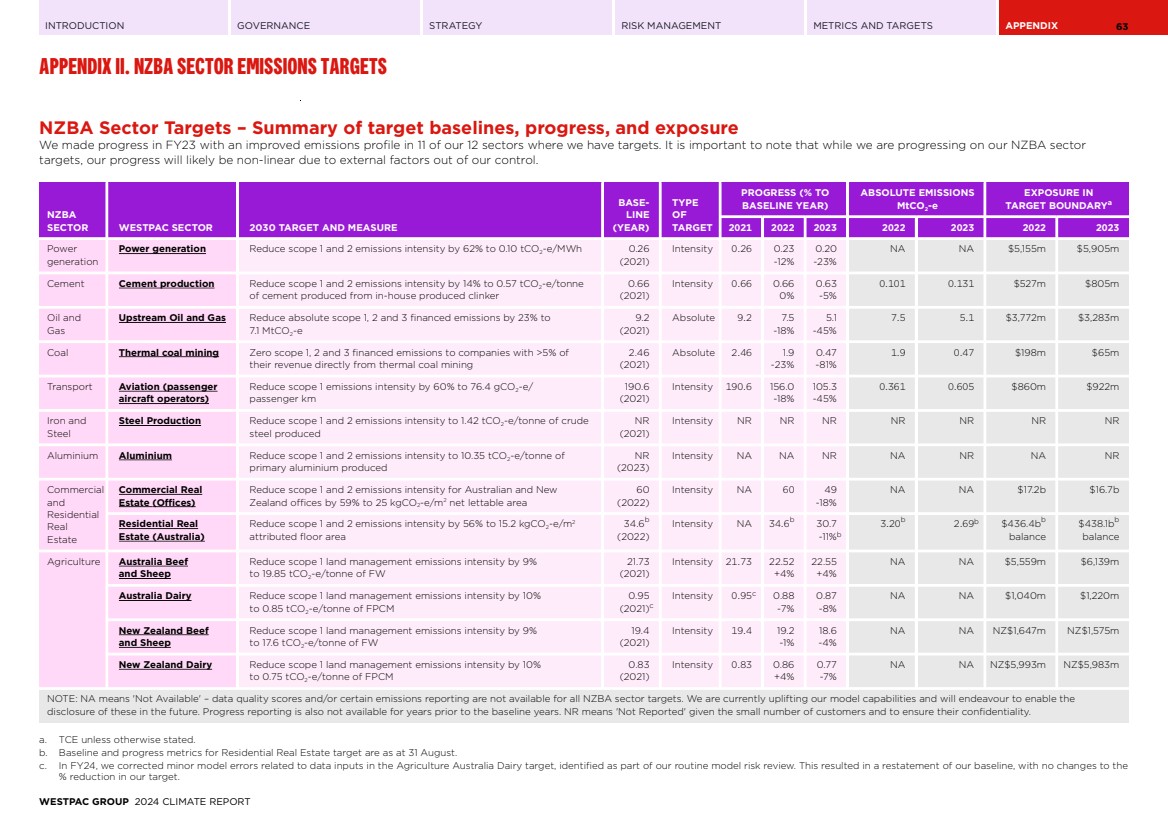

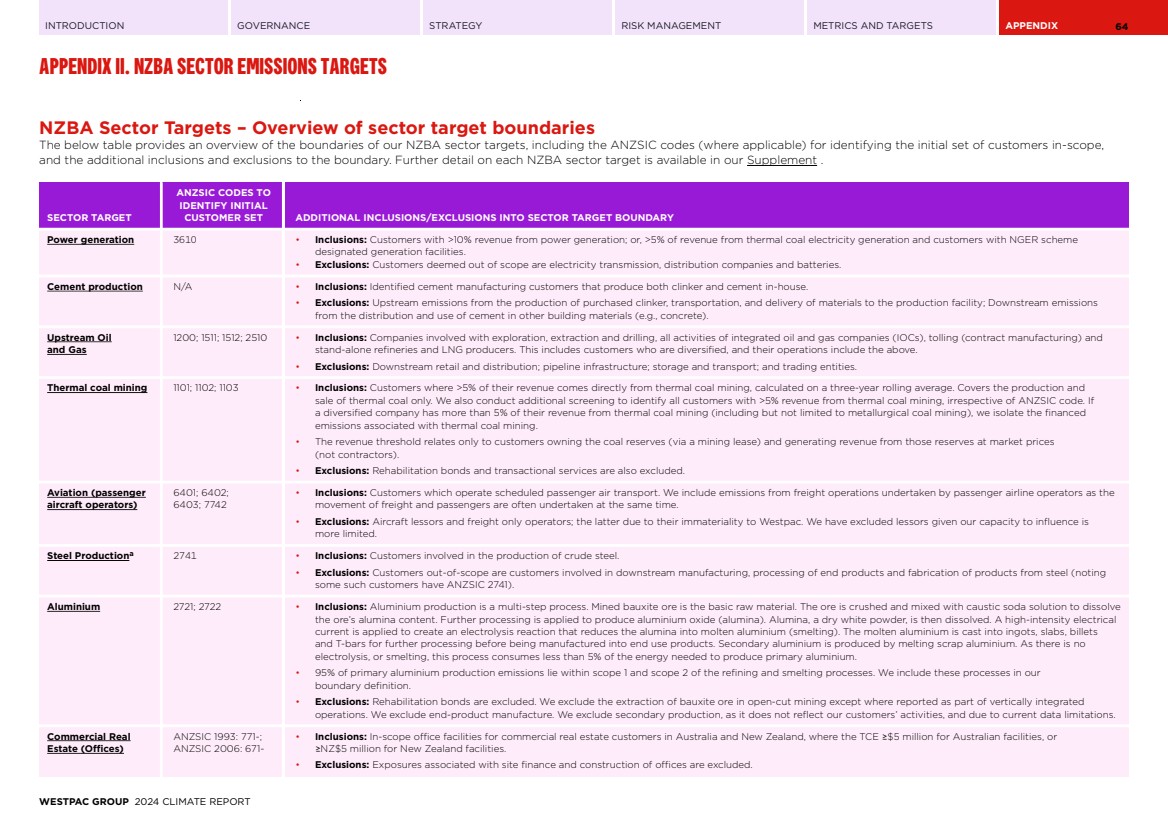

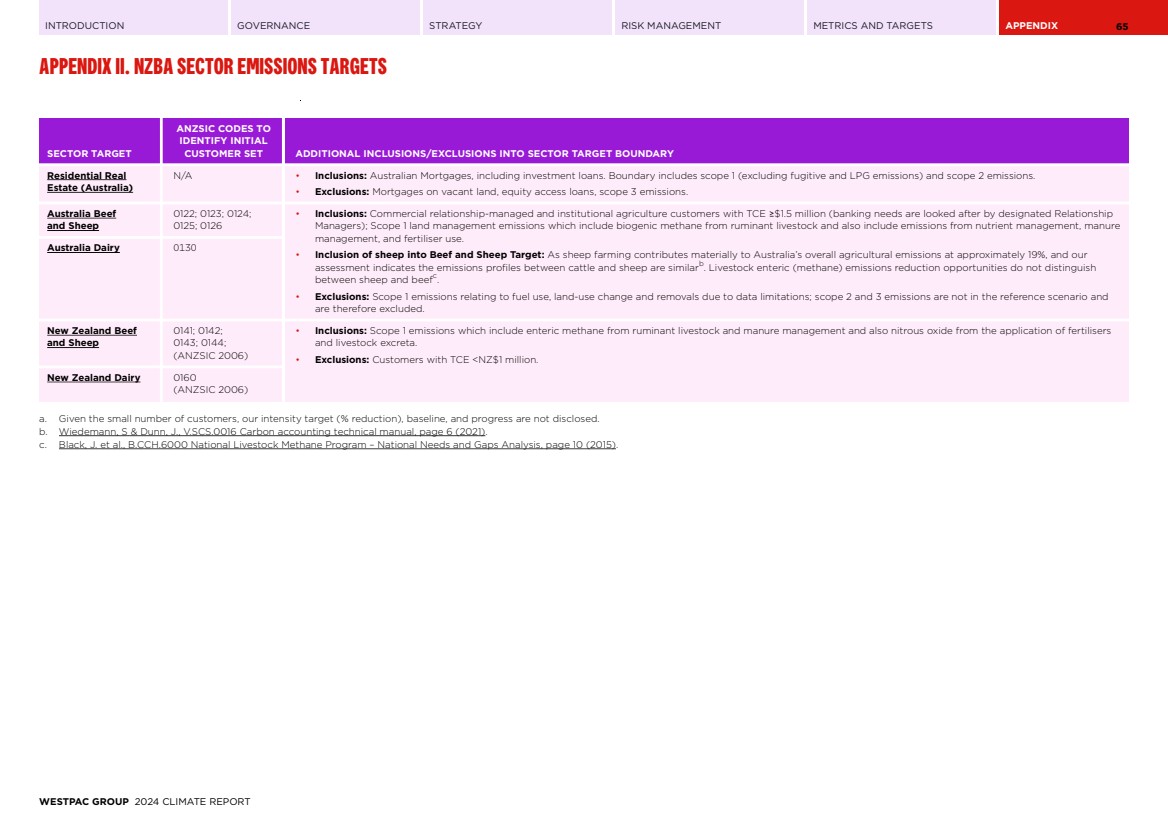

| INTRODUCTION GOVERNANCE STRATEGY RISK MANAGEMENT METRICS AND TARGETS APPENDIX ACTION AREA 2: SUPPORTING CUSTOMERS’ TRANSITION TO NET-ZERO AND TO BUILD THEIR CLIMATE RESILIENCE 17 Progress on our NZBA commitment The table below summarises our NZBA sector targets and our latest progress. More information on each target is available in the following pages, in the Appendix, and in our Supplement . TABLE 9: PROGRESS ON OUR NZBA SECTOR TARGETS NZBA SECTOR WESTPAC SECTOR TYPE OF TARGET CUMULATIVE CHANGE IN EMISSIONS FROM BASELINE YEARa (%) PROGRESS FY22 PROGRESS FY23 IMPLIED 2030 TARGET Power generation Power generation Intensity -12 -23 -62 Cement Cement production Intensity 0 -5 -14 Oil and Gas Upstream Oil and Gas Absolute -18 -45 -23 Coal Thermal coal mining Absolute -23 -81 -100 Transport Aviation (passenger aircraft operators) Intensity -18 -45 -60 Iron and Steel Steel Production Intensity In FY23, we are on track to achieve our 2030 target and progress is below our emissions pathway. Given the small number of customers, this information is not publicly disclosed. Aluminium Aluminium Intensity The baseline year for this target is 2023. Given the small number of customers, this information is not publicly disclosed. Commercial and Residential Real Estate Commercial Real Estate (Offices) Intensity NA – baseline year is 2022 -18 -59 Residential Real Estate (Australia) Intensity NA – baseline year is 2022 -11 -56 Agriculture Australia Beef and Sheep Intensity +4 +4 -9 Australia Dairy Intensity -7 -8 -10 New Zealand Beef and Sheep Intensity -1 -4 -9 New Zealand Dairy Intensity +4 -7 -10 a. Baseline year for Commercial Real Estate and Residential Real Estate targets is 2022. Baseline year for Aluminium is 2023. Baseline year for all other NZBA sector targets is 2021. Baseline and progress metrics for Residential Real Estate target are as at 31 August. WESTPAC GROUP 2024 CLIMATE REPORT |

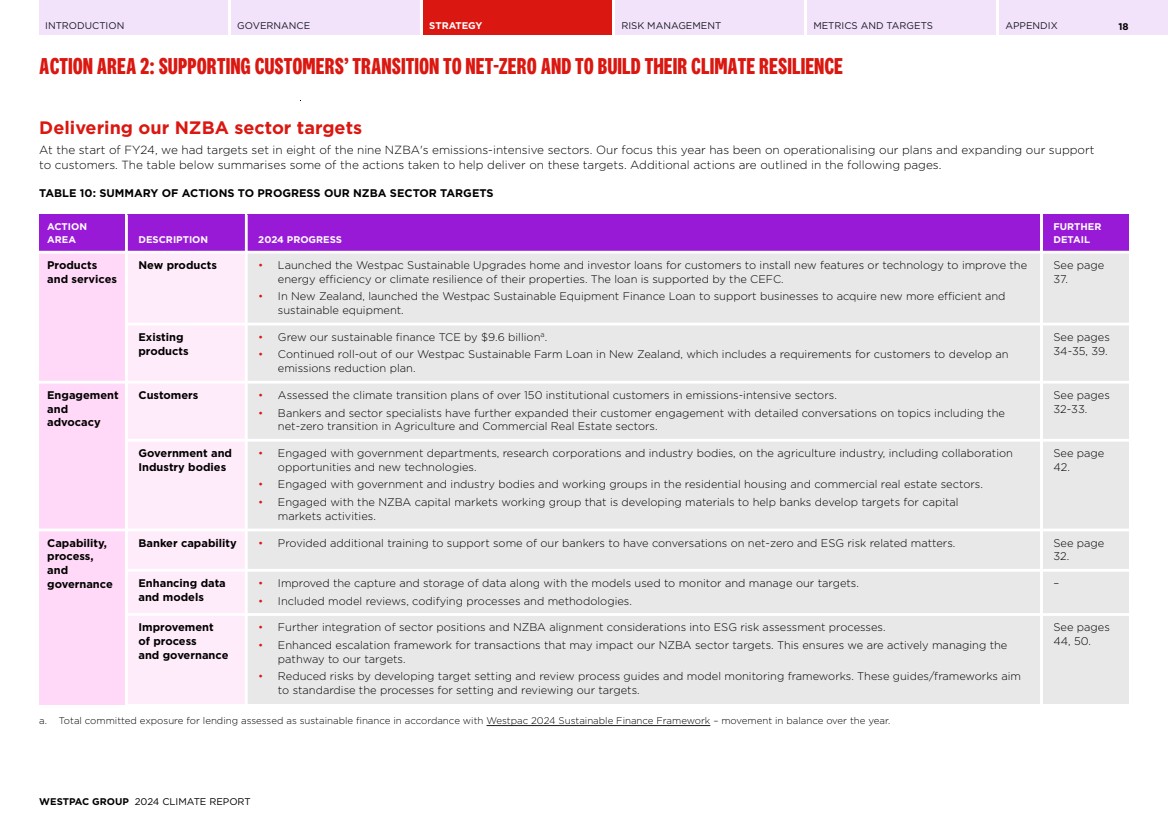

| INTRODUCTION GOVERNANCE STRATEGY RISK MANAGEMENT METRICS AND TARGETS APPENDIX ACTION AREA 2: SUPPORTING CUSTOMERS’ TRANSITION TO NET-ZERO AND TO BUILD THEIR CLIMATE RESILIENCE 18 Delivering our NZBA sector targets At the start of FY24, we had targets set in eight of the nine NZBA's emissions-intensive sectors. Our focus this year has been on operationalising our plans and expanding our support to customers. The table below summarises some of the actions taken to help deliver on these targets. Additional actions are outlined in the following pages. TABLE 10: SUMMARY OF ACTIONS TO PROGRESS OUR NZBA SECTOR TARGETS ACTION AREA DESCRIPTION 2024 PROGRESS FURTHER DETAIL Products and services New products • Launched the Westpac Sustainable Upgrades home and investor loans for customers to install new features or technology to improve the energy efficiency or climate resilience of their properties. The loan is supported by the CEFC. • In New Zealand, launched the Westpac Sustainable Equipment Finance Loan to support businesses to acquire new more efficient and sustainable equipment. See page 37. Existing products • Grew our sustainable finance TCE by $9.6 billiona .. • Continued roll-out of our Westpac Sustainable Farm Loan in New Zealand, which includes a requirements for customers to develop an emissions reduction plan. See pages 34-35, 39. Engagement and advocacy Customers • Assessed the climate transition plans of over 150 institutional customers in emissions-intensive sectors. • Bankers and sector specialists have further expanded their customer engagement with detailed conversations on topics including the net-zero transition in Agriculture and Commercial Real Estate sectors. See pages 32-33. Government and Industry bodies • Engaged with government departments, research corporations and industry bodies, on the agriculture industry, including collaboration opportunities and new technologies. • Engaged with government and industry bodies and working groups in the residential housing and commercial real estate sectors. • Engaged with the NZBA capital markets working group that is developing materials to help banks develop targets for capital markets activities. See page 42. Capability, process, and governance Banker capability • Provided additional training to support some of our bankers to have conversations on net-zero and ESG risk related matters. See page 32. Enhancing data and models • Improved the capture and storage of data along with the models used to monitor and manage our targets. • Included model reviews, codifying processes and methodologies. – Improvement of process and governance • Further integration of sector positions and NZBA alignment considerations into ESG risk assessment processes. • Enhanced escalation framework for transactions that may impact our NZBA sector targets. This ensures we are actively managing the pathway to our targets. • Reduced risks by developing target setting and review process guides and model monitoring frameworks. These guides/frameworks aim to standardise the processes for setting and reviewing our targets. See pages 44, 50. a. Total committed exposure for lending assessed as sustainable finance in accordance with Westpac 2024 Sustainable Finance Framework – movement in balance over the year. WESTPAC GROUP 2024 CLIMATE REPORT |

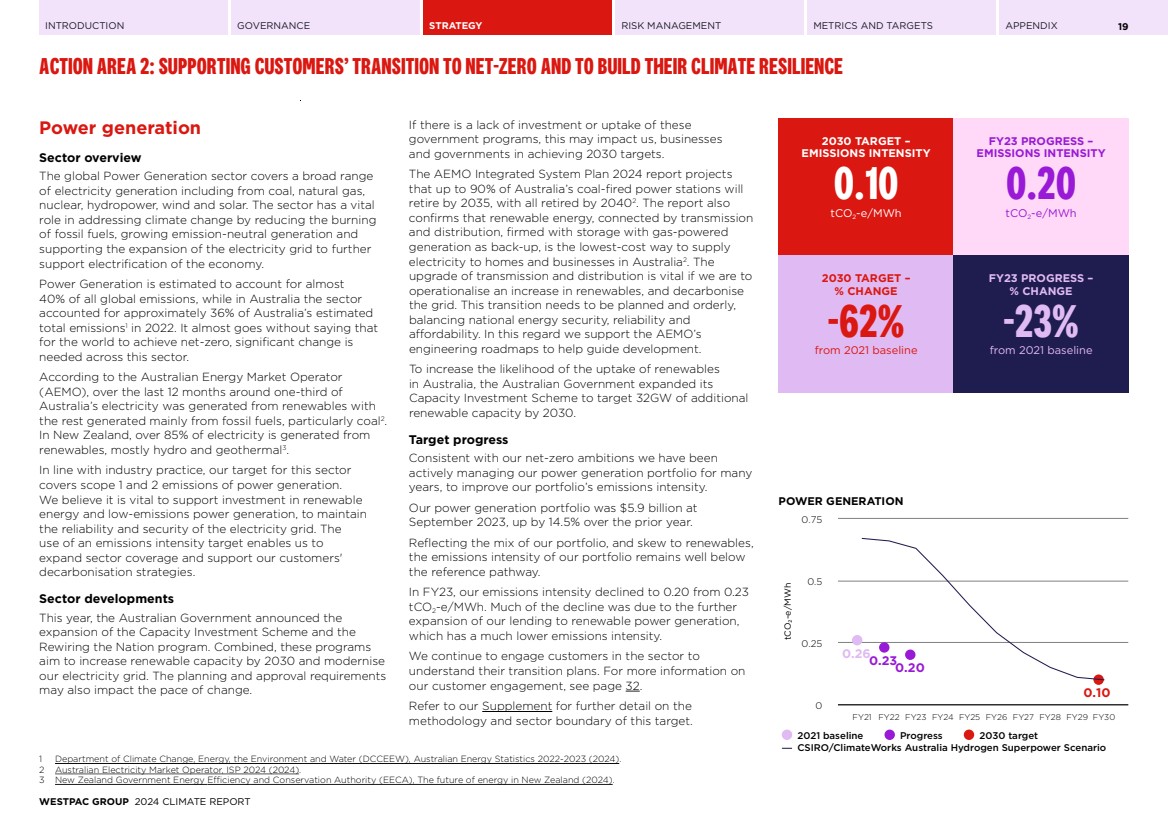

| INTRODUCTION GOVERNANCE STRATEGY RISK MANAGEMENT METRICS AND TARGETS APPENDIX ACTION AREA 2: SUPPORTING CUSTOMERS’ TRANSITION TO NET-ZERO AND TO BUILD THEIR CLIMATE RESILIENCE 19 Power generation Sector overview The global Power Generation sector covers a broad range of electricity generation including from coal, natural gas, nuclear, hydropower, wind and solar. The sector has a vital role in addressing climate change by reducing the burning of fossil fuels, growing emission-neutral generation and supporting the expansion of the electricity grid to further support electrification of the economy. Power Generation is estimated to account for almost 40% of all global emissions, while in Australia the sector accounted for approximately 36% of Australia’s estimated total emissions1 in 2022. It almost goes without saying that for the world to achieve net-zero, significant change is needed across this sector. According to the Australian Energy Market Operator (AEMO), over the last 12 months around one-third of Australia’s electricity was generated from renewables with the rest generated mainly from fossil fuels, particularly coal2 .. In New Zealand, over 85% of electricity is generated from renewables, mostly hydro and geothermal3 .. In line with industry practice, our target for this sector covers scope 1 and 2 emissions of power generation. We believe it is vital to support investment in renewable energy and low-emissions power generation, to maintain the reliability and security of the electricity grid. The use of an emissions intensity target enables us to expand sector coverage and support our customers' decarbonisation strategies. Sector developments This year, the Australian Government announced the expansion of the Capacity Investment Scheme and the Rewiring the Nation program. Combined, these programs aim to increase renewable capacity by 2030 and modernise our electricity grid. The planning and approval requirements may also impact the pace of change. If there is a lack of investment or uptake of these government programs, this may impact us, businesses and governments in achieving 2030 targets. The AEMO Integrated System Plan 2024 report projects that up to 90% of Australia’s coal-fired power stations will retire by 2035, with all retired by 20402 .. The report also confirms that renewable energy, connected by transmission and distribution, firmed with storage with gas-powered generation as back-up, is the lowest-cost way to supply electricity to homes and businesses in Australia2 .. The upgrade of transmission and distribution is vital if we are to operationalise an increase in renewables, and decarbonise the grid. This transition needs to be planned and orderly, balancing national energy security, reliability and affordability. In this regard we support the AEMO’s engineering roadmaps to help guide development. To increase the likelihood of the uptake of renewables in Australia, the Australian Government expanded its Capacity Investment Scheme to target 32GW of additional renewable capacity by 2030. Target progress Consistent with our net-zero ambitions we have been actively managing our power generation portfolio for many years, to improve our portfolio’s emissions intensity. Our power generation portfolio was $5.9 billion at September 2023, up by 14.5% over the prior year. Reflecting the mix of our portfolio, and skew to renewables, the emissions intensity of our portfolio remains well below the reference pathway. In FY23, our emissions intensity declined to 0.20 from 0.23 tCO2-e/MWh. Much of the decline was due to the further expansion of our lending to renewable power generation, which has a much lower emissions intensity. We continue to engage customers in the sector to understand their transition plans. For more information on our customer engagement, see page 32. Refer to our Supplement for further detail on the methodology and sector boundary of this target. 1 Department of Climate Change, Energy, the Environment and Water (DCCEEW), Australian Energy Statistics 2022-2023 (2024). 2 Australian Electricity Market Operator, ISP 2024 (2024). 3 New Zealand Government Energy Efficiency and Conservation Authority (EECA), The future of energy in New Zealand (2024). 2030 TARGET – EMISSIONS INTENSITY 0.10 tCO2-e/MWh FY23 PROGRESS – EMISSIONS INTENSITY 0.20 tCO2-e/MWh 2030 TARGET – % CHANGE -62% from 2021 baseline FY23 PROGRESS – % CHANGE -23% from 2021 baseline POWER GENERATION tCO₂-e/MWh 0.260.230.20 0.10 2021 baseline Progress 2030 target CSIRO/ClimateWorks Australia Hydrogen Superpower Scenario FY21 FY22 FY23 FY24 FY25 FY26 FY27 FY28 FY29 FY30 0 0.25 0.5 0.75 WESTPAC GROUP 2024 CLIMATE REPORT |

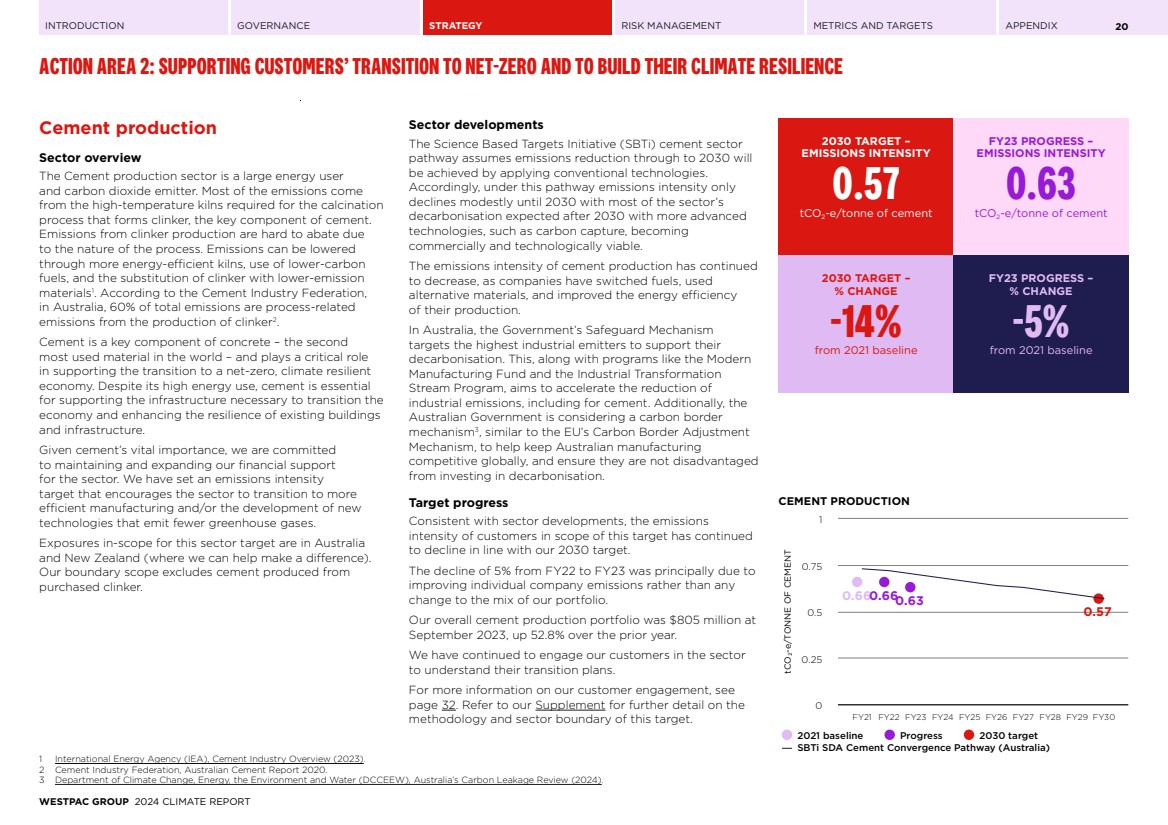

| INTRODUCTION GOVERNANCE STRATEGY RISK MANAGEMENT METRICS AND TARGETS APPENDIX ACTION AREA 2: SUPPORTING CUSTOMERS’ TRANSITION TO NET-ZERO AND TO BUILD THEIR CLIMATE RESILIENCE 20 Cement production Sector overview The Cement production sector is a large energy user and carbon dioxide emitter. Most of the emissions come from the high-temperature kilns required for the calcination process that forms clinker, the key component of cement. Emissions from clinker production are hard to abate due to the nature of the process. Emissions can be lowered through more energy-efficient kilns, use of lower-carbon fuels, and the substitution of clinker with lower-emission materials1 .. According to the Cement Industry Federation, in Australia, 60% of total emissions are process-related emissions from the production of clinker2 .. Cement is a key component of concrete – the second most used material in the world – and plays a critical role in supporting the transition to a net-zero, climate resilient economy. Despite its high energy use, cement is essential for supporting the infrastructure necessary to transition the economy and enhancing the resilience of existing buildings and infrastructure. Given cement’s vital importance, we are committed to maintaining and expanding our financial support for the sector. We have set an emissions intensity target that encourages the sector to transition to more efficient manufacturing and/or the development of new technologies that emit fewer greenhouse gases. Exposures in-scope for this sector target are in Australia and New Zealand (where we can help make a difference). Our boundary scope excludes cement produced from purchased clinker. Sector developments The Science Based Targets Initiative (SBTi) cement sector pathway assumes emissions reduction through to 2030 will be achieved by applying conventional technologies. Accordingly, under this pathway emissions intensity only declines modestly until 2030 with most of the sector’s decarbonisation expected after 2030 with more advanced technologies, such as carbon capture, becoming commercially and technologically viable. The emissions intensity of cement production has continued to decrease, as companies have switched fuels, used alternative materials, and improved the energy efficiency of their production. In Australia, the Government’s Safeguard Mechanism targets the highest industrial emitters to support their decarbonisation. This, along with programs like the Modern Manufacturing Fund and the Industrial Transformation Stream Program, aims to accelerate the reduction of industrial emissions, including for cement. Additionally, the Australian Government is considering a carbon border mechanism3 , similar to the EU’s Carbon Border Adjustment Mechanism, to help keep Australian manufacturing competitive globally, and ensure they are not disadvantaged from investing in decarbonisation. Target progress Consistent with sector developments, the emissions intensity of customers in scope of this target has continued to decline in line with our 2030 target. The decline of 5% from FY22 to FY23 was principally due to improving individual company emissions rather than any change to the mix of our portfolio. Our overall cement production portfolio was $805 million at September 2023, up 52.8% over the prior year. We have continued to engage our customers in the sector to understand their transition plans. For more information on our customer engagement, see page 32. Refer to our Supplement for further detail on the methodology and sector boundary of this target. 1 International Energy Agency (IEA), Cement Industry Overview (2023). 2 Cement Industry Federation, Australian Cement Report 2020. 3 Department of Climate Change, Energy, the Environment and Water (DCCEEW), Australia’s Carbon Leakage Review (2024). 2030 TARGET – EMISSIONS INTENSITY 0.57 tCO2-e/tonne of cement FY23 PROGRESS – EMISSIONS INTENSITY 0.63 tCO2-e/tonne of cement 2030 TARGET – % CHANGE -14% from 2021 baseline FY23 PROGRESS – % CHANGE -5% from 2021 baseline CEMENT PRODUCTION tCO₂-e/TONNE OF CEMENT 0.660.660.63 0.57 2021 baseline Progress 2030 target SBTi SDA Cement Convergence Pathway (Australia) FY21 FY22 FY23 FY24 FY25 FY26 FY27 FY28 FY29 FY30 0 0.25 0.5 0.75 1 WESTPAC GROUP 2024 CLIMATE REPORT |

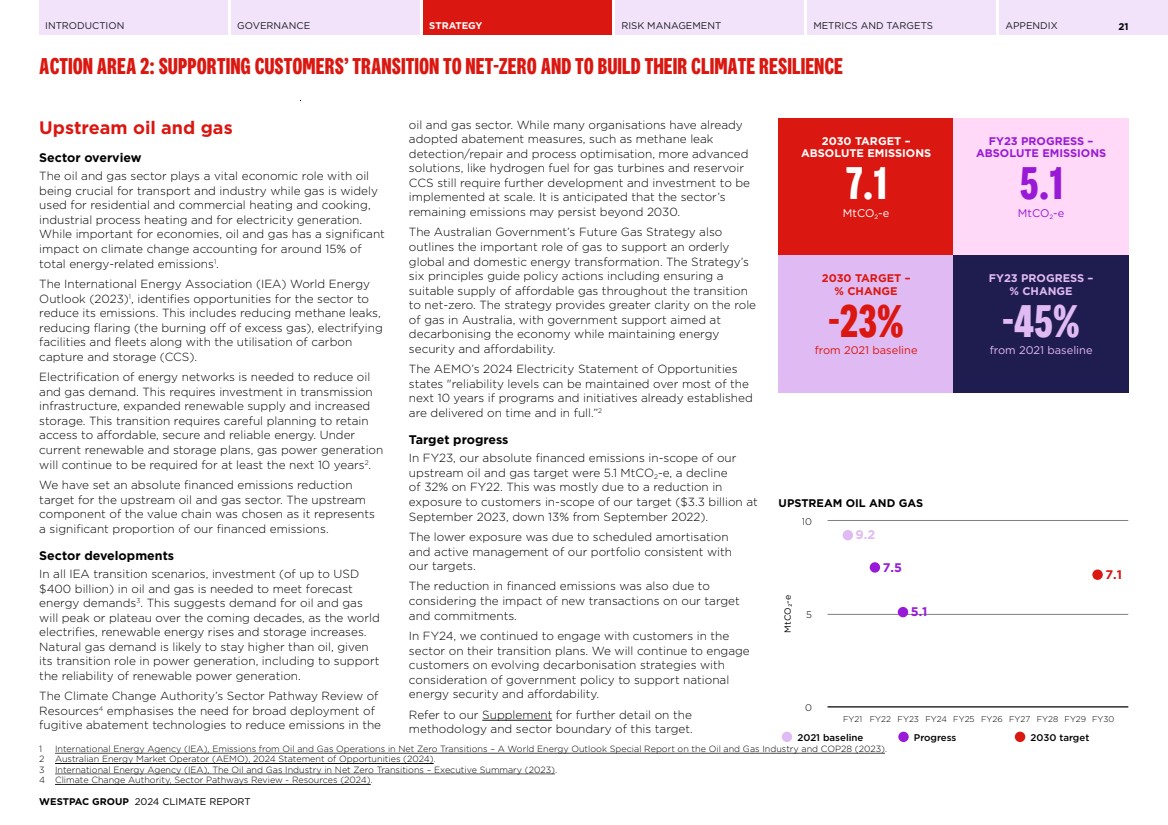

| INTRODUCTION GOVERNANCE STRATEGY RISK MANAGEMENT METRICS AND TARGETS APPENDIX ACTION AREA 2: SUPPORTING CUSTOMERS’ TRANSITION TO NET-ZERO AND TO BUILD THEIR CLIMATE RESILIENCE 21 Upstream oil and gas Sector overview The oil and gas sector plays a vital economic role with oil being crucial for transport and industry while gas is widely used for residential and commercial heating and cooking, industrial process heating and for electricity generation. While important for economies, oil and gas has a significant impact on climate change accounting for around 15% of total energy-related emissions1 .. The International Energy Association (IEA) World Energy Outlook (2023)1 , identifies opportunities for the sector to reduce its emissions. This includes reducing methane leaks, reducing flaring (the burning off of excess gas), electrifying facilities and fleets along with the utilisation of carbon capture and storage (CCS). Electrification of energy networks is needed to reduce oil and gas demand. This requires investment in transmission infrastructure, expanded renewable supply and increased storage. This transition requires careful planning to retain access to affordable, secure and reliable energy. Under current renewable and storage plans, gas power generation will continue to be required for at least the next 10 years2 .. We have set an absolute financed emissions reduction target for the upstream oil and gas sector. The upstream component of the value chain was chosen as it represents a significant proportion of our financed emissions. Sector developments In all IEA transition scenarios, investment (of up to USD $400 billion) in oil and gas is needed to meet forecast energy demands3 .. This suggests demand for oil and gas will peak or plateau over the coming decades, as the world electrifies, renewable energy rises and storage increases. Natural gas demand is likely to stay higher than oil, given its transition role in power generation, including to support the reliability of renewable power generation. The Climate Change Authority’s Sector Pathway Review of Resources4 emphasises the need for broad deployment of fugitive abatement technologies to reduce emissions in the oil and gas sector. While many organisations have already adopted abatement measures, such as methane leak detection/repair and process optimisation, more advanced solutions, like hydrogen fuel for gas turbines and reservoir CCS still require further development and investment to be implemented at scale. It is anticipated that the sector’s remaining emissions may persist beyond 2030. The Australian Government’s Future Gas Strategy also outlines the important role of gas to support an orderly global and domestic energy transformation. The Strategy’s six principles guide policy actions including ensuring a suitable supply of affordable gas throughout the transition to net-zero. The strategy provides greater clarity on the role of gas in Australia, with government support aimed at decarbonising the economy while maintaining energy security and affordability. The AEMO’s 2024 Electricity Statement of Opportunities states "reliability levels can be maintained over most of the next 10 years if programs and initiatives already established are delivered on time and in full.”2 Target progress In FY23, our absolute financed emissions in-scope of our upstream oil and gas target were 5.1 MtCO2-e, a decline of 32% on FY22. This was mostly due to a reduction in exposure to customers in-scope of our target ($3.3 billion at September 2023, down 13% from September 2022). The lower exposure was due to scheduled amortisation and active management of our portfolio consistent with our targets. The reduction in financed emissions was also due to considering the impact of new transactions on our target and commitments. In FY24, we continued to engage with customers in the sector on their transition plans. We will continue to engage customers on evolving decarbonisation strategies with consideration of government policy to support national energy security and affordability. Refer to our Supplement for further detail on the methodology and sector boundary of this target. 1 International Energy Agency (IEA), Emissions from Oil and Gas Operations in Net Zero Transitions – A World Energy Outlook Special Report on the Oil and Gas Industry and COP28 (2023). 2 Australian Energy Market Operator (AEMO), 2024 Statement of Opportunities (2024). 3 International Energy Agency (IEA), The Oil and Gas Industry in Net Zero Transitions – Executive Summary (2023). 4 Climate Change Authority, Sector Pathways Review - Resources (2024). 2030 TARGET – ABSOLUTE EMISSIONS 7.1 MtCO2-e FY23 PROGRESS – ABSOLUTE EMISSIONS 5.1 MtCO2-e 2030 TARGET – % CHANGE -23% from 2021 baseline FY23 PROGRESS – % CHANGE -45% from 2021 baseline UPSTREAM OIL AND GAS MtCO₂-e 9.2 7.5 5.1 7.1 2021 baseline Progress 2030 target FY21 FY22 FY23 FY24 FY25 FY26 FY27 FY28 FY29 FY30 0 5 10 WESTPAC GROUP 2024 CLIMATE REPORT |

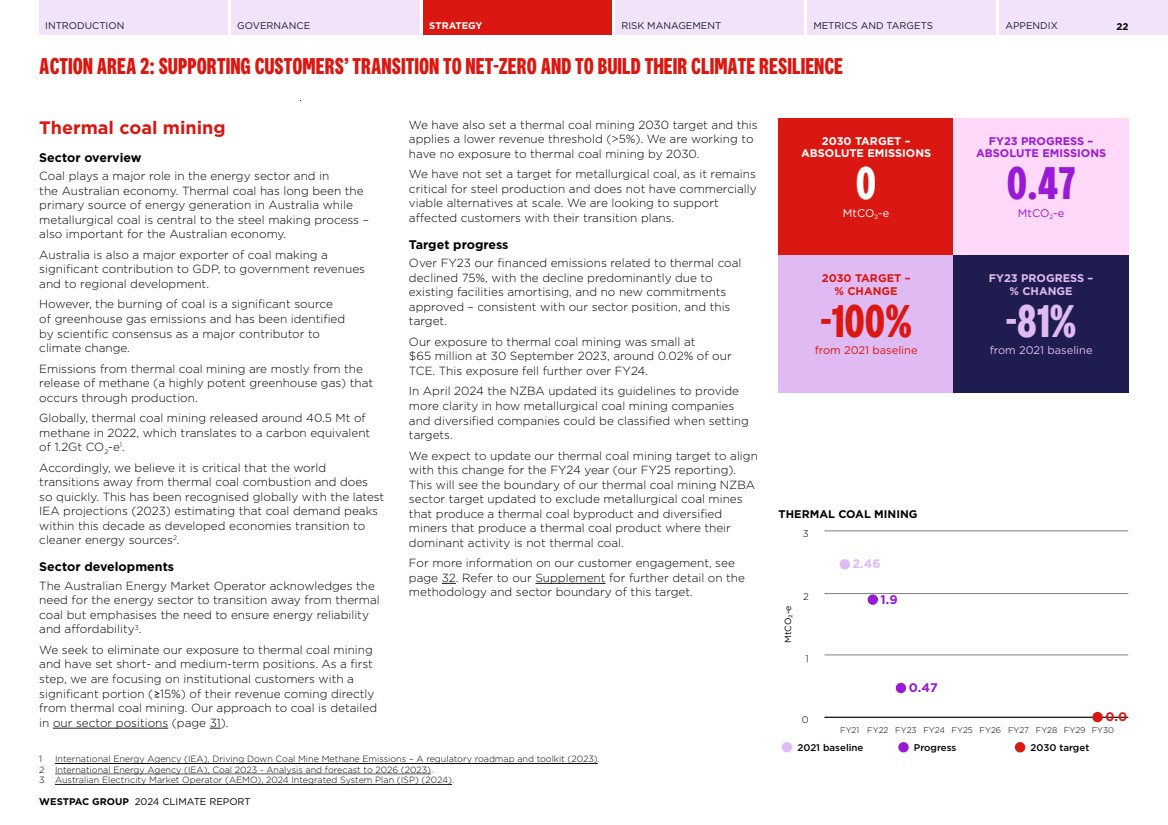

| INTRODUCTION GOVERNANCE STRATEGY RISK MANAGEMENT METRICS AND TARGETS APPENDIX ACTION AREA 2: SUPPORTING CUSTOMERS’ TRANSITION TO NET-ZERO AND TO BUILD THEIR CLIMATE RESILIENCE 22 Thermal coal mining Sector overview Coal plays a major role in the energy sector and in the Australian economy. Thermal coal has long been the primary source of energy generation in Australia while metallurgical coal is central to the steel making process – also important for the Australian economy. Australia is also a major exporter of coal making a significant contribution to GDP, to government revenues and to regional development. However, the burning of coal is a significant source of greenhouse gas emissions and has been identified by scientific consensus as a major contributor to climate change. Emissions from thermal coal mining are mostly from the release of methane (a highly potent greenhouse gas) that occurs through production. Globally, thermal coal mining released around 40.5 Mt of methane in 2022, which translates to a carbon equivalent of 1.2Gt CO2-e1 .. Accordingly, we believe it is critical that the world transitions away from thermal coal combustion and does so quickly. This has been recognised globally with the latest IEA projections (2023) estimating that coal demand peaks within this decade as developed economies transition to cleaner energy sources2 .. Sector developments The Australian Energy Market Operator acknowledges the need for the energy sector to transition away from thermal coal but emphasises the need to ensure energy reliability and affordability3 .. We seek to eliminate our exposure to thermal coal mining and have set short- and medium-term positions. As a first step, we are focusing on institutional customers with a significant portion (≥15%) of their revenue coming directly from thermal coal mining. Our approach to coal is detailed in our sector positions (page 31). We have also set a thermal coal mining 2030 target and this applies a lower revenue threshold (>5%). We are working to have no exposure to thermal coal mining by 2030. We have not set a target for metallurgical coal, as it remains critical for steel production and does not have commercially viable alternatives at scale. We are looking to support affected customers with their transition plans. Target progress Over FY23 our financed emissions related to thermal coal declined 75%, with the decline predominantly due to existing facilities amortising, and no new commitments approved – consistent with our sector position, and this target. Our exposure to thermal coal mining was small at $65 million at 30 September 2023, around 0.02% of our TCE. This exposure fell further over FY24. In April 2024 the NZBA updated its guidelines to provide more clarity in how metallurgical coal mining companies and diversified companies could be classified when setting targets. We expect to update our thermal coal mining target to align with this change for the FY24 year (our FY25 reporting). This will see the boundary of our thermal coal mining NZBA sector target updated to exclude metallurgical coal mines that produce a thermal coal byproduct and diversified miners that produce a thermal coal product where their dominant activity is not thermal coal. For more information on our customer engagement, see page 32. Refer to our Supplement for further detail on the methodology and sector boundary of this target. 1 International Energy Agency (IEA), Driving Down Coal Mine Methane Emissions – A regulatory roadmap and toolkit (2023). 2 International Energy Agency (IEA), Coal 2023 - Analysis and forecast to 2026 (2023). 3 Australian Electricity Market Operator (AEMO), 2024 Integrated System Plan (ISP) (2024). 2030 TARGET – ABSOLUTE EMISSIONS 0 MtCO2-e FY23 PROGRESS – ABSOLUTE EMISSIONS 0.47 MtCO2-e 2030 TARGET – % CHANGE -100% from 2021 baseline FY23 PROGRESS – % CHANGE -81% from 2021 baseline THERMAL COAL MINING MtCO₂-e 2.46 1.9 0.47 0.0 2021 baseline Progress 2030 target FY21 FY22 FY23 FY24 FY25 FY26 FY27 FY28 FY29 FY30 0 1 2 3 WESTPAC GROUP 2024 CLIMATE REPORT |