UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

Certified Shareholder Report of

Registered Management Investment Companies

Investment Company Act File Number: 811-03734

EuroPacific Growth Fund

(Exact Name of Registrant as Specified in Charter)

333 South Hope Street

Los Angeles, California 90071

(Address of Principal Executive Offices)

Registrant's telephone number, including area code: (213) 486-9200

Date of fiscal year end: March 31

Date of reporting period: March 31, 2010

Vincent P. Corti

Capital Research and Management Company

333 South Hope Street

Los Angeles, California 90071

(Name and Address of Agent for Service)

Copies to:

Mark D. Perlow

K&L Gates LLP

Four Embarcadero Center, Suite 1200

San Francisco, California 94111

(Counsel for the Registrant)

ITEM 1 – Reports to Stockholders

|  |

EuroPacific Growth Fund

Lost in translation:

What does currency mean for investors?

[photo of currency in a person's hands]

Annual report for the year ended March 31, 2010

EuroPacific Growth Fund® seeks long-term capital appreciation by investing primarily in the securities of companies based in Europe and the Pacific Basin. More than half of the world’s investment opportunities can be found beyond the borders of our country. As a shareholder in the fund, you have access to what we believe are the best of those opportunities.

This fund is one of the 30 American Funds. American Funds is one of the nation’s largest mutual fund families. For nearly 80 years, Capital Research and Management Company,SM the American Funds adviser, has invested with a long-term focus based on thorough research and attention to risk.

Fund results shown in this report, unless otherwise indicated, are for Class A shares at net asset value. If a sales charge (maximum 5.75%) had been deducted, the results would have been lower. Results are for past periods and are not predictive of results for future periods. Current and future results may be lower or higher than those shown. Share prices and returns will vary, so investors may lose money. Investing for short periods makes losses more likely. Investments are not FDIC-insured, nor are they deposits of or guaranteed by a bank or any other entity, so they may lose value. For current information and month-end results, visit americanfunds.com.

Investment results assume all distributions are reinvested and reflect applicable fees and expenses. The fund’s investment adviser waived a portion of its management fees from September 1, 2004, through December 31, 2008. Fund results shown reflect the waiver, without which they would have been lower. See the Financial Highlights table on pages 27 and 28 for details.

See page 4 for Class A share results with relevant sales charges deducted. Results for other share classes can be found on page 33.

Equity investments are subject to market fluctuations. Investing outside the United States may be subject to risks, such as currency fluctuations, periods of illiquidity and price volatility. These risks may be heightened in connection with investments in developing countries. See the prospectus and the Risk Factors section of this report for more information on these and other risks associated with investing in the fund.

| In this report | |

| Special feature | |

| 6 | Lost in translation: What does currency mean for investors? |

| Currency movements can create both headwinds and tailwinds for U.S. investors, depending on | |

| the company and currency. The fund’s investment professionals discuss their views on foreign exchange and its impact on international investing. | |

| Contents | |

| 1 | Letter to shareholders |

| 4 | The value of a long-term perspective |

| 12 | Summary investment portfolio |

| 17 | Financial statements |

| 34 | Board of trustees and other officers |

Fellow shareholders:

[photo of currency in a person's hands]

EuroPacific Growth Fund’s fiscal year proved to be vastly different than the previous one. The fund reported a total return of 52.2%, with dividends reinvested, for the year ended March 31, 2010. That compares to the previous year’s decline of 40.5%. Although we do not often compare year-over-year changes, we think these results are noteworthy and underscore the dramatic volatility and resiliency of the world markets. The extent and speed of the rebound made it a remarkable period.

The fund’s year began on April 1, 2009, just a few weeks after markets around the world hit their crisis lows. The severe selloff had been global, beginning in the United States with mortgage loan troubles, followed by a sharp credit contraction and economic recessions around the world. By April, however, the tenor of the markets was uncertain but hopeful, as governments aggressively pulled the levers of fiscal and monetary policy to stabilize markets and reduce investor fears. The markets then started a recovery that in hindsight was truly striking. The developing markets, including China and India, surprised many with their rapid growth at a time when most of the developed nations were struggling.

During the year, governments responded swiftly and aggressively by injecting unprecedented cash into their economies to shore up growth and add to stability. The Chinese government launched the largest stimulus plan in its history, pledging US$586 billion to invest in housing, infrastructure, transportation, health care and education; China’s markets rose by 62.6%* in 2009. In addition, three other large developing-country stock markets — Russia, India and Brazil — rose more than 100% during the year. This underscores the increasing importance of these markets on the world stage. In the early stages of economic development, these countries have been generating tremendous demand for basic commodities, which in turn was a power ful boost for resource-rich countries in the developed world such as Australia, Canada and Norway.

*Unless otherwise indicated, country and region returns are based on MSCI indexes and measured in U.S. dollars with gross dividends reinvested.

Our long-term view

After the tumultuous 12 months that ended last March, we entered the new year conservatively in positioning the fund for an expected recovery. Partly because of that conservatism, EuroPacific’s strong 52.2% gain still lagged the 61.7% return of the unmanaged MSCI ACWI (All Country World Index) ex USA, which measures more than 40 country indexes in developed and developing countries. The fund’s return during the fiscal period also was behind the 54.6% return of the Lipper International Funds Average.

[Begin Sidebar]

| Results at a glance | ||||||||||||||||

| For periods ended March 31, 2010, with all distributions reinvested | ||||||||||||||||

| Total returns | Average annual total returns | |||||||||||||||

| 1 year | 5 years | 10 years | Lifetime1 | |||||||||||||

| EuroPacific Growth Fund (Class A shares) | 52.23 | % | 7.91 | % | 3.33 | % | 12.19 | % | ||||||||

MSCI ACWI (All Country World Index) ex USA2,3 | 61.67 | 6.59 | 3.20 | — | ||||||||||||

Lipper International Funds Average4 | 54.63 | 4.16 | 1.87 | 9.68 | ||||||||||||

MSCI EAFE (Europe, Australasia, Far East) Index2 | 55.20 | 4.24 | 1.68 | 9.57 | ||||||||||||

1 Since April 16, 1984. | ||||||||||||||||

2 The index is unmanaged and its return does not reflect the effect of sales charges, commissions or expenses. | ||||||||||||||||

3 The index did not exist prior to December 31, 1987. | ||||||||||||||||

4 Source: Lipper. Lipper averages do not reflect the effect of sales charges. | ||||||||||||||||

[End Sidebar]

[Begin Sidebar]

| Where the fund’s assets are invested | ||||||||||||

| (percent invested by country) | ||||||||||||

EuroPacific Growth Fund invests primarily in the stocks of companies based in Europe and the Pacific Basin.1 | ||||||||||||

| MSCI | ||||||||||||

| All Country | ||||||||||||

| EuroPacific | World Index | |||||||||||

| Growth Fund | ex USA2 | |||||||||||

| (3/31/10) | (3/31/09) | (3/31/10) | ||||||||||

| Europe | ||||||||||||

Euro zone3 | 30.0 | % | 30.0 | % | 22.2 | % | ||||||

| United Kingdom | 10.1 | 8.3 | 14.6 | |||||||||

| Switzerland | 8.0 | 8.3 | 5.5 | |||||||||

| Denmark | 2.0 | 2.4 | .7 | |||||||||

| Russia | 1.9 | 2.1 | 1.5 | |||||||||

| Sweden | 1.6 | 1.2 | 1.9 | |||||||||

| Norway | .8 | .7 | .5 | |||||||||

| Other Europe | .7 | .5 | .9 | |||||||||

| 55.1 | 53.5 | 47.8 | ||||||||||

| Pacific Basin | ||||||||||||

| Japan | 10.1 | 7.8 | 15.5 | |||||||||

| Mexico | 3.5 | 3.2 | 1.0 | |||||||||

| China | 3.5 | 3.0 | 4.0 | |||||||||

| Canada | 3.2 | 2.4 | 7.6 | |||||||||

| South Korea | 2.6 | 1.9 | 2.9 | |||||||||

| Australia | 2.4 | 1.9 | 6.0 | |||||||||

| Taiwan | 2.0 | 2.4 | 2.4 | |||||||||

| Hong Kong | 1.2 | 1.9 | 1.7 | |||||||||

| Indonesia | .6 | .3 | .5 | |||||||||

| Other Pacific Basin | 1.0 | 1.1 | 2.1 | |||||||||

| 30.1 | 25.9 | 43.7 | ||||||||||

| Other | ||||||||||||

| Brazil | 3.1 | 2.7 | 3.7 | |||||||||

| India | 3.0 | 2.8 | 1.7 | |||||||||

| South Africa | 1.6 | 1.2 | 1.6 | |||||||||

| Israel | 1.1 | 1.7 | .7 | |||||||||

| Other countries | .1 | .1 | .8 | |||||||||

| 8.9 | 8.5 | 8.5 | ||||||||||

| Short-term securities & | ||||||||||||

| other assets less liabilities | 5.9 | 12.1 | — | |||||||||

| Total | 100.0 | % | 100.0 | % | 100.0 | % | ||||||

1 A country is considered part of the Pacific Basin if any of its borders touches the Pacific Ocean. | ||||||||||||

2 Weighted by market capitalization. | ||||||||||||

3 Countries using the euro as a common currency: Austria, Belgium, Cyprus, Finland, France, Germany, Greece, Ireland, Italy, Luxembourg, Malta, the Netherlands, Portugal, Slovakia, Slovenia and Spain. | ||||||||||||

[End Sidebar]

However, over longer time periods, EuroPacific Growth Fund has had an advantage over its benchmark and its peers; as shown in the table on page 1, its results have been superior to those indexes on a five-year, 10-year and lifetime basis since it began operations on April 16, 1984. We focus on long-term investing and while we strive to surpass our benchmarks, we also seek to mitigate risks.

How the fund responded

Many of the fund’s holdings faced challenges during 2008–09, but we had conviction in the strength of their underlying businesses. The fund’s second-largest holding is an example: Anheuser-Busch InBev, a global beverage company headquartered in Belgium, had taken on a large amount of debt before the crisis and looked ready to stumble; however, it cleaned up its balance sheet and the stock rose 83.0% in the period. Other examples include metals and mining company Xstrata (+184.6%), global banks Banco Santander (+93.9%) and Barclays (+156.9%), semiconductor maker Samsung (+74.1%), and automakers Honda (+47.7%) and Daimler (+85.8%).

Despite volatility in western European markets — sparked by the general economic downturn and fears over Greek debt — the fund’s European holdings did well. The fund has maintained meaningful investments in Europe, particularly in Germany, Switzerland and France. About 55% of the fund’s net assets were invested there at the end of the fiscal year, roughly the same as a year earlier. In fact, eight out of the top 10 holdings were global companies based in Europe, and most of these stocks fared quite well, including the pharmaceutical makers Bayer (+41.7%), Novartis (+43.8%), Novo Nordisk (+62.3%) and, to a lesser extent, Roche (+18.7%). German business software maker SAP, the seventh-largest holding, gained 36.8%.

On an absolute basis, only 11 of the fund’s holdings — out of more than 260 stocks — fell during the year. These included U.K. building materials firm Wolseley (–26.8%), U.K.-based Lloyds Banking Group (–4.1%) and Hong Kong’s Cheung Kong Infrastructure (–3.3%). Many of the fund’s holdings showed large gains but on a relative basis were not as strong as others. Some energy and utility holdings detracted from results.

The fund’s overall holdings in Japan rose to 10.1% of the fund’s net assets, up from 7.8% a year ago; likewise, U.K. holdings made up a bigger percentage of the fund at 10.1%, up from 8.3% a year prior. Several developing markets that led the rebound in global equity markets continued to make up a large part of the fund, accounting for more than 15% of its assets.

After a steady weakening over the past several years, the U.S. dollar saw periods of strength this fiscal year as investors sought the relative safety of the world reserve currency. This impacted the results of a number of holdings. However, fundamental research and a long-term perspective drives our investment strategy, and we seek to avoid making short-term decisions based on volatile currency fluctuations. For more on how our investment professionals look at currency issues, please see the feature “Lost in translation: What does currency mean for investors?” beginning on page 6.

Looking ahead

While we are pleased that markets have rebounded, the global economy remains fragile, particularly for a number of countries in the developed world. This includes much of Europe, where the common currency, the euro, came under considerable strain during the crisis. And while developing countries’ economies are likely to prove robust on the whole, we caution that some divergence in growth rates is likely to occur as authorities unwind monetary stimulus. So far this year, central banks in India, Malaysia and Vietnam, as well as Australia, have increased their interest rates to resist inflationary pressures caused by high growth. We continue to monitor the countervailing pressures of threats to the euro and inflation in Asia, as well as other issues around the world.

We believe that stock valuations remain attractive, even in cases where share prices have rebounded strongly, because we think the earnings outlook has improved as much or more than the share prices. In addition, many companies have taken steps to strengthen their balance sheets and lower their level of financial risk so they are on more solid footing. It is worth noting that despite the strong gains last year, there are many international markets that are well below their peak levels. The brisk growth in China and India and the rest of the developing world has also opened up new markets and business opportunities. Risks do exist in the global economy, some of which could be significant down the road, and we continue to position the fund to he lp protect against these risks. Nonetheless, we remain confident in our ability to find companies that we think will do well over time, and we see encouraging signs of growth and recovery.

We thank all of EuroPacific’s shareholders for your confidence in us, and we look forward to serving you for many years to come.

Sincerely,

/s/ Gina H. Despres

Gina H. Despres

Vice Chairman of the Board

/s/ Carl Kawaja

Carl Kawaja

President

May 7, 2010

For current information about the fund, visit americanfunds.com.

The value of a long-term perspective

Fund results shown are for Class A shares and reflect deduction of the maximum sales charge of 5.75% on the $10,000 investment.1 Thus, the net amount invested was $9,425.2 Results are for past periods and are not predictive of results for future periods. Current and future results may be lower or higher than those shown. Share prices and returns will vary, so investors may lose money. For current information and month-end results, visit americanfunds.com.

How a $10,000 investment has grown

While notable for their volatility in recent years, financial markets have tended to reward investors over the long term. Active management — bolstered by experience and careful research — can add even more value. As the chart shows, over its lifetime, EuroPacific Growth Fund has done demonstrably better than its relevant benchmark.

| Average annual total returns based on a $1,000 investment | ||||||||||||

| (for periods ended March 31, 2010)* | ||||||||||||

| 1 year | 5 years | 10 years | ||||||||||

| Class A shares | 43.49 | % | 6.64 | % | 2.72 | % | ||||||

| * Assumes reinvestment of all distributions and payment of the maximum 5.75% sales charge. | ||||||||||||

The total annual fund operating expense ratio was 0.85% for Class A shares as of March 31, 2010. This figure does not reflect the fee waiver described below.

Investment results assume all distributions are reinvested and reflect applicable fees and expenses. The fund’s investment adviser waived a portion of its management fees from September 1, 2004, through December 31, 2008. Fund results shown reflect the waiver, without which they would have been lower. See the Financial Highlights table on pages 27 and 28 for details.

[begin mountain chart]

Year ended March 31 | EuroPacific Growth Fund, with dividends reinvested4 | MSCI ACWI ex USA Index, with dividends reinvested5,6 | Consumer Price Index (inflation)7 | |||||||||||||||

| Initial Investment | 04/16/84 | $ | 9,425 | $ | 10,000 | $ | 10,000 | |||||||||||

| 1985 | Low | 07/23/84 | 8,696 | Low | 07/23/84 | 8,155 | Low | 04/30/84 | $ | 10,000 | ||||||||

| Hi | 03/28/85 | 9,955 | Hi | 03/31/85 | 10,348 | Hi | 03/31/85 | 10,320 | ||||||||||

| Close | 03/31/85 | 9,941 | Close | 03/31/85 | 10,348 | Close | 03/31/85 | 10,320 | ||||||||||

| 1986 | Low | 04/08/85 | 9,775 | Low | 04/09/85 | 10,115 | Low | 04/30/85 | 10,369 | |||||||||

| Hi | 03/21/86 | 15,364 | Hi | 03/31/86 | 19,228 | Hi | 01/31/86 | 10,630 | ||||||||||

| Close | 03/31/86 | 15,357 | Close | 03/31/86 | 19,228 | Close | 03/31/86 | 10,553 | ||||||||||

| 1987 | Low | 07/22/86 | 15,634 | Low | 04/07/86 | 18,448 | Low | 04/30/86 | 10,533 | |||||||||

| Hi | 03/27/87 | 19,887 | Hi | 03/27/87 | 31,405 | Hi | 03/31/87 | 10,873 | ||||||||||

| Close | 03/31/87 | 19,813 | Close | 03/31/87 | 31,010 | Close | 03/31/87 | 10,873 | ||||||||||

| 1988 | Hi | 10/08/87 | 24,499 | Hi | 10/14/87 | 36,201 | Low | 04/30/87 | 10,931 | |||||||||

| Low | 12/11/87 | 17,992 | Low | 11/11/87 | 28,389 | Hi | 03/31/88 | 11,300 | ||||||||||

| Close | 03/31/88 | 21,422 | Close | 03/31/88 | 36,179 | Close | 03/31/88 | 11,300 | ||||||||||

| 1989 | Low | 09/01/88 | 21,189 | Low | 08/31/88 | 33,481 | Low | 04/30/88 | 11,358 | |||||||||

| Hi | 02/09/89 | 24,835 | Hi | 02/28/89 | 41,150 | Hi | 03/31/89 | 11,862 | ||||||||||

| Close | 03/31/89 | 24,569 | Close | 03/31/89 | 40,446 | Close | 03/31/89 | 11,862 | ||||||||||

| 1990 | Low | 06/13/89 | 24,282 | Hi | 12/31/89 | 45,003 | Low | 04/30/89 | 11,940 | |||||||||

| Hi | 12/06/89 | 28,391 | Low | 03/31/90 | 36,338 | Hi | 03/31/90 | 12,483 | ||||||||||

| Close | 03/31/90 | 28,742 | Close | 03/31/90 | 36,338 | Close | 03/31/90 | 12,483 | ||||||||||

| 1991 | Hi | 07/18/90 | 33,103 | Hi | 07/31/90 | 40,323 | Low | 04/30/90 | 12,502 | |||||||||

| Low | 01/16/91 | 27,795 | Low | 09/30/90 | 31,618 | Hi | 03/31/91 | 13,094 | ||||||||||

| Close | 03/31/91 | 31,359 | Close | 03/31/91 | 37,523 | Close | 03/31/91 | 13,094 | ||||||||||

| 1992 | Low | 08/19/91 | 30,061 | Hi | 12/31/91 | 39,623 | Low | 04/30/91 | 13,113 | |||||||||

| Hi | 02/28/92 | 36,033 | Low | 03/31/92 | 35,581 | Hi | 03/31/92 | 13,511 | ||||||||||

| Close | 03/31/92 | 35,033 | Close | 03/31/92 | 35,581 | Close | 03/31/92 | 13,511 | ||||||||||

| 1993 | Hi | 06/02/92 | 37,465 | Low | 10/31/92 | 34,792 | Low | 04/30/92 | 13,531 | |||||||||

| Low | 11/17/92 | 33,764 | Hi | 03/31/93 | 39,345 | Hi | 03/31/93 | 13,928 | ||||||||||

| Close | 03/31/93 | 37,728 | Close | 03/31/93 | 39,345 | Close | 03/31/93 | 13,928 | ||||||||||

| 1994 | Low | 04/02/93 | 37,813 | Low | 04/30/93 | 42,820 | Low | 04/30/93 | 13,967 | |||||||||

| Hi | 02/02/94 | 50,611 | Hi | 01/31/94 | 51,503 | Hi | 03/31/94 | 14,277 | ||||||||||

| Close | 03/31/94 | 47,638 | Close | 03/31/94 | 48,772 | Close | 03/31/94 | 14,277 | ||||||||||

| 1995 | Hi | 09/02/94 | 51,011 | Hi | 10/31/94 | 53,443 | Low | 04/30/94 | 14,297 | |||||||||

| Low | 01/31/95 | 46,642 | Low | 02/16/95 | 48,179 | Hi | 03/31/95 | 14,685 | ||||||||||

| Close | 03/31/95 | 47,974 | Close | 03/31/95 | 50,901 | Close | 03/31/95 | 14,685 | ||||||||||

| 1996 | Low | 04/03/95 | 47,928 | Low | 06/30/95 | 51,925 | Low | 04/30/95 | 14,733 | |||||||||

| Hi | 03/25/96 | 57,612 | Hi | 03/31/96 | 57,610 | Hi | 03/31/96 | 15,102 | ||||||||||

| Close | 03/31/96 | 57,494 | Close | 03/31/96 | 57,610 | Close | 03/31/96 | 15,102 | ||||||||||

| 1997 | Low | 07/24/96 | 57,229 | Low | 07/31/96 | 56,809 | Low | 04/30/96 | 15,160 | |||||||||

| Hi | 03/11/97 | 67,625 | Hi | 11/30/96 | 60,212 | Hi | 03/31/97 | 15,519 | ||||||||||

| Close | 03/31/97 | 66,627 | Close | 03/31/97 | 59,368 | Close | 03/31/97 | 15,519 | ||||||||||

| 1998 | Hi | 10/03/97 | 77,523 | Low | 04/30/97 | 59,868 | Low | 05/31/97 | 15,529 | |||||||||

| Low | 01/12/98 | 67,131 | Hi | 03/31/98 | 69,026 | Hi | 03/31/98 | 15,732 | ||||||||||

| Close | 03/31/98 | 80,601 | Close | 03/31/98 | 69,026 | Close | 03/31/98 | 15,732 | ||||||||||

| 1999 | Hi | 04/15/98 | 83,900 | Low | 09/30/98 | 57,722 | Low | 04/30/98 | 15,761 | |||||||||

| Low | 10/05/98 | 65,404 | Hi | 03/31/99 | 71,159 | Hi | 03/31/99 | 16,004 | ||||||||||

| Close | 03/31/99 | 87,198 | Close | 03/31/99 | 71,159 | Close | 03/31/99 | 16,004 | ||||||||||

| 2000 | Low | 04/01/99 | 87,833 | Low | 05/31/99 | 71,208 | Low | 06/30/99 | 16,120 | |||||||||

| Hi | 03/29/00 | 137,516 | Hi | 03/31/00 | 91,706 | Hi | 03/31/00 | 16,605 | ||||||||||

| Close | 03/31/00 | 134,560 | Close | 03/31/00 | 91,706 | Close | 03/31/00 | 16,605 | ||||||||||

| 2001 | Hi | 04/10/00 | 134,710 | Hi | 06/30/00 | 87,965 | Low | 04/30/00 | 16,615 | |||||||||

| Low | 03/22/01 | 94,189 | Low | 03/22/01 | 64,313 | Hi | 03/31/01 | 17,090 | ||||||||||

| Close | 03/31/01 | 96,853 | Close | 03/31/01 | 67,112 | Close | 03/31/01 | 17,090 | ||||||||||

| 2002 | Hi | 05/21/01 | 104,778 | Hi | 05/02/01 | 72,556 | Low | 12/31/01 | 17,139 | |||||||||

| Low | 09/21/01 | 79,958 | Low | 09/21/01 | 52,947 | Hi | 03/31/02 | 17,342 | ||||||||||

| Close | 03/31/02 | 94,302 | Close | 03/31/02 | 63,225.6 | Close | 03/31/02 | 17,342 | ||||||||||

| 2003 | Hi | 05/17/02 | 96,306 | Hi | 05/17/02 | 65,397 | Low | 04/30/02 | 17,439 | |||||||||

| Low | 03/12/03 | 69,809 | Low | 03/12/03 | 46,776 | Hi | 03/31/03 | 17,866 | ||||||||||

| Close | 03/31/03 | 72,463 | Close | 03/31/03 | 49,204 | Close | 03/31/03 | 17,866 | ||||||||||

| 2004 | Low | 04/01/03 | 73,091 | Low | 04/01/03 | 49,620 | Low | 05/31/03 | 17,798 | |||||||||

| High | 03/01/04 | 114,695 | High | 02/17/04 | 79,825 | Hi | 03/31/04 | 18,177 | ||||||||||

| Close | 03/31/04 | 113,848 | Close | 03/31/04 | 78,684 | Close | 03/31/04 | 18,177 | ||||||||||

| 2005 | Low | 05/17/04 | 103,225 | Low | 05/17/04 | 71,764 | Low | 04/30/04 | 18,235 | |||||||||

| High | 03/04/05 | 132,976 | High | 03/08/05 | 95,174 | Hi | 03/31/05 | 18,749 | ||||||||||

| Close | 03/31/05 | 127,604 | Close | 03/31/05 | 91,389 | Close | 03/31/05 | 18,749 | ||||||||||

| 2006 | Low | 04/28/05 | 123,628 | Low | 05/17/05 | 88,203 | Low | 05/31/05 | 18,855 | |||||||||

| High | 03/30/06 | 166,244 | High | 03/30/06 | 117,805 | Hi | 03/31/06 | 19,379 | ||||||||||

| Close | 03/31/06 | 166,207 | Close | 03/31/06 | 117,092 | Close | 03/31/06 | 19,379 | ||||||||||

| 2007 | Low | 06/13/06 | 150,639 | Low | 06/13/06 | 107,730 | Low | 04/30/06 | 19,544 | |||||||||

| High | 12/20/06 | 186,512 | High | 02/26/07 | 142,457 | Hi | 03/31/07 | 19,918 | ||||||||||

| Close | 03/31/07 | 193,850 | Close | 03/31/07 | 140,848 | Close | 03/31/07 | 19,918 | ||||||||||

| 2008 | High | 10/31/07 | 234,626 | High | 10/31/2007 | 168,788 | Low | 04/30/07 | 20,047 | |||||||||

| Low | 03/19/08 | 197,139 | Low | 1/23/2008 | 135,249 | Hi | 03/31/08 | 20,711 | ||||||||||

| Close | 03/31/08 | 206,256 | Close | 3/31/2008 | 144,476 | Close | 03/31/08 | 20,711 | ||||||||||

| 2009 | High | 05/19/08 | 222,332 | High | 05/19/08 | 160,099 | Hi | 07/31/08 | 21,335 | |||||||||

| Low | 03/09/09 | 107,894 | Low | 03/09/09 | 66,530 | Low | 12/31/08 | 20,391 | ||||||||||

| Close | 03/31/09 | 122,641 | Close | 03/31/09 | 77,762 | Close | 03/31/09 | 20,631 | ||||||||||

| 2010 | Low | 04/01/09 | 124,925 | Low | 04/01/09 | 78,971 | Low | 04/30/09 | 20,683 | |||||||||

| High | 11/16/09 | 188,719 | High | 01/11/10 | 128,321 | Hi | 03/31/10 | 21,109 | ||||||||||

| Close | 03/31/10 | 186,699 | Close | 03/31/10 | 125,715 | Close | 03/31/10 | 21,109 | ||||||||||

[end mountain chart]

| Year ended March 31 | 1985 | 3 | 1986 | 1987 | 1988 | 1989 | 1990 | 1991 | 1992 | |||||||||||||||||||||||

| TOTAL VALUE | ||||||||||||||||||||||||||||||||

| Dividends reinvested | $ | 69 | 35 | 118 | 491 | 316 | 527 | 656 | 611 | |||||||||||||||||||||||

| Value at year-end | $ | 9,941 | 15,357 | 19,813 | 21,422 | 24,569 | 28,742 | 31,359 | 35,033 | |||||||||||||||||||||||

| Total return | (0.6 | )% | 54.5 | 29.0 | 8.1 | 14.7 | 17.0 | 9.1 | 11.7 | |||||||||||||||||||||||

| Year ended March 31 | 1993 | 1994 | 1995 | 1996 | 1997 | 1998 | 1999 | 2000 | ||||||||||||||||||||||||

| TOTAL VALUE | ||||||||||||||||||||||||||||||||

| Dividends reinvested | 538 | 515 | 715 | 1,131 | 1,062 | 1,155 | 991 | 841 | ||||||||||||||||||||||||

| Value at year-end | 37,728 | 47,638 | 47,974 | 57,494 | 66,627 | 80,601 | 87,198 | 134,560 | ||||||||||||||||||||||||

| Total return | 7.7 | 26.3 | 0.7 | 19.8 | 15.9 | 21.0 | 8.2 | 54.3 | ||||||||||||||||||||||||

| Year ended March 31 | 2001 | 2002 | 2003 | 2004 | 2005 | 2006 | 2007 | 2008 | ||||||||||||||||||||||||

| TOTAL VALUE | ||||||||||||||||||||||||||||||||

| Dividends reinvested | 637 | 2,209 | 836 | 1,083 | 1,796 | 2,575 | 2,899 | 4,070 | ||||||||||||||||||||||||

| Value at year-end | 96,853 | 94,302 | 72,463 | 113,848 | 127,604 | 166,207 | 193,850 | 206,256 | ||||||||||||||||||||||||

| Total return | (28.0 | ) | (2.6 | ) | (23.2 | ) | 57.1 | 12.1 | 30.3 | 16.6 | 6.4 | |||||||||||||||||||||

| Year ended March 31 | 2009 | 2010 | Average | |||||||||||||||||||||||||||||

| TOTAL VALUE | annual total | |||||||||||||||||||||||||||||||

| Dividends reinvested | 3,422 | 2,959 | return for | |||||||||||||||||||||||||||||

| Value at year-end | 122,641 | 186,699 | fund’s lifetime: | |||||||||||||||||||||||||||||

| Total return | (40.5 | ) | 52.2 | 11.9 | %4 | |||||||||||||||||||||||||||

The results shown are before taxes on fund distributions and sale of fund shares.

1As outlined in the prospectus, the sales charge is reduced for accounts (and aggregated investments) of $25,000 or more and is eliminated for purchases of $1 million or more. There is no sales charge on dividends or capital gain distributions that are reinvested in additional shares. |

2The maximum initial sales charge was 8.5% prior to July 1, 1988. |

3For the period April 16, 1984 (commencement of operations), through March 31, 1985. |

4Includes reinvested dividends of $32,256 and reinvested capital gain distributions of $70,634. |

5The market indexes are unmanaged and their results include reinvested dividends and/or distributions, but do not reflect the effect of sales charges, commissions, expenses or taxes. |

6From April 16, 1984, through December 31, 1987, the MSCI EAFE Index was used because the MSCI ACWI ex USA Index did not yet exist. Since January 1, 1988, the MSCI ACWI ex USA Index has been used. |

7Computed from data supplied by the U.S. Department of Labor, Bureau of Labor Statistics. |

Lost in translation:

What does currency mean for investors?

[photo of a fruit and vegetable stand - signs posted with prices]

[photo of people buying and selling at a farmer's market]

[photo of shelves of candy]

[Begin Sidebar]

EuroPacific Growth Fund’s investment professionals keep a close watch on the complex factors involved in currency fluctuations. Here, they discuss some of their views on foreign exchange and its impact on international investing.

[End Sidebar]

On any given day, headlines call out the effects of the currency market’s volatility: “Dollar Retreats as Risk Appetite Returns,” “Euro Gains but Rally Fizzles,” “Dollar Revival Gains Pace,” and “Currency Markets Foxed by Greece” are a few recent Wall Street Journal headlines. These highlight the erratic and short-term nature of foreign exchange fluctuations, as well as the unpredictability.

So what does currency exchange mean for investments in EuroPacific Growth Fund? Currency movements can create both headwinds and tailwinds for U.S. investors, depending on the company and currency. Foreign exchange has always been a factor in international investing; however, in this interconnected world, currency issues now matter slightly less than they did in the past. The reason is that many multinational companies have operations and sales in many parts of the world, decreasing the potential for severe repercussions from foreign exchange volatility.

Looking for major trends

The fund’s investment professionals carefully monitor the macroeconomic and political issues that influence currency prices, but there’s no formula that can predict foreign exchange fluctuations. “Currencies are difficult to predict, but one of the things that we try to anticipate is major trend changes in currency movements,” says Philip Chitty, a London-based macroeconomist for the fund. “Currency plays an important role in determining economic growth and corporate profitability, so we always want to understand the currency aspects of investing.”

[Begin Pull Quote]

“Currency plays an important role in determining economic growth and corporate profitability, so we always want to understand the currency aspects of investing.”

Philip Chitty

Macroeconomist

[End Pull Quote]

Investment professionals for EuroPacific Growth Fund think deeply about these issues and realize the complexity of the factors involved in currency prices. These include trade deficits, interest rate differentials, fiscal policy, money supply and purchasing power parity, among other issues.

“In some instances, currency has provided a substantial tailwind to our investments in certain countries and, on the other side, a headwind in others,” says portfolio counselor Mark Denning, based in London, pointing to the resource-rich countries of Brazil, Canada and Australia and their relative strength against the U.S. dollar in the last few years. “And in some cases, currency has held back the returns of some companies, as we saw in South Korea and certainly the euro zone in 2008,” he adds.

Currency can also have an effect on the timing of a stock purchase when an investment analyst likes the fundamentals of a company. “We try to understand the currency as it relates to the historic cycle over time,” says Matt Wolf, an investment analyst based in Hong Kong. “I might wait to buy a stock that I found compelling if it didn’t look like a good time for foreign exchange or I could be aggressive if it appeared to be a favorable time. But foreign exchange wouldn’t change the nature of my fundamental investment thesis.”

Multinational smoothing effect

In the end, foreign exchange is just one of the many considerations that EuroPacific Growth Fund’s investment professionals think about when making investments.

“Even though sometimes I feel strongly about the direction of some of the various currencies, I have to temper that with the understanding that over the broad sweep of time, few people are consistently accurate about currency movements,” says Carl Kawaja, president of the fund and a portfolio counselor based in San Francisco. “We look at the fundamentals of the company first, and overlay that thesis with our expectations for currency, not the other way around.”

[Begin Sidebar]

The U.S. dollar as the world reserve currency

A short history

How did the U.S. dollar become the world’s reserve currency? The British pound sterling played this role in the 18th and 19th centuries. At the end of World War II, government leaders met at New Hampshire’s Bretton Woods and established the basic rules and regulations that govern international exchange today, including the International Monetary Fund. The Bretton Woods Accord fixed currencies to the U.S. dollar instead of gold; the dollar in turn was pegged to gold at $35 per ounce. The gold peg was maintained until 1971, when the U.S. dollar could no longer hold the value of the pegged rate. From then on, there has been a floating exchange rate system. Several attempts to move back to a global gold peg were unsuccessful.

Dollar under pressure

Recently, many have questioned whether the U.S. dollar can continue as the world reserve currency. China, in particular, has complained about the dollar’s limitations. However, it’s necessary to remember the aspects of a reserve currency: a store of value and a medium of exchange, in a country where the rule of law is strong and there is no risk of confiscation. And because the dollar is the denominator for almost all commodities, there is a bias for countries to hold significant reserves in dollars. “There is not yet any single currency, country or region that could reasonably replace the prominent role of the U.S. dollar as the world’s reserve currency,” says Tomonori Tani, an investment analyst for the fund bas ed in Tokyo. He says that if the U.S. current account deficit were to remain high for a prolonged time, the dollar’s status could be hurt. “At some point, we might need a comprehensive new world currency regime: A multi-polar currency block would be the most likely outcome.” Mark Brett, a London-based global currency analyst for the fund, points out that while the U.S. has fiscal problems, so do many other countries. “Central banks today are free to diversify away from the dollar, and while that is to be expected, history shows that these movements happen at a glacial pace,” he says. “Despite all the hype about the end of the dollar standard, the facts do not support the story.”

[End Sidebar]

Anheuser-Busch InBev, based in Belgium, is an example of how currency matters less for profitability in an increasingly interconnected global economy. It makes its beverage products in Europe, the U.S. and Brazil, and it sells its products in those countries and around the world, earning revenues in many currencies and often paying for its costs in those same various currencies. This tends to create an internal economy in which the home currency doesn’t need to be repatriated immediately and takes away some of the uncertainty of whether the company will be forced to lose or gain on the translation. So the price of beer in Belgium doesn’t necessarily impact the price of beer in Brazil.

“Fundamentally, if we invest in good companies with good management teams that handle their businesses well, over time the currency issues become far less important,” says investment analyst Julian Abdey, based in San Francisco. “In some years the currencies go against them and in some years they go in their favor, but we think company fundamentals over a long period of time will shine through the currency fluctuations.”

Matt echoes this sentiment, saying that the potential for strong gains or losses based on currency are often smoothed through international operations. He studies these issues carefully but says that they become less significant over the long term. “Most of the time, it doesn’t matter very much because of my three- to five-year investment horizon,” he says. For example, Softbank, a Japanese telecommunications company, has considerable investments in China. To the extent that the Chinese currency becomes stronger and the yen weakens, the value of those Chinese investments would increase. The more important questions, though, involve a company’s competitive position, product offerings and prospects for earnings growth. &# 8220;All of those questions don’t factor much into currencies.”

When London-based investment analyst Bruno Rodrigues looks at metals and mining companies, he analyzes them from a U.S. dollar perspective — regardless of the companies’ domestic currencies. That makes sense, because the dollar is used internationally for commodity prices and it is the financial reporting standard for most of the companies in the industry. However, understanding currency movements is important for a third and less obvious reason: “For companies operating in large commodity-producing countries, the local currency tends to provide some offset to commodity price movements. That’s because high commodity prices often translate into both higher exports and foreign investment inflows, which pressures the local currency to appreciate and vice-versa,” he says. “So when commodity prices rise, operating costs measured in U.S. dollars tend to also rise due to local currency appreciation.” That is the case, for example, when researching global natural resources producer BHP Billiton, which has more than 70% of its assets in countries that have currencies historically correlated to commodity prices: Australia, Chile and South Africa.

[photo of a currency exchange counter]

[photo of paper and coin currency in a dish]

[Begin Pull Quote]

“Fundamentally, if we invest in good companies with good management teams that handle their businesses well, over time the currency issues become far less important.”

Julian Abdey

Investment analyst

[End Pull Quote]

Strong currency, weak currency

Whether a currency is weak or strong does not necessarily guide the prospects of a particular company in that country. There are companies that get a boost when their home currency is strong and others that do better when it’s weak. A stronger currency can make exports more expensive for international customers and make imports cheaper within that country. Domestic industries that produce goods for export or have to compete with imports from other countries will face more difficult times when the domestic currency is strong, and better times when it is relatively weaker.

A weaker U.S. dollar environment in theory could have a positive effect on companies that have revenues in another currency and costs in U.S. dollars. Under those conditions, non-U.S. companies with local costs and U.S. sales, as well as companies with costs outside the U.S. that sell commodities priced in dollars, could be stung by a weakened dollar.

It is also important to remember that currencies can be volatile from year to year as well as within the same year. “Exchange rates are relative prices, not absolute. In fact, nine of the top 10 currencies of 2009 were featured in the bottom 17 currencies of 2008,” says Mark Brett, a global currency analyst for the fund who works out of London. “Last year, the big three currencies — U.S. dollar, euro and yen — all had their own particular and compelling negatives. Depending on which was least ugly at the time, they swung around through the year, but they ended close to unchanged.”

A strong currency could arise when a country is growing more slowly than its trading partners, with imports falling more than exports due to weak domestic income growth. With reduced imports, there could be lower demand for foreign currency and the domestic currency may appreciate. In this case, a strong currency could be a symptom of underlying weakness in the economy. On the flip side, a weak currency, like the dollar in recent years, could be a side effect of relatively strong growth compared with trading partners, which drives up the domestic demand for imports faster than the foreign demand for exports.

Clearly, the question of whether relative currency strength is a good or bad thing for a company is very complicated. It is critical for companies to operate their businesses seamlessly on a global scale so they can capture the benefits of global adjustment processes, says Tomonori Tani, an investment analyst for the fund based in Tokyo. “Investment opportunities are not restricted to wealthier countries, and there are companies outside those areas that are positioned to capture stronger economic growth by offering goods and services that are needed globally,” Tomonori says. “Understanding these intricacies is a way we excel as a truly global investment management company.”

Fundamental research on currency issues

Currency effects remain in sharp focus for the fund’s investment analysts — particularly in some of the countries with more volatile currency markets — and the analysts study these issues closely. Currency issues are complex, and company disclosures in the financial statements can be opaque. To understand the accounting behind currency exposures of revenues and costs in foreign countries, “we want to know what is unhedged versus hedged, and understand the geographical distribution of revenues and costs, and a host of other concerns,” says Elizabeth Mooney, a global accounting analyst based in San Francisco.

It’s easy to get lost in translation. Some of the more intricate accounting work the investment analysts dig into involves looking at currency from all angles in the financial statements. Some of the more technical questions that the fund’s investment analysts ask themselves are: “What are the currency exposures in core operations, net investments and within subsidiaries?” and “What is the potential for earnings growth if non-U.S. companies have taken advantage of a stronger dollar and entered hedges at more favorable rates?”

At the end of the day, headlines aside, currency effects can add or detract from a company’s earnings to various degrees. However, as Bruno adds, “The best companies are the ones that don’t have to rely on benefits of currency to be competitive and do well.” n

[Begin Pull Quote]

“From a long-term investment perspective, the best companies are the ones that don’t have to rely on benefits of currency to be competitive and do well.”

Bruno Rodrigues

Investment analyst

[End Pull Quote]

[photo of blocks of cheese]

[photo of a fruit and vegetable stand]

| Tapping global potential | ||||

| 1985 | 1986 | 1987 | 1988 | 1989 |

| MSCI ACWI | MSCI ACWI | MSCI ACWI | MSCI ACWI | MSCI |

| ex USA Index | ex USA Index | ex USA Index | ex USA Index | USA Index |

| +57%* (black) | +70%* (black) | +25%* (black) | +28% (black) | +31% (red) |

| +33% (red) | +18% (red) | +4% (red) | +16% (red) | +12% (black) |

| 1990 | 1991 | 1992 | 1993 | 1994 |

| MSCI | MSCI | MSCI | MSCI ACWI | MSCI ACWI |

| USA Index | USA Index | USA Index | ex USA Index | ex USA Index |

| –2% (red) | +31% (red) | +7% (red) | +35% (black) | +7% (black) |

| –23% (black) | +14% (black) | –11% (black) | +10% (red) | +2% (red) |

| 1995 | 1996 | 1997 | 1998 | 1999 |

| MSCI | MSCI | MSCI | MSCI | MSCI ACWI |

| USA Index | USA Index | USA Index | USA Index | ex USA Index |

| +38% (red) | +24% (red) | +34% (red) | +31% (red) | +31% (black) |

| +10% (black) | +7% (black) | +2% (black) | +14% (black) | +22% (red) |

| 2000 | 2001 | 2002 | 2003 | 2004 |

| MSCI | MSCI | MSCI ACWI | MSCI ACWI | MSCI ACWI |

| USA Index | USA Index | ex USA Index | ex USA Index | ex USA Index |

| –13% (red) | –12% (red) | –15% (black) | +41% (black) | +21% (black) |

| –15% (black) | –20% (black) | –23% (red) | +29% (red) | +11% (red) |

| 2005 | 2006 | 2007 | 2008 | 2009 |

| MSCI ACWI | MSCI ACWI | MSCI ACWI | MSCI | MSCI ACWI |

| ex USA Index | ex USA Index | ex USA Index | USA Index | ex USA Index |

| +17% (black) | +27% (black) | +17% (black) | –37% (red) | +42% (black) |

| +6% (red) | +15% (red) | +6% (red) | –45% (black) | +27% (red) |

| The table above compares total returns for the unmanaged MSCI ACWI (All Country World Index) ex USA (shown in black), and U.S. indexes (shown in red), over the past 25 calendar years. | ||||

| *Inception date of the MSCI ACWI ex USA Index is December 31, 1987; data prior to that is based on the MSCI EAFE (Europe, Australasia, Far East) Index. | ||||

A world of opportunity

With more than half of the world’s investment opportunities located beyond our shores, an international focus gives U.S. investors access to growth potential that would otherwise be out of reach. As the chart shows, international stocks have outpaced their U.S. counterparts in 14 of the past 25 calendar years.

Tempered volatility

Diversifying among many markets can also help investors mitigate fluctuations in the value of their investments. Over the past 30 calendar years, the least volatile equity portfolio would have been composed of approximately 65% U.S. stocks and 35% non-U.S. stocks (rebalanced monthly), and been nearly as rewarding as one invested entirely in U.S. stocks. (Volatility is measured by annualized standard deviation, based on monthly returns, or how returns have varied from the mean over time.)

Active management

Negotiating the unfamiliar terrain of international markets can be challenging. That is why so many people choose to invest overseas through professionally managed mutual funds. EuroPacific Growth Fund draws on the global research experience of its investment adviser, Capital Research and Management Company, to find attractive companies based chiefly in Europe and the Pacific Basin.

Summary investment portfolio, March 31, 2010

The following summary investment portfolio is designed to streamline the report and help investors better focus on a fund’s principal holdings. See the inside back cover for details on how to obtain a complete schedule of portfolio holdings.

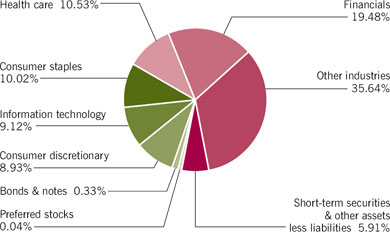

Industry sector diversification (percent of net assets)

Country diversification (percent of net assets) | ||||

| Euro zone* | 30.0 | % | ||

| Japan | 10.1 | |||

| United Kingdom | 10.1 | |||

| Switzerland | 8.0 | |||

| Mexico | 3.5 | |||

| China | 3.5 | |||

| Canada | 3.2 | |||

| Brazil | 3.1 | |||

| India | 3.0 | |||

| South Korea | 2.6 | |||

| Australia | 2.4 | |||

| Taiwan | 2.0 | |||

| Other countries | 12.6 | |||

| Short-term securities & other assets less liabilities | 5.9 | |||

| *Countries using the euro as a common currency; those represented in the fund's portfolio are Austria, Belgium, Finland, France, Germany, Greece, Ireland, Italy, the Netherlands, Portugal and Spain. | ||||

| Percent | ||||||||||||

| Value | of net | |||||||||||

| Common stocks - 93.72% | Shares | (000 | ) | assets | ||||||||

| Financials - 19.48% | ||||||||||||

| Banco Santander, SA | 96,355,254 | $ | 1,283,017 | 1.25 | % | |||||||

| A leading Spanish bank, with a strong franchise in Latin America and the U.K. | ||||||||||||

| Barclays PLC | 200,644,707 | 1,097,831 | ||||||||||

| Barclays PLC (1) | 6,192,900 | 33,885 | 1.10 | |||||||||

| One of the largest retail and commercial banking groups in the U.K. | ||||||||||||

| UBS AG (2) | 62,434,976 | 1,017,916 | .99 | |||||||||

| One of the world's largest financial services companies, providing wealth management, investment banking and asset management. | ||||||||||||

| Prudential PLC | 119,635,824 | 994,692 | .97 | |||||||||

| A leading life insurance and pension provider. Has significant operations in the U.S. and the U.K. and is growing in the Asia/Pacific region. | ||||||||||||

| Industrial and Commercial Bank of China Ltd., Class H | 1,139,854,000 | 869,131 | .85 | |||||||||

| A state-owned commercial bank in China and one of the world's largest banks. | ||||||||||||

| Société Générale | 13,111,355 | 826,170 | .81 | |||||||||

| Has retail, corporate and investment banking operations around the world, with particular strength in Europe. | ||||||||||||

| Housing Development Finance Corp. Ltd. | 12,702,073 | 770,060 | .75 | |||||||||

| Offers home loans and other financial services through a network of offices in India. | ||||||||||||

| Deutsche Bank AG | 9,193,504 | 709,490 | .69 | |||||||||

| Provides corporate banking, investment banking and worldwide asset management. | ||||||||||||

| Banco Bradesco SA, preferred nominative | 35,653,805 | 657,176 | .64 | |||||||||

| One of the largest private banks in Brazil. | ||||||||||||

| Itaú Unibanco Holding SA, preferred nominative | 17,739,630 | 388,786 | ||||||||||

| Itaú Unibanco Holding SA, preferred nominative (ADR) | 11,638,203 | 255,924 | .63 | |||||||||

| One of Brazil's leading private commercial banks. | ||||||||||||

| Bank of China Ltd., Class H | 1,181,106,000 | 629,801 | .62 | |||||||||

| One of China's largest commercial banks. | ||||||||||||

| AXA SA | 26,896,837 | 599,455 | .59 | |||||||||

| One of the world's largest insurance and financial services companies. | ||||||||||||

| Other securities | 9,824,209 | 9.59 | ||||||||||

| 19,957,543 | 19.48 | |||||||||||

| Health care - 10.53% | ||||||||||||

| Bayer AG | 29,735,750 | 2,015,140 | 1.97 | |||||||||

| Makes pharmaceuticals and over-the-counter medicines, and develops medical diagnostic equipment. | ||||||||||||

| Novartis AG | 34,611,325 | 1,874,931 | 1.83 | |||||||||

| One of the world's largest pharmaceutical companies. | ||||||||||||

| Novo Nordisk A/S, Class B | 22,139,400 | 1,721,703 | 1.68 | |||||||||

| A global leader in drugs to treat diabetes. | ||||||||||||

| Roche Holding AG | 10,065,636 | 1,637,234 | 1.60 | |||||||||

| A world leader in pharmaceuticals and diagnostic research. | ||||||||||||

| Teva Pharmaceutical Industries Ltd. (ADR) | 17,536,100 | 1,106,177 | 1.08 | |||||||||

| The leading drug company in Israel, and one of the largest generic drug companies in the U.S. | ||||||||||||

| CSL Ltd. | 19,767,862 | 660,659 | .64 | |||||||||

| Develops pharmaceuticals, including vaccines and products derived from human plasma. | ||||||||||||

| Other securities | 1,776,027 | 1.73 | ||||||||||

| 10,791,871 | 10.53 | |||||||||||

| Consumer staples - 10.02% | ||||||||||||

| Anheuser-Busch InBev NV | 41,213,464 | 2,079,944 | ||||||||||

| Anheuser-Busch InBev NV, VVPR STRIPS (2) | 10,093,238 | 96 | 2.03 | |||||||||

| One of the world's largest brewers. | ||||||||||||

| Nestlé SA | 23,552,000 | 1,209,748 | 1.18 | |||||||||

| Global packaged food and beverage company based in Switzerland. | ||||||||||||

| Pernod Ricard SA | 10,705,051 | 910,740 | .89 | |||||||||

| Produces wine, spirits and nonalcoholic beverages. | ||||||||||||

| Tesco PLC | 127,197,773 | 841,126 | .82 | |||||||||

| Major international retailer based in the United Kingdom. | ||||||||||||

| Danone SA | 12,511,168 | 755,083 | .74 | |||||||||

| One of the world's largest food manufacturers and a leader in dairy products, bottled water and biscuits. | ||||||||||||

| British American Tobacco PLC | 21,589,999 | 744,747 | .72 | |||||||||

| The world's second-largest tobacco company. | ||||||||||||

| Other securities | 3,728,453 | 3.64 | ||||||||||

| 10,269,937 | 10.02 | |||||||||||

| Information technology - 9.12% | ||||||||||||

| SAP AG | 24,000,795 | 1,164,657 | ||||||||||

| SAP AG (ADR) | 4,117,500 | 198,340 | 1.33 | |||||||||

| A leading developer of software for business applications. Also provides information technology services. | ||||||||||||

| Samsung Electronics Co. Ltd. | 1,665,659 | 1,204,481 | ||||||||||

| Samsung Electronics Co. Ltd., nonvoting preferred | 48,800 | 23,209 | 1.20 | |||||||||

| Korea's top electronics manufacturer and a global leader in semiconductor production. | ||||||||||||

| Canon, Inc. | 20,576,700 | 954,339 | .93 | |||||||||

| One of the world's premier manufacturers of cameras, copiers, printers and optical equipment. | ||||||||||||

| HOYA CORP. (3) | 23,734,700 | 653,111 | .64 | |||||||||

| A large manufacturer of specialty glass and crystal used in electronics and vision care. | ||||||||||||

| Taiwan Semiconductor Manufacturing Co. Ltd. | 295,735,170 | 573,202 | ||||||||||

| Taiwan Semiconductor Manufacturing Co. Ltd. (ADR) | 5,822,723 | 61,080 | .62 | |||||||||

| One of the world's largest semiconductor manufacturers. | ||||||||||||

| Telefonaktiebolaget LM Ericsson, Class B | 57,255,964 | 605,744 | .59 | |||||||||

| One of the world's largest suppliers of wired and wireless telephone infrastructure. | ||||||||||||

| Other securities | 3,907,838 | 3.81 | ||||||||||

| 9,346,001 | 9.12 | |||||||||||

| Consumer discretionary - 8.93% | ||||||||||||

| Honda Motor Co., Ltd. | 29,109,250 | 1,028,926 | 1.00 | |||||||||

| Develops, manufactures and sells automobiles, motorcycles and power equipment globally. | ||||||||||||

| Daimler AG | 17,128,778 | 807,892 | ||||||||||

| Daimler AG (New York registered) | 250,000 | 11,753 | .80 | |||||||||

| One of the world's largest automakers and heavy truck manufacturers. | ||||||||||||

| Industria de Diseño Textil, SA | 10,683,042 | 705,539 | .69 | |||||||||

| Designs and retails up-to-the-minute clothing. Most of its shops are in Europe. | ||||||||||||

| Toyota Motor Corp. | 14,438,300 | 579,171 | .56 | |||||||||

| One of the world's largest automotive manufacturers. | ||||||||||||

| Other securities | 6,022,366 | 5.88 | ||||||||||

| 9,155,647 | 8.93 | |||||||||||

| Materials - 8.73% | ||||||||||||

| Xstrata PLC (2) | 56,660,053 | 1,074,259 | 1.05 | |||||||||

| A global diversified metals and mining group. | ||||||||||||

| ArcelorMittal | 17,758,136 | 780,745 | .76 | |||||||||

| One of the world's largest steel producers. | ||||||||||||

| Linde AG | 5,178,200 | 619,011 | .61 | |||||||||

| Major industrial gas company headquartered in Germany. | ||||||||||||

| Impala Platinum Holdings Ltd. | 19,110,488 | 562,498 | .55 | |||||||||

| One of the world's largest platinum producers. | ||||||||||||

| Syngenta AG | 1,974,315 | 549,871 | .54 | |||||||||

| One of the world's largest agrochemical companies. Develops seeds and crop protection products. | ||||||||||||

| Holcim Ltd (2) | 7,314,544 | 546,869 | .53 | |||||||||

| One of the world's largest producers of cement, concrete products and mineral aggregates. | ||||||||||||

| Other securities | 4,809,102 | 4.69 | ||||||||||

| 8,942,355 | 8.73 | |||||||||||

| Telecommunication services - 8.63% | ||||||||||||

| América Móvil, SAB de CV, Series L (ADR) | 50,366,501 | 2,535,450 | ||||||||||

| América Móvil, SAB de CV, Series L | 74,020,000 | 186,420 | 2.66 | |||||||||

| Latin America's largest cellular communications provider. | ||||||||||||

| Telefónica, SA | 55,730,000 | 1,322,759 | 1.29 | |||||||||

| One of the premier providers of fixed and mobile telephone and Internet services in Spain and Latin America. | ||||||||||||

| SOFTBANK CORP. | 32,506,000 | 801,856 | .78 | |||||||||

| Internet and telecommunications conglomerate and distributor of digital media and software. | ||||||||||||

| Koninklijke KPN NV | 40,348,800 | 640,458 | .63 | |||||||||

| Global telecommunication services provider based in the Netherlands. | ||||||||||||

| Other securities | 3,352,692 | 3.27 | ||||||||||

| 8,839,635 | 8.63 | |||||||||||

| Energy - 7.01% | ||||||||||||

| OAO Gazprom (ADR) | 49,942,000 | 1,165,147 | 1.14 | |||||||||

| The largest natural gas producer and transporter in Russia. | ||||||||||||

| Petróleo Brasileiro SA - Petrobras, ordinary nominative (ADR) | 16,506,340 | 734,367 | .72 | |||||||||

| One of the world's largest oil companies. Engaged in exploration, production, refining, marketing and chemicals. | ||||||||||||

| Reliance Industries Ltd. | 29,630,000 | 710,175 | .69 | |||||||||

| Manufactures a wide range of synthetic textiles, petrochemicals and plastics. Also involved in oil exploration and production, and electricity generation and distribution. | ||||||||||||

| Other securities | 4,574,326 | 4.46 | ||||||||||

| 7,184,015 | 7.01 | |||||||||||

| Industrials - 6.05% | ||||||||||||

| Siemens AG | 6,787,900 | 681,096 | .66 | |||||||||

| A major worldwide producer of electrical and electronic equipment used in industrial and professional applications. | ||||||||||||

| Other securities | 5,519,085 | 5.39 | ||||||||||

| 6,200,181 | 6.05 | |||||||||||

| Utilities - 2.65% | ||||||||||||

| GDF SUEZ | 14,851,539 | 574,777 | .56 | |||||||||

| Major natural gas and electricity company based in France. | ||||||||||||

| Other securities | 2,144,281 | 2.09 | ||||||||||

| 2,719,058 | 2.65 | |||||||||||

| Miscellaneous - 2.57% | ||||||||||||

| Other common stocks in initial period of acquisition | 2,638,010 | 2.57 | ||||||||||

| Total common stocks (cost: $74,002,319,000) | 96,044,253 | 93.72 | ||||||||||

| Percent | ||||||||||||

| Value | of net | |||||||||||

| Preferred stocks - 0.04% | (000 | ) | assets | |||||||||

| Financials - 0.04% | ||||||||||||

| Other securities | 35,611 | .04 | ||||||||||

| Total preferred stocks (cost: $28,674,000) | 35,611 | .04 | ||||||||||

| Principal | Percent | |||||||||||

| amount | Value | of net | ||||||||||

| Bonds & notes - 0.33% | (000 | ) | (000 | ) | assets | |||||||

| Other - 0.33% | ||||||||||||

| Gazprom International SA 7.201% 2020 (4) | $ | 19,397 | 20,635 | |||||||||

| Open Joint Stock Co. Gazprom, Series 2, 8.625% 2034 | 5,875 | 6,874 | ||||||||||

| Gaz Capital SA 7.288%-8.146% 2013-2037 | 43,480 | 48,367 | .07 | |||||||||

| Other securities | 261,819 | .26 | ||||||||||

| Total bonds & notes (cost: $254,073,000) | 337,695 | .33 | ||||||||||

| Principal | Percent | |||||||||||

| amount | Value | of net | ||||||||||

| Short-term securities - 5.86% | (000 | ) | (000 | ) | assets | |||||||

| Freddie Mac 0.12%-0.435% due 4/6/2010-1/10/2011 | 2,486,060 | 2,485,097 | 2.42 | |||||||||

| Fannie Mae 0.15%-0.43% due 4/7/2010-1/18/2011 | 1,001,400 | 1,000,465 | .98 | |||||||||

| Barclays U.S. Funding Corp. 0.07% due 4/1/2010 | 98,550 | 98,550 | .10 | |||||||||

| Nestlé Capital Corp. 0.31% due 9/14/2010 (1) | 36,500 | 36,458 | .03 | |||||||||

| Other securities | 2,388,021 | 2.33 | ||||||||||

| Total short-term securities (cost: $6,008,158,000) | 6,008,591 | 5.86 | ||||||||||

| Total investment securities (cost: $80,293,224,000) | 102,426,150 | 99.95 | ||||||||||

| Other assets less liabilities | 53,245 | .05 | ||||||||||

| Net assets | $ | 102,479,395 | 100.00 | % | ||||||||

| "Miscellaneous" securities include holdings in their initial period of acquisition that have not previously been publicly disclosed. |

| "Other securities" includes all issues that are not disclosed separately in the summary investment portfolio, including securities which were valued under fair value procedures adopted by authority of the board of trustees. The total value of all such securities was $298,463,000, which represented .29% of the net assets of the fund. |

| Investments in affiliates | ||||||

| A company is considered to be an affiliate of the fund under the Investment Company Act of 1940 if the fund's holdings in that company represent 5% or more of the outstanding voting shares. The value of the fund's affiliated-company holdings is either shown in the summary investment portfolio or included in the value of "Other securities" under the respective industry sectors. Further details on such holdings and related transactions during the year ended March 31, 2010, appear below. |

| Dividend | Value of affiliates | |||||||||||||||||||||||

| Beginning | Ending | income | at 3/31/10 | |||||||||||||||||||||

| shares | Additions | Reductions | shares | (000 | ) | (000 | ) | |||||||||||||||||

| HOYA CORP. | 26,989,700 | - | 3,255,000 | 23,734,700 | $ | 16,794 | $ | 653,111 | ||||||||||||||||

| UCB SA | 10,179,479 | 718,329 | 147,877 | 10,749,931 | 10,656 | 459,897 | ||||||||||||||||||

| Hirose Electric Co., Ltd. | 2,547,000 | - | 144,500 | 2,402,500 | 2,914 | 277,409 | ||||||||||||||||||

| Techtronic Industries Co. Ltd. | 86,710,000 | - | - | 86,710,000 | 671 | 70,360 | ||||||||||||||||||

| adidas AG (5) | 6,843,000 | 4,530,000 | 1,550,000 | 9,823,000 | 5,344 | - | ||||||||||||||||||

| Housing Development Finance Corp. Ltd. (5) | 15,436,346 | 72,727 | 2,807,000 | 12,702,073 | 7,928 | - | ||||||||||||||||||

| HTC Corp. (5) | 38,751,100 | 3,292,555 | 18,225,500 | 23,818,155 | 22,319 | - | ||||||||||||||||||

| Qantas Airways Ltd. (2) (5) | 127,259,300 | - | 82,267,823 | 44,991,477 | - | - | ||||||||||||||||||

| $ | 66,626 | $ | 1,460,777 | |||||||||||||||||||||

| The following footnotes apply to either the individual securities noted or one or more of the securities aggregated and listed as a single line item. |

| (1) Purchased in a transaction exempt from registration under the Securities Act of 1933. May be resold in the U.S. in transactions exempt from registration, normally to qualified institutional buyers. The total value of all such securities, including those in "Other securities," was $916,682,000, which represented .89% of the net assets of the fund. |

| (2) Security did not produce income during the last 12 months. |

| (3) Represents an affiliated company as defined under the Investment Company Act of 1940. |

| (4) Principal payments may be made periodically. Therefore, the effective maturity date may be earlier than the stated maturity date. |

| (5) Unaffiliated issuer at 3/31/2010. |

| Key to abbreviation |

| ADR = American Depositary Receipts |

| The descriptions of the companies shown in the summary investment portfolio, which were obtained from published reports and other sources believed to be reliable, are supplemental and are not covered by the Report of Independent Registered Public Accounting Firm. |

| See Notes to Financial Statements |

Financial statements

| Statement of assets and liabilities | ||||||||

| at March 31, 2010 | (dollars in thousands) | |||||||

| Assets: | ||||||||

| Investment securities, at value: | ||||||||

| Unaffiliated issuers (cost: $78,928,280) | $ | 100,965,373 | ||||||

| Affiliated issuers (cost: $1,364,944) | 1,460,777 | $ | 102,426,150 | |||||

| Cash denominated in currencies other than U.S. dollars (cost: $39,028) | 39,227 | |||||||

| Cash | 53 | |||||||

| Unrealized appreciation on open forward currency contracts | 7,975 | |||||||

| Receivables for: | ||||||||

| Sales of investments | 293,418 | |||||||

| Sales of fund's shares | 937,547 | |||||||

| Dividends and interest | 265,610 | |||||||

| Other | 29,802 | 1,526,377 | ||||||

| 103,999,782 | ||||||||

| Liabilities: | ||||||||

| Unrealized depreciation on open forward currency contracts | 1,115 | |||||||

| Payables for: | ||||||||

| Purchases of investments | 610,676 | |||||||

| Repurchases of fund's shares | 784,566 | |||||||

| Investment advisory services | 36,074 | |||||||

| Services provided by affiliates | 32,780 | |||||||

| Trustees' deferred compensation | 2,726 | |||||||

| Non-U.S. taxes | 50,318 | |||||||

| Other | 2,132 | 1,519,272 | ||||||

| Net assets at March 31, 2010 | $ | 102,479,395 | ||||||

| Net assets consist of: | ||||||||

| Capital paid in on shares of beneficial interest | $ | 94,404,742 | ||||||

| Distributions in excess of net investment income | (119,556 | ) | ||||||

| Accumulated net realized loss | (13,899,074 | ) | ||||||

| Net unrealized appreciation | 22,093,283 | |||||||

| Net assets at March 31, 2010 | $ | 102,479,395 | ||||||

| (dollars and shares in thousands, except per-share amounts) | ||||||||||||

| Shares of beneficial interest issued and outstanding (no stated par value) - unlimited shares authorized (2,666,683 total shares outstanding) | ||||||||||||

| Net assets | Shares outstanding | Net asset value per share* | ||||||||||

| Class A | $ | 40,425,730 | 1,046,780 | $ | 38.62 | |||||||

| Class B | 923,417 | 24,165 | 38.21 | |||||||||

| Class C | 2,901,063 | 76,951 | 37.70 | |||||||||

| Class F-1 | 8,601,559 | 223,829 | 38.43 | |||||||||

| Class F-2 | 4,028,093 | 104,307 | 38.62 | |||||||||

| Class 529-A | 825,709 | 21,552 | 38.31 | |||||||||

| Class 529-B | 91,336 | 2,424 | 37.68 | |||||||||

| Class 529-C | 312,603 | 8,318 | 37.58 | |||||||||

| Class 529-E | 46,152 | 1,214 | 38.02 | |||||||||

| Class 529-F-1 | 56,423 | 1,473 | 38.30 | |||||||||

| Class R-1 | 279,104 | 7,471 | 37.36 | |||||||||

| Class R-2 | 1,302,671 | 34,678 | 37.56 | |||||||||

| Class R-3 | 7,130,564 | 188,004 | 37.93 | |||||||||

| Class R-4 | 11,204,126 | 294,867 | 38.00 | |||||||||

| Class R-5 | 16,716,168 | 433,132 | 38.59 | |||||||||

| Class R-6 | 7,634,677 | 197,518 | 38.65 | |||||||||

| (*) Maximum offering price and redemption price per share were equal to the net asset value per share for all share classes, except for Classes A and 529-A, for which the maximum offering prices per share were $40.98 and $40.65, respectively. | ||||||||||||

| See Notes to Financial Statements | ||||||||||||

| Statement of operations | ||||||||

| for the year ended March 31, 2010 | (dollars in thousands) | |||||||

| Investment income: | ||||||||

| Income: | ||||||||

| Dividends (net of non-U.S. taxes of $239,937; also includes $66,626 from affiliates) | $ | 1,954,763 | ||||||

| Interest | 78,320 | $ | 2,033,083 | |||||

| Fees and expenses*: | ||||||||

| Investment advisory services | 382,008 | |||||||

| Distribution services | 214,833 | |||||||

| Transfer agent services | 51,768 | |||||||

| Administrative services | 69,583 | |||||||

| Reports to shareholders | 3,609 | |||||||

| Registration statement and prospectus | 10,902 | |||||||

| Trustees' compensation | 1,234 | |||||||

| Auditing and legal | 306 | |||||||

| Custodian | 19,527 | |||||||

| State and local taxes | 1,098 | |||||||

| Other | 2,889 | 757,757 | ||||||

| Net investment income | 1,275,326 | |||||||

| Net realized loss and unrealized appreciation on investments, forward currency contracts and currency: | ||||||||

| Net realized (loss) gain on: | ||||||||

| Investments (including $9,364 net loss from affiliates) | (1,258,004 | ) | ||||||

| Currency transactions | 4,935 | (1,253,069 | ) | |||||

| Net unrealized appreciation on: | ||||||||

| Investments (net of non-U.S. taxes of $50,318) | 33,633,587 | |||||||

| Forward currency contracts | 6,860 | |||||||

| Currency translations | 5,527 | 33,645,974 | ||||||

| Net realized loss and unrealized appreciation on investments, forward currency contracts and currency | 32,392,905 | |||||||

| Net increase in net assets resulting from operations | $ | 33,668,231 | ||||||

| (*) Additional information related to class-specific fees and expenses is included in the Notes to Financial Statements. | ||||||||

| See Notes to Financial Statements | ||||||||

| Statements of changes in net assets | (dollars in thousands) | |||||||

| Year ended March 31 | ||||||||

| 2010 | 2009 | |||||||

| Operations: | ||||||||

| Net investment income | $ | 1,275,326 | $ | 2,108,347 | ||||

| Net realized loss on investments and currency transactions | (1,253,069 | ) | (12,486,045 | ) | ||||

| Net unrealized appreciation (depreciation) on investments, forward currency contracts and currency translations | 33,645,974 | (36,391,191 | ) | |||||

| Net increase (decrease) in net assets resulting from operations | 33,668,231 | (46,768,889 | ) | |||||

| Dividends and distributions paid to shareholders: | ||||||||

| Dividends from net investment income | (1,624,677 | ) | (1,815,409 | ) | ||||

| Distributions from net realized gain on investments | - | (3,253,052 | ) | |||||

| Total dividends and distributions paid to shareholders | (1,624,677 | ) | (5,068,461 | ) | ||||

| Net capital share transactions | 6,951,394 | 546,261 | ||||||

| Total increase (decrease) in net assets | 38,994,948 | (51,291,089 | ) | |||||

| Net assets: | ||||||||

| Beginning of year | 63,484,447 | 114,775,536 | ||||||

| End of year (including distributions in excess of and undistributed net investment income: $(119,556) and $166,473, respectively) | $ | 102,479,395 | $ | 63,484,447 | ||||

| See Notes to Financial Statements | ||||||||

Notes to financial statements

| 1. | Organization |

EuroPacific Growth Fund (the "fund") is registered under the Investment Company Act of 1940 as an open-end, diversified management investment company. The fund seeks long-term growth of capital by investing primarily in the securities of companies based in Europe and the Pacific Basin.

On November 24, 2009, shareholders approved amendments to the fund’s Investment Advisory and Service Agreement and amendments to and elimination of certain fundamental investment policies of the fund. On December 23, 2009, shareholders approved a proposal to reorganize the fund from a Massachusetts business trust to a Delaware statutory trust. The reorganization may be completed in 2010 or early 2011; however, the fund reserves the right to delay the implementation.

The fund has 16 share classes consisting of five retail share classes, five 529 college savings plan share classes and six retirement plan share classes. The 529 college savings plan share classes (529-A, 529-B, 529-C, 529-E and 529-F-1) can be used to save for college education. The six retirement plan share classes (R-1, R-2, R-3, R-4, R-5 and R-6) are generally offered only through eligible employer-sponsored retirement plans. The fund’s share classes are described below:

| Share class | Initial sales charge | Contingent deferred sales charge upon redemption | Conversion feature |

| Classes A and 529-A | Up to 5.75% | None (except 1% for certain redemptions within one year of purchase without an initial sales charge) | None |

| Classes B and 529-B* | None | Declines from 5% to 0% for redemptions within six years of purchase | Classes B and 529-B convert to Classes A and 529-A, respectively, after eight years |

| Class C | None | 1% for redemptions within one year of purchase | Class C converts to Class F-1 after 10 years |

| Class 529-C | None | 1% for redemptions within one year of purchase | None |

| Class 529-E | None | None | None |

| Classes F-1, F-2 and 529-F-1 | None | None | None |

| Classes R-1, R-2, R-3, R-4, R-5 and R-6 | None | None | None |

*Effective April 21, 2009, Class B and 529-B shares of the fund are not available for purchase.

On May 1, 2009, the fund made an additional retirement plan share class (Class R-6) available for sale pursuant to an amendment to its registration statement filed with the Securities and Exchange Commission (“SEC”). Refer to the fund’s retirement plan prospectus for more details.

Holders of all share classes have equal pro rata rights to assets, dividends and liquidation proceeds. Each share class has identical voting rights, except for the exclusive right to vote on matters affecting only its class. Share classes have different fees and expenses ("class-specific fees and expenses"), primarily due to different arrangements for distribution, administrative and shareholder services. Differences in class-specific fees and expenses will result in differences in net investment income and, therefore, the payment of different per-share dividends by each class.

| 2. | Significant accounting policies |

The financial statements have been prepared to comply with accounting principles generally accepted in the United States of America. These principles require management to make estimates and assumptions that affect reported amounts and disclosures. Actual results could differ from those estimates. The fund follows the significant accounting policies described below, as well as the valuation policies described in the next section on valuation.

Security transactions and related investment income – Security transactions are recorded by the fund as of the date the trades are executed with brokers. Realized gains and losses from security transactions are determined based on the specific identified cost of the securities. In the event a security is purchased with a delayed payment date, the fund will segregate liquid assets sufficient to meet its payment obligations. Dividend income is recognized on the ex-dividend date and interest income is recognized on an accrual basis. Market discounts, premiums and original issue discounts on fixed-income securities are amortized daily over the expected life of the security.

Class allocations – Income, fees and expenses (other than class-specific fees and expenses) and realized and unrealized gains and losses are allocated daily among the various share classes based on their relative net assets. Class-specific fees and expenses, such as distribution, administrative and shareholder services, are charged directly to the respective share class.

Dividends and distributions to shareholders – Dividends and distributions paid to shareholders are recorded on the ex-dividend date.

Currency translation – Assets and liabilities, including investment securities, denominated in currencies other than U.S. dollars are translated into U.S. dollars at the exchange rates in effect on the valuation date. Purchases and sales of investment securities and income and expenses are translated into U.S. dollars at the exchange rates on the dates of such transactions. On the accompanying financial statements, the effects of changes in exchange rates on investment securities are included with the net realized gain or loss and net unrealized appreciation or depreciation on investments. The realized gain or loss and unrealized appreciation or dep reciation resulting from all other transactions denominated in currencies other than U.S. dollars are disclosed separately.

| 3. | Valuation |

The fund’s investments are reported at fair value as defined by accounting principles generally accepted in the United States of America. The fund generally determines its net asset value as of approximately 4:00 p.m. New York time each day the New York Stock Exchange is open.

Methods and inputs – The fund uses the following methods and inputs to establish the fair value of its assets and liabilities. Use of particular methods and inputs may vary over time based on availability and relevance as market and economic conditions evolve.

Equity securities are generally valued at the official closing price of, or the last reported sale price on, the exchange or market on which such securities are traded, as of the close of business on the day the securities are being valued or, lacking any sales, at the last available bid price. Prices for each security are taken from the principal exchange or market in which the security trades.

Fixed-income securities, including short-term securities purchased with more than 60 days left to maturity, are generally valued at prices obtained as of approximately 3:00 p.m. New York time from one or more pricing vendors. Vendors value such securities based on one or more of the inputs described in the following table. The table provides examples of inputs that are commonly relevant for valuing particular classes of fixed-income securities in which the fund is authorized to invest. However, these classifications are not exclusive and any of the inputs may be used to value any other class of fixed-income security.

| Fixed-income class | Examples of standard inputs |

| All | Benchmark yields, transactions, bids, offers, quotations from dealers and trading systems, new issues, spreads and other relationships observed in the markets among comparable securities and proprietary pricing models such as yield measures calculated using factors such as cash flows, financial or collateral performance and other reference data (collectively referred to as “standard inputs”) |

| Corporate bonds & notes; convertible securities | Standard inputs and underlying equity of the issuer |

| Bonds & notes of governments & government agencies | Standard inputs and interest rate volatilities |

Where the investment adviser deems it appropriate to do so (such as when vendor prices are unavailable or not deemed to be representative), fixed-income securities will be valued in good faith at the mean quoted bid and asked prices that are reasonably and timely available (or bid prices, if asked prices are not available) or at prices for securities of comparable maturity, quality and type.