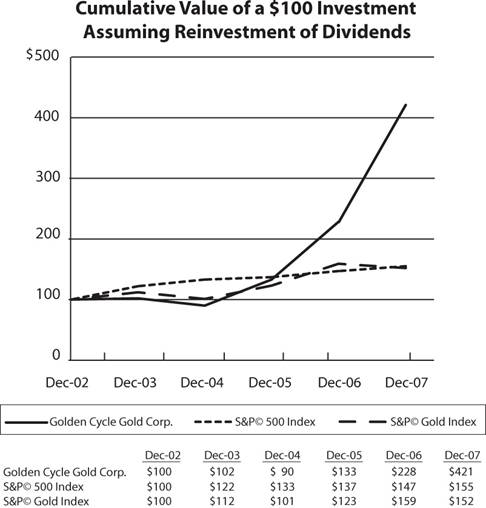

Messrs. Hampton, Anagnoston, Ruder, Thul and Gustafson and their respective affiliates beneficially owned approximately 0.6 percent, 5.0 percent, less than 0.1 percent, less than 0.1 percent and zero percent, respectively, of the shares of Golden Cycle common stock outstanding as of March 18, 2008 (excluding shares of the Company’s common stock which such person had the right to acquire as of such date upon exercise of stock options).

The Agreement and Plan of Merger requires the surviving company in the merger to indemnify the Company’s directors and officers and to honor all rights to indemnification and exculpation existing in favor of a director or officer of the Company and its subsidiaries under the Company’s articles of incorporation and by-laws as in effect on the date of the Agreement and Plan of Merger for a period of six years after the effective time of the merger and to maintain for a period of three years after the closing date of the merger director and officer liability insurance for the benefit of the Company’s officers and directors with respect to acts or omissions occurring prior to the closing date.

In connection with the merger, each unexpired and unexercised option to purchase the Company’s common stock granted under the Company’s stock option plans, whether vested or unvested, will be automatically converted into an option to purchase a number of AngloGold Ashanti ADSs equal to the number of shares of the Company’s common stock that could have been purchased (assuming full vesting) under such option multiplied by the exchange ratio of 0.29 (rounded down to the nearest whole number of AngloGold Ashanti ADSs) at a price per AngloGold Ashanti ADS equal to the per share option exercise price specified in the Company option divided by the exchange ratio of 0.29 (rounded up to the nearest whole cent). Each substituted option shall otherwise be subject to the same terms and conditions as the option to purchase the Company’s common stock that it was issued in respect of. Prior to the closing of the merger, each director and officer of the Company will voluntarily tender his resignation and, under the terms of the option plans pursuant to which the Company’s stock options were issued, each substituted option will therefore expire six months following the closing of the merger.

Pursuant to a resolution of the Company’s board of directors, the Company has agreed to pay Mr. Hampton severance following the closing of the merger in a lump sum amount equal to $8,404 per month from the closing of the merger through August 31, 2008.

ITEM 14. PRINCIPAL ACCOUNTING FEES AND SERVICES

Audit Fees

The fees paid by the Corporation to Ehrhardt Keefe Steiner & Hottman (“EKS&H”) for services provided:

| 2007 | 2006 |

|---|

| 1) Audit fees, including audits of our annual financial statements, | | $22,500(a) | | $21,100 | |

| review of our quarterly financial statements and statutory audits | |

| of our foreign subsidiaries. | |

| 2) Audit-related fees | | 7,500(b) | | 6,900 | |

| 3) Tax fees (including tax compliance and advice) | | — | | 4,400 | |

| 4) All other fees | | 293(c) | ( | 6,629 | * |

| | | | | |

(a) Represents billing of $22,500 for the 2006 audit

(b) Includes billings related to the first, second and third quarter reviews

(c) represents $293 of out-of-pocket expenses

* Includes $3,850 related to assistance with a potential merger with Fronteer Development Group, Inc., $1,500 related to research of potential phantom income, $800 related to the Illipah sale and $479 of out-of-pocket expenses.

The Audit Committee determined that the provision of tax preparation services by EKS&H is compatible with maintaining the independence of EKS&H, however, decided to engage the services of Stockman Kast Ryan & Co, LLP for the preparation of the Company’s 2006 and 2007 State and Federal income tax returns.

Policy on Audit Committee Pre-Approval of Audit and Non-Audit Services of Independent Auditor

The Audit Committee’s policy is to pre-approve all audit and non-audit services provided by the independent auditors. These services may include audit services, audit IT-related services, tax services and other services. Pre-approval is generally granted for up to one year and any pre-approval is detailed as to the particular service and generally subject to a specific budget. The independent auditors and management are required to report to the full Audit Committee regarding the extent of services provided by the independent auditors in accordance with this pre-approval, and the fees for the services performed to date. During 2007 and 2006, the Audit Committee pre-approved the EKS&H audit services for quarterly review of four quarterly periods.

PART IV

ITEM 15. EXHIBITS, FINANCIAL STATEMENT SCHEDULES

Documents Filed as Part of This Report

Documents Filed as Part of This Report

| Financial Statements | Page |

|---|

| (a) | | Report of Independent Registered Accounting Firm, | | | |

| | Ehrhardt Keefe Steiner & Hottman, P.C. | | 41 | |

| (b) | | Consolidated Balance Sheets, December 31, 2007 and 2006 | | 42 | |

| (c) | | Consolidated Statements of Operations for the Years | | | |

| | Ended December 31, 2007, 2006 and 2005 | | 43 | |

| (d) | | Consolidated Statements of Shareholders' Equity for the Years | | | |

| | Ended December 31, 2007, 2006 and 2005 | | 44 | |

| (e) | | Consolidated Statements of Cash Flows for the Years | | | |

| | Ended December 31, 2007, 2006 and 2005 | | 45 | |

38

| (f) | | Notes to Consolidated Financial Statements | | 46 | |

Financial Statement Schedules

Financial statement schedules are omitted because they are not applicable or the required information is shown in the financial statements or notes thereto.

Exhibit Index

| 3.1. | | Articles of Incorporation, as amended, effective June 15, 2004, (incorporated by reference to Exhibit 3.1 to the Company’s Quarterly Report on Form 10-Q for the quarter ended March 31, 2006) |

| 3.2 | | Articles of Amendment to the Articles of Incorporation of Golden Cycle Gold Corporation (incorporated by reference to Exhibit 3.1 to the Company’s Form 8-K filed May 12, 2006. |

| 3.3. | | By-laws (incorporated by reference to Exhibit 2 to the Company’s Form 10 dated May 19, 1983). |

| 10.1. | | Amended and Restated Joint Venture Agreement between AngloGold Ashanti (Colorado) Inc. and the Company dated as of January 1, 1991 (incorporated by reference to Exhibit 1 to the Company’s Current Report on Form 8-K dated June 17, 1991). |

| 10.2 | | 1997 Officers’ & Directors’ Stock Option Plan (incorporated by reference to Appendix A of the Company’s Definitive Proxy Statement dated April 30, 1997). |

| 10.3 | | 2002 Stock Option Plan (incorporated by reference to Appendix A of the Company’s Definitive Proxy Statement dated April 27, 2001). |

| 10.5 | | Employment Agreement dated December 2, 2004 with R. Herbert Hampton (incorporated by reference to Exhibit 1 to the Company’s Form 8-K dated December 3, 2004). |

| 10.6 | | Agreement of Plan of Merger dated January 11, 2008 by and between the Company and AngloGold Ashanti Limited (incorporated by reference to the Company’s Form 8-K dated January 15, 2008). |

| 10.7 | | Form of Shareholder Agreement between AngloGold Ashanti and principal shareholders of the Company (incorporated by reference to the Company’s Form 8-K dated January 15, 2008). |

| 10.8 | | Engagement Letter dated December 18, 2007, by and between the Company and PI Financial (USA) Corp. (incorporate by reference to the Company’s Form 8-K dated January 15, 2008). |

| 21.1. | | Subsidiary of the Company: Golden Cycle Philippines Inc. incorporated in the Republic of the Philippines. |

| 21.2. | | Subsidiary of the Company: Golden Cycle Gold Exploration Inc. incorporated in the state of Nevada. |

| 23.1 | | Consent of Ehrhardt Keefe Steiner & Hottman P.C. |

| 31.1 | | Certification of Chief Executive Officer and Principal Financial and Accounting Officer pursuant to the Sarbanes-Oxley Act of 2002, Section 302 |

| 32.1 | | Certification of Chief Executive Officer and Principal Financial and Accounting Officer aaaa pursuant to the Sarbanes-Oxley Act of 2002, Section 906. |

39

SIGNATURES

Pursuant to the requirements of Section 13 or 15(d) of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereto duly authorized.

\s\ R. Herbert Hampton____________________

R. Herbert Hampton, President, Chief Executive Officer, and Treasurer (Principal Executive Officer, Principal Financial Officer, and Principal Accounting Officer)

Date: March 18, 2008

Pursuant to the requirements of the Securities Exchange Act of 1934, this report has been signed below by the following persons on behalf of the registrant in the capacities and on the dates indicated.

\s\ R. Herbert Hampton

___________________________________ | March 18, 2008 |

R. Herbert Hampton, President, Chief | Date |

Executive Officer, and Treasurer

(Principal Executive Officer, Principal

Financial Officer, and Principal Accounting

Officer)

\s\ James C. Ruder

___________________________________ | March 18, 2008 |

James C. Ruder, Director | Date |

\s\ Robert T. Thul

___________________________________ | March 18, 2008 |

Robert T. Thul, Director | Date |

\s\ Dr. Taki N. Anagnoston

___________________________________ | March 18, 2008 |

Dr. Taki N. Anagnoston, Director | Date |

\s\ Donald L. Gustafson

___________________________________ | March 18, 2008 |

Donald L. Gustafson, Director | Date |

40

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

Board of Directors and Stockholders

Golden Cycle Gold Corporation

Colorado Springs, Colorado

We have audited the accompanying consolidated balance sheets of Golden Cycle Gold Corporation and Subsidiaries (a Colorado Corporation) as of December 31, 2007 and 2006, and the related consolidated statements of operations, changes in stockholders' equity and comprehensive income (loss), and cash flows for the years ended December 31, 2007, 2006 and 2005. These consolidated financial statements are the responsibility of the Company's management. Our responsibility is to express an opinion on these consolidated financial statements based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the consolidated financial statements are free of material misstatement. The Company is not required to have, nor were we engaged to perform an audit of its internal control over financial reporting. Our audit included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Company’s internal control over financial reporting. Accordingly, we express no such opinion. An audit also includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the consolidated financial statements referred to above present fairly, in all material respects, the financial position of Golden Cycle Gold Corporation and Subsidiaries as of December 31, 2007 and 2006, and the consolidated results of their operations and their cash flows for the years ended December 31, 2007, 2006 and 2005 in conformity with accounting principals generally accepted in the United States of America.

| /s/ Ehrhardt Keefe Steiner & Hottman P.C. |

March 18, 2008

Denver, Colorado

41

GOLDEN CYCLE GOLD CORPORATION AND SUBSIDIARIES Consolidated Balance Sheets |

|

| | December 31, | | December 31, |

Assets | | 2007 | | 2006 |

Current assets: | | | | |

Cash and cash equivalents | $ | 25,617 | $ | 53,142 |

Short-term investments (note 2) | | 658,514 | | 677,944 |

Interest receivable and other current assets | | 48,677 | | 19,168 |

Prepaid insurance | | 21,597 | | 25,203 |

Total current assets | | 754,405 | | 775,457 |

Property and equipment, at cost: | | | | |

Land | | 2,025 | | 2,025 |

Mineral claims | | 8,657 | | 20,657 |

Furniture and fixtures | | 9,354 | | 9,354 |

Machinery and equipment | | 21,516 | | 21,516 |

| | 41,552 | | 53,552 |

Less accumulated depreciation | | (28,491) | | (26,131) |

| | 13,061 | | 27,421 |

Total assets | $ | 767,466 | $ | 802,878 |

| | | | |

Liabilities and Shareholders’ Equity | | | | |

Current liabilities: | | | | |

Accounts payable and accrued liabilities | $ | 106,835 | | 18,373 |

Total current liabilities | | 106,835 | | 18,373 |

| | | | |

Commitments and contingencies (note 7) | | | | |

Shareholders’ equity (note 5): | | | | |

Common stock, no par value. Authorized 100,000,000 shares; issued and outstanding 9,769,250 shares in 2007 and 9,744,250 shares in 2006 | | 7,544,429 | | 7,499,429 |

Additional paid-in capital | | 3,189,799 | | 2,728,273 |

Accumulated deficit | | (10,000,086) | | (9,411,686) |

Accumulated other comprehensive loss | | (73,511) | | (31,511) |

Total shareholders’ equity | | 660,631 | | 784,505 |

| | | | |

Total liabilities and shareholders' equity | $ | 767,466 | $ | 802,878 |

See accompanying notes to consolidated financial statements.

42

GOLDEN CYCLE GOLD CORPORATION AND SUBSIDIARIES Consolidated Statements of Operations | |

| For the Years Ended December 31, |

| | 2007 | | 2006 | | 2005 |

Revenue: | | | | | | |

Distributions from mining joint venture in excess of carrying value (note 3) | $ | 250,000 | $ | 250,000 | $ | 250,000 |

Expenses: | | | | | | |

General and administrative expense | | 992,963 | | 1,502,938 | | 603,044 |

Depreciation expense | | 2,360 | | 2,224 | | 3,973 |

Exploration expense | | 9,259 | | 8,410 | | 305,661 |

| | 1,004,582 | | 1,513,572 | | 912,678 |

Operating loss | | (754,582) | | (1,263,572) | | (662,678) |

Other income: | | | | | | |

Interest and other income | | 27,107 | | 30,787 | | 35,667 |

Gold bullion mark to market | | 62,575 | | 35,650 | | 24,986 |

Gain on assets sold (net) | | 76,500 | | 100,000 | | — |

| | 166,182 | | 166,437 | | 60,653 |

Net loss | $ | (588,400) | $ | (1,097,135) | $ | (602,025) |

Basic loss per share | $ | (0.06) | $ | (0.11) | $ | (0.06) |

Diluted loss per share | $ | (0.06) | $ | (0.11) | $ | (0.06) |

| | | | | | |

Basic weighted average shares outstanding | | 9,760,346 | | 9,744,250 | | 9,738,086 |

| | | | | | |

Diluted weighted average shares outstanding | | 9,760,346 | | 9,744,250 | | 9,738,086 |

See accompanying notes to consolidated financial statements.

43

GOLDEN CYCLE GOLD CORPORATION AND SUBSIDIARIES Consolidated Statements of Shareholders’ Equity and Comprehensive Income (Loss) For the Years ended December 31, 2007, 2006, and 2005 | |

| Common stock | | Additional paid-in capital | | Accumulated deficit | | Accumulated other comprehensive loss–foreign currency translation adjustment | | Total |

Shares | | Amount |

Balance at December 31, 2004 | 9,669,250 | $ | 7,406,317 | $ | 1,927,736 | $ | (7,712,526) | $ | (31,813) | $ | 1,589,714 |

Stock options exercised | 75,000 | | 93,112 | | — | | — | | — | | 93,112 |

Net loss | — | | — | | — | | (602,025) | | — | | (602,025) |

Foreign currency translation adjustment | — | | — | | — | | — | | 302 | | 302 |

Comprehensive net loss | | | | | | | | | | | (601,723) |

Balance at December 31, 2005 | 9,744,250 | | 7,499,429 | | 1,927,736 | | (8,314,551) | | (31,511) | | 1,081,103 |

Net loss | — | | — | | — | | (1,097,135) | | — | | (1,097,135) |

Non-cash stock-based compensation | — | | — | | 791,597 | | — | | — | | 791,597 |

Non-cash compensation liability accrual | | | | | | | | | | | |

Reclassified to contributed capital | — | | — | | 8,940 | | — | | — | | 8,940 |

Balance at December 31, 2006 | 9,744,250 | | 7,499,429 | | 2,728,273 | | (9,411,686) | | (31,511) | | 784,505 |

Stock options exercised | 25,000 | | 45,000 | | — | | — | | — | | 45,000 |

Non-cash stock-based compensation | — | | — | | 461,526 | | — | | — | | 461,526 |

Net loss | — | | — | | — | | (588,400) | | — | | (588,400) |

Other comprehensive loss | — | | — | | — | | — | | (42,000) | | (42,000) |

Comprehensive net loss | | | | | | | | | | | (630,400) |

Balance at December 31, 2007 | 9,769,250 | $ | 7,544,429 | $ | 3,189,799 | $ | (10,000,086) | $ | (73,511) | $ | 660,631 |

| | | | | | | | | |

See accompanying notes to consolidated financial statements.

44

GOLDEN CYCLE GOLD CORPORATION AND SUBSIDIARIES Consolidated Statement of Cash Flows | |

| | For the Years Ended December 31, |

| 2007 | | 2006 | | 2005 |

Cash flows from operating activities: | | | | | | |

Net loss | $ | (588,400) | $ | (1,097,135) | $ | (602,025) |

Adjustments to reconcile net loss to net cash used in operating activities: | | | | | | |

Depreciation expense | | 2,360 | | 2,224 | | 3,973 |

Gain on sale of Illipah | | (76,500) | | — | | — |

Increase in market value of gold asset | | (62,575) | | (35,650) | | (24,986) |

Stock based compensation expense | | 461,526 | | 791,597 | | — |

Non-cash Compensation liability accrual reclassified to contributed capital | | — | | 8,940 | | — |

Write-down of investment in subsidiary | | — | | (2,964) | | — |

Decrease (increase) in interest receivable and other current assets | | 491 | | (3,415) | | (2,229) |

Decrease (increase) in prepaid insurance | | 3,606 | | (376) | | (447) |

Increase (decrease) in accounts payable and accrued liabilities | | 88,462 | | (25,435) | | (13,060) |

Net cash used in operating activities | | (171,030) | | (362,214) | | (638,774) |

| | | | | | |

Cash flows from investing activities: | | | | | | |

Decrease in short-term investments, net | | 98,505 | | 249,297 | | 256,632 |

Purchases of property and equipment, net | | — | | (1,110) | | (1,103) |

Net cash provided by investing activities | | 98,505 | | 248,187 | | 255,529 |

| | | | | | |

Cash flows provided by financing activity: | | | | | | |

Proceeds on exercise of stock options | | 45,000 | | — | | 93,112 |

Net cash provided by financing activities | | 45,000 | | — | | 93,112 |

| | | | | | |

Effect of exchange rate changes on cash | | — | | — | | 302 |

| | | | | | |

Net decrease in cash and cash equivalents | | (27,525) | | (114,027) | | (289,831) |

Cash and cash equivalents, beginning of year | | 53,142 | | 167,169 | | 457,000 |

Cash and cash equivalents, end of year | $ | 25,617 | $ | 53,142 | $ | 167,169 |

See accompanying notes to consolidated financial statements.

45

GOLDEN CYCLE GOLD CORPORATION

AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(1) | Summary of Significant Accounting Policies |

Golden Cycle Gold Corporation (the Company), a Colorado corporation, acquires and explores mining properties in Colorado, Nevada, and the Republic of the Philippines. The Company’s principal investment consists of its joint venture participation in the Cripple Creek and Victor Gold Mining Company (the Joint Venture), a precious metals mining company in the Cripple Creek Mining District of Teller County, Colorado. In addition, during 1997 the Company established Golden Cycle Philippines, Inc. (GCPI), a wholly owned subsidiary of the Company, in the Republic of the Philippines in order to participate in potential mining opportunities. In January 2002, the Company established Golden Cycle Gold Exploration, Inc. (GCGE), a wholly owned subsidiary, to conduct exploration activities for the Company.

The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America requires management to make various estimates and assumptions in determining the reported amounts of assets, liabilities, revenues, and expenses for each period presented, and in the disclosure of commitments and contingencies. Actual results could differ significantly from those estimates. Changes in these estimates and assumptions will occur based on the passage of time and the occurrence of future events.

| (b) | Principles of Consolidation |

The consolidated financial statements include the accounts of the Company and its wholly owned subsidiaries. All significant inter-company transactions and balances have been eliminated in consolidation.

| (c) | Cash and Cash Equivalents |

The Company considers all highly liquid instruments purchased with an original maturity of three months or less to be cash equivalent.

| (d) | Short-Term Investments |

Short-term investments consist primarily of certificates of deposit. Short-term investments also include 310 troy ounces of gold bullion purchased by the Company in 2002. Interest revenue and the increase or decrease in the value of the gold bullion is included in the consolidated statement of operations.

| (e) | Marketable Equity Securities |

The Company’s investments in marketable equity securities are classified as available-for-sale and are carried at fair value, which is based upon quoted prices of the securities owned. The cost of marketable equity securities sold is determined by the specific identification method. Changes in market value are recorded in accumulated other comprehensive income within stockholders’ equity, unless a decline in market value is considered other than temporary, in which case the decline is recognized as a loss in the consolidated statement of operations. The Company had marketable equity securities with fair values of $16,500 and $0 respectively, and cost of $58,500 and $0, respectively, at December 31, 2007 and December 31, 2006. Golden Cycle has accumulated other comprehensive income for unrealized holding losses of $42,000 and $0 at December 31, 2007 and December 31, 2006, respectively, related to our marketable equity securities.

46

| (f) | Investment in Mining Joint Venture |

The Company accounts for its investment in the Joint Venture on the equity method. In prior years, the Company’s share of Joint Venture losses exceeded the remaining carrying value of the investment and, accordingly, the investment was reduced to zero. Joint Venture distributions in excess of the investment carrying value are recorded as income. The Company has not recorded its share of Joint Venture losses incurred subsequent to the reduction of its investment balance to zero, as the Company has no obligation to fund operating losses. To the extent the Joint Venture is profitable, the Company records its share of equity income. However, the Company currently offsets the Joint Venture equity income with an allowance account due to the uncertainty that the actual receipt of cash distributions by the Company attributable to current year increases in joint venture equity will occur given that those cash distributions are far in the future due to the necessity of repaying the Joint Venture’s Initial Loans.

| (g) | Mineral Exploration and Development Costs |

Mineral exploration costs are expensed as incurred. Mineral property development costs are capitalized and depleted based upon estimated proven and probable recoverable reserves. The Company has no capitalized mineral property development costs at December 31, 2007 or December 31, 2006.

The Company assesses the carrying value of its long-lived assets for impairment whenever changes in facts or circumstances indicate that they may be impaired. Potential impairment is estimated by comparing estimated future undiscounted cash flows expected to be generated from such assets with their net book value. If net book value exceeds estimated cash flows, the asset is written down to fair value. The Company has not recorded impairment costs at December 31, 2007 or December 31, 2006.

| (h) | Property and Equipment |

Office furniture, fixtures, and equipment are stated at cost and depreciated using the straight-line method over estimated useful lives ranging from three to ten years.

| (i) | Foreign Currency Translation |

The GCPI operations’ functional currency is the local currency and, accordingly, the assets and liabilities of its Philippines operations are translated into their United States dollar equivalent at rates of exchange prevailing at each balance sheet date. Revenue and expenses are translated at average exchange rates prevailing during the periods in which such items are recognized in operations.

Gains and losses arising from translation of the consolidated financial statements of GCPI operations are included in accumulated other comprehensive income (loss) in shareholders’ equity. Amounts in this account are recognized in the consolidated statements of operations when the related net foreign investment is reduced. Gains and losses on foreign currency transactions are included in the consolidated statements of operations.

On June 5, 2007, the Company’s one active stock-based compensation plan was completed and closed with the issue of 100,000 stock options to four directors. Four of the Company’s directors were granted 25,000 stock options each on June 5, 2007 at the prevailing market price of $6.25 per share. One director exercised options for 25,000 shares of the Company’s stock May 10, 2007 for proceeds to the Company of $45,000. There were no stock options exercised during the 2006 period. The Company accounts for stock option grants in accordance with FASB Statement 123(R), Share-Based Payment. Compensation costs related to share-based payments in the amount of $461,526

47

and $791,597 were recognized in the consolidated statements of operations for the periods ended June 30, 2007 and 2006 respectively.

The Company adopted SFAS 123R using the modified prospective method. Under this method, compensation cost recognized in the years ended December 31, 2007 and 2006 include: a) compensation cost for all stock-based payments granted prior to, but not yet vested as of January 1, 2006, based on the grant-date fair value estimated in accordance with the original provisions of SFAS 123, and b) compensation cost for all stock-based payments granted subsequent to January 1, 2006, based on the grant-date fair value estimated in accordance with the provisions of SFAS 123R. The results for prior periods have not been restated.

The adoption of SFAS 123R increased the Company’s net loss for the twelve months ended December 31, 2007 and December 31, 2006 by $461,525 and $791,597 respectively. This expense increased the basic and diluted loss per share by $0.05 for the twelve months ended December 31, 2007 and $0.08 for the twelve months ended December 31, 2006. The Company did not recognize a tax benefit from stock-based compensation expense because the Company considers it is more likely than not that the related deferred tax assets, which have been reduced by a full valuation allowance, will not be realized.

The following illustrates the effect on net income and earnings per share if the fair value based method had been applied to the prior comparable period.

| | Twelve Months Ended

December 31, |

| | 2005 |

| | |

Reported net loss | $ | (602,025) |

Stock-based employee compensation under the fair value based method prior to adoption of SFAS 123R, net of related tax effects | | (244,360) |

| | |

Pro forma net loss | $ | (846,385) |

| | |

Loss per share: | | |

Basic – as reported | $ | (0.06) |

Basic – pro forma | $ | (0.09) |

Diluted – as reported | $ | (0.06) |

Diluted – pro forma | $ | (0.09) |

The Company recognized compensation expense of $461,525 and $791,597 for the twelve months ended December 31, 2007 and December 31, 2006 respectively for employee stock options that prior to January 1, 2006 would not have been recognized under APB 25. The following summarizes the activity of the Company’s stock options for the twelve months ended December 31, 2007:

48

| | | | | | Weighted | | |

| | | | Weighted | | Average | | |

| | | | Average | | Remaining | | Aggregate |

| | | | Exercise | | Contractual | | Intrinsic |

| | Shares | | Price | | Term | | Value (1) |

Number of shares under option: | | | | | | | | |

Outstanding at January 1, 2006 | | 510,000 | $ | 3.69 | | | | |

Granted | | 100,000 | | 6.25 | | | | |

Exercised | | (25,000) | | 1.80 | | | | |

Canceled or expired | | - | | - | | | | |

Outstanding at December 31, 2007 | | 635,000 | $ | 4.55 | | 6.65 | $ | 3,129,750 |

Exercisable at December 31, 2007 | | 585,000 | $ | 4.55 | | 6.65 | $ | 3,129,750 |

| (1) | The intrinsic value of a stock option is the amount by which the current market value of the underlying stock exceeds the exercise price of the option. |

As of December 31, 2007, there are no unvested stock options outstanding. As of December 31, 2007, there was no unrecognized compensation expense related to unvested stock options.

The fair value of each option grant was estimated on the date of grant using the Black-Scholes option-pricing model with the following weighted average assumptions used for options granted:

| | Dividend yield | | Expected volatility | | Risk-free interest rate | | Expected life (in years) | | Weighted- average fair value of option |

| | | | | |

| | | | | |

| | | | | |

| | | | | | | | | | |

Options granted in 2005 | | 0% | | 70% | | 4.05% | | 10 | | $1.95 |

Options granted in 2006 | | 0% | | 61% | | 5.03% | | 10 | | $6.33 |

Options granted in 2007 | | 0% | | 61% | | 4.75% | | 10 | | $4.62 |

The Company utilizes the asset and liability method of accounting for income taxes. Under the asset and liability method, deferred tax assets and liabilities are recognized for the future tax consequences attributable to differences between the financial statement carrying amounts and the tax basis of existing assets and liabilities using enacted tax rates expected to apply in the years in which such temporary differences are expected to be recovered or settled. Changes in tax rates are recognized in the period of the enactment date. A valuation allowance is recognized unless tax assets are more likely than not to be realized. Golden Cycle adopted FIN 48 on January 1, 2007 and it has not had an impact on its financial position, results of operations or cash flows. For more information see Notes to the Financial Statements, note 6, “Recently Issued Financial Accounting Standards”.

In 1998, the Company adopted SFAS No. 130, Reporting Comprehensive Income. SFAS No. 130 requires that all components of comprehensive income (loss), including net income (loss), be reported in the financial statements in the period they are recognized. Comprehensive income (loss) is defined as the change in equity during a period from transactions and other events and circumstances from non-owner sources. Net income

49

(loss) and other comprehensive income (loss), including foreign currency translation adjustments, shall be reported, net of their related tax effect, to arrive at comprehensive income (loss). We have recorded a ($42,000) decrease in the fair market value of Tornado common stock and disclosed comprehensive income (loss) in our consolidated financial statements at December 31, 2007.

The Company recognizes revenue as Minimum Annual Distributions from the Joint Venture are received as all services necessary for revenue recognition have been previously provided to the Joint Venture by the Company. The Joint Venture Agreement, as amended, provides for the Company to receive a minimum annual distribution of $250,000 during the Initial Phase (see Note 3). Beginning in 1994, such Minimum Annual Distributions are recoupable against the Company’s future share of Net Proceeds, if any. Whether future gold prices and the results of the Joint Venture’s operations will reach and maintain a level necessary to repay the Initial Loans (see Note 3), complete the Initial Phase, and thereafter generate net income from which Minimum Annual Distributions can be recouped, cannot be assured due to uncertainties inherent within any mining operation. Based on the amount of Initial Loans payable to the Manager and the uncertainty of future operating revenues, there is no assurance that the Company will receive more than the Minimum Annual Distribution from the Joint Venture in the foreseeable future.

Basic earnings (loss) per common share are computed as net income (loss) divided by the weighted average number of common shares outstanding during the period. Diluted earnings (loss) per common share are computed as net income (loss) divided by the weighted average number of common shares and potential common shares, using the treasury stock method, outstanding during the period.

(2) | Short-Term Investments |

The Company held certificates of deposit of approximately $285,000 and $380,000 at December 31, 2007 and 2006, respectively. All certificates of deposit held at December 31, 2007 mature within one year. Short-term investments also include 310 troy ounces of gold bullion purchased by the Company in 2002 at a cost of $102,859 and is carried at market value of $258,340 at December 31, 2007. The Company has reflected unrealized gains of $62,575, $35,650, and $24,986 for the years ended December 31, 2007, 2006 and 2005, respectively, in the consolidated statement of operations.

(3) | Investment in Mining Joint Venture |

The Company owns an interest in the Joint Venture with AngloGold Ashanti (Colorado) Corp. (AngloGold). AngloGold manages the Joint Venture. The Joint Venture conducts exploration, development, and mining of certain properties in the Cripple Creek Mining District, Teller County, Colorado. The Joint Venture owns or controls surface and/or mineral rights in the Cripple Creek Mining District, certain portions of which are being actively explored and developed.

The Joint Venture Agreement, as amended, generally requires AngloGold to finance operations and capital expenditures of the Joint Venture. The Joint Venture is currently operating in an Initial Phase. The Joint Venture Agreement defines an Initial Phase that will end when (i) the Initial Loans (defined below) have been repaid (ii) a cash reserve has been established to fund accrued reclamation and severance tax obligations, plus an amount approximating nine months of estimated operating costs, plus an amount approximating twelve months of estimated capital costs, and (iii) Net Proceeds (defined in the Joint Venture Agreement generally as gross revenues less costs) in the amount of $58 million have been distributed as follows: 80% to

50

AngloGold and 20% to the Company. After the Initial Phase, the Joint Venture will distribute metal in kind in the proportion of 67% to AngloGold and 33% to the Company. In addition, the Company will generally be entitled to receive, in each year during the Initial Phase or until the mining of ore by the Joint Venture ceases due to the exhaustion of economically recoverable reserves, whichever occurs first, an annual minimum distribution of $250,000 (a "Minimum Annual Distribution"). The first three Minimum Annual Distributions in 1991, 1992 and 1993 were not deemed to be a distribution of Net Proceeds to the Company and were not applied against the Company's share of any Net Proceeds. The Minimum Annual Distributions received on January 15, 1994 and thereafter constitute an advance on Net Proceeds and will be recouped against future shares of Net Proceeds to the Company. As of December 31, 2007, Initial Loans were approximately $310.8 million and no Net Proceeds have been distributed.

Whether future gold prices and the results of the Joint Venture’s operations will reach and maintain a level necessary to repay the Initial Loans, complete the Initial Phase, and thereafter generate net income cannot be assured due to uncertainties inherent within any mining operation. Based on the amount of Initial Loans payable to the manager and the uncertainty of future operating revenues, there is no assurance that the Company will receive more than the Minimum Annual Distribution from the Joint Venture in the foreseeable future.

The Company’s share of the Joint Venture net income, which has not been recorded in its consolidated financial statements, is approximately $11.8 million, $7.7 million and $1.9 million in 2007, 2006 and 2005, respectively. The Company’s accumulated unrecorded losses from the Joint Venture were $7.9 million as of December 31, 2006. As such, as of December 31, 2007, the Company’s accumulated unrecorded losses from the Joint Venture were eliminated and the Company recorded Joint Venture equity of $3.9 million. As of December 31, 2007 the receipt of cash distributions from the Joint Venture is highly uncertain as the Joint Venture’s Initial Loans totaling $310,823,000 have not been repaid nor is it anticipated they will be repaid in the foreseeable future based on anticipated future cash flows from the Joint Venture’s operations.

As a result, the Company has accounted for this uncertainty by creating a 100% valuation allowance against the Joint Venture equity interest of $3.9 million. It is anticipated by management that this valuation allowance against the Joint Venture equity will remain until it is determined by management that the collectibility of the investment in the form of future cash distributions becomes probable.

51

The condensed balance sheets of the Joint Venture as of December 31, 2007 and 2006 are summarized as follows:

| Assets | | 2007 | | 2006 |

| | | | (In thousands) | |

Current assets: | | | | |

| Cash and cash equivalents | $ | 1 | $ | 1 |

| Inventory | | 46,360 | | 42,615 |

| Other current assets | | - | | 1,037 |

| Prepaid expenses | | 766 | | - |

Total current assets | | 47,127 | | 43,653 |

| | | | | |

Property, plant, and equipment | | | | |

| Land and mineral properties | | 19,085 | | 27,768 |

| Mine development not currently being depleted | | 9,854 | | - |

| Structures and equipment | | 461,469 | | 438,378 |

| Construction - work-in-progress | | 595 | | 2,112 |

| | | 491,003 | | 468,258 |

| Accumulated depreciation, depletion, | | | | |

| and amortization | | (319,676) | | (292,151) |

Property, plant, and equipment, net | | 171,327 | | 176,107 |

Inventories | | 187,986 | | 148,761 |

Total assets | $ | 406,440 | $ | 368,521 |

| | | | | |

| Liabilities | | | | |

| | | | | |

Current liabilities | | | | |

| Accounts payable | $ | 9,951 | $ | 9,060 |

| Accrued liabilities | | 3,841 | | 3,494 |

| Current portion of capital lease obligations | | 2,670 | | 2,734 |

Total current liabilities | | 16,462 | | 15,288 |

| | | | | |

Loans payable to AngloGold Ashanti (Colorado) Corp. | | 310,823 | | 333,843 |

| | | | | |

Capital lease obligations | | 2,498 | | 5,168 |

| | | | | |

Asset retirement obligation | | 29,681 | | 24,029 |

Other long-term liabilities | | 8 | | 1,867 |

Venturers' equity: | | | | |

| Venturers' investments | | 60,062 | | 60,062 |

| Accumulated deficit | | (13,094) | | (71,736) |

Total venturers' equity (deficit) | | 46,968 | | (11,674) |

Total liabilities and venturers' equity | $ | 406,440 | $ | 368,521 |

52

The condensed statements of operations of the Joint Venture for each of the years in the three-year period ended December 31, 2007 are summarized as follows:

| | 2007 | | 2006 | | 2005 |

| | (In thousands) |

| | | | | | |

Revenue | $ | 194,848 | $ | 172,827 | $ | 145,347 |

Operating expenses | | | | | | |

Production costs | | 75,805 | | 70,437 | | 75,662 |

Depreciation, depletion, amortization, | | | | | | |

and reclamation | | 25,418 | | 26,454 | | 30,151 |

Accretion expense | | 1,769 | | 1,398 | | 1,113 |

| | 102,992 | | 98,289 | | 106,926 |

Mineral exploration expense | | - | | - | | 17 |

Total operating costs | | 102,992 | | 98,289 | | 106,943 |

| | | | | | |

Income from operations | | 91,856 | | 74,538 | | 38,404 |

Other Expenses: | | | | | | |

Interest expense | | (32,757) | | (34,408) | | (29,243) |

Other income (expense) | | (207) | | (1,738) | | 299 |

| | | | | | |

Net income | $ | 58,892 | $ | 38,392 | $ | 9,460 |

The tax effects of temporary differences that give rise to significant portions of the deferred tax assets at December 31, 2007 and 2006 are presented below:

| | | | | 2007 | | | 2006 |

Deferred tax assets: | | | | | | |

| Net operating loss carryforwards | | $ | 1,113,000 | | | 967,000 |

| Exploration expenditures | | | 11,000 | | | 145,000 |

| FAS 123R non-qualified | | | | | | |

| stock options | | | 464,000 | | | 293,000 |

| Other | | | - | | | 1,000 |

| | Total deferred tax assets | | | 1,588,000 | | | 1,406,000 |

| | | | | | | | |

Deferred tax liability: | | | | | | |

| Gold bullion mark to market | | | (96,000) | | | (73,000) |

| Tornado Stock- Mark to Market | | | 37,000 | | | - |

| | Total deferred tax assets | | | 1,529,000 | | | 1,333,000 |

| | | | | | | | |

Valuation allowance | | | (1,529,000) | | | (1,333,000) |

| | Net deferred tax assets | | $ | - | | | - |

53

A reconciliation of the statutory federal income tax rate to the effective tax rate follows:

| | | | 2007 | | 2006 |

Statutory federal | | | |

| income tax rate | 34.00% | | 34.00% |

| Effect of: | | | | |

| | State and local | | | |

| | | income taxes | 3.05% | | 3.05% |

| | Other - net | 0.21% | | 0.10% |

| | Change in valuation | | | |

| | | allowance | 36.84% | | 36.95% |

Effective tax rate | 0.00% | | 0.00% |

| | | | | | | |

At December 31, 2007, the Company has net operating loss carryforwards for income tax purposes of approximately $3,003,379 which expire beginning in 2008 through 2027.

The Company has not recorded an income tax benefit in 2007 or 2006 as it does not believe it is more likely than not that the benefit of the deferred tax assets will be realized in the future.

During 1992, the Company’s Board of Directors adopted a Directors’ Stock Option Plan (the Directors’ Plan) and a 1992 Stock Option Plan (the 1992 Plan). All options available under the Directors’ Plan were granted prior to December 31, 1994. During 1997, shareholders approved the 1997 Officers’ and Directors’ Stock Option Plan, and during 2002, shareholders approved the 2002 Stock Option Plan pursuant to which 1,000,000 and 625,000 shares, respectively, of the Corporation’s common stock were reserved for issuance pursuant to options to be granted. The 1992 Plan provided for the grant of options on a discretionary basis to certain employees and consultants. Under each plan, the exercise price cannot be less than the fair market value of the common stock on the date of the grant. The expiration of the options is ten years from the date of the grant.

During 2007, the Company granted 100,000 options to directors of the Corporation, and during 2006 and 2005 the Company granted 125,000 options each year to directors of the Corporation under the above plans.

Changes in stock options for each of the years in the three-year period ended December 31, 2007 are as follows:

54

| | | | Shares | | Option price per share | | Weighted average exercise price |

| | | | | |

| | | | | |

| | | | | | | | |

Outstanding and exercisable at | | | | | | |

| December 31, 2004 | | 410,000 | $ | 1.04 - 2.60 | | $1.92 |

| | Granted | | 125,000 | | 2.50 | | 2.50 |

| | Exercised | | (75,000) | | 1.04 - 1.50 | | 1.24 |

| | Expired | | (75,000) | | 2.33 - 2.60 | | 2.51 |

| | | | | | | | |

Outstanding and exercisable at | | | | | | |

| December 31, 2005 | | 385,000 | $ | 1.04 - 2.60 | | 2.13 |

| | Granted | | 125,000 | | 8.50 | | 8.50 |

| | | | | | | | |

Outstanding and exercisable at | | | | | | |

| December 31, 2006 | | 510,000 | $ | 1.04 - 8.50 | | 3.69 |

| | Granted | | 100,000 | | 6.25 | | 6.25 |

| | Exercised | | (25,000) | | 1.80 | | 1.80 |

| | | | | | | | |

Outstanding and exercisable at | | | | | | |

| December 31, 2007 | | 585,000 | $ | 1.04 - 8.50 | | $4.55 |

The weighted average remaining term of options outstanding was 6.65 and 6.81 years at December 31, 2007 and 2006, respectively.

(6) | Recently Issued Financial Accounting Standards: |

In December 2007, the FASB issued SFAS No. 141 (revised 2007), “Business Combinations” (“SFAS No. 141R”), which replaces FASB Statement No. 141. SFAS No. 141R establishes principles and requirements for how an acquirer recognizes and measures in its financial statements the identifiable assets acquired, the liabilities assumed, any non controlling interest in the acquiree and the goodwill acquired, and establishes that acquisition costs will be generally expensed as incurred. This statement also establishes disclosure requirements which will enable users to evaluate the nature and financial effects of the business combination. SFAS No. 141R is effective as of the beginning of an entity’s fiscal year that begins after December 15, 2008, which will be the Company’s year beginning January 1, 2009. The Company is currently evaluating the potential impact, if any, of the adoption of SFAS No. 141R on the Company’s financial statements.

In December 2007, the FASB issued SFAS No. 160, “Noncontrolling Interests in Consolidated Financial Statement-amendments of ARB No. 51” (“SFAS No. 160”). SFAS No. 160 states that accounting and reporting for minority interests will be recharacterized as noncontrolling interests and classified as a component of equity. The SFAS No. 160 also establishes reporting requirements that provide sufficient disclosures that clearly identify and distinguish between the interests of the parent and the interests of the noncontrolling owners. This statement is effective as of the beginning of an entity’s first fiscal year beginning after December 15, 2008, which corresponds to the Company’s year beginning January 1, 2009. The Company is currently evaluating the potential impact, if any, of the adoption of SFAS No. 160 on the Company’s financial statements.

In February 2007, the Financial Accounting Standards Board (“FASB”) issued Statement of Financial Accounting Standard No. 159, “The Fair Value Option For Financial Assets and Financial Liabilities” (SFAS No. 159). SFAS No. 159 permits entities to choose to measure many financial instruments and certain other items at fair value. The provisions of SFAS No. 159 are effective for Golden Cycle as of January 1, 2008. Golden Cycle has not yet determined

55

the impact of adopting SFAS No. 159 on its financial position, results of operations or cash flows.

In September 2006, the FASB issued Statement of Financial Accounting Standard No. 157 “Fair Value Measurements” (SFAS No. 157). SFAS No. 157 clarifies that fair value is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date in the most advantageous market for the asset or liability. SFAS No. 157 clarifies that the transaction to sell an asset or transfer a liability is a hypothetical transaction at a measurement date, considered from the perspective of a market participant that holds the asset or owes the liability. SFAS No. 157 states that fair value is a market-based measurement, not an entity specific measurement and that market assumptions should be based upon independent observations of the reporting entity over a reporting entity’s observations about market participant assumptions. SFAS No. 157 states that market participant assumptions should include risk, restrictions on asset sales, non-performance risk, but that quoted market prices for financial instruments should not be adjusted for the size of a position relative to trading volume (block discounts). SFAS No. 157 expands disclosures about, among other things, the use of fair value to measure assets and liabilities in interim and annual periods, including the use of unobservable inputs, and the effect of fair value on earnings and changes in net assets. SFAS No. 157 is effective for financial statements issued for fiscal years beginning after November 15, 2007, and interim periods within those fiscal years. Golden Cycle adopted SFAS No. 157 on January 1, 2007 and it has not had an impact on its financial position, results of operations or cash flows.

In June 2006, the FASB issued FASB Interpretation No. 48, “Accounting for uncertainty in Income Taxes,” (“FIN 48”) an interpretation of FASB Statement No. 109, “Accounting for Income Taxes.” FIN 48 prescribes a recognition threshold and measurement attribute for the financial statement recognition and measurement of a tax position taken or expected to be taken in a tax return. The interpretation requires that the entities recognize in the financial statements, the impact of a tax position, if that position is more likely than not of being sustained on audit, based on the technical merits of the position. FIN 48 also provides guidance on de-recognition, classification, interest and penalties, accounting in interim periods and disclosure. The provisions of FIN 48 are effective beginning January 1, 2007 with the cumulative effect of the change in accounting principle recorded as an adjustment to the opening balance of retained earnings. Golden Cycle adopted FIN 48 on January 1, 2007 and it has not had an impact on its financial position, results of operations or cash flows.

In February 2006, the FASB issued SFAS No. 155, “Accounting for Certain Hybrid Financial Instruments-an amendment of FASB Statements No. 133 and 140” (SFAS No. 155”). SFAS No. 155 resolves issues addressed in SFAS No. 133 Implementation Issue No. D1, “Application of Statement 133 to Beneficial Interest in Securitized Financial Assets.” SFAS No. 155 became effective January 1, 2007 and is applicable based upon the nature and extent of any new derivatives entered into after that date. Golden Cycle adopted SFAS No. 155 on January 1, 2007 and it has not had an impact on its financial position, results of operations or cash flows.

(7) | Commitments and Contingencies |

The Company, owner of a 33% interest in Cripple Creek & Victor Gold Company ("CC&V"), and the owner of the other 67% interest therein, AngloGold (Colorado) Corp., now AngloGold Ashanti (Colorado) Corp., and its direct parent AngloGold North America Inc., now AngloGold Ashanti North America Inc., were sued together with CC&V, the owner and operator of the Cresson Project, by the Sierra Club and Mineral Policy Center in 2001. The Plaintiffs asserted numerous violations of the U.S. Clean Water Act which went to trial in the United States District Court for the District of Colorado early in 2006, resulting in a judgment in favor of all Defendants and against all Plaintiffs on all claims, as well as an award of costs and attorneys

56

fees incurred after the point in time at which the Plaintiffs knew or should have known that their "dogged pursuit of factually unsupported claims" was unreasonable.

The Plaintiffs appealed both the judgment and the fee award to the United States Court of Appeals in Denver. Briefs were timely filed by the Plaintiffs in that court, but the parties reached an agreement to settle all disputes before the Defendants commenced briefing, and the cases have been dismissed. The settlement preserved the Defendants' complete success on all of the alleged violations of the Clean Water Act, and left each of the parties responsible for their own fees. So long as judicial review of the judgment and the monetary award remained possible, the Company did not record a receivable for any of its own fees, then approximately $130,000. The settlement eliminated the possibility of recovering any of the Company’s fees or costs.

| (b) | Illipah sale contingency |

Should Tornado Gold International Inc. (“Tornado Gold”) fail to complete the conditions of its purchase of the Illipah property, Golden Cycle may be entitled to full possession of the property and later market the property again. Tornado Gold is required to provide Golden Cycle a report of the completion of its first year’s (ending August 23, 2007) exploration program totaling more than $250,000 in exploration and development expenses. During the second twelve months of the contract which concludes August 23, 2008, Tornado is responsible for the minimum annual royalty payment and the Bureau of Land Management and County claim maintenance fees which it paid. Further, Tornado is required to expend an additional $500,000 in exploration and developments expenses on the Illipah property bringing the total required exploration and development expenditures to a total of $750,000 during the first two years. Tornado has not yet expended the required exploration funds in compliance with the agreement.

On January 11, 2008, the Company entered into an Agreement and Plan of Merger, dated January 11, 2008 (the “Agreement and Plan of Merger”), with AngloGold Ashanti Limited, a corporation organized under the laws of the Republic of South Africa, AngloGold Ashanti USA Incorporated, a Delaware corporation, and GCGC LLC, a Colorado limited liability company and a direct wholly-owned subsidiary of AngloGold Ashanti USA Incorporated. Under the terms of the Agreement and Plan of Merger, the Company agreed to be acquired by AngloGold Ashanti through a transaction in which the Company’s shareholders will receive consideration consisting of 0.29 American Depositary Shares (“ADS”) of AngloGold Ashanti Limited for each issued and outstanding share of the Company’s common stock, rounded up to the next whole ADS, each whole ADS representing one ordinary share, par value 25 South African cents per share, of AngloGold Ashanti Limited. The Agreement is subject to the approval of two-thirds of the Company’s shareholders entitled to vote.

For a description of the terms and conditions of the Agreement and Plan of Merger and the contemplated transaction, see the disclosure under Item 12 “Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters – Changes in Control.”

57

(9) Selected quarterly financial data

(unaudited)

| | | | | 2007 | | | |

| | First Quarter | | Second Quarter | | Third Quarter | | Fourth Quarter |

| | | | |

Distributions from mining | | | | | | | | |

joint venture in excess | | | | | | | | |

of carrying value (note 4) | $ | 250,000 | $ | - | $ | - | $ | - |

| | | | | | | | |

Operating income (loss) | | 130,877 | | (605,471) | | (86,419) | | (193,569) |

| | | | | | | | |

Other income | | 73,758 | | 4,796 | | 33,488 | | 54,140 |

| | | | | | | | |

Net income (loss) | | 204,635 | | (600,675) | | (52,931) | | (139,429) |

Net income (loss) per share | | 0.02 | | (0.06) | | (0.01) | | (0.01) |

Pro forma net income (loss) | | | | | | | | |

per share | | 0.02 | | (0.06) | | (0.01) | | (0.01) |

| | | | | | | | |

| | | | | | | | |

| | | | | 2006 | | | |

| | First Quarter | | Second Quarter | | Third Quarter | | Fourth Quarter |

| | | | |

Distributions from mining | | | | | | | | |

joint venture in excess | | | | | | | | |

of carrying value (note 4) | $ | 250,000 | $ | - | $ | - | $ | - |

| | | | | | | | |

Operating income (loss) | | 40,243 | | (1,071,681) | | (82,557) | | (149,577) |

| | | | | | | | |

Net income (loss) | | 66,701 | | (1,053,636) | | (77,874) | | (32,326) |

Net income (loss) per share | | 0.01 | | (0.11) | | (0.01) | | (0.00) |

Pro forma net income (loss) | | | | | | | | |

per share | | 0.01 | | (0.11) | | (0.01) | | (0.00) |

| | | | | | | | |

| | | | | | | | |

| | | | | 2005 | | | |

| | First Quarter | | Second Quarter | | Third Quarter | | Fourth Quarter |

| | | | |

Distributions from mining | | | | | | | | |

joint venture in excess | | | | | | | | |

of carrying value (note 4) | $ | 250,000 | $ | - | $ | - | $ | - |

| | | | | | | | |

Operating income (loss) | | 138,885 | | (164,566) | | (322,861) | | (314,136) |

| | | | | | | | |

Net income (loss) | | 146,486 | | (154,505) | | (313,041) | | (280,965) |

Net income (loss) per share | | 0.02 | | (0.02) | | (0.03) | | (0.03) |

Pro forma net income (loss) | | | | | | | | |

per share | | 0.02 | | (0.04) | | (0.03) | | (0.03) |

58