UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| [X] | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| | For the fiscal year ended December 31, 2009 |

or

| [ ] | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission File Number 1-7297

NICOR INC.

(Exact name of registrant as specified in its charter)

| Illinois | | 36-2855175 |

| (State of Incorporation) | | (I.R.S. Employer Identification No.) |

| | | |

| 1844 Ferry Road | | |

| Naperville, Illinois 60563-9600 | | (630) 305-9500 |

| (Address of principal executive offices) (Zip Code) | | (Registrant’s telephone number, including area code) |

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | | Name of each exchange on which registered |

| Common Stock, par value $2.50 per share | | New York Stock Exchange |

| | | Chicago Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes [X] No [ ]

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes [ ] No [X]

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months, and (2) has been subject to such filing requirements for the past 90 days. Yes [ X ] No [ ]

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months. Yes [ ] No [ ]

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer [X] | Accelerated filer [ ] |

| | |

| Non-accelerated filer [ ] | Smaller reporting company [ ] |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes [ ] No [X]

The aggregate market value of common stock (based on the June 30, 2009 closing price of $34.62) held by non-affiliates of the registrant was approximately $1.5 billion. As of February 17, 2010, there were 45,245,188 shares of common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the company’s 2010 Annual Meeting Definitive Proxy Statement, to be filed on or about March 10, 2010, are incorporated by reference into Part III.

Nicor Inc.

| |

| | | |

| Item No. | Description | Page No. |

| | | |

| | | ii |

| | | |

| | Part I | |

| 1. | | 1 |

| 1A. | | 7 |

| 1B. | | 13 |

| 2. | | 13 |

| 3. | | 13 |

| 4. | | 13 |

| | | 14 |

| | | |

| | Part II | |

| 5. | | 15 |

| 6. | | 17 |

| 7. | | 18 |

| 7A. | | 38 |

| 8. | | 40 |

| 9. | | 76 |

| 9A. | | 76 |

| 9B. | | 77 |

| | | |

| | Part III | |

| 10. | | 78 |

| 11. | | 78 |

| 12. | | 78 |

| 13. | | 79 |

| 14. | | 79 |

| | | |

| | Part IV | |

| 15. | | 80 |

| | | 82 |

| | | 83 |

Nicor Inc.

ALJs. Administrative Law Judges.

ARO. Asset retirement obligation.

Central Valley. Central Valley Gas Storage, L.L.C., a wholly owned business that is developing a natural gas storage facility in the Sacramento River valley of north-central California.

Chicago Hub. A venture of Nicor Gas, which provides natural gas storage and transmission-related services to marketers and other gas distribution companies.

Degree day. The extent to which the daily average temperature falls below 65 degrees Fahrenheit. Normal weather for Nicor Gas’ service territory, for purposes of this report, is considered to be 5,600 degree days per year for 2009 and 5,830 degree days per year for 2008 and 2007.

EN Engineering. EN Engineering, L.L.C., a previously owned joint venture that provides engineering and consulting services. Nicor sold its ownership on March 31, 2009.

FERC. Federal Energy Regulatory Commission, the agency that regulates the interstate transportation of natural gas, oil and electricity.

Horizon Pipeline. Horizon Pipeline Company, L.L.C., a 50-percent-owned joint venture that operates an interstate regulated natural gas pipeline of approximately 70 miles, stretching from Joliet, Illinois to near the Wisconsin/Illinois border.

ICC. Illinois Commerce Commission, the agency that establishes the rules and regulations governing utility rates and services in Illinois.

IDR. Illinois Department of Revenue.

IRS. Internal Revenue Service.

Jobs Act. American Jobs Creation Act of 2004.

LIFO. Last-in, first-out.

Mcf, MMcf, Bcf. Thousand cubic feet, million cubic feet, billion cubic feet.

Nicor. Nicor Inc., or the registrant.

Nicor Advanced Energy. Prairie Point Energy, L.L.C. (doing business as Nicor Advanced Energy), a wholly owned business that provides natural gas and related services on an unregulated basis to residential and small commercial customers.

Nicor Enerchange. Nicor Enerchange, L.L.C., a wholly owned business that engages in wholesale marketing of natural gas supply services primarily in the Midwest, administers the Chicago Hub for Nicor Gas, serves commercial and industrial customers in the Chicago market area, and manages Nicor Solutions’ and Nicor Advanced Energy’s product risks, including the purchase of natural gas supplies.

Nicor Gas. Northern Illinois Gas Company (doing business as Nicor Gas Company) is a regulated wholly owned public utility business and one of the nation’s largest distributors of natural gas.

Nicor Services. Nicor Energy Services Company, a wholly owned business that provides customer move connection services for utilities and product warranty contracts, heating, ventilation and air conditioning repair, maintenance and installation services and equipment to retail markets, including residential and small commercial customers.

Nicor Solutions. Nicor Solutions, L.L.C., a wholly owned business that offers residential and small commercial customers energy-related products that provide for natural gas cost stability and management of their utility bill.

NYMEX. New York Mercantile Exchange.

PBR. Performance-based rate, a regulatory plan which ended on January 1, 2003, that provided economic incentives based on natural gas cost performance.

PCBs. Polychlorinated Biphenyls.

PGA. Purchased Gas Adjustment, a rate rider that passes natural gas costs directly through to customers without markup, subject to ICC review.

Rider. A rate adjustment mechanism that is part of a utility’s tariff which authorizes it to provide specific services or assess specific charges.

SEC. The United States Securities and Exchange Commission.

TEL. Tropic Equipment Leasing, Inc., a wholly owned subsidiary of Nicor, holds the company’s interest in Triton.

TEU. Twenty-foot equivalent unit, a measure of volume in containerized shipping equal to one 20-foot-long container.

Triton. Triton Container Investments L.L.C., a cargo container leasing company in which Nicor Inc. has an investment.

Tropical Shipping. A wholly owned business and a carrier of containerized freight in the Bahamas and the Caribbean region.

U.S. United States of America.

PART I

Nicor, an Illinois corporation formed in 1976, is a holding company. Gas distribution is Nicor’s primary business. Nicor’s major subsidiaries include Nicor Gas, one of the nation’s largest distributors of natural gas, and Tropical Shipping, a transporter of containerized freight in the Bahamas and the Caribbean region. Nicor also owns several energy-related ventures, including Nicor Services, Nicor Solutions and Nicor Advanced Energy, which provide energy-related products and services to retail markets, and Nicor Enerchange, a wholesale natural gas marketing company. As a consolidated group, Nicor had approximately 3,900 employees at year-end 2009.

Summary financial information for Nicor’s major businesses is included in Item 8 – Notes to the Consolidated Financial Statements – Note 15 – Business Segment and Geographic Information. The following sections describe Nicor’s larger businesses. Certain terms used herein are defined in the glossary on pages ii and iii.

GAS DISTRIBUTION

General

Nicor Gas, a regulated natural gas distribution utility, serves 2.2 million customers in a service territory that encompasses most of the northern third of Illinois, excluding the city of Chicago. The company’s service territory is diverse, providing the company with a well-balanced mix of residential, commercial and industrial customers. Residential customers typically account for approximately 50 percent of natural gas deliveries, while commercial and industrial customers each typically account for approximately 25 percent. See Gas Distribution Statistics on page 26 for operating revenues, deliveries and number of customers by customer classification. Nicor Gas had approximately 2,200 employees at year-end 2009.

Nicor Gas maintains franchise agreements with most of the incorporated municipalities it serves, allowing it to construct, operate and maintain distribution facilities in those incorporated municipalities. Franchise agreement terms range up to 50 years. Currently, about one-third of the agreements will expire within five years.

Customers have the option of purchasing their own natural gas supplies, with delivery of the gas by Nicor Gas. The larger of these transportation customers also have options that include the use of Nicor Gas’ storage system and the ability to choose varying supply backup levels. The choice of transportation service as compared to natural gas sales service results in less revenue for Nicor Gas but has no direct impact on net operating results. Nicor Gas continues to deliver natural gas, maintain its distribution system and respond to emergencies.

Nicor Gas also operates the Chicago Hub, which provides natural gas storage and transmission-related services to marketers and other gas distribution companies. The Chicago area is a major market hub for natural gas, and demand exists for storage and transmission-related services by marketers, other gas distribution companies and electric power-generation facilities. Nicor Gas’ Chicago Hub addresses that demand. Chicago Hub revenues are passed directly through to customers as a credit to Nicor Gas’ PGA rider.

Sources of Natural Gas Supply

Nicor Gas purchases natural gas supplies in the open market by contracting with producers and marketers. It also purchases transportation and storage services from interstate pipelines that are regulated by the FERC. When firm pipeline services are temporarily not needed, Nicor Gas may release the services in the secondary market under FERC-mandated capacity release provisions, with proceeds reducing the cost of natural gas charged to customers.

Peak-use requirements are met through utilization of company-owned storage facilities, pipeline transportation capacity, purchased storage services and other supply sources, arranged by either Nicor Gas or its transportation customers. Nicor Gas has been able to obtain sufficient supplies of natural gas to meet customer requirements. The company believes natural gas supply and pipeline capacity will be sufficiently available to meet market demands in the foreseeable future.

Natural gas supply. Nicor Gas maintains a diversified portfolio of natural gas supply contracts. Supply purchases are diversified by supplier, producing region, quantity, credit limits and available transportation. Natural gas supply pricing is generally tied to published price indices so as to approximate current market prices. These supply contracts also may require the payment of fixed demand charges to ensure the availability of supplies on any given day. The company also purchases natural gas supplies on the spot market to fulfill its supply requirements or to take advantage of favorable short-term pricing.

As part of its purchasing practices, Nicor Gas maintains a price risk hedging strategy to reduce the risk of price volatility. A disciplined approach is used to systematically forward hedge a predetermined portion of forecasted monthly volumes.

As noted previously, transportation customers purchase their own natural gas supplies. About one-half of the natural gas that the company delivers is purchased by transportation customers directly from producers and marketers.

Pipeline transportation. The Nicor Gas distribution and storage system is directly connected to eight interstate pipelines. This provides the company with direct access to most of the major natural gas producing regions in North America. The company has long-term transportation contracts with nearly all of these interstate pipelines and generally has a right-of-first-refusal for contract extensions. The largest of these long-term transportation contracts is with Natural Gas Pipeline Company of America (“NGPL”) which provides approximately 70 percent of the firm transportation capacity. In addition, Nicor Gas enters into short-term winter-only transportation contracts and market-area transportation contracts that enhance Nicor Gas’ operational flexibility.

Storage. Nicor Gas owns and operates eight underground natural gas storage facilities. This storage system is one of the largest in the gas distribution industry. The storage reservoirs provide a total inventory capacity of about 150 Bcf, approximately 135 Bcf of which can be cycled on an annual basis. The system is designed to meet about 50 percent of the company’s estimated peak-day deliveries and approximately 40 percent of its normal winter deliveries. In addition to company-owned facilities, Nicor Gas has about 40 Bcf of purchased storage services under contracts with NGPL that expire in 2012 and 2013. This level of storage capability provides Nicor Gas with supply flexibility, improves the reliability of deliveries, and can mitigate the risk associated with seasonal price movements.

Competition/Demand

Nicor Gas is the largest natural gas distributor in Illinois and is regulated by the ICC. The company is the sole distributor of natural gas in essentially all of its service territory. Substantially all single-family homes in Nicor Gas’ service territory are heated with natural gas. In the commercial and industrial markets, the company’s natural gas services compete with other forms of energy, such as electricity, coal, propane and oil, based on such factors as price, service, reliability and environmental impact. In addition, the company has a tariff that allows negotiation with potential bypass customers. Nicor Gas also offers commercial and industrial customers alternatives in rates and service, increasing its ability to compete in these markets. Other significant factors that impact demand for natural gas include weather, conservation and economic conditions.

Natural gas deliveries are temperature-sensitive and seasonal since about one-half of all deliveries are used for space heating. Typically, about three-quarters of the deliveries and revenues occur from October through March. Fluctuations in weather have the potential to significantly impact year-to-year comparisons of operating income and cash flow. It is estimated that a 100 degree-day variation from normal weather impacts Nicor Gas’ distribution margin, net of income taxes, by approximately $1.3 million under the company’s current rate structure.

The effect of weather variations on Nicor Gas’ results is offset, in part, due to weather risks within the consolidated Nicor group related to the utility-bill management products marketed by Nicor Solutions and Nicor Advanced Energy. The amount of this offset has approximated 30 percent to 65 percent and will vary depending upon the time of year, weather patterns, the number of customers for these products and the market price for natural gas.

Nicor Gas’ large residential customer base provides for a relatively stable level of natural gas deliveries during weak economic conditions. The company’s industrial and commercial customer base is well diversified, lessening the impact of industry-specific economic swings. However, during periods of high natural gas prices, deliveries of natural gas can be negatively affected by conservation and the use of alternative energy sources.

Regulation

Nicor Gas is regulated by the ICC, which governs utility rates and services in Illinois. Those ICC orders and regulations that may significantly affect business performance include the following:

| · | Base rates, which are set by the ICC, are designed to allow the company an opportunity to recover its costs and earn a fair return for investors. On March 25, 2009, the ICC issued an order approving an increase in Nicor Gas’ base revenues of approximately $69 million, a rate of return on rate base of 7.58 percent and a rate of return on equity of 10.17 percent. On October 7, 2009, the ICC increased the annual base revenues approved for Nicor Gas in the March 25, 2009 order by approximately $11 million as a result of a rehearing decision and increased the rate of return on rate base to 8.09 percent. Therefore, the total annual base revenue increase resulting from these ICC orders is approximately $80 million. For additional information about the rate proceeding, see Item 7 – Management’s Discussion and Analysis of Financial Condition and Results of Operations and Item 8 – Notes to the Consolidated Financial Statements – Note 19 – Regulatory Proceedings. |

| · | The company’s ICC-approved tariffs provide that the cost of natural gas purchased for customers will be fully charged to customers without markup. Therefore, the company does not profit from the sale of natural gas. Rather, the company earns income from fixed monthly charges and from variable transportation charges for delivering natural gas to customers. Annually, the ICC initiates a review of the company’s natural gas purchasing practices for prudence, and may disallow the pass-through of costs considered imprudent. The annual prudence reviews for calendar years 1999-2009 are open for review. |

| · | As with the cost of natural gas, the company has ICC-approved tariffs that provide for the pass-through of prudently incurred environmental costs (related to the remediation of former manufactured gas plant sites) and, effective in 2009, franchise gas costs and costs associated with an energy efficiency program. These costs are also subject to annual ICC review. |

| · | On February 2, 2010, the ICC approved a bad debt rider that was filed for in 2009. The bad debt rider provides for the recovery from (or refund to) customers of the difference between the actual bad debt expense Nicor Gas incurs on an annual basis and the benchmark bad debt expense included in its base rates for the respective year. For additional information about the bad debt rider, see Item 7 – Management’s Discussion and Analysis of Financial Condition and Results of Operations and Item 8 – Notes to the Consolidated Financial Statements – Note 19 – Regulatory Proceedings. |

Nicor Gas enters into various service agreements with Nicor and its affiliates. Nicor Gas, to the extent required, obtains ICC approvals for these agreements.

The ICC has other rules that impact the operations of utilities in Illinois.

A PBR plan for natural gas costs went into effect in 2000 and was terminated by the company effective January 1, 2003. Under the PBR plan, Nicor Gas’ total natural gas supply costs were compared to a market-sensitive benchmark. Savings and losses relative to the benchmark were determined annually and shared equally with sales customers. The results of the PBR plan are currently under ICC review. Additional information on the plan and the ICC review are presented in Item 8 – Notes to the Consolidated Financial Statements – Note 21 – Contingencies – PBR Plan.

Gas distribution, transmission and storage system, and other properties

The gas distribution, transmission and storage system includes approximately 34,000 miles of steel, plastic and cast iron main; approximately 2.0 million steel, plastic/aluminum composite, plastic and copper services connecting the mains to customers’ premises; and eight underground storage fields. Other properties include buildings, land, motor vehicles, meters, regulators, compressors, construction equipment, tools, communication and computer equipment, software and office equipment.

Most of the company’s distribution and transmission property, and underground storage fields are located on property owned by others and used by the company through easements, permits or licenses. The company owns most of the buildings housing its administrative offices and the land on which they sit.

Substantially all gas distribution properties are subject to the lien of the indenture securing Nicor Gas’ First Mortgage Bonds.

Additional information about Nicor Gas’ business is presented in Item 1A – Risk Factors, Item 7 – Management’s Discussion and Analysis of Financial Condition and Results of Operations and Item 8 – Notes to the Consolidated Financial Statements.

SHIPPING

Tropical Shipping is a transporter of containerized freight in the Bahamas and the Caribbean, a region generally characterized by modest market growth and intense competition. The company is a major carrier of exports from the east coast of the United States and Canada to these regions. The company’s shipments consist primarily of southbound cargo such as building materials, food and other necessities for developers, manufacturers and residents in the Caribbean and the Bahamas, as well as tourist-related shipments intended for use in hotels and resorts, and on cruise ships. The balance of Tropical Shipping’s cargo consists primarily of interisland shipments and northbound shipments of apparel and agricultural products. Other related services such as inland transportation and cargo insurance are also provided by Tropical Shipping or other Nicor subsidiaries.

At December 31, 2009, Tropical Shipping’s operating fleet consisted of 11 owned vessels and 4 chartered vessels with a container capacity totaling approximately 5,270 TEUs. In addition to the vessels, the company owns and/or leases containers, container-handling equipment, chassis and other equipment. Real property, more than half of which is leased, includes office buildings, cargo handling facilities and warehouses located in the United States, Canada and some of the ports served.

Additional information about Tropical Shipping’s business is presented in Item 1A – Risk Factors, Item 7 – Management’s Discussion and Analysis of Financial Condition and Results of Operations and Item 8 – Notes to the Consolidated Financial Statements.

OTHER ENERGY VENTURES

Nicor owns several energy-related ventures, including three companies marketing energy-related products and services and a wholesale natural gas marketing company. Nicor is also developing natural gas storage facilities and owns an interest in an interstate natural gas pipeline.

Nicor Services, Nicor Solutions and Nicor Advanced Energy are businesses that provide energy-related products and services to retail markets, including residential and small commercial customers. Nicor Services operates primarily in northern Illinois and provides warranty and maintenance contracts, as well as repair and installation services of heating, air conditioning and indoor air-quality equipment, and customer move connection services for utilities. In conjunction with national expansion efforts, Nicor Services began doing business under the Nicor National brand in 2009. Nicor Solutions offers its residential and small commercial customers, primarily in the Nicor Gas service territory, energy-related products that provide for natural gas price stability and management of their utility bill. These products mitigate and/or eliminate the risks to customers of colder than normal weather and/or changes in natural gas prices. Nicor Advanced Energy is certified by the ICC as an Alternate Gas Supplier, authorizing it to be a non-utility marketer of natural gas for residential and small commercial customers. Nicor Advanced Energy presently operates in northern Illinois, offering customers an alternative to the utility as its natural gas supplier.

Nicor Enerchange is a business that engages in wholesale marketing of natural gas supply services primarily in the Midwest, administers the Chicago Hub for Nicor Gas, serves commercial and industrial customers in the Chicago market area, and manages Nicor Solutions’ and Nicor Advanced Energy’s product risks, including the purchases of natural gas supplies.

Central Valley is developing a natural gas storage facility in the Sacramento River valley of north-central California and plans to provide approximately 10 Bcf of working natural gas capacity, offering flexible, high-deliverability multi-cycle services and interconnection to regional pipelines. Central Valley currently expects to begin injections of natural gas starting in 2010 and to begin to offer initial service in 2012. Nicor also is evaluating the development of other natural gas storage facilities in the United States.

Horizon Pipeline, a 50-percent-owned joint venture with NGPL, operates a natural gas pipeline of approximately 70 miles, stretching from Joliet, Illinois to near the Wisconsin/Illinois border. Nicor Gas has contracted for approximately 80 percent of Horizon Pipeline’s capacity under an agreement expiring in 2012 at rates that have been accepted by FERC.

EN Engineering, a previously-owned joint venture between Nicor and A. Epstein & Sons International, is an engineering and consulting firm that specializes in the design, installation and maintenance of natural gas, petroleum and liquid pipeline facilities. EN Engineering provides engineering and corrosion services to Nicor Gas. Nicor sold its ownership on March 31, 2009.

Additional information about Nicor’s other energy ventures is presented in Item 1A – Risk Factors, Item 7 – Management’s Discussion and Analysis of Financial Condition and Results of Operations and Item 8 – Notes to the Consolidated Financial Statements.

CORPORATE

Nicor has equity investments in a cargo container leasing business and certain affordable housing investments. Additional information on Nicor’s equity investments are presented in Item 8 – Notes to the Consolidated Financial Statements – Note 16 – Equity Investment Income, Net.

AVAILABLE INFORMATION

Nicor files various reports with the SEC. These reports include the annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13 (a) of the Securities Exchange Act of 1934. Nicor makes all of these reports available without charge to the public on the investor section of the company’s Internet site at www.nicor.com as soon as reasonably practicable after Nicor files them with, or furnishes them to, the SEC.

The following factors are the most significant factors that can impact year-to-year comparisons and may affect the future performance of the company’s businesses. New risks may emerge and management cannot predict those risks or estimate the extent to which they may affect the company’s financial performance.

Regulation of Nicor Gas, including changes in the regulatory environment in general, may adversely affect the company’s results of operations, cash flows and financial condition.

Nicor Gas is regulated by the ICC, which has general regulatory power over practically all phases of the public utility business in Illinois, including rates and charges, issuance of securities, services and facilities, system of accounts, investments, safety standards, transactions with affiliated interests and other matters.

Nicor Gas is permitted by the ICC’s PGA regulation to adjust the charge to its sales customers on a monthly basis to recover the company’s prudently incurred actual costs to acquire the natural gas it delivers to them. The company’s gas costs are subject to subsequent prudence reviews by the ICC for which the company makes annual filings. The annual prudence reviews for calendar years 1999-2009 are open for review and any disallowance of costs in those proceedings could adversely affect Nicor Gas’ results of operations, cash flows and financial condition.

Additionally, Nicor Gas is permitted by ICC regulations to periodically adjust the charge to its customers to recover the company’s prudently incurred actual costs associated with environmental remediation at former manufactured gas plant sites, franchise payments to municipalities, energy efficiency programs and, as approved in February 2010, bad debt expense. These charges are subject to subsequent prudence reviews by the ICC and any disallowance of costs by the ICC could adversely affect Nicor Gas’ results of operations, cash flows and financial condition.

Most of Nicor Gas’ other charges are changed only through a rate case proceeding with the ICC. The charges established in a rate case proceeding are based on an approved level of operating costs and investment in utility property and are designed to allow the company an opportunity to recover those costs and to earn a fair return on that investment based upon an estimated volume of annual natural gas deliveries. To the extent Nicor Gas’ actual costs to provide utility service are higher than the levels approved by the ICC, or its actual natural gas deliveries are less than the annual volume estimated by the ICC, Nicor Gas’ results of operations, cash flows and financial condition could be adversely affected until such time as it files for and obtains ICC approval for new charges through a rate case proceeding.

Nicor Gas is subject to rules and regulations pertaining to the integrity of its distribution system and environmental compliance. The company’s results of operations, cash flows and financial condition could be adversely affected by any additional laws or regulations that are enacted that require significant increases in the amount of expenditures for system integrity and environmental compliance.

The ICC has other rules that impact the operations of utilities in Illinois. Changes in these rules could impact the company’s results of operations, cash flows and financial condition.

Nicor Gas enters into various service agreements with Nicor and its affiliates. Nicor Gas obtains the required ICC approvals for these agreements. The company’s results of operations, cash flows and financial condition could be adversely affected if, as a result of a change in law or action by the ICC, new restrictions are imposed that limit or prohibit certain service agreements between Nicor Gas and its affiliates.

A change in the ICC’s approved rate mechanism for recovery of environmental remediation costs at former manufactured gas plant sites, or adverse decisions with respect to the prudence of costs actually incurred, could adversely affect the company’s results of operations, cash flows and financial condition.

Current environmental laws may require the cleanup of coal tar at certain former manufactured gas plant sites for which the company may in part be responsible. Management believes that any such costs that are not recoverable from other entities or from insurance carriers are recoverable through rates for utility services under an ICC-approved mechanism for the recovery of prudently incurred costs. A change in this rate recovery mechanism, however, or a decision by the ICC that some or all of these costs were not prudently incurred, could adversely affect the company’s results of operations, cash flows and financial condition.

An adverse decision in the proceeding concerning Nicor Gas’ PBR plan could result in a refund obligation which could adversely affect the company’s results of operations, cash flows and financial condition.

In 2000, Nicor Gas instituted a PBR plan for natural gas costs. Under the PBR plan, Nicor Gas’ total gas supply costs were compared to a market-sensitive benchmark. Savings and losses relative to the benchmark were determined annually and shared equally with sales customers. The PBR plan was terminated effective January 1, 2003. There are allegations that Nicor Gas acted improperly in connection with the PBR plan, and the ICC is reviewing these allegations in a pending proceeding. An adverse decision in this proceeding could result in a refund to ratepayers or other obligations which could adversely affect the company’s results of operations, cash flows and financial condition.

Nicor Gas relies on direct connections to eight interstate pipelines and extensive underground storage capacity. If these pipelines or storage facilities were unable to deliver natural gas for any reason it could impair Nicor Gas’ ability to meet its customers’ full requirements which could adversely affect the company’s results of operations, cash flows and financial condition.

Nicor Gas meets its customers’ peak day, seasonal and annual gas requirements through deliveries of natural gas transported on interstate pipelines, with which it or its natural gas suppliers have contracts, and through withdrawals of natural gas from storage fields it owns or leases. Nicor Gas contracts with multiple pipelines for transportation services. If a pipeline were to fail to perform transportation or storage service, including as a result of war, acts or threats of terrorism, mechanical problems or natural disaster, on a peak day or other day with high volume gas requirements, Nicor Gas’ ability to meet all of its customers’ natural gas requirements may be impaired unless or until alternative arrangements for delivery of supply were put in place. Likewise, if a storage field owned by Nicor Gas, or a principal Nicor Gas-owned transmission or distribution pipeline used to deliver natural gas to the market, were to be out of service for any reason, including as a result of war, acts or threats of terrorism, mechanical problems or natural disaster, this could impair Nicor Gas’ ability to meet its customers’ full requirements which could adversely affect the company’s results of operations, cash flows and financial condition.

Fluctuations in weather, economic conditions and use of alternative fuel sources have the potential to adversely affect the company’s results of operations, cash flows and financial condition.

When weather conditions are milder than normal, Nicor Gas has historically delivered less natural gas, and consequently may earn less income. Nicor Gas’ natural gas deliveries are temperature-sensitive and seasonal since about one-half of all deliveries are used for space heating. Typically, about three-quarters of the deliveries and revenues occur from October through March. Mild weather in the future could adversely affect the company’s results of operations, cash flows and financial condition. In addition, factors including, but not limited to, conservation, economic conditions and the use of alternative fuel sources could also result in lower customer demand.

Conversely, results from products sold by Nicor Solutions and Nicor Advanced Energy generally benefit from milder than normal weather. Nicor Solutions and Nicor Advanced Energy offer utility-bill management products that mitigate and/or eliminate the risks to customers of variations in weather. Benefits or costs related to these products resulting from variances from normal weather are recorded primarily at the corporate level as a result of an agreement between the parent company and certain of its subsidiaries. To the extent weather is colder than normal in the future, Nicor Solutions and Nicor Advanced Energy’s results of operations, cash flows and financial condition could be adversely affected.

Conservation could adversely affect the company's results of operations, cash flows and financial condition.

As a result of recent legislative and regulatory initiatives, the company is putting in place programs to promote additional energy efficiency by its customers. Funding for such programs will be recovered through a cost recovery rider. However, the adverse impact of lower deliveries and resulting reduced margin could adversely affect the company's results of operations, cash flows and financial condition until such time as it files for and obtains ICC approval for new charges through a rate case proceeding.

Possible legislation or regulation intended to address concerns about climate change could adversely affect the company’s results of operations, cash flows and financial condition.

Governmental agencies are evaluating changes in laws to address concerns about the possible effects of greenhouse gas emissions on climate. Among other things, future laws may mandate reductions in future emissions by the company and its customers. If enacted, such laws could require the company to reduce emissions and to incur compliance costs that could adversely affect the company’s results of operations, cash flows and financial condition.

Natural gas commodity price changes may affect the operating costs and competitive positions of the company’s businesses which could adversely affect its results of operations, cash flows and financial condition.

Nicor’s energy-related businesses are sensitive to changes in natural gas prices. Natural gas prices historically have been volatile and may continue to be volatile in the future. Prices for natural gas are subject to a variety of factors that are beyond Nicor’s control. These factors include, but are not limited to, the level of consumer demand for, and the supply of, natural gas, processing, gathering and transportation availability, the level of imports of, and the price of foreign natural gas, the price and availability of alternative fuel sources, weather conditions, natural disasters and political conditions or hostilities in natural gas producing regions.

Any changes in natural gas prices could affect the prices Nicor’s energy-related businesses charge, operating costs and the competitive position of products and services. In accordance with the ICC’s PGA regulations, Nicor Gas adjusts its gas cost charges to sales customers on a monthly basis to account for changes in the price of natural gas. However, changes in natural gas prices can also impact certain operating and financing costs that can only be reflected in Nicor Gas’ charges to customers if approved by the ICC in a rate case. Increases in natural gas prices can also have an adverse effect on natural gas distribution margin because such increases can result in lower customer demand.

Nicor’s other energy businesses are also subject to natural gas commodity price risk, arising primarily from fixed-price purchase and sale agreements, natural gas inventories and utility-bill management arrangements. Derivative instruments such as futures, options, forwards and swaps may be used to hedge these risks.

Nicor’s use of derivative instruments could adversely affect the company’s results of operations, cash flows and financial condition.

Nicor uses derivative instruments, including futures, options, forwards and swaps, either traded on exchanges or executed over-the-counter with natural gas merchants as well as financial institutions, to hedge natural gas price risk. Fluctuating natural gas prices cause earnings and financing costs of Nicor to be impacted. The use of derivative instruments that are not perfectly matched to the exposure could adversely affect the company’s results of operations, cash flows and financial condition. Also, when Nicor’s derivative instruments do not qualify for hedge accounting treatment or for which hedge accounting is not elected, the company’s results of operations, cash flows and financial condition could be adversely affected.

Nicor is subject to margin requirements in connection with the use of derivative financial instruments and these requirements could escalate if prices move adversely.

Adverse decisions in lawsuits seeking a variety of damages allegedly caused by mercury spillage could adversely affect the company’s results of operations, cash flows and financial condition.

Nicor Gas has incurred, and expects to continue to incur, costs related to its historical use of mercury in various kinds of equipment. Nicor Gas remains a defendant in several private lawsuits, all in the Circuit Court of Cook County, Illinois, seeking a variety of unquantified damages (including bodily injury and property damages) allegedly caused by mercury spillage resulting from the removal of mercury-containing regulators. Potential liabilities relating to these claims have been assumed by a contractor’s insurer subject to certain limitations. Adverse decisions regarding these claims, if not fully covered by such insurance, could adversely affect the company’s results of operations, cash flows and financial condition.

Transporting and storing natural gas involves numerous risks that may result in accidents and other operating risks and costs that could adversely affect the company’s results of operations, cash flows and financial condition.

Nicor Gas’ activities involve a variety of inherent hazards and operating risks, such as leaks, accidents and mechanical problems, which could cause substantial financial losses. In addition, these risks could result in loss of human life, significant damage to property, environmental pollution and impairment of Nicor Gas’ operations, which in turn could lead to substantial losses. In accordance with customary industry practice, Nicor Gas maintains insurance against some, but not all, of these risks and losses. The location of pipelines and storage facilities near populated areas, including residential areas, commercial business centers and industrial sites, could increase the level of damages resulting from these risks. The occurrence of any of these events if not fully covered by insurance could adversely affect the company’s results of operations, cash flows and financial condition.

A significant decline in the market value of investments held within the pension trust maintained by Nicor Gas adversely affects the company’s results of operations, cash flows and financial condition.

Nicor Gas sponsors a defined benefit pension plan and, over the years, has made contributions to a trust to fund future benefit obligations of the pension plan participants. A significant decline in the market value of investments held in the trust of the pension plan unfavorably impacts the benefit costs associated with the pension plan and could adversely affect Nicor Gas’ liquidity if additional contributions to the trust are required. These impacts, either individually or in aggregate, may adversely affect the company’s results of operations, cash flows and financial condition.

An inability to access financial markets could affect the execution of Nicor’s business plan and could adversely affect the company’s results of operations, cash flows and financial condition.

Nicor relies on access to both short- and long-term capital markets as a significant source of liquidity for capital and operating requirements not satisfied by the cash flows from its operations. Management believes that Nicor and its subsidiaries will maintain sufficient access to these financial markets based upon current credit ratings. However, certain disruptions outside of Nicor’s control or events of default under its debt agreements may increase its cost of borrowing or restrict its ability to access one or more financial markets. Such disruptions could include an economic downturn, the bankruptcy of an unrelated energy company or downgrades to Nicor’s credit ratings. Restrictions on Nicor’s ability to access financial markets may affect its ability to execute its business plan as scheduled and could adversely affect the company’s results of operations, cash flows and financial condition.

Changes in the rules and regulations of certain regulatory agencies could adversely affect the results of operations, cash flows and financial condition of Tropical Shipping.

Tropical Shipping is subject to the International Ship and Port-facility Security Code and is also subject to the United States Maritime Transportation Security Act, both of which require extensive security assessments, plans and procedures. Tropical Shipping is also subject to the regulations of both the Federal Maritime Commission, and the Surface Transportation Board, other federal agencies as well as local laws, where applicable. Additional costs that could result from changes in the rules and regulations of these regulatory agencies would adversely affect the results of operations, cash flows and financial condition of Tropical Shipping.

Tropical Shipping’s business is dependent on general economic conditions. Changes or downturns in the economy could adversely affect the results of operations, cash flows and financial condition of Tropical Shipping.

Tropical Shipping’s business consists primarily of the shipment of building materials, food and other necessities from the United States and Canada to developers, manufacturers and residents in the Bahamas and the Caribbean region, as well as tourist-related shipments intended for use in hotels and resorts, and on cruise ships. As a result, Tropical Shipping’s results of operations, cash flows and financial condition can be significantly affected by adverse general economic conditions in the United States, Bahamas, Caribbean region and Canada. Also, a shift in buying patterns that results in such goods being sourced directly from other parts of the world, including China and India, rather than the United States and Canada, could significantly affect Tropical Shipping’s results of operations, cash flows and financial condition.

The occurrence of hurricanes, storms and other natural disasters in Tropical Shipping’s area of operations could adversely affect its results of operations, cash flows and financial condition.

Tropical Shipping’s operations are affected by weather conditions in Florida, Canada, the Bahamas and Caribbean regions. During hurricane season in the summer and fall, Tropical Shipping may be subject to revenue loss, higher operating expenses, business interruptions, delays, and ship, equipment and facilities damage which could adversely affect Tropical Shipping’s results of operations, cash flows and financial condition.

Nicor has credit risk that could adversely affect the company’s results of operations, cash flows and financial condition.

Nicor extends credit to its counterparties. Despite what the company believes to be prudent credit policies and the maintenance of netting arrangements, the company is exposed to the risk that it may not be able to collect amounts owed to it. If counterparties fail to perform and any collateral the company has secured is inadequate, it could adversely affect the company’s results of operations, cash flows and financial condition.

The company is involved in legal or administrative proceedings before various courts and governmental bodies that could adversely affect the company’s results of operations, cash flows and financial condition.

The company is involved in legal or administrative proceedings before various courts and governmental bodies with respect to general claims, rates, taxes, environmental issues, billing, credit and collection matters, intersegment services, gas cost prudence reviews and other matters. Adverse decisions regarding these matters, to the extent they require the company to make payments in excess of amounts provided for in its financial statements, could adversely affect the company’s results of operations, cash flows and financial condition.

Changes in taxation could adversely affect the company’s results of operations, cash flows and financial condition.

Various tax and fee increases may occur in locations in which the company operates. The company cannot predict whether legislation or regulation will be introduced, the form of any legislation or regulation, or whether any such legislation or regulation will be passed by the legislatures or other governmental bodies. New taxes or an increase in tax rates would increase tax expense and could adversely affect the company’s results of operations, cash flows and financial condition.

Changes in the laws and regulations regarding the sale and marketing of products and services offered by Nicor’s other energy ventures could adversely affect the results of operations, cash flows and financial condition of Nicor.

Nicor’s other energy ventures provide various energy-related products and services. These include sales of natural gas and utility-bill management services to residential and small commercial customers, the sale, repair, maintenance and warranty of heating, air conditioning and indoor air quality equipment and wholesale natural gas supply services. The sale and marketing of these products and services by Nicor’s other energy ventures are subject to various state and federal laws and regulations. Changes in these laws and regulations could impose additional costs on, or restrict or prohibit certain activities by, Nicor’s other energy ventures which could adversely affect the results of operations, cash flows and financial condition of Nicor.

The risks described above should be carefully considered in addition to the other cautionary statements and risks described elsewhere, and the other information contained in this report and in Nicor’s other filings with the SEC, including its subsequent reports on Forms 10-Q and 8-K. The risks and uncertainties described above are not the only risks Nicor faces although they are the most significant risks. See Item 7 – Management’s Discussion and Analysis of Financial Condition and Results of Operations, Item 7A – Quantitative and Qualitative Disclosures About Market Risk, and Item 8 – Notes to the Consolidated Financial Statements – Note 10 – Income Taxes and Note 21 – Contingencies for further discussion of these and other risks Nicor faces.

None.

Information concerning Nicor and its major subsidiaries’ properties is included in Item 1 – Business, and is incorporated herein by reference. These properties are suitable, adequate and utilized in the company’s operations.

Illinois Attorney General Subpoena. On February 8, 2010, the Office of the Attorney General for the State of Illinois (“IOAG”) issued a subpoena to Nicor to provide documents in connection with an IOAG investigation pursuant to the Illinois Whistleblower Reward and Protection Act. According to the subpoena, the IOAG investigation relates to billing practices used with certain customer accounts involving government funds. While the company believes its billing practices comply with ICC requirements, the company is unable to predict the outcome of this matter or reasonably estimate its potential exposure, if any, and has not recorded a liability associated with this matter.

Also see Item 8 – Notes to the Consolidated Financial Statements – Note 21 – Contingencies, which is incorporated herein by reference.

| Submission of Matters to a Vote of Security Holders |

None.

| Name | | Age | | Position and Business Experience during past five years |

| | | | | |

| Russ M. Strobel | | 57 | | Chairman, Nicor and Nicor Gas (since 2005); Chief Executive Officer, Nicor (since 2005); Chief Executive Officer, Nicor Gas (since 2003); President, Nicor and Nicor Gas (since 2002). |

| | | | | |

| Richard L. Hawley | | 60 | | Executive Vice President and Chief Financial Officer, Nicor and Nicor Gas (since 2003). |

| | | | | |

| Rocco J. D’Alessandro | | 51 | | Executive Vice President Operations, Nicor Gas (since 2006); Senior Vice President Operations, Nicor Gas (2002-2006). |

| | | | | |

| Daniel R. Dodge | | 56 | | Executive Vice President Diversified Ventures, Nicor (since 2007); Senior Vice President Diversified Ventures and Corporate Planning, Nicor and Nicor Gas (2002-2007). |

| | | | | |

| Claudia J. Colalillo | | 60 | | Senior Vice President Human Resources and Corporate Communications, Nicor (since 2002) and Nicor Gas (since 2006); Senior Vice President Human Resources and Customer Care, Nicor Gas (2002-2006). |

| | | | | |

| Paul C. Gracey, Jr. | | 50 | | Senior Vice President, General Counsel and Secretary, Nicor and Nicor Gas (since 2006); Vice President, General Counsel and Secretary, Nicor and Nicor Gas (2002-2006). |

| | | | | |

Gerald P. O’Connor | | 58 | | Senior Vice President Finance and Strategic Planning, Nicor and Nicor Gas (since 2007); Senior Vice President Finance and Treasurer, Nicor and Nicor Gas (2007); Vice President Administration and Finance, Nicor and Nicor Gas (2004-2006). |

| | | | | |

| Karen K. Pepping | | 45 | | Vice President and Controller, Nicor and Nicor Gas (since 2006); Assistant Vice President and Controller, Nicor and Nicor Gas (2005-2006); Assistant Controller, Nicor and Nicor Gas (2003-2005). |

| | | | | |

| Douglas M. Ruschau | | 51 | | Vice President and Treasurer, Nicor and Nicor Gas (since 2007); Vice President Finance and Treasurer, Peoples Energy Corporation (2002-2007). |

| | | | | |

| Rick Murrell | | 63 | | Chairman and President, Tropical Shipping and Construction Company Limited (since 2006); President and CEO, Tropical Shipping and Birdsall Inc. (1986-2005). |

| Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities |

Nicor common stock is listed on the New York and Chicago Stock Exchanges. At February 17, 2010, there were approximately 17,700 common stockholders of record and the closing stock price was $39.92.

| | | | Stock price | | | Dividends | |

| Quarter | | | High | | | Low | | | Declared | |

| | | | | | | | | | | |

| 2009 | | | | | | | | | | |

| First | | | $ | 36.34 | | | $ | 27.50 | | | $ | .465 | |

| Second | | | | 35.37 | | | | 30.28 | | | | .465 | |

| Third | | | | 38.08 | | | | 32.83 | | | | .465 | |

| Fourth | | | | 43.39 | | | | 34.96 | | | | .465 | |

| | | | | | | | | | | | | | |

| 2008 | | | | | | | | | | | | | |

| First | | | $ | 42.70 | | | $ | 32.35 | | | $ | .465 | |

| Second | | | | 44.55 | | | | 33.33 | | | | .465 | |

| Third | | | | 51.99 | | | | 38.01 | | | | .465 | |

| Fourth | | | | 48.42 | | | | 32.53 | | | | .465 | |

| | | | | | | | | | | | | | |

In 2001, Nicor announced a $50 million common stock repurchase program, under which Nicor may purchase its common stock as market conditions permit through open market transactions and to the extent cash flow is available after other cash needs and investment opportunities. There have been no repurchases under this program during 2009 or 2008. As of December 31, 2009, $21.5 million remained authorized for the repurchase of common stock.

STOCK PERFORMANCE GRAPH

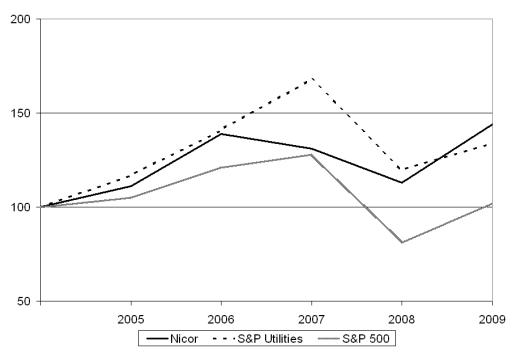

The following graph shows a five-year comparison of cumulative total returns for Nicor Common Stock, the S&P Utilities Index and the S&P 500 Index (both of which include Nicor Common Stock) as of December 31 of each of the years indicated, assuming $100 was invested on January 1, 2005, and all dividends were reinvested.

Comparison of Five-Year Cumulative Total Return

| | | 2005 | | | 2006 | | | 2007 | | | 2008 | | | 2009 | |

| | | | | | | | | | | | | | | | |

| Nicor | | $ | 111 | | | $ | 139 | | | $ | 131 | | | $ | 113 | | | $ | 144 | |

| S&P Utilities | | | 117 | | | | 141 | | | | 168 | | | | 120 | | | | 134 | |

| S&P 500 | | | 105 | | | | 121 | | | | 128 | | | | 81 | | | | 102 | |

| Nicor Inc. | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

| (in millions, except per share data) | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| | | | Year ended December 31 | |

| | | | 2009 | | | 2008 | | | 2007 | | | 2006 | | | 2005 | |

| | | | | | | | | | | | | | | | | |

| Operating revenues | | $ | 2,652.1 | | | $ | 3,776.6 | | | $ | 3,176.3 | | | $ | 2,960.0 | | | $ | 3,357.8 | |

| | | | | | | | | | | | | | | | | | | | | | |

| Operating income | | $ | 220.3 | | | $ | 185.0 | | | $ | 206.5 | | | $ | 202.5 | | | $ | 201.7 | |

| | | | | | | | | | | | | | | | | | | | | | |

| Net income | | | $ | 135.5 | | | $ | 119.5 | | | $ | 135.2 | | | $ | 128.3 | | | $ | 136.3 | |

| | | | | | | | | | | | | | | | | | | | | | |

| Earnings per average share of common stock | | | | | | | | | | | | | | | | | |

| Basic | | | $ | 2.99 | | | $ | 2.64 | | | $ | 2.99 | | | $ | 2.88 | | | $ | 3.08 | |

| Diluted | | | 2.98 | | | | 2.63 | | | | 2.99 | | | | 2.87 | | | | 3.07 | |

| | | | | | | | | | | | | | | | | | | | | | |

| Dividends declared per common share | | $ | 1.86 | | | $ | 1.86 | | | $ | 1.86 | | | $ | 1.86 | | | $ | 1.86 | |

| | | | | | | | | | | | | | | | | | | | | | |

| Property, plant and equipment | | | | | | | | | | | | | | | | | | | | |

| Gross | | | $ | 4,961.0 | | | $ | 4,802.4 | | | $ | 4,611.7 | | | $ | 4,479.7 | | | $ | 4,351.3 | |

| Net | | | | 2,939.1 | | | | 2,858.6 | | | | 2,757.3 | | | | 2,714.7 | | | | 2,659.1 | |

| | | | | | | | | | | | | | | | | | | | | | |

| Total assets | | $ | 4,435.7 | | | $ | 4,784.0 | | | $ | 4,271.3 | | | $ | 4,137.2 | | | $ | 4,453.4 | |

| | | | | | | | | | | | | | | | | | | | | | |

| Capitalization | | | | | | | | | | | | | | | | | | | | |

Long-term debt, net of unamortized discount | | $ | 498.2 | | | $ | 448.0 | | | $ | 422.8 | | | $ | 497.5 | | | $ | 485.8 | |

| Mandatorily redeemable preferred stock | | | .1 | | | | .6 | | | | .6 | | | | .6 | | | | .6 | |

| Common equity | | | 1,037.7 | | | | 973.1 | | | | 945.2 | | | | 876.1 | | | | 814.8 | |

| | | | $ | 1,536.0 | | | $ | 1,421.7 | | | $ | 1,368.6 | | | $ | 1,374.2 | | | $ | 1,301.2 | |

| | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | |

See Item 1A - Risk Factors and Item 7 - Management's Discussion and Analysis of Financial Condition and Results of Operations for factors that can impact year-to-year comparisons and may affect the future performance of Nicor's business. | |

| |

| Management’s Discussion and Analysis of Financial Condition and Results of Operations |

The purpose of this financial review is to explain changes in operating results and financial condition from 2007 to 2009 and to discuss business trends that might affect Nicor. Certain terms used herein are defined in the glossary on pages ii and iii. The discussion is organized into six sections – Summary, Results of Operations, Financial Condition and Liquidity, Outlook, Contingencies and Critical Accounting Estimates.

SUMMARY

Nicor is a holding company. Gas distribution is Nicor’s primary business. Nicor’s subsidiaries include Nicor Gas, one of the nation’s largest distributors of natural gas, and Tropical Shipping, a transporter of containerized freight in the Bahamas and the Caribbean region. Nicor also owns several energy-related ventures, including Nicor Services, Nicor Solutions and Nicor Advanced Energy, which provide energy-related products and services to retail markets, and Nicor Enerchange, a wholesale natural gas marketing company. Nicor also has equity interests in a cargo container leasing business, a FERC-regulated natural gas pipeline and certain affordable housing investments.

Net income and diluted earnings per common share are presented below (in millions, except per share data):

| | | 2009 | | | 2008 | | | 2007 | |

| | | | | | | | | | |

| Net income | | $ | 135.5 | | | $ | 119.5 | | | $ | 135.2 | |

| | | | | | | | | | | | | |

| Diluted earnings per common share | | $ | 2.98 | | | $ | 2.63 | | | $ | 2.99 | |

When comparing 2009 results to 2008, net income and diluted earnings per common share for 2008 include pretax mercury-related costs of $0.6 million ($.01 per share). Year over year comparisons (excluding the effect of the mercury-related costs) reflect improved operating results in the company’s gas distribution business and other energy-related businesses and higher equity investment income, partially offset by lower operating income in the company’s shipping business, lower interest income and a higher effective income tax rate.

When comparing 2008 results to 2007, net income and diluted earnings per common share for 2007 include pretax mercury-related recoveries of $8.0 million ($.11 per share) associated with Nicor Gas’ mercury inspection and repair program which included a reduction of $7.2 million to the company’s previously established reserve and $0.8 million in cost recoveries. Net income and diluted earnings per common share for 2008 include pretax mercury-related costs of $0.6 million ($.01 per share). Year over year comparisons (excluding the effects of the items noted above) reflect improved operating results in the company’s gas distribution business and higher equity investment income, which were more than offset by lower operating income in the company’s shipping business and other energy-related businesses, lower corporate operating results and higher interest expense.

Rate proceeding. On March 25, 2009, the ICC issued an order approving an increase in base revenues of approximately $69 million, a rate of return on rate base of 7.58 percent and a rate of return on equity of 10.17 percent. The order also approved an energy efficiency rider. Nicor Gas placed the rates approved in the March 25, 2009 order into effect on April 3, 2009.

On April 24, 2009, Nicor Gas filed a request for rehearing with the ICC concerning the capital structure and return on equity contained in the ICC’s rate order contending the company’s return on rate base should be higher. On May 13, 2009, the ICC agreed to conduct a rehearing concerning the capital structure but denied the remainder of the company’s request. On October 7, 2009, the ICC issued its decision on rehearing in which it increased the annual base revenues approved for Nicor Gas in the March 25, 2009 order by approximately $11 million, increasing the rate of return on rate base to 8.09 percent. Nicor Gas placed the rates approved in the rehearing decision into effect on a prospective basis on October 15, 2009. Therefore, the total annual base revenue increase resulting from the rate case originally filed by the company in April 2008 is approximately $80 million. In December 2009, Nicor Gas withdrew appeals of the ICC rate orders that it previously had filed in state appellate court. The ICC’s decision on rehearing, therefore, is final and no longer subject to appeal.

As a result of the rates placed into effect in 2009, it is estimated that a 100-degree day variation from normal (5,600 degree days annually) impacts Nicor Gas’ distribution margin, net of income taxes, by approximately $1.3 million.

Bad debt rider. In September 2009, Nicor Gas filed for approval of a bad debt rider with the ICC under an Illinois state law which took effect in July 2009. On February 2, 2010, the ICC issued an order approving the company’s proposed bad debt rider. This rider will provide for recovery from customers of the amount over the benchmark for bad debt expense established in the company’s rate cases. It will also provide for refunds to customers if bad debt expense is below such benchmarks.

As a result of the February order, Nicor Gas will record in the first quarter of 2010 a net recovery related to 2008 and 2009 of approximately $32 million; substantially all of this amount is expected to be collected in 2010. The benchmark, against which 2010 actual bad debt expense will be compared, is approximately $63 million.

Capital market environment. The volatility in the capital markets over the past two years has caused general concern over the valuations of investments, exposure to increased credit risk and pressures on liquidity. The company continues to review its investments, exposure to credit risk and sources of liquidity and does not currently expect any future material adverse impacts relating to these items.

Operating income. Operating income (loss) by the company’s major businesses is presented below (in millions):

| | | 2009 | | | 2008 | | | 2007 | |

| | | | | | | | | | |

| Gas distribution | | $ | 149.7 | | | $ | 124.4 | | | $ | 128.7 | |

| Shipping | | | 29.2 | | | | 39.3 | | | | 45.4 | |

| Other energy ventures | | | 45.5 | | | | 25.3 | | | | 34.0 | |

| Corporate and eliminations | | | (4.1 | ) | | | (4.0 | ) | | | (1.6 | ) |

| | | $ | 220.3 | | | $ | 185.0 | | | $ | 206.5 | |

The following summarizes operating income (loss) comparisons by the company’s major businesses:

| · | Gas distribution operating income increased $25.3 million in 2009 compared to the prior year due to higher gas distribution margin ($39.0 million increase), partially offset by higher depreciation expense ($6.5 million increase) and operating and maintenance expense ($5.8 million increase). |

Gas distribution operating income decreased $4.3 million in 2008 compared to the prior year due primarily to higher operating and maintenance expense ($24.8 million increase), the absence of $8.0 million in mercury-related recoveries recorded in 2007, higher depreciation expense ($5.3 million increase) and lower gains on property sales ($1.2 million decrease), partially offset by higher gas distribution margin ($35.7 million increase).

| · | Shipping operating income decreased $10.1 million in 2009 compared to the prior year due to lower operating revenues ($72.6 million decrease), which were partially offset by lower operating costs ($62.5 million decrease). Lower operating revenues were attributable to lower volumes shipped and lower average rates. Operating costs were lower due primarily to lower transportation-related costs, charter costs and payroll and benefit-related costs. |

Shipping operating income decreased $6.1 million in 2008 compared to the prior year as higher operating revenues ($21.3 million increase) were more than offset by higher operating costs ($27.4 million increase). Higher operating revenues were attributable to higher average rates, partially offset by lower volumes shipped. Operating costs were higher due primarily to higher transportation-related costs.

| · | Nicor’s other energy ventures operating income increased $20.2 million in 2009 compared to the prior year due primarily to higher operating income at Nicor’s wholesale natural gas marketing business, Nicor Enerchange ($18.2 million increase) and at Nicor’s energy-related products and services businesses ($1.7 million increase). Higher operating income at Nicor Enerchange was due primarily to favorable results from the company’s risk management activities associated with hedging the product risks of the utility-bill management contracts offered by Nicor’s energy-related products and services businesses. Higher operating income at Nicor’s energy-related products and services businesses was due to lower operating expenses ($7.0 million decrease), partially offset by lower operating revenues ($5.3 million decrease). |

Nicor’s other energy ventures operating income decreased $8.7 million in 2008 compared to the prior year due primarily to lower operating income at Nicor Enerchange ($11.9 million decrease), partially offset by higher operating income at Nicor’s energy-related products and services businesses ($4.8 million increase). Lower operating income at Nicor Enerchange was due primarily to unfavorable changes in valuations of derivative instruments used to hedge purchases and sales of natural gas inventory and lower results from the company’s risk management activities associated with hedging the product risks of the utility-bill management contracts offered by Nicor’s energy-related products and services businesses, partially offset by the favorable costing of physical sales activity. Improved operating results at Nicor’s energy-related products and services businesses were due to lower operating expenses ($12.2 million decrease), partially offset by lower operating revenues ($7.4 million decrease).

Nicor Enerchange uses derivatives to mitigate commodity price risk in order to substantially lock-in the profit margin that will ultimately be realized. A source of commodity price risk arises as Nicor Enerchange purchases and holds natural gas in storage to earn a profit margin from its ultimate sale. However, gas stored in inventory is required to be accounted for at the lower of weighted-average cost or market, whereas the derivatives used to reduce the risk associated with a change in the value of the inventory are carried at fair value, with changes in fair value recorded in operating results in the period of change. In addition, Nicor Enerchange also uses derivatives to mitigate the commodity price risks of the utility-bill management products offered by Nicor’s energy-related products and services businesses. The gains and losses associated with the utility-bill management products are recognized in the months that the services are provided. However, the underlying derivatives used to hedge the price exposure are carried at fair value. For derivatives that either do not meet the requirements for hedge accounting or for which hedge accounting is not elected, the changes in fair value are recorded in operating results in the period of change. As a result, earnings are subject to volatility as the fair value of derivatives change. The volatility resulting from this accounting can be significant from period to period.

| · | Corporate and eliminations’ operating income for 2009, 2008 and 2007 was impacted by the following items: |

In 2009 and 2008, corporate and eliminations’ operating income included costs of $3.7 million and $6.2 million, respectively, associated with Nicor’s other energy ventures’ utility-bill management products attributable to colder than normal weather. Both periods exclude costs of approximately $0.6 million recorded within other energy ventures. In 2007, there was no material weather impact related to other energy ventures’ utility-bill management contracts. The above noted benefits or costs resulting from variances from normal weather related to these products are recorded primarily at the corporate level as a result of an agreement between the parent company and certain of its subsidiaries. The weather impact of these contracts generally serves to partially offset the gas distribution business weather risk. The amount of the offset attributable to the utility-bill management products marketed by Nicor’s other energy ventures will vary depending upon a number of factors including the time of year, weather patterns, the number of customers for these products and the market price for natural gas.

In 2008, corporate and eliminations’ operating income included recoveries of previously incurred legal costs of $3.1 million. The legal cost recoveries were from a counterparty with whom Nicor previously did business during the PBR timeframe. The total recovery was $5.0 million, of which $3.1 million was allocated to corporate and $1.9 million was allocated to the gas distribution business (recorded as a reduction to operating and maintenance expense).

RESULTS OF OPERATIONS

Details of various financial and operating information by major business can be found in the tables throughout this review. The following discussion summarizes the major items impacting Nicor’s operating income.

Operating revenues. Operating revenues by the company’s major businesses are presented below (in millions):

| | | 2009 | | | 2008 | | | 2007 | |

| | | | | | | | | | |

| Gas distribution | | $ | 2,140.8 | | | $ | 3,206.9 | | | $ | 2,627.5 | |

| Shipping | | | 352.6 | | | | 425.2 | | | | 403.9 | |

| Other energy ventures | | | 239.0 | | | | 230.3 | | | | 244.5 | |

| Corporate and eliminations | | | (80.3 | ) | | | (85.8 | ) | | | (99.6 | ) |

| | | $ | 2,652.1 | | | $ | 3,776.6 | | | $ | 3,176.3 | |

Gas distribution operating revenues are impacted by changes in natural gas costs, which are passed directly through to customers without markup, subject to ICC review. Gas distribution operating revenues decreased $1,066.1 million in 2009 compared to the prior year due primarily to lower natural gas costs (approximately $900 million decrease), warmer weather in 2009 (approximately $140 million decrease) and lower demand unrelated to weather (approximately $60 million decrease), partially offset by the impact of the increase in base rates (approximately $60 million increase).

Gas distribution operating revenues increased $579.4 million in 2008 compared to the prior year due primarily to higher natural gas costs (approximately $370 million increase) and colder weather in 2008 (approximately $185 million increase).

Shipping operating revenues decreased $72.6 million in 2009 compared to the prior year due to lower volumes shipped ($44.2 million decrease) and lower average rates ($28.4 million decrease). Volumes shipped were adversely impacted by the economic slowdown. Lower average rates were attributable to lower cost-recovery surcharges for fuel.

Shipping operating revenues increased $21.3 million in 2008 compared to the prior year due to higher average rates ($39.9 million increase), partially offset by lower volumes shipped ($18.6 million decrease). Rates were higher due primarily to cost-recovery surcharges for fuel. Volumes shipped were adversely impacted by decreased construction cargo, decreased tourism and increased competition.

Nicor’s other energy ventures operating revenues increased $8.7 million in 2009 compared to the prior year due primarily to higher operating revenues at Nicor Enerchange ($13.9 million increase) partially offset by lower operating revenues at Nicor’s energy-related products and services businesses ($5.3 million decrease). Higher operating revenues at Nicor Enerchange were due to favorable results from the company’s risk management activities associated with hedging the product risks of the utility-bill management contracts offered by Nicor’s energy-related products and services businesses. Lower revenues at Nicor’s energy-related products and services businesses were due to lower average revenue per utility-bill management contract, partially offset by higher average contract volumes.

Nicor’s other energy ventures operating revenues decreased $14.2 million in 2008 compared to the prior year due primarily to lower revenues at Nicor’s energy-related products and services businesses ($7.4 million decrease) and Nicor Enerchange ($6.7 million decrease). Lower revenues at Nicor’s energy-related products and services businesses were due to lower average revenue per utility-bill management

contract, attributable to product mix. Lower revenues at Nicor Enerchange were due primarily to unfavorable changes in valuations of derivative instruments used to hedge purchases and sales of natural gas inventory and lower results from the company’s risk management activities associated with hedging the product risks of the utility-bill management contracts offered by Nicor’s energy-related products and services businesses, partially offset by the favorable costing of physical sales activity.

Corporate and eliminations primarily reflects the elimination of revenues against Nicor Solutions’ expenses for customers purchasing the utility-bill management products.

Gas distribution margin. Nicor utilizes a measure it refers to as “gas distribution margin” to evaluate the operating income impact of gas distribution revenues. Gas distribution revenues include natural gas costs, which are passed directly through to customers without markup, subject to ICC review, and revenue taxes, for which Nicor Gas earns a small administrative fee. These items often cause significant fluctuations in gas distribution revenues, with equal and offsetting fluctuations in cost of gas and revenue tax expense, with no direct impact on gas distribution margin. The 2009 rate orders included a franchise gas cost recovery rider and a rider to recover the costs associated with energy efficiency programs. As a result, changes in revenue included in gas distribution margin attributable to these items are expected to generally be offset by changes within operating and maintenance expense.

A reconciliation of gas distribution revenues and margin follows (in millions):

| | | 2009 | | | 2008 | | | 2007 | |

| | | | | | | | | | |

| Gas distribution revenues | | $ | 2,140.8 | | | $ | 3,206.9 | | | $ | 2,627.5 | |

| Cost of gas | | | (1,345.7 | ) | | | (2,427.8 | ) | | | (1,906.5 | ) |

| Revenue tax expense | | | (148.1 | ) | | | (171.1 | ) | | | (148.7 | ) |

| Gas distribution margin | | $ | 647.0 | | | $ | 608.0 | | | $ | 572.3 | |