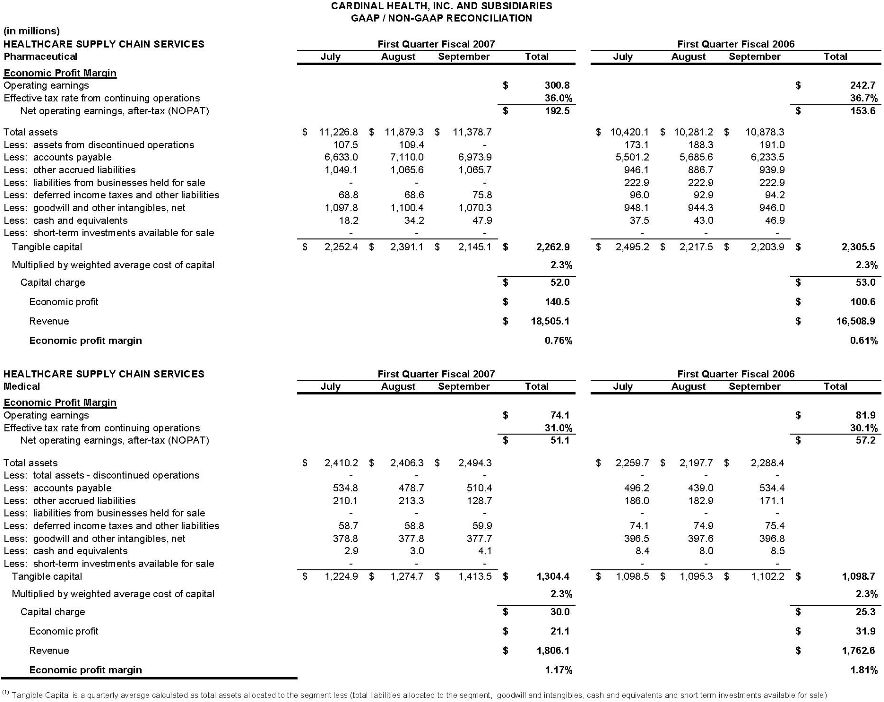

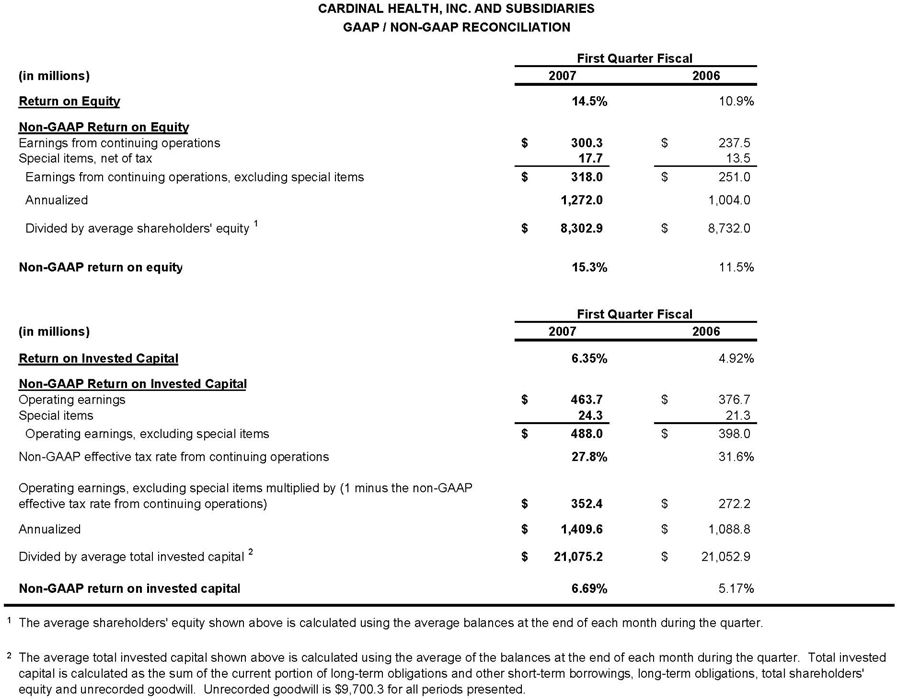

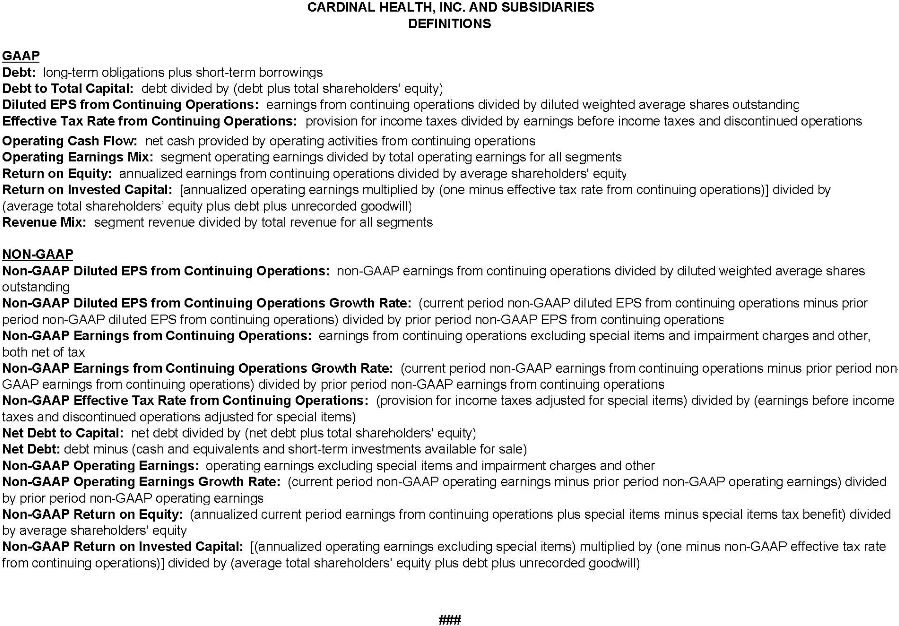

2 Forward-Looking Statements and GAAP Reconciliation Except for historical information, all other information in this presentation consists of forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995, as amended. These forward-looking statements are subject to risks and uncertainties that could cause actual results to differ materially from those projected, anticipated or implied. The most significant of these uncertainties are described in Cardinal Health's Form 10-K, Form 10-Q and Form 8-K reports (including all amendments to those reports) and exhibits to those reports, and include (but are not limited to) the following: competitive pressures in its various lines of businesses; the loss of one or more key customer or supplier relationships or changes to the terms of those relationships; changes in the distribution patterns or reimbursement rates for health-care products and/or services; the results, consequences, effects or timing of any inquiry or investigation by or settlement discussions with any regulatory authority or any legal and administrative proceedings, including shareholder litigation; difficulties in opening new facilities or fully utilizing existing capacity; the costs, difficulties and uncertainties related the integration of acquired businesses; with respect to future dividends, the decision by the board of directors to declare such dividends, which is expected to consider Cardinal Health’s surplus, earnings, cash flows, financial condition and prospects at the time any such action is considered; with respect to future share repurchases, the approval of the board of directors, which is expected to consider Cardinal Health’s then-current stock price, earnings, cash flows, financial condition and prospects as well as alternatives available to Cardinal Health at the time any such action is considered; and general economic and market conditions. Except to the extent required by applicable law, Cardinal Health undertakes no obligation to update or revise any forward-looking statement. In addition, this presentation includes non-GAAP financial measures. Cardinal Health provides definitions and a reconciliation between GAAP and non-GAAP financial information at the end of this presentation and on its investor relations page at www.cardinalhealth.com. |