Essential to care September 29, 2008 Exhibit 99.2 |

2 Forward-looking statements and GAAP reconciliation This presentation contains forward-looking statements addressing expected financial results of Cardinal Health, the planned spin-off of Cardinal Health’s clinical and medical products businesses as a separate company, the expected financial results of the new company and of Cardinal Health after giving effect to the spin-off of the new company, the operation, business and prospects of Cardinal Health and the new company following the planned spin-off and other expectations, prospects, estimates and other matters that are dependent upon future events or developments. These matters are subject to risks and uncertainties that could cause actual results to differ materially from those projected, anticipated or implied. These risks and uncertainties include uncertainties regarding the planned spin-off of the clinical and medical products businesses as a new stand-alone entity, including the timing and terms of any such spin-off and whether such spin-off will be completed, and uncertainties regarding the impacts on Cardinal Health, the new clinical and medical products company and the market for their respective securities if the spin-off is accomplished. In addition, Cardinal Health and the proposed new clinical and medical products company are subject to additional risks and uncertainties described in Cardinal Health's Form 10-K, Form 10-Q and Form 8-K reports (including all amendments to those reports) and exhibits to those reports, including (but not limited to) the following: competitive pressures in Cardinal Health’s various lines of business; the loss of one or more key customer or supplier relationships or changes to the terms of those relationships; uncertainties relating to timing of generic and branded pharmaceutical introductions and the frequency or rate of branded pharmaceutical price appreciation or generic pharmaceutical price deflation; changes in the distribution patterns or reimbursement rates for health-care products and/or services; the results, consequences, effects or timing of any inquiry or investigation by any regulatory authority or any legal or administrative proceedings; future actions of regulatory bodies or government authorities relating to Cardinal Health’s manufacturing or sale of products and other costs or claims that could arise from its manufacturing, compounding or repackaging operations or from its other services; difficulties and uncertainties related to the integration of acquired businesses; and conditions in the pharmaceutical market and general economic and market conditions. This presentation reflects management’s views as of September 29, 2008. Except to the extent required by applicable law, Cardinal Health undertakes no obligation to update or revise any forward-looking statement. Cardinal Health presents non-GAAP earnings from continuing operations (and presentations derived from this financial measure, including per share calculations) on a forward-looking basis. Non-GAAP diluted EPS from continuing operations is calculated by dividing earnings from continuing operations, excluding special items and impairments, (gain)/loss on sale of assets and other, net, both net of tax, by diluted weighted average shares outstanding. The most directly comparable forward-looking GAAP measure is earnings from continuing operations. Cardinal Health is unable to provide a quantitative reconciliation of this forward-looking non-GAAP measure to the most directly comparable forward-looking GAAP measure, because the company cannot reliably forecast special items and impairments, (gain)/loss on sale of assets and other, net, which are difficult to predict and estimate. Please note that the unavailable reconciling items could significantly impact Cardinal Health's future financial results. |

3 Creating SpinCo: Decision to spin-off CMP |

4 Disciplined review process and rationale • Disciplined review involving Board of Directors, executive leadership team and experienced external advisors • Separation of businesses will better position each to realize its long-term potential - Sharper strategic vision and enhanced management focus - Enhanced ability to make investments in respective growth areas - Improved opportunities to access / allocate capital - Better alignment of management / employee incentives and rewards • One-time costs and potential dis-synergies are manageable - Separation, transaction and stand-up costs - Public company infrastructure - Planned services agreements - Hospital selling efforts • Significant scale in each business • Analyzing collaboration/partnering alternatives |

5 Steps to completion • File Form 10 Registration Statement for SpinCo with SEC in Q3FY09 (est.) – SEC will declare Form 10 effective when review complete • Seek confirmation on the tax-free nature of the transaction from appropriate authorities • Complete separation and related agreements • Board declares pro rata distribution of SpinCo stock to Cardinal Health shareholders, sets record date / payment date / distribution ratio when final process is complete – Information statement mailed to CAH shareholders |

6 Capital structure and capital deployment • We plan to: – For Cardinal Health in FY09: • Share repurchases to no more than offset equity compensation issuances • Continue regular $0.14 quarterly dividend until the spin-off is completed – For Cardinal Health Post-Spin-off: • Have a balance sheet, financial policies and credit metrics commensurate with investment-grade credit ratings • Continue to pay a dividend – For SpinCo: • Have a balance sheet, financial policies and credit metrics commensurate with investment-grade credit ratings • Not pay dividends, but instead reinvest in R&D |

7 Leadership teams Cardinal Health SpinCo Clinical and Medical Products CEO: George Barrett, ~25 years in healthcare CFO: Jeff Henderson, ~10 years in healthcare CEO, pharmacy supply chain solutions*: Mike Kaufmann, ~17 years in healthcare CEO, medical / surgical solutions*: Mike Lynch, ~24 years in healthcare CEO: Dave Schlotterbeck, ~14 years in healthcare COO (Chief Operating Officer): Dwight Winstead, ~30 years in healthcare CFO: Outside search in process *Official business names to be determined at later date. |

8 Business structure *Includes Specialty Distribution **Cardinal Health is continuing to conduct an analysis of Pharmacy Services and Medicine Shoppe International to evaluate their future strategic fit. Healthcare Supply Chain Services (HSCS) Pharmaceutical Supply Chain* Medical Supply Chain - U.S. • Hospital Supply • Ambulatory Care • Scientific Products (Laboratory) Specialty / Nuclear Pharmacy Presource Cardinal Health – Canada Cardinal Health – Puerto Rico (including Borschow) Martindale Fluid management Convertors (drapes, gowns) Gloves (exam and surgical) Pharmacy Services** Medicine Shoppe International** Cardinal Health (RemainCo) Clinical and Medical Products (CMP) Clinical Technologies • Infusion Technologies • Dispensing Technologies • Supply Technologies Clinical Services Respiratory / Neurocare Infection Prevention • Skin Prep Solutions (includes Enturia) International (excl. Canada and Puerto Rico) Medical Specialties (surgical products) V. Mueller / On-site Services • Interventional Specialties SpinCo • |

9 Cardinal Health post-spin Business portfolio Cardinal Health Post-Spin >$90B FY09 pro forma revenue* Pharma and Specialty distribution U.S. / Canada Med Supply Distribution Medicine Shoppe Int’l** Nuclear/ Specialty Pharma Improve healthcare productivity, quality and efficiency through our superior supply chain execution and innovative products and services Pharmacy Services** **Cardinal Health is continuing to conduct an analysis of Pharmacy Services and Medicine Shoppe International to evaluate their future strategic fit. Operating Room related products/ services *An estimate of the pro forma revenue for fiscal 2009 in accordance with generally accepted accounting principles with adjustments expected to reflect each company as a stand-alone entity. The estimate is based on assumptions that management currently believes are reasonable, but actual revenue may vary materially from the estimate. |

10 SpinCo business portfolio SpinCo Clinical and Medical Products >$4B FY09 pro forma revenue* Infusion Dispensing Respiratory and Neurocare Medical Specialties (surgical products) Improving lives through better technology at the point of care Infection Prevention Clinical Services *An estimate of the pro forma revenue for the 12 months ended June 30, 2009 in accordance with generally accepted accounting principles with adjustments expected to reflect each company as a stand-alone entity. The estimate is based on assumptions that management currently believes are reasonable, but actual revenue may vary materially from the estimate. |

11 Key milestones Expected record date Q4 FY09? Expected effective date Q4 FY09 / Q1 FY10? Announcement of exploration Aug. 7, 2008 Announcement of Board decision to pursue Sept. 29, 2008 Q1 FY09 earnings Oct. 29, 2008 Annual analyst & investor day May 8, 2009 Expected Form 10 filing Q3 FY09 Annual shareholder meeting Nov. 5, 2008 |

12 Why invest in current Cardinal Health? Two industry-leading business … With talented, experienced management … Well-positioned to drive future growth … With a focus on and commitment to … Delivering value to shareholders. |

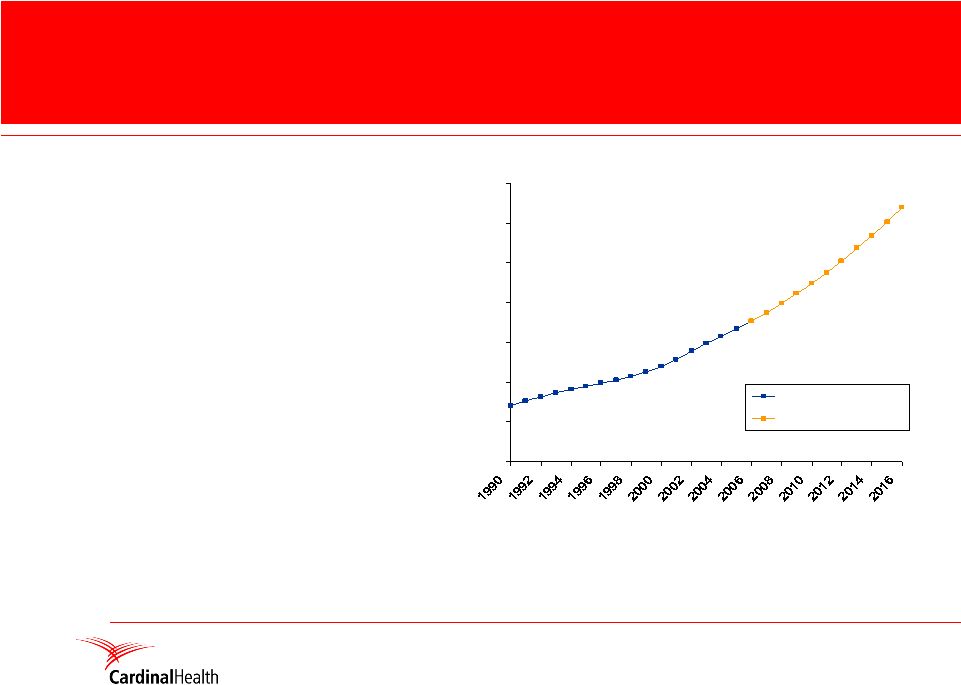

13 13 • US projected to spend over $2.2 trillion on healthcare in 2007 (16.2% of GDP) • Healthcare spending has risen at a rate 2.4% faster than GDP since 1970 • CMS estimates that by 2016 US healthcare spending will nearly double, exceeding $4.1 trillion The Landscape: U.S. healthcare costs are rising at alarming rate $0 $2,000 $4,000 $6,000 $8,000 $10,000 $12,000 $14,000 Per Capita Projected Per Capita National Health Expenditures per Capita (1990-2016) Note: Figures from 1990 through 2005 represent historical data; data from 2006- 2016 are projected. Source: Centers for Medicare and Medicaid Services, Office of the Actuary, National Health Statistics Group, at http://www.cms.hhs.gov/NationalHealthExpendData/ (Historical data from NHE summary including share of GDP, CY 1960-2005, file nhegdp05.zip; Projected data from NHE Projections 2006-2016, Forecast summary and selected tables, file proj2006.pdf). $12,782 (2016) $7,498 (2007) $2,813 (1990) |

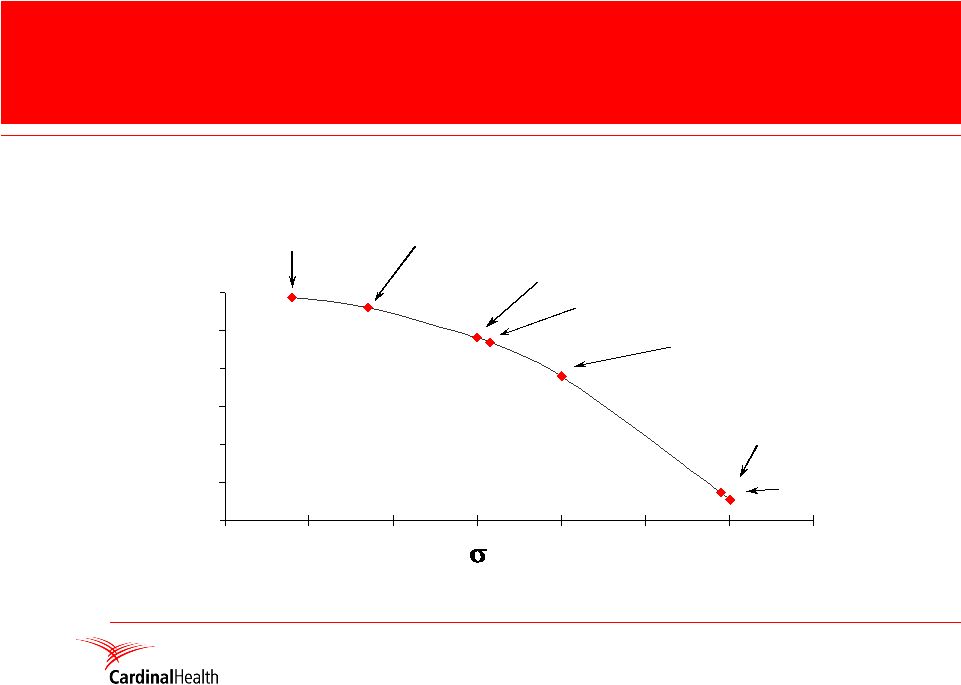

14 Source: C. Buck, GE, 2007 U.S. industry Best-in-Class Anesthesia-related fatality rate Airline baggage handling Breast cancer screening (65-69) Adverse drug events Hospital-acquired infections 1 10 100 1,000 10,000 100,000 1,000,000 Defects per million levels 1 2 3 4 5 6 Overall healthcare in U.S. (RAND) The Landscape: Errors and inefficiencies plague the system However, history suggests these errors can be prevented |

15 Cardinal Health (Post-Spin) |

16 Cardinal Health post-spin Business portfolio Cardinal Health Post-Spin >$90B FY09 pro forma revenue* Pharma and Specialty distribution U.S. / Canada Med Supply Distribution Medicine Shoppe Int’l** Nuclear/ Specialty Pharma Improve healthcare productivity, quality and efficiency through our superior supply chain execution and innovative products and services Pharmacy Services** **Cardinal Health is continuing to conduct an analysis of Pharmacy Services and Medicine Shoppe International to evaluate their future strategic fit. Operating Room related products/ services *An estimate of the pro forma revenue for fiscal 2009 in accordance with generally accepted accounting principles with adjustments expected to reflect each company as a stand-alone entity. The estimate is based on assumptions that management currently believes are reasonable, but actual revenue may vary materially from the estimate. |

17 The Business Case: Significant footprint and scale • 90% of U.S. hospitals use our products or services • More than 50,000 deliveries are made each day to 40,000 customer sites in U.S. • Leading distributor of U.S. prescriptions, medical/surgical and lab products through our system • Largest U.S. nuclear pharmacy provider, with more than 13 million prescriptions dispensed each year • Largest provider of products / services to acute care hospitals in North America |

18 Our value proposition • Large, deep and broad footprint across health channels – Retail, hospital, sub-acute, mail-order, ambulatory • Provide products / services that empower doctors, pharmacists and nurses to focus on what’s most important patients • Our scale and breadth position us to help reduce costs, improve quality and outcomes, and satisfy needs across the healthcare system – |

19 Growth drivers • Pressure on healthcare system to be more accessible, more productive, higher quality and safer • Demographics – aging population demands more health care products / services • Increasing use of generic pharmaceuticals • Opportunities to increase formulary-type Cardinal Health private label programs • Strong positioning in all retail channels • Highly efficient cost structure |

20 We provide valuable solutions throughout the pharma distribution channel Aligning offerings Suppliers Customers Retail Independents • Pharmaceutical/ distribution services • Pharmacy brands • Leader® brand • Rx purchasing programs • FirstScript – customized Autoshipment to stock new brand or generic items fast • Front-end purchasing & merchandising • Managed care programs • Ordering / inventory management Chains/ Warehousing and Non-warehousing •Distribution / operational excellence •Ordering / inventory management •Purchasing solutions •SOURCE generics (primary and back-up formulary) •Home health care, packaging, FirstScript •Managed care Hospital • Pharma distribution • Medication packaging • Fluid management products • Infection prevention (gloves, convertors) • Surgical kitting • Consulting/ design services Generic • Market share • Launch speed • Contract mgt • Efficient reach to every COT • AR / returns mgt • Centralized shipping • Data reporting Branded • Inventory mgt • Data reporting • High service levels • Contract mgt • AR / returns mgt • Special handling • Centralized shipping • Efficient reach to every COT |

21 For example… Retail Independent Pharmacy “CEO” = Pharmacist Increasing marketshare Leader® increases market share and establishes strong brand recognition by optimizing advertising strategies, implementing effective store signage and providing a profitable private label line. Improving reimbursements Leader® improves reimbursements by taking the guesswork out of dealing with PBMs, providing reimbursement support, protecting margins and providing reassurances that each claim is submitted and collected properly. Streamlining operations Leader® streamlines operations through proactive inventory management and addressing workflow issues related to staffing shortages, high labor costs, increasing scripts, decreasing margins and patient safety requirements. Creating alternate revenue streams Leader® creates alternate revenue streams such as home healthcare, durable medical equipment and diabetes management to solidify an independent pharmacy as a community’s complete healthcare destination. |

22 And we provide valuable solutions throughout the medical/surgical distribution channel • Leading position in acute care • Meaningful presence in lab setting • Focused on critical areas of hospital from quality and economic standpoint – Operating room – Presource ® , convertors, fluid management, gloves – Cardiac imaging – nuclear pharmacy • Increasing position in ambulatory/alternate sites as care moves out of acute care setting |

23 For example… Logistics and replenishment Valuelink – leading just-in-time inventory solution Optifreight – help customers manage freight costs Custom solutions Product Portfolio Broad portfolio of brand / proprietary products Expanding private label line Operational improvements Order-to-cash and SG&A Kitting Presource ® - product offerings tailored to customer needs to improve supply chain management Hospital CEO/COO/Head of Purchasing |

24 Improve the quality and productivity of healthcare Sweeten our mix (customer and product) Innovate to improve customer loyalty by segment Rebuild a winning culture Enabled through information, insight and technology Invest and execute flawlessly to build core capabilities FY09 priorities and key initiatives |

25 Near-term performance indicators • Increase direct-store-door sales • Resolve anti-diversion challenges • Increase proprietary generic Source program sales • Maintain U.S. medical distribution momentum and grow the private label |

26 SpinCo |

27 SpinCo business portfolio SpinCo Clinical and Medical Products >$4B FY09 pro forma revenue* Infusion Dispensing Respiratory and Neurocare Medical Specialties (surgical products) Improving lives through better technology at the point of care Infection Prevention Clinical Services *An estimate of the pro forma revenue for the 12 months ended June 30, 2009 in accordance with generally accepted accounting principles with adjustments expected to reflect each company as a stand-alone entity. The estimate is based on assumptions that management currently believes are reasonable, but actual revenue may vary materially from the estimate. |

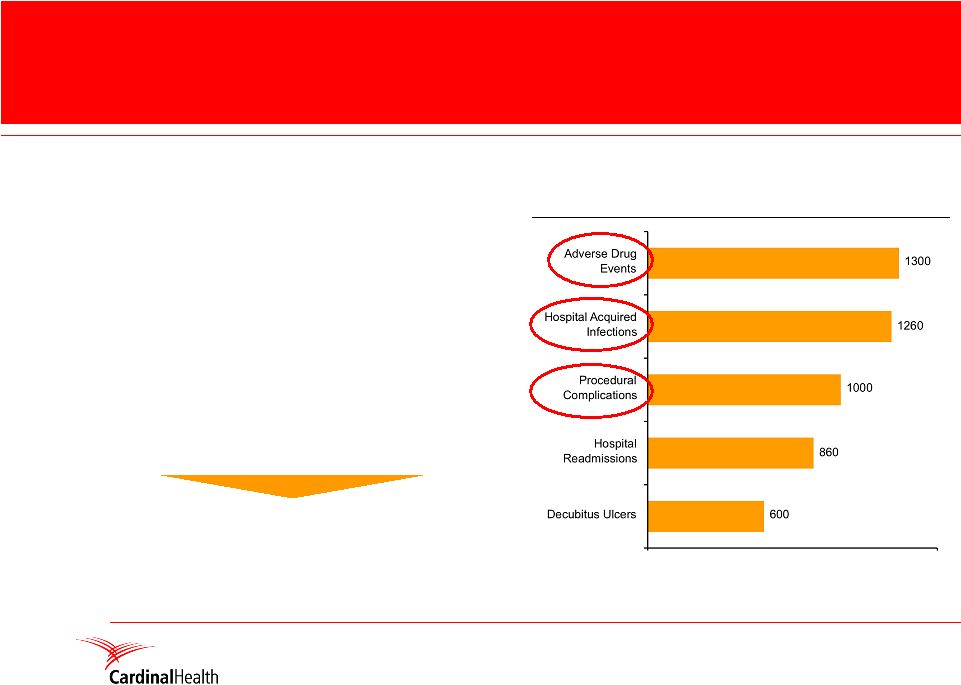

28 28 Quality and patient safety issues abound • Hospital costs alone from adverse drug events are estimated at $3-6B – Excludes costs associated with patient injury and legal claims • Hospital infections add an estimated $30B to the nation’s hospital costs annually • Costs are largely borne by the providers, payers, and government CMP is uniquely focused on addressing the top 3 hospital patient safety issues Sources: Solucient, First Consulting Group, 2004 Annual Serious Adverse Events in a Typical 300-Bed Hospital |

29 29 CMP is uniquely positioned to focus on key issues… Improve medication management Enhance infection prevention • Integrating our offers and knowledge to manage all medications • Uniquely positioned to improve safety and productivity Minimize risk and cost of procedures Help hospitals identify patients at risk • Established role and presence in the surgical suite • Expansion into the large respiratory market • Focus on protocol compliance and clinically differentiated products • Expanding our capability with high impact procedures • Tackling our customers latest concerns • Leading market offering in infection detection • Building our data to address top hospital concerns |

30 30 …with industry leading positions • Global leader in medication safety and infusion systems • Largest U.S. hospital footprint in dispensing systems • Largest acute-care respiratory company worldwide • Industry’s most comprehensive medication management solution • Leader in hospital-acquired infection (HAI) prevention • Leader in positive patient identification • Leader in U.S. surgical instrumentation |

31 31 In key product areas, critical to care… Dispensing Ventilation Infection Prevention Infusion Surgical instruments |

32 32 • Significantly outperform competition – Revenue growth – Operating margin • Strong domestic demand – Committed contracts and strong backlog provide continuous momentum – Consistent, high renewal rate • Next generation innovation and integrated offerings Renewal rates on 5-year leases are 95 – 99% Dispensing revenue Competitor 1 Competitor 2 CAH …such as dispensing, where we have a significant portion of the installed U.S. base CAH Cardinal Health data analysis; data extrapolated from earnings releases. |

33 33 And infusion, where we took >60% of business from competition in FY08 • Continued both premium pricing / gains in placements – 37% of U.S. installed base – 63% of U.S. placements • Strong international expansion – Expanded manufacturing capacity – Exceeding our expectation Disposable contracts create 5-year annuity stream for infusion pumps |

34 34 • Industry leadership – Ventilation leader - 50% growth in VIASYS installed base in past 3 years – Leading cardiopulmonary testing platform • Leading innovator – Leading technology in ventilation (critical care & portable) and diagnostics (respiratory & sleep) – Innovative offerings that address ventilator-associated pneumonia – Over 200 active patents, 300 engineers and credentialed clinicians • Unique breadth – Capital equipment and disposables for adult, pediatric, neonatal, invasive, non-invasive, nCPAP, high-frequency – Continuum of offerings beyond hospital setting – VIASYS adds strong international channel Combined with being world’s largest acute-care respiratory company |

35 35 • Innovation – Leading-edge infection prevention continuum in development • Revenue expansion – Expanding demand for infection detection and prevention – Enturia acquisition – International penetration • Margin expansion – Mix-shift in base products – Operational Excellence/Lean – Flexible manufacturing/sourcing model And a strong player in infection prevention, with next-generation products |

36 36 CMP (SpinCo) key near- to mid-term priorities Drive innovation and clinical differentiation – R&D pipeline is loaded - expecting to launch ~45-50 new products and enhanced solutions over the next 18 months 1 2 3 4 Use industry leading positions to accelerate growth – Grow international sales by expanding country specific strengths Successfully complete integrations (VIASYS and Enturia) – Cost and revenue synergies – Respiratory business model transformation Continue rounding out our solutions – Expand organically through product and solution innovation – Strategic tuck-ins |

37 Total Company Priorities |

38 Total company FY 2009 priorities • Achieve FY09 operational and financial objectives • Resolve outstanding regulatory issues • Enhanced investment in R&D and IT • Return HSCS to steady growth • Successfully complete integrations (VIASYS, Enturia, Borschow) • Efficiently execute a spin-off of the CMP businesses, while minimizing disruption |

39 FY09 financial goals >20% >10% Clinical and Medical Products (CMP) Flat to (5%) >6% Healthcare Supply Chain Services (HSCS) Profit Growth Revenue Growth Segment $3.80 - $3.95 Non-GAAP EPS : 6-7% Total revenue growth: August 7, 2008 1 Non-GAAP diluted earnings per share from continuing operations 1 |

40 FY09 assumptions update • Capital deployment – Share repurchases to no more than offset equity compensation issuances – Continue regular $0.14 quarterly dividend until spin-off is completed • Portfolio rationalization/review – MedSystems sale closed 8/29/08 – Tecomet sale closed 9/26/08 – Review of MSI and Pharmacy Services ongoing • Special items and/or other expenses / charges related to spin-off not included in guidance – Anticipate a significant portion of costs related to spin-off may be classified as special items in accordance with company practices |

41 Two industry-leading business … With talented, experienced management … Well-positioned to drive future growth … With a focus on and commitment to … Delivering value to shareholders. Summary: So why invest in current Cardinal Health now? |

Q&A |

|