Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

Proxy Statement Pursuant to Section 14(a) of the

Securities Exchange Act of 1934

Filed by the Registrant ☒

Filed by a Party other than the Registrant ☐

Check the appropriate box:

| ☐ | Preliminary Proxy Statement |

| ☐ | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) |

| ☒ | Definitive Proxy Statement |

| ☐ | Definitive Additional Materials |

| ☐ | Soliciting Material under Rule 240.14a-12 |

NOBILITY HOMES, INC.

(Name of Registrant as Specified in Its Charter)

(Name of Person(s) Filing Proxy Statement, if Other Than the Registrant)

Payment of Filing Fee (Check the appropriate box):

| ☒ | No fee required. |

| ☐ | Fee paid previously with preliminary materials. |

| ☐ | Fee computed on table in exhibit required by Item 25(b) per Exchange Act Rules 14a-6(i)(1) and0-11. |

Table of Contents

NOBILITY HOMES, INC.

Notice and Proxy Statement

NOTICE OF ANNUAL MEETING OF SHAREHOLDERS

TO BE HELD MARCH 14, 2025

TO THE HOLDERS OF COMMON STOCK:

PLEASE TAKE NOTICE that the annual meeting of the shareholders of NOBILITY HOMES, INC. will be held on Monday, the 14th day of March, 2025, at 10:00 A.M. local time, at our executive offices, 3741 S.W. 7th Street, Ocala, Florida.

The meeting will be held for the following purposes:

| 1. | To elect as directors the four nominees named in the attached proxy statement to serve terms expiring at the annual meeting of shareholders to be held in 2026 and until their successors have been elected and qualified. |

| 2. | To transact such other business as may properly come before the meeting or any adjournment. |

To be sure that your shares will be represented at the meeting, please date, sign and return your proxy, even if you plan to attend in person. A form of proxy and a self-addressed, postage prepaid envelope are enclosed. If you do attend the meeting, you may withdraw your proxy and vote in person.

By Order of the Board of Directors,

Jean Etheredge, Secretary

DATED: February 7, 2025

Table of Contents

TABLE OF CONTENTS

| Page | ||||

| 2 | ||||

| 3 | ||||

| 4 | ||||

| 6 | ||||

| 11 | ||||

| 12 | ||||

| 14 | ||||

SHAREHOLDER PROPOSALS AND COMMUNICATION WITH THE BOARD OF DIRECTORS | 14 | |||

IMPORTANT NOTICE REGARDING THE AVAILABILITY OF PROXY MATERIALS | 15 | |||

| 15 | ||||

| 15 | ||||

i

Table of Contents

NOBILITY HOMES, INC.

PROXY STATEMENT FOR ANNUAL MEETING OF SHAREHOLDERS

TO BE HELD MARCH 14, 2025

This proxy material and the enclosed form of proxy are being sent to the shareholders of Nobility Homes, Inc. on or about February 7, 2025, in connection with the solicitation by our board of directors of proxies to be used at the annual meeting of our shareholders. The meeting will be held at our executive offices, 3741 S.W. 7th Street, Ocala, Florida, at 10:00 A.M. local time, on Friday, March 14, 2025.

If the enclosed form of proxy is executed and returned, you may revoke it at any time if it has not yet been exercised, by delivering a later dated proxy or written notice of revocation to our corporate secretary or by attending the annual meeting and electing to vote in person. The shares represented by the proxy will be voted unless the proxy is received in such form as to render it not votable. The proxy is in ballot form so that you may specifically grant or withhold authority to vote for the election of each director. Our board of directors has designated Terry E. Trexler and Jean Etheredge, and each or either of them, as proxies to vote the shares of common stock solicited on its behalf.

In the election of directors, you may vote “FOR” all or some of the nominees or your vote may be “WITHHELD” with respect to one or more of the nominees. Directors are elected by a plurality of the votes cast at the meeting, which means that the four nominees who receive the highest number of properly executed votes will be elected as directors, even if those nominees do not receive a majority of the votes cast. A properly executed proxy marked “withhold authority” with respect to the election of one or more directors will not be voted with respect to the director or directors indicated, although it will be counted for purposes of determining whether there is a quorum.

Shareholders of record at the close of business on February 4, 2025, the record date for the annual meeting, will be entitled to vote. Each share of common stock is entitled to one vote on any matter to come before the meeting. As of February 4, 2025, we had 3,268,829 shares of common stock outstanding and entitled to vote.

The complete mailing address of our principal executive office is 3741 S.W. 7th Street, Ocala, Florida 34474.

1

Table of Contents

PRINCIPAL HOLDERS OF OUR COMMON STOCK

The following table sets forth, based on 3,268,829 shares of common stock as of February 4, 2025, information as to our common stock owned beneficially, directly or indirectly, (1) by each person who is known by us to own beneficially more than 5% of our outstanding voting securities, (2) by each director and nominee, (3) by each executive officer and (4) by all directors, nominees, and executive officers as a group:

Name of Beneficial Owner | Number of Common Shares Beneficially Owned (1) | Percent of Class | ||||||

Terry E. Trexler (2) | 1,683,232 | (3) | 51.49 | % | ||||

Thomas W. Trexler (2) | 423,456 | (4) | 12.94 | % | ||||

Robert P. Saltsman (5) | 2,537 | * | ||||||

Arthur L. Havener, Jr. (6) | — | * | ||||||

Lynn J. Cramer (2) | 1,962 | (7) | * | |||||

Jean Etheredge (2) | 46,477 | (8) | 1.42 | % | ||||

| Directors, nominees, and executive officers as a group (6 persons) | 2,157,664 | 66.01 | % | |||||

5% Shareholders | ||||||||

GAMCO Investors, Inc. (9) | 484,158 | 14.81 | % | |||||

| * | Less than 1% |

| (1) | Unless otherwise noted, information contained in this table is based upon information furnished by the beneficial owners, and all shares are owned directly with sole voting and dispositive power. |

| (2) | The business address is c/o Nobility Homes, Inc. at 3741 S.W. 7 th Street, Ocala, Florida 34474. |

| (3) | Includes 1,680,535 shares owned by the Terry E. Trexler Revocable Trust for which Mr. Trexler is the sole trustee and 2,697 shares owned through our 401(k) plan. |

| (4) | Includes 14,587 shares owned through our 401(k) plan. |

| (5) | Mr. Saltsman’s address is 222 South Pennsylvania Avenue, Suite 200, Winter Park, Florida 32789. |

| (6) | Mr. Havener’s address is 9825 Sunset Greens Drive, St. Louis, Missouri 63127. |

| (7) | Includes 243 shares owned through our 401(k) plan. |

| (8) | Includes 2,720 shares owned directly by Ms. Etheredge, 42,111 shares held in trust over which Ms. Etheredge has voting and investment power, and 1,646 shares owned through our 401(k) plan. |

| (9) | GAMCO Investors, Inc.’s address is One Corporate Center, Rye, New York 10580. Information is based on a report on Schedule 13D/A filed with the SEC on June 25, 2024 by GAMCO Investors, Inc. According to the information provided in the Schedule 13D/A, Mario Gabelli, through various entities which he directly or indirectly controls or which he acts as chief investment officer, has investment control over these shares. Each of these entities has voting and dispositive power over the shares shown as follows: |

Sole Voting and Dispositive Power | Shared Voting and Dispositive Power | |||||||

| Gabelli Funds, LLC | 130,148 | — | ||||||

| GAMCO Asset Management, Inc. | 253,150 | — | ||||||

| Teton Advisors, Inc. | 100,860 | — | ||||||

Delinquent Section 16(a) Reports

Section 16(a) of the Securities Exchange Act of 1934 requires our directors, certain officers and greater than 10% shareholders to file with the SEC certain reports regarding their beneficial ownership of our common stock. To our knowledge, based solely on a review of SEC filings, we believe that, with respect to fiscal year 2024, all such reports were filed timely.

Insider Trading Policy

Our Board of Directors has adopted an Insider Trading Policy which governs the purchase, sale, and other dispositions of securities by directors, officers, and employees, and is designed to promote compliance with insider trading laws, rules and regulations, as well as applicable listing standards.

2

Table of Contents

PROPOSAL 1: NOMINATION AND ELECTION OF DIRECTORS

At the annual meeting, four directors will be elected to serve for one year expiring at the annual meeting of shareholders to be held in 2026 and until their successors have been elected and qualified. Your proxy will be voted, unless you withhold authority to do so, for the election as directors of the persons named below, who have been nominated by our current board of directors.

Our bylaws provide that the board of directors shall be made up of no fewer than one nor more than ten directors. The current board of directors has determined that four directors are appropriate for the present time. Proxies cannot be voted for more than four nominees.

Each nominee has consented to being named as such in this proxy statement and is presently available for election. Our board of directors nominated all of the other existing members of our board to stand for re-election at the 2025 meeting.

If any nominee should become unavailable, the persons voting the accompanying proxy may, in their discretion, vote for a substitute. Additional information concerning the nominees, based on data furnished by them, is set forth below. Terry E. Trexler is the father of Thomas W. Trexler.

The board of directors recommends a vote “for” the election of each of the following nominees. Proxies solicited by the board of directors will be so voted unless shareholders specify in their proxies a contrary choice.

Name (Age) | Principal Occupation or Employment; Certain Other Directorships | Director Since: | ||

| Terry E. Trexler (85) | Mr. Trexler is our chairman of the board, chief executive officer and president for more than five years; Mr. Trexler is also president of TLT, Inc., the general partner of limited partnerships which are developing manufactured housing communities in Central Florida. Mr. Trexler has a long history as the Company’s chief executive officer and extensive experience in the manufactured and modular home industry. | 1967 | ||

| Thomas W. Trexler (61) | Mr. Trexler is our executive vice president and chief financial officer since December 1994; president of Prestige Home Centers, Inc. since June 1995 and president of Mountain Financial, Inc. since August 1992. Mr. Trexler is also vice president of TLT, Inc. since September 1991. Mr. Trexler has extensive experience in the manufactured and modular home industry. | 1993 | ||

| Arthur L. Havener, Jr. (58) | Mr. Havener is and has been since 2007 principal of Stampede Capital LLC, a real estate advisory and investment firm. Prior to forming Stampede Capital LLC, he was a Vice President of A.G. Edwards and Sons Inc., and Head of Real Estate Research. From 2007 to 2009, Mr. Havener served on the Board of Directors of MDC North American Real Estate Fund I, a private real estate equity fund. From 1997 to 2022, Mr. Havener served as Local Trustee of Boardwalk REIT, a Canadian Real Estate Investment Trust traded on the Toronto Stock Exchange. From 2015 to 2022 he served as a Board member, the Chair of the Audit Committee, and as a member of the Nominating and Governance Committee of Life Storage, Inc. (NYSE–LSI), which was acquired by Extra Space Storage Inc. (NYSE-EXR) in July 2023. Mr. Havener is a graduate of the Director Education Program from the Institute of Corporate Directors. | 2019 | ||

| Robert P. Saltsman (72) | Mr. Saltsman is an attorney in private practice since 1983 and prior to 2017 in private practice as CPA; prior to 1983 Mr. Saltsman was employed as a CPA by Arthur Andersen & Co. in Orlando, Florida. Mr. Saltsman has extensive expertise in accounting. | 1988 | ||

3

Table of Contents

BOARD OF DIRECTORS AND COMMITTEES

Board Composition

Our board of directors is comprised of four members, half of whom are independent directors. Although the Company is currently listed on the OTCQX and not on a national securities exchange, the board of directors has elected to use the NASDAQ definition of independence for determining whether a director or nominee is independent. The board of directors has determined that our non-management directors, Robert Saltsman and Arthur Havener, Jr., are “independent” according to NASDAQ rules. During the fiscal year ended November 2, 2024, the board of directors held four (4) regular meetings. Our non-management directors meet in executive sessions without management on a regular basis. All directors attended all of the meetings of the board of directors and committees of the board on which they served.

Board Role in Risk Oversight

Our board is involved in the oversight of risks that could affect the Company. Although this oversight is conducted in part through the committees of the board as disclosed in the descriptions of the committees below and in the charters of each of the committees, the full board has retained responsibility for the general oversight of risks. The board satisfies this responsibility through full reports by each committee chair regarding the committee’s considerations and actions, as well as through regular reports directly from officers responsible for oversight of particular risks within the Company.

Risk Considerations in our Compensation Policies

Our board believes that our compensation policies and practices are reasonable and properly align our employees’ interests with those of our shareholders. The board believes that the fact that incentive compensation for our executive officers and other employees is tied to earnings encourages actions that improve the Company’s profitability over the short and long term. In addition, the compensation committee reviews changes to our compensation policies and practices to ensure that such policies and practices do not encourage our executive officers and other employees to take actions that are likely to result in a material adverse effect on the Company.

Board Committees

Our board of directors has established three standing committees: a compensation committee, an audit committee and a nominating committee. The board of directors has elected to use the NASDAQ definitions of independence with respect to determining independence of members of specific committees. The charter of each committee is available on our website at www.nobilityhomes.com.

Compensation Committee. The compensation committee is presently comprised of Arthur Havener and Robert Saltsman. The compensation committee evaluates the performance of the CEO and other executive officers and recommends to the board of directors the salaries and bonuses, if any, to be paid to the executive officers. The compensation committee met four (4) times during fiscal year 2024.

Audit Committee. The audit committee is presently comprised of Robert Saltsman and Arthur Havener, both of whom are considered independent under current NASDAQ rules. The audit committee has a written charter which establishes the scope of the committee’s responsibilities and how it is to carry out those responsibilities. The audit committee charter charges the committee with overseeing management’s conduct of our financial reporting process, including: (1) the integrity of our financial statements, (2) our compliance with legal and regulatory requirements, and (3) the independence and performance of our external auditors. The audit committee met four (4) times during fiscal year 2024.

The board of directors has determined that Mr. Robert Saltsman is the audit committee financial expert.

Nominating Committee. The board of directors has established a nominating committee comprised of Robert Saltsman and Arthur Havener. The nominating committee will consider suggestions for potential director nominees nominated by our board from many sources, including management and our shareholders. Any such nominations, together with appropriate biographical information, should be submitted to the nominating committee no later than October 10, 2025 by sending a letter to our corporate secretary at 3741 S.W. 7th Street, Ocala, Florida 34474. The mailing envelope should contain a clear notation indicating that the enclosed letter is a “Shareholder Nomination for Director.” The nominating committee did not meet separately from the board of directors during fiscal year 2024.

4

Table of Contents

In evaluating director nominees, including candidates submitted by shareholders, the nominating committee will consider the candidate’s experience, integrity, ability to make independent analytical inquiries, understanding of our business environment and willingness to devote adequate time to board duties. The nominating committee will also consider whether a candidate meets the definition of “independent director” under NASDAQ rules. There are no stated minimum criteria for director nominees, and the nominating committee may also consider such other factors as it deems to be in the best interest of Nobility Homes and its shareholders.

5

Table of Contents

EXECUTIVE COMPENSATION

Overview

The compensation committee of our board of directors established, subject to the approval of the full board of directors, the compensation for our chief executive officer and our chief financial officer, who are our only officers whose total compensation for the fiscal year ended November 2, 2024 exceeded $100,000. We refer to these individuals as the “named executive officers.”

Because we are a small company, our compensation committee has sought to avoid the expense of retaining an outside compensation consultant to assist the committee with compensation plan design. The compensation committee takes into consideration recommendations of our CEO for compensation for officers other than our CEO.

Base Salary. The compensation committee sets salary levels for named executive officers so as to reflect the duties and level of responsibilities inherent in their positions and current economic conditions relating to our business. In establishing salary levels, the compensation committee considers the particular qualifications and level of experience of the individual.

At his request, our CEO’s base salary has remained fixed for over twenty five fiscal years because a major incentive for his performance is the value of his substantial stock ownership in Nobility Homes. Our CFO receives the same base salary as our CEO. We have not increased our CFO’s base salary since 2005.

Quarterly Incentive Bonuses. We provide certain employees, including the named executive officers, the opportunity to earn a quarterly incentive bonus based on an evaluation of the employee’s individual performance and our performance. The bonus pool is based on a specified percentage of earnings before interest and taxes for the quarter. The bonus pool is divided among eligible employees on a discretionary basis. In considering bonuses for named executive officers other than the CEO, the compensation committee consults with our chairman and CEO regarding instances of exceptional effort demonstrated by an employee. No named executive officer is automatically entitled to a bonus or a bonus in any particular amount.

Change of Control/Severance Arrangements. None of the company’s executive officers have any employment agreements or change of control/severance agreements.

6

Table of Contents

Summary Compensation Table

For Fiscal Years Ended November 2, 2024 and November 4, 2023

The following table provides information about all compensation awarded to, earned by or paid to our named executive officers during the fiscal years ended November 2, 2024 and November 4, 2023.

Name and Principal Positions | Year | Salary | Bonus | Non-Equity Incentive Plan Compensation | All Other Compensation | Total | ||||||||||||||||||

Terry E. Trexler | 2024 | $ | 93,500 | $ | 280,000 | $ | — | $ | 19,975 | (1) | $ | 393,475 | ||||||||||||

President, Chief Executive Officer | 2023 | $ | 93,500 | $ | 280,000 | $ | — | $ | 19,975 | (1) | $ | 393,475 | ||||||||||||

Thomas W. Trexler | 2024 | $ | 93,500 | $ | 280,000 | $ | — | $ | 16,220 | (2) | $ | 389,720 | ||||||||||||

Executive Vice President and Chief Financial Officer | 2023 | $ | 93,500 | $ | 280,000 | $ | — | $ | 16,220 | (2) | $ | 389,720 | ||||||||||||

| (1) | All other compensation for Mr. Terry E. Trexler for fiscal years 2024 and 2023 includes $19,975 in annual insurance premiums paid or accrued by us on two life insurance policies on the life of Mr. Terry E. Trexler. In the event of Mr. Trexler’s death, the proceeds will be paid to Mr. Trexler’s designated beneficiaries. |

| (2) | All other compensation for Mr. Thomas W. Trexler for fiscal years 2024 and 2023 includes $16,220 in annual insurance premiums paid or accrued by us for an insurance policy on the life of Mr. Thomas W. Trexler. In the event of Mr. Trexler’s death, the proceeds will be paid to Mr. Trexler’s designated beneficiaries. |

We did not grant any stock options, restricted stock awards or other equity-based awards to the named executive officers during fiscal year 2024. No equity awards vested for our named executive officers during fiscal 2024. Our named executive officers did not exercise any stock options during fiscal year 2024 nor did they hold any stock options or other equity awards as of the end of fiscal year 2024.

7

Table of Contents

Pay Versus Performance

This section is required by Section 953(a) of the Dodd-Frank Wall Street Reform and Consumer Protection Act, and Item 402(v) of Regulation

S-K.

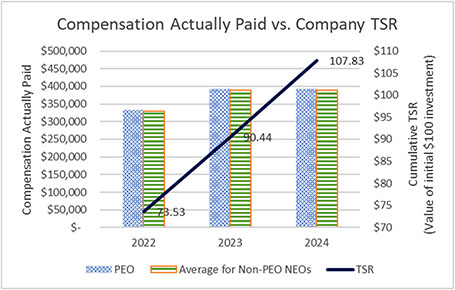

The following table shows the total compensation for the Company’s principal executive officer (“PEO”) and other named executive officers (“NEO”) as set forth in the Summary Compensation Table, the compensation “actually paid” (“CAP”) to the NEOs, the Company’s total shareholder return (“TSR”), and our net income (loss) for the fiscal years ended November 2, 2024 and November 4, 2023:Fiscal Year | Summary Compensation Table Total For PEO ($)(1) | Compensation Actually Paid to PEO ($)(1)(4) | Average Summary Compensation Table Total for Non-PEO NEOs ($)(2) | Average Compensation Actually Paid to Non-PEO NEOs ($)(4) | Value of Initial Fixed $100 Investment Based on TSR ($)(3) | Net Income (Loss)($) | ||||||||||||||||||

| 2024 | 393,475 | 393,475 | 389,720 | 389,720 | 107.83 | 8,611,262 | ||||||||||||||||||

| 2023 | 393,475 | 393,475 | 389,720 | 389,720 | 90.44 | 10,898,864 | ||||||||||||||||||

| 2022 | 333,475 | 333,475 | 329,720 | 329,720 | 73.53 | 7,232,029 | ||||||||||||||||||

| (1) | For fiscal years 2024, 2023, and 2022 the Company’s PEO was Mr. Terry E. Trexler. |

| (2) | For fiscal years 2024, 2023, and 2022, the Company’s Non-PEO NEO wasT homas W. Trexler. |

| (3) | TSR is calculated by dividing the difference between the Company’s share price at the end and the beginning of the measurement period by the Company’s share price at the beginning of the measurement period. |

| (4) | SEC rules require that certain adjustments be made to the Summary Compensation Table totals to determine CAP, as reported in the Pay versus Performance Table above. In accordance with the requirements of Item 402(v)(2)(iii) of Regulation S-K, there were no adjustments required to be made to the summary compensation table total for each year to determine CAP for either our PEO or ournon-PEO NEOs. |

8

PEO and

Non-PEO

Compensation Actually Paid and Company Total Stockholder ReturnThe following chart sets forth the relationship between CAP paid to our PEO, the average CAP paid to our

Non-PEO

NEOs, and the Company’s TSR over the period covering fiscal years 2022 to 2024.

PEO and

Non-PEO

CompensationActually

Paid and Net IncomeThe following chart sets forth the relationship between CAP paid to our PEO, the averageNEOs, and the Company’s Net Income over the period covering fiscal years 2022 to 2024.

CAP

paid to ourNon

-PEO

9

Independent

Director CompensationFor Fiscal Year Ended November 2, 2024

The following table summarizes compensation paid to independent directors for the fiscal year ended November 2, 2024. Directors who are not employees of Nobility Homes received a fee of $3,000 per board meeting. The chairman of the Audit Committee received an additional $1,250 per board meeting. Mr. Havener received an additional $3,757 for travel expenses and costs associated with attending the board meetings. We do not provide our independent directors with any compensation, equity awards or other benefits other than cash fees. No directors hold any stock options or other awards under our stock option plan.

Name | Total Fees Earned or Paid in Cash | |||

| Arthur Havener | $ | 15,757 | ||

| Robert P. Saltsman | $ | 17,000 | ||

10

Table of Contents

AUDIT COMMITTEE REPORT

The purpose of the Audit Committee is to assist the board of directors in its oversight of management’s conduct of our financial reporting process. The audit committee is presently comprised of Robert Saltsman and Arthur Havener, each of whom is “independent” under NASDAQ rules. For the fiscal year ended November 2, 2024 the audit committee:

| • | Reviewed and discussed our fiscal 2024 audited financial statements with management and representatives of Hancock Askew & Co., LLP (“Hancock”), our independent public accountants; |

| • | Received the written disclosures and the letter from Hancock mandated by applicable requirements of the Public Company Accounting Oversight Board regarding the independent accountant’s communications with the audit committee concerning independence, and discussed with Hancock its independence; and |

| • | Based on the foregoing review, discussions and disclosures, recommended to the board of directors that our audited financial statements for the fiscal year ended November 2, 2024 be included in our annual report on Form 10-K for the fiscal year. |

Robert Saltsman, Chairman

Arthur Havener

11

Table of Contents

INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

On March 9, 2023, as previously disclosed in our Current Report on Form 8-K filed with the SEC on March 15, 2023, as amended by the Current Report on Form 8-K/A filed with the SEC on May 19, 2023, the Company was advised by Daszkal Bolton, LLP (“Daszkal”), our previous independent registered public accounting firm, that Daszkal completed a business combination with CohnReznick in March 2023 and that Daszkal would resign as our independent registered public accounting firm upon the filing of the Company’s quarterly report on Form 10-Q for the quarter ended February 4, 2023. Daszkal had audited our financial statements since 2018.

On May 16, 2023, upon the approval of the Audit Committee, the Company engaged CohnReznick as our independent registered public accounting firm for the fiscal year ending November 4, 2023 and the interim periods starting with the quarter ended May 6, 2023. On February 15, 2024, as previously disclosed in our Current Report on Form 8-K filed with the SEC on February 16, 2024, the Company was advised by CohnReznick that it was resigning, effective immediately.

During the Company’s fiscal year ended November 4, 2023 and the subsequent interim periods, there were no (i) disagreements (as described in Item 304(a)(1)(iv) of Regulation S-K and the related instructions) between the Company and CohnReznick on any matter of accounting principles or practices, financial statement disclosure, or auditing scope or procedure, which, if not resolved to CohnReznick’s satisfaction, would have caused CohnReznick to make reference thereto in its reports on the financial statements for such years, except that the Company and CohnReznick disagreed as to the scope and nature of audit evidence required to substantiate the capitalization of material, labor and overhead costs in the Company’s finished goods inventory, or (ii) reportable events within the meaning of Item 304(a)(1)(v) of Regulation S-K. During the Company’s fiscal year ended November 5, 2022 there were no (i) disagreements (as described in Item 304(a)(1)(iv) of Regulation S-K and the related instructions) between the Company and Daszkal on any matter of accounting principles or practices, financial statement disclosure, or auditing scope or procedure, which, if not resolved to Daszkal’s satisfaction, would have caused Daszkal to make reference thereto in its reports on the financial statements for such years, or (ii) reportable events within the meaning of Item 304(a)(1)(v) of Regulation S-K.

On February 15, 2024, upon the approval of the Audit Committee, the Company engaged Hancock Askew & Co., LLP (“Hancock”) as our independent registered public accounting firm effective immediately. During the Company’s two most recent fiscal years ended November 4, 2023 and November 5, 2022, and the subsequent interim period through the date of engagement of Hancock: (i) the Company did not consult with Hancock regarding the application of accounting principles to a specified transaction, either completed or proposed, or the type of audit opinion that might be rendered on the Company’s financial statements; (ii) Hancock did not provide a written report or oral advice on any accounting, auditing or financial reporting issue that Hancock concluded was an important factor considered by the Company in reaching a decision as to the accounting, auditing or financial reporting issue; and (iii) the Company did not consult with Hancock regarding any matter that was either the subject of a disagreement, as defined in Item 304(a)(1)(iv) of Regulation S-K and the related instructions, or a “reportable event,” as described in Item 304(a)(1)(v) of Regulation S-K.

Since the date of Hancock’s appointment in February 2024, there were no (i) disagreements (as described in Item 304(a)(1)(iv) of Regulation S-K and the related instructions) between the Company and Hancock on any matter of accounting principles or practices, financial statement disclosure, or auditing scope or procedure, which, if not resolved to Hancock’s satisfaction, would have caused Hancock to make reference thereto in its reports on the financial statements for such years, or (ii) reportable events within the meaning of Item 304(a)(1)(v) of Regulation S-K.

Representatives of Hancock will be present at the annual meeting and will have an opportunity to make a statement if they so desire and will be available to respond to appropriate questions from shareholders.

The following table provides information relating to the fees billed by Hancock for services performed during the fiscal year ended November 2, 2024 and by Daszkal and CohnReznick for services performed during the fiscal year ended November 4, 2023.

Audit Fees(1) | Tax Fees | All Other Fees | Total Fees | |||||||||||||

Fiscal Year 2024 | $ | 277,227 | (2) | $ | 0 | $ | 0 | $ | 277,227 | |||||||

Fiscal Year 2023 | $ | 139,769 | (3) | $ | 0 | $ | 0 | $ | 139,769 | |||||||

| (1) | Audit fees include all fees for services in connection with the annual audit of our financial statements and review of our quarterly financial statements. |

| (2) | Includes $141,564 of fees from Hancock relating to the audit of the 2024 financial statements and $135,663 of fees from Hancock relating to the audit of the 2023 financial statements, with all of such services being performed during 2024 as a result of the engagement of Hancock during February 2024. |

| (3) | Includes $25,150 and $114,619 of fees from Daszkal and CohnReznick, respectively. |

12

Table of Contents

All decisions regarding selection of independent accounting firms and approval of accounting services and fees are made by our audit committee in accordance with the provisions of the Sarbanes-Oxley Act of 2002. There are no exceptions to the policy of securing pre-approval of our audit committee for any service provided by our independent accounting firm.

13

Table of Contents

TRANSACTIONS WITH RELATED PERSONS

With the exception of the transactions set forth below, we were not a party to any transaction (in which the amount involved exceeded the lesser of $120,000 or one percent of the average of our assets for the last two fiscal years) in which a director, executive officer, holder of one or more than five percent of our common stock, or any member of the immediate family of any such person has or will have a direct or indirect material interest and no such transactions are currently proposed.

Our President, Chief Executive Officer, and Chairman of the Board of Directors, Terry Trexler, and Executive Vice President and Chief Financial Officer, Thomas Trexler, each own 50% of the stock of TLT, Inc., the general partner of limited partnerships which are developing manufactured housing communities in Central Florida. Sales to such communities during fiscal 2024 were $221,620.

On June 22, 2023, the Company repurchased 100,000 shares of common stock from our President, Chief Executive Officer, and Chairman of the Board of Directors, Terry Trexler, for an aggregate purchase price of $2.8 million.

SHAREHOLDER PROPOSALS AND

COMMUNICATION WITH THE BOARD OF DIRECTORS

Any shareholder desiring to present a proposal to be included in our proxy statement for the next annual meeting of shareholders pursuant to Rule 14a-8 under the Securities Exchange Act of 1934 (the “Exchange Act”) should submit a written copy of such proposal to our principal offices no later than October 10, 2025, which is 120 calendar days prior to the anniversary of this year’s mailing date. If the date of next year’s annual meeting is changed by more than 30 days from the anniversary date of this year’s annual meeting, then the deadline is a reasonable time before we begin to print and mail proxy materials. Proposals must comply with the proxy rules relating to shareholder proposals, in particular Rule 14a-8 under the Exchange Act, in order to be included in our proxy materials.

If a shareholder wishes to present a proposal at our annual meeting in the year 2026 or to nominate one or more directors, and the proposal is not intended to be included in our proxy statement relating to that meeting pursuant to Rule 14a-8 under the Exchange Act, the shareholder must give advance written notice to us prior to the deadline for such meeting determined in accordance with our bylaws. In general, our bylaws provide that such notice should be received at our principal offices by close of business no fewer than 120 days prior to the first anniversary of this year’s mailing date. For purposes of our 2026 annual meeting, such notice must be received no later than the close of business on October 10, 2025.

In addition to satisfying the foregoing requirements under the Company’s bylaws, to comply with the universal proxy rules, shareholders who intend to solicit proxies in support of director nominees other than the Company’s nominees must provide notice that sets forth the information required by Rule 14a-19 under the Exchange Act no later than January 13, 2026, the date that is sixty days prior to the first anniversary of this year’s annual meeting date, or if the date of the annual meeting has changed by more than thirty days from the prior year’s annual meeting date, by the later of 60 calendar days prior to the date of the annual meeting or the tenth calendar day following the day on which public announcement of the date of the annual meeting is first made by the Company.

Proposals should be submitted by certified mail, return receipt requested.

Shareholders who wish to communicate with the board of directors or with a particular director may send a letter to our corporate secretary at 3741 S.W. 7th Street, Ocala, Florida 34474. The mailing envelope should contain a clear notation indicating that the enclosed letter is a “Shareholder-Board Communication” or “Shareholder-Director Communication.” All such letters should identify the author as a shareholder and clearly state whether the intended recipients are all members of the board or just certain specified individual directors. Our corporate secretary will make copies of all such letters and circulate them to the appropriate director or directors.

We do not have a formal policy requiring directors to attend annual meetings. However, because the annual meeting generally is held on the same day as a regular board meeting, we anticipate that directors will attend the annual meeting unless, for some reason, they are unable to attend the board meeting on the same date. All directors attended the 2024 annual meeting of shareholders.

14

Table of Contents

IMPORTANT NOTICE REGARDING THE AVAILABILITY OF

PROXY MATERIALS

A copy of our annual report for the fiscal year ended November 2, 2024 accompanies this proxy statement. The proxy statement and our annual report to shareholders are also available online at: www.nobilityhomes.com. A shareholder who would like to obtain an additional copy of the proxy statement or annual report may obtain one by (i) writing to our corporate secretary at 3741 S.W. 7th Street, Ocala, Florida 34474; (ii) by calling our corporate secretary at the following toll-free number 1-800-476-6624, extension 121; or (iii) by downloading a copy at www.nobilityhomes.com. A shareholder who would like to obtain directions to the annual meeting may (i) write to our corporate secretary at the address above or (ii) call the corporate secretary at the toll-free number listed above.

OTHER MATTERS

Management does not know of any other matters to come before the meeting. However, if any other matters properly come before the meeting, it is the intention of the persons designated as proxies to vote in accordance with their best judgment on such matters.

EXPENSES OF SOLICITATION

The cost of soliciting proxies will be borne by us. We do not expect to pay any compensation for the solicitation of proxies but may reimburse brokers and other persons holding stock in their names, or in the names of nominees, for their expenses of sending proxy material to principals and obtaining their proxies.

Please specify your choices, date, sign and return the enclosed proxy in the enclosed envelope, postage for which has been provided. A prompt response is helpful. Your cooperation will be appreciated.

15

Table of Contents

|

| |

NOBILITY HOMES, INC. C/O BROADRIDGE CORPORATE ISSUER SOLUTIONS, INC. P.O. BOX 1342 BRENTWOOD, NY 11717 |

VOTE BY INTERNET - www.proxyvote.com or scan the QR Barcode above Use the Internet to transmit your voting instructions and for electronic delivery of information up until 11:59 p.m. Eastern Time the day before the cut-off date or meeting date. Follow the instructions to obtain your records and to create an electronic voting instruction form. ELECTRONIC DELIVERY OF FUTURE PROXY MATERIALS If you would like to reduce the costs incurred by our company in mailing proxy materials, you can consent to receiving all future proxy statements, proxy cards and annual reports electronically via e-mail or the Internet. To sign up for electronic delivery, please follow the instructions above to vote using the Internet and, when prompted, indicate that you agree to receive or access proxy materials electronically in future years. VOTE BY PHONE - 1-800-690-6903 Use any touch-tone telephone to transmit your voting instructions up until 11:59 p.m. Eastern Time the day before the cut-off date or meeting date. Have your proxy card in hand when you call and then follow the instructions. VOTE BY MAIL Mark, sign and date your proxy card and return it in the postage-paid envelope we have provided or return it to Vote Processing, c/o Broadridge, 51 Mercedes Way, Edgewood, NY 11717. |

TO VOTE, MARK BLOCKS BELOW IN BLUE OR BLACK INK AS FOLLOWS: | KEEP THIS PORTION FOR YOUR RECORDS |

— — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — –

DETACH AND RETURN THIS PORTION ONLY

THIS PROXY CARD IS VALID ONLY WHEN SIGNED AND DATED.

For All | Withhold All | For All Except |

To withhold authority to vote for any individual nominee(s), mark “For All Except” and write the number(s) of the nominee(s) on the line below. |

| ||||||||||||||||

The Board of Directors recommends you vote FOR the following:

| ☐ | ☐ | ☐ | |||||||||||||||||

1. | Election of Directors | |||||||||||||||||||

| Nominees | ||||||||||||||||||||

01) Terry E. Trexler 02) Thomas W. Trexler 03) Arthur L. Havener, Jr. 04) Robert P. Saltsman | ||||||||||||||||||||

| NOTE: Such other business as may properly come before the meeting or any adjournment thereof. |

| |||||||||||||||||||

Please sign exactly as your name(s) appear(s) hereon. When signing as attorney, executor, administrator, or other fiduciary, please give full title as such. Joint owners should each sign personally. All holders must sign. If a corporation or partnership, please sign in full corporate or partnership name by authorized officer.

Signature [PLEASE SIGN WITHIN BOX] | Date | Signature (Joint Owners) | Date | |||||||

Table of Contents

Important Notice Regarding the Availability of Proxy Materials for the Annual Meeting:

The Notice and Proxy Statement and Annual Report are available at www.proxyvote.com

— — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — — —

REVOCABLE PROXY NOBILITY HOMES, INC.

Proxy Solicited on Behalf of the Board of Directors

for Annual Meeting of Shareholders March 14, 2025

The undersigned, having received the Notice of Annual Meeting of Shareholders and Proxy Statement appoints Terry E. Trexler and Jean Etheredge, and each or either of them, as proxies, with full power of substitution, to represent the undersigned and to vote all shares of common stock of Nobility Homes, Inc. which the undersigned is entitled to vote at the Annual Meeting of Shareholders of the Company to be held on March 14, 2025 and at any and all adjournments thereof, in the manner specified.

THIS PROXY WILL BE VOTED AS DIRECTED, OR IF NO DIRECTION IS INDICATED, WILL BE VOTED IN ACCORDANCE WITH THE BOARD OF DIRECTORS’ RECOMMENDATION.

Should any other matters requiring a vote of the shareholders arise, the above named proxies are authorized to vote the same in accordance with their best judgment in the interest of the Company. The board of directors is not aware of any matter which is to be presented for action at the meeting other than the matters set forth herein.

Continued and to be signed on reverse side

|